Embed Size (px)

Citation preview

Taking accountability to improve audit outcomes

INTEGRATED DEVELOPMENT PLAN (IDP)

3

“Plan-Do-Check-Act Cycle”, also the Deming cycle , courtesy of the International Organization for Standardization

4

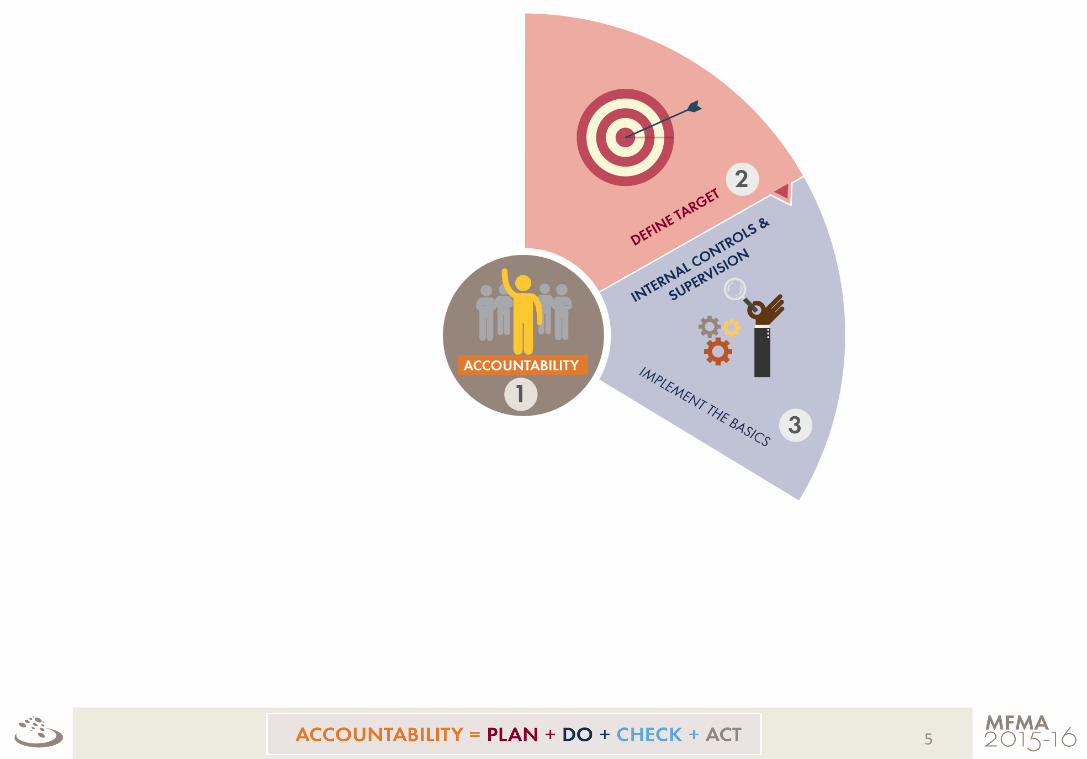

5

6

7

8

9

DO

PLAN

CHECK ACT

10

The AGSA has a constitutional

mandate and exists to strengthen

our democracy by enabling

oversight, accountability and good governance in the public

sector through auditing, thereby

building public confidence

Delivering a valuable and relevant product

focusing on the things that matter

We have improved our audit methodology and audit report

11

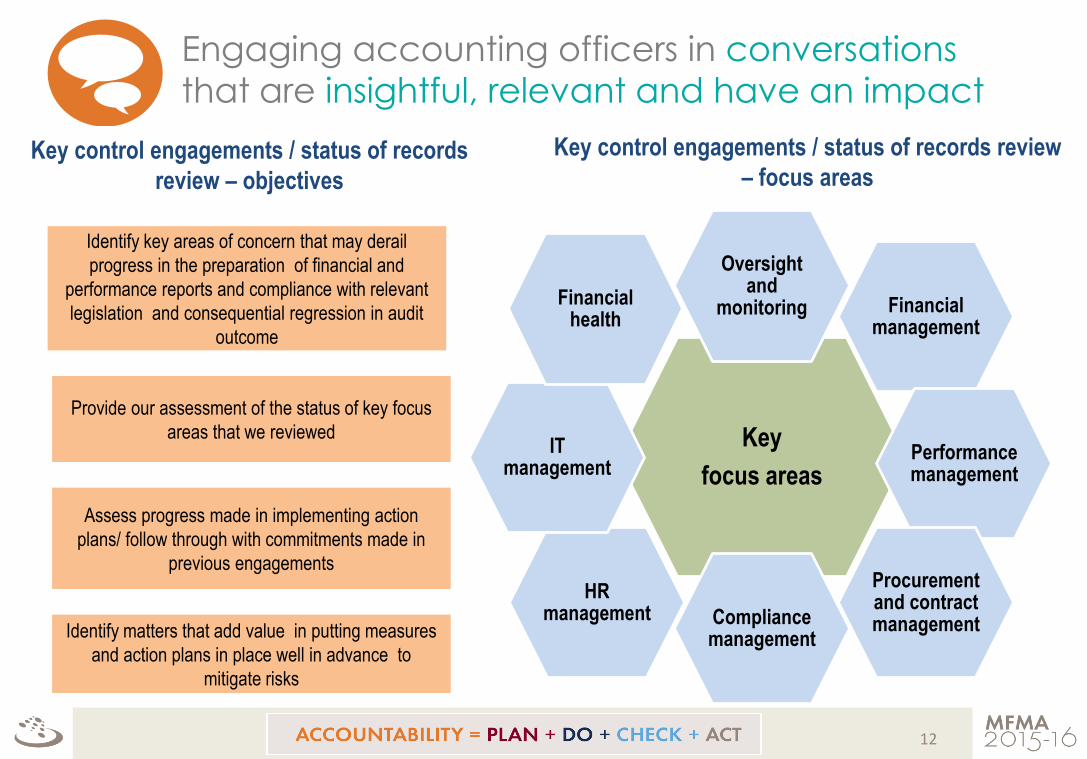

Key control engagements / status of records

review – objectives

Identify matters that add value in putting measures

and action plans in place well in advance to

mitigate risks

Assess progress made in implementing action

plans/ follow through with commitments made in

previous engagements

Provide our assessment of the status of key focus

areas that we reviewed

Identify key areas of concern that may derail

progress in the preparation of financial and

performance reports and compliance with relevant

legislation and consequential regression in audit

outcome

Key

focus areas

Oversight and

monitoring Financial management

Performance management

Procurement and contract management Compliance

management

HR management

IT management

Financial health

Key control engagements / status of records review

– focus areas

12

Engaging accounting officers in conversations

that are insightful, relevant and have an impact

13

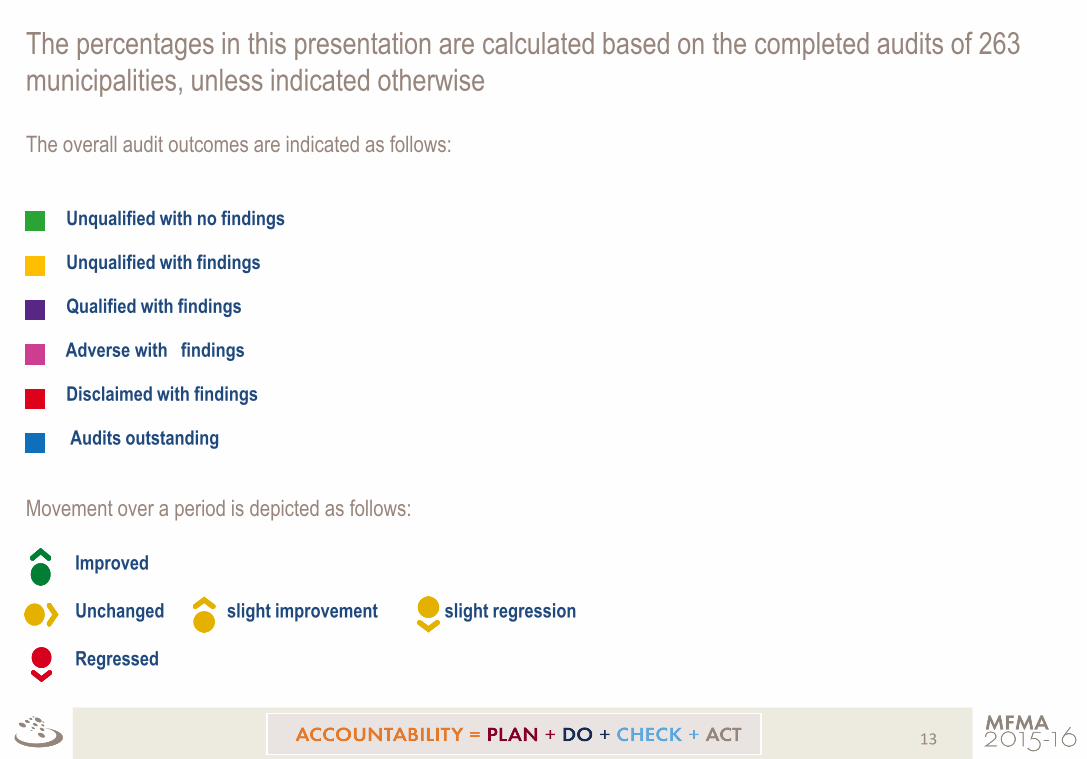

The percentages in this presentation are calculated based on the completed audits of 263

municipalities, unless indicated otherwise

The overall audit outcomes are indicated as follows:

Unqualified with no findings

Unqualified with findings

Qualified with findings

Adverse with findings

Disclaimed with findings

Audits outstanding

Movement over a period is depicted as follows:

Improved

Unchanged slight improvement slight regression

Regressed

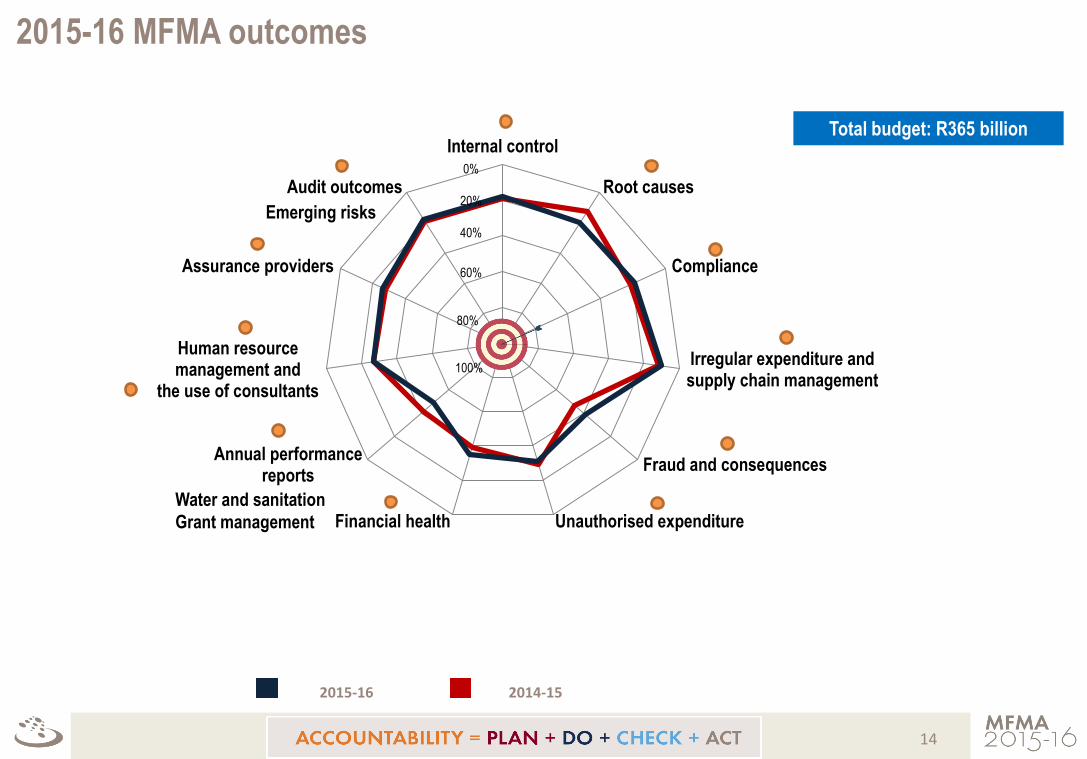

2015-16 MFMA outcomes

Internal control

Root causes

Compliance

Irregular expenditure andsupply chain management

Fraud and consequences

Unauthorised expenditureFinancial health

Annual performancereports

Human resourcemanagement and

the use of consultants

Assurance providers

Audit outcomes

Total budget: R365 billion

14

2015-16 2014-15

80%

100%

60%

40%

20%

0%

Water and sanitation

Grant management

Emerging risks

25% 43% 32% Leadership

Internal controls

23% 47% 30%

Financial andperformancemanagement

37% 38% 25% Governance

Good Of concern Intervention required

18%

15

Good controls =

Root causes

86% (185)

73% (157)

73% (158)

Slow response to improving key controls and addressing risk areas

Inadequate consequences for poor performance and transgressions

Instability or vacancies in key positions

16

Management (accounting officers and senior management), the political

leadership (mayor and council) and oversight bodies MPACs and portfolio

committees) do not respond with the required urgency to our messages

about addressing risks and improving internal controls

If officials who deliberately or negligently ignore their duties and contravene

legislation are not held accountable for their actions, such behaviour can

be seen as acceptable and tolerated.

The instability and prolonged vacancies in key positions can cause a

competency gap that leads to a high demand for consultants and

support.

18% Best practices =

73% (191)

68% (178)

63% (167)

52% (136)

45% (119)

Prevention of unauthorised, irregular and fruitless and wasteful expenditure

Quality of financial statements submitted

Management ofprocurement and/ or contracts

Consequence management

Expenditure management

Little improvement in areas of compliance

17

19% With no findings =

Irregular expenditure over three years 2015-16

MFMA

R10 791 m (64%)

R6 999 m (63%)

R5 369 m (47%)

R6 019 m (36%)

R4 137 m (37%)

R5 965 m (53%)

2015-16 2014-15 2013-14

R16 810 m

(236 municipalities [90%])

R11 334 m

(225 municipalities [86%]) R11 136 m

(232 municipalities [88%])

Identified by auditees Identified during audit

31% (R5 269 m)

19% (R2 179 m)

24%

(R2 662 m)

Incurred in previous years – identified in current year

18

10% 98% (2014-15: 96%) of occurrences were related to contraventions of SCM prescripts

EC R5 657 million (34%)

FS R361 million

(2%) GP R1 499

million (9%)

KZN R2 361 million (14%)

LP R1 636 million (10%)

MP R2 279 million (13%)

NC R287 million

(2%)

NW R2 520 million (15%)

WC R210 million

(1%)

Provincial breakdown of

irregular expenditure incurred

With no IE =

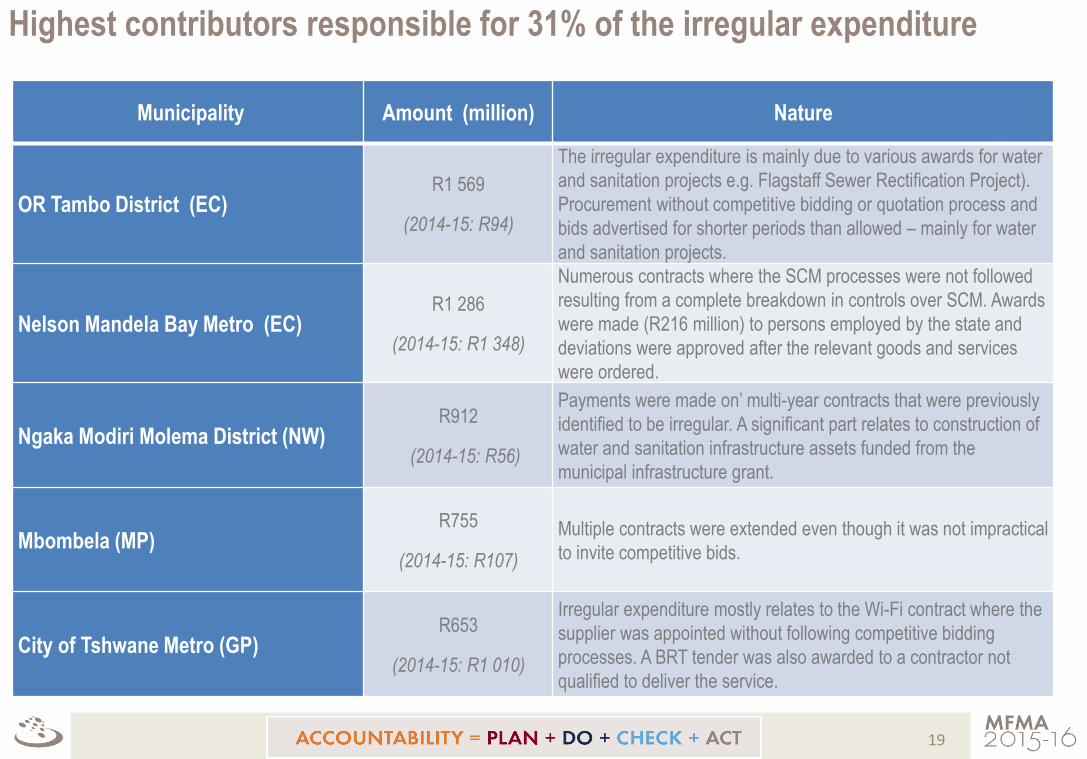

Highest contributors responsible for 31% of the irregular expenditure

19

Municipality Amount (million) Nature

OR Tambo District (EC) R1 569

(2014-15: R94)

The irregular expenditure is mainly due to various awards for water

and sanitation projects e.g. Flagstaff Sewer Rectification Project).

Procurement without competitive bidding or quotation process and

bids advertised for shorter periods than allowed – mainly for water

and sanitation projects.

Nelson Mandela Bay Metro (EC) R1 286

(2014-15: R1 348)

Numerous contracts where the SCM processes were not followed

resulting from a complete breakdown in controls over SCM. Awards

were made (R216 million) to persons employed by the state and

deviations were approved after the relevant goods and services

were ordered.

Ngaka Modiri Molema District (NW) R912

(2014-15: R56)

Payments were made on’ multi-year contracts that were previously

identified to be irregular. A significant part relates to construction of

water and sanitation infrastructure assets funded from the

municipal infrastructure grant.

Mbombela (MP) R755

(2014-15: R107)

Multiple contracts were extended even though it was not impractical

to invite competitive bids.

City of Tshwane Metro (GP) R653

(2014-15: R1 010)

Irregular expenditure mostly relates to the Wi-Fi contract where the

supplier was appointed without following competitive bidding

processes. A BRT tender was also awarded to a contractor not

qualified to deliver the service.

Little movement in SCM findings since previous year

10% (26)

14% (36)

19% (51)

18% (46)

41% (107)

23% (64)

10% (26)

6% (16)

9% (23)

26% (69)

17% (46)

59% (155)

Limitation in planned scope of audit awards

Awards to employees

Awards to close familymembers of employees

Inadequate contract management

Awards to other state officials

Uncompetitive or unfairprocurement processes

20% (52)

20% (52), R56 million

28% (74), R1 396 million

44% (115)

58% (153), R2 520 million

83% (219)

20

With findings With material findings (reported in audit report)

21

Recommendations for improving SCM findings

• A less tolerant approach by all parties, including those charged with governance and oversight, will result in

accountability and consequences being enforced against those who intentionally fail to comply with legislation

• Strengthen the SCM control environment by appointing suitably skilled and qualified heads of SCM where

vacancies exist and conduct regular training to improve skills – this will reduce possible irregular expenditure

• Implement SCM compliance checklists to supplement policies and procedures

• Submit regular reports to management and governance structures on compliance with key legislation

• Corrective or disciplinary action for misconduct

• Focus on preventing irregular expenditure and non-compliance – these should be a key performance

measure in senior official’s contracts

Fraud and consequence management

46% (118)

54% (136)

254

MUN

22

Not investigated Investigated

Allegations of financial and/or fraud and

SCM misconduct (151 municipalities)

39%

Control environment

101 (38%) municipalities did not have sufficient mechanisms for reporting and investigating transgressions or possible fraud

Most common findings:

• Disciplinary board not established at 73 municipalities

• No hot-line at 53 municipalities

• No policies for investigations at 50 municipalities

Previous year unauthorised, irregular and fruitless and

wasteful expenditure reported for investigation

28% (43)

17% (26)

9% (14)

Allegations not investigated

Investigations took longer than three months

Allegations not properly investigated

23

R22 763 m (82%)

R18 824 m (78%)

R2 088 m (89%)

R3 937 m (14%)

R3 639 m (15%)

R242 m (10%)

R1 m <1%

R 7 m < 1%

R6 m (1%)

Irregular expenditure(R27 887 million)

Unauthorisedexpenditure

(R24 259 million)

Fruitless and wastefulexpenditure

(R2 336 million)

Recovered Condoned or authorised through

adjustment budget Written off Not dealt with

R6 012 m (54%)

R7 296 m (57%)

R893 m (78%)

R3 937 m (35%)

R3 639 m (29%)

R242 m (21%)

R 1 m < 1%

R 7 m < 1%

R6 m (1%)

Irregular expenditure(R11 136 million)

Unauthorisedexpenditure

(R12 731 million)

Fruitless and wastefulexpenditure

(R1 141 million)

Movement of unauthorised, irregular and

fruitless and wasteful expenditure as a

percentage of amount incurred in previous year

Movement of unauthorised, irregular and

fruitless and wasteful expenditure as a

percentage of previous year’s closing balance

R1 186 m (4%)

R1 789 m (7%)

R1 186 m (11%)

R1 789 m (14%)

Movement in UIFW balances

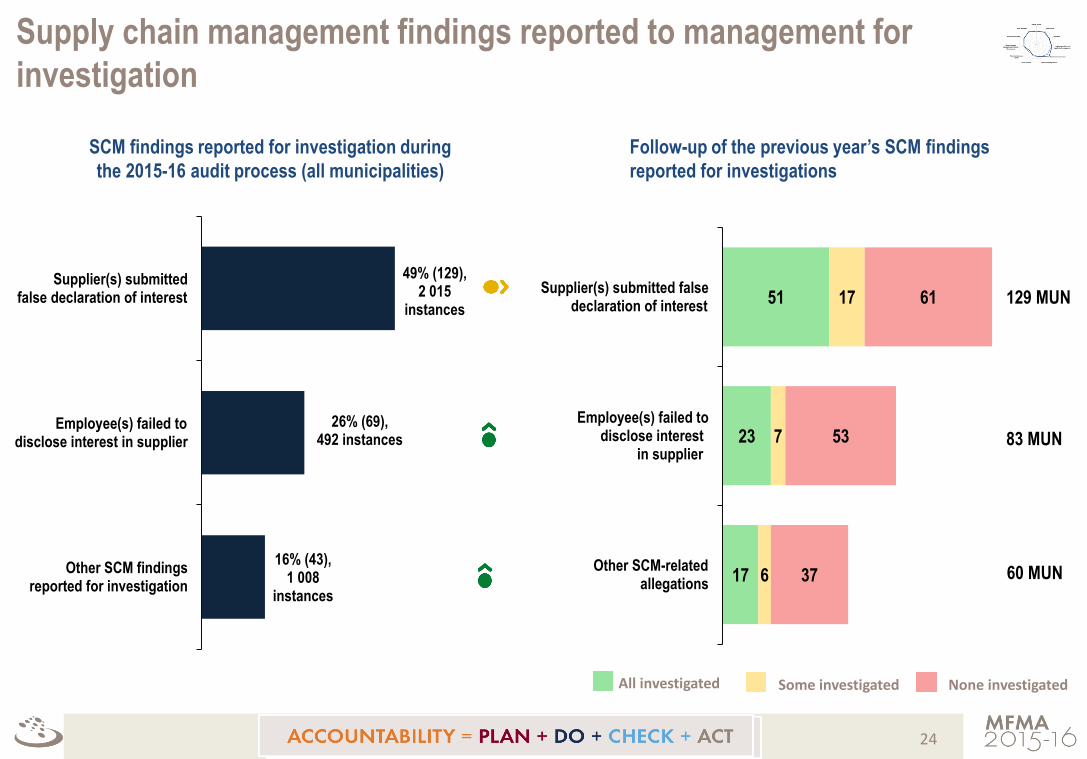

Supply chain management findings reported to management for

investigation

16% (43), 1 008

instances

26% (69), 492 instances

49% (129), 2 015

instances

Other SCM findingsreported for investigation

Employee(s) failed todisclose interest in supplier

Supplier(s) submittedfalse declaration of interest

SCM findings reported for investigation during

the 2015-16 audit process (all municipalities)

24

Follow-up of the previous year’s SCM findings

reported for investigations

All investigated Some investigated None investigated

17

23

51

6

7

17

37

53

61

Other SCM-related allegations

Employee(s) failed to disclose interest in supplier

Supplier(s) submitted false declaration of interest

129 MUN

83 MUN

60 MUN

Unauthorised expenditure over three years 2015-16

MFMA

R10 181 m (80%)

R9 029 m (72%)

R7 006 m (70%)

R2 590 m (20%) R3 702 m

(28%)

R3 067 m (30%)

2015-16 2014-15 2013-14

R12 771 m

(181 municipalities [69%])

R10 073 m

(187 municipalities [71%])

R12 731 m

(190 municipalities [72%])

Identified by auditees Identified during audit

55% (R7 024 m)

64% (R8 146 m)

59% (R5 939 m)

Non-cash items including depreciations, impairments, debt

written off etc.

25

31%

99% (2014-15: 97%) of occurrences caused by overspending of budget / main sections in budget

EC R856 million

(7%) FS R1 294 million (10%)

GP R3 536 million (28%) KZN

R1 623 million (13%) LP

R1 017 million (8%)

MP R1 713 million (13%)

NC R568 million

(4%)

NW R1 954 million (15%)

WC R210 million

(2%)

Provincial breakdown of

unauthorised expenditure incurred

Financial health

35% (93)

33% (86)

32% (84)

Financial viability of municipalities is on a steady decline

• incurred a deficit

• in net current liability position

• were able to pay their creditors in less than 30 days

• took more than 120 days to pay their creditors

• are able to collect monies owed to them in less than 90 days

• took more than 120 days to collect money owed to them

• deem more than 10% of their debt to be non-recoverable

26

Good

Of concern

Intervention required

35%

93%

44%

46%

40%

17%

33%

44%

Planning, managing and reporting on performance

27

The process

Plan and budget

Monitor and in-year reporting

Report performance in annual

performance report (APR)

49%

The findings

• 37 municipalities (14%) did not set key performance indicators for delivery of

basic services (water, electricity, sanitation and refuse removal)

• Indicators not well defined (23%) or verifiable (21%)

• Targets not measurable (18%) or specific enough (16%)

• 27 municipalities (10%) had no performance management systems

• 26 municipalities (10%) had inadequate performance management systems

• 17 municipalities (6%) had no mechanisms to monitor or review performance

• 3% did not prepare APR – 6 from the Northern Cape

• Reported information not consistent with what was included in the plan (24%)

• Reported achievement was not reliable at 45% municipalities

• 80% of APR submitted for audit was materially misstated. After corrections were made, it was 49%, an improvement from the 38% in 2014-15

• Progress made towards useful and reliable performance reporting is slow. This affects the ability of communities to hold municipalities

accountable and makes it difficult for provincial and national government to track progress towards the service delivery goals.

Water and sanitation – grant funding and performance reporting

79% (117)

18% (27)

3% (4)

85% (127)

13% (20)

2% (2)

Sanitation (150 WSA) Water (148 WSA)

72% (107)

14% (21)

14% (20)

75% (113)

16% (24)

9% (13)

Grant funding

Performance

reporting

Reliable reporting

Reported but not reliable

No reporting

Grant used

Grant not fully used

Grant funding used for other purposes

28

16 of these municipalities also

did not plan for the provision

of water services in the

SDBIP/IDP

21 of these municipalities also

did not plan for the provision

of sanitation services in the

SDBIP/IDP

29

Performance audit report on Water infrastructure

• Focused on the planning, project management

and implementation of projects in ten district

municipalities in six provinces

• Tabled on 30 November 2016

• Weaknesses identified in areas of leadership

and oversight, funding, project management

and operations and intergovernmental

coordination

The projects in progress do not address the cause of the water backlog reported

Projects exceeded planned completion date

Projects had significant findings on supply chain management

Findings on water infrastructure projects and maintenance in local government

Water infrastructure projects

at 148 municipalities

Maintenance of water infrastructure

at 148 municipalities

20%

28%

22%

No policy on maintenance of water infrastructure

No maintenance plan

Conditional assessment not done to inform the maintenance plan and budget

Maintenance was not budgeted for

Appropriate steps not taken to prevent over-/underspending of the budget allocation for routine water infrastructure maintenance

Targets and time frames for routine maintenance of water infrastructure were not achieved

56%

45%

34%

24%

20%

16%

30

Sanitation infrastructure projects and maintenance

Sanitation infrastructure projects at 150 municipalities

The projects do not address the cause of the sanitation backlog reported

Projects exceeded planned completion date

Projects had significant findings on supply chain management

18%

25%

19%

31

65% (426)

35% (226)

Key projects funded by the municipal infrastructure grant (MIG)

32

Targets achieved Targets not achieved / not evaluated

• 652 key projects audited at 234 municipalities

• municipalities did not use grants in line with the grants framework

• Only of the R15,04 billion in grants was not spent

SCM findings and incorrect

accounting identified

Achievement of planned targets - projects

29% (192)

13% (84)

SCM findings(652 projects)

Incorrect accounting(652 projects)

Projects managed by municipalities

18%( 7)

3% (1)

SCM findings(38 projects)

Incorrect accounting(38 projects)

Projects managed by implementing agents

652

projects 7%

15

Management of USDG and PTNG

Urban settlements

development grant (USDG)

2015-16

R10,55 billion

(7 municipalities [3%])

89% (16)

11% (2)

2015-16

18 projects

2015-16

84% (16)

16% (3)

2015-16

33

Public transport

network grant (PTNG)

R5,36 billion

(11 municipalities [4%]) R0,54 billion (5%)

R10,01 billion (95%) R0,55 billion (10%)

R4,8 billion (90%)

19 projects

Spent Not spent

Targets achieved Targets not achieved/ not evaluated

• Projects have generally been

successfully implemented and

goods and services received for

the money spent

• In some projects, delays resulted in

variation orders; quality issues due

to lack of maintenance and project

management failures due to

inadequate planning

• All design specifications were not

approved before tenders were invited

for projects

• SCM findings on grant projects were

reported in some cases.

Human resource management

27% (72)

47% (122)

26% (69)

• Biggest improvements in EC

• Biggest regression in KZN

• Inadequate performance management at 125 municipalities (no signed performance contracts for some senior managers at 38 municipalities)

• 59 of 72 (82%) municipalities maintained their status of “good” assessment

• 57 of 69 (83%) municipalities remained in the red zone from the previous year

34

Good

Of concern

Intervention required

27%

Status of human resource management controls

Vacancies, stability and achievement of competency requirements –

municipal managers and chief financial officers

35

7% (18)

8% (20)

5% (14)

4% (11)

13% (35)

19% (50)

12% (30)

16% (41)

2014-15

2015-16

2014-15

2015-16 20% (52)

17% (44)

27% (70)

20% (53)

Vacant for less than 6 months Vacant for 6 months

or more

Average number of months in

position

Did not meet minimum

competency requirements

Minimum competencies

not assessed/ limitation

40 months

47 months

43 months

50 months

2014-15

2015-16

2014-15

2015-16

8% (17)

9% (20)

8% (16)

12% (26)

6% (12)

7% (16)

3% (6)

6% (12)

2015-16

2014-15

2015-16

2014-15

14% (29)

16% (36)

11% (22)

18% (38)

Vacancy at

year-end

Stability (average of

months in

position)

Competency (non-achievement

of minimum

competency

requirements)

Municipal managers

Chief financial officers

Municipal managers

Chief financial officers

Municipal managers

Chief financial officers

33% (85)

49% (125)

60% (152)

Inadequate planning and appointment process

No transfer of skills

Poor performance management and monitoring

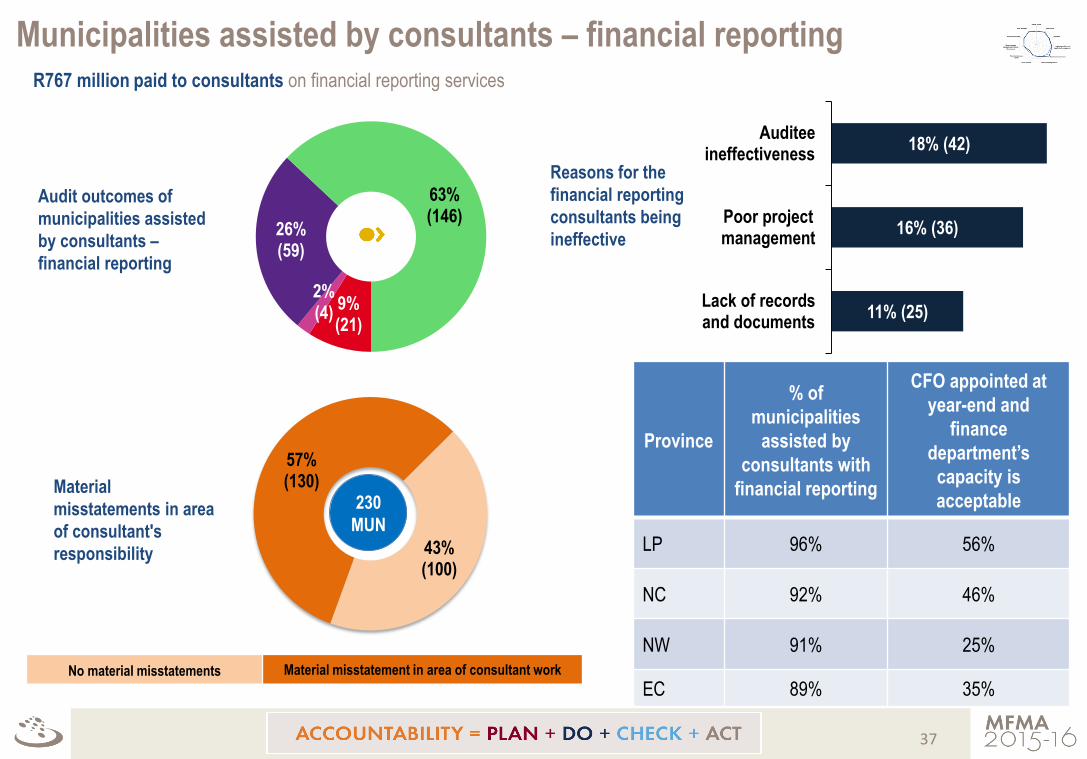

Effective use of consultants – overall

Findings from the audit on the use of consultants at 254 municipalities where consulting services were intellectual or advisory in

nature on financial reporting services, preparation of performance information, IT related services or other services.

36

• Measures to monitor contract performance and delivery not defined and/ or implemented

(82 municipalities)

• No evaluation performed to determine if the consultancy rendered, meet the initial project objectives,

needs and deliverables (36 municipalities)

• No evidence that skills transfer or training programmes took place (101 municipalities)

• Measures to monitor the transfer of skills according to contract not implemented (80 municipalities)

• Requirements/ objectives/ key details of transfer of skills not included in the terms of reference

(65 municipalities)

• Consultants appointed without conducting needs assessment or gap analysis (65 municipalities)

• Consultants appointed without any terms of reference (34 municipalities)

• Inadequate terms of reference used (19 municipalities)

9% (21)

2% (4)

26% (59)

63% (146)

Municipalities assisted by consultants – financial reporting

Audit outcomes of

municipalities assisted

by consultants –

financial reporting

37

Province

% of

municipalities

assisted by

consultants with

financial reporting

CFO appointed at

year-end and

finance

department’s

capacity is

acceptable

LP 96% 56%

NC 92% 46%

NW 91% 25%

EC 89% 35%

57% (130)

43% (100)

230

MUN

No material misstatements Material misstatement in area of consultant work

Material

misstatements in area

of consultant's

responsibility

11% (25)

16% (36)

18% (42)

Lack of recordsand documents

Poor projectmanagement

Auditeeineffectiveness

Reasons for the

financial reporting

consultants being

ineffective

R767 million paid to consultants on financial reporting services

27% 23% 25%

60% 61%

49%

13% 16% 26%

Sen

ior

m

anag

emen

t

Mun

icip

al m

anag

ers

/ ch

ief e

xecu

tive

offic

ers

May

ors

First level of assurance – management/leadership

Assurance

provider

Responsibility

Senior

managers

• Task/project leadership

• “Doing the basics right”

• Supervision and review

• Timely implementation of action plans and recommendations

Municipal

managers/

CFOs

• Administrative leadership, guidance and oversight

• Enabling delivery

• Monitor and report on progress of action plans

• Hold staff accountable

• Investigate all allegations of fraud

• Reporting channel between administrative and political leadership

Mayors

• Political leadership, guidance and oversight

• Reporting channel between executive leadership and legislature

• Political accountability

38

Provides assurance Provides some assurance Provides limited/no assurance

26%

Inte

rnal

aud

it

units

Aud

it co

mm

ittee

s

Second level of assurance – Internal independent assurance and

oversight

Tre

asur

ies,

coo

pera

tive

gove

rnan

ce

depa

rtm

ents

,

prem

ier’s

offi

ces

1% 3%

17% 16% 28%

45% 43%

62%

37% 38%

10%

Assurance

provider

Responsibility

Internal audit

• Report to strengthen control environment

• Advise on organisational systems, processes and practices

• Advise on organisational effectiveness

Audit

committee

• Interrogate and advise management

• Review financial and performance reporting before audit

• Ensure appropriate reaction to findings

Coordinating /

monitoring

departments

• Guide and enable service delivery in coordinated effort (OTP)

• Ensure proper inter-governmental coordination (OTP)

• Hold cabinet / executive committee accountable (OTP)

• Monitor and provide oversight (OTP)

• Guide proper financial management / SCM (Treasuries)

• Skills development (Treasuries)

• Guide proper strategic planning and performance management

(Cogta)

• Facilitate the fight against corruption (Cogta)

39

Provides assurance Provides some assurance Provides limited/no assurance Not established

Third level of assurance – external independent assurance

and oversight M

unic

ipal

cou

ncils

Mun

icip

al p

ublic

ac

coun

ts

com

mitt

ees

1%

27% 32%

40%

47% 43%

60%

26% 24%

Por

tfolio

com

mitt

ees

on

loca

l gov

ernm

ent

Assurance

provider

Responsibility

Municipal

council/

MPAC

• Enable proper financial oversight

• Interrogate the audit outcomes

• Ensure corrective action / proper consequence management

Portfolio

committees

• Review strategic plans and related budgets, and guide government

on appropriate delivery targets and resource use

• Review performance reports and guiding appropriate action

• Ensure proper consequence management

External

audits

• Engage pro-actively

• Conducti annual audits and reporting on these

• Engage with governance structures

• Enable the work of oversight

40

Provides assurance Provides some assurance Provides limited/no assurance Not established

Audit outcomes over three years

5% (15)

9% (25) 12% (33)

20% (55)

1% (4) 1% (4)

1% (3)

23% (63) 27% (76)

26% (71)

44% (122) 41% (111)

39% (109)

18% (49) 19% (54) 14% (40)

2015-16 2014-15 2013-14

41

18%

278 municipalities

Improved

Unchanged

Regressed

Outstanding

audits

Unqualified with no

findings = 49 2 (DM), 7 (LM)

1 (MET)

12 (DM)

27 (LM)

Unqualified with

findings = 122

3 (DM), 16 (LM)

2 (LM)

2 (MET)

11 (DM)

75 (LM)

2 (MET)

4 (DM)

7 (LM)

1 (MET)

2 (LM)

Qualified with

findings = 63

1 (LM)

8 (LM)

2 (MET)

4 (DM)

38 (LM)

1 (LM)

3 (DM), 6 (LM) 3 (LM)

Adverse with

findings = 4 2 (DM), 1 (LM) 1 (LM)

Disclaimed with

findings = 25

2 (DM)

11 (LM)

1 (LM)

10 (LM)

1 (DM)

9 (LM)

Movement table (2015-16 over 2014-15)

42 36 185 15

MET – metro

DM – district municipality

LM – local municipality

Colour of the number

indicates the audit opinion

from which the auditee has

moved.

42

Status of audits that were outstanding at 15 January 2017

43

• 15 audits were outstanding on 15 January 2017 (our cut-off date), compared to

six in 2014-15

• Reasons include late (eight) or non-submission of annual financial statements (four)

and disagreements on accounting and other matters (three)

• Eleven audits were subsequently finalised resulting in:

˗ four unqualified (Mangaung Metro, Matjhabeng and Phumelela – FS, Gamagara

- NC)

˗ six qualified (Maluti-A-Phofung – FS, Grater Giyani and Mutale – LP, Dikgatlong

and Tsantsabane – NC, Rustenburg – NW)

˗ one adverse opinions (Mogalakwena – LP)

Gau

ten

g

2

6 11

4

1

2014-15 2015-16

Lim

po

po

4 5 2 1 1

14 10

10 13

2014-15 2015-16

Mp

um

alan

ga

4 2

5 8

10 8

2 3

2014-15 2015-16

Kw

aZu

lu-N

atal

1 2 1 7 5

35 42

18 11

2014-15 2015-16

Fre

e S

tate

4 3

3 8

3

12 13

1 1

2014-15 2015-16

No

rth

Wes

t 1

7 7

10 11

6 4

2014-15 2015-16

Eas

tern

Cap

e

5 4 2

19 14

16 18

5 7

2014-15 2015-16

No

rth

ern

Cap

e

6 8

4

13 11

9 9

2 2

2014-15 2015-16

Wes

tern

Cap

e

1 1 1 7 4

22 24

2014-15 2015-16

Movement per province

(municipalities)

44

1

1

2

3

1 6

2

4

4

2

2

7

14

7 4

3

5

6

1

2

3

1

2 10

3

7

1

1

1

1

Gau

ten

g

2

16 24

15 10

2014-15 2015-16

Lim

po

po

4 6 2

1 1

14 10

12 16

2014-15 2015-16

Mp

um

alan

ga

4 2

5 8

10 8

2 3

2014-15 2015-16

Kw

aZu

lu-N

atal

1 2 1 8 6

37 43

22 16

2014-15 2015-16

Fre

e S

tate

4 3

3 8

3

15 16

1 1

2014-15 2015-16

No

rth

Wes

t 1

7 7

10 12

9 6

2014-15 2015-16

Eas

tern

Cap

e

6 4 2

20 15

22 25

7 10

2014-15 2015-16

No

rth

ern

Cap

e

6 8

4

13 11

9 9

2 2

2014-15 2015-16

Wes

tern

Cap

e

1 1 1 8 5

23 25

2014-15 2015-16

Movement per province

(all auditees)

45

2

5

3

7

2

5

4

2

2

8

14

6

4

3

1

14

4

10

3

1

2

5

7

2

1

2

1

Emerging risks

1. mSCOA will be implemented from 1 July 2017

2. The use of the central supplier database (CSD) and the eTender portal was compulsory from 1 July 2016

• The SCM policy at 139 municipalities was not updated to invite quotations from suppliers registered on the CSD

• 118 municipalities still use their own database of prospective suppliers that is not synchronised with the CSD

• The SCM policy at 144 municipalities was not updated to invite competitive bids through the eTender portal

3. Contracts of municipal managers and senior management (including CFOs) are ending in 2016-17

46

18% (43)

72% (176)

10% (26)

Ready for implementation

Readiness is of concern

Readiness requires intervention

47

Source: Robert Klitgaard (academic anti-corruption research)

48

Source: Robert Klitgaard (academic anti-corruption research)

49

Source: Robert Klitgaard (academic anti-corruption research)

Stay in touch with the AGSA

50