Embed Size (px)

Citation preview

Force Motors

Religare Investment Call

31 August 2016

Force Motors Ltd. (FML) is a fully, vertically integrated automobile company specializing in manufacture of Small Commercial Vehicles (SCV), Multi-Utility Vehicles (MUV), Light Commercial Vehicles (LCV), Sports Utility Vehicles (SUV) and Agricultural tractors. It also has expertise in design, development and manufacture of the full spectrum of automotive components and aggregates.

The company has presence across automobiles, components and aggregates segments. Force's Traveller is one of the most popular inter and intra city mobility vehicles in the country. In traveller segment, it is the market leader with market share of 67%. It has also forayed into defense, fire and rescue segment with the launch of paramilitary ambulances and emergency rescue vehicles.

Force Motors is engaged in the assembling of engines, axles and gear boxes for both Mercedes and BMW in India. It is the only company in the world to supply engines to two of the world's biggest luxury car makers. It has set up two plants in Chennai and Pune to cater to BMW and Mercedes respectively with an aggregate investment of Rs. 300Cr.

According to IHS Automotive, a global research and analysis company, luxury car sales in India stood at 35,300 units in 2015. The sale of luxury vehicles is expected to more than double at 87,300 units by 2020. Hence, Force Motors is expected to benefit from the demand of luxury cars, which in turn, will boost its revenue and earnings from components business in the coming years.

The company has reported good growth across segments in the past 2 years. With normal monsoon expected this year, the demand for tractors should improve further with revival in rural economy. We expect the demand for Traveller to improve further with launch of new variants and models. The demand for Force Traveller ambulance and school buses has been on rise since the last few quarters.

FML has set up 'Advanced Technology Centre' at Akurdi for engine and vehicle testing. It undertakes project work on design, development and up gradation of engine configurations in various displacements and capacities. The Company continues to maintain its emphasis on research, development and tool engineering activities.

We expect the company to report revenue and profit CAGR of 16.2% and 20% respectively over FY16-18E. The company's profit margin is expected to improve from 5.9% currently to 6.3% in FY18E due to change in product mix and higher capacity utilisation. Going forward, we expect it to generate healthy cash flows and improve its return ratios. Force has a strong balance sheet with cash and cash equivalents of Rs. 318Cr as on March, 2016 (Rs. 241/share). At cmp of Rs. 3,088, it is trading at FY18E PE of ~15.7x respectively. We recommend a Buy on the stock with a target price of Rs. 3,940.

Automobile

CMP (Rs)

Target Price (Rs)

Potential Upside

Sensex

Nifty

Key Stock data

BSE Code

NSE Code

Bloomberg

Shares o/s, mn (FV 10)

Market Cap (Rs Cr)

3M Avg Volume

52 week H/L

Shareholding Pattern

(%)

Promoter

FII

DII

Others

1 Year price performance

3,088

3,940

27.6%

28,445

8,787

500033

-

FML IN

13.2

4,070

57,400

3,785/1,911

Dec-15

60.1

4.6

0.7

34.6

Mar-16

60.1

4.4

0.8

34.7

Jun-16

60.1

4.6

0.9

34.4

Analyst

Ajay Pasari, [email protected]+91 - 22 - 67288188

Particulars, Rs cr FY14

FY15 FY16 FY17E FY18E

Source : Company & RSL Research

Total income

EBITDA

EBITDAM (%)

PAT

PATM (%)

eps, Rs

RoC (%)

RoE (%)

2,022

97

4.8

78

3.8

59.0

7.2

6.5

2,364

147

6.2

101

4.3

76.9

8.2

8.0

3,060

274

9.0

179

5.9

136.2

12.6

12.8

3,563

334

9.4

219

6.1

166.7

13.3

13.9

4,131

397

9.6

259

6.3

197.0

13.9

14.5

Investment rationale:

Outlook and valuation:

Initiating Coverage

80

Sep -

15

100

120

140

160

180

Force Motors Sensex

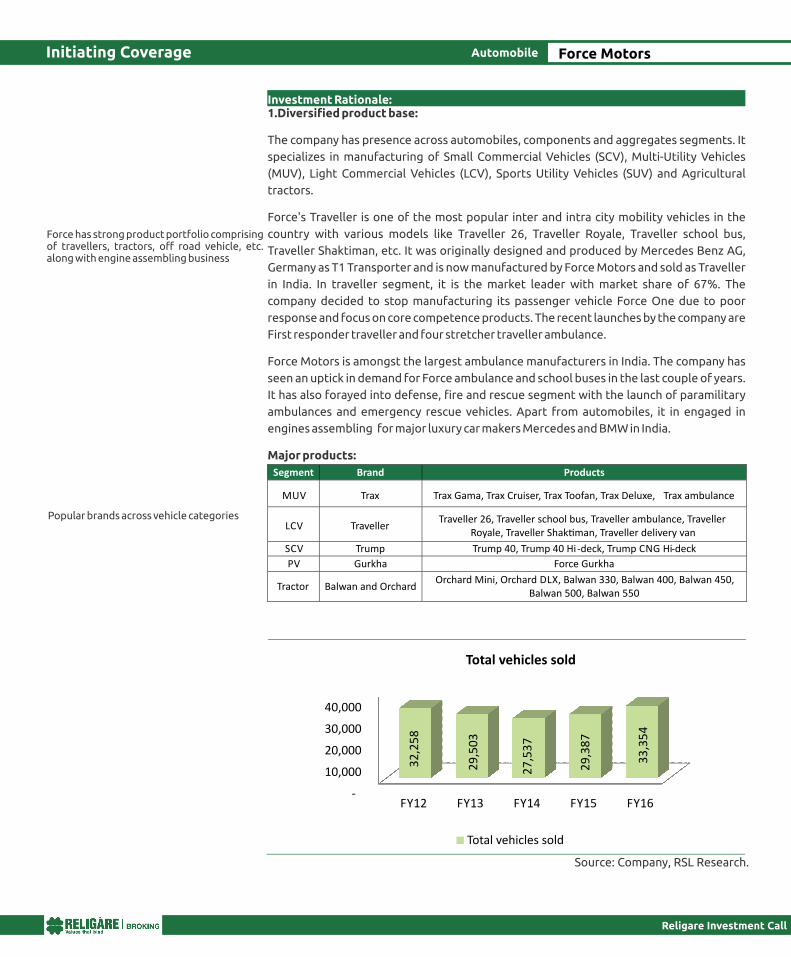

Investment Rationale:1.Diversified product base:

The company has presence across automobiles, components and aggregates segments. It

specializes in manufacturing of Small Commercial Vehicles (SCV), Multi-Utility Vehicles

(MUV), Light Commercial Vehicles (LCV), Sports Utility Vehicles (SUV) and Agricultural

tractors.

Force's Traveller is one of the most popular inter and intra city mobility vehicles in the

country with various models like Traveller 26, Traveller Royale, Traveller school bus,

Traveller Shaktiman, etc. It was originally designed and produced by Mercedes Benz AG,

Germany as T1 Transporter and is now manufactured by Force Motors and sold as Traveller

in India. In traveller segment, it is the market leader with market share of 67%. The

company decided to stop manufacturing its passenger vehicle Force One due to poor

response and focus on core competence products. The recent launches by the company are

First responder traveller and four stretcher traveller ambulance.

Force Motors is amongst the largest ambulance manufacturers in India. The company has

seen an uptick in demand for Force ambulance and school buses in the last couple of years.

It has also forayed into defense, fire and rescue segment with the launch of paramilitary

ambulances and emergency rescue vehicles. Apart from automobiles, it in engaged in

engines assembling for major luxury car makers Mercedes and BMW in India.

Major products:

Religare Investment Call

Initiating Coverage Force MotorsAutomobile

Segment Brand Products MUV

Trax

Trax Gama, Trax Cruiser, Trax Toofan, Trax Deluxe, Trax ambulance

LCV

Traveller

Traveller 26, Traveller school bus, Traveller ambulance, Traveller Royale, Traveller Shak�man, Traveller delivery van

SCV

Trump

Trump 40, Trump 40 Hi-deck, Trump CNG Hi-deck

PV Gurkha Force Gurkha

Tractor Balwan and OrchardOrchard Mini, Orchard DLX, Balwan 330, Balwan 400, Balwan 450,

Balwan 500, Balwan 550

-

10,000

20,000

30,000

40,000

FY12 FY13 FY14 FY15 FY16

32

,25

8

29

,50

3

27

,53

7

29

,38

7

33

,35

4

Total vehicles sold

Total vehicles sold

Source: Company, RSL Research.

Force has strong product portfolio comprising of travellers, tractors, off road vehicle, etc. along with engine assembling business

Popular brands across vehicle categories

2. Revenue growth boost to come from engines sales to Mercedes and BMW:

Force Motors is engaged in the assembling of engines, axles and gear boxes for both

Mercedes and BMW in India. It is the only company in the world to supply engines to two of

the world's biggest luxury car makers. Mercedes has been buying engines for its C, E, S, GL

and M class cars and SUVs from Force since 1997. Till June 2016, Force has supplied close to

60,000 engines and 50,000 axles to Mercedes. Recently in June 2016, the company

inaugurated a new plant in Pune to supply engines to Mercedes with an investment of

Rs. 100 Cr. The plant has an annual capacity of 20,000 engines and 20,000 front and rear

axles.

Also in 2015, the company opened a plant in Mahindra World City, near Chennai, that

produces powertrains and gearboxes for BMW with an investment cost of Rs. 200Cr. This is

the first independent plant of BMW that assembles and tests engines. The plant can

produce 20,000 units of premium engines and can be further expanded up to 50,000 units.

The plant assembles diesel engines for the BMW X1, X3, X5, 3 Series and 3 GT, 5 Series and

7 Series.

Currently engine assembling business contributes around Rs. 1,000 Cr to the total revenue.

The management expects to increase its revenue from the segment by three-folds to

Rs. 3,000 Cr in the next three years driven by its contract manufacturing business with both

luxury car makers.

According to IHS Automotive, a global research and analysis company, luxury car sales in

India stood at 35,300 units in 2015. The market was led by Mercedes followed by Audi and

BMW. The sale of luxury vehicles is expected to more than double at 87,300 units by 2020.

Hence, Force Motors is expected to benefit from the demand of luxury cars which in turn

will boost its revenue and earnings from components business in the coming years.

Religare Investment Call

Initiating Coverage Force MotorsAutomobile

-

10,000

20,000

30,000

40,000

CY2010 CY2011 CY2012 CY2013 CY2014 CY2015

17

,14

0

24

,76

1

29

,39

8

31

,42

7

33

,81

8

35

,30

0

Total luxury car sales

Total luxury car sales

Source: IHS Automotive, RSL Research

Auto component business to benefit from tie up with BMW and Mercedes for engine assembling

The demand for luxury vehicles have been on the rise due to surge in discretionary spending and improving income levels

3. Demand to come from better monsoon and revival in the economy:

We expect the automobile segment of the company which, includes LCV, MUV, SCV, SUV

and tractors, to grow at 16-17% from FY16-FY18E. The company has reported good growth

across segments in the past 2 years. The tractor business reported better growth in

volumes compared to the industry volumes in FY15 and FY16.

With normal monsoon this year, the demand for tractors should improve further with

revival in rural economy. Force has two strong brands in the tractor segment, Balwan and

Orchard. The 25-hp Orchard Tractor has performed well in select markets, the company

similarly wants to enhance the penetration of higher hp tractors from the Balwan range. In

LCVs, its Traveller is amongst the most popular vehicle used as tourist vehicles, ambulances

and school buses. We expect the demand for Traveller to improve further with launch of

new variants and models. The demand for Force Traveller ambulance and school buses has

been on the rise since last few quarters

Religare Investment Call

Initiating Coverage

Source: Various sources

Source: IHS Automotive, RSL Research

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

CY2010 CY2011 CY2012 CY2013 CY2014 CY2015

Total Luxury car sales units

BMW Mercedes Benz

-

20,000

40,000

60,000

80,000

100,000

CY2015 CY2020E

35,300

87,300

Luxury car segment growth expecta�ons

Luxury cars volume

Force MotorsAutomobile

Demand to come from revival in economy, normal monsoon and new product launches

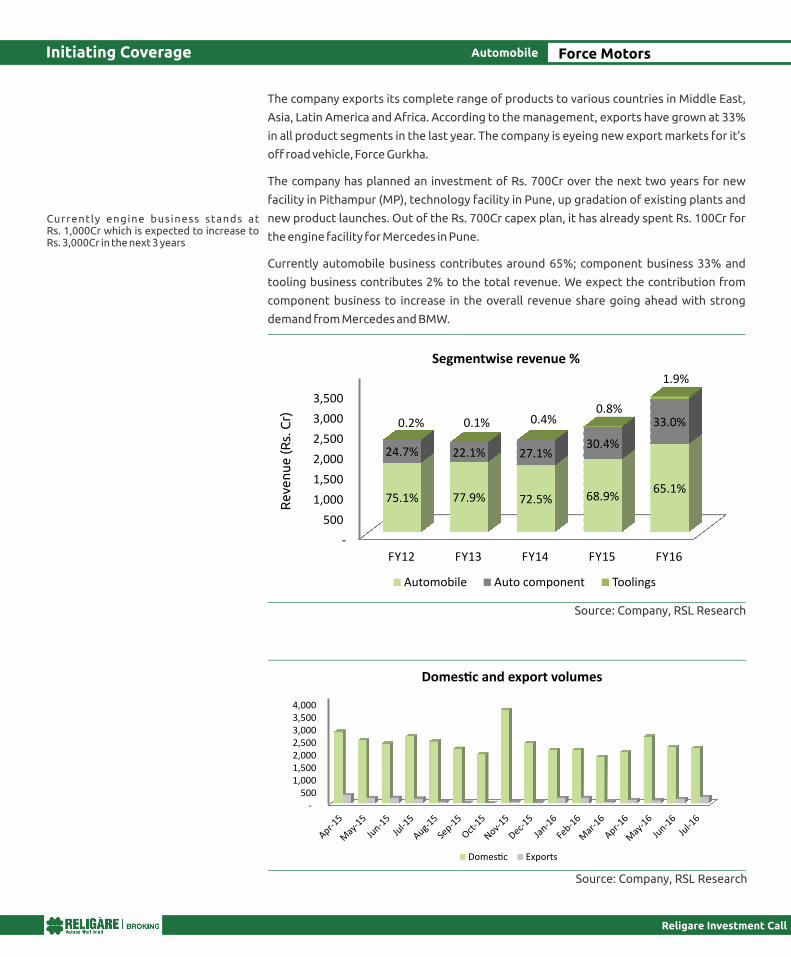

The company exports its complete range of products to various countries in Middle East,

Asia, Latin America and Africa. According to the management, exports have grown at 33%

in all product segments in the last year. The company is eyeing new export markets for it's

off road vehicle, Force Gurkha.

The company has planned an investment of Rs. 700Cr over the next two years for new

facility in Pithampur (MP), technology facility in Pune, up gradation of existing plants and

new product launches. Out of the Rs. 700Cr capex plan, it has already spent Rs. 100Cr for

the engine facility for Mercedes in Pune.

Currently automobile business contributes around 65%; component business 33% and

tooling business contributes 2% to the total revenue. We expect the contribution from

component business to increase in the overall revenue share going ahead with strong

demand from Mercedes and BMW.

Religare Investment Call

Initiating Coverage

Segmentwise revenue %

Source: Company, RSL Research

Force MotorsAutomobile

- 500

1,000 1,500 2,000 2,500 3,000 3,500 4,000

Domes�c and export volumes

Domes�c Exports

Source: Company, RSL Research

Currently engine business stands at Rs. 1,000Cr which is expected to increase to Rs. 3,000Cr in the next 3 years

-

500

Re

ven

ue

(R

s. C

r)

1,000

1,500

2,000

2,500

3,000

3,500

FY12 FY13 FY14 FY15 FY16

75.1% 77.9% 72.5% 68.9%65.1%

24.7% 22.1% 27.1%30.4%

33.0%0.2% 0.1% 0.4% 0.8%

1.9%

Automobile Auto component Toolings

4. Foreign and domestic collaborations aid in technological developments:

Over the years, the company has collaborated with different foreign and domestic

companies for technological assistance and development. Earlier it entered into a JV with

MAN (Man Truck and Bus AG) into heavy commercial vehicles segment but later, the

company ceased to be a JV partner with MAN. Force also entered into a licensing

agreement with Daimler AG, Germany for drawings and designs of vehicles (excluding

engine and transmission systems) in MPV category. It obtained technical assistance from

M/s. AVL, Graz, Austria for the engineering and development of a series of common rail

engines capable of BS IV/Euro IV emission norms, further enhancement and reliability,

strength and life cycle of the engines.

It also received technology assistance from Magna Steyr India Pvt. Ltd. for up gradation of

transmissions. Force had a license agreement with ZF Friedrichshafen AG, Germany for the

technology for truck gearboxes. Even though the agreement has ended, it has the right to

continue to manufacture the products.

The company has set up 'Advanced Technology Centre' at Akurdi for engine and vehicle

testing. It undertakes project work on design, development and up gradation of engine

configurations in various displacements and capacities. The company spends around 3-4%

of the operational turnover on Research and Development for new products including

expenditure on tool engineering. It has made satisfactory progress in developing a

complete range of engines, with various displacement capacities such as 2 litres, 2.6 litres

and 3.2 litres. These engines are capable of meeting BS V and BS VI emission regulations. It

is also developing light weight vans in T-2 range of Traveller vehicles and other seating

capacities. The Company continues to maintain its emphasis on research, development and

tool engineering activities. It has been launching new vehicles with latest and upgraded

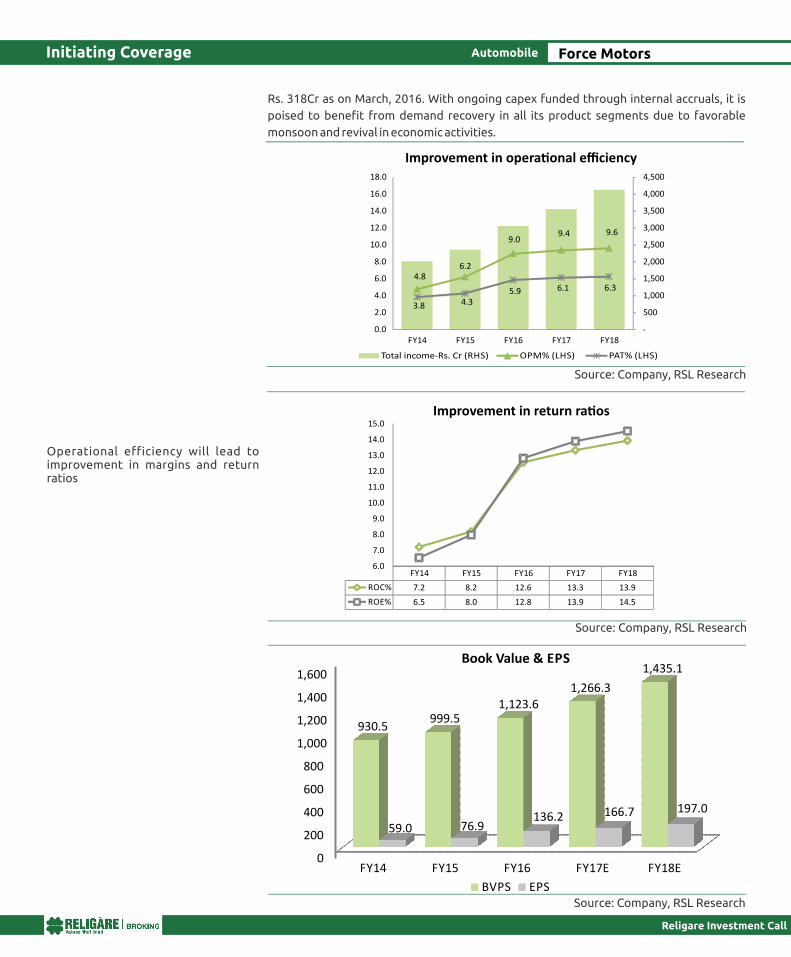

technologies. 5. Operational efficiency to improve with increasing topline:

We expect the company to report revenue and profit CAGR of 16.2% and 20% respectively

over FY16-18E. The company's profit margin is expected to improve from 5.9% currently to

6.3% in FY18E due to change in product mix and higher capacity utilisation. Going forward,

we expect it to generate healthy cash flows and improve its return ratios. It has a robust

balance sheet with stable working capital cycle and cash and cash equivalents balance of

Religare Investment Call

Initiating Coverage

Source: Company, RSL Research

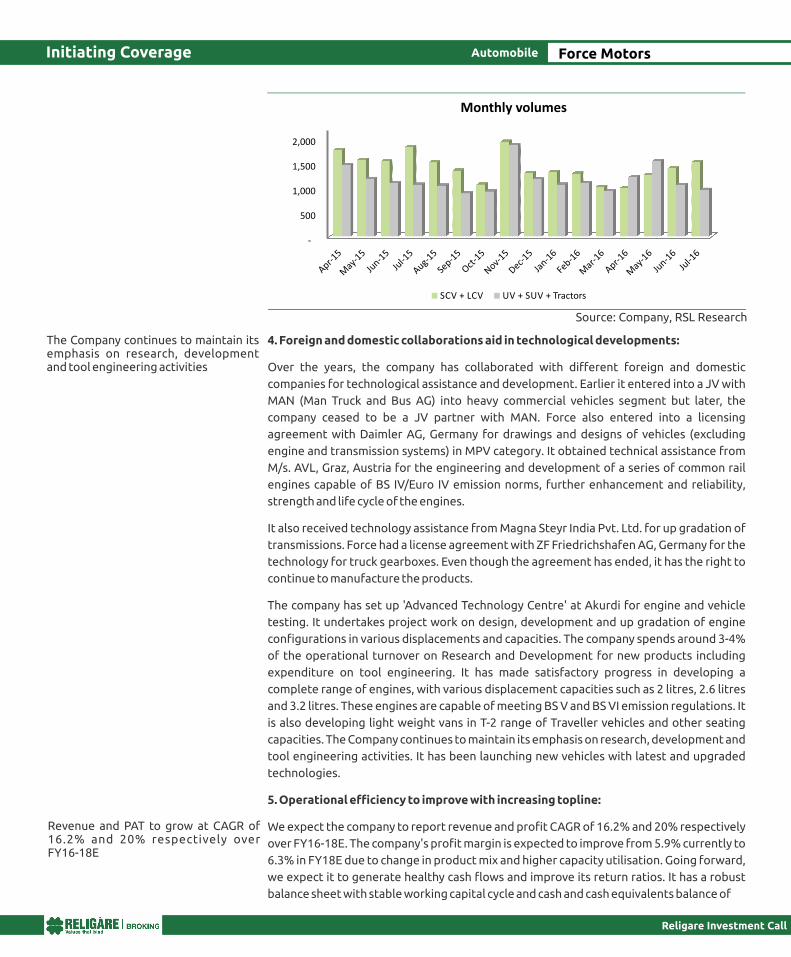

-

500

1,000

1,500

2,000

Monthly volumes

SCV + LCV UV + SUV + Tractors

Force MotorsAutomobile

The Company continues to maintain its emphasis on research, development and tool engineering activities

Revenue and PAT to grow at CAGR of 16.2% and 20% respectively over FY16-18E

Rs. 318Cr as on March, 2016. With ongoing capex funded through internal accruals, it is

poised to benefit from demand recovery in all its product segments due to favorable

monsoon and revival in economic activities.

Religare Investment Call

Initiating Coverage

Source: Company, RSL Research

Source: Company, RSL Research

Force MotorsAutomobile

Total income-Rs. Cr (RHS) OPM% (LHS) PAT% (LHS)

0

200

400

600

800

1,000

1,200

1,400

1,600

FY14 FY15 FY16 FY17E FY18E

930.5999.5

1,123.61,266.3

1,435.1

59.0 76.9136.2 166.7 197.0

BVPS EPSSource: Company, RSL Research

Improvement in opera�onal efficiency

Improvement in return ra�os

Book Value & EPS

Operational efficiency will lead to improvement in margins and return ratios

FY14 FY15 FY16 FY17 FY18

ROC% 7.2 8.2 12.6 13.3 13.9

ROE% 6.5 8.0 12.8 13.9 14.5

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

4.86.2

9.09.4 9.6

3.8 4.35.9 6.1 6.3

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY14 FY15 FY16 FY17 FY18

Religare Investment Call

Initiating Coverage

Force MotorsAutomobile

Company background

Force Motors Ltd. (FML) is a fully, vertically integrated automobile company specializing in

manufacture of Small Commercial Vehicles (SCV), Multi-Utility Vehicles (MUV), Light

Commercial Vehicles (LCV), Sports Utility Vehicles (SUV) and Agricultural tractors. It also

has expertise in design, development and manufacture of the full spectrum of automotive

components and aggregates. Under Automotive parts, the company produces engines,

transmissions and axles for luxury car segments of companies. The company has been a

pioneer in the field of light commercial vehicle with its iconic brands such as the Tempo,

Matador and the Minidor.

Some of the popular brand in SCV, MUV and LCV includes Traveller, Trax and Force Gurkha.

In tractor segment, Balwan and Orchard are the primary brands. Apart from these, the

company also assembles engines and axles for Mercedes and BMW in India.

The company has 5 manufacturing facilities located at Akurdi (Maharashtra), Pithampur

(Madhya Pradesh), Urse (Maharashtra), Chengalpattu (Tamil Nadu) and Chakan

(Maharashtra).

Risk and concerns:

Slowdown in Automobile industry will impact sales of the company in all of its product

segments. Delay in demand recovery from rural areas can impact tractor business.

Changing emission and regulatory norms can negatively impact its business. According

to SIAM, ban on registration of diesel vehicles above 2,000 CC in NCR impacted the

auto industry by Rs. 4,000Cr.

Slowdown in luxury car segment can impact its engine assembling business. Also entry

of new global players will increase competition for luxury vehicles market.

Force Motors is a fully, vertically integrated automobile company specializing in manufacture of SCV, MUV, LCV, SUV and Agricultural tractors

Source: Company

Religare Investment Call

Initiating Coverage

Particulars, Rs cr FY14

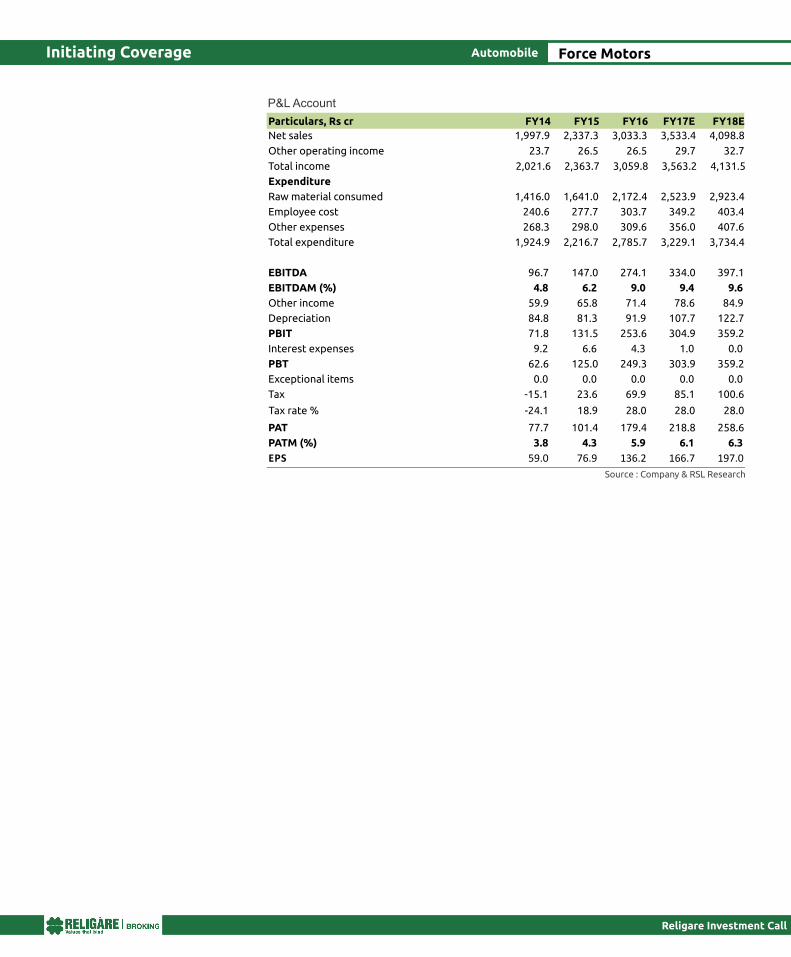

Total income

Net sales

Other operating income

2,021.6

1,997.9

23.7

Expenditure

Raw material consumed 1,416.0

Employee cost 240.6

Other expenses 268.3

Total expenditure 1,924.9

EBITDA 96.7

EBITDAM (%) 4.8

Other income 59.9

Depreciation 84.8

PBIT 71.8

Interest expenses 9.2

PBT 62.6

Exceptional items 0.0

Tax

Tax rate %

-15.1

-24.1

PAT 77.7

PATM (%) 3.8

EPS 59.0

FY15 FY16 FY17E FY18E

2,363.7

2,337.3

26.5

3,059.8

3,033.3

26.5

3,563.2

3,533.4

29.7

4,131.5

4,098.8

32.7

1,641.0 2,172.4 2,523.9 2,923.4

277.7 303.7 349.2 403.4

298.0 309.6 356.0 407.6

2,216.7 2,785.7 3,229.1 3,734.4

147.0 274.1 334.0 397.1

6.2 9.0 9.4 9.6

65.8 71.4 78.6 84.9

81.3 91.9 107.7 122.7

131.5 253.6 304.9 359.2

6.6 4.3 1.0 0.0

125.0 249.3 303.9 359.2

0.0 0.0 0.0 0.0

23.6

18.9

69.9

28.0

85.1

28.0

100.6

28.0

101.4 179.4 218.8 258.6

4.3 5.9 6.1 6.3

76.9 136.2 166.7 197.0

Source : Company & RSL Research

P&L Account

Force MotorsAutomobile

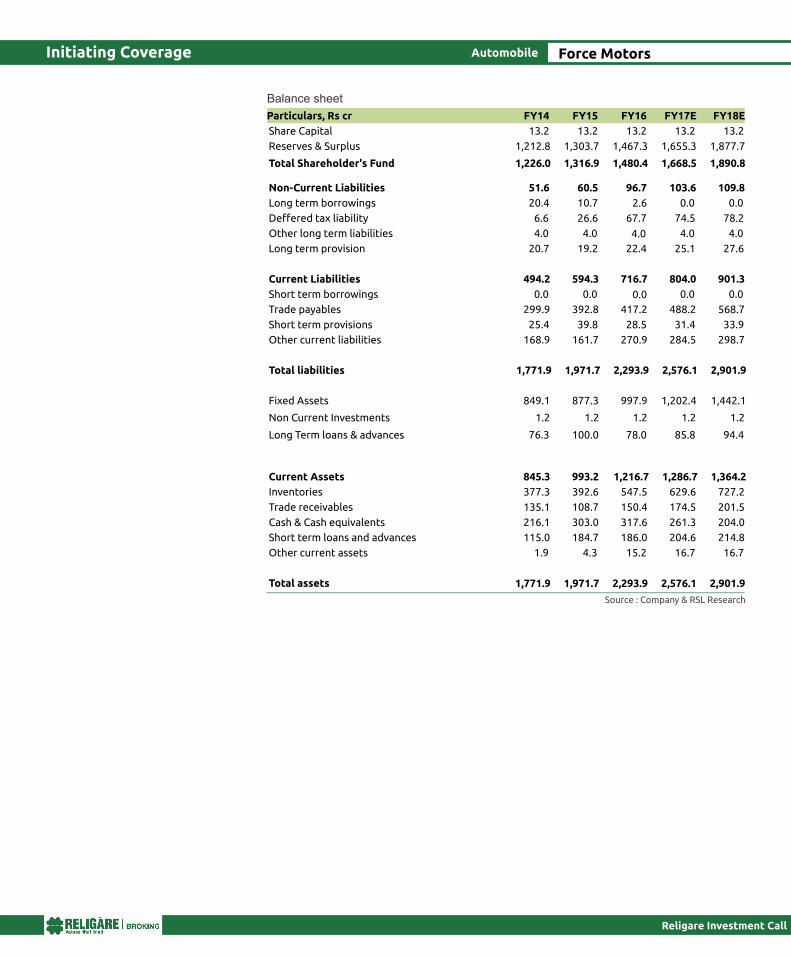

Balance sheet

Initiating Coverage

Religare Investment Call

Particulars, Rs cr FY14 FY15 FY16 FY17E FY18E

Share Capital 13.2 13.2 13.2 13.2 13.2

Reserves & Surplus 1,212.8 1,303.7 1,467.3 1,655.3 1,877.7

Total Shareholder's Fund 1,226.0 1,316.9 1,480.4 1,668.5 1,890.8

Non-Current Liabilities 51.6 60.5 96.7 103.6 109.8

Long term borrowings 20.4 10.7 0.02.6

4.0

0.0

0.0

Deffered tax liability 6.6 26.6 67.7 74.5 78.2

Other long term liabilities 4.0 4.0 4.0 4.0

Long term provision 20.7 19.2 22.4 25.1 27.6

Current Liabilities 494.2 594.3 716.7 804.0 901.3

Short term borrowings 0.0 0.0 0.0 0.0

Trade payables 299.9 392.8 417.2 488.2 568.7

Short term provisions 25.4 39.8 28.5 31.4 33.9

Other current liabilities 168.9 161.7 270.9 284.5 298.7

Total liabilities 1,771.9

1,771.9

1,971.7

1,971.7

2,293.9

2,293.9

2,576.1

2,576.1

2,901.9

2,901.9

Fixed Assets 849.1 877.3 997.9 1,202.4 1,442.1

Non Current Investments

Long Term loans & advances

1.2

76.3

1.2

100.0

1.2

78.0

1.2

85.8

1.2

94.4

Current Assets 845.3 993.2 1,216.7 1,286.7 1,364.2

Inventories 377.3 392.6 547.5 629.6 727.2

Trade receivables 135.1 108.7 150.4 174.5 201.5

Cash & Cash equivalents 216.1 303.0 317.6 261.3 204.0

Short term loans and advances 115.0 184.7 186.0 204.6 214.8

Other current assets 1.9 4.3 15.2 16.7 16.7

Total assets

Source : Company & RSL Research

Force MotorsAutomobile

Cash Flow statement

Initiating Coverage

Religare Investment Call

Particulars, Rs cr FY14 FY15 FY16 FY17E FY18E

Profit Before Tax 62.6 124.9 249.3 303.9 359.2

Add: Depreciation 84.8 81.3 91.9 107.7 122.7

Add: Interest cost -5.5 -14.1 4.3 1.0 0.0

Others 1.0 1.1 -2.0 0.0 0.0

Op profit before working capital changes 143.0 193.3 343.6 412.6 481.9

Changes In working Capital -25.2 65.1 -39.5 -41.1 -43.7

Direct taxes -2.1 -32.4 -69.9 -85.1 -100.6

Cash Flow From Operating Activities 115.7 226.0 234.2 286.5 337.7

Cash Flow from Investing Activities

Purchase of Fixed assets -128.2 -117.3 -177.1 -300.0 -350.0

Sale of Fixed assets 13.9 0.3 0.0 0.0 0.0

Others 14.8 20.8 0.0 -8.4 -8.7

Cash Flow from Investing Activities -99.6 -96.2 -177.1 -308.4 -358.7

Cash from Financing Activities

Net proceeds from borrowings -16.1 -31.6 -8.1 -2.6 0.0

Dividend (incl dividend tax) -4.6 -4.6 -23.1 -30.7 -36.3

Interest cost -9.5 -8.3 -4.3 -1.0 0.0

Cash Flow from Financing Activities -30.2 -44.6 -35.5 -34.4 -36.3

Net Cash Inflow / Outflow -14.1 85.2 21.6 -56.3 -57.3

Opening Cash & Cash Equivalents 225.0 210.9 296.1 317.6 261.3

Closing Cash & Cash Equivalent 210.9 296.1 317.6 261.3 204.0

Source : Company & RSL Research

Force MotorsAutomobile

Religare Investment Call

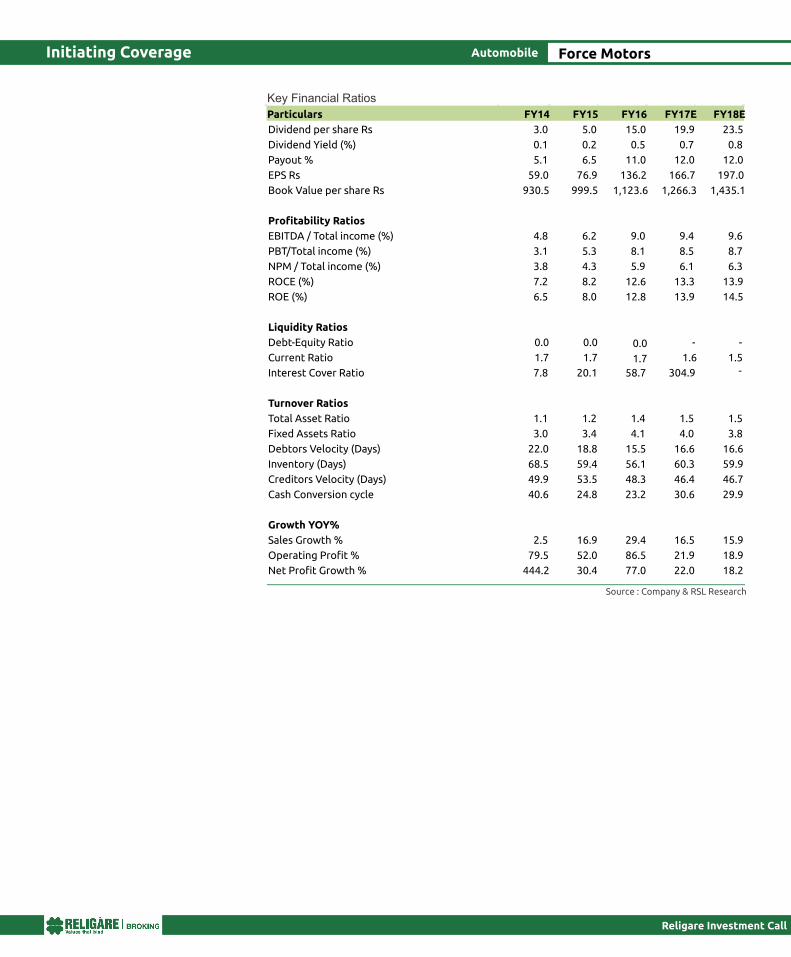

Key Financial Ratios

Initiating Coverage

Particulars FY14 FY15 FY16 FY17E FY18E

Dividend per share Rs 3.0 5.0 15.0 19.9 23.5

Dividend Yield (%) 0.1 0.2 0.5 0.7 0.8

Payout % 5.1 6.5 11.0 12.0 12.0

EPS Rs 59.0 76.9 136.2 166.7 197.0

Book Value per share Rs 930.5 999.5 1,123.6 1,266.3 1,435.1

Profitability Ratios

EBITDA / Total income (%) 4.8 6.2 9.0 9.4 9.6

PBT/Total income (%) 3.1 5.3 8.1 8.5 8.7

NPM / Total income (%) 3.8 4.3 5.9 6.1 6.3

ROCE (%) 7.2 8.2 12.6 13.3 13.9

ROE (%) 6.5 8.0 12.8 13.9 14.5

Liquidity Ratios

Debt-Equity Ratio 0.0

0.0

0.0 - -

-Current Ratio 1.7

1.7

1.7 1.6 1.5

Interest Cover Ratio 7.8 20.1 58.7 304.9

Turnover Ratios

Total Asset Ratio 1.1 1.2 1.4 1.5 1.5

Fixed Assets Ratio 3.0 3.4 4.1 4.0 3.8

Debtors Velocity (Days) 22.0 18.8 15.5 16.6 16.6

Inventory (Days) 68.5 59.4 56.1 60.3 59.9

Creditors Velocity (Days) 49.9 53.5 48.3 46.4 46.7

Cash Conversion cycle 40.6 24.8 23.2 30.6 29.9

Growth YOY%

Sales Growth % 2.5 16.9 29.4 16.5 15.9

Operating Profit % 79.5 52.0 86.5 21.9 18.9

Net Profit Growth % 444.2 30.4 77.0 22.0 18.2

Force MotorsAutomobile

Source : Company & RSL Research

Religare Investment Call

Before you use this research report , please ensure to go through thedisclosure inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulat ions , 2014 and Research Disc la imer at the fol lowing l ink : http://old.religareonline.com/research/Disclaimer/Disclaimer_RSL.htmlSpecific analyst(s) specific disclosure(s) inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulations, 2014 is/are as under:Statements on ownership and material conflicts of interest , compensation– Research Analyst (RA) [Please note that only in case of multiple RAs, if in the event answers differ inter-se between the RAs, then RA specific answer with respect to questions under F (a) to F(j) below , are given separately]

S. No. Statement Answer

Tick appropriate

I/we or any of my/our relative has any financial interest in the subject company? [If answer is yes, nature of Interestis given below this table]

I/we or any of my/our relatives, have actual/beneficial ownership of one per cent. or more securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance?

I / we or any of my/our relative, has any other material conflict of interest at the time of publication of the research report or at the time of public appearance?

I/we have received any compensation from the subject company in the past twelve months?

I/we have managed or co-managed public offering of securities for the subject company in the past twelve months?

I/we have received any compensation for brokerage services from the subject company in the past twelve months?

I/we have received any compensation for products or services other than brokerage services from the subject company in the past twelve months?

I/we have received any compensation or other benefits from the subject company or third party in connection with the research report?

I/we have served as an officer, director or employee of the subject company?

I/we have been engaged in market making activity for the subject company?

YES NO

NO

NO

NO

NO

NO

NO

NO

NO

NO

NO

Nature of Interest ( if answer to F (a) aboveis Yes : …………………………………………………………………………………………………………………………………………………............................................Name(s)with Signature(s)of RA(s).[Please note that only in case of multiple RAs andif the answers differ inter-se between the RAs, then RA specific answer with respect to questions under F (a) to F(j) above , are given below]

SS.No Name(s) of RA Signatures of RASerial Question of question which the signing RA needs

to make separate declaration / answer YES NO

Copyright in this document vests exclusively with RSL. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose, without prior written permission from RSL. We do not guarantee the integrity of any emails or attached files and are not responsible for any changes made to them by any other person.

Disclaimer: www.religareonline.com/research/Disclaimer/Disclaimer_RSL.html

Initiating Coverage Force MotorsAutomobile