Embed Size (px)

Citation preview

INNOVACT PLATFORMValue Chain CocoaGroup 414:00-16:30

Anna Laven5 June 2018

Creating value in the cocoa chain

3

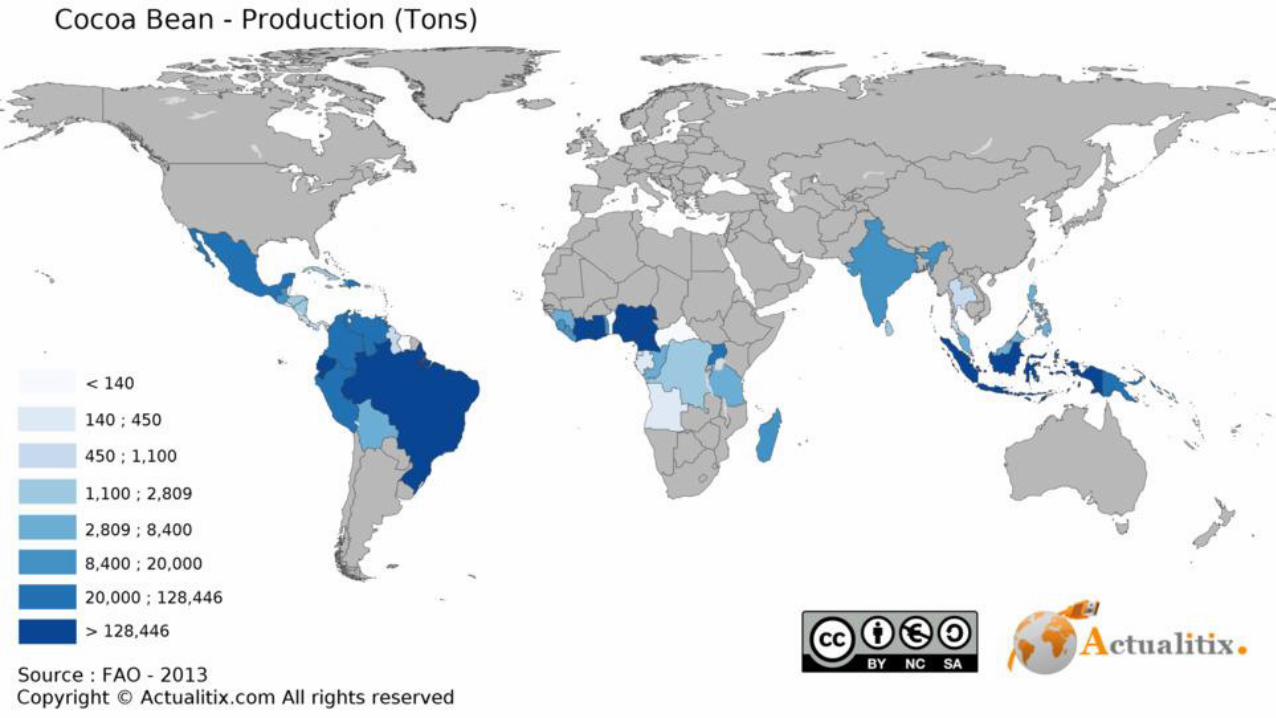

Bon: FAO

4

1

2

3 4

56

79

10

11

1

2

12

8

5

6

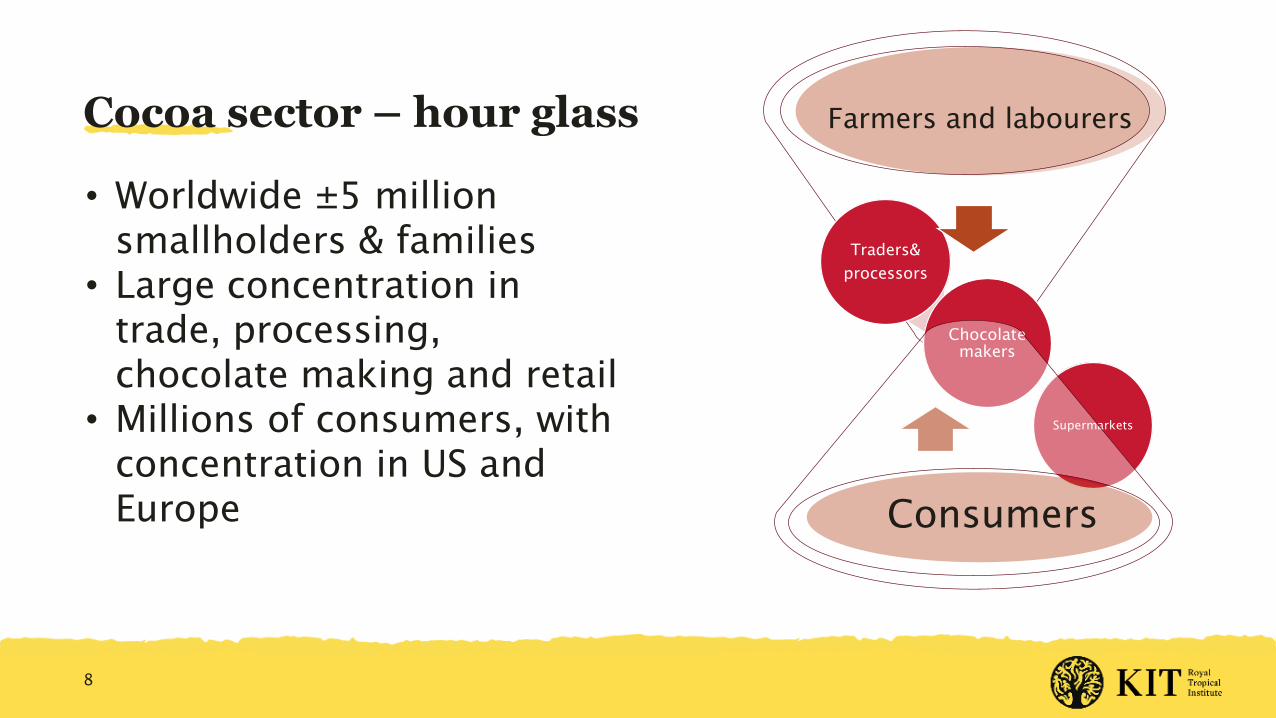

Cocoa sector – hour glass

8

Farmers and labourers

Supermarkets

Consumers

Chocolate

makers

Traders&

processors

• Worldwide ±5 million

smallholders & families

• Large concentration in

trade, processing,

chocolate making and retail

• Millions of consumers, with

concentration in US and

Europe

Worldwide commitment towards sustainability

• Sustainability has become mainstream

9

Why?

• Global, regional and local risks for supplier failure (e.g. climate change, aging farmer population,

aging trees, soil erosion, migration, deforestation, child labour…)

• Increasing role for private sector in economic development in cocoa producing countries

• Demand for (sustainable) cocoa continues to grow

• Increased competition for (sustainable) cocoa

• Active role of civil society (e.g. media – Tony Chocolonely; Oxfam – Behind the brands campaign)

• Consumer demand for sustainable and traceable cocoa grows

11

Beyond certification

• ‘Verification’

• ISO/CEN Sustainable & Traceable Cocoa - Framework

• National Sustainability Initiatives

• Origin Chocolate (direct trade)

• Quality

12

Can taste be a catalyst for sustainability?

13

Quality (taste) has been neglected in sustainability discourse Bulk market

Theory of Change: Fine flavour higher quality higher prices higher rewards for farmers

Fine flavour cocoa

• A specific origin and grade of cocoa beans of a unique flavour or colour, sought after by makers of

high quality, specialty chocolate.

Fine flavour chocolate (products)

• A high quality of cocoa beans and chocolate, with a specific taste for which a higher price is paid. It is

often combined with terms such as ‘high quality’, ‘single origin’ and/or ‘bean to bar’ chocolate. The

combination of cocoa genetics, cultivation methods, environmental conditions, post-harvest practices

and processing techniques are all contributing factors.

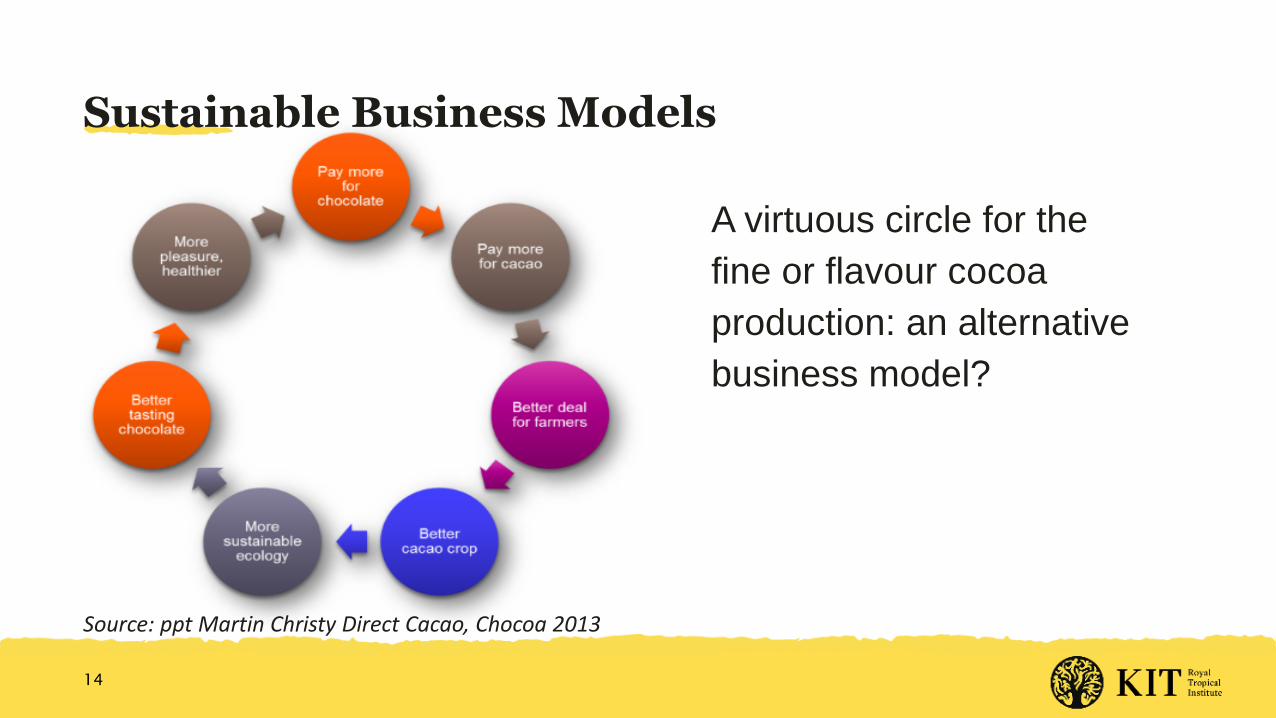

Sustainable Business Models

14

Source: ppt Martin Christy Direct Cacao, Chocoa 2013

A virtuous circle for the

fine or flavour cocoa

production: an alternative

business model?

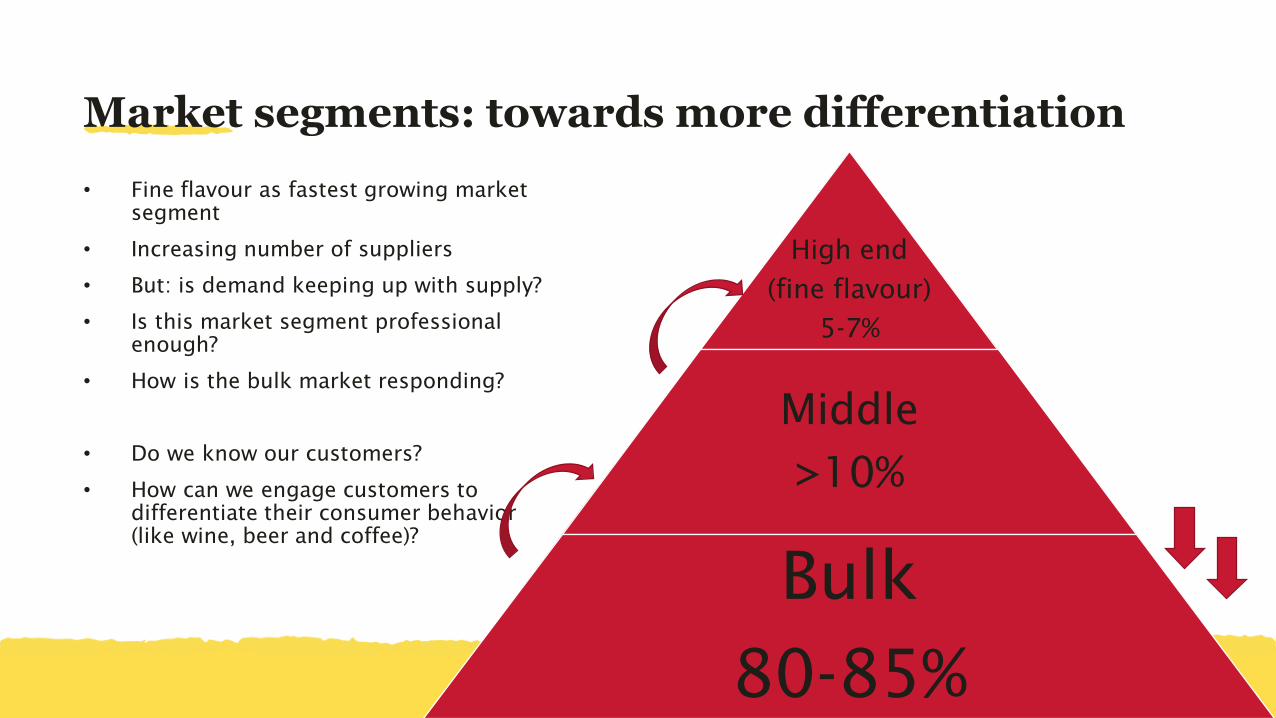

Market segments: towards more differentiation

• Fine flavour as fastest growing market

segment

• Increasing number of suppliers

• But: is demand keeping up with supply?

• Is this market segment professional

enough?

• How is the bulk market responding?

• Do we know our customers?

• How can we engage customers to

differentiate their consumer behavior

(like wine, beer and coffee)?

High end

(fine flavour)

5-7%

Middle

>10%

Bulk

80-85%

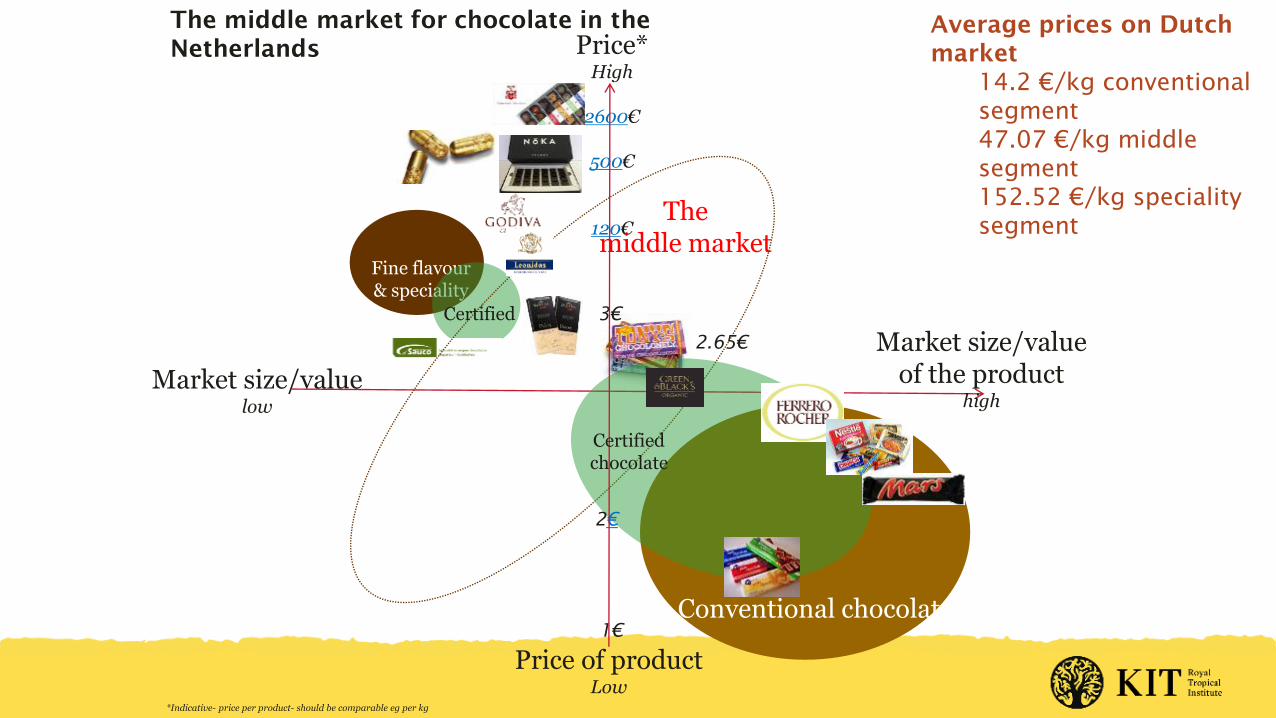

Fine flavour & speciality

Price*High

2600€

500€

120€

Market size/value of the product

highMarket size/value

low

Price of productLow

The middle market for chocolate in the

Netherlands

1€

Certified

The middle market

3€

2.65€

2€

Conventional chocolate

Certifiedchocolate

*Indicative- price per product- should be comparable eg per kg

Average prices on Dutch

market

14.2 €/kg conventional

segment

47.07 €/kg middle

segment

152.52 €/kg speciality

segment

Differences between markets & their productsConventional chocolate

products

Middle-market chocolate

products

Specialty products

Quality low medium high

Price Low Medium high

Sustainable cocoa Certification Certification, story telling &

branding

Story-telling, bean2bar,

traceability

Origin Important for blending Important for marketing Important for taste

Region Focus on West Africa and Asia All regions Focus on Latin America

Size of company Large Medium-large Small-medium

Example of companies Nestle, Mondelez, Mars,

Hershey, Ferrero

Tony Chocolonely, Lindt,

Mondelez, Chocolate

makers

Pacari, Marou, Original

Beans, Duffy, Akkessons

Example of products Chocolate products chocolate bars & chocolate

milk

Chocolate bars

Example of retailer Albert Heijn, Coop, Jumbo, Plus Marqt, Ekoplaza, Ahold,

chocolatiers

Coffee shops, Online, Trade

fairs

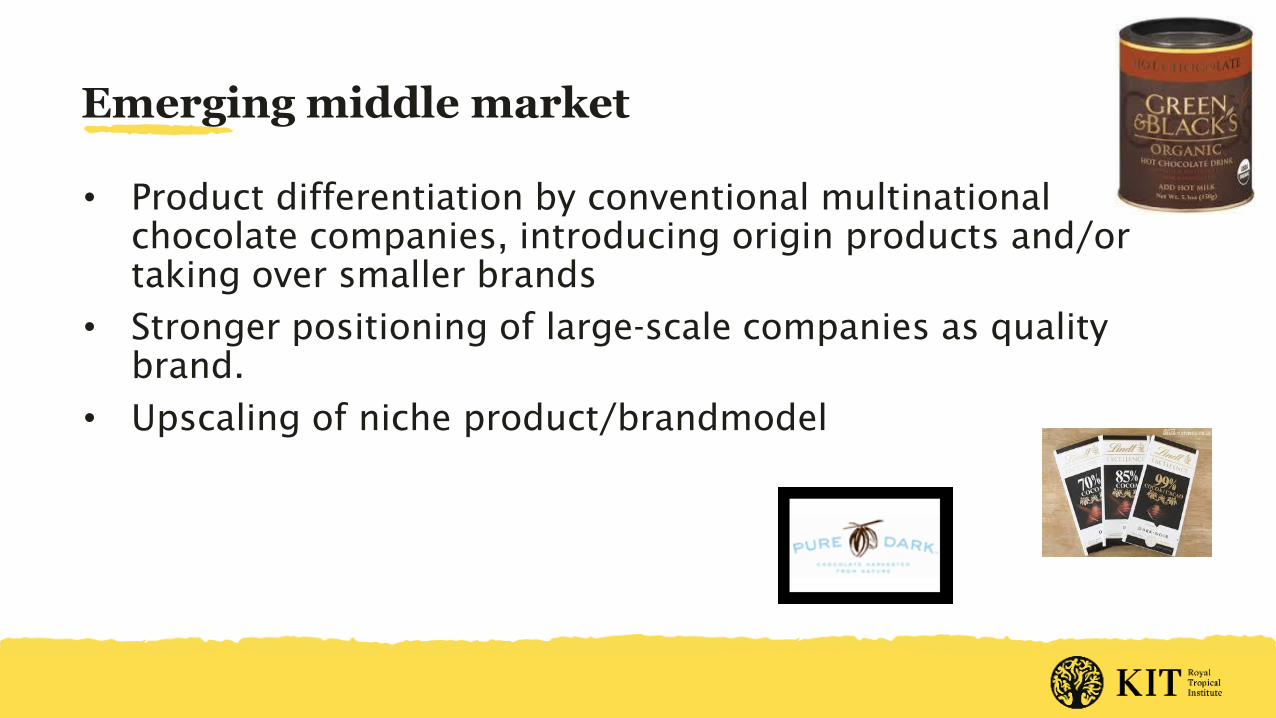

Emerging middle market

• Product differentiation by conventional multinational

chocolate companies, introducing origin products and/or

taking over smaller brands

• Stronger positioning of large-scale companies as quality

brand.

• Upscaling of niche product/brandmodel

Middle market and sustainability?

• Provides more choices for consumers: requires transparency and traceability

• Creates space for alternative business models

• Higher quality translates in higher price, also for producers (but can also include higher costs or

risks): show evidence!

• Closer collaboration with value chain actors, including farmer (organizations)

• Risk management strategy: differentiation

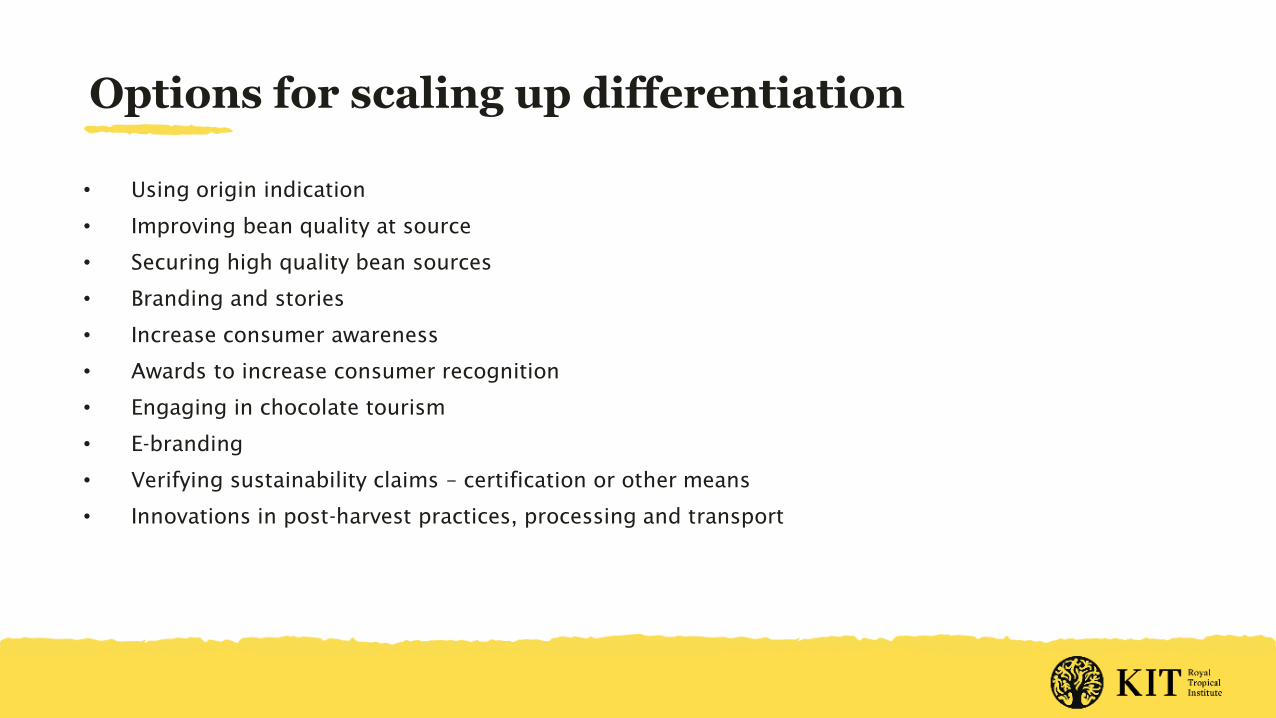

Options for scaling up differentiation

• Using origin indication

• Improving bean quality at source

• Securing high quality bean sources

• Branding and stories

• Increase consumer awareness

• Awards to increase consumer recognition

• Engaging in chocolate tourism

• E-branding

• Verifying sustainability claims – certification or other means

• Innovations in post-harvest practices, processing and transport

21

KIT – Royal Tropical Institute

Mauritskade 64

1092 AD Amsterdam

Contact

Anna Laven

www.kit.nl/sed

22