Embed Size (px)

Citation preview

© Copyright 2012 Kantar Retail

Presented by:

NEW STRATEGIES FOR NEW RETAIL REALITIESWINNERS IN MODERN RETAIL 2016

Vadim KhetsurianiRetail Insight Director Central Europe and Middle East

May 31, 2012PROGRESSIVE Conference

Sandanski, BULGARIASource: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Kantar Retail was formed from four Insight and Consulting businesses. It serves leading Retailers and Manufacturers globally, delivering a competitive advantage and enhanced revenue and profitability.Leading suppliers, brand manufacturers, retailers, financial services and strategic marketing firms rely on Kantar Retail’s expertise to transform their businesses.Kantar Retail is headquartered in London and is part of the Kantar Group of WPP.

OUR PEOPLEOur people are specialist practitioners with experience in working at a senior level within and for Global Brands.

WHO IS KANTAR RETAIL?

© Copyright 2012 Kantar Retail

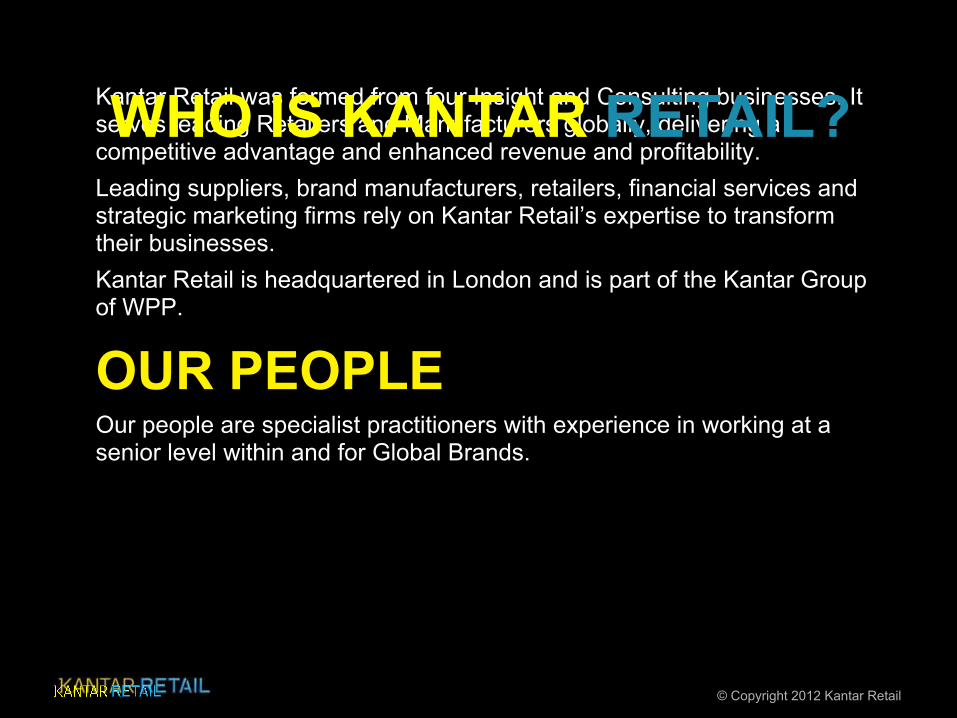

Retail landscape and consumer shopping modes are becoming more complex

Where

What

How

Whe

n

●Proximity or convenient solutions●Online

●Everyday and on the weekends

●Spontaneously and planned

●24-7

●Retailer brands●Real deals

●Real innovation

●To a list●Digitally enabled

●With a clear mission

Source: Kantar Retail analysis

© Copyright 2012 Kantar Retail

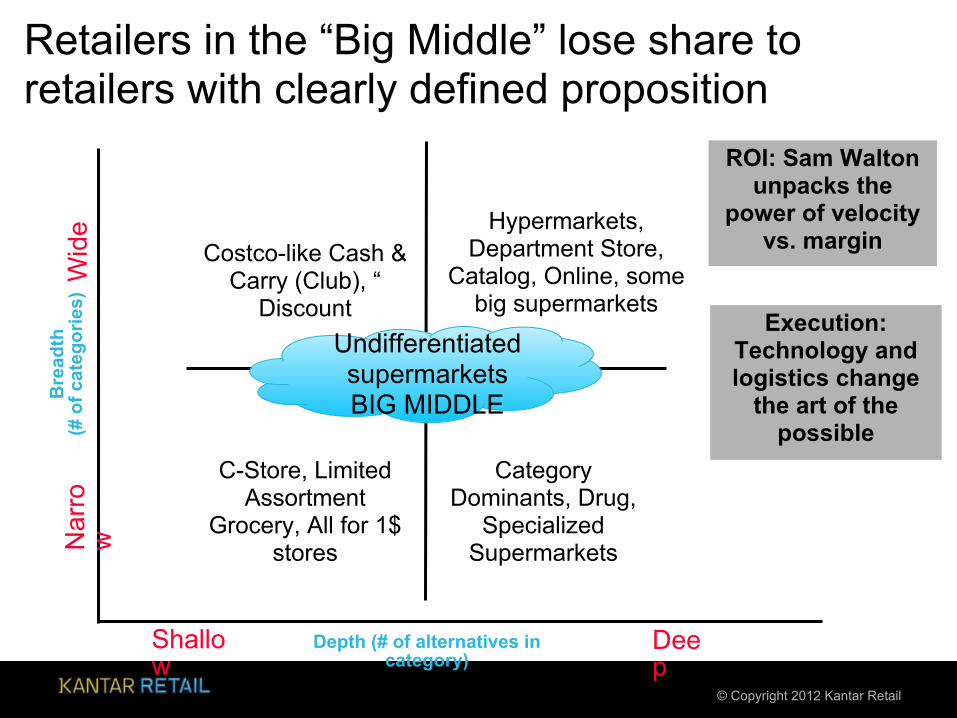

Retailers in the “Big Middle” lose share to retailers with clearly defined proposition

Costco-like Cash & Carry (Club), “

Discount

C-Store, Limited Assortment

Grocery, All for 1$ stores

Hypermarkets, Department Store,

Catalog, Online, some big supermarkets

Category Dominants, Drug,

Specialized Supermarkets

Execution: Technology and logistics change

the art of the possible

ROI: Sam Walton unpacks the

power of velocity vs. margin

Shallow

Deep

Wid

e N

arro

w

Depth (# of alternatives in category)

Bre

adth

(# o

f cat

egor

ies)

Undifferentiated supermarketsBIG MIDDLE

© Copyright 2012 Kantar Retail

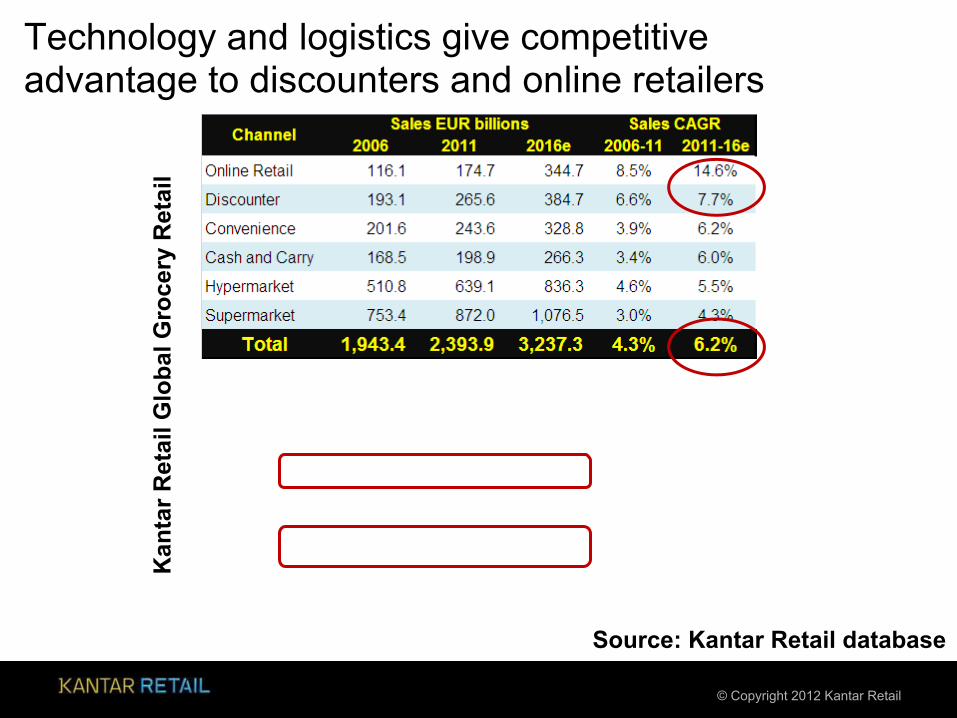

Technology and logistics give competitive advantage to discounters and online retailers

Source: Kantar Retail database

Kan

tar R

etai

l Glo

bal G

roce

ry R

etai

l

© Copyright 2012 Kantar Retail

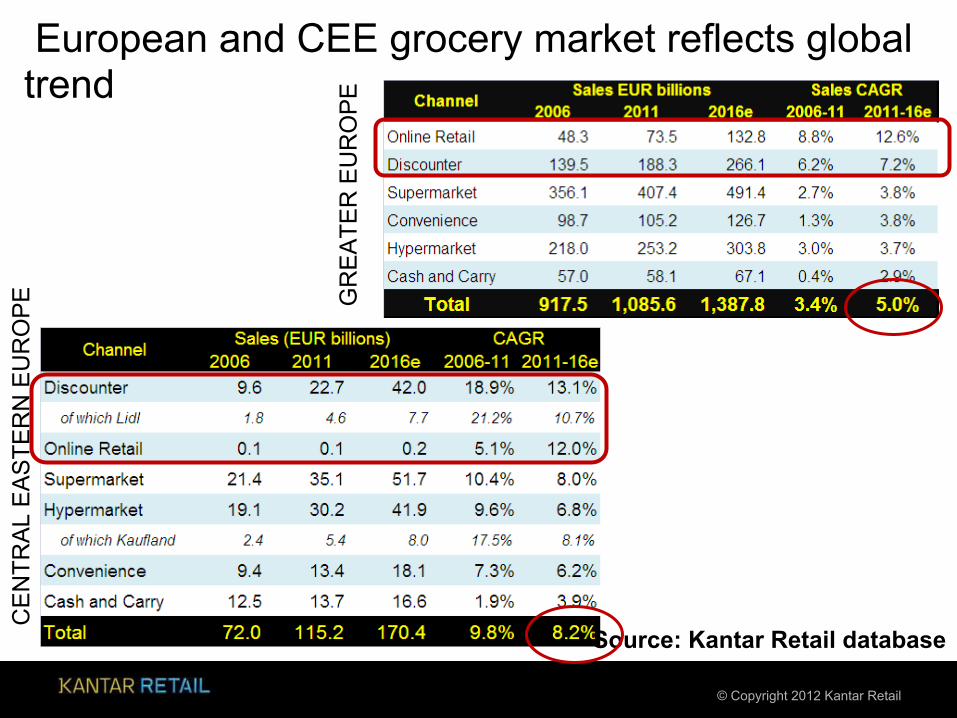

European and CEE grocery market reflects global trend

GR

EA

TER

EU

RO

PE

CE

NTR

AL

EA

STE

RN

EU

RO

PE

Source: Kantar Retail database

© Copyright 2012 Kantar Retail

Key takeaways from global and euro views on modern retail growth prospects 2012-2016

● Discounters and online retailers make retailer “economics” work to their advantage

● Convenience channel growth – higher profit

requirements to cover higher cost of real estate and service

● Cash & carry is shifting to ‘integrated franchise’ model

for traditional trade and HoReCa across all markets

● Hypermarkets and supermarkets mixed growth prospects depending on the evolution stage of a market

© Copyright 2012 Kantar Retail

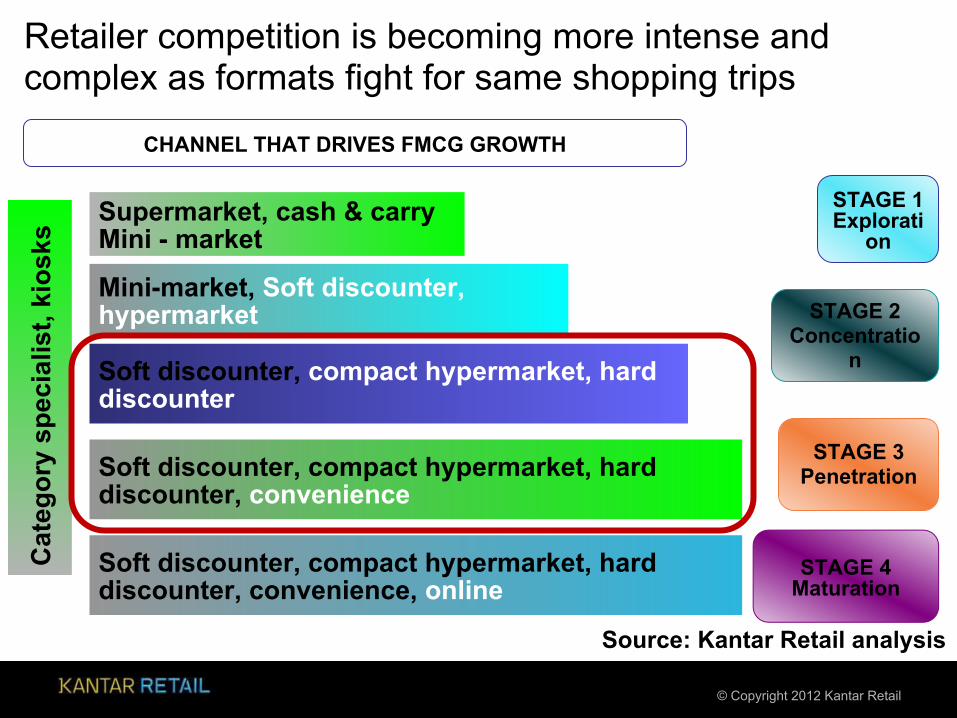

Retailer competition is becoming more intense and complex as formats fight for same shopping trips

STAGE 1Explorati

on

STAGE 2Concentratio

n

STAGE 3Penetration

Soft discounter, compact hypermarket, hard discounter, convenience, online

Soft discounter, compact hypermarket, hard discounter

Mini-market, Soft discounter, hypermarket

Supermarket, cash & carryMini - market

Soft discounter, compact hypermarket, hard discounter, convenience

CHANNEL THAT DRIVES FMCG GROWTH

Cat

egor

y sp

ecia

list,

kios

ks

STAGE 4Maturation

Source: Kantar Retail analysis

© Copyright 2012 Kantar Retail

Takeaway 1: New capabilities for customer and channel management for suppliers

Exploration I

Concentration II

Penetration III

Wholesale and distributor partnership, market share, numerical distribution

● Move from transactional approach to complete return on investment discussion with accounts

● Regional and channel merchandise planningusing shopper insights

Understand retailer format differences and align with winning retailers-formats

● Transparent and defensible pricing and trade spend models, measure return on all investment,

smooth transition from traditional to modern

© Copyright 2012 Kantar Retail

Takeaway 2: People shop ‘Missions’ and not ‘Brands’ or ‘Categories’ – fitting into a mission or inventing one

Understand shopper missions in modern trade – this will help build the right selling story and identify opportunities

together with key accounts/retailers

CO

NS

UM

ER

SH

OP

PE

R

SH

OP

PE

R

MIS

SIO

N

STO

RE

FO

RM

AT

CA

TEG

OR

Y

BR

AN

D

© Copyright 2012 Kantar Retail

At current organic forecast top 10 retailer ranking in CEE is changing

* Top 10 CEE excluding Russia

CENTRAL EASTERN EUROPE (EXCLUDING RUSSIA, INCLUDING TURKEY AND UKRAINE)

Source: Kantar Retail database,Company reports, estimates

© Copyright 2012 Kantar Retail

Discounters: Lidl flexibility has allowed it to grow and sustain leadership in Europe

Source: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Flexible business model allows discounters to grow faster than more ‘conservative’ competition

2011 Sales Rank

RetailerSales CUR EUR CAGR

2006 2011 2016E 06-'11 11-16E

1 Lidl 30.4 45.7 60.4 8.5% 5.7%2 Aldi Süd 16.5 21.1 26.5 5.0% 4.7%3 Aldi Nord 16.7 17.5 18.8 1.0% 1.4%4 Edeka - Netto 4.8 13.4 15.6 23.1% 3.1%5 Penny 7.8 11.3 13.2 7.6% 3.2%6 X5 Retail Group 2.4 9.5 20.2 31.8% 16.3%7 Magnit 2.0 7.4 19.2 30.4% 21.0%8 Dia 7.4 5.9 6.2 -4.6% 1.1%9 Biedronka 1.7 5.8 13.3 27.8% 17.9%

10 Rema 1000 2.8 4.5 5.7 10.1% 4.9%Top 10 Total 92.4 142.1 199.0 9.0% 7.0%

Top 10 Share of Total 66.0% 73.9% 74.3% na na

Source: Kantar Retail database

GREATER EUROPE DISCOUNTER RANKING

© Copyright 2012 Kantar Retail

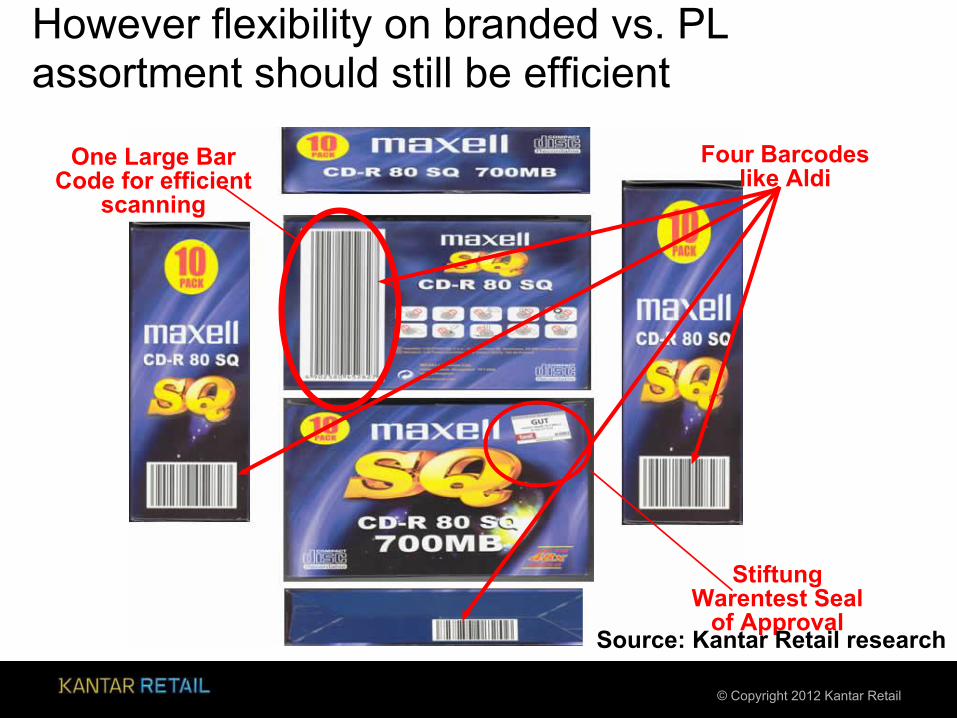

However flexibility on branded vs. PL assortment should still be efficient

Four Barcodes like Aldi

One Large Bar Code for efficient

scanning

Stiftung Warentest Seal

of Approval

Source: Kantar Retail research

© Copyright 2012 Kantar Retail

Hard or Soft – shoppers accept discounters as a substitute to traditional trade

Russia Magnit store

Turkey BIM store

Russia traditional food store

Turkey traditional food store

Magnit hybrid between soft discount, minimarket and convenience store

Bim model is hard discounter

Source: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Discounter provide VALUE and build ACCEPTANCE on the back of quality brands

New Stores

Build Awareness

Bigger Stores

More Categories

Market Entry

Grow Shopper Base

National/Local Brands

Promotions

Build Basket

Drive Frequency

Range Optimization

Operational Efficiency

Market MaturitySource: Kantar Retail analysis

© Copyright 2012 Kantar Retail

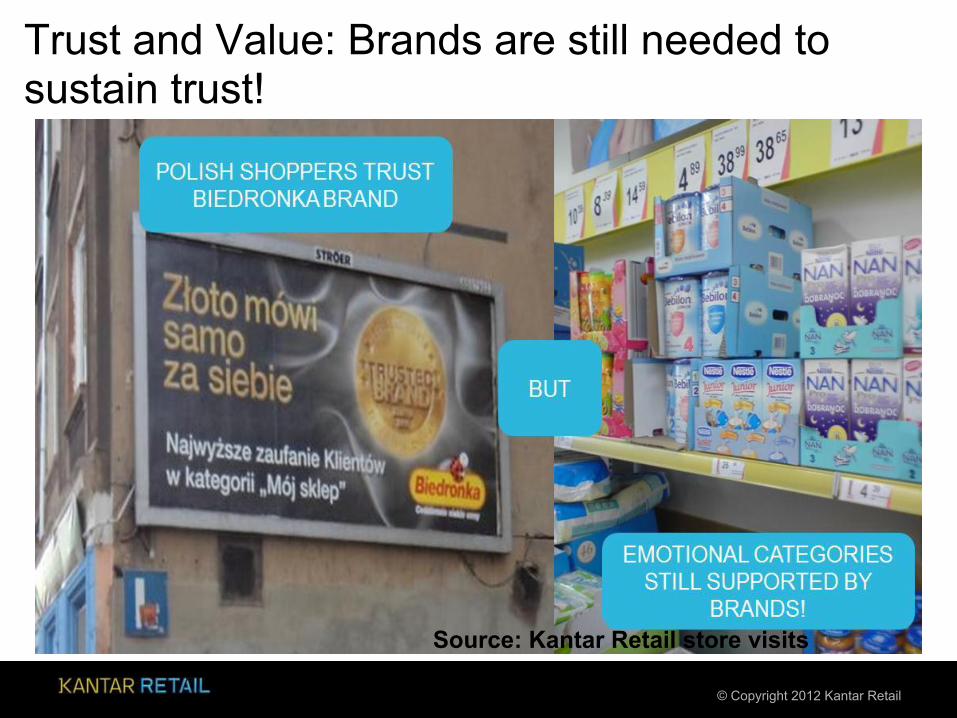

Trust and Value: Brands are still needed to sustain trust!

Source: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Real Value?? - Promotions and private label are common tools for retailers

Source: Kantar Group company research

© Copyright 2012 Kantar Retail

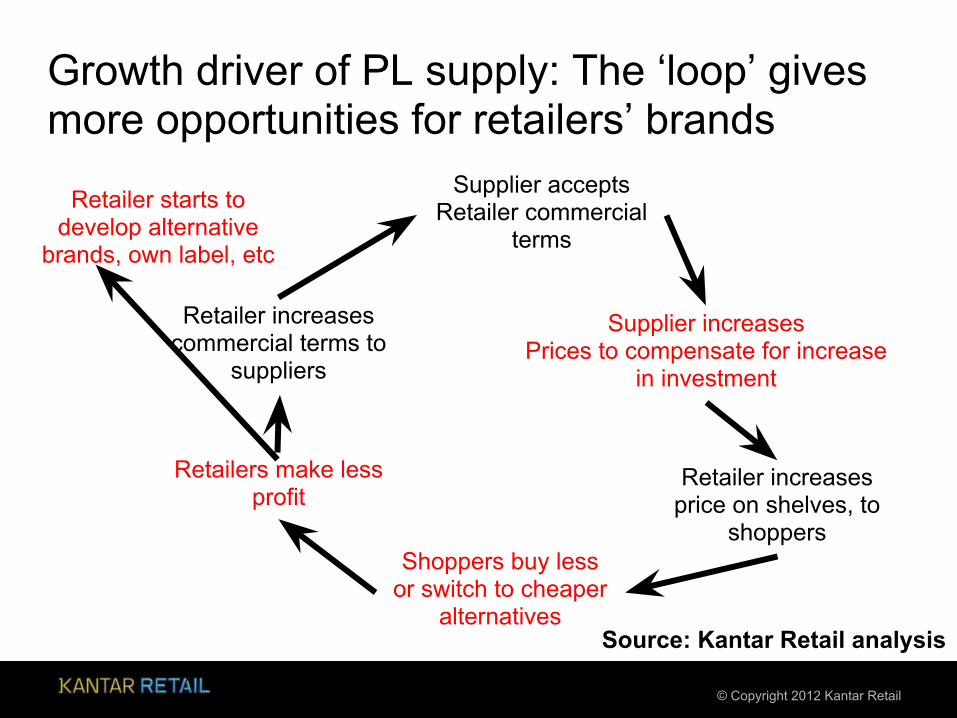

Growth driver of PL supply: The ‘loop’ gives more opportunities for retailers’ brands

Supplier accepts Retailer commercial

terms

Supplier increasesPrices to compensate for increase

in investment

Retailer increases price on shelves, to

shoppersShoppers buy less

or switch to cheaper alternatives

Retailers make less profit

Retailer increases commercial terms to

suppliers

Retailer starts to develop alternative

brands, own label, etc

Source: Kantar Retail analysis

© Copyright 2012 Kantar Retail

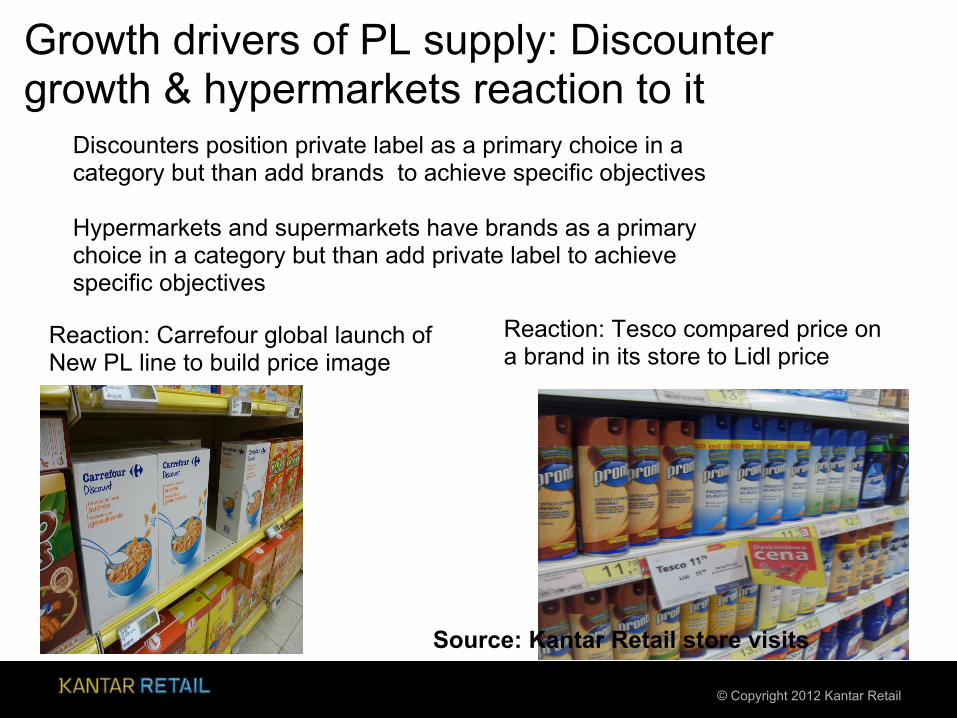

Growth drivers of PL supply: Discounter growth & hypermarkets reaction to it

Source: Kantar Retail store visits

Discounters position private label as a primary choice in a category but than add brands to achieve specific objectives Hypermarkets and supermarkets have brands as a primary choice in a category but than add private label to achieve specific objectives

Reaction: Tesco compared price on a brand in its store to Lidl price

Reaction: Carrefour global launch of New PL line to build price image

© Copyright 2012 Kantar Retail

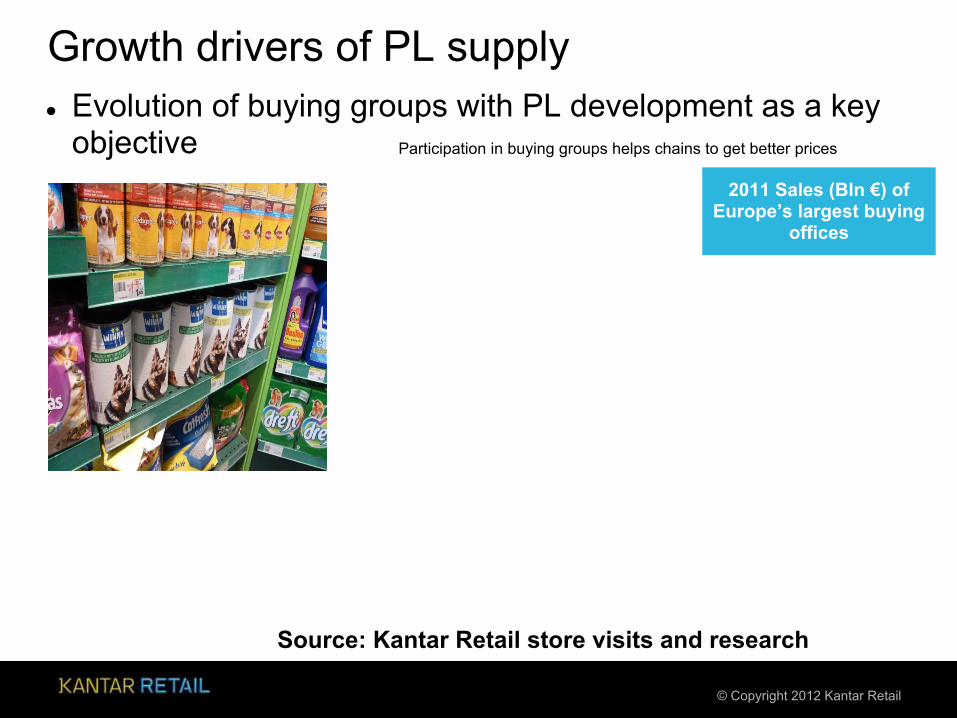

2011 Sales (Bln €) of Europe’s largest buying

offices

Participation in buying groups helps chains to get better prices

Growth drivers of PL supply● Evolution of buying groups with PL development as a key

objective

Source: Kantar Retail store visits and research

© Copyright 2012 Kantar Retail

Brands to be prepared for PL “invasion” once category is activated in discounters

Half the price of branded beer

sold in the same store

“German” butter signifies quality

and “Quality Made in Germany” seal

Educating shoppers to buy

frequent purchase category with beer

and butterSource: Lidl web flyer

© Copyright 2012 Kantar Retail

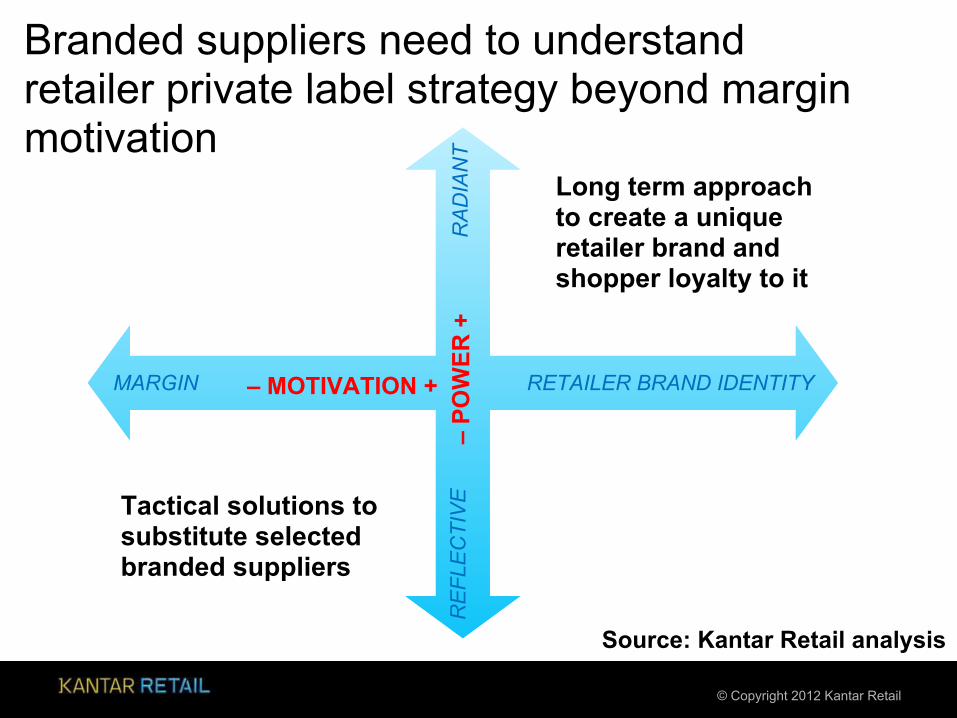

Branded suppliers need to understand retailer private label strategy beyond margin motivation

RA

DIA

NT

MARGIN RETAILER BRAND IDENTITY – MOTIVATION +

– PO

WER

+

RE

FLE

CTI

VETactical solutions to

substitute selected branded suppliers

Long term approach to create a unique retailer brand and shopper loyalty to it

Source: Kantar Retail analysis

© Copyright 2012 Kantar Retail

● Will increase share of market in most Central Eastern European countries

● Growth will slow in some mature markets in Western

Europe but own label evolving beyond the tier ‘good-better-best’

● Economic rationale will remain strong for both retailers &

shoppers (and for some manufacturers with production capacity)

PL outlook

© Copyright 2012 Kantar Retail

Supplier strategies to disarm PL threat

● Instinctive reaction of OPP, price decrease or promo

● Economy brands to take PL head on

● With PL gaining share in the middle ground, some suppliers are embarking on polar strategy (economy AND premium)

● Innovation (despite the inevitable mimicry from PL)

● Marketing

© Copyright 2012 Kantar Retail

Supplier strategies to disarm PL threat

● Striking instore marketing can activate brand demand & steer shoppers away from PL

Source: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Supplier strategies to disarm PL threat● Launch of economy/OPP brands by manufacturers

● “Simply Duracell provides the quality consumers can expect from Duracell at an affordable price”

Source: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Supplier strategies to disarm PL threat● Launch of economy/OPP brands by manufacturers

e.g. P&G launch of Ariel Básico – now aiming to have value versions in 75% of categories by 2012

2009 launch of Pampers Simply Dry ('no-frills performance at a value price point‘) & 2010 launch of Pampers Dry Max ('thinnest, driest nappy ever'.)

Source: Company Website and reports

© Copyright 2012 Kantar Retail

Premiumization / solutions a successful approachE.g. Launch by Reckitt

Benckiser of Air Wick Odour Detect & Dettol No Touch

“These have step-changed the dynamics of categories that have been declining for

quite some time.”

Source: Kantar Retail store visits and RB reports

© Copyright 2012 Kantar Retail

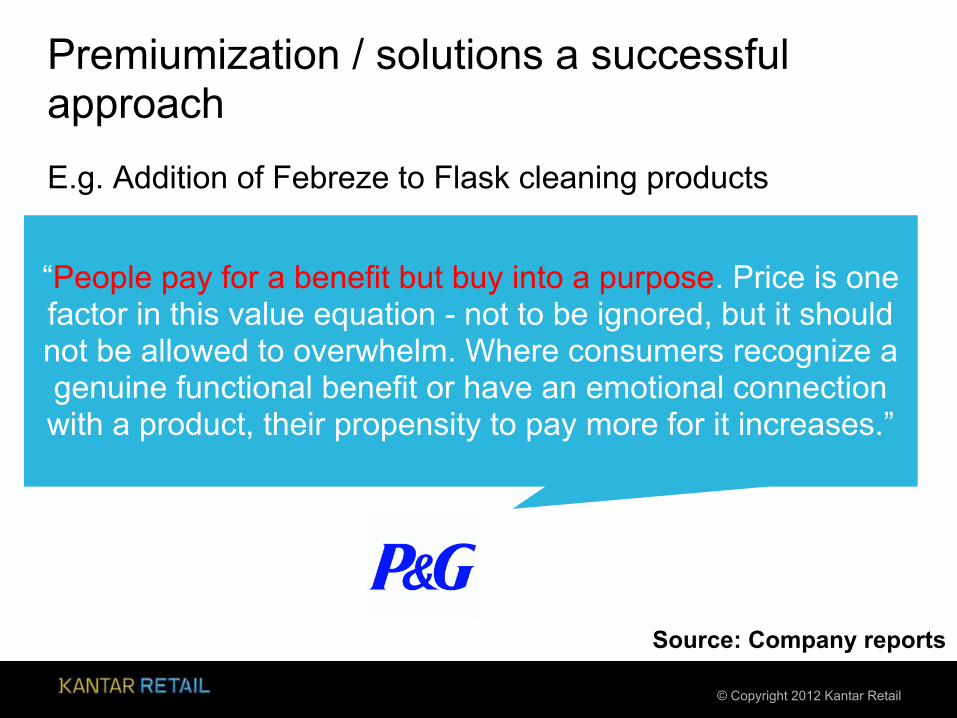

Premiumization / solutions a successful approach E.g. Addition of Febreze to Flask cleaning products

“People pay for a benefit but buy into a purpose. Price is one factor in this value equation - not to be ignored, but it should not be allowed to overwhelm. Where consumers recognize a genuine functional benefit or have an emotional connection with a product, their propensity to pay more for it increases.”

Source: Company reports

© Copyright 2012 Kantar Retail

… How can promotions help brands build emotional, ‘purpose-linked’ connection with shoppers?

“A single conversation across the table with a wise person is worth a month’s study of books”

-Chinese Proverb “It was impossible to get a conversation started. Everyone was talking too much” -Yogi Berra - famous baseball

player and a “malaproposer”

© Copyright 2012 Kantar Retail

Source: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Source: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Real value ≠ low pricesReal Value = Price + Quality + Service

Turkey Shopper Survey% at Presence who think

the brand costs more than they are prepared to pay

Source: Brandz and KR store visit

© Copyright 2012 Kantar Retail

Migros has strong loyalty (bonding) with shoppers by providing value BEYOND price

Real Value = Price + Quality + Service = Loyalty (Bonding)

Source: Brandz

© Copyright 2012 Kantar Retail

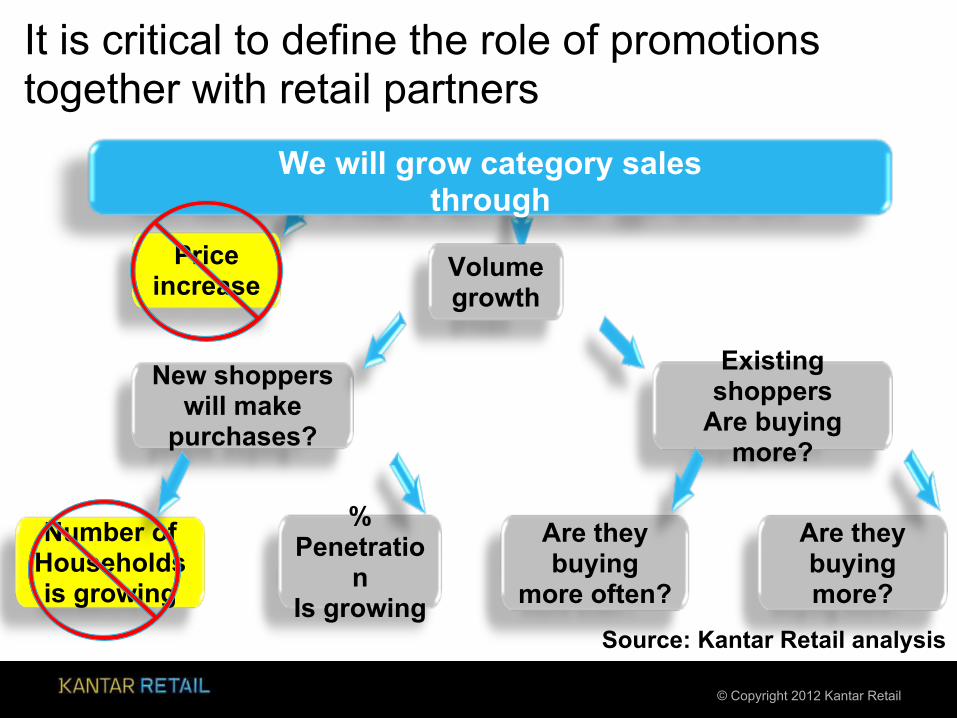

It is critical to define the role of promotions together with retail partners

We will grow category salesthrough

Volumegrowth

Price increase

New shopperswill make

purchases?

Existing shoppers

Are buying more?

Are they buying

more often?

Are they buying more?

% Penetratio

nIs growing

Number ofHouseholds is growing

Source: Kantar Retail analysis

© Copyright 2012 Kantar Retail

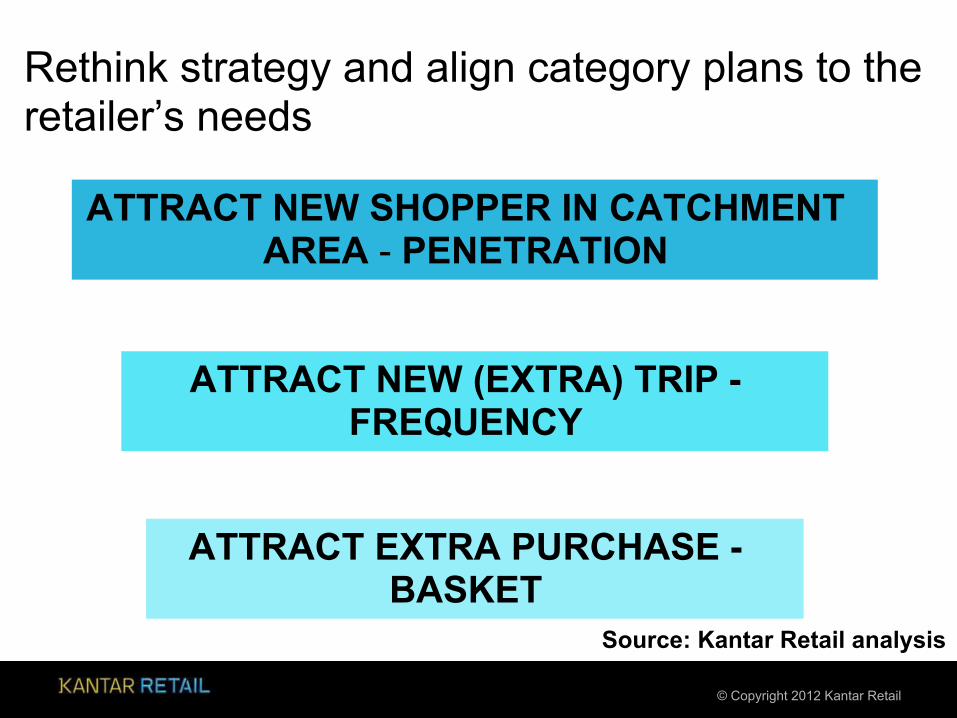

Rethink strategy and align category plans to the retailer’s needs

ATTRACT NEW (EXTRA) TRIP - FREQUENCY

ATTRACT NEW SHOPPER IN CATCHMENT AREA - PENETRATION

ATTRACT EXTRA PURCHASE - BASKET

Source: Kantar Retail analysis

© Copyright 2012 Kantar Retail

Retailers are building departments to increase penetration and frequency

Source: Kantar Retail store visits

HEALTH AND BEAUTY SHOP IN SHOP TESCO EXTRA

ADDITIONAL SERVICES

© Copyright 2012 Kantar Retail

Good promotions multi brand promotions generate traffic and activate many categories

Source: Kantar Retail store visits

REAL HYPERMARKET – A QUEST FOR SWEETS!

© Copyright 2012 Kantar Retail

Smart retailers consistently focus on traffic driving promotions in catchment areas

Source: Kantar Retail store visits

KAUFLAND HYPERMARKET – FIND A ‘STAR’ AND GET A PRIZE, RADIO ADVERTIZED, OUTSIDE AND INSIDE

STORE

© Copyright 2012 Kantar Retail

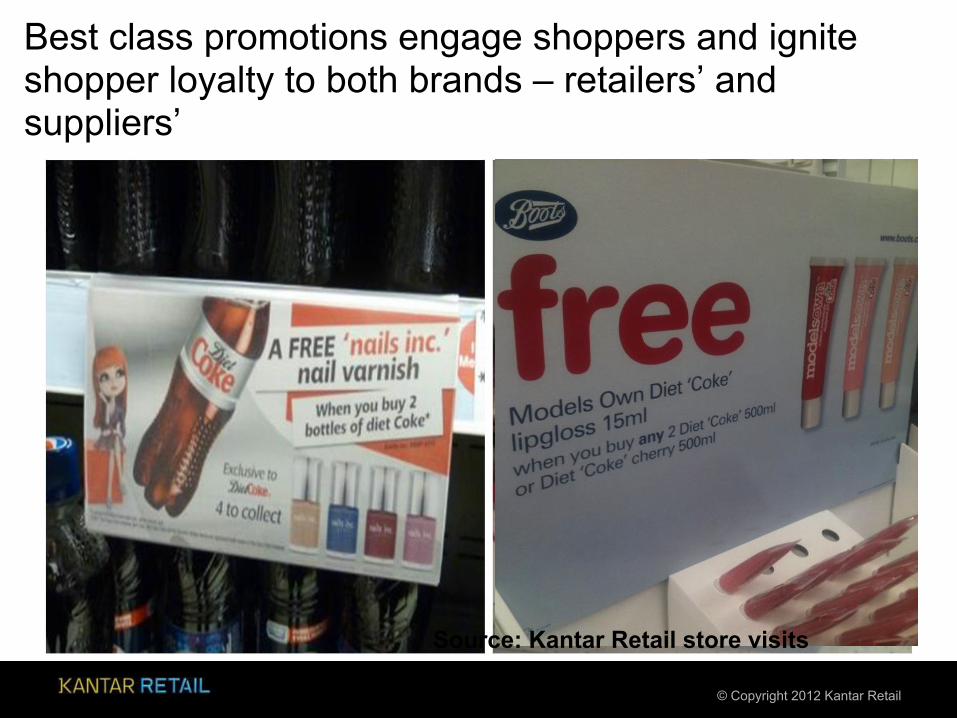

Best class promotions engage shoppers and ignite shopper loyalty to both brands – retailers’ and suppliers’

Source: Kantar Retail store visits

© Copyright 2012 Kantar Retail

Winning retailers 2016: How can we identify them?

ATTRIBUTES and ENABLERS

STRATEGIC PARTNER RETAILERS HAVE THESE:

Source: Kantar Retail analysis

Where will I shop? Why will I shop there? How will it work?

INVEST IN LOYALTY TO RETAIL BRAND BEYOND JUST

CONVENIENCE/PROXIMITY

Convenience vs.Loyalty

DEVELOP CONSISTENT SHOPPER EXPERIENCE (AND RETAIL BRAND)

PROVIDE REAL VALUE = PRICE+QUALITY+SERVICE

Experience vs.Value

HAVE A COMPREHENSIVE SET OF FINANCIAL KPIS TO FOCUS

ORGANIZATION BEYOND MARGIN %

Execution vs.RETURN ON INVESTMENT

© Copyright 2012 Kantar Retail

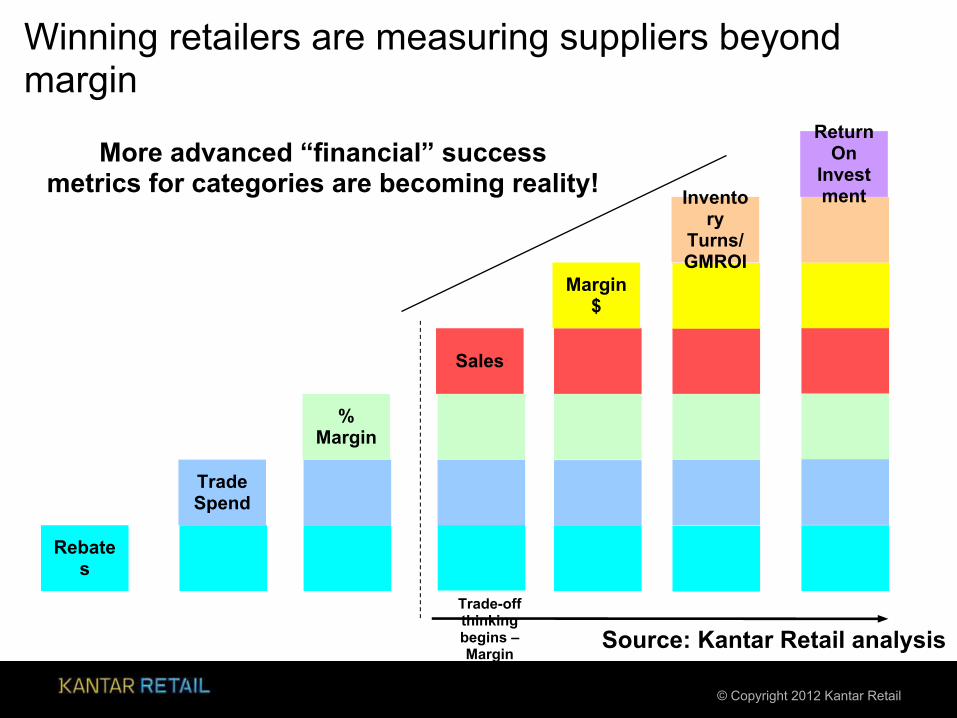

Winning retailers are measuring suppliers beyond margin

Trade-off thinking begins – Margin

vs. Velocity

Rebates

Trade Spend

% Margin

Sales

Margin $

Invento

ryTurns/GMROI

ReturnOn

Investment

More advanced “financial” success metrics for categories are becoming reality!

Source: Kantar Retail analysis

© Copyright 2012 Kantar Retail

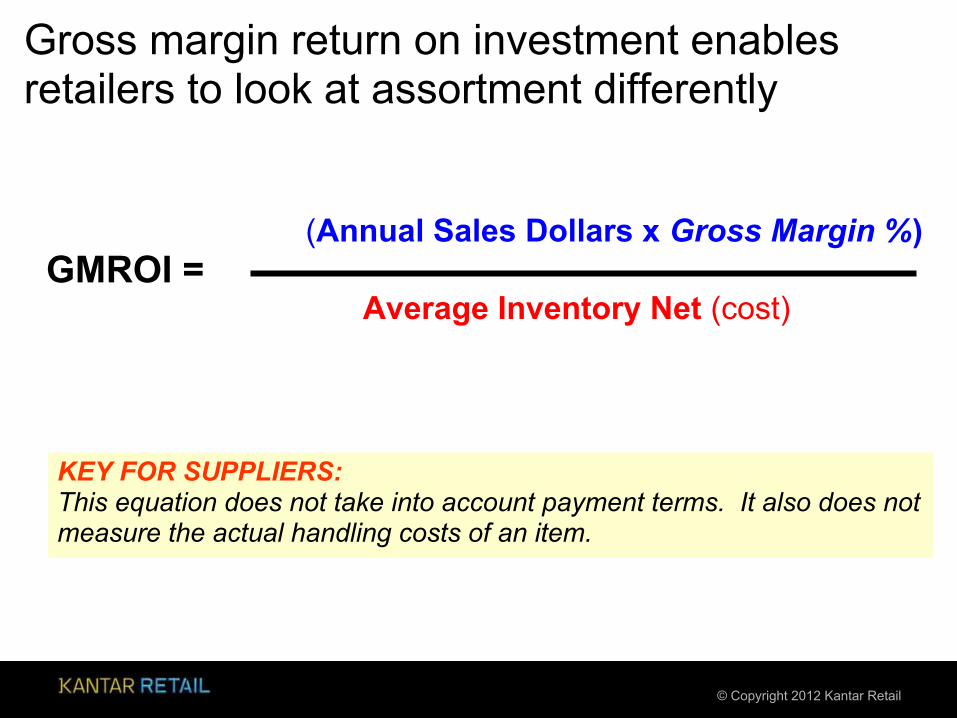

Gross margin return on investment enables retailers to look at assortment differently

(Annual Sales Dollars x Gross Margin %)GMROI =

KEY FOR SUPPLIERS: This equation does not take into account payment terms. It also does not measure the actual handling costs of an item.

Average Inventory Net (cost)

© Copyright 2012 Kantar Retail

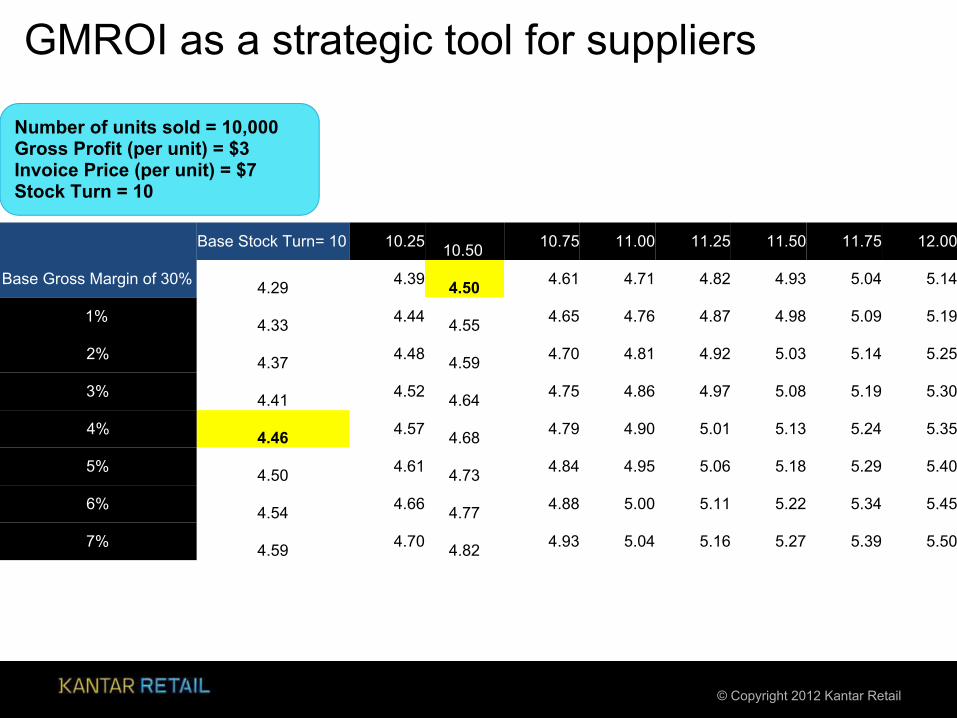

GMROI as a strategic tool for suppliers

Base Stock Turn= 10 10.25 10.50 10.75 11.00 11.25 11.50 11.75 12.00

Base Gross Margin of 30% 4.29 4.39

4.50 4.61 4.71 4.82 4.93 5.04 5.14

1% 4.33 4.44

4.55 4.65 4.76 4.87 4.98 5.09 5.19

2% 4.37 4.48

4.59 4.70 4.81 4.92 5.03 5.14 5.25

3% 4.41 4.52

4.64 4.75 4.86 4.97 5.08 5.19 5.30

4% 4.46 4.57

4.68 4.79 4.90 5.01 5.13 5.24 5.35

5% 4.50 4.61

4.73 4.84 4.95 5.06 5.18 5.29 5.40

6% 4.54 4.66

4.77 4.88 5.00 5.11 5.22 5.34 5.45

7% 4.59 4.70

4.82 4.93 5.04 5.16 5.27 5.39 5.50

Number of units sold = 10,000Gross Profit (per unit) = $3Invoice Price (per unit) = $7Stock Turn = 10

© Copyright 2012 Kantar Retail

Winning retailers are C_L_E_V_E_R

WIN SHOPPERS FROM TRADITIONAL

RETAIL

WIN SHOPPERS FROM MODERN COMPETITORS

PRICE AND

CONVENIENCE (EASE OF ACCESS)

LOYALTY

Where will I shop?Convenience vs.Loyalty

Why will I shop there?Experience vs.Value

How will it work?Execution vs.RETURN ON INVESTMENT

Source: Kantar Retail analysis

© Copyright 2012 Kantar Retail

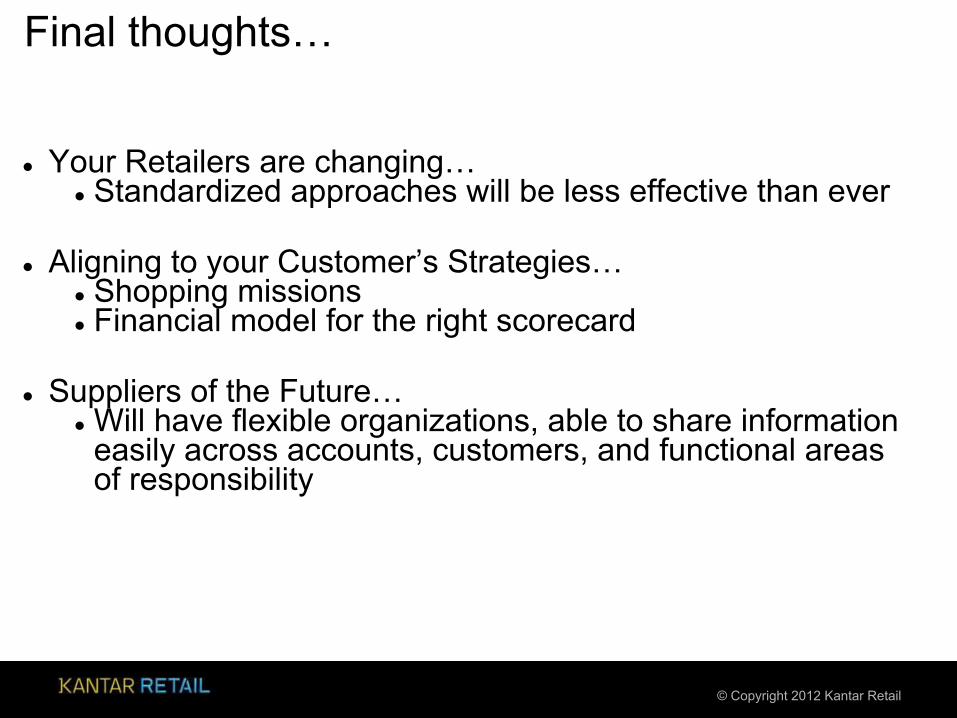

Final thoughts…

● Your Retailers are changing…● Standardized approaches will be less effective than ever

● Aligning to your Customer’s Strategies…

● Shopping missions● Financial model for the right scorecard

● Suppliers of the Future…

● Will have flexible organizations, able to share information easily across accounts, customers, and functional areas of responsibility

© Copyright 2012 Kantar Retail

6 More London PlaceTooley StreetLondon SE1 2QYUK

T +44 (0)207 031 0272F +44 (0)207 031 0270www.KantarRetailiq.eu

Vadim Khetsuriani

Modern Trade Insights [email protected]@yahoo.comTel +7 915 000 1471

THANK YOU FOR LISTENING!