Embed Size (px)

Citation preview

PP10551/09/2011(028936) 28 January 2011

OSK Research | See important disclosures at the end of this report 1

MALAYSIA EQUITYInvestment Research

Daily

Initiating Coverage The Research Team +60 (3) 9207 7600 [email protected]

KimLun Corporation Sturdy Southern Sensation

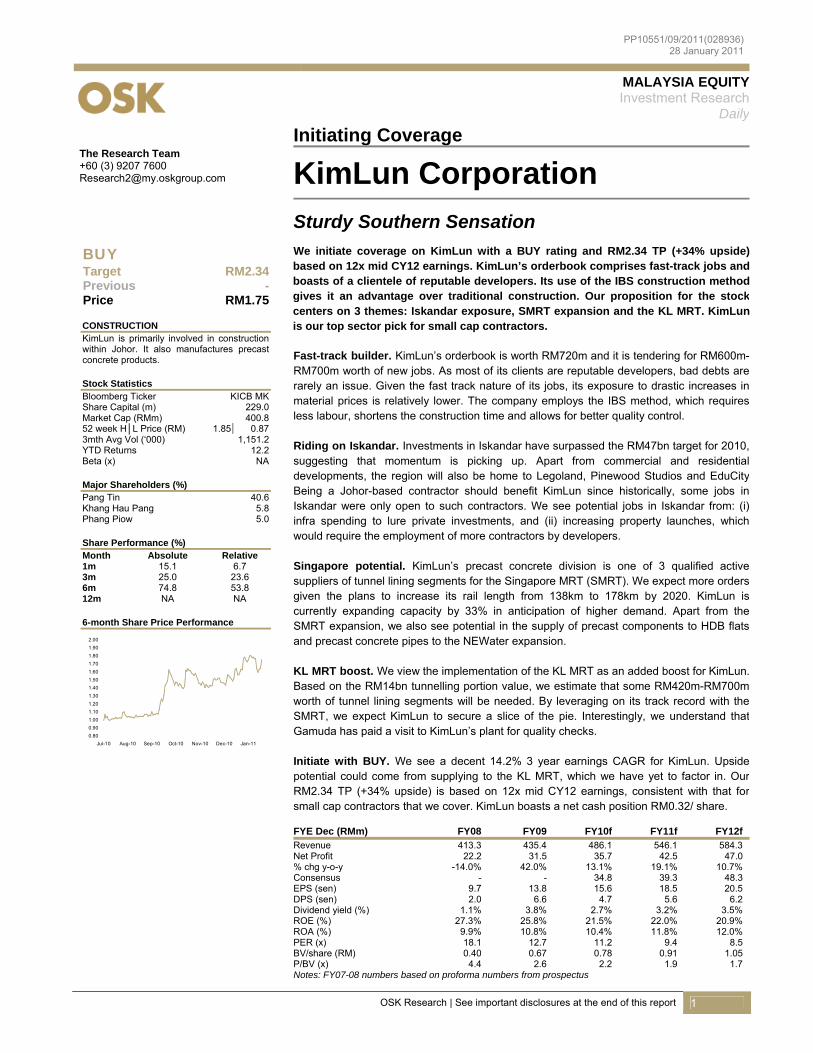

BUY Target RM2.34 Previous - Price RM1.75

CONSTRUCTION KimLun is primarily involved in construction within Johor. It also manufactures precast concrete products.

Stock Statistics Bloomberg Ticker KICB MK Share Capital (m) 229.0 Market Cap (RMm) 400.8 52 week H│L Price (RM) 1.85 0.87 3mth Avg Vol (‘000) 1,151.2 YTD Returns 12.2 Beta (x) NA Major Shareholders (%) Pang Tin 40.6 Khang Hau Pang 5.8 Phang Piow 5.0 Share Performance (%) Month Absolute Relative 1m 15.1 6.7 3m 25.0 23.6 6m 74.8 53.8 12m NA NA

6-month Share Price Performance

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

2.00

Jul-10 Aug-10 Sep-10 Oct-10 Nov-10 Dec-10 Jan-11

We initiate coverage on KimLun with a BUY rating and RM2.34 TP (+34% upside)based on 12x mid CY12 earnings. KimLun’s orderbook comprises fast-track jobs andboasts of a clientele of reputable developers. Its use of the IBS construction methodgives it an advantage over traditional construction. Our proposition for the stockcenters on 3 themes: Iskandar exposure, SMRT expansion and the KL MRT. KimLunis our top sector pick for small cap contractors.

Fast-track builder. KimLun’s orderbook is worth RM720m and it is tendering for RM600m-RM700m worth of new jobs. As most of its clients are reputable developers, bad debts arerarely an issue. Given the fast track nature of its jobs, its exposure to drastic increases in material prices is relatively lower. The company employs the IBS method, which requires less labour, shortens the construction time and allows for better quality control. Riding on Iskandar. Investments in Iskandar have surpassed the RM47bn target for 2010,suggesting that momentum is picking up. Apart from commercial and residential developments, the region will also be home to Legoland, Pinewood Studios and EduCityBeing a Johor-based contractor should benefit KimLun since historically, some jobs in Iskandar were only open to such contractors. We see potential jobs in Iskandar from: (i)infra spending to lure private investments, and (ii) increasing property launches, which would require the employment of more contractors by developers. Singapore potential. KimLun’s precast concrete division is one of 3 qualified active suppliers of tunnel lining segments for the Singapore MRT (SMRT). We expect more orders given the plans to increase its rail length from 138km to 178km by 2020. KimLun is currently expanding capacity by 33% in anticipation of higher demand. Apart from the SMRT expansion, we also see potential in the supply of precast components to HDB flats and precast concrete pipes to the NEWater expansion. KL MRT boost. We view the implementation of the KL MRT as an added boost for KimLun. Based on the RM14bn tunnelling portion value, we estimate that some RM420m-RM700m worth of tunnel lining segments will be needed. By leveraging on its track record with the SMRT, we expect KimLun to secure a slice of the pie. Interestingly, we understand that Gamuda has paid a visit to KimLun’s plant for quality checks. Initiate with BUY. We see a decent 14.2% 3 year earnings CAGR for KimLun. Upside potential could come from supplying to the KL MRT, which we have yet to factor in. Our RM2.34 TP (+34% upside) is based on 12x mid CY12 earnings, consistent with that for small cap contractors that we cover. KimLun boasts a net cash position RM0.32/ share.

FYE Dec (RMm) FY08 FY09 FY10f FY11f FY12f Revenue 413.3 435.4 486.1 546.1 584.3 Net Profit 22.2 31.5 35.7 42.5 47.0 % chg y-o-y -14.0% 42.0% 13.1% 19.1% 10.7%Consensus - - 34.8 39.3 48.3 EPS (sen) 9.7 13.8 15.6 18.5 20.5 DPS (sen) 2.0 6.6 4.7 5.6 6.2 Dividend yield (%) 1.1% 3.8% 2.7% 3.2% 3.5%ROE (%) 27.3% 25.8% 21.5% 22.0% 20.9% ROA (%) 9.9% 10.8% 10.4% 11.8% 12.0% PER (x) 18.1 12.7 11.2 9.4 8.5 BV/share (RM) 0.40 0.67 0.78 0.91 1.05 P/BV (x) 4.4 2.6 2.2 1.9 1.7 Notes: FY07-08 numbers based on proforma numbers from prospectus

OSK Research

OSK Research | See important disclosures at the end of this report 2

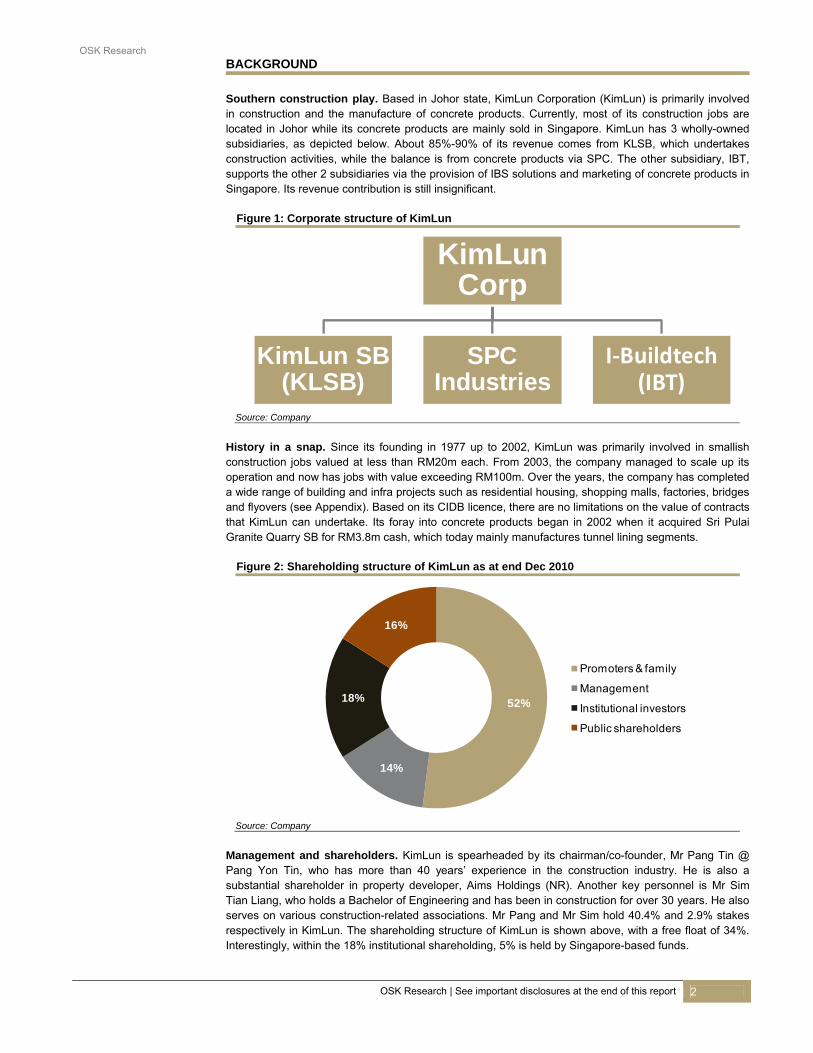

BACKGROUND Southern construction play. Based in Johor state, KimLun Corporation (KimLun) is primarily involved

in construction and the manufacture of concrete products. Currently, most of its construction jobs arelocated in Johor while its concrete products are mainly sold in Singapore. KimLun has 3 wholly-owned subsidiaries, as depicted below. About 85%-90% of its revenue comes from KLSB, which undertakes construction activities, while the balance is from concrete products via SPC. The other subsidiary, IBT, supports the other 2 subsidiaries via the provision of IBS solutions and marketing of concrete products inSingapore. Its revenue contribution is still insignificant.

Figure 1: Corporate structure of KimLun

KimLun Corp

KimLun SB (KLSB)

SPC Industries

I‐Buildtech(IBT)

Source: Company

History in a snap. Since its founding in 1977 up to 2002, KimLun was primarily involved in smallish construction jobs valued at less than RM20m each. From 2003, the company managed to scale up its operation and now has jobs with value exceeding RM100m. Over the years, the company has completed a wide range of building and infra projects such as residential housing, shopping malls, factories, bridgesand flyovers (see Appendix). Based on its CIDB licence, there are no limitations on the value of contracts that KimLun can undertake. Its foray into concrete products began in 2002 when it acquired Sri PulaiGranite Quarry SB for RM3.8m cash, which today mainly manufactures tunnel lining segments.

Figure 2: Shareholding structure of KimLun as at end Dec 2010

52%

14%

18%

16%

Promoters & family

Management

Institutional investors

Public shareholders

Source: Company

Management and shareholders. KimLun is spearheaded by its chairman/co-founder, Mr Pang Tin @ Pang Yon Tin, who has more than 40 years’ experience in the construction industry. He is also a substantial shareholder in property developer, Aims Holdings (NR). Another key personnel is Mr Sim Tian Liang, who holds a Bachelor of Engineering and has been in construction for over 30 years. He alsoserves on various construction-related associations. Mr Pang and Mr Sim hold 40.4% and 2.9% stakes respectively in KimLun. The shareholding structure of KimLun is shown above, with a free float of 34%. Interestingly, within the 18% institutional shareholding, 5% is held by Singapore-based funds.

OSK Research

OSK Research | See important disclosures at the end of this report 3

INVESTMENT THESIS Our investment thesis on KimLun centers on 3 simple, yet bankable themes: (i) exposure to

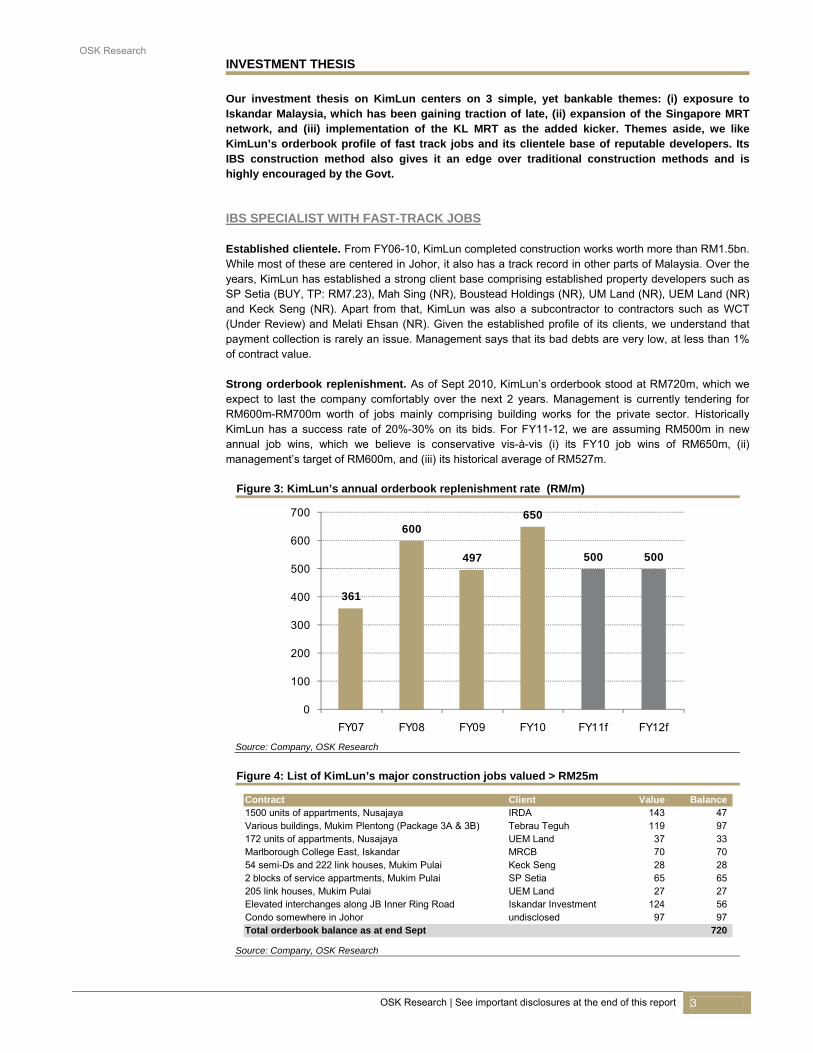

Iskandar Malaysia, which has been gaining traction of late, (ii) expansion of the Singapore MRTnetwork, and (iii) implementation of the KL MRT as the added kicker. Themes aside, we likeKimLun’s orderbook profile of fast track jobs and its clientele base of reputable developers. Its IBS construction method also gives it an edge over traditional construction methods and is highly encouraged by the Govt. IBS SPECIALIST WITH FAST-TRACK JOBS Established clientele. From FY06-10, KimLun completed construction works worth more than RM1.5bn. While most of these are centered in Johor, it also has a track record in other parts of Malaysia. Over the years, KimLun has established a strong client base comprising established property developers such as SP Setia (BUY, TP: RM7.23), Mah Sing (NR), Boustead Holdings (NR), UM Land (NR), UEM Land (NR)and Keck Seng (NR). Apart from that, KimLun was also a subcontractor to contractors such as WCT (Under Review) and Melati Ehsan (NR). Given the established profile of its clients, we understand that payment collection is rarely an issue. Management says that its bad debts are very low, at less than 1% of contract value. Strong orderbook replenishment. As of Sept 2010, KimLun’s orderbook stood at RM720m, which we expect to last the company comfortably over the next 2 years. Management is currently tendering for RM600m-RM700m worth of jobs mainly comprising building works for the private sector. Historically KimLun has a success rate of 20%-30% on its bids. For FY11-12, we are assuming RM500m in new annual job wins, which we believe is conservative vis-à-vis (i) its FY10 job wins of RM650m, (ii) management’s target of RM600m, and (iii) its historical average of RM527m.

Figure 3: KimLun’s annual orderbook replenishment rate (RM/m)

361

600

497

650

500 500

0

100

200

300

400

500

600

700

FY07 FY08 FY09 FY10 FY11f FY12f

Source: Company, OSK Research

Figure 4: List of KimLun’s major construction jobs valued > RM25m

Contract Client Value Balance1500 units of appartments, Nusajaya IRDA 143 47 Various buildings, Mukim Plentong (Package 3A & 3B) Tebrau Teguh 119 97 172 units of appartments, Nusajaya UEM Land 37 33 Marlborough College East, Iskandar MRCB 70 70 54 semi-Ds and 222 link houses, Mukim Pulai Keck Seng 28 28 2 blocks of service appartments, Mukim Pulai SP Setia 65 65 205 link houses, Mukim Pulai UEM Land 27 27 Elevated interchanges along JB Inner Ring Road Iskandar Investment 124 56 Condo somewhere in Johor undisclosed 97 97 Total orderbook balance as at end Sept 720

Source: Company, OSK Research

OSK Research

OSK Research | See important disclosures at the end of this report 4

Mainly fast-track jobs. Most of KimLun’s jobs are fast track in nature, with an average duration of 1.5 years compared to other contractors, whose jobs usually stretch for 2-3 years. Having an orderbook profile of fast-track jobs means that KimLun’s exposure to any drastic increase in raw material prices will be somewhat minimal since these jobs are completed in a relatively shorter time and its newer jobs will be priced to reflect higher prices. For example, when building material prices rose sharply in 2008,KimLun’s gross construction margins fell from 11.7% to 8.2% but recovered quickly in 2009 to 12.3%. While most of the larger contractors did see some margin recovery in 2009, their construction marginswere still below the levels witnessed in 2007 before the material price run-up.

Figure 5: KimLun’s construction margins recovered faster than its larger peers’

0%

2%

4%

6%

8%

10%

12%

14%

2007 2008 2008

KimLun Gamuda IJM WCT

Note: Data for Gamuda and IJM has been calendarised due to non Dec FYE Source: Company annual reports, KimLun prospectus

Understanding the IBS method. In 2008, KimLun set up an Industrial Building System (IBS) division tofacilitate the execution of construction projects based on the IBS concept. Before we dwell further on this,it would be useful to differentiate between traditional construction techniques and the IBS method. Forillustration purposes, consider the construction of an office block. Under traditional construction, thebuilding is constructed as a whole “layer-by-layer” on site. In contrast, under IBS, the various building components (e.g. walls, staircase) are manufactured first and then assembled to make up the building (think of a Lego set!).

Figure 6: Illustration of the IBS method

Source: Company

OSK Research

OSK Research | See important disclosures at the end of this report 5

The merits of IBS. As most of the building components are fabricated and assembled to form thestructure, the IBS method is less labour intensive. The offsite fabrication of components also reduces vulnerability to adverse weather and promotes quality control. Management says the IBS method shortens construction time by 40%-50% versus traditional construction methods. Govt support for IBS. We gather that the Govt encourages the use of IBS for the implementation ofpublic sector jobs. Beginning from Oct 2008, the IBS component of Govt projects must be no less than70%, unless under special circumstances. The Govt is also looking to reduce the number of foreign workers in Malaysia from the current 1.9m to 1.5m (-21%) within the next 3 years. Construction is the second largest sector where foreigners work in, at 19%. As such, the proposed rise in foreign labour levy and mandatory medical insurance would definitely increase contractors’ labour cost. With the lower labour intensity under IBS, we feel that such contractors would be less impacted.

Figure 7: Construction is the 2nd largest sector where foreigners work

Figure 8: Composition of foreign labour nationality in Malaysia

39%

19%

14%

12%

10%

6%

Manufacturing

Construction

Plantations

House maids

Services

Agriculture

Source : Various media sources

51%

17%

10%

8%

8%6%

Indonesia

Bangladesh

Nepal

Vietnam

Myanmar

India

Source : Various media sources

RIDING HIGH ON ISKANDAR Enter Iskandar. Launched in 2006, Iskandar Malaysia (Iskandar) is one of Malaysia’s 5 growth corridors. Iskandar, with a land area of 221,634 hectares in Johor state, is 3 times the size of neighboring Singapore. There are roughly 1.35m people in Iskandar, making up 43% of Johor’s population. It isenvisioned that Iskandar will become a thriving metropolis, with living standards equivalent to that of a developed city. Being located next to Singapore, Iskandar is attempting to mimic Shenzhen, which has benefited from its proximity to Hong Kong and Macau. There are 5 major growth nodes in Iskandar, with Nusajaya being the first to be developed.

Figure 9: Major growth nodes in Iskandar

Source: Iskandar Malaysia

OSK Research

OSK Research | See important disclosures at the end of this report 6

Exceeding investment target. Iskandar Investment Bhd (IIB) was formed to spearhead and coordinate the development of Iskandar. Total investments in Iskandar are expected to total RM382bn by 2025. From 2006-Sept 2010, investments reached RM64.4bn, surpassing the RM47bn target for 2010. IIB has thus far awarded more than RM3bn worth of construction contracts to put in place the necessary infrastructure to lure private investments. Some of the sizeable contracts include a RM766m infra works job to WCT and utility packages worth RM142m and RM94m each to Loh&Loh Corp (NR) and Salcon(BUY, TP: RM0.80). Notable proposed projects in Iskandar include:

Legoland Theme Park, which will be the 5th of its kind in the world and estimated to cost RM750m. Tenders for some small packages (e.g. primary infra, car parks, admin building) havebeen called but are restricted to Johor-based contractors.

Pinewood Studios has agreed to invest RM400m to set up a studio in Iskandar by 2013. TheEuropean studio was involved in blockbusters such as Batman, Lara Croft and Superman.

IIB is also in talks with various local and foreign investors to build a 3- and 4-star hotel, retail mall and high-rise tower in Medini North collectively worth RM1bn.

Bio-XCell is a biotech and ecosystem park in Iskandar jointly developed by UEM Land and BiotechCorp SB. Investments in the development total RM750m, with a RM1bn target set for end-2010. India’s Biocon Ltd plans to invest RM500m to set up an insulin R&D facility there while French based Metex will set up a propanediol plant.

EduCity@Iskandar will be developed into an education hub from 2008-2018. Construction of Phase 1 has commenced with Newcastle University Medicine (NUMed) building a RM300mcampus. Recently, the University of Southampton signed an agreement to open a campus in EduCity. Other education institutions such as Netherlands Maritime Institute of Technology,Management Development Institute of Singapore and Raffles Education have all expressedinterest to set up their campuses there.

There will also be 6 buildings to house federal government departments and agencies in Kota Iskandar worth a total of RM1bn.

Figure 10: Progress of Kota Iskandar in Nusajaya from 2006-2010

Source: Media sources

Connectivity to spur property prices. The governments of Malaysia and Singapore have numerous plans to boost transport connectivity. These include: (i) a 30% reduction in toll rates on the Malaysia-Singapore 2nd Link in Aug 2010, (ii) additional cross border buses and liberalization of taxi services, (iii)proposed MRT link between Iskandar and Singapore, and (iv) proposed High Speed Rail from Kuala Lumpur to Singapore which will pass Johor. We believe that greater connectivity between Iskandar and Singapore will spur property prices in the former and narrow the price difference. This will in turn encourage property developments in Iskandar. KimLun is the best construction proxy to Iskandar. Despite a slow start initially, we believe the growth momentum in Iskandar is finally gaining traction. Just as UEM Land is being viewed as the best proxy for the Iskandar property play, we see KimLun as the favoured proxy on the construction side. As KimLun is Johor based and given its strong track record in the state, KimLun is in a strategic position to ride on the developments at Iskandar. In the past, some of the projects in Iskandar were only awarded toJohor based contractors. KimLun stands to benefit from Iskandar in 2 ways: (i) via the implementation of more infra jobs by the Govt to encourage private sector investment, and (ii) as a contractor to property developers within Iskandar.

OSK Research

OSK Research | See important disclosures at the end of this report 7

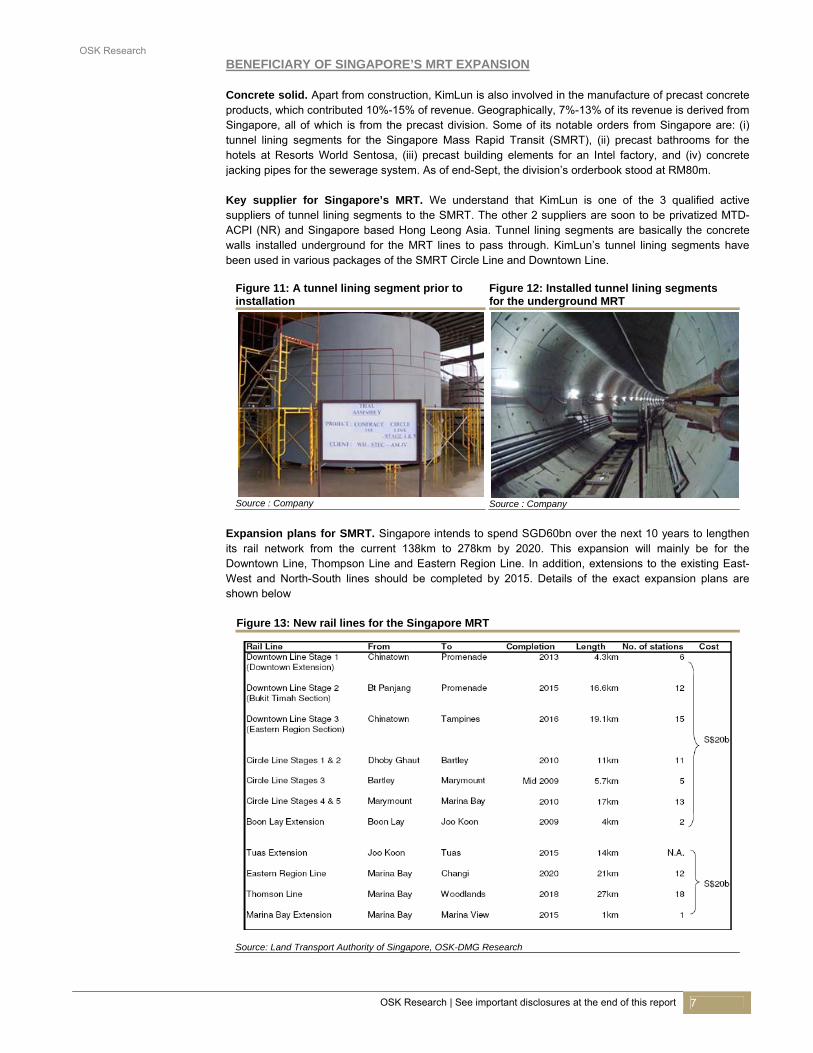

BENEFICIARY OF SINGAPORE’S MRT EXPANSION Concrete solid. Apart from construction, KimLun is also involved in the manufacture of precast concreteproducts, which contributed 10%-15% of revenue. Geographically, 7%-13% of its revenue is derived fromSingapore, all of which is from the precast division. Some of its notable orders from Singapore are: (i) tunnel lining segments for the Singapore Mass Rapid Transit (SMRT), (ii) precast bathrooms for the hotels at Resorts World Sentosa, (iii) precast building elements for an Intel factory, and (iv) concrete jacking pipes for the sewerage system. As of end-Sept, the division’s orderbook stood at RM80m. Key supplier for Singapore’s MRT. We understand that KimLun is one of the 3 qualified active suppliers of tunnel lining segments to the SMRT. The other 2 suppliers are soon to be privatized MTD-ACPI (NR) and Singapore based Hong Leong Asia. Tunnel lining segments are basically the concretewalls installed underground for the MRT lines to pass through. KimLun’s tunnel lining segments havebeen used in various packages of the SMRT Circle Line and Downtown Line.

Figure 11: A tunnel lining segment prior to installation

Figure 12: Installed tunnel lining segments for the underground MRT

Source : Company Source : Company

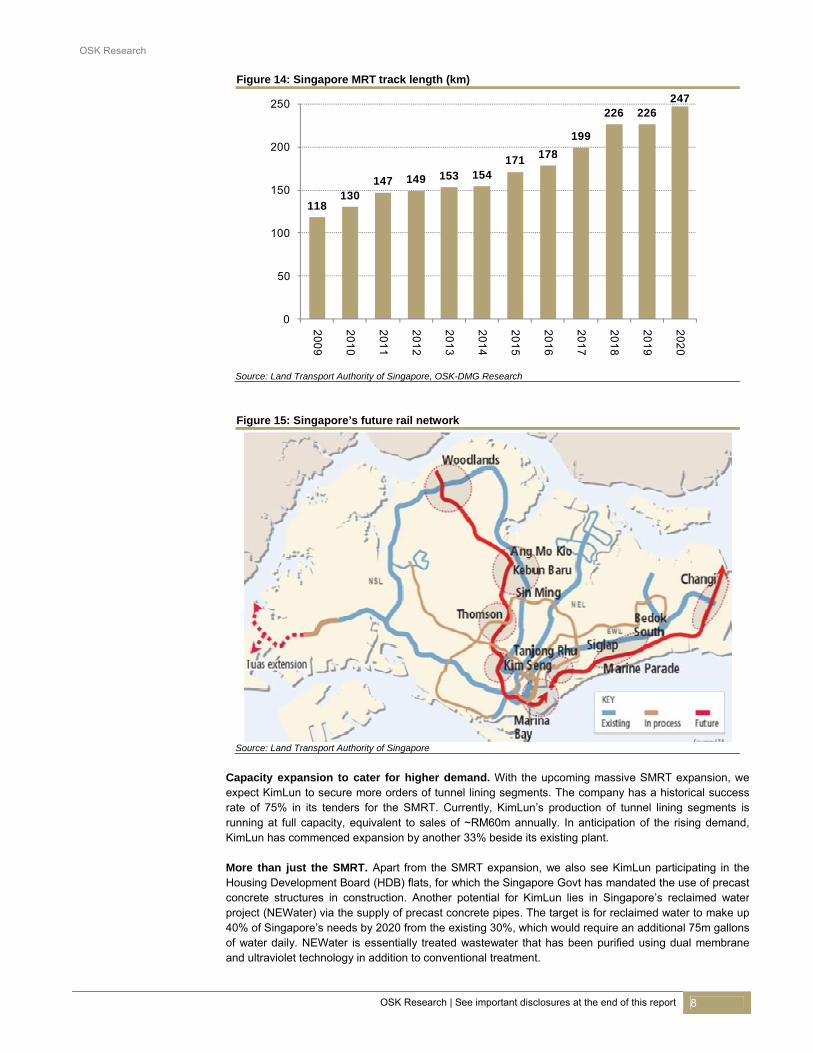

Expansion plans for SMRT. Singapore intends to spend SGD60bn over the next 10 years to lengthen its rail network from the current 138km to 278km by 2020. This expansion will mainly be for the Downtown Line, Thompson Line and Eastern Region Line. In addition, extensions to the existing East-West and North-South lines should be completed by 2015. Details of the exact expansion plans are shown below

Figure 13: New rail lines for the Singapore MRT

Source: Land Transport Authority of Singapore, OSK-DMG Research

OSK Research

OSK Research | See important disclosures at the end of this report 8

Figure 14: Singapore MRT track length (km)

118130

147 149 153 154171 178

199

226 226247

0

50

100

150

200

250

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Source: Land Transport Authority of Singapore, OSK-DMG Research

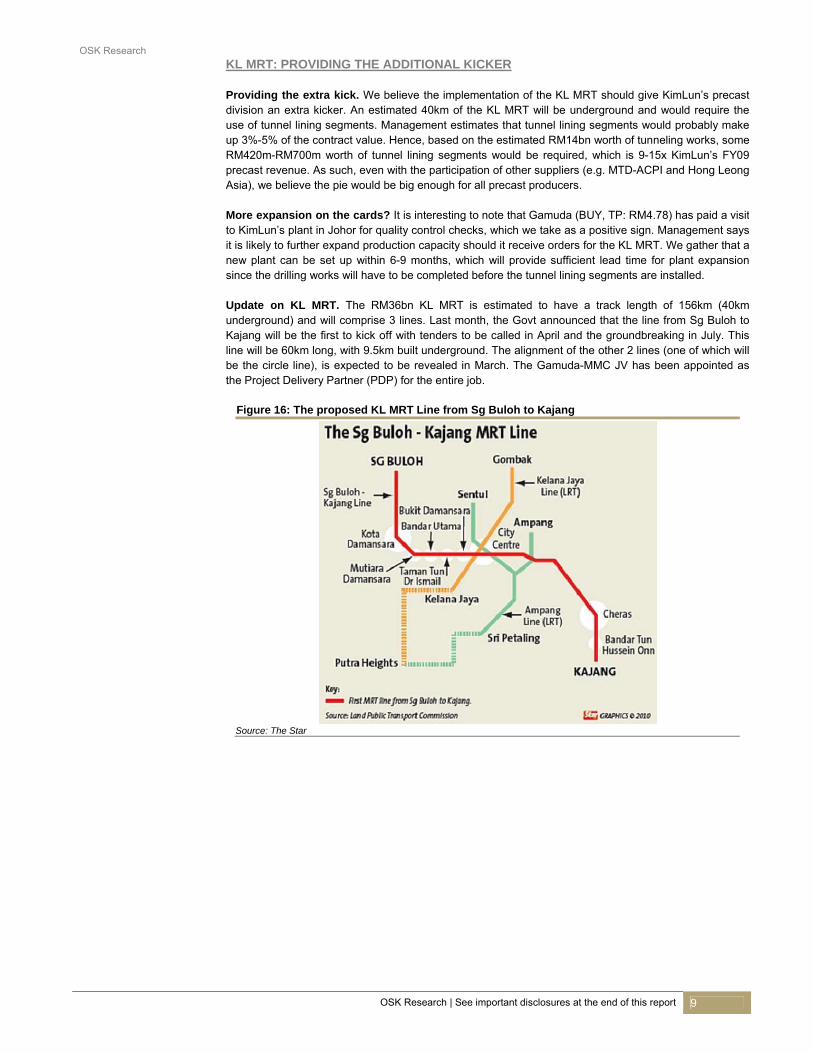

Figure 15: Singapore’s future rail network

Source: Land Transport Authority of Singapore

Capacity expansion to cater for higher demand. With the upcoming massive SMRT expansion, we expect KimLun to secure more orders of tunnel lining segments. The company has a historical success rate of 75% in its tenders for the SMRT. Currently, KimLun’s production of tunnel lining segments is running at full capacity, equivalent to sales of ~RM60m annually. In anticipation of the rising demand, KimLun has commenced expansion by another 33% beside its existing plant. More than just the SMRT. Apart from the SMRT expansion, we also see KimLun participating in the Housing Development Board (HDB) flats, for which the Singapore Govt has mandated the use of precast concrete structures in construction. Another potential for KimLun lies in Singapore’s reclaimed waterproject (NEWater) via the supply of precast concrete pipes. The target is for reclaimed water to make up 40% of Singapore’s needs by 2020 from the existing 30%, which would require an additional 75m gallons of water daily. NEWater is essentially treated wastewater that has been purified using dual membraneand ultraviolet technology in addition to conventional treatment.

OSK Research

OSK Research | See important disclosures at the end of this report 9

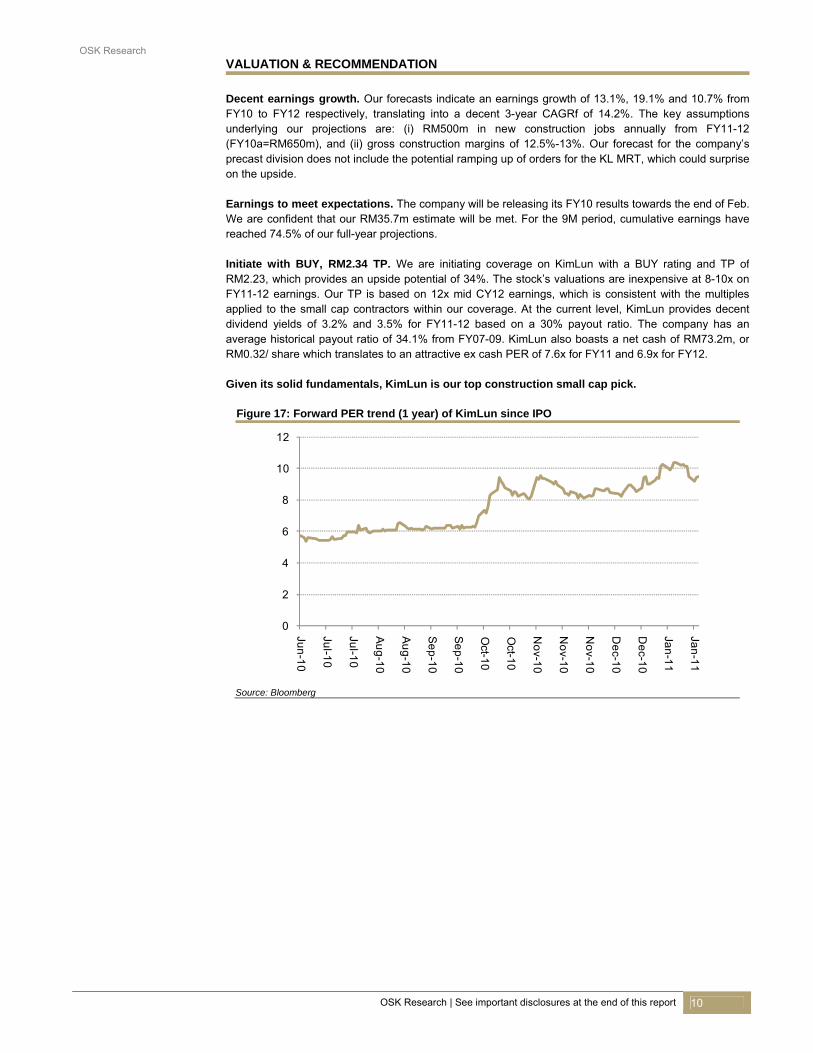

KL MRT: PROVIDING THE ADDITIONAL KICKER Providing the extra kick. We believe the implementation of the KL MRT should give KimLun’s precast division an extra kicker. An estimated 40km of the KL MRT will be underground and would require the use of tunnel lining segments. Management estimates that tunnel lining segments would probably make up 3%-5% of the contract value. Hence, based on the estimated RM14bn worth of tunneling works, some RM420m-RM700m worth of tunnel lining segments would be required, which is 9-15x KimLun’s FY09 precast revenue. As such, even with the participation of other suppliers (e.g. MTD-ACPI and Hong Leong Asia), we believe the pie would be big enough for all precast producers. More expansion on the cards? It is interesting to note that Gamuda (BUY, TP: RM4.78) has paid a visitto KimLun’s plant in Johor for quality control checks, which we take as a positive sign. Management says it is likely to further expand production capacity should it receive orders for the KL MRT. We gather that a new plant can be set up within 6-9 months, which will provide sufficient lead time for plant expansion since the drilling works will have to be completed before the tunnel lining segments are installed. Update on KL MRT. The RM36bn KL MRT is estimated to have a track length of 156km (40kmunderground) and will comprise 3 lines. Last month, the Govt announced that the line from Sg Buloh to Kajang will be the first to kick off with tenders to be called in April and the groundbreaking in July. This line will be 60km long, with 9.5km built underground. The alignment of the other 2 lines (one of which will be the circle line), is expected to be revealed in March. The Gamuda-MMC JV has been appointed as the Project Delivery Partner (PDP) for the entire job.

Figure 16: The proposed KL MRT Line from Sg Buloh to Kajang

Source: The Star

OSK Research

OSK Research | See important disclosures at the end of this report 10

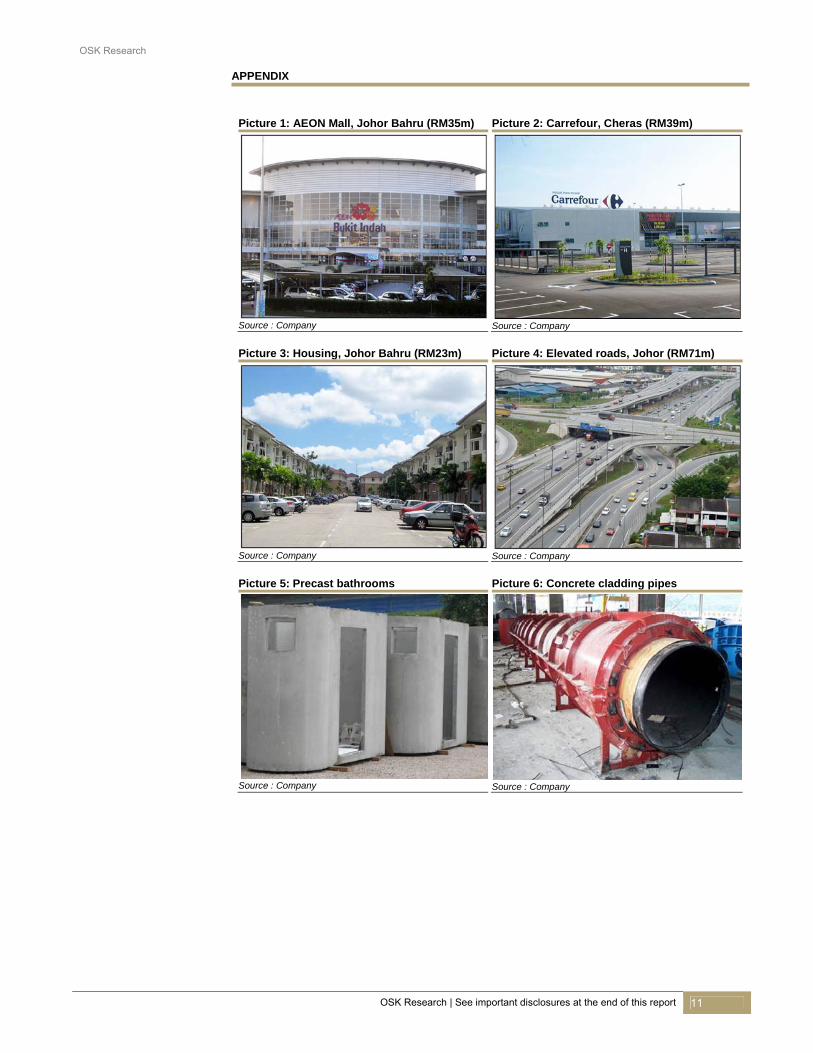

VALUATION & RECOMMENDATION Decent earnings growth. Our forecasts indicate an earnings growth of 13.1%, 19.1% and 10.7% from

FY10 to FY12 respectively, translating into a decent 3-year CAGRf of 14.2%. The key assumptions underlying our projections are: (i) RM500m in new construction jobs annually from FY11-12 (FY10a=RM650m), and (ii) gross construction margins of 12.5%-13%. Our forecast for the company’s precast division does not include the potential ramping up of orders for the KL MRT, which could surprise on the upside. Earnings to meet expectations. The company will be releasing its FY10 results towards the end of Feb. We are confident that our RM35.7m estimate will be met. For the 9M period, cumulative earnings havereached 74.5% of our full-year projections. Initiate with BUY, RM2.34 TP. We are initiating coverage on KimLun with a BUY rating and TP ofRM2.23, which provides an upside potential of 34%. The stock’s valuations are inexpensive at 8-10x on FY11-12 earnings. Our TP is based on 12x mid CY12 earnings, which is consistent with the multiples applied to the small cap contractors within our coverage. At the current level, KimLun provides decent dividend yields of 3.2% and 3.5% for FY11-12 based on a 30% payout ratio. The company has an average historical payout ratio of 34.1% from FY07-09. KimLun also boasts a net cash of RM73.2m, or RM0.32/ share which translates to an attractive ex cash PER of 7.6x for FY11 and 6.9x for FY12. Given its solid fundamentals, KimLun is our top construction small cap pick.

Figure 17: Forward PER trend (1 year) of KimLun since IPO

0

2

4

6

8

10

12

Jun

-10

Jul-1

0

Jul-1

0

Au

g-1

0

Au

g-1

0

Se

p-1

0

Se

p-1

0

Oct-1

0

Oct-1

0

No

v-10

No

v-10

No

v-10

De

c-10

De

c-10

Jan

-11

Jan

-11

Source: Bloomberg

OSK Research

OSK Research | See important disclosures at the end of this report 11

APPENDIX

Picture 1: AEON Mall, Johor Bahru (RM35m) Picture 2: Carrefour, Cheras (RM39m)

Source : Company Source : Company

Picture 3: Housing, Johor Bahru (RM23m) Picture 4: Elevated roads, Johor (RM71m)

Source : Company Source : Company

Picture 5: Precast bathrooms Picture 6: Concrete cladding pipes

Source : Company Source : Company

OSK Research

OSK Research | See important disclosures at the end of this report 12

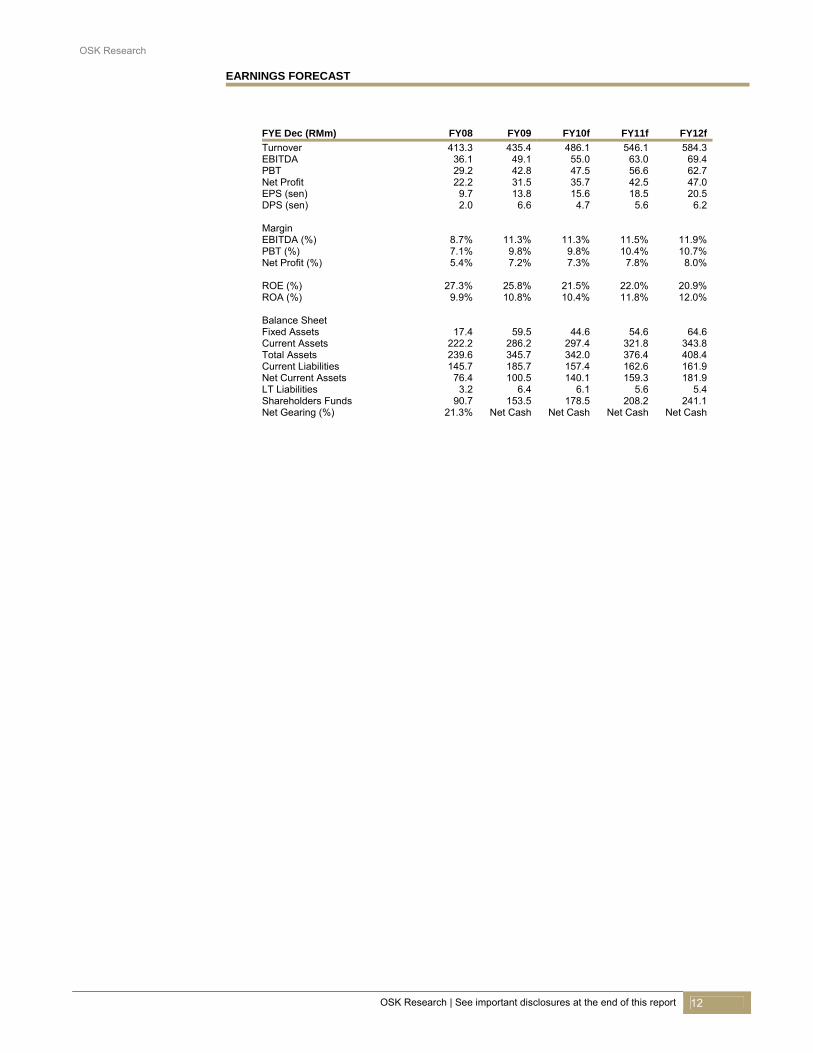

EARNINGS FORECAST

FYE Dec (RMm) FY08 FY09 FY10f FY11f FY12f

Turnover 413.3 435.4 486.1 546.1 584.3EBITDA 36.1 49.1 55.0 63.0 69.4PBT 29.2 42.8 47.5 56.6 62.7Net Profit 22.2 31.5 35.7 42.5 47.0EPS (sen) 9.7 13.8 15.6 18.5 20.5DPS (sen) 2.0 6.6 4.7 5.6 6.2

Margin EBITDA (%) 8.7% 11.3% 11.3% 11.5% 11.9%PBT (%) 7.1% 9.8% 9.8% 10.4% 10.7%Net Profit (%) 5.4% 7.2% 7.3% 7.8% 8.0%

ROE (%) 27.3% 25.8% 21.5% 22.0% 20.9%ROA (%) 9.9% 10.8% 10.4% 11.8% 12.0%

Balance Sheet Fixed Assets 17.4 59.5 44.6 54.6 64.6Current Assets 222.2 286.2 297.4 321.8 343.8Total Assets 239.6 345.7 342.0 376.4 408.4Current Liabilities 145.7 185.7 157.4 162.6 161.9Net Current Assets 76.4 100.5 140.1 159.3 181.9LT Liabilities 3.2 6.4 6.1 5.6 5.4Shareholders Funds 90.7 153.5 178.5 208.2 241.1Net Gearing (%) 21.3% Net Cash Net Cash Net Cash Net Cash

OSK Research

OSK Research | See important disclosures at the end of this report 13

OSK Research Guide to Investment Ratings Buy: Share price may exceed 10% over the next 12 months

Trading Buy: Share price may exceed 15% over the next 3 months, however longer-term outlook remains uncertain

Neutral: Share price may fall within the range of +/- 10% over the next 12 months

Take Profit: Target price has been attained. Look to accumulate at lower levels

Sell: Share price may fall by more than 10% over the next 12 months

Not Rated (NR): Stock is not within regular research coverage All research is based on material compiled from data considered to be reliable at the time of writing. However, information and opinions expressed will be subject to change at short notice, and no part of this report is to be construed as an offer or solicitation of an offer to transact any securities or financial instruments whether referred to herein or otherwise. We do not accept any liability directly or indirectly that may arise from investment decision-making based on this report. The company, its directors, officers, employees and/or connected persons may periodically hold an interest and/or underwriting commitments in the securities mentioned. Distribution in Singapore This research report produced by OSK Research Sdn Bhd is distributed in Singapore only to “Institutional Investors”, “Expert Investors” or “Accredited Investors” as defined in the Securities and Futures Act, CAP. 289 of Singapore. If you are not an “Institutional Investor”, “Expert Investor” or “Accredited Investor”, this research report is not intended for you and you should disregard this research report in its entirety. In respect of any matters arising from, or in connection with, this research report, you are to contact our Singapore Office, DMG & Partners Securities Pte Ltd (“DMG”). All Rights Reserved. No part of this publication may be used or re-produced without expressed permission from OSK Research. Published and printed by :- OSK RESEARCH SDN. BHD. (206591-V) (A wholly-owned subsidiary of OSK Investment Bank Berhad)

Chris Eng

Kuala Lumpur Hong Kong Singapore

Jakarta Shanghai Phnom Penh

Shanghai Office OSK (China) Investment

Advisory Co. Ltd. Room 6506, Plaza 66

No.1266, West Nan Jing Road 200040 Shanghai

China Tel : +(8621) 6288 9611 Fax : +(8621) 6288 9633

PT OSK Nusadana Securities Indonesia

Plaza CIMB Niaga, 14th Floor,

Jl. Jend. Sudirman Kav.25, Jakarta Selatan 12920,

Indonesia. Tel : (6221) 2598 6888 Fax : (6221) 2598 6777

Malaysia Research Office OSK Research Sdn. Bhd.

6th Floor, Plaza OSK Jalan Ampang

50450 Kuala Lumpur Malaysia

Tel : +(60) 3 9207 7688 Fax : +(60) 3 2175 3202

Hong Kong Office OSK Securities Hong Kong Ltd.

12th Floor, World-Wide House

19 Des Voeux Road Central, Hong Kong

Tel : +(852) 2525 1118 Fax : +(852) 2810 0908

Singapore Office DMG & Partners

Securities Pte. Ltd. 20 Raffles Place

#22-01 Ocean Towers Singapore 048620

Tel : +(65) 6533 1818 Fax : +(65) 6532 6211

OSK Indochina Securities Limited No. 263, Ang Duong Street (St. 110),

Sangkat Wat Phnom, Khan Daun Penh,

Phnom Penh, Cambodia. Tel: (855) 2399 2833 Fax: (855) 2399 1822