Embed Size (px)

Citation preview

1

w

Ashok Leyland is one of the leading commercial vehicle manufacturer in India with its headquarters in Chennai, with medium & heavy commercial vehicles (MHCV) as its core business. Ashok Leyland is the 2nd largest manufacturer of commercial vehicles in India and also the 4th largest manufacturer of buses in the world. With Strong manufacturing capabilities, growing market share and international presence, the company has a good potential of future growth. We remain positive on AL’s future prospects and initiate coverage with a BUY rating with a target price of Rs 151, which gives an upside potential of 29 %.

Key Investment Rationale:

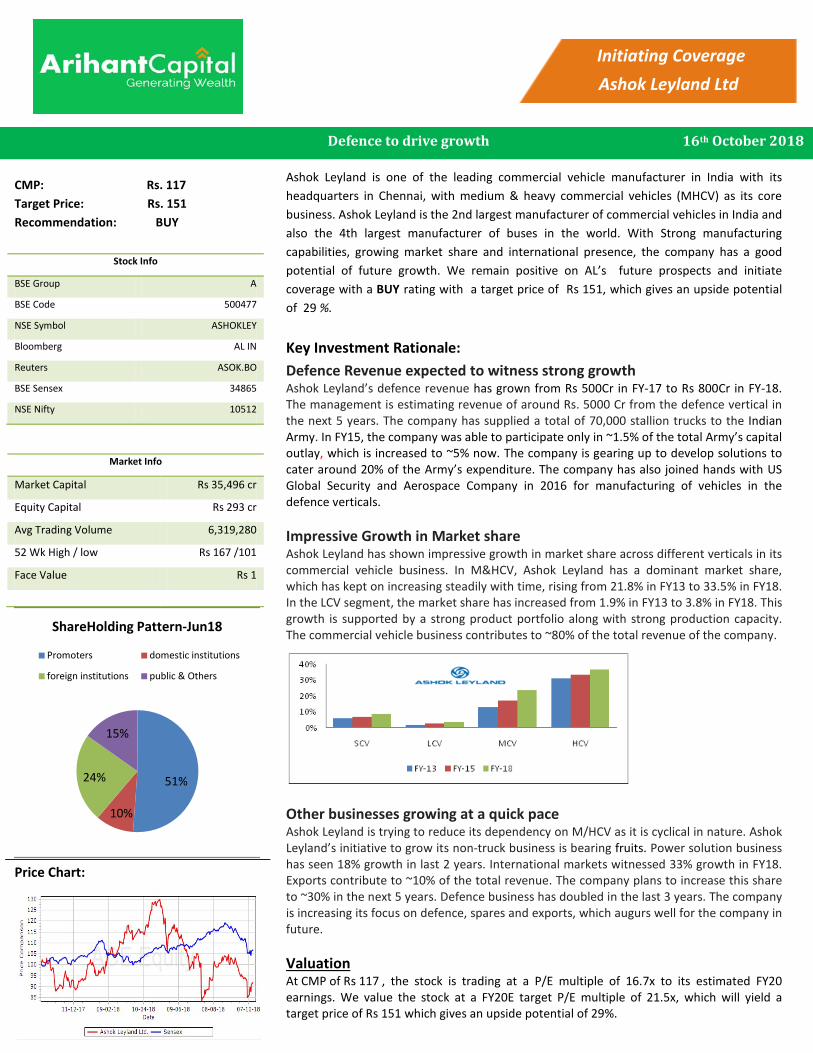

Defence Revenue expected to witness strong growth Ashok Leyland’s defence revenue has grown from Rs 500Cr in FY-17 to Rs 800Cr in FY-18. The management is estimating revenue of around Rs. 5000 Cr from the defence vertical in the next 5 years. The company has supplied a total of 70,000 stallion trucks to the Indian Army. In FY15, the company was able to participate only in ~1.5% of the total Army’s capital outlay, which is increased to ~5% now. The company is gearing up to develop solutions to cater around 20% of the Army’s expenditure. The company has also joined hands with US Global Security and Aerospace Company in 2016 for manufacturing of vehicles in the defence verticals. Impressive Growth in Market share Ashok Leyland has shown impressive growth in market share across different verticals in its commercial vehicle business. In M&HCV, Ashok Leyland has a dominant market share, which has kept on increasing steadily with time, rising from 21.8% in FY13 to 33.5% in FY18. In the LCV segment, the market share has increased from 1.9% in FY13 to 3.8% in FY18. This growth is supported by a strong product portfolio along with strong production capacity. The commercial vehicle business contributes to ~80% of the total revenue of the company.

Other businesses growing at a quick pace Ashok Leyland is trying to reduce its dependency on M/HCV as it is cyclical in nature. Ashok Leyland’s initiative to grow its non-truck business is bearing fruits. Power solution business has seen 18% growth in last 2 years. International markets witnessed 33% growth in FY18. Exports contribute to ~10% of the total revenue. The company plans to increase this share to ~30% in the next 5 years. Defence business has doubled in the last 3 years. The company is increasing its focus on defence, spares and exports, which augurs well for the company in future. Valuation At CMP of Rs 117 , the stock is trading at a P/E multiple of 16.7x to its estimated FY20 earnings. We value the stock at a FY20E target P/E multiple of 21.5x, which will yield a target price of Rs 151 which gives an upside potential of 29%.

CMP: Rs. 117 Target Price: Rs. 151 Recommendation: BUY

Stock Info

BSE Group A

BSE Code 500477

NSE Symbol ASHOKLEY

Bloomberg AL IN

Reuters ASOK.BO

BSE Sensex 34865

NSE Nifty 10512

Market Info

Market Capital Rs 35,496 cr

Equity Capital Rs 293 cr

Avg Trading Volume 6,319,280

52 Wk High / low Rs 167 /101

Face Value Rs 1

Price Chart:

51%

10%

24%

15%

ShareHolding Pattern-Jun18

Promoters domestic institutions

foreign institutions public & Others

Initiating Coverage

Ashok Leyland Ltd

Defence to drive growth 16th October 2018

2

Automobile

Industry Overview Automobile Industry of India As India's transport network is developing, Indian Automobile Industry is growing too. Also, the Automobile industry growth has a strong co-relation with GDP growth because it is directly linked with the growth of road network, infrastructure growth, and it provides employment to a large section of the population. Thus, the role of Automobile Industry is very essential for Indian economy. The industry can be broadly classified into the following, car manufacturing, two-wheeler manufacturing, and heavy vehicles manufacturing.

Indian Commercial Vehicle Industry: Classification The CV Industry in India is split into the following segments; Light Commercial Vehicles(LCV), MCV (Medium Commercial Vehicles) and HCV(Heavy Commercial Vehicles). These are classified according to GVW(Gross Vehicle Weight).According to Industry norms, vehicles with GVW less than 7.5 tonnes are classified as LCVs while the ones heavier than these are termed M/HCV. These segments can be classified further into various sub-segments based on their applications.

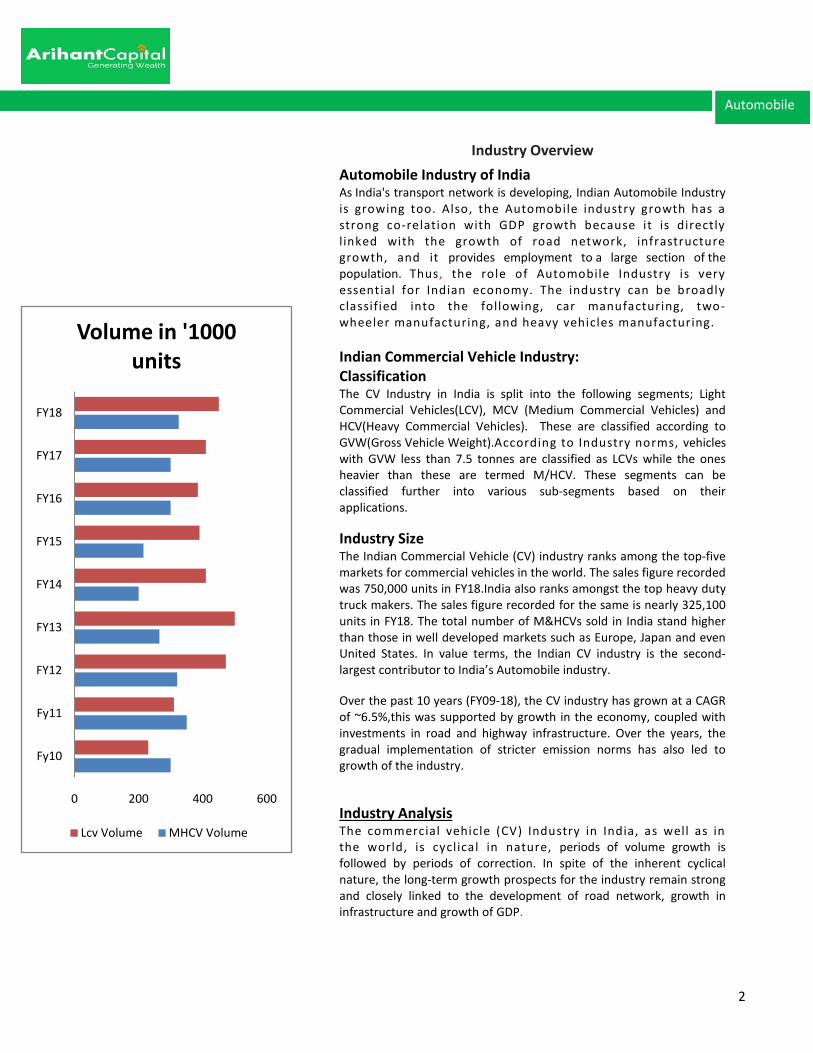

Industry Size The Indian Commercial Vehicle (CV) industry ranks among the top-five markets for commercial vehicles in the world. The sales figure recorded was 750,000 units in FY18.India also ranks amongst the top heavy duty truck makers. The sales figure recorded for the same is nearly 325,100 units in FY18. The total number of M&HCVs sold in India stand higher than those in well developed markets such as Europe, Japan and even United States. In value terms, the Indian CV industry is the second-largest contributor to India’s Automobile industry. Over the past 10 years (FY09-18), the CV industry has grown at a CAGR of ~6.5%,this was supported by growth in the economy, coupled with investments in road and highway infrastructure. Over the years, the gradual implementation of stricter emission norms has also led to growth of the industry.

Industry Analysis The commercial vehicle (CV) Industry in India, as well as in the world, is cycl ical in nature, periods of volume growth is followed by periods of correction. In spite of the inherent cyclical nature, the long-term growth prospects for the industry remain strong and closely linked to the development of road network, growth in infrastructure and growth of GDP.

0 200 400 600

Fy10

Fy11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

Volume in '1000 units

Lcv Volume MHCV Volume

3

Automobile

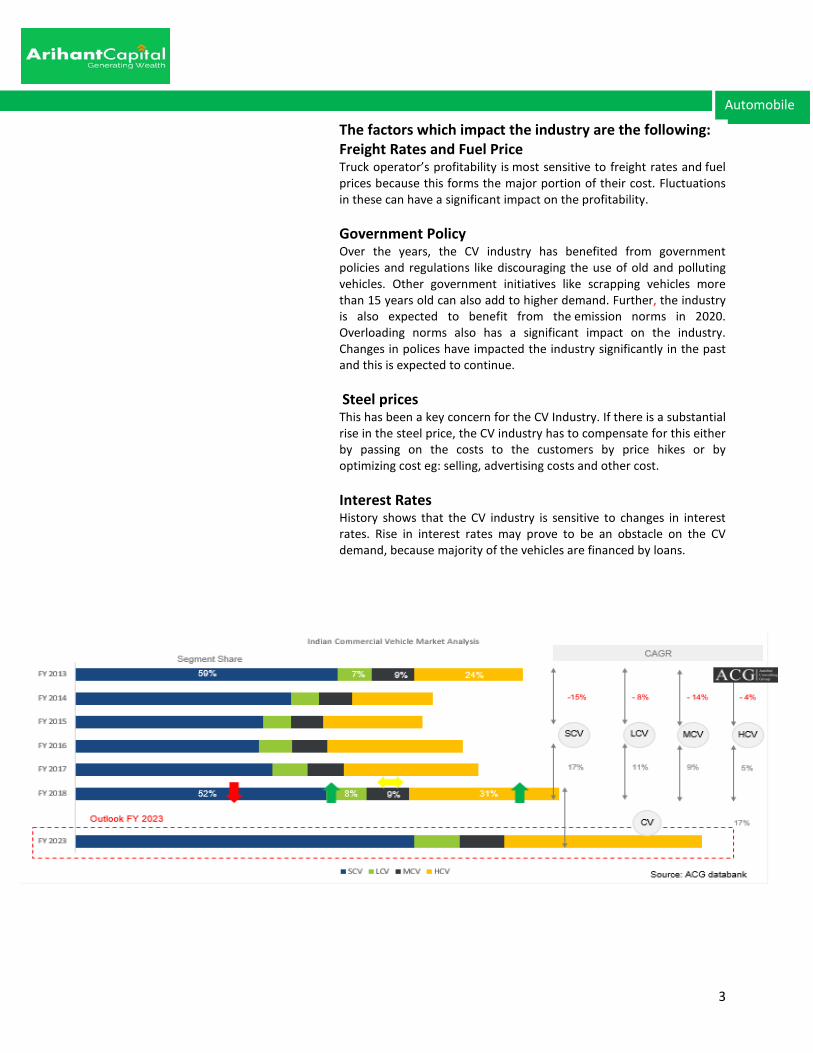

The factors which impact the industry are the following: Freight Rates and Fuel Price Truck operator’s profitability is most sensitive to freight rates and fuel prices because this forms the major portion of their cost. Fluctuations in these can have a significant impact on the profitability. Government Policy Over the years, the CV industry has benefited from government policies and regulations like discouraging the use of old and polluting vehicles. Other government initiatives like scrapping vehicles more than 15 years old can also add to higher demand. Further, the industry is also expected to benefit from the emission norms in 2020. Overloading norms also has a significant impact on the industry. Changes in polices have impacted the industry significantly in the past and this is expected to continue. Steel prices This has been a key concern for the CV Industry. If there is a substantial rise in the steel price, the CV industry has to compensate for this either by passing on the costs to the customers by price hikes or by optimizing cost eg: selling, advertising costs and other cost. Interest Rates History shows that the CV industry is sensitive to changes in interest rates. Rise in interest rates may prove to be an obstacle on the CV demand, because majority of the vehicles are financed by loans.

4

Automobile

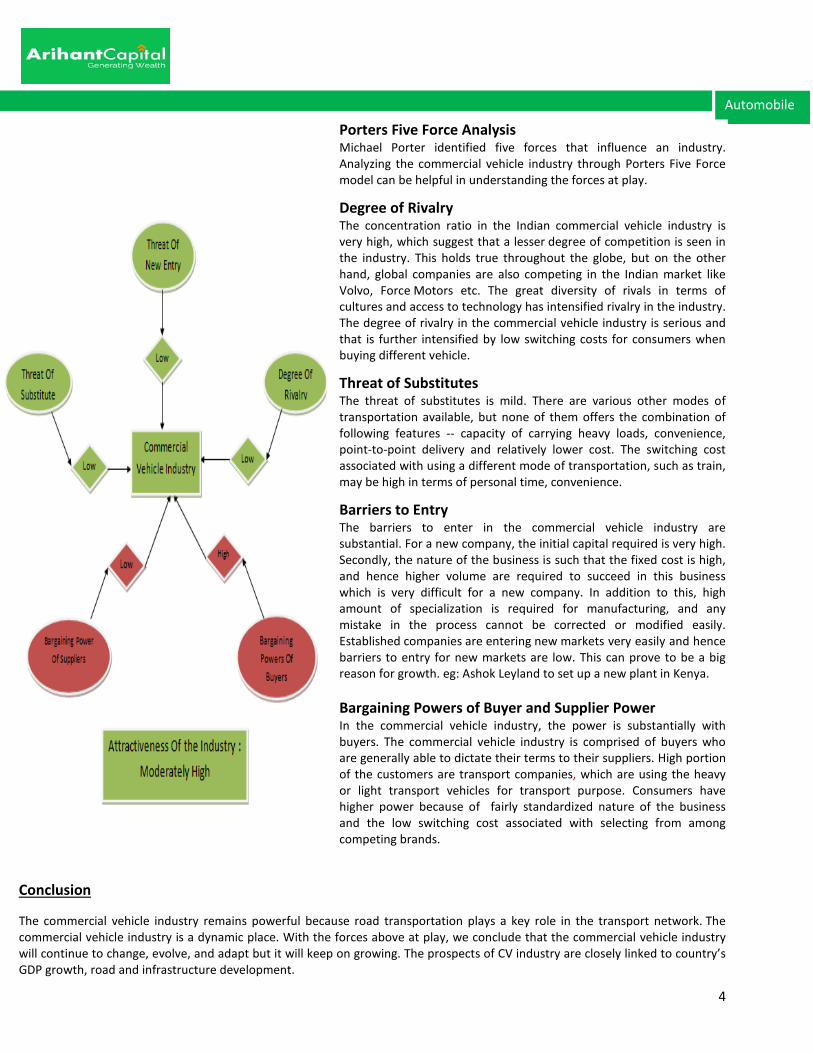

Porters Five Force Analysis Michael Porter identified five forces that influence an industry. Analyzing the commercial vehicle industry through Porters Five Force model can be helpful in understanding the forces at play.

Degree of Rivalry The concentration ratio in the Indian commercial vehicle industry is very high, which suggest that a lesser degree of competition is seen in the industry. This holds true throughout the globe, but on the other hand, global companies are also competing in the Indian market like Volvo, Force Motors etc. The great diversity of rivals in terms of cultures and access to technology has intensified rivalry in the industry. The degree of rivalry in the commercial vehicle industry is serious and that is further intensified by low switching costs for consumers when buying different vehicle.

Threat of Substitutes The threat of substitutes is mild. There are various other modes of transportation available, but none of them offers the combination of following features -- capacity of carrying heavy loads, convenience, point-to-point delivery and relatively lower cost. The switching cost associated with using a different mode of transportation, such as train, may be high in terms of personal time, convenience.

Barriers to Entry The barriers to enter in the commercial vehicle industry are substantial. For a new company, the initial capital required is very high. Secondly, the nature of the business is such that the fixed cost is high, and hence higher volume are required to succeed in this business which is very difficult for a new company. In addition to this, high amount of specialization is required for manufacturing, and any mistake in the process cannot be corrected or modified easily. Established companies are entering new markets very easily and hence barriers to entry for new markets are low. This can prove to be a big reason for growth. eg: Ashok Leyland to set up a new plant in Kenya. Bargaining Powers of Buyer and Supplier Power In the commercial vehicle industry, the power is substantially with buyers. The commercial vehicle industry is comprised of buyers who are generally able to dictate their terms to their suppliers. High portion of the customers are transport companies, which are using the heavy or light transport vehicles for transport purpose. Consumers have higher power because of fairly standardized nature of the business and the low switching cost associated with selecting from among competing brands.

Conclusion

The commercial vehicle industry remains powerful because road transportation plays a key role in the transport network. The commercial vehicle industry is a dynamic place. With the forces above at play, we conclude that the commercial vehicle industry will continue to change, evolve, and adapt but it will keep on growing. The prospects of CV industry are closely linked to country’s GDP growth, road and infrastructure development.

5

Automobile

Key Investment Rationale Impressive Growth in Market share Ashok Leyland has shown impressive growth in market share across different verticals in its commercial vehicle business. In M&HCV, Ashok Leyland has a dominant market share, which has kept on increasing steadily with time increasing it from 21.8% in FY13 to 33.5% in FY18.In the LCV segment, the market share has increased from 1.9% in FY13 to 3.9% in FY18. This growth is supported by a strong product portfolio along with strong production capacity. Defence Revenue expected to witness strong growth Ashok Leyland had earned a revenue of Rs 500 crore from the defence vertical in FY17 and Rs 800 crore in FY18.The management is estimating a revenue of around Rs. 5000 Cr from the defence sector in the next 5 years. The company has also joined hands with US Global Security and Aerospace Company in 2016 for manufacturing of vehicles in the defence verticals.

LCV Business has been a big positive LCV business has seen a 35% growth in volume in FY18.The market share has also increased from 1.9% in FY-13 to 3.9% in FY18. Margins have also improved in the LCV category. Management plans to invest Rs. 400Cr in this particular segment over the next 2 years. Other businesses growing at a quick pace Ashok Leyland is trying to reduce its dependency on M/HCVS as it is cyclical in nature. Ashok Leyland’s initiative to grow its non-truck business is bearing fruit. Power solution business has seen 18% growth in last 2 years. International markets witnessed 33% growth in FY18. Defence business has doubled in the last 3 years. The company is increasing its focus on defence, spares and exports, which augurs well for the company in future. Company Background

Ashok Leyland is the 2nd largest manufacturer of commercial vehicles in India, the 4th largest manufacturer of buses in the world, and one of the largest manufacturers of trucks. Ashok Leyland has been a major player in India's commercial vehicle industry with a reputation of technological leadership, achieved through tie-ups with international technological leaders and high quality internal research and development. Access to international technology has given the company a reputation of being first with technology. The company offers a wide range of products like buses, trucks, engines, defence & special vehicles. It has its headquarters in Chennai.

6

Automobile

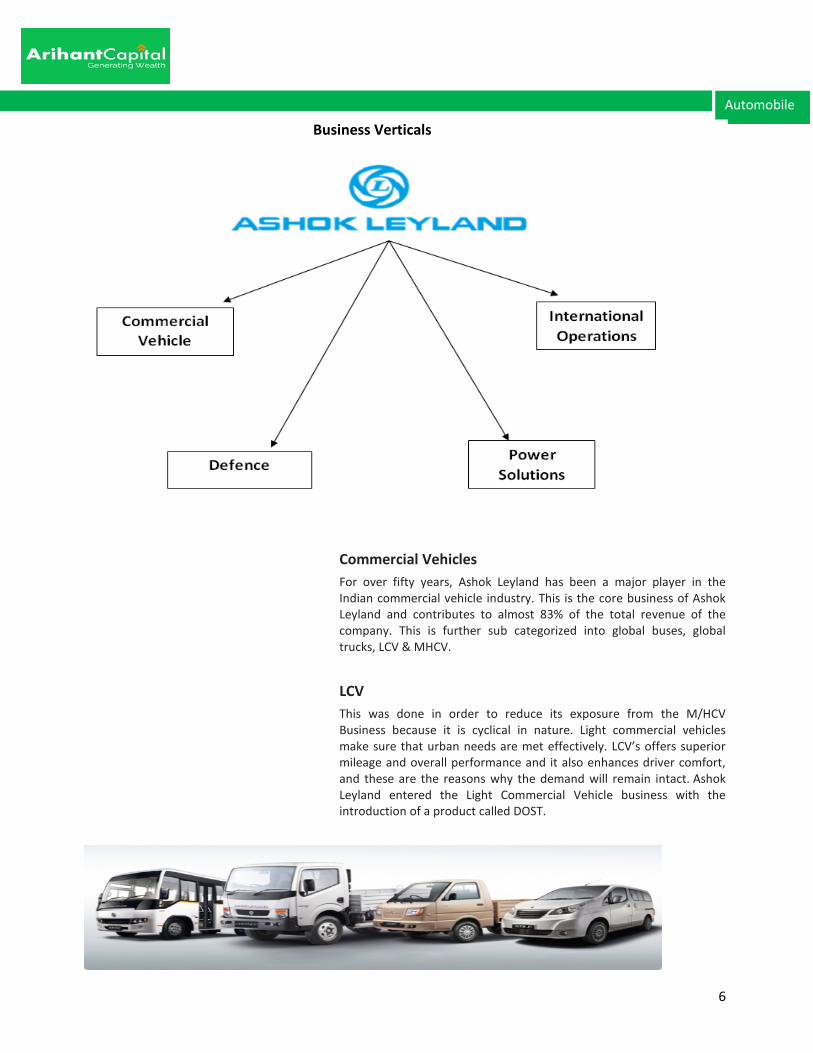

Business Verticals

Commercial Vehicles For over fifty years, Ashok Leyland has been a major player in the Indian commercial vehicle industry. This is the core business of Ashok Leyland and contributes to almost 83% of the total revenue of the company. This is further sub categorized into global buses, global trucks, LCV & MHCV.

LCV This was done in order to reduce its exposure from the M/HCV Business because it is cyclical in nature. Light commercial vehicles make sure that urban needs are met effectively. LCV’s offers superior mileage and overall performance and it also enhances driver comfort, and these are the reasons why the demand will remain intact. Ashok Leyland entered the Light Commercial Vehicle business with the introduction of a product called DOST.

7

Automobile

Some of the products offered by Ashok Leyland Light Vehicles include:

DOST A friend in the true sense, is an SCV with 1.25 ton payload, car-like comfort, low turning radius and superior mileage.

PARTNER The big brother of DOST is a next generation LCV truck with 4 ton payload capacity. Partner with its superior advanced ZD30 engine, excellent mileage and comfortable cabin design.

MiTR The new age LCV bus, is one of the most stylishly designed 27-seater with class leading comfort. It has the superior advanced ZD30 engine, quiet interiors, 15% higher mileage than competitor products and excellent safety features.

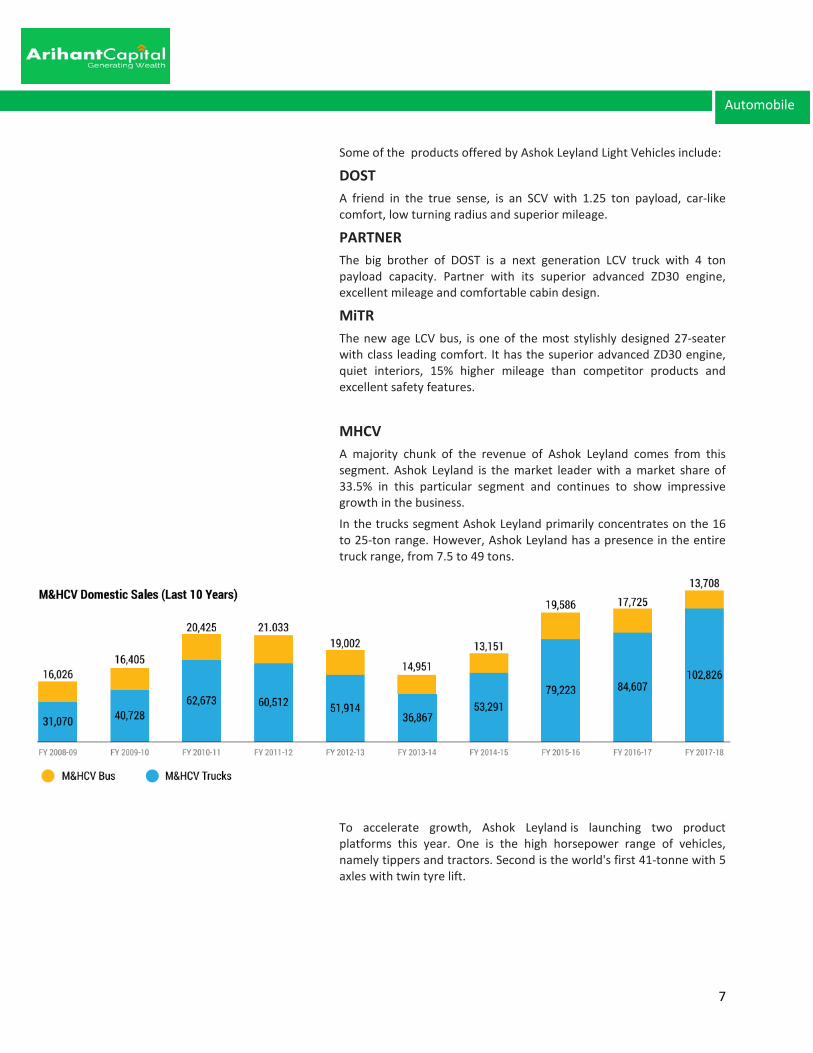

MHCV A majority chunk of the revenue of Ashok Leyland comes from this segment. Ashok Leyland is the market leader with a market share of 33.5% in this particular segment and continues to show impressive growth in the business.

In the trucks segment Ashok Leyland primarily concentrates on the 16 to 25-ton range. However, Ashok Leyland has a presence in the entire truck range, from 7.5 to 49 tons.

To accelerate growth, Ashok Leyland is launching two product platforms this year. One is the high horsepower range of vehicles, namely tippers and tractors. Second is the world's first 41-tonne with 5 axles with twin tyre lift.

8

Automobile

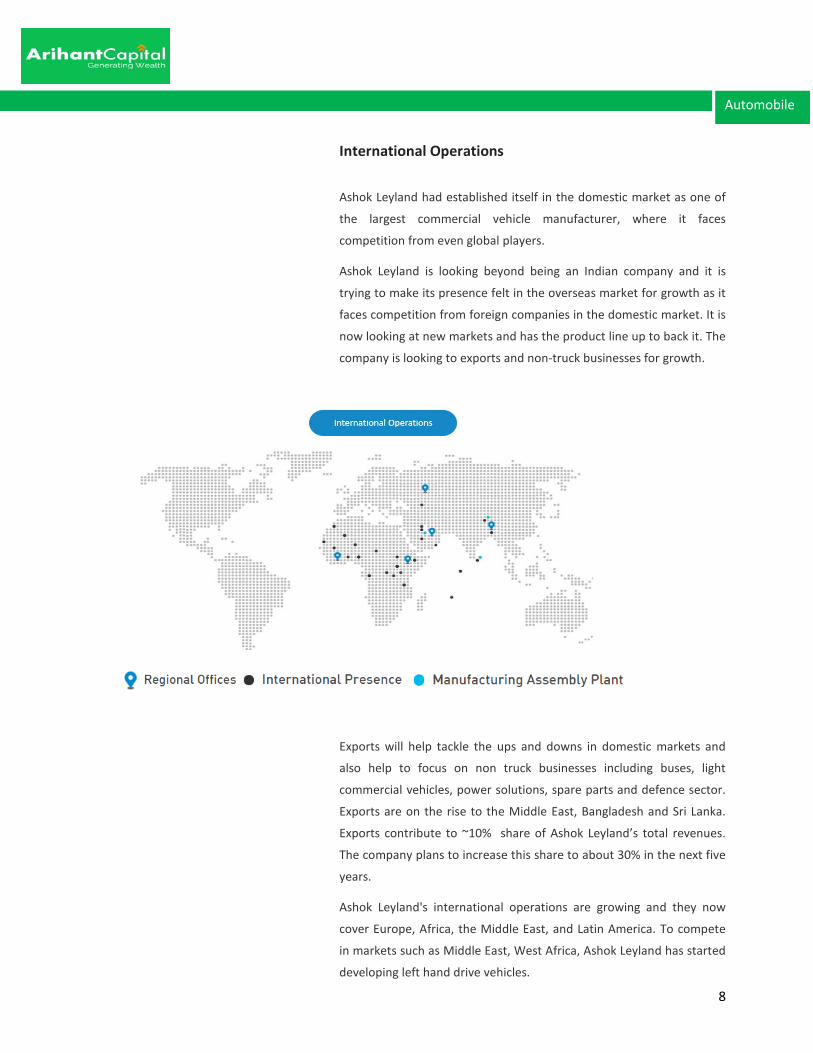

International Operations

Ashok Leyland had established itself in the domestic market as one of

the largest commercial vehicle manufacturer, where it faces

competition from even global players.

Ashok Leyland is looking beyond being an Indian company and it is

trying to make its presence felt in the overseas market for growth as it

faces competition from foreign companies in the domestic market. It is

now looking at new markets and has the product line up to back it. The

company is looking to exports and non-truck businesses for growth.

Exports will help tackle the ups and downs in domestic markets and

also help to focus on non truck businesses including buses, light

commercial vehicles, power solutions, spare parts and defence sector.

Exports are on the rise to the Middle East, Bangladesh and Sri Lanka.

Exports contribute to ~10% share of Ashok Leyland’s total revenues.

The company plans to increase this share to about 30% in the next five

years.

Ashok Leyland's international operations are growing and they now

cover Europe, Africa, the Middle East, and Latin America. To compete

in markets such as Middle East, West Africa, Ashok Leyland has started

developing left hand drive vehicles.

9

Automobile

Defence

Ashok Leyland has been involved in the design, development and manufacture of vehicles for the Indian armed forces. Ashok Leyland’s defence vehicles are serving armed forces in ground support roles from troop carriers to special application logistical and tactical vehicles. Its diesel engines have been used to power vehicles, boats, cranes, ground starter aggregates, compressors and generators.

Ashok Leyland products for the army are logistical vehicles with military payloads, some of which include the following : Protected Vehicles, General Services Role, Light Recovery Vehicles, High Mobility Vehicles, Fire Fighting Trucks, Field Artillery etc.

In the year 2015, company was able to participate only in 1-2% of the total Army’s capital outlay, which is increased to 5% now. The company is gearing up to develop solutions to cater around 20% of the Army’s expenditure. Initially Ashok Leyland was catering only to logistics space, now it caters to various applications including missile launchers and rocket launchers. Defence contribute to about 4% share of Ashok Leyland’s total revenues.

Power Solutions

This business contributed to a revenue of ~450Cr in Fy-18. Such

businesses help in reduction of the total risk because it helps in

diversifying the business.

The products on offer are certified diesel engines for various industrial

applications, which includes earthmoving equipment, compressor,

cranes, harvester combines, road construction machinery.

10

Automobile

SWOT Analysis of Ashok Leyland Ashok Leyland is known for manufacturing, marketing and distribution of commercial vehicles. It is one of the top most commercial vehicles supplier in India and has products, which are trusted by most companies who use trucks and heavy vehicles. Ashok Leyland is engaged in manufacturing and marketing commercial vehicles.

Strengths Leader in Domestic market Ashok Leyland has a strong market share (32%) in medium and heavy commercial vehicles. It is one of the largest manufacturer of commercial vehicles in India and one of the largest manufacturers of buses in the world. This strong market position in multiple domains gives the company access to a wider customer base and a strong brand name. Strong Product Mix Ashok Leyland has its presence in different segments of heavy, medium and light vehicles, which include buses, trucks, defence vehicles etc. The company also offers diesel engines for various purposes like marine, industrial and generator related applications. This strong product portfolio helps in the expansion of its customer base. Ashok Leyland offers a variety of products that serve diverse set of customers and help in fulfilling their requirements. Most of the products are as per current market needs and ensure safety to the customers. Ashok Leyland also takes care of fuel efficiency because of the kind of technology available to them.

Strong Manufacturing capabilities The manufacturing capabilities of the company is spread all over India and it has also started witnessing international presence. Strong manufacturing capabilities helps the company to maintain economies of scale

11

Automobile

Distribution Network Ashok Leyland has a strong distribution network with ~3000 customer outlets. These are divided into the following categories: 1) 1s ->Only sales. 2) 2s-> Sales +Services 3) 3s ->Sales +Service +Scrap This gives the company presence through the country and a dominant market share. For the LCV business, the company has adopted the hub-and-spoke model, which is also showing signs of success. Weakness Higher dependency on the domestic market In the last 5 years, Ashok Leyland generated about 86.3% of its revenue from the domestic market. This makes it vulnerable to any economic and political changes in the country. This gives an advantage to its competitors like Tata Motors, which has a wider base geographically. End of Joint Venture Nissan Motors terminated 3 Joint Ventures with Ashok Leyland in the year 2016.They were in a business relationship of more than 8 years. The matter is currently in the court of law. If such instances happen, it can affect the brand name of the company and have an impact on the financial condition. Opportunities: Exports An attempt of diversification is made by Ashok leyland, as it has started exports of its products & much better return is expected of this market in the Long Run. Exports contribute to about 8% of the companies total revenue. BS-VI Norms In the year of 2020, a lot of pre-buying is expected to happen with the advent of BS VI norms. This would be a great opportunity for the company to tap this additional demand. The primary reason for the same is that the vehicles will become expensive after the new norms take shape. Threats: Competiton This industry faces cut–throat competition by players like Eicher Motors, Tata Motors, Mahindra&Mahindra etc. In addition to this, government has allowed 100% foreign equity ownership in vehicle manufacturing sector.

12

Automobile

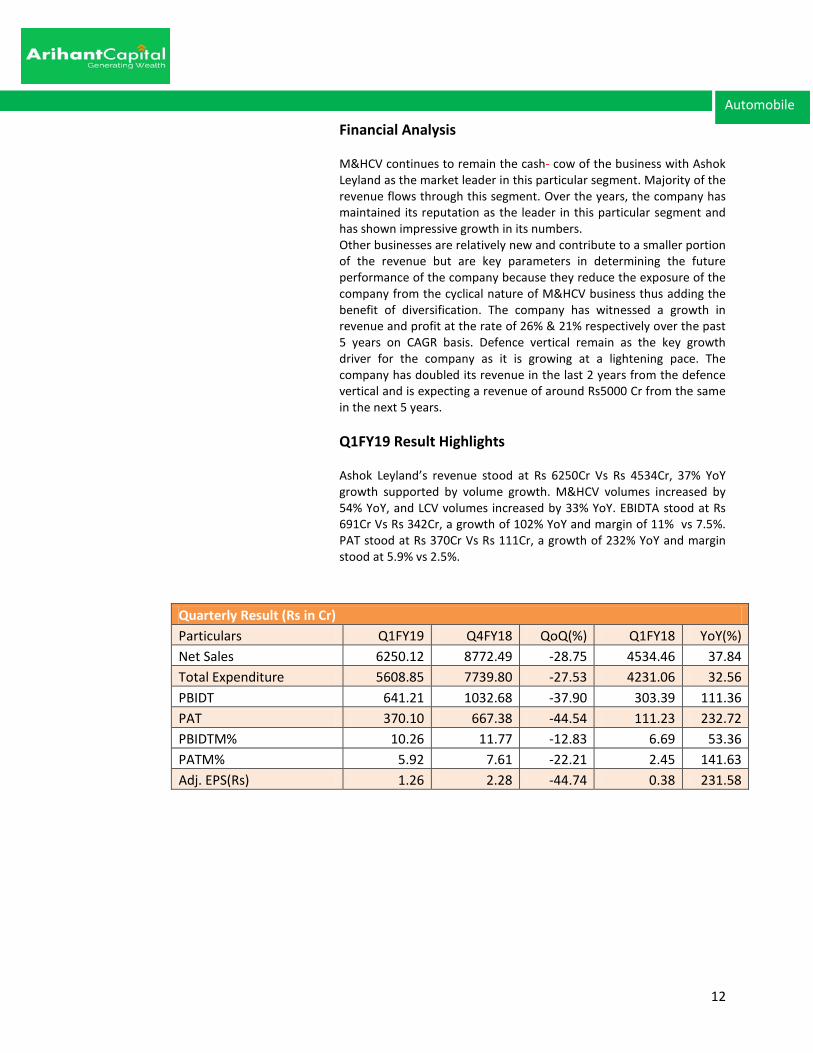

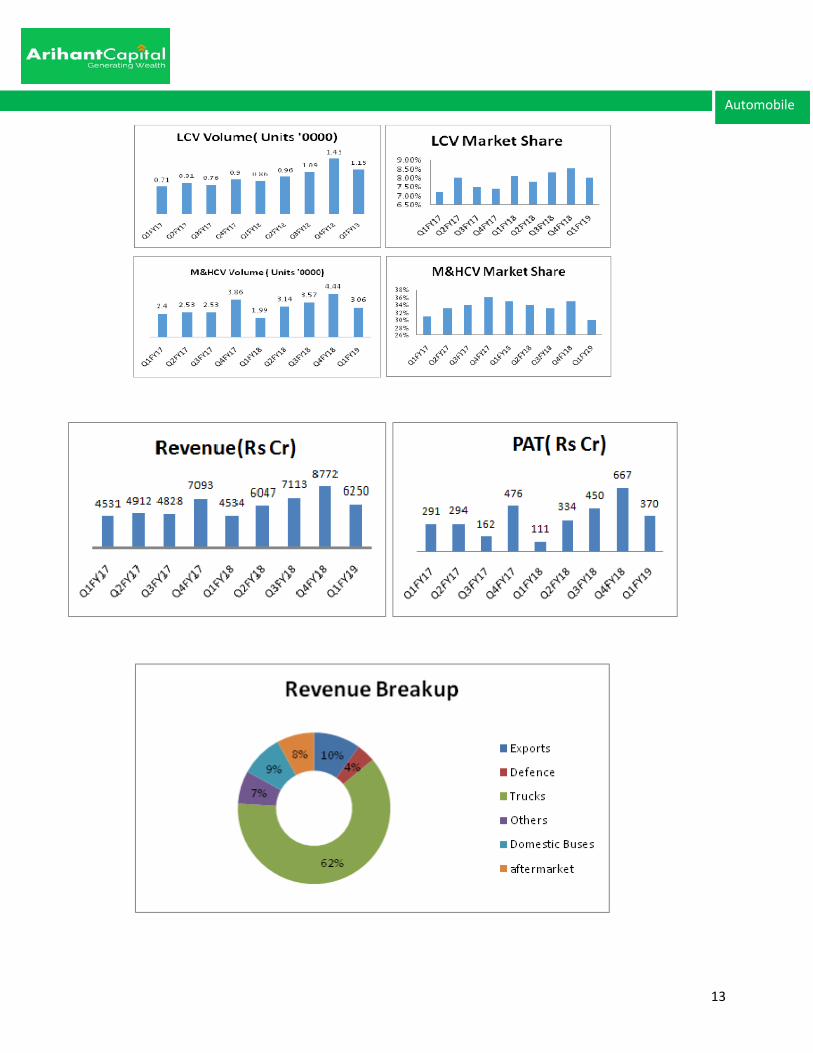

Financial Analysis M&HCV continues to remain the cash- cow of the business with Ashok Leyland as the market leader in this particular segment. Majority of the revenue flows through this segment. Over the years, the company has maintained its reputation as the leader in this particular segment and has shown impressive growth in its numbers. Other businesses are relatively new and contribute to a smaller portion of the revenue but are key parameters in determining the future performance of the company because they reduce the exposure of the company from the cyclical nature of M&HCV business thus adding the benefit of diversification. The company has witnessed a growth in revenue and profit at the rate of 26% & 21% respectively over the past 5 years on CAGR basis. Defence vertical remain as the key growth driver for the company as it is growing at a lightening pace. The company has doubled its revenue in the last 2 years from the defence vertical and is expecting a revenue of around Rs5000 Cr from the same in the next 5 years.

Q1FY19 Result Highlights Ashok Leyland’s revenue stood at Rs 6250Cr Vs Rs 4534Cr, 37% YoY growth supported by volume growth. M&HCV volumes increased by 54% YoY, and LCV volumes increased by 33% YoY. EBIDTA stood at Rs 691Cr Vs Rs 342Cr, a growth of 102% YoY and margin of 11% vs 7.5%. PAT stood at Rs 370Cr Vs Rs 111Cr, a growth of 232% YoY and margin stood at 5.9% vs 2.5%.

Quarterly Result (Rs in Cr) Particulars Q1FY19 Q4FY18 QoQ(%) Q1FY18 YoY(%) Net Sales 6250.12 8772.49 -28.75 4534.46 37.84 Total Expenditure 5608.85 7739.80 -27.53 4231.06 32.56 PBIDT 641.21 1032.68 -37.90 303.39 111.36 PAT 370.10 667.38 -44.54 111.23 232.72 PBIDTM% 10.26 11.77 -12.83 6.69 53.36 PATM% 5.92 7.61 -22.21 2.45 141.63 Adj. EPS(Rs) 1.26 2.28 -44.74 0.38 231.58

13

Automobile

14

Automobile

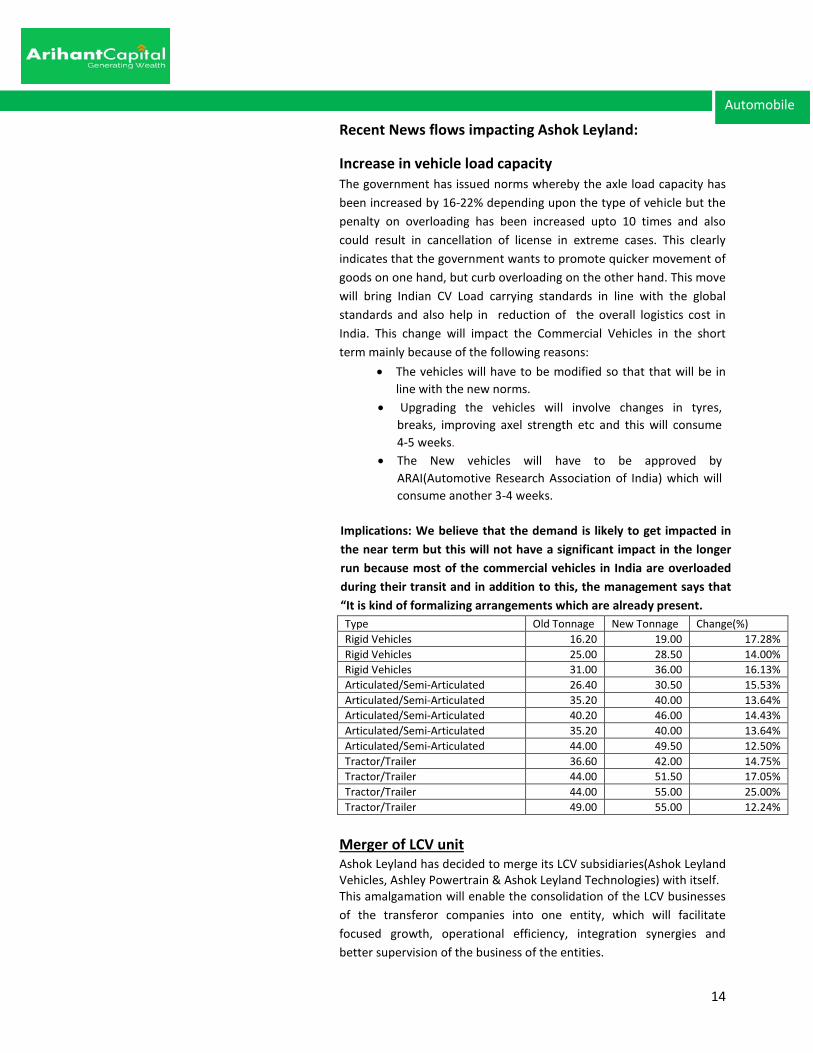

Recent News flows impacting Ashok Leyland:

Increase in vehicle load capacity The government has issued norms whereby the axle load capacity has been increased by 16-22% depending upon the type of vehicle but the penalty on overloading has been increased upto 10 times and also could result in cancellation of license in extreme cases. This clearly indicates that the government wants to promote quicker movement of goods on one hand, but curb overloading on the other hand. This move will bring Indian CV Load carrying standards in line with the global standards and also help in reduction of the overall logistics cost in India. This change will impact the Commercial Vehicles in the short term mainly because of the following reasons:

• The vehicles will have to be modified so that that will be in line with the new norms.

Merger of LCV unit

Ashok Leyland has decided to merge its LCV subsidiaries(Ashok Leyland Vehicles, Ashley Powertrain & Ashok Leyland Technologies) with itself. This amalgamation will enable the consolidation of the LCV businesses of the transferor companies into one entity, which will facilitate focused growth, operational efficiency, integration synergies and better supervision of the business of the entities.

• Upgrading the vehicles will involve changes in tyres, breaks, improving axel strength etc and this will consume 4-5 weeks.

• The New vehicles will have to be approved by ARAI(Automotive Research Association of India) which will consume another 3-4 weeks.

Implications: We believe that the demand is likely to get impacted in the near term but this will not have a significant impact in the longer run because most of the commercial vehicles in India are overloaded during their transit and in addition to this, the management says that “It is kind of formalizing arrangements which are already present. Type Old Tonnage New Tonnage Change(%) Rigid Vehicles 16.20 19.00 17.28% Rigid Vehicles 25.00 28.50 14.00% Rigid Vehicles 31.00 36.00 16.13% Articulated/Semi-Articulated 26.40 30.50 15.53% Articulated/Semi-Articulated 35.20 40.00 13.64% Articulated/Semi-Articulated 40.20 46.00 14.43% Articulated/Semi-Articulated 35.20 40.00 13.64% Articulated/Semi-Articulated 44.00 49.50 12.50% Tractor/Trailer 36.60 42.00 14.75% Tractor/Trailer 44.00 51.50 17.05% Tractor/Trailer 44.00 55.00 25.00% Tractor/Trailer 49.00 55.00 12.24%

15

Automobile

Digital Initiatives Innovative new products was the key focus at the global conference. Ashok Leyland displayed multiple domestic and international products at this show. This conference witnessed more than 50 innovative products and solution, some of which include the following : IAlert , Service Mandi ,E-Diagnostics and Leykart etc.

Electric vehicles Hinduja group announced the following partnership: Ashok Leyland and SUN Mobility, in July 2017, this took new heights at the Auto Expo 2018. This partnership was aimed at creating smart mobility solutions for upcoming Smart cities. Ashok Leyland unveiled electric vehicles like electric bus – Circuit-S – powered by SUN Mobility’s Smart Battery. The two companies have come together, to develop a world-class solution for smart mobility . This could also prove to be a very good solution not only for India but also for the entire globe for the need to improve and innovate in the sector of public transportation. This is a very good example of ‘Make in India’ initiative. Implications: The above news clearly show that management is keeping a close eye on what possibly could impact the industry in the future or what could possibly be a key growth driver for the company in the coming years.

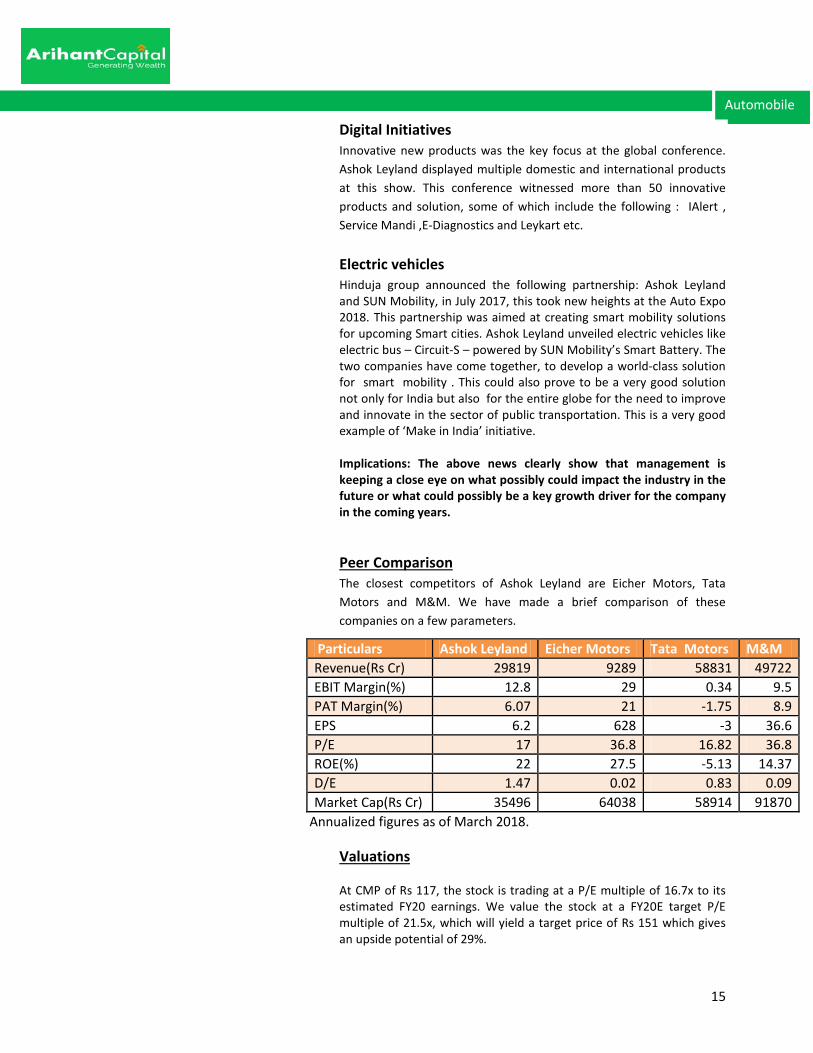

Peer Comparison The closest competitors of Ashok Leyland are Eicher Motors, Tata Motors and M&M. We have made a brief comparison of these companies on a few parameters.

Particulars Ashok Leyland Eicher Motors Tata Motors M&M Revenue(Rs Cr) 29819 9289 58831 49722 EBIT Margin(%) 12.8 29 0.34 9.5 PAT Margin(%) 6.07 21 -1.75 8.9 EPS 6.2 628 -3 36.6 P/E 17 36.8 16.82 36.8 ROE(%) 22 27.5 -5.13 14.37 D/E 1.47 0.02 0.83 0.09 Market Cap(Rs Cr) 35496 64038 58914 91870

Annualized figures as of March 2018.

Valuations

At CMP of Rs 117, the stock is trading at a P/E multiple of 16.7x to its estimated FY20 earnings. We value the stock at a FY20E target P/E multiple of 21.5x, which will yield a target price of Rs 151 which gives an upside potential of 29%.

16

Automobile

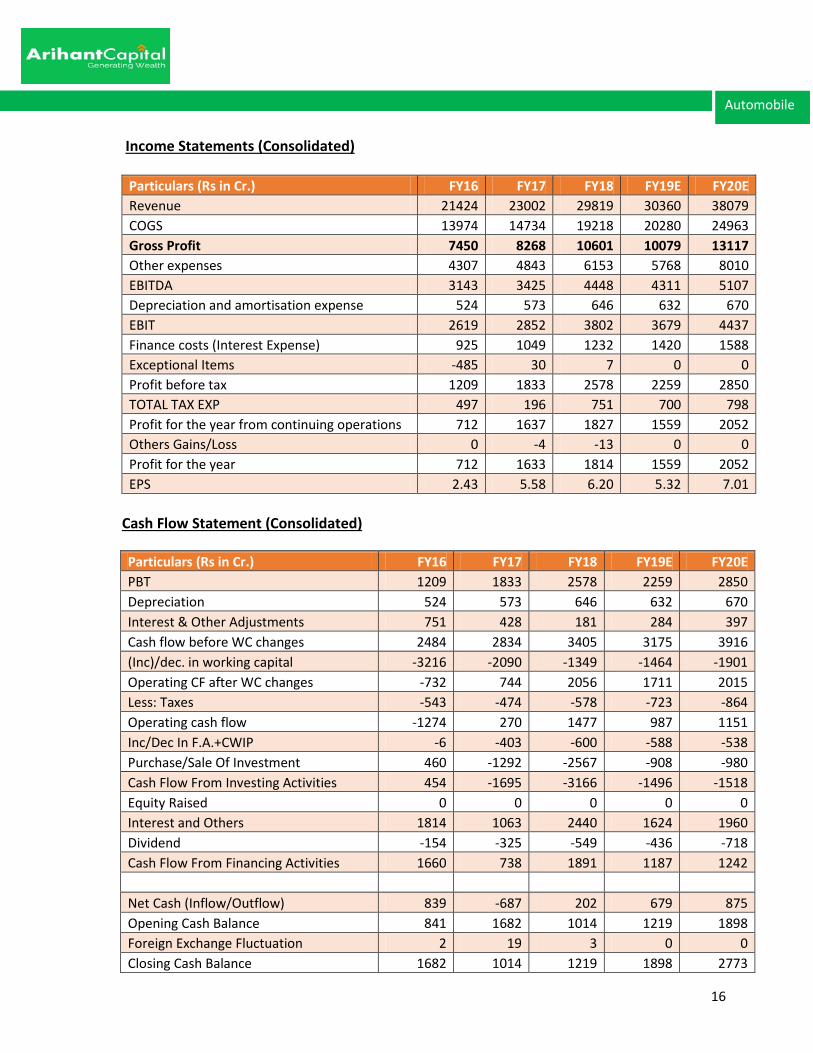

Income Statements (Consolidated)

Particulars (Rs in Cr.) FY16 FY17 FY18 FY19E FY20E Revenue 21424 23002 29819 30360 38079 COGS 13974 14734 19218 20280 24963 Gross Profit 7450 8268 10601 10079 13117 Other expenses 4307 4843 6153 5768 8010 EBITDA 3143 3425 4448 4311 5107 Depreciation and amortisation expense 524 573 646 632 670 EBIT 2619 2852 3802 3679 4437 Finance costs (Interest Expense) 925 1049 1232 1420 1588 Exceptional Items -485 30 7 0 0 Profit before tax 1209 1833 2578 2259 2850 TOTAL TAX EXP 497 196 751 700 798 Profit for the year from continuing operations 712 1637 1827 1559 2052 Others Gains/Loss 0 -4 -13 0 0 Profit for the year 712 1633 1814 1559 2052 EPS 2.43 5.58 6.20 5.32 7.01

Cash Flow Statement (Consolidated)

Particulars (Rs in Cr.) FY16 FY17 FY18 FY19E FY20E PBT 1209 1833 2578 2259 2850 Depreciation 524 573 646 632 670 Interest & Other Adjustments 751 428 181 284 397 Cash flow before WC changes 2484 2834 3405 3175 3916 (Inc)/dec. in working capital -3216 -2090 -1349 -1464 -1901 Operating CF after WC changes -732 744 2056 1711 2015 Less: Taxes -543 -474 -578 -723 -864 Operating cash flow -1274 270 1477 987 1151 Inc/Dec In F.A.+CWIP -6 -403 -600 -588 -538 Purchase/Sale Of Investment 460 -1292 -2567 -908 -980 Cash Flow From Investing Activities 454 -1695 -3166 -1496 -1518 Equity Raised 0 0 0 0 0 Interest and Others 1814 1063 2440 1624 1960 Dividend -154 -325 -549 -436 -718 Cash Flow From Financing Activities 1660 738 1891 1187 1242 Net Cash (Inflow/Outflow) 839 -687 202 679 875 Opening Cash Balance 841 1682 1014 1219 1898 Foreign Exchange Fluctuation 2 19 3 0 0 Closing Cash Balance 1682 1014 1219 1898 2773

17

Automobile

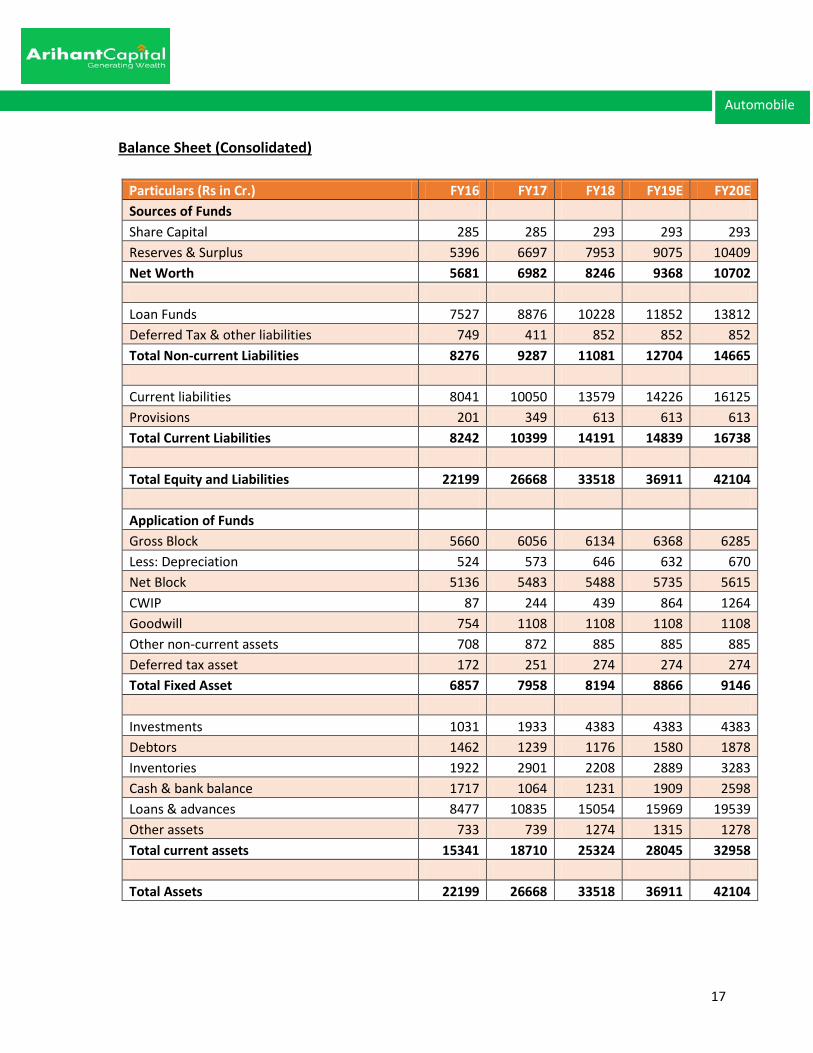

Balance Sheet (Consolidated)

Particulars (Rs in Cr.) FY16 FY17 FY18 FY19E FY20E Sources of Funds Share Capital 285 285 293 293 293 Reserves & Surplus 5396 6697 7953 9075 10409 Net Worth 5681 6982 8246 9368 10702 Loan Funds 7527 8876 10228 11852 13812 Deferred Tax & other liabilities 749 411 852 852 852 Total Non-current Liabilities 8276 9287 11081 12704 14665 Current liabilities 8041 10050 13579 14226 16125 Provisions 201 349 613 613 613 Total Current Liabilities 8242 10399 14191 14839 16738 Total Equity and Liabilities 22199 26668 33518 36911 42104 Application of Funds Gross Block 5660 6056 6134 6368 6285 Less: Depreciation 524 573 646 632 670 Net Block 5136 5483 5488 5735 5615 CWIP 87 244 439 864 1264 Goodwill 754 1108 1108 1108 1108 Other non-current assets 708 872 885 885 885 Deferred tax asset 172 251 274 274 274 Total Fixed Asset 6857 7958 8194 8866 9146 Investments 1031 1933 4383 4383 4383 Debtors 1462 1239 1176 1580 1878 Inventories 1922 2901 2208 2889 3283 Cash & bank balance 1717 1064 1231 1909 2598 Loans & advances 8477 10835 15054 15969 19539 Other assets 733 739 1274 1315 1278 Total current assets 15341 18710 25324 28045 32958 Total Assets 22199 26668 33518 36911 42104

18

Automobile

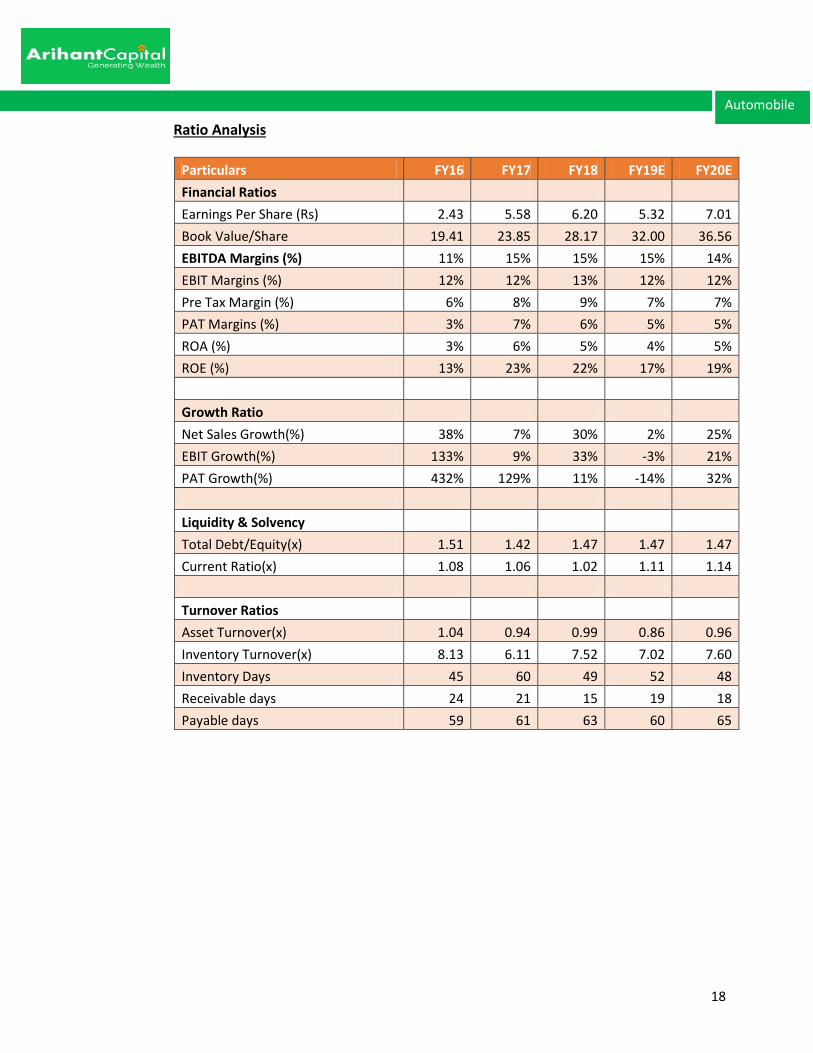

Ratio Analysis

Particulars FY16 FY17 FY18 FY19E FY20E Financial Ratios

Earnings Per Share (Rs) 2.43 5.58 6.20 5.32 7.01

Book Value/Share 19.41 23.85 28.17 32.00 36.56

EBITDA Margins (%) 11% 15% 15% 15% 14%

EBIT Margins (%) 12% 12% 13% 12% 12%

Pre Tax Margin (%) 6% 8% 9% 7% 7%

PAT Margins (%) 3% 7% 6% 5% 5%

ROA (%) 3% 6% 5% 4% 5%

ROE (%) 13% 23% 22% 17% 19%

Growth Ratio

Net Sales Growth(%) 38% 7% 30% 2% 25%

EBIT Growth(%) 133% 9% 33% -3% 21%

PAT Growth(%) 432% 129% 11% -14% 32%

Liquidity & Solvency

Total Debt/Equity(x) 1.51 1.42 1.47 1.47 1.47

Current Ratio(x) 1.08 1.06 1.02 1.11 1.14

Turnover Ratios

Asset Turnover(x) 1.04 0.94 0.99 0.86 0.96

Inventory Turnover(x) 8.13 6.11 7.52 7.02 7.60

Inventory Days 45 60 49 52 48

Receivable days 24 21 15 19 18

Payable days 59 61 63 60 65

19

Automobile

Arihant Research Desk

E. [email protected] T. 022-42254800

Head Office Registered Office

#1011, Solitaire Corporate park, Building No. 10, 1st Floor, Andheri Ghatkopar Link Road, Chakala, Andheri (E). Mumbai - 400093 Tel: (91-22) 42254800 Fax: (91-22) 42254880

E-5 Ratlam Kothi Indore - 452003, (M.P.) Tel: (91-731) 3016100 Fax: (91-731) 3016199

Stock Rating Scale Absolute Return

Buy > 20% Accumulate 12% to 20% Hold Neutral

5% to 12% -5% to 5%

Reduce <-5%

Research Analyst Registration No. Contact Website Email Id

INH000002764 SMS: ‘Arihant’ to 56677 www.arihantcapital.com [email protected]

Arihant Capital Markets Ltd.

1011, Solitaire Corporate park, Building No. 10, 1st Floor, Andheri Ghatkopar Link Road Chakala, Andheri (E) Tel. 022-42254800 Fax. 0224225488

www.arihantcapital.com

Disclaimer:This document has been prepared by Arihant Capital Markets Ltd. This document does not constitute an offer or solicitation for the purchase and sale of any financial instrument by Arihant. This document has been prepared and issued on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst meticulous care has been taken to ensure that the facts stated are accurate and opinions given are fair and reasonable, neither the analyst nor any employee of our company is in any way is responsible for its contents and nor is its accuracy or completeness guaranteed. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Arihant may trade in investments, which are the subject of this document or in related investments and may have acted upon or used the information contained in this document or the research or the analysis on which it is based, before its publication. This is just a suggestion and Arihant will not be responsible for any profit or loss arising out of the decision taken by the reader of this document. Affiliates of Arihant may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. No matter contained in this document may be reproduced or copied without the consent of the firm.