Embed Size (px)

Citation preview

Initial Public Offering Allocations

by Sturla Lyngnes Fjesme

A dissertation submitted to BI Norwegian Business School for the degree of PhD

PhD specialization: Financial Economics

Series of Dissertations 9/2011

BI Norwegian Business School

Sturla Lyngnes Fjesme Initial Public Offering Allocations © Sturla Lyngnes Fjesme 2011 Series of Dissertations 9/2011 ISBN: 978-82-8247-029-2 ISSN: 1502-2099 BI Norwegian Business School N-0442 Oslo Phone: +47 4641 0000 www.bi.no Printing: Nordberg Trykk The dissertation may be downloaded or ordered from our website www.bi.no/en/Research/Research-Publications/

Abstract Stock exchanges have rules on the minimum equity level and the minimum number of shareholders that are required to list publicly. Most private companies that want to list publicly must issue equity to be able to meet these minimum requirements. Most companies that list on the Oslo stock exchange (OSE) are restricted to selling shares in an IPO to a large group of dispersed investors or in a negotiated private placement to a small group of specialized investors. Initial equity offerings have high expected returns and this makes them very popular investments. Ritter (2003) and Jenkinson and Jones (2004) argue that there are three views on how shares are allocated in the IPO setting. First, is the academic view based on Benveniste and Spindt (1989). In this view investment banks allocate IPO shares to informed investors in return for true valuation and demand information. Informed investors are allocated shares because they help to price the issue. Second, is the pitchbook view where investment banks allocate shares to institutional investors that are likely to hold shares in the long run. It is argued, by investment banks, that buy-and-hold investors will create price stability that is good for the issuing companies. Finally, is the rent seeking view, or profit sharing view, where investment banks allocate shares to investors in return for kickbacks. There are four types of IPO rent seeking that have been investigated by U.S. regulators (the SEC and the NASD), see Liu and Ritter (2010). IPO allocations can be tied to future corporate business for the banks (IPO spinning), after-listing purchases of the IPO shares (IPO laddering) and stock-trading commissions. Investment banks and companies can also agree on high underpricing in return for after-listing company share coverage from a star analysts provided by the bank (analyst conflict of interest). Underpriced shares are then allocated to bank clients that generate high stock-trading commission for the investment bank. In the paper 'Laddering in Initial Public Offering Allocations' it is investigated if IPO allocations are tied to after-listing purchases of the IPO shares (IPO laddering). In the paper 'Using Stock-trading Commissions to Secure IPO Allocations' it is investigated if IPO allocations are tied to investor stock-trading commission. Private companies that want to list publicly can, as an alternative to the IPO allocation, issue shares in a negotiated private placement to a small group of specialized investors. Most theoretical papers on equity offerings, however, show that IPOs will almost always be preferred to the negotiated private placement by the seller, see Bulow and Klemperer (1996), Bulow and Klemperer (2009) and French and McCormick (1984). Why some companies use private placements has therefore been the focus of many empirical studies in finance, see Wruck (1989), Hertzel and Smith (1993), Barclay et al. (2007), Anshuman et al. (2010) and Cronqvist and Nilsson (2005). The research question addressed in the paper 'Initial Public Offering or Initial Private Placement?' is whether private placements are used, instead of IPOs, to transfer private benefits of control from sellers to buyers. A common contribution of all papers is that we introduce new and unique data on private company share ownership. This data allow us to investigate share allocations questions it has previously been difficult to investigate.

Acknowledgements I am deeply indebted to Professor Øyvind Norli, my supervisor, for all the continued support, guidance and encouragement throughout my time as a PhD student. I would also like to thank Professor Roni Michaely for help and guidance, and for making my stay at Cornell University such a great experience. I am very grateful to François Derrien and Øyvind Bøhren, who gave me many helpful and detailed suggestions on my pre-doctoral defense and who helped me with the job market process. I am grateful to Bruno Gerard for supervising my master degree thesis and for helping me with the job market process and my PhD thesis. I would also like to thank Karin Thorburn, Diane Denis, William Megginson, Paul Ehling, Christopher Vincent, David De Angelis, Alyssa Anderson, Maury Saslaff, Yelena Larkin, Gideon Saar, Jay Ritter, Dag Michalsen and Richard Priestley for support and for commenting on the thesis. I would like to thank my fellow PhD students, Limei Che, Christian Heyerdahl-Larsen, Morten Josefsen, Siv Staubo, Siri Valseth, Nam Huong Dau, Ignacio Garcia de Olalla Lopez, Junhua Zhong, and my friends, Per Helmer Thorkildsen, Henrik Hasner, Kjell Olav Dalen, Jan Kenneth Evanger, Dag Djurovic, Martin Jensen, Per-Eilert Vierli and Øystein Larsen, for support and many interesting economic discussions. Finally, I would like to thank my family, Sølvi Lyngnes, Torbjørn Fjesme, Arvid Lyngnes Fjesme, Sunniva Victoria Fjesme and Hanna Kristiansen, for all the help and support during my time as a PhD student.

Contents

1 Introduction 31.1 Laddering in Initial Public Offering Allocations . . . . . . . . . . . . . . . 41.2 Using Stock-trading Commissions to Secure IPO Allocations . . . . . . . . 41.3 Initial Public Offering or Initial Private Placement? . . . . . . . . . . . . . 4

2 Laddering in Initial Public Offering Allocations 7

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.2 Related literature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112.3 Predictions and testable implications . . . . . . . . . . . . . . . . . . . . . 12

2.3.1 The IPO laddering hypothesis . . . . . . . . . . . . . . . . . . . . . 132.3.2 Other testable implications of IPO laddering . . . . . . . . . . . . . 14

2.4 The listing process and the incentives to engage in IPO laddering . . . . . 152.4.1 Why investment banks use IPO laddering . . . . . . . . . . . . . . . 152.4.2 Why laddering investors agree to buy more shares . . . . . . . . . . 162.4.3 Why IPO laddering is a problem . . . . . . . . . . . . . . . . . . . . 16

2.5 Data description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.5.1 The IPO sample . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182.5.2 The remaining IPOs . . . . . . . . . . . . . . . . . . . . . . . . . . 182.5.3 Aggregate laddering . . . . . . . . . . . . . . . . . . . . . . . . . . . 182.5.4 Variable explanations . . . . . . . . . . . . . . . . . . . . . . . . . . 19

2.6 Empirical results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.6.1 Optimal holdings . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242.6.2 The effect of IPO laddering . . . . . . . . . . . . . . . . . . . . . . 242.6.3 Robustness and aggregate IPO laddering . . . . . . . . . . . . . . . 24

2.7 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3 Using Stock-trading Commissions to Secure IPO Allocations 43

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 453.2 Related literature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 463.3 Theoretical predictions and testable implications . . . . . . . . . . . . . . . 47

3.3.1 The rent seeking view of IPO allocations . . . . . . . . . . . . . . . 483.3.2 The pitchbook view of IPO allocations . . . . . . . . . . . . . . . . . 493.3.3 The academic view of IPO allocations . . . . . . . . . . . . . . . . . 50

3.4 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 503.4.1 IPO allocations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 513.4.2 After-listing ownership . . . . . . . . . . . . . . . . . . . . . . . . . 513.4.3 Variable description . . . . . . . . . . . . . . . . . . . . . . . . . . 52

3.5 Empirical results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 533.5.1 The rent seeking view of IPO allocations . . . . . . . . . . . . . . . 543.5.2 The pitchbook view of IPO allocations . . . . . . . . . . . . . . . . . 553.5.3 The academic view of IPO allocations . . . . . . . . . . . . . . . . . 553.5.4 Robustness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

3.6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

1

4 Initial Public Offering or Initial Private Placement? 734.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 744.2 Literature review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 754.3 The road to the listing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

4.3.1 The formal listing process . . . . . . . . . . . . . . . . . . . . . . . 774.3.2 A public or a private offering? . . . . . . . . . . . . . . . . . . . . . 78

4.4 Theoretical predictions and testable implications . . . . . . . . . . . . . . . 794.4.1 The private benefits of control hypothesis . . . . . . . . . . . . . . . 804.4.2 Alternative explanations . . . . . . . . . . . . . . . . . . . . . . . . 814.4.3 Other control measures . . . . . . . . . . . . . . . . . . . . . . . . . 824.4.4 Private benefits of control also after the listing . . . . . . . . . . . . 83

4.5 Data and descriptive statistics . . . . . . . . . . . . . . . . . . . . . . . . . 834.5.1 Descriptive statistics . . . . . . . . . . . . . . . . . . . . . . . . . . 844.5.2 Variable description . . . . . . . . . . . . . . . . . . . . . . . . . . 84

4.6 Empirical Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 854.6.1 The private benefits of control hypothesis . . . . . . . . . . . . . . 854.6.2 Alternative explanations . . . . . . . . . . . . . . . . . . . . . . . . 864.6.3 Private benefits of control also after the listing . . . . . . . . . . . . 86

4.7 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

5 Summary 100

2

1 Introduction

This dissertation consists of three papers; ’Laddering in Initial Public Offering Alloca-tions’, ’Using Stock-trading Commissions to Secure IPO Allocations’and ’Initial PublicOffering or Initial Private Placement?’ The rest of this section is organized as follows. Ifirst discuss the common feature of the papers, namely the allocations of Initial PublicOffering (IPO) shares. I then briefly discuss the main results in each of the papers.Stock exchanges have rules on the minimum equity level and the minimum number

of shareholders that are required to list publicly. Most private companies that want tolist publicly must issue equity to be able to meet these minimum requirements. Mostcompanies, that list on the Oslo stock exchange (OSE), are restricted to selling sharesin an IPO to a large group of dispersed investors or in a negotiated private placementto a small group of specialized investors. Initial equity offerings have high expectedreturns and this makes them very popular investments. Ritter (2003) and Jenkinson andJones (2004) argue that there are three views on how shares are allocated in the IPOsetting. First, is the academic view based on Benveniste and Spindt (1989). In this viewinvestment banks allocate IPO shares to informed investors in return for true valuationand demand information. Informed investors are allocated shares because they help toprice the issue. Second, is the pitchbook view where investment banks allocate sharesto institutional investors that are likely to hold shares in the long run. It is argued, byinvestment banks, that buy-and-hold investors will create price stability that is good forthe issuing companies. Finally, is the rent seeking view, or profit sharing view, whereinvestment banks allocate shares to investors in return for kickbacks. There are fourtypes of IPO rent seeking that have been investigated by U.S. regulators (the SEC andthe NASD), see Liu and Ritter (2010). IPO allocations can be tied to future corporatebusiness for the banks (IPO spinning), after-listing purchases of the IPO shares (IPOladdering) and stock-trading commissions. Investment banks and companies can alsoagree on high underpricing in return for after-listing company share coverage from a staranalysts provided by the bank (analyst conflict of interest). Underpriced shares are thenallocated to bank clients that generate high stock-trading commission for the investmentbank. In the paper ’Laddering in Initial Public Offering Allocations’it is investigated ifIPO allocations are tied to after-listing purchases of the IPO shares (IPO laddering). Inthe paper ’Using Stock-trading Commissions to Secure IPO Allocations’it is investigatedif IPO allocations are tied to investor stock-trading commission.Private companies can, as an alternative to the IPO, issue shares in a negotiated

private placement to a small group of specialized investors. Most theoretical papers onequity offerings, however, show that IPOs will almost always be preferred to the negotiatedprivate placement by the seller, see Bulow and Klemperer (1996), Bulow and Klemperer(2009) and French and McCormick (1984). Why some companies use private placementshas therefore been the focus of many empirical studies in finance, see Wruck (1989),Hertzel and Smith (1993), Barclay et al. (2007), Anshuman et al. (2010) and Cronqvistand Nilsson (2005). The research question addressed in the paper ’Initial Public Offeringor Initial Private Placement?’ is whether private placements are used, instead of IPOs, totransfer private benefits of control from sellers to buyers. A common contribution of allpapers is that we introduce new and unique data on private company share ownership.This data allow us to investigate share allocations questions it has previously been diffi cultto investigate.

3

1.1 Laddering in Initial Public Offering Allocations

IPO laddering is the process where share allocations are tied to the after-listing purchasesof the company shares. IPO laddering has been known by regulators for a long time(the SEC sent out warnings to investment banks that laddering is illegal the first timein 1961), but there has been limited empirical research on IPO laddering. A potentialreason for this is that it is very diffi cult to investigate laddering because investment banksrarely distribute information about allocation practices. In this paper we use unique datafrom the Oslo Stock Exchange (OSE) that allow us to observe the after-listing tradingof investors that are allocated IPO shares. The data consists of 16,593 combinations ofinvestor IPO allocations, stock-trading commission and after-listing trading on the OSEin the period from 1993 to 2007. This data allow us to investigate laddering at theinvestor level. The main contribution of this paper is that we show a strong and robustrelationship between IPO allocations and the number of shares that are purchased afternew listings at the investor level. This relationship is stronger for investors that sell allshares again right after the listing, in underpriced IPOs and in IPOs with a positive driftin the share price after the listing. These are the investors and the IPOs that the existingresearch identifies as the most likely laddering investors. These findings are consistentwith the suspicion that IPO shares are allocated to investors that buy shares dictated bythe investment bank after the listing (laddering). This finding extends to Hao (2007) andGriffi n et al. (2007).

1.2 Using Stock-trading Commissions to Secure IPO Alloca-tions

Another concern for regulators is that IPO allocations are tied to excessively large stock-trading commissions and that such a practice is illegal kickbacks from investors to invest-ment banks. Using the same data as in ’Laddering in Initial Public Offering Allocations’,we are able to link stock-trading commission and IPO allocation at the investor level. Themain finding of the paper is a strong and robust positive relationship between the levelof stock-trading commission generated by an investor prior to the IPO and the numberof shares the same investor receives through the IPO allocation. This finding indicatesthat investors are able to buy IPO allocations by trading excessively to generate com-mission. The finding extends to Reuter (2006), Nimalendran, Ritter and Zhang (2006),Ritter (2003) and Jenkinson and Jones (2004) who all argue that investment banks arelikely to allocate IPO shares in return for stock-trading commission.

1.3 Initial Public Offering or Initial Private Placement?

Companies can, as an alternative to the IPO, sell shares in a negotiated private placement.Most theoretical research on equity offerings show that auctions, that are similar to IPOs,will in most cases be preferred by the seller of a company. In practice, however, there aremany companies that use negotiated private placements to raise equity. Several studieshave proposed explanations to this private placement choice. Some papers argue thatprivate placements are used to attract certain investors, to keep management in control,to reduce undervaluation or to reduce problems associated with information asymmetry(Wruck, 1989; Hertzel and Smith, 1993; Barclay et al.,2007; Anshuman et al., 2010;

4

Cronqvist and Nilsson, 2005). Other papers suggests that private placements are usedwhen buyers value private benefits of control over the stand alone cash flow value of thecompany (Zingales, 1994; Zingales, 1995; Zwiebel, 1995 and Damodaran, 2005). Themain contribution of our paper is that we show a strong and robust relationship betweenprivate benefits of control, before the initial offering, and the use of private placements.This indicates that private placements are used to transfer private benefits of control fromsellers to buyers. This finding supports Zingales (1995) in that private placements areused to transfer company control rights.

5

.

6

2 Laddering in Initial Public Offering Allocations

Sturla Lyngnes Fjesme1

BI Norwegian Business School

.

.

.

.

.

.

.

.

JEL classification: G3; G24Keywords: IPO allocations; Laddering; Tie-in agreements; Rent seeking; Equity offer-

ings

1I am very grateful to Øyvind Norli (supervisor), François Derrien, Roni Michaely, Øyvind Bøhren,Bruno Gerard, Karin Thorburn (discussant), Diane Denis (discussant), William Megginson (discussant),Paul Ehling, Christopher Vincent, David De Angelis, Alyssa Anderson, Maury Saslaff, Yelena Larkin,Gideon Saar, and seminar participants at Cornell University, BI Norwegian Business School, the NordicFinance Network (NFN) workshop in Lund 2010, the Financial Management Association (FMA) Doc-toral Student Consortium in Hamburg 2010, Stockholm University, the University of Gothenburg, theUniversity of Warwick and the University of Melbourne for valuable suggestions. I thank the Oslo StockExchange VPS for providing the data, the Financial Supervisory Authority of Norway (Finanstilsynet)and the companies and investment banks that helped locate the listing prospectuses. Part of the articlewas written while I was a visiting PhD student at the S.C. Johnson Graduate School of Managementat Cornell University. I also thank the American-Scandinavian-Association and the Norwegian CentralBank for financial support. All errors are my own.Correspondence: BI Norwegian Business School, Nydalsveien 37, 0484 Oslo, Norway, Email address:

[email protected], Telephone (USA): +1-607-793-6911, Telephone (Norway): +47-957-722-43.

7

Abstract

Tying Initial Public Offering (IPO) allocations of common stock to after-listing purchases in the IPO shares, a process referred to as IPO laddering,has resulted in large-scale investigations of the major investment banks by theSEC and the National Association of Securities Dealers (NASD). This processis claimed to drive after-listing share prices above their fundamental values,and is illegal under the laws against market manipulation and fraud. As aresult, investment banks are reluctant to distribute information about theirallocation practices, so investigating the alleged laddering and its implicationshas proven to be diffi cult. With a new and unique data set of 16,593 IPOallocations on the Oslo Stock Exchange (OSE), we confirm the SEC’s suspicionthat IPO allocations are dependent on after-listing trading. Allocations toafter-listing purchasing investors has been combined with allocations to highstock-trading commissions generating investors that can take advantage of theIPO laddering, thereby allowing investment banks to recapture some of themoney left on the table in IPOs. Allocated IPO investors buy more shares afternew listings because they are rewarded for doing so with more IPO allocations.

8

2.1 Introduction

On December 6, 2000 the Wall Street Journal (WSJ) reported that the SEC and theNASD were investigating some of the major investment banks for tying IPO allocationsto after-listing purchases. An investment banker interviewed for the article admits thatIPO allocations to investors with after-listing interest could occur, but explains thatafter-listing interest is a signal that the investor is of the buy-and-hold type. Since banksstrive to allocate shares to buy-and-hold investors to create price stability, after-listingpurchases are related to IPO allocations. An investor confirms that expressing an interestin after-listing purchases is one way of obtaining more IPO allocations.Three U.S. investment banks have been sued by the SEC over allegations of IPO

laddering after the WSJ article, though all three later settled (without admitting guilt).2

The allegations made by the SEC are that the banks promised investors that they wouldreceive an increased allocation in current hot IPOs if they bought additional shares afterthe listing of the same IPOs.3 The banks, allegedly asked IPO applicants if they wouldbe interested in buying more shares after the listings and at what price and quantity.Since IPO laddering is illegal, there are no formal records of tying IPO allocations toafter-listing trading, as agreements are likely to be made over the phone or in personrather than in a written agreement.4 It is, however, possible to see if there is a positiveand consistent relationship between IPO allocations and after-listing trading by investors.Such a relationship would strongly indicate that IPO allocations are tied to after-listingbuy trades, although this data is very hard to obtain in the U.S. (even for the SEC andNASD). Using data from the Oslo Stock Exchange (OSE), we are able to observe theafter-listing trading of investors that were allocated shares in IPOs. The data consistsof 16,593 IPO allocations with stock-trading commissions and after-listing trading on theOSE in the period from 1993 to 2007. Stock ownership by investor ID is observed for allcompanies throughout the listing process, and is used to calculate actual IPO allocations.It is, from this data that the relationship between IPO allocations, after-listing purchases,commissions and future IPO allocations is investigated.The main contribution of this paper is that we show a strong and robust relationship

between the number of shares that are purchased after new listings and IPO allocationsby laddering investors. This is consistent with the SEC’s suspicion that IPO sharesare allocated to investors that buy shares dictated by the investment bank. We defineladdering as allocated IPO investors that continue to buy shares right after the listingbefore they sell all shares within six months of the listing date. This sales requirementis included to remove rationed investors that buy shares to reach optimal holding levelsafter the listing. We also show that IPO laddering benefits both investors and investmentbanks and that the specified trading can not be attributed to other explanations such asshare rationing. In the 50% IPOs with the highest laddering there is an average aggregateIPO allocation to laddering investors of 4%. On average these investors buy 6% more ofthe aggregate IPO shares after the listing, and then sell on average 10% of the aggregate

2See the litigation releases made by the SEC at http://www.sec.gov/litigation/litreleases/lr18385.htm,http://www.sec.gov/litigation/litreleases/lr19050.htm, and http://www.sec.gov/litigation/litreleases/lr19051.htm.

3There are many news articles and web pages that cover laddering and the laddering casesin the U.S. For excellent overviews please see Deneen and Hooghuis (2001), Aggarwal etal. (2006) and the IPO securities litigation websites at http://www.iposecuritieslitigation.com/,http://www.dandodiary.com/articles/ipo-laddering-cases/ and the articles by Susan Pulliam and RandallSmith, the journalists that first published the laddering scandal in the Wall Street Journal series in 2000.http://www.pbs.org/wgbh/pages/frontline/shows/dotcon/interviews/pulliam-smith.html

4In both Norway and the U.S. IPO laddering is illegal under the law against market manipulation.

9

IPO shares shortly after the listing. As a consequence of this, we are not able to rejectthat IPO allocations are tied to after-listing purchases of IPO shares.The SEC is investigating IPO laddering because laddering falsely increases the price

and demand of specific shares (price manipulation). In addition to being abusive anddiscriminatory, IPO laddering is undesirable because it increases adverse selection prob-lems (by deterring non-laddering investors from applying for IPO shares).5 Investmentbanks use IPO laddering because this practice will boost share prices after the listings.IPO shares that will go up in price for sure can also be allocated to bank clients thatprovide high levels of stock-trading commissions, thereby ensuring a future relationshipbetween banks and investors that generate high levels of income for the banks. We showthat investment banks and laddering inventors earn money on IPO laddering, while mostcompanies with high levels of IPO laddering fall in price in the first six months after thelisting (8 out of 11).IPOs generally have high first day returns (on average 8% in Norway in the sample

period) and IPO shares are therefore very popular investments. Most IPOs are manytimes oversubscribed and few investors are allowed to buy IPO shares. Investment banksare reluctant to distribute information about their allocation practices, and the continuedinvestigation by the SEC and the NASD on investment bank allocation practices has notmade data collection any easier. Ritter (2003) and Jenkinson and Jones (2004) arguethat there are three main views on how IPOs are allocated. First, the academic viewbased on Benveniste and Spindt (1989) is that investors obtain IPO allocations in returnfor revealing their true valuations of the IPO shares. These investors help to price theissue. Second, the pitchbook view argues that IPO shares are allocated to buy-and-holdinvestors, and long-term buy-and-hold investors will create price stability. Finally, therent seeking view argues that IPOs are allocated in return for kickbacks. The types ofrent seeking that have been under SEC investigation are to condition IPO allocationson generated stock-trading commissions, future corporate business (IPO spinning) orafter-listing purchases of IPO shares (IPO laddering), see Liu and Ritter (2010). IPOscan also be intentionally underpriced in exchange for future analyst coverage (analystconflict of interest). There are many articles that have studied both the academic andpitchbook view, but a lack of data has limited the number of articles which have studiedthe rent seeking view.6 Cliff and Denis (2004) show that IPO underpricing is relatedto after-listing analyst coverage, Liu and Ritter (2010) reveal that IPOs are allocated inreturn for IPO spinning and Fjesme, Michaely and Norli (2011) document that IPOs areallocated in return for stock-trading commissions. No empirical papers have been able toestablish a relationship between IPO allocations and after-listing purchases of IPO shares(IPO laddering). Hao (2007) identifies the incentives to engage in IPO laddering and theimplications of IPO laddering theoretically. Griffi n, Harris and Topaloglu (2007) showempirically that it is likely that IPO laddering is used by studying aggregate after-listingtrading at the brokerage house level. Griffi n et al. (2007) find that after-listing buy tradesprimarily go through lead managers, whereas after-listing sell trades go through othermanagers in the weeks after new listings. This is consistent with IPO laddering becauseladdering investors will place their orders through the lead manager as evidence that thetrades have been made. Previous research has not been able to study the relationship

5Laddering is not new. The SEC sent out warnings that laddering was illegal in 1961, 1984 and 2000(Griffi n et al., 2007).

6See, amongst others, Jenkinson and Jones (2004), Ritter (2003) and Fjesme, Michaely and Norli(2011) for papers that summarizes studies on IPO allocations.

10

between IPO allocations and after-listing trading of the IPO shares at the investor leveldue to data limitations.7 The main research question addressed in this paper is whetherinvestors are able to increase allocations in IPOs by committing to buy more shares afterthe listing of the same IPOs. We also investigate whether future IPO allocations are tiedto after-listing purchases in past IPOs.The rest of the paper is organized as follows: Section 2.2 describes related literature.

Section 2.3 describes predictions and testable implications. Section 2.4 describes the IPOprocess and the factors that create the incentives to engage in IPO laddering. Section2.5 describes the data set. Section 2.6 describes the empirical results, and Section 2.7concludes.

2.2 Related literature

The two main theoretical papers that model IPO laddering are Hao (2007) and Aggarwalet al. (2006). Hao (2007) first show the factors that create the incentives to engagein IPO laddering. Then, the effects of IPO laddering on companies are identified. Hao(2007) argue that IPO laddering can benefit the underwriter from two sources. First,IPO laddering can boost the after-listing market price. This will reduce the underwritersexpected cost of price support after the listing. From this it is expected that IPO ladderingwill be stronger when there is a positive drift in the after-listing share price. Second, IPOladdering can benefit the underwriter through rent seeking. If some allocated investors paya part of their profit from IPO allocations back to the underwriter through stock-tradingcommission payments, then a part of the laddering generated profits will go back to theunderwriter. Hao (2007) argue that when the underwriter share in on the profit fromthe underpricing, then laddering is stronger when the realized percentage underpricing ishigher. Hao (2007) also show that expected underpricing increases IPO laddering. Fromthis it is expected that laddering will be stronger when there is a positive underpricing.Hao (2007) also predicts that laddering is positively related to IPO allocations to high

stock-trading commission generating investors. IPO laddering will inflate prices after thelisting, so investment banks use laddering to make share prices go up after the listing(more than they otherwise would have). Shares that go up in price for sure are thenbe allocated to clients that generate high stock-trading commissions. Hao (2007) finallypredicts that laddering will increase the IPO offer price, the first day closing price, themoney left on the table and the long-run underperformance of the newly listed companies.Aggarwal et al. (2006) predict that IPO laddering increases underpricing, turnover andlong-run underperformance of the newly listed companies. These are all effects of anincreased demand of the IPO shares right after the listing that will fall in the long-run.There are three main empirical papers that provide indirect evidence of the existence

of IPO laddering. Griffi n et al. (2007) look at investors who buy shares through leadand other underwriters in the three weeks after the listing of 1,294 Nasdaq IPOs inthe period 1997 to 2002. As opposed to this study, they examine aggregate trading atthe brokerage house level. They argue that the after-listing buy trades through the lead

7Griffi n, Harris and Topaloglu (2007) find that it is very likely that investment banks tie IPO alloca-tions to after-listing purchases. The major difference is that Griffi n et al. (2007) study the after-listingtrading through co and lead managers at the brokerage house level, and we study actual IPO allocationsand after-listing trading on the investor level. Griffi n et al. (2007) show that it is likely that laddering isbeing used by investigating through what manager after-listing buy orders are placed, and we show thatafter-listing buy orders are related to current and future IPO allocations by investors.

11

manager (main underwriter) in the weeks after the listings are likely to be part of ladderingagreements, while buy trades through other managers (co-underwriters that help to spreadthe issue) in the same period are likely to not be part of the agreements. The paper findsthat it is likely that IPO allocations are tied to after-listing purchases because thereare unproportional high levels of buy trades through lead managers after new listings.Aggarwal et al. (2006) study IPOs that have been sued on laddering allegations to testthe implications of laddering. The data includes 33 IPOs sued by the SEC, 140 classaction law suits and 735 non-laddering IPOs on Nasdaq, NYSE and AMEX in the period1998 to 2000. The main findings are that IPO laddering leads to underpricing and long-run underperformance. Ellis (2006) investigates the trading volume in IPO shares afterthe listing for 311 Nasdaq IPOs in the period 1996 to 1997. She shows that investor buytrades through the lead underwriter account for 22% of trading volume after IPOs, andthis is consistent with laddering being used.8

2.3 Predictions and testable implications

An IPO investor is rationed when the number of shares sought in the IPO is larger thanthe allocation. Rationing will lead to a smaller IPO allocation than the applied for sharesfor most investors. Rationed investors may buy more shares after the listing to get tothe desired holding level. This has similar implications as IPO laddering. Griffi n etal. (2007) argue that investment banks may strategically allocate toe-holds to investorsthat the bank knows have higher optimal holding levels (share rationing)9. The bankdoes this in hopes that the investor will buy more shares after the listing to reach theoptimal holding level. It is expected that most optimal holding investors will reach theirdetermined holding level and then hold this in the longer run. Laddering investors, onthe other hand, buy shares right after the listing to fulfill an obligation.10 Many laddering

8There are also three other types of IPO rent seeking that have led to investigations and subsequentsettlements with the SEC or the NASD (Liu and Ritter, 2010). IPO allocations can be dependent onfuture corporate business (IPO spinning), stock-trading commissions or companies can agree to underpriceIPOs in exchange for after-listing company coverage from a star analyst provided by the investment bank(analyst conflict of interest). All of these allocation practices have been investigated in empirical papers.Liu and Ritter (2010) investigate 56 U.S. IPOs in the period 1996 to 2000 and show that IPO sharesare allocated to corporate executives in return for future corporate business (IPO spinning). Cliff andDenis (2004) show that IPO underpricing is positively related to the after-listing coverage by the leadunderwriter and an all star analyst (analyst conflict of interest). Nimalendran, Ritter and Zhang (2007),Reuter (2006) and Fjesme, Michaely and Norli (2011) show that IPO allocations are related to stock-trading commissions.

9The SEC makes a big point about selling shares early in their cases. It is claimed that banks frequentlyallocated shares to investors that had no plans of holding the shares in the long run. Apparently, thebanks asked the investors if they would agree to buy more shares after the listing and not if the investorswere planning to hold the shares in the long run. If the reason for the after-listing purchases is to increaseallocations, then this is laddering.

10Allocated IPO investors that buy more shares after new listings can be explained by either IPOladdering or by IPO share rationing. Most of the IPO first day return takes place between the offer priceand the first day opening price (not between the first day opening and the first day close). This meansthat any additional purchased shares have an expected return commensurate with risk and nothing more.It is therefore expected that investors that buy more shares after the listing do so because they want tohold more of the specific stock in their portfolio. If there is laddering, there should then be a strongerrelation between after-listing purchases and allocations for short term investors. Short term investors aremore likely to be laddering investors than long term investors.

12

investors will therefore sell their shares when the agreement is completed. The argumentis not that laddering investors will always liquidate their holdings early. The argumentis that investors that buy more shares because of optimal holding are more likely to holdtheir shares in the long-run. Some laddering investors are likely to hold their shares in thelong-run as well, but some laddering investors will also liquidate their shares early becausethey have no interest in holding the shares. It is important to note that the intention ofthe after-listing buyer to buy-and-hold does not remove the possibility of IPO laddering(Griffi n et al., 2007).11

Optimal holding is also not a very good explanation for the observed after-listingbuying in Norway. Investment banks rank investors on A, B and C lists before the IPOallocations.12 We do not know how investors are placed on the lists, but we believe thatit is related to the investors’past trading characteristics. Investors on the A list are likelyto be rationed less than investors on the B list, and investors on the B list are likely to berationed less than investors on the C list. It is therefore expected that IPO applicants onthe A list are awarded a big allocation and will buy few shares after the listing. Investorson the C list will be allocated few shares and will therefore buy many shares to reachtheir optimal holding level. This will create a negative correlation between the number ofshares allocated and the number of shares purchased after the listing for these investors.

2.3.1 The IPO laddering hypothesis

Hao (2007) argue that there are two reasons why underwriters use laddering. First, Hao(2007) argue that banks use laddering to boost prices after the listing. Boosted pricesare good for investment banks because the expected price support cost is then reduced.IPOs with boosted after-listing prices will also be viewed as more successful. Second,Hao (2007) argue that when the underwriter share in on the profit from the underpricing,laddering is stronger when the realized percentage underpricing is higher. Hao (2007) alsoshow that expected underpricing increases IPO laddering. (It is likely that the expectedunderpricing is highly related to the realized underpricing). If there is IPO laddering, it isexpected that the relationship between allocations and after-listing purchases is strongerwhen the realized underpricing is higher. From Griffi n et al. (2007) and the first argumentin Hao (2007) we expect that laddering is more likely when there is a positive drift inthe share price after the listing (boosted price) and after-listing investors sell their sharessoon after the listing date. This is formalized in H0.1. From Griffi n et al. (2007) andthe second argument in Hao (2007) we expect that laddering is more likely when there isa positive underpricing and after-listing investors sell their shares soon after the listing.This is formalized in H0.2. If the relationship between IPO allocations and after-listingpurchases is explained by share rationing, there is no reason why the relation should bestronger in IPOs where investors sell their shares soon after the listing, the price increasein the first week after the listing and the IPO is underpriced. This is formalized in HA.

11Griffi n et al. (2007) test between IPO laddering and optimal holding by studying how the aggregateinstitutional holding percentage evolves from the listing date to the first quarter and the first year afterthe listing. They argue that laddering investors are mainly institutional, so the aggregate institutionalholding percentage should go down in companies with IPO laddering - since laddering investors will reducetheir holding percentage and optimal holding investors will not. In the Norwegian data we observe thatthe investors are allocated IPO shares buy more IPO shares after the listing and then sell shares soonafter the listing. It is more likely that investors that follow this three stage IPO share investment processare laddering investors than optimal holding investors.12Information about allocation practices are obtained from meetings with former investment bankers

in Norway.

13

H0 and HA are tested by regression equation (1).13 If the relationship between allocationsand after-listing shares is significantly stronger for (After-listing shares/shares issued)%i

* D1 * D2 * D3 than for (After-listing shares/shares issued)%i, then we are not able toreject H0. This will, however, reject HA.

H0.1: The relationship between allocations and after-listing purchases is stronger wheninvestors sell all shares within six months after the listing and the price after one weekexceed the first day closing price.

H0.2: The relationship between allocations and after-listing purchases is stronger wheninvestors sell all shares within six months after the listing and the first day closing priceexceeds the offer price.HA: The relationship between IPO allocations and after-listing purchases is the same

for all investors.

(1) (Allocated shares/shares issued )%i= α+ β1(After-listing shares/shares issued)%i

+ β2(After-listing shares/shares issued)%i * D1 * D2 * D3 + β[Control variables] + εi

2.3.2 Other testable implications of IPO laddering

There are two other testable implications of IPO laddering besides that relation betweenafter-listing purchases and IPO allocations. First, it can be tested if IPO laddering isbeneficial for investors. In hot IPOs it is expected that investors that buy more sharesafter the listing will earn money because they are allocated an increased portion of hotshares. It is possible that the investors either lose or earn money on the additional sharespurchased after the listing (this is uncertain and can go both ways according to an e-mailby Goldman Sachs referred to in the SEC release), but it is expected that buying moreshares should be profitable overall. Money earned on the hot IPO allocations shouldoutweigh any loss on the additional shares. This is tested by investigating if ladderinginvestors earn money overall. In cold IPOs it is expected that the investors earn moneyon future IPO allocations. Although investors are not enthusiastic about cold IPOs it isexpected that investors will follow through with the laddering to not be excluded fromfuture IPOs, see Griffi n et al. (2007). This is tested by regressing past laddering on futureIPO allocations.Second, it can be tested if IPO laddering is beneficial for investment banks. Investment

banks tie allocations to after-listing purchases partly to earn money on stock-tradingcommissions. Laddering investors buy more shares after new listings so total IPOs withladdering increase more in price than IPOs with no laddering. Investment banks canthen charge more stock-trading commissions for IPO allocations with laddering, see Hao(2007). If this is the case, there will be a relation between stock-trading commissiongenerated before IPOs, by non-laddering allocated investors, and the aggregate after-listing purchases made by laddering investors. This is tested by regressing the aggregated

13D1: A dummy that takes the value of one if the investor have sold all allocated and after-listing shareswithin six months of the listing date.D2: A dummy variable that takes the value of one if there is a positive drift in the share price in the

week following the listing (from the first day closing price to the first week closing price).D3: A dummy variable that takes the value of one if the IPO have a positive underpricing.

14

IPO after-listing purchases made by the laddering investors on the average commissiongenerated per share before the IPO (by the non-laddering allocated investors).

2.4 The listing process and the incentives to engage in IPO lad-dering

The OSE requires that companies have suffi cient levels of equity to survive for 12 monthswithout a positive cash flow after a listing. The OSE also requires that public companiesmust have a minimum number of owners before they can list (500 for the main list).14

This means that most companies need to issue equity before they are able to list publicly.Table 1 gives the annual distribution of IPOs on the OSE in the sample period. Mostcompanies are assisted by an investment bank in their equity issuance and in the listingprocess. The investment bank makes a list with proposed IPO allocations that is given tothe board of the issuing company for approval. Anecdotal evidence suggests that this listtypically is approved without adjustments. Investment banks and investors have differentreasons for why they participate in IPO laddering. Regulators investigate IPO ladderingbecause it is manipulative.15

2.4.1 Why investment banks use IPO laddering

IPO laddering can be advantageous for investment banks in both hot and cold IPOs.There are two main reasons why investment banks use IPO laddering in hot IPOs. Firstly,investment banks can earn money on combining allocations to investors that generate highstock-trading commission and to laddering investors. IPO laddering will boost pricesafter the listing. This will give the companies attention as more successful IPOs (Hao,2007; Aggarwal et al., 2006; Griffi n et al., 2007). Secondly, IPO laddering will increaseunderpricing. The IPO allocations will then be valued higher by investors that are willingto pay stock-trading commissions to obtain allocations (Hao, 2007; Aggarwal et al., 2006).In related papers, Reuter (2006), Nimalendran et al. (2006) and Fjesme, Michaely andNorli (2011) show that stock-trading commissions are related to IPO allocations.Laddering can also be beneficial for investment banks in cold IPOs. IPO laddering

will reduce the after-listing price uncertainty in cold IPOs. This is good for investmentbanks because IPOs that fall in price may cause reputation damage (and price supportif used without over allotment options is potentially expensive) (Hao, 2007; Aggarwal etal., 2006; Griffi n et al., 2007). Investment banks use IPO laddering to earn more moneyon stock-trading commissions, to increase the likelihood of successful IPOs and to reducethe risk of after-listing price falls.16 The after-listing purchases will also increase directcommission from the extra trades. According to Griffi n et al. (2007), it is uncertainwhether laddering is more beneficial for the investment banks in hot or cold IPOs.17

14The information about the listing process is obtained from the seminar “The road to the listing”November 3, 2009 by Deloitte Public Accountants and the Oslo Stock Exchange and from meetings withformer investment bankers in Norway.15Figure 1 describes the incentives to engage in IPO laddering for the different market participants.16It is probably more common that bidders will offer laddering than that banks require laddering.

Investors will offer laddering if they believe that this will increase allocations and lead to future allocations.Hao (2007) argues that it does not matter for the effect of laddering if it is bidder or investment bankinitiated.17Laddering in cold IPOs creates a relation between after-listing purchases and future allocations (not

necessarily between allocations and after-listing purchases). Laddering in hot IPOs will create a relationbetween allocations and after-listing purchases in specific IPOs.

15

2.4.2 Why laddering investors agree to buy more shares

Investors agree to buy more shares after cold IPOs to get future allocations in hot IPOs.Investors are not likely to be enthusiastic about laddering in cold IPOs, but investors whowant continued access to future hot IPO allocations are likely to follow through with theagreements (Griffi n et al., 2007). Investors accept laddering in hot IPOs in order to getmore allocations in the specific IPOs. Laddering investors may either earn or lose moneyon the extra shares purchased after the listing, but it is expected that the return of thehot allocated shares will outweigh any loss on the additional shares.18 Investment banksdo not require laddering by all investors. Griffi n et al. (2007) argue that laddering ispre arranged buying support by large institutional clients. It is easier to control that theshares are purchased when there are only a few investors involved.

2.4.3 Why IPO laddering is a problem

The reason why the SEC is investigating IPO laddering is because laddering violates bothanti-price-manipulation and anti-fraud regulations. Laddering will falsely increase priceand demand in specific shares. Investors who are not aware of the laddering will buyshares on false market demand information. Regulators (the SEC) try to ensure that theIPO allocation process is fair and open to all investors. Any abusive allocation practiceswill not be tolerated. Laddering is a problem because it is discriminatory against investorsthat are not willing to engage in price manipulation to receive IPO shares. In a fair IPOwith high demand the offer price will increase and more money will go to the issuingcompany. In an IPO with laddering the price will go up after the listing and more moneywill go to the allocated investors.Other investors can also lose money on IPO laddering. The investors that are allocated

less (or no) IPO shares because the laddering investors are allocated more hot shares aremissing out on good investment opportunities. Non-allocated investors that buy sharesafter the listing lose money if the laddering investors sell their shares so that prices fallafter the listing. IPO laddering will also increase adverse selection problems. Wheninvestors know that it is possible to buy allocations with after-listing trading, it is notlikely that investors will participate in IPOs. Investors that do not provide any form ofkickback will not want to participate in IPOs because they expect shares to be overpricedwhenever they are offered allocations.The allegation made by the SEC is that investment banks have promised investors

that they will get favorable IPO allocations if they buy additional shares after the listingof the same IPO.19 The banks have, allegedly, asked IPO share applicants if they areinterested in buying more shares after the listings and at what prices and quantities. Thebanks have also allocated shares to investors with after-listing interest -investors the banks

18See the litigation releases made by the SEC at http://www.sec.gov/litigation/litreleases/lr18385.htm,http://www.sec.gov/litigation/litreleases/lr19050.htm, and http://www.sec.gov/litigation/litreleases/lr19051.htm.19Three U.S. Investment banks that have been sued and later settled with the SEC on IPO laddering

allegations. None of the banks have admitted to the laddering charges, but all banks have agreed to paypenalties of $40 million (Morgan Stanley), $40 million (Goldman Sachs) and $25 million (J.P. Morgan).The charge by the SEC is that the banks have violated Rule 101 of Regulation M under the Securities andExchange Act of 1934. This rule is, among other things, in place to prohibit underwriters in a restrictedperiod, prior to their completion of the distribution of the IPO shares, from bidding for or attemptingto induce any person to bid for or purchase any offered security in the aftermarket. Regulation M isdesigned to prohibit activities that can artificially influence the market and the perceived demand of theIPO shares.

16

knew were likely to sell their shares soon after the listing (laddering investors). The bankshave made follow up calls to investors that indicated after-listing interest to make surethe purchases are made. Arguably, the only reason investors have provided after-listinginterest is because the investors understand that this will help them get favorable IPOallocations. Banks and investors have agreed that investors will buy after-listing sharesproportional to the allocations they receive.20

2.5 Data description

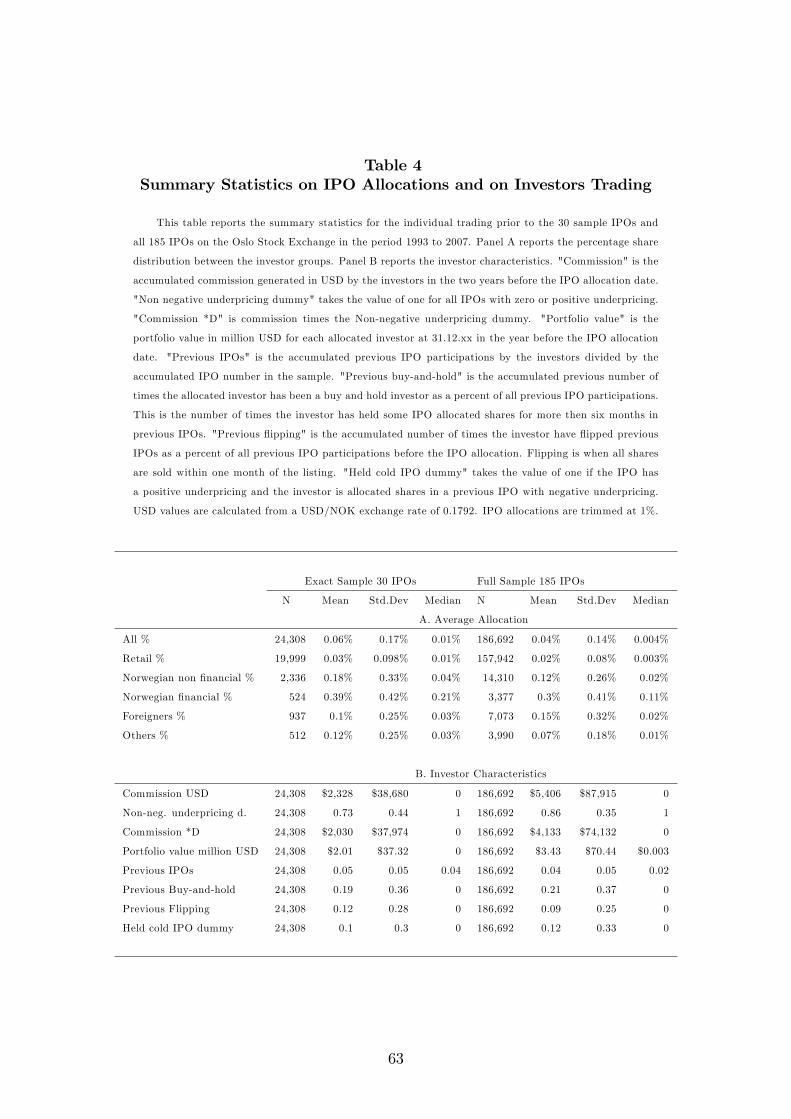

There are 403 new listings on the OSE in the period January 1993 to September 2007(210 of the 403 companies listed through IPOs)21. New listings are identified from theannual statistics published by the OSE. Allocation dates are collected from the IPOlisting prospectuses. One listing requirement on the OSE is that all shareholders mustbe registered in the Norwegian Central Depository (VPS) before the listing. The numberof shares owned by each investor must be given to the VPS before any company can listpublicly. This database is 100% accurate, as it is not possible to list otherwise. TheVPS database includes month end ownership by all shareholders in all companies thatare publicly listed or intend to list publicly. Some companies list in the VPS databaseyears before the listing. Other companies list in the VPS as part of the listing process.See Figure 3 for a detailed description of the timeline in the listing process.IPO allocations are obtained from the VPS database by taking the difference in com-

pany ownership before and after IPO allocation dates. We only investigate IPO allocationsto new shareholders. More allocations to existing shareholders, if any, are not included inthe analysis. All companies list in the VPS, sell shares in the IPO and list on the OSE.There are three dates that are important in the listing process to determine IPO alloca-tions,: -when companies list in the VPS ownership database, when companies distributeshares in the IPO and when companies list on the OSE. All three dates influence data onIPO allocations. Companies do this process in different orders, and this leads to differentlevels of the obtained IPO allocations.There are 15 savings banks (PCC list) out of the 210 IPOs on the OSE in the sample

periods. In total, 14 and seven of these savings banks are in the 185 IPOs with allocationdata and in 30 exact sample respectively. These banks are owned by the bank guaranteefund before they are publicly listed. All results remain unchanged if the banks are includedin the analysis or not. These savings banks are removed in the main analysis because itcan be argued that these banks are causing the results. The savings banks does nothave previous owners before the listing, so it can be argued that different investors tryto gain control over these companies after the listing. Investors who are not able to getcontrol will eventually sell their shares. This will create similar findings, as the ladderinghypothesis, for these savings banks.

20In addition to these allegations, the NASD claims that J.P. Morgan tied cold IPO allocations to hotIPO allocations and that J.P. Morgan allocated hot IPO shares to investors in the return for acceptingcold IPO allocations. This is also part of the J.P. Morgan settlement. Hao (2007) explains that IPOorder books often have investors that are marked with the number of shares that will be purchased afterthe listing.21In total 14 savings banks listed on the PCC list of the OSE are removed from the analysis. Most of the

PCC companies are listed by the Norwegian bank guarantee fund. When including the PCC companiesthe findings remain unchanged.

17

2.5.1 The IPO sample

When the listing in the VPS database, the IPO allocation and the listing on the OSE are inseparate calendar months, we are able to calculate exact IPO allocations (the ownershipdata is in monthly observations). Group one companies list in the VPS in good timebefore the IPO. These companies also list on the OSE in a separate calendar month fromthe IPO (for most companies, the IPO is in the calendar month right before the listingmonth). For group one companies the IPO allocations are completely accurate. Thereare 16,593 IPO allocations in group one companies (23 IPOs). After-listing purchases arethe increase in the number of shares by the allocated investors from the IPO allocationto the end of the listing month (and to the end of the month after the listing).22

2.5.2 The remaining IPOs

The data set also includes 158,789 IPO allocations in 148 IPOs that are used in robustnesstests.23 The allocations in these IPOs include either some existing owners or some after-listing trading. Group two companies list in the VPS in good time before the IPO, butthey list on the OSE in the same calendar month as the IPO allocation month. Thesecompanies have allocations that include the actual IPO allocations and some after-listingtrading. These IPO allocations includes from one to 30 days of after-listing trading.The companies in group two are used to test the relationship between past and futureafter-listing IPO holdings.

2.5.3 Aggregate laddering

There are 317 investors who sell all allocated and all after-listing shares within six monthsof the listing date in IPOs with a positive underpricing (in the 50% IPOs with the highestladdering). The aggregate allocations to these investors is 4% of the IPO shares. Theybuy in aggregate 6% of the IPO shares after the listing. Within six months they havesold all IPO shares (in aggregate 10% of the IPO shares). There are 174 investors whosell all allocated and all after-listing shares within six months of the listing date in IPOsthat appreciate in price in the week after the listing (in the 50% IPOs with the highestladdering). The aggregate allocations to these investors is 5% of the IPO shares. Theybuy in aggregate 8% of the IPO shares after the listing. Within six months they havesold all IPO shares (in aggregate 13% of the IPO shares).

22Shares sold over the counter (OTC trading) in the period between the allocation day and the endof the allocation month will not be detected in the data. Investors that buy shares in the OTC marketbetween the allocation day and the end of the allocation month will be treated as allocated investors.OTC trading is, however, expected to be a very small issue. It is unlikely that many investors that havebeen allocated IPO shares will sell these shares in the weeks before the listing. The average number ofdays between payment date in the IPO (when shares are transferred) and the listing date is just belowtwo weeks23The reason it is 148 IPOs and not 172 (195-23=172) is because in 15 IPOs it has not been possible

to calculate IPO allocations from the ownership data. These companies are listed in the VPS in thesame month as the listing month. These companies are therefore removed from the sample. In 6 IPOsit has not been possible to locate the pricing information. These IPOs are therefore not included in theanalysis. There are three privatizations in the period that are removed.

18

2.5.4 Variable explanations

IPO level characteristics are given in Table 2. Market value is the total market value(in USD) at the listing date of the IPO company. This is calculated as the number ofoutstanding shares times the first day closing price. Book/Market is the book to marketratio of the IPO company at the listing date. This is calculated as the book value ofequity, after the IPO, divided by the market value. Offer price is the IPO offer price (inUSD) reported in the listing prospectus or in the newspapers. VC dummy is a dummyvariable that takes the value of one for companies with venture capital backing. High-tech dummy is a dummy variable that takes the value of one for IT -companies. The IPOcompany variables are used to control that the results are not driven by company specificcharacteristics. Market value and the book to market ratio are included in the regressionsto make sure that company size is not driving the results. Offer price is included to makesure that it is not very high or low priced IPOs that drive the results. The VC dummyand the high-tech dummy are included to make sure that the results are not driven byventure capital backing or high technology companies. All regressions include IPO andyear fixed effects. These are dummy variables that take the value of one for each of thecompanies and sample years.Investor characteristics, for the investors on the OSE in the period 1993 to 2007,

are described in Table 3. (After-listing shares/shares issued) % is the additional sharespurchased after the listing divided by the total number of shares issued in the IPO.24 Theafter-listing shares are calculated as the share increase from the IPO allocation to theend of the listing month for the 23 sample IPOs. (We also include the share increase tothe end of the month after the listing because some companies list late in the month andIPO laddering may go on as long as three weeks after the listing, see Griffi n et al., 2007).For the remaining IPOs the share increase is measured from the end of the listing monthto the end of the month after the listing. This is likely to underestimate the after-listingpurchases in the IPOs used for robustness. D1 is a dummy variable that takes the valueof one if the investor have sold all allocated and after-listing shares within six months ofthe listing date. D2 is a dummy variable that takes the value of one if there is a positivedrift in the share price in the week following the listing (from the first day closing priceto the first week closing price). D3 is a dummy variable that takes the value of one if theIPO have a positive underpricing. (Allocated shares/shares issued) % is allocated sharesto each investor divided by the total number of shares issued in the IPO.25 This is thepercentage allocation of shares given to each investor in each IPO. Previous laddering isthe accumulated number of times an investor has laddered divided by the accumulatednumber of times the investor has participated in IPOs. This is a measure of how frequently

24The number of shares sold in the IPO is the number of actual shares sold to new shareholders fromthe VPS database. In the listing prospectuses the number of shares sold is often listed as a range. E.g. inthe Aqua Bio IPO the listing prospectus says that the number of shares sold will be between 1.2 millionand 4 million shares. It is also uncertain if Over Allotment Options (OAO) is used or not. This mayincrease the number of shares sold from the listing prospectus to actual shares sold up to 20%. E.g. inthe Nutri Pharma IPO the minimum number of shares sold is 10 million. The lead manager is given 2million extra shares in an OAO. From the prospectus it is impossible to know the exact number of sharesthat will actually be sold. This number is observable in the VPS database.25(Allocated shares/shares issued) % is trimmed at 1% at the total 171 IPO level to remove the highest

IPO allocations. These allocations are not likely to be made to investors based on trading characteristics.This is included to be consistent with Fjesme, Michaely and Norli (2011). This trimming has no influenceon the findings in this article.

19

an investor engages in laddering, relative to its total participations in IPOs.26

Commission is the accumulated commission (in USD) generated by each investor inthe two years before the IPO allocation dates.27 Commission is calculated as the monthlyportfolio turnover times share prices and a fixed percentage commission rate (0.075%).The 0.075% commission rate is the average used by 15 Norwegian brokerage houses.Commission is calculated as buy generated commission only. Generated commission belowthe minimum rate is replaced by the fixed minimum fee for one transaction ($15). Portfoliovalue is the total investor portfolio value (in million USD) for each allocated investor at31.12.xx in the year before the IPO allocation date. This is calculated as the shares heldat 31.12.xx times the appropriate share prices. Financial institution dummy is a dummyvariable that takes the value of one for investors that are either Norwegian or foreignfinancial institutions.Previous IPOs is the accumulated previous IPO participations by the investors di-

vided by the accumulated number of IPOs in the sample.28 This is used to measure howmany IPOs, out of all possible in the sample, each investor has participated in. Pre-vious buy-and-hold is the accumulated previous number of times the allocated investorhas been a buy-and-hold investor divided by all previous IPO participations. This is thenumber of times, out of all previous IPO participations, the investor has held some ofthe IPO allocated shares for more than six months after the listing. Previous flipping isthe accumulated number of times the investor has flipped previous IPOs divided by allprevious IPO participations. Flipping is when all shares are sold within one month aftera listing. This is the number of times, out of all previous IPO participations, the investorhas held all IPO allocated shares for less than one month. The previous trading variablesare used to control that the results are not driven by investor size, trading activity orholding periods.Other control variables includes the Percentage change in pricing range that is the

change from the midpoint in the pricing range to the offer price in book-building IPOs.This variable measures price information collected in the book-building period, see Ljungqvistand Wilhelm (2002). Number of sentiment investors is the number of allocated retail in-vestors that buy less than 1,000 shares in the IPO. We use this as our sentiment measureas we believe that small retail investors are more sentiment driven in their IPO applica-tions as they spend less time on fundamental analysis, see Kumar and Lee (2006). Averagecommission per share is calculated as the total commission generated by non-after-listingpurchasing investors in the 24 month period before the IPO divided by the number ofshares allocated in the IPO. This is the average dollar generated commission per share be-

26An investor that has participated in one IPO and bought more shares after the listing and then soldshares will take the value of 1 (1/1). An investor that has participated in two IPOs and bought and soldmore shares after the listing in one of these IPOs will take the value of 0.5 (1/2).27Commissions are generated from monthly data and not daily data.28Many IPOs are underwritten by more than one investment bank. If there is more than one investment

bank involved in the IPO, the bank that appears on the top left of the front page of the listing prospectusis assumed to be the lead investment bank. Carter and Manaster (1990) use the investment bank thatappears top left on the tombstone as the lead investment bank. In most IPOs there are also co-managersthat help with spreading the shares. Co-managers will allocate shares to their own clients. Investmentbanks can be co-managers in many IPOs, and this creates the situation where investors can be allocatedshares as a reward in an IPO by another lead bank. There are also some mergers between investmentbanks in the period and this will also create the situation where award shares can come from other leadbanks. Because of this, we investigate past trading behavior in all past IPOs in relation to current IPOallocations. We also study IPOs by one single bank separately. When this is done, we only investigatepast trading in the IPOs where the one bank has been the lead.

20

fore the allocation (by non-laddering investors). Combined commission % is calculated asthe commission generated by all the allocated investors in the 24 month period before eachIPO divided by the accumulated commission generated by all the allocated IPO investorsin the 24 month period before all IPOs. Average commission and Combined commissionare used to measure how important stock-trading commission is for allocations in eachspecific IPO. These variables measure if there is a relationship between commission gener-ated before an IPO (by the allocated investors) and the aggregated after-listing purchasesof the IPO shares.We do not know the exact oversubscription numbers in each IPO. Normally, oversub-

scription numbers are used to define if IPOs are hot (popular/oversubscribed) or cold(less popular/undersubscribed). We proxy for hot/cold by a dummy that takes the valueof zero if there is negative first day return (cold) and one otherwise (hot). We expect thatunderpriced IPOs are hot and non-underpriced IPOs are cold.

2.6 Empirical results

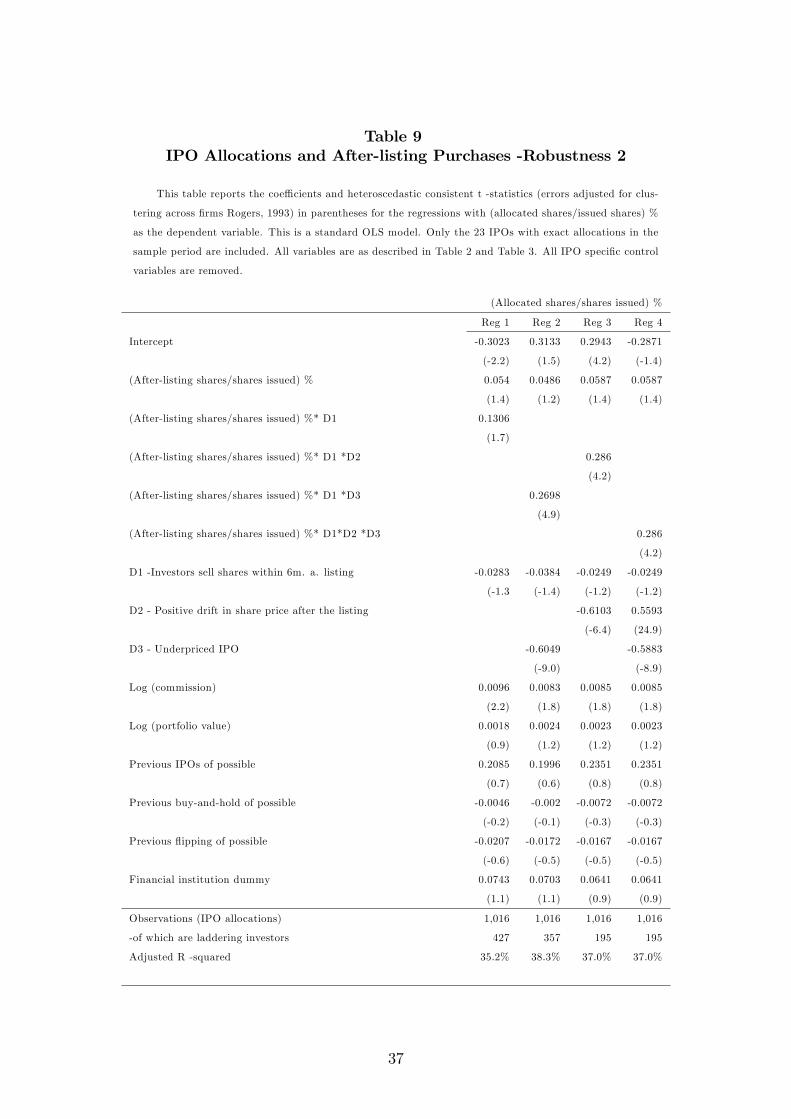

From Table 4 it can be seen that there is a positive relationship between IPO allocationsand after-listing purchases (regression 1). This relationship is significantly stronger forinvestors who sell their shares soon after the listing (regression 2). The relationship isalso significantly stronger for investors that sell all shares soon after the listing in IPOswith a positive drift in the share price in the week after the listing (regression 3). Thisis consistent with H0.1. The relationship is also significantly stronger when investors sellshares soon after the listing and the IPO have a positive realized underpricing (regression4). This is consistent with H0.2. The relationship between allocations and after-listingpurchases is also significantly stronger for investors that sell all shares soon after thelisting, in IPOs with a positive underpricing, and in IPOs with a positive drift in theshare price after the listing (regression 5). The point estimate for the allocation andafter-listing purchase relationship is typically two to five times as large for the caseswhere H0 specify that the relationship should be stronger.The relationship is also economically significant. The coeffi cient between allocation

and after-listing purchases is about 0.25. This means that for each 1% of the issues that isallocated these investors buy 4% more after the listing, controlling for all other variables.The average number of shares purchased after the listing is close to 7,000 shares for the 427laddering investors. This indicates that the allocation rule is that investors who committo buy 7,000 shares after the listing are allocated close to 2,000 more shares in the IPOs.The results are robust to how many shares and how early the shares must be sold

for investors to be regarded as laddering investors. The results remain unchanged wheninvestors who have sold 50% of their shares within three months of the listing date areregarded as laddering investors. The relationship between IPO allocations and after-listing purchases is significantly stronger for investors that sell 50% of total shares withinthree months after the listing, in IPOs with a positive underpricing, and in IPOs with apositive drift in the share price after the listing than for other investors (regression 6).The relationship is also significantly stronger for investors that sell 50% of total shareswithin six months after the listing, in IPOs with a positive underpricing, and in IPOs witha positive drift in the share price after the listing (regression 7). This is consistent withH0.29 Most of the control variables are unrelated to the level of allocations. Generated29Both allocated shares and after-listing shares are scaled by the number of shares issued in the IPOs.

21

stock-trading commission is positively related to allocations. This indicates that ladderinginvestors are active investors.To make sure that the results are not driven by the other allocations views suggested by

Ritter (2003) and Jenkinson and Jones (2004) we control for these views in all regressions.To control for the pricing information view (the academic view) we include a dummyvariable that takes the value of one for all professional investors (financial institutiondummy). If there is allocation to buy-and-hold type investors, there will be a relationbetween holding periods and IPO allocations (buy-and-hold view). This is controlled forby including the past IPO holding period of the allocated investors in all regressions (pastbuy-and-hold and past flipping). Neither of these variables are consistently related toallocations. It is also possible that allocations are made to commission generating investorsonly (rent seeking view). This view is controlled for, and ruled out by including theportfolio value and the generated commission before the IPOs by the allocated investorsin the regressions.30

In Table 5 the relation between past IPO laddering and future ownership of IPO sharesis investigated more closely. If there is IPO laddering, it is expected that investors maybe rewarded with allocations in future IPOs as well. Testing the relation between pastladdering and future allocations is hard in the 23 IPO sample because there may be sometime between each observed IPO. This is therefore tested on the full sample where IPOallocations include after-listing trading. Here we test whether investors that buy more(and then sell) shares after the listing of IPOs also hold shares after the listing of futureIPOs. In Table 5 all 171 IPOs (with 175,382 IPO allocations) are investigated. Mostof these IPOs are of group two allocations. This means that the IPO allocations maybe overestimated and the after-listing purchases may be underestimated in these IPOs.31

Therefore, we are not studying allocations. Rather, this table investigates whether pastafter-listing buying leads to future after-listing holding of IPO shares.In Table 5 we regress after-listing holdings of IPO shares on the number of times in the

past (out of all IPO participations) allocated investors have bought (and then sold) moreshares after IPOs. There is a strong relation between past IPO laddering and shares heldafter future IPOs. This indicates that banks tie IPO allocations together. This indicatesthat IPO shares are also rewards for past laddering in IPOs.32 There is a consistent

There are very different numbers of shares sold in each IPO. Capital raised depends on both the numberof shares and on the offer price in the IPO. The numbers we are interested in are therefore allocatedshares and after-listing shares in percent of issued shares. This tests the relationship regardless of thenumber of shares issued in the IPO. We also regress allocated shares on after-listing shares directlywithout adjusting for issued shares in all regressions. This does not alter the findings. There are somechanges to significance levels and adjusted R —squares, but the results remain the same (not reported).30We are not able to control for IPO spinning. IPO spinning is when IPO shares are allocated to

company executives for future corporate business. Spinning will not generate the same implications asIPO laddering, so we argue that this is not a problem.31These shares are still purchased by the investors. Aftermarket purchases for group two IPO allocations

are calculated as the share increase from the end of the listing month to the end of the month after thelisting. This means that all of these investors have an increase in the IPO shares in this period. Allof these investors are buying shares after the listing of IPOs. These investors also hold significantlymore IPO shares in subsequent IPOs. Table 5 shows that investors who hold shares after the listing ofIPOs, before they buy more shares in the following month, also hold more shares of future IPOs. This isconsistent with the laddering story. We cannot show that IPO allocated investors who buy more sharesafter a listing are allocated more hot IPO shares, but we show that investors who buy more (and thensell) shares after the listing of an IPO have more IPO shares in their future portfolios.32Past aftermarket buying is less statistically and economically related to IPO allocations in the 20

IPOs by the least active investment banks (not reported). The tie-in agreement variables are highly

22

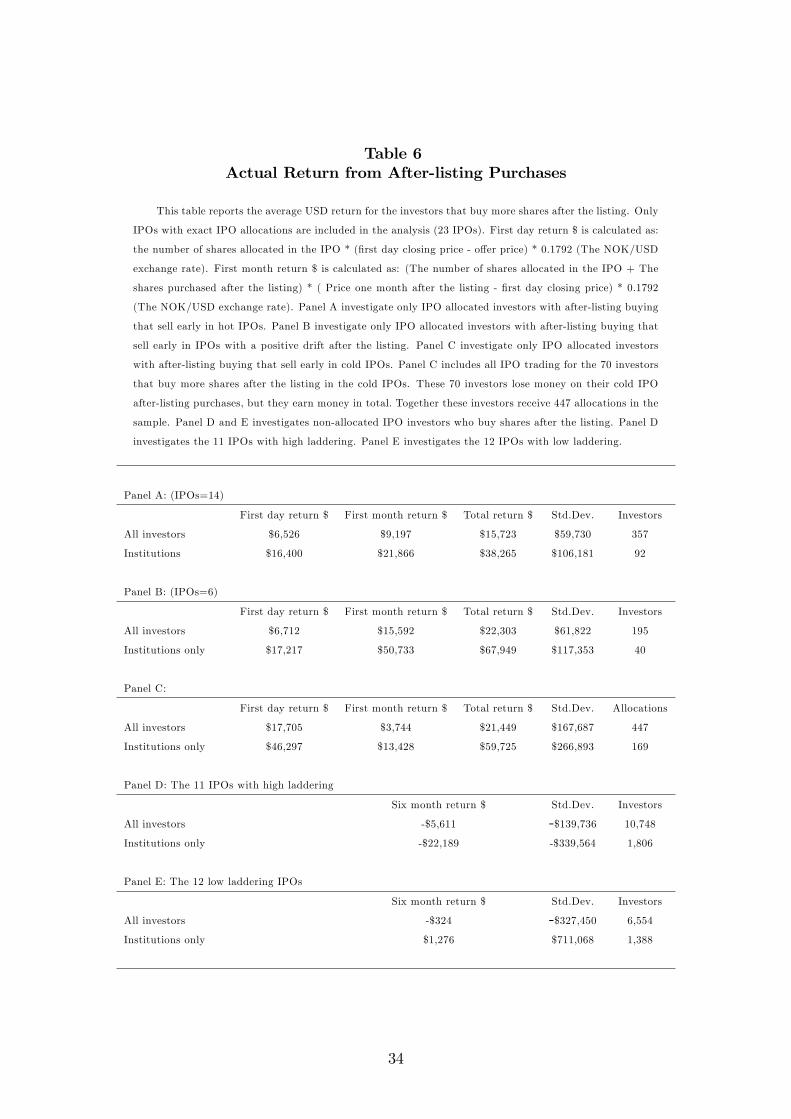

negative relationship between past buy-and-hold and IPO allocations. Investors are notallocated shares because they repeatedly hold their shares in the long-run. Investors are,however, punished for flipping shares in the past. Flipping investors are kept out of futurehot IPOs. These findings also show that investment banks keep records of how investorstrade in IPOs. The banks use these records in their future IPO allocations. This isconsistent with the SEC releases where it is claimed that banks track investor tradingand use this in their future allocation decisions.From Table 6 it can be seen that investors are able to earn a profit from IPO laddering.