Embed Size (px)

Citation preview

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 1/9

1

INFORMAL RISK CAPITAL MARKET

Introduction

The informal risk capital market is the most misunderstood type of risk capital. It consists of

virtually invisible group of wealthy investors, often called Business angels, who are looking

for equity-type investment opportunities, in a wide variety of entrepreneurial ventures.

Typically investing anywhere from $10,000 to $500,000, these angels provide the funds

needed in all stages of financing, but particularly in start-up (first stage) financing. Firms

funded from the informal risk-capital market frequently raise second- and third-round

financing from professional venture-capital firms or the public-equity market.

Despite being misunderstood by, and virtually inaccessible to, many entrepreneurs, the

informal investment market contains the largest pool of risk capital in the United States.

Although there is no verification of the size of this pool or the total amount of financing

provided by these business angels, related statistics provide some indication. A 1980 survey

of sample of issuers of private placements by corporations, reported to the Securities and

Exchange Commission under Rule 146, found that 87 percent of those buying these issues

were individual investors or personal trusts, investing an average of $74,000. Private

placements filed under Rule 145 averages over $1 billion per year. Another indication

becomes apparent on examination of the filings under Regulation D-the regulation exempting

certain private and limited offerings from the registration requirements of the Securities Act

of 1933, discussed in Chapter 11. In its first year, over 7,200 filings worth $15.5 billion were

made under Regulation D. Corporations accounted for 43 percent of the value ($6.7 billion),

or 32 percent of the total number of offerings (2,304). Corporations filing limited offerings

(under $500,000) raised $220 million, an average of $200,000 per firm. The typical corporate

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 2/9

2

issuers tended to be small, with fewer than 10 stockholders, revenues and assets less than

$500,000, stockholders equity of $50,000 or less, and five or fewer employees.

Characteristics of informal investor

Demographic pattern and relationship

Well educated, with many having graduate degrees.

Will finance firm anywhere, particularly in the United States.

Most firms financed within one days travel.

Majority expect to play an active role in ventures financed.

Many belong to angel clubs.

Investment Record

Range of investment : $10,000 - $5,00,000

Average investment : $50,000

One or two deals each year.

Venture Preferences

Most financing in start-ups or ventures less than 5 years old

Most interested in financing

o Manufacturing – industrial/commercial products

o Manufacturing - consumer products

o Energy/natural resources

o Services

o Software

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 3/9

3

Risk/Reward Expectations

Median 5 - year capital gains of 10 times for start-ups

Median 5 - year capital gains of 6 times for the firm under 1 year old

Median 5 - year capital gains of 5 times for firms 1-5 years old

Median 5 - year capital gains of 3 times for established firm over 5 year old

Reasons for rejecting proposal

Risk/return ratio not adequate

Inadequate management team

Not interested in proposed business area

Unable to agree on price

Principle not sufficiently committed

Unfamiliar with area of business

VENTURE CAPITAL

The important and little understood area of venture capital will be discussed in terms of its

nature, the venture-capital industry in the United States, and the venture-capital process.

Nature of Venture Capital

Venture Capital is one of the least understood areas in entrepreneurship. Some think that the

Venture capitalists do the early – stage financing of relatively small, rapidly growing

technology companies. It is more accurate to view venture capital broadly as a professionally

managed pool of equity capital. Frequently, the equity pool is formed from the resources of

wealthy limited partners. Other principal investors in venture-capital limited partnerships are

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 4/9

4

pension funds, endowment funds, and other institutions, including foreign investors. The pool

is managed by a general partner — that is, the venture-capital firm — in exchange for a

percentage of the gain realized on the investment and a fee. The investments are in early-

stage deals as well as second- and third-stage deals and leveraged buyouts. In fact, venture

capital can best be characterized as a long-term investment discipline, usually occurring over

a five-year period, that is found in the creation of early-stage companies, the expansion and

revitalizing of existing businesses, and the financing of leveraged buyouts of existing

divisions of major corporations or privately owned businesses. In each investment, the

venture capitalist takes equity participation through stock, warrants, and/or convertible

securities and has an active involvement in the monitoring of each portfolio company

bringing investment, financing planning, and business skills to the firm.

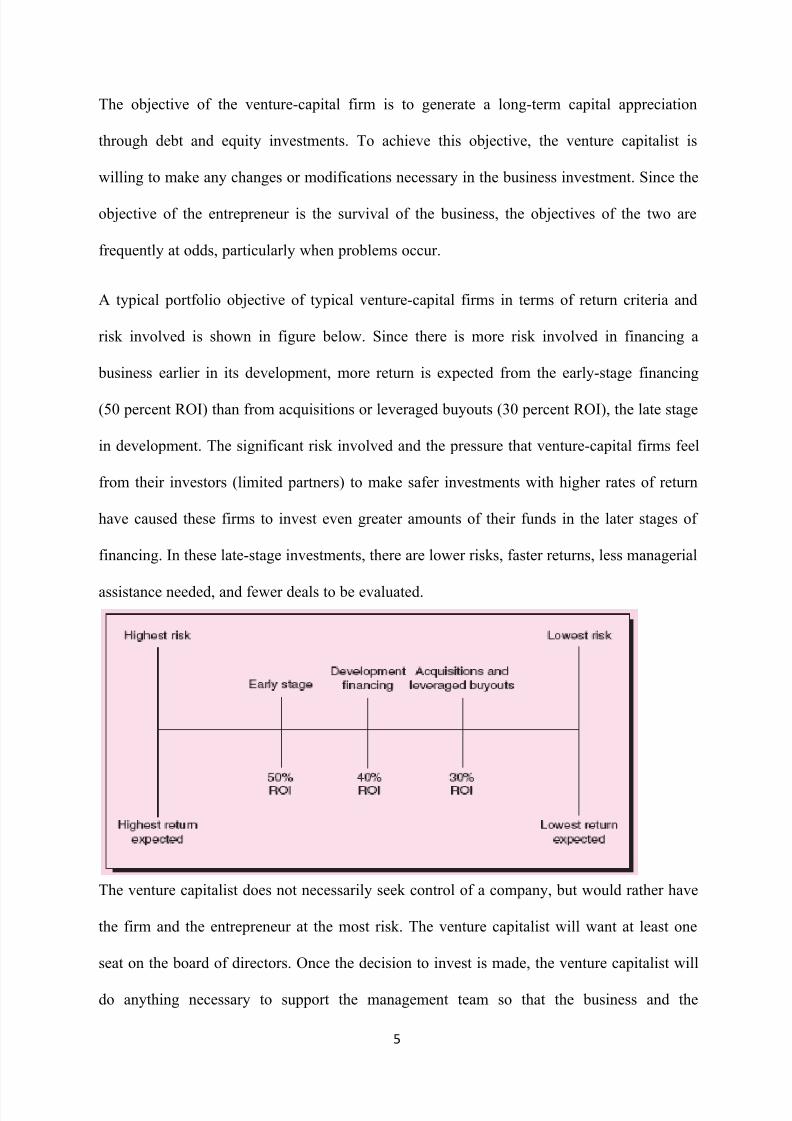

VENTURE CAPITAL PROCESS

To be in a position to secure the fund s needed, an entrepreneur must understand the

philosophy and objectives of a venture-capital firm, as well as the venture-capital process.

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 5/9

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 6/9

6

investment prosper. Whereas the venture capitalist expects to provide guidance as the

member of the board of directors, the management team is expected to direct and run the

daily operations of the company. A venture capitalist will support the management team with

the investment dollars, financial skills, planning, and expertise in any area needed.

Since the venture capitalist provides long-term investment (typically five years or more), it is

important that there be mutual trust and understanding between the entrepreneur and the

venture capitalist. There should be no surprises in the firm’s performance. Bothe good and

bad news should be shared, with the objective of taking the necessary action to allow the

company to grow and develop in the long run. The venture capitalist should be available to

the entrepreneur to discuss the problems and develop strategic plans.

The venture capitalist expects a company to satisfy three general criteria before he or she will

commit to the venture. First, the company must have a strong management team that consists

of individuals with solid experience and backgrounds, a strong commitment to the company,

capabilities in their specific areas of expertise, the ability to meet challenges, and the

flexibility to scramble wherever necessary. A venture capitalist would rather invest in a first-

rate management team and a second-rate product than the reverse. The management te am’s

commitment should be reflected in dollars invested in the company. Although the amount of

the investment is important, more telling is the size of this investment relative to the

management team’s ability to invest. The commitment of the management te am should be

backed by the support of the family, particularly the spouse, of each key team player. A

positive family environment and spousal support allow team members to spend the 60 to 70

hours per week necessary to start and grow the company. One successful venture capitalist

makes it a point to have a dinner with the entrepreneur and spouse, and even visit the

entrepreneur’s home, before making an investment decision. According to the venture

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 7/9

7

cap italist, ―I find it difficult to believe an entrepreneur can successfully run and manage a

business and put in the necessary time when the home environment is out of control .

The second criteria is that the product and/or market opportunity must be unique, having a

differential advantage in the growing market. Securing a market niche is essential since the

product and the service must be able to compete and grow during the investment period. This

uniqueness needs to be carefully spelled out in the marketing portion of the business plan and

is even better when it is protected by a patent or a trade secret.

The final criterion for investment is that the business opportunity must have significantcapital appreciation. The exact amount of capital appreciation varies, depending on such

factors as the size of the deal, the stage of development of the company, the upside potential,

the downside risks, and the available exits. The venture capitalist typically expects a 40 to 60

percent return on investment in most investment situations.

The venture-capital process that implements these criteria is both an art and a science. Theelement of art is illustrated in the venture capitalist’s intuition, gut feeling, and creative

thinking that guide the process. The process is scientific due to the systematic approach and

data-gathering techniques involved in the assessment.

The process starts with the venture-capitalist firm establishing its philosophy and investment

objectives. The firm must decide on the following: the composition of its portfolio mix,

including the number of start-ups, expansion companies, and management buyouts; the types

of industries; the geographic region for the investment; and any product or industry

specializations.

The venture-capital process can be broken down into four primary stages: preliminary

screening, agreement on principal terms, due diligence, and final approval. The preliminary

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 8/9

8

screening begins with the receipt of the business plan. A good business plan is essential in the

venture-capital process. Most venture capitalists will not even talk to an entrepreneur who

doesn’t have one. As the starting point, the business plan must have a clear -cut mission and

clearly stated objectives that are supported by an in-depth industry and market analysis and

pro forma income statements. The executive summary is an important part of this business

plan, as it is used for initial screening in this preliminary evaluation. Many business plans are

never evaluated beyond the executive summary. When evaluating the business, the venture

capitalist first determines if the deal or similar deals have been seen previously. The investor

then determines if the proposal fits in his or her long-term policy and short-term needs in

developing a portfolio balance. In this preliminary screening, the venture capitalist

investigates the economy of the industry and evaluates whether he or she has the appropriate

knowledge and ability to invest in that industry. The investor reviews the numbers presented

to determine whether the business can reasonably deliver the ROI required. In addition, the

credentials and capability of the management team are evaluated to determine if they can

carry out the plan presented.

The second stage is the agreement on principal terms between the entrepreneur and the

venture capitalist. The venture capitalist wants a basic understanding of the principal terms of

the deal at this stage of the process before making the major commitment of time and effort

involved in the formal due diligence process.

The third stage, detailed review and due diligence, is the longest stage, involving anywhere

from one to three months. There is a detailed review of the compan y’s history, the business

plan, the resumes of the individuals, their financial history, and target market customers. The

upside potential and downside risk are assessed, and there is a thorough evaluation of the

markets, industry, finances, suppliers, customers, and management.

8/12/2019 Informal Risk Capital Market1

http://slidepdf.com/reader/full/informal-risk-capital-market1 9/9

9

In the last stage, final approval, a comprehensive, internal investment memorandum is

prepared. This document reviews the venture capitalist ’s findings and details the investment

terms and conditions of the investment transaction. This information is used to prepare the

formal legal documents that both the entrepreneur and venture capitalist will sign to finalize

the deal.

Locating Venture Capitalist

One of the most important decisions for the entrepreneur lies in selecting which venture-

capital firm to approach. Since venture capitalists tend to specialize either geographically byindustry (manufacturing industrial products or consumer products, high technology, or

service) or by size and type of investment, the entrepreneur should approach only those that

may have interest in the investment opportunity. Where do you find this venture capitalist?

Although venture capitalists are located throughout the United States, the traditional areas of

concentration are found in Los Angeles, New York, Chicago, Boston and San Francisco. Anentrepreneur should carefully research the names and addresses of prospective venture-capital

firms that might have an interest in the particular investment opportunity. There are also

regional and national venture-capital associations. For a nominal fee or non at all, these

associations will frequently send the entrepreneur a directory that lists their members, the

types of businesses their members invest in, and any investment restrictions. Whenever

possible, the entrepreneur should be introduced to the venture capitalist. Bankers,

accountants, lawyers. And professors are good sources for introductions.