Embed Size (px)

Citation preview

Christopher Vojta, MD, MBADirector, Deloitte Consulting, LLPChicago, IL

Randall Williams, MD Chief Executive Officer, Pharos Innovations, LLCNorthfield, IL

Sandeep Wadhwa, MD, MBA Medical Director, Colorado Department for Health Care Policy and Financing Denver, CO

David Gorstein, MD James L. Dooley & Associates, Inc Mt. Pleasant, SC

Innovations in Innovations in Population HealthPopulation Health

Still questions about the cost effectiveness of current DM Models

One recent article:

“Cost-effectiveness of Telephonic Disease Management in Heart Failure” (Am J Manag Care. 2008;14:106-115)

Conclusions: The intervention was effective but costly to implement and did not reduce utilization.

Why is this so hard?

Introduction

Being bad is more fun than being good

What are some potential drivers of incremental ROI in DM?

What are some of the ways to align incentives for physicians to be active, enthusiastic partners in chronic care management?

What are the keys to incenting healthy consumer behavior?

Introduction

Innovations in Population Health:Innovations in Population Health:Implications for Consumers, Implications for Consumers, Health Plans and ProvidersHealth Plans and Providers

Chris Vojta, Director, Deloitte Healthcare Consulting, LLP

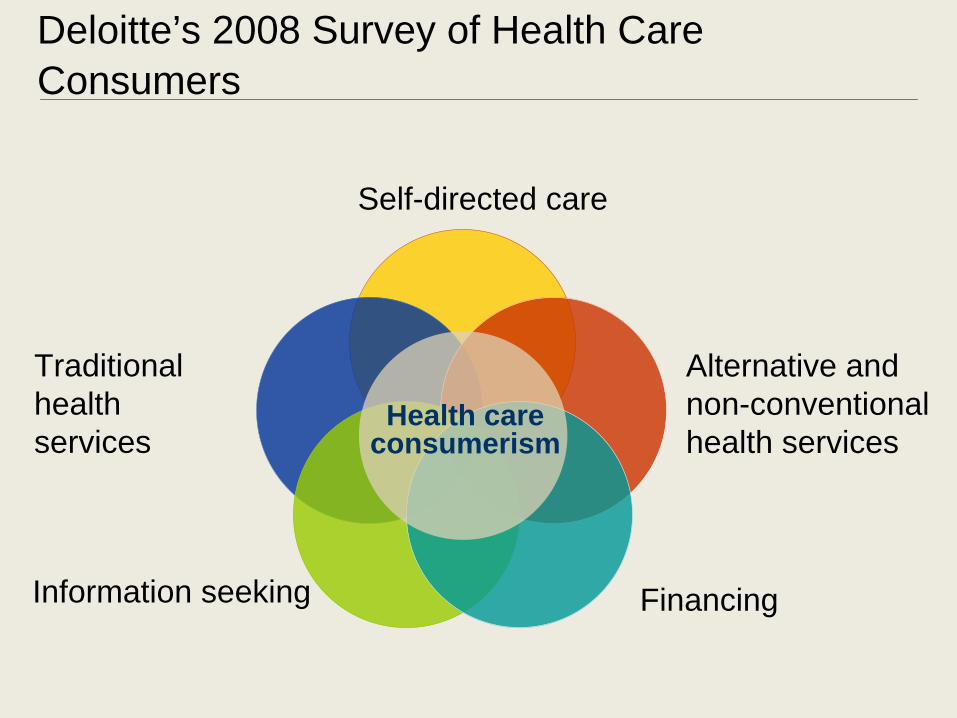

Traditional health services

Self-directed care

Information seeking

Alternative and non-conventional health services

Financing

Health care consumerism

Deloitte’s 2008 Survey of Health Care Consumers

Factor Content & Compliant

Sick & Savvy

Online & Onboard

Shop & Save

Out & About

Casual & Cautious

Segment size 29% 24% 8% 2% 9% 28%

System use Medium Highest High Medium Medium Lowest

Preferences regarding care Traditional Traditional

Traditional, but open to non- conventional settings

Traditional, but open to alternative and non- conventional settings

Alternative approaches and non- conventional settings

Disengaged, but currently leans toward traditional

Dependence on providers

Accepts what doctor recommends

Takes charge of own care

Leans toward relying on self

Leans toward allowing doctor to make decisions

Makes own decisions/ independent

Leans toward relying on self

Compliance with treatment Most compliant Compliant Compliant Less compliant Least

compliant Less compliant

Satisfaction with providers and plans

Most satisfied Satisfied Satisfied Less satisfied Least satisfied Less satisfied

Other important distinctions

Less likely to seek information; less likely to use value- added services; least interested in shopping for and customizing insurance

Seeks information; sensitive to quality; uses some value- added services; wants to shop for and customize insurance

Seeks information; uses online tools the most; sensitive to quality; maximizes use of value-added services

Makes changes to insurance; price-sensitive; uses value- added services; most likely to travel for care

Seeks information; sensitive to quality; uses some value- added services; wants to shop for and customize insurance

Price-sensitive; unprepared financially for future needs; less likely to seek information; less likely to use value- added services

Consumer Segments have varying attitudes and preferences

Integrated Health Management Vision: One Seamless Organization Focused on the Members; Value and Transparency Throughout...

Inbound Claims/Benefits Calls become a major lever

Predictive Modeling / Gaps in Care

Health Risk Assessment

Utilization Management

Provider Referrals

Nurse Call-in Lines

Pharmacy

Lab results

Referrals from providers & vendors

Information Sources

Health Coaches:Wellness Programs

Lifestyle Management

Coaching

Network Direction

Clinical Specialists:Chronic Disease Management

Care Management

Specialty Networks

End-of-Life

Hospice

PersonalizedHealth Record

Benefit Design & Financial

Management Integration

Web-based EducationAnd tools

Robust Reporting: Operational, Clinical, Financial

Enhanced Member Services

Integrated Common Platform:

Real-time Member Profiles &

Opportunities ID

Next Generation Health Plan Medical Management Strategy

Employers

Individuals

Provider

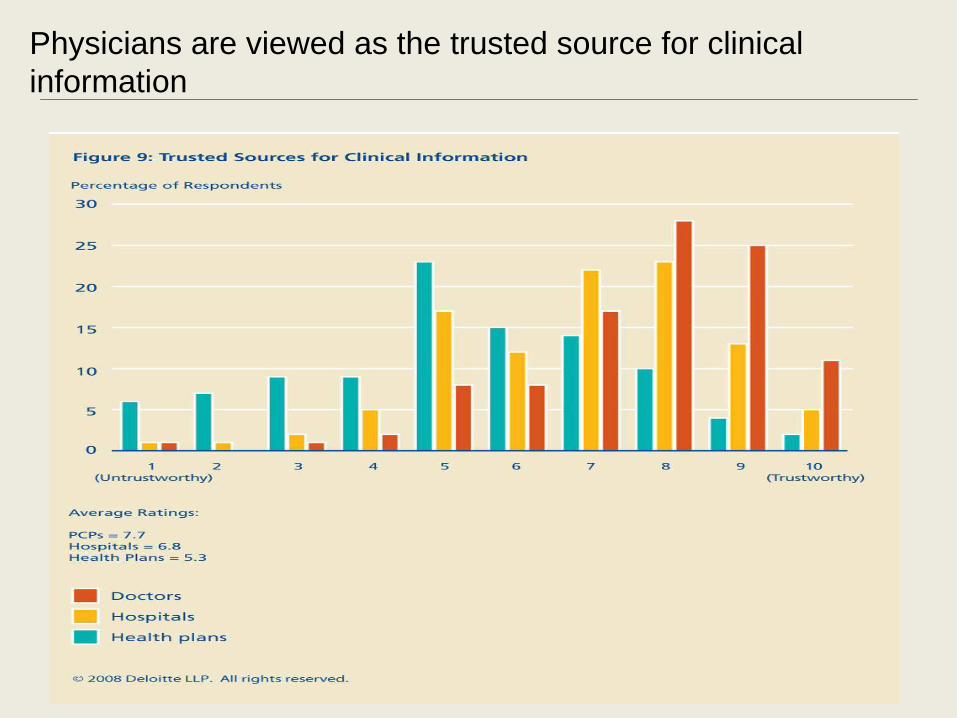

Physicians are viewed as the trusted source for clinical information

Primary Care PhysicianIncentives: VisitsInvestments: NAIncremental Costs: NAPanel Size: 1,500 activeNet Revenues: $350,000-$600,000

Future StatePrimary Care Physician/Health CoachesIncentives: Increased adherenceInvestments: EMR ($100,000)Incremental Costs: $115,000 per PCP/$78,000 per CoachPanel Size: 1,500 activeNet Revenues: $500,000-$1,000,000

Requires $150 per patient per month reduction to break evenHospitals risk 10% of admissions and 20% of ED visits

Data sharing capability is key

Medical Home Models

Current State

Future Directions in DM: Role of Future Directions in DM: Role of Technology; Role of the PatientTechnology; Role of the Patient--

Provider ConnectionProvider Connection

Randy Williams, M.D.Pharos Innovations

Technology Leveraged DM

• RPM Defined• Specific

operational leverage points

• Model nuances and unanswered questions

• Improvement in ROI

• Results

Provider-Patient Engagement• New models of

provider engagement– P4P Demonstrations– Medical Home

evolving models– Hospitals as Hubs

• New approaches to patient engagement– Population

segmentation approaches

– Non-clinical engagers– Role of physician

endorsement

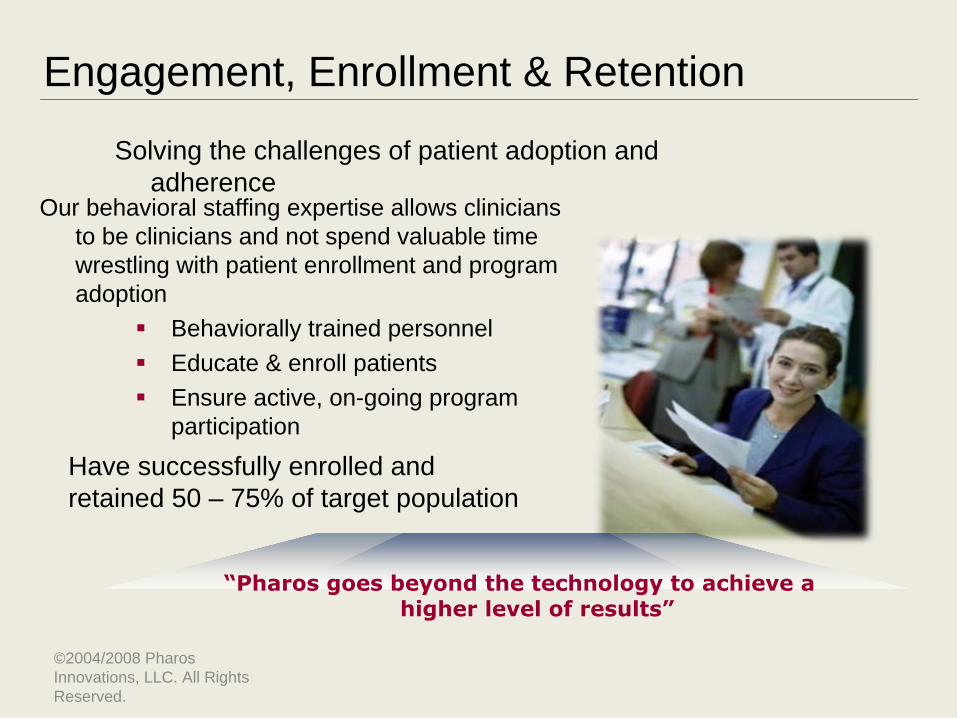

Engagement, Enrollment & Retention

Our behavioral staffing expertise allows clinicians to be clinicians and not spend valuable time wrestling with patient enrollment and program adoption

Behaviorally trained personnelEducate & enroll patientsEnsure active, on-going program participation

Solving the challenges of patient adoption and adherence

Have successfully enrolled and retained 50 – 75% of target population

“Pharos goes beyond the technology to achieve a higher level of results”

©2004/2008 Pharos Innovations, LLC. All Rights Reserved.

Patient phones with daily clinical & behavioral

status report

Patient phones with daily clinical & behavioral

status report

Nurse Care Manager accesses variance

dashboard

Nurse Care Manager accesses variance

dashboard

Care Manager telephonic patient

assessment

Care Manager telephonic patient

assessment

Reviews adherence to treatment plan

Reviews adherence to treatment plan

Reinforcement of treatment plan,

alteration as needed

Reinforcement of treatment plan,

alteration as needed

Computer collects daily touch-tone patient responses

Algorithms trigger “exception reports”

Patients who have not called in receive automated outbound reminders

Clinical change or self- care compliance

challenge

Clinical change or self- care compliance

challenge

©2004/2008 Pharos Innovations, LLC. All Rights Reserved.

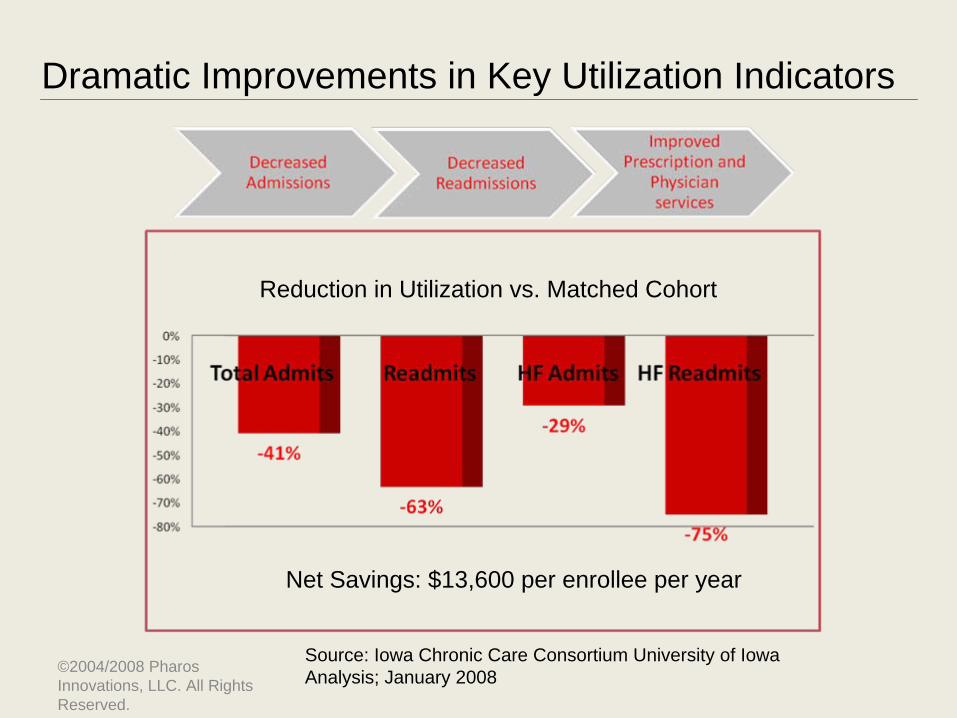

Reduction in Utilization vs. Matched Cohort

Dramatic Improvements in Key Utilization Indicators

Source: Iowa Chronic Care Consortium University of Iowa Analysis; January 2008

Net Savings: $13,600 per enrollee per year

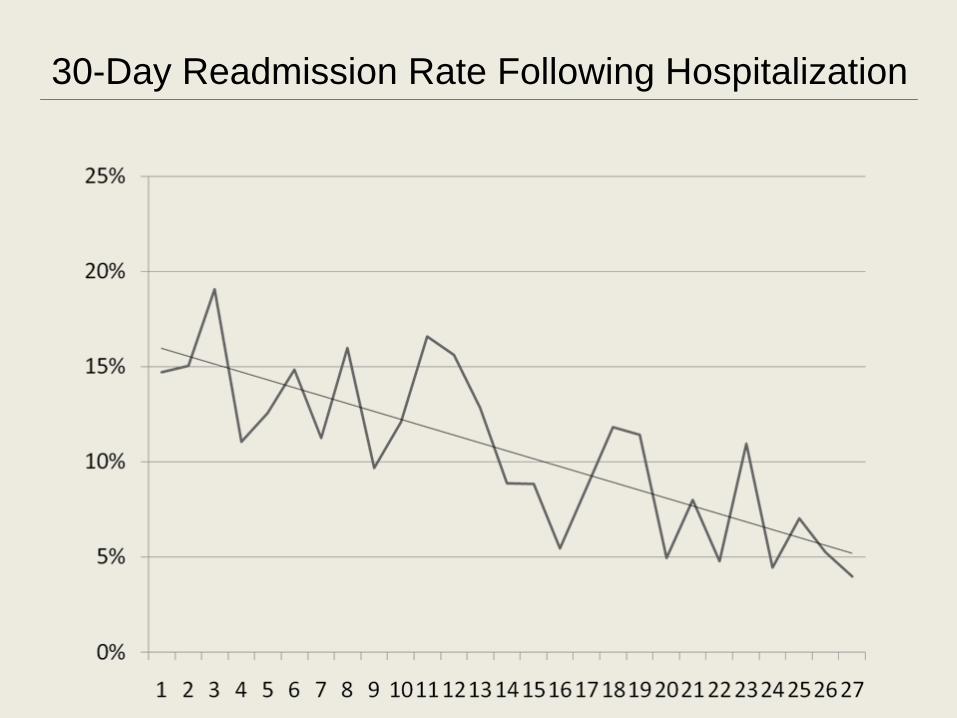

30-Day Readmission Rate Following Hospitalization

Colorado Medicaid PerspectiveColorado Medicaid Perspective

Sandeep Wadhwa, MD, MBAMedicaid Director

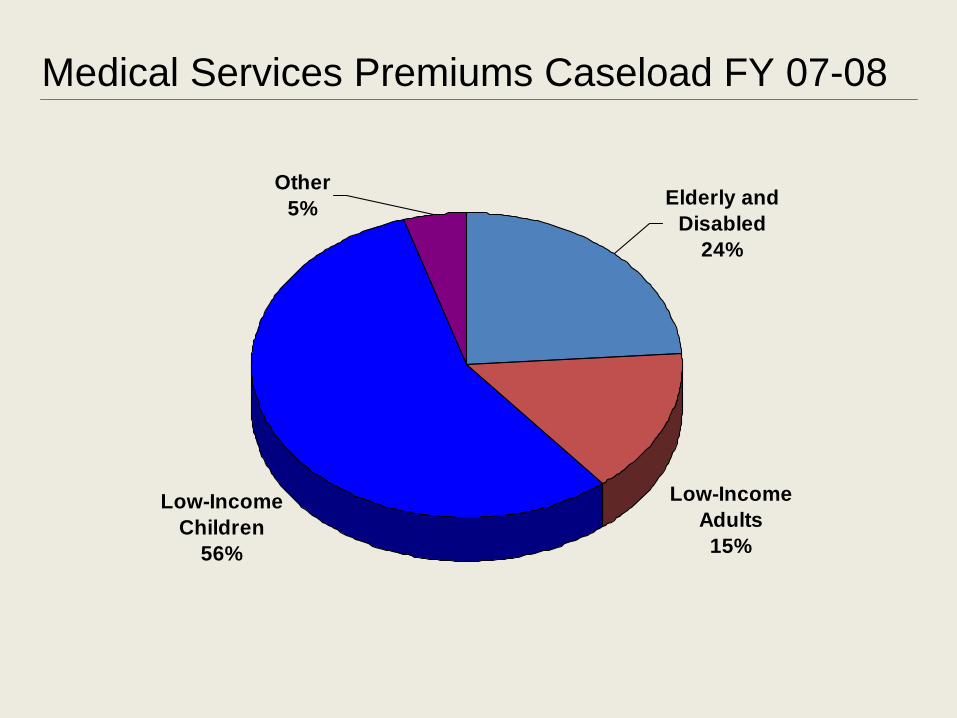

Medical Services Premiums Caseload FY 07-08

Other5% Elderly and

Disabled24%

Low-Income Adults15%

Low-Income Children

56%

Medical Services Premiums Expenditure FY 07-08

Other3%

Elderly and Disabled

66%

Low-Income Adults12%

Low-Income Children

19%

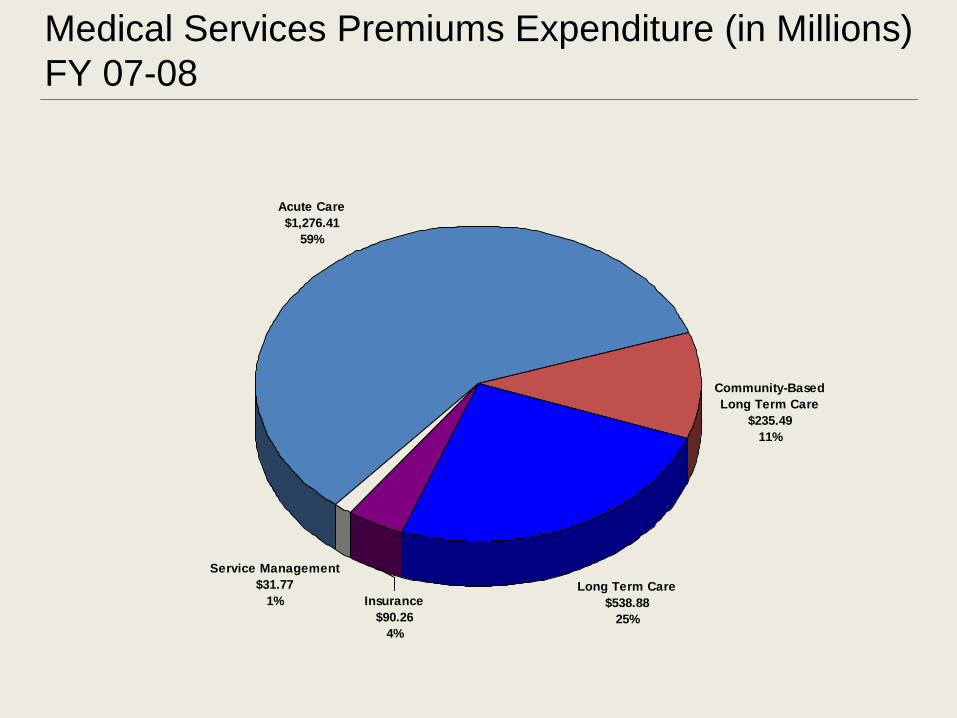

Medical Services Premiums Expenditure (in Millions) FY 07-08

Service Management$31.77

1% Insurance$90.26

4%

Acute Care$1,276.41

59%

Community-Based Long Term Care

$235.49 11%

Long Term Care$538.88

25%

Medical Home• Provide a Medical Home for over

270,000 children enrolled in Medicaid and CHP+ within three years

• Develop reimbursement methodology for Medical Home providers

Medical Homes• Created a pilot program

involving 11,000 children that provides continuous, comprehensive and accessible medical and non-medical care

Disease Management ProgramsImplemented disease management programs to serve approximately 6,000 clients•Heart disease•Lung disease•Weight management•High-risk pregnancy•Diabetes

Care Management• Piloting new integrated care

management model for Medicaid disabled individuals with multiple, chronic conditions with a fully capitated PMPM

CORHIO• Participate in funding Colorado

Regional Health Information Organization (CORHIO)

Value in Health Care• Lead the Center for Improving Value

in Health Care

Thank You!

David Gorstein MDJames L. Dooley & Associates, Inc.266 W. Coleman Blvd., Suite 102Mt. Pleasant, SC 29464877-434-6837 x19843-856-0547 [email protected]

http://www.theheadhunter.com/contents/mrinetwor kjobs.php