Embed Size (px)

Citation preview

InsideTelecommunications

Jonathan Dharmapalan Global Telecommunications Leader

New device form factors and network technologiesWelcome to the 12th edition of Inside Telecommunications, EY’s review of the most significant developments in the telecoms sector. In this issue, we consider a number of industry themes, from innovations in mobile payments and advertising platforms to wearable devices and technology developments in super-fast broadband.

We hope you find this material useful. Please do not hesitate to share your feedback with me or any of my colleagues at EY.

Issue 12

Service innovation 4

New moves to combine mobile payments and marketing 4

Mobile data pricing evolves in new directions 6

Regulation 12

US ruling reignites net neutrality debate 12

India receives clarity on M&A regime 14

Mergers and Acquisitions 16

Introduction 16

Latin America in the spotlight 16

Private equity activity on the rise 17

Stake increases in India 18

Consolidation comes to Hong Kong 19

Japanese telcos look overseas for growth 19

Technology 8

Wearable technology comes of age 8

New technologies improve the economics of super-fast broadband rollouts 10

Contents

3Issue 12 |

All told, 2013 was a bumper year for deals across technology, media and telecommunications, with global deal value hitting US$510.3 billion, an increase of 54% on the preceding year.1 Looking ahead, growing enterprise demands for cloud and mobility, coupled with high innovation rates in mobile retail and social networking, are likely to trigger further transactions as the lines blur between industry subsegments.

While operators are considering how far they can adapt to new ecosystems that straddle different industry verticals, their relationships with web and technology giants is coming under ever more scrutiny. Facebook’s February acquisition of mobile messaging provider WhatsApp coupled with Google’s swoop for thermostat maker Nest in January reveal high ambition levels in domains as diverse as social messaging and the smart home. How operators position themselves for growth will be considered ever more closely as a result.

However, it’s easy to forget the importance of innovation in core market segments. Operators have long been looking for ways to mitigate costly upgrades to super-fast broadband infrastructure, particularly in Western markets, where the pace of change has underperformed other regions. In recent months, vectoring deployments have gathered pace, while G.Fast technology promises to extend the life of carriers’ copper assets, which are vital if national fiber broadband coverage targets are to be met in the long term.

Innovative technologies have an important role to play in easing the migration path to more robust infrastructure that can handle the growing data demands of end users, whether consumers or businesses. However, the future-proofing of networks is no easy task, particularly as technology cycles shorten. In October, UK researchers revealed they had achieved data transmission speeds of 10Gbps using Li-Fi — wireless internet connectivity using light that could prove more efficient than current wireless radio systems.

The move from the laboratory to a fully fledged commercial proposition is by no means guaranteed, but such innovations demonstrate how the telecommunications sector remains the scene of considerable technological innovation. At the same time, disruptive service providers remain a solid feature of the industry landscape. Google is already earmarking 10Gbps speeds for its own fiber broadband offering, although coverage levels of its super-fast service currently remain limited to three cities in the US.

Service pricing remains another area where operators are experimenting in droves. Family and shared data plans have been in place for some time in the US, yet the pace of change is quickening, with recent developments in machine-to-machine pricing and AT&T’s launch of sponsored data underlining that service providers just cannot stand still as they look for the optimal mix of pricing options for mobile data.

Foreword

Adrian BaschnongaLead AnalystGlobal Telecommunications [email protected]

Deal activity remains on the rise in the telecommunications sector, which is bracing itself for a new round of consolidation in core markets as operators also consider moves into adjacent areas. Yet while regulators continue to mull over consolidation scenarios, technology providers are keen to strengthen their footholds in growth areas too — and operator relationships with over-the-top (OTT) players was a leading theme at this year’s Mobile World Congress in Barcelona.

1. Mergermarket.

4 | Inside Telecommunications

4. “Weve takes on tech giants in battle of m-commerce,” Campaign, 3 October 2013; “Weve Mobile Display Service goes into Beta,” Weve, 29 January 2014. 5. “Mobile Location-based Marketing Solutions Analysis and Market Forecast 2013-2018,” PR Newswire, 13 November 2013.

2. “Gartner Says Worldwide Mobile Payment Transaction Value to Surpass $235 Billion in 2013,” Gartner, 4 June 2013. 3. Ibid; “Global Mobile Economy 2013,” GSMA/AT Kearney, 2013.

In this light, mobile operators are considering new ways of adding value, differentiating their retail POS-driven payments propositions in developed markets to include additional functionalities such as customer analytics and marketing for retailers.

Partnerships are a key consideration as operators refine their proximity payments initiatives. Three of the UK’s four mobile operators have formed a joint venture called Weve, which is offering mobile advertising and loyalty services to brands ahead of providing mobile payments capability. The mobile payments alliance has been stepping up its activities over the last year. By October 2013, it had built an audience of 20m mobile users, with some 400 SMS and MMS marketing campaigns delivered for 175 brands, and in January 2014 announced it was trialing a beta version of its mobile display advertising service.4

Location sensitivity has been built into a number of campaigns — on an anonymized basis — and advertisers can target users via postal area, as well as other attributes such as handset brand and type of mobile contract. Weve believes that such capabilities represent a differential advantage, while the UK mobile advertising market itself is forecast to grow strongly in the next few years, accounting for 31% of total media advertising spending by 2017. Optimism in the potential for location-based marketing is grounded in higher click-through rates (CTRs), with industry watchers predicting that location-sensitive advertising will generate double the industry average by 2020.5

New moves to combine mobile payments and marketingMuch has been made of the long-term growth potential of mobile payments and the role operators have been playing in bringing financial services to the unbanked or providing contactless payments at the retail point-of-sale (POS). Current take-up rates are encouraging: last year, Gartner predicted that the number of mobile payment users worldwide would reach 245.2 million by the end of 2013, up 22% year-on-year.2

Nevertheless, the number of mobile payment users is equivalent to just 7% of global mobile phone users, underlining that device-based payments are still very much in their infancy.3 This is particularly true of developed markets, where a wide range of pre-existing payments instruments, high levels of cross-sector competition, fragmented technologies and regulatory complexity have tempered take-up rates.

1.Service innovation

5Issue 12 |

6. “Belgacom and partners to launch mobile wallet,” Mobile World Live, 13 March 2013. 7. “CaixaBank, Santander and Telefonica to create the first joint venture between banks and telecom operators in Europe to develop new digital businesses,” Telefonica blog, 20 May 2013. 8. “AT&T and Vantiv Announce New Mobile Payments Solutions for Businesses of All Sizes,” AT&T, 14 January 2014.

Operators are collaborating more than ever before on mobile payments platforms in developed markets, forgoing traditional rivalries to make the most of their sizable customer bases and fend off competition from web and e-commerce giants.

Yet mobile operators are also forming national joint ventures with banks as they seek to combine a unique set of core competencies as part of more inclusive payments ecosystems. Last year, Belgacom and BNP Paribas Fortis announced an m-commerce joint venture, which was subsequently approved by the European Commission.

The partners plan a mix of functions, including purchasing goods and redeeming coupons, with in-app payment services highlighted as an anchor service. Moreover, the joint venture plans to open the platform to any subscriber with a smartphone or bank customer with a debit or credit card.6

This new form of interaction between operators and retail banks is also evident in Spain, where Telefonica has announced a joint venture with CaixaBank and Santander. Together, they plan to commence activities by providing an online interface between merchants and consumers for offers, discounts and promotions. A digital wallet is also in the offing, with person-to-person as well as merchant payments in the pipeline. Initially, the joint venture is targeting some 600,000 businesses in Spain but has also revealed plans to internationalize its services — at the same time underlining that it remains open to new partners.7

While European initiatives point to a growing intersection of payments and marketing solutions in the mobile world, some operators are looking to broaden their payments solutions even further, taking on disruptive innovators at the mobile POS. In January, AT&T announced it had partnered with payments technology specialist Vantiv Inc. to offer an app-based credit and debit card reader solution for smartphones and tablets.8 This is designed as a rival offering to products from Square and iZettle, which have proved popular with sole traders wishing to sidestep the cost of chip and PIN card readers.

Figure 1: UK mobile advertising spending, 2012–17

Source: “UK Mobile Ad Spending to Pass the £1 Billion Mark This Year!,” eMarketer, 19 December 2013.

% total media ad spending

0

20

40

60

80

100

0

1,000

2,000

3,000

4,000

5,000

6,000

2012 2013 2014 2015 2016 2017

UK mobile ad spending (£m)

6 | Inside Telecommunications

While operator partnerships now extend in many different directions — encompassing card issuers, mobile loyalty and m-commerce providers, retail banks, and fellow operators — some carriers are also investing in early-stage technology start-ups. Sweden’s TeliaSonera has invested in NorthID and Accumulate, which develop applications and processes for digital identity and mobile payments, respectively. Meanwhile, Telefonica Digital has invested in US-based mobile payments platform Boku along with venture capital firms. Such activity is not restricted to developed market operators — in October, Jamaica-based Digicel invested in Flint, a start-up that leverages the smartphone camera instead of a dongle to scan credit and debit cards.9

While mobile operators are certainly showing themselves to be more agile as they strike new horizontal and vertical partnerships, a number of challenges continue to overshadow the mobile payments market. Fragmentation is a very real problem — in the US, there are now a number of competing ecosystems, with merchants and mobile operators forming separate industry initiatives. Furthermore, the mobile POS reader market is increasingly congested as a raft of “me too” hardware products hit the market.

There are also new technologies coming to market that will widen the landscape for innovation in POS mobile payments. Bluetooth low energy (BLE) technology and beacon applications are likely to gain traction as an alternative to NFC while hosted card emulation (HCE) could also disrupt existing business models by allowing a greater range of players to take control of service provisioning.

For merchants eager to make the most of smartphone usage and location-sensitive services in a retail environment, the choice of solutions can be bewildering. Couple this with the fact that technologies continue to proliferate, and it is clear that migration to mobile solutions will take time — with service success dependent on a range of factors, from the costs of upgrading legacy POS infrastructure to appetite for value-added solutions that incorporate many use cases.

Mobile data pricing evolves in new directionsStrong growth in demand for mobile data is leading operators to provide new monthly packages to subscribers, targeting end users that want the flexibility to share connectivity across multiple devices or with other family members, as well as those seeking more flexible handset payment options. The benefits for operators are clear: revenue upside and churn reduction through new value propositions alongside lower customer acquisition and retention costs.

The prognosis for take-up is positive. By 2015, some 186m mobile broadband devices worldwide are expected to be sold on shared data plans, equivalent to 15% of total devices sold.10 Smartphones are set to account for 47% of shared data plan devices worldwide by 2015, with USB cards accounting for 25% of shared data devices and tablets an additional 15% of the total.11

Operators in the US have been the first to adopt such pricing models, catalyzed by their early migration to LTE networks. Having moved to tiered data tariffs following the launch of 4G, US carriers began offering data plans for users with multiple devices in 2012. Subscriber take-up has been strong, with an increasing number of shared data plan customers upgrading to packages with higher usage allowances.

9. “Mobile Payments Startup Flint Raises $6M Series B Led By Digicel Group,” TechCrunch, 25 October 2013.

10. “Infonetics Research Whitepaper: The New Requirements of Shared Data Plans,” Infonetics, October 2011. 11. Ibid.

Figure 2: Global mobile broadband devices sold on shared plans, 2015Millions of units

Source: “Infonetics Research Whitepaper: The New Requirements of Shared Data Plans,” Infonetics, October 2011.

0102030405060708090

100

Smar

tpho

nes

USB

car

ds

Tabl

ets

Net

book

s

Mob

ile in

tern

etde

vice

s (M

IDs)

Mob

ile ro

uter

s

Embe

dded

lapt

ops

7Issue 12 |

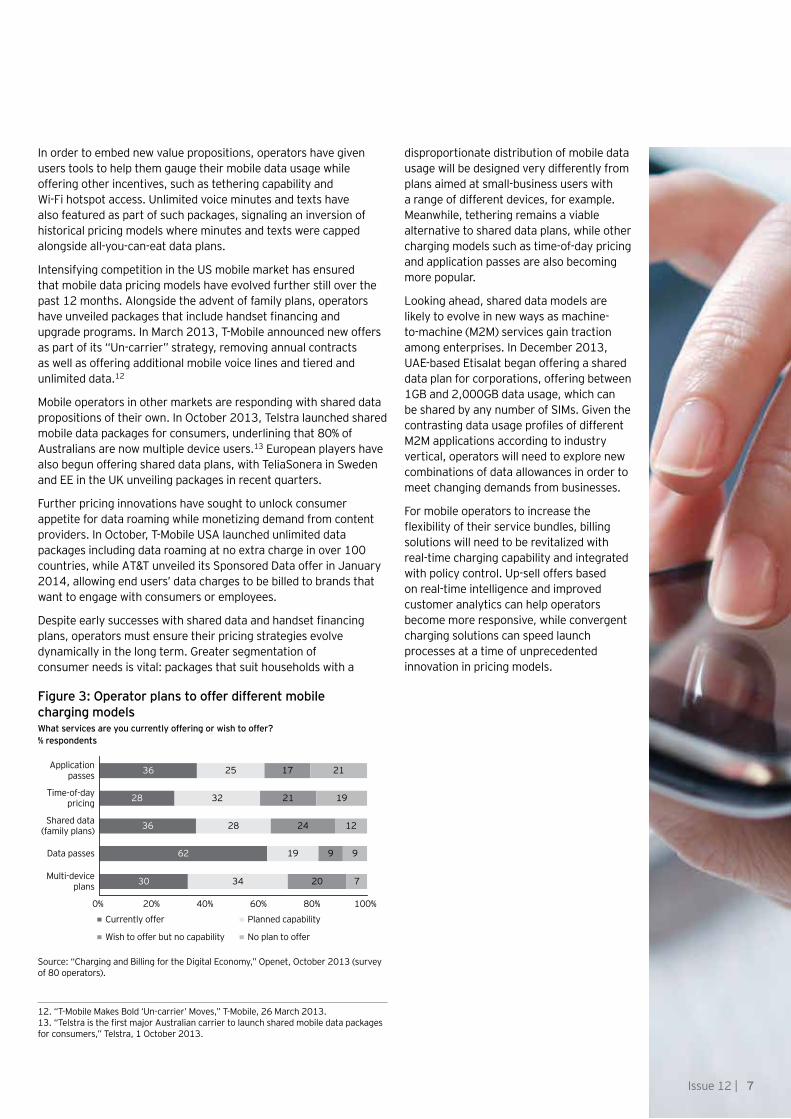

In order to embed new value propositions, operators have given users tools to help them gauge their mobile data usage while offering other incentives, such as tethering capability and Wi-Fi hotspot access. Unlimited voice minutes and texts have also featured as part of such packages, signaling an inversion of historical pricing models where minutes and texts were capped alongside all-you-can-eat data plans.

Intensifying competition in the US mobile market has ensured that mobile data pricing models have evolved further still over the past 12 months. Alongside the advent of family plans, operators have unveiled packages that include handset financing and upgrade programs. In March 2013, T-Mobile announced new offers as part of its “Un-carrier” strategy, removing annual contracts as well as offering additional mobile voice lines and tiered and unlimited data.12

Mobile operators in other markets are responding with shared data propositions of their own. In October 2013, Telstra launched shared mobile data packages for consumers, underlining that 80% of Australians are now multiple device users.13 European players have also begun offering shared data plans, with TeliaSonera in Sweden and EE in the UK unveiling packages in recent quarters.

Further pricing innovations have sought to unlock consumer appetite for data roaming while monetizing demand from content providers. In October, T-Mobile USA launched unlimited data packages including data roaming at no extra charge in over 100 countries, while AT&T unveiled its Sponsored Data offer in January 2014, allowing end users’ data charges to be billed to brands that want to engage with consumers or employees.

Despite early successes with shared data and handset financing plans, operators must ensure their pricing strategies evolve dynamically in the long term. Greater segmentation of consumer needs is vital: packages that suit households with a

12. “T-Mobile Makes Bold ‘Un-carrier’ Moves,” T-Mobile, 26 March 2013. 13. “Telstra is the first major Australian carrier to launch shared mobile data packages for consumers,” Telstra, 1 October 2013.

disproportionate distribution of mobile data usage will be designed very differently from plans aimed at small-business users with a range of different devices, for example. Meanwhile, tethering remains a viable alternative to shared data plans, while other charging models such as time-of-day pricing and application passes are also becoming more popular.

Looking ahead, shared data models are likely to evolve in new ways as machine-to-machine (M2M) services gain traction among enterprises. In December 2013, UAE-based Etisalat began offering a shared data plan for corporations, offering between 1GB and 2,000GB data usage, which can be shared by any number of SIMs. Given the contrasting data usage profiles of different M2M applications according to industry vertical, operators will need to explore new combinations of data allowances in order to meet changing demands from businesses.

For mobile operators to increase the flexibility of their service bundles, billing solutions will need to be revitalized with real-time charging capability and integrated with policy control. Up-sell offers based on real-time intelligence and improved customer analytics can help operators become more responsive, while convergent charging solutions can speed launch processes at a time of unprecedented innovation in pricing models.

Figure 3: Operator plans to offer different mobile charging modelsWhat services are you currently offering or wish to offer?% respondents

Source: “Charging and Billing for the Digital Economy,” Openet, October 2013 (survey of 80 operators).

34

19

28

32

2536

36

62

30

28

20

9

24

21

17

7

9

12

19

21

0% 20% 40% 60% 80% 100%

Multi-deviceplans

Data passes

Shared data(family plans)

Time-of-daypricing

Applicationpasses

Currently offer

Wish to offer but no capability

Planned capability

No plan to offer

8 | Inside Telecommunications

14. “Cisco Visual Networking Index: Global Mobile Data Traffic Forecast Update,” Cisco, 5 February 2014.

Wearable technology comes of age

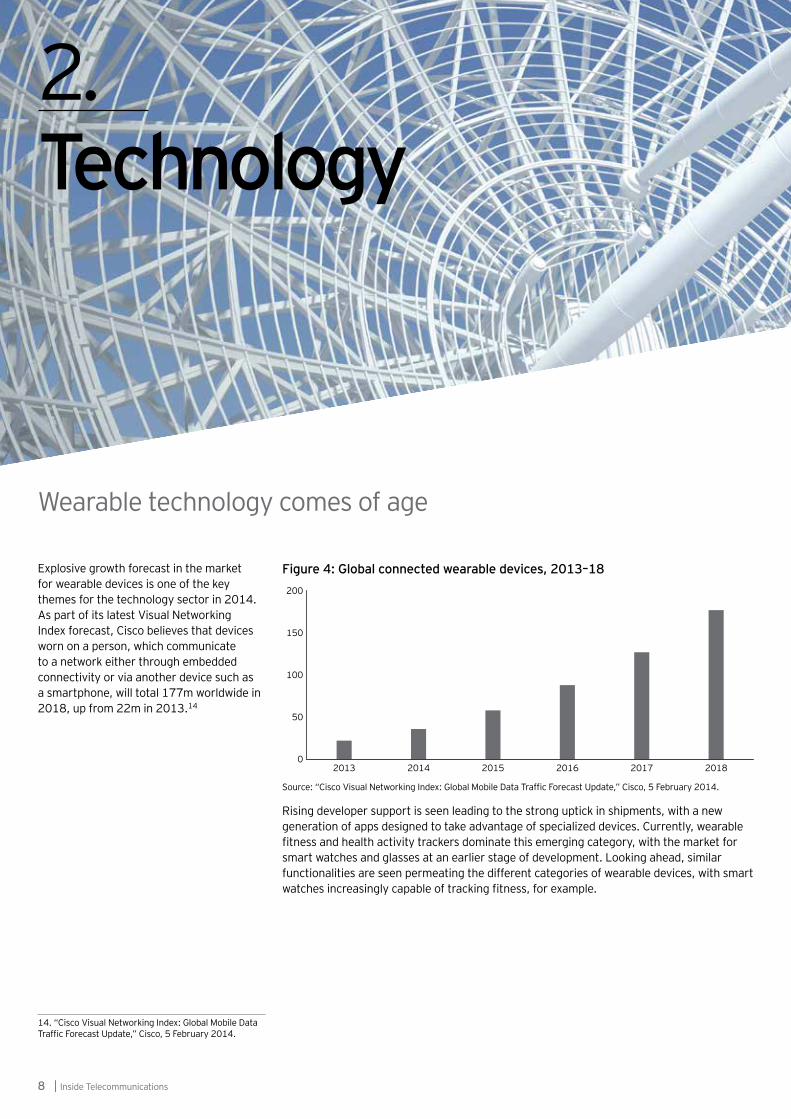

Explosive growth forecast in the market for wearable devices is one of the key themes for the technology sector in 2014. As part of its latest Visual Networking Index forecast, Cisco believes that devices worn on a person, which communicate to a network either through embedded connectivity or via another device such as a smartphone, will total 177m worldwide in 2018, up from 22m in 2013.14

2.Technology

Rising developer support is seen leading to the strong uptick in shipments, with a new generation of apps designed to take advantage of specialized devices. Currently, wearable fitness and health activity trackers dominate this emerging category, with the market for smart watches and glasses at an earlier stage of development. Looking ahead, similar functionalities are seen permeating the different categories of wearable devices, with smart watches increasingly capable of tracking fitness, for example.

Source: “Cisco Visual Networking Index: Global Mobile Data Traffic Forecast Update,” Cisco, 5 February 2014.

Figure 4: Global connected wearable devices, 2013–18

0

50

100

150

200

2013 2014 2015 2016 2017 2018

9Issue 12 |

At present, wearable devices are seen as an offshoot of the smartphone market, yet rising vendor support is likely to spur its evolution as a stand-alone device category. Samsung and Sony are two consumer electronics giants with clear ambitions in this space. Samsung’s Galaxy Gear sports a 1.6-inch screen and includes a 1.9-megapixel camera on its wrist strap, while Sony’s SmartWatch 2 features NFC capability and comes with universal Android compatibility.

Other leading vendors such as Apple, Google, HTC and Microsoft all have plans to launch smart watches this year. In view of this, established device vendors will be forced to rethink their product lines in years to come — the co-existence of smartphones, tablets and wearable devices will create new points of differentiation and integration in terms of functionality and price points, for example.

Nevertheless, the emerging wearables segment also has its fair share of specialist device manufacturers. Fitbit, a US-based maker of health monitor gadgets, launched its first product in 2009 and has received backing from the venture capital arms of both chip maker Qualcomm and Japanese mobile operator SoftBank. Another notable start-up is French technology firm Withings, which last year launched a wearable fitness tracker — Smart Activity Tracker — to track personal physiological data, using a companion app to collect and store information in real time.

Wearable devices are expected to drive growth across a number of technology subsegments. Increasing demand for sensors in wearable technology will translate into a higher proportion of semiconductor components in such devices, for example. Moreover, while smartphones are the principal companion device for wearable

gadgets at present, wireless connectivity through Wi-Fi or cellular modules will become increasingly important, signaling new opportunities for specialist vendors.

The wearables segment in all its guises forms an important aspect of the Internet of Things (IoT), the catchall term used to describe a network of physical objects containing embedded technology that allows them to interact with each other or the external environment. Eye-catching product announcements aside, device vendors and operators are considering how the advent of wearable technology will redefine demands from consumers and enterprises. On the consumer side, recent surveys highlight willingness to purchase wearable devices but also underline concerns regarding personal privacy.

Source: “SSI Survey On Popularity Of Wearable Computers,” SSI, September 2013 (sample of 3,645 people).

Figure 5: Attitudes to wearable technology in different markets% respondents

% very or somewhat likely to purchase

Australia France Germany Japan Netherlands UK US

35 36

0

10

20

30

40

50

37

46

22

3633

2227 29

21

32

43

35

% believe it will lead to an invasion of people's privacy

10 | Inside Telecommunications

16. “Broadband coverage in Europe in 2012,” European Commission, November 2013.15. “SSI Survey On Popularity Of Wearable Computers,” SSI, September 2013 (sample of 3,645 people).

Wristbands and glasses are the preferred form factors for the majority of end users, yet many consumers deem invasion of privacy a very real threat. When asked about their feelings on wearable technology’s ability to record data, concern over privacy was cited more often than perceptions of added convenience, highlighting how end users are greeting new device use cases with a mixture of curiosity and caution.15

For their part, mobile operators will need to ensure that they understand end users’ shifting attitudes as they look to harness wearable device capabilities as part of their own service offerings. Although wearables are not seen placing new demands on the network — Cisco believes they will account for just 0.4% of mobile data traffic by 2018 — wearable technologies will certainly impact M2M and IoT strategies, where operators see themselves providing service enablement platforms for different industry verticals.

Device management capabilities must evolve to keep pace with the different device types being added to the network, while the analytics underpinning different use cases is also likely to prove lucrative in years to come. New wearable devices will also impact service provider pricing and subsidy models — perhaps through bundling data packages with particular devices, or reselling low-cost, mass-market gadgets.

Looking ahead, partnering frameworks should also be revisited as wearable devices alter consumer demands. While tie-ups with specialist device manufacturers will no doubt increase in importance on a per-vertical basis, relationships with fashion and sports brands may also provide upside in the long term as a range of players look to take advantage of these new form factors.

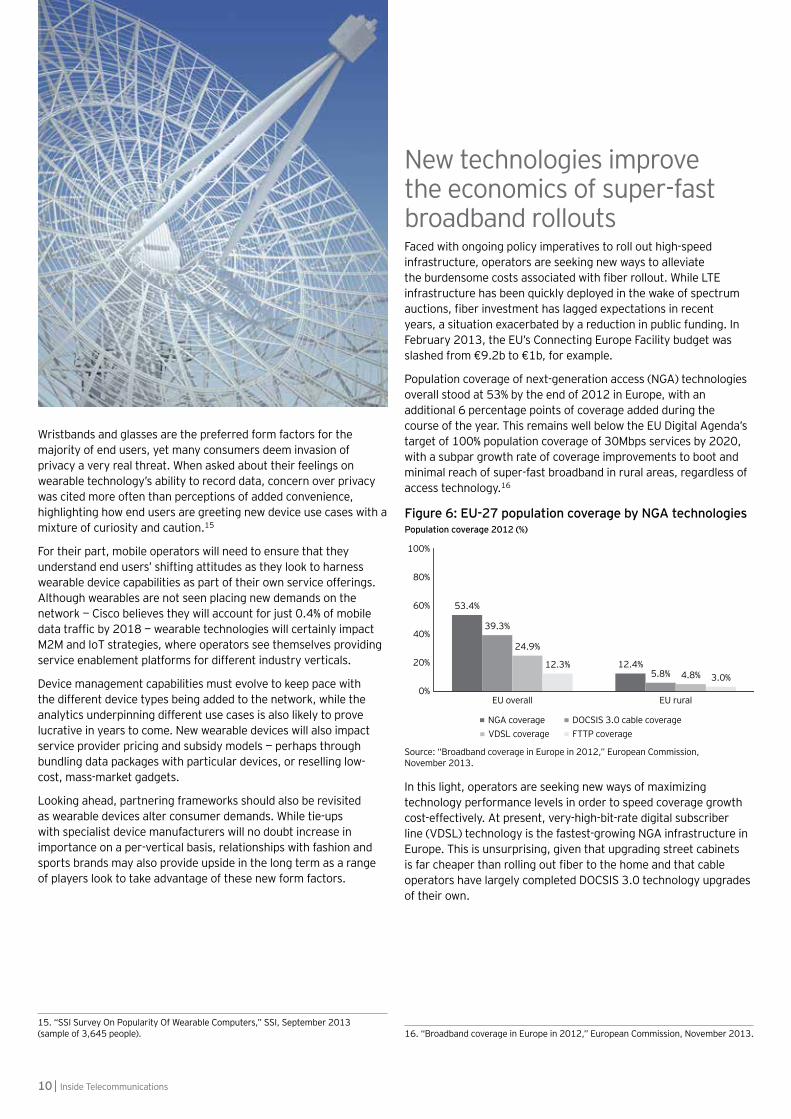

New technologies improve the economics of super-fast broadband rolloutsFaced with ongoing policy imperatives to roll out high-speed infrastructure, operators are seeking new ways to alleviate the burdensome costs associated with fiber rollout. While LTE infrastructure has been quickly deployed in the wake of spectrum auctions, fiber investment has lagged expectations in recent years, a situation exacerbated by a reduction in public funding. In February 2013, the EU’s Connecting Europe Facility budget was slashed from €9.2b to €1b, for example.

Population coverage of next-generation access (NGA) technologies overall stood at 53% by the end of 2012 in Europe, with an additional 6 percentage points of coverage added during the course of the year. This remains well below the EU Digital Agenda’s target of 100% population coverage of 30Mbps services by 2020, with a subpar growth rate of coverage improvements to boot and minimal reach of super-fast broadband in rural areas, regardless of access technology.16

In this light, operators are seeking new ways of maximizing technology performance levels in order to speed coverage growth cost-effectively. At present, very-high-bit-rate digital subscriber line (VDSL) technology is the fastest-growing NGA infrastructure in Europe. This is unsurprising, given that upgrading street cabinets is far cheaper than rolling out fiber to the home and that cable operators have largely completed DOCSIS 3.0 technology upgrades of their own.

Source: “Broadband coverage in Europe in 2012,” European Commission, November 2013.

Figure 6: EU-27 population coverage by NGA technologiesPopulation coverage 2012 (%)

0%

20%

40%

60%

80%

100%

53.4%

39.3%

24.9%

12.3%

EU overall

12.4%5.8% 4.8% 3.0%

EU rural

NGA coverageVDSL coverage

DOCSIS 3.0 cable coverageFTTP coverage

11Issue 12 |

17. “Webinar VDSL-Vectoring,” Deutsche Telekom, 2013. 18. “eircom’s Fibre Network to Offer Broadband Speeds of 100Mb,” eircom, 25 September 2013. 19. “Orange, the leader on fibre deployment, is reaffirming its ambition of offering its customers the highest speeds with the launch of VDSL2 technology,” Orange, 1 October 2013. 20. “KPN to expand VDSL vectoring coverage,” Telecompaper, 9 September 2013. 21. “Revised NBN to deliver access to fast broadband to Australians sooner and at less cost to taxpayers,” NBNCo, 12 December 2013. 22. “BT To Trial Huawei G.FAST FTTdp Copper Broadband Technology,” Tech Week Europe, 21 October 2013. 23. “The Numbers are in: Vectoring 2.0 Makes G.fast Faster,” Alcatel-Lucent, 4 July 2013.

11Issue 12 |

Crucially, a number of technologies now exist to help operators extract improved performance from VDSL technology: line bonding, vectoring and phantom mode. Of the three, vectoring signals the greatest opportunity because it doesn’t require the use of two or more phone lines per household. The cost savings compared with fiber-to-the-premises (FTTP) rollouts are substantial, with Deutsche Telekom highlighting a 70% capex reduction per home passed via vectored VDSL compared with FTTP.17

Although the first incumbent trials were announced two years ago, the technology has gained significant ground among carriers in recent months. In September, Irish incumbent Eircom confirmed it would deploy vectoring on its fiber network, estimating that by June 2015 more than 400,000 premises nationwide would receive downloads speeds of 100Mbps.18 Announcing a subsequent extension to its fiber rollout plans in November, the Irish incumbent promised that 70% of the country would receive such speeds by 2016.

In October, Orange announced it would launch VDSL2 technology as part of its network modernization program in France, offering speeds of up to 100Mbps to customers depending on location.19 The preceding month, Dutch incumbent KPN said it would expand its vectored VDSL coverage to an additional 270,000 households.20 Meanwhile, Australia’s Telstra has announced that it too is trialing the technology. This follows rollout delays affecting the country’s FTTP-based National Broadband Network, culminating in a strategic review that has proposed a new mix of lower-cost technologies, enabling two-thirds of Australians to have access to speeds of at least 100Mbps by 2019.21

Beyond vectoring, even newer technologies are emerging for the benefit of fiber deployments involving copper. Chinese vendor Huawei has pioneered the use of G.Fast technology, which enables VDSL networks to provide speeds of up to 1,000Mbps. In October, BT Group revealed plans for a technical trial of G.Fast broadband alongside another technological enhancement, fiber to the distribution point (FTTdp), which takes the fiber to a location closer to the customer’s premises.22 G.Fast technology itself can benefit from vectoring solutions in order to boost performance, as highlighted by vectoring vendor Alcatel-Lucent.23

All told, such developments herald many positives for operators, allowing them to extend the life of their copper networks. However, the improved economics of fiber rollout bring attendant challenges. The changing performance profiles offered by copper-fiber network combinations will require support from regulators, particularly since vectoring can be installed by only one DSL-based operator at

distribution boxes. In this light, G.Fast may trigger new regulatory recommendations, with the UK’s Ofcom for one recognizing the cost benefits of installing FTTdp with copper wire as opposed to FTTP.

Support from vendors is also vital — different incarnations of vectoring, such as system-level solutions that that work across different multi-service access nodes (MSAN), are now being adopted by a range of suppliers, for example. Standardization initiatives also have a vital role to play for G.Fast adoption, and encouraging steps have been made in this direction, with the International Telecommunications Union (ITU) awarding it first-stage approval in December.

Looking ahead, the prognosis for new broadband access technologies remains highly positive. While many European operators have been the first to recognize the benefits of vectoring and G.Fast, even carriers in developed Asia that have historically favored FTTP recognize their advantages. At the same time, operator interest in coaxial-cable TV wiring to provide super-fast broadband is growing, underlining how accepted infrastructure upgrade paths are evolving in new ways.

However, all players will need to carefully consider their deployment strategies — some may use new vectoring approaches to gain speed advantages over cable rivals, while others may leverage it to ease the capacity burden in overloaded parts of their network. In some instances, operators will need to ensure that their aging copper networks are robust enough to support vectoring speed gains. And while the capex advantages of G.Fast are clear enough, operators will need to conduct a thorough assessment of the opex involved in the rollout of these new technologies.

12 | Inside Telecommunications

US ruling reignites net neutrality debateNet neutrality remains a thorny issue in the telecommunications industry, with regulators historically keen to limit operators’ ability to charge content providers for data so as to safeguard an open internet. To date, US legislation has epitomized such attitudes, yet a US court decision in January to remove the basis for rules by the Federal Communications Commission (FCC) has reignited debate over the best approach to regulate internet traffic.

The FCC’s Open Internet Order of 2010 had required ISPs, both network and cable operators, to treat all web traffic equally, regardless of source. It has since been queried on a number of occasions before a challenge by Verizon Communications led a US appeals court to repeal two of the three mainstays of this legislation. The court has decided that while the FCC does have the authority to regulate broadband access, it does not have a mandate to impose anti-discrimination rules on broadband providers.

The court’s decision has raised anxiety among consumer protection groups that uncensored access to the web is under threat, with the prospect that ISPs could in time prioritize certain internet services or block some types of traffic. While operators have long argued that charging content providers is justified in view of the heavy network investments required to meet data traffic demands — particularly for bandwidth-hungry video services — over-the-top (OTT) service providers continue to stress the need for an open internet and an unfettered end-user experience.

For its part, the FCC underlined that it would seek all available options to respond to the court’s opinion, including an appeal.24 Meanwhile, a group of Democratic lawmakers introduced a bill — the Open Internet Preservation Act — in both the U.S. Senate and House of Representatives to restore the FCC’s net neutrality rules in February, highlighting the contentious political atmosphere surrounding open internet rules.

In one respect, the court’s decision hinges on a technicality, namely that the FCC has overreached its statutory powers because its net neutrality order has been based on a law that applies to “common carriers,” not broadband providers, which are instead classified as an information service. Nevertheless, the court has upheld the FCC’s argument that Section 706 of the Telecommunications Act of 1996 gives it the authority to regulate ISPs’ network management practices, paving the way for the US regulator to pursue a different path to impose rules regarding net neutrality.

3.Regulation

24. “Chairman Wheeler Statement on Court Opinion On Open Internet Rules,” Federal Communications Commission, 14 January 2014.

13Issue 12 |

25. “Netflix CEO on Net Neutrality: We Will ‘Vigorously Protest’ a ‘Draconian Scenario,’” The Wall Street Journal, 22 January 2014. 26. “ARCEP closes the administrative inquiry involving several companies, including Free and Google, on the technical and financial terms governing IP traffic routing,” ARCEP, 19 July 2013.

27. “Telecoms package reform: EC proposal must be sent back to the drawing board,” Committee of the Regions, 31 January 2014.

Although the FCC can appeal, an alternative outcome is not guaranteed, while any reclassification of broadband providers to help rescind the latest ruling would likely prove controversial in its own right. Content providers are eager to preserve the status quo and are confident that end users support the open internet argument at large: in a letter to investors, the CEO of Netflix highlighted that “ISPs are generally aware of the broad public support for net neutrality.”25

All considered, the ruling in itself hardly marks a paradigm shift in internet policy, yet it has sent shockwaves through the industry, underlining idiosyncratic national and regional approaches to the issue. In Europe, for example, net neutrality is typically not legally enshrined, except in the Netherlands, where it was introduced in 2011 to help protect OTT service delivery. The European Commission (EC) has traditionally hinged upon ensuring competition at the level of infrastructure access, whereby network operators would lack the bargaining power to charge content providers due to the presence of asset-light alternative operators.

At the same time, the EU has singled out transparency of communications from ISPs on traffic management policies as a focus area, while national regulators reserve the right to intervene if a lack of competition undermines the open internet. Such a scenario arose in France when ARCEP responded to a consumer protection agency request to investigate Free’s handling of Google’s YouTube service.26

While the recent US ruling signifies a new round of debate in North America, European policy makers are likely to maintain their “wait

and see” approach, which could itself favor commercial agreements between operators and content providers while safeguarding consumers from the blocking of services.

As part of its Connected Continent legislative package, the EC has promised to clarify its existing approach, yet this is also the scene of controversy. In January, the EU’s Committee of the Regions warned that new legislation as part of single telecoms market reform may undermine protection of end-user rights if it makes provisions for agreements between operators and content providers.27 At a national level, most regulators have typically disclosed official positions on net neutrality. A minority has introduced specific laws, yet more countries have announced plans to tackle the issue.

Source: “Net Neutrality in the EU — Country Factsheets,” Openforum Academy, September 2013.

Figure 7: EU-28 member state positions on net neutralityNumber of member states

0

10

20

30

22

47

Member states thathave disclosed anofficial position on

net neutrality

Member states thathave included net

neutrality in a law orlegislative proposal

Member states thathave announced future

measures on net neutrality

14 | Inside Telecommunications

29. “Telecom industry cracking under financial pressure,” The Hindu, 11 July 2013; “TRAI Indicator Reports,” TRAI; EY Analysis.

Other markets are experiencing their own debates over open internet legislation. Last year, Brazilian regulator Anatel passed a resolution giving it greater power to enforce net neutrality. Meanwhile, a bill introduced in 2011, called the Marco Civil da Internet (Civil Rights Framework for the Internet), has been passing through Brazil’s National Congress, underscored by an extensive public consultation process. In September of last year, the Brazilian president formally requested that this bill be treated with constitutional urgency.28

Despite an industry climate of continuing uncertainty, operators are innovating their business models in ways that enshrine new forms of relationships with content providers. In January, US-based AT&T unveiled its “Sponsored Data” service for 4G contract customers. The service allows sponsors across various industries such as health care, retail, media and entertainment, and financial services to engage with their customers and employees in new ways. Data charges are billed directly to the sponsoring company, which can then promote content such as movie trailers or games, or pay directly for employee usage of business-related apps and services.

Looking ahead, it is clear that the debate over net neutrality will continue, whether driven by operator demands to develop new business models in the face of heavy network or investment, by OTT players eager to safeguard their current business models, or by governments and regulators as part of a wider set of themes relating to internet governance and consumer rights.

India receives clarity on M&A regimeIn early December, M&A rules were announced for India’s mobile industry, paving the way for consolidation in one of the world’s most overcrowded markets, where 13 operators compete for subscribers. An empowered group of ministers (EGOM) approved a previous recommendation from the Telecom Commission, allowing two or more service providers to merge as long as their post-deal market share does not exceed 50% of the country’s subscribers.

Previously the cap had stood at 35%, barring many of the top two operators in the country’s 22 telecom service “circles” from the opportunity to merge. Following the announcement of new guidelines, long-held hopes for consolidation can be realized. The Indian mobile remains highly fragmented, with the Herfindahl-Hirschman Index (HHI) — a measure of market concentration — reflecting a congested sector where many operators are under 10% subscriber market share.

The new M&A policy — which is still awaiting final Cabinet approval — also offers an exit option to operators that are struggling to remain financially viable or have not been able to surrender underutilized spectrum or licenses. Such options may prove invaluable: in 2013, total sector debt stood at US$45.8b, greater than gross revenue of US$38.9b.29

28. “Marco Civil: Brazil’s Push to Govern the Internet,” The Huffington Post, 22 October 2013.

Figure 8: Herfindahl-Hirschman Index in selected mobile markets

Sources: BMI country telecommunications reports, 1Q14; EY analysis.

Herfindahl-Hirschman Index (HHI) based on subscriber market share

Between 0.15 and 0.25

Above 0.25

Indicates moderate concentration

Indicates high concentration

0.470.40 0.40 0.36 0.36 0.34

0.28 0.26 0.25 0.25 0.210.14

Highconcentration

Lowconcentration

Chin

a

Nor

way

Phili

ppin

es

Sing

apor

e

Sout

h A

fric

a

Mal

aysi

a

UK

Indo

nesi

a

Braz

il

Russ

ia US

Indi

a

15Issue 12 |

30. “BRIEF — India telecom spectrum bids total $9.8 bln, 900 MHZ prices unchanged since Monday,” Reuters India, 12 February 2014. 31. “Changes in Tele M&A Policy Get EGoM Nod,” The Economic Times Delhi Edition, 4 December 2013.

15Issue 12 |

The new guidelines also come as operators are participating in a new spectrum auction: by day nine of the country’s 900MHz and 1800MHz auction, bids totaling US$9.8b had been received.30 Auction rules themselves have only recently been agreed upon. In January, a ministerial panel reduced the annual spectrum fee payable by auction winners to 5% as an inducement for larger carriers to participate. Earlier, floor bid prices had also been cut, again in order to stimulate operator interest.

Adapting both M&A and spectrum auction rules will generate greater confidence in the Indian telecommunications landscape, cementing two different routes for operators to gain scale. The new M&A rules themselves directly address spectrum holdings, with any merged entity now able to hold up to two blocks of 3G and broadband wireless (BWA) spectrum.

Nevertheless, pre-existing spectrum caps remain in place, meaning a merged entity can hold no more than 25% of total airwaves assigned for access services and no more than 50% of the bandwidth assigned in a given frequency band in a particular service circle.31 This could certainly act as a brake on mergers between leading players.

Indeed, the issue of spectrum usage charges (SUCs) is likely to prove a thorny one. Under the new rules, if a company acquires new spectrum beyond 4.4MHz in the GSM band and beyond 2.5MHz in the CDMA band — via M&A — then the acquirer must pay the Government the difference between the original price and the auction-determined price for the spectrum. While this underlines the Government’s preference for spectrum acquisition to take place via auctions, it may inhibit certain M&A deals.

In this light, operators must take care to isolate the best routes to obtaining scale and accumulating the spectrum assets they require. A holistic view is essential: SUC profiles and the potential to share or trade spectrum must be considered alongside the rationale for a takeover, particularly if spectrum needs are the primary deal driver. At the same time, the highly leveraged status of many operators, coupled with expected synergy gains and integration costs, will doubtless impact the economics of future M&A in the Indian mobile sector.

16 | Inside Telecommunications

Introduction

Momentum in global mergers and acquisitions remains strong. Deal volume in the final three months of 2013 stood at 157 transactions, in line with the 155 deals registered in the third quarter and 165 in the second. Total deal value in the final quarter of the year stood at US$39.4b — although this represented a sharp sequential drop of US$173b registered in Q3 2013, the latter figure including Verizon Communications’ acquisition of Vodafone’s 45% stake in Verizon Wireless, one of the largest corporate transactions of all time.

Considering regional trends, Europe, Middle East, India and Africa (EMEIA) continues to act as a focal point for deal activity, comprising more than half of global deal value during the quarter at US$21.3 billion, although below the US$30.7b registered in the preceding quarter. Cross-border transactions are rising within this region, although consolidation scenarios remain a key talking point in markets as diverse and Germany and India. Elsewhere, deal volume was down quarter-on-quarter in both the Americas and Asia-Pacific.

4.Mergers and Acquisitions

Latin America in the spotlightThe largest deal of the quarter saw Portugal Telecom announce in October that it would merge with its Brazilian affiliate Oi. This move bolsters Oi’s ability to combat heightening competition in Brazil — particularly in the mobile segment — as well as reduce debt, improve operational efficiency and forge more favorable contracts with equipment vendors. Portugal Telecom is no stranger to the Brazilian market, formerly owning a 50% stake in Oi’s competitor Telefonica Vivo before exiting and acquiring a minority stake in Oi the following year.

Figure 9: Telecoms M&A deal value by target area, Q3–Q4 2013

Source: ThomsonOne, Capital IQ, Mergermarket.

4Q13 3Q13

US$-US$206

US$1,124US$4,354

US$141,518US$13,504

US$30,743US$21,317

Japan*

Asia-Pacific

Americas

EMEIA

17Issue 12 |

Brazil’s competition watchdog Cade approved the deal in January, paving the for the way for the two companies to create a new company with more than 100 million subscribers and almost US$19 billion in annual revenue.32 For Portugal Telecom, the merger will help offset tough conditions in its home market in the wake of macroeconomic pressures. Meanwhile, the combination of Portugal Telecom’s pay-TV expertise with Oi’s growing fiber network footprint will help strengthen the Brazilian player’s residential bundle proposition.

Elsewhere in the region, France-based Orange has agreed to sell its Dominican Republican unit to Luxembourg-based investment company Altice for US$1.44 billion. The deal marks the latest step in Orange’s efforts to optimize its assets portfolio, a strategy announced in 2011.33 In addition, Altice acquired an 88% stake in Tricom, a cable company that offers both fixed and mobile services in the Dominican Republic, which it intends to combine with Orange’s mobile business.

The combined company, targeting upside in the quadruple-play market, will boast some 4 million subscribers. Local press reports suggest that merged entity will adopt the Orange Dominicana brand name, with the new owner planning to invest US$390 million over three years in order to extend 4G mobile and fiber-optic coverage in the country.34 The transactions strengthen Altice’s presence in the

Caribbean, where it already offers pay-TV, high-speed broadband and mobile services in Martinique, Guadeloupe and French Guiana.

Private equity activity on the riseAltice is one of a number of private equity firms increasing its exposure to the telecommunications sector. Beyond its acquisition of mobile and cable assets in the Dominican Republic, Altice has also increased its stake in Numericable, the French cable operator. Via its 100%-owned European subsidiary, Altice VII, it has paid US$467m to increase its holding from 30% to 40%, giving it voting control in the board of directors.35

Other private equity players have also been active. In November, Czech investment company PPF Group announced an agreement to buy out Telefonica’s majority stake in its Czech unit for US$3.3 billion, also acquiring the Spanish carrier’s operations in Slovakia. Although the holding companies in both countries will change their names, the unit will continue to operate under the O2 brand for the next four years. European antitrust authorities approved the deal in January, and the Spanish incumbent will retain a 4.9% stake in its Czech business following the transaction. The divestment forms part of Telefonica’s drive to reduce debts and narrow its geographical focus.

32. “UPDATE 1 — Brazil competition watchdog approves Oi, Portugal Telecom merger,” Reuters, 14 January 2014. 33. “Orange reached an agreement with Altice for the disposal of Orange Dominicana,” Orange, 27 November 2013. 34. “Altice to merge Tricom and Orange Dominicana following dual takeover,” Telegeography, 17 December 2013.

35. “Altice increases Numericable position and forms new consolidated Altice Group,” Altice, 18 November 2013.

18 | Inside Telecommunications

36. “Deutsche Telekom acquires GTS Central Europe,” Deutsche Telekom, 11 November 2013.

37. “Boku Acquires Qubecell, India’s Leader in Direct Carrier Billing,” Boku, 21 November 2013.

Meanwhile, Kohlberg Kravis Roberts, a US-based private equity firm, acquired United Group from UK-based investment firm Mid Europa Partners in October 2013. Luxembourg-based United Group offers a range of telecoms and media services through subsidiaries including Serbia Broadband, Telemach Slovenia and Telemach Bosnia — all cable operators in the Balkans — as well as Total TV, a satellite TV platform in Southeastern Europe. Broadband and pay-TV penetration remain low in the region compared with other European markets, and the transaction marks KKR’s first direct investment in these territories.

While private equity players are now eager to invest in telecommunication assets to take advantage of consolidation opportunities, many have been active in fixed-line and cable segments for a number of years. In November 2013, Deutsche Telekom announced the acquisition of GTS, a central European infrastructure business, from a group of private equity firms in a transaction valued at €546m. GTS serves 38,000 customers via its fiber-optic network and has 14 data centers across Eastern Europe.

The acquisition is seen underpinning the German incumbent’s efforts to provide cross-border services in the region, with fiber-optic capability benefiting Deutsche Telekom’s mobile-centric subsidiaries in the Czech Republic and Poland in particular. The deal also helps the German player strengthen its customer relationships in the enterprise segment, another key tenet of its stated strategy.36

Stake increases in IndiaBefore new guidelines were announced in the M&A sector, a number of transactions took place in India during the final three months of 2013. A number of players have taken advantage of sector liberalization whereby foreign entities are allowed up to 100% ownership of local companies.

In October, Vodafone filed for regulatory approval to fully acquire its Indian subsidiary in a deal worth US$1.7b, upping its stake from 64%. Elsewhere, Norwegian incumbent Telenor bought a 25% stake in Telewings, taking its holding in the company that operates the Uninor brand to 74%.

Other notable transactions in India during the quarter included Boku’s acquisition of Qubecell in November. US-based Boku is a global leader in carrier billing and cross-platform mobile payments, and the acquisition of the leading Indian provider of such services gives it relationships with four of India’s largest mobile carriers, enabling the US player to reach more than 75% of the country’s mobile users.37 Deal terms were undisclosed.

Figure 10: Top telecoms M&A by deal value, Q4 2013

Source: ThomsonOne, Capital IQ, Mergermarket.

$1,356

$1,400

$1,530

$1,653

$2,000

$2,021

$2,425

$3,317

$4,850

$4,876

Kohlberg Kravis Roberts/United Group

Altice VII Sarl/Orange Dominicana

SoftBank/Supercell

Vodafone/Vodafone India

Frontier Communications/AT&T wireline assets

Hellman & Friedman/Scout24 Holding

HKT Group/CSL New World Mobility

PPF Group/Telefónica Czech Republic

Crown Castle/AT&T tower assets

Oi/Portugal Telecom

Buyer/Seller Deal value ($USm)

19Issue 12 |

38. “Stringent conditions eyed for HKT takeover of CSL New World,” South China Morning Post, 13 February 2014.

19Issue 12 |

Consolidation comes to Hong KongThe single largest deal in Asia-Pacific during the last three months of 2013 arrived in the form of HKT’s acquisition of Hong Kong-based mobile operator CSL from Australia’s Telstra for US$2.4b. HKT, the fixed-line unit of PCCW, has bought CSL, which it had originally sold in 2000 to Telstra, as it seeks greater scale in Hong Kong’s telecommunications sector.

Previously the smallest mobile operator by subscribers, PCCW is set to become the market leader, matching its fixed-line market position, while Telstra’s exit comes as it refocuses its regional strategy on the enterprise market. In January, Telstra completed the acquisition of O2 Networks, an Australia-based provider of security consulting and integration services for corporations, while in August last year it announced the takeover of NSC Group., a unified communications and contact center specialist with clients in Australia, New Zealand and Asia-Pacific.

Nevertheless, regulatory scrutiny has accompanied HKT’s proposed takeover of CSL. PCCW’s unit may face restrictions, including the surrender of 4G spectrum, following the merger. While HKT has already offered to return an additional block of 3G spectrum as part of the Government’s existing spectrum reassignment plan, it would still hold 38% of Hong Kong’s available mobile spectrum following the deal.38

Japanese telcos look overseas for growthJapan’s carriers continue to demonstrate considerable appetite for foreign expansion, with all three of the country’s leading players striking deals in the last three months of 2013. NTT Communications, the ICT arm of NTT, undertook two acquisitions, taking full control of Virtela Technology Services, a US-based IT infrastructure and security management services provider, as well as an 80% stake in RagingWire, a US enterprise data center service provider.

Both transactions conform to NTT’s stated strategy to expand its international footprint in enterprise services. The merger with Virtela will expand NTT’s global presence from 160 markets to more than 190, while the investment in RagingWire will more than double NTT’s existing data center presence in the US. Meanwhile, the Japanese incumbent’s mobile arm has also been active, with NTT DoCoMo acquiring a majority stake in local cooking school operator ABC Holdings in order to ramp up its smartphone content offering.

Elsewhere, SoftBank is increasing its focus on opportunities in adjacent retail and technology segments. Deals during the quarter include the acquisition of a 57% stake in handset distributor Brightstar Corp. for US$1.26b, a move designed to boost its bargaining power with device manufacturers as a route toward cost reduction. SoftBank was also involved in one of the quarter’s largest deals globally, acquiring Finnish mobile games maker Supercell Oy for US$1.53b in October as it bids to widen its mobile internet service capabilities.

For Japan’s number two operator, KDDI, attention has turned to refocusing its business in its home market. In December, it acquired an additional 27% stake in LAC Co., a listed network security service provider, helping the carrier to strengthen its security operation center business. Furthermore, KDDI divested its wholly owned cable TV business, Japan Cablenet, to Jupiter Telecom, in which the operator holds a 50% stake.

20 | Inside Telecommunications

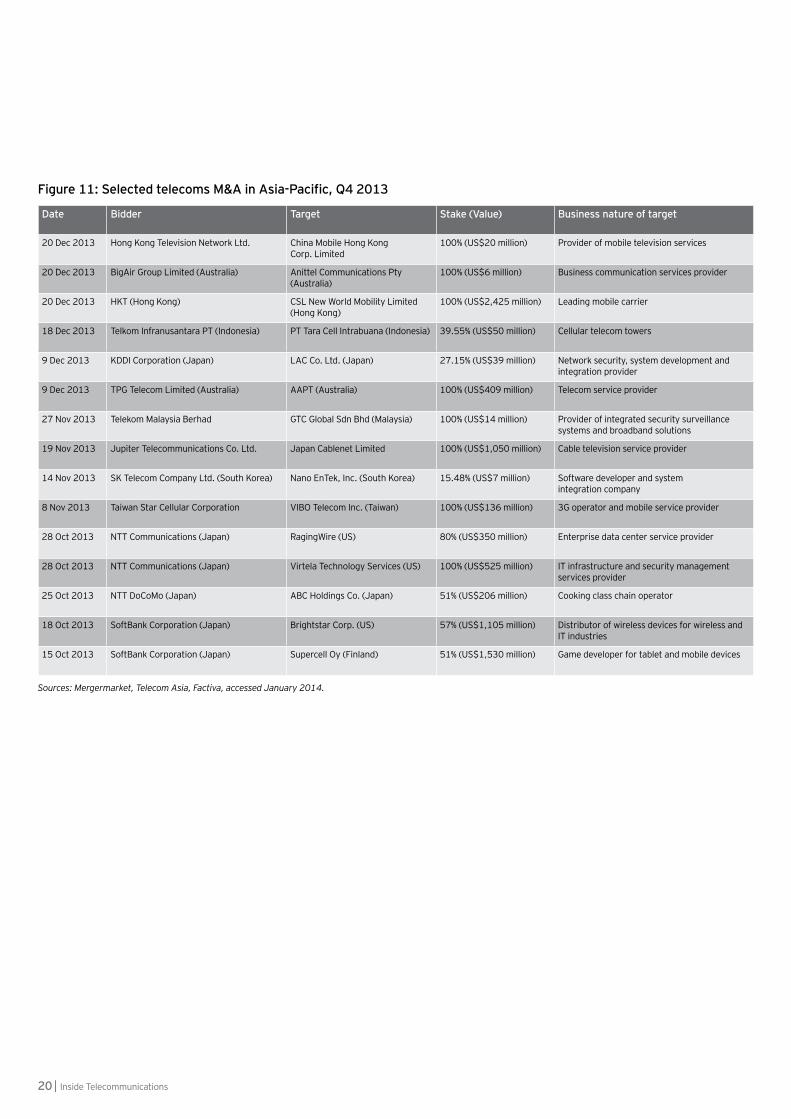

Figure 11: Selected telecoms M&A in Asia-Pacific, Q4 2013

Date Bidder Target Stake (Value) Business nature of target

20 Dec 2013 Hong Kong Television Network Ltd. China Mobile Hong Kong Corp. Limited

100% (US$20 million) Provider of mobile television services

20 Dec 2013 BigAir Group Limited (Australia) Anittel Communications Pty (Australia)

100% (US$6 million) Business communication services provider

20 Dec 2013 HKT (Hong Kong) CSL New World Mobility Limited (Hong Kong)

100% (US$2,425 million) Leading mobile carrier

18 Dec 2013 Telkom Infranusantara PT (Indonesia) PT Tara Cell Intrabuana (Indonesia) 39.55% (US$50 million) Cellular telecom towers

9 Dec 2013 KDDI Corporation (Japan) LAC Co. Ltd. (Japan) 27.15% (US$39 million) Network security, system development and integration provider

9 Dec 2013 TPG Telecom Limited (Australia) AAPT (Australia) 100% (US$409 million) Telecom service provider

27 Nov 2013 Telekom Malaysia Berhad GTC Global Sdn Bhd (Malaysia) 100% (US$14 million) Provider of integrated security surveillance systems and broadband solutions

19 Nov 2013 Jupiter Telecommunications Co. Ltd. Japan Cablenet Limited 100% (US$1,050 million) Cable television service provider

14 Nov 2013 SK Telecom Company Ltd. (South Korea) Nano EnTek, Inc. (South Korea) 15.48% (US$7 million) Software developer and system integration company

8 Nov 2013 Taiwan Star Cellular Corporation VIBO Telecom Inc. (Taiwan) 100% (US$136 million) 3G operator and mobile service provider

28 Oct 2013 NTT Communications (Japan) RagingWire (US) 80% (US$350 million) Enterprise data center service provider

28 Oct 2013 NTT Communications (Japan) Virtela Technology Services (US) 100% (US$525 million) IT infrastructure and security management services provider

25 Oct 2013 NTT DoCoMo (Japan) ABC Holdings Co. (Japan) 51% (US$206 million) Cooking class chain operator

18 Oct 2013 SoftBank Corporation (Japan) Brightstar Corp. (US) 57% (US$1,105 million) Distributor of wireless devices for wireless and IT industries

15 Oct 2013 SoftBank Corporation (Japan) Supercell Oy (Finland) 51% (US$1,530 million) Game developer for tablet and mobile devices

Sources: Mergermarket, Telecom Asia, Factiva, accessed January 2014.

21Issue 12 |

22 | Inside Telecommunications

23Issue 12 |

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com

How EY’s Global Telecommunications Center can help your businessTelecommunications operators are facing a rapidly transforming business model. Competition from technology companies is creating challenges around customer ownership; and service innovation, and pricing pressures and network capacity are intensifying scrutiny on return on investment. Additionally, regulatory pressures and shareholder expectations require agility and cost efficiency. If you are facing these challenges, we can provide a sector-based perspective to addressing your assurance, advisory, transaction and tax needs. Our Global Telecommunications Center is a virtual hub that brings together people, cultures and leading ideas from across the world. Whatever your need, we can help you improve the performance of your business.

© 2014 EYGM Limited. All Rights Reserved.

EYG no. EF0137CSG/GSC2014/1298029ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/telecommunications

@EY_Telecoms

Jonathan Dharmapalan Global Telecommunications [email protected]

Holger Forst Global Telecommunications Assurance Leader [email protected]

Staffan Ekström Global Telecommunications TAS [email protected]

Amit Sachdeva Global Telecommunications Advisory [email protected]

Bart van Droogenbroek Global Telecommunications Tax Leader [email protected]

Contacts