Embed Size (px)

Citation preview

Institutional Equities

Initi

atin

g C

over

age

Reuters: SUN.NS; Bloomberg: SUNP IN

Sun Pharmaceutical Industries

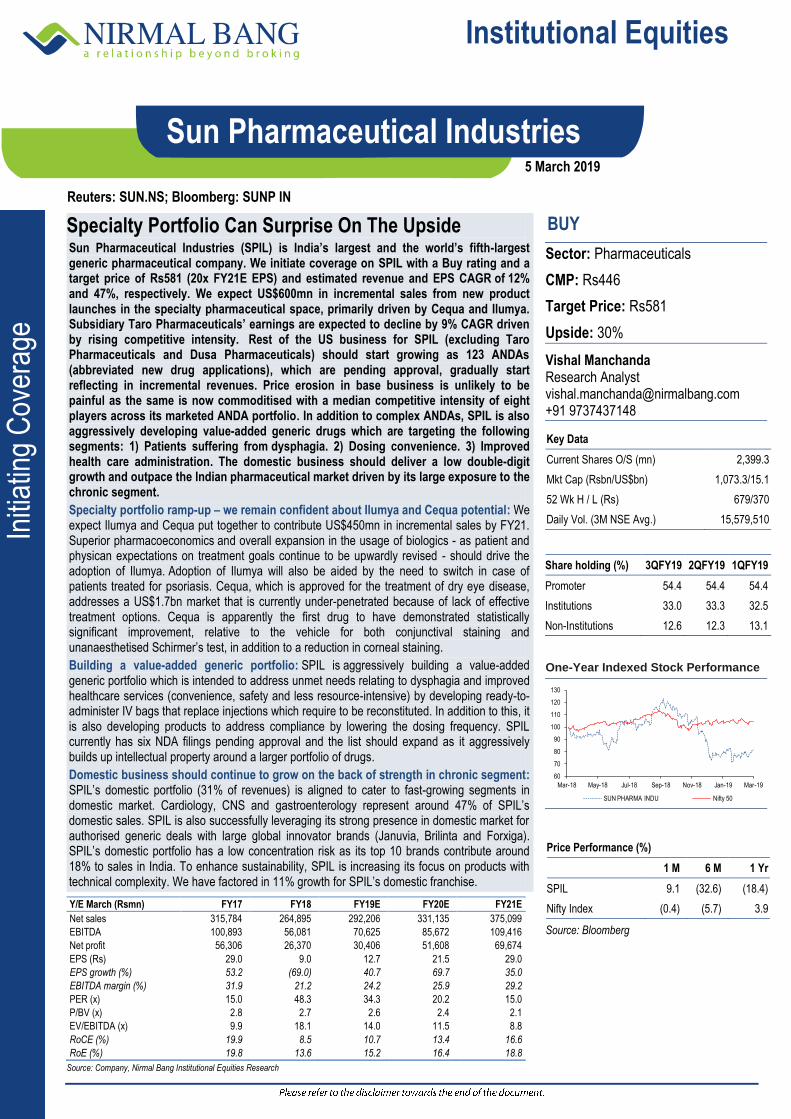

Specialty Portfolio Can Surprise On The Upside Sun Pharmaceutical Industries (SPIL) is India’s largest and the world’s fifth-largest generic pharmaceutical company. We initiate coverage on SPIL with a Buy rating and a target price of Rs581 (20x FY21E EPS) and estimated revenue and EPS CAGR of 12% and 47%, respectively. We expect US$600mn in incremental sales from new product launches in the specialty pharmaceutical space, primarily driven by Cequa and Ilumya. Subsidiary Taro Pharmaceuticals’ earnings are expected to decline by 9% CAGR driven by rising competitive intensity. Rest of the US business for SPIL (excluding Taro Pharmaceuticals and Dusa Pharmaceuticals) should start growing as 123 ANDAs (abbreviated new drug applications), which are pending approval, gradually start reflecting in incremental revenues. Price erosion in base business is unlikely to be painful as the same is now commoditised with a median competitive intensity of eight players across its marketed ANDA portfolio. In addition to complex ANDAs, SPIL is also aggressively developing value-added generic drugs which are targeting the following segments: 1) Patients suffering from dysphagia. 2) Dosing convenience. 3) Improved health care administration. The domestic business should deliver a low double-digit growth and outpace the Indian pharmaceutical market driven by its large exposure to the chronic segment.

Specialty portfolio ramp-up – we remain confident about Ilumya and Cequa potential: We expect Ilumya and Cequa put together to contribute US$450mn in incremental sales by FY21. Superior pharmacoeconomics and overall expansion in the usage of biologics - as patient and physican expectations on treatment goals continue to be upwardly revised - should drive the adoption of Ilumya. Adoption of Ilumya will also be aided by the need to switch in case of patients treated for psoriasis. Cequa, which is approved for the treatment of dry eye disease, addresses a US$1.7bn market that is currently under-penetrated because of lack of effective treatment options. Cequa is apparently the first drug to have demonstrated statistically significant improvement, relative to the vehicle for both conjunctival staining and unanaesthetised Schirmer’s test, in addition to a reduction in corneal staining.

Building a value-added generic portfolio: SPIL is aggressively building a value-added generic portfolio which is intended to address unmet needs relating to dysphagia and improved healthcare services (convenience, safety and less resource-intensive) by developing ready-to-administer IV bags that replace injections which require to be reconstituted. In addition to this, it is also developing products to address compliance by lowering the dosing frequency. SPIL currently has six NDA filings pending approval and the list should expand as it aggressively builds up intellectual property around a larger portfolio of drugs.

Domestic business should continue to grow on the back of strength in chronic segment: SPIL’s domestic portfolio (31% of revenues) is aligned to cater to fast-growing segments in domestic market. Cardiology, CNS and gastroenterology represent around 47% of SPIL’s domestic sales. SPIL is also successfully leveraging its strong presence in domestic market for authorised generic deals with large global innovator brands (Januvia, Brilinta and Forxiga). SPIL’s domestic portfolio has a low concentration risk as its top 10 brands contribute around 18% to sales in India. To enhance sustainability, SPIL is increasing its focus on products with technical complexity. We have factored in 11% growth for SPIL’s domestic franchise.

BUY

Sector: Pharmaceuticals

CMP: Rs446

Target Price: Rs581

Upside: 30%

Vishal Manchanda Research Analyst [email protected] +91 9737437148

Key Data

Current Shares O/S (mn) 2,399.3

Mkt Cap (Rsbn/US$bn) 1,073.3/15.1

52 Wk H / L (Rs) 679/370

Daily Vol. (3M NSE Avg.) 15,579,510

Share holding (%) 3QFY19 2QFY19 1QFY19

Promoter 54.4 54.4 54.4

Institutions 33.0 33.3 32.5

Non-Institutions 12.6 12.3 13.1

One-Year Indexed Stock Performance

60

70

80

90

100

110

120

130

Mar-18 May-18 Jul-18 Sep-18 Nov-18 Jan-19 Mar-19

SUN PHARMA INDU Nifty 50

Price Performance (%)

1 M 6 M 1 Yr

SPIL 9.1 (32.6) (18.4)

Nifty Index (0.4) (5.7) 3.9

Source: Bloomberg

Y/E March (Rsmn) FY17 FY18 FY19E FY20E FY21E

Net sales 315,784 264,895 292,206 331,135 375,099

EBITDA 100,893 56,081 70,625 85,672 109,416

Net profit 56,306 26,370 30,406 51,608 69,674

EPS (Rs) 29.0 9.0 12.7 21.5 29.0

EPS growth (%) 53.2 (69.0) 40.7 69.7 35.0

EBITDA margin (%) 31.9 21.2 24.2 25.9 29.2

PER (x) 15.0 48.3 34.3 20.2 15.0

P/BV (x) 2.8 2.7 2.6 2.4 2.1

EV/EBITDA (x) 9.9 18.1 14.0 11.5 8.8

RoCE (%) 19.9 8.5 10.7 13.4 16.6

RoE (%) 19.8 13.6 15.2 16.4 18.8

Source: Company, Nirmal Bang Institutional Equities Research

5 March 2019

Institutional Equities

Sun Pharmaceutical Industries 2

Investment Rationale

Ilumya has more than a fair chance to beat expectations: We forecast peak sales of US$500mn to US$1,000mn for Ilumya in the US. Ilumya ramp-up is expected to be slower than other marketed biologics, primarily as SPIL is a new entrant and will take some time for it to garner acceptance by physicians.

Key elements that will shape the success of Ilumya:

1) Pharmacoeconomics: A comparison of retail prices of various biologics indicates that Ilumya has been competitively priced. We believe pharmacoeconomics for a drug that has shown credibility on safety is the single-most important critical success factor.

2) Clinical profile better than most commonly prescribed drugs - Overall Ilumya provides to the patient a good package of best-in-class safety, dosing convenience and efficacy which is better or comparable to the most commonly prescribed drugs.

3) Better durability of response compared to anti-TNF alpha drugs.

4) The need to switch to alternative biologics allows a fair chance.

5) Safety and dosing convenience is the differentiator.

6) Expanding market for biologics driven by rising expectations on the outcome and also rising evidence around healthcare savings through a wider use of biologics.

Key limitations we foresee in a quick ramp-up for Ilumya are:

1) Ilumya is yet to get an approval for psoriatic arthritis which is a comorbid condition in 20% of psoriasis patients.

2) Limited capability to invest in marketing compared to competitors.

Biologic market continues to expand – there is still a significant unmet need

Psoriasis market has the potential to grow multi-fold from the current level driven by more frequent usage of biologics. With new biologics gaining approval, there is a gradual increase in the number of patients being treated with biologics every year. Currently, around 0.15mn patients are treated with a biologic and in the US there are 0.7mn patients who have severe psoriasis (BSA > 10%). At an annual cost of US$36,000, the potential market for biologics can expand up to US$25bn. Biologics remain under-penetrated as topical and oral systemic agents remain the preferred choice of insurers and physicians. However, insurers and physicians are gradually adapting to the change as physician/patient expectation on the treatment outcome is getting upwardly revised with treatment outcome from new age biologics being significantly better than under the old systemic/topical agents that are widely used. Most drugs have a good chance to gain a fair market share as patients need to switch

Psoriasis, unfortunately, is a chronic disease and patients have to keep switching from one drug to another. The length of time a patient continues with a drug is known as drug survival. Most commonly prescribed biologic medications used in the treatment of psoriasis are associated with very low drug survival based on a systematic review of literature. The median overall drug survival for Ustekinumab, Adalimumab, Infliximab and Etanercept was 38.0, 36.5, 26.6 and 24.7 months, respectively. The mean annual drug survival rate for TNF inhibitors was 70%, 57%, 51%, 45% and 41% at 1, 2, 3, 4 and 5 years, respectively. Efficacy is better/comparable to most widely used drugs for psoriasis

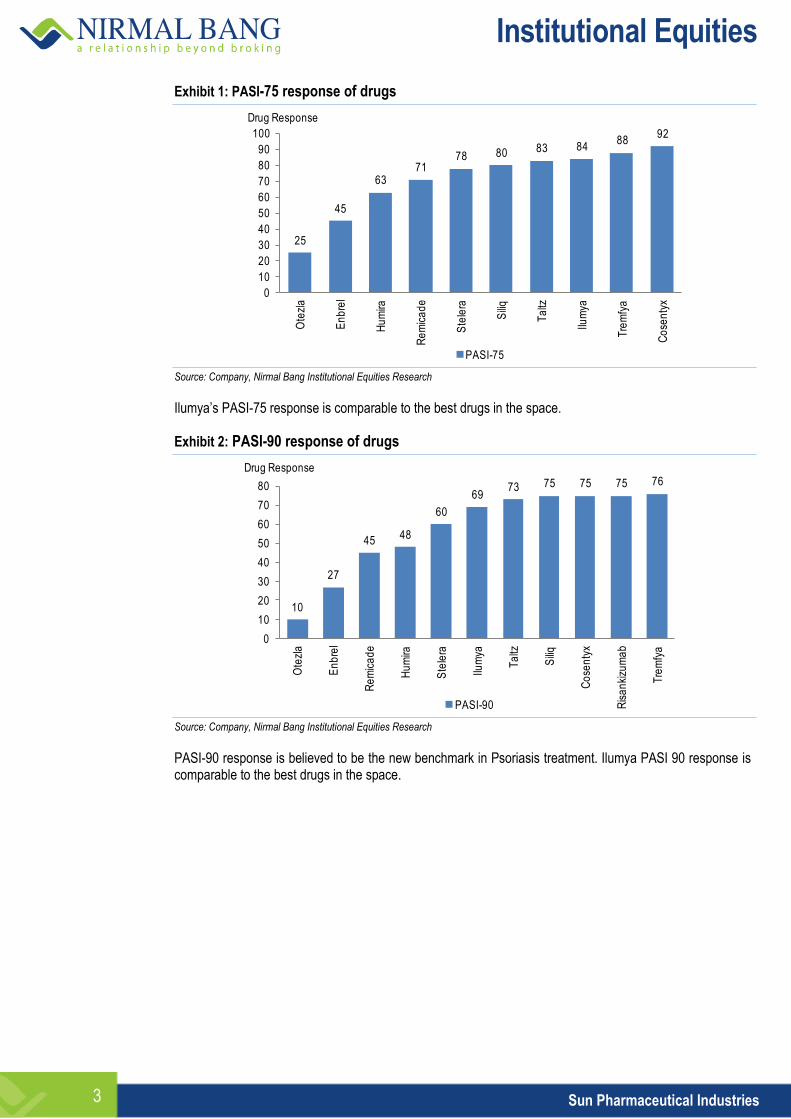

Based on a cross-trial comparison, efficacy of Tildrakizumb is better/comparable to the most widely used drugs for psoriasis - Humira, Otezla and Stelara - whose market share put together add up to around 70% of psoriasis market. This should allow Tildrakizumab a fair share of the pie. While SPIL may not have comparable marketing strength as its competitors, it will only restrict the company’s peak potential and lead to some delay in ramp-up.

Institutional Equities

Sun Pharmaceutical Industries 3

Exhibit 1: PASI-75 response of drugs

25

45

6371

78 80 83 8488

92

0

10

20

30

40

50

60

70

80

90

100

Ote

zla

En

bre

l

Hu

mira

Re

mic

ad

e

Ste

lera

Sili

q

Ta

ltz

Ilum

ya

Tre

mfy

a

Co

sen

tyx

Drug Response

PASI-75 Source: Company, Nirmal Bang Institutional Equities Research

Ilumya’s PASI-75 response is comparable to the best drugs in the space.

Exhibit 2: PASI-90 response of drugs

10

27

4548

60

6973 75 75 75 76

0

10

20

30

40

50

60

70

80

Ote

zla

En

bre

l

Re

mic

ad

e

Hu

mira

Ste

lera

Ilum

ya

Ta

ltz

Sili

q

Co

sen

tyx

Ris

an

kizu

ma

b

Tre

mfy

a

Drug Response

PASI-90 Source: Company, Nirmal Bang Institutional Equities Research

PASI-90 response is believed to be the new benchmark in Psoriasis treatment. Ilumya PASI 90 response is comparable to the best drugs in the space.

Institutional Equities

Sun Pharmaceutical Industries 4

Exhibit 3: PASI-100 response of drugs

8

23

3337

45 4751

55 56

0

10

20

30

40

50

60

En

bre

l

Hu

mira

Ilum

ya

Ste

lera

Co

sen

tyx

Tre

mfy

a

Ris

an

kizu

ma

b

Ta

ltz

Sili

q

Drug Response

PASI-100 Source: Company, Nirmal Bang Institutional Equities Research

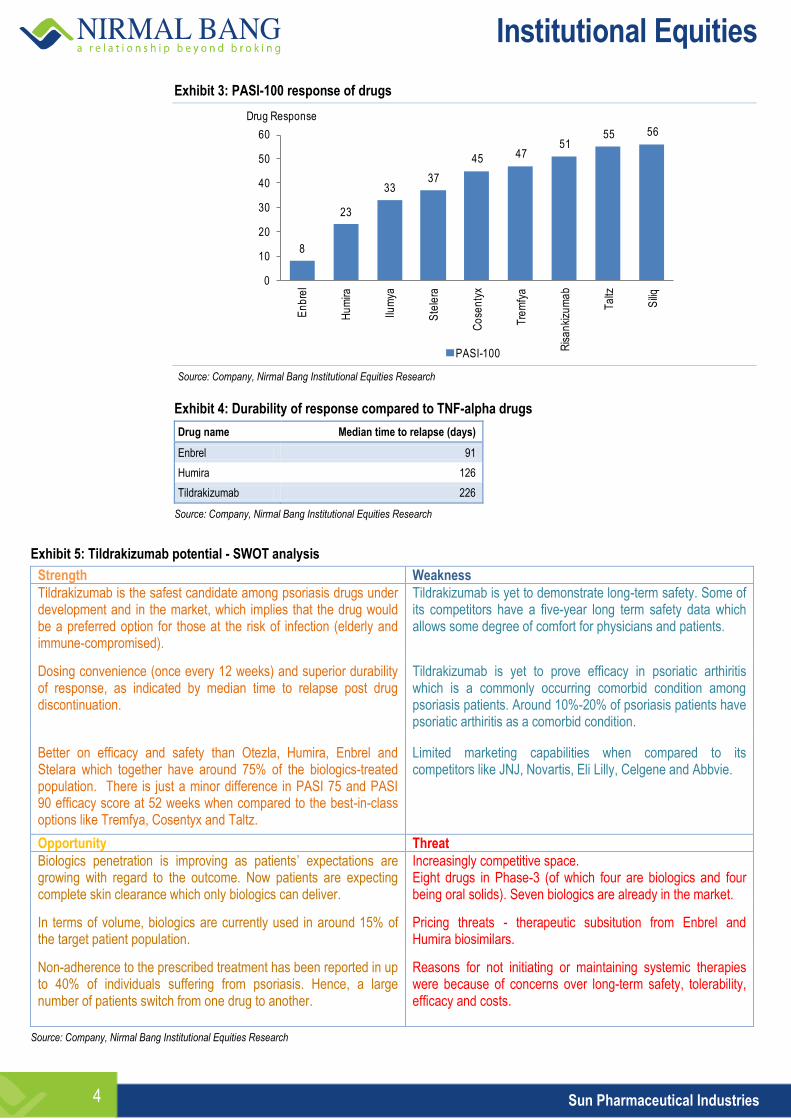

Exhibit 4: Durability of response compared to TNF-alpha drugs

Drug name Median time to relapse (days)

Enbrel 91

Humira 126

Tildrakizumab 226

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 5: Tildrakizumab potential - SWOT analysis

Strength Weakness

Tildrakizumab is the safest candidate among psoriasis drugs under development and in the market, which implies that the drug would be a preferred option for those at the risk of infection (elderly and immune-compromised).

Tildrakizumab is yet to demonstrate long-term safety. Some of its competitors have a five-year long term safety data which allows some degree of comfort for physicians and patients.

Dosing convenience (once every 12 weeks) and superior durability of response, as indicated by median time to relapse post drug discontinuation.

Tildrakizumab is yet to prove efficacy in psoriatic arthiritis which is a commonly occurring comorbid condition among psoriasis patients. Around 10%-20% of psoriasis patients have psoriatic arthiritis as a comorbid condition.

Better on efficacy and safety than Otezla, Humira, Enbrel and Stelara which together have around 75% of the biologics-treated population. There is just a minor difference in PASI 75 and PASI 90 efficacy score at 52 weeks when compared to the best-in-class options like Tremfya, Cosentyx and Taltz.

Limited marketing capabilities when compared to its competitors like JNJ, Novartis, Eli Lilly, Celgene and Abbvie.

Opportunity Threat

Biologics penetration is improving as patients’ expectations are growing with regard to the outcome. Now patients are expecting complete skin clearance which only biologics can deliver.

Increasingly competitive space. Eight drugs in Phase-3 (of which four are biologics and four being oral solids). Seven biologics are already in the market.

In terms of volume, biologics are currently used in around 15% of the target patient population.

Pricing threats - therapeutic subsitution from Enbrel and Humira biosimilars.

Non-adherence to the prescribed treatment has been reported in up to 40% of individuals suffering from psoriasis. Hence, a large number of patients switch from one drug to another.

Reasons for not initiating or maintaining systemic therapies were because of concerns over long-term safety, tolerability, efficacy and costs.

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

Sun Pharmaceutical Industries 5

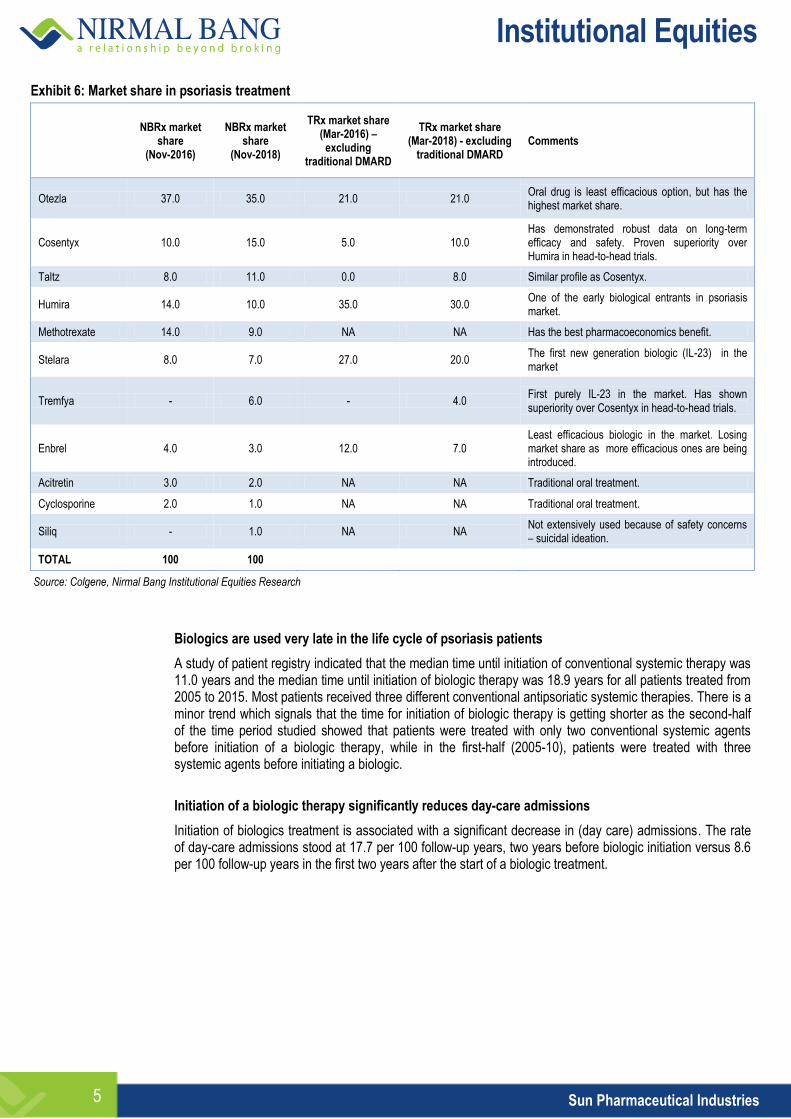

Exhibit 6: Market share in psoriasis treatment

NBRx market

share (Nov-2016)

NBRx market share

(Nov-2018)

TRx market share (Mar-2016) –

excluding traditional DMARD

TRx market share (Mar-2018) - excluding

traditional DMARD Comments

Otezla 37.0 35.0 21.0 21.0 Oral drug is least efficacious option, but has the highest market share.

Cosentyx 10.0 15.0 5.0 10.0 Has demonstrated robust data on long-term efficacy and safety. Proven superiority over Humira in head-to-head trials.

Taltz 8.0 11.0 0.0 8.0 Similar profile as Cosentyx.

Humira 14.0 10.0 35.0 30.0 One of the early biological entrants in psoriasis market.

Methotrexate 14.0 9.0 NA NA Has the best pharmacoeconomics benefit.

Stelara 8.0 7.0 27.0 20.0 The first new generation biologic (IL-23) in the market

Tremfya - 6.0 - 4.0 First purely IL-23 in the market. Has shown superiority over Cosentyx in head-to-head trials.

Enbrel 4.0 3.0 12.0 7.0 Least efficacious biologic in the market. Losing market share as more efficacious ones are being introduced.

Acitretin 3.0 2.0 NA NA Traditional oral treatment.

Cyclosporine 2.0 1.0 NA NA Traditional oral treatment.

Siliq - 1.0 NA NA Not extensively used because of safety concerns – suicidal ideation.

TOTAL 100 100

Source: Colgene, Nirmal Bang Institutional Equities Research

Biologics are used very late in the life cycle of psoriasis patients

A study of patient registry indicated that the median time until initiation of conventional systemic therapy was 11.0 years and the median time until initiation of biologic therapy was 18.9 years for all patients treated from 2005 to 2015. Most patients received three different conventional antipsoriatic systemic therapies. There is a minor trend which signals that the time for initiation of biologic therapy is getting shorter as the second-half of the time period studied showed that patients were treated with only two conventional systemic agents before initiation of a biologic therapy, while in the first-half (2005-10), patients were treated with three systemic agents before initiating a biologic.

Initiation of a biologic therapy significantly reduces day-care admissions

Initiation of biologics treatment is associated with a significant decrease in (day care) admissions. The rate of day-care admissions stood at 17.7 per 100 follow-up years, two years before biologic initiation versus 8.6 per 100 follow-up years in the first two years after the start of a biologic treatment.

Institutional Equities

Sun Pharmaceutical Industries 6

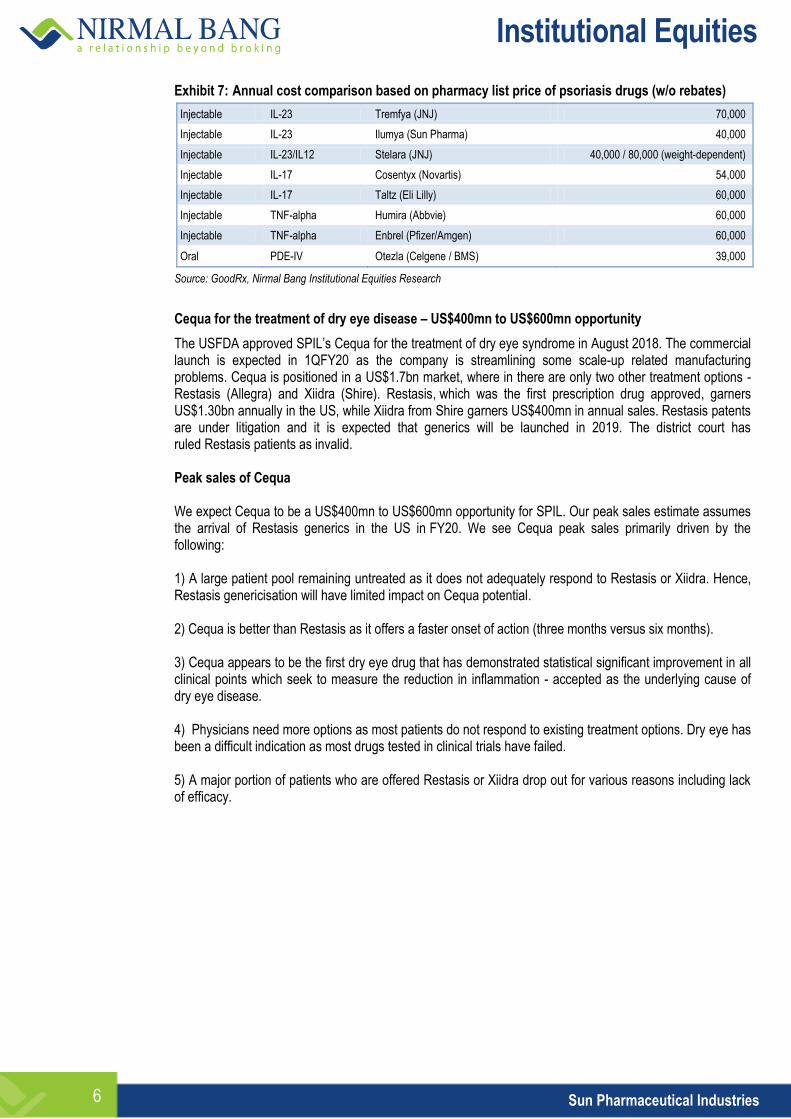

Exhibit 7: Annual cost comparison based on pharmacy list price of psoriasis drugs (w/o rebates)

Injectable IL-23 Tremfya (JNJ) 70,000

Injectable IL-23 Ilumya (Sun Pharma) 40,000

Injectable IL-23/IL12 Stelara (JNJ) 40,000 / 80,000 (weight-dependent)

Injectable IL-17 Cosentyx (Novartis) 54,000

Injectable IL-17 Taltz (Eli Lilly) 60,000

Injectable TNF-alpha Humira (Abbvie) 60,000

Injectable TNF-alpha Enbrel (Pfizer/Amgen) 60,000

Oral PDE-IV Otezla (Celgene / BMS) 39,000

Source: GoodRx, Nirmal Bang Institutional Equities Research

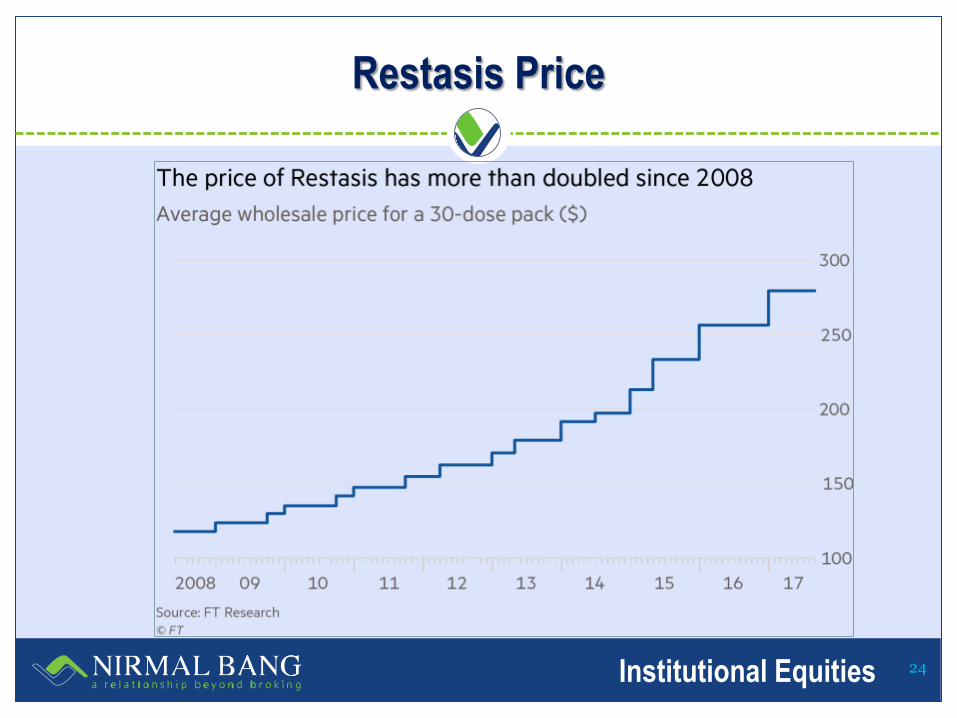

Cequa for the treatment of dry eye disease – US$400mn to US$600mn opportunity

The USFDA approved SPIL’s Cequa for the treatment of dry eye syndrome in August 2018. The commercial launch is expected in 1QFY20 as the company is streamlining some scale-up related manufacturing problems. Cequa is positioned in a US$1.7bn market, where in there are only two other treatment options - Restasis (Allegra) and Xiidra (Shire). Restasis, which was the first prescription drug approved, garners US$1.30bn annually in the US, while Xiidra from Shire garners US$400mn in annual sales. Restasis patents are under litigation and it is expected that generics will be launched in 2019. The district court has ruled Restasis patients as invalid. Peak sales of Cequa We expect Cequa to be a US$400mn to US$600mn opportunity for SPIL. Our peak sales estimate assumes the arrival of Restasis generics in the US in FY20. We see Cequa peak sales primarily driven by the following: 1) A large patient pool remaining untreated as it does not adequately respond to Restasis or Xiidra. Hence, Restasis genericisation will have limited impact on Cequa potential. 2) Cequa is better than Restasis as it offers a faster onset of action (three months versus six months). 3) Cequa appears to be the first dry eye drug that has demonstrated statistical significant improvement in all clinical points which seek to measure the reduction in inflammation - accepted as the underlying cause of dry eye disease. 4) Physicians need more options as most patients do not respond to existing treatment options. Dry eye has been a difficult indication as most drugs tested in clinical trials have failed. 5) A major portion of patients who are offered Restasis or Xiidra drop out for various reasons including lack of efficacy.

Institutional Equities

Sun Pharmaceutical Industries 7

Impact of Restasis genericisation on Cequa peak sales

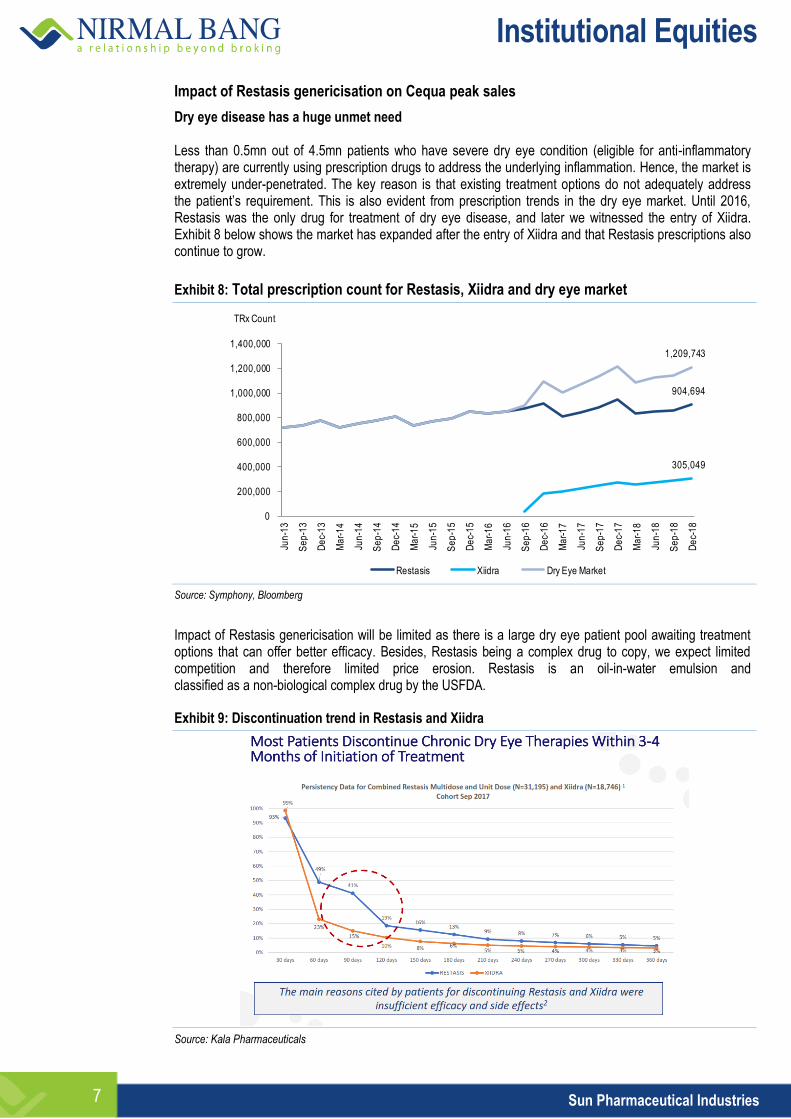

Dry eye disease has a huge unmet need Less than 0.5mn out of 4.5mn patients who have severe dry eye condition (eligible for anti-inflammatory therapy) are currently using prescription drugs to address the underlying inflammation. Hence, the market is extremely under-penetrated. The key reason is that existing treatment options do not adequately address the patient’s requirement. This is also evident from prescription trends in the dry eye market. Until 2016, Restasis was the only drug for treatment of dry eye disease, and later we witnessed the entry of Xiidra. Exhibit 8 below shows the market has expanded after the entry of Xiidra and that Restasis prescriptions also continue to grow.

Exhibit 8: Total prescription count for Restasis, Xiidra and dry eye market

904,694

305,049

1,209,743

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Jun

-13

Se

p-1

3

De

c-1

3

Ma

r-1

4

Jun

-14

Se

p-1

4

De

c-1

4

Ma

r-1

5

Jun

-15

Se

p-1

5

De

c-1

5

Ma

r-1

6

Jun

-16

Se

p-1

6

De

c-1

6

Ma

r-1

7

Jun

-17

Se

p-1

7

De

c-1

7

Ma

r-1

8

Jun

-18

Se

p-1

8

De

c-1

8

TRx Count

Restasis Xiidra Dry Eye Market

Source: Symphony, Bloomberg

Impact of Restasis genericisation will be limited as there is a large dry eye patient pool awaiting treatment options that can offer better efficacy. Besides, Restasis being a complex drug to copy, we expect limited competition and therefore limited price erosion. Restasis is an oil-in-water emulsion and classified as a non-biological complex drug by the USFDA.

Exhibit 9: Discontinuation trend in Restasis and Xiidra

Source: Kala Pharmaceuticals

Institutional Equities

Sun Pharmaceutical Industries 8

Is Cequa differentiated to expand the market?

Cequa’s clinical profile versus Restasis and Xiidra (cross-trial comparision): Cequa has demonstrated superiority across end-points like:

Conjunctival staining – used to detect early signs of damage because of dry eye: Cequa has demonstrated statistically significant improvement in the conjunctival staining score compared to placebo, while Restasis and Xiidra have not shown statistically significant reduction comparable to placebo.

Corneal staining is a measure of eye damage in corneal region: In case of Xiidra, the study results were inconsistent as they demonstrated statistically significant reduction in only one out of three Phase -3 studies. The same was the case with Restasis. Cequa has demonstrated statistically significant reduction in the corneal staining score.

Schirmer test measures tear production: In case of Cequa, tear production was superior with both concentrations of the active treatment compared with the vehicle. The 0.09% drug concentration was significantly better (p = 0.007) compared with the vehicle and resulted in 17.9% of the patients having a 10mm or greater improvement in Schirmer test versus 7.6% of the patients assigned to the vehicle. Xiidra did not demonstrate statistically significant improvement over the vehicle across all studies. Restasis results are comparable to Cequa on the Schirmer test end-point, but the same was at six months versus 84 days in Cequa. 15% patients on Restasis achieved 10mm or greater improvement on Schirmer testing as compared to 5% on placebo.

Symptomatic improvement: In terms of onset of action, Cequa provides relief from the 12th week onwards, in line with Xiidra, but Restasis takes as long as six months.

Superior performance in reducing central corneal inflammation is a more relevant end-point: Unlike Restasis and Xiidra, Cequa has shown benefit in central corneal inflammation which has higher correlation with dry eye symptoms. The central cornea has five to six times as many nerve fibres as the peripheral cornea. Consequently, corneal sensitivity is higher in central cornea compared to the periphery. It may be noted that symptoms of dry eye are more prevalent in patients who exhibit greater occular surface damage of central cornea.

Xelpros (BAK-free formulation of Latanoprost) - commercial opportunity constrained by generic availability

Xelpros is in-licensed by SPIL from SPARC and was approved by the USFDA in September 2018. Xelpros represents a novel drug formulation of Xalatan (Latanoprost) - the most widely prescribed treatment for glaucoma. Xelpros is different from Xalatan and its generics as it is formulated without the commonly used preservative, benzalkonium chloride (BAK).

Importance of BAK-free drug

There is evidence that long-term use of ophthalmic drugs containing BAK lead to ocular surface damage. Glaucoma is a chronic condition and, hence, the drugs need to be prescribed for the long term. While BAK is a useful preservative, several studies conducted in the past have shown that long-term usage of drugs with such preservatives can lead to ocular surface changes, ocular discomfort, tear film instability, conjunctival inflammation, sub-conjunctival fibrosis, epithelial apoptosis, corneal surface impairment, and the potential risk of failure of further glaucoma surgery. In some cases, patients have even discontinued usage of the drugs because of discomfort. Hence, a BAK-free drug is an unmet need.

Commercial potential of Xelpros

Xalatan belongs to the class of drugs called prostaglandin analogue which has a 36% prescription share. Prior to genericisation, Xalatan generated peak sales of US$650mn in the US. Xalatan’s patents have expired and there are multiple generic options.

Acceptance of BAK-free agents in the US so far is not very encouraging, as they comprise just 10% of the prostaglandin market in terms of prescription volume. The current market for single-agent BAK-free products in the US for treatment of glaucoma is around US$200mn. The low acceptance of BAK-free formulations can be primarily attributed to the pricing difference as Travatan Z - which is the only prostaglandin analogue that is BAK-free - is priced several times higher than generics. We expect Xelpros’ peak sales potential to be around US$50mn, assuming a 25% market share in the single-agent BAK-free formulations market.

Institutional Equities

Sun Pharmaceutical Industries 9

Availability of Xelpros should also expand the market opportunity because of enhanced promotional efforts on BAK-free agents.

Xelpros economics: SPIL had in-licensed Xelpros from Sun Pharma Advanced Research Company (SPARC) in 2015 for an upfront fee of US$3mn and it needs to make a milestone payment up to US$16mn. In addition, SPIL has to pay royalty on sales of Xelpros, which we believe is in the mid-teen range. We expect net margin contribution from Xelpros at peak sales to be 35%. The key assumptions are 20% spending on royalty/cost of sales and 30% on SG&A expenses.

Institutional Equities

Sun Pharmaceutical Industries 10

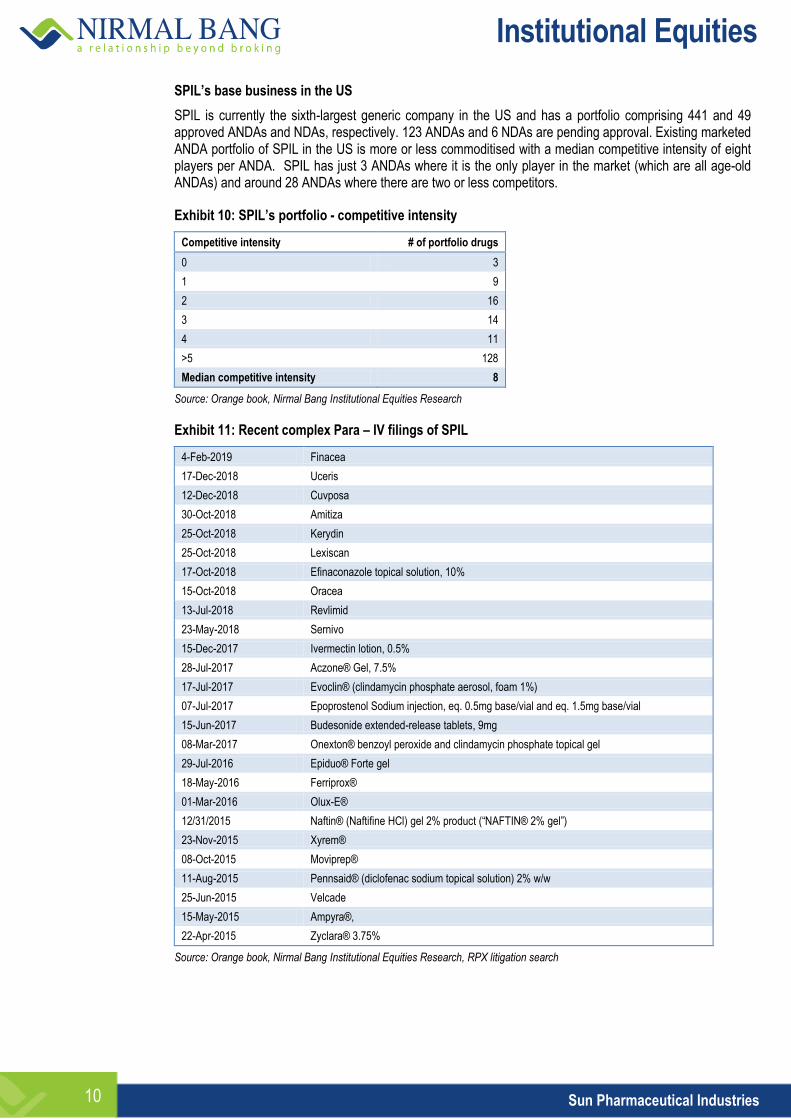

SPIL’s base business in the US

SPIL is currently the sixth-largest generic company in the US and has a portfolio comprising 441 and 49 approved ANDAs and NDAs, respectively. 123 ANDAs and 6 NDAs are pending approval. Existing marketed ANDA portfolio of SPIL in the US is more or less commoditised with a median competitive intensity of eight players per ANDA. SPIL has just 3 ANDAs where it is the only player in the market (which are all age-old ANDAs) and around 28 ANDAs where there are two or less competitors.

Exhibit 10: SPIL’s portfolio - competitive intensity

Competitive intensity # of portfolio drugs

0 3

1 9

2 16

3 14

4 11

>5 128

Median competitive intensity 8

Source: Orange book, Nirmal Bang Institutional Equities Research

Exhibit 11: Recent complex Para – IV filings of SPIL

4-Feb-2019 Finacea

17-Dec-2018 Uceris

12-Dec-2018 Cuvposa

30-Oct-2018 Amitiza

25-Oct-2018 Kerydin

25-Oct-2018 Lexiscan

17-Oct-2018 Efinaconazole topical solution, 10%

15-Oct-2018 Oracea

13-Jul-2018 Revlimid

23-May-2018 Sernivo

15-Dec-2017 Ivermectin lotion, 0.5%

28-Jul-2017 Aczone® Gel, 7.5%

17-Jul-2017 Evoclin® (clindamycin phosphate aerosol, foam 1%)

07-Jul-2017 Epoprostenol Sodium injection, eq. 0.5mg base/vial and eq. 1.5mg base/vial

15-Jun-2017 Budesonide extended-release tablets, 9mg

08-Mar-2017 Onexton® benzoyl peroxide and clindamycin phosphate topical gel

29-Jul-2016 Epiduo® Forte gel

18-May-2016 Ferriprox®

01-Mar-2016 Olux-E®

12/31/2015 Naftin® (Naftifine HCl) gel 2% product (“NAFTIN® 2% gel”)

23-Nov-2015 Xyrem®

08-Oct-2015 Moviprep®

11-Aug-2015 Pennsaid® (diclofenac sodium topical solution) 2% w/w

25-Jun-2015 Velcade

15-May-2015 Ampyra®,

22-Apr-2015 Zyclara® 3.75%

Source: Orange book, Nirmal Bang Institutional Equities Research, RPX litigation search

Institutional Equities

Sun Pharmaceutical Industries 11

Portfolio of value-added generics (Filed NDA’s and potential NDA filings)

SPIL has been investing to build a portfolio of value-added generics that are novel formulations and designed to offer the following benefits:

1) Patients with dysphagia - The problem of dysphagia pertains to difficulty in swallowing. According to SPIL, 40% of the patients who need long-term care have this problem. SPIL is in the process of creating a portfolio of products which will help the patients to deal with this problem. In the most recent past, SPIL launched a few 505 (b) (2) products which intend to cater to patients with dysphagia suffering from common ailments like Dyslipidemia and hypertension. Some recent launches in this category include:

Ezallor - Ezallor is a 505(b)(2) version of Crestor (Rosuvastatin) which is one of the most commonly prescribed generic for dyslipidemia.Unlike the commonly used Crestor tablets, Ezallor is a capsule which can be opened up and the granules in the capsule emptied in a spoon and consumed along with apple sauce. The capsule can also be used in patients who are consuming food via naso-gastric tube.

Kapspargo sprinkle (Metoprolol Succinate) - Kapspargo Sprinkle is a 505(b)(2) version of the commonly used anti-hypertension drug (Toprol XL). Like Ezallor, Kapspargo can be consumed with apple sauce or sprinkled on soft food and consumed. It can also be used in patients with a naso-gastric tube.

In addition to these recent launches, SPIL is further enhancing its portfolio with several products under development. These include:

Raloxifene sprinkle - Raloxifene is marketed under the brand Evista in the US, and is indicated for osteoporosis and breast cancer in post-menopausal women. Raloxifene, when powdered, tastes bitter and it also becomes hazardous (being cytotoxic). To address the problem of compliance in patients with swallowing problems, SPIL is developing a sprinkle version that is coated for the bitter taste and can be sprinkled over food or used as a capsule.

Duloxetine sprinkle – Duloxetine (brand name: Cymbalta) is indicated for the treatment of depression. It is sold as a hard gelatine capsule which makes it difficult for pediatric, geriatric, dysphagic or patients on naso-gastric tubes to swallow the drug. Thus, there exists a need for an alternate gastro-resistant Duloxetine composition suitable for administration to such patients. Hence, SPIL is developing a sprinkle version of the same to ease compliance.

Oral liquid composition of Guanfacine – Guanfacine is indicated for the treatment of Attention Deficit Hyperactive Disorder (ADHD) and hypertension. The marketed versions are sold only as tablets and, hence, compliance becomes a problem for some paediatric patients or incapacitated patients. SPIL is developing ready-to-use oral syrup for the same.

2) Lower healthcare burden in administration of injectables

Administering injectables in a hospital environment requires the use of resources which increase overheads for the hospital, increases the risk of contamination, have safety consequences and also lead to more time being spent by hospital staff and patients. Hence, SPIL is extensively working on developing ready-to-administer intravenous bags for injectables which otherwise require reconstitution before administration. The most recent launch under this category is:

1) InfuGem – SPIL received the USFDA approval for the drug last year. Infugem is a ready-to-administer version of commonly used Cytotoxic injection.

Leveraging on the proprietary technology which allows injectable products to be premixed in a sterile environment and supplied to prescribers in RTA bags, SPIL is developing a host of other products and these include:

1) Intravenous dosage form of commonly used Cytotoxin injectable – Alimta

2) Morphine

3) Fentanyl Citrate

4) Norepinephrine

5) Amiodarone

6) Vinca alkaloid drugs like Vinblastine, Vincristine, Vindesine and Vinorelbine.

Institutional Equities

Sun Pharmaceutical Industries 12

3) Dosing convenience – Dosing convenience is important as it impacts compliance which, in turn, has implications on the disease outcome. SPIL is working on a slew of drugs that are intended to deliver reduction in dosing frequency. Key drugs that SPIL is working on include:

1) Budesonide

2) Divalproex ER (Depakote ER)

3) Brimonidine Tartrate ophthalmic suspension (once daily versus thrice daily).

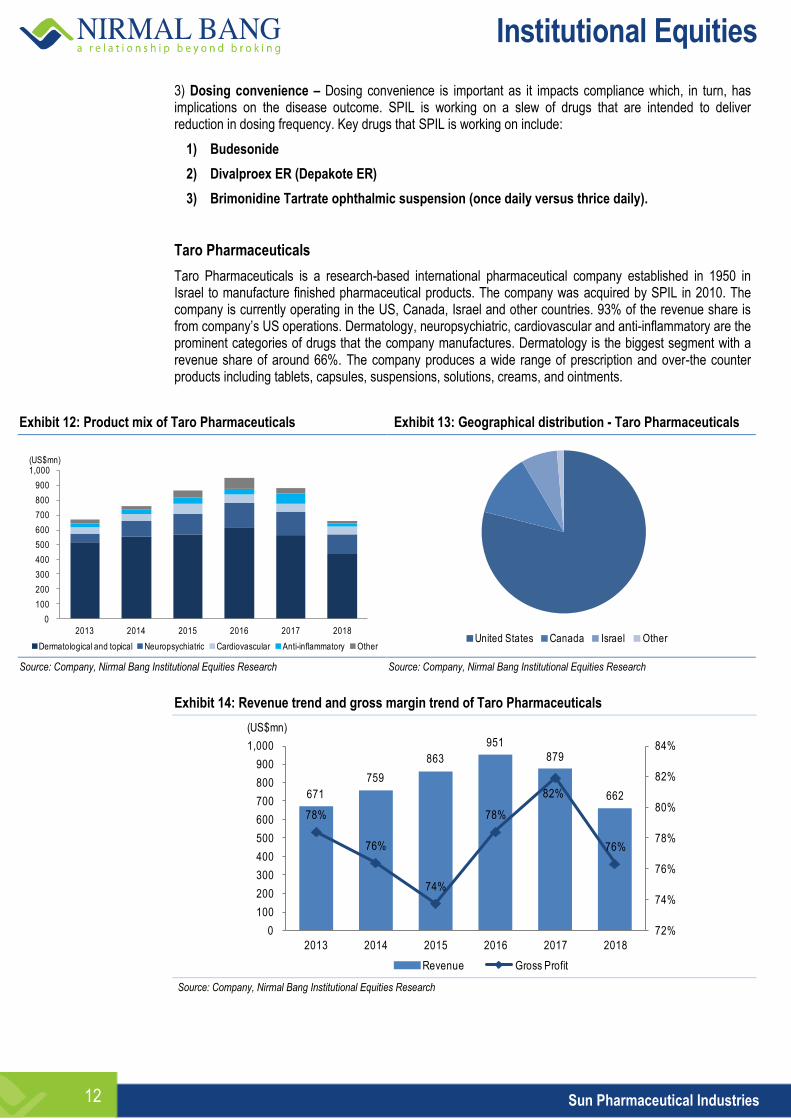

Taro Pharmaceuticals

Taro Pharmaceuticals is a research-based international pharmaceutical company established in 1950 in Israel to manufacture finished pharmaceutical products. The company was acquired by SPIL in 2010. The company is currently operating in the US, Canada, Israel and other countries. 93% of the revenue share is from company’s US operations. Dermatology, neuropsychiatric, cardiovascular and anti-inflammatory are the prominent categories of drugs that the company manufactures. Dermatology is the biggest segment with a revenue share of around 66%. The company produces a wide range of prescription and over-the counter products including tablets, capsules, suspensions, solutions, creams, and ointments.

Exhibit 12: Product mix of Taro Pharmaceuticals Exhibit 13: Geographical distribution - Taro Pharmaceuticals

0

100

200

300

400

500

600

700

800

900

1,000

2013 2014 2015 2016 2017 2018

(US$mn)

Dermatological and topical Neuropsychiatric Cardiovascular Anti-inflammatory Other

United States Canada Israel Other

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 14: Revenue trend and gross margin trend of Taro Pharmaceuticals

671

759

863

951

879

662

78%

76%

74%

78%

82%

76%

72%

74%

76%

78%

80%

82%

84%

0

100

200

300

400

500

600

700

800

900

1,000

2013 2014 2015 2016 2017 2018

(US$mn)

Revenue Gross Profit Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

Sun Pharmaceutical Industries 13

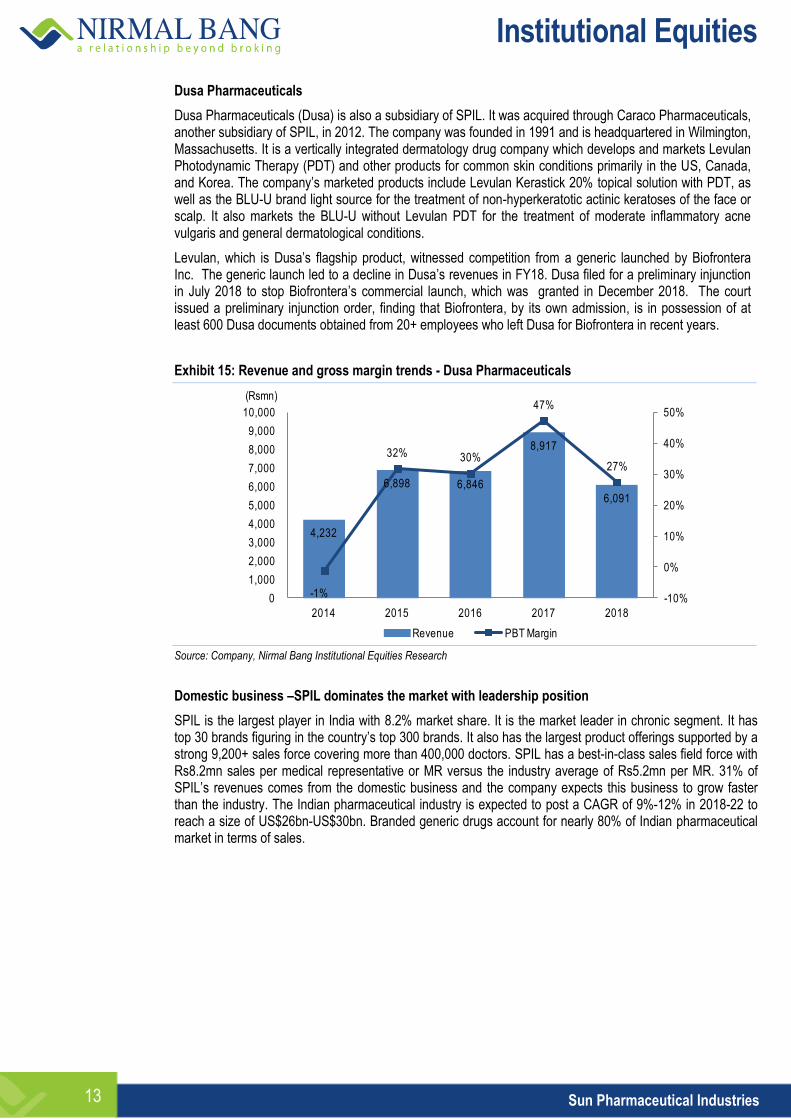

Dusa Pharmaceuticals

Dusa Pharmaceuticals (Dusa) is also a subsidiary of SPIL. It was acquired through Caraco Pharmaceuticals, another subsidiary of SPIL, in 2012. The company was founded in 1991 and is headquartered in Wilmington, Massachusetts. It is a vertically integrated dermatology drug company which develops and markets Levulan Photodynamic Therapy (PDT) and other products for common skin conditions primarily in the US, Canada, and Korea. The company’s marketed products include Levulan Kerastick 20% topical solution with PDT, as well as the BLU-U brand light source for the treatment of non-hyperkeratotic actinic keratoses of the face or scalp. It also markets the BLU-U without Levulan PDT for the treatment of moderate inflammatory acne vulgaris and general dermatological conditions.

Levulan, which is Dusa’s flagship product, witnessed competition from a generic launched by Biofrontera Inc. The generic launch led to a decline in Dusa’s revenues in FY18. Dusa filed for a preliminary injunction in July 2018 to stop Biofrontera’s commercial launch, which was granted in December 2018. The court issued a preliminary injunction order, finding that Biofrontera, by its own admission, is in possession of at least 600 Dusa documents obtained from 20+ employees who left Dusa for Biofrontera in recent years.

Exhibit 15: Revenue and gross margin trends - Dusa Pharmaceuticals

4,232

6,898 6,846

8,917

6,091

-1%

32% 30%

47%

27%

-10%

0%

10%

20%

30%

40%

50%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2014 2015 2016 2017 2018

(Rsmn)

Revenue PBT Margin Source: Company, Nirmal Bang Institutional Equities Research

Domestic business –SPIL dominates the market with leadership position

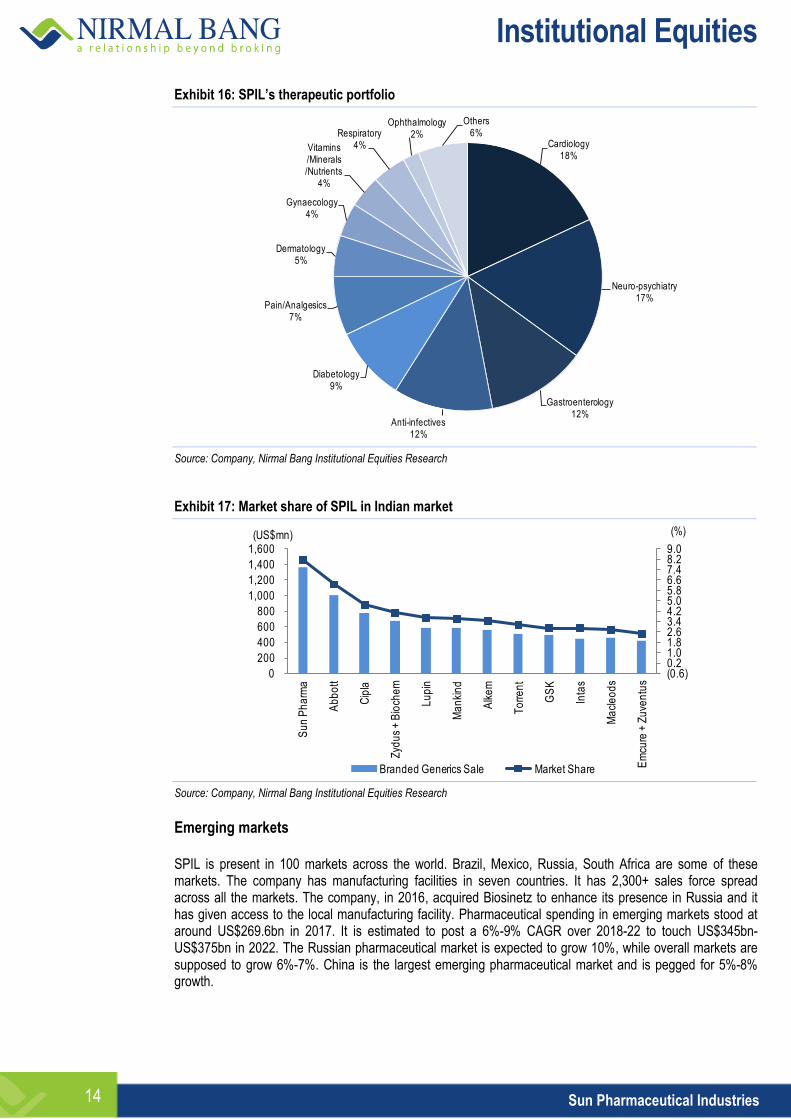

SPIL is the largest player in India with 8.2% market share. It is the market leader in chronic segment. It has top 30 brands figuring in the country’s top 300 brands. It also has the largest product offerings supported by a strong 9,200+ sales force covering more than 400,000 doctors. SPIL has a best-in-class sales field force with Rs8.2mn sales per medical representative or MR versus the industry average of Rs5.2mn per MR. 31% of SPIL’s revenues comes from the domestic business and the company expects this business to grow faster than the industry. The Indian pharmaceutical industry is expected to post a CAGR of 9%-12% in 2018-22 to reach a size of US$26bn-US$30bn. Branded generic drugs account for nearly 80% of Indian pharmaceutical market in terms of sales.

Institutional Equities

Sun Pharmaceutical Industries 14

Exhibit 16: SPIL’s therapeutic portfolio

Cardiology18%

Neuro-psychiatry17%

Gastroenterology12%

Anti-infectives12%

Diabetology9%

Pain/Analgesics7%

Dermatology5%

Gynaecology4%

Vitamins/Minerals/Nutrients

4%

Respiratory4%

Ophthalmology2%

Others6%

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 17: Market share of SPIL in Indian market

(0.6)0.2 1.0 1.8 2.6 3.4 4.2 5.0 5.8 6.6 7.4 8.2 9.0

0

200

400

600

800

1,000

1,200

1,400

1,600

Su

n P

ha

rma

Ab

bo

tt

Cip

la

Zyd

us

+ B

ioch

em

Lu

pin

Ma

nki

nd

Alk

em

To

rre

nt

GS

K

Inta

s

Ma

cle

od

s

Em

cure

+ Z

uve

ntu

s

(%)(US$mn)

Branded Generics Sale Market Share Source: Company, Nirmal Bang Institutional Equities Research

Emerging markets

SPIL is present in 100 markets across the world. Brazil, Mexico, Russia, South Africa are some of these markets. The company has manufacturing facilities in seven countries. It has 2,300+ sales force spread across all the markets. The company, in 2016, acquired Biosinetz to enhance its presence in Russia and it has given access to the local manufacturing facility. Pharmaceutical spending in emerging markets stood at around US$269.6bn in 2017. It is estimated to post a 6%-9% CAGR over 2018-22 to touch US$345bn-US$375bn in 2022. The Russian pharmaceutical market is expected to grow 10%, while overall markets are supposed to grow 6%-7%. China is the largest emerging pharmaceutical market and is pegged for 5%-8% growth.

Institutional Equities

Sun Pharmaceutical Industries 15

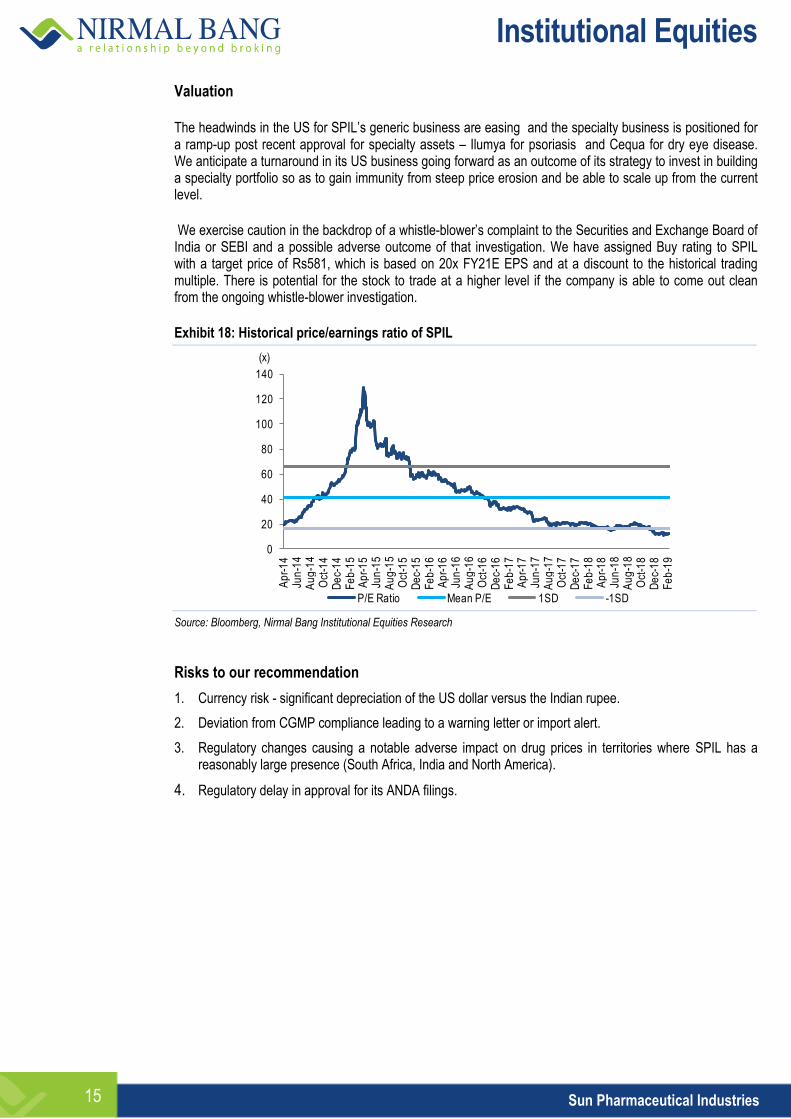

Valuation

The headwinds in the US for SPIL’s generic business are easing and the specialty business is positioned for a ramp-up post recent approval for specialty assets – Ilumya for psoriasis and Cequa for dry eye disease. We anticipate a turnaround in its US business going forward as an outcome of its strategy to invest in building a specialty portfolio so as to gain immunity from steep price erosion and be able to scale up from the current level.

We exercise caution in the backdrop of a whistle-blower’s complaint to the Securities and Exchange Board of India or SEBI and a possible adverse outcome of that investigation. We have assigned Buy rating to SPIL with a target price of Rs581, which is based on 20x FY21E EPS and at a discount to the historical trading multiple. There is potential for the stock to trade at a higher level if the company is able to come out clean from the ongoing whistle-blower investigation.

Exhibit 18: Historical price/earnings ratio of SPIL

0

20

40

60

80

100

120

140

Ap

r-1

4Ju

n-1

4A

ug

-14

Oct

-14

De

c-1

4F

eb

-15

Ap

r-1

5Ju

n-1

5A

ug

-15

Oct

-15

De

c-1

5F

eb

-16

Ap

r-1

6Ju

n-1

6A

ug

-16

Oct

-16

De

c-1

6F

eb

-17

Ap

r-1

7Ju

n-1

7A

ug

-17

Oct

-17

De

c-1

7F

eb

-18

Ap

r-1

8Ju

n-1

8A

ug

-18

Oct

-18

De

c-1

8F

eb

-19

(x)

P/E Ratio Mean P/E 1SD -1SD

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Risks to our recommendation

1. Currency risk - significant depreciation of the US dollar versus the Indian rupee.

2. Deviation from CGMP compliance leading to a warning letter or import alert.

3. Regulatory changes causing a notable adverse impact on drug prices in territories where SPIL has a reasonably large presence (South Africa, India and North America).

4. Regulatory delay in approval for its ANDA filings.

Institutional Equities

Sun Pharmaceutical Industries 16

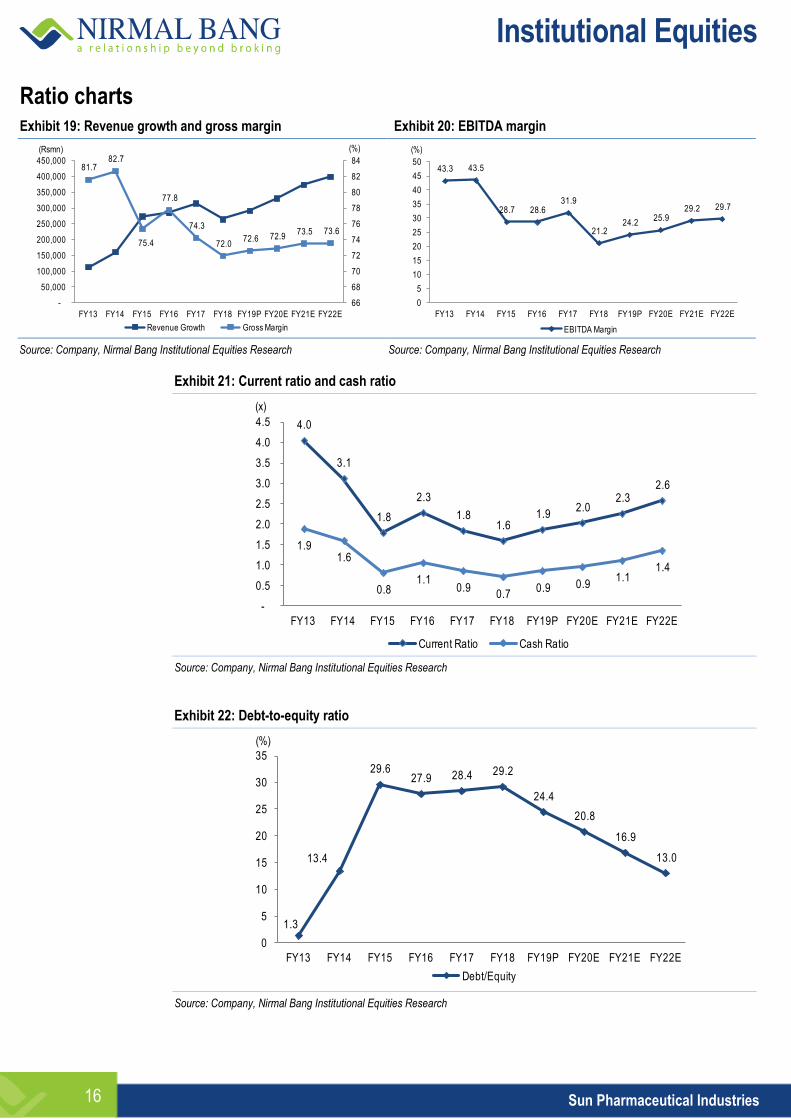

Ratio charts Exhibit 19: Revenue growth and gross margin Exhibit 20: EBITDA margin

81.7 82.7

75.4

77.8

74.3

72.0 72.6 72.9

73.5 73.6

66

68

70

72

74

76

78

80

82

84

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

FY13 FY14 FY15 FY16 FY17 FY18 FY19P FY20E FY21E FY22E

(%)(Rsmn)

Revenue Growth Gross Margin

43.3 43.5

28.7 28.6 31.9

21.2 24.2

25.9 29.2 29.7

0

5

10

15

20

25

30

35

40

45

50

FY13 FY14 FY15 FY16 FY17 FY18 FY19P FY20E FY21E FY22E

(%)

EBITDA Margin Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 21: Current ratio and cash ratio

4.0

3.1

1.8

2.3

1.8 1.6

1.9 2.0

2.3 2.6

1.9 1.6

0.8 1.1

0.9 0.7

0.9 0.9 1.1

1.4

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

FY13 FY14 FY15 FY16 FY17 FY18 FY19P FY20E FY21E FY22E

(x)

Current Ratio Cash Ratio Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 22: Debt-to-equity ratio

1.3

13.4

29.6 27.9 28.4 29.2

24.4

20.8

16.9

13.0

0

5

10

15

20

25

30

35

FY13 FY14 FY15 FY16 FY17 FY18 FY19P FY20E FY21E FY22E

(%)

Debt/Equity

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

Sun Pharmaceutical Industries 17

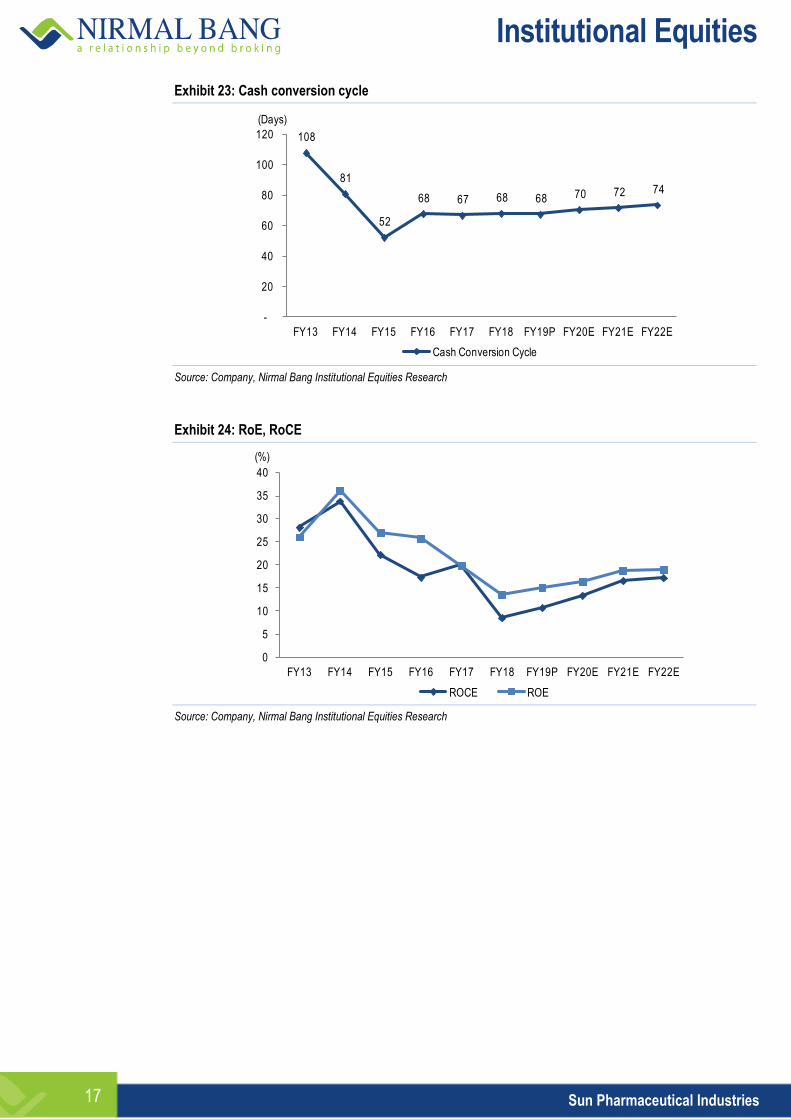

Exhibit 23: Cash conversion cycle

108

81

52

68 67 68 68 70 72 74

-

20

40

60

80

100

120

FY13 FY14 FY15 FY16 FY17 FY18 FY19P FY20E FY21E FY22E

(Days)

Cash Conversion Cycle

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 24: RoE, RoCE

0

5

10

15

20

25

30

35

40

FY13 FY14 FY15 FY16 FY17 FY18 FY19P FY20E FY21E FY22E

ROCE ROE

(%)

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

Sun Pharmaceutical Industries 18

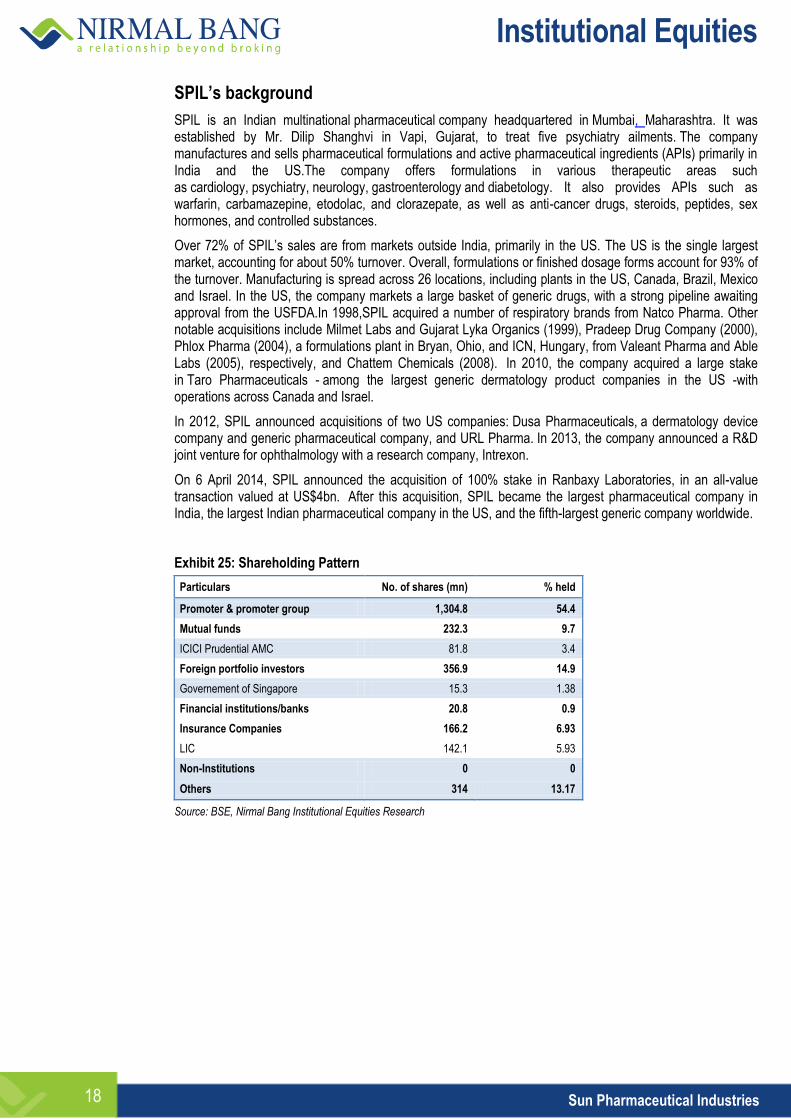

SPIL’s background

SPIL is an Indian multinational pharmaceutical company headquartered in Mumbai, Maharashtra. It was established by Mr. Dilip Shanghvi in Vapi, Gujarat, to treat five psychiatry ailments. The company manufactures and sells pharmaceutical formulations and active pharmaceutical ingredients (APIs) primarily in India and the US.The company offers formulations in various therapeutic areas such as cardiology, psychiatry, neurology, gastroenterology and diabetology. It also provides APIs such as warfarin, carbamazepine, etodolac, and clorazepate, as well as anti-cancer drugs, steroids, peptides, sex hormones, and controlled substances.

Over 72% of SPIL’s sales are from markets outside India, primarily in the US. The US is the single largest market, accounting for about 50% turnover. Overall, formulations or finished dosage forms account for 93% of the turnover. Manufacturing is spread across 26 locations, including plants in the US, Canada, Brazil, Mexico and Israel. In the US, the company markets a large basket of generic drugs, with a strong pipeline awaiting approval from the USFDA.In 1998,SPIL acquired a number of respiratory brands from Natco Pharma. Other notable acquisitions include Milmet Labs and Gujarat Lyka Organics (1999), Pradeep Drug Company (2000), Phlox Pharma (2004), a formulations plant in Bryan, Ohio, and ICN, Hungary, from Valeant Pharma and Able Labs (2005), respectively, and Chattem Chemicals (2008). In 2010, the company acquired a large stake in Taro Pharmaceuticals - among the largest generic dermatology product companies in the US -with operations across Canada and Israel.

In 2012, SPIL announced acquisitions of two US companies: Dusa Pharmaceuticals, a dermatology device company and generic pharmaceutical company, and URL Pharma. In 2013, the company announced a R&D joint venture for ophthalmology with a research company, Intrexon.

On 6 April 2014, SPIL announced the acquisition of 100% stake in Ranbaxy Laboratories, in an all-value transaction valued at US$4bn. After this acquisition, SPIL became the largest pharmaceutical company in India, the largest Indian pharmaceutical company in the US, and the fifth-largest generic company worldwide.

Exhibit 25: Shareholding Pattern

Particulars No. of shares (mn) % held

Promoter & promoter group 1,304.8 54.4

Mutual funds 232.3 9.7

ICICI Prudential AMC 81.8 3.4

Foreign portfolio investors 356.9 14.9

Governement of Singapore 15.3 1.38

Financial institutions/banks 20.8 0.9

Insurance Companies 166.2 6.93

LIC 142.1 5.93

Non-Institutions 0 0

Others 314 13.17

Source: BSE, Nirmal Bang Institutional Equities Research

Institutional Equities

Sun Pharmaceutical Industries 19

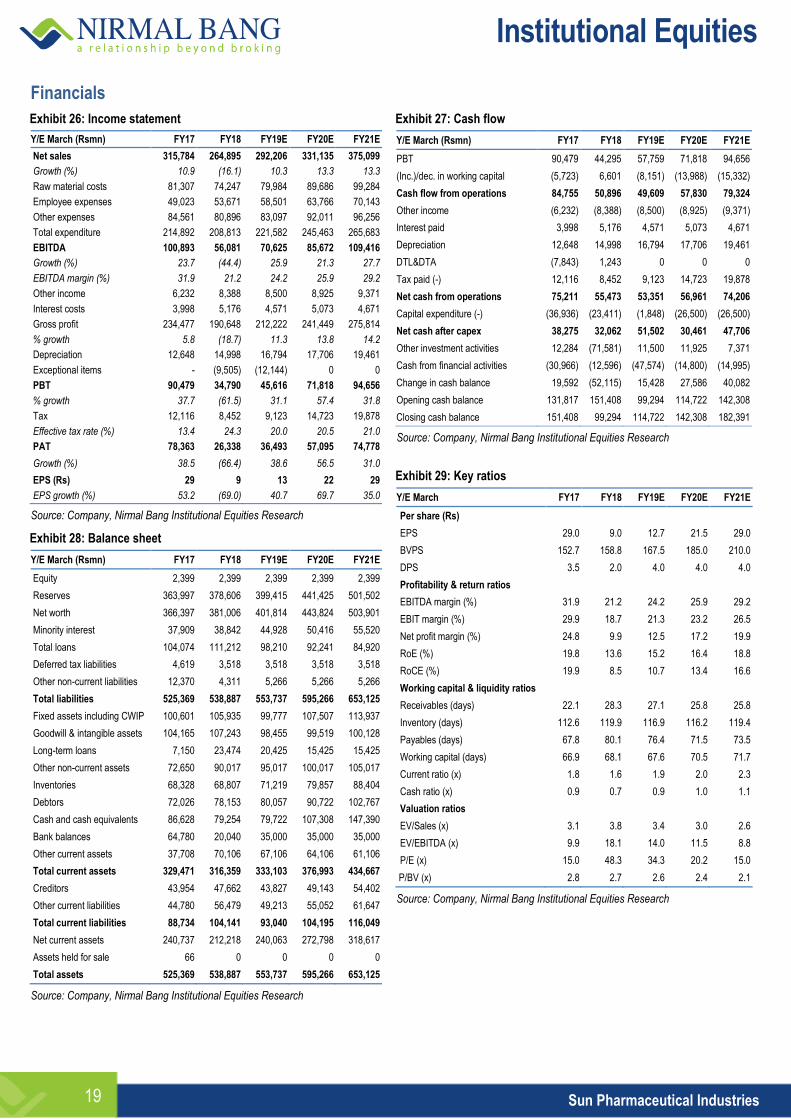

Financials

Exhibit 26: Income statement

Y/E March (Rsmn) FY17 FY18 FY19E FY20E FY21E

Net sales 315,784 264,895 292,206 331,135 375,099

Growth (%) 10.9 (16.1) 10.3 13.3 13.3

Raw material costs 81,307 74,247 79,984 89,686 99,284

Employee expenses 49,023 53,671 58,501 63,766 70,143

Other expenses 84,561 80,896 83,097 92,011 96,256

Total expenditure 214,892 208,813 221,582 245,463 265,683

EBITDA 100,893 56,081 70,625 85,672 109,416

Growth (%) 23.7 (44.4) 25.9 21.3 27.7

EBITDA margin (%) 31.9 21.2 24.2 25.9 29.2

Other income 6,232 8,388 8,500 8,925 9,371

Interest costs 3,998 5,176 4,571 5,073 4,671

Gross profit 234,477 190,648 212,222 241,449 275,814

% growth 5.8 (18.7) 11.3 13.8 14.2

Depreciation 12,648 14,998 16,794 17,706 19,461

Exceptional items - (9,505) (12,144) 0 0

PBT 90,479 34,790 45,616 71,818 94,656

% growth 37.7 (61.5) 31.1 57.4 31.8

Tax 12,116 8,452 9,123 14,723 19,878

Effective tax rate (%) 13.4 24.3 20.0 20.5 21.0

PAT 78,363 26,338 36,493 57,095 74,778

Growth (%) 38.5 (66.4) 38.6 56.5 31.0 19 EPS (Rs) 29 9 13 22 29

EPS growth (%) 53.2 (69.0) 40.7 69.7 35.0

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 28: Balance sheet

Y/E March (Rsmn) FY17 FY18 FY19E FY20E FY21E

Equity 2,399 2,399 2,399 2,399 2,399

Reserves 363,997 378,606 399,415 441,425 501,502

Net worth 366,397 381,006 401,814 443,824 503,901

Minority interest 37,909 38,842 44,928 50,416 55,520

Total loans 104,074 111,212 98,210 92,241 84,920

Deferred tax liabilities 4,619 3,518 3,518 3,518 3,518

Other non-current liabilities 12,370 4,311 5,266 5,266 5,266

Total liabilities 525,369 538,887 553,737 595,266 653,125

Fixed assets including CWIP 100,601 105,935 99,777 107,507 113,937

Goodwill & intangible assets 104,165 107,243 98,455 99,519 100,128

Long-term loans 7,150 23,474 20,425 15,425 15,425

Other non-current assets 72,650 90,017 95,017 100,017 105,017

Inventories 68,328 68,807 71,219 79,857 88,404

Debtors 72,026 78,153 80,057 90,722 102,767

Cash and cash equivalents 86,628 79,254 79,722 107,308 147,390

Bank balances 64,780 20,040 35,000 35,000 35,000

Other current assets 37,708 70,106 67,106 64,106 61,106

Total current assets 329,471 316,359 333,103 376,993 434,667

Creditors 43,954 47,662 43,827 49,143 54,402

Other current liabilities 44,780 56,479 49,213 55,052 61,647

Total current liabilities 88,734 104,141 93,040 104,195 116,049

Net current assets 240,737 212,218 240,063 272,798 318,617

Assets held for sale 66 0 0 0 0

Total assets 525,369 538,887 553,737 595,266 653,125

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 27: Cash flow

Y/E March (Rsmn) FY17 FY18 FY19E FY20E FY21E

PBT 90,479 44,295 57,759 71,818 94,656

(Inc.)/dec. in working capital (5,723) 6,601 (8,151) (13,988) (15,332)

Cash flow from operations 84,755 50,896 49,609 57,830 79,324

Other income (6,232) (8,388) (8,500) (8,925) (9,371)

Interest paid 3,998 5,176 4,571 5,073 4,671

Depreciation 12,648 14,998 16,794 17,706 19,461

DTL&DTA (7,843) 1,243 0 0 0

Tax paid (-) 12,116 8,452 9,123 14,723 19,878

Net cash from operations 75,211 55,473 53,351 56,961 74,206

Capital expenditure (-) (36,936) (23,411) (1,848) (26,500) (26,500)

Net cash after capex 38,275 32,062 51,502 30,461 47,706

Other investment activities 12,284 (71,581) 11,500 11,925 7,371

Cash from financial activities (30,966) (12,596) (47,574) (14,800) (14,995)

Change in cash balance 19,592 (52,115) 15,428 27,586 40,082

Opening cash balance 131,817 151,408 99,294 114,722 142,308

Closing cash balance 151,408 99,294 114,722 142,308 182,391

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 29: Key ratios

Y/E March FY17 FY18 FY19E FY20E FY21E

Per share (Rs)

EPS 29.0 9.0 12.7 21.5 29.0

BVPS 152.7 158.8 167.5 185.0 210.0

DPS 3.5 2.0 4.0 4.0 4.0

Profitability & return ratios

EBITDA margin (%) 31.9 21.2 24.2 25.9 29.2

EBIT margin (%) 29.9 18.7 21.3 23.2 26.5

Net profit margin (%) 24.8 9.9 12.5 17.2 19.9

RoE (%) 19.8 13.6 15.2 16.4 18.8

RoCE (%) 19.9 8.5 10.7 13.4 16.6

Working capital & liquidity ratios

Receivables (days) 22.1 28.3 27.1 25.8 25.8

Inventory (days) 112.6 119.9 116.9 116.2 119.4

Payables (days) 67.8 80.1 76.4 71.5 73.5

Working capital (days) 66.9 68.1 67.6 70.5 71.7

Current ratio (x) 1.8 1.6 1.9 2.0 2.3

Cash ratio (x) 0.9 0.7 0.9 1.0 1.1

Valuation ratios

EV/Sales (x) 3.1 3.8 3.4 3.0 2.6

EV/EBITDA (x) 9.9 18.1 14.0 11.5 8.8

P/E (x) 15.0 48.3 34.3 20.2 15.0

P/BV (x) 2.8 2.7 2.6 2.4 2.1

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

Sun Pharmaceutical Industries 20

DISCLOSURES

This Report is published by Nirmal Bang Equities Private Limited (hereinafter referred to as “NBEPL”) for private circulation. NBEPL is a registered Research Analyst under SEBI (Research Analyst) Regulations, 2014 having Registration no. INH000001436. NBEPL is also a registered Stock Broker with National Stock Exchange of India Limited and BSE Limited in cash and derivatives segments. NBEPL has other business divisions with independent research teams separated by Chinese walls, and therefore may, at times, have different or contrary views on stocks and markets. NBEPL or its associates have not been debarred / suspended by SEBI or any other regulatory authority for accessing / dealing in securities Market. NBEPL, its associates or analyst or his relatives do not hold any financial interest in the subject company. NBEPL or its associates or Analyst do not have any conflict or material conflict of interest at the time of publication of the research report with the subject company. NBEPL or its associates or Analyst or his relatives do not hold beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of this research report. NBEPL or its associates / analyst has not received any compensation / managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. NBEPL or its associates have not received any compensation or other benefits from the company covered by Analyst or third party in connection with the research report. Analyst has not served as an officer, director or employee of Subject Company and NBEPL / analyst has not been engaged in market making activity of the subject company. Analyst Certification: I, Mr. Vishal Manchanda, research analyst and the author of this report, hereby certify that the views expressed in this research report accurately reflects my personal views about the subject securities, issuers, products, sectors or industries. It is also certified that no part of the compensation of the analyst was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst is principally responsible for the preparation of this research report and has taken reasonable care to achieve and maintain independence and objectivity in making any recommendations.

Institutional Equities

Sun Pharmaceutical Industries 21

Disclaimer

Stock Ratings Absolute Returns

BUY > 15%

ACCUMULATE -5% to15%

SELL < -5%

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. NBEPL is not soliciting any action based upon it. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any such transaction. In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader.

This research has been prepared for the general use of the clients of NBEPL and must not be copied, either in whole or in part, or distributed or redistributed to any other person in any form. If you are not the intended recipient you must not use or disclose the information in this research in any way. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. NBEPL will not treat recipients as customers by virtue of their receiving this report. This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject NBEPL & its group companies to registration or licensing requirements within such jurisdictions.

The report is based on the information obtained from sources believed to be reliable, but we do not make any representation or warranty that it is accurate, complete or up-to-date and it should not be relied upon as such. We accept no obligation to correct or update the information or opinions in it. NBEPL or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. NBEPL or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations.

This information is subject to change without any prior notice. NBEPL reserves its absolute discretion and right to make or refrain from making modifications and alterations to this statement from time to time. Nevertheless, NBEPL is committed to providing independent and transparent recommendations to its clients, and would be happy to provide information in response to specific client queries.

Before making an investment decision on the basis of this research, the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of the investment. Opinions expressed are subject to change without any notice. Neither the company nor the director or the employees of NBEPL accept any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Here it may be noted that neither NBEPL, nor its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profit that may arise from or in connection with the use of the information contained in this report.

Copyright of this document vests exclusively with NBEPL.

Our reports are also available on our website www.nirmalbang.com

Access all our reports on Bloomberg, Thomson Reuters and Factset.

Team Details:

Name Email Id Direct Line

Rahul Arora CEO [email protected] -

Girish Pai Head of Research [email protected] +91 22 6273 8017 / 18

Dealing

Ravi Jagtiani Dealing Desk [email protected] +91 22 6273 8230, +91 22 6636 8833

Pradeep Kasat Dealing Desk [email protected] +91 22 6273 8100/8101, +91 22 6636 8831

Michael Pillai Dealing Desk [email protected] +91 22 6273 8102/8103, +91 22 6636 8830

Nirmal Bang Equities Pvt. Ltd.

Correspondence Address

B-2, 301/302, Marathon Innova,

Nr. Peninsula Corporate Park,

Lower Parel (W), Mumbai-400013.

Board No. : 91 22 6273 8000/1; Fax. : 022 6273 8010

Institutional Equities

Sun Pharmaceutical Industries 22

APPENDIX

Institutional Equities

Sun Pharma – Seciera Potential

in Dry Eye Market

Seciera Positioning

Restasis Genericisation Impact

Threat from Pipeline Drug Candidates

Vishal Manchanda

Research Analyst

+91-97374-37148

12 March 2018

Institutional Equities

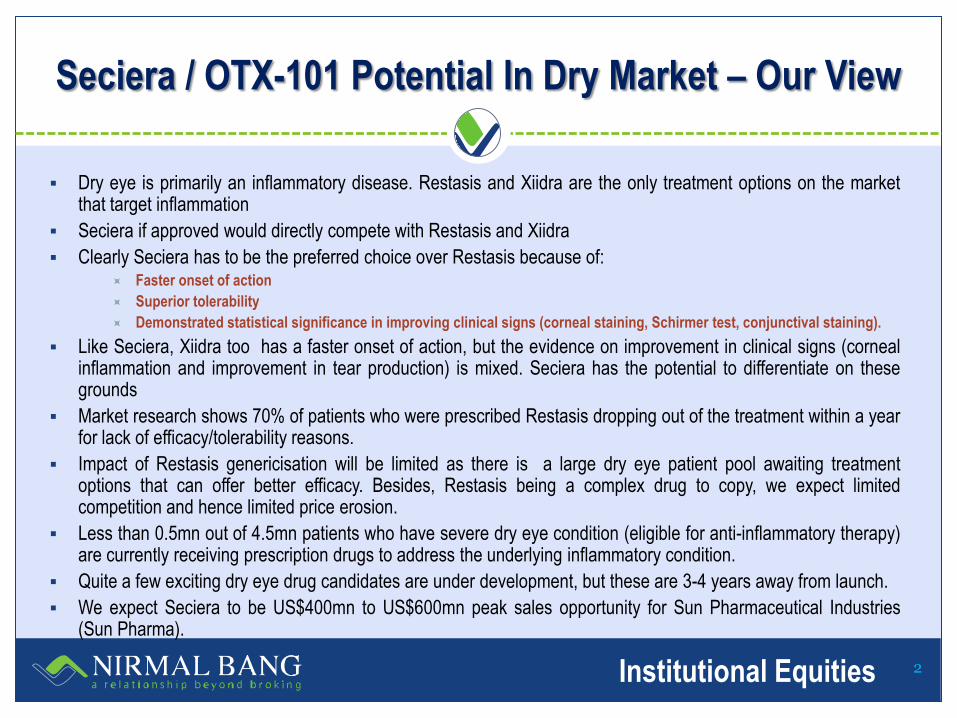

Seciera / OTX-101 Potential In Dry Market – Our View

Dry eye is primarily an inflammatory disease. Restasis and Xiidra are the only treatment options on the market that target inflammation

Seciera if approved would directly compete with Restasis and Xiidra

Clearly Seciera has to be the preferred choice over Restasis because of: Faster onset of action

Superior tolerability

Demonstrated statistical significance in improving clinical signs (corneal staining, Schirmer test, conjunctival staining).

Like Seciera, Xiidra too has a faster onset of action, but the evidence on improvement in clinical signs (corneal inflammation and improvement in tear production) is mixed. Seciera has the potential to differentiate on these grounds

Market research shows 70% of patients who were prescribed Restasis dropping out of the treatment within a year for lack of efficacy/tolerability reasons.

Impact of Restasis genericisation will be limited as there is a large dry eye patient pool awaiting treatment options that can offer better efficacy. Besides, Restasis being a complex drug to copy, we expect limited competition and hence limited price erosion.

Less than 0.5mn out of 4.5mn patients who have severe dry eye condition (eligible for anti-inflammatory therapy) are currently receiving prescription drugs to address the underlying inflammatory condition.

Quite a few exciting dry eye drug candidates are under development, but these are 3-4 years away from launch.

We expect Seciera to be US$400mn to US$600mn peak sales opportunity for Sun Pharmaceutical Industries (Sun Pharma).

2

Institutional Equities

About Seciera / OTX-101 and Dry Eye Market

Sun Pharma’s NDA filing on Seciera (nanomicellar Cyclosporine A) for the treatment of dry eye was accepted for review

by the USFDA in December 2017. A favourable review will potentially mean a launch in calendar year 2018.

Dry eye is a condition in which there are insufficient tears to lubricate and nourish the eye. Tears are necessary for

maintaining the health of the front surface of the eye and for providing clear vision. When severe and left untreated, this

condition can lead to pain, ulcers or scars on the part of the eye called the cornea which translates to tearing, redness,

pain, soreness, and blurred vision.

About 22% of the patients visiting ophthalmologists are dry eye patients.

Seciera or OTX-101 is a novel formulation of widely used drug Restasis (Cyclosporine) for dry eye treatment.

Currently dry eye disease is primarily treated with artificial tears (OTC drugs), while only a small fraction of patients are

treated with prescription drugs.

Restasis (Cyclosporine, US$1.6bn) was the only prescription drug approved for dry eye since long, until the recent

approval for Xiidra (Lifitegrast, US$200mn). Seceira, if approved, will be the third drug in the market. OTC drugs, which

include lubricants / artificial tears, garner around US$540mn in sales annually.

There are 20mn-30mn dry eye patients in the US, of which only 0.4mn are treated with prescription drugs. Prescription

drugs have not seen penetration for two reasons:

Higher cost – Prescription drugs are almost 20x-30x expensive than OTC lubricants.

Reimbursement – Insurance plans require patients to fail on multiple trials of OTC lubricants before they can be prescribed prescription drugs.

Efficacy is limited and most patients fail to get a satisfactory response.

3

Institutional Equities

About Seciera / OTX-101 and Dry Eye Market

Seciera is a nanomicellar formulation of Cyclosporine A in a preservative free aqueous base.

Restasis comes as an oil-in-water emulsion which leads to typical tolerability issues (burning of the

eye).

Seciera is expected to offer the following benefits:

Enhance occular bioavailability of Cyclosporine.

Improve tolerability as nanomicellar formulation allows it to be delivered in a preservative free

aqueous solution.

Seciera has higher concentration (0.09% vs. 0.05%) of Cyclosporine and hence has the

potential to be more effective.

In Phase 2/3 studies, Seciera demonstrated statistically significant improvement in key endpoints:

Tear production – As measured by Schirmer test

Reduction in eye inflammation as measured by corneal and conjunctival staining score.

Reported 30% improvement in SANDE score (to measure symptomatic improvement) which

was comparable to vehicle.

4

Institutional Equities

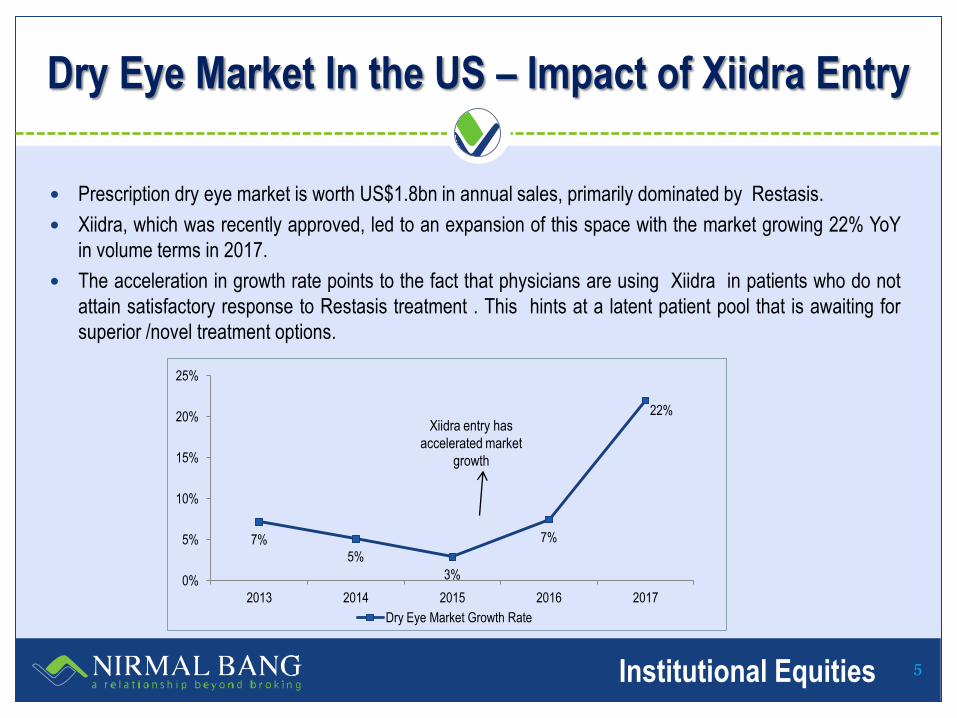

Dry Eye Market In the US – Impact of Xiidra Entry

Prescription dry eye market is worth US$1.8bn in annual sales, primarily dominated by Restasis.

Xiidra, which was recently approved, led to an expansion of this space with the market growing 22% YoY

in volume terms in 2017.

The acceleration in growth rate points to the fact that physicians are using Xiidra in patients who do not

attain satisfactory response to Restasis treatment . This hints at a latent patient pool that is awaiting for

superior /novel treatment options.

7%

5%

3%

7%

22%

0%

5%

10%

15%

20%

25%

2013 2014 2015 2016 2017

Dry Eye Market Growth Rate

Xiidra entry has

accelerated market

growth

5

Institutional Equities

Xiidra Versus Restasis – NBRx Share

6

Institutional Equities

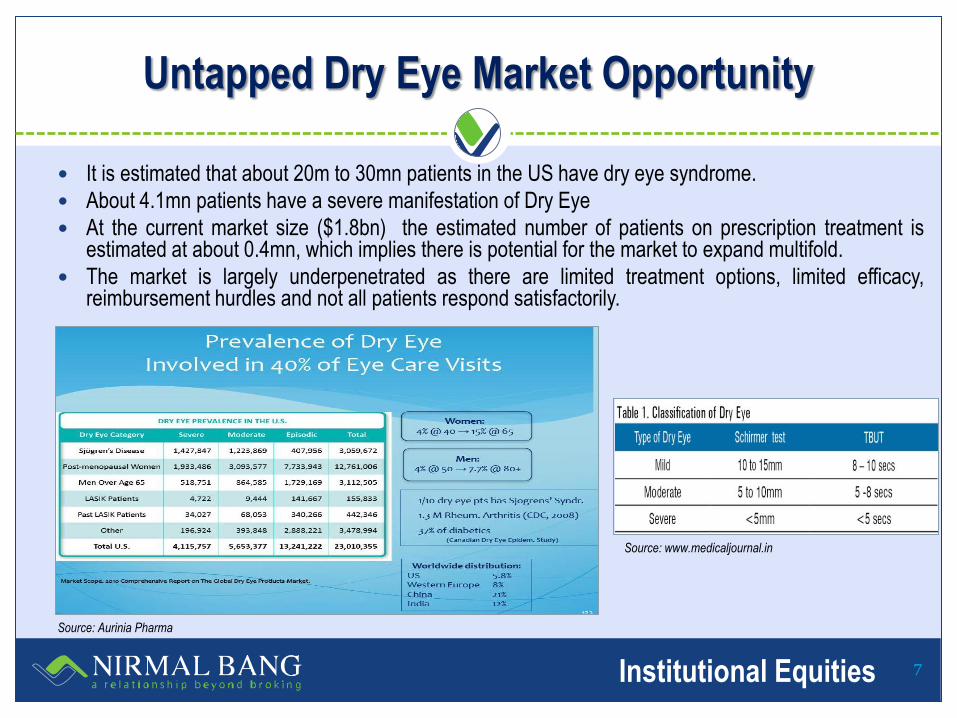

Untapped Dry Eye Market Opportunity

It is estimated that about 20m to 30mn patients in the US have dry eye syndrome.

About 4.1mn patients have a severe manifestation of Dry Eye

At the current market size ($1.8bn) the estimated number of patients on prescription treatment is estimated at about 0.4mn, which implies there is potential for the market to expand multifold.

The market is largely underpenetrated as there are limited treatment options, limited efficacy, reimbursement hurdles and not all patients respond satisfactorily.

Source: Aurinia Pharma

Source: www.medicaljournal.in

7

Institutional Equities

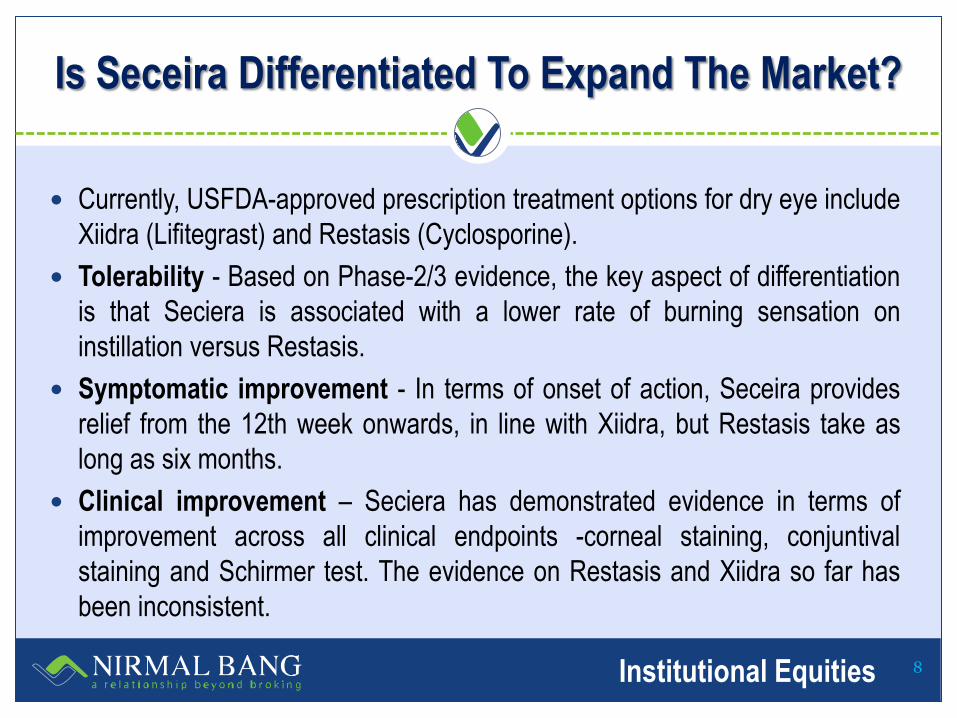

Is Seceira Differentiated To Expand The Market?

Currently, USFDA-approved prescription treatment options for dry eye include

Xiidra (Lifitegrast) and Restasis (Cyclosporine).

Tolerability - Based on Phase-2/3 evidence, the key aspect of differentiation

is that Seciera is associated with a lower rate of burning sensation on

instillation versus Restasis.

Symptomatic improvement - In terms of onset of action, Seceira provides

relief from the 12th week onwards, in line with Xiidra, but Restasis take as

long as six months.

Clinical improvement – Seciera has demonstrated evidence in terms of

improvement across all clinical endpoints -corneal staining, conjuntival

staining and Schirmer test. The evidence on Restasis and Xiidra so far has

been inconsistent.

8

Institutional Equities

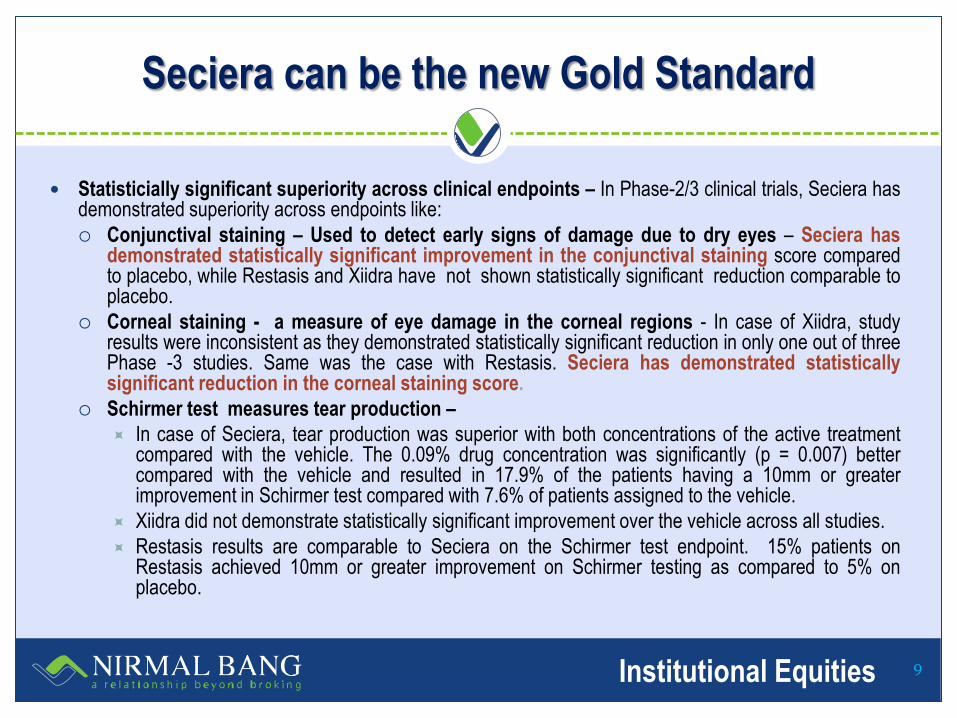

Seciera can be the new Gold Standard

Statisticially significant superiority across clinical endpoints – In Phase-2/3 clinical trials, Seciera has demonstrated superiority across endpoints like:

Conjunctival staining – Used to detect early signs of damage due to dry eyes – Seciera has demonstrated statistically significant improvement in the conjunctival staining score compared to placebo, while Restasis and Xiidra have not shown statistically significant reduction comparable to placebo.

Corneal staining - a measure of eye damage in the corneal regions - In case of Xiidra, study results were inconsistent as they demonstrated statistically significant reduction in only one out of three Phase -3 studies. Same was the case with Restasis. Seciera has demonstrated statistically significant reduction in the corneal staining score.

Schirmer test measures tear production –

In case of Seciera, tear production was superior with both concentrations of the active treatment compared with the vehicle. The 0.09% drug concentration was significantly (p = 0.007) better compared with the vehicle and resulted in 17.9% of the patients having a 10mm or greater improvement in Schirmer test compared with 7.6% of patients assigned to the vehicle.

Xiidra did not demonstrate statistically significant improvement over the vehicle across all studies.

Restasis results are comparable to Seciera on the Schirmer test endpoint. 15% patients on Restasis achieved 10mm or greater improvement on Schirmer testing as compared to 5% on placebo.

9

Institutional Equities

Seciera can be the new Gold Standard

Superior performance in reducing central corneal inflammation - a more relevant endpoint -

Unlike Restasis and Xiidra, Seciera has shown benefit in central corneal inflammation which has higher

correlation with dry eye symptoms.

The central cornea has five to six times as many nerve fibres as the peripheral cornea. Consequently,

corneal sensitivity is higher in central cornea compared to the periphery. It may be noted that symptoms of

dry eye are more prevalent in patients who exhibit greater occular surface damage of central cornea.

Lower burning sensation - The most commonly reported adverse effect with OTX-101 and Restasis is

burning upon instillation of the drops, which can affect patient compliance. With Restasis, about 17% of

the patients reported burning on instillation. In contrast, 1.3% of patients assigned to both OTX-101

concentrations reported severe discomfort. Moderate or severe instillation site pain or discomfort was

reported by only 5.6% of the patients receiving active treatment.

Early onset of action – Seciera improves tear production in patients as early as 12 weeks, (in line with

Xiidra), but much quicker than Restasis which takes as long as six months.

10

Institutional Equities

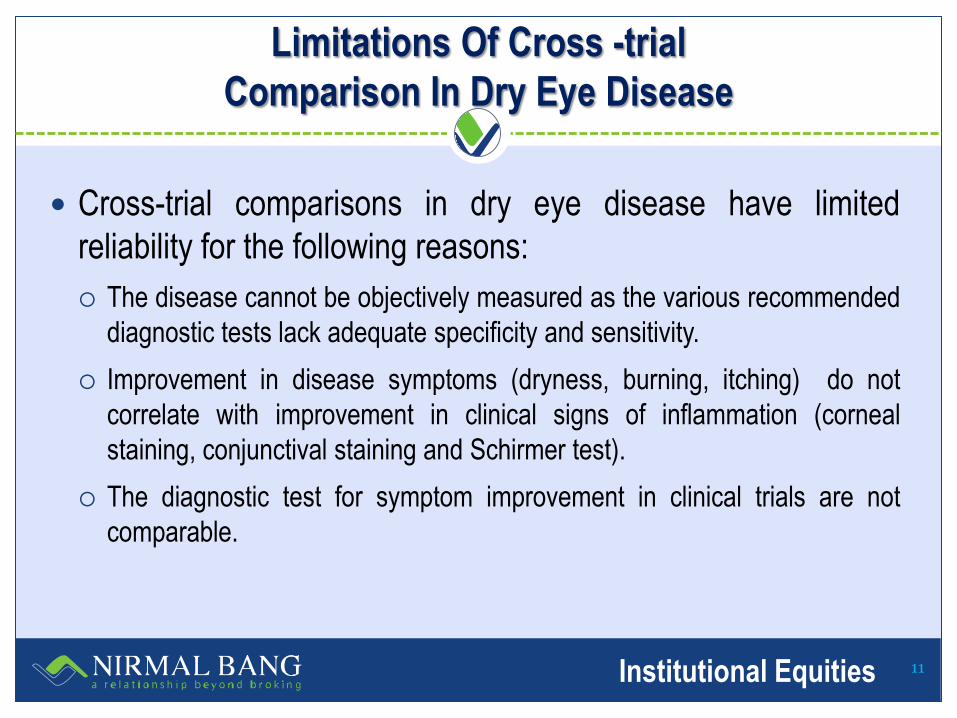

Limitations Of Cross -trial

Comparison In Dry Eye Disease

Cross-trial comparisons in dry eye disease have limited

reliability for the following reasons:

The disease cannot be objectively measured as the various recommended

diagnostic tests lack adequate specificity and sensitivity.

Improvement in disease symptoms (dryness, burning, itching) do not

correlate with improvement in clinical signs of inflammation (corneal

staining, conjunctival staining and Schirmer test).

The diagnostic test for symptom improvement in clinical trials are not

comparable.

11

Institutional Equities

Impact of Restasis Genericisation

on Seciera Market Potential

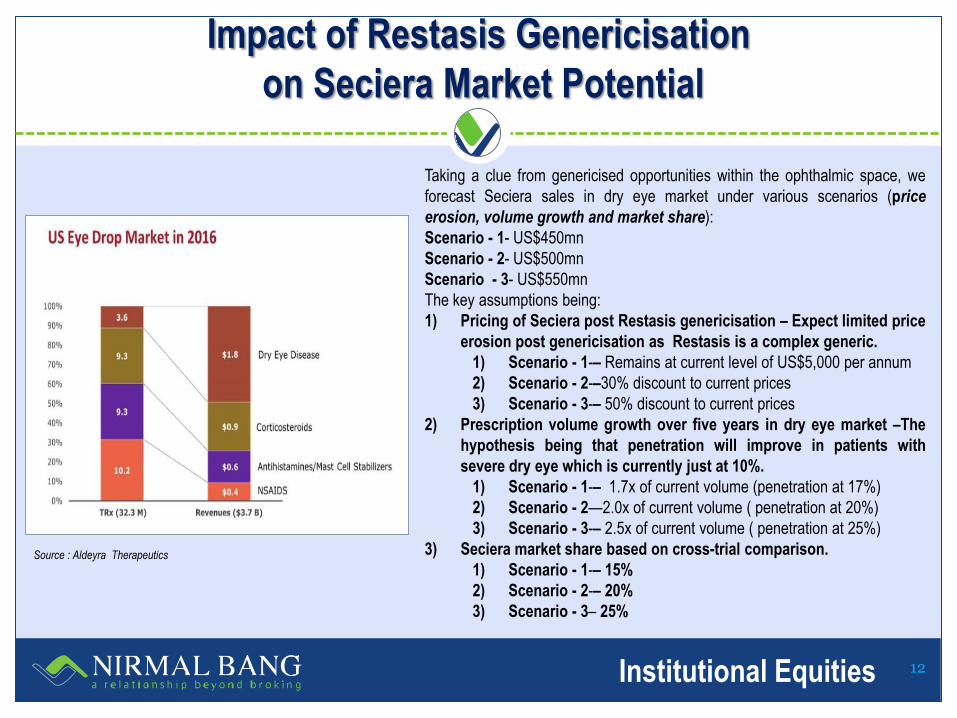

Taking a clue from genericised opportunities within the ophthalmic space, we

forecast Seciera sales in dry eye market under various scenarios (price

erosion, volume growth and market share):

Scenario - 1- US$450mn

Scenario - 2- US$500mn

Scenario - 3- US$550mn

The key assumptions being:

1) Pricing of Seciera post Restasis genericisation – Expect limited price

erosion post genericisation as Restasis is a complex generic.

1) Scenario - 1-– Remains at current level of US$5,000 per annum

2) Scenario - 2-–30% discount to current prices

3) Scenario - 3-– 50% discount to current prices

2) Prescription volume growth over five years in dry eye market –The

hypothesis being that penetration will improve in patients with

severe dry eye which is currently just at 10%.

1) Scenario - 1-– 1.7x of current volume (penetration at 17%)

2) Scenario - 2—2.0x of current volume ( penetration at 20%)

3) Scenario - 3-– 2.5x of current volume ( penetration at 25%)

3) Seciera market share based on cross-trial comparison.

1) Scenario - 1-– 15%

2) Scenario - 2-– 20%

3) Scenario - 3– 25%

Source : Aldeyra Therapeutics

12

Institutional Equities

The dry eye drug pipeline can be categorised into two parts:

Novel Cyclosporine formulations

Novel molecules

Drugs in the Pipeline

for Dry Eye Disease

13

Institutional Equities

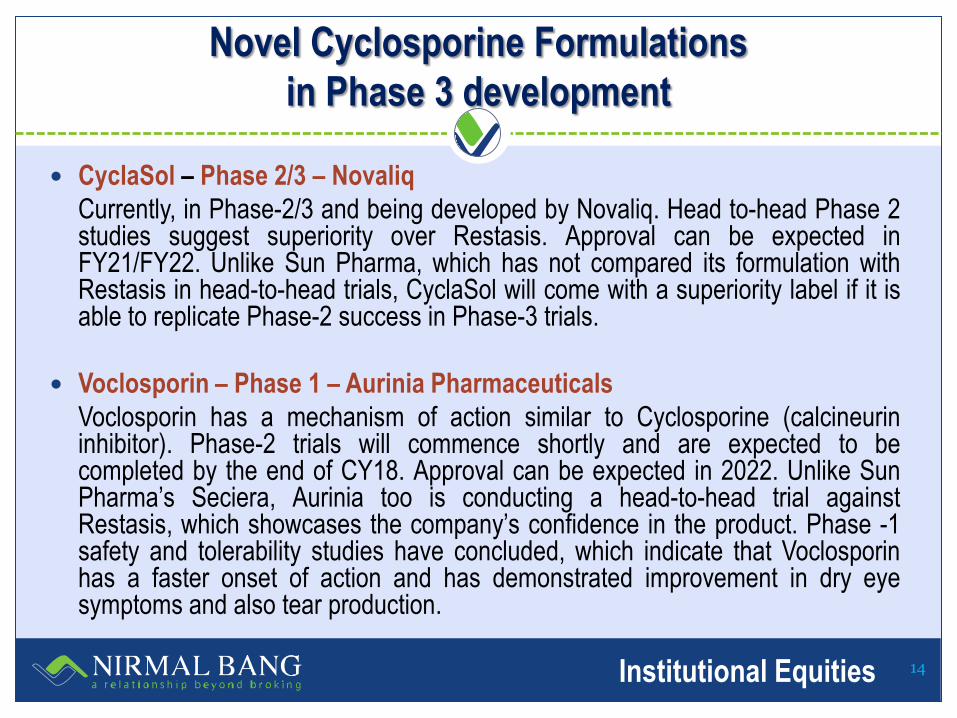

Novel Cyclosporine Formulations

in Phase 3 development

CyclaSol – Phase 2/3 – Novaliq

Currently, in Phase-2/3 and being developed by Novaliq. Head to-head Phase 2 studies suggest superiority over Restasis. Approval can be expected in FY21/FY22. Unlike Sun Pharma, which has not compared its formulation with Restasis in head-to-head trials, CyclaSol will come with a superiority label if it is able to replicate Phase-2 success in Phase-3 trials.

Voclosporin – Phase 1 – Aurinia Pharmaceuticals

Voclosporin has a mechanism of action similar to Cyclosporine (calcineurin inhibitor). Phase-2 trials will commence shortly and are expected to be completed by the end of CY18. Approval can be expected in 2022. Unlike Sun Pharma’s Seciera, Aurinia too is conducting a head-to-head trial against Restasis, which showcases the company’s confidence in the product. Phase -1 safety and tolerability studies have concluded, which indicate that Voclosporin has a faster onset of action and has demonstrated improvement in dry eye symptoms and also tear production.

14

Institutional Equities

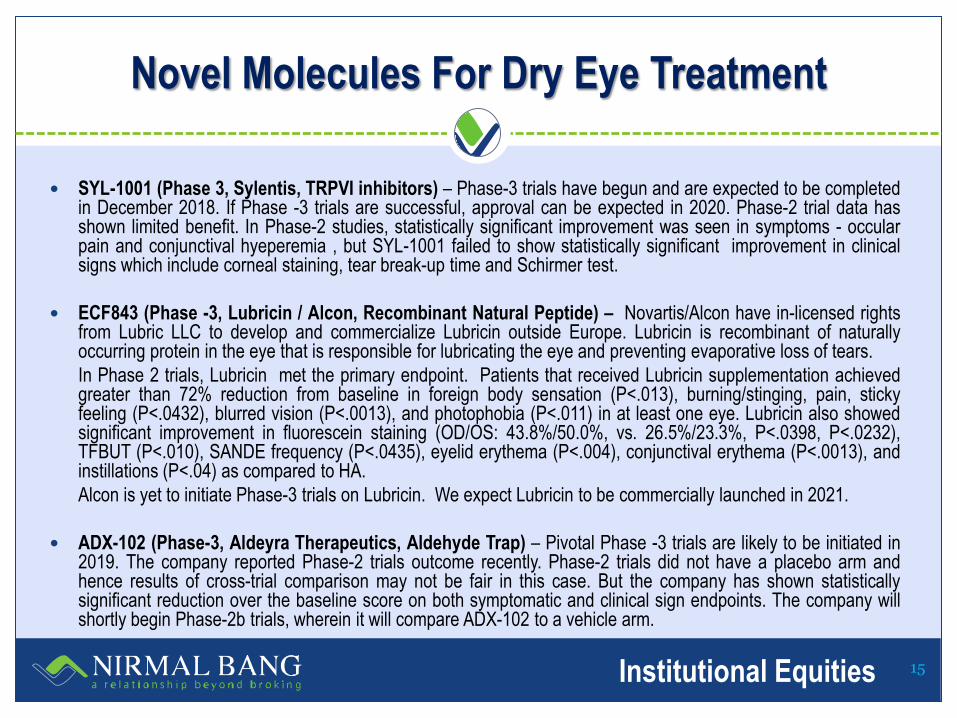

Novel Molecules For Dry Eye Treatment

SYL-1001 (Phase 3, Sylentis, TRPVI inhibitors) – Phase-3 trials have begun and are expected to be completed in December 2018. If Phase -3 trials are successful, approval can be expected in 2020. Phase-2 trial data has shown limited benefit. In Phase-2 studies, statistically significant improvement was seen in symptoms - occular pain and conjunctival hyeperemia , but SYL-1001 failed to show statistically significant improvement in clinical signs which include corneal staining, tear break-up time and Schirmer test.

ECF843 (Phase -3, Lubricin / Alcon, Recombinant Natural Peptide) – Novartis/Alcon have in-licensed rights from Lubric LLC to develop and commercialize Lubricin outside Europe. Lubricin is recombinant of naturally occurring protein in the eye that is responsible for lubricating the eye and preventing evaporative loss of tears.

In Phase 2 trials, Lubricin met the primary endpoint. Patients that received Lubricin supplementation achieved greater than 72% reduction from baseline in foreign body sensation (P<.013), burning/stinging, pain, sticky feeling (P<.0432), blurred vision (P<.0013), and photophobia (P<.011) in at least one eye. Lubricin also showed significant improvement in fluorescein staining (OD/OS: 43.8%/50.0%, vs. 26.5%/23.3%, P<.0398, P<.0232), TFBUT (P<.010), SANDE frequency (P<.0435), eyelid erythema (P<.004), conjunctival erythema (P<.0013), and instillations (P<.04) as compared to HA.

Alcon is yet to initiate Phase-3 trials on Lubricin. We expect Lubricin to be commercially launched in 2021.

ADX-102 (Phase-3, Aldeyra Therapeutics, Aldehyde Trap) – Pivotal Phase -3 trials are likely to be initiated in 2019. The company reported Phase-2 trials outcome recently. Phase-2 trials did not have a placebo arm and hence results of cross-trial comparison may not be fair in this case. But the company has shown statistically significant reduction over the baseline score on both symptomatic and clinical sign endpoints. The company will shortly begin Phase-2b trials, wherein it will compare ADX-102 to a vehicle arm.

15

Institutional Equities

Novel Molecules For Dry Eye Treatment

Tavilermide (Phase -3, Allergan/Mimetogen, Neutrophin Mimetic)– Allergan has in-licensed rights for Tavilermide from innovator

Mimetogen. Phase -3 trials on Tavilermide has been recently completed and the data is yet to be reported. Tavilermide is a neurotrophin

mimetic that acts as a partial agonist of the nerve growth factor receptor TrkA.

In Phase-2 trials which evaluated symptomatic and improvement in clinical signs post four weeks of treatment, the evidence pointed to a

positive effect but statistical significance was not achieved. Tavilermide did not demonstrate statistical significance over placebo, but there

was evidence of positive effect.

RGN-259 (Phase -3, RegenerX, Thymosin Beta 4)- RGN-259 is an antagonist of Thymosin Beta-4, a peptide naturally found in various

human blood cells that has anti-inflammatory activity and promotes tissue repair. RGN-259 demonstrated a rapid onset of action in a Phase-2

clinical trial and is being developed in a preservative-free formulation. On the final day of dosing (Day 28), patients receiving 0.1% RGN-259

had a statistically significant reduction in occular discomfort during CAESM (Controlled Adverse Environment) exposure when compared to

placebo (Intent-to-Treat Population (ITT), p=0.043). Importantly, this result was also observed in previous Phase-2 trial in patients treated with

0.1% RGN-259 (ITT, p=0.024), thereby demonstrating a symptom endpoint in two independent trials. A statistically significant occular

discomfort improvement after CAESM exposure on Day 28 was also observed in the 0.05% and 0.1% RGN-259 treatment arms when

compared to placebo (ITT, p=0.0366 and p=0.0072, respectively) indicating a dose- dependent response.

In this population, patients receiving 0.1% RGN-259 had a statistically significant reduction in corneal fluorescein staining prior to entering the

CAESM on Day 28 when compared to placebo (p=0.034). The same result was observed in previous Phase-2 trial for patients treated with

0.1% RGN-259, although it was not statistically significant in the smaller sample size of this previous Phase-2 trial. Additionally, a change from

baseline analysis (Day 28 minus Day 0) demonstrated statistically significant improvement in inferior corneal staining for the 0.1% RGN-259

treatment arm when compared to placebo (p=0.003). This finding was also observed at Day 14 compared to placebo (p=0.035). The data

suggests that RGN-259 has a fast-acting treatment effect on dry eye sign after 14 and 28 days of dosing.

16

Institutional Equities

View – Seciera Positioning In Dry Eye Market

Current dry eye treatment options offer limited satisfaction as only a fraction of patients are able to reach the treatment goal. As dry eye is a multifactorial disease, a variety of approaches including combination treatment is required. Newer treatment options as they reach the market will expand the market.

Currently less than 0.5mn out of 4.1mn severe dry eye patients are being treated for inflammation.

Seciera is differentiated to the extent that it has a superior onset of action which is critical, as in the absence of symptomatic improvement patients tend to discontinue treatment because they perceive it to be ineffective.

Clinical evidence suggests that Seciera addresses inflammatory aspect more efficiently than Restasis. This is probably because of better occular bioavailability (nanomicellar formulation) and a higher dose concentration (0.09% vs. 0.05%).

Tolerability issues like burning on instillation are much lower with Seciera than Restasis as Seciera comes in an aqueous solution, while Restasis comes in an oil-in-water emulsion.