Embed Size (px)

Citation preview

70

90

110

130

150

170

190

Mar

-16

Mar

-17

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

Jan

-17

Feb

-17

BFL NSE

Bajaj Finance (BFL), owned by Bajaj Finserv (58%) and part of the Bajaj Group, is a fast growing, well-diversified leading NBFC in the country. BFL focuses on four broad categories viz. consumer, commercial, SME and rural compared to the single product focus of most NBFCs on CV finance, gold finance or auto finance.

Focus of BFL's business model has been on building scale with profitability. So, the product portfolio of the company has been balanced with Home Loans, LAP, commercial lending (high ticket sizes) with 2/3 wheelers, consumer durables, lifestyle finance and personal loans (high yields) resulting in AUM growth coupled with profit maximisation.

The company's diverse portfolio offers good scope for cross selling of products to its creditworthy customers. The ability to mine the existing client base augurs well for profitability as it reduces client acquisition costs. To enable faster loan appraisal for repeat customers, company provides an EMI card to all its consumer durable customers.

BLF has reduced the turnaround time for loan applications through considerable investments in business analytics, from a few hours to 15 minutes thus allowing it to compete with credit cards in this segment. The turnaround time is maintained due to large in-house database and better data availability with CIBIL.

Asset quality has been amongst the best in the BFSI space(NNPA at 0.3%), attained by being alert to potential asset quality risks and taking steps like exiting construction equipment and infrastructure lending and slowing down financing in LAP, 3 wheeler financing in a timely manner.

BFL has benefitted from strong retail credit demand reflected in its strong AUM CAGR of 36% over FY12-FY16. At the same time, diligent lending has resulted in stable margins (NIMs 10.8%) and healthy return ratios (ROAA 3.2%, ROAE 20.9%).

BFL's business model has a competitive edge over other NBFCs on risk and growth profile. Its loan book has compounded at 36% over FY12-FY16, due to its active churning of portfolio products keeping in mind the macro picture, its choice of borrowers as well as its robust risk management. Further, the USP of BFL is its stronghold in the consumer durable (CD) & lifestyle product financing business wherein it does not have any major competition. Despite strong growth in loans, the asset quality and provisioning remain among the best in the system. Given the strong growth rate, high margins and return ratios, its premium valuations within the NBFC space is justified. We recommend a BUY on BFL with a target price of 1,421(5.5x FY19E P/ABV).

Financial Summary - consolidated

Particulars, Rs cr FY15 FY16 FY17E FY18E FY19E

Net Interest Income

PPOP

PAT

EPS (Rs)

ROAE (%)

ROAA (%)

Adj. BVPS (Rs)

P/ABV (x)

2,872

1,742

898

18.0

20.4

3.1

92.8

12.7

4,030

2,508

1,279

23.9

20.9

3.2

136.4

8.7

5,326

3,510

1,819

33.8

22.0

3.2

164.4

7.2

7,179

4,738

2,415

44.8

23.7

3.1

202.4

5.8

9,444

6,247

3,204

59.4

25.1

3.0

258.4

4.6Source : Company; RSL Research

Religare Investment Call

March 31, 2017

BFSI

CMP (Rs)

Target Price (Rs)

Potential Upside

Sensex

Nifty

Key Stock data

BSE Code

NSE Code

Bloomberg

Shares o/s, Cr (FV 2)

Market Cap (Rs Cr)

3M Avg Volume

52 week H/L

Shareholding Pattern

(%)

Promoter

FII

DII

Others

1 Year relative price performance

1,170

1,421

21.5%

29,598

9,163

500034

BAJFINANCE

BAFIN

53.6

63,229.2

1,249,864

1,206/664

Jun-16

57.4

19.7

5.5

17.5

Sep-16

57.4

19.4

5.1

18.2

Dec-16

58.1

18.5

5.5

18.0

Research Analyst

Siji A [email protected]

Investment rationale

Outlook & Valuation

Initiating Coverage Bajaj Finance Ltd

Best placed for sustained outperformance...BUY

Initiating Coverage BFSI

Religare Investment Call

Bajaj Finance Ltd

Investment rationale

Diversified product profile mitigates portfolio concentration risk

BFL, one of the leading NBFCs in India, started as a captive financier to 2/3 wheelers manufactured by Bajaj Auto. Since then, the company has explored various other lending segments and became an industry bell-weather in the retail asset financing segment. Its diversified product portfolio currently comprises of more than 30 products divided broadly into four categories like consumer, SME, commercial and rural. It is the largest financier of 2 wheelers and consumer durables in the country.

The company has Rs 44,229 crs (FY16) of Assets under Management (AUM) and witnessed strong growth at 36% CAGR over FY12-FY16. The portfolio mix is skewed towards Consumer (43%) and SME (42%) segments while Commercial (12%) and Rural (3%) form the rest. The company's reach and distribution channels are strong with a presence of 304 consumer branches and 519 rural locations with over 35,000+ distribution points. Further, for various product lines, BFL has tie-ups with all major manufacturers and dealers in consumer durables, lifestyle financing, digital products, etc.

Consumer financing segment continues its positive traction

In the four broad categories, Consumer Finance book (CF) as on FY16 was at Rs 18,996 cr, comprising 43% of the total AUM. Within the CF book, Consumer Durable financing (CD) and Lifestyle Product financing book were at Rs 5,556 cr and Rs 1,016 cr, respectively. Apart from these, the CF book includes 2/3 wheeler finance, personal loans and home loans to salaried individuals.

Consumer Finance (43% of AUM) SME (42% of AUM) Commercial (12% of AUM) Rural (3% of AUM)

Vendor Financing Consumer Durable FinancingAuto Financing Small Business Loans

Loan Against Property Construction Equipment Financing Gold Loans

Infra Lending Personal Loans

Consumer Durable

Loan Against Securities

Business Loans

Lifestyle Financing

Personal Loans

Home Loans

Professional Loans

Loans Against Property

SME Cross Sell

Digital Product Financing

Salaried Personal Loans

Source : Company; RSL Research

Portfolio Mix Increasing Share of Consumer Finance

42.9

42.3

11.83.0

Consumer Finance SME Commercial Rural

40.7 38.8 40.7 42.944.249.9 48.0

42.3

15.011.1 10.3 11.8

0.0 0.2 1.0 3.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

FY13 FY14 FY15 FY16

Consumer Finance SME Commercial Rural

Four broad business categories viz. consumer, SME, commercial and rural

Consumer Finance and SME Finance are the two dominant categories with +42% share

Growth in Consumer Finance driven by Consumer Durable and Lifestyle Product Financing

Initiating Coverage BFSI

Religare Investment Call

Bajaj Finance Ltd

In the past five years, BFL has witnessed strong accretion in new customer acquisition each year in the CD financing business with increase in Point of sales from 3,500 in FY13 to 9,400 in FY16 resulting in an increased new customer base of ~47 lacs from ~19 lacs in FY13. Even lifestyle product finance (that includes digital products financing i.e. mobile phones, laptops, etc and non-digital i.e. furniture, furnishing etc.) started in FY13 saw a robust increase from 37,000 new customers served in FY13 to ~7 lac new customers in FY16.

Currently, BFL is amongst the largest new client acquirers in India with an overall increase of new clients from 28 lacs in FY13 to 68 lacs in FY16. This increase is owing to BFL's large distribution network and reach. It has 193 branches with 9,400+ point of sales or distribution franchises in CD finance. Further, it has 8,400+ points of sales in lifestyle products (5,200+ in digital financing and 3,200+ in non-digital financing).

CD financing is largely a duopoly market with the two prominent players in the organized market, being BFL and Capital First. BFL enjoys the dominant market share and is the largest consumer electronic lender financing high value items such LCD, refrigerators, air-conditioners, mobile phones, etc.

It has capitalised strongly on its “0% financing” product, which enabled it to gain customer popularity. Almost the entire CD financing and lifestyle product financing business is through “0% financing”. Under this scheme, the customer does not have to pay any interest on his purchase, also getting the convenience of paying the purchase price in easy installments. The customer pays ~30% as down payment and the balance amount in EMI of seven to eight months. BFL gets 1-1.5% processing fees and ~6-8% of the product value as subvention from manufacturers. Further, the company offers EMI (Existing Membership Identification) cards to its existing customers. This card enables the holder to purchase consumer durables & lifestyle products by availing a loan from BFL thus providing quick & hassle-free finance. Customers simply have to Swipe & Sign to buy using an EMI card. As of Q3FY17, about 68 lac EMI cards have been offered.

BFL's stronghold in the CD financing business is on the back of its large reach, formidable relationships with dealers and manufacturers, strong brand, expertise of several years and database of such large customers. These factors act as entry barriers in the CD financing business and give BFL a competitive advantage.

Lifestyle Financing Personal Loans (PL)

2012 2012

Digital & Non Digital viz Mobiles, Furniture

PL to existing clients

Consumer Durable

Mass Affluent Existing clients

1995

~0.4lacs ~5lacs 12m 30 - 36m

TV, AC,LED

25 - 26% 16 - 18%

Mass Affluent

~0.3lacs

9m

24 - 26%

Auto Financing

1987

2/3 Wheeler

Mass clients

~0.5 - 1.5lacs2 - 3 yrs

22 - 25%

Particulars

Year

Product

Target

Ticket size

Duration

Yield range

Source : Company; RSL Research

CF AUM – Growth & Share (%)

EMI cards and 0% financing popular features of Consumer Financing

30.7

41.5

43.9

42.1

38.8 40.7

42.9

46.9

25.0

30.0

35.0

40.0

45.0

50.0

5,000

10,000

15,000

20,000

25,000

30,000

FY14 FY15 FY16 YTDFY17

CF (Rs cr, LHS) Growth (%) % of AUM

Further, we believe the competition will remain low as banks are largely focused on housing finance or auto financing within retail loans while other NBFCs are in niche areas like auto finance, housing finance, gold finance or infrastructure finance.

Sizeable financing market in consumer category products offers great opportunity

Overall macro indicators are very conducive for fast paced growth in the consumer financing space. Higher spending by a growing middle class population, increasing penetration in rural areas, growing urbanization rate would aid surge in demand for white goods, which will keep the need for financing in this space robust.

2/3 wheeler financing business – captive financing model

BFL has been present in 2/3 wheeler financing since its inception and is the largest 2 wheeler financier, focused on semi-urban and rural markets. This business has a captive financing model wherein BFL finances 2 wheelers produced by its group company Bajaj Auto and contributes ~30% of the total Bajaj Auto's domestic 2 wheeler sales. BFL also finances ~15% of Bajaj Auto's 3 wheeler sales. BFL continues to capitalize on Bajaj Auto's distribution network to build its loan book and has access to >3,000 dealers.

Though there has been a decline in the 2 wheeler financing proportion in BFL's overall AUM, the company is still the largest 2 wheeler lender with a market share of ~20%.

Cross selling opportunities reduce client acquisition costs

The large number of customers acquired through the CD financing business allows BFL to cross-sell various other products to customers with a healthy credit history. These products include personal loans, life/general insurance, etc. Further, home loans to salaried individuals are also covered in CF financing and have a book size of ~3% of AUM.

Initiating Coverage

Religare Investment Call

Macro indicators conducive for robust growth in Consumer Finance category

Proportion of 2/3 wheeler finance less than 10% in overall AUM

BFSI Bajaj Finance Ltd

Source : Mckinsey Global Institute, IMF, RSL Research

Increase in Per Capita Income Rise in Middle Class Population

Source : Mckinsey Global Institute, IMF, RSL Research

Growth in Urbanisation Growth in White Goods & TV Market

1,4

30

1,5

22

1,4

96

1,5

08

1,6

27

1,8

08 2

,67

2

0

500

1,000

1,500

2,000

2,500

3,000

2010 2011 2012 2013 2014 2015 2020

India's per capita GDP (in USD)

CAGR 8.1%

1 1 91 2 419

32

618

41

43

3693

80

5436

21

0

20

40

60

80

100

1985 1995 2005 2015E 2025E

Globals (%) Strivers (%) Seekers (%) Aspirers (%) Deprived (%)

Middle Class

0

500

1,000

1,500

2,000

2,500

2013 2014 2015 2016E 2020P

Washing Machine (Rs bn) Refrigerator (Rs bn)

AC (Rs bn) TV (Rs bn)

18.0

18.223.3

25.7

27.8

31.238.0

0

5

10

15

20

25

30

35

40

1960-61 1980-81 2000-01 2024-25E

Urbanisa�on rate in India (%)

We expect the share of the CF segment in total AUM mix to increase mainly led by CD financing & lifestyle financing segment, on the back of a rise in sales of consumer durable, increased finance penetration and jump in the share of BFL in the overall financing market.

Mortgage heavy SME financing book – steady growth

Share of BFL's SME book has come down gradually from ~50% in FY14 to ~42% in FY16 and includes small business loans, loan against property (LAP), home loans to self-employed & loan against securities (LAS). The slowdown in SME book was deliberate on management's assessment that the LAP market was getting overheated. Share of LAP book in overall AUM has come down to 19% in FY16 from 25% in FY15; though it continues to have the highest share in the overall AUM. To diversify its mortgage business, BFL also lends to non-salaried individuals which stood at ~10% of AUM.

Business loans (~10% of AUM) are mostly working capital loans with a ticket size of Rs 10-30 lacs with an average maturity of 2-3 yrs. In the LAS segment, company provides working capital and growth capital to high net worth SMEs, with established financials against marketable securities.

Commercial financing – traction dependent on underlying economic trend

In the commercial segment, BFL provides finance in the construction equipment (CE) and infrastructure space. Apart from these, BFL also offers wholesale lending products covering short, medium and long term needs of auto component vendors in India. The proportion of commercial segment has increased from 10.3% in FY15 to 12% in FY16. There has been a continuous run down in the book related to CE and infra financing. These segments witnessed asset quality pressures in the past resulting in actively slowing down exposure. Going ahead, share of commercial lending could improve as macro recovery gradually picks up.

Initiating Coverage

Religare Investment Call

BFSI Bajaj Finance Ltd

Home LoansLoan Against Securities (LAS)

SME Cross Sell

Small Business Loans

Particulars

2009 20102009Year

Self employed HNIs & Ultra HNIs SME clients2010

SME clients1 - 2cr

Target50lacs75lacs - 2cr

10 - 30lacs

Ticket size15 - 20yrs 1yr NA

2 - 3yrsDuration

12 - 13.8% 10.3 - 20%18 - 20%Yield range 10.3 - 12%

Infra Lending

2010

Particulars Vendor Financing

Year

Affluent

Construction Equipment Financing

2009

NA

Target

1 - 15yrs

2010

Ticket size

Bajaj Auto Vendors

12 - 14%

NA

Duration

Strategic & Retail

Yield range

Loan Against Property (LAP)

2009

NA

HNIs & Ultra HNIs1cr - 5cr15 - 20yrs

11.5 - 13%

1cr - 3cr

NA

3yrs

10.5 - 12.5%

Source : Company; RSL Research

SME AUM – Growth & Share (%)

55.0

29.5

20.2

12.8

49.948.0

42.3

36.6

5.0

15.0

25.0

35.0

45.0

55.0

65.0

1,000

5,000

9,000

13,000

17,000

21,000

25,000

FY14 FY15 FY16 YTDFY17

SME (Rs cr, LHS) Growth (%) % of AUM

SME Financing dominated by LAP

Lending in Commercial category set to increase

Initiating Coverage

Religare Investment Call

Rural financing to maintain strong growth on lower base, increasing reach

In the rural financing category, BFL is a highly diversified lender. The company is currently present in CD financing, asset backed financing, gold loans, personal loans, etc. BFL functions through a hub & spoke model. The company operates its rural business in Maharashtra, Gujarat, Karnataka, Madhya Pradesh and Rajasthan. As the business commenced in FY13, the book size is small and witnessed sharp traction. We expect the rural portfolio to continue to witness robust growth, going ahead.

Strong operating metrics to sustain

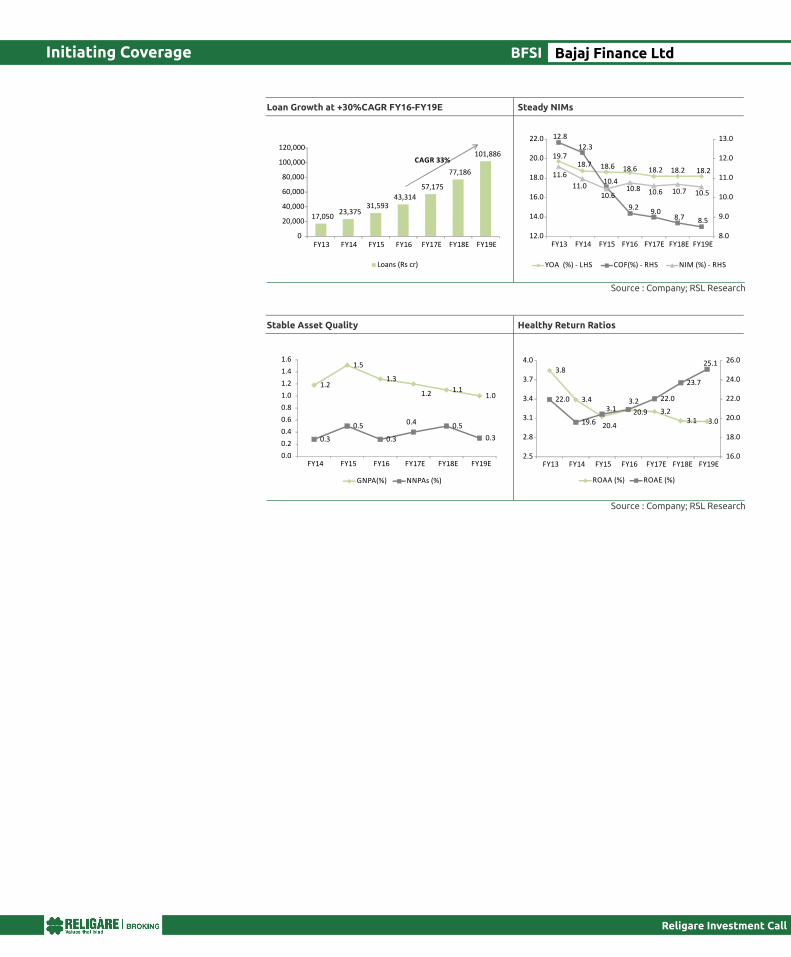

Overall book expected to grow at +30% CAGR over FY16-19E

BFL has a diversified loan portfolio with a leadership position in under penetrated & growing segments like CD financing, lifestyle product financing, 2 wheeler financing, LAP, etc. These factors have allowed BFL to clock strong AUM CAGR of 36% over FY12-16. This has been despite a weak economic environment in the past few years.

The traction in AUM in the past four years has been led by the Consumer Finance segment, which grew 39% followed by SME (34%) and Commercial Lending (26%). The LAP portfolio in the SME segment, accounts for highest proportion (~19%) in overall AUM. CD financing

Rural financing spread across five states currently

L o a n g r o w t h e x p e c t e d t o b e maintained at +30% CAGR over FY16-FY19E

BFSI Bajaj Finance Ltd

Commercial AUM – Growth & Share (%)

Source : Company; RSL Research

Source : Company; RSL Research

1.7

24.3

56.5

33.7

11.1 10.3 11.8 12.1

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY14 FY15 FY16 YTDFY17

Commercial (Rs cr, LHS) Growth (%) % of AUM

Rural AUM – Growth & Share (%)

0.2

1.0

3.0

4.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

500

1,000

1,500

2,000

2,500

3,000

FY14 FY15 FY16 YTDFY17

Rural (Rs cr, LHS) % of AUM

Initiating Coverage

Religare Investment Call

is 13% of the entire portfolio. Of the total AUM, BFL places about 3-5% for securitisation for better asset liability management which leads to a difference in the AUM and actual advances outstanding in the balance sheet. Going ahead, we expect overall advances traction to continue at +30% CAGR over FY16- 19E, primarily driven by CF segment.

NIMs expected to sustain

The margins of BFL are one of the highest among its peers. Its margins during FY16 were at 10.8% on the back of strong blended yields of 18.6% (pushed by high yields in CF segment) and competitive Cost of Funds, which helps the company to earn an overall spread of 9.2%.

With banks reducing their base rates, the company could benefit going ahead on the Cost of Funds front. However, lower yields expected in segments like SME (which is predominantly mortgage) could pare some of these savings. We expect margins to moderate a bit, but still remain healthy compared to peers and remain in +10% range.

Operational efficiency to be maintained

In the past, BFL had to resort to continuous investments to streamline operations, expanding its network, upgrade technology for maintaining large database of customers, their behavioral pattern and on other analytics in CD, lifestyle financing and the SME business to meet increasing asset generation. However, we believe that, to a large extent, fixed costs have been incurred, BFL since then is reaping the benefits of the same. BFL's cost-to-income ratio has improved to 43.7% in FY16 from 46% in FY14. Cost to average assets has also been stable at ~5% in the last two years. We expect further improvement as incremental costs comes down.

Asset quality stable & well capitalized

BFL's gross NPA ratio at 1.3% as on FY16 is relatively better than some of its peers and also considering the weak economic environment of the past two or three years. Post setbacks in FY09-FY10, the company has focused on improving its risk management process and framework which included focusing on safer products like LAP and mortgages, increased use of Cibil scores, focusing on repeat customers with good repayment pattern and on affluent & mass affluent customers. These efforts helped in maintaining stable asset quality with NNPAs at less than 1% in the last five years.

BFL is in a comfortable position on the capital adequacy front with CAR of 19.5% and Tier I of 16.1%, which is well above the RBI capital requirements. We expect the current capital to be sufficient to meet growth requirements for the next two or three years.

Diversified borrowing profile

Funding profile is diversified among banks, debentures, commercial papers and fixed deposits. As on FY16, the borrowing mix remains skewed towards banks (48%) followed by debt markets (46%) and retail deposits (6%). Being a highly rated company (viz. Credit rating of AAA/Stable by India Ratings (Fitch), AA+/Positive by CRISIL & AA+/Stable by ICRA), cost of funds is lower and stood at 9.2%. Further, at regular intervals, the company was able to raise funds via QIP, which also helped in reducing its funding costs. We expect funding costs to continue at lower levels and derive further savings in a lower interest rate scenario.

Return ratios to sustain

BFL has delivered strong earnings growth supported by improved credit profile, strong NIMs and best in class asset quality with lower credit costs. PAT has compounded at +30% over last four years, posting PAT of Rs 1,279 cr in FY16. Consequently, ROAAs have remained steady at +3%. We expect the strong growth in profitability to continue with return ratios staying healthy.

Steady NIMs of +10% improving over last four years

Asset quality stable through prudent risk management processes; NNPA less than 1%

Funding profile a mix of banks (48%), debt markets (46%) and retail deposits (6%)

ROAA to be maintained at +3%

BFSI Bajaj Finance Ltd

Initiating Coverage

Religare Investment Call

Source : Company; RSL Research

Loan Growth at +30%CAGR FY16-FY19E Steady NIMs

BFSI Bajaj Finance Ltd

17,05023,375

31,59343,314

57,175

77,186

101,886

0

20,000

40,000

60,000

80,000

100,000

120,000

FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Loans (Rs cr)

CAGR 33%

Source : Company; RSL Research

Stable Asset Quality Healthy Return Ratios

1.2

1.5

1.3

1.2 1.11.0

0.3

0.5

0.3

0.4 0.5

0.3

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

FY14 FY15 FY16 FY17E FY18E FY19E

GNPA(%) NNPAs (%)

3.8

3.43.1

3.2

3.23.1 3.0

22.0

19.6 20.4

20.9

22.0

23.7

25.1

16.0

18.0

20.0

22.0

24.0

26.0

2.5

2.8

3.1

3.4

3.7

4.0

FY13 FY14 FY15 FY16 FY17E FY18E FY19E

ROAA (%) ROAE (%)

19.718.7 18.6 18.6 18.2 18.2 18.2

12.8

12.3

10.6

9.29.0

8.7 8.5

11.6

11.010.4

10.8 10.6 10.7 10.5

8.0

9.0

10.0

11.0

12.0

13.0

12.0

14.0

16.0

18.0

20.0

22.0

FY13 FY14 FY15 FY16 FY17E FY18E FY19E

YOA (%) - LHS COF(%) - RHS NIM (%) - RHS

Initiating Coverage

Religare Investment Call

Bajaj Finance (BFL) is one of the leading NBFCs in India and is part of the well-known Bajaj group. Incorporated in 1987, it started as a captive financier to Bajaj Auto's vehicles. Initially, BFL was promoted by the erstwhile Bajaj Auto and Bajaj Auto Holdings. However, as per the scheme of de-merger of erstwhile Bajaj Auto in 2007, the shareholding of Bajaj Auto in the company has been vested with Bajaj Finserv, which is the financial services arm of the Bajaj Group. Subsequent to being a primarily, two wheeler financier, company entered into various other lending segments and became one of the significant players in the retail asset-financing industry. BFL's diversified product suite now comprises >30 product lines divided broadly into four categories like consumer, SME, commercial and rural. The company is the largest financier of two-wheelers and consumer durables in India.

Company Background

BFSI Bajaj Finance Ltd

Bajaj Finance

Legacy

CD Financing

2W & 3W Financing

FY08

Life Insurance

Personal Loans

Cross Selll

FY09&FY10

Rs 4,000 cr

Business Loans

Loan Against Shares -

Promoter

Loans Against

Property

Vendor Financing

Extended Warranty Cross Sell

FY11

Rs 7,600 cr

Home Loans - Self

Employed

Loan Against Shares -

Retail

ConstructionEquipment Financing*

FY12

Rs 13,100 cr

Salaried Personal

Loans

Professional Loans

Relationship

Mngmt

InfrastructureFinancing*

Co-branded Credit Card*

EMI Card

FY13

Rs 17,500 cr

Lifestyle Product

Financing

Home Loans -Salaried

Lease Rental Disc.

FY14

Rs 24,100 cr

Consumer Rural

Lending

Retailer Finance

General Insurance

Distribution

Crisil SME Rating

Consumer Financial Fitness Report

FY15

Rs 32,400 cr

Digital Finance

Property Fitness Report

MSME Rural

Lending

FY16

Rs 44,200 cr

E-Commerce

Seller Finance

SME Financial Fitness Report

Financial Institutions

Lending Business

Light Engineering

Business

Corporate Finance Business

Urban Gold Loans

BFL Product Journey

*Exited Businesses Source : Company; RSL Research

Initiating Coverage

Religare Investment Call

Segment concentration risk: Though BFL's loan book is well diversified; certain products like LAP, CD financing have higher share. Any large decline in property price could lead to asset quality stress cropping up in the LAP segment. Demand for consumer durables depends on various factors like state of the economy, employment opportunities etc. Any letdown can also impact demand for consumer durables and other lifestyle products. In turn, this could impact the advances growth of BFL and consequently, its profitability.

Increasing competition in CF segment: BFL's key strength against its peers is in its stronghold in the CD financing business and lifestyle product financing business. Currently no major player except Capital First Ltd is in this business who can pose a challenge to BFL but there are no entry barriers too. With demand for corporate loans and SME loans expected to remain weak, other financial institutions like banks and NBFCs may look towards this under penetrated CD financing business. This may reduce BFL's strong positioning or compel it to resort to risky ways of going about its business. This may lead to a reduction in the premium multiple it gets currently.

MCLR applied to banks may get imposed to NBFCs: RBI has imposed a Marginal Cost Lending Rate (MCLR) on banks which slightly impacted margins. As has been witnessed in the past, the RBI has gradually subjected NBFCs to the same NPA provisioning guidelines as applicable to banks. Similar instance can also happen in lending rate calculation for NBFCs which can have negative implications NBFC's margins.

Risks & Concerns

BFSI Bajaj Finance Ltd

Interest Earned

Interest Expended

Net Interest Income

Other Income

Total Income

Total Operating Exp

PPOP

Provisions & Contingencies

PBT

Provision for Tax

PAT

Particulars, Rs cr FY16

FY18E FY15 FY19E

FY17E

Source : Company; RSL Research

6,957

2,927

4,030

427

4,457

1,949

2,508

543

1,965

686

1,279

12,273

5,094

7,179

892

8,071

3,333

4,738

1,022

3,716

1,300

2,415

5,120

2,248

2,872

298

3,170

1,429

1,742

385

1,357

459

898

16,098

6,654

9,444

1,061

10,505

4,258

6,247

1,317

4,930

1,725

3,204

9,205

3,879

5,326

729

6,055

2,545

3,510

711

2,799

980

1,819

P&L Account

Religare Investment Call

Initiating Coverage BFSI Bajaj Finance Ltd

SOURCES OF FUNDS

Share capital

Reserves and surplus

Shareholders' funds

Total Borrowings

Other Liabilities, provisions

Total

APPLICATION OF FUNDS

Advances

Investments

Fixed assets

Other Assets

Total assets

Particulars, Rs cr FY16

FY18E FY15 FY19E

FY17E

Source : Company; RSL Research

107

7,320

7,427

37,025

2,005

46,456

43,314

1,029

290

1,823

46,457

108

11,190

11,298

67,924

11,576

90,798

77,186

1,245

296

12,070

90,798

100

4,700

4,800

26,655

1,325

32,780

31,593

326

252

608

32,780

108

14,124

14,232

88,641

16,457

119,330

101,886

1,370

299

15,775

119,330

108

8,982

9,090

49,171

8,837

67,097

57,175

1,132

293

8,496

67,097

Balance sheet

Religare Investment Call

Initiating Coverage BFSI Bajaj Finance Ltd

VALUATION RATIOS

EPS

Earnings Growth (%)

BVPS (ex reval.)

Adj. BVPS (ex reval. & 100% cover)

RoAA (%)

ROAE (%)

P/E (x)

P/ABV (x)

P/PPOP (x)

Dividend Yield (%)

PROFITABILITY

Yield on Advances (%)

Cost of Funds (%)

Core Spread (%)

NIM (%)

OPERATING EFFICIENCY

Cost/Avg. Asset Ratio (%)

Cost-Income Ratio (%)

BALANCE SHEET STRUCTURE RATIOS

Loan Growth (%)

Borrowing Growth (%)

Equity/Assets (%)

Equity/Loans (%)

Total Capital Adequacy Ratio (CAR)

ASSET QUALITY

Gross NPL (%)

Net NPLs (%)

Provision/Avg. AUM (%)

Particulars, Rs cr FY16

FY18E FY15 FY19E

FY17E

Source : Company; RSL Research

23.9

42.4

138.7

136.4

3.2

20.9

49.5

8.7

5.0

0.2

18.6

9.2

9.4

10.8

4.9

43.7

38.9

16.0

17.1

19.5

16.1

1.3

0.3

1.4

44.8

32.8

209.6

202.4

3.1

23.7

26.4

5.8

2.7

0.3

18.2

8.7

9.5

10.7

4.2

41.3

38.1

12.4

14.6

15.9

12.4

1.1

0.5

1.5

18.0

24.9

96.0

92.8

3.1

20.4

65.8

12.7

6.8

0.2

18.6

10.6

8.1

10.4

5.0

45.1

67.1

14.6

15.2

18.0

14.2

1.5

0.5

1.4

59.4

32.7

264.0

258.4

3.0

25.1

19.9

4.6

2.0

0.4

18.2

8.5

9.7

10.5

4.1

40.5

30.5

11.9

14.0

15.4

11.9

1.0

0.3

1.5

33.8

42.3

168.6

164.4

3.2

22.0

35.0

7.2

3.6

0.2

18.2

9.0

9.2

10.6

4.5

42.0

32.8

13.5

15.9

17.0

13.5

1.2

0.4

1.4

Key Ratios

Religare Investment Call

Initiating Coverage BFSI Bajaj Finance Ltd

Net Interest Income

Non Interest Income

Operating Cost

Provisions

Tax

ROAA

Leverage (x)

ROAE

Particulars, Rs cr FY16

FY18E FY15 FY19E

FY17E

Source : Company; RSL Research

10.8

1.1

5.2

1.4

1.8

3.4

6.1

20.9

10.7

1.3

5.0

1.5

1.9

3.6

6.6

23.7

10.4

1.1

5.2

1.4

1.7

3.3

6.3

20.4

10.5

1.2

4.8

1.5

1.9

3.6

7.0

25.1

10.6

1.5

5.1

1.4

1.9

3.6

6.1

22.0

ROAA TREE

Religare Investment Call

Before you use this research report , please ensure to go through thedisclosure inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulat ions , 2014 and Research Disc la imer at the fol lowing l ink : http://old.religareonline.com/research/Disclaimer/Disclaimer_RSL.htmlSpecific analyst(s) specific disclosure(s) inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulations, 2014 is/are as under:Statements on ownership and material conflicts of interest , compensation– Research Analyst (RA) [Please note that only in case of multiple RAs, if in the event answers differ inter-se between the RAs, then RA specific answer with respect to questions under F (a) to F(j) below , are given separately]

S. No. Statement Answer

Tick appropriate

I/we or any of my/our relative has any financial interest in the subject company? [If answer is yes, nature of Interestis given below this table]

I/we or any of my/our relatives, have actual/beneficial ownership of one per cent. or more securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance?

I / we or any of my/our relative, has any other material conflict of interest at the time of publication of the research report or at the time of public appearance?

I/we have received any compensation from the subject company in the past twelve months?

I/we have managed or co-managed public offering of securities for the subject company in the past twelve months?

I/we have received any compensation for brokerage services from the subject company in the past twelve months?

I/we have received any compensation for products or services other than brokerage services from the subject company in the past twelve months?

I/we have received any compensation or other benefits from the subject company or third party in connection with the research report?

I/we have served as an officer, director or employee of the subject company?

I/we have been engaged in market making activity for the subject company?

YES NO

NO

NO

NO

NO

NO

NO

NO

NO

NO

NO

Nature of Interest ( if answer to F (a) aboveis Yes : …………………………………………………………………………………………………………………………………………………............................................Name(s)with Signature(s)of RA(s).[Please note that only in case of multiple RAs andif the answers differ inter-se between the RAs, then RA specific answer with respect to questions under F (a) to F(j) above , are given below]

SS.No Name(s) of RA Signatures of RASerial Question of question which the signing RA needs

to make separate declaration / answer YES NO

Copyright in this document vests exclusively with RSL. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose, without prior written permission from RSL. We do not guarantee the integrity of any emails or attached files and are not responsible for any changes made to them by any other person.

Disclaimer: www.religareonline.com/research/Disclaimer/Disclaimer_RSL.html

Initiating Coverage BFSI Bajaj Finance Ltd