Embed Size (px)

Citation preview

Insurance

© Allen C. Goodman 2014

This may be the HARDEST stuff you do in undergraduate economics!

Key IDEA

• Risk = We don’t KNOW if something will happen.

• Many (most?) of us DO NOT LIKE risk.

• We will PAY to avoid the consequences of risk.

Consider a club!

We are equal opportunity!

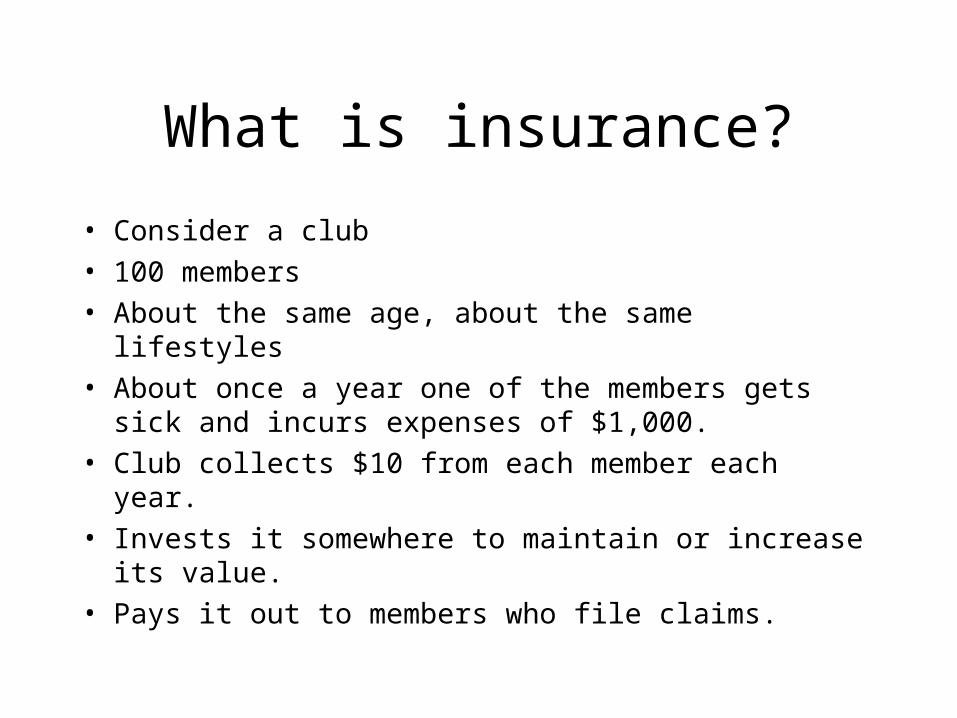

What is insurance?

• Consider a club• 100 members• About the same age, about the same lifestyles• About once a year one of the members gets sick and

incurs expenses of $1,000. • Club collects $10 from each member each year. • Invests it somewhere to maintain or increase its

value.• Pays it out to members who file claims.

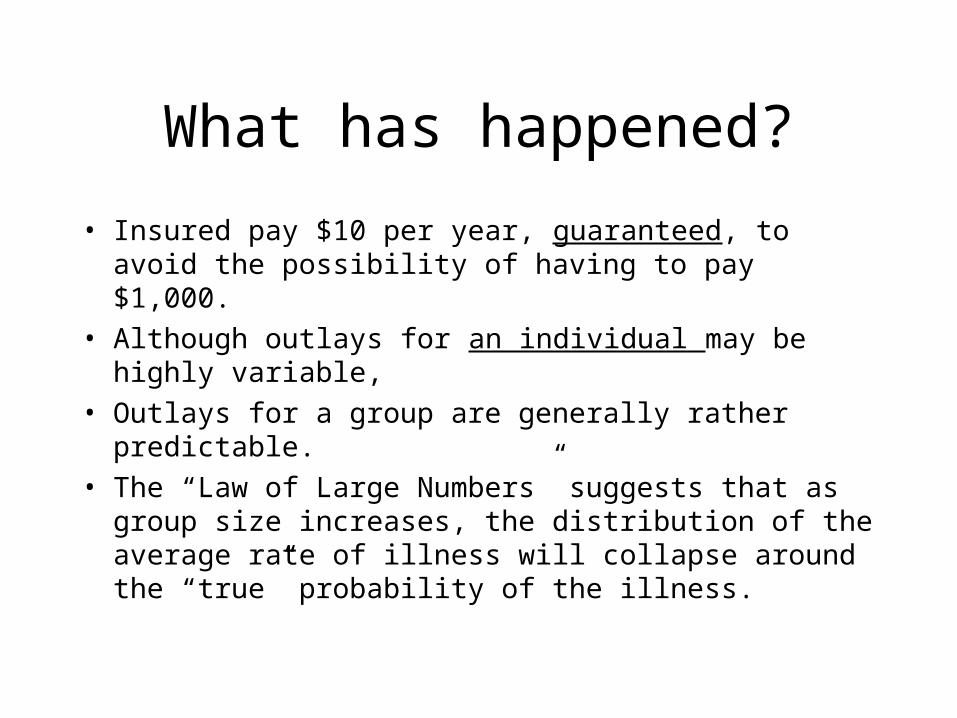

What has happened?

• Insured pay $10 per year, guaranteed, to avoid the possibility of having to pay $1,000.

• Although outlays for an individual may be highly variable,

• Outlays for a group are generally rather predictable.• The “Law of Large Numbers” suggests that as group

size increases, the distribution of the average rate of illness will collapse around the “true” probability of the illness.

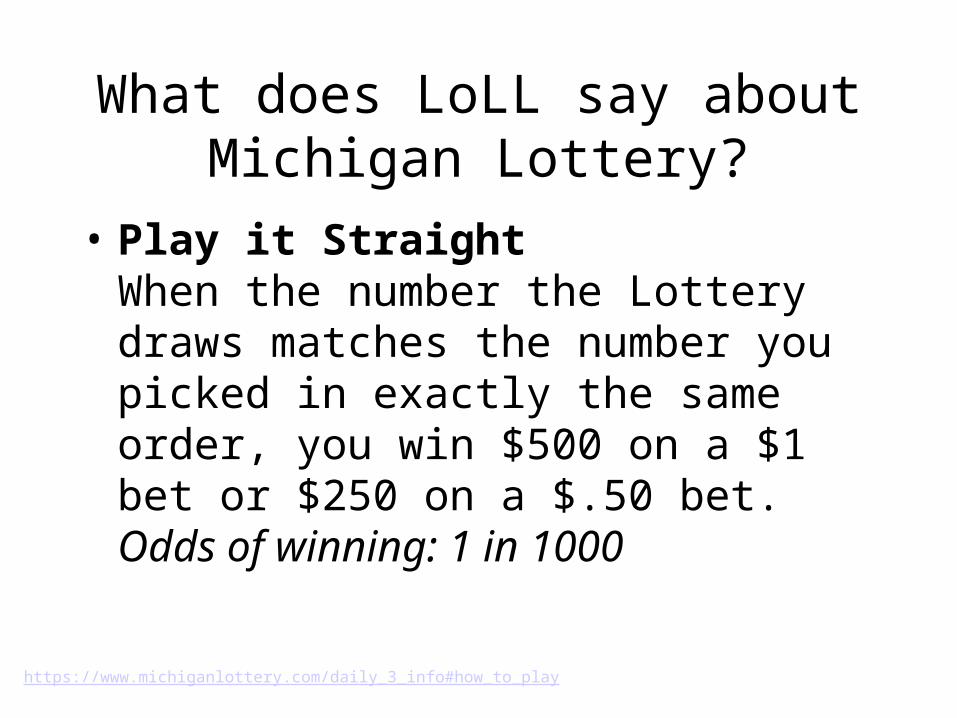

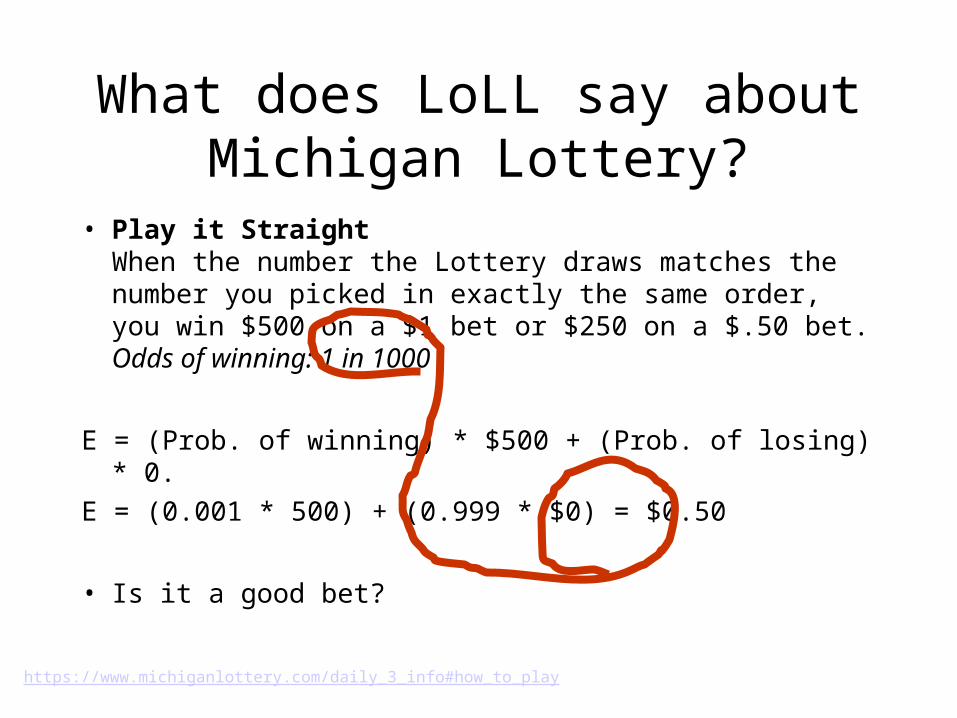

What does LoLL say about Michigan Lottery?

• Play it StraightWhen the number the Lottery draws matches the number you picked in exactly the same order, you win $500 on a $1 bet or $250 on a $.50 bet.Odds of winning: 1 in 1000

https://www.michiganlottery.com/daily_3_info#how_to_play

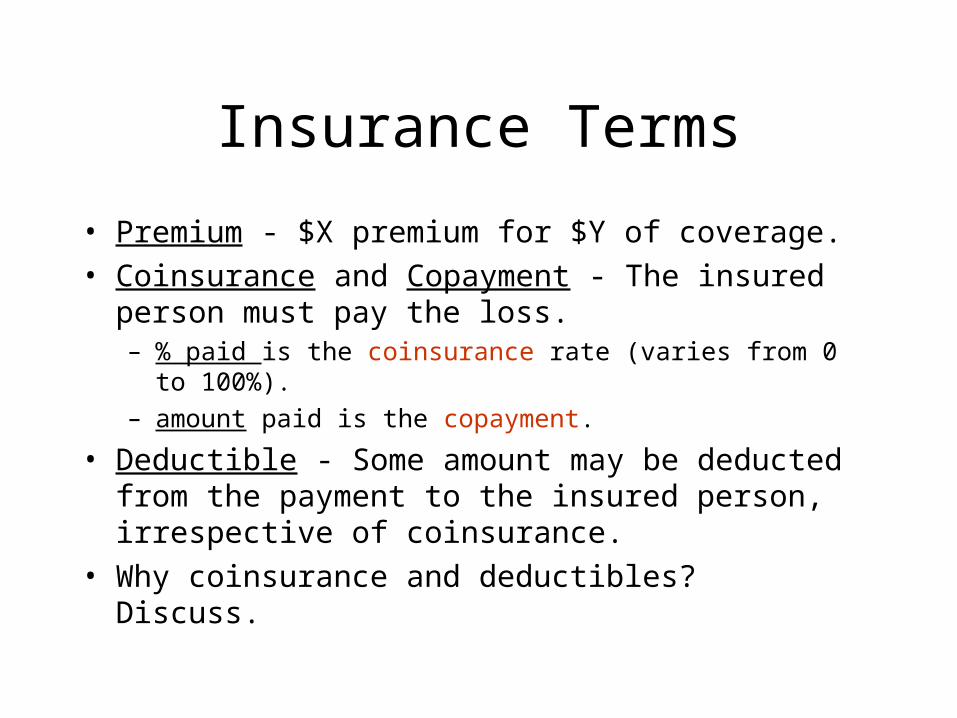

Insurance Terms

• Premium - $X premium for $Y of coverage.• Coinsurance and Copayment - The insured person

must pay the loss. – % paid is the coinsurance rate (varies from 0 to 100%).– amount paid is the copayment.

• Deductible - Some amount may be deducted from the payment to the insured person, irrespective of coinsurance.

• Why coinsurance and deductibles? Discuss.

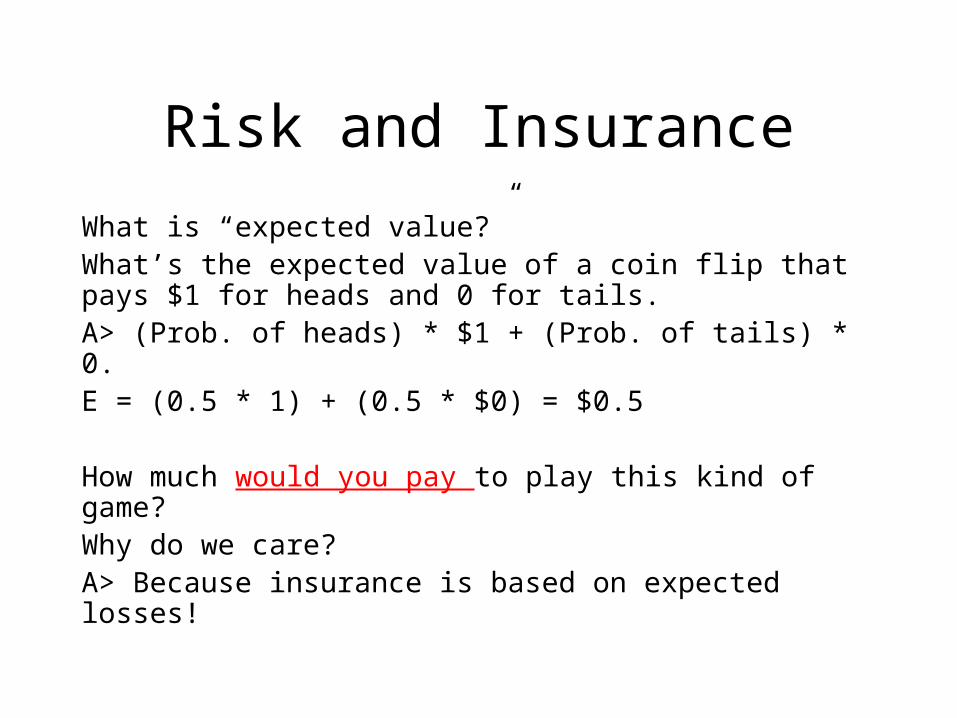

Risk and Insurance

What is “expected value?”What’s the expected value of a coin flip that pays $1 for heads and 0 for tails.A> (Prob. of heads) * $1 + (Prob. of tails) * 0.E = (0.5 * 1) + (0.5 * $0) = $0.5

How much would you pay to play this kind of game?Why do we care?A> Because insurance is based on expected losses!

What does LoLL say about Michigan Lottery?

• Play it StraightWhen the number the Lottery draws matches the number you picked in exactly the same order, you win $500 on a $1 bet or $250 on a $.50 bet.Odds of winning: 1 in 1000

E = (Prob. of winning) * $500 + (Prob. of losing) * 0.

E = (0.001 * 500) + (0.999 * $0) = $0.50

• Is it a good bet?

https://www.michiganlottery.com/daily_3_info#how_to_play

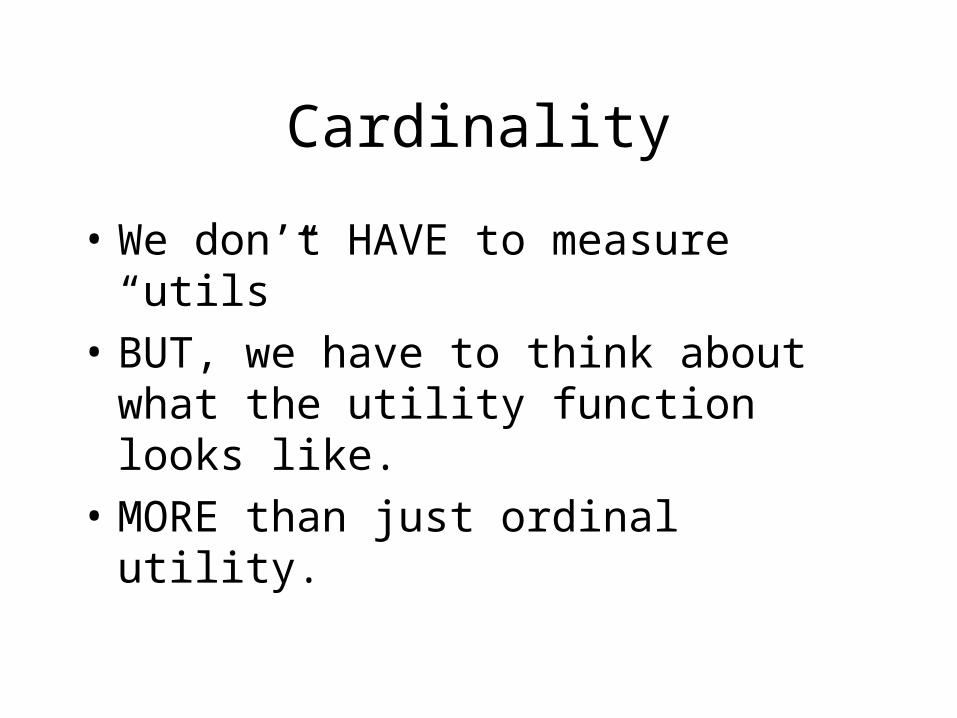

Cardinality

• We don’t HAVE to measure “utils”

• BUT, we have to think about what the utility function looks like.

• MORE than just ordinal utility.

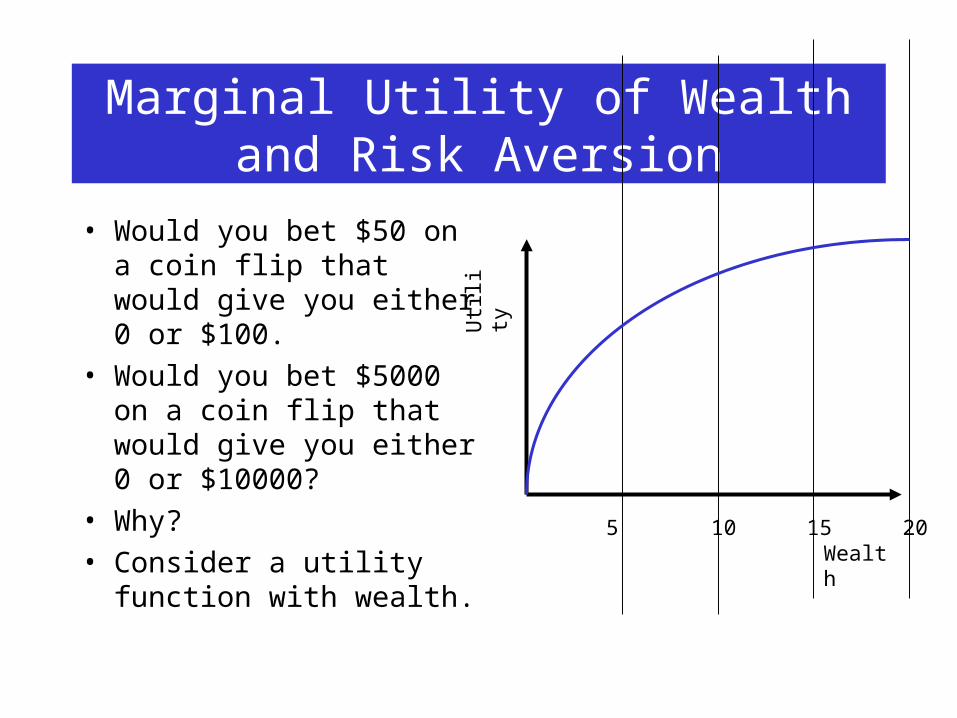

Marginal Utility of Wealth and Risk Aversion

• Would you bet $50 on a coin flip that would give you either 0 or $100.

• Would you bet $5000 on a coin flip that would give you either 0 or $10000?

• Why?• Consider a utility function

with wealth. Wealth

Util

ity

5 10 15 20

Marginal Utility of Wealth and Risk Aversion

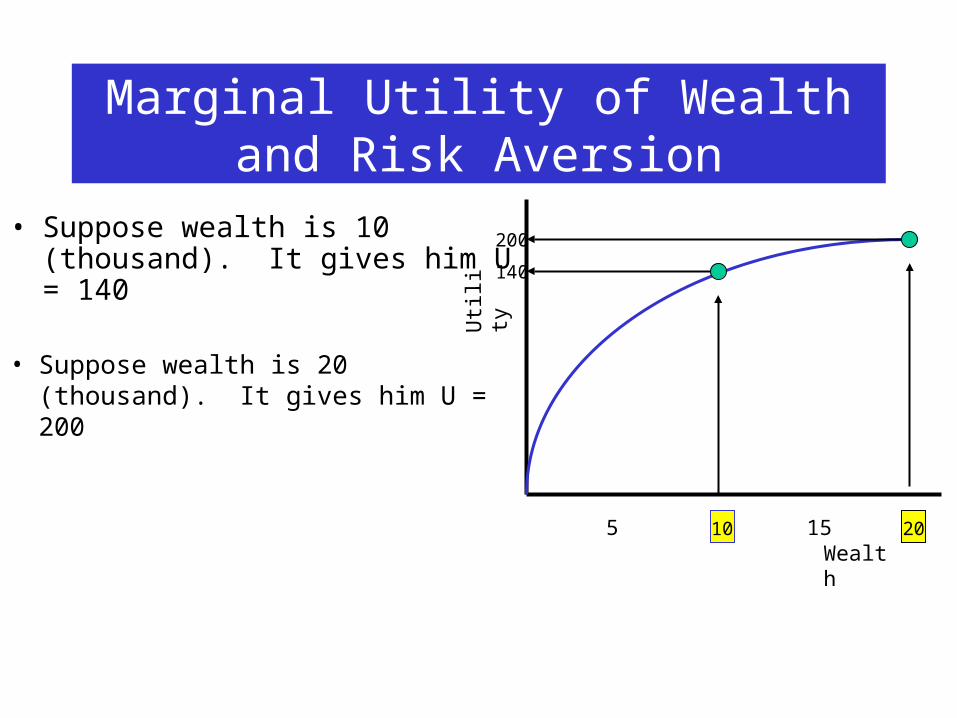

• Suppose wealth is 10 (thousand). It gives him U = 140

Wealth

Util

ity

5 10 15 20

140

• Suppose wealth is 20 (thousand). It gives him U = 200

200

Cardinal Utility

• Just about everywhere else in microeconomics we use “ordinal utility”.

• Here we use “cardinal utility.”

• Why?

Expected wealth is due to risk

Wealth

Util

ity

5 10 15 20

140

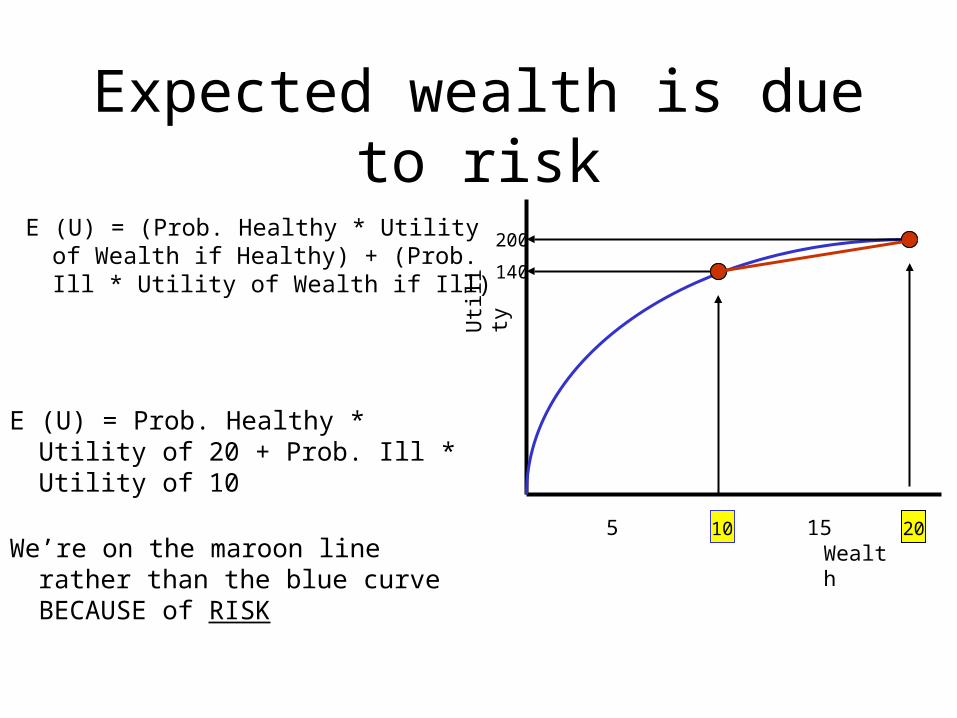

200E (U) = (Prob. Healthy * Utility of Wealth if Healthy) + (Prob. Ill * Utility of Wealth if Ill)

E (U) = Prob. Healthy * Utility of 20 + Prob. Ill * Utility of 10

We’re on the maroon line rather than the blue curve BECAUSE of RISK

Expected wealth is due to risk

Wealth

Util

ity

5 10 15 20

140

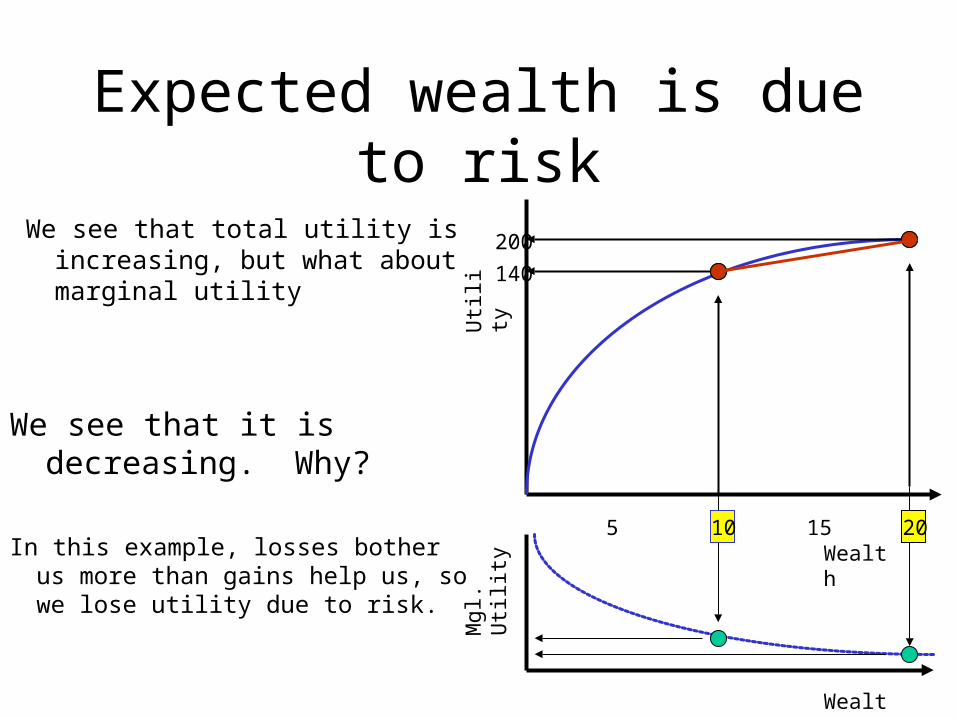

200We see that total utility is increasing, but what about marginal utility

We see that it is decreasing. Why?

In this example, losses bother us more than gains help us, so we lose utility due to risk.

Wealth

Mgl

. Util

ity

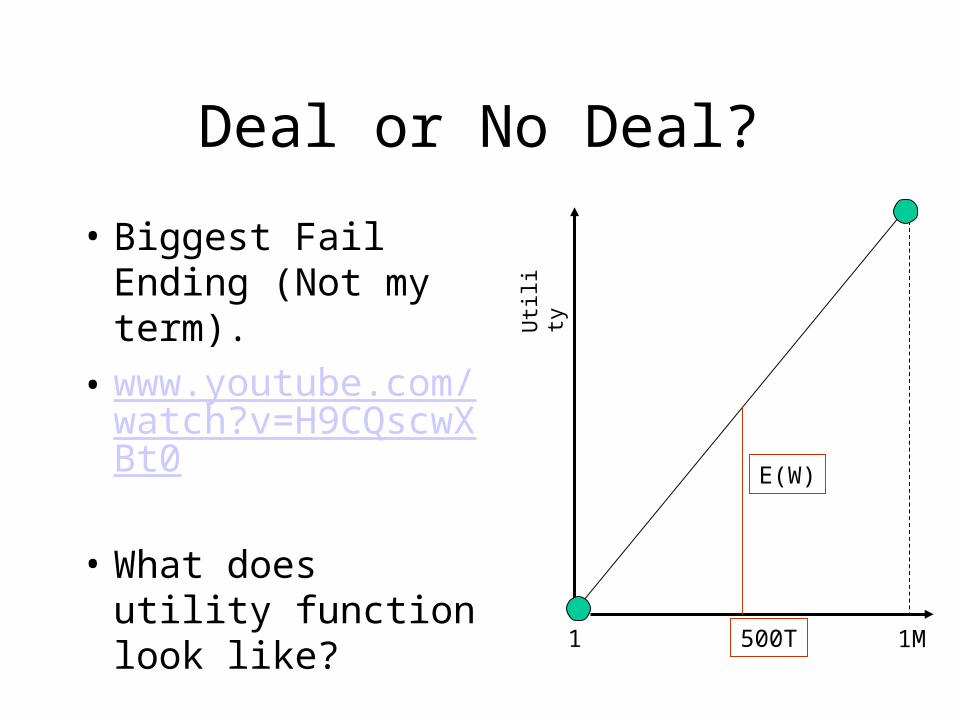

Deal or No Deal?

• Biggest Fail Ending (Not my term).

• www.youtube.com/watch?v=H9CQscwXBt0

• What does utility function look like?

1 1M500T

E(W)

Util

ity

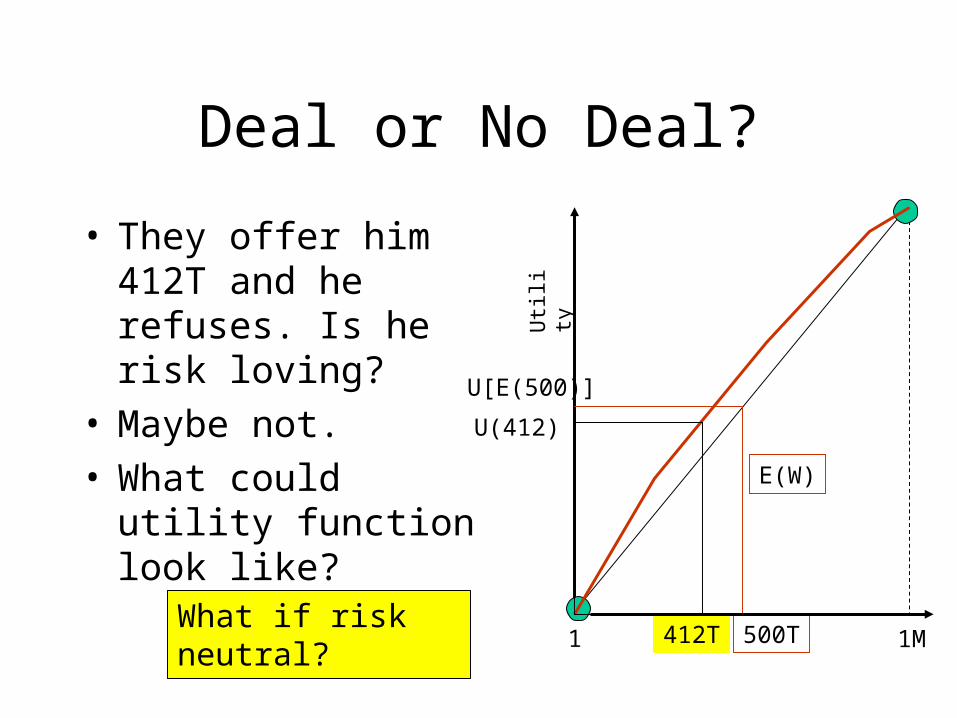

Deal or No Deal?

• They offer him 412T and he refuses. Is he risk loving?

• Maybe not.• What could utility

function look like?

1 1M500T

E(W)

412T

U(412)

U[E(500)]

Util

ity

What if risk neutral?

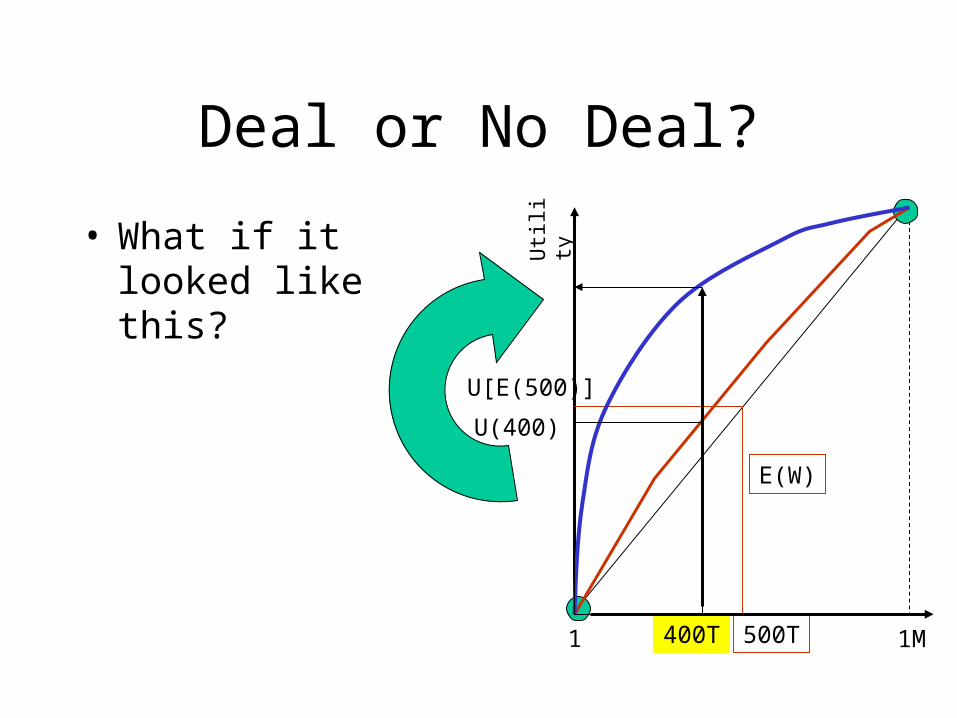

Deal or No Deal?

• What if it looked like this?

1 1M500T

E(W)

400T

U(400)

U[E(500)]

Util

ity

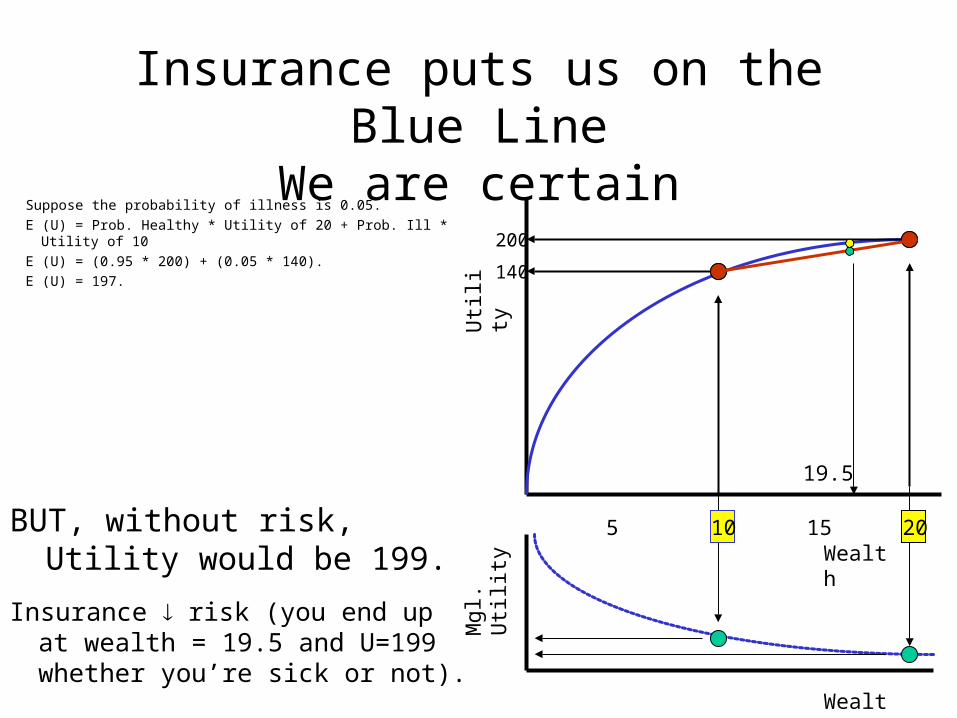

Insurance puts us on the Blue LineWe are certain

Wealth

Util

ity

5 10 15 20

140

200

Suppose the probability of illness is 0.05.

E (U) = Prob. Healthy * Utility of 20 + Prob. Ill * Utility of 10

E (U) = (0.95 * 200) + (0.05 * 140).

E (U) = 197.

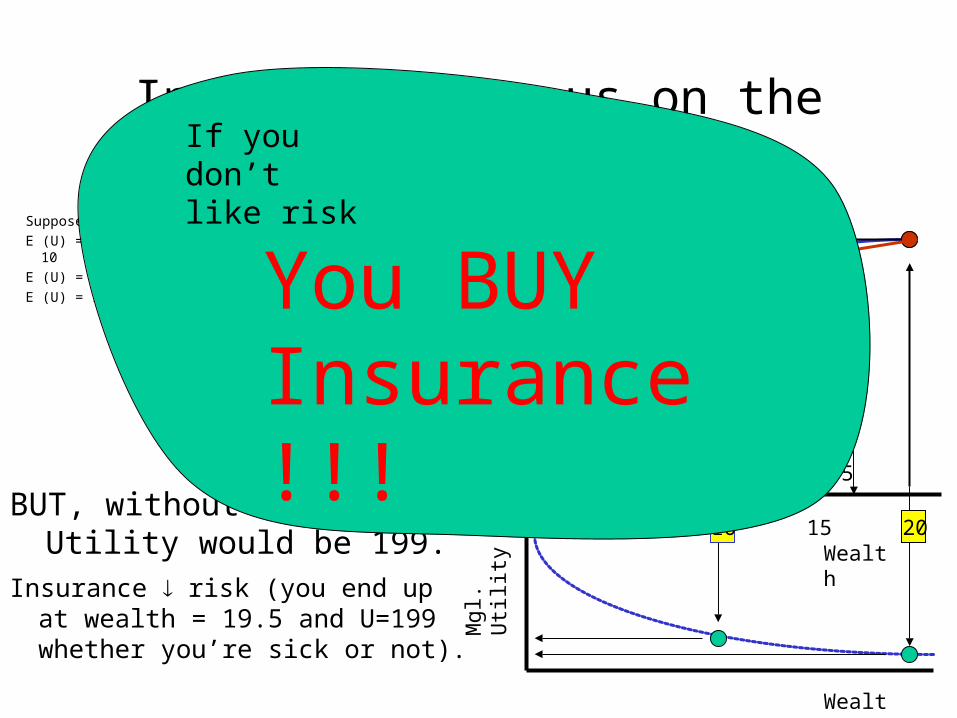

BUT, without risk, Utility would be 199.

Wealth

Mgl

. Util

ity

Insurance risk (you end up at wealth = 19.5 and U=199 whether you’re sick or not).

19.5

Insurance puts us on the Blue Line

Wealth

Util

ity

5 10 15 20

140

200Suppose the probability of illness is 0.05.

E (U) = Prob. Healthy * Utility of 20 + Prob. Ill * Utility of 10

E (U) = (0.95 * 200) + (0.05 * 140).

E (U) = 197.

BUT, without risk, Utility would be 199.

Wealth

Mgl

. Util

ity

Insurance risk (you end up at wealth = 19.5 and U=199 whether you’re sick or not).

19.5

If you don’t like risk

You BUY Insurance !!!

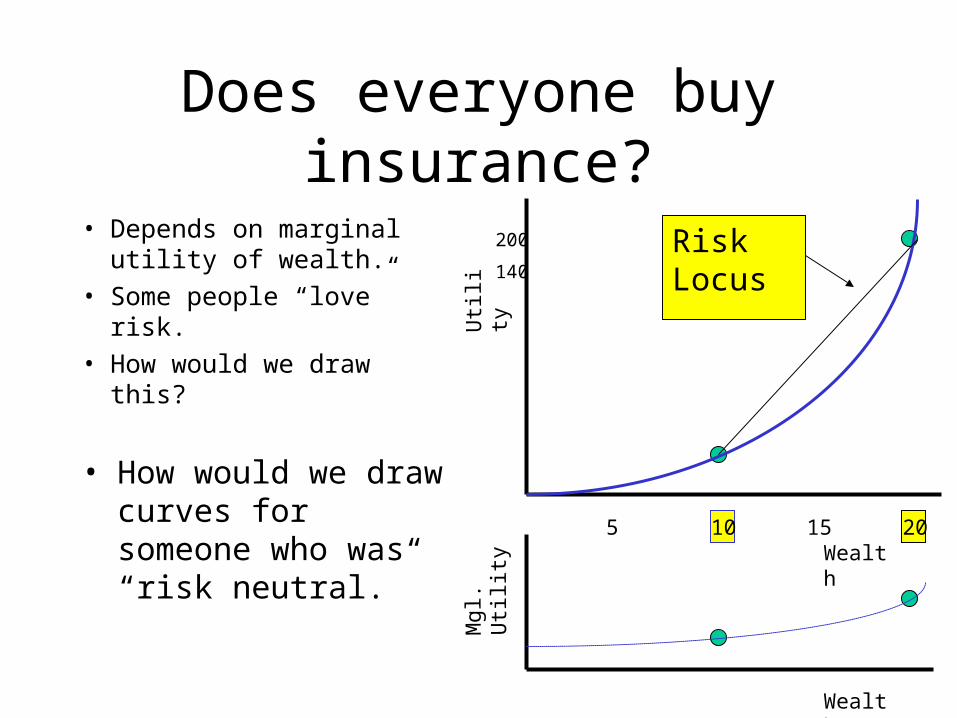

Does everyone buy insurance?

• Depends on marginal utility of wealth.

• Some people “love” risk.

• How would we draw this?

Wealth

Util

ity

5 10 15 20

140

200

Wealth

Mgl

. Util

ity• How would we draw

curves for someone who was “risk neutral.”

RiskLocus

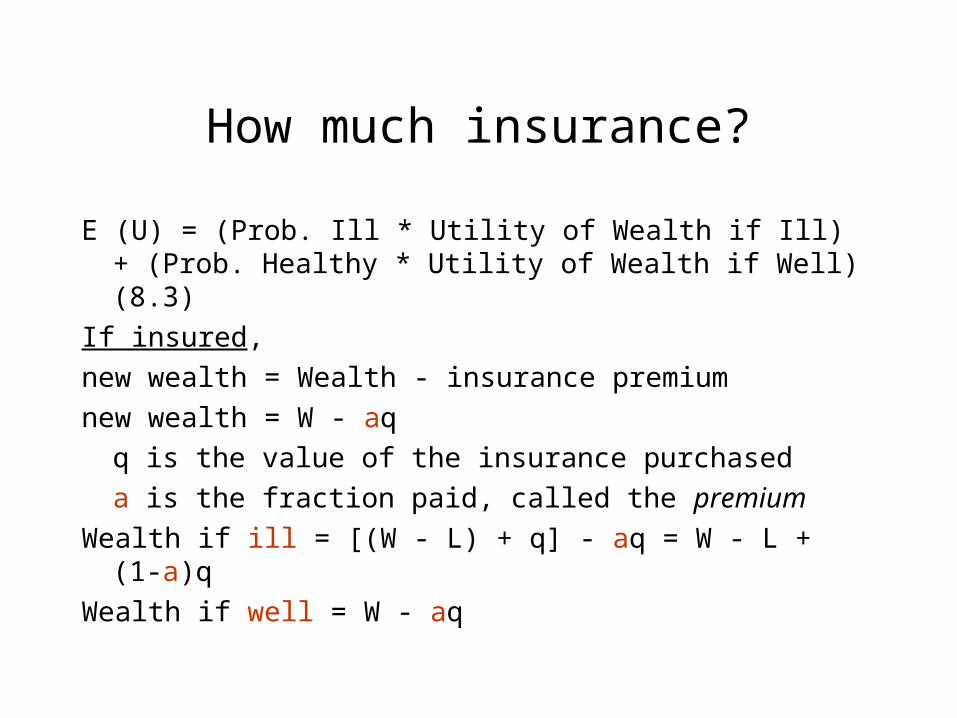

How much insurance?

E (U) = (Prob. Ill * Utility of Wealth if Ill) + (Prob. Healthy * Utility of Wealth if Well) (8.3)

If insured,

new wealth = Wealth - insurance premium

new wealth = W - aq

q is the value of the insurance purchased

a is the fraction paid, called the premium

Wealth if ill = [(W - L) + q] - aq = W - L + (1-a)q

Wealth if well = W - aq

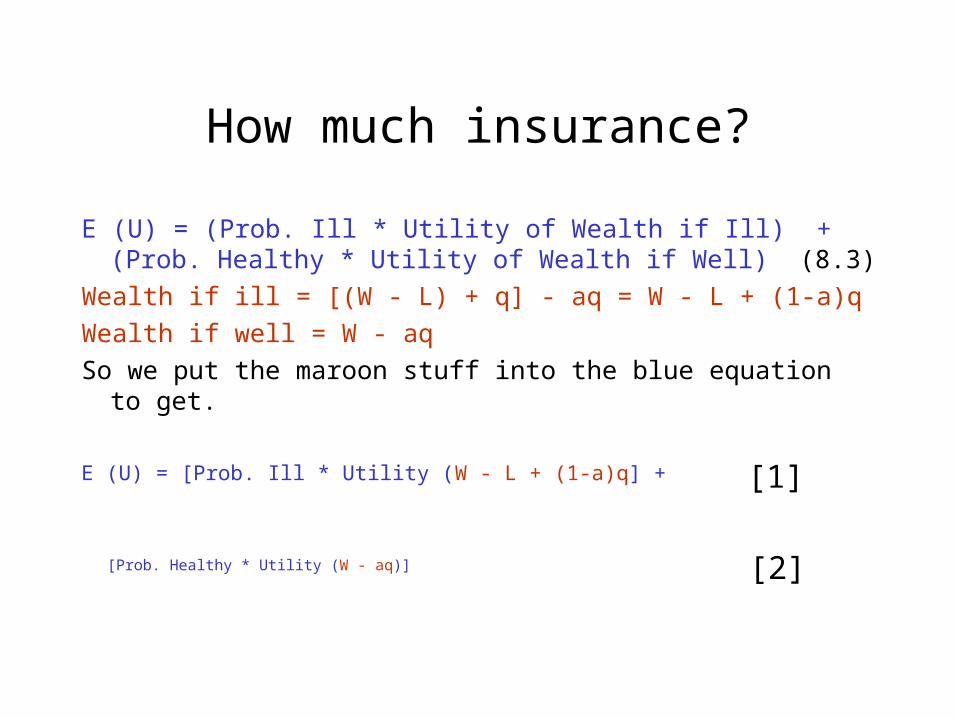

How much insurance?

E (U) = (Prob. Ill * Utility of Wealth if Ill) + (Prob. Healthy * Utility of Wealth if Well) (8.3)

Wealth if ill = [(W - L) + q] - aq = W - L + (1-a)q

Wealth if well = W - aq

So we put the maroon stuff into the blue equation to get.

E (U) = [Prob. Ill * Utility (W - L + (1-a)q] +

[Prob. Healthy * Utility (W - aq)]

[1]

[2]

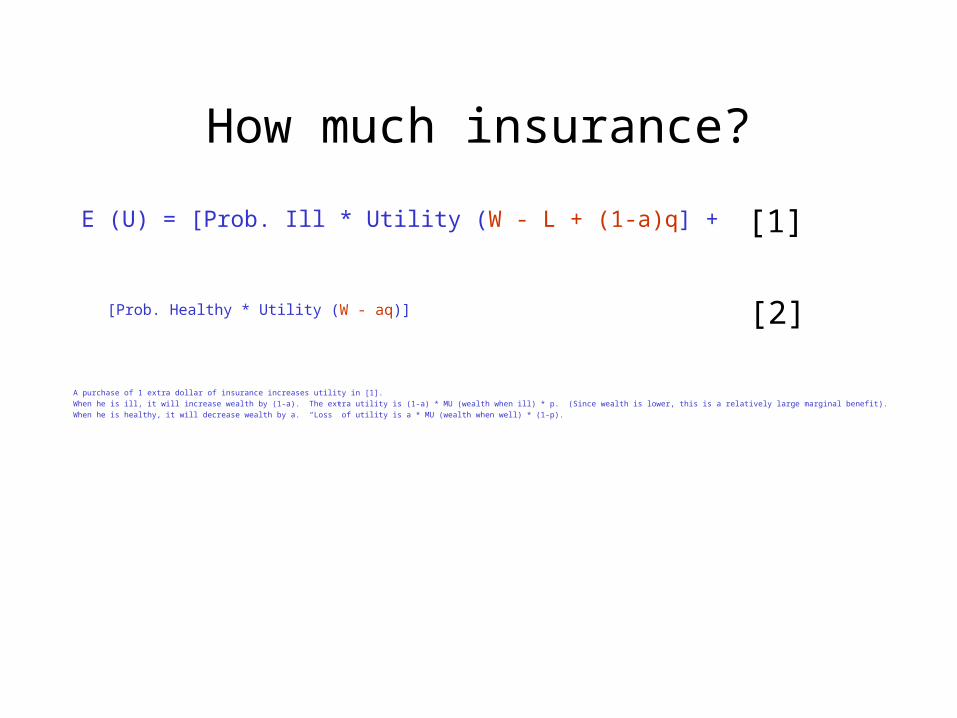

How much insurance?

E (U) = [Prob. Ill * Utility (W - L + (1-a)q] +

[Prob. Healthy * Utility (W - aq)]

[1]

[2]

A purchase of 1 extra dollar of insurance increases utility in [1].

When he is ill, it will increase wealth by (1-a). The extra utility is (1-a) * MU (wealth when ill) * p. (Since wealth is lower, this is a relatively large marginal benefit).

When he is healthy, it will decrease wealth by a. “Loss” of utility is a * MU (wealth when well) * (1-p).

Amount of Insurance

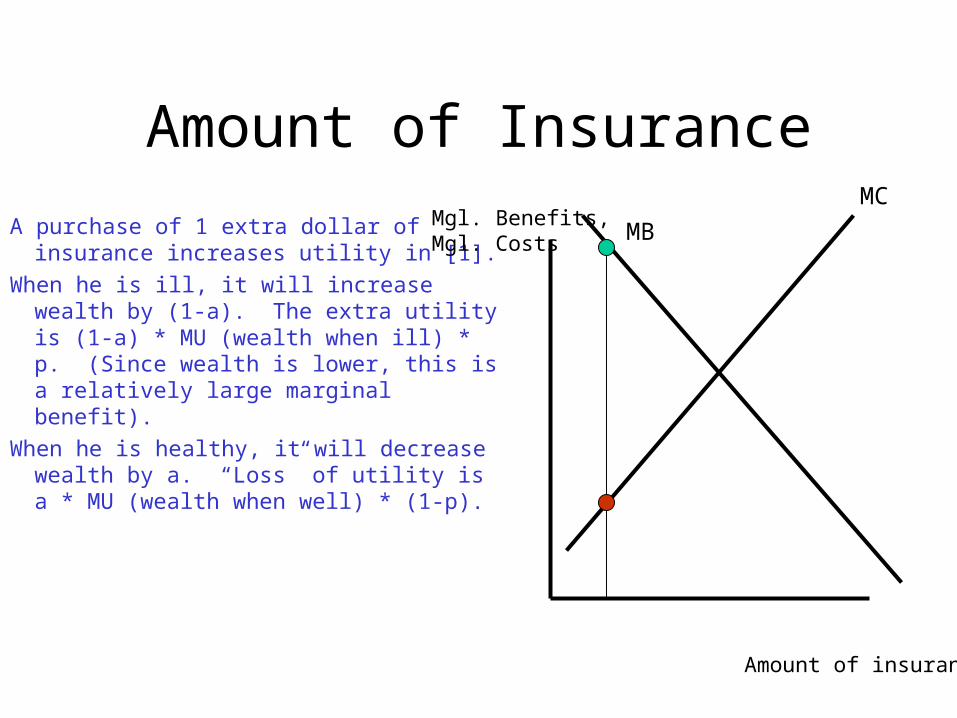

A purchase of 1 extra dollar of insurance increases utility in [1].

When he is ill, it will increase wealth by (1-a). The extra utility is (1-a) * MU (wealth when ill) * p. (Since wealth is lower, this is a relatively large marginal benefit).

When he is healthy, it will decrease wealth by a. “Loss” of utility is a * MU (wealth when well) * (1-p).

Amount of insurance

Mgl. Benefits,Mgl. Costs MB

MC

Amount of Insurance

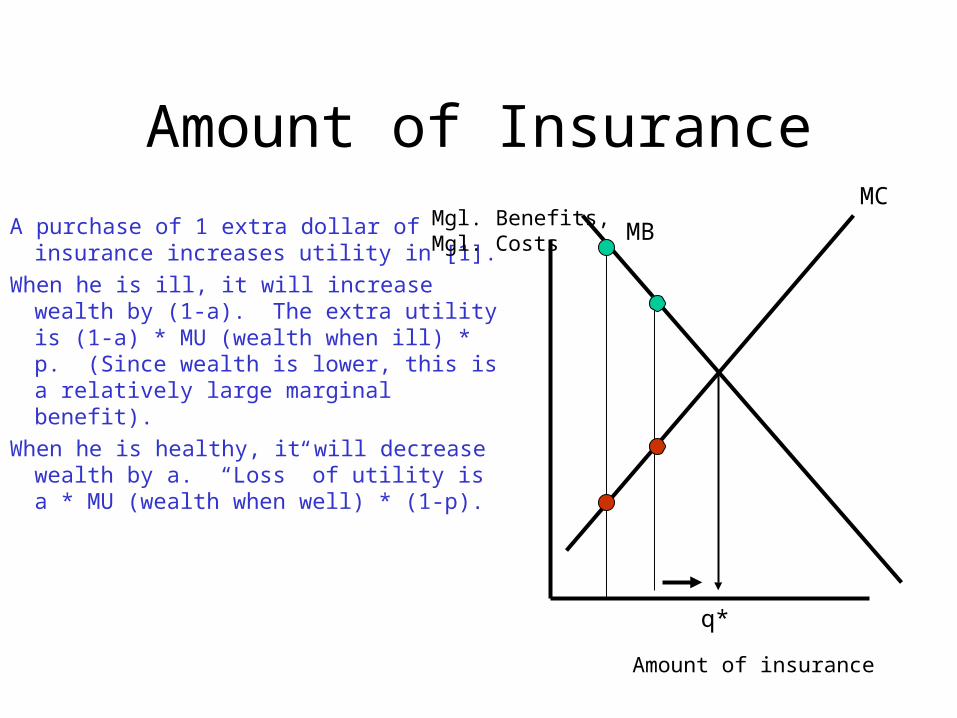

A purchase of 1 extra dollar of insurance increases utility in [1].

When he is ill, it will increase wealth by (1-a). The extra utility is (1-a) * MU (wealth when ill) * p. (Since wealth is lower, this is a relatively large marginal benefit).

When he is healthy, it will decrease wealth by a. “Loss” of utility is a * MU (wealth when well) * (1-p).

Amount of insurance

Mgl. Benefits,Mgl. Costs MB

MC

q*

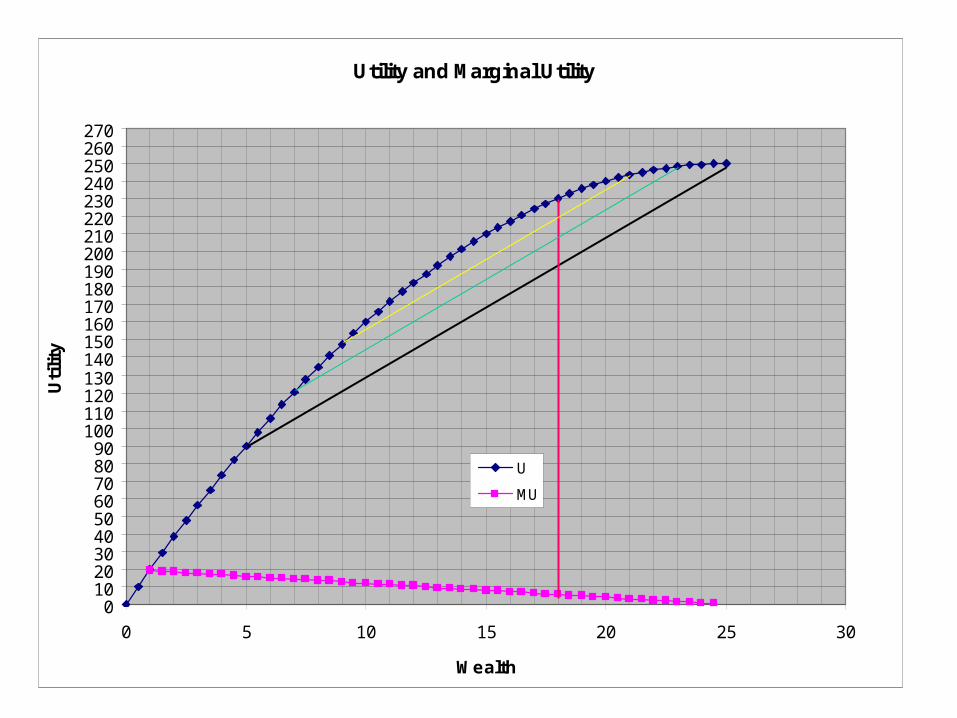

Utility and Marginal Utility

0102030405060708090

100110120130140150160170180190200210220230240250260270

0 5 10 15 20 25 30

Wealth

Uti

lity

U

MU

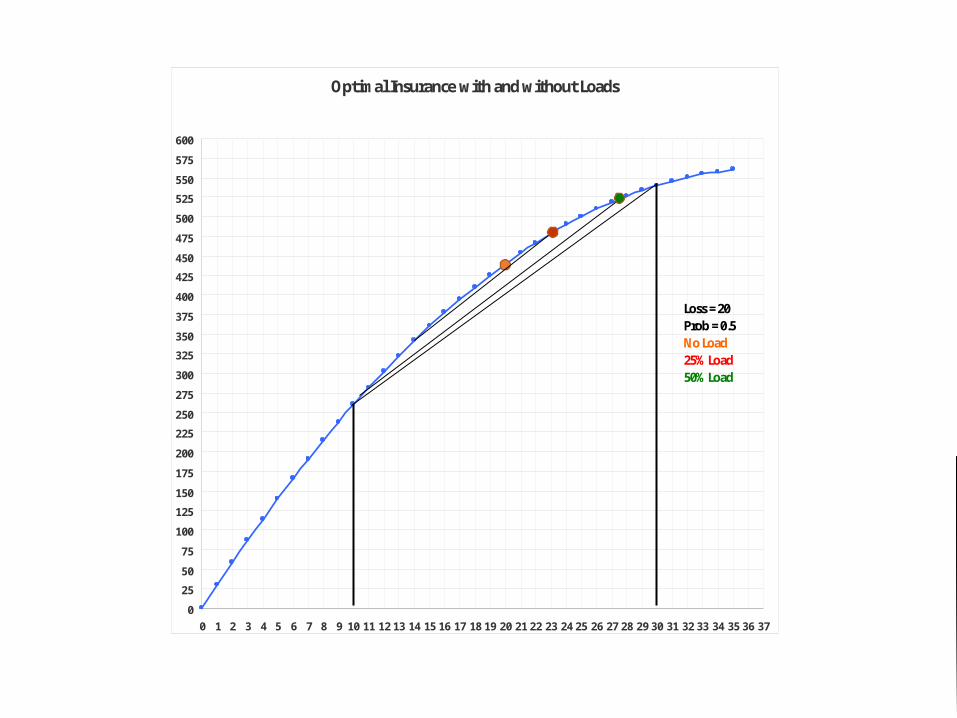

Optimal Insurance with and without Loads

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

375

400

425

450

475

500

525

550

575

600

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37

Loss = 20Prob = 0.5No Load25% Load50% Load