Embed Size (px)

Citation preview

Page 1 of 40

INDIA October 27, 2009

K.P.R. Mill Limited is well poised for sustained growth driven by its positioning as a complete textile solutions provider; supported by a unique procurement policy with a focus on premium products that offer higher margins. The company is expanding into export markets by leveraging its vertically integrated operations to complement its growth strategy.

Founded in 1984, K.P.R. Mill Limited (KPR) is amongst the largest vertically integrated textile manufacturers in South India having a presence across the entire value chain — from fibre to fashion (including production of yarn & fabric, designing, dyeing and manufacturing of readymade garments).

The company has marquee relationships of over 15 years with about 1,000 regular domestic clients for yarn and fabric and around 40 international apparel retailers including key clients such as Tesco, Decathlon, Marks & Spencer, Primark Stores, Ernsting’s Family, Carrefour, C&A, Kiabi, 3 Suisses, Wal-Mart, SA Vetir and Coles amongst others.

First spinning mill in India to obtain all three international certifications including ISO 9001:2000, ISO 14001:2004 and SA 8000:2001 for production facilities; demonstrating strong commitment towards process excellence.

Certified as a One Star Export House by the Ministry of Commerce and Trade.

In December 2006, a consortium of private equity funds including Ares Investments, Brandot Investments and Argonaut invested about Rs 1.05bn acquiring 11% combined stake in the company.

To support expansion, KPR raised Rs 1.33bn through an IPO of 5.91mn equity shares of Rs 10 each in August 2007. The issue was priced at Rs 225 per share and was oversubscribed by 1.19 times, receiving good response from the investors.

Mr. K.P. Ramasamy, the chairman of the company, brings with him rich experience of 38 years in textile industry particularly in the production and marketing of woven fabric, knitted apparel and cotton yarn along with experience in yarn and fabric dyeing industry.

Financial Summary

Period Ending FY'06 FY'07 FY'08 FY'09 Q1 FY'09 Q1 FY'10 Total Operating Revenue *(Rs Mn)

4,391.4

4,973.9

6,063.6

7,476.9 1,723.9

1,839.0

Growth % (YoY) - 13.3% 21.9% 23.3% - 6.7%

EBITDA (Rs Mn)

1,164.5

1,358.9

1,384.2

1,096.8 383.9

363.6

EBITDA Margin (%) 26.5% 27.3% 22.8% 14.7% 22.3% 19.8%

Net Profit (Rs Mn) 755.2 584.2 793.5 101.0 119.5 65.6

Net Profit Margin (%) 17.2% 11.7% 13.1% 1.4% 6.9% 3.6%

RoE (%) 33.6% 17.6% 15.6% 2.0% - - RoCE (%)

17.7% 16.2% 8.2% 5.2% - -

Initiating Coverage (Not Rated) K.P.R. Mill Limited

CMP: Rs 76.35 Sector: Textile Fiscal Year: April-March

52-W High (Rs.) 86.0

52-W Low (Rs.) 19.1

Average Daily Volume (‘000)

1M 37.66

3M 59.71

6M 34.53

Bloomberg KPR:IN NSE KPRMILL

BSE 532889

Face Value (Rs) 10

Equity Shares (mn) 37.68 Market Cap (Rs mn) 2,877.09

Shareholding Pattern (Jun’09)

Promoters 72.4%

FIIs 0.4%

MF/ Banks 1.5% Bodies Corporate 7.1% Foreign Venture Capital Investors 9.3%

Others 9.3%

Stock Performance

-

500

1,000

1,500

2,000

Apr-09 Jul-09 Oct-09

0

30

60

90

120

Total Volume ('000) KPR M ill

Nifty (Rebased)

Revenue Mix – FY’09

Background and Business Overview

State-of-the-art Facilities Manufacturing Capacity

Business Mix (FY’09)

Production Facilities 6 state-of-the-art production facilities located in Tamilnadu

Sathyamangalam Coimbatore Karumathampatti, Neelambur & Arasur

Tirupur and Perundurai

Total capacity of 212,064 spindles; 185 circular knitting machines; and 1,750 sewing machines Manufacturing capacity of 54,000MT of yarn; 19,000MT of fabric and 63mn pieces (double shift) of readymade knitted apparel p.a. Processing facility to handle 23MT of fabric per day Installed 40 wind mills with a total power capacity of 40MW

Products: Yarn (50.9%) Knitted Garments (24.4%)

Fabric (12.6%) Others (12.1%)

Geographies:

Domestic (74.9%) Exports to markets including Europe, US and others (25.1%)

Yarn,

50.9%

Fabric,

12.6%

Garments,

24.4%

Others,

12.1%

Source: Company data, Four-S Research *Note: Total Operating Revenue includes only Operating Income and excludes ‘Other Income’

K.P.R. Mill Limited – Initiating Coverage

Page 2 of 40

Sr. No. Contents

Page Nos.

1. Investment Positives 3-5

2.

Peer Group Benchmarking

Financial Comparison on TTM Basis

Financial Comparison on Quarterly Basis

Valuation

6-9

3.

Investment Risks

Internal Risks

External Risks

10-12

4. Business Analysis 13-17

5. Growth Plans & Drivers 18-19

6. Financial Analysis

Annual Review

YTD Performance

20-24

7.

Industry Opportunity Mapping

25-27

8.

Annexures (1-10)

28-39

K.P.R. Mill Limited – Initiating Coverage

Page 3 of 40

KPR provides a unique investment opportunity to partner with an end to end textile solutions provider with vertically integrated operations in South India, spread across the entire textile value chain from fibre to fashion. The company is amongst the fastest growing textile companies in terms of FY’09 revenue growth of over 23% (YoY) as compared to peer group average growth of 12% and has maintained superior EBITDA margin at 15% as compared to peer group average margin of 10% in the same period. With a well planned strategy focusing on higher margin garment exporting business and effective cost control measures, KPR is strongly positioned to witness substantial increase in its revenues and profitability.

Improving market environment with huge opportunity in the offing With estimated investments of Rs 69bn (CII Estimates) in textile projects during the current financial year, the Indian textile industry is expected to come out of the lull phase of FY’09. The revival in growth is based on the following key drivers:

Increased sourcing from India by top global retailers with improving export demand for products on the back of positive consumer sentiment in the developed economies. India’s total apparel export to USA increased by 5% to reach 584mn units in the first seven months of CY2009, compared to the corresponding period in CY2008.

Despite global economic slowdown affecting the overall textile exports in FY’09, India was able to grow its readymade garments exports (the key focus area of KPR) at 13% YoY to $10.24bn during FY’09. Garment exports (accounting for about 49% of the country’s total textile exports) are expected to drive growth in sourcing from India, at an annual average rate of 12% to reach $35bn-$37bn by 2011. (Source: CII - Ernst & Young Textiles and Apparel Report)

Strong support extended from the Government of India (GoI) in the form of stimulus packages including: Fresh allocation of Rs 14bn for Technology Upgradation Fund Scheme

(TUFS) to quicken subsidy release; in August 2009, GoI released Rs 25.5bn against pending TUFS dues;

Increased allocation for market development assistance scheme to Rs 1.24bn in 2009-10;

Interest subvention of 2% on pre-shipment and post-shipment credit; Extension of the duty entitlement pass book (DEPB) scheme till December

2009, with an increase of rates by 3%; Imposition of anti-dumping duty of up to $527 per ton on yarn and fabric

imported from China, to discourage imports.

Stabilising prices of domestic cotton which have come down by 20% from peak prices of Rs 79.6/per kg (long staple) in FY’09 coupled with a comfortable cotton crop, projected at 30-32mn bales for the new 2009-10 season which would further push prices down thereby increasing price competitiveness of Indian products.

Well positioned to benefit from strategic initiatives underway

KPR increased focus on its key export markets of EU & USA and is developing new markets in Australia:

Growth in exports to large and long term customers by leveraging long standing client relationships of over 15 years. The company was able to increase billing with a number of major clients such as Primark, Carrefour, 3 Suisses, etc; resulting in 25% YoY increase in total revenues from top 10 clients to Rs 1,448mn in FY’09. This was possible because of the company’s premium quality products, track record of timely delivery and strict adherence to compliance norms.

Investment Positives

Investments worth Rs 69bn in textile projects estimated

during FY’10

Readymade Garment exports grew at 13% YoY to

reach $10.24bn in FY’09

Long staple (Shankar-6) cotton prices down 20%

from peak of FY’09

Total export revenues from Top 10 clients increased

25% YoY in FY’09

K.P.R. Mill Limited – Initiating Coverage

Page 4 of 40

Addition of new clients such as Tesco, Decathlon, Coles, etc resulted in export order flow of Rs 302mn during FY’09. The company has an outstanding order book of Rs 1,000mn as of September 2009.

KPR increased its export revenues by 27% YoY to reach Rs 1.8bn in FY’09 and further plans to grow it to Rs 4.7bn by FY’12, contributing 40% to the total revenues with the backing of a large in-house marketing team. The key marketing personnel make regular visits across Europe & US to maintain personal contact and obtain regular feedback from KPR’s major clients.

The company scaled up operations under garmenting (the highest value add

segment with 22%-25% margins) for in-house execution of the bulk orders from large clients. It has recently set up a dedicated garment manufacturing facility at Arasur plant with a capacity of 85,000 pieces (single shift) per day. The plant is currently operating at a capacity utilization of 60% providing significant potential to meet growing demand in the segment. The contribution from garment exports, increased from 18% (Rs 293.2mn) of the company’s total sales in Q1 FY’09 to around 34% (Rs 603.5mn) in Q1 FY’10.

Low cost operations to drive improvement in margins

KPR follows a unique procurement policy of purchasing substantially all of its raw materials during the start of the cotton year (Oct-Sep) which ensures highest quality at lower prices due to abundant supply. The company procured high quality Shankar-6 cotton at Rs 22,500 per candy (excluding transportation cost) as against its minimum support price (MSP) of Rs 24,000 per candy in FY’09.

The company has a specialist procurement advisory team based in Gujarat to help in buying decisions after thorough inspection, testing and verification of the quality.

KPR has installed 40 windmills with total captive power generation capacity of 40MW (sufficient to meet around 75% of its power requirement operating at full capacity) so as to combat the excessive power shortage in the state of Tamil Nadu. With one of the largest in-house power capacities in southern India, the company achieves substantial self sufficiency in generating power which lowers the energy cost. KPR’s power cost as a percentage of revenue stood at just 3% compared to the industry average of 6% during FY’09.

The company is involved in continuous technological upgradation for efficient operations in order to reduce manpower requirements; resulting in employee cost at 6.6% as a percentage of revenues, compared to the industry average of 10% in FY’09. In addition to above, KPR follows a distinct ‘employee motivation model’ which helps to keep its attrition rate below 1% as compared to industry average of 10%.

KPR has created strong execution capabilities to achieve economies of scale

and synergies in operations. The company has been successfully implementing its capacity expansion programmes leading to cost savings and improvement in overall margins.

Export revenues to increase from Rs 1.8bn in FY’09 to

Rs 4.7bn in FY’12

High margin (22%-25%) garment division

contributed 34% of total revenues in Q1 FY’10

Captive power of 40MW to keep energy costs low and

combat power shortage

Lowest attrition rate and personnel cost

1,159

1,448

400

800

1200

1600

FY'08 FY'09

Increase in Contribution from Top Clients (Rs Mn)

Source: Company data, Four-S Research

25%

K.P.R. Mill Limited – Initiating Coverage

Page 5 of 40

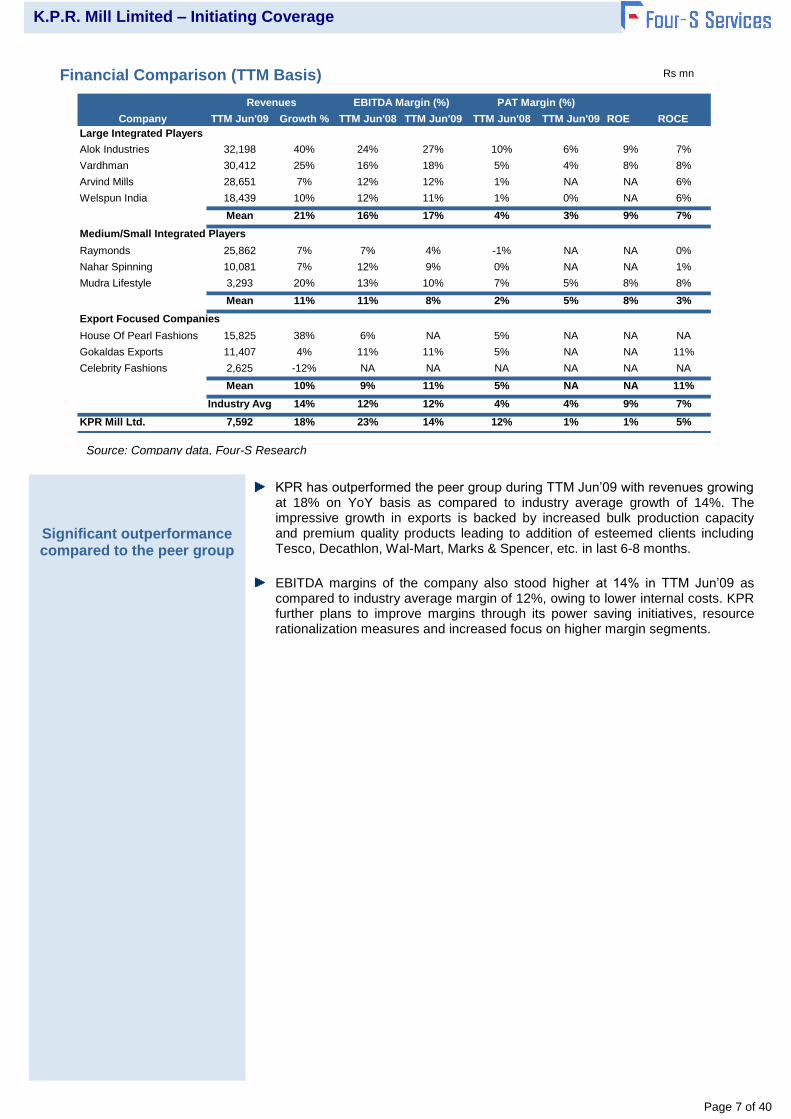

Strong competitive positioning with significant out performance compared to the peer group KPR, being the largest supplier of yarn and fabric in Tirupur market, outperformed its peer group in both revenue growth (18% YoY during TTM Jun’09 as compared to peer group average of 14%) as well as EBITDA margins (14% for TTM Jun’09 as compared to peer group average of 12%) based on the following:

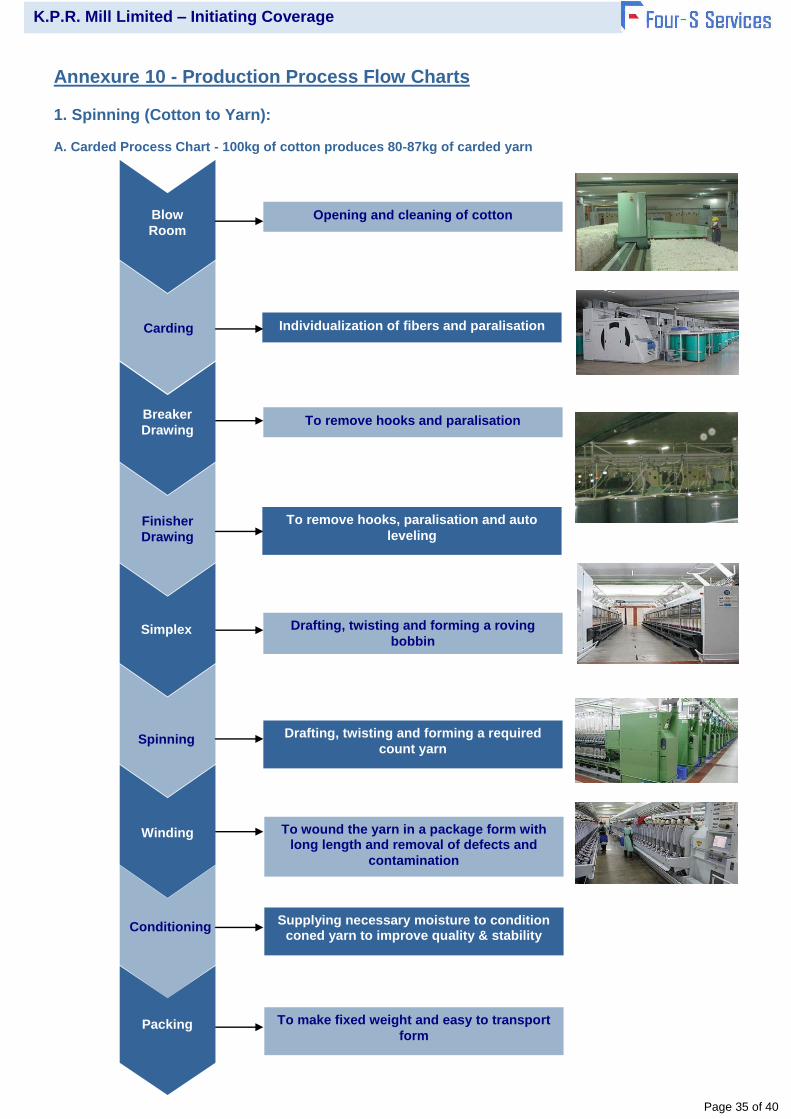

The company has developed one of the largest vertically integrated operations in South India with a total manufacturing capacity of 212,064 spindles; 185 circular knitting machines; 1,750 sewing machines with approx. 63mn pieces of readymade knitted apparel (51mn pieces in-house operating double shift and 12mn outsourced); 54,000MT of yarn making and production of 19,000MT of fabric p. a. along with processing facility to handle 23MT of fabric per day. Its presence across the entire textile manufacturing value chain helps to meet end to end requirements of clients; offering spinning, knitting & garmenting at one location.

All of KPR’s operations are strategically located within a 50km radius around Tirupur, regarded as one of Asia’s largest apparel manufacturing clusters. The close proximity to buyers helps to reduce the material handling costs and facilitates immediate feedback regarding the quality of the product. The location of the facilities helps to utilize the key technical personnel across all plant sites and allows taking advantage of Coimbatore’s climate, conducive for spinning operations.

With its captive power production and distinct workforce model, KPR achieves significant cost competitiveness as compared to its peers leading to an overall reduction in the operating costs of the company.

The company strongly emphasizes quality control to achieve zero defects, which results in premium pricing for its yarn and fabric (2% - 3% higher than the average market price) and repeat orders for its products. KPR has received various international accreditations and recognitions for its process and quality excellence.

Minimal capex requirement to double revenues

The company successfully completed Rs 5.44bn Phase-I of its capex program during FY’08 and has further expended Rs 609.9mn during FY’09. It has already created excess capacity across segments to meet any increase in demand. Additional capex will be required only after the present facilities reach their optimum utilization levels, which currently hovers around 60%-65%.

Professional management team to spearhead future growth

The 16-member core management team (including board of directors and key managerial personnel - see Annexure on Page 32 for details) at KPR brings with it a rich experience of 1-4 decades and domain expertise acquired in world class organizations in the textile industry. Mr. K.P. Ramasamy, the chairman, has rich industry experience in manufacturing and marketing across all the product segments and holds memberships in many key industry associations such as Southern India Mills' Association (SIMA).

Revenue growth of 18% YoY in TTM Jun’09 as compared to industry average of 14%

Vertically integrated operations

Strong promoter and management background

K.P.R. Mill Limited – Initiating Coverage

Page 6 of 40

Company Cotton / Polyester

Yarn

Fabrics Designing Dyeing Readymade Garments /

Home Furnishing

Retailing

Large Integrated Players

Alok Industries

Vardhman

Arvind Mills

Welspun India

Medium/Small Integrated

Players

Raymonds

Nahar Spinning

Mudra Lifestyle

Export Focused Companies

House Of Pearl Fashions

Gokaldas Exports

Celebrity Fashions

KPR Mill Ltd.

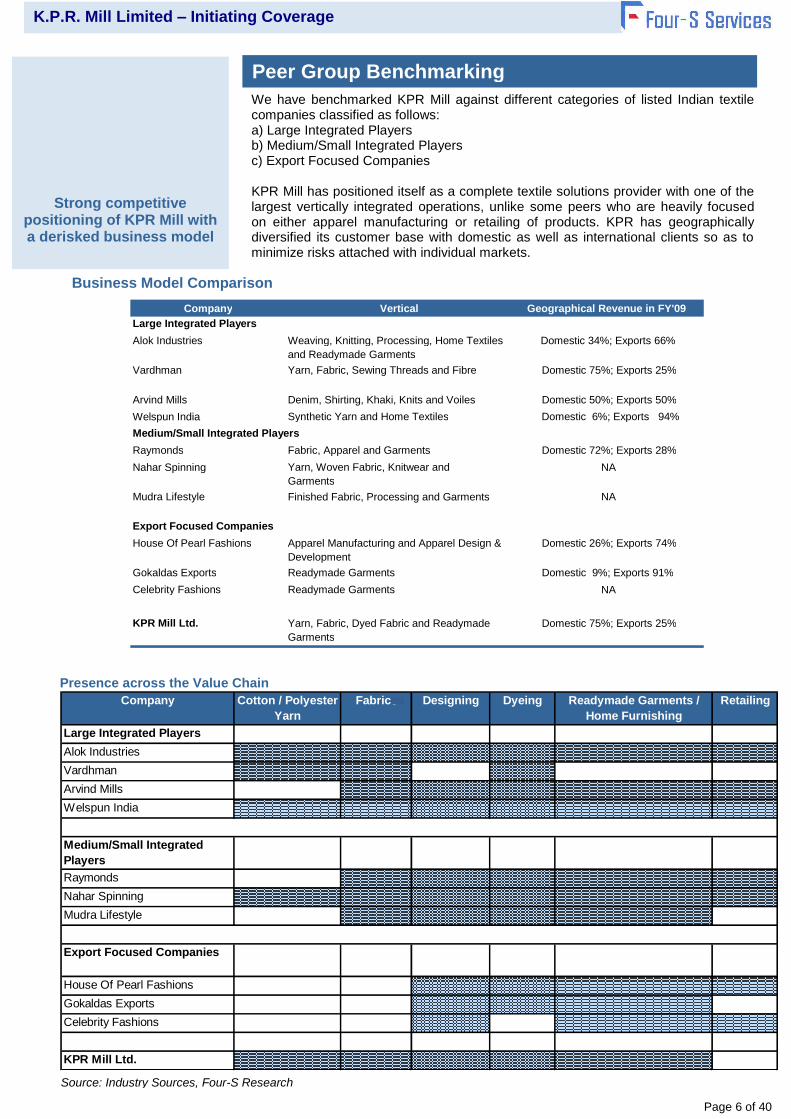

We have benchmarked KPR Mill against different categories of listed Indian textile companies classified as follows: a) Large Integrated Players b) Medium/Small Integrated Players c) Export Focused Companies KPR Mill has positioned itself as a complete textile solutions provider with one of the largest vertically integrated operations, unlike some peers who are heavily focused on either apparel manufacturing or retailing of products. KPR has geographically diversified its customer base with domestic as well as international clients so as to minimize risks attached with individual markets.

Business Model Comparison

Presence across the Value Chain

Peer Group Benchmarking

Strong competitive positioning of KPR Mill with a derisked business model

Source: Company data, Four-S Research

Source: Industry Sources, Four-S Research

Company Vertical Geographical Revenue in FY'09 Large Integrated Players Alok Industries Weaving, Knitting, Processing, Home Textiles

and Readymade Garments Domestic 34%; Exports 66%

Vardhman Yarn, Fabric, Sewing Threads and Fibre Domestic 75%; Exports 25%

Arvind Mills Denim, Shirting, Khaki, Knits and Voiles Domestic 50%; Exports 50% Welspun India Synthetic Yarn and Home Textiles Domestic 6%; Exports 94% Medium/Small Integrated Players Raymonds Fabric, Apparel and Garments Domestic 72%; Exports 28% Nahar Spinning Yarn, Woven Fabric, Knitwear and

Garments NA

Mudra Lifestyle Finished Fabric, Processing and Garments NA

Export Focused Companies House Of Pearl Fashions Apparel Manufacturing and Apparel Design &

Development Domestic 26%; Exports 74%

Gokaldas Exports Readymade Garments Domestic 9%; Exports 91% Celebrity Fashions Readymade Garments NA

KPR Mill Ltd. Yarn, Fabric, Dyed Fabric and Readymade Garments

Domestic 75%; Exports 25%

K.P.R. Mill Limited – Initiating Coverage

Page 7 of 40

TTM Jun'09 Growth % TTM Jun'08 TTM Jun'09 TTM Jun'08 TTM Jun'09 ROE ROCE

Large Integrated Players

Alok Industries 32,198 40% 24% 27% 10% 6% 9% 7%

Vardhman 30,412 25% 16% 18% 5% 4% 8% 8%

Arvind Mills 28,651 7% 12% 12% 1% NA NA 6%

Welspun India 18,439 10% 12% 11% 1% 0% NA 6%

Mean 21% 16% 17% 4% 3% 9% 7%

Medium/Small Integrated Players

Raymonds 25,862 7% 7% 4% -1% NA NA 0%

Nahar Spinning 10,081 7% 12% 9% 0% NA NA 1%

Mudra Lifestyle 3,293 20% 13% 10% 7% 5% 8% 8%

Mean 11% 11% 8% 2% 5% 8% 3%

Export Focused Companies

House Of Pearl Fashions 15,825 38% 6% NA 5% NA NA NA

Gokaldas Exports 11,407 4% 11% 11% 5% NA NA 11%

Celebrity Fashions 2,625 -12% NA NA NA NA NA NA

Mean 10% 9% 11% 5% NA NA 11%

Industry Avg 14% 12% 12% 4% 4% 9% 7%

KPR Mill Ltd. 7,592 18% 23% 14% 12% 1% 1% 5%

Revenues

Company

EBITDA Margin (%) PAT Margin (%)

Financial Comparison (TTM Basis)

KPR has outperformed the peer group during TTM Jun’09 with revenues growing at 18% on YoY basis as compared to industry average growth of 14%. The impressive growth in exports is backed by increased bulk production capacity and premium quality products leading to addition of esteemed clients including Tesco, Decathlon, Wal-Mart, Marks & Spencer, etc. in last 6-8 months.

EBITDA margins of the company also stood higher at 14% in TTM Jun’09 as

compared to industry average margin of 12%, owing to lower internal costs. KPR further plans to improve margins through its power saving initiatives, resource rationalization measures and increased focus on higher margin segments.

Significant outperformance compared to the peer group

Source: Company Data, Four-S Research

Source: Company data, Four-S Research

Rs mn

K.P.R. Mill Limited – Initiating Coverage

Page 8 of 40

Revenues Revenue

Q1 FY'10 Growth % Q1 FY'09 Q1 FY'10 Q1 FY'09 Q1 FY'10

Alok Industries 7,863 45% 25% 27% 5% 4%

Vardhman 6,241 10% 16% 18% 1% 6%

Arvind Mills 6,749 24% 10% 13% 1% 1%

Welspun India 4,178 47% 20% 24% 2% 8%

Mean 31% 18% 21% 2% 5%

Raymonds 2,399 0% NA NA NA NA

Nahar Spinning 2,581 1% 13% 14% 1% 3%

Mudra Lifestyle 904 38% 11% 10% 5% 0%

Mean 13% 12% 12% 3% 2%

House Of Pearl Fashions 4,452 36% 5% NA 3% NA

Gokaldas Exports 2,572 -11% 16% 9% 4% 1%

Celebrity Fashions 537 14% NA NA NA NA

Mean 13% 10% 9% 4% 1%

Industry

Mean

19% 13% 14% 3% 3%

KPR Mill Ltd. 1,839 7% 22% 20% 7% 4%

Company

EBITDA Margin (%) PAT Margin (%)

Medium/Small Integrated Players

Large Integrated Players

Export Focused Companies

Quarterly Comparison

Highest EBITDA margins among medium/small integrated and export focused players…

KPR continued to maintain higher margins compared to its peer group during the quarter ended Jun’09. The company has witnessed higher EBITDA margin of 20% in Q1 FY’10 as compared to industry average margin of 14% during the same period. Also the net margins of the company stood higher at 4% as compared to industry average of 3% in Q1 FY’10.

Highest operating margins compared to industry average in Q1 FY’10

Source: Company data, Four-S Research

Source: Company data, Four-S Research

Rs mn

K.P.R. Mill Limited – Initiating Coverage

Page 9 of 40

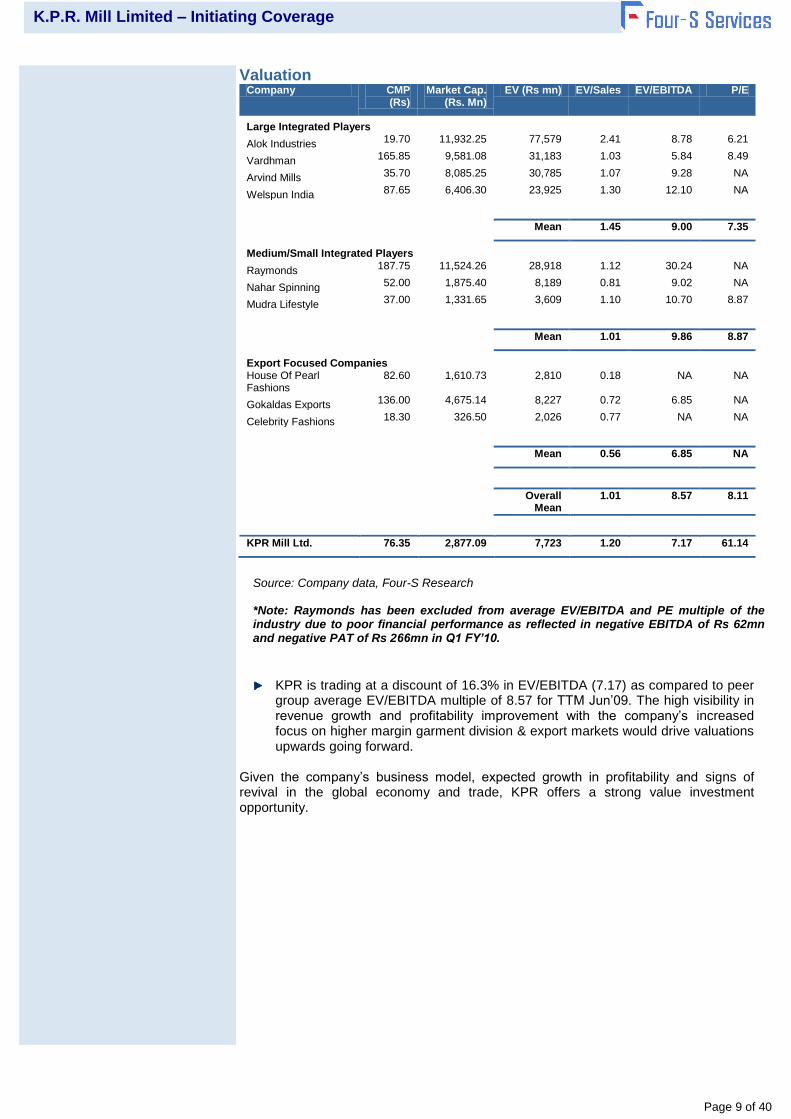

Valuation Company CMP

(Rs) Market Cap.

(Rs. Mn) EV (Rs mn) EV/Sales EV/EBITDA P/E

Large Integrated Players

Alok Industries 19.70 11,932.25 77,579 2.41 8.78 6.21

Vardhman 165.85 9,581.08 31,183 1.03 5.84 8.49

Arvind Mills 35.70 8,085.25 30,785 1.07 9.28 NA

Welspun India 87.65 6,406.30 23,925 1.30 12.10 NA

Mean 1.45 9.00 7.35

Medium/Small Integrated Players

Raymonds 187.75 11,524.26 28,918 1.12 30.24 NA

Nahar Spinning 52.00 1,875.40 8,189 0.81 9.02 NA

Mudra Lifestyle 37.00 1,331.65 3,609 1.10 10.70 8.87

Mean 1.01 9.86 8.87

Export Focused Companies

House Of Pearl Fashions

82.60 1,610.73 2,810 0.18 NA NA

Gokaldas Exports 136.00 4,675.14 8,227 0.72 6.85 NA

Celebrity Fashions 18.30 326.50 2,026 0.77 NA NA

Mean 0.56 6.85 NA

Overall

Mean 1.01 8.57 8.11

KPR Mill Ltd. 76.35 2,877.09 7,723 1.20 7.17 61.14

KPR is trading at a discount of 16.3% in EV/EBITDA (7.17) as compared to peer group average EV/EBITDA multiple of 8.57 for TTM Jun’09. The high visibility in revenue growth and profitability improvement with the company’s increased focus on higher margin garment division & export markets would drive valuations upwards going forward.

Given the company’s business model, expected growth in profitability and signs of revival in the global economy and trade, KPR offers a strong value investment opportunity.

Source: Company data, Four-S Research *Note: Raymonds has been excluded from average EV/EBITDA and PE multiple of the industry due to poor financial performance as reflected in negative EBITDA of Rs 62mn and negative PAT of Rs 266mn in Q1 FY’10.

K.P.R. Mill Limited – Initiating Coverage

Page 10 of 40

Internal Risks

Geographical concentration of export revenues The company derives majority of its export revenues (90% in FY’09) from the European countries, and is subject to risks relating to political, economic, legal and regulatory conditions in the region. Mitigate: The company is increasing its focus on export markets of US and Australia. It is in the process of negotiations with a few leading retailers in these regions, which are expected to enhance the export order book of the company. In addition, the company is also planning to achieve greater diversification in European markets by exploring new areas in that continent. Lack of long term contracts with suppliers or customers KPR’s dealings with its suppliers and customers are primarily on an order to order basis. The company has not entered into any long term agreements with respect to procurement of raw material from suppliers or sale of goods to customers. The company’s performance might be significantly impacted in the event of attrition among its suppliers or customers.

Mitigate: The company maintains strong relationships with its clients, developed over a long period of time. This is reflected in the YoY growth of over 23% in FY’09 revenues despite the slowdown, with export revenue contribution from its top client increasing to 42% in FY’09, up from 34% in FY’08. Addition of new clients such as Tesco, Decathlon, Coles, etc has helped to diversify its client base. KPR follows the policy of procuring raw materials directly from the suppliers without any middlemen, thus gaining cost benefits. The company has a dedicated procurement team to advice on the best quality purchases. Impact on sale of yarn and fabric products carried out through third-party agents

KPR depends in part on third-party sales agents especially for initial contact with new customers. The agents promote the company’s products among clients in the Tirupur region, which accounts for a major portion of total sales of yarn and fabric products. The company has no agreements in place with the sales agents and they are not exclusive to any company. The company’s sales figures could be adversely affected if its agents significantly reduce their efforts. Mitigate: The company has long standing relationships of over 10 years with its agents. Within the Tirupur area and surrounding markets, it has been a tradition to build trust over the years rather than rely on formal agreements. The management closely monitors its agent network and the marketing manager is in continuous contact with the agents to ensure that sales opportunities are not missed. KPR’s marketing office in Tirupur is located within a 10km radius of all its customers and hence it is easy for the marketing team to be in constant touch with its end customers.

Investment Risks

K.P.R. Mill Limited – Initiating Coverage

Page 11 of 40

External Risks Increase in prices of raw material Cotton, the primary raw material constitutes a significant percentage of total expenses incurred by the company. Therefore, any increase in cotton prices and any decrease in supply of cotton could materially and adversely affect the business. Mitigate:

KPR procures bulk of its raw material requirement immediately after the harvesting season followed by the peak season of cotton supply i.e. Oct – March. This ensures abundant supply of high quality cotton at lower prices.

Foreign exchange risk due to enhanced focus on exports The company has increased its focus towards exports that would expose it to the risk of foreign exchange fluctuations. Mitigate: The company manages its forex exposure through close monitoring of market conditions and by hedging around 25-40% of its export order values through forward contracts mainly in Euro, British Pound and U.S. Dollar. Power shortage in the region leading to lower capacity utilization The company has been facing the problem of significant power outages in the state of Tamil Nadu which is having an adverse effect on the overall capacity utilization and therefore impacting the revenues and profitability of the company. Mitigate:

The company has been making continuous strides towards becoming self-sufficient for all its power requirements. The company is using various energy saving methods & line balancing initiatives for reducing the overall power consumption level and is also buying power from third parties in case of shortage. Competition from domestic players and other low cost countries KPR competes with number of organized and unorganized players in the textile industry. Pricing is one of the factors that play an important role in selection of the products. Stiff price competition from domestic players as well as international players from countries like Bangladesh, Indonesia and China with lower labour costs can adversely impact operations and profitability. Mitigate: With its vertically integrated operations, KPR is able to maintain superior quality for its products and command a better price. The strong track record of the company in timely delivery of premium quality products has helped it to establish strong relationships with its clients. Economic slowdown in global markets The company derives majority of its export revenues from the European markets which are facing economic slowdown due to the global financial crisis. This could adversely affect the business of the company.

Mitigate: The company has started targeting other countries such as US, Australia, etc to diversify its export markets for future revenue generation. KPR has also initiated the process of studying buyer’s profile with respect to their financial strength, track record

K.P.R. Mill Limited – Initiating Coverage

Page 12 of 40

of performance, years of existence in the industry, etc so as to cushion itself from unhealthy buyers. The company undertakes credit insurance cover for both domestic as well as international clients in order to provide full cover to its bad debts. Changes in technology may render current technologies obsolete

The apparel industry has experienced rapid improvements in technology and sophistication in production equipment, the use of which is essential to reduce costs and accelerate execution. The company may be required to implement new technology or upgrade the machinery at regular intervals, requiring significant capital investment. Mitigate:

KPR’s manufacturing facilities utilize a large base of sophisticated and automated production equipment. Most of its machinery is imported from Germany, Italy, Switzerland and other European countries as well as countries such as Japan, United States and Taiwan, in order to take advantage of the latest manufacturing process technologies. The company has a policy of reviewing its technology vis-à-vis that available in the market, at regular intervals, so as to introduce any latest technological innovation which would help the company to reduce cost and improve efficiency.

K.P.R. Mill Limited – Initiating Coverage

Page 13 of 40

49% 51%58%

51%63%

46%

17% 17%14%

13%

13%

13%

27%24%

18%

34%24%30%

4% 5% 4% 12% 6% 7%

0%

20%

40%

60%

80%

100%

FY06 FY 07 FY 08 FY 09 Q1 FY'09 Q1 FY'10

Yarns Fabrics Knitted Garments Export Others

Well-defined vertically integrated operations

KPR has established one of the largest vertically integrated manufacturing capacities in South India with the capability to produce readymade knitted apparel, knitted fabric and carded and combed cotton yarn. The integrated manufacturing operations enable the company to better customize products as per the client specifications and provide consistent quality assurance in a cost-effective manner.

Yarn: Yarn is the largest revenue contributing segment of the company with over 50% contribution to total revenues and average margins in the range of 17%-18%. KPR produces both carded and combed yarn. It consumes about 25% - 30% % of its yarn production in-house and the remaining 70% - 75% is sold in the domestic markets.

Fabric: Fabric contributes about 13% to the total revenues and has average margins of 15%-20%. KPR consumes about 25% - 30% of its fabric production for in-house garmenting and the remaining is sold in domestic markets.

Knitted Garment: Knitted Garments segment contributes 24% to the total revenues and enjoys highest margins of about 22% - 25%. Of the total garment capacity, 12mn pieces of the garment are outsourced through the Tirupur facility and the remaining is produced in-house. The company outsources small orders to local manufacturers and executes bulk orders in-house in order to achieve efficiency. 90-93% of the garment production is exported to the US and European countries.

Independent garmenting unit to facilitate branding - KPR formed a wholly owned subsidiary, Quantum Knits Pvt Ltd in June 2009, to provide independent and exclusive control of all operations, management and transactions of the Garment Unit at Arasur to this subsidiary. The primary purpose of having a separate identity is to meet additional market demand and gain marketing and administrative advantages.

…..leading to a diversified sales mix

The breakup of KPR’s revenues reflects yarn as the largest contributor in the total sales of the company during FY’06-FY’09. Revenue contribution from yarn has increased from 49% in FY’06 to 51% in FY’09, at a 3 yr CAGR of 21% to reach Rs 3,654mn in FY’09. Yarn revenues grew substantially in FY’08 due to addition of 1,00,800 spindles at Arasur plant in 2008 owing to increased demand in Tirupur market, the knitwear capital of India. Revenues derived from the fabric segment increased by 23% during the same period. KPR is the largest supplier in Tirupur with 7-8% share of the yarn market and 5% of the fabric market.

Business Analysis

Complete textile solutions provider offering a

diversified product mix

Yarn Manufacturing

Fabric Processing

Knitted Garments

Increased focus on higher margin segments

Product – wise Revenue Break-up

Source: Company data, Four-S Research

Source: Company data, Four-S Research

KPR’s presence across the Textile Value Chain

Sourcing of

Raw materials

Spinning (212,064 Spindles) (54,000MT Yarn)

Weaving/ Knitting

(185 Knitting

machines) (19,000MT Fabric)

Processing (23MT of fabric

per day)

Apparel Making

(63mn pieces of garments; operating

double shift)

Distribution/

Retailing

K.P.R. Mill Limited – Initiating Coverage

Page 14 of 40

29% 29% 25% 25% 19%34%

71% 71% 75% 75% 81% 66%

0%

20%

40%

60%

80%

100%

FY06 FY 07 FY 08 FY 09 Q1 FY'09 Q1 FY'10

Export Domestic

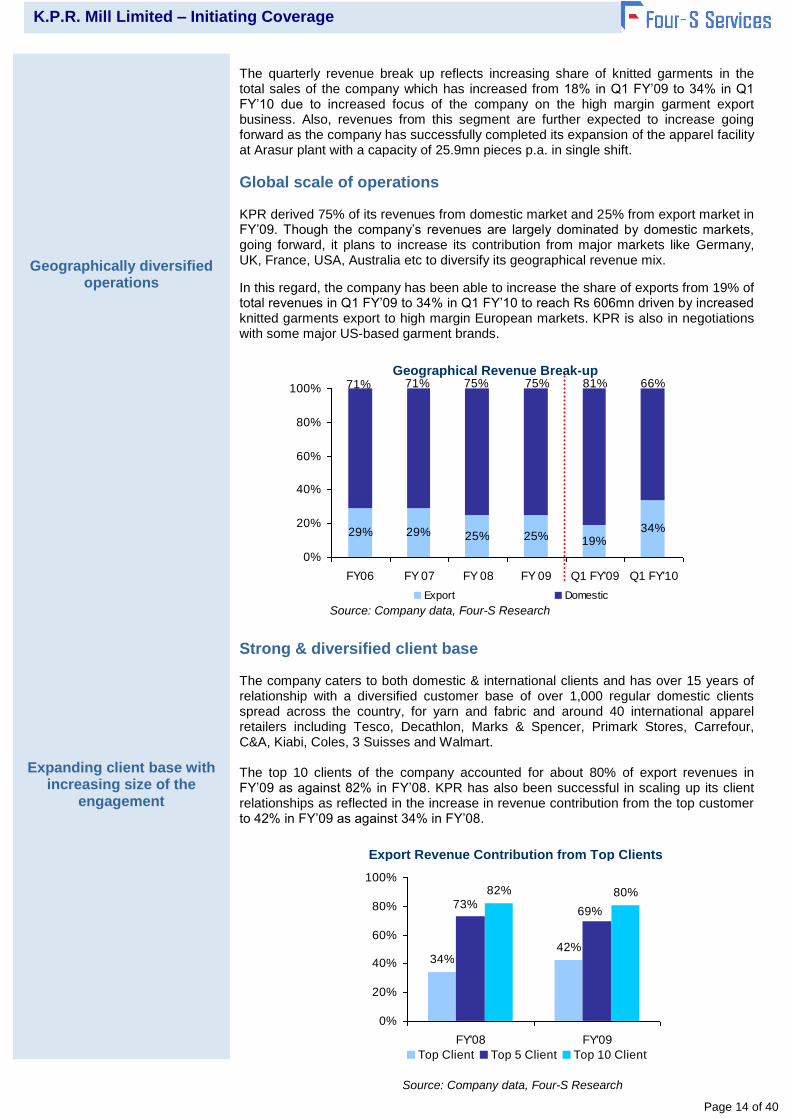

The quarterly revenue break up reflects increasing share of knitted garments in the total sales of the company which has increased from 18% in Q1 FY’09 to 34% in Q1 FY’10 due to increased focus of the company on the high margin garment export business. Also, revenues from this segment are further expected to increase going forward as the company has successfully completed its expansion of the apparel facility at Arasur plant with a capacity of 25.9mn pieces p.a. in single shift.

Global scale of operations KPR derived 75% of its revenues from domestic market and 25% from export market in FY’09. Though the company’s revenues are largely dominated by domestic markets, going forward, it plans to increase its contribution from major markets like Germany, UK, France, USA, Australia etc to diversify its geographical revenue mix.

In this regard, the company has been able to increase the share of exports from 19% of total revenues in Q1 FY’09 to 34% in Q1 FY’10 to reach Rs 606mn driven by increased knitted garments export to high margin European markets. KPR is also in negotiations with some major US-based garment brands.

Strong & diversified client base The company caters to both domestic & international clients and has over 15 years of relationship with a diversified customer base of over 1,000 regular domestic clients spread across the country, for yarn and fabric and around 40 international apparel retailers including Tesco, Decathlon, Marks & Spencer, Primark Stores, Carrefour, C&A, Kiabi, Coles, 3 Suisses and Walmart. The top 10 clients of the company accounted for about 80% of export revenues in FY’09 as against 82% in FY’08. KPR has also been successful in scaling up its client relationships as reflected in the increase in revenue contribution from the top customer to 42% in FY’09 as against 34% in FY’08.

Geographical Revenue Break-up

34%42%

82% 80%73%

69%

0%

20%

40%

60%

80%

100%

FY'08 FY'09

Top Client Top 5 Client Top 10 Client

Export Revenue Contribution from Top Clients

Source: Company data, Four-S Research

Source: Company data, Four-S Research

Geographically diversified operations

Expanding client base with increasing size of the

engagement

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 15 of 40

Cost-effective operating model to reduce internal overheads and ensure better margins at premium pricing Unique raw material procurement policy

KPR, with the help of its experienced procurement advisory team, buys high quality Shankar - 6 cotton from Gujarat (the largest producer of extra long staple (ELS) cotton in India) during the buying season i.e. October - March, to ensure highest & uniform quality of cotton at an economical cost. The harvesting of cotton is done in October and the company procures majority of its cotton requirement during December to January when the availability is at its peak and the prices are lower. During FY’09, KPR procured Shankar-6 at Rs 22,500 per candy (of 356kg) as against its minimum support price (MSP) of Rs 24,000 per candy. This helps the company to ensure high quality standards for its homogenous products throughout the year which command premium pricing (2% - 3% higher) in the market.

Distinctive workforce model to lower attrition and personnel costs

KPR uses a balanced approach towards attracting, training and retaining its employees and spends close to Rs 10mn per year on employee education and other welfare programmes. The company provides boarding and lodging to its workers and other amenities like higher education, yoga, swimming pool, etc. It strictly enforces an 8 hour workday policy without overtime. The employees have to go through a fitness test before joining and a 3 months on the job training. This model helps to keep a check on the staff costs of the company and also increase their over-all productivity keeping the attrition rate low. KPR’s staff cost as a percentage of revenues was 6.6% as compared to the industry average of 10% in FY’09. The attrition rate is also below 1% as against the industry rate of 10%. KPR has a workforce of 8,473 full time employees (as of Sept. 2009) in management and administration, research and development, technical functions, marketing and manufacturing amongst others. Strategic investment in windmill farms to become self-sufficient with reduced dependence on state for energy needs

The company has installed 40 wind mills with a total generation capacity of 40MW for captive consumption at Tirunelveli, Tenkasi and Coimbatore districts with an objective to become self- reliant in power consumption needs, support its expanding operations and reduce dependence on the state electrical grid. With one of the largest in-house power capacities in southern India, the company achieves substantial competitive advantage in power costs. KPR’s power cost as a percentage of revenue stood at 3% as compared to industry average of 6% during FY’09. The windmills, operating during April-March of each year, help the company to meet about 75% of its power requirement through captive consumption.

Strong marketing setup with focused strategy on acquisition of large and long term buyers The company has a strong marketing team, which is in charge of continuous acquisition of new and potential buyers who would stay with the company for a long period of time. The marketing team pitches for new buyers after making a detailed study of the buyer’s profile with respect to their years of existence, financial strength, track record of performance etc in the market. This helps the company to add large and potential buyers to its portfolio from key markets of EU, US and Australia.

Unique operating strategies to achieve cost effectiveness

Focusing on employee welfare & education

Generating 40MW through Windmills

Experienced marketing team

K.P.R. Mill Limited – Initiating Coverage

Page 16 of 40

Internationally accredited processes with stringent quality control measures The manufacturing facilities at KPR are internationally accredited and are staffed with trained supervisors and equipped with high tech quality control equipment. The company enforces stringent quality control measures to ensure end products of international standards. International accreditations include:

ISO 9001: 2000 – certification for quality management system.

ISO 14001: 2004 – certification for environmental management systems.

SA 8000: 2001 – certification for social accountability management system for the manufacture of cotton yarn.

World-wide Responsible Apparel Production Certificate (WRAP) –ensuring apparel production under lawful, humane and ethical conditions.

Ethical Trade Initiative (ETI) – for sound working conditions of workers.

Global Organic Textile Standard (GOTS) - for organic cotton products.

OEKO-TEX – for responsible and ethical endeavors.

Certified by International Association for Research and Testing in the field of Textile Ecology with respect to apparel manufacturing operations.

Certified as a One Star Export House by the Indian Ministry of Commerce and Trade.

Quality control initiatives include:

Procurement of highest quality raw materials.

Installation of high-tech quality control equipment such as Uster Tester-4, Uster HVI Spectrum, Uster AFIS Pro, Zweigle Hariness Tester-G566 and Uster Classimat Quantum.

Uses latest technology equipment Jossi Vision Shield for contamination free yarn.

Installed Schlafhorst Autoconer that ensures sophistication and homogenous quality in yarn and better productivity.

Mandatory usage of hand gloves, hair net, mask, aprons, etc for the twin benefits of safety and quality.

Special customer service department headed by a textile technologist for continuous improvement and customer satisfaction.

Inspection at every stage to ensure stringent quality conformance.

Strategicaly located manufacturing facilities All of KPR’s manufacturing facilities are located near Coimbatore, which is known to be conducive for spinning operations. This helps in significant savings in production, labour and transportation costs and helps the company to utilize the key technical personnel across the manufacuring facilities. KPR’s operations are spread in the Tirupur-Coimbatore belt, which is regarded as one of Asia’s largest apparel manufacturing clusters. The close proximity to buyers helps to reduce the material handling costs and facilitates immediate feedback regarding the quality of the product. KPR is the only player in the industry to set up a large exclusive showroom of over 7,000 sq ft to facilitate buying for its clients.

Strong commitment towards process excellence

demonstrated through international accreditations

and quality control initiatives

Quality Control Lab

Raw Cotton Tester

Exclusive showroom of more

than 7,000 sq ft – for displaying garments to clients

K.P.R. Mill Limited – Initiating Coverage

Page 17 of 40

Continuous involvement towards overall social development KPR continues to involve itself in activities aimed at overall development of the society. It has contributed actively towards community welfare measures, taking several initiatives related to education, health, environmental improvement and other development measures as follows:

Installed 40 windmills having a total capacity of 40MW of power to meet its energy requirements through eco-friendly renewable sources of energy.

Collaborated with Italy’s Water Treatment Technology to reuse 100% of the waste water. The ‘effluent treatment plant’ has a total capacity to handle 1.5mn litres of waste water and achieved Zero discharge as per the PCB norms.

Invested in municipal infrastructure by constructing short road linkages to manufacturing facilities from the national highways and state roads with an objective to provide quality infrastructure and connectivity.

Established an educational institution in Coimbatore in 2009 through its charitable trust, ‘KPR Charities’ promoted by M/s K.P.Ramasamy, KPD Sigamani and P.Nataraj (permanent trustees) with an objective to provide education to all. The trust promoted educational institutions in the name of ‘KPR Institute of Engineering and Technology’ & ‘KPR School of Business’ approved by AICTE and affiliated with Anna University.

Location of Facilities Nature of Work Capacity

Sathyamangalam Spinning 30,240 spindles

Karumathampatti Spinning 30,240 spindles

Neelambur Spinning & Knitting 50,784 spindles

Arasur Spinning, Knitting & Garmenting

1,00,800 spindles Garmenting :85,000 pieces per day (single shift) Storage : 450 tons of raw cotton

Tirupur Garmenting 12mn pieces p.a. capacity outsource

SIPCOT, Perundurai Fabric Processing 23 tons/day

Tirunelveli, Tenkasi & Coimbatore

Wind Mills (40 nos.) 40MW

Source: Company data, Four-S Research

Arasur Facility

Focused approach towards green energy efforts and

community development to attract global clients

ETP – converting effluent to

clear water for 100% recycling

K.P.R. Mill Limited – Initiating Coverage

Page 18 of 40

Target revenue growth at a 3 year CAGR of 18% during FY’09-FY’12 The company has targeted a 3 year CAGR of 18% in revenues to reach Rs 11.75bn by FY’12; driven largely by export revenues. Export revenues are expected to increase at a 3 yr CAGR of 38% and domestic revenues at a 3 yr CAGR of 9% during FY’10 - FY’12. Increased focus on high margin garment exporting segment to provide significant opportunity for growth KPR plans to increase contribution from the export business to 40% in FY’12 up from 25% in FY’09. The company has set up a separate garmenting facility in Arasur for this purpose. It plans to increase its presence in newer markets and is in the final round of negotiations with a few leading international companies in US and Australia; which is expected to increase the export order book of the company.

The company has a confirmed export order book of Rs 1,000mn as of September 2009, to be executed within the next 150 days.

Foray into new high growth regions to diversify geographically With the global economy showing early signs of recovery, KPR plans to reduce dependence on European markets and increase its exposure in US and other countries like Australia. The company plans to double its contribution from US and other markets to 20% in next 4-5 years from 10% in FY’09.

Growth Plans & Drivers

Target to achieve Rs 11.75bn of revenues

by FY’12

Contribution from exports to increase to 40% of the total revenues by FY’12

US &

Others,

10%

Europe,

90%

Europe,

80%

US &

Others,

20%

66% 63% 60%

40%37%34%

0%

20%

40%

60%

80%

100%

FY'10 FY'11 FY'12

Domestic Export

Projected Revenue Mix

Source: Company data, Four-S Research

Source: Company data, Four-S Research

Major Export Markets

K.P.R. Mill Limited – Initiating Coverage

Page 19 of 40

Expanding capacity to be better equipped for future demand KPR has successfully completed Phase I of its capacity expansion programme during FY’2008 at an outlay of Rs 5,440.5mn. The company further completed the following Phase II capacity expansion during FY’09:

Added a design studio for garment operations.

Expanded garment facility at Arasur with balancing machines.

52 new knitting machines have been commissioned at Arasur

6 compact spinning machines for value addition have been installed

However, going forward, KPR would take a measured approach in implementing the Phase II of the capacity expansion programme only after achieving optimum utilization at the existing capacities.

Unit Name Investment

Rs. Mn Capacity Addition

Sathyamangalam – Spinning Division 118.9 Modernization

Arasur– Spinning Division 2,800.0 1,00,800 spindles

SIPCOT – Processing 667.1 23MT fabric processing

Arasur - Garment 692.6 25.9mn pieces production (single shift)

Wind Mill 1,161.9 12 wind mills with 19.80MW

Total 5,440.5

Unit Name Investment Rs. Mn

Capacity Addition

Arasur – Apparel 105.9 Expansion of the apparel facility at Arasur plant to increase capacity from 25.9mn pieces to 51.8mn pieces.

Arasur – Design Studio 5.6 Addition of a design studio for garment operations.

Arasur– Hostel 71.3 Additional hostel facility for workers for double shift.

Arasur– Knitting 259.6 New knitting facility

SIPCOT – Processing 397.0 Doubling of 23MT Fabric Processing to 46MT per day

Spinning facility 138.1 Compact spinning facility for value addition to yarn produced

General Corporate Expenses

241.6 Normal capex to be incurred for general corporate purposes

Total 1,219.1

Power saving initiatives to lead to significant cost savings In addition to having a total power generation capacity of 40MW through windmills, KPR is taking steps to control the overall energy cost and become self sufficient in power.

Energy conservation measures undertaken: All spinning units are installed with HUMI FOG water-spray systems in the autoconer, carding and blow room departments to improve the relative humidity (RH). By optimizing the usage of water pumps and fans, the company is saving 23,000 units per day. Various line balancing operations have been undertaken along with use of power saving devices, to make optimum utilization of available power.

Successfully executed Rs 5.44bn Phase – I of

Capex Programme

Processing Unit at SIPCOT

Garmenting Unit at Arasur

Design Studio at Arasur

Phase-II Capacity Expansion Programme (In Process)

Source: Company data, Four-S Research

Phase-I Capacity Expansion Programme (Already Completed)

K.P.R. Mill Limited – Initiating Coverage

Page 20 of 40

Annual Review Revenues grew at a 3 year CAGR of 19.4% during FY’06-FY’09 The Company’s net revenues grew at a CAGR of 19.4% over FY’06-’09 to Rs 7,182mn led by strong growth across key business segments:

Yarn segment grew at a 3-year CAGR of 21% to Rs 3,654mn in FY’09 due to impressive growth (1.6x) in volumes to 32,440MT along with growth in realization by 10% over the period led by superior quality products. The revenue growth was in line with the doubling of capacity under the segment to 2.12 lakh spindles in 2008 which led to increase in contribution from yarn segment to 58% during the same period. However, the contribution declined to 51% in FY’09 due to decline in capacity utilization of the segment on the back of increased power shortage in the state.

Fabric segment grew at a 3-year CAGR of 7% to Rs 902mn based on 1.5x growth in volumes to 9,029MT.

Knitted Garments grew at a 3-year CAGR of 12% to Rs 1,749mn due to significant increase in sales volume by 2x to 20.5mn pieces in FY’09 owing to the in-house execution of bulk orders with increased capacity from Arasur plant; coupled with increased mining of the major clients and addition of new clients such as Decathlon, Tesco, Kmart etc. Prior to 2008, the company was able to execute only small export orders outsourced to local manufacturers. Going forward, KPR would be able to increase revenue contribution from garments with better capacity utilization (Target - 70% in FY’10 as against 55%-60% in FY’09).

Financial Analysis

High revenue growth with CAGR of 19.4% during

FY’06-09

Significant growth in sales volume of key segments

4,2154,816

5,739

7,182

0

2,000

4,000

6,000

8,000

FY'06 FY'07 FY'08 FY'09

CAGR= 19.4%

Source: Company data, Four-S Research

Expanding Topline (Rs Mn)

2,067 2,4503,335 3,654

810

776902

736

1,255

1,299

1,392

1,749

877

237

258

157

FY'06 FY'07 FY'08 FY'09

Yarn Fabrics Knitted Garments Others

Segment-wise increase in sales volume Segment-wise sales break up (Rs mn)

20,274 22,473

32,793 32,440

5,608

7,325 9,029

6,139

10,42810,586

14,50620,540

FY'06 FY'07 FY'08 FY'09

Yarn (MT) Fabrics (MT) Knitted Garments ('000 pieces)

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 21 of 40

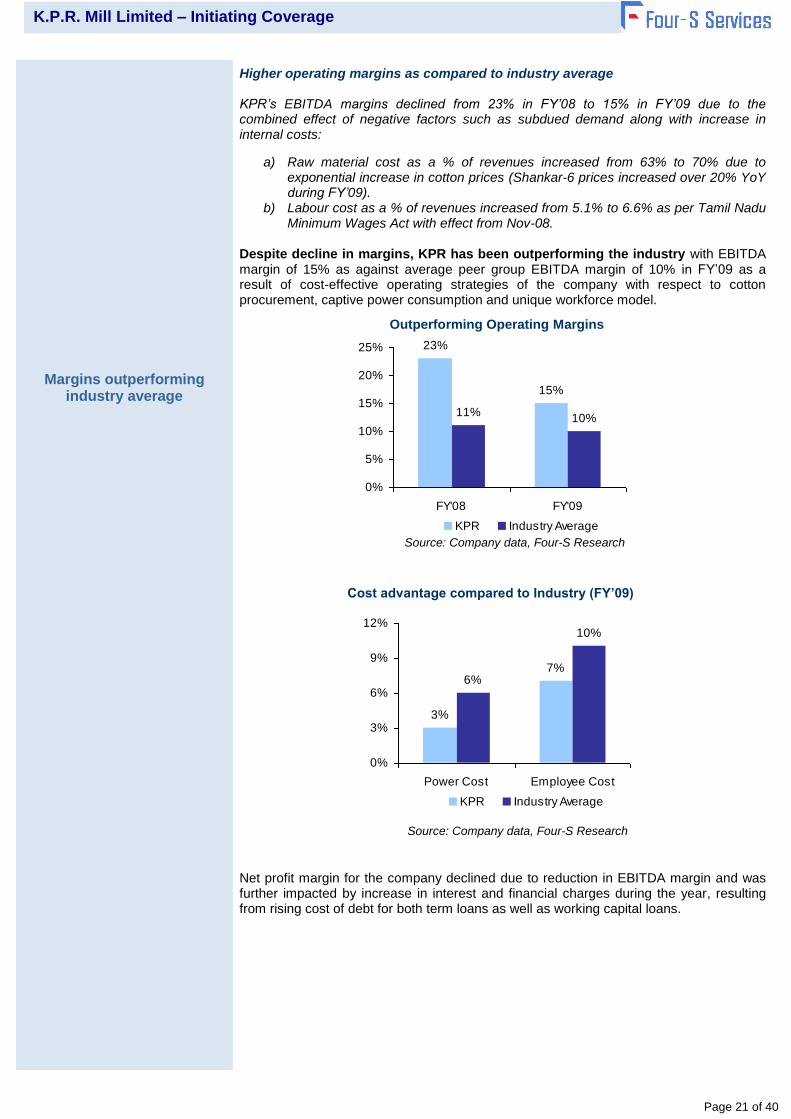

Higher operating margins as compared to industry average KPR’s EBITDA margins declined from 23% in FY’08 to 15% in FY’09 due to the combined effect of negative factors such as subdued demand along with increase in internal costs:

a) Raw material cost as a % of revenues increased from 63% to 70% due to exponential increase in cotton prices (Shankar-6 prices increased over 20% YoY during FY’09).

b) Labour cost as a % of revenues increased from 5.1% to 6.6% as per Tamil Nadu Minimum Wages Act with effect from Nov-08.

Despite decline in margins, KPR has been outperforming the industry with EBITDA margin of 15% as against average peer group EBITDA margin of 10% in FY’09 as a result of cost-effective operating strategies of the company with respect to cotton procurement, captive power consumption and unique workforce model.

Net profit margin for the company declined due to reduction in EBITDA margin and was further impacted by increase in interest and financial charges during the year, resulting from rising cost of debt for both term loans as well as working capital loans.

23%

15%

11%10%

0%

5%

10%

15%

20%

25%

FY'08 FY'09

KPR Industry Average

Margins outperforming industry average

Outperforming Operating Margins

Source: Company data, Four-S Research

Cost advantage compared to Industry (FY’09)

3%

7%6%

10%

0%

3%

6%

9%

12%

Power Cost Employee Cost

KPR Industry Average

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 22 of 40

Particulars FY 07 FY 08 FY 09

Capitalisation Ratios

Debt / Equity 1.25 1.23 1.04

Liquidity Ratios

Current Ratio 1.75 4.89 2.36

Turnover Ratios

Debtors Days 37.17 46.36 51.88

Creditors Turnover – Days

Inventory Days 103.60 113.04 107.26

Net Working Capital Turnover Ratio 4.44 1.92 2.88

Fixed Assets Turnover Ratio 0.99 0.89 0.90

Balance Sheet Ratios

KPR adopts a regular repayment strategy for its term loans with about Rs 750 mn of loans repaid every year, resulting in an optimum debt equity mix of 1:1 for the company. The liquidity position was affected in FY’09 due to increase in liabilities on account of capital expenditure incurred by the company. Owing to the difficult market conditions in the last fiscal, KPR followed a lenient credit policy (collection period ranged from 30-60 days) for its long standing clients which resulted in an increase in debtor days during FY’09. Inspite of an increase in inventory, debtors and other current assets of the company, the working capital turnover has shown an improvement in FY’09 indicating healthy growth in revenues with greater client penetration.

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 23 of 40

YTD Performance

Revenues grew 5% YoY in Q1 FY’10 despite slowdown in textile industry Net revenues grew 5% on YoY basis from Rs 1,679.2mn in Q1 FY’09 to Rs 1,758.5mn in Q1 FY’10 driven by a) increase in realizations for yarn from Rs 109,880 per MT to Rs 118,468 per MT and for fabric from Rs 113,489 per MT to 124,912 per MT and b) strong growth in volumes under export segment which grew 92.7% YoY to Rs 605.9mn in Q1 FY’10 due to impressive growth in volumes of knitted garments to over 8mn pieces driven by increased focus of the company towards garment exports.

Driven by strong growth across key segments Revenues from Knitted Garments export increased significantly at 105.9% YoY from Rs 293.2mn to Rs 603.5mn driven by 3x increase in sales volume with continuous addition of new clients such as Marks & Spencer, Wal-Mart etc. Also the realization from yarn and fabric increased by 8%-10% YoY during Q1 FY’10. Despite growth in revenues, the margins declined on YoY basis during Q1 FY’10 owing to external factors such as rising employee bill on the back of increase in labour costs as per Tamil Nadu Minimum Wages Act and underutilization of capacity due to power shortage in Tamil Nadu.

YoY revenue growth of 5% in Q1 FY’10 led by higher

exports sales

1,3651,153

314 606

0

300

600

900

1,200

1,500

1,800

Q1 FY'09 Q1 FY'10

Domestic ExportsSource: Company data, Four-S Research

Extended Revenue Growth in Q1 FY’10 (Rs Mn)

1,061806

217

231

293604

119108

0

300

600

900

1,200

1,500

1,800

Q1 FY'09 Q1 FY'10

Yarn Fabric Knitted Garments Others

Segmental Performance (Rs Mn)

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 24 of 40

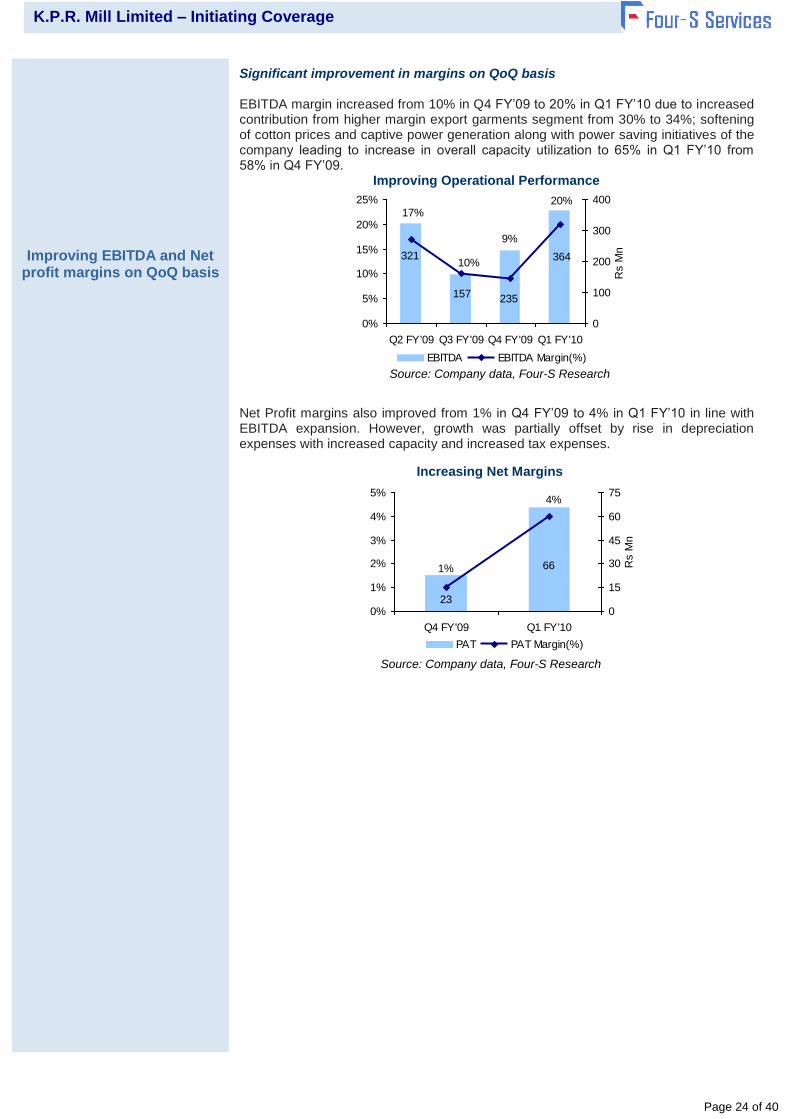

Significant improvement in margins on QoQ basis EBITDA margin increased from 10% in Q4 FY’09 to 20% in Q1 FY’10 due to increased contribution from higher margin export garments segment from 30% to 34%; softening of cotton prices and captive power generation along with power saving initiatives of the company leading to increase in overall capacity utilization to 65% in Q1 FY’10 from 58% in Q4 FY’09. Improving Operational Performance

Net Profit margins also improved from 1% in Q4 FY’09 to 4% in Q1 FY’10 in line with EBITDA expansion. However, growth was partially offset by rise in depreciation expenses with increased capacity and increased tax expenses.

364

235157

32110%

17%20%

9%

0%

5%

10%

15%

20%

25%

Q2 FY'09 Q3 FY'09 Q4 FY'09 Q1 FY'10

0

100

200

300

400

Rs M

n

EBITDA EBITDA Margin(%)

66

23

4%

1%

0%

1%

2%

3%

4%

5%

Q4 FY'09 Q1 FY'10

0

15

30

45

60

75

Rs M

n

PAT PAT Margin(%)

Source: Company data, Four-S Research

Increasing Net Margins

Source: Company data, Four-S Research

Improving EBITDA and Net profit margins on QoQ basis

K.P.R. Mill Limited – Initiating Coverage

Page 25 of 40

Large & Growing Market The Indian textiles industry is currently pegged at $52bn in size and is likely to grow by 2.2x to reach $115bn by 2012. Being one of the largest contributing sectors of India's exports worldwide, India's textiles and clothing industry (T&C) is one of the mainstays of the national economy. The industry accounts for 4% of the gross domestic product; 14% of industrial production; employs 35mn people and accounts for nearly 12% share of the country's total exports basket driven by superior quality, design and cost arbitrage of outsourcing work to India.

Exports to grow at a faster rate compared to domestic market According to IBEF, the domestic market, which currently constitutes about 66% of the total T&C market, is expected to increase from $34.6bn to $60bn by 2012. On the other hand, the export market, which has witnessed an increase of over 48% in last 5 years, would more than double itself to reach $55bn by 2012. Contribution of the export market to the total industry size is estimated to increase from 34% at present to 48% by 2012. This would help India to increase its share of exports to the world from the current 4% to around 7% during this period.

Increased demand for Readymade Garments, the key focus area for KPR, with increase in global sourcing Despite slowdown in overall textile exports during FY’09 due to slump in demand from major global economies like the US and Europe which are reeling under the impact of financial meltdown, the readymade garment exports witnessed an increase of 12.5% YoY to reach $10.2bn of export revenues during FY’09. Readymade garments constituted about 49% of the country’s total textile exports. The abolition of the Multi-Fibre Arrangement (MFA) has triggered growth in the quantum of sourcing of top global retailers from India leading to 4-fold increase in India’s share in the US apparel imports from 4% pre-quota to 15% post-quota and in

Expectation of robust growth in future

Export contribution to increase to 48% by 2012

13% YoY growth in readymade garment export

revenues in FY’09

Industry Opportunity Mapping

14.1

17.619.1

22.1 20.9

0

5

10

15

20

25

2004-

05

2005-

06

2006-

07

2007-

08

2008-

09

Size of Indian Textile Industry ($ bn)

Readymade Garment Export ($ bn) India’s Export Performance ($ bn)

Export Vs Domestic

52.0

115.0

0

20

40

60

80

100

120

140

2008 2012E

Growth: 2.2x

Source: IBEF, Ministry of Textiles

66%

52%

34%48%

0%

20%

40%

60%

80%

100%

2008 2012E

Domestic Export

Source: IBEF

Source: Ministry of Textiles, Industry Sources

10.29.1

0

3

6

9

12

15

2007-08 2008-09

Growth: 12.5%

Source: Ministry of Textiles, Industry Sources

K.P.R. Mill Limited – Initiating Coverage

Page 26 of 40

EU imports from 6% pre-quota to 9% post-quota. To save on logistics and procurement costs, large global buyers are actively going in for vendor consolidation. A majority of them plan to step up their sourcing from India by setting up closely-held sourcing and buying entities. The expected sourcing market size is projected to grow from $22-25bn in 2008 to $35-37bn in 2011. India is expected to be one of the biggest beneficiaries of this move, with retailers expected to limit their sourcing to countries that offer large scale integrated operations and good quality products at low cost in a timely fashion.

Key Growth Drivers

India’s Advantage

Abundant availability of raw materials: India has abundant resources of raw materials for textile industry. It is the second largest producer of cotton in the world and accounts for 12% of the world's production of textile fibre and yarn. This inherent strength in availability of raw materials prevents any supply-side shocks. Downward movements in cotton price post FY’09 – Cotton and cotton prices, to a large extent, determine the profitability of cotton textile units. The average cotton prices have declined by 17% to 20% post FY’09 as compared to the peak prices of 2008-09 which increased by as much as 47% in some cases, following the hike in MSP for cotton by Government of India. Average cotton prices (per kg) increased in the range of 20%-24% in FY’09 over previous year rendering the Indian cotton and textile prices non competitive in the world markets.

According to industry sources, cotton prices are expected to decline further on the back of increased availability with the new cotton supply season just about to start and positive indications of a bumper crop. India's crop for the 2009-10 season starting in October is expected to expand 11% to 32.5mn bales, each weighing 170 kg. Low cost skilled labour: India has abundant availability of manpower, with skill-sets across all activities of the textile-industry value chain. India has a cost advantage over comparative countries with labour cost of $0.57 per hour as against that for China ($0.69), South Korea ($5.73), HongKong ($6.15) and USA ($15.13). (Source: IBEF) Growing domestic demand: Indian domestic textile market is growing at a very good pace driven by favorable consumer demographics. The consuming class in India i.e. population with annual income of over Rs 90,000; is expected to constitute 80% of the population by 2010.

Abundant Raw Material

Availability

Low Cost

Skilled Labour

Growing Domestic Demand

Government Support &

Initiatives

Average Cotton Prices (Rs per kg)

54

56

67

6467

62

50

55

60

65

70

FY'08 FY'09 Post FY'09 till Aug

Long staple (27.5mm to 32mm) Raw Cotton

Source: Ministry of Textiles, Industry Sources

Declining cotton prices

K.P.R. Mill Limited – Initiating Coverage

Page 27 of 40

Government support and initiatives: To counter the slowdown impact on exports, Government has recently announced relief packages & steps as follows:

Extension of Technology Upgradation Fund Scheme (TUFS benefits include 5% interest reimbursement on the normal interest charged by the lending agency and an upfront capital subsidy of 10% for some specified processing machines) till 2012 and fresh allocation of Rs 14bn and release of Rs 25.5bn towards clearance of the backlog of disbursements due under TUFS.

Reduction in Central Value Added Tax Rate by 4%. Interest rate cut of 0.5% for small and 1% for micro enterprises by PSU banks. Interest subvention of 2% to March 2009 for pre and post-shipment export credit

for labour-intensive exports (textiles, leather, marine products) and SME sector. Relief in the value cap of duty drawback rates for certain categories of cotton

yarn and extension of the duty entitlement pass book (DEPB) scheme up to December 31, 2009.

Imposition of anti-dumping duty of up to $527 per ton on yarn and fabric imported from China to discourage imports.

Increased Investment in the Sector Textiles sector has witnessed an unprecedented spurt in investments over the last few years. As per Ministry of Textiles, industry has seen investments worth Rs 1,681.43bn during the last 3 years. Despite downturn, the textile industry managed to keep the investment momentum going with Rs 466.13bn worth of investment in FY’09, 49.6% up from Rs 311.6bn 2007-08.

Government stimulus packages

Over 49% YoY increase in investments in FY’09

Total Investments in Textile Industry in last 3 years (Rs bn)

466

312

904

0

200

400

600

800

1000

2006-07 2007-08 2008-09

Source: PIB Press Release

K.P.R. Mill Limited – Initiating Coverage

Page 28 of 40

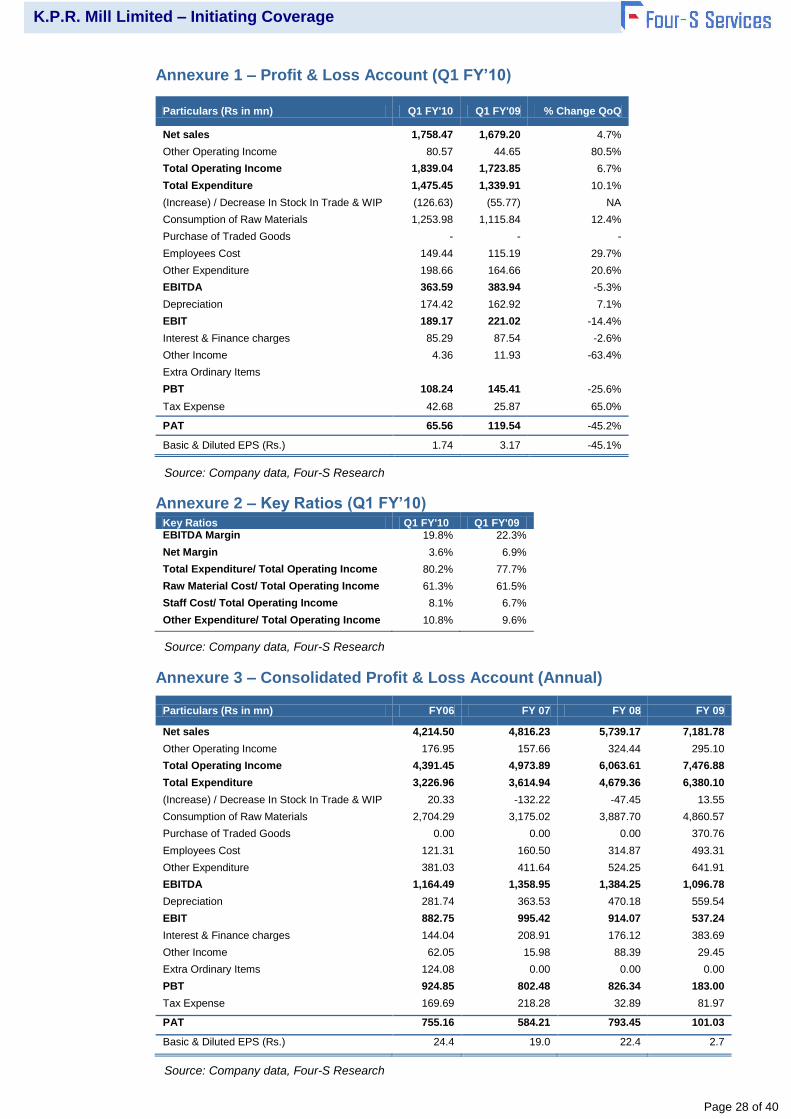

Annexure 1 – Profit & Loss Account (Q1 FY’10)

Particulars (Rs in mn) Q1 FY'10 Q1 FY'09 % Change QoQ

Net sales 1,758.47 1,679.20 4.7%

Other Operating Income 80.57 44.65 80.5%

Total Operating Income 1,839.04 1,723.85 6.7%

Total Expenditure 1,475.45 1,339.91 10.1%

(Increase) / Decrease In Stock In Trade & WIP (126.63) (55.77) NA

Consumption of Raw Materials 1,253.98 1,115.84 12.4%

Purchase of Traded Goods - - -

Employees Cost 149.44 115.19 29.7%

Other Expenditure 198.66 164.66 20.6%

EBITDA 363.59 383.94 -5.3%

Depreciation 174.42 162.92 7.1%

EBIT 189.17 221.02 -14.4%

Interest & Finance charges 85.29 87.54 -2.6%

Other Income 4.36 11.93 -63.4%

Extra Ordinary Items

PBT 108.24 145.41 -25.6%

Tax Expense 42.68 25.87 65.0%

PAT 65.56 119.54 -45.2%

Basic & Diluted EPS (Rs.) 1.74 3.17 -45.1%

Annexure 2 – Key Ratios (Q1 FY’10) Key Ratios Q1 FY'10 Q1 FY'09 EBITDA Margin 19.8% 22.3%

Net Margin 3.6% 6.9%

Total Expenditure/ Total Operating Income 80.2% 77.7%

Raw Material Cost/ Total Operating Income 61.3% 61.5%

Staff Cost/ Total Operating Income 8.1% 6.7%

Other Expenditure/ Total Operating Income 10.8% 9.6%

Annexure 3 – Consolidated Profit & Loss Account (Annual)

Particulars (Rs in mn) FY06 FY 07 FY 08 FY 09

Net sales 4,214.50 4,816.23 5,739.17 7,181.78

Other Operating Income 176.95 157.66 324.44 295.10

Total Operating Income 4,391.45 4,973.89 6,063.61 7,476.88

Total Expenditure 3,226.96 3,614.94 4,679.36 6,380.10

(Increase) / Decrease In Stock In Trade & WIP 20.33 -132.22 -47.45 13.55

Consumption of Raw Materials 2,704.29 3,175.02 3,887.70 4,860.57

Purchase of Traded Goods 0.00 0.00 0.00 370.76

Employees Cost 121.31 160.50 314.87 493.31

Other Expenditure 381.03 411.64 524.25 641.91

EBITDA 1,164.49 1,358.95 1,384.25 1,096.78

Depreciation 281.74 363.53 470.18 559.54

EBIT 882.75 995.42 914.07 537.24

Interest & Finance charges 144.04 208.91 176.12 383.69

Other Income 62.05 15.98 88.39 29.45

Extra Ordinary Items 124.08 0.00 0.00 0.00

PBT 924.85 802.48 826.34 183.00

Tax Expense 169.69 218.28 32.89 81.97

PAT 755.16 584.21 793.45 101.03

Basic & Diluted EPS (Rs.) 24.4 19.0 22.4 2.7

Source: Company data, Four-S Research

Source: Company data, Four-S Research

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 29 of 40

Rs in Mn. FY06 FY 07 FY 08 FY 09

Sources of Funds:

Shareholders' Funds

Share Capital 150.08 317.71 376.83 376.83

Reserves and Surplus 2,095.68 3,008.98 4,710.55 4,722.35

2,245.77 3,326.68 5,087.38 5,099.18

Loan Funds

Secures Loans 2,895.24 3,938.05 6,032.34 5,118.21

Unsecured Loans 216.50 225.40 212.09 189.98

3,111.74 4,163.45 6,244.43 5,308.19

Deferred Tax Liablity 190.20 316.85 336.88 395.74

Total 5,547.71 7,806.98 11,668.69 10,803.11

Application of Funds :

Fixed Assets

Gross Block 5,032.02 6,053.50 9,493.58 9,924.44

Less: Deprication 341.11 698.18 1,160.45 1,718.63

Net Block 4,690.91 5,355.31 8,333.13 8,205.81

Add: Capital Work-in-Progress 374.46 1,328.08 135.63 3.01

5,065.37 6,683.39 8,468.77 8,208.81

Investments 2.50 2.50 50.00

Current Assets, Loans & Advances

Inventories 832.90 1,219.13 1,679.37 2,070.37

Sundry Debtors 414.50 598.57 941.76 1,183.82

Cash and Bank Balances 152.22 272.48 594.11 462.32

Other Current Assets 96.16 133.35 181.84 229.44

Loan and Advances 248.00 383.49 562.02 551.41

1,743.77 2,607.03 3,959.09 4,497.37

Less: Current Liabilities & Provision

Current Liablities 1,179.49 1,365.02 580.97 1,791.55

Provision 84.84 120.92 228.19 111.53

1,264.33 1,485.94 809.16 1,903.07

Net Current Assets 479.44 1,121.09 3,149.93 2,594.29

Miscellaneous Expenditure 0.40

Total 5,547.71 7,806.98 11,668.69 10,803.11

Annexure 4 – Consolidated Balance Sheet (Annual)

Source: Company Data, Four-S Research

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 30 of 40

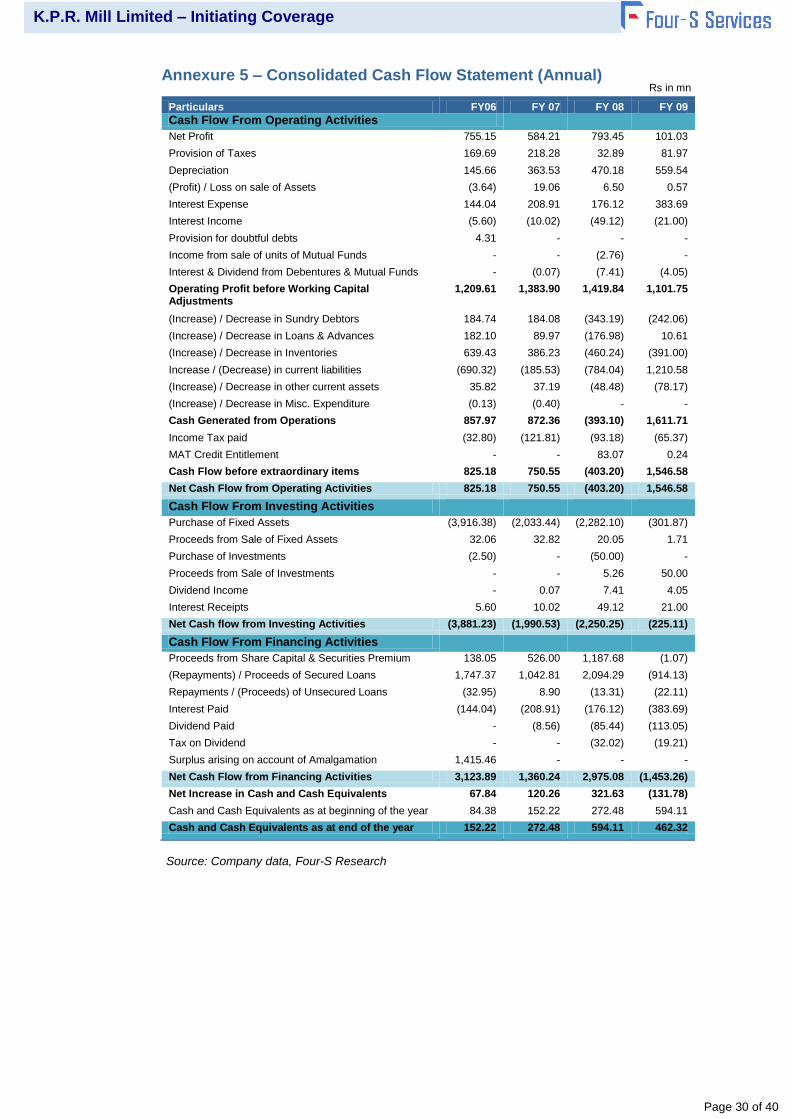

Annexure 5 – Consolidated Cash Flow Statement (Annual)

Particulars FY06 FY 07 FY 08 FY 09

Cash Flow From Operating Activities

Net Profit 755.15 584.21 793.45 101.03

Provision of Taxes 169.69 218.28 32.89 81.97

Depreciation 145.66 363.53 470.18 559.54

(Profit) / Loss on sale of Assets (3.64) 19.06 6.50 0.57

Interest Expense 144.04 208.91 176.12 383.69

Interest Income (5.60) (10.02) (49.12) (21.00)

Provision for doubtful debts 4.31 - - -

Income from sale of units of Mutual Funds - - (2.76) -

Interest & Dividend from Debentures & Mutual Funds - (0.07) (7.41) (4.05)

Operating Profit before Working Capital Adjustments

1,209.61 1,383.90 1,419.84 1,101.75

(Increase) / Decrease in Sundry Debtors 184.74 184.08 (343.19) (242.06)

(Increase) / Decrease in Loans & Advances 182.10 89.97 (176.98) 10.61

(Increase) / Decrease in Inventories 639.43 386.23 (460.24) (391.00)

Increase / (Decrease) in current liabilities (690.32) (185.53) (784.04) 1,210.58

(Increase) / Decrease in other current assets 35.82 37.19 (48.48) (78.17)

(Increase) / Decrease in Misc. Expenditure (0.13) (0.40) - -

Cash Generated from Operations 857.97 872.36 (393.10) 1,611.71

Income Tax paid (32.80) (121.81) (93.18) (65.37)

MAT Credit Entitlement - - 83.07 0.24

Cash Flow before extraordinary items 825.18 750.55 (403.20) 1,546.58

Net Cash Flow from Operating Activities 825.18 750.55 (403.20) 1,546.58

Cash Flow From Investing Activities

Purchase of Fixed Assets (3,916.38) (2,033.44) (2,282.10) (301.87)

Proceeds from Sale of Fixed Assets 32.06 32.82 20.05 1.71

Purchase of Investments (2.50) - (50.00) -

Proceeds from Sale of Investments - - 5.26 50.00

Dividend Income - 0.07 7.41 4.05

Interest Receipts 5.60 10.02 49.12 21.00

Net Cash flow from Investing Activities (3,881.23) (1,990.53) (2,250.25) (225.11)

Cash Flow From Financing Activities

Proceeds from Share Capital & Securities Premium 138.05 526.00 1,187.68 (1.07)

(Repayments) / Proceeds of Secured Loans 1,747.37 1,042.81 2,094.29 (914.13)

Repayments / (Proceeds) of Unsecured Loans (32.95) 8.90 (13.31) (22.11)

Interest Paid (144.04) (208.91) (176.12) (383.69)

Dividend Paid - (8.56) (85.44) (113.05)

Tax on Dividend - - (32.02) (19.21)

Surplus arising on account of Amalgamation 1,415.46 - - -

Net Cash Flow from Financing Activities 3,123.89 1,360.24 2,975.08 (1,453.26)

Net Increase in Cash and Cash Equivalents 67.84 120.26 321.63 (131.78)

Cash and Cash Equivalents as at beginning of the year 84.38 152.22 272.48 594.11

Cash and Cash Equivalents as at end of the year 152.22 272.48 594.11 462.32

Source: Company Data, Four-S Research

Rs in mn

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 31 of 40

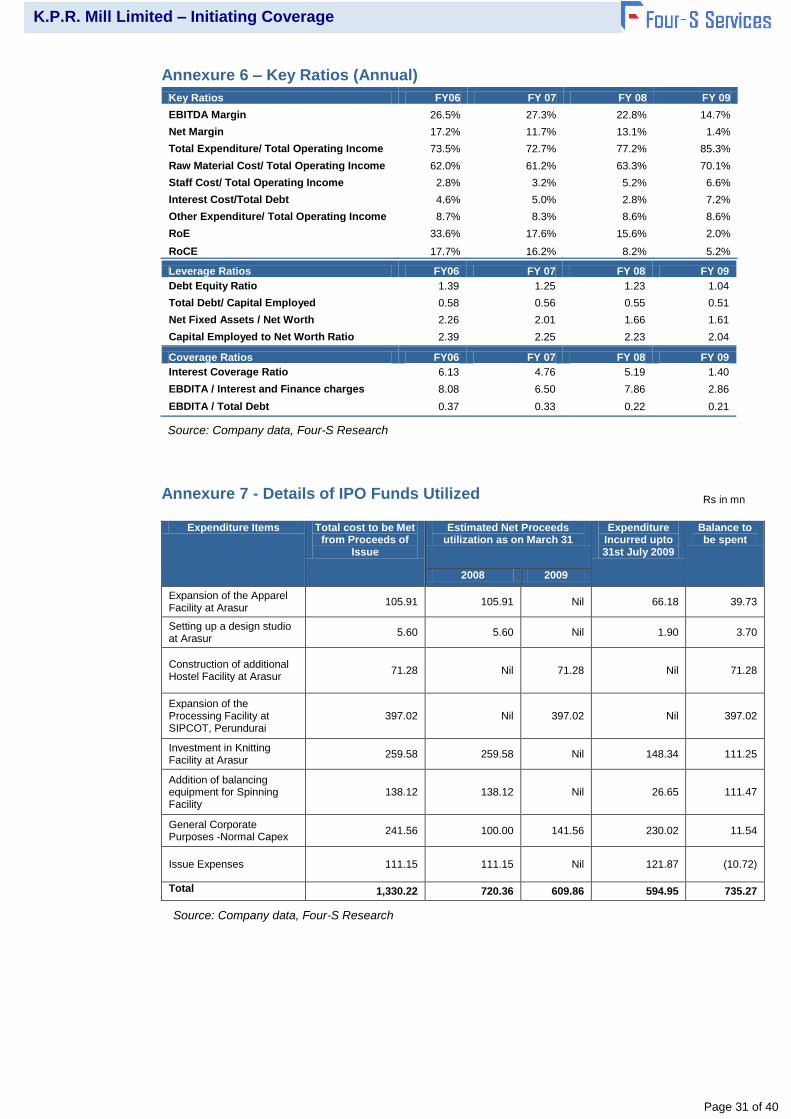

Annexure 6 – Key Ratios (Annual)

Key Ratios FY06 FY 07 FY 08 FY 09

EBITDA Margin 26.5% 27.3% 22.8% 14.7%

Net Margin 17.2% 11.7% 13.1% 1.4%

Total Expenditure/ Total Operating Income 73.5% 72.7% 77.2% 85.3%

Raw Material Cost/ Total Operating Income 62.0% 61.2% 63.3% 70.1%

Staff Cost/ Total Operating Income 2.8% 3.2% 5.2% 6.6%

Interest Cost/Total Debt 4.6% 5.0% 2.8% 7.2%

Other Expenditure/ Total Operating Income 8.7% 8.3% 8.6% 8.6%

RoE 33.6% 17.6% 15.6% 2.0%

RoCE 17.7% 16.2% 8.2% 5.2%

Leverage Ratios FY06 FY 07 FY 08 FY 09

Debt Equity Ratio 1.39 1.25 1.23 1.04

Total Debt/ Capital Employed 0.58 0.56 0.55 0.51

Net Fixed Assets / Net Worth 2.26 2.01 1.66 1.61

Capital Employed to Net Worth Ratio 2.39 2.25 2.23 2.04

Coverage Ratios FY06 FY 07 FY 08 FY 09

Interest Coverage Ratio 6.13 4.76 5.19 1.40

EBDITA / Interest and Finance charges 8.08 6.50 7.86 2.86

EBDITA / Total Debt 0.37 0.33 0.22 0.21

Annexure 7 - Details of IPO Funds Utilized

Expenditure Items Total cost to be Met

from Proceeds of Issue

Estimated Net Proceeds utilization as on March 31

Expenditure Incurred upto 31st July 2009

Balance to be spent

2008 2009

Expansion of the Apparel Facility at Arasur

105.91 105.91 Nil 66.18 39.73

Setting up a design studio at Arasur

5.60 5.60 Nil 1.90 3.70

Construction of additional Hostel Facility at Arasur

71.28 Nil 71.28 Nil 71.28

Expansion of the Processing Facility at SIPCOT, Perundurai

397.02 Nil 397.02 Nil 397.02

Investment in Knitting Facility at Arasur

259.58 259.58 Nil 148.34 111.25

Addition of balancing equipment for Spinning Facility

138.12 138.12 Nil 26.65 111.47

General Corporate Purposes -Normal Capex

241.56 100.00 141.56 230.02 11.54

Issue Expenses 111.15 111.15 Nil 121.87 (10.72)

Total 1,330.22 720.36 609.86 594.95 735.27

Source: Company data, Four-S Research

Rs in mn

Source: Company data, Four-S Research

K.P.R. Mill Limited – Initiating Coverage

Page 32 of 40

Annexure 8 - Key Milestones

Month and Year

Event

Jul-04 The company started a spinning facility with a capacity of 50,784 spindles.

Aug-05 The company initiated implementation of new projects at an outlay of Rs 5,440.5mn comprising a spinning facility with 100,800 spindles, a garment unit with 1,440 sewing machines, a fabric processing unit with capacity to process 23MT of fabric per day and 12 windmills of 1.65MW each with an aggregate capacity of 19.8MW and modernization of the spinning facility located at Sathyamangalam.

Aug-05 K.P.R. Mill Private Limited (for its operations located at Sathyamangalam) and K.P.R. Spinning Mill Private Limited (for its operations located at Karumathampatti) received ISO 14001:2004 certification for their environmental management systems.

Sep-05 K.P.R. Mill Private Limited (for its operations located at Sathyamangalam) and K.P.R. Spinning Mill Private Limited (for its operations located at Karumathampatti) received SA 8000:2001 certification for their social accountability management system certifications for the manufacture of cotton yarn.

Feb-06 The business of K.P.R. Knits was acquired by the company with effect from April 1, 2005.

Mar-06 The company completed installation of 12 windmills with an aggregate capacity of 19.8MW.

Aug-06 K.P.R. Mill Private Limited and K.P.R. Spinning Mill Private Limited merged with and into the company with effect from April 1, 2005.

Nov-06 Private equity investment in the company by Ares Investments, Brandot Investments Limited and Argonaut Ventures.

Aug-07 The company successfully completed its IPO by issuing Rs 10/- paid up equity shares at a premium of Rs 215/- per share thereby enhancing it’s paid up capital to Rs 376.8mn.

Jun-09 The company promoted a wholly owned subsidiary company in the name of Quantum Knits Pvt. Limited and entrusted the management and operation of garment division at Arasur to the subsidiary company.

*Rs. 735.27mn reduction in Overdrafts

Source: Company data

K.P.R. Mill Limited – Initiating Coverage

Page 33 of 40

Annexure 9 – Management Profile Board of Directors

Mr. K. P. Ramasamy Chairman

Mr. Ramasamy, 60 years, is the Chairman of the company. He has over 38 years of experience in the apparel business, particularly in the production and marketing of woven fabric, knitted apparel, cotton yarn and hosiery fabric as well as in dyeing of yarn and fabric. Mr. Ramasamy spearheads the strategic expansion plan initiatives of the company and supervises manufacturing and human resources related functions.