Embed Size (px)

Citation preview

c o m e . c o n n e c t . c r e a t e

STS 543Effectiveness of policies to address household indebtedness:

Evidence from credit registry data in Malaysia

Muizz Aziz

Bank Negara Malaysia

19th August 2019, 2.00 pm – 3.40 pm

Insert your logo here

2

Outline

1

2

3

4

Malaysia’s experience with macroprudential policy

Micro data for macro-financial insights

Conclusion and policy implications

Results

3

Outline

1

2

3

4

Malaysia’s experience with macroprudential policy

Micro data for macro-financial insights

Conclusion and policy implications

Results

• Where we were, what we did, and what followed

4

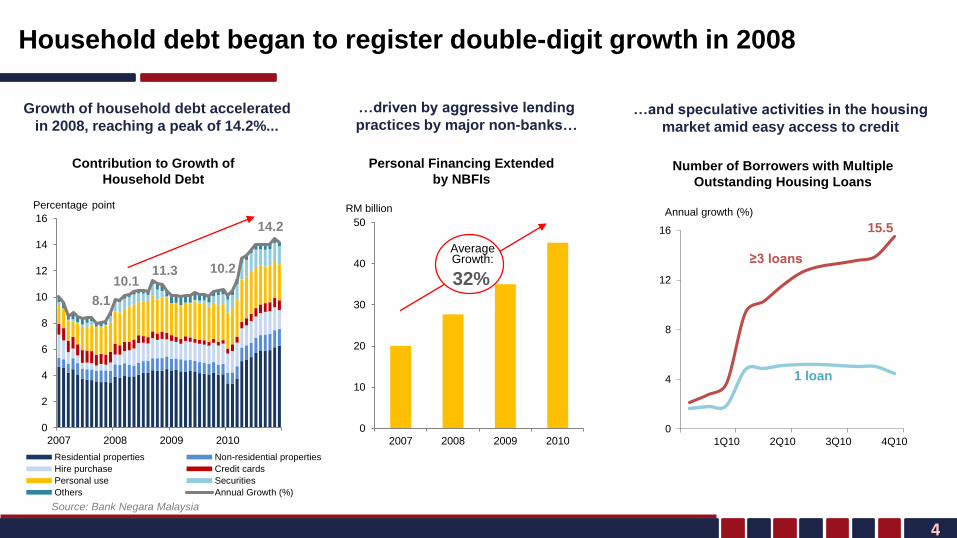

Growth of household debt accelerated

in 2008, reaching a peak of 14.2%...

Contribution to Growth of

Household Debt

8.1

10.111.3 10.2

14.2

0

2

4

6

8

10

12

14

16

2007 2008 2009 2010

Percentage point

…driven by aggressive lending

practices by major non-banks…

0

10

20

30

40

50

2007 2008 2009 2010

Personal Financing Extended

by NBFIs

RM billion

32

%32%

Average Growth:

…and speculative activities in the housing

market amid easy access to credit

Number of Borrowers with Multiple

Outstanding Housing Loans

15.5

0

4

8

12

16

1Q10 2Q10 3Q10 4Q10

≥3 loans

1 loan

Annual growth (%)

Household debt began to register double-digit growth in 2008

8.1 10.1 11.3 10.2 14.20246810121416

2007 2008 2009 2010

Residential properties Non-residential properties

Hire purchase Credit cards

Personal use Securities

Others Annual Growth (%)

Source: Bank Negara Malaysia

5

7.98.0

0

2

4

6

8

10

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

Overall national house price growth outpaced 10-year average,

with signs of increasing risks to financial stability

Annual Growth (%)

Overall national house price recorded an accelerated pace

of growth…

Malaysian House Price Index (MHPI)

Source: National Property Information Centre (NAPIC)

10-year average: 3.4%

…with increasing vulnerabilities among borrowers with

multiple residential property loans

Delinquencies of Borrowers With Multiple Housing Loans

Source: Bank Negara Malaysia

Annual Growth (%)

Annual Growth (%)

Disbursement vs. Repayment for Residential Property Loans

-10

0

10

20

30

2007 2008 2009 2010

Disbursement

Repayment

-40

-20

0

20

2007 2008 2009 2010

2 Loans 3 Loans 4 Loans 5 Housing Loans

6

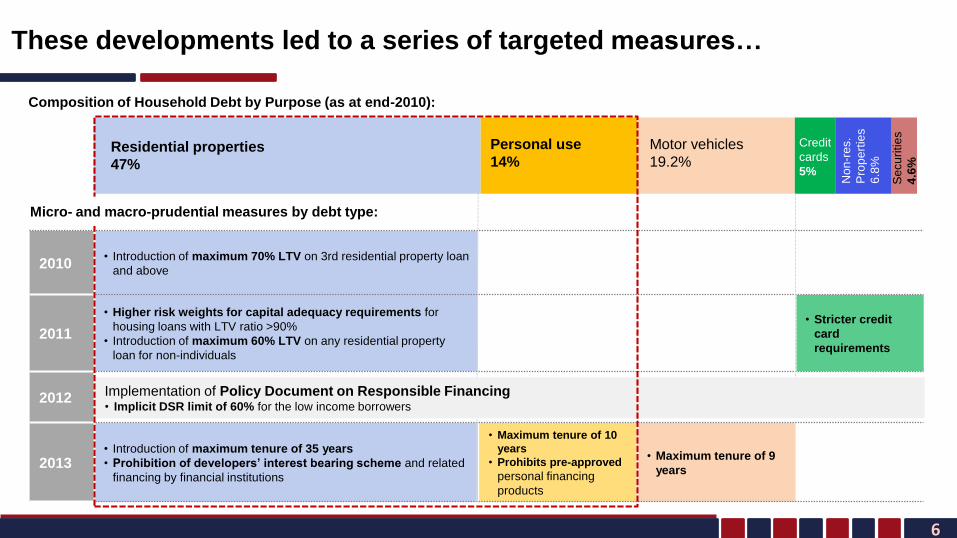

These developments led to a series of targeted measures…

Composition of Household Debt by Purpose (as at end-2010):

2010• Introduction of maximum 70% LTV on 3rd residential property loan

and above

2011

• Higher risk weights for capital adequacy requirements for

housing loans with LTV ratio >90%

• Introduction of maximum 60% LTV on any residential property

loan for non-individuals

• Stricter credit

card

requirements

2012

2013• Introduction of maximum tenure of 35 years

• Prohibition of developers’ interest bearing scheme and related

financing by financial institutions

• Maximum tenure of 10

years

• Prohibits pre-approved

personal financing

products

• Maximum tenure of 9

years

Residential properties

47%

Motor vehicles

19.2%

Personal use

14%

No

n-r

es.

Pro

pe

rtie

s

6.8

%

Credit

cards

5%

Se

cu

ritie

s

4.6

%

Implementation of Policy Document on Responsible Financing • Implicit DSR limit of 60% for the low income borrowers

Micro- and macro-prudential measures by debt type:

7

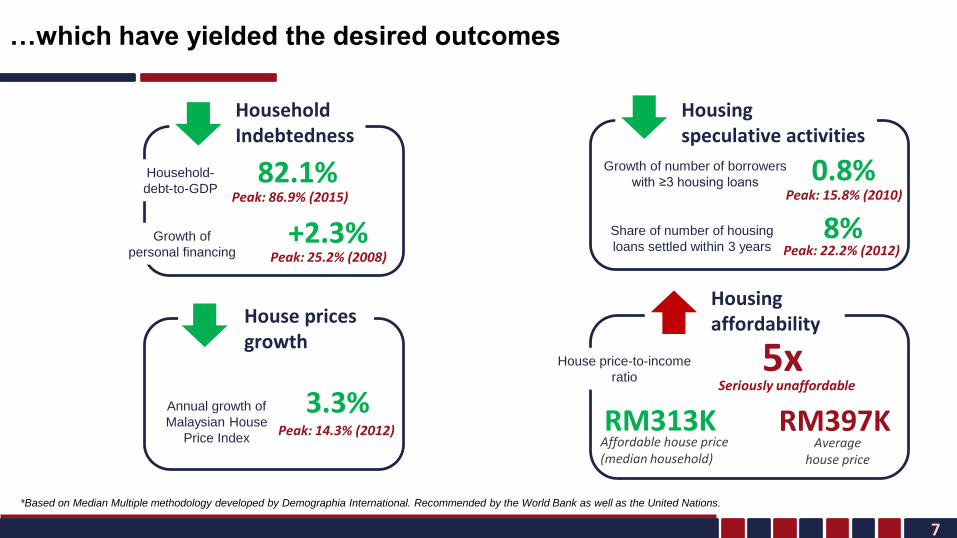

…which have yielded the desired outcomes

Household Indebtedness

Household-

debt-to-GDP82.1%

Peak: 86.9% (2015)

Growth of

personal financing+2.3%

Peak: 25.2% (2008)

Housing speculative activities

Growth of number of borrowers

with ≥3 housing loans 0.8%Peak: 15.8% (2010)

Share of number of housing

loans settled within 3 years8%

Peak: 22.2% (2012)

House pricesgrowth

Annual growth of

Malaysian House

Price Index

3.3%Peak: 14.3% (2012)

*Based on Median Multiple methodology developed by Demographia International. Recommended by the World Bank as well as the United Nations.

vs

Housing affordability

House price-to-income

ratio5x

Seriously unaffordable

RM313KAffordable house price (median household)

RM397KAverage

house price

8

Outline

1

2

3

4

Malaysia’s experience with macroprudential policy

Micro data for macro-financial insights

Conclusion and policy implications

Results

• Research questions, data and empirical strategy

9Copyright ISIWSC2019

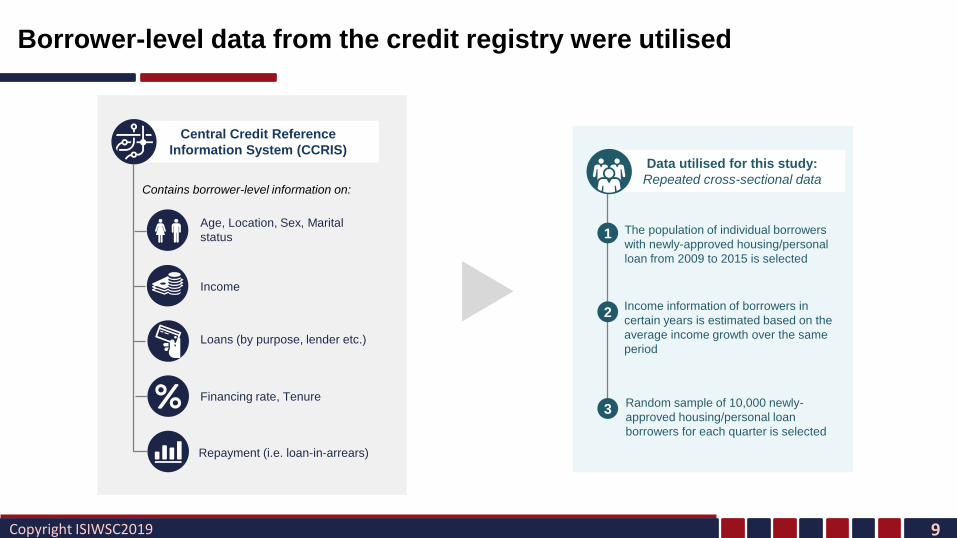

Borrower-level data from the credit registry were utilised

Central Credit Reference

Information System (CCRIS)

Contains borrower-level information on:

Age, Location, Sex, Marital

status

Income

Loans (by purpose, lender etc.)

Financing rate, Tenure

Repayment (i.e. loan-in-arrears)

Data utilised for this study:

Repeated cross-sectional data

The population of individual borrowers

with newly-approved housing/personal

loan from 2009 to 2015 is selected

Income information of borrowers in

certain years is estimated based on the

average income growth over the same

period

Random sample of 10,000 newly-

approved housing/personal loan

borrowers for each quarter is selected

2

3

1

10

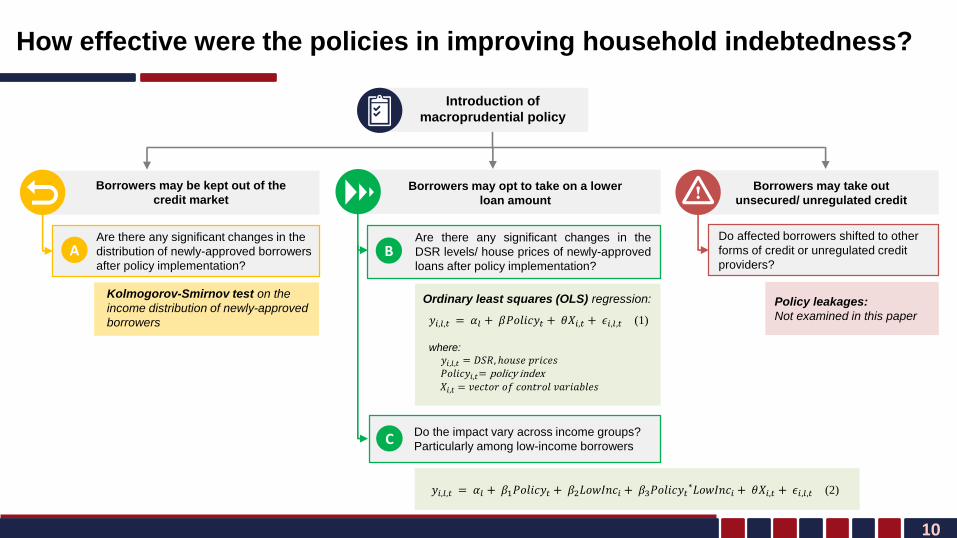

How effective were the policies in improving household indebtedness?

Introduction of

macroprudential policy

Borrowers may be kept out of the

credit marketBorrowers may opt to take on a lower

loan amount

Borrowers may take out

unsecured/ unregulated credit

Are there any significant changes in the

distribution of newly-approved borrowers

after policy implementation?

Are there any significant changes in the

DSR levels/ house prices of newly-approved

loans after policy implementation?

Do the impact vary across income groups?

Particularly among low-income borrowers

Do affected borrowers shifted to other

forms of credit or unregulated credit

providers?

Kolmogorov-Smirnov test on the

income distribution of newly-approved

borrowers

Ordinary least squares (OLS) regression:

𝑦𝑖,𝑙,𝑡 = 𝛼𝑙 + 𝛽𝑃𝑜𝑙𝑖𝑐𝑦𝑡 + 𝜃𝑋𝑖,𝑡 + 𝜖𝑖,𝑙,𝑡 (1)

𝑦𝑖,𝑙,𝑡 = 𝛼𝑙 + 𝛽1𝑃𝑜𝑙𝑖𝑐𝑦𝑡 + 𝛽2𝐿𝑜𝑤𝐼𝑛𝑐𝑖 + 𝛽3𝑃𝑜𝑙𝑖𝑐𝑦𝑡∗𝐿𝑜𝑤𝐼𝑛𝑐𝑖 + 𝜃𝑋𝑖,𝑡 + 𝜖𝑖,𝑙,𝑡 (2)

where:

𝑦𝑖,𝑙,𝑡 = 𝐷𝑆𝑅, ℎ𝑜𝑢𝑠𝑒 𝑝𝑟𝑖𝑐𝑒𝑠𝑃𝑜𝑙𝑖𝑐𝑦𝑖,𝑡= policy index𝑋𝑖,𝑡 = 𝑣𝑒𝑐𝑡𝑜𝑟 𝑜𝑓 𝑐𝑜𝑛𝑡𝑟𝑜𝑙 𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒𝑠

Policy leakages:

Not examined in this paper

A B

C

11

Outline

1

2

3

4

Malaysia’s experience with macroprudential policy

Micro data for macro-financial insights

Conclusion and policy implications

Results

• Key findings

12

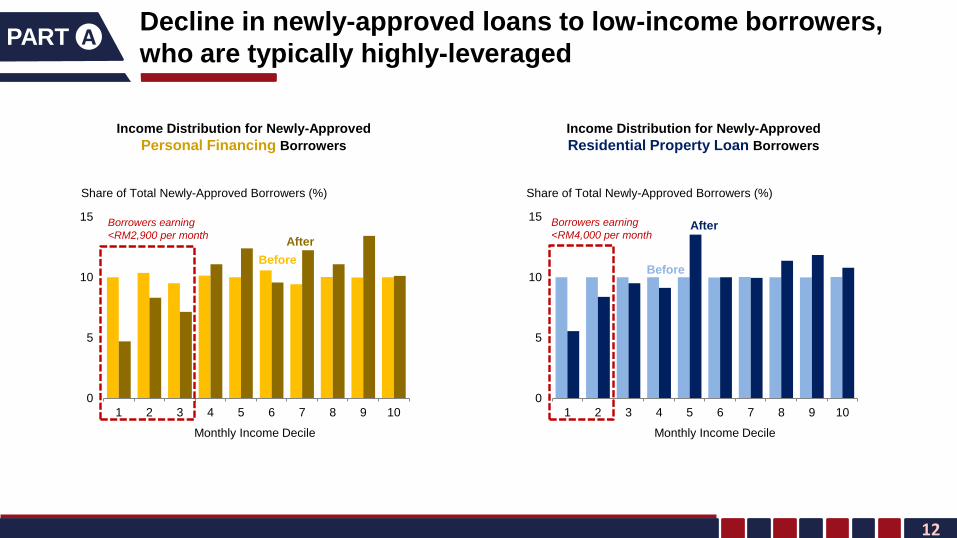

Decline in newly-approved loans to low-income borrowers,

who are typically highly-leveragedAPART

Income Distribution for Newly-Approved

Personal Financing Borrowers

0

5

10

15

1 2 3 4 5 6 7 8 9 10

Share of Total Newly-Approved Borrowers (%)

Monthly Income Decile

Income Distribution for Newly-Approved

Residential Property Loan Borrowers

0

5

10

15

1 2 3 4 5 6 7 8 9 10

Share of Total Newly-Approved Borrowers (%)

Monthly Income Decile

Borrowers earning

<RM2,900 per month

Borrowers earning

<RM4,000 per month

Before

After

Before

After

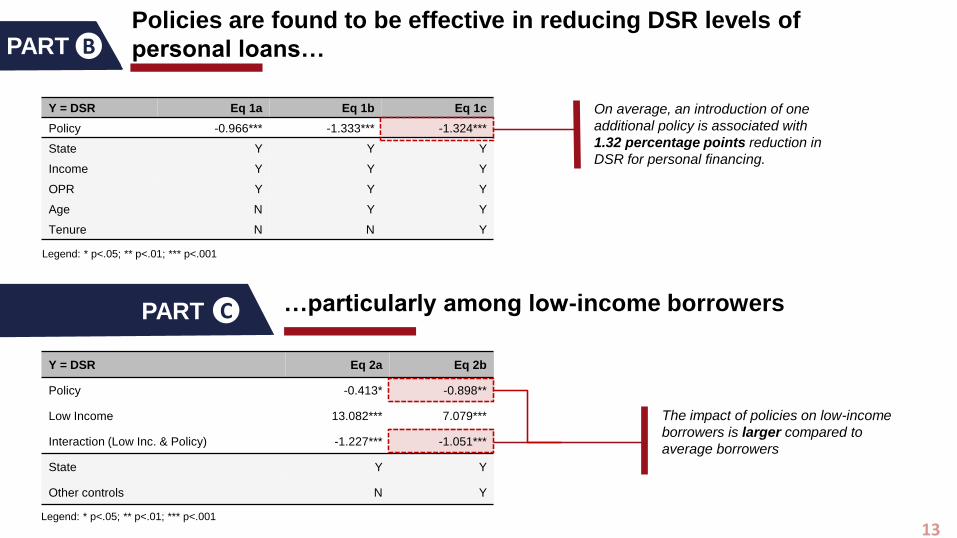

Policies are found to be effective in reducing DSR levels of

personal loans…BPART

PART C …particularly among low-income borrowers

Y = DSR Eq 1a Eq 1b Eq 1c

Policy -0.966*** -1.333*** -1.324***

State Y Y Y

Income Y Y Y

OPR Y Y Y

Age N Y Y

Tenure N N Y

On average, an introduction of one

additional policy is associated with

1.32 percentage points reduction in

DSR for personal financing.

Legend: * p<.05; ** p<.01; *** p<.001

Y = DSR Eq 2a Eq 2b

Policy -0.413* -0.898**

Low Income 13.082*** 7.079***

Interaction (Low Inc. & Policy) -1.227*** -1.051***

State Y Y

Other controls N Y

Legend: * p<.05; ** p<.01; *** p<.001

The impact of policies on low-income

borrowers is larger compared to

average borrowers

13

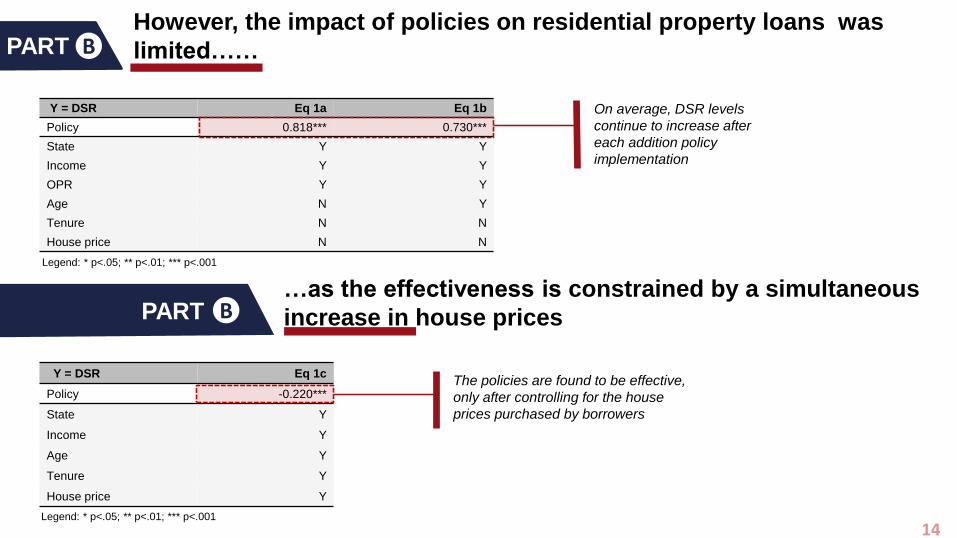

Y = DSR Eq 1c

Policy -0.220***

State Y

Income Y

Age Y

Tenure Y

House price Y

Y = DSR Eq 1a Eq 1b

Policy 0.818*** 0.730***

State Y Y

Income Y Y

OPR Y Y

Age N Y

Tenure N N

House price N N

However, the impact of policies on residential property loans was

limited……BPART

PART B…as the effectiveness is constrained by a simultaneous

increase in house prices

On average, DSR levels

continue to increase after

each addition policy

implementation

Legend: * p<.05; ** p<.01; *** p<.001

Legend: * p<.05; ** p<.01; *** p<.001

The policies are found to be effective,

only after controlling for the house

prices purchased by borrowers

14

15

Outline

1

2

3

4

Malaysia’s experience with macroprudential policy

Micro data for macro-financial insights

Conclusion and future research

Results

• Summary and what’s next?

16

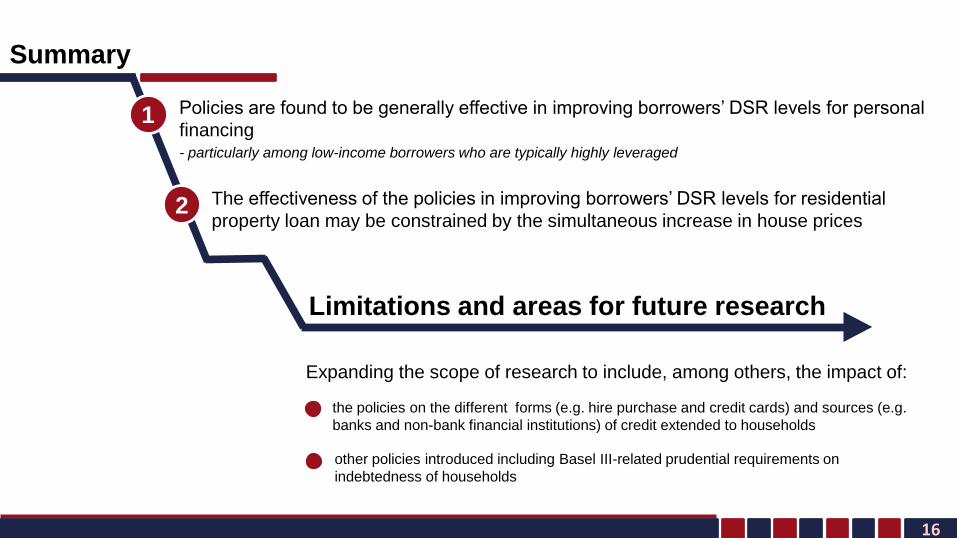

Summary

1

2

Limitations and areas for future research

Policies are found to be generally effective in improving borrowers’ DSR levels for personal

financing- particularly among low-income borrowers who are typically highly leveraged

The effectiveness of the policies in improving borrowers’ DSR levels for residential

property loan may be constrained by the simultaneous increase in house prices

Expanding the scope of research to include, among others, the impact of:

the policies on the different forms (e.g. hire purchase and credit cards) and sources (e.g.

banks and non-bank financial institutions) of credit extended to households

other policies introduced including Basel III-related prudential requirements on

indebtedness of households

c o m e . c o n n e c t . c r e a t e

THANK YOU