Embed Size (px)

Citation preview

Innovation Clusters: Understanding Life Cycles

Commisioned by:

BRIEFING PAPER

A BRIEFING PAPER FROM THE ECONOMIST INTELLIGENCE UNIT

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 2

ABOUT THIS REPORT

Innovation clusters: Understanding life cycles was written by The Economist Intelli-gence Unit. It examines the life cycles of five innovation clusters and the factors that determine success. The report is based on desk research and ten expert interviews. The case studies have been selected to cover both established and emerging mar-kets, and to explore a range of cluster success factors such as demographics and talent; infrastructure; quality of life; policy; and geography. The report was written by Michael Martins. The editor was Adam Green. The study was commissioned by Dubai Tourism.

The Economist Intelligence Unit would like to thank the following individuals (listed alphabetically) for sharing their insights and expertise during the research for this paper.

Professor Erkko Autio - Chair in Technology Venturing and Entrepreneurship, and Director of the Doctoral Programme at Imperial College London Business SchoolDr Cristina Chaminade - Professor in Innovation Studies at Lund University Dr Andrew Corbett - Professor of Entrepreneurship and Faculty Director for the John E. & Alice L. Butler Venture Accelerator, Babson CollegeDr Riccardo Crescenzi - Associate Professor of Economic Geography at the London School of EconomicsDr Luisa Gagliardi - Fellow in the London School of Economics Department of Geography and Environment, and Research Affiliate at Bocconi UniversityClif Harald - Executive Director at Boulder Economic CouncilCharlotte Holloway - Director of Policy, techUKProfessor Florian Täube - Emile Bernheim Chair of Entrepreneurship in a Global Context at Université Libre de BruxellesProfessor Tony Venables - BP Professor of Economics, Oxford UniversityProfessor Poh Kam Wong - Director of National University of Singapore’s Entrepreneurship Centre

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 3

Chapter One: Innovation clusters: Why companies are better togetherChapter Two: Silicon Roundabout, LondonChapter Three: Bangalore: Emerging market-makers?Chapter Four: From zero to hero, with a little help from government: Estonia and SingaporeChapter Five: Boulder, Colorado: Delivering on Quality of Life Conclusion: Innovation clusters: The ‘big 6’ success factors

Innovation clusters: Understanding life cycles

Innovation clusters are like the companies they host: they can grow rapidly at inception, peak, and eventually – if they do not adapt – they stagnate or die. There are thousands of clusters around the world, but many struggle to achieve sustainability or scalability. Sometimes, the very factors that made them successful, cause them to fail later on.

What allows clusters to combine the innovative spirit of start-ups with the resilience of established conglomerates, to extend their life cycle? Through case study evidence across five countries, and an expert interview program, the Economist Intelligence Unit explores ‘cluster life cycles’ in Silicon Roundabout (UK), Bangalore (India), Boulder (United States), Singapore, and Estonia and draws out key lessons from their experiences.

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 4

Chapter 1: Innovation clusters: Why companies are better together

Innovation is often associated with triumphant lone inventors. The likes of Thomas Edison, Louis Pasteur or Bill Gates are the central characters in this narrative. But all innovators spring out of a specific context. The environments that foster their individ-ual and collective success are very often ‘innovation clusters’: ecosystems that appear to have a magical ability to nurture the best ideas and attract the brightest talents.

Clusters emerge when a network of companies co-exists within a geographic loca-tion, allowing each of them to collaborate – and compete – in a way which delivers greater productivity gains than they would achieve in isolation. Silicon Valley is the most famous, but there are countless others, from Russia to Chile.

Clusters attract innovative people. They network, leading to the cross-pollination of ideas. Companies benefit from each other’s success: What one invents, rivals can access – think of a productivity-boosting tool like Dropbox. And what one firm invents, others can build on. Think of the ‘sharing economy’, led by trailblazers Uber and Airbnb, in turn giving rise to an army of start-ups taking the same idea to new applications.

Yet for all their benefits, innovation clusters are not straightforward to build – and many do not last. To prosper, clusters need six key success factors: skills and talent, accommodating policy frameworks, infrastructure, low costs (especially in the early stages), a good lifestyle offering to draw talent, and finally - good luck, whether ge-ography (proximity to key markets), historical accidents or even serendipity.

These six factors are necessary conditions, although they are not sufficient. Many places in the world lay claim to these six, but never give rise to a successful cluster. These factors are best seen as the necessary conditions for clusters, but not – on their own – sufficient. Cluster success depends both on individual factors, but also the interplay between them. Good universities are little use if there is no connectivity with industry. A high standard of living is not helpful if immigration policies prevent global talent from moving to the cluster. This paper explores the six success factors, and assesses how they change over the life cycle of a cluster.

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 5

Chapter 2: ‘Silicon Roundabout’, London

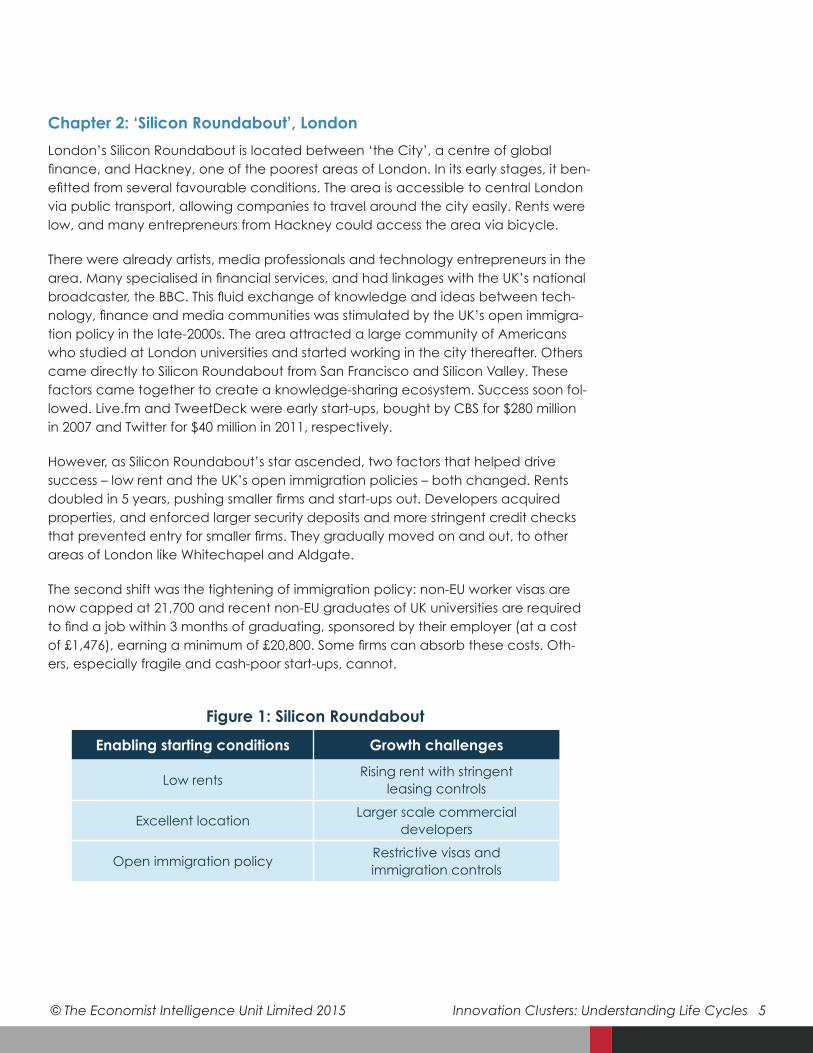

London’s Silicon Roundabout is located between ‘the City’, a centre of global finance, and Hackney, one of the poorest areas of London. In its early stages, it ben-efitted from several favourable conditions. The area is accessible to central London via public transport, allowing companies to travel around the city easily. Rents were low, and many entrepreneurs from Hackney could access the area via bicycle.

There were already artists, media professionals and technology entrepreneurs in the area. Many specialised in financial services, and had linkages with the UK’s national broadcaster, the BBC. This fluid exchange of knowledge and ideas between tech-nology, finance and media communities was stimulated by the UK’s open immigra-tion policy in the late-2000s. The area attracted a large community of Americans who studied at London universities and started working in the city thereafter. Others came directly to Silicon Roundabout from San Francisco and Silicon Valley. These factors came together to create a knowledge-sharing ecosystem. Success soon fol-lowed. Live.fm and TweetDeck were early start-ups, bought by CBS for $280 million in 2007 and Twitter for $40 million in 2011, respectively.

However, as Silicon Roundabout’s star ascended, two factors that helped drive success – low rent and the UK’s open immigration policies – both changed. Rents doubled in 5 years, pushing smaller firms and start-ups out. Developers acquired properties, and enforced larger security deposits and more stringent credit checks that prevented entry for smaller firms. They gradually moved on and out, to other areas of London like Whitechapel and Aldgate.

The second shift was the tightening of immigration policy: non-EU worker visas are now capped at 21,700 and recent non-EU graduates of UK universities are required to find a job within 3 months of graduating, sponsored by their employer (at a cost of £1,476), earning a minimum of £20,800. Some firms can absorb these costs. Oth-ers, especially fragile and cash-poor start-ups, cannot.

Enabling starting conditions Growth challenges

Low rentsRising rent with stringent

leasing controls

Excellent locationLarger scale commercial

developers

Open immigration policyRestrictive visas and immigration controls

Figure 1: Silicon Roundabout

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 6

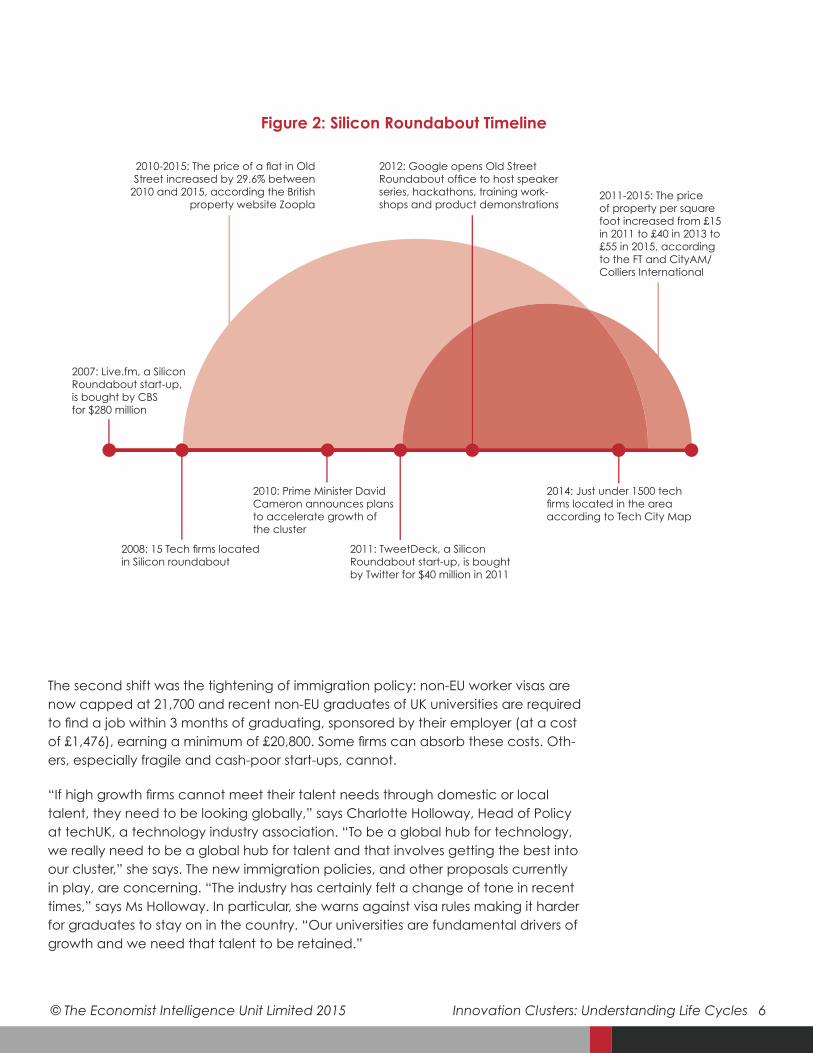

The second shift was the tightening of immigration policy: non-EU worker visas are now capped at 21,700 and recent non-EU graduates of UK universities are required to find a job within 3 months of graduating, sponsored by their employer (at a cost of £1,476), earning a minimum of £20,800. Some firms can absorb these costs. Oth-ers, especially fragile and cash-poor start-ups, cannot.

“If high growth firms cannot meet their talent needs through domestic or local talent, they need to be looking globally,” says Charlotte Holloway, Head of Policy at techUK, a technology industry association. “To be a global hub for technology, we really need to be a global hub for talent and that involves getting the best into our cluster,” she says. The new immigration policies, and other proposals currently in play, are concerning. “The industry has certainly felt a change of tone in recent times,” says Ms Holloway. In particular, she warns against visa rules making it harder for graduates to stay on in the country. “Our universities are fundamental drivers of growth and we need that talent to be retained.”

Figure 2: Silicon Roundabout Timeline

2007: Live.fm, a Silicon Roundabout start-up, is bought by CBS for $280 million

2010-2015: The price of a flat in Old Street increased by 29.6% between

2010 and 2015, according the British property website Zoopla

2008: 15 Tech firms located in Silicon roundabout

2010: Prime Minister David Cameron announces plans to accelerate growth of the cluster

2011: TweetDeck, a Silicon Roundabout start-up, is bought by Twitter for $40 million in 2011

2012: Google opens Old Street Roundabout office to host speaker series, hackathons, training work-shops and product demonstrations

2014: Just under 1500 tech firms located in the area according to Tech City Map

2011-2015: The price of property per square foot increased from £15 in 2011 to £40 in 2013 to £55 in 2015, according to the FT and CityAM/Colliers International

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 7

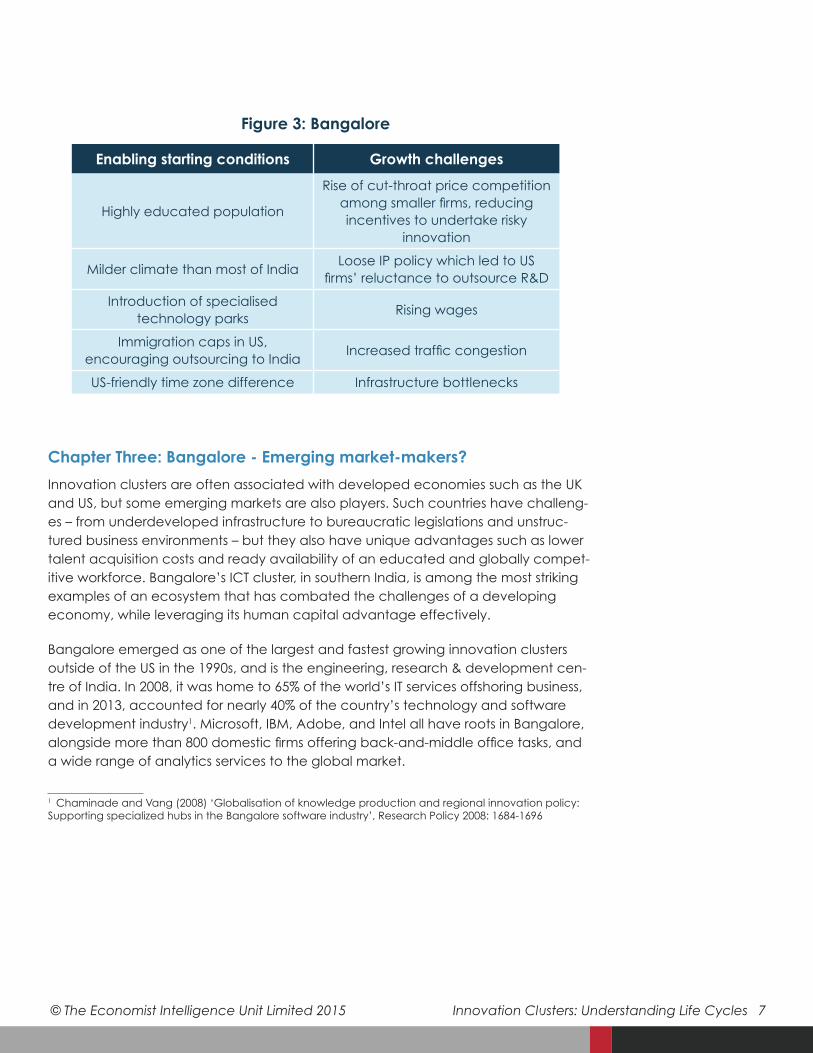

Chapter Three: Bangalore - Emerging market-makers?

Innovation clusters are often associated with developed economies such as the UK and US, but some emerging markets are also players. Such countries have challeng-es – from underdeveloped infrastructure to bureaucratic legislations and unstruc-tured business environments – but they also have unique advantages such as lower talent acquisition costs and ready availability of an edu cated and globally compet-itive workforce. Bangalore’s ICT cluster, in southern India, is among the most striking examples of an ecosystem that has combated the challenges of a developing economy, while leveraging its human capital advantage effectively.

Bangalore emerged as one of the largest and fastest growing innovation clusters outside of the US in the 1990s, and is the engineering, research & development cen-tre of India. In 2008, it was home to 65% of the world’s IT services offshoring business, and in 2013, accounted for nearly 40% of the country’s technology and software development industry1. Microsoft, IBM, Adobe, and Intel all have roots in Bangalore, alongside more than 800 domestic firms offering back-and-middle office tasks, and a wide range of analytics services to the global market.

1 Chaminade and Vang (2008) ‘Globalisation of knowledge production and regional innovation policy: Supporting specialized hubs in the Bangalore software industry’, Research Policy 2008: 1684-1696

Enabling starting conditions Growth challenges

Highly educated population

Rise of cut-throat price competition among smaller firms, reducing incentives to undertake risky

innovation

Milder climate than most of IndiaLoose IP policy which led to US

firms’ reluctance to outsource R&D

Introduction of specialised technology parks

Rising wages

Immigration caps in US, encouraging outsourcing to India

Increased traffic congestion

US-friendly time zone difference Infrastructure bottlenecks

Figure 3: Bangalore

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 8

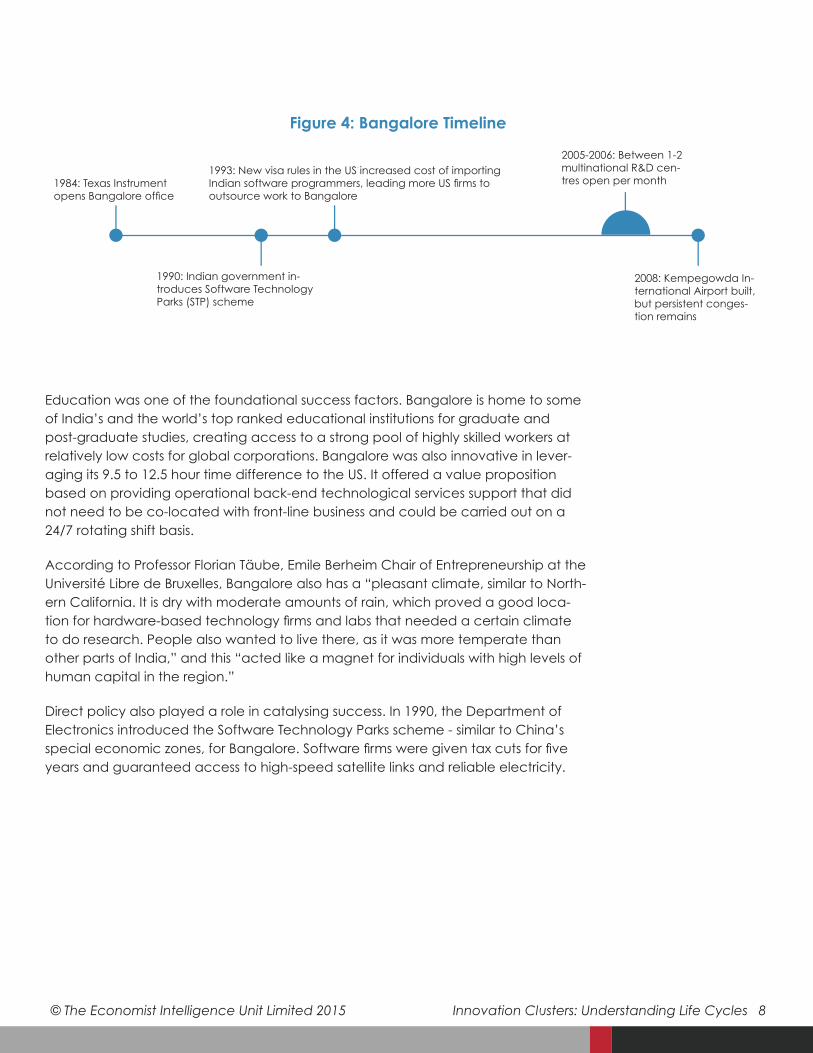

Education was one of the foundational success factors. Bangalore is home to some of India’s and the world’s top ranked educational institutions for graduate and post-graduate studies, creating access to a strong pool of highly skilled workers at relatively low costs for global corporations. Bangalore was also innovative in lever-aging its 9.5 to 12.5 hour time difference to the US. It offered a value proposition based on providing operational back-end technological services support that did not need to be co-located with front-line business and could be carried out on a 24/7 rotating shift basis.

According to Professor Florian Täube, Emile Berheim Chair of Entrepreneurship at the Université Libre de Bruxelles, Bangalore also has a “pleasant climate, similar to North-ern California. It is dry with moderate amounts of rain, which proved a good loca-tion for hardware-based technology firms and labs that needed a certain climate to do research. People also wanted to live there, as it was more temperate than other parts of India,” and this “acted like a magnet for individuals with high levels of human capital in the region.”

Direct policy also played a role in catalysing success. In 1990, the Department of Electronics introduced the Software Technology Parks scheme - similar to China’s special economic zones, for Bangalore. Software firms were given tax cuts for five years and guaranteed access to high-speed satellite links and reliable electricity.

Figure 4: Bangalore Timeline

1984: Texas Instrument opens Bangalore office

1990: Indian government in-troduces Software Technology Parks (STP) scheme

1993: New visa rules in the US increased cost of importing Indian software programmers, leading more US firms to outsource work to Bangalore

2005-2006: Between 1-2 multinational R&D cen-tres open per month

2008: Kempegowda In-ternational Airport built, but persistent conges-tion remains

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 9

US-based technology firms began offshoring to Bangalore, incentivising local SMEs to specialise in services like coding. Initially, this often meant importing Indian pro-grammers to the US to provide maintenance. However, in 1993, the US made it more difficult to obtain non-immigrant visas. This led US firms to outsource work back to Bangalore. Indian firms quickly adapted to the requirements of US firms, for example punctual delivery and product quality. Some Indian firms developed reputations as reliable suppliers in the US market, such as Infosys. Over time, the US-India relation-ship evolved yet further. Once US firms saw the quality of top tier Indian companies, they began to outsource internal R&D tasks.

However, Bangalore has run into its own problems over time. Its ability to climb the value chain has been inhibited by India’s loose stance on intellectual property protection – foreign firms have been increasingly reluctant to outsource much R&D. Many of Bangalore’s companies still provide standardised services and, because there are now so many firms, multinationals have little incentive to create a long-term relationship with any single supplier.

The mushrooming of companies has also led to a problem of ‘over-competition’. As of today, the top 20 Indian software exporters account for over 50% of total exports, leaving over 800 firms with the rest of the market. Competition is fierce among the bottom 800, leading to a lack of collaboration. Because competition is so aggres-sive, firms instil in their employees a culture of “get it right the first time.” This ensures customer satisfaction, but low levels of experimentation and risk-taking. As a result, Bangalore is finding it difficult to climb the value chain.

Bangalore’s success has also created cost inflation due to rising wages, and con-gestion has increased. Infrastructure projects have been difficult to implement rela-tive to China, one of India’s main global competitors. Even Bangalore’s new airport, built in 2008, cannot relieve the traffic that makes the two main technology parks inaccessible during the day, according to Cristina Chaminade, professor of innova-tion studies at Lund University. Taken together, cost increases, low R&D outsourcing and congestion all show the need for Bangalore to evolve if it wants to stay ahead.

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 10

Chapter Four: From zero to hero – with a little help from government

For Bangalore and Silicon Roundabout, policy decisions over IP and immigration arguably harmed their cluster’s evolution. But the government is not always an ob-stacle. It can, through smart interventions, allow clusters to flourish.

Despite being a small country of just 1.3 million people, Estonia has produced one of the most epic technological disrupters of the modern era: Skype. The government’s actions over the last 20 years sowed the seeds for this success and others.

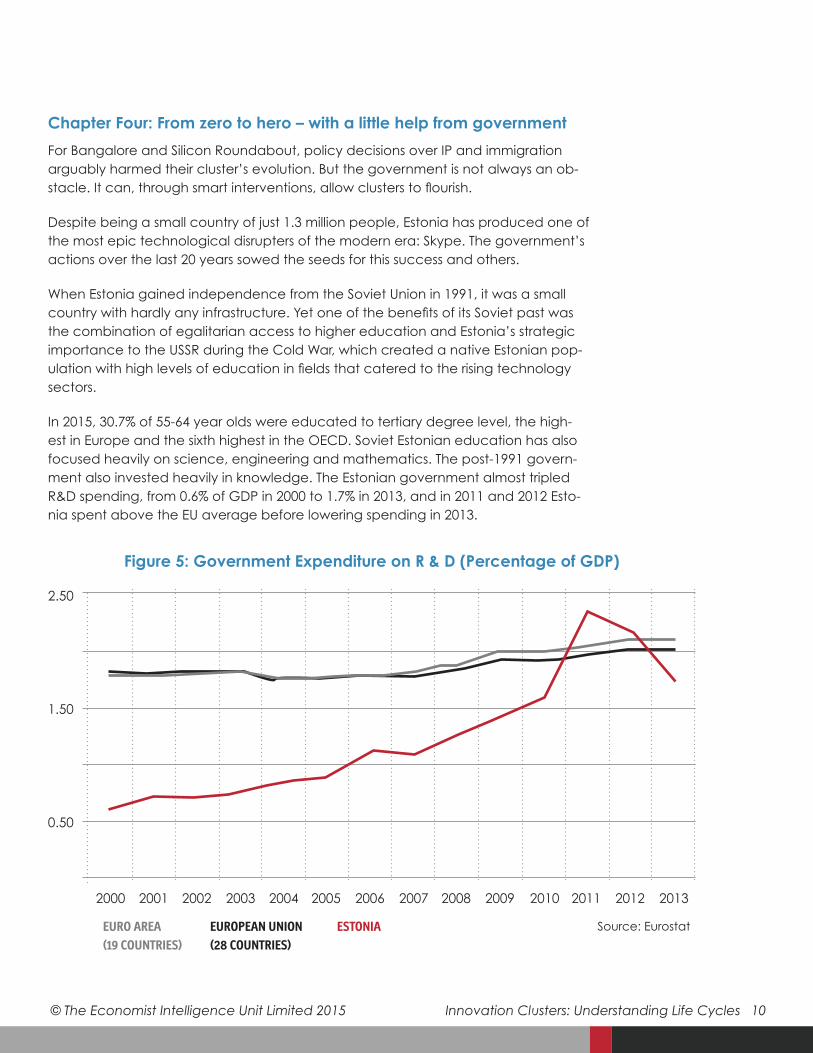

When Estonia gained independence from the Soviet Union in 1991, it was a small country with hardly any infrastructure. Yet one of the benefits of its Soviet past was the combination of egalitarian access to higher education and Estonia’s strategic importance to the USSR during the Cold War, which created a native Estonian pop-ulation with high levels of education in fields that catered to the rising technology sectors.

In 2015, 30.7% of 55-64 year olds were educated to tertiary degree level, the high-est in Europe and the sixth highest in the OECD. Soviet Estonian education has also focused heavily on science, engineering and mathematics. The post-1991 govern-ment also invested heavily in knowledge. The Estonian government almost tripled R&D spending, from 0.6% of GDP in 2000 to 1.7% in 2013, and in 2011 and 2012 Esto-nia spent above the EU average before lowering spending in 2013.

Figure 5: Government Expenditure on R & D (Percentage of GDP)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

0.50

1.50

2.50

EUROPEAN UNION (28 COUNTRIES)

Source: EurostatEURO AREA (19 COUNTRIES)

ESTONIA

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 11

The Estonian government did not just develop skills – it also invested in digital tech-nology for public services, creating a population of ‘digital natives’. Milestones include the 2005 internet-based general elections, and the issuance of electronic identity cards. The e-ID card proved a more secure identification system for banks and other private sector agents to use. Uptake increased as e-cards came to be used for purchasing bus tickets, paying bills, renewing medical prescriptions online and much more.

Digital public services, combined with a well-educated and tech-savvy population, made Estonia a fertile ground for innovation. Indeed, the country’s high ICT pene-tration - the percentage of the population with Internet access increased from 0.3% in 1993 to 80% in 2013 - left Estonia exposed to cyber-crime, which led entrepreneurs to explore new ways to boost security. The video linkage program Skype and file sharing program Kazaa were both produced and scaled by Estonians by utilising security-related technology. Estonia is thus a good example of how government in-vestment in the broader innovation ecosystem – spanning education, digital service delivery and R&D spending – can catalyse clusters.

Singapore: Built from scratch

Like Estonia, Singapore is an emerging market whose government has a pro-innova-tion agenda. Singapore was an agrarian society when it became independent in 1965. A tropical island with few natural resources, a lack of fresh water, rapid popu-lation growth and domestic ethnic and religious conflict, as well as hostilities in the broader region, it hardly had an auspicious start.

Since then, the country has focused with laser-like precision on becoming as eco-nomically powerful as possible, as fast as possible. Singapore established itself first as a centre for low-cost manufacturing and later on electronics and, more recently, life sciences. Its innovation credentials have strengthened since the early 2000s in particular, and it is now a world-leading centre in areas such as biotechnology.

Its strengths as an innovation cluster are down to three factors: talent, supportive government policy, and direct public investment. The first is the result of a major and sustained public commitment to education. From a very low base, Singapore now ranks consistently at or near the top of most major world education ranking systems over the last decade according to the OECDw2. The strategy started with the ‘build-ing’ stage of 1959-1978, which saw the rapid construction of schools, mass teacher recruitment and unification of a single Singaporean education system – as well as the introduction of bilingualism to bring English language skills to the population. Universal primary education was attained in 1965 and universal lower secondary by the early 1970s.

2 OECD 2010, “Strong Performers and Successful Reformers in Education: Lessons from PISA for the United States”

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 12

The second phase, from 1979 to 1996, focused on improving education quali-ty – lowering dropout rates, raising grades, and developing more practical and vocational skills. Reforms included ‘academic streaming’ to differentiate students according to their abilities, and the formation of a more diverse range of education institutions (including academic high schools, polytechnic high schools and tech-nical institutes). Singaporean students were already ranking among the best in the world in maths and science by 1995, meaning the country had ascended to the top tier in little over a generation.

In the final phase, from 1997 to the present day, the education system was further refined, for instance through allowing schools greater management autonomy and more nuanced accountability models. More recently, the tertiary education system has come to play a greater role in promoting the high level skills on which innova-tion depends, for instance through the building of new universities like the Singapore University of Technology and Design (in 2012). Industry-academia coordination has been strengthened by a public agency, the Biomedical Sciences Industry Partner-ship Office, whose mandate is to identify research strengths in Singapore’s univer-sities, research institutes, hospitals and medical centres, and match them with the interests of relevant companies.

Singapore city in sunset time

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 13

Due to its small population, Singapore has also looked to attract students from nearby countries through the ASEAN scholarship, which covers fees and tuition for qualified students, and the Tuition Grant Scheme (TGS) for international students, which covers up to ten semesters of tertiary education. Both schemes require that graduates remain in Singapore for up to 6 years and for 3 years, respectively. Pro-grams like the Agency for Science, Technology and Research (A*STAR) fellowship, which covers both undergraduate and graduate education, also helped attract and retain global talent. These tactics, as well as a liberal immigration policy, aided global inflows of highly skilled labour, leading to technology and skills transfer be-tween large multinationals and domestic companies.Supportive government policy has also played a role – through efforts to create an efficient and easy business environment, and direct investments. As the economy shifted to knowledge-based sectors and the skills base improved, the government sought to attract multinational companies by offering tax incentives, eliminating political corruption, and bolstering IP protection.

Supportive government policy has also played a role – through efforts to create an efficient and easy business environment, and direct investments. As the economy shifted to knowledge-based sectors and the skills base improved, the government sought to attract multinational companies by offering tax incentives, eliminating political corruption, and bolstering IP protection.

Singapore topped the World Bank’s Ease of Doing Business index in 2014 and 2015 and is a consistent top performer in multiple categories from contract enforcement and trading across borders. One of its strongest performance areas is the ease of setting up a business and carrying out processes. Simple registration procedures makes it possible to incorporate a company and register for taxes using the same online document, for instance, while digitisation has been extended to applications for construction permits and property registration. In 2015, it introduced an electron-ic litigation system to streamline proceedings.

Along with ease of business reforms, there are also grants to encourage business for-mation and start-ups, such as the ACE Start-up Grant, dedicated to newly formed, local majority-owned companies developing a differentiated business concept. The government has been a direct active investor in broader innovation infrastructures,

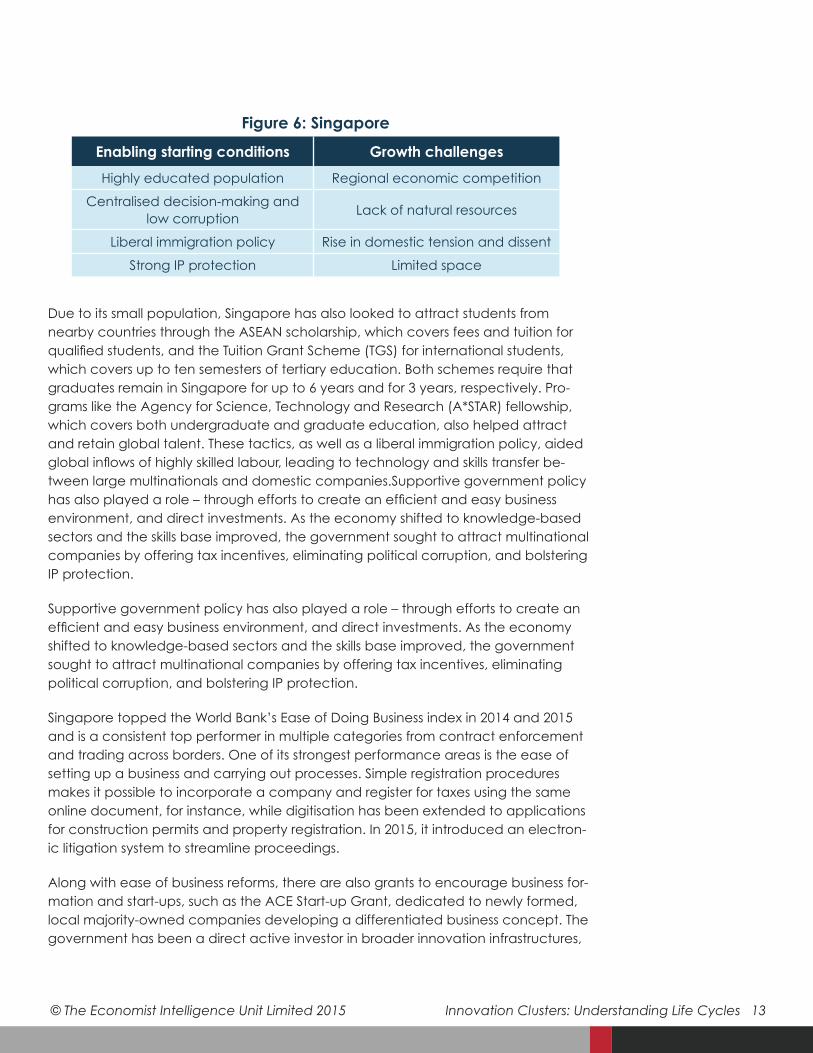

Enabling starting conditions Growth challenges

Highly educated population Regional economic competition

Centralised decision-making and low corruption

Lack of natural resources

Liberal immigration policy Rise in domestic tension and dissent

Strong IP protection Limited space

Figure 6: Singapore

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 14

too, spending around $6 billion between 2000 and 2005 in biomedical sciences in-cluding the formation of Biopolis, a biomedical research and development hub. This is perhaps Singapore’s most promising cluster.

Singapore began looking to biotechnology in the 2000s to diversify its economic base, and utilised a combination of tax holidays and incentives - such as paying up to 30% of building costs of companies undertaking basic drug research and devel-opment. Its ability to attract stem cell investment was also helped by a reduction in funding in the US due to ethical objections from the Bush administration. Singa-pore is a legally more liberal research environment, allowing a number of research practices, such as use of the early stage human embryos for therapeutic research, which is banned in other countries. Between 2008 and 2012, Singapore – along with Korea – showed the largest increase in stem cell research activity3. It also, along with Switzerland and Denmark, has an unusually high level of academic-corporate partnerships, and international collaboration. As a result, top biotechnology experts from leading establishments such as the Massachusetts Institutes of Technology, the National Cancer Institute in Maryland and the University of California 4 have come to Singapore over the last decade, citing greater funding, more organisational free-dom, a more liberal research policy, and a greater appreciation of the benefits of long term R&D.

A busy island

So far, Singapore has successfully adapted its model through each successive stage – moving from low cost manufacturing to electronics to a more diversified econo-my, positioning itself as a hub for multinationals wishing to build their Asian business-es. Nestle, Abbott Laboratories and Google are among the companies who have even set up research institutes in Singapore.

But as with all clusters and highly productive economic geographies, it faces emerging challenges – especially with regards to the workforce. While immigration brings new workers and ideas to the host country, it is not without risks. Singapore is a small island, roughly half the size of London, and two-thirds the size of Hong Kong, and is home to 5,469,700 people. The population has increased by 3% annually from 2005 to 2013, according to the World Bank, and population density, measured as the number of people per square kilometer, has increased 27.7% between 2000 and 2013, according to Singstat, the Singaporean statistical agency.

As the population has increased, so has the number of immigrants, more than doubling between 2000 and 2014. The strain on public services, and competition for space, has combined with ever-growing demand for housing, increasing property prices and prompting domestic dissent, according to Dr Poh Kan Wong, Director of National University of Singapore’s Entrepreneurship Centre.

3 http://www.eurostemcell.org/files/ “Stem cell research: Trends and Perspectives on the evolving interna-tional landscape”4 “Singapore Acts as Haven for Stem Cell Research”, New York Times, August 17 2006

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 15

Dr Wong argues that foreign immigration has perhaps reached a critical mass where enclaves of foreigners are starting to form, reducing assimilation and integra-tion, in turn undermining the idea of a ’Singaporean identity’. At the same time, poli-cy makers know that they are in a race for global talent and must remain open to highly skilled labour. As a result, the governing party has started focusing on filtering immigration, attracting highly skilled immigrants that can contribute to Singapore on the global value chain through knowledge and technology transfer, while making it more difficult for lower skilled immigrants to settle. As with all clusters, Singapore’s success created its own new problems, which the city state has to adapt to.

Chapter Five: Boulder, Colorado: Delivering on Quality of Life

A pro-business climate might attract companies– but on its own, it is not enough to attract highly skilled workers. Smart people aren’t just interested in work: they also care about their surroundings, quality of schools and hospitals, leisure and entertain-ment and a host of other lifestyle factors. In Hong Kong, for example, the SAR gov-ernment built ‘Cyberport’, a large campus where entrepreneurs could rent cheap office space and collaborate, but this cluster failed due to its distance from the city centre where people wanted to live and work.

Lifestyle factors have certainly been contributors to the historical evolution of Boul-der in Colorado, US. Boulder is a small town (population 102,760 in July 2013) that punches above its weight as an innovation hub. From 2009 to 2013, there were 10.20 patents per 1,000 residents, the fifth highest in the US, after San Jose, California, and above San Francisco5. It is home to clusters of aerospace companies like Ball Aero-space and Technologies Corporation, one of the top 100 defence contractors in the world, and biosciences companies like Covidien.

Part of Boulder’s cluster evolution is “thanks to large corporations, a university, and publicly-funded technical research organisations locating in Boulder in the past, which led to a large number of firm spin-offs,” according to Dr Andrew Corbett, Professor of Entrepreneurship at Babson College in Massachusetts. In 1965 IBM es-tablished an office, and four years later a group of technicians left to found Storag-eTek. Throughout the years, both companies downsized, leaving many highly skilled people with roots in the local area. They founded companies that either still exist or served as the incubators for later firms. Much of this talent pool had affiliations and linkages with government research organisations in the area6.

But in addition to historical happenstance, Boulder’s success is also integrally linked to its high performance on liveability metrics, particularly in light of competition from

5 Courtney Miller, ‘America’s Most Innovative Tech Hubs’, NerdWallet, 9 February 2015.6 Namely the University of Colorado Boulder, the US Air Force Academy, the Cooperative Institute for Research in Environmental Sciences (CIRES), the Joint Institute for Lab Astrophysics (JILA), the Laboratory for Atmospheric and Space Physics (LASP), the National Ecological Observatory Network (NEON), the National Oceanic and Atmospheric Administration (NOAA), the National Institute of Standards and Tech-nology (NIST), the National Telecommunications and Information Administration (NTIA), the University Cor-poration for Atmospheric Research (UCAR), and the National Center for Atmospheric Research (NCAR).

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 16

the strong well-developed clusters in other parts of the US. Boulder’s proximity to the Rocky Mountains, its parks and outdoor activities, and cultural and public amenities like art galleries and highly ranked public schools, make for a good overall quality of life. Both the government of Boulder and Boulder’s private sector place emphasis on skills attraction and retention because “it is the skills, the talent, and the expertise that is attracting the world-class scientists, engineers, entrepreneurs, the companies and investment that are fuelling Boulder’s economy,” according to Clif Harald, Ex-ecutive Director of Boulder Economic Council.

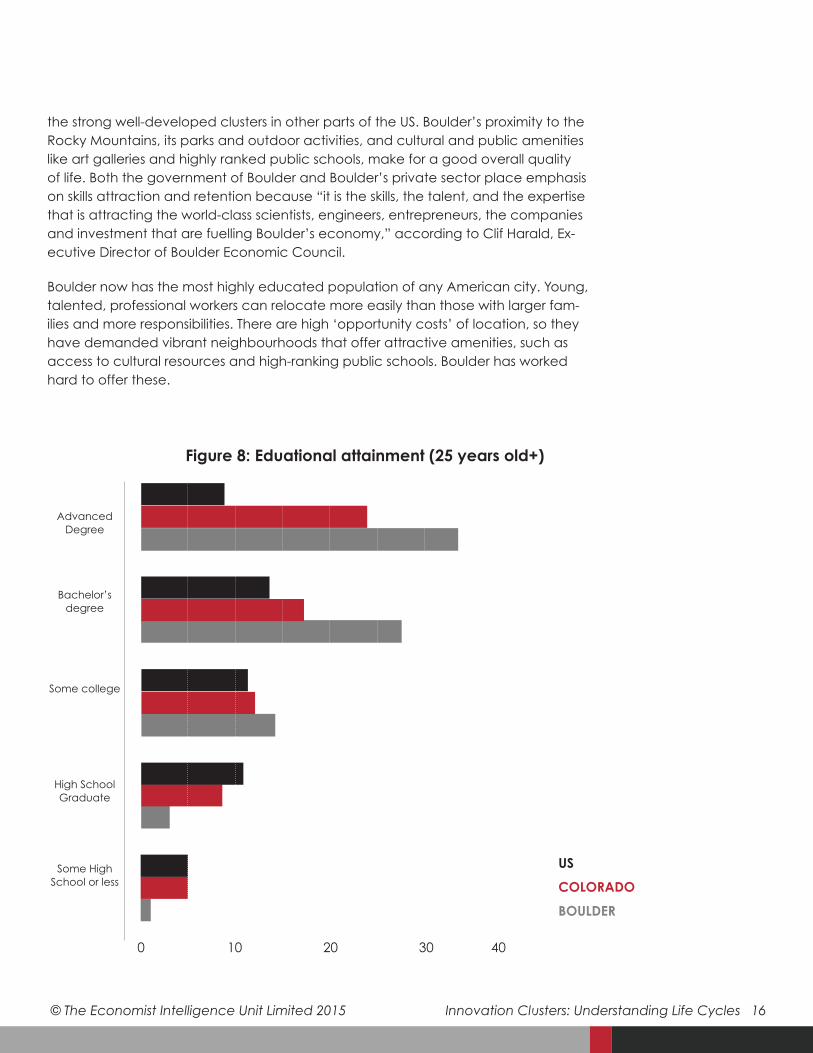

Boulder now has the most highly educated population of any American city. Young, talented, professional workers can relocate more easily than those with larger fam-ilies and more responsibilities. There are high ‘opportunity costs’ of location, so they have demanded vibrant neighbourhoods that offer attractive amenities, such as access to cultural resources and high-ranking public schools. Boulder has worked hard to offer these.

Figure 8: Eduational attainment (25 years old+)

0 10 20 30 40

BOULDER

COLORADO

USSome High School or less

High School Graduate

Some college

Bachelor’s degree

Advanced Degree

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 17

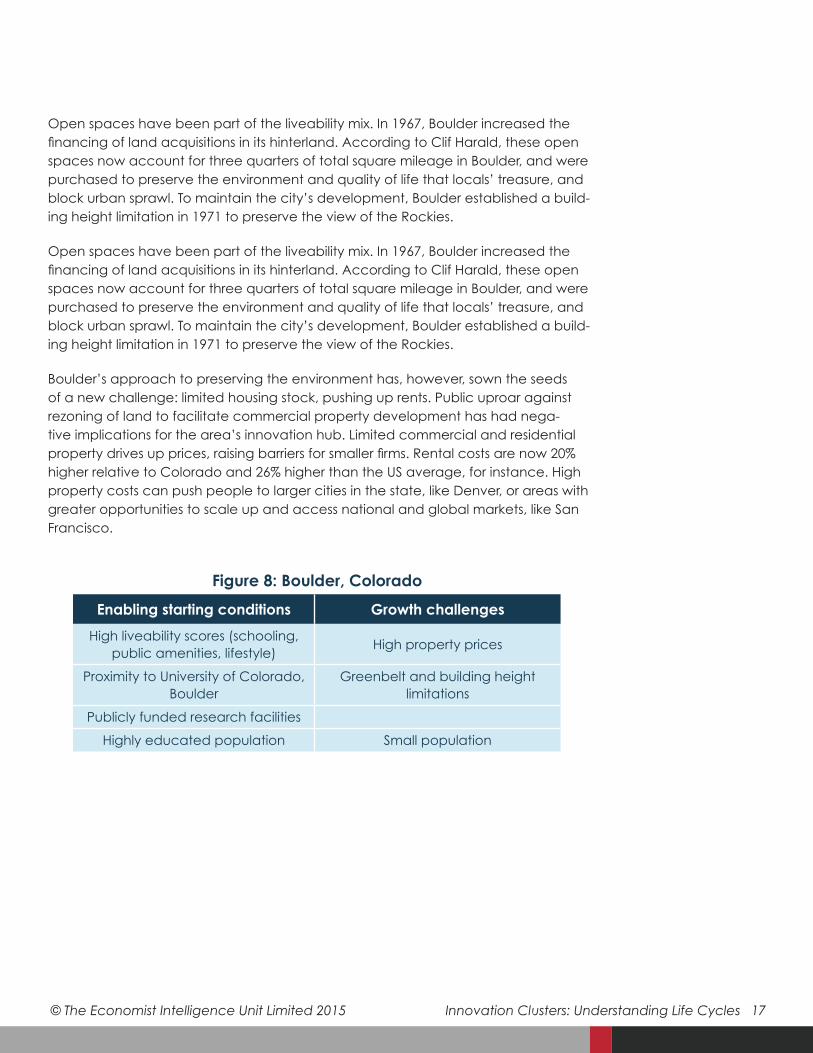

Open spaces have been part of the liveability mix. In 1967, Boulder increased the financing of land acquisitions in its hinterland. According to Clif Harald, these open spaces now account for three quarters of total square mileage in Boulder, and were purchased to preserve the environment and quality of life that locals’ treasure, and block urban sprawl. To maintain the city’s development, Boulder established a build-ing height limitation in 1971 to preserve the view of the Rockies.

Open spaces have been part of the liveability mix. In 1967, Boulder increased the financing of land acquisitions in its hinterland. According to Clif Harald, these open spaces now account for three quarters of total square mileage in Boulder, and were purchased to preserve the environment and quality of life that locals’ treasure, and block urban sprawl. To maintain the city’s development, Boulder established a build-ing height limitation in 1971 to preserve the view of the Rockies.

Boulder’s approach to preserving the environment has, however, sown the seeds of a new challenge: limited housing stock, pushing up rents. Public uproar against rezoning of land to facilitate commercial property development has had nega-tive implications for the area’s innovation hub. Limited commercial and residential property drives up prices, raising barriers for smaller firms. Rental costs are now 20% higher relative to Colorado and 26% higher than the US average, for instance. High property costs can push people to larger cities in the state, like Denver, or areas with greater opportunities to scale up and access national and global markets, like San Francisco.

Enabling starting conditions Growth challenges

High liveability scores (schooling, public amenities, lifestyle)

High property prices

Proximity to University of Colorado, Boulder

Greenbelt and building height limitations

Publicly funded research facilities

Highly educated population Small population

Figure 8: Boulder, Colorado

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 18

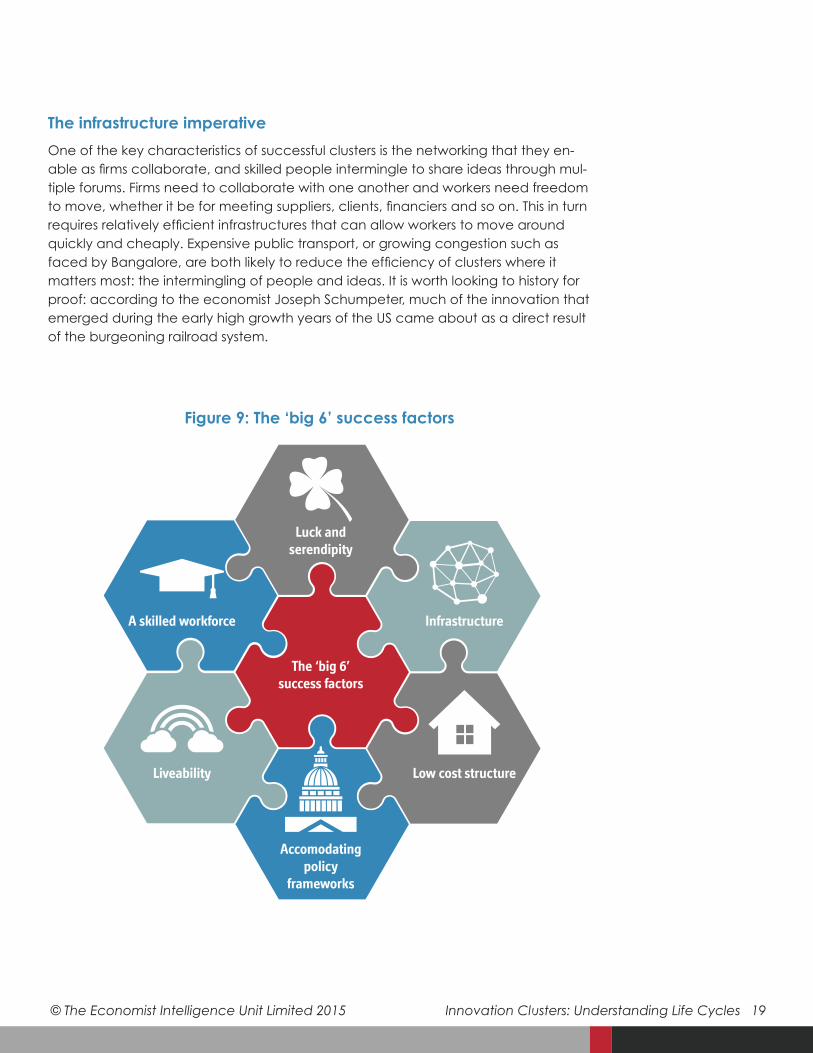

Innovation clusters: The ‘big 6’ success factors

Innovation clusters are crucial laboratories in which novel tools, technologies and techniques are created and applied. But they are not just the ‘background’ to inno-vation; they are living organisms integral to everything that happens within their ‘walls’.

No two clusters are the same – and there can be no hard and fast ‘formula’ for what makes clusters work. But these case studies do point towards six broad prin-ciples necessary for laying the groundwork for success. While the case studies explored in this paper are distinctive in terms of their sectors, their histories and the types of innovation they have fostered, these factors have played a catalytic role in their success.

A skilled workforce

All successful clusters, both in this study and the many others published on the topic, have a marked edge when it comes to human capital, either local or imported. This highly skilled workforce has emerged and manifested in several ways. A dense net-work of top tier higher education establishments has been critical to the success of Silicon Roundabout in London, Boulder in Colorado and Bangalore. Estonia lacked this kind of university network, but compensated for it by having a highly educated population thanks to the country’s fairly egalitarian access to education historically, buttressed by the government’s eagerness to promote digital skills in the population. Singapore, with a small population, leveraged both its national academic institu-tions along with a talent attraction strategy and a solid business environment – both of which have given it a strong national workforce whether indigenous or expa-triate. While natural resources have supported the emergence of some clusters in history, they are knowledge-intensive phenomena and thus skills enhancement with a diversified global workforce are key ingredients.

Accommodating policy frameworks

Governments have a relevant role to play in promoting clusters, but their interven-tions just as often prevent success as cultivating it. Evidence from this study suggests the best interventions for government are not necessarily fiscal and taxation policies related specifically to a cluster, but rather interventions which support the broader inputs that clusters depend on such as education, infrastructure and connectivity. More importantly, governments must carefully weigh the impact of other policy changes, such as migration caps or visa restrictions, on their national clusters’ ac-cess to talent. The best practice principle is for government to invest in the funda-mentals and continuously evolve the nature of its intervention based on the needs of the growing cluster, and leave the specifics of the innovation cluster process to the companies and innovators themselves.

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 19

The infrastructure imperative

One of the key characteristics of successful clusters is the networking that they en-able as firms collaborate, and skilled people intermingle to share ideas through mul-tiple forums. Firms need to collaborate with one another and workers need freedom to move, whether it be for meeting suppliers, clients, financiers and so on. This in turn requires relatively efficient infrastructures that can allow workers to move around quickly and cheaply. Expensive public transport, or growing congestion such as faced by Bangalore, are both likely to reduce the efficiency of clusters where it matters most: the intermingling of people and ideas. It is worth looking to history for proof: according to the economist Joseph Schumpeter, much of the innovation that emerged during the early high growth years of the US came about as a direct result of the burgeoning railroad system.

A skilled workforce

Liveability

Accomodating policy

frameworks

Luck and serendipity

Infrastructure

Low cost structure

The ‘big 6’ success factors

Figure 9: The ‘big 6’ success factors

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 20

Luck and serendipity

Sadly for planners, luck and serendipity play a key role in determining the success of clusters. By luck, we refer to all of those dynamics which could not have been brought about with foresight or purpose, but which – having existed – came to ca-talyse innovation. Historical luck is one example. Estonia’s past position in relation to the USSR had two impacts on its later technological success: high levels of educa-tion, especially in maths and engineering, due to a relatively egalitarian education system, and a continuing cyber security threat in more recent years that impelled innovation. Boulder built on the decision of large technology companies to locate there in the distant past that set up a process of talent circulation leading to spinoffs who became innovators more recently.

Geography is also a ‘luck’ factor, especially in terms of positioning a cluster close to key markets. While not a case study in this project, Costa Rica is a good example of a country whose life sciences cluster has benefited considerably from its proximity to US markets. But crucially, luck does not mean there is no role for human decisions. Companies and governments must consciously recognise the benefits that such happenstance occurrences provide, and build on them systematically to create a competitive positioning. There are plenty of countries that were formerly part of the USSR, and are still closely located to Russia, that did not build on that as Estonia has. Similarly, there are many countries in Central America with proximity to the US, but who have not carved out a life sciences cluster such as Costa Rica.

Low cost structure

Low operating costs, especially rents on commercial property, have been essen-tial drivers of a cluster’s success in the early start up phases. This applies to rental of office space but also the residential needs of the cluster’s workers. Other low costs can also help, such as tax breaks on innovation related activities. Over time, low rental costs are the first to disappear – this is as near to a hard law as one can find in the field of cluster analysis. This dynamic is hard to eradicate, but can at least be offset by policy makers, for instance through fiscal incentives on innovation related activities in the cluster, or through a planning policy which allows expansion of the stock of property to moderate price rises.

Liveability

The clusters explored in this case study are generally high performers in terms of liveability, at least on relative terms compared to other cities within their countries where talented workers might otherwise choose to go. Liveability is not a specific metric and no two cities offer the same advantages. But it can cover such critical is-sues as public safety and political stability, good public amenities, culture and enter-tainment, and good schools and hospitals. These are all factors which policy makers or public institutions can influence if they want to nurture cluster success, in order to ensure their cluster appeals to those top tier skilled workers who, in the modern era more than ever before, have so many choices about where to locate themselves.

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 21

While every effort has been taken to verify the accuracy of this information, The Economist Intelligence Unit Ltd. cannot accept any responsibility or liability for reli-ance by any person on this report or any of the information, opinions or conclusions set out in this report.

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 22

Copyright

© 2015 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior permission of the Economist Group. Whilst every effort has been taken to verify the accura-cy of information presented in this document, neither The Economist Group nor its affiliates can accept any responsibility or liability for reliance by any person on this information.

Economist Intelligence Unit

The Economist Intelligence Unit (EIU) is the world’s leading resource for economic and business research, forecasting, and analysis. It provides accurate and impartial intelligence to companies, government agencies, financial institutions and academic organizations around the globe, inspiring business leaders to act with confidence since 1946.

© The Economist Intelligence Unit Limited 2015 Innovation Clusters: Understanding Life Cycles 23

LONDON 20 Cabot Square London E14 4QW United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

NEW YORK 750 Third Avenue 5th Floor New York, NY 10017, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

HONG KONG 6001, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

GENEVA Rue de l’Athénée 32 1206 Geneva Switzerland Tel: (41) 22 566 2470 Fax: (41) 22 346 9347 E-mail: [email protected]