Embed Size (px)

Citation preview

Investor presentation Autumn 2015

Cautionary statement

This Review is intended to focus on matters which are relevant to the interests of shareholders in the

Company. The purpose of the Review is to assist shareholders in assessing the strategies adopted and

performance delivered by the Company and the potential for those strategies to succeed. It should not

be relied upon by any other party or for any other purpose.

Forward looking statements are made in good faith, based on a number of assumptions concerning

future events and information available to Directors at the time of their approval of this report. These

forward looking statements should be treated with caution due to the inherent uncertainties underlying

any such forward looking information. The user of these accounts should not rely unduly on these

forward looking statements, which are not a guarantee of performance and which are subject to a

number of uncertainties and other facts, many of which are outside of the Company’s control and could

cause actual events to differ materially from those in these statements. No guarantee can be given of

future results, levels of activity, performance or achievements.

2

Unless otherwise stated, all profit, margin and EPS data refer to normalised results, which can be found on the face of the Group Income

Statement in the first column. The definition of normalised profit is as follows: IFRS result excluding charges for intangible asset amortisation,

exceptional items (nil in 2015), loss on disposal of a business and tax relief thereon. The Board believes that the normalised result gives a better

indication of the underlying performance of the Group.

Contents

o Group strategy, investment case and business model

o Our markets

o Strategic focus and areas for growth

o Divisional highlights – Half Year 2015

o Financial results – Half Year 2015

o Appendix

3

Group strategy

Investment case

Business model

4

5

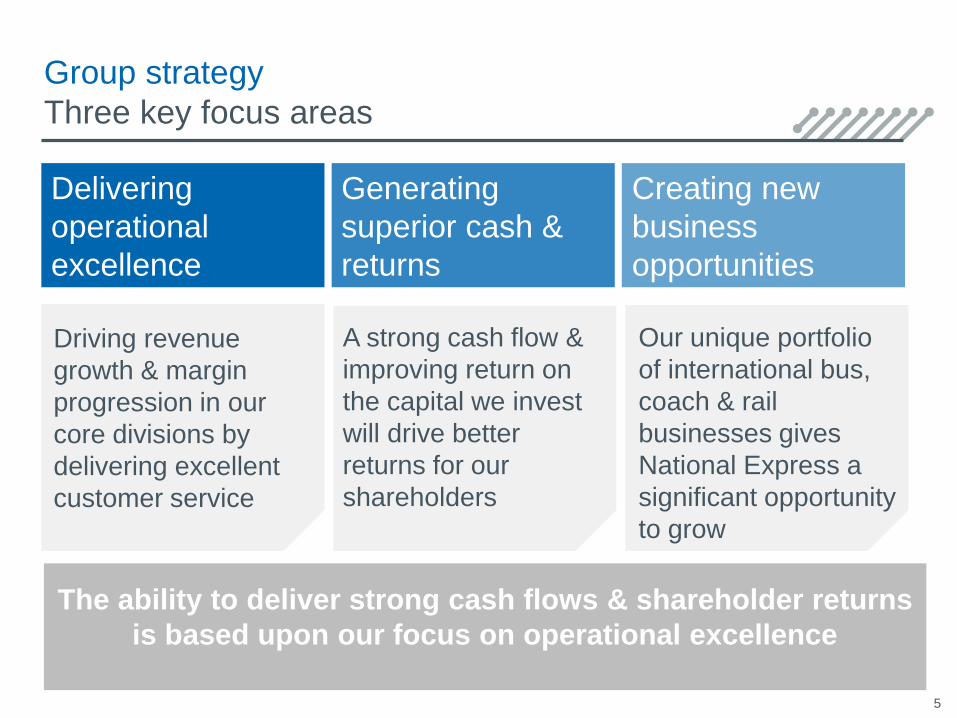

Group strategy

Three key focus areas

Delivering

operational

excellence

Generating

superior cash &

returns

Creating new

business

opportunities

Driving revenue

growth & margin

progression in our

core divisions by

delivering excellent

customer service

A strong cash flow &

improving return on

the capital we invest

will drive better

returns for our

shareholders

Our unique portfolio

of international bus,

coach & rail

businesses gives

National Express a

significant opportunity

to grow

The ability to deliver strong cash flows & shareholder returns

is based upon our focus on operational excellence

Investment case

Our diversity is our strength

6

o Best in class public transport operator with differentiated proposition to

deliver sustainable, long-term shareholder value:

o Well balanced and diversified portfolio

o Strong recurring revenue streams from perpetuity businesses and

established contract markets

o Strong free cash flow helping to drive organic growth and position us for

growth in new markets:

o Fast developing pipeline of substantial capital-light growth opportunities;

successful conversion of pipeline in German rail and the Middle East

o Bolt-on acquisition opportunities in North America

o Stable, long-term financing and commitment to investment grade rating

o Dividend policy: 2x Group earnings including long-term rail earnings

Business model

Using operational expertise & experience…

7

o Constantly improving service

standards to drive growth in

passenger volumes & revenues

o Driving cost efficiencies across the

Group to protect & grow margins

o Ensuring customers & employees

are safe

o Focus on operational excellence

helps to drive strong cash flows &

shareholder returns

…to provide best in class transport services

Providing safe, punctual & frequent services

at affordable prices

26%

33%

34%

8%Bus

School Bus

Coach

Rail

Business model

Differentiating through diversification

(1) Data: 2014 excluding central costs and German coach

Diversified revenue stream (1)

Diversified modal breadth (1)

8

o Diversified portfolio with leading positions in

many of our markets

o Lower geographical and regulatory exposure

to any one market

o Deep understanding of & expertise in

managing regulated concessions

o Ability to apply our experience & expertise to

build revenue & profit streams in new markets

o Morocco experience entry into

Middle East

o Successful UK rail franchise entry

into German rail

o Rail – revenue & profit stream now secured

through to 2029 in UK & to 2033 in Germany

National Express

Group Revenue £1.89bn

Balanced portfolio with attractive geographic & modal exposure

29%

33%15%

15%

8%Spain

N America

UK Bus

UK Coach

Rail

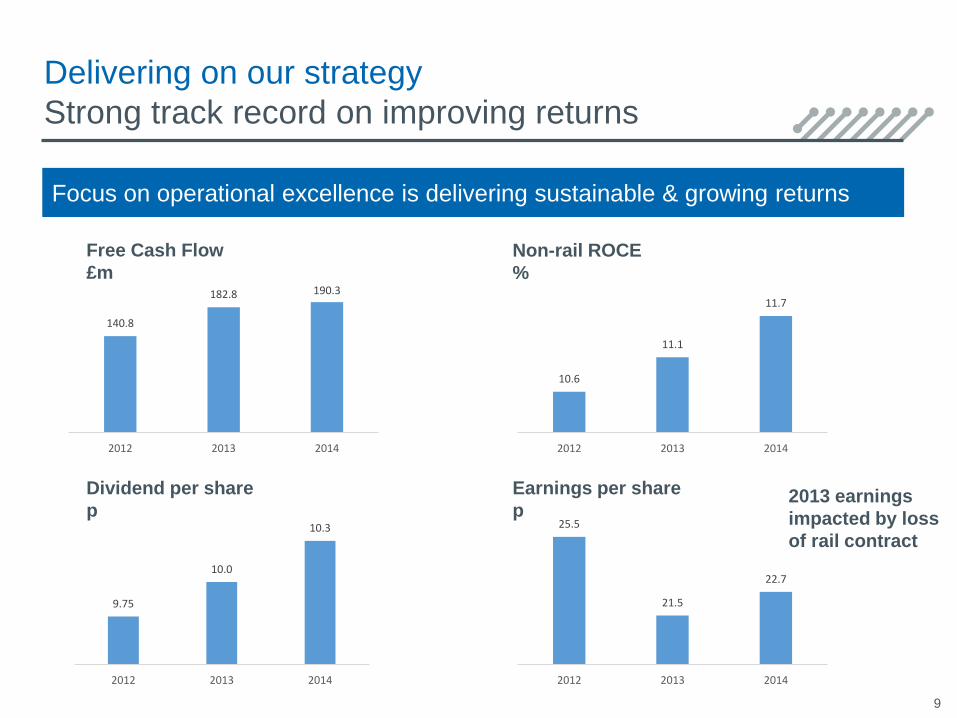

Delivering on our strategy

Strong track record on improving returns

9

Focus on operational excellence is delivering sustainable & growing returns

140.8

182.8 190.3

2012 2013 2014

9.75

10.0

10.3

2012 2013 2014

10.6

11.1

11.7

2012 2013 2014

25.5

21.5

22.7

2012 2013 2014

Free Cash Flow

£m

Non-rail ROCE

%

Dividend per share

p

Earnings per share

p2013 earnings

impacted by loss

of rail contract

10

Our markets

Our markets

Attractive markets with opportunity for growth

11

Spain & Morocco

Bus & Coach

€3.8bn market

30% market share

North America

School Bus & Transit

$24bn market

14% market share

UK Bus

Regional Bus

£4.8bn market

(excluding London)

80% local market share

UK Coach

Scheduled Coach

£300m market

60% share

Rail

UK & Germany

£8.5bn UK

€6bn

Germany

Our markets

Spain & Morocco

12

• €3.8bn

Market size

• Regulated & highly segmented market with 3 levels of Government regulation; national, regional & urban

• Each concession is exclusive to the operator

Features

• Intercity competition from state-backed rail & low cost airlines

• Concessions awarded through competitive public tender, typically 10 years

Competition

• Concession renewals, urban contract wins in Spain & Morocco

Growth drivers

ALSA has leading position in a highly fragmented market

National Express adding value through quality of service with ALSA the top

rated transport company in Spain

Introduction of RMS providing competitive advantage

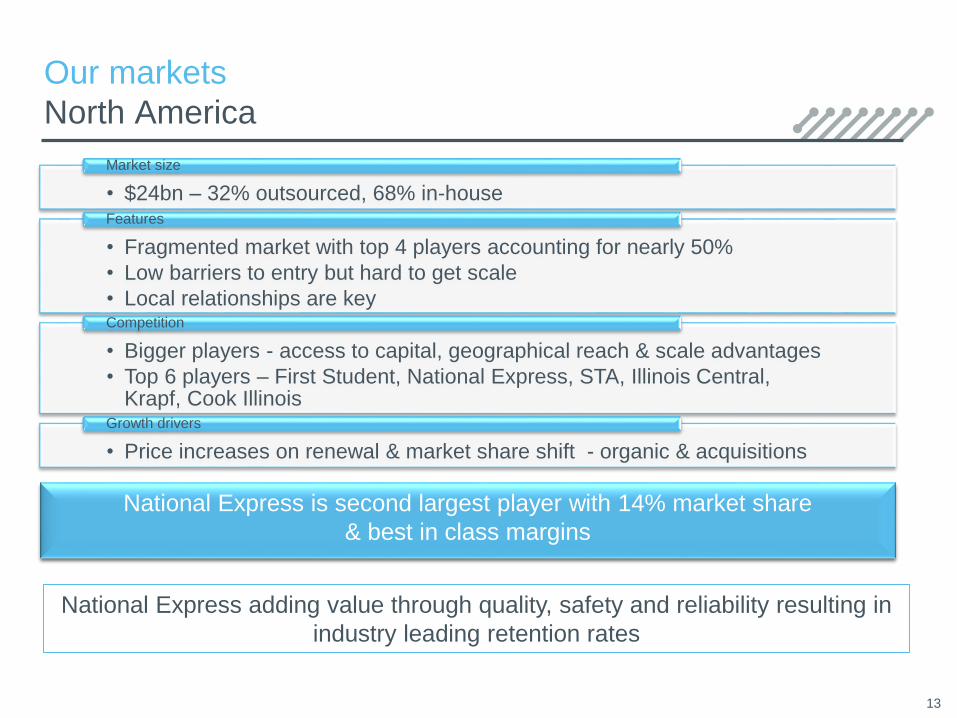

Our markets

North America

13

• $24bn – 32% outsourced, 68% in-house

Market size

• Fragmented market with top 4 players accounting for nearly 50%

• Low barriers to entry but hard to get scale

• Local relationships are key

Features

• Bigger players - access to capital, geographical reach & scale advantages

• Top 6 players – First Student, National Express, STA, Illinois Central, Krapf, Cook Illinois

Competition

• Price increases on renewal & market share shift - organic & acquisitions

Growth drivers

National Express is second largest player with 14% market share

& best in class margins

National Express adding value through quality, safety and reliability resulting in

industry leading retention rates

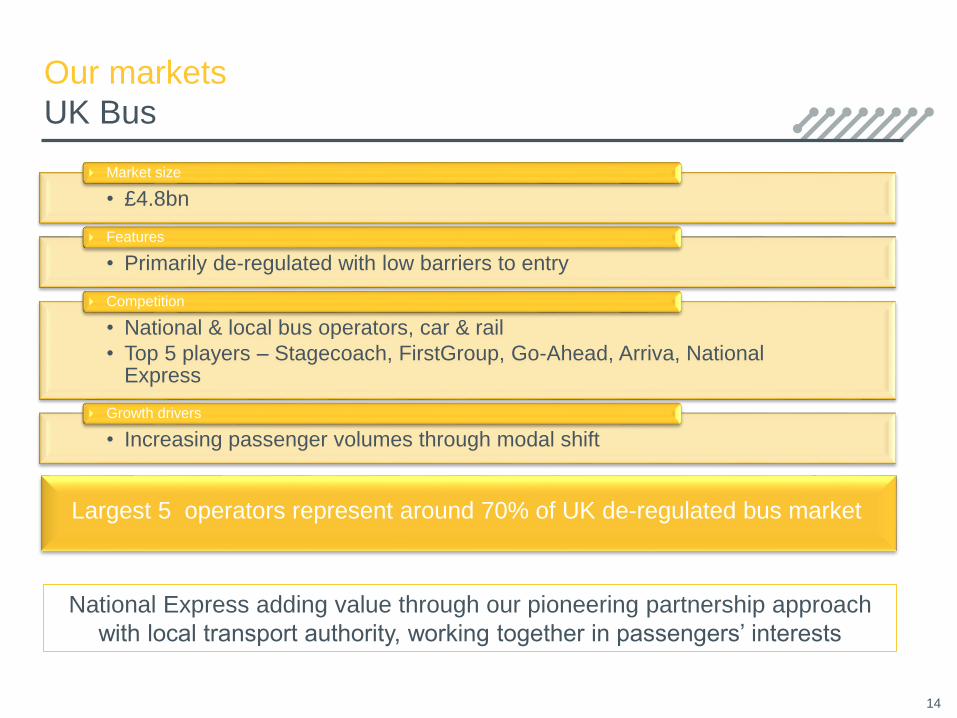

Our markets

UK Bus

14

• £4.8bn

Market size

• Primarily de-regulated with low barriers to entry

Features

• National & local bus operators, car & rail

• Top 5 players – Stagecoach, FirstGroup, Go-Ahead, Arriva, National Express

Competition

• Increasing passenger volumes through modal shift

Growth drivers

Largest 5 operators represent around 70% of UK de-regulated bus market

National Express adding value through our pioneering partnership approach

with local transport authority, working together in passengers’ interests

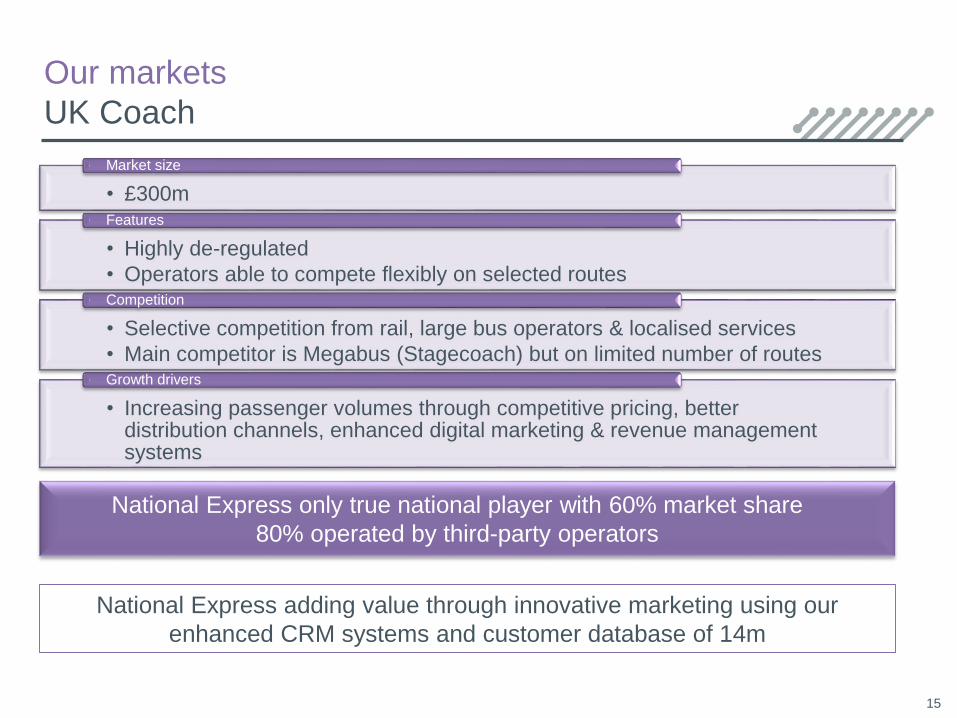

Our markets

UK Coach

15

• £300m

Market size

• Highly de-regulated

• Operators able to compete flexibly on selected routes

Features

• Selective competition from rail, large bus operators & localised services

• Main competitor is Megabus (Stagecoach) but on limited number of routes

Competition

• Increasing passenger volumes through competitive pricing, better distribution channels, enhanced digital marketing & revenue management systems

Growth drivers

National Express only true national player with 60% market share

80% operated by third-party operators

National Express adding value through innovative marketing using our

enhanced CRM systems and customer database of 14m

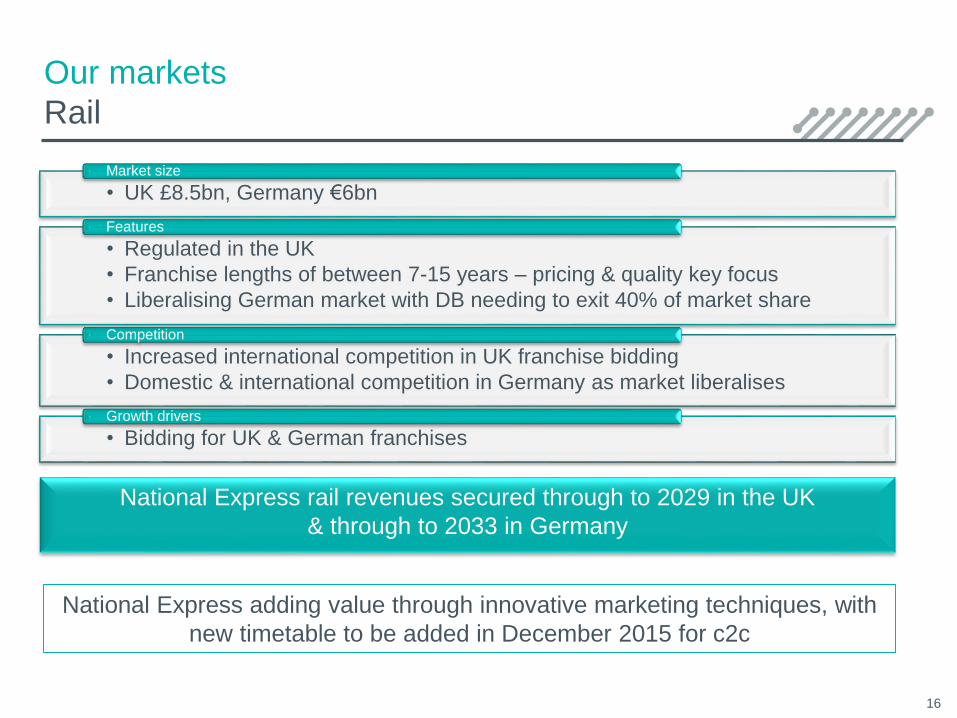

Our markets

Rail

16

• UK £8.5bn, Germany €6bnMarket size

• Regulated in the UK

• Franchise lengths of between 7-15 years – pricing & quality key focus

• Liberalising German market with DB needing to exit 40% of market share

Features

• Increased international competition in UK franchise bidding

• Domestic & international competition in Germany as market liberalises

Competition

• Bidding for UK & German franchises Growth drivers

National Express rail revenues secured through to 2029 in the UK

& through to 2033 in Germany

National Express adding value through innovative marketing techniques, with

new timetable to be added in December 2015 for c2c

17

Strategic focus &

growth opportunities

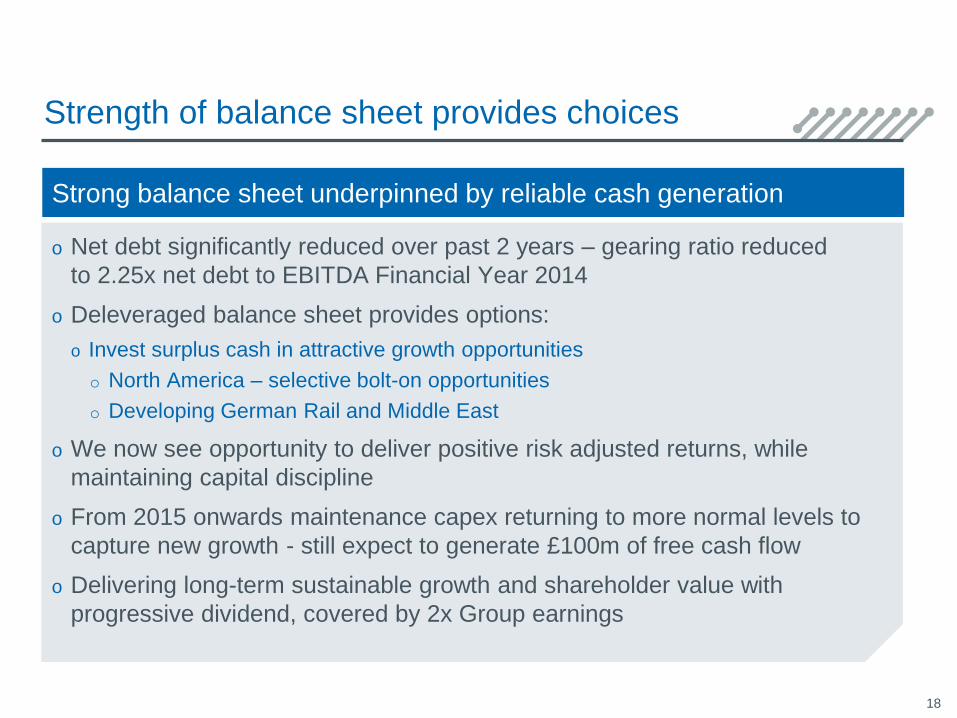

Strength of balance sheet provides choices

o Net debt significantly reduced over past 2 years – gearing ratio reduced

to 2.25x net debt to EBITDA Financial Year 2014

o Deleveraged balance sheet provides options:

o Invest surplus cash in attractive growth opportunities

o North America – selective bolt-on opportunities

o Developing German Rail and Middle East

o We now see opportunity to deliver positive risk adjusted returns, while

maintaining capital discipline

o From 2015 onwards maintenance capex returning to more normal levels to

capture new growth - still expect to generate £100m of free cash flow

o Delivering long-term sustainable growth and shareholder value with

progressive dividend, covered by 2x Group earnings

18

Strong balance sheet underpinned by reliable cash generation

North America

Opportunity for growth of 50% over 5 years

o NA school bus market worth $24bn, with 10,000+ private operators

o National Express has a strong platform

o US business doubled profits in past 5 years – potential for further significant increase

o Excellent acquisition track record: Petermann & Philadelphia

o Operational excellence reflected in industry-leading contract retention rates &

successful conversions (e.g. Memphis)

o Relentless focus on improving returns or exiting unprofitable contracts & on driving

ROA through more effective asset utilisation & capital employment

o Strong returns versus cost of capital19

695 712.1772.2

919.41009.4 1021.8

0

200

400

600

800

1000

1200

2009 2010 2011 2012 2013 2014

Revenue growth – CAGR 8.0% $m

39.6

57.1

76.9

94.0 97.9 98.0

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014

Operating profit growth – CAGR 19.9%$m

North American divisional performance over last 5 years

German Rail and Middle East

o German Rail – largest rail market in Europe

o €9bn p.a. market in regional and urban

o Built a pipeline of €2.6bn of revenue in just 2 years

o Momentum gathering: pre-qualified for 2 further bids – worth a potential €100m

revenues

o Strong pipeline of bid opportunities with around 30 contracts up for tender

in next 2 years

o Middle East - first mover advantage in fast developing markets

o Won first urban bus contract in Bahrain

o Provides platform for further growth in the region

o Submitted a further bid in the region to operate urban bus services in Makkah,

Saudi Arabia

o Active pipeline of opportunities – worth c.£0.8bn of revenue

20

Attractive growth markets with capital-light characteristics

Divisional highlightsHalf year 2015

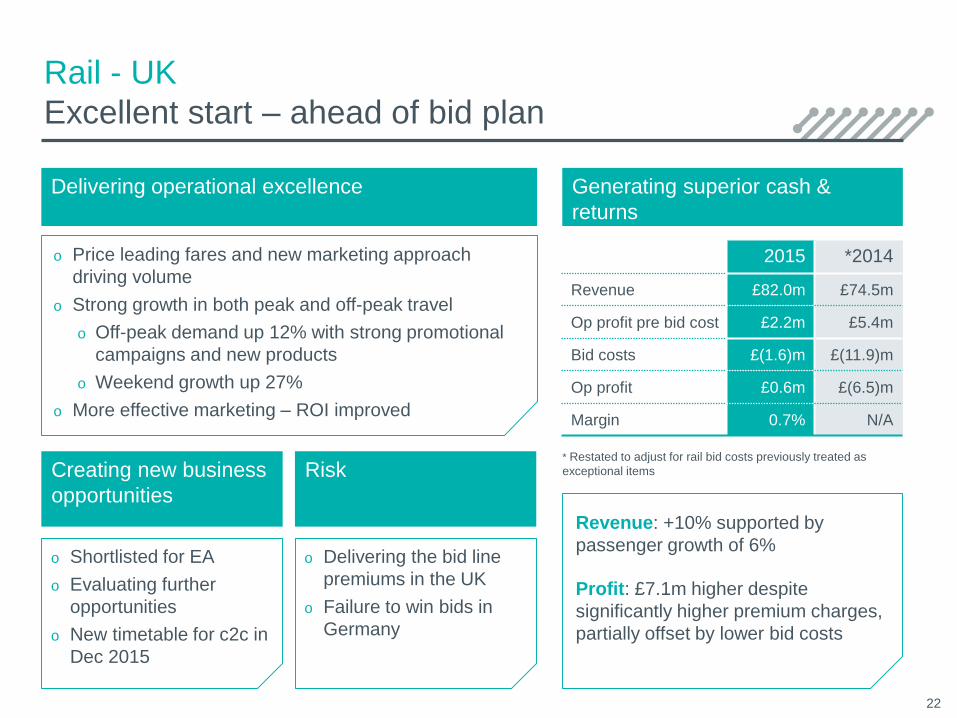

Rail - UK

Excellent start – ahead of bid plan

Delivering operational excellence

Creating new business

opportunities

22

2015 *2014

Revenue £82.0m £74.5m

Op profit pre bid cost £2.2m £5.4m

Bid costs £(1.6)m £(11.9)m

Op profit £0.6m £(6.5)m

Margin 0.7% N/A

o Price leading fares and new marketing approach

driving volume

o Strong growth in both peak and off-peak travel

o Off-peak demand up 12% with strong promotional

campaigns and new products

o Weekend growth up 27%

o More effective marketing – ROI improved

o Shortlisted for EA

o Evaluating further

opportunities

o New timetable for c2c in

Dec 2015

Revenue: +10% supported by

passenger growth of 6%

Profit: £7.1m higher despite

significantly higher premium charges,

partially offset by lower bid costs

o Delivering the bid line

premiums in the UK

o Failure to win bids in

Germany

* Restated to adjust for rail bid costs previously treated as

exceptional itemsRisk

Generating superior cash &

returns

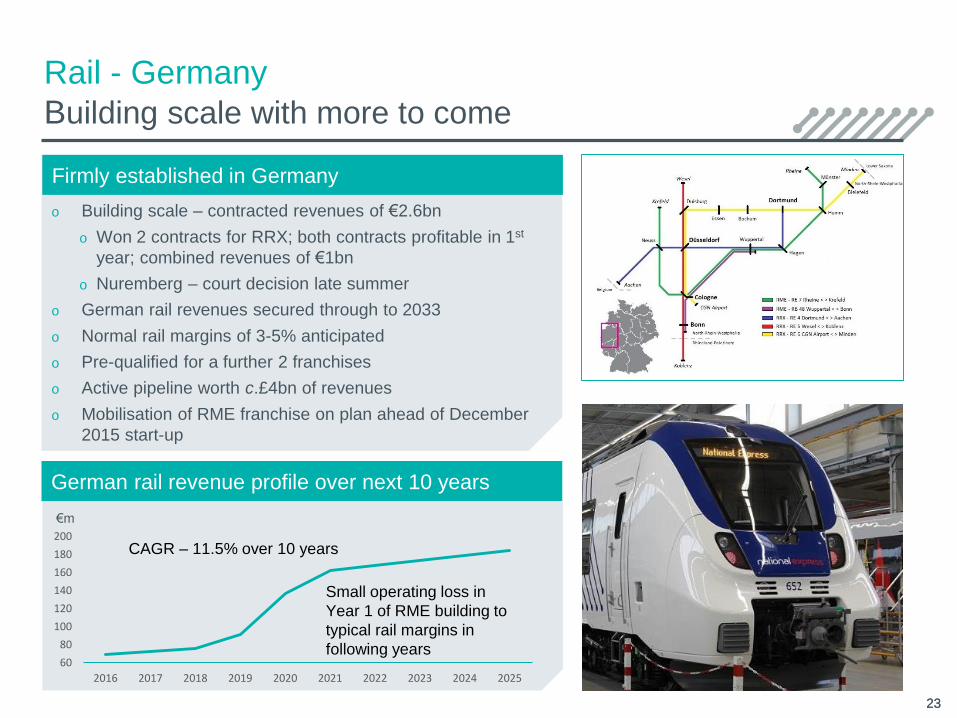

o Building scale – contracted revenues of €2.6bn

o Won 2 contracts for RRX; both contracts profitable in 1st

year; combined revenues of €1bn

o Nuremberg – court decision late summer

o German rail revenues secured through to 2033

o Normal rail margins of 3-5% anticipated

o Pre-qualified for a further 2 franchises

o Active pipeline worth c.£4bn of revenues

o Mobilisation of RME franchise on plan ahead of December

2015 start-up

Firmly established in Germany

Rail - Germany

Building scale with more to come

2323

New photo

required

60

80

100

120

140

160

180

200

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

CAGR – 11.5% over 10 years

Small operating loss in

Year 1 of RME building to

typical rail margins in

following years

€m

German rail revenue profile over next 10 years

UK Bus

Investment in services delivering clear progress

Delivering operational excellence

Creating new business

opportunities

24

2015 2014

Revenue £141.4m £137.7m

Op profit £17.1m £15.3m

Margin 12.1% 11.1%

o Robust revenue growth: commercial revenue +3%

o Launched all 83 partnership commitments for TBT3*

o Major fleet upgrade driving passenger volumes

o 8% increase on Platinum bus routes

o Continued roll-out of industry leading multi operator

smartcards & launch of new PAYG smartcard

o Bus Alliance with Centro

& West Midlands ITA

o Midland Metro

extension opens in H2

2015

Revenue: +3% driven by commercial

revenues, concessionary revenues

flat

Profit: Revenue growth and cost

efficiencies

H2 concession revenues to decline -

£3m annualised impact

o Possible reduction in

BSOG

o Concession income

under pressure

Risk

Generating superior cash &

returns

* Transforming Bus Travel agreement with Centro

UK Coach

Leveraging our enhanced CRM capabilities

Delivering operational excellence

Creating new business

opportunities

25

2015 2014

Revenue £132.2m £130.5m

Op profit £10.0m £9.3m

Margin 7.6% 7.1%

o Enhanced marketing activity driving revenue growth

o CRM driving 60% incremental growth on targeted

campaigns

o Launching strong summer campaigns building on

success of Easter and spring

o Record weekend for Glastonbury

o RM increasing yields & coach occupancy (up 3.7%)

o Contract wins; BA,

Stansted, UWL & RBS

o O’seas retail expansion

o Enhanced presence on

Trainline app

Revenue: Strong core growth of

2.4%, partially offset by the timing of

contract revenues, picking up in H2

Profit: +8% with growth in margin,

network optimisation and back office

consolidation delivering cost

efficiencies

o Advanced ticket

discounting in rail

o Government policy

(BSOG)

Risk

Generating superior cash &

returns

North America

Positive bid season & improving market

Delivering operational excellence

Creating new business

opportunities

26

2015 *2014

Revenue $553.2m $547.7m

Op profit $59.8m $57.5m

Margin 10.8% 10.5%

o Strong bid season for 2015/16

o Strong contract retention – 99% for renewals

(excluding “up or out” contracts)

o Average price increase +2.8% across portfolio, over

5% on our re-bid contracts

o On-going exit from poor performing contracts, winning

new business on higher margin

o 1 transit & 1 school bus

acquisition - combined

cash consideration of

£22m at 6x EBITDA

Revenue: +1% in constant currency,

with exit from “up or out” contracts

offsetting price increases and contract

wins

Profit: Margin up 30bps - exit from

lower margin business & higher

prices offset by wage pressures, CAD

and less operating days

o Healthcare costs

o Wage pressure

Risk

Generating superior cash &

returns

* Constant currency at 2015 FX rates

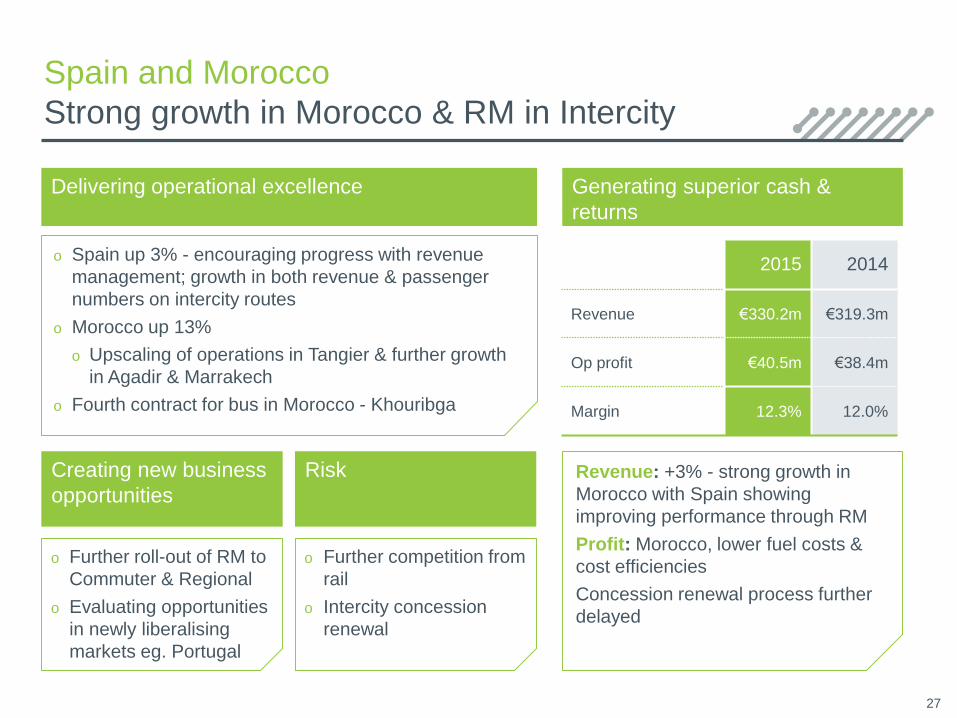

Spain and Morocco

Strong growth in Morocco & RM in Intercity

Delivering operational excellence

Creating new business

opportunities

27

2015 2014

Revenue €330.2m €319.3m

Op profit €40.5m €38.4m

Margin 12.3% 12.0%

o Spain up 3% - encouraging progress with revenue

management; growth in both revenue & passenger

numbers on intercity routes

o Morocco up 13%

o Upscaling of operations in Tangier & further growth

in Agadir & Marrakech

o Fourth contract for bus in Morocco - Khouribga

o Further roll-out of RM to

Commuter & Regional

o Evaluating opportunities

in newly liberalising

markets eg. Portugal

Revenue: +3% - strong growth in

Morocco with Spain showing

improving performance through RM

Profit: Morocco, lower fuel costs &

cost efficiencies

Concession renewal process further

delayed

o Further competition from

rail

o Intercity concession

renewal

Risk

Generating superior cash &

returns

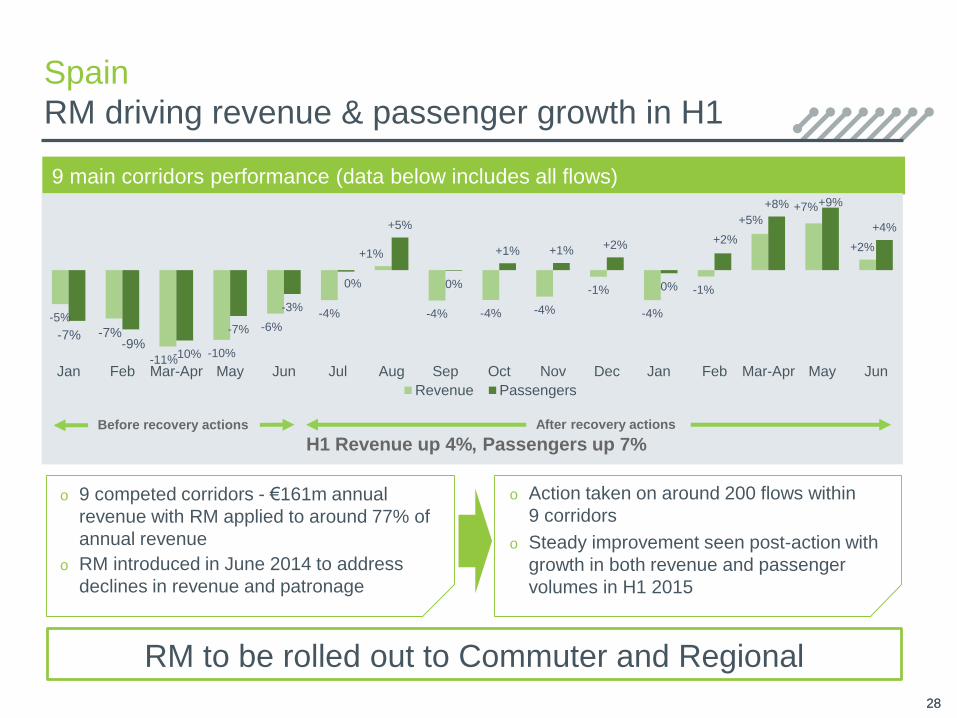

Spain

RM driving revenue & passenger growth in H1

2828

o 9 competed corridors - €161m annual

revenue with RM applied to around 77% of

annual revenue

o RM introduced in June 2014 to address

declines in revenue and patronage

o Action taken on around 200 flows within

9 corridors

o Steady improvement seen post-action with

growth in both revenue and passenger

volumes in H1 2015

9 main corridors performance (data below includes all flows)

-5%

-7%

-11%-10%

-6%-4%

+1%

-4% -4% -4%

-1%

-4%

-1%

+5%+7%

+2%

-7%-9%

-10%

-7%

-3%

0%

+5%

0%

+1% +1% +2%

0%

+2%

+8% +9%

+4%

Jan Feb Mar-Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar-Apr May Jun

Revenue Passengers

H1 Revenue up 4%, Passengers up 7%After recovery actionsBefore recovery actions

RM to be rolled out to Commuter and Regional

29

Middle East

Successful mobilisation providing a stepping stone

Delivering operational excellence

Creating new business opportunities

o Successful mobilisation of first phase in Bahrain

o 70 vehicles in service with a further 70 in phase 2

o Serving 35 routes

o 1.7m passengers already transported

o Learnings from Bahrain to be applied to future

mobilisations in the region

o Submitted a JV bid to operate bus services in

Makkah, Saudi Arabia

o Further opportunities being evaluated

o Active pipeline of c.£0.8bn revenues

30

Delivering our strategy

Further significant progress to come

Delivering

operational

excellence

Generating

superior cash &

returns

Creating new

business

opportunities

2015

30

o Margin progress across the business (excluding Rail)

o No exceptionals

o Strong growth in profit with statutory profit more than doubling

o Continued cash generation – on target to generate £100m FCF in 2015

o Lower fuel costs and potentially lower bond interest costs

o Strong pipeline of opportunities across the business

o Interim dividend up 10%

31

Financial results

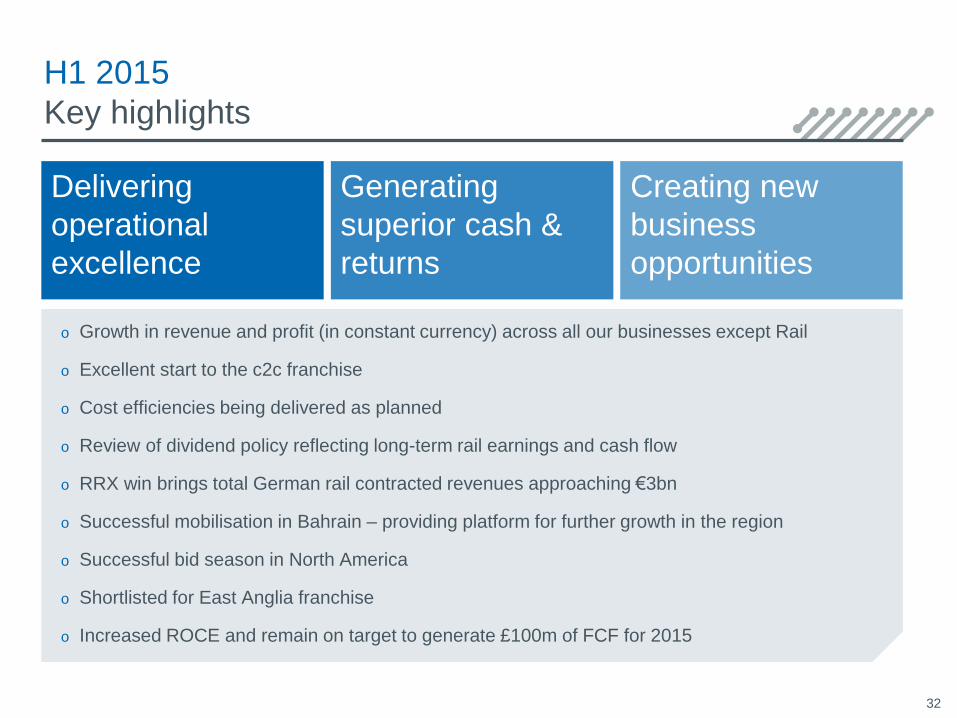

Half year 2015

H1 2015

Key highlights

o Growth in revenue and profit (in constant currency) across all our businesses except Rail

o Excellent start to the c2c franchise

o Cost efficiencies being delivered as planned

o Review of dividend policy reflecting long-term rail earnings and cash flow

o RRX win brings total German rail contracted revenues approaching €3bn

o Successful mobilisation in Bahrain – providing platform for further growth in the region

o Successful bid season in North America

o Shortlisted for East Anglia franchise

o Increased ROCE and remain on target to generate £100m of FCF for 2015

32

Delivering

operational

excellence

Generating

superior cash &

returns

Creating new

business

opportunities

33

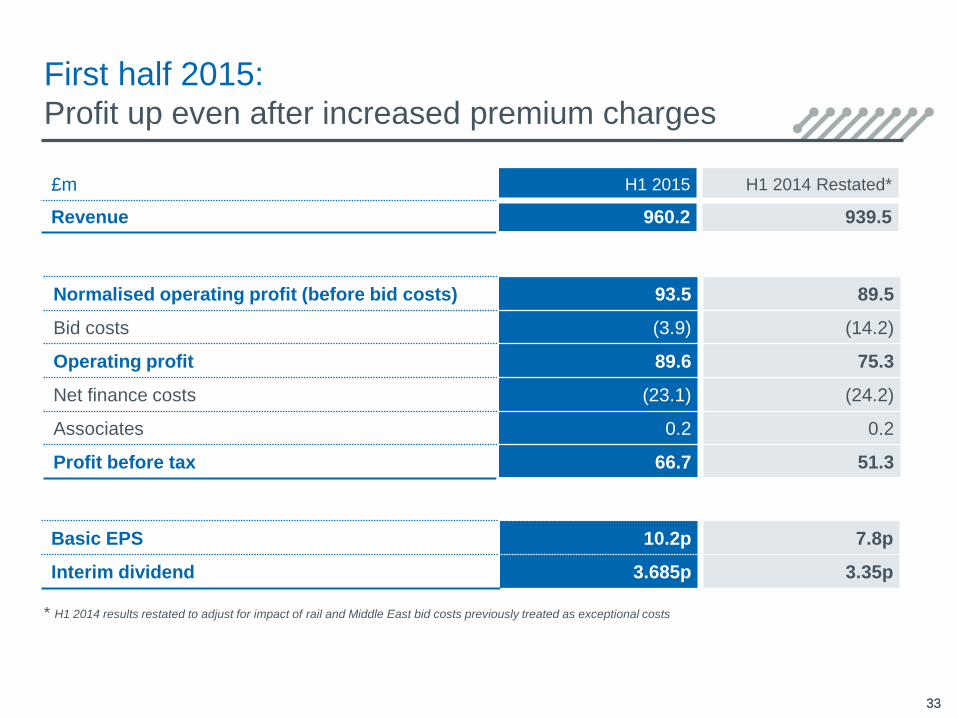

£m H1 2015 H1 2014 Restated*

Revenue 960.2 939.5

Normalised operating profit (before bid costs) 93.5 89.5

Bid costs (3.9) (14.2)

Operating profit 89.6 75.3

Net finance costs (23.1) (24.2)

Associates 0.2 0.2

Profit before tax 66.7 51.3

First half 2015:Profit up even after increased premium charges

Basic EPS 10.2p 7.8p

Interim dividend 3.685p 3.35p

33

* H1 2014 results restated to adjust for impact of rail and Middle East bid costs previously treated as exceptional costs

34

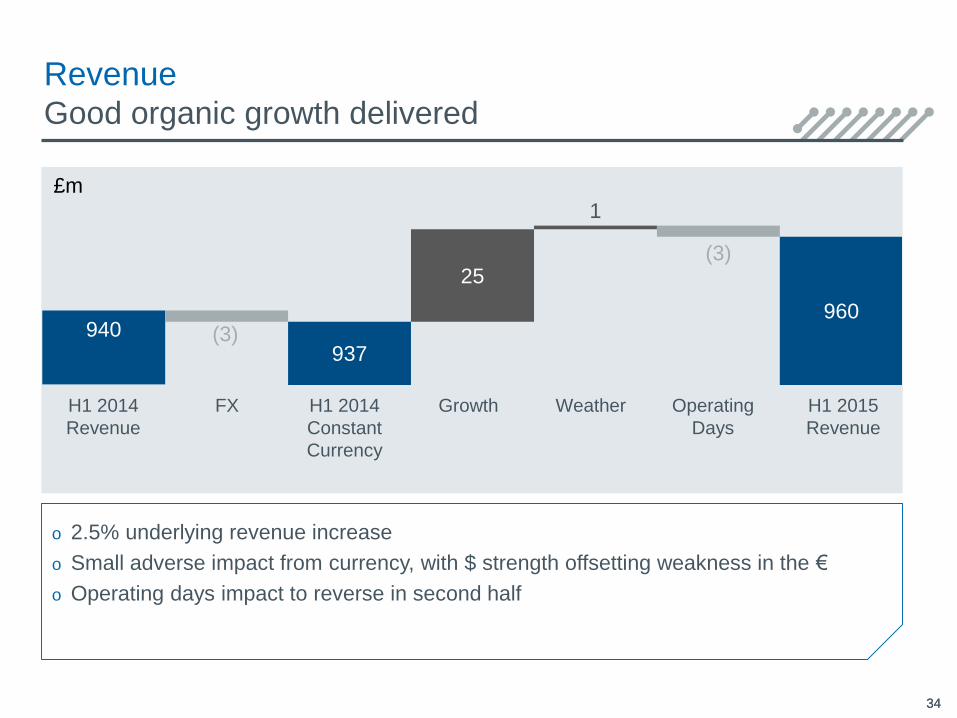

RevenueGood organic growth delivered

940 (3)937

25

1

(3)

960

£m

H1 2014

Revenue

Growth Operating

Days

H1 2015

Revenue

H1 2014

Constant

Currency

FX Weather

34

o 2.5% underlying revenue increase

o Small adverse impact from currency, with $ strength offsetting weakness in the €

o Operating days impact to reverse in second half

H1 2015

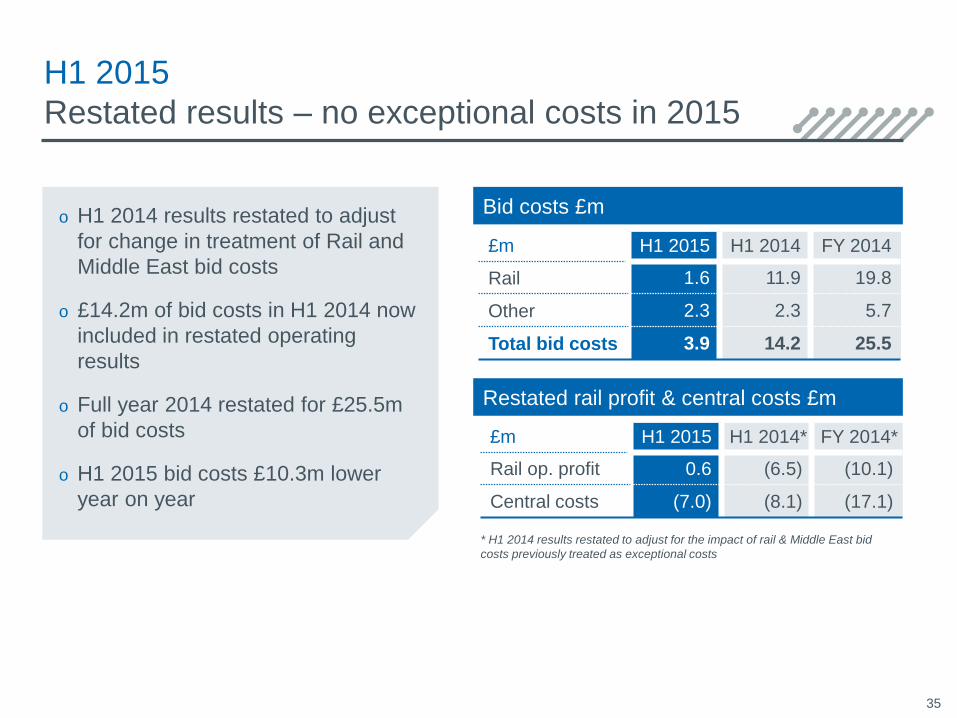

Restated results – no exceptional costs in 2015

£m H1 2015 H1 2014 FY 2014

Rail 1.6 11.9 19.8

Other 2.3 2.3 5.7

Total bid costs 3.9 14.2 25.5

* H1 2014 results restated to adjust for the impact of rail & Middle East bid

costs previously treated as exceptional costs

35

£m H1 2015 H1 2014* FY 2014*

Rail op. profit 0.6 (6.5) (10.1)

Central costs (7.0) (8.1) (17.1)

o H1 2014 results restated to adjust

for change in treatment of Rail and

Middle East bid costs

o £14.2m of bid costs in H1 2014 now

included in restated operating

results

o Full year 2014 restated for £25.5m

of bid costs

o H1 2015 bid costs £10.3m lower

year on year

Bid costs £m

Restated rail profit & central costs £m

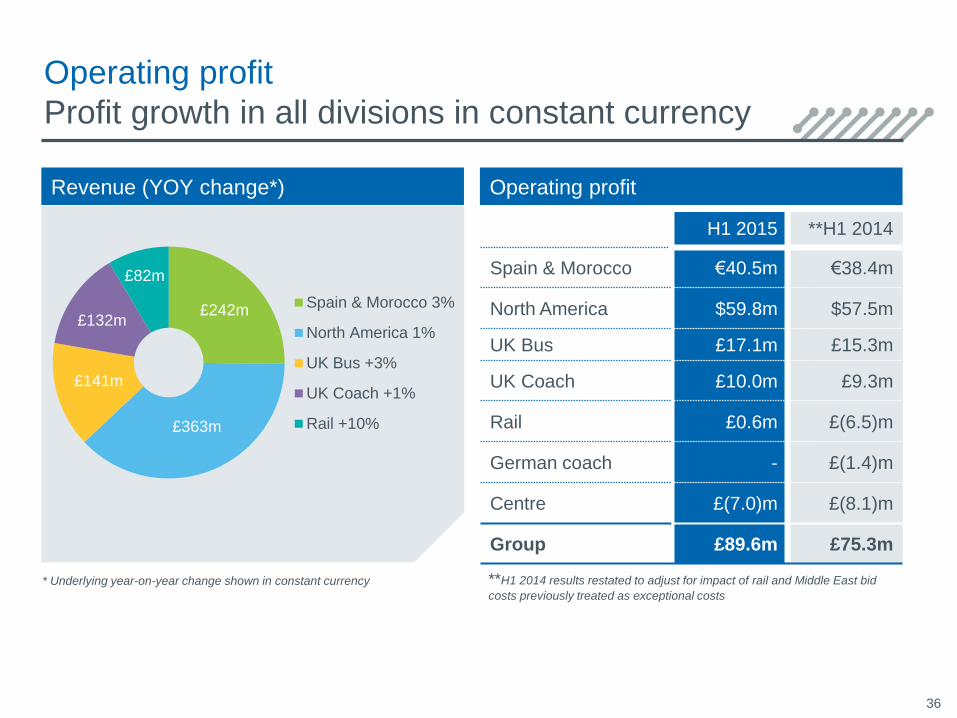

Revenue (YOY change*) Operating profit

£242m

£363m

£141m

£132m

£82m

Spain & Morocco 3%

North America 1%

UK Bus +3%

UK Coach +1%

Rail +10%

Operating profit

Profit growth in all divisions in constant currency

H1 2015 **H1 2014

Spain & Morocco €40.5m €38.4m

North America $59.8m $57.5m

UK Bus £17.1m £15.3m

UK Coach £10.0m £9.3m

Rail £0.6m £(6.5)m

German coach - £(1.4)m

Centre £(7.0)m £(8.1)m

Group £89.6m £75.3m

* Underlying year-on-year change shown in constant currency

36

**H1 2014 results restated to adjust for impact of rail and Middle East bid

costs previously treated as exceptional costs

37

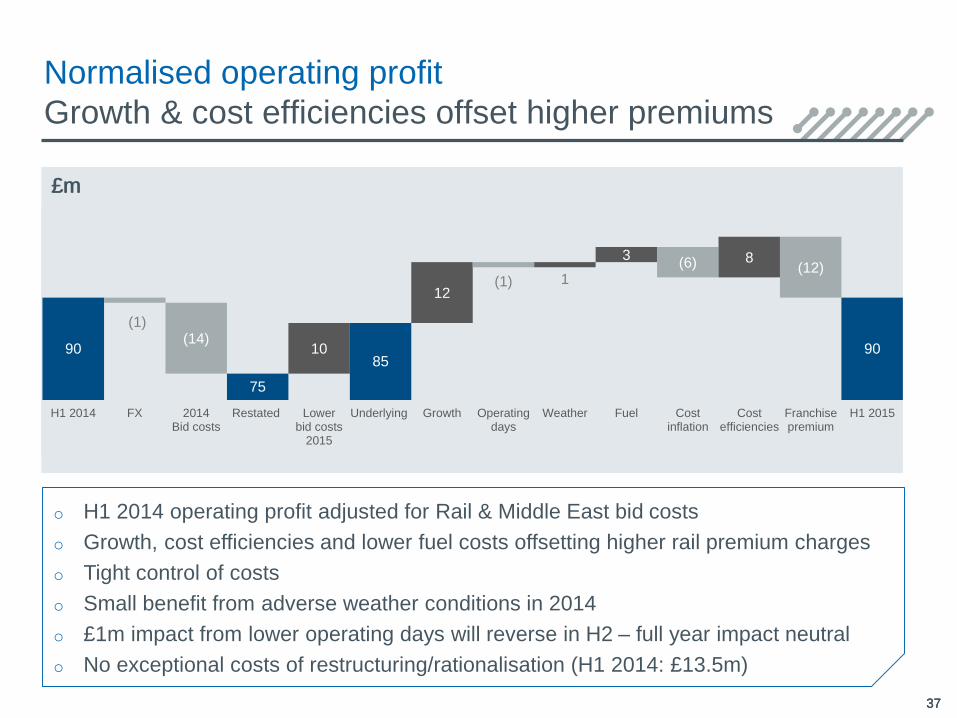

Normalised operating profit

Growth & cost efficiencies offset higher premiums

3737

£m£m

o H1 2014 operating profit adjusted for Rail & Middle East bid costs

o Growth, cost efficiencies and lower fuel costs offsetting higher rail premium charges

o Tight control of costs

o Small benefit from adverse weather conditions in 2014

o £1m impact from lower operating days will reverse in H2 – full year impact neutral

o No exceptional costs of restructuring/rationalisation (H1 2014: £13.5m)

90(14)

75

1085

12(1) 1

3(6) 8

(12)

90

H1 2014 FX 2014Bid costs

Restated Lowerbid costs

2015

Underlying Growth Operatingdays

Weather Fuel Costinflation

Costefficiencies

Franchisepremium

H1 2015

(1)

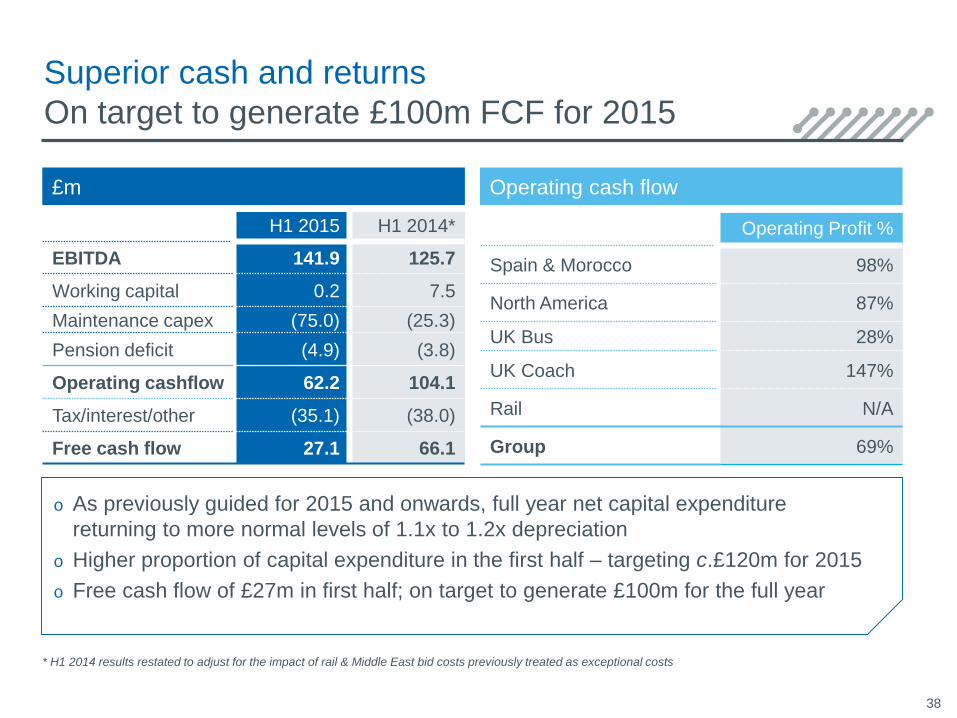

Operating cash flow

Superior cash and returns

On target to generate £100m FCF for 2015

Operating Profit %

Spain & Morocco 98%

North America 87%

UK Bus 28%

UK Coach 147%

Rail N/A

Group 69%

£m

H1 2015 H1 2014*

EBITDA 141.9 125.7

Working capital 0.2 7.5

Maintenance capex (75.0) (25.3)

Pension deficit (4.9) (3.8)

Operating cashflow 62.2 104.1

Tax/interest/other (35.1) (38.0)

Free cash flow 27.1 66.1

o As previously guided for 2015 and onwards, full year net capital expenditure

returning to more normal levels of 1.1x to 1.2x depreciation

o Higher proportion of capital expenditure in the first half – targeting c.£120m for 2015

o Free cash flow of £27m in first half; on target to generate £100m for the full year

* H1 2014 results restated to adjust for the impact of rail & Middle East bid costs previously treated as exceptional costs

38

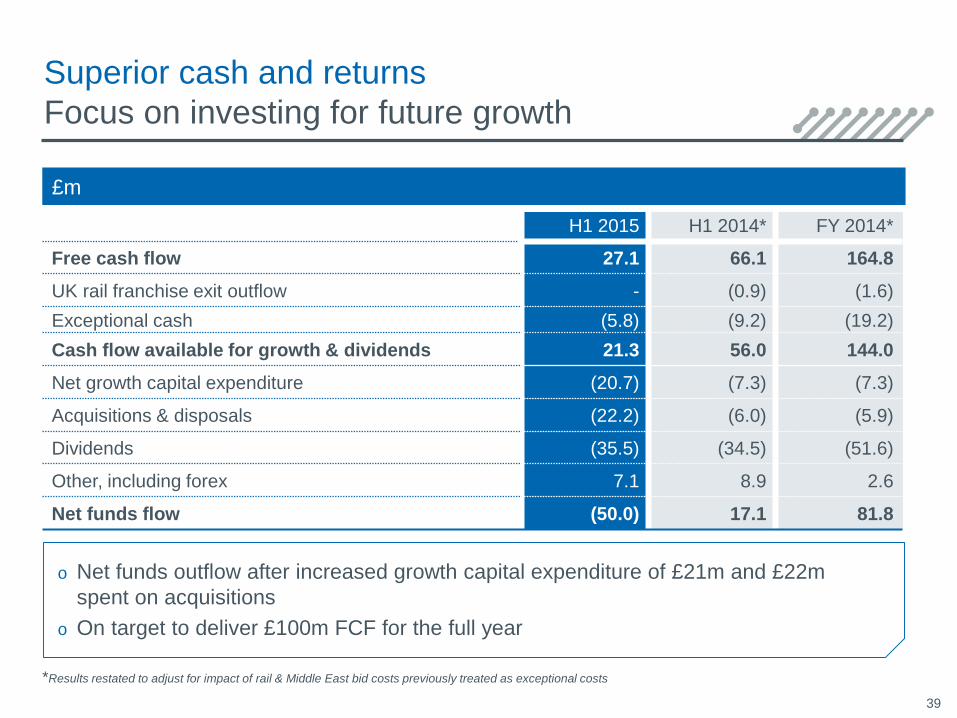

Superior cash and returns

Focus on investing for future growth

£m

H1 2015 H1 2014* FY 2014*

Free cash flow 27.1 66.1 164.8

UK rail franchise exit outflow - (0.9) (1.6)

Exceptional cash (5.8) (9.2) (19.2)

Cash flow available for growth & dividends 21.3 56.0 144.0

Net growth capital expenditure (20.7) (7.3) (7.3)

Acquisitions & disposals (22.2) (6.0) (5.9)

Dividends (35.5) (34.5) (51.6)

Other, including forex 7.1 8.9 2.6

Net funds flow (50.0) 17.1 81.8

39

o Net funds outflow after increased growth capital expenditure of £21m and £22m

spent on acquisitions

o On target to deliver £100m FCF for the full year

*Results restated to adjust for impact of rail & Middle East bid costs previously treated as exceptional costs

40

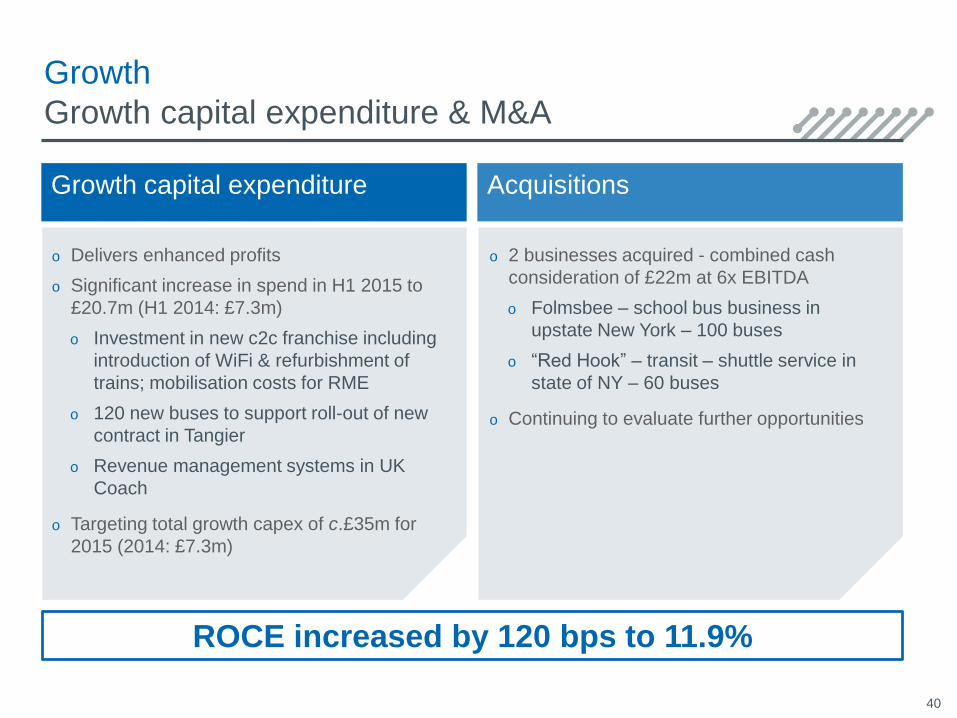

Growth

Growth capital expenditure & M&A

Growth capital expenditure Acquisitions

o Delivers enhanced profits

o Significant increase in spend in H1 2015 to

£20.7m (H1 2014: £7.3m)

o Investment in new c2c franchise including

introduction of WiFi & refurbishment of

trains; mobilisation costs for RME

o 120 new buses to support roll-out of new

contract in Tangier

o Revenue management systems in UK

Coach

o Targeting total growth capex of c.£35m for

2015 (2014: £7.3m)

o 2 businesses acquired - combined cash

consideration of £22m at 6x EBITDA

o Folmsbee – school bus business in

upstate New York – 100 buses

o “Red Hook” – transit – shuttle service in

state of NY – 60 buses

o Continuing to evaluate further opportunities

ROCE increased by 120 bps to 11.9%

Debt maturity profile

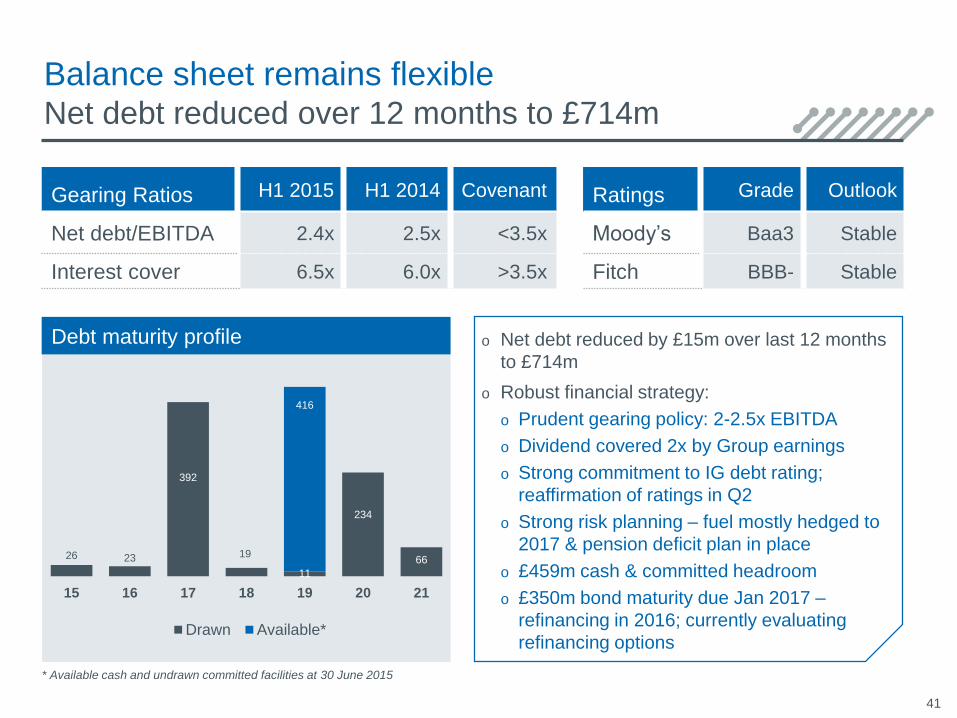

Balance sheet remains flexibleNet debt reduced over 12 months to £714m

o Net debt reduced by £15m over last 12 months

to £714m

o Robust financial strategy:

o Prudent gearing policy: 2-2.5x EBITDA

o Dividend covered 2x by Group earnings

o Strong commitment to IG debt rating;

reaffirmation of ratings in Q2

o Strong risk planning – fuel mostly hedged to

2017 & pension deficit plan in place

o £459m cash & committed headroom

o £350m bond maturity due Jan 2017 –

refinancing in 2016; currently evaluating

refinancing options

* Available cash and undrawn committed facilities at 30 June 2015

26 23

392

19

11

234

66

416

15 16 17 18 19 20 21

Drawn Available*

Gearing Ratios H1 2015 H1 2014 Covenant

Net debt/EBITDA 2.4x 2.5x <3.5x

Interest cover 6.5x 6.0x >3.5x

Ratings Grade Outlook

Moody’s Baa3 Stable

Fitch BBB- Stable

41

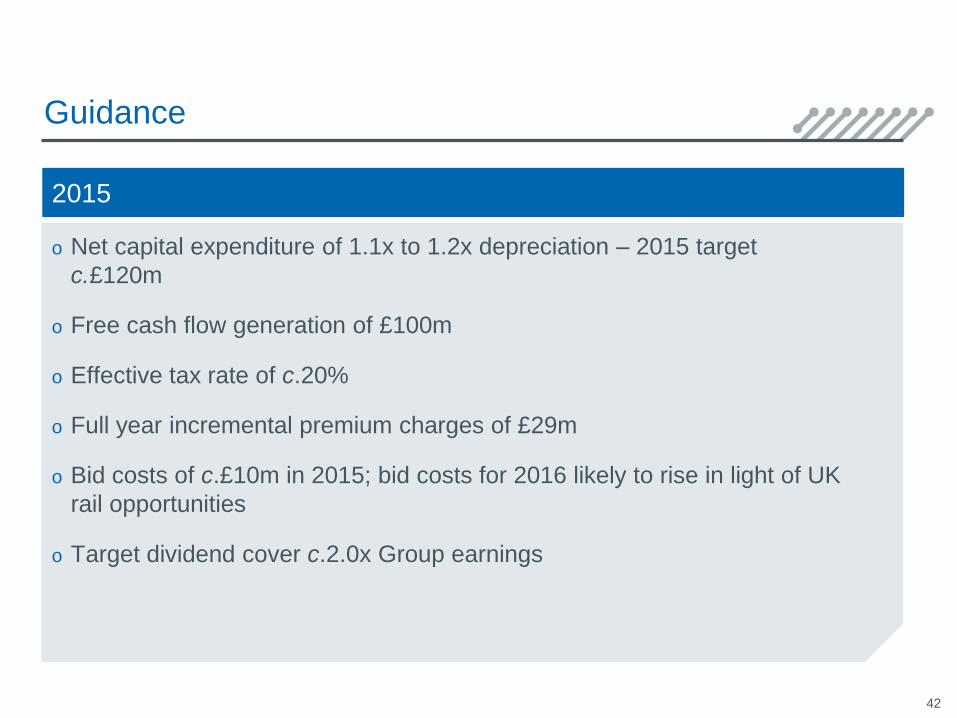

Guidance

o Net capital expenditure of 1.1x to 1.2x depreciation – 2015 target

c.£120m

o Free cash flow generation of £100m

o Effective tax rate of c.20%

o Full year incremental premium charges of £29m

o Bid costs of c.£10m in 2015; bid costs for 2016 likely to rise in light of UK

rail opportunities

o Target dividend cover c.2.0x Group earnings

42

2015

Appendix

44

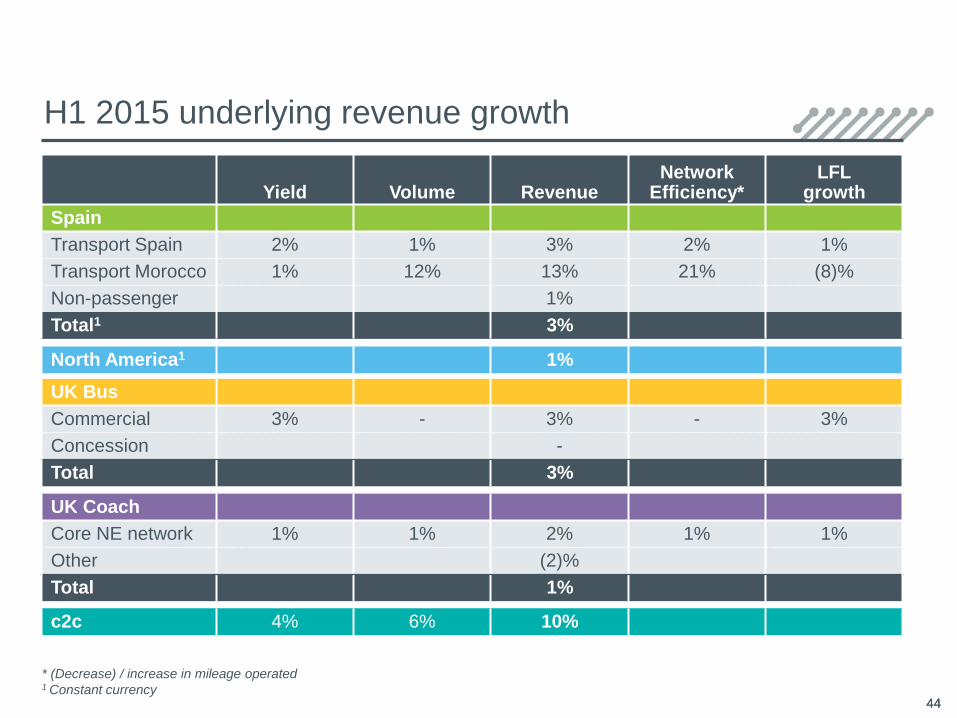

H1 2015 underlying revenue growth

Yield Volume RevenueNetwork

Efficiency*LFL

growth

Spain

Transport Spain 2% 1% 3% 2% 1%

Transport Morocco 1% 12% 13% 21% (8)%

Non-passenger 1%

Total1 3%

North America1 1%

UK Bus

Commercial 3% - 3% - 3%

Concession -

Total 3%

UK Coach

Core NE network 1% 1% 2% 1% 1%

Other (2)%

Total 1%

c2c 4% 6% 10%

* (Decrease) / increase in mileage operated1 Constant currency

44

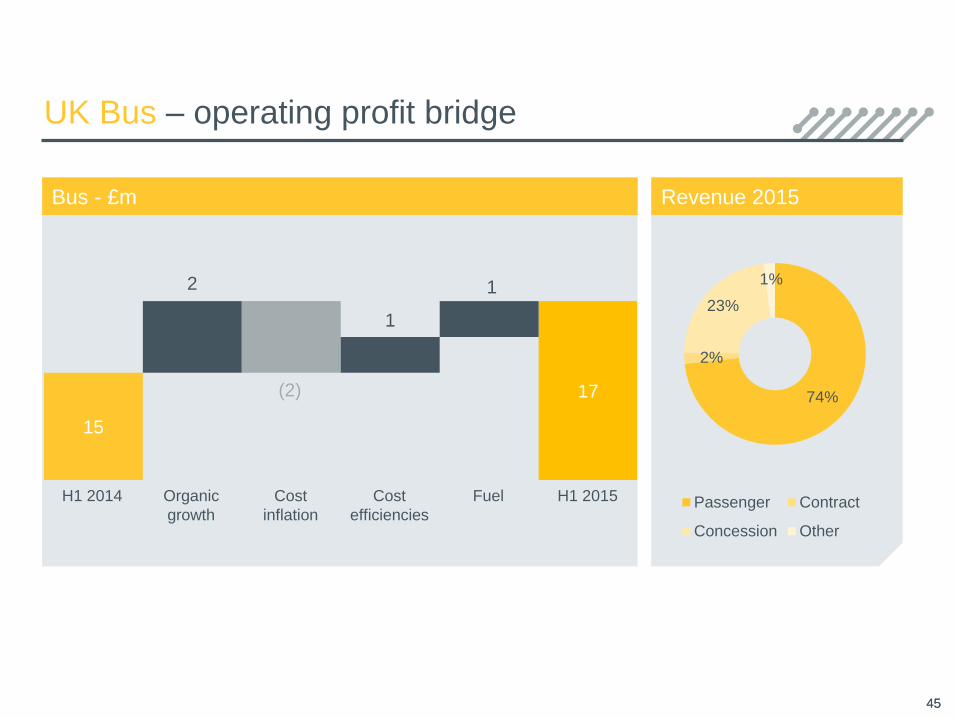

Bus - £m

UK Bus – operating profit bridge

45

Revenue 2015

74%

2%

23%

1%

Passenger Contract

Concession Other

Organic

growth

FuelCost

inflation

Cost

efficiencies

45

H1 2014 H1 2015

15

17

2

(2)

1

1

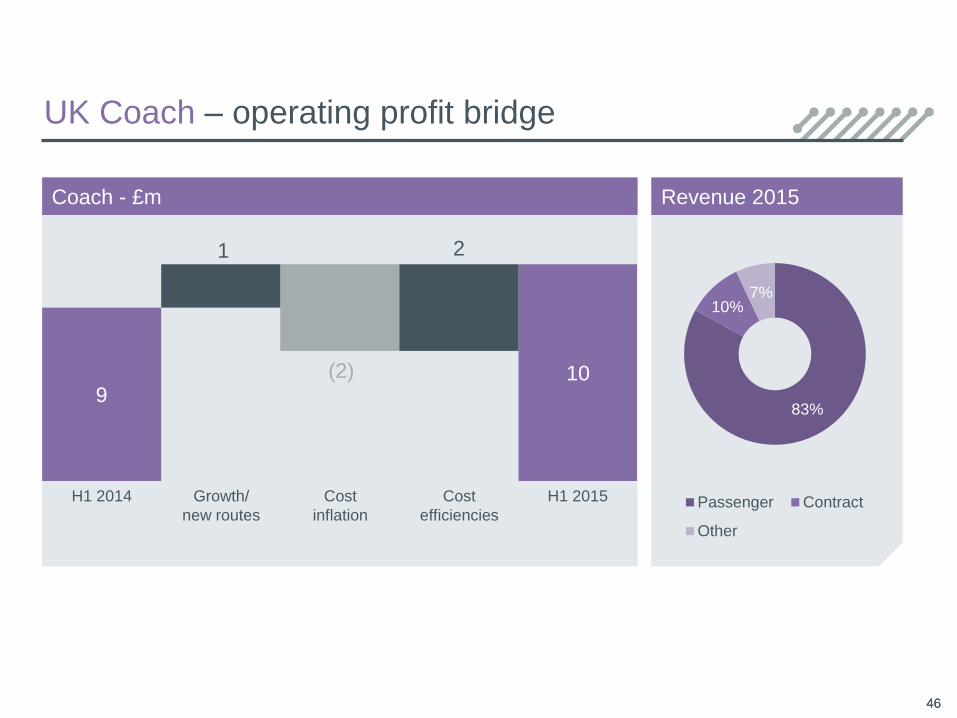

Coach - £m

UK Coach – operating profit bridge

46

Revenue 2015

83%

10%7%

Passenger Contract

Other

H1 2014 Cost

inflation

Cost

efficiencies

Growth/

new routes

H1 2015

46

9 10

1

(2)

2

61%

29%

3%

7%

Passenger Contract

Concession Other

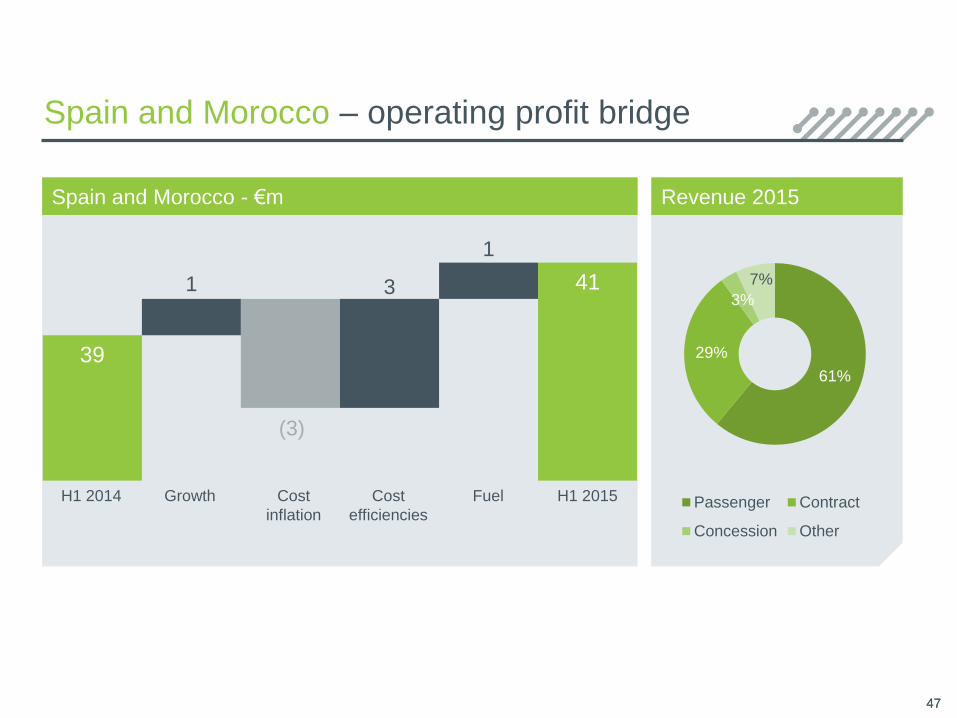

Spain and Morocco – operating profit bridge

47

Revenue 2015

FuelCost

inflation

Cost

efficiencies

47

Growth

39

41 1

(3)

3

1

Spain and Morocco - €m

H1 2014 H1 2015

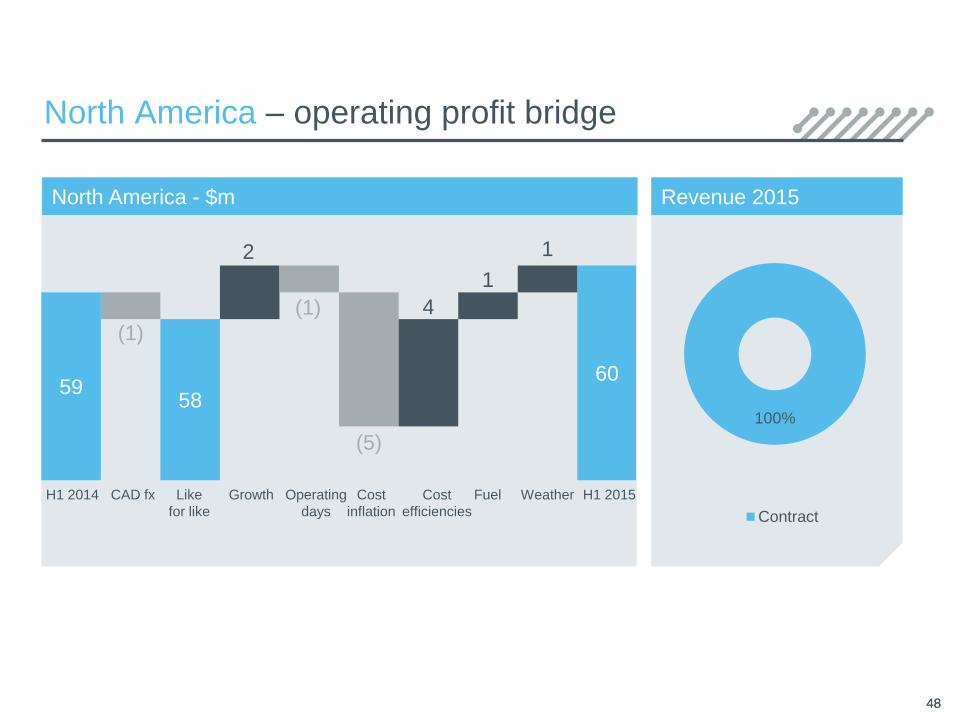

North America - $m

North America – operating profit bridge

48

Revenue 2015

Cost

inflation

Cost

efficiencies

Like

for like

Fuel

48

WeatherH1 2014 H1 2015CAD fx

100%

Contract

59 58

60

(1)

2

(1)

(5)

4

1

1

Growth Operating

days

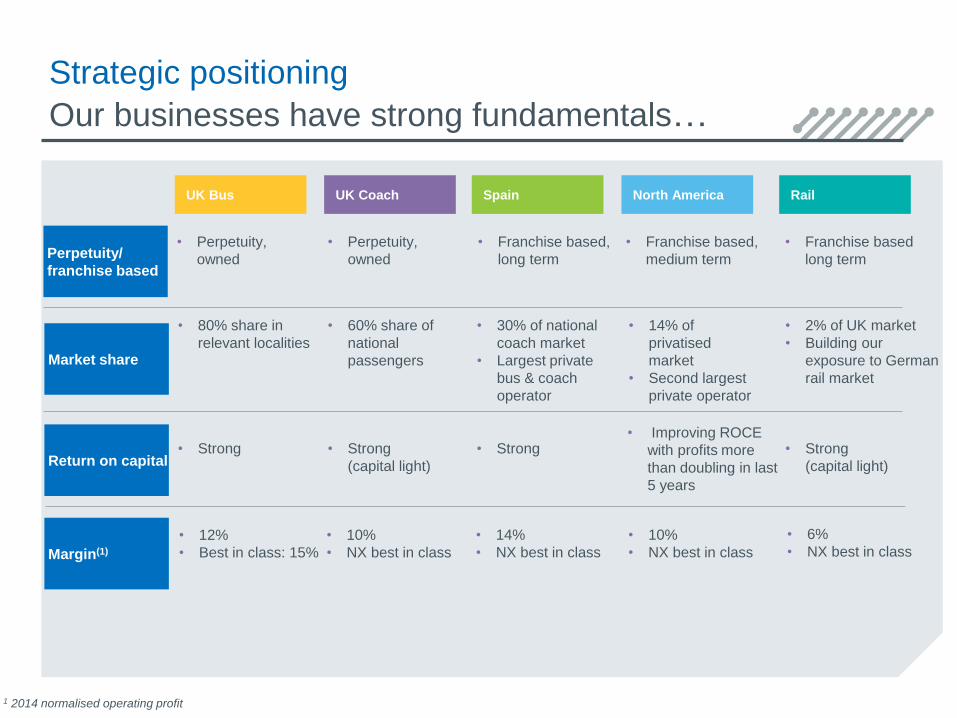

Perpetuity/

franchise based

• Perpetuity,

owned

• Perpetuity,

owned

• Franchise based,

long term

• Franchise based,

medium term

UK Bus UK Coach Spain North America

Strategic positioning

Our businesses have strong fundamentals…

Margin(1)

Return on capital• Strong • Strong

(capital light)

• Strong

(capital light)

Market share

• 80% share in

relevant localities

• 60% share of

national

passengers

• 2% of UK market

• Building our

exposure to German

rail market

• 30% of national

coach market

• Largest private

bus & coach

operator

• 14% of

privatised

market

• Second largest

private operator

• Strong• Improving ROCE

with profits more

than doubling in last

5 years

• 12%

• Best in class: 15%

• 10%

• NX best in class

• 6%

• NX best in class• 14%

• NX best in class

• 10%

• NX best in class

1 2014 normalised operating profit

• Franchise based

long term

Rail

Pipeline of opportunities remains exciting

50

UK Rail North America German Rail Middle East

Target market £8.5bn – franchised

£150-1,000m each

7-15 year life

$8bn Transit

$24bn School Bus

Contracts $5-100m

3-5 year life

€6bn regional

DB main operator

Pro-competition

€20-100m each

Selected geography

Bus, coach & rail

Liberalisation trend

New public transport

models

Revenue risk Yes/

Possible underpin

Contracted/

Some risk

Gross cost/

Net cost mix

Mix

Attractiveness*:

Revenue growth

Margin

Capital req’d

ROCE

H

L

L

H

Transit School Bus

H H

L M

L H

H M

L

L

L

H

H

L

L

H

3 year target

opportunity

£4.5bn annual revenues $0.5bn €4bn total contract

revenues

£3bn total contract

revenues

Active pipeline 4 contracts

£2bn annual revenues

East Anglia bid underway

100+ contracts

$0.4bn

3 Transit wins,

10+ School Bus wins

5+ contracts

€0.2bn annual revenues

RRX secured

4 opportunities

£0.8bn total contract

revenues

In evaluation on other

key opportunities

* H – High; M- Medium; L- Low

Risk managementFuel risk largely fixed until 2017

o Future year-on-year savings locked in (2014: 49p)

2015 2016 2017 2018

% hedged* 100% 100% 88% 22%

Price per litre 44p 42p 41p 34p

Fuel Hedging

51

* Of addressable volume (c240 million litres)

Risk managementPension deficit plan in place through 2017

£m

Surplus /(Deficit)

H1 2015

Surplus /(Deficit)

31 Dec 2014

Profit /(charge)

H1 2015

Profit /(charge)

H1 2014

UK Bus (51.1) (50.6) (2.7) (2.1)

UK Coach 30.5 30.6 0.6 0.3

Rail 10.9 10.0 (1.3) (1.3)

Other (2.0) (1.9) (0.1) -

52

588 606680 678

619 646705 704

12 10 13 14

(19) (30) (12) (12)

2012 2013 2014 H1 2015

Assets

Liabilities

Members Share

Surplus/(Deficit)

Pensions £m (IAS19)

National Express Group PLC