Embed Size (px)

Citation preview

Information Asymmetry and Managerial Myopia in High-

technology Firms

Name: Ke Wang

Student number: 11826568

Thesis supervisor: Alexandros Sikalidis

Date: June 25, 2018

Word count: 13076

MSc Accountancy & Control, specialization Control

Faculty of Economics and Business, University of Amsterdam

2

Statement of Originality

This document is written by student Ke Wang who declares to take full responsibility for the

contents of this document.

I declare that the text and the work presented in this document is original and that no sources

other than those mentioned in the text and its references have been used in creating it.

The Faculty of Economics and Business is responsible solely for the supervision of completion

of the work, not for the contents.

3

Abstract

This study examines the association between information asymmetry and managerial myopia

in the background of high-technology firms. Using U.S. firms reporting over the period 2010–

2016, I provide evidence that increased managerial myopia in capital investment is associated

with the growing information asymmetry between investors and managers. In particular, a

positive association is found at the higher level of trading volume, and a negative association

is found at the higher level of stock return volatility and bid-ask spread. These findings suggest

that managers can mitigate myopic behaviors by increasing information transparency.

4

Contents

1 Introduction .......................................................................................................................................... 5

2 Literature review ................................................................................................................................. 8

2.1 Information asymmetry and investor sentiment ................................................................... 8

2.2 Investor sentiment and stock price ........................................................................................ 11

2.3 Concerned manager and managerial myopia ...................................................................... 13

2.3.1 Concerned Managers .......................................................................................... 14

2.3.2 Managerial myopia ............................................................................................. 18

2.3.3 The relationship between concerned manager and managerial myopia ............. 22

2.4 Testable hypothesis in high-technology firms setting ....................................................... 22

2.4.1 Testable hypothesis ............................................................................................. 23

3 Research design ................................................................................................................................ 25

3.1 Measuring information asymmetry ....................................................................................... 25

3.2 Measuring managerial myopia ............................................................................................... 25

3.3 Control variables ........................................................................................................................ 26

3.4 Model ............................................................................................................................................ 27

3.5 Sample selection ........................................................................................................................ 27

4 Results ................................................................................................................................................. 29

4.1 Descriptive statistics ................................................................................................................. 29

4.2 Regression results ...................................................................................................................... 29

5 Summary and conclusion ................................................................................................................ 33

References ................................................................................................................................................... 35

5

1 Introduction

The threat of myopic decisions on corporate performance has attracted significant attention for

more than 30 years, with much discussion focusing on whether it destroys firm’s value.

(Graham et al. 2005; Bhojraj and Libby 2005; Marginson and Mcaulay 2008). Myopic

problems occur when executives have the opportunity to make short-term decisions that benefit

current corporate performance but at the expense of long-term revenue (Antia et al. 2010). In

2013, BlackRock, the Canada Pension Plan Investment Board (CPPIB) and McKinsey &

Company came together to create the Focusing Capital on the Long Term initiative with the

aim of conducting research on long-termism and developing practical tools and solutions.

Unfortunately, according to a recent survey, they found that the pressure on companies to focus

more on long-term objectives is not decreasing. Similarly, another survey shows that although

the share S&P 500 companies spent on buybacks is 58% higher, nearly 30 times than the share

in 1981, investments in fixed assets keep low all the time, which, in a sense, short-termism is

increasing. McKinsey Global Institute has also investigated in this area. The recent surveys of

C-level executives and board members show that respondents are under more short-term

pressure in the last five years. Some companies even admitted that they are using excessively

short-term strategic planning. Unlike the result of survey 2013, more of them focused on the

result within two years or less. It is a time to reexplore how managerial myopia happens and

how to keep the balance between short-term accountability and long-term value creation.

Additionally, McKinsey report 2015 has shown that profits have increasingly migrated to idea-

intensive industries. The findings of the report also suggest that idea-intensive industries are

the most long-term oriented on an industry level, especially compared with capital-intensive

industries. It is worthy to note that long-term investment, like R&D investments, is one of the

most important strategies that the managers in high-technology firms must take into

consideration (Greve 1998), indicating that myopic behaviors can cause more serious damages

to high-technology sectors than other industries, as their profits mainly depend on long-term

investment. I choose the setting of high-technology firms, mainly for providing some

implications for the sector and its executive managers.

Although myopia is an important element in many theories, prior research provides limited

evidence regarding the role of information asymmetry in managerial myopia. On the one hand,

there are some difficulties in measuring the phenomenon, which does not correspond to any

single quantifiable metric and is a confluence of many complex factors. Thus, empirically

identifying the effect of information asymmetry on myopia is a challenging task. One the other

6

hand, many types of researches only examine some apparent factors that lead to managerial

myopia, rather than get into deeply into the bottom.

Based on supported literatures, I found that there is a reasoning link from information

asymmetry to managerial myopia. First, information asymmetry between investors and

managers might lead to negative investor sentiment, as investors can’t distinguish long-term

investments that don’t benefit in the short-term from the misbehavior of management. Second,

the stock price fluctuates positively and immediately with investor sentiment by future cash

flow, selling signal, risk exposure, etc. As a result, negative sentiment tends to cause lower

stock price. Third, it is possible that managers who are concerned about stock price would

manipulate myopic investment to meet short-term objectives.

Using a sample of 307 high-technology companies from 2010 to 2016, I have tested the

hypothesis that the information asymmetry is positively related to managerial myopia in high-

technology firms and the result supported predicted the positive association. I distinguish

capital investment from R&D investment, to investigate different effects of asymmetric

information on them. The results indicate that the predicted relations between information

asymmetry and capital investments are observed. But there is a contradiction in the result of

R&D without control variables, and I found that frequent information disclosure sometimes

encourages managers to focus on short-term earnings, which increases managerial myopia.

My paper makes two contributions to extant literature and practice. First, I contribute to the

literature on innovation, especially towards high-technology firms. Unlike prior studies, the

sample of my study consists of firms in the high-technology sector. High-technology firms are

particularly relevant for examining effects on myopia, because, as I introduced, their survival

and performance heavily depend on the capability to effectively set long-term strategies and

planning. They play a significant role in economic development of any country, as the profit

center has moved from capability-intensive industry to ideal-intensive industry. Practically, my

results can help controller in high-technology groups determine whether there is a strong level

of information asymmetry and try to mitigate and cure myopic problem.

Second, it contributes to the literature by extending the research into the depth about the factors

that have effects on managerial myopia. Extant literatures focus on how institutional investors

play the role of the decision-making process of myopic behaviours. For example, the results

reported by (Bushee 1998) indicate that when the institutional ownership is high, managers are

less likely to cut R&D investment to reverse an earnings decline. Prior research also documents

7

that the evidence of CEOs’ job changes, such as retirement of CEOs in the form of reductions

in R&D expenditures (Dechow and Sloan 1991; Lundstrum 2002; Barker and Mueller 2002),

potentially earning declines and loss (Habib and Hansen 2008), impending acquisitions that

have higher returns but lower post-merger long-term stock performance (Gao 2010), and

earning management to increase pension contributions (Kalyta 2009), also cause short-horizon

decisions. Some observers also comment that control systems and frequent reporting tend to

cause an excessive short-term orientation and stimulate manipulation (Thurow 1981; Schlender

1982; Arthur et al. 2018). But I find that information asymmetry is one of the underlying

reasons of depth, suggesting that researchers and practitioners should consider causes rather

than effortlessly solve superficial phenomena. In general, my paper adds to extant literatures

in the research of myopia management.

The paper is structured as follows: Section 2 develops hypotheses on the association between

information asymmetry and managerial myopia. Section 3 describes the research design, while

Section 4 reports the main results. Section 5 summarizes and concludes this paper.

8

2 Literature review

I rely on past research, both theory and evidence, to prove that my hypothesis regarding the

implications of asymmetric information for managers within companies. My focus is on the

relation between asymmetric information and managerial myopia. This relation depends on

three links, as illustrated in figure 1.

I will explain each link in turn.

Figure 1: Linking information asymmetry with managerial myopia

2.1 Information asymmetry and investor sentiment

In agency theory (Jensen and Meckling 1976), if both parties to any relationship are profit

maximizers, it is reasonable that the agent will not always behave to align with the best interests

and desires of the principal. And one of the consequences is asymmetric information.

Information asymmetry, as known as information failure, represents the difference between

one party’s information and another party’s information about the same thing. The more

available information is what called private information.

Asymmetric information can come in two possible ways, depending on the information known

when taking the decision. Ex ante is related to adverse selection and ex post to moral hazard.

Some studies use adverse selectin cost to prove the existence of information asymmetry (Chen

et al., 2003). In the corporate studies, there are two types of information asymmetry, one

between top management and divisional managers, another between internal managers and

external investors. The knowledge is dispersed across different levels and divisions within a

company. Top managers have a clearer overall view of business strategy, while divisional

managers, who execute the strategy or plan in their positions, have more detailed and specific

knowledge or information, such as operational management and competitive advantages (Chen

et al., 2017). Compared with information to assess a company used by external investors,

internal managers are easier to get more information to make decisions. For example, managers

have an incentive to issue equity when the firm is overvalued.

Information asymmetry has been proved to have affects on a lot of aspects, especially in stock

market performance and corporate governance. Lowry (2001) uses the cost of adverse selection

Information Asymmetry

Investor Sentiment

Stock PriceManagerial

Myopia

9

as the proxy of information asymmetry to explain why IPO volume fluctuate substantially over

time. Kelly and Ljungqvist (2012) suggest that information asymmetry has a substantial effect

on asset pricing through a liquidity channel. Companies operate in the environments with high

information asymmetry hold smaller cashes (Chung et al. 2015)

In this thesis, I mainly focus on its relationship with managerial behavior, involving outside

investors and stock market. Similarly, tax avoidance, as one of measurements of managerial

myopia, is more aggressive after a reduction in analyst coverage caused by broker closures and

mergers (Tao and Chen 2017). This paper researches on analyst, who care about companies’

tax policies, analyze tax planning, distribute public and private information, and assess the risk

of tax. Therefore, this scrutiny, as information transparency, discourages aggressive tax

avoidance. My thesis links information asymmetry with investor. Uninformed investors are

able to stimulate more myopic behaviors.

Efficient market hypothesis indicates that public available information can be fully reflected

by securities prices (Eugene F. Fama 1970), while some other economists challenged the EMH

with behavioral finance, for the reason that psychological and behavioral elements have

influence on stock prices.

Investor sentiment reflects investors’ willingness, anticipation, opinion, and emotion towards

investment or market as a whole. Investor sentiment surveys have long influence on investors

attitudes over years. There are some irrational individual actions not driven by facts at hands.

For example, despite large April 2000 market losses, investor expectations of future returns did

not significantly fall (Dreman et al. 2001). And many individual investors expected a negative

result with current financial facts and figures.

Stock market and behavioral finance are the most two big and likely effects from investors

sentiment. Before I explore how investor sentiment influence stock price, I should examine the

literature bases provided by behavioral finance area. According to Shefrin (1999), one of the

three behavioral finance topics is inefficient markets, which represent the price or rate of stock

return is contractionary to EMH. It is useful for overconfidence to explain and analyze market

inefficiency. Human beings have the tendency to overestimate their abilities. One the hand,

private information of investors weighted higher than public available information when

making decisions (Barber and Odean, 1999; Daniel, Hirshleifer, and Subrahmanyam 1998;

Chuang and Lee 2006). Thus, investors have biases and could overact towards private

information. On the other hand, private information plays role in an earlier stage and for a

10

longer period. Interestingly, Barberies, Shleifer, and Vishny (1998) find that investors are

indifferent or under-react to the objective accounting information, like earnings announcements,

dividend distribution, and share repurchases in financial statements, but over-react to some

records of extreme performance, such as some big events in bullish market.

Many studies have proved that investor sentiment’s impact on stock market. I will introduce

more related literatures in the next section.

Prior literatures have shown that asymmetric information leads to negative investor sentiment.

When there is information asymmetry between corporate managers and investors about

investment expenditure, it is likely that investors can’t distinguish the investments that only

benefit in the long term from those that will not. The reason is that the amount of investment

is sometimes not directly observed by investors. Clearly, this argument is not applicable to all

situation, i.e. the expenditures on tangible assets, such as plant or equipment, can be easily

identified. However, according to Stein (1989), there are many invisible investment and money

spent on them can’t be obviously recognized from increased operating costs. For example, a

commitment to increase the resources distributed to client coverage for the short term is

expected to generate long-term loyalty benefits. But the costs, as an increase in operating costs,

is averse to the result of profitability. And if investors don’t have reasonable explanation or are

not persuaded convincingly by managers at this time, as a result, investors may attribute the

long-term investment to managerial misbehavior or poor business prospects, which means

negative investor sentiment.

The work of Laffont and Tirole (1987), which pays attention to the design of efficient contracts

of managers to encourage managerial effort, also indicated the relation between information

asymmetry and investor sentiment. They found that if information asymmetry lead to invisible

investment, high-cost investments will be misunderstood as low managerial effort.

Regarding investor sentiment literatures, this argument is also consistent with the expectation

of overconfidence hypothesis. Overconfident investors conduct trades based on the private

information they observe and believe, of which they think is a better option than others. (Odean

1998). With the image of misbehavior or poor management, they are overconfident to make

irrational decisions, influencing the stock return and price of the company.

Then I will show how negative sentiment will influence stock price, and further change myopic

behaviors.

11

2.2 Investor sentiment and stock price

Studies of behavioral finance hold that investors might be irrational to make decisions, driven

by their psychological or cognitive factors. Thus, the stock price is not only influenced by

intrinsic value, such as accounting information, but also by investor sentiment. There are some

interesting observations of investor sentiment. A number of big movements in stock market are

caused by investor sentiment, further raising the attention to this behavioral indicator. And In

early 2001, researchers investigated how investors reacted to the fact that publicly traded stock

values decreased sharply. In the expectation, they would be more conservative and responded

pessimistically. Dreman et al. (2001), however, surprisingly found that there was only little

difference between investor sentiment in 2001 and in prior years.

Existing studies have shown investor sentiment may affect the earning growth, rate of return,

and stock valuation of stock market.

First, investors have positive attitudes toward the stock when they have optimistic sentiment

and analysts tend to distribute the information of high ratings for those stocks, therefore the

prediction of earnings growth can be affected (Cornell et al., 2014). Secondly, the required rate

of return, which equals the product of risk quantity and risk price, is subjective to the effect of

investor sentiment, but in a more complicated way. Although investors may undervalue the

risk disclosure when investors are in high sentiment period, they need higher compensation of

the return for bearing the risks. Thirdly, Wang et al. (2010) implies in the study that investor

behaviors are also able to influence the stock valuation. For example, De Long et al. (1990)

found that the stock price is determined by the combination of rational intrinsic value and

irrational noise trader risk, which can be caused by the irrational and intuitive investors. And

two other studies have investigated further.

Investor sentiment can affect stock price in these several aspects.

Certain studies (Hribar and McInnis 2012; Cornell et al. 2014) found that when investor

sentiment is high, analysts have positive attitudes towards the future profitability. Thus, they

are potential to distribute more buying signals. Brown and Cliff (2004) indicate that high

sentiment may alter the investors' expectation of future cash flows and thus affect prices.

Investors may have incorrect subjective beliefs or the so-called private information to value

stock. Furthermore, Baker and Wurgler (2007) argue that sentiment could also affect stock

price by altering the anticipated risk exposure of investors, and Shefrin (2008) constructs an

SDF (Stochastic Discount Factor) based on the sentiment and link the required rate of return to

12

investor sentiment. In addition, Baker and Wurgler (2006) discover certain cross-sectional

differences of the sentiment effect; they find that investor sentiment provides more evident

impact on stocks that are difficult to value or risky and costly to arbitrage. They define investor

sentiment as the propensity to speculate, and the key predictions come from two parts. When

arbitrage is equally across through the firm, sentiment-baes stock demands also differ across

through the firm; when sentiment increases, the investor sentiment is defined as a higher

demand of speculative stocks. Stambaugh et al. (2012) detect an asymmetric effect of investor

sentiment, i.e., the optimistic sentiment always leads to overpricing, which is greater than the

underpricing resulting from pessimism. And investor sentiment represents the overall

optimistic and pessimistic perception toward the stock market. Similarly, investor sentiment is

identified as the behavior of noise traders (Lee et al., 1991).

Furthermore, some studies have also examined that the fluctuation and the reaction of stock

price. Li (2015) has shown that sentiment stock lead to not only much larger fluctuations of

stock prices, but also more immediate response. When investor sentiment has effect on stock

price, its responses are more drastic in the stock market downturn than in the stock market

expansion. Similarly, this effect last longer in bull market than bear market. Additionally,

different direction and stock prices under the two market states can be caused by the same

stimulating factors. Unlike other indicators that influence stock price, there is no lag but

immediate effect for the responses of stock.

Rajan and Servaes (1997; 2003), Lowry (2001), and Lee et al. (1991), conclude that sentiment

hypothesis could also explain why IPO volume and price fluctuate so much over time. In some

periods, investors are excessively optimistic and are willing to bear for the value higher than

that it is worthy. Therefore, corporations are encouraged by this behavior and can’t wait to go

public. Contrarily, investors my underestimate company’s value in low sentiment and IPO

volume is also very low. There are some literatures that support his finding. When the IPO

price is overvalued, the stock price in the first day would be very high but keep low constantly

for the next five years, because investor sentiment’s influence can be consistent with the stock

price all the time (Purnanandam and Swaminathan 2001). Besides, Jindra’s (2001) results

indicate that it is no wonder that companies are more likely to issue new equities when they

are overvalued.

Then I would like to introduce some literatures who regard investor sentiment as a strong

forecasting model. Baker and Wurgler (2006) suggest that there are clearly identifiable,

important, and regular pattern on individual firms for investor sentiment to forecast the stock

13

market. Although Thorp (2004) notes that the changes of sentiment do not mean the meaningful

relationship between sentiment and stock market, he indeed discovers that abnormal optimistic

or pessimistic sentiment would signal an opposing direction in the next several weeks, driving

the stock prices with irrational emotions. This perspective leads to viewing the investor

sentiment as a contrarian indicator in the specific situations of extremely bullish or bearish

environments

Overall, investor sentiment has an effect on stock price in the following ways. First, with

negative sentiment, investors will have lower prediction of earning growth and stock valuation

and believe the investment will be risker. If they want to bear the higher risk caused, higher

compensation or the rate of return is required, which means companies have to pay more to

investors. Which ever the effect is, companies would suffer loss in the prediction or

compensation. Second, there are a number of ways to lower stock price by investor sentiment.

Lower future cash flow, selling signal, and more risk exposure are all the consequence of

negative sentiment. Even though we know that some investors’ behaviors are irrational, some

researchers also conclude that the stock price is determined by intrinsic value and investor

attitudes jointly. In addition, stock market can fluctuate with sentiment, and, compared with

other factors, there is an immediate effect without lagging feature.

As I deduce in the last section, higher information asymmetry might lead to negative investor

sentiment. Now I can conclude that negative sentiment can stimulate lower stock price, either

in prediction or in practice. Therefore, asymmetric information between investors and

managers is likely to induce lower stock price, which is definitely not the result that managers

who concerned stock price want to see.

In the next section, I will introduce how managers who concerned the stock price might

implement myopic strategies, reducing the whole value of the company.

2.3 Concerned manager and managerial myopia

Agency theory addresses problems that arise due to differences between the goals or desires

between the principal and agent. The most typical agency relationship occurs between

shareholders and executive managers. For example, managers may sacrifice long-term benefits

of the company to achieve the short-term profitability, as their salaries are not flexible with

long-term incomes. However, even when managers exhibit some concern for stock-prices when

evaluating investments because of reasonable compensation design, they are still reluctant to

undertake long-term-oriented projects to increase the company’s whole value.

14

2.3.1 Concerned Managers

Theoretical and evidence studies argue that lower stock prices may expose managers to the risk

of hostile takeover, lower stock-based compensation, or managers may concerned about the

job dismissal due to poor stock performance caused by their management. Then I will introduce

some relevant literatures in the three areas.

2.3.1.1 Takeover threats

Some researchers, like Jensen and Meckling (1976) and Fama (1980), contend that

management control from outside can improve the efficiency of market and enhance wealth.

They also suggested that, as a useful external governance mechanism, takeover is able to reduce

agency costs by promote disciplined management (Scharfstein 1988; Grossman and Hart 1980).

However, opponents argue that takeovers sometimes damage the firm value because managers

within companies are subject to hostile takeover. In addition, firms are bound to adopt anti-

takeover provisions to mitigate takeover threats and increase the difficulty of hostile takeover.

I think the reason why managers are under substantial takeover threats is that they are likely to

be replaced after acquisition.

First, as a result, managers will manipulate accruals management. One major concern on

takeover threats of managers is that the firm stock would be undervalued for the short-term

(Froot et al. 1992). Consequently, it is possible that managers are induced to rely on a large

variety of ways, like earning management to mitigate and stop takeover. Some literatures have

supported this argument. Managers under takeover pressure exercise accounting discretion to

contest hostile takeover and reduce the threats (DeAngelo 1988). Similarly, Zhao and Chen

(2008) report that there is a negative relationship between the likelihood and level of accrurals

management and staggered boards.

Second, real activities management are potential to be triggered, which is also my focus in this

thesis. Stein (1998) has an extensive research and suggest that managers are willing to cut long-

term investments, like R&D investment to support short-term performance growth. Short-term

investments can offer immediate return while long-term project is less productive and low-

yielding. As a result, the profit of the company is sacrificed. Prior studies also indicate that

managers’ engagement in real activities manipulation is a response to increased capital market

pressure or short-term participated investor (Cohen and Zarowin 2010; Bhojraj and Libby 2005;

Bushee 1998). In short, less-protected from the takeover pressure are likely manipulate real

activities. On contrary, when takeover protection alleviates the pressure and threats, they are

15

less likely to participate in the manipulation. For example, more-protected firms such as

staggered-board firms are associated with lower levels of abnormal real activities used to just

meet near-term earnings targets.

2.3.1.2 Executive compensation

There are also enormous studies about the executive compensation that can also explain why

managers are concerned on short-term stock price.

Executive compensation is a complex and contentious subject. The high level of CEO pay has

encouraged a heated debate about the nature and the outcomes that it produces. Murphy (2012)

and Carola & Dirk (2010) have reported the development history of executive compensation.

Since 1930s, shareholders have begun to have rights to know the details of the compensation

paid to top executives in publicly traded corporations. Following the Securities Act of 1934,

the responsibility for enforcing pay disclosures for top executives in publicly traded

corporations was consolidated into the newly created Securities and Exchange Commission

(SEC). And SEC demanded all companies to disclosure all compensation information

(including salaries, bonuses, stock, and stock options). In 1950s, restricted stock options

became a relatively efficient way to convey after tax compensation to executives, therefore it

was popular from that time. From the mid-1970s to the early 2000s, compensation levels grew

dramatically, differences in pay across managers and firms widened, and equity incentives tied

managers’ wealth closer to firm performance. By far, stock options have become the single

largest component of CEO pay in the 1990s. And the sensitivity of CEO wealth to performance

also surged in the 1990s, mostly due to rapidly growing option portfolios. Lately, average CEO

pay declined from 2000 to 2008, and restricted stock grants have replaced stock options as the

most popular form of equity compensation.

Because more and more corporation separated the ownership from control, the agency problem

between management and shareholders has been a central topic (Berle & Means 1932). Most

research on executive compensation has been firmly rooted in agency problem: compensation

system are designed to align the interests of executives with those of ownership. If managers

are self-interested and can’t be monitored and stopped by companies’ owners, managers are

potential to use the expense of shareholder value to pursue their own benefits and welfare.

Some evidence on studies has supported this argument. Managers pay perquisite compensation

and prestige in daily life with company value, which is highly damaged to the whole company

(Jensen 1986; Jensen & Meckling 1976; Bertrand & Mullainathan 2003; Morck et al. 1990).

16

Some researchers put forward that executive compensation is able to mitigate and even

eliminate agency problems for that it ties managers with the interest of company (Jensen &

Meckling 1976). By effectively granting the executive an ownership stake in the firm, equity-

linked compensation, such as restricted stocks and stock options, creates incentives for them to

take actions that benefit both shareholders and themselves.

There are two hypotheses from academic literatures that explain why executive compensation

is increased: efficient contracting and managerial power (Murphy 2012). Efficient contracting

views that executive compensation can mitigate agency problems between executives and

shareholders to optimize firm value. The level, structure, and component of compensation

represent a competitive equilibrium for managerial talent, to compensate their contribution to

the company. While managerial power hypothesis holds that powerful executives, who have

effect on board committees, determine the level, structure, and component of compensation

rather than the competitive market (Bebchuk & Fried 2004). Some studies regard the two

hypotheses as competing theory, but Murphy (2012) argues that it is not necessary to

distinguish them empirically. Frist, the two hypotheses are not mutually exclusive; on contrary,

mitigating conflicts of interested between managers and shareholders and renting extraction

tend to be achieved simultaneously. Second, if researchers focus on the competition of the two

hypotheses, other important indicators that explain the trends will be ignored.

In summary, when control and ownership is separated, it is possible that principals act to benefit

themselves and destroy shareholders’ value. As executive compensation is able to solve agency

problems owing to either efficient contracting hypothesis or managerial power hypothesis,

managers will be motivated to align with the interest of company. From history, we also know

that both the level and the composition of CEO pay have changed dramatically over time and

stock-based compensation has been a primary way to pay for executives. Therefore, executives

are concerned about stock price if they are tied with stock compensation, because low stock

price not only hurt the future economic revenue of company but also damage their own benefits.

2.3.1.3 Job termination

Except takeover threats and executive compensation, managers also may be concerned on the

job termination due to poor stock performance caused by their management.

Chen et al. (2001) defines job termination as a permanent layoff of employees from a company.

And Freeman & Cameron (1993) contend that downsizing that is a series of activities

17

undertaken and executed by top management to improve organizational efficiency and

competitiveness, reducing the size of labor force.

There are a lot of reasons examined by academic literatures that lead to layoff. One important

source is the relative poor performance to competitors (Hart 1983). This is also confirmed by

Jensen (1993), who describes product market discipline as an instrument to remove the top

management and stop the poor performance. Other external pressures force manager to engage

in downsizing. For example, Gombola and Tsetsekos (1992) find that increase in leverage is a

characteristic of sample firms before the layoff announcements. Since the improvement of

productivity is one of the expected results of employee layoffs (Cascio 1993), it seems

reasonable to assume that job termination is a reaction to poor productivity and operating profit

in companies. Hillier (2007) also find that the frequency of layoffs is increased following

threats to management control.

In this thesis, I pay much attention to layoff pressure and threats caused by the poor stock price

performance. Several studies have backed the relationship and highlighted the important role

of stock price.

Gilson (1990) claims that poor operating and stock price performance has increased the level

of financial distress, further resulting in possibility of employee dismissal. The author creates

a sample of firms from publicly traded companies whose stock price dropped sharply. He

assumes that the list of poor stock performance would incorporates firms that were relatively

in financial distress, i.e. default on debt, bankrupt, or debts restructuring. For the sample of 111

firms, he finds that there is a shift in ownership from incumbent management and the board

committees to blockholders and creditors. Specifically, only 46% and 43% of directors and

CEOs respectively still keep their positions after decreased stock price led by the disclosure of

bankruptcy and debt restructuring. Billger and Hallock (2005) also find strong evidence that

layoffs related with negative stock price are more likely to cause SEO turnover than that related

with positive stock price.

Two different theories can explain why organizations downsize and dismiss employees. One

perspective is psychological contract theory and another one is economic theory (Lumpur

2005). The psychological contract theory views that each party of employees and organization

will fulfill their responsibilities. This relationship, in terms of employee, means that individuals

will meet their commitments to work for the organization and gain profits. (De Meuse et al.

2004). Likewise, organizations are expected to provide a stable and prospective working

18

environment, compensate for employees who perform well, and offer future opportunities in

promotion and trainings. Therefore, employees will perceive that organizations violate their

responsibility to protect a stable employment and environment (Morrison & Robinson 1997),

while organizations fire employees because employees don’t achieve their committed goals or

even damage the firm value.

The other perspective assumes that organization downsize primarily depends on the economic

costs and revenues of layoffs. Executives engage in layoffs to reduce organizational cost and

improve financial performance simultaneously, such as the operating profits. There is a trade-

off analysis between the short-term costs related to layoffs and long-term labour costs. The

reduction in the size of workforce will decrease the labour costs and increase the profitability

(Neinstedt 1989). Companies also need to pay for hiring and training new employees following

layoffs (Atchison 1991). But the view that long-term benefits are higher than the short-term

costs dominate in companies and labour market (Abraham & Kim 1999). Thus, layoffs play a

significant role to encourage employees to work hard, be more responsive to customers’ needs,

improve communication skills, and expedite decision-making process. Moreover, employees

work under the dismissal pressure or they will be fired for low performance, because the benefit

of replacing them exceeds the costs of developing new employees.

Overall, I explain what factors lead to layoffs and why organizations downsize. If employees

cause poor stock performance, the firm benefits will be damaged. From the perspective of either

psychological theory or economic theory, it is possible that they would be fired. On the one

hand, companies argue that the employees don’t meet their commitments, and it is reasonable

to lay off them and hire new employees who can bring benefits. On the other hand, companies

need to stop further loss in the future, and the economic advantages in financial performance

are supposed to be more than the disadvantages of costs related with new employees. So, any

employee in a company, including managers, is concerned on possibility of layoffs.

2.3.2 Managerial myopia

Over the past decade, many critics have expressed concerns that myopic managerial and

investment behaviours have caused firms to lost competitiveness and economic development.

(Jacobs 1991; Porter 1992; Laverty 1996). Myopia, in the filed of business and economy, refers

to underinvestment behaviours of firms to meet short-term goals rather ran long-term benefits.

A lot of studies have explored why executives would implement myopic decisions, an agency

problem that hurts the value of shareholders and firms.

19

Many researchers focus on how institutional investors play the role of decision-making process

of myopic behaviours. Institutional investors can monitor and encourage to gain higher overall

performances (Almazan et al. 2005; Hartzell and Starks 2003). Dobrzynski (1993) and Monks

and Minow (1995) have examined that managers are allowed to choose investments that

maximize long-term value rather than meet short-term earnings goals under the pressure of

institutional invests and large shareholders. The results reported by (Bushee 1998) indicate that

when the institutional ownership is high, managers are less likely to cut R&D investment to

reverse an earning decline. The presence of institutional investors decreases the likelihood of

misvaluations managers perceive.

Prior research documents that the evidence of CEOs’ job changes, such as retirement of CEOs

in the form of reductions in R&D expenditures (Dechow and Sloan 1991; Barker and Mueller

2002; Lundstrum 2002), potentially earning declines and loss (Habib and Hansen 2008),

impending acquisitions that have higher returns but lower post-merger long-term stock

performance (Gao 2010), and earning management to increase pension contributions (Kalyta

2009), also cause short-horizon decisions. And no matter the absence of career concerns or

excessive career concerns of CEOs, job changes are likely to lead to the overweight on short-

term performance at the expense of long-term firm value. First, CEOs have the tendency to

reduce R&D and engage in earning management near retirement. (Lundstrum 2002; Kalyta

2009). Second, Habib and Hansen (2008) documents that CEOs are overly concerned about the

firm value to manipulate and avoid earning declines and losses.

Some observers also comment that control systems tend to cause an excessive short-term

orientation and stimulate manipulation (Thurow 1981; Schlender 1982). The survey result of

Merchant (1990) is evident to show that myopic behaviours are positively associated with the

felt pressure to meet financial targets.

Consistent my thesis, some studies research that frequent financial reporting, a proxy of

information transparency, is likely to influence myopic behaviours. There are some reasons to

believe that increased frequent reporting could mitigate investment myopia and encourage

long-term orientation of managers. For example, increased public disclosure could improve

firms’ access to financing by decreasing investment contradictions between firms and capital

investors, even helping firms in identifying positive NPV projects to gain benefits. Second, the

increased internal and external monitoring can construct a system to discipline corporate

managers and mitigate agency problems. As a result, managers are more willing to invest in

20

long-term projects. Thus, decreased information asymmetry are believed to might mitigate

corporate myopia.

In addition, we should know more about the impacts of investment and managerial myopia.

Specifically, what are the differences between short-term and long-term oriented firms? How

these differences impact firms and economy? The finding in a McKinsey report (2017) has

revealed the impact of short termism.

Regarding internal benefits, long-term firms exhibit strong financial performance. The long-

term companies outperformed other companies in terms of revenue and earnings growth. Even

in financial crisis, they suffered less earning decline and recovered more quickly after crisis.

Economic profits measure not only companies’ profitability but also how companies allocate

resources and use capital effectively to get better options and opportunities. And the companies

that orient the long-term horizon performed better in economic benefits. Moreover, long-term

firms can deliver more returns to shareholders than other companies. Regarding the impact to

economy, researchers of McKinsey conclude that more advantages in macroeconomy have

been brought by long-term firms. Even in financial crisis, these companies that have more

sustainable ability to invest can maintain their earning growth and achieve long-term goals. In

addition, they can add more to economic output and growth. For example, long-term companies

have provided more opportunities and hired more worker, mitigating the financial burden of

government and unlock potential value.

Other literatures are dedicated to developing how to mitigate and cure myopic behaviours.

Almost all studies concentrate on performance measures to manage myopia.

As the problem of institutional investor and job changes, performance measurement designed

for compensation contracting of executives are suggested. Dikolli et al. (2009) show that on

average, the contracting weight on CEO cash bonus decreases and annual return increases,

following the increases of the level of transient ownership. The authors assume that firms will

trade off between contractual explicit incentive and implicit incentives brought by institutional

investors. Specifically, the design of contacts is purposed to efficiently balance the effort

allocation between generating short-term earning and increasing long-term value. The result is

that the level of institutional ownership is positively related with equity incentives in contracts.

Dikolli et al. (2013) identify possible job changes and, likewise, find that compared with CEOs

not identified as short-horizon, the contracting weight placed on future-looking information in

CEO compensation system is larger for those identified as short-horizon. Contracts emphasize

21

more on R&D expenses and non-financial performance measures if CEOs approach retirement

(Cheng 2004; Matejka et al. 2009). Furthermore, the authors also indicate that more external

and internal monitoring are negatively with managerial myopia. Increased shareholder right,

as the proxy of external monitoring, can prevent managerial entrenchment, thereby further

reducing the myopic behaviours. Some studies suggest that contacts should compensate CEO

for increase employment risk that internal monitoring creates (Hoskisson et al. 2009). Thus,

the contracting and internal monitoring complements reinforce for each other.

Merchant and Bruns (1986) divide measurements into top and middle management. The return

realized by shareholders are a better yardstick for top management, while a good measure that

combines economic returns with cash flow generated is more suitable for middle management.

Abernethy et al. (2013) have researched the role of both accounting measures and non-financial

measures to solve myopia problem. Accounting returns, such as return on investment, residual

income, incorporate not only the summary of all relevant actions but also cost of capital, which

is helpful to align managers’ actions with shareholders’ interests. Therefore, accounting

measures are believed to be highly congruous as they measure the economic value generated

from resources (Anthony and Govindarajan 2004; Scapens 1979; Zimmerman 1997;). The

main benefit of non-financial measurements is that it can focus on forward-looking indicators

and motivate managers to achieve long-term profits. Further, this kind of measurement can be

tailored for specific companies and activities. For example, customer satisfaction that can’t be

measured by numbers are suitable for customer-oriented companies. Thus, the design of non-

financial measures dominates the literatures of myopia management. (Ittner and Larcker 1998;

Thevaranjan et al. 2000).

Except performance measurements, intrinsic investors, defined in the McKinsey analysis as

those who have deep understanding of a company’s intrinsic value, can help firm to solve the

problem of myopia (Darr and Koller 2017). They are believed to have willingness to invest for

long term and accept bad financial news, which instead could be an opportunity to increase

their holdings. Therefore, the presence of intrinsic investors gives executives enough room to

create values and help long-term shareholders achieve integrated strategies. This report

concludes that if managers want to achieve long-term goals and value more easily, they should

find, work, and cooperate with intrinsic investors.

22

2.3.3 The relationship between concerned manager and managerial myopia

Managers who are concerned on stock price are more potential to make myopic decisions and

hurt the long-term value of firms.

First, in such a climate where takeover is prevalent, managers found themselves distracted

towards short term and reduce long-term investment to stretch quarterly earnings target

(Auletta 1986). When there is a chance that the company will be bought at an unfairly low

price, managers may boost earning or reduce R&D expenses to boost short-term profits,

attempting to satisfy shareholders. Setting a takeover barrier seems to be a reasonable solution.

Second, incentive compensation should encourage behaviours aligned with firm value, while

stock-based incentives compensation can surprisingly motivate management myopia. When

managers are concerned about the personal incomes influenced by stock price, they will inflate

short-term earnings and increase stock price. In addition, some results suggest that the equity

incentives are negatively related to the level of risk bearing (Guay 1999; Tufano 1996;

Lewellen 2006; Rajgopal & Shevlin 2002; Coles et al. 2006), and long-term investment is

riskier than that of short term.

In most cases, as Gilson (1990) claimed, poor performance in stock market has increased the

level of financial distress, further resulting in possibility of employee dismissal. If employees

work under the pressure of layoffs related with stock price, they are concerned about the stock

performance and take initiative to manipulate short-term profits at the expense of future value.

And a typical study (Stein 1989) that uses signal-jamming model also illustrates why the more

managers concerned about stock price, the worse the problems become. Managers who know

that higher earnings today are correlated with better future forecast of firm value, they will

manipulate the signals to shareholders. But in equilibrium the market can identify the inflation

and take it into consideration of forecasts. Nonetheless, managers are trapped into myopic

behaviours.

Taken together, all these arguments contend that managers’ concern on lower stock price leads

to focus more heavily on short-term profits rather than on long-term objectives, which is

defined as managerial myopia.

2.4 Testable hypothesis in high-technology firms setting

McKinsey report 2015 has shown that, in the context of competitive landscapes, profits have

increasingly migrated to idea-intensive industries, such as pharmaceuticals, technology,

23

software, and biotechnology. The findings of report also suggest that idea-intensive industries

are the most long-term oriented on an industry level, especially compared with capital-intensive

industries. Regarding the explanation, it seems reasonable that the growing profit pool in high-

technology firms encourages long-termism.

It is worthy to note that long-term investment, like R&D investments, are one of the most

important strategies that the managers in high-technology firms must take into consideration

(Greve 1998). The argument indicates that myopic behaviors can cause more serious damages

to high-technology sectors than other industries, as their profits mainly depend on long-term

investment. Consistently, some literatures also point out their concerns. Innovations in high-

technology firms generated more than half economic growth from1945 to 2002 (Leary 2002).

Due to the rapid and discontinuous development in market, innovation, organizational learning,

and the creation of new knowledge are significant for their long-term survival and success.

(Makri et. al 2006). R&D intensity are particularly relevant with high-technology firms because

their performance is heavily correlated with effective generation of innovations (Li et al. 2008).

Additional, high-technology firms are perceived to be not reluctant to reveal their information.

Many firms are privately hold. Even the firms whose information are publicly available, the

information asymmetry of them is larger than that of other industries.

Therefore, the above suggests that it is plausible to explore how information asymmetry has

effect on managerial myopia in high-technology firms.

2.4.1 Testable hypothesis

Prior literatures have shown that asymmetric information leads to negative investor sentiment.

When there is information asymmetry between corporate managers and investors about

investment expenditure, it is likely that investors can’t distinguish the investments that only

benefit in the long term from those that will not. And if investors don’t have reasonable

explanation or are not persuaded convincingly by managers at this time, as a result, investors

may attribute the long-term investment to managerial misbehavior or poor business prospects,

which means negative investor sentiment.

Investor sentiment has an effect on stock price in the following ways. First, with negative

sentiment, investors will have lower prediction of earning growth and stock valuation and

believe the investment will be risker. Second, there are a number of ways to lower stock price

by investor sentiment. Lower future cash flow, selling signal, and more risk exposure are all

the consequence of negative sentiment. In addition, stock market can fluctuate with sentiment,

24

and, compared with other factors, there is an immediate effect without lagging feature. The

conclusion is that negative sentiment can stimulate lower stock price, either in prediction or in

practice.

I have identified three types of managers who are concerned on stock price and my have

influence on managerial myopia. First, in such a climate where takeover is prevalent, managers

found themselves distracted towards short term and reduce long-term investment to stretch

quarterly earnings target (Auletta 1986). Second, incentive compensation should encourage

behaviors aligned with firm value, while stock-based incentives compensation can surprisingly

motivate management myopia. Third, if employees work under the pressure of layoffs related

with stock price, they are concerned about the stock performance and take initiative to

manipulate short-term profits at the expense of future value.

Taken together, if investors can observe everything that managers do, any decision that

management make is not aligned with long-term benefits would lower the stock price. If, on

the other hand, not all information can’t be observed by investors and they have to reply on

some imperfect summaries, managers may be concerned about lower stock price caused by the

misunderstanding of strategies. Consequently, they have strong motivation to, for example,

reduce future R&D expenses to boost the current earnings and present a better short-term

financial performance, avoiding undervaluation of stock price. Overall, this association can be

approximated as positive, and stated formally,

H1: The information asymmetry is positively related to managerial myopia in high-technology

firms.

25

3 Research design

3.1 Measuring information asymmetry

As there are no general measurements of information asymmetry, I chose four indicators that

are most commonly used in prior literatures: the market value of shared traded in market

(TRADEVALUE), the number of shares traded in market (TRADEVOLUME), bid ask spread

(SPREAD), and volatility of stock (VOLATILITY).

TRADEVALUE and TRADEVOLUME are measured by Compustat database and SPREAD

and VOLATILITY are reported by CRSP database.

Draper and Paudyal (2008) find that asymmetric information is negatively related to trading

volume, the number of outstanding shares. Gajewski (1999) also indicates that potential release

of information may lead to higher trading volume, as the average trading volume on

announcement days tend to be larger. Van Ness et al. (2001) report that because trading volume

and trading value mean more information known by investor, the two proxies are related to

information asymmetry. Hence, I expect that the higher trading volume or the larger trading

value, the lower degree of information asymmetry.

According to the finding of Ness and Warr (2000), the realized spread on London Stock

Exchange was dominated by asymmetric information components. Consistently, other studies

also suggest that the adverse selection costs are positively correlated with the entire spread.

Therefore, using the bid ask spread as a proxy of information asymmetry is justified, and I

assume that the larger percentage change of bid ask spread, the larger the level of information

asymmetry.

The volatility of a stock measure the dispersion of returns for the given security. In general, the

higher the volatility, the riskier the security. Wang (1993) shows that information asymmetry

among investors can increase volatility. Thus, it is reasonable to assume that higher volatility

of stock return lead to larger degree of information asymmetry.

3.2 Measuring managerial myopia

I use the investment decline as the managerial myopia. The investment decline measures the

myopic underinvestment by managers due to concerns on possible lower stock price caused by

investor sentiment. Both survey-based and archival research suggest that managerial myopia

can manifest in the form of underinvestment. Graham et al. (2005) find that managers have

26

admitted cutting current investment expenditures and reducing equipment maintenance to meet

short-term earnings targets.

R&D expense are regarded as a typical proxy of managerial myopia. R&D offer a way to

measure the extent how a company implement its long-term plan, by which they can identify a

sustainable product or technology that benefit them permanently and then bring it to life. Prior

research provides some evidence that managers reduce R&D to meet short-term earning goals

(Jacobs 1991; Dechow and Sloan 1991).

But many literatures only take R&D investment into consideration (Lev and Sougiannis 1996;

Bushee 1998), I also use measures to capture firms’ capital investment. Capital investment

projects commonly generate value over long term. For example, a capital investment for a

product to penetrate a new market may take more than half of year to attract new customers’

loyalty and attention. Thus, benefits of such capital investment are also not immediate, and

investors should be patient to the returns. Similarly, when investors don’t observe the future

prospects of the capital investment, they will also mistakenly have negative investor sentiment

and attribute to investment to inferior management.

My first measure CAPEX is defined as the amount of capital expenditures scaled by beginning-

of-year total assets. Edmans et al. (2017); Ladika and Sautner (2015); and Asker et al. (2015)

find from archival evidence that reduced capital expenditure is one of forms of managerial

myopia. The second measure of capital investment CHPPE is defined as the change in net fixed

assets scaled by beginning-of-year total assets. CHPPE captures not only the direct capital

expenditures, but also the fixed assets purchased from merger and acquisitions and from long-

term leases record.

CAPEX, CHPPE, R&D are measured by information from Compustat database.

3.3 Control variables

First, I control firm size (SIZE), as the natural logarithm of total assets for any given company

in a given year. I also control firms’ profitability (EBITDA), as EBITDA scaled by total assets

for any given company in a given year. And the beginning-of-year cash scaled by assets (CASH)

is controlled. Taken together, I think firms with higher level of size, EBITDA, and cash have

more opportunities to explore investment improvements. And as I introduced in the cure of

myopia from literature review, bigger firms tend to have higher degree of external and internal

monitoring, therefore, firms have lower level of myopia behaviors. In addition, I control the

27

beginning-of-year long-term debts scaled by total assets (LEVERAGE). Likewise, firms with

higher level of leverage will be limited in myopia management. I use Compustat database to

find all information of control linvariables.

3.4 Model

This study uses the following model to assess the association between information asymmetry

and managerial myopia:

INVESTMENT𝑖

= 𝛽1 + 𝛽2𝑇𝑅𝐴𝐷𝐸𝑉𝐴𝐿𝑈𝐸 + 𝛽3𝑇𝑅𝐴𝐷𝐸𝑉𝑂𝐿𝑈𝑀𝐸 + 𝛽4𝑆𝑃𝑅𝐸𝐴𝐷

+ 𝛽5𝑉𝑂𝐿𝐴𝑇𝐼𝐿𝐼𝑇𝑌 + 𝛽6𝐶𝐴𝑆𝐻 + 𝛽7𝑆𝐼𝑍𝐸 + 𝛽8𝐿𝐸𝑉𝐸𝑅𝐴𝐺𝐸 + 𝛽9𝐸𝐵𝐼𝑇𝐷𝐴 + 𝜖𝑖

where:

INVESTMENTi CHPEX, the amount of capital expenditure scaled by beginning-of-

year total assets for firm I; CHPPEX, the change in net fixed assets

scaled by beginning-of-year total assets for firm I; R&D, the R&D

expenses scaled by beginning-of-year total assets for firm i

TRADEVALUEi the market value (in thousands) of a stock divided by the number of

shares for firm i

TRADEVOLUMEi the number of shares traded for a stock divided by the number of shares

in issue for firm i

SPREADi the percentage change in the bid ask spread from previous day to today

averaged over the year for firm i

VOLATILITYi the annual average of daily stock return volatility for firm i

CASHi the beginning-of-year cash scaled by total assets for firm i

SIZEi the natural logarithm of total assets for firm i

LEVERAGEi the beginning-of-year long-term debts scaled by total assets for firm i

EBITDAi the EBITDA scaled by total assets for firm i

3.5 Sample selection

The sample concludes high-technology firms between 2010 and 2016. Firms with specific SIC

code are regarded as high-technology firms. Based on Elizabeth (2015), I will include the

28

following firms in the sample: high-tech manufacturing (SIC 357, 365, 366, 367, 381, 382, 384,

and 386), high-tech services including communications services (SIC 481, 482, 484, and 489),

and computer-related services and software (SIC 737). Firms with insufficient data are

excluded, and the final sample consists of 307 firm-year observations. Variables of R&D and

trading volume have some extreme values, therefore, I use the winsorize command to deal with

all variables in Stata.

29

4 Results

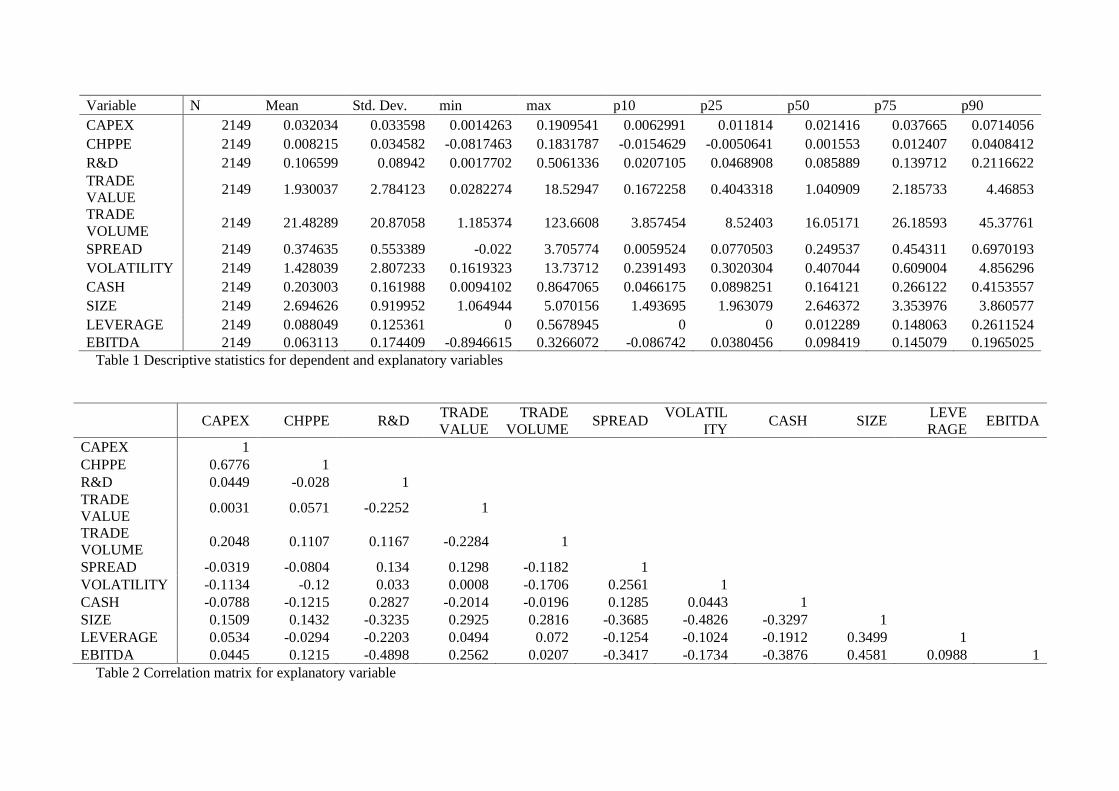

4.1 Descriptive statistics

Table 1 reports the descriptive statistics for the dependent and explanatory variables. The mean

and median for capital expenditures, CAPEX, are 0.032034 and 0.021416 of prior year total

assets respectively. On average, CHPPE and R&D expenditures are 0.008215 and 0.106599

respectively, which are higher than the investment level reported by whole industries.

Other characteristics of the sample firms include the volatility of stock returns, VOLATILITY,

of 1.428039, with more than half of the sample firms having the value of less than 0.407044.

Furthermore, more than 50% of samples have the level of bid ask spread more than 0.249537.

Also, 50% of the sample firms have the size and profitability of 0.164121 in cash, 2.646372 in

total assets, and 0.098419 in operating profits. And firms have an average of leverage 8.8049%,

which is lower compared with 15.8% (Arthur et al. 2018), the level within all industries.

Correlations between the explanatory variables are documented in Table 2. As expected, for

the investments CAPEX and CHPPE, the trading value (TRADEVALUE) and trading volume

(TRRADEVOLUME) are positively with them, and the SPREAD and VOLATILITY are

negatively with them. But for R&D expenditures, the results are not much correlated with

expectations, and I will explain further in the next section. A negative correlation between SIZE

or EBITDA and CAPEX or CHPPE indicates that larger firms are less likely to behave

myopically. Leverage is negatively correlated with CHPPEX and R&D, suggesting that higher

leverage level leads to lower investment amounts.

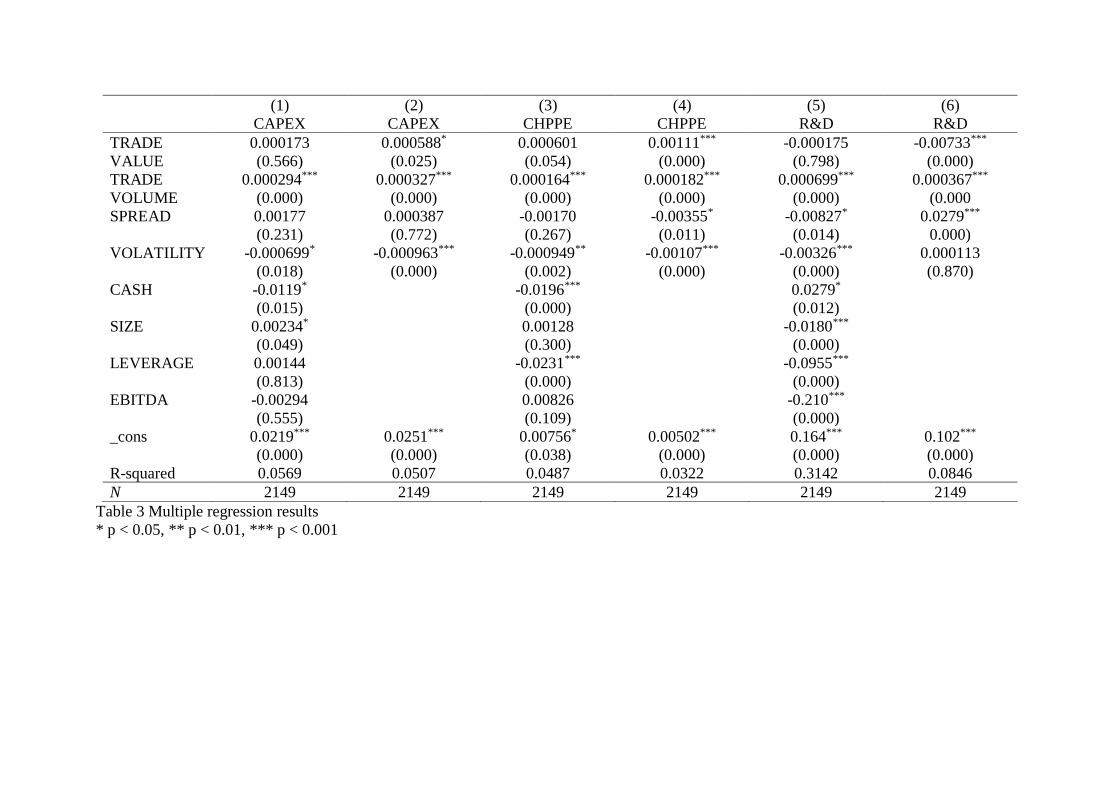

4.2 Regression results

A positive relation between trading volume or trading volume and investments is supported by

a positive estimated coefficient, and a negative relation between spread or volatility and

investments is supported by a negative estimated coefficient. Results in tables 3 indicate that

the coefficient between trading volume and all investments are statistically significant and have

expected signs. And for CAPEX and CHPPE, the hypothesis about capital investment can be

justified, as coefficients for the four independent variables meet my expectation.

However, there are some differences in the estimated results in R&D. When I don’t incorporate

the four control variables, the signs of TRADEVALUE and SPREAD are deviated from my

hypothesis. But after I control these variables, I can see the predicted signs in the results. This

Variable N Mean Std. Dev. min max p10 p25 p50 p75 p90

CAPEX 2149 0.032034 0.033598 0.0014263 0.1909541 0.0062991 0.011814 0.021416 0.037665 0.0714056

CHPPE 2149 0.008215 0.034582 -0.0817463 0.1831787 -0.0154629 -0.0050641 0.001553 0.012407 0.0408412

R&D 2149 0.106599 0.08942 0.0017702 0.5061336 0.0207105 0.0468908 0.085889 0.139712 0.2116622

TRADE

VALUE 2149 1.930037 2.784123 0.0282274 18.52947 0.1672258 0.4043318 1.040909 2.185733 4.46853

TRADE

VOLUME 2149 21.48289 20.87058 1.185374 123.6608 3.857454 8.52403 16.05171 26.18593 45.37761

SPREAD 2149 0.374635 0.553389 -0.022 3.705774 0.0059524 0.0770503 0.249537 0.454311 0.6970193

VOLATILITY 2149 1.428039 2.807233 0.1619323 13.73712 0.2391493 0.3020304 0.407044 0.609004 4.856296

CASH 2149 0.203003 0.161988 0.0094102 0.8647065 0.0466175 0.0898251 0.164121 0.266122 0.4153557

SIZE 2149 2.694626 0.919952 1.064944 5.070156 1.493695 1.963079 2.646372 3.353976 3.860577

LEVERAGE 2149 0.088049 0.125361 0 0.5678945 0 0 0.012289 0.148063 0.2611524

EBITDA 2149 0.063113 0.174409 -0.8946615 0.3266072 -0.086742 0.0380456 0.098419 0.145079 0.1965025

Table 1 Descriptive statistics for dependent and explanatory variables

CAPEX CHPPE R&D TRADE

VALUE

TRADE

VOLUME SPREAD

VOLATIL

ITY CASH SIZE

LEVE

RAGE EBITDA

CAPEX 1

CHPPE 0.6776 1

R&D 0.0449 -0.028 1

TRADE

VALUE 0.0031 0.0571 -0.2252 1

TRADE

VOLUME 0.2048 0.1107 0.1167 -0.2284 1

SPREAD -0.0319 -0.0804 0.134 0.1298 -0.1182 1

VOLATILITY -0.1134 -0.12 0.033 0.0008 -0.1706 0.2561 1

CASH -0.0788 -0.1215 0.2827 -0.2014 -0.0196 0.1285 0.0443 1

SIZE 0.1509 0.1432 -0.3235 0.2925 0.2816 -0.3685 -0.4826 -0.3297 1

LEVERAGE 0.0534 -0.0294 -0.2203 0.0494 0.072 -0.1254 -0.1024 -0.1912 0.3499 1

EBITDA 0.0445 0.1215 -0.4898 0.2562 0.0207 -0.3417 -0.1734 -0.3876 0.4581 0.0988 1

Table 2 Correlation matrix for explanatory variable

performance, to some extent, accord with my expectation, as the control variables play their

roles in the regression. I also find some other literatures that can explain the result.

Although some opponents argue that the lack of information disclosure encourages managers

to engage in such myopic investment, others hold that large shareholdings and intrinsic

investors allow managers to focus on long-term objective rather short-term earnings.

As the dealer rather than the owner, institutional investors pay much attention to short-term

performance and result, influencing managers to fear the undervaluation of stock price and

selling caused by their dissatisfaction towards earning. (Graves and Waddock 1990; Jacobs

1991; Porter 1992). Therefore, it is possible that managers cut R&D investment, a kind of proxy

for long-term investment, to avoid investors’ disappointment. There are two assumptions that

managers have incentives to stop undervaluation. First, managers have enough concerns about

the stock price, as we also explained in the last section. Second, supported by Bernard et al.

(1993), managers believe that the market is capable of overreacting to unmanaged earning

declines or underreacting to artificial earning boost.

Further, in an influential survey, CEOs complained that the culture of meeting short-term

targets restrain their abilities from increasing long-term firm value (Graham, Harvey, and

Rajgopal 2005). Most of them even expressed their willingness to sacrifice long-term value to

present a better shot-term result. Recent theoretical studies (Gigler et al. 2014; Edmans et al.

2016; Hermalin and Weisbach 2012) also support the argument that the greater disclosure on

financial reporting, the more possibility that managers make myopic decisions.

Hence, the reasons above are helpful to explain why the trading value, in the regression result

from table 3, is negatively related with R&D and spread is positively correlated with R&D.

Overall, the results support my hypothesis, since all variables perform expectedly to CAPEX

and CHPPE, and after controlling four related variables, the result between dependent and

explanatory variables also is also consistent with the hypothesis.

(1) (2) (3) (4) (5) (6)

CAPEX CAPEX CHPPE CHPPE R&D R&D

TRADE 0.000173 0.000588* 0.000601 0.00111*** -0.000175 -0.00733***

VALUE (0.566) (0.025) (0.054) (0.000) (0.798) (0.000)

TRADE 0.000294*** 0.000327*** 0.000164*** 0.000182*** 0.000699*** 0.000367***

VOLUME (0.000) (0.000) (0.000) (0.000) (0.000) (0.000

SPREAD 0.00177 0.000387 -0.00170 -0.00355* -0.00827* 0.0279***

(0.231) (0.772) (0.267) (0.011) (0.014) 0.000)

VOLATILITY -0.000699* -0.000963*** -0.000949** -0.00107*** -0.00326*** 0.000113

(0.018) (0.000) (0.002) (0.000) (0.000) (0.870)

CASH -0.0119* -0.0196*** 0.0279*

(0.015) (0.000) (0.012)

SIZE 0.00234* 0.00128 -0.0180***

(0.049) (0.300) (0.000)

LEVERAGE 0.00144 -0.0231*** -0.0955***

(0.813) (0.000) (0.000)

EBITDA -0.00294 0.00826 -0.210***

(0.555) (0.109) (0.000)

_cons 0.0219*** 0.0251*** 0.00756* 0.00502*** 0.164*** 0.102***

(0.000) (0.000) (0.038) (0.000) (0.000) (0.000)

R-squared 0.0569 0.0507 0.0487 0.0322 0.3142 0.0846

N 2149 2149 2149 2149 2149 2149

Table 3 Multiple regression results

* p < 0.05, ** p < 0.01, *** p < 0.001

5 Summary and conclusion

This paper examines the association between information asymmetry and managerial myopia

in high-technology firms. Extant literatures posit a theoretical reasoning link from information

asymmetry to managerial myopia. The first link between information asymmetry and investor

sentiment argue that information asymmetry between investors and managers might lead to

negative investor sentiment, as investors can’t distinguish long-term investments that don’t

benefit in the short-term from the misbehavior of management. The second link between

investor sentiment and stock price argue that, according to some proved evidences, the stock

price fluctuates positively and immediately with investor sentiment by future cash flow, selling

signal, risk exposure, etc. As a result, negative sentiment tends to cause lower stock price. The

third link between concerned manager and managerial myopia argue that it is possible that

managers who are concerned about stock price would manipulate myopic investment to meet

short-term objectives.

Using a sample of 307 high-technology companies from 2010 to 2016, I have tested the

hypothesis and the result supported predicted the positive association. The predicted positive

relations between trading value / trading volume and investments are observed, consistent with

the hypothesis that firms with higher level of trading volume have more opportunities to

improve investment shot-termism and reduce managerial myopia. The negative associations

are found between volatility / spread and investments, also consistent with the hypothesis.

There is a contradiction in the result of R&D without control variables, and I found that

frequent information disclosure sometimes encourages managers to focus on short-term

earnings, which increases managerial myopia.

The result offers supports in favor of increasing managerial myopia by asymmetric information,

indicating that executives and shareholders should try to reduce information asymmetry, such

as adding more institutional investors, to mitigate managerial myopia, the problem that has

negative impacts on internal financial performance and external macro-economy. For example,

long-term oriented firms have better future earnings growth and create more employment

opportunities even in financial crisis. My paper also has the implication for practice because

several regions, including Europe, Singapore, and Australia, have debated the merits of

mandating quarterly reporting. And compared with annual reporting, quarterly reporting that

is regarded as the decreased level of information asymmetry can mitigate myopic investment

with the results from this paper.

34

This study has some limitations. First, it is limited in that it focuses on high-technology

companies in the U.S., suggesting that that future research could extend this study to other

developed or developing countries. As restrained by the available database, it is difficult for

me to collect data from other countries. And the results incorporate information from other

areas would be more profound and helpful, as high-technology firms have developed very well

in some developing countries. Second, since information asymmetry can lead to managerial

myopia, what’s the result about the level of myopic behaviors if information transparency is

improved? With more time, I will explore whether informed institutional investor or frequency

of financial reporting would decrease the level of myopia, to verify my results from another

perspective.

35

References

Almazan, A., J. C. Hartzell, and L. T. Starks (2005) Active institutional shareholders and