Embed Size (px)

Citation preview

Infrastructure and Real Estate:Long Term Investments Building Europe’s Future

23 November, Brussels

Infrastructure and Real Estate:Long Term Investments Building Europe’s Future

Brenna O’Roarty, RHL Strategic Solutions

Agenda

3

• The importance of long-term Real Asset investments to pension funds and insurance companies

• Real Assets are fundamental to progressing a sustainable built environment

- Enabling commercial activity

- Functional management of the built environment

- Catalyst for urban regeneration

- Mutuality of transport infrastructure and real estate

- Create solutions to structural and cyclical challenges

• Investment Structure

- Ownership models

- Range of investment profiles with distinct risk characteristic

- Lifecycle of real assets extended by investment across the risk spectrum

The Importance of long-term Real Asset Investments to

Pension Funds and Insurance Companies

Why do pension funds andinsurance companies invest in real assets?

Real Assets - Infrastructure and Real Estate – allow long-term investors to capture higher returns

from these assets’ relatively lower liquidity and transparency, in turn enabling themto:

• Match long-term liabilities

• Protect against inflation

• Deliver commitments to pensioners and savers

• Diversify portfolio risks and returns with

equities and bonds

Short-term bondsLong-term bonds

Public Equity

Commodities

Hedge Funds

Private Equity FundsReal Estate

Venture Capital Funds

Public Equity Strategic

Direct Private Equity

Other Real Assets Infrastructure

Direct Venture Capital

Longer-TermShorter-Term

Lo

w L

iqu

idity

Hig

h L

iqu

idity

Source: Adapted from World Economic Forum (2011)

5

Infrastructure and Real Estate

investments have a synergistic

relationship:

• The success of projects is mutually

interdependent

• Real estate often secures the financial

viability of private sector infrastructure

investments

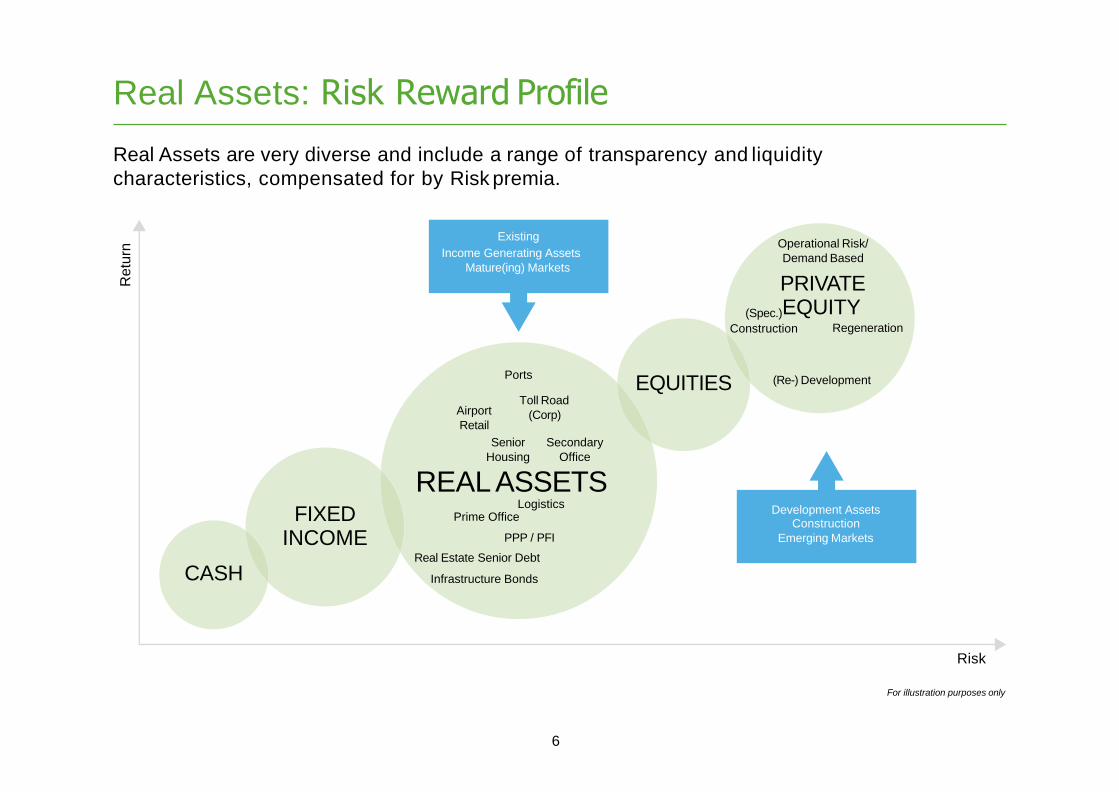

Real Assets: Risk Reward Profile

Real Assets are very diverse and include a range of transparency and liquidity

characteristics, compensated for by Risk premia.

Ports

Airport

Retail

Toll Road

(Corp)

Senior Secondary

Housing Office

Logistics

PPP / PFI

Real Estate Senior Debt

Infrastructure Bonds

(Re-) Development

Operational Risk/

Demand Based

PRIVATE

(Spec.)EQUITYConstruction Regeneration

EQUITIES

REALASSETSFIXED

INCOME

CASH

Retu

rn

Risk

For illustration purposes only

Existing

6

Income Generating Assets

Mature(ing) Markets

Development AssetsConstruction

Emerging Markets

Prime Office

Real Assets are Fundamental to progressing a

Sustainable Built Environment

Three Dimensions to a Sustainable Built Environment

Adams, W. (2006); Dreo, J. (2009)

8

Social

Sustainable

Bearable Equitable

EconomicEnvironmental

Viable

9

Economic Social Environmental

Real A

ssets

UtilitiesProvision of fundamental

requirements of energy, water,

waste and communication

systems and networks

Inclusive access to

energy, water, waste and

communication systems and

fibre optic networks

Renewal of systems to reduce

waste, recycle materials,

reuse water and incorporate

renewable energy sources.

Requires close integration

with built environment through

smart technologies including

smart grid and renewable

technology, rainwater collection

etc.

TransportAccessibility; efficiently linking

workforce to jobs; customers to

business and goods to market

Democratising mobility and

access to employment, public

services including health &

education and other public

services, and community

services and activities

Reducing energy consumption,

congestion and carbon

emissions

Real Estate

Physical manifestation of

strategic planning. Co-location

of compatible and competing

activities. Provision of built

environment as a factor of

production for commerce

including offices, retail outlets,

industrial units, distribution

centres, hotels, data centres,

transport hubs (stations,

airports) etc. Respond to macro

drivers to facilitate change

Place-making. Housing. Public

space. Respond to drivers

of social change (eg socio-

demographics). Provision of

physical infrastructure for

health, education and other

services including hospitals,

health centres, senior living,

student accommodation etc.

Ensures progression of

built environment through

protecting, restoring and

retrofitting existing real estate

and developing smart buildings

for the future. In doing so,

is a major contributor to

achieving reductions in energy

consumption and emission

targets

Infrastructure and Real Estate:Enabling Commercial Activity

• Creation of marketplace through provision

of suitable premises with appropriate

adjacencies to transport, public services,

workers, customers and other public

and private services

• Co-location of compatible activities

• Increased accessibility,

especially SMEs who could not

afford to purchase premises

• Physical assets require regular

maintenance, upgrades and

investment

• Increased energy, water and waste

efficiency

• Increases social inclusion (especially

accessibility)

• Creates cost efficiencies for business

• Enables businesses to more readily

adapt real estate holdings to

opportunities (expansion / contraction of

space and / or locations)

• Real Estate transforms from a potential

constraint to a facilitator of commerce

• A lease essentially allows business owners

an option to purchase premises for an

agreed time period and pay in installments

• Releases capital for business

investment in expansion, plant,

machinery & equipment, R & D,

training and jobsCapital

Efficiency

Market

Accessibility

Agility &

Flexibility

Professional

Management

10

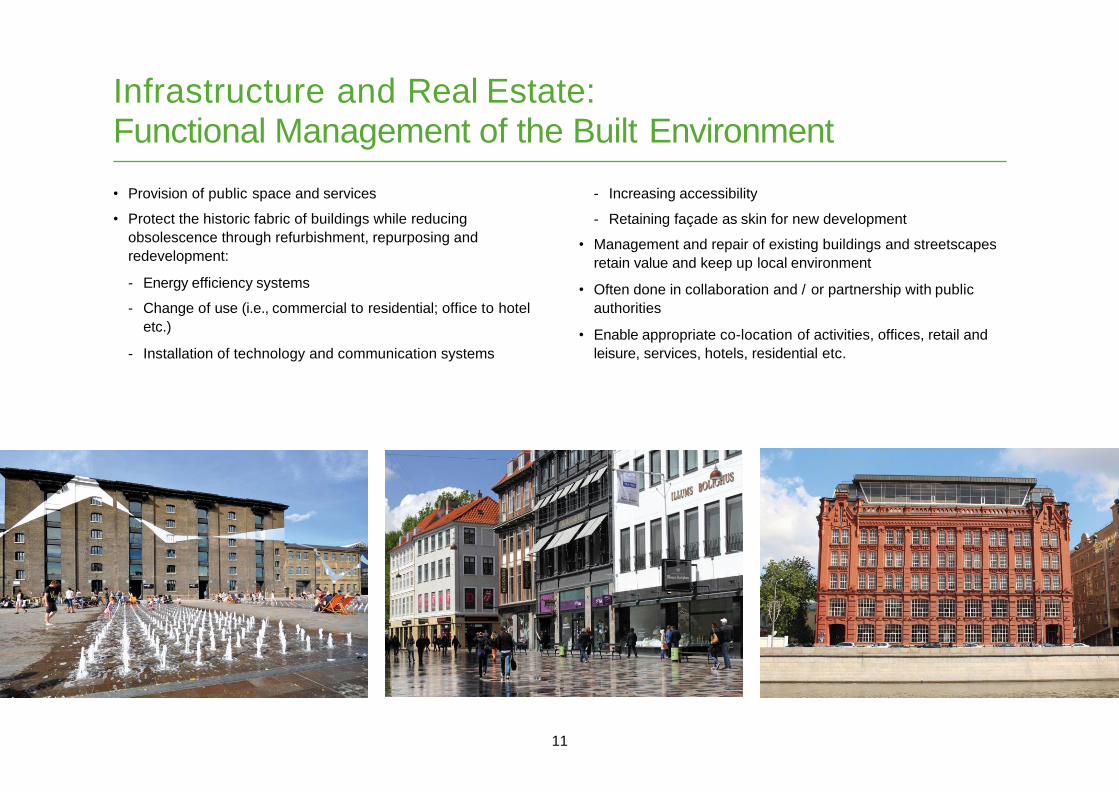

Infrastructure and Real Estate:Functional Management of the Built Environment

• Provision of public space and services

• Protect the historic fabric of buildings while reducing

obsolescence through refurbishment, repurposing and

redevelopment:

- Energy efficiency systems

- Change of use (i.e., commercial to residential; office to hotel

etc.)

- Installation of technology and communication systems

- Increasing accessibility

- Retaining façade as skin for new development

• Management and repair of existing buildings and streetscapes

retain value and keep up local environment

• Often done in collaboration and / or partnership with public

authorities

• Enable appropriate co-location of activities, offices, retail and

leisure, services, hotels, residential etc.

11

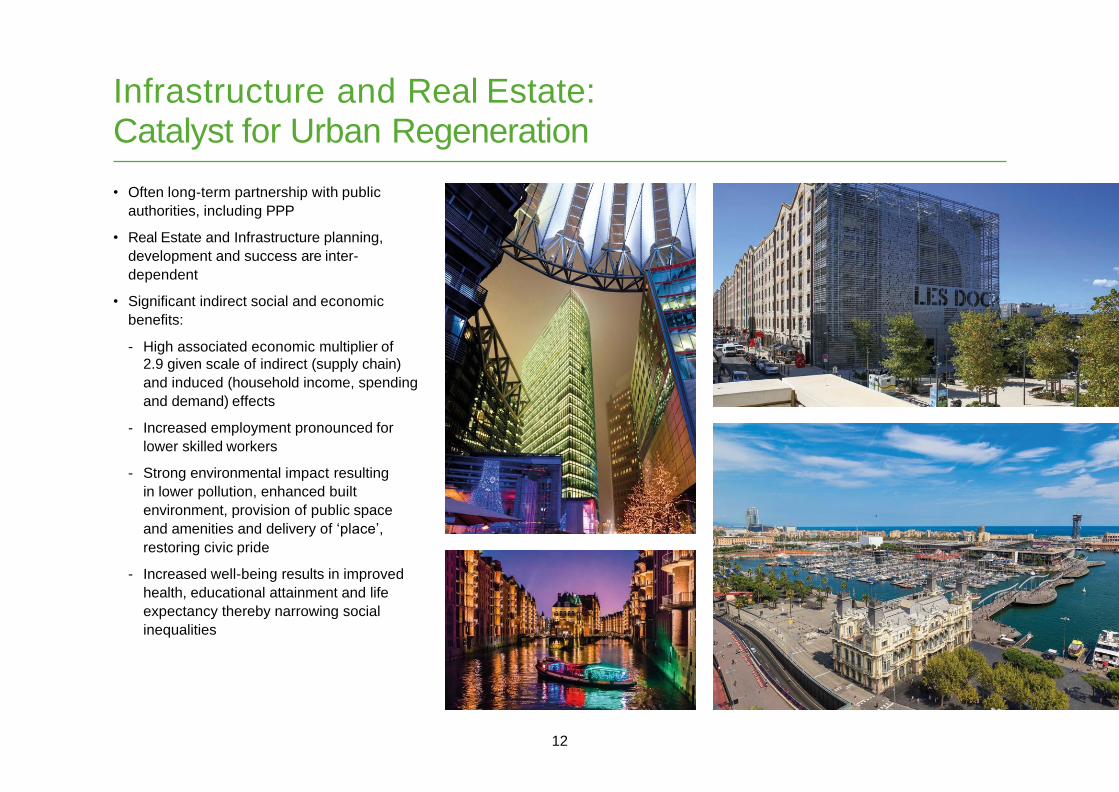

Infrastructure and Real Estate:Catalyst for Urban Regeneration

• Often long-term partnership with public

authorities, including PPP

• Real Estate and Infrastructure planning,

development and success are inter-

dependent

• Significant indirect social and economic

benefits:

- High associated economic multiplier of

2.9 given scale of indirect (supply chain)

and induced (household income, spending

and demand) effects

- Increased employment pronounced for

lower skilled workers

- Strong environmental impact resulting

in lower pollution, enhanced built

environment, provision of public space

and amenities and delivery of ‘place’,

restoring civic pride

- Increased well-being results in improved

health, educational attainment and life

expectancy thereby narrowing social

inequalities

12

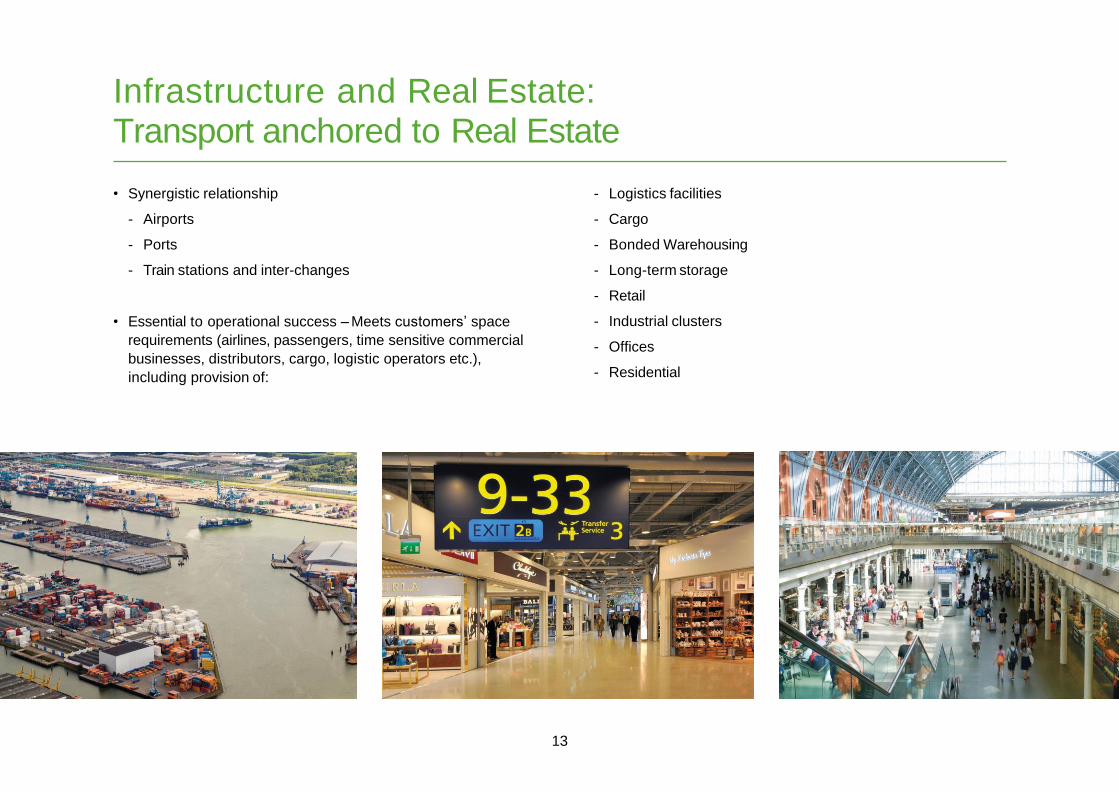

Infrastructure and Real Estate:Transport anchored to Real Estate

• Synergistic relationship

- Airports

- Ports

- Train stations and inter-changes

• Essential to operational success – Meets customers’ space

requirements (airlines, passengers, time sensitive commercial

businesses, distributors, cargo, logistic operators etc.),

including provision of:

- Logistics facilities

- Cargo

- Bonded Warehousing

- Long-term storage

- Retail

- Industrial clusters

- Offices

- Residential

13

Infrastructure and Real Estate: Real Estate supports financial viability of many transport projects

• Revenues from transport operators

(airlines, shipping, trains) are often

controlled or capped

• Revenues from commercial real

estate development and management

offer higher returns and rental growth

potential

- Bond income + growth often

required to attract institutional

investment in order to:

- Generate required risk adjusted

return relative to other investments

- Deliver returns for pensioners and

savers

Source: John D. Kasarda and Taoyuan Aerotropolis

14

Infrastructure and Real Estate:Create solutions to meet structural and cyclical challenges

• Real estate industry responds to ever changing demands of

business and society, financing solutions in face of constraints on

public finances

• Examples of the industries’ ability to continually innovate are

widespread and integral to building design, new sectors and

segments, as well as re-conceiving / re-purposing established

sectors. Illustrations of these include:

Building Design:

Businesses are continually under pressure to improve

productivity and since the GFC, lowering the cost base has been

the primary focus of achieving such gains given challenges to

revenue growth. Many companies have achieved this through

greater efficiencies in their occupational portfolio, enabled

by advances in the (re-)design and (re-)construction of office

space that has delivered greater space efficiency, higher

functionality and reduced energy costs resulting in a lower

cost of occupation per employee. It also greatly lowers the

environmental cost. Yet, such advances also benefit savers and

pensioners as such buildings command higher rents, and being

in greater demand, at a lower risk given the greater security of

income.

15

Infrastructure and Real Estate:Create solutions to meet structural and cyclical challenges

New Sectors:

Megatrends such as ageing society create new demands

for senior housing and / or healthcare facilities that have

also increased demands on public finances in an era of

constraint. The CRE sector has responded through the private

funding of new solutions in the form of both senior housing

developments and senior care facilities, leased to specialist

operators.

Similarly, expanding university places and increased use of

university facilities for conferences/ exhibitions increased the

quantity and quality of student housing needed. Meeting the

needs of institutional investors demands for long-term secure

income, the CRE sector has invested in the sector, providing

a solution that meets the accommodation requirement and

eased the pressure on university finances.

Technological advances pervade all aspects of real estate

including changing occupier needs, increased mobility of

workers, the demands of a shift towards omni-channel retail

and related new customer services and revenue streams, high

tech distribution facilities and the expansion of third-party

logistics providers. The latter involves changing requirements

for major distribution hubs through to the more emergent need

for local fulfillment centres. The shift towards a technology

enabled world creates a direct need for specialist real estate to

house related facilities, for example, data centres.

16

Responding to Structural

Change:

Demographic, economic, technological and

environmental megatrends create waves of

change that create societal and behavioural

change in how we live, work and play. CRE

investors continually adapt their real estate

holdings in all sectors to respond to such

change.

The design of office space has evolved

from a cellular office and central admin

pool model to accommodation that is more

tailored from the outset to activity based

workspaces that can accommodate

multiple working modes. Moreover, the role

of the accommodation in attracting and

retaining talent is central to its purpose,

resulting in mixed use developments that

co-locate retail, leisure and residential

amenities and at the same time, build

social activity.

Social and technological change is

transforming the retail sector from being

a mere point of sale to a sector driven on

delivering experience and a sense of place,

community and belonging. Retail spaces

are transforming into people places,

increasingly anchored by social space and

services, where real and virtual worlds

collide to enhance consumers’ knowledge,

choice and experience.

17

Real Assets: Investment Structure

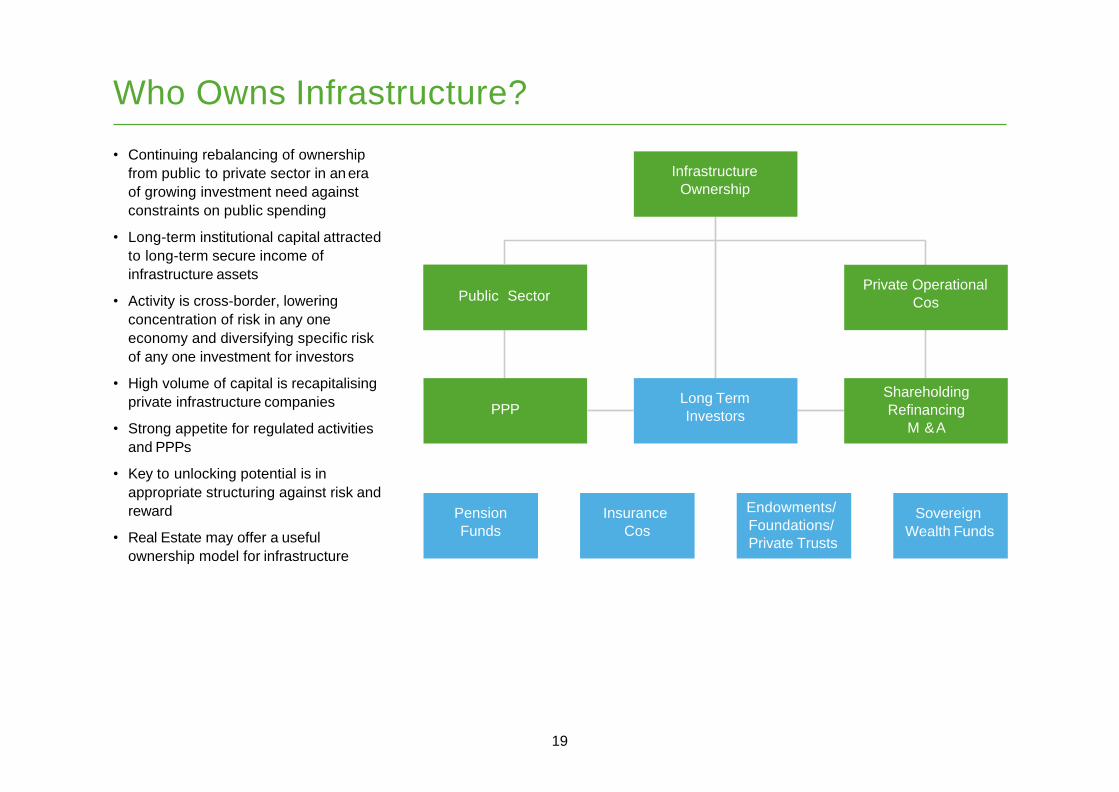

Who Owns Infrastructure?

• Continuing rebalancing of ownership

from public to private sector in an era

of growing investment need against

constraints on public spending

• Long-term institutional capital attracted

to long-term secure income of

infrastructure assets

• Activity is cross-border, lowering

concentration of risk in any one

economy and diversifying specific risk

of any one investment for investors

• High volume of capital is recapitalising

private infrastructure companies

• Strong appetite for regulated activities

and PPPs

• Key to unlocking potential is in

appropriate structuring against risk and

reward

• Real Estate may offer a useful

ownership model for infrastructure

Infrastructure

Ownership

Public SectorPrivate Operational

Cos

19

Long Term

Investors

Shareholding

Refinancing

M &A

PPP

Pension

Funds

Sovereign

Wealth Funds

Endowments/

Foundations/

Private Trusts

Insurance

Cos

Who owns Commercial Real Estate?

Real Estate

Ownership

20

Owner Occupiers (60%)Long Term

Investors (40%)

Government

Manufacturers/

Specialist

Plants

Major

CorporationsInstitutions

EU Prop

Cos/ REITS

Pension

Funds

Insurance

Cos

Sovereign

Wealth Funds

Endowments/

Foundations/

Private Trusts

HNWIs

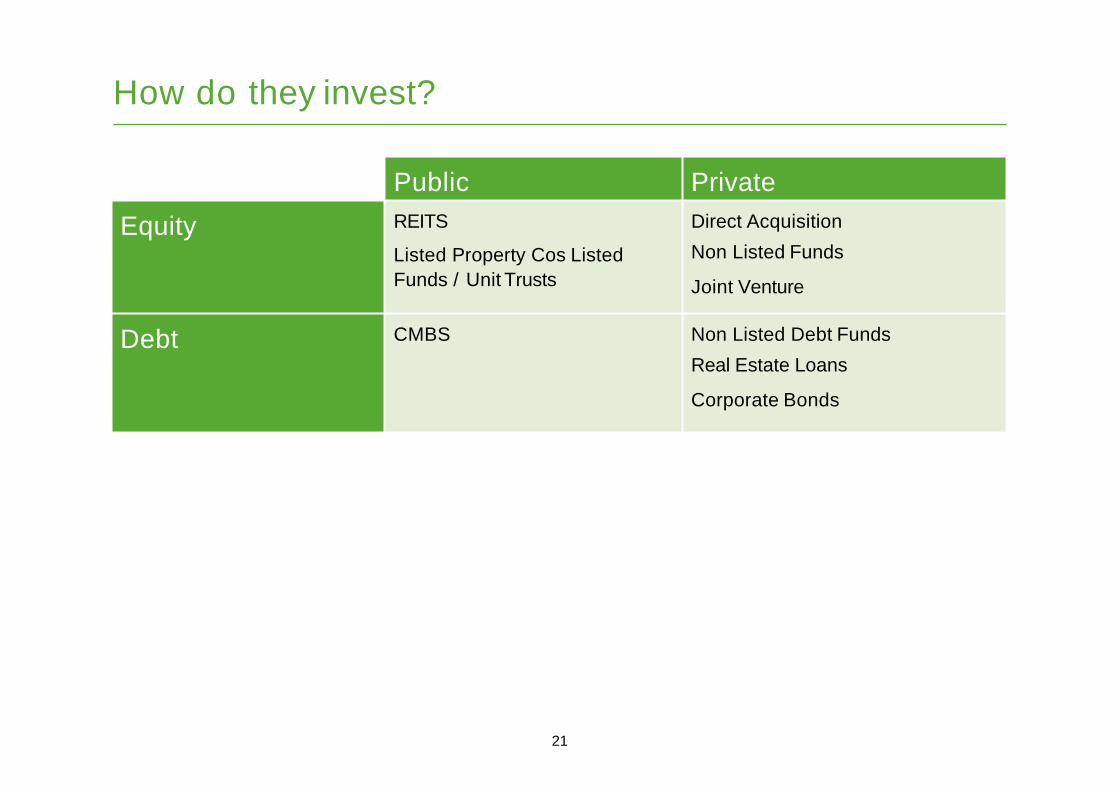

How do they invest?

21

Public Private

Equity REITS

Listed Property Cos Listed

Funds / Unit Trusts

Direct Acquisition

Non Listed Funds

Joint Venture

Debt CMBS Non Listed Debt Funds

Real Estate Loans

Corporate Bonds

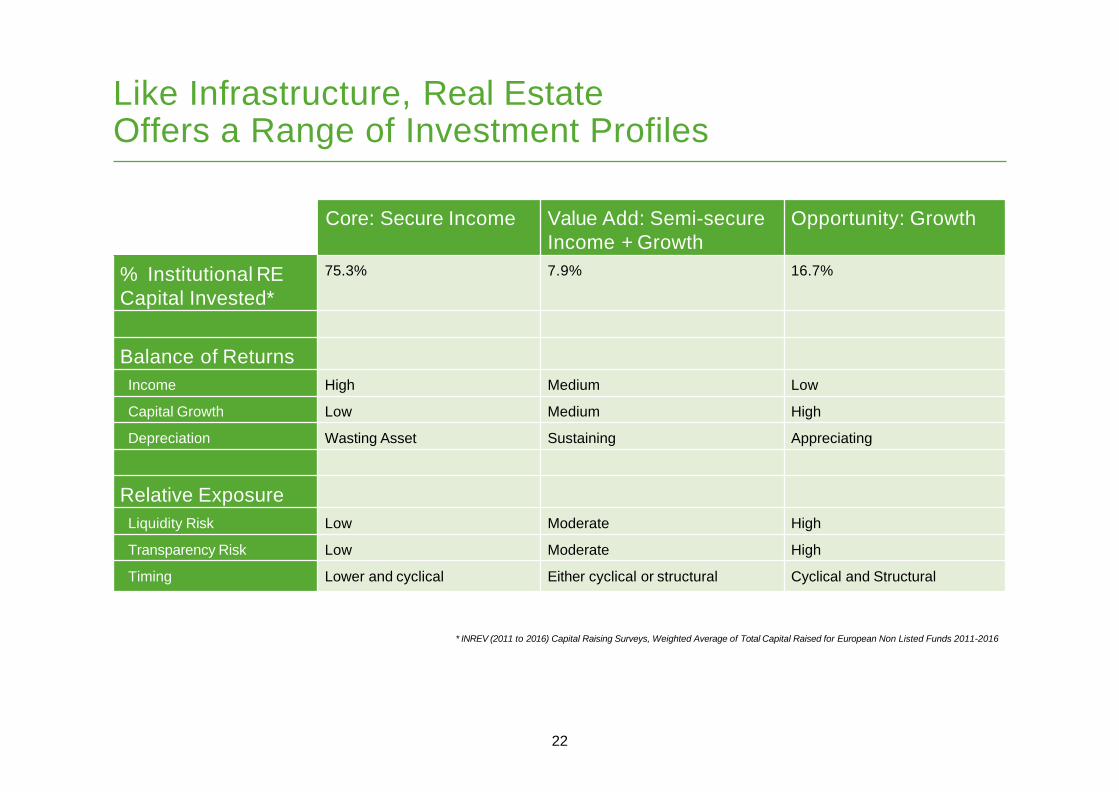

Like Infrastructure, Real Estate Offers a Range of Investment Profiles

22

Core: Secure Income Value Add: Semi-secure

Income + Growth

Opportunity: Growth

% Institutional RE

Capital Invested*

75.3% 7.9% 16.7%

Balance of Returns

Income High Medium Low

Capital Growth Low Medium High

Depreciation Wasting Asset Sustaining Appreciating

Relative Exposure

Liquidity Risk Low Moderate High

Transparency Risk Low Moderate High

Timing Lower and cyclical Either cyclical or structural Cyclical and Structural

* INREV (2011 to 2016) Capital Raising Surveys, Weighted Average of Total Capital Raised for European Non Listed Funds 2011-2016

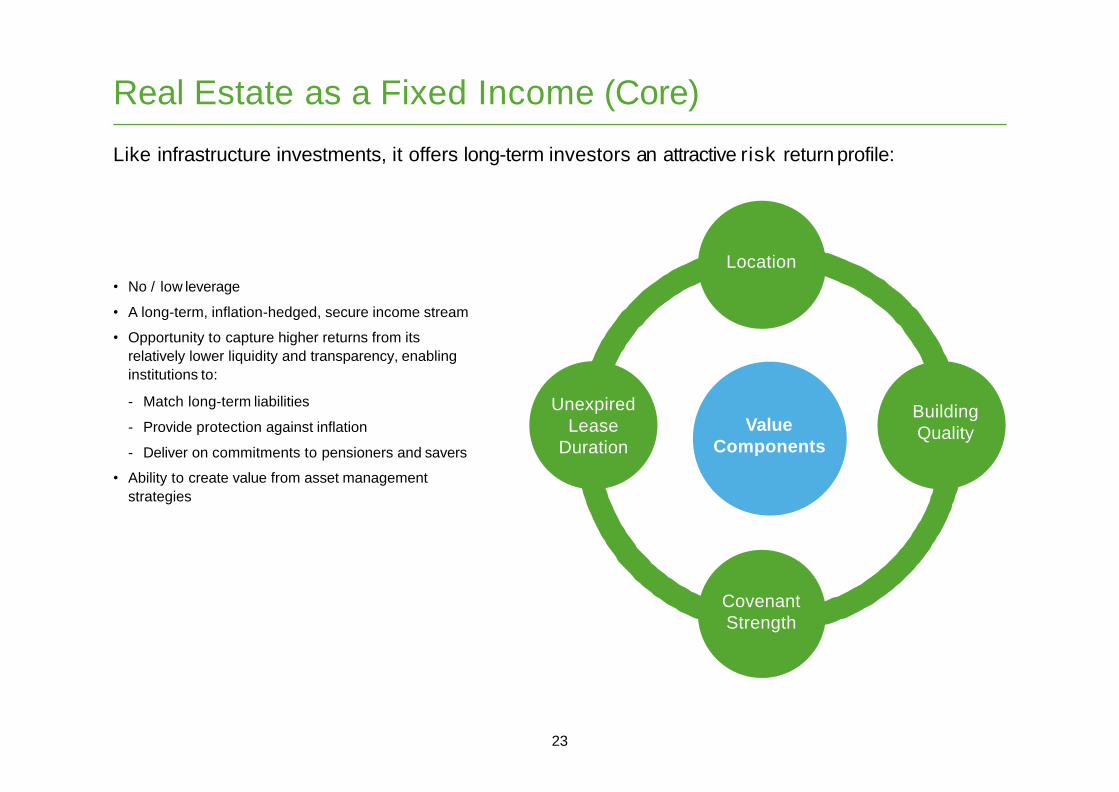

Real Estate as a Fixed Income (Core)

Like infrastructure investments, it offers long-term investors an attractive risk return profile:

Location

23

Value

Components

Covenant

Strength

Building

Quality

Unexpired

Lease

Duration

• No / low leverage

• A long-term, inflation-hedged, secure income stream

• Opportunity to capture higher returns from its

relatively lower liquidity and transparency, enabling

institutions to:

- Match long-term liabilities

- Provide protection against inflation

- Deliver on commitments to pensioners and savers

• Ability to create value from asset management

strategies

19

Like infrastructure investments, it offers long-term investors an attractive risk return profile:

• Purchase of a quality asset at a discounted price due to a

weakness impacting on the certainty of income

• Retain safety net of moderately riskier asset, but compensated

by a higher yielding income stream

• Remedy through active asset management to increase and / or

secure income stream, for example:

- Rolling refurbishment programme and re-leasing strategy

(increase value of space, stronger covenants, longer terms)

- Refurbishment / redevelopment / extension of asset to

increase space and building efficiency (increase lettable

space and value of space, stronger covenants, longer leases)

- Requires moderate levels of leverage

• Capacity to capitalise on expertise and create added value

from asset management strategies

Real Estate as Fixed Income + Growth (Value Add)

Real Estate as Growth (Opportunity)

Professional fees

(architect, engineers,

planning) Site Clearance

Acquisition Price,

Professional Fees

Building Costs,

Marketing,

Professional Fees

Income (rent or sale)

Less Agency Fees

and Finance costsSale & Profit

Is similar to infrastructure investments that carry construction, development or operational risk:

• Purchase of an under-utilised asset

for redevelopment, repositioning or

repurposing to meet existing demand

• Pre-leasing can reduce risk

• Development component necessitates

high leverage

• Can generate high returns

• Remedies obsolescence and spiral of

urban decay

• Generates strongest externalities for wider

economy and society

• Activity creates core investments

characterised by stabilized longer-term

income streams

25

The Life-Cycle of Infrastructure and Real Estate: Depreciating assets need re-investment to maintain value and reverse obsolescence

EquityPurchase of residual value and

opportunity for value creation of new

income secure asset

Focus on short-term growth creation

through exploitation of temporal & cyclical

market dislocations at sacrifice of existing

income. Creation of institutionally

attractive investmentPurchase of shorter-term income stream of

depreciating asset, opportunity to extend

and enhance dividend through tenant

engineering, re-configuration or

refurbishment, thereby restoring asset value

Focus on rebuilding and increasing

income streams of mis-priced asset using

counter-cyclical strategies to enhance

income and thereby generates value

growth in re-creation of institutional

investment

BondPurchase of long-term income stream of

depreciating asset. Residual value in land

Focus on purchase of long-term income

stream with asset value depreciation

Capital Growth –Equity

Opportunistic

Value Added

Core

Income –Bond

26

Infrastructure and Real Estate are Vital to Delivering Liveable and Sustainable Cities and Towns

27

Hauke Brede

Chief Risk Officer

European Parliament

23 November 2017

29

Recycling insurance premiums into investments as

basis for our activities

Allianz Real Estate is Allianz’s captive asset & investment manager in RE space

AGI / PIMCO(Stocks & Bonds)

Allianz Real Estate(Real Estate Equity and Debt)

Allianz Capital Partners(Infrastructure, Renewables,

P/E Fund investments)

1) Based on relative investment assets value at Allianz

Life/

Health1

(80%)

Property

Casualty1

(20%)

Premiums

Annuities

Claims

AIM

(Asset

Allocation)

Cash

Cash

Investment

Managers

Bonds

Stocks

RE

Other

Investment performance

Investment performance

30

New Transactions 2017

Direct Equity European Debt

Indirect Equity U.S. Debt

Vertigo

CXP

Porta Nuova Eni

Liffey Valley Project Waou

55 Baker Street

Project Rainbow II Redwood

Project Grand Combination

1111 Lincoln

Road

Northpoint

Market

Center

Rowan A3

East 26th

Street

PGGM´s Investments in Real Estate &Infrastructure

Invest Week

Brussels, November 23, 2017

Hans Op ´t VeldHead of Listed Real Estate

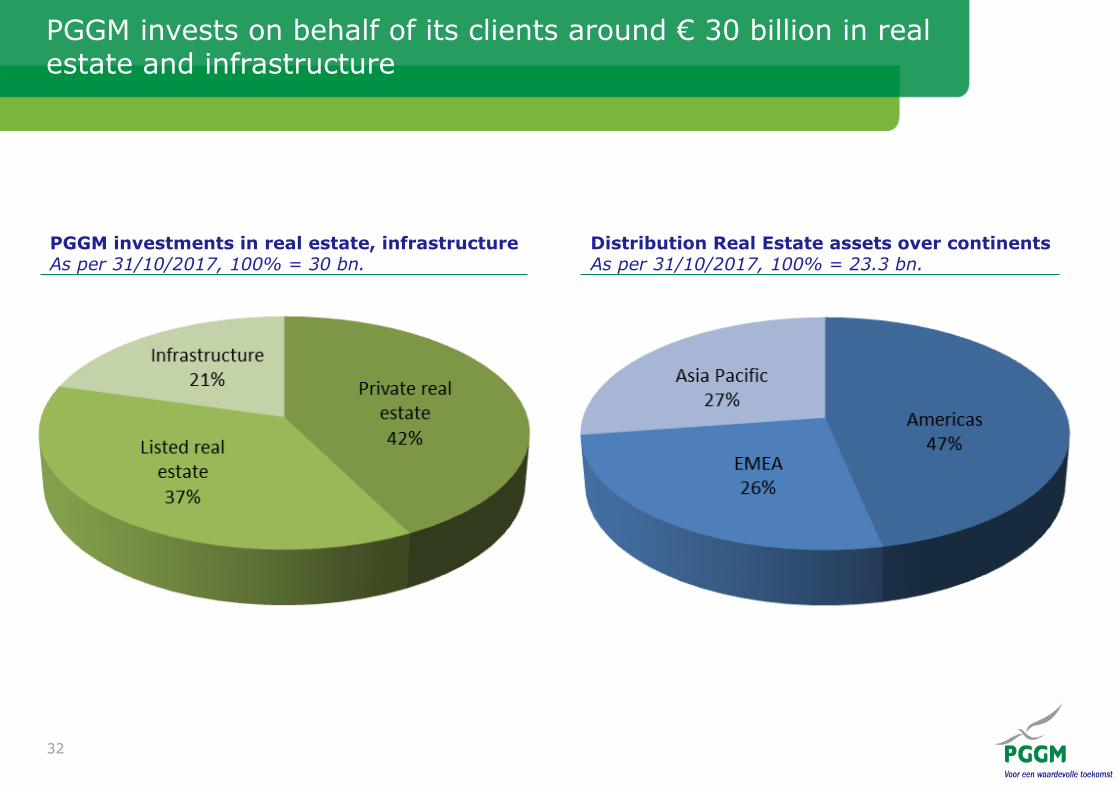

PGGM invests on behalf of its clients around € 30 billion in real estate and infrastructure

32

PGGM investments in real estate, infrastructureAs per 31/10/2017, 100% = 30 bn.

Distribution Real Estate assets over continentsAs per 31/10/2017, 100% = 23.3 bn.

PGGM has a long term approach and directs capital at societalthemes

• Pension plans are uniquely positioned to provide long-term private capital into key

economic challenges:

• Energy transition

• Infrastructure requirements

• Challenges of an ageing population

• Real assets are key categories to deliver change as they directly impact these

challenges:

• Future proofing real estate

• Offering solutions in housing (both regular as senior housing)

• Developing and securing electricty grids

33

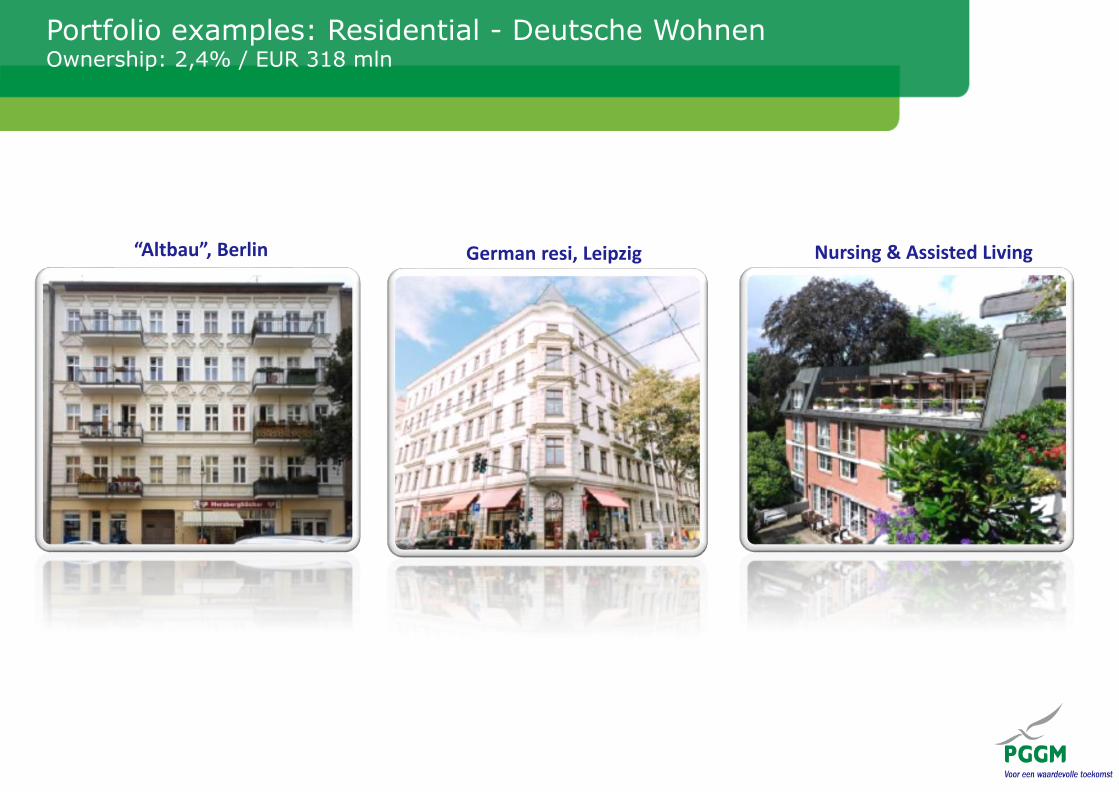

Portfolio examples: Residential - Deutsche WohnenOwnership: 2,4% / EUR 318 mln

“Altbau”, Berlin German resi, Leipzig Nursing & Assisted Living

Prerequisites to grow European pension plan investment are homogeneity, visibility on policy and consistent treatment

35

• Standardization is needed both in legislation. Industry

standards can be highly efficient to achieve this goal.

• Long term stable policy is needed with clear ambitions on

sustainable finance, both by EU and member states

• Treatment of assets should be less dependent on

implementation form. Use direct, listed and non-listed

solutions to privately fund investments in order to ‘Fire on

all Cylinders’

1. Homogeneity

2. Visibility

3. Consistency

Prerequisite Explanation

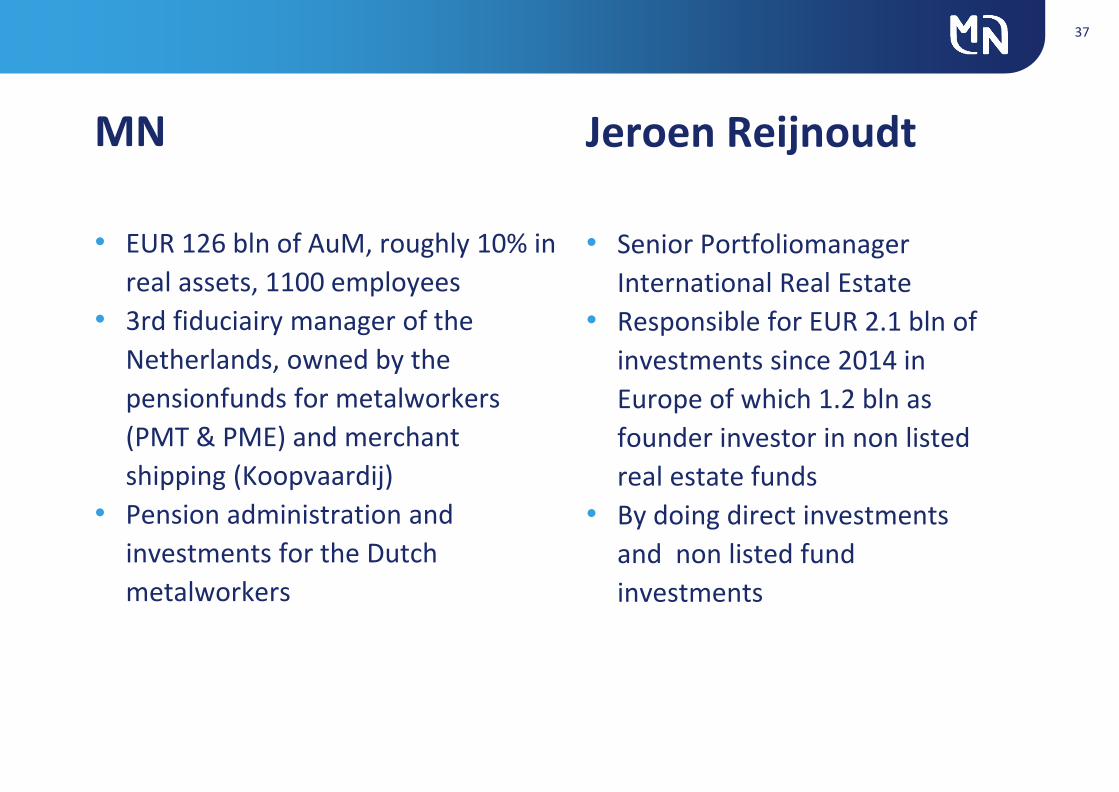

MN

activities in European Real Estate &

Infrastructure

Jeroen Reijnoudt MSC MRE MRICS

23 november 2017

MN

• EUR 126 bln of AuM, roughly 10% in

real assets, 1100 employees

• 3rd fiduciairy manager of the

Netherlands, owned by the

pensionfunds for metalworkers

(PMT & PME) and merchant

shipping (Koopvaardij)

• Pension administration and

investments for the Dutch

metalworkers

37

Jeroen Reijnoudt

• Senior Portfoliomanager

International Real Estate

• Responsible for EUR 2.1 bln of

investments since 2014 in

Europe of which 1.2 bln as

founder investor in non listed

real estate funds

• By doing direct investments

and non listed fund

investments

Real Estate• Clients of MN are focused on core real estate in Europe and the

Netherlands specific.

• MN has around EUR 7,5 bln of active mandates for real estate, yearly

roughly 500 mln is invested in European real estate.

• We have a preference for direct investments in the Netherlands and non

listed funds in Europe.

Infrastructure• Clients of MN are keen to invest in infrastructure as it fits their long term

objectives. There is a special focus on investing in renewable energy

related infrastructure to enable Energy Transition for the future.

• To enable this MN invests in managers focusing on investments in Wind

energy, Biomass and Solar in Europe. Furthermore, there is a strong

interest in investing in Storage infrastructure

38

Limited Universe core IRE 25 bln euro,

work to be done!

39

• Deutsche AWM European Core

• BNP Paribas Next Estate Income Fund II

• M&G Secured Property Income Fund

• Invesco European Fund

• Cornerstone Social Infrastructure Fund

• Hines Pan European Core Fund

• M&G European long lease real estate

• CBRE Pan European Core Fund

• Aviva La Salle Encore +

• Aberdeen European Balanced Property Fund

• UBS European Core Fund

• Standard Life European Growth Fund

•Cordea Savills UK Income and Growth Fund

• L&G PIF II

• Standard Life Long Lease Property Fund

• Standard Life UK Property Trust

• Standard Life Pooled Pension Fund

•UBS Triton

•Aberdeen Property Fund Norway I IS/AS

•CBRE EIF

•AEW European Logistic Fund

•Goodman European Logistics Fund

•Prologis

•Cordea Savills European Retail Fund

•Tishman Speyer European Core Fund

• Standard Life European Property Growth Fund

•Aberdeen German Residential / Stadt & Wohnen Fund

•Aberdeen Resi Fund Sweden

•Healthcare Property Fund UK

•TIAA Henderson Real Estate UK ShoppingCentre Fund

• Shopping Property Fund 2

• Standard Life UK shopping center trust

• Standard Life UK Shopping Cntre Trust

• Standard Life UK Long Lease Property Fund

•Henderson UK Property Fund

•Henderson UK Shopping Centre Fund• Henderson UK retail Warehouse Fund single

sector single

country

single sector

multiple countries

multiple sector

multiple landen

multiple sector single

country

Recent European real estate initiatives by MN

• Founder capital (300 mln) for CBRE DHC, a Dutch inner cities focused

retail fund, 2017

• Founder capital (300 mln) for TH European Cities Fund, a Pan European

fund focused on growing cities, in offices, logistics and retail 2016

• Founder capital for Barings European Core Fund, a pan European fund

focused on core real estate deals in offices, logistics and retail

• Founder capital in DEAM Europe II (300 mln), a pan European fund

focused on core real estate deals in offices, logistics and retail

• Founder capital in Aberdeen Pan European residential fund (150 mln),

the first Pan European residential fund, 2017

40

41

Residential Senior living

Logistics Student housing

Focus Real Estate 2018 and 2019 by MN

A public long-term investor supporting

urban policies :

The Caisse des Dépôts Group

David Percheron, Permanent Representative to

the EU of Caisse des Depots GroupNovember 23, 2017

43

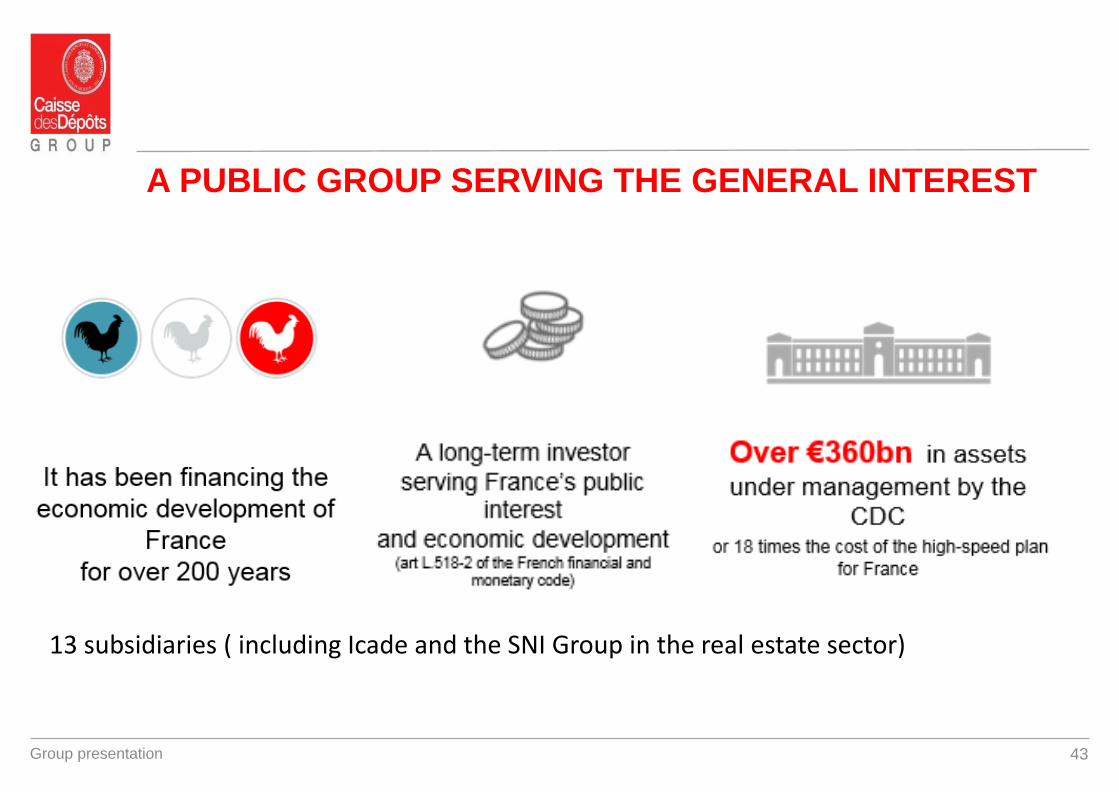

A PUBLIC GROUP SERVING THE GENERAL INTEREST

Group presentation

13 subsidiaries ( including Icade and the SNI Group in the real estate sector)

44

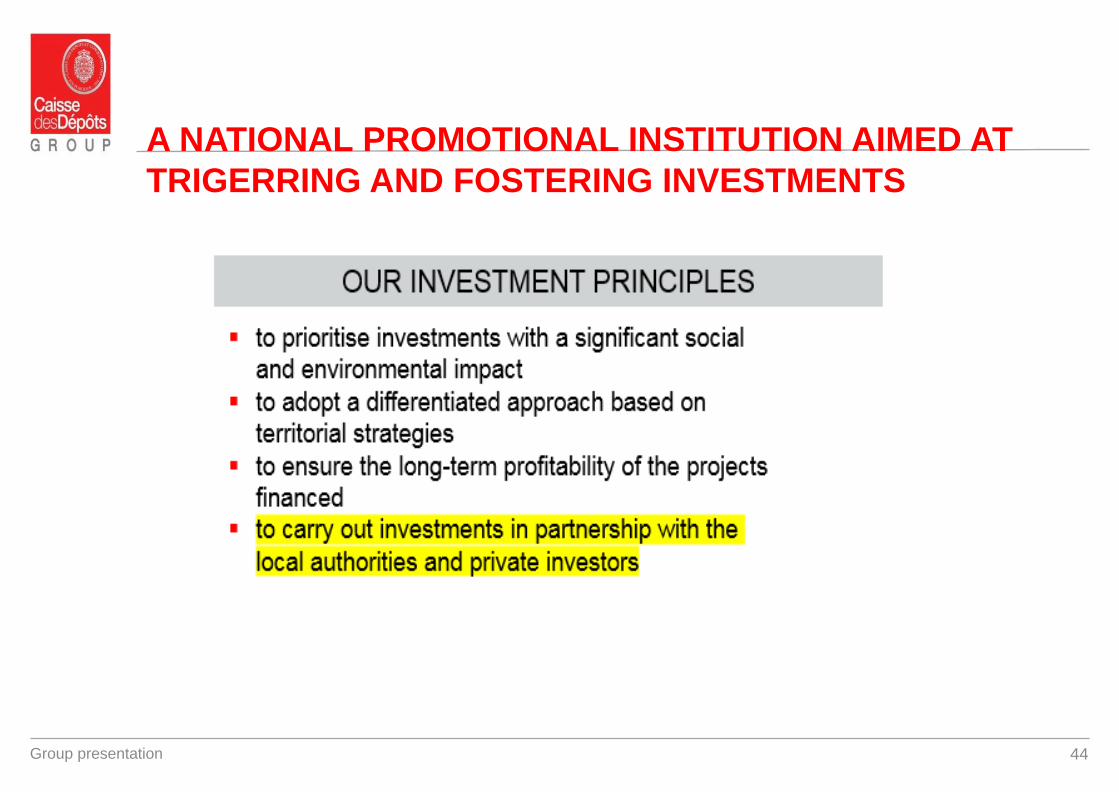

A NATIONAL PROMOTIONAL INSTITUTION AIMED AT

TRIGERRING AND FOSTERING INVESTMENTS

Group presentation

45

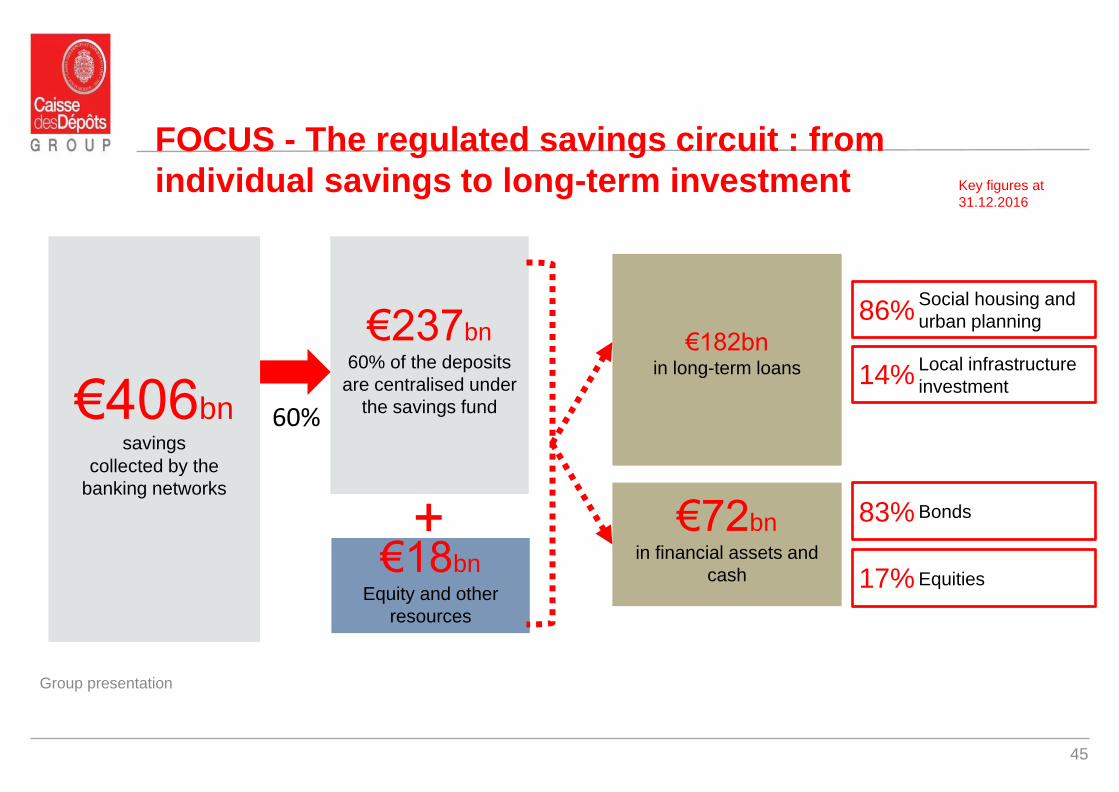

FOCUS - The regulated savings circuit : from

individual savings to long-term investment

Group presentation

Key figures at

31.12.2016

€237bn 60% of the deposits

are centralised under

the savings fund€406bn savings

collected by the

banking networks

€182bn in long-term loans

€72bnin financial assets and

cash

Social housing and

urban planning86%

Local infrastructure

investment14%

Bonds83%

Equities17%€18bn

Equity and other

resources

60%

46

A major contributor in territorial funding and urban

policies

Group presentation

LOCAL PUBLIC SECTOR

€20 billion package,

including €5bn for

green growth loans

at a subsidised rate.

Equal treatment irrespective of

the size

of the local authority

CONTRIBUTION OF THE SAVINGS

FUND TO THE FRENCH ECONOMY

2013-2016: €20bn in loans on average per year

4.2% of all investments carried out in France

each year, or 0.9% of GDP

A counter-cyclical role involving support for

public policies

SOCIAL HOUSING

€14.3bn in loans signed

in 2016

Construction or acquisition

of 109,000 housing units

Renovation

of 310,000 housing units

Thermal renovation

of 40,600 housing units