Embed Size (px)

Citation preview

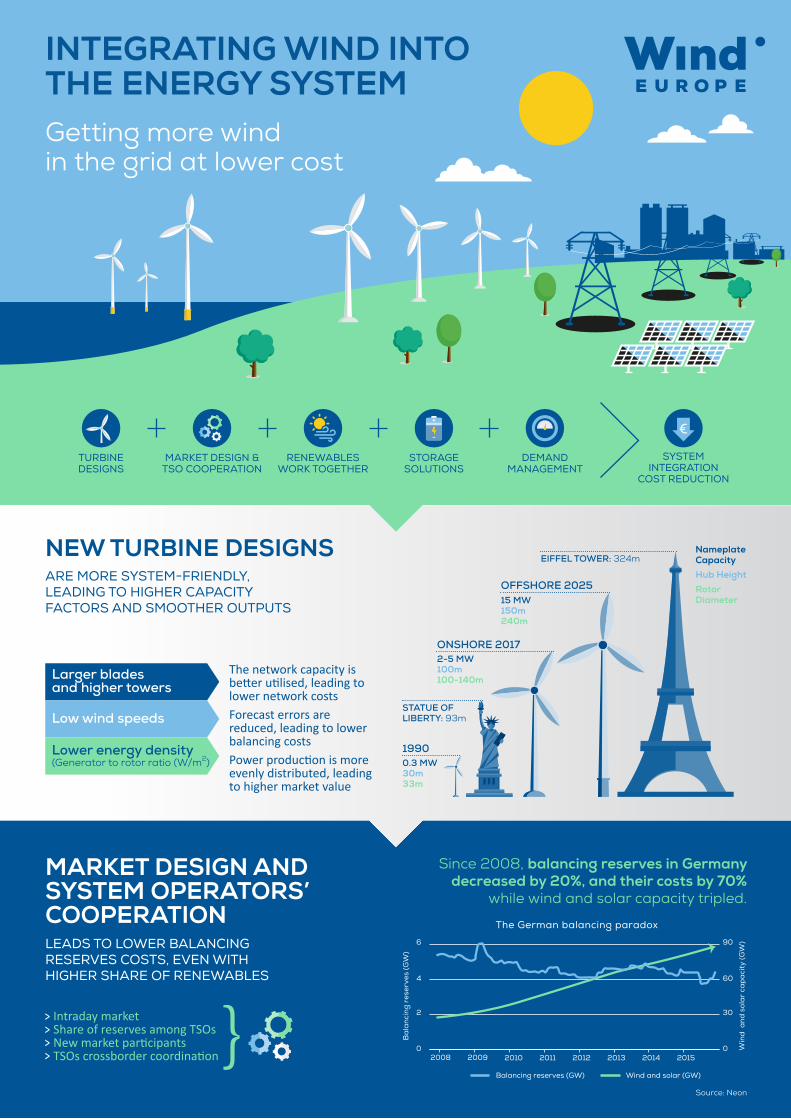

NEW TURBINE DESIGNSARE MORE SYSTEM-FRIENDLY, LEADING TO HIGHER CAPACITY FACTORS AND SMOOTHER OUTPUTS

The network capacity is better utilised, leading to lower network costs Forecast errors are reduced, leading to lower balancing costs Power production is more evenly distributed, leading to higher market value

MARKET DESIGN AND SYSTEM OPERATORS’ COOPERATION LEADS TO LOWER BALANCING RESERVES COSTS, EVEN WITH HIGHER SHARE OF RENEWABLES

2-5 MW100m100-140m

15 MW150m240m

0.3 MW30m33m

STATUE OF LIBERTY: 93m

EIFFEL TOWER: 324m

ONSHORE 2017

OFFSHORE 2025

1990

Nameplate Capacity

Hub Height

Rotor Diameter

Since 2008, balancing reserves in Germany decreased by 20%, and their costs by 70%

while wind and solar capacity tripled.

Source: Neon

Larger bladesand higher towers

Low wind speeds

Lower energy density (Generator to rotor ratio (W/m2)

The German balancing paradox

Balancing reserves (GW) Wind and solar (GW)

2008 2009 2010 2011 2012 2013 2014 20150 0

2 30

604

906

Ba

lanc

ing

rese

rves

(GW

)

Win

d a

nd s

ola

r ca

pa

city

(GW

)

Intraday market Share of reserves among TSOs New market participantsTSOs crossborder coordination

INTEGRATING WIND INTO THE ENERGY SYSTEMGetting more windin the grid at lower cost

RENEWABLESWORK TOGETHER

TURBINEDESIGNS

MARKET DESIGN & TSO COOPERATION

STORAGESOLUTIONS

DEMANDMANAGEMENT

SYSTEM INTEGRATION

COST REDUCTION

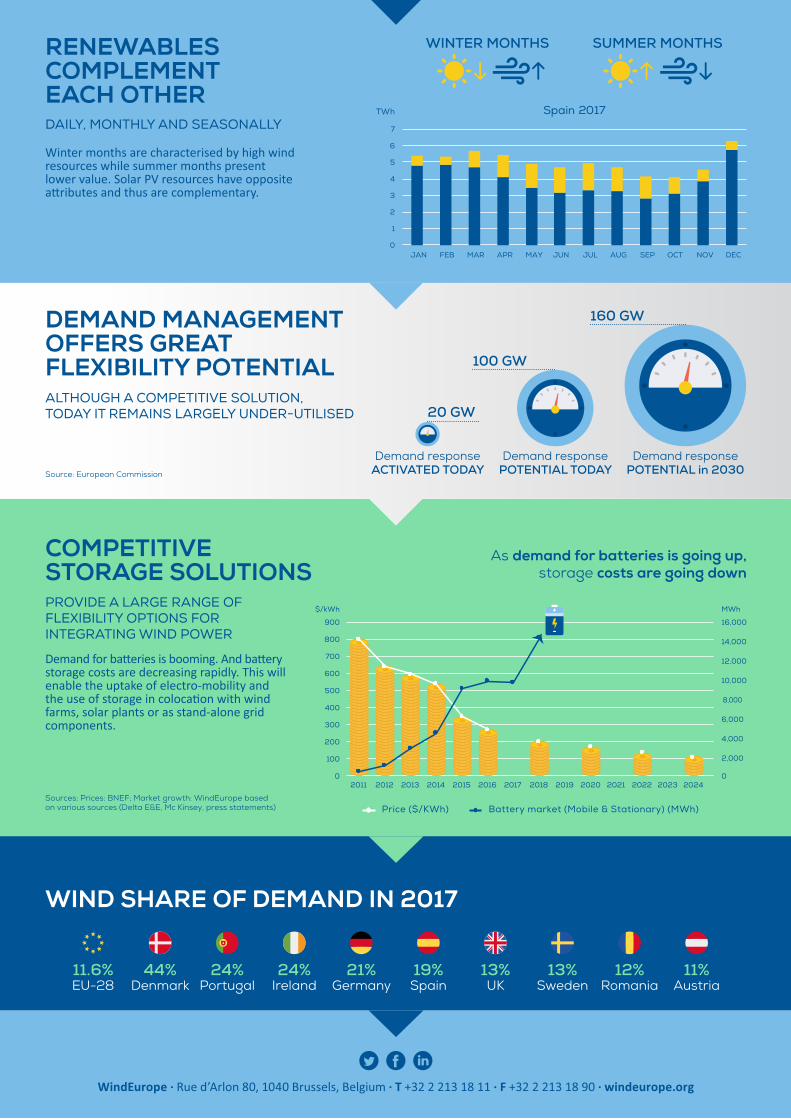

WIND SHARE OF DEMAND IN 2017

11.6%EU-28

44%Denmark

24%Portugal

24%Ireland

21%Germany

19%Spain

13%UK

13%Sweden

12%Romania

11%Austria

COMPETITIVE STORAGE SOLUTIONSPROVIDE A LARGE RANGE OF FLEXIBILITY OPTIONS FOR INTEGRATING WIND POWER

Demand for batteries is booming. And battery storage costs are decreasing rapidly. This will enable the uptake of electro-mobility and the use of storage in colocation with wind farms, solar plants or as stand-alone grid components.

As demand for batteries is going up,storage costs are going down

Sources: Prices: BNEF; Market growth: WindEurope basedon various sources (Delta E&E, Mc Kinsey, press statements)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

0

100

200

300

400

500

600

700

800

900

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

MWh$/kWh

Price ($/KWh) Battery market (Mobile & Stationary) (MWh)

DEMAND MANAGEMENTOFFERS GREATFLEXIBILITY POTENTIALALTHOUGH A COMPETITIVE SOLUTION,TODAY IT REMAINS LARGELY UNDER-UTILISED

Demand responsePOTENTIAL in 2030

Demand response POTENTIAL TODAY

Demand response ACTIVATED TODAY

160 GW

100 GW

20 GW

Source: European Commission

DAILY, MONTHLY AND SEASONALLY

RENEWABLESCOMPLEMENTEACH OTHER

Winter months are characterised by high wind resources while summer months present lower value. Solar PV resources have opposite attributes and thus are complementary.

0

1

2

3

4

5

6

7

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

TWh Spain 2017

SUMMER MONTHSWINTER MONTHS