Embed Size (px)

Citation preview

Informal finance, trade creditand private firm performance

Jun Su and Yuefan SunBusiness School, Beijing Technology and Business University,

Beijing, People’s Republic of China

Abstract

Purpose – The purpose of this paper is to test the effect of informal finance and trade credit on theperformance of private firms.

Design/methodology/approach – Based on a survey to private firms in 19 cities, the paperempirically tests the promoting effects of informal finance and trade credit on the performance ofprivate firms in China.

Findings – It was found that informal finance and trade credit have positive effects on private firms’performance measured by ROA. The net income reinvestment rate of private firms is positively relatedto whether or not the firm adopts informal financing or trade credit financing. A private firm havinglimited access to formal finance is more inclined to rely on self-funds and is more limited by financingchoices. Informal financing and trade credit can relieve the tension of cash flow chain but cannot solvethe financing constraints. The empirical results also show that bank credit is still not the main financingchoice for private firms and has not yet played a promoting role in private firms’ performance andgrowth. Informal finance is more important to promote performance in manufacturing industry,while trade credit is more effective in wholesale and trading industry. The results show thecoexistence viability of informal financing channels and formal financial institutions in China.

Practical implications – The policy implication is the Chinese Government should take carefulsteps to regulate informal financing sources.

Originality/value – After some theoretical literature, such as Lin and Sun, this paper explores forthe first time the effect of informal financing channels on the performance of private firms.

Keywords China, Financing, Credit, Private companies, Informal finance, Trade credit, Bank credit

Paper type Research paper

1. IntroductionChina’s dynamic private sector has increasingly been contributing to the rapideconomic growth in recent years. It has been producing over half of industry value addand around half of China’s trade surplus[1]. Private sector is the main force of economicdevelopment and playing more and more important role in pushing economics’

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/2040-8749.htm

The authors are grateful to Professor Jia He and Professor Ming Liu from the Chinese Universityof Hong Kong and the participants in the Annual Asian Finance Association Conference of 2009in Brisbane, Australia for their helpful comments. This paper is supported by Funding Projectfor Academic Human Resources Development in Institutions of Higher Learning under theJurisdiction of Beijing Municipality (PHR20100512), Capital Groups’ Finance and AccountingResearch Base, which is included in the Innovation Scientific Program of Beijing MunicipalCommission of Education, Funding Project for Innovation on Science, Technology and GraduateEducation in Institutions of Higher Learning Under the Jurisdiction of Beijing Municipality,Funding Project of Humanities and Social Sciences under the Ministry of Education of the PRC(10YJC790374) and the Research Foundation for Youth Scholars of Beijing Technology andBusiness University.

Informal finance

383

Received 27 October 2010Revised 4 January 2011,

19 April 2011Accepted 28 June 2011

Nankai Business ReviewInternational

Vol. 2 No. 4, 2011pp. 383-401

q Emerald Group Publishing Limited2040-8749

DOI 10.1108/20408741111178816

continuous growth in China. The positive relationship between private sector growthand economic growth is testified by Western academic world and applicable both indeveloped and developing countries. Countries throughout the world adopted all sortsof policies and mechanisms to support the development of private firms, for example,USA adopted a series of tax cut to help private firms and the mature venture capitalnetwork also supports the small and medium enterprise (SME) funding and growth(Audretsch, 2003). Private firms in China are facing developmental opportunities,challenges and strategic industrial upgrading and transition at the same time. How tomigrate private firms smoothly from labor intensive to high-tech, service oriented,how to efficiently establish favorable institutional environment and how to solve thefunding shortage and improve funding efficiency for private firms are all importanttasks the academic world and Chinese Government face.

It has been almost two decades since the establishment of Chinese capital market.Financing methods of large enterprises and business groups have gradually migratedfrom banking credit to capital market direct financing. Private firms are becoming theimportant and steady client source for commercial banks. While commercial banks inChina are used to operate in a non-commercial way, the service quality is not satisfyingand the types of financial products are limited. At the same time, that private firms areinformation opaque, operation inefficient, lack of credit ratings impeded banks grantingcredits. To solve funding gap between enterprises necessities and bank credits, privatefirms in China, besides retained earnings and family investment, internal financing andbank credits, always turn to other informal channels for financing, including but notlimited to informal financing and trade credit. Informal financing indicates financingtrough non-banking private financial institutions such as the Hehui, the Biaohui or theTaihui and trade credit means mutual credit derived from products transactions such asthrough account payables, account receivables and prepayment and, etc.

The informal finance is not necessarily illegal and some informal financial contractsare even protected legally. Informal finance is not regulated by the government, thusthere is no interest rate regulation, no needs to conform to reserves and liquidityrequirements, which is the competitive advantage of informal financial firms overformal banking finance especially under the repressive period (Montiel et al., 1993). Theinformal nature of the informal finance can be damaging to a country’s financial stabilityin financial crisis. In one word, informal financing channels exist and have positiveeffects to private firm growth in developing countries while its effects are double-folded.In this paper, we show that informal financing channels play positive role to the privatefirms’ performance. Our paper mainly focuses on the research of:

(1) roles of informal financing channel and trade credit on private firm performancein China; and

(2) complimentary effects between formal banking credit and informal finance toprivate firms in China.

2. Literature reviewTracing back the literature, the earliest theory on informal finance was from highrepayment risk and high lending cost angle to testify the rationale of informal finance(unorganized money markets) (Bottomley, 1975). After that, theoretical focus changedto information asymmetry and informal finance angle. The credit rationing theoryof Stiglitz and Weiss (1981) set force that market frictions such as information

NBRI2,4

384

asymmetries and agency costs may explain why capital does not always flow to firmswith profitable investment opportunities. The central issue addressed in the literature onfinancing private firms is that of credit rationing stemming from asymmetricinformation (Stiglitz and Weiss, 1981; De Meza and Webb, 1987). These papers arguethat, in equilibrium, markets are imperfect since credit is allocated by rationing, ratherthan by price. The difference between the two papers is that, whereas Stiglitz and Weiss’sassumptions lead to credit rationing, those of De Meza and Webb lead to over-supply.The theoretical issues addressed in these papers underpin a huge raft of empirical paperson credit rationing in many countries, of which those by Berger and Udell (1992) and byPetersen and Rajan (1994) are examples. Stiglitz and Weiss discuss adverse selection andincentive (moral hazard) effects and say “Both effects derive directly from the residualimperfect information which is present in loan markets after banks have evaluated loanapplications”. That’s the reason that banks incline to lend to mature, large-scale,transparent and high credit ratings company. While for younger and smaller companies,lack of public transparent information, banks spend much more information andtransaction costs and bank credits are short term mostly. It is very hard to meet long termand continuous financing needs for private firms. Stiglitz (1990) and Besley and Coate(1995) illustrated that how to screen and monitor projects lack of collaterals to lower thedegree of information asymmetry and that various forms, such as bundling of financingwith other relations and group lending are effective tools. Petersen and Rajan (1994)tested relationship-banking theory in USA and Berger and Udell (1995) put forward thatsmall banks are more suitable for servicing private firms. Mauri (2000) tested thatinformal finance and formal banking credit are complementary in developmentcountries. Bose (1998) theoretically proves that cheap credit through the formal sectorcan worse the credit availability in informal sector by analyzing small cultivators’ creditin developing countries. That is cheap formal credit is not always good.

Lin and Li (2001) also illustrates that developing small- and medium-sized financialinstitutions is a good way to relieve the financing difficulties of private firms and thetheory is applied already in the fast developing small and medium commercial banks.The research on private firms’ financing choices is limited mostly to banking financeand concentrate on mature western world. Lin and Sun (2005) tries to rationalize theextensiveness of informal finance. Private firms’ financing suffers more seriousinformation asymmetry to the extent that most private firms are more informationopaque and can only provide no or less collateral. Informal lenders have an advantageover formal financial institutions in collecting soft information about private sectorborrowers. Lin and Sun (2005) shows that the credit market in which informal financeis eliminated will allocate funds in some inefficient way, and the efficiency of allocatingcredit funds can be improved once informal finance is allowed to coexist with formalfinance.

Allen et al. (2005) attributes China’s fast growth to the alternative financingchannels and governance mechanisms of private firms while their sample was limitedto 17 firms in Zhejiang district and did not test the relationship between enterpriseperformance and informal financing channels, their results are not adaptable to a widerarea. While by using a database of 2,400 Chinese firms, Ayyagari et al. (2008) find thatfinancing from the formal financial system is associated with faster firm growth,whereas fund raising from alternative channels is not and that the role of reputation

Informal finance

385

and relationship based financing and governance mechanisms in financing the fastestgrowing firms in China is likely to be overestimated.

Notwithstanding the increasing role of the private firms in supporting growth andcontribution of the informal financial sector to its expansion, the largest part ofliterature on enterprises financing in China has focused on other aspects such asownership and financing (Cull and Xu, 2005). The scarcity of literature on private firmsinformal financing in China may largely be attributable to the lack of available data ona nationwide basis. The major contribution of the article to existing literature is tomake an attempt to fill the gap in assessing the role informal finance and trade creditplay in providing funds for the SME sector using empirical analysis.

China Banking Regulatory Commissions has been promoting the village banks inrural area in the past few years, starting to admit the role of informal finance inextensive rural areas. While the government is still cautious on liberating the vastnumbers of informal institutions in urban area, which are believe to be the majorpropellers for SMEs in China in the past decades. Our research concentrates on the roleplayed by informal finance on SMEs in Urban area.

Researchers in China studied intensively on the relationship between informal andformal finance. To name a few, Wang et al. (2009) review the domestic and foreignexperiences in the development of informal finance from the historical perspective,explore the relationship between informal and formal finance. Yang (2008) usesthe theories of financial ecology to analyze the economic foundation of informal financeand the function of informal system. It is the features of obscure legal status, secreteoperation pattern and out of the reach of supervision that make the informal financemay induce the hidden danger of financial risks. At the same time, the marketizedinterest mechanism of informal finance would have some negative effects to formalcredit market. Zhang (2009) argue that informal finance has comparative advantage insmall- and medium-size financing, mainly on information cost, negotiation cost,regulation cost, and so on. As the size of informal financing increases, the comparativeadvantage on trading cost will gradually diminish or even disappear. Policy should notalways provide pressures to informal finance but regulate the proper boundaryaccording to the comparative advantage of informal finance.

From macroeconomic angle, Ren and Zheng (2010) discusses the dynamic effects ofinformal finance on financial constraints of enterprises by taking informal finance as afactor into Euler investment model and in this expanded framework, it tests therelieving impact that informal finance has on the financial constraints of privateenterprises based on the listed private enterprises in China as the sample. This studyfinds that due to credit rationing and institutional discrimination within the systemunder financial suppression, investments of private enterprises in our country havehigh sensitivity to their internal cash flow and these enterprises are faced with strongfinancial constraints, while the expansion of informal finance has reduced such kind ofconstraints to a great extent. Besides, private enterprises transfer their reliance oninternal cash flow to informal finance in part, which exacerbates the company’sbusiness risk to some extent.

From interest rate angle, Li and Kuang (2010A) introduce the concept of invisiblecost in formal financial organizations to show that the informal financial interest ratenot only needs to refer to the formal financial interest rate but also contains theinvisible cost which borrowers need to pay when they accept the interest rate of formal

NBRI2,4

386

finance, they construct a partial equilibrium model to explain that invisible cost is themain reason for the high interest rate of informal finance and put forward somesuggestions for lowering invisible cost effectively. Pan and Luo (2009) developasymmetric-information oligopolistic model to analyze the informal financial market.When outside investors’ monitoring is quite easy, the equilibrium interest rate is lowand the project is financed with high investment level and vice versa. In China’s ruralarea, where people have deep social interaction with each other and entrepreneursinvest mostly in the labor-intensive business with low technology, outside investorseasily monitor entrepreneur, and good project is invested and the equilibrium informalfinancial market is characterized with low interest rate and high investment level. Thispaper also argues that it is the inefficiency of the formal financial system that leads tothe existence of informal financial equilibrium with high interest rate, which mayinduce local financial crises. Li and Kuang (2010B) prove that the formal financialagency has a inherent named “implied constraint” which increases borrower’s burden,and it is a crowd-out effect if borrower do not pay for the “implied constraint” throughthe comparison of informal finance and formal finance. They also explain how theborrowers choose formal or informal finance based on their own characteristics.

From institutions angle, Yao (2009) asserts that informal financial development inChina is significantly different among regions, which is related with commercialculture, financial support to private enterprises from formal finance, the degree ofprivate capital abundance and so on. Under the framework of the neo-classical theoryof economic growth, the paper empirically studies on the effect of financialdevelopment on economic growth through regional macroeconomic data. It finds thatregional differences of informal financial development provide a sound explanation forregional differences of economic growth. Through the re-construction of the indicatorof financial development degree, it shows that both the formal financial and informalfinancial have the significant effects on economic growth.

From real case angle, Lei and Deng (2009) analyze the informal finance situation inOrdos of Inner Mongolia where is a hot spot with widespread informal finance. Theyconclude that Ordos’ informal finance will evolve to formal finance even without theintervention of Chinese Government. However, the Chinese Government should notallow all the informal finance in Ordos to be formalized. It is optimal to allow theco-existence of both formal and informal finance in Ordos. Yao (2009) advocates thatthe reactive character of informal finance can provide an adequate explanation of themajority typical facts in Wenzhou’s informal financial market. The fact that Wenzhou’sinformal financial market is featured by reactive character is supported by relatedGranger causality test and impulse response analysis. Empirical analyses state thatcredit expansion to SMEs made by formal financial market has a significant impact onthe short-term trend of capital price of informal financial market. But the co-integrationanalysis shows that there does not exist a long-term balance relation between interestrate of informal financial market and the credit level of SMEs, so Wenzhou’s informalfinancial market should be understood based on an integrated analytical framework.

From the legalization angle, Xiao (2008) finds that the needs of normalization ofinformal finance emerges during the process of Chinese society transition. Thenormalization depends on whether the role of informal institutions as informationagencies can change into credit agencies. They advocate that the supervision authorityneeds to admit the legality of informal institutions. From the informal financial

Informal finance

387

volume angle, Wu and Deng (2010) shows that the population density of formal financehas distinctive effect on the environment volume of informal finance. The volume offormal and informal finance is largely affected by outside factors, such as income level,price level and interest rate level. Gao (2008) regards neutral “inform finance is legalized”as the route to choose. He also supports that China should adopt the passivism freesystem as for the inform finance and sets legal boundary for inform finance. For thoseinside the boundary, the government should grant legal status and for those outside theboundary, inform finance should be allowed to develop autonomously. Particularly,China Government should first regulate those nationwide and large-scale informalfinancial institutions.

Both literatures internationally and in China confirmed the advantages of informalfinance and trade credit in monitoring comparing to banking credit out of its closepeople or district proximity. While the researches that directly show the quantitativerelationship between informal finance, trade credit and the SME performance arescarcely seen. Our research definitely bridges the gap. Some researchers in Chinaattribute trade credit as one source of informal finance while our research separatetrade credit out from informal finance in that trade credit is the traditional wayenterprises undertake in daily operations and international research does not taketrade credit as informal finance channel. In our research, we asked separately on tradecredit financing and informal finance starting from the questionnaire. Informal financein our research refers to financing from non-bank institutions specifically.

The research on how informal finance and trade credit relive the tension of SMEcash chain is still not known either. Our data are from a random survey covering19 cities with 569 private firms responses conducted by three shareholding-banks fromJuly to December 2007. We find that:

(1) performance of private firms with informal financing and trade credit is betterthan those without;

(2) informal finance and trade credit are positively related to private firm return onasset (ROA), and positively related to private firm reinvestment rate; and

(3) Informal finance works better in manufacturing industry and trade creditfinancing works better in wholesale and trading industry.

The remainder of the paper is structured as follows: the section we introduces the dataand sample selection, Section 2 reports OLS regression results on SME performanceand Section 3 concludes and gave policy implication of the paper.

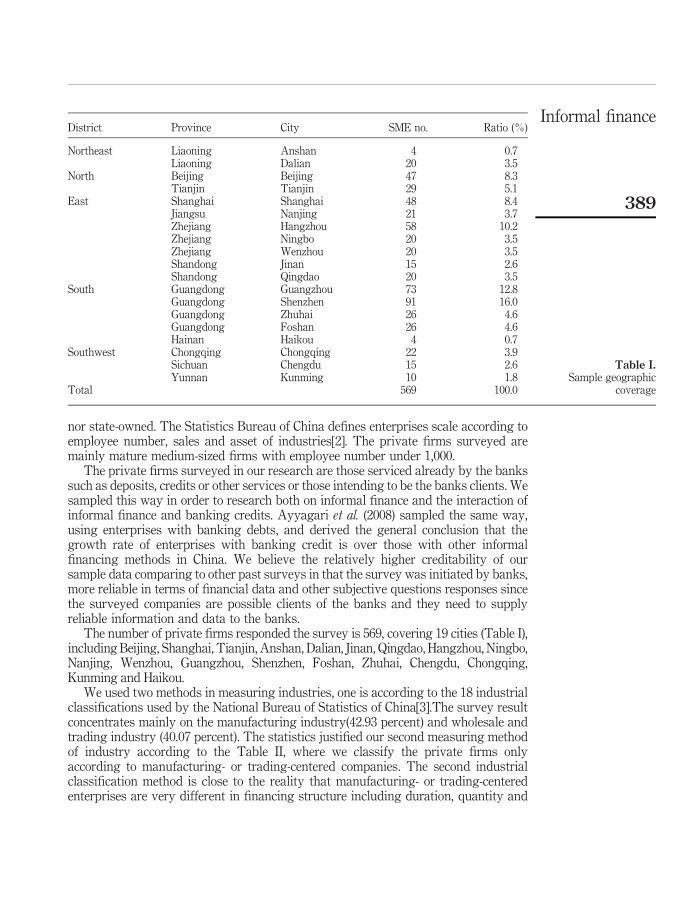

3. DataOur data are from a random survey conducted by provincial branches of three listedshareholding banks of China between July 2007 and December 2007. The surveys weresent to the private firms by e-mails and the private firms mailed filled surveys back tothe headquarters of the banks. To make the samples representative, we first chose thecities where the questioners were going to sent and calculated the numbers ofquestionnaires to collect according to the per capita GDP of each city and we stopcollecting questionnaires once we reach the pre-specified number. From Table I, we cansee that our samples cover major industrial areas randomly according to per capitaGDP in Eastern and Southern China. The financial data of the survey were fromthe end of 2004 to the end of 2006. Private firms are those firms that are neither listed

NBRI2,4

388

nor state-owned. The Statistics Bureau of China defines enterprises scale according toemployee number, sales and asset of industries[2]. The private firms surveyed aremainly mature medium-sized firms with employee number under 1,000.

The private firms surveyed in our research are those serviced already by the bankssuch as deposits, credits or other services or those intending to be the banks clients. Wesampled this way in order to research both on informal finance and the interaction ofinformal finance and banking credits. Ayyagari et al. (2008) sampled the same way,using enterprises with banking debts, and derived the general conclusion that thegrowth rate of enterprises with banking credit is over those with other informalfinancing methods in China. We believe the relatively higher creditability of oursample data comparing to other past surveys in that the survey was initiated by banks,more reliable in terms of financial data and other subjective questions responses sincethe surveyed companies are possible clients of the banks and they need to supplyreliable information and data to the banks.

The number of private firms responded the survey is 569, covering 19 cities (Table I),including Beijing, Shanghai, Tianjin, Anshan, Dalian, Jinan, Qingdao, Hangzhou, Ningbo,Nanjing, Wenzhou, Guangzhou, Shenzhen, Foshan, Zhuhai, Chengdu, Chongqing,Kunming and Haikou.

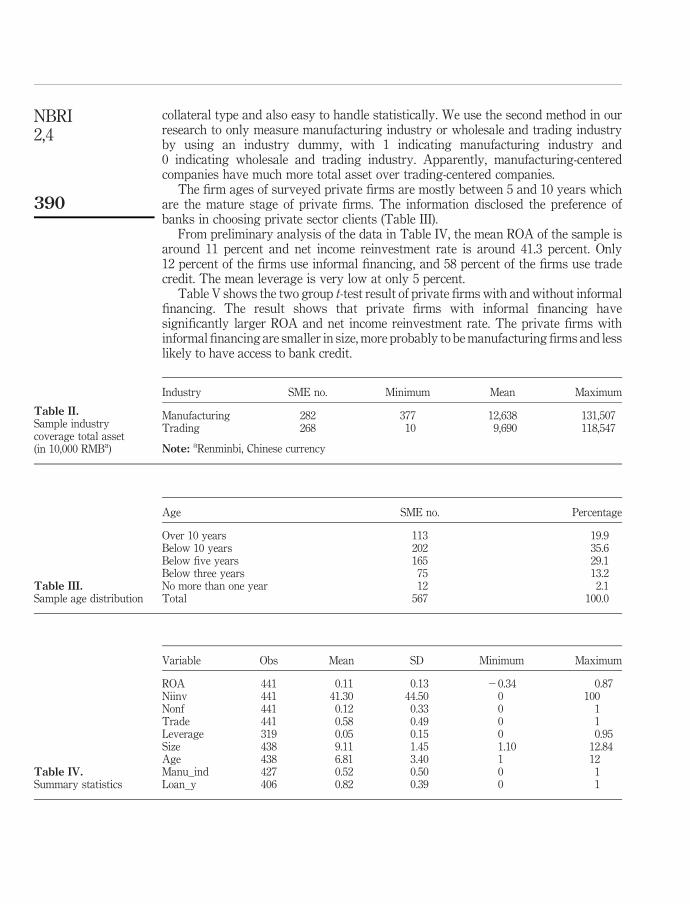

We used two methods in measuring industries, one is according to the 18 industrialclassifications used by the National Bureau of Statistics of China[3].The survey resultconcentrates mainly on the manufacturing industry(42.93 percent) and wholesale andtrading industry (40.07 percent). The statistics justified our second measuring methodof industry according to the Table II, where we classify the private firms onlyaccording to manufacturing- or trading-centered companies. The second industrialclassification method is close to the reality that manufacturing- or trading-centeredenterprises are very different in financing structure including duration, quantity and

District Province City SME no. Ratio (%)

Northeast Liaoning Anshan 4 0.7Liaoning Dalian 20 3.5

North Beijing Beijing 47 8.3Tianjin Tianjin 29 5.1

East Shanghai Shanghai 48 8.4Jiangsu Nanjing 21 3.7Zhejiang Hangzhou 58 10.2Zhejiang Ningbo 20 3.5Zhejiang Wenzhou 20 3.5Shandong Jinan 15 2.6Shandong Qingdao 20 3.5

South Guangdong Guangzhou 73 12.8Guangdong Shenzhen 91 16.0Guangdong Zhuhai 26 4.6Guangdong Foshan 26 4.6Hainan Haikou 4 0.7

Southwest Chongqing Chongqing 22 3.9Sichuan Chengdu 15 2.6Yunnan Kunming 10 1.8

Total 569 100.0

Table I.Sample geographic

coverage

Informal finance

389

collateral type and also easy to handle statistically. We use the second method in ourresearch to only measure manufacturing industry or wholesale and trading industryby using an industry dummy, with 1 indicating manufacturing industry and0 indicating wholesale and trading industry. Apparently, manufacturing-centeredcompanies have much more total asset over trading-centered companies.

The firm ages of surveyed private firms are mostly between 5 and 10 years whichare the mature stage of private firms. The information disclosed the preference ofbanks in choosing private sector clients (Table III).

From preliminary analysis of the data in Table IV, the mean ROA of the sample isaround 11 percent and net income reinvestment rate is around 41.3 percent. Only12 percent of the firms use informal financing, and 58 percent of the firms use tradecredit. The mean leverage is very low at only 5 percent.

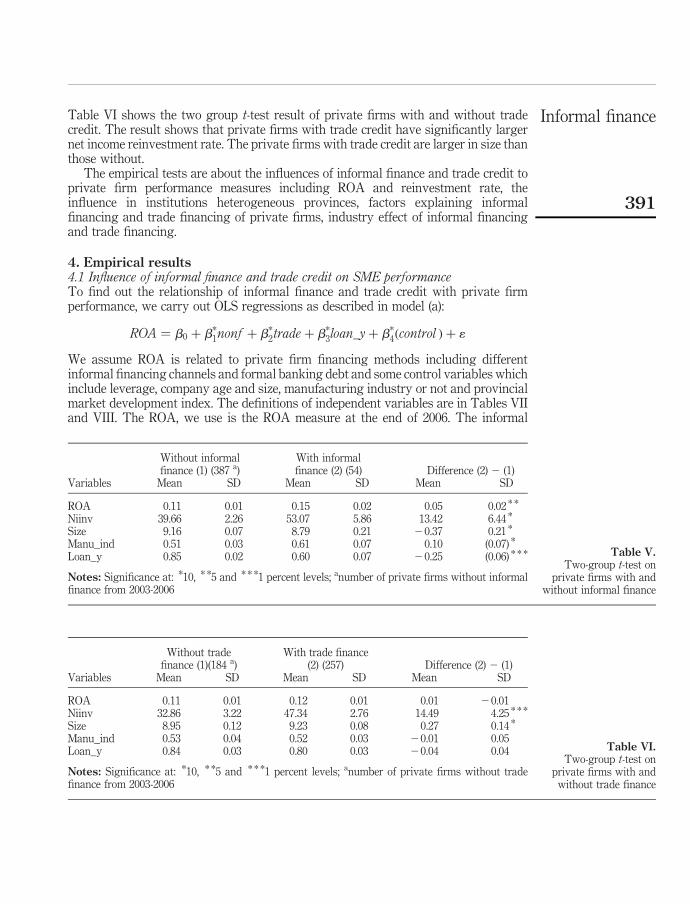

Table V shows the two group t-test result of private firms with and without informalfinancing. The result shows that private firms with informal financing havesignificantly larger ROA and net income reinvestment rate. The private firms withinformal financing are smaller in size, more probably to be manufacturing firms and lesslikely to have access to bank credit.

Variable Obs Mean SD Minimum Maximum

ROA 441 0.11 0.13 20.34 0.87Niinv 441 41.30 44.50 0 100Nonf 441 0.12 0.33 0 1Trade 441 0.58 0.49 0 1Leverage 319 0.05 0.15 0 0.95Size 438 9.11 1.45 1.10 12.84Age 438 6.81 3.40 1 12Manu_ind 427 0.52 0.50 0 1Loan_y 406 0.82 0.39 0 1

Table IV.Summary statistics

Age SME no. Percentage

Over 10 years 113 19.9Below 10 years 202 35.6Below five years 165 29.1Below three years 75 13.2No more than one year 12 2.1Total 567 100.0

Table III.Sample age distribution

Industry SME no. Minimum Mean Maximum

Manufacturing 282 377 12,638 131,507Trading 268 10 9,690 118,547

Note: aRenminbi, Chinese currency

Table II.Sample industrycoverage total asset(in 10,000 RMBa)

NBRI2,4

390

Table VI shows the two group t-test result of private firms with and without tradecredit. The result shows that private firms with trade credit have significantly largernet income reinvestment rate. The private firms with trade credit are larger in size thanthose without.

The empirical tests are about the influences of informal finance and trade credit toprivate firm performance measures including ROA and reinvestment rate, theinfluence in institutions heterogeneous provinces, factors explaining informalfinancing and trade financing of private firms, industry effect of informal financingand trade financing.

4. Empirical results4.1 Influence of informal finance and trade credit on SME performanceTo find out the relationship of informal finance and trade credit with private firmperformance, we carry out OLS regressions as described in model (a):

ROA ¼ b0 þ b*1nonf þ b*

2trade þ b*3loan_y þ b*

4ðcontrol Þ þ 1

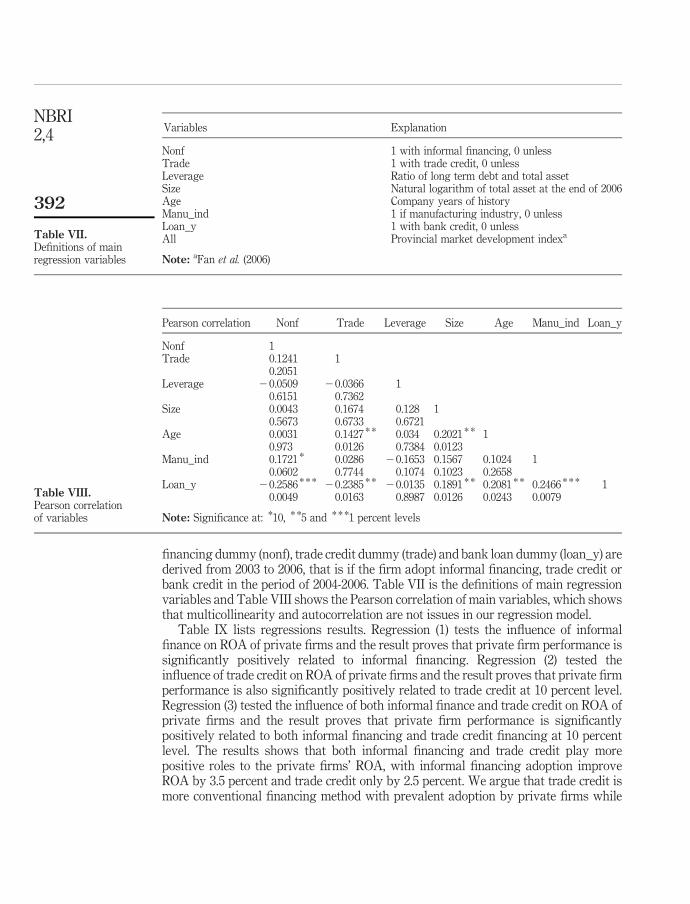

We assume ROA is related to private firm financing methods including differentinformal financing channels and formal banking debt and some control variables whichinclude leverage, company age and size, manufacturing industry or not and provincialmarket development index. The definitions of independent variables are in Tables VIIand VIII. The ROA, we use is the ROA measure at the end of 2006. The informal

Without informalfinance (1) (387 a)

With informalfinance (2) (54) Difference (2) 2 (1)

Variables Mean SD Mean SD Mean SD

ROA 0.11 0.01 0.15 0.02 0.05 0.02 * *

Niinv 39.66 2.26 53.07 5.86 13.42 6.44 *

Size 9.16 0.07 8.79 0.21 20.37 0.21 *

Manu_ind 0.51 0.03 0.61 0.07 0.10 (0.07) *

Loan_y 0.85 0.02 0.60 0.07 20.25 (0.06) * * *

Notes: Significance at: *10, * *5 and * * *1 percent levels; anumber of private firms without informalfinance from 2003-2006

Table V.Two-group t-test on

private firms with andwithout informal finance

Without tradefinance (1)(184 a)

With trade finance(2) (257) Difference (2) 2 (1)

Variables Mean SD Mean SD Mean SD

ROA 0.11 0.01 0.12 0.01 0.01 20.01Niinv 32.86 3.22 47.34 2.76 14.49 4.25 * * *

Size 8.95 0.12 9.23 0.08 0.27 0.14 *

Manu_ind 0.53 0.04 0.52 0.03 20.01 0.05Loan_y 0.84 0.03 0.80 0.03 20.04 0.04

Notes: Significance at: *10, * *5 and * * *1 percent levels; anumber of private firms without tradefinance from 2003-2006

Table VI.Two-group t-test on

private firms with andwithout trade finance

Informal finance

391

financing dummy (nonf), trade credit dummy (trade) and bank loan dummy (loan_y) arederived from 2003 to 2006, that is if the firm adopt informal financing, trade credit orbank credit in the period of 2004-2006. Table VII is the definitions of main regressionvariables and Table VIII shows the Pearson correlation of main variables, which showsthat multicollinearity and autocorrelation are not issues in our regression model.

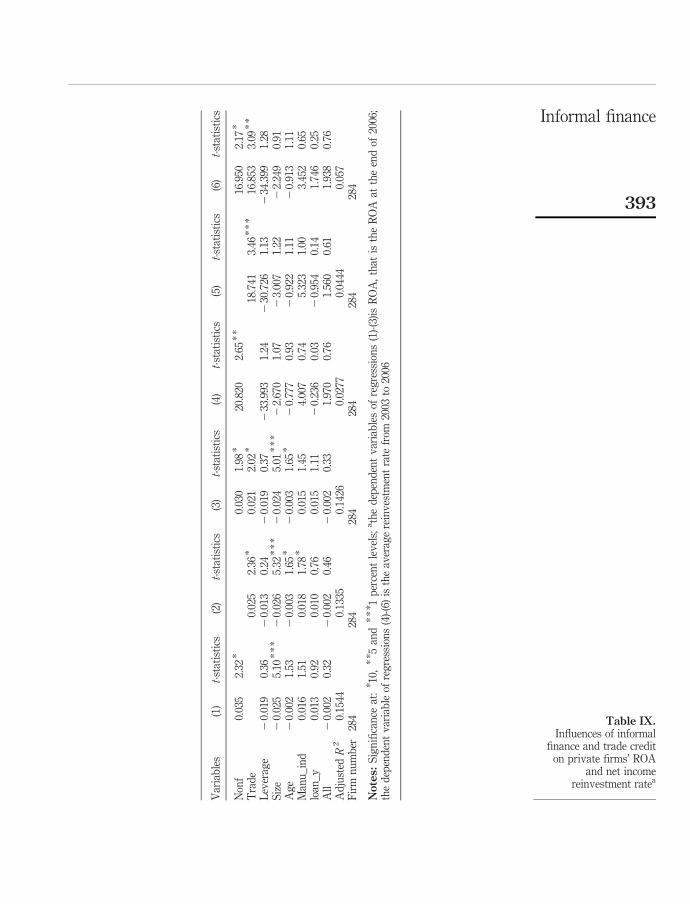

Table IX lists regressions results. Regression (1) tests the influence of informalfinance on ROA of private firms and the result proves that private firm performance issignificantly positively related to informal financing. Regression (2) tested theinfluence of trade credit on ROA of private firms and the result proves that private firmperformance is also significantly positively related to trade credit at 10 percent level.Regression (3) tested the influence of both informal finance and trade credit on ROA ofprivate firms and the result proves that private firm performance is significantlypositively related to both informal financing and trade credit financing at 10 percentlevel. The results shows that both informal financing and trade credit play morepositive roles to the private firms’ ROA, with informal financing adoption improveROA by 3.5 percent and trade credit only by 2.5 percent. We argue that trade credit ismore conventional financing method with prevalent adoption by private firms while

Pearson correlation Nonf Trade Leverage Size Age Manu_ind Loan_y

Nonf 1Trade 0.1241 1

0.2051Leverage 20.0509 20.0366 1

0.6151 0.7362Size 0.0043 0.1674 0.128 1

0.5673 0.6733 0.6721Age 0.0031 0.1427 * * 0.034 0.2021 * * 1

0.973 0.0126 0.7384 0.0123Manu_ind 0.1721 * 0.0286 20.1653 0.1567 0.1024 1

0.0602 0.7744 0.1074 0.1023 0.2658Loan_y 20.2586 * * * 20.2385 * * 20.0135 0.1891 * * 0.2081 * * 0.2466 * * * 1

0.0049 0.0163 0.8987 0.0126 0.0243 0.0079

Note: Significance at: *10, * *5 and * * *1 percent levels

Table VIII.Pearson correlationof variables

Variables Explanation

Nonf 1 with informal financing, 0 unlessTrade 1 with trade credit, 0 unlessLeverage Ratio of long term debt and total assetSize Natural logarithm of total asset at the end of 2006Age Company years of historyManu_ind 1 if manufacturing industry, 0 unlessLoan_y 1 with bank credit, 0 unlessAll Provincial market development indexa

Note: aFan et al. (2006)

Table VII.Definitions of mainregression variables

NBRI2,4

392

Var

iab

les

(1)

t-st

atis

tics

(2)

t-st

atis

tics

(3)

t-st

atis

tics

(4)

t-st

atis

tics

(5)

t-st

atis

tics

(6)

t-st

atis

tics

Non

f0.

035

2.32

*0.

030

1.98

*20

.820

2.65

**

16.9

502.

17*

Tra

de

0.02

52.

36*

0.02

12.

02*

18.7

413.

46*

**

16.8

533.

09*

*

Lev

erag

e2

0.01

90.

362

0.01

30.

242

0.01

90.

372

33.9

931.

242

30.7

261.

132

34.3

991.

28S

ize

20.

025

5.10

**

*2

0.02

65.

32*

**

20.

024

5.01

**

*2

2.67

01.

072

3.00

71.

222

2.24

90.

91A

ge

20.

002

1.53

20.

003

1.65

*2

0.00

31.

65*

20.

777

0.93

20.

922

1.11

20.

913

1.11

Man

u_

ind

0.01

61.

510.

018

1.78

*0.

015

1.45

4.00

70.

745.

323

1.00

3.45

20.

65lo

an_

y0.

013

0.92

0.01

00.

760.

015

1.11

20.

236

0.03

20.

954

0.14

1.74

60.

25A

ll2

0.00

20.

322

0.00

20.

462

0.00

20.

331.

970

0.76

1.56

00.

611.

938

0.76

Ad

just

edR

20.

1544

0.13

350.

1426

0.02

770.

0444

0.05

7F

irm

nu

mb

er28

428

428

428

428

428

4

Notes:

Sig

nifi

can

ceat

:* 1

0,*

* 5an

d*

** 1

per

cen

tle

vel

s;ath

ed

epen

den

tv

aria

ble

sof

reg

ress

ion

s(1

)-(3

)is

RO

A,

that

isth

eR

OA

atth

een

dof

2006

;th

ed

epen

den

tv

aria

ble

ofre

gre

ssio

ns

(4)-

(6)

isth

eav

erag

ere

inv

estm

ent

rate

from

2003

to20

06

Table IX.Influences of informal

finance and trade crediton private firms’ ROA

and net incomereinvestment ratea

Informal finance

393

unconventional financing method as informal financing adoption makes the differenceto private firms by meeting tight financing needs.

Besides the favoring roles of the informal financing and trade credit, interestingly tonote that formal banking loan play neglectful role to private firms’ performancemeasured by ROA, the bank loan dummy are not significant at all. The regressionresult also shows that as private firms grow older, the ROA decline.

4.2 Influence of informal finance and trade credit on net income reinvestment rateAfter deriving firm performance and growth results from previous regressions of(a) and (b), to further explore the relationship between alternative financing channels ofinformal finance and trade credit on private firm investment behavior, We use firm netincome reinvestment rate as the dependent variable while independent and controlvariables remain the same. The OLS regression is described in model (c):

Niinv ¼ b0 þ b*1nonf þ b*

2trade þ b*3loan_y þ b*

4ðcontrol Þ þ 1

We assume the average net income reinvestment rate of the private firms between theyear of 2003 and 2006 is related to private firm financing methods including differentinformal financing channels and formal banking debt and some control variableswhich include leverage, company age and size, manufacturing industry or not andprovincial market development index. The definitions of independent variables are inTables VII and VIII.

Table IX lists regressions results using the same set of control variables and netincome reinvestment rate is the average rate from 2003 to 2006. Regression (4) testedthe influence of informal finance on net income reinvestment rate of private firms andthe result proves that private firm performance is significantly positively related toinformal financing at 5 percent level. Regression (5) tested the influence of trade crediton net income reinvestment rate of private firms and the result proves that private firmperformance is also significantly positively related to trade credit at 1 percent level.Regression (6) tested the influence of both informal finance and trade credit on netincome reinvestment rate of private firms and the result proves that private firmperformance is significantly positively related to both informal financing at 10 percentlevel and trade credit financing at 5 percent level. The results suggest that informalfinance and trade credit are positively associated with private firm net incomereinvestment rate both in scale and in the significance level while the bank loandummy (loan_y) is negative consistently from (7) to (8). We argue that private firmsusing alternative financing channels tend to invest more from self-accumulatedresources instead of from banking credit and private firms using formal financingchannel (bank loan) tend to invest less of net income. Our result suggest that peckingorder financing theory is not applicable for private firms in China, whereas thefinancing capability from formal channel of bank loan is one of the determinants of thenet income reinvestment rate among private firms.

4.3 Robustness testsWe carried out the robustness tests using two substitutes of informal finance dummyand trade credit dummy. Regression (1) use the informal finance percentage as of totaldebt as the main variable of interest and (2) use the number of trade finance partners ofa firm as the main variable of interest.

NBRI2,4

394

From Table X the dependent variable of regression is ROA, that is the ROA at theend of 2006, the results of (1) and (2) are similar to the base result in Table IX thatinformal finance and trade credit are conducive to private firms’ performance.

The robustness test of the positive effect of informal finance and trade credit on netincome reinvestment rate is carried out by reducing samples of state-owned enterprises,listed firms and joint venture firms, and the results significance remain the same[4].

We tried 2SLS to solve the reverse causality issue in the regression model while didnot find proper IV in that our data are based on survey where only one year enterprisescharacteristics are available. In addition, the surveyed enterprises are all privatecompanies, we did not ask about ownership questions in the questionnaire. We use thesales growth from 2003 to 2006 to proxy enterprise growth and use the ratio of sales overemployee number to proxy productivity. After controlling the growth and productivity,the regression results remain.

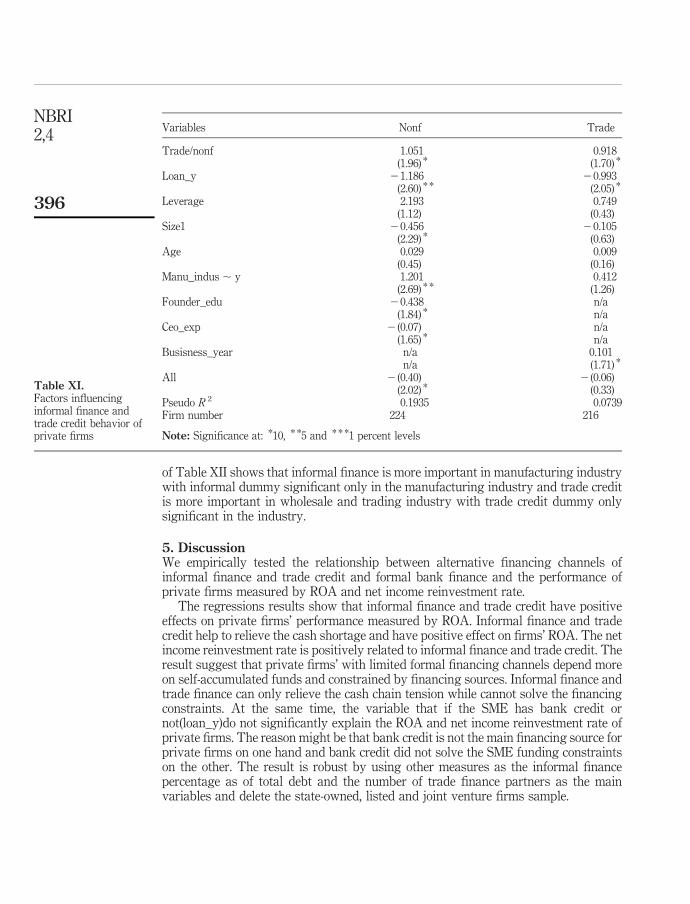

4.4 Factors influencing informal financing and trade credit behavior of private firmsBy exploring the factors that influences private firms’ informal financing and trade creditbehavior, We find from Table XI that informal finance is related to trade credit and bankfinancing, industry and size matter to informal finance while not to trade credit, foundereducation level and CEO industry experience are negatively related to informal financingbehavior both at 10 percent level and the time private firm conduct business with apartner significantly influence trade credit adoption with the partner at 10 percent level.

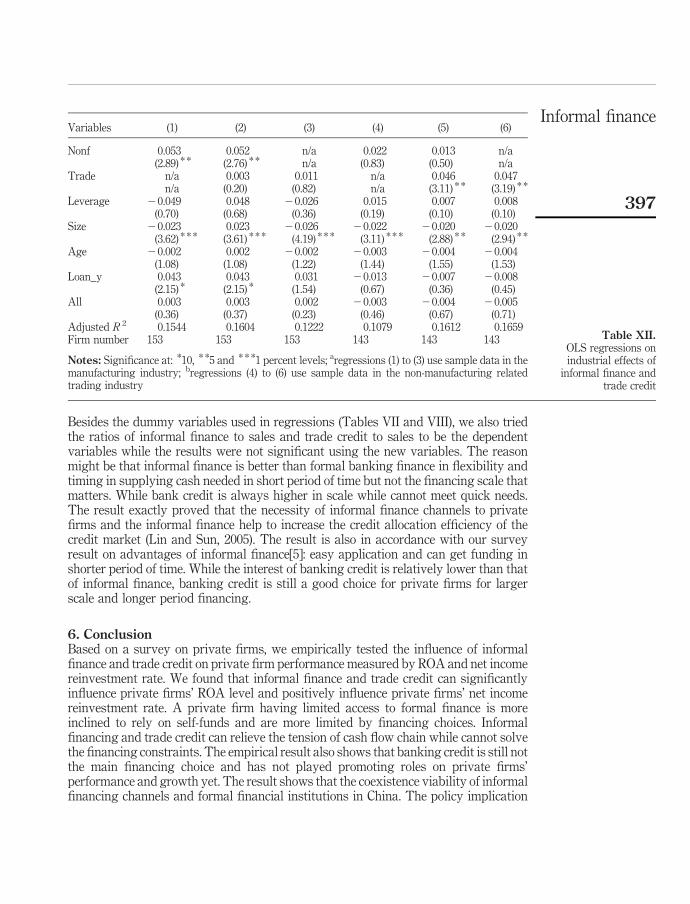

4.5 Industrial preference on informal financing and trade credit behavior of private firmsFrom results of previous section, industry matters to informal finance and trade creditfinancing behavior of private firms, We thus divide the full sample to sub-samples ofmanufacturing industry (1)-(3) and wholesale and trading industry (4)-(6), the result

Variables (1) (2)

Substitute 0.152 0.116(2.36) * (2.16) *

Leverage 20.021 0.0004(0.39) (0.01)

Size 20.024 20.026(5.01) * * * (5.49) * * *

Age 20.002 20.002(1.52) (1.55)

Manu_ind 0.015 0.020(1.46) (1.96) *

Loan_y 0.012 0.008(0.86) (0.57)

All 20.001 20.004(0.22) (0.76)

Adjusted R 2 0.134 0.131Firm number 284 284

Notes: Significance at: *10, * *5 and * * *1 percent levels; athe dependent variable of regression (1) and(2) are both ROA of 2005; substitute of (1) is the informal finance percentage as of total debt andsubstitute of (2) is the number of trade finance partners of a firm

Table X.Robustness tests of

influences of informalfinance and trade crediton private firms’ ROAa

Informal finance

395

of Table XII shows that informal finance is more important in manufacturing industrywith informal dummy significant only in the manufacturing industry and trade creditis more important in wholesale and trading industry with trade credit dummy onlysignificant in the industry.

5. DiscussionWe empirically tested the relationship between alternative financing channels ofinformal finance and trade credit and formal bank finance and the performance ofprivate firms measured by ROA and net income reinvestment rate.

The regressions results show that informal finance and trade credit have positiveeffects on private firms’ performance measured by ROA. Informal finance and tradecredit help to relieve the cash shortage and have positive effect on firms’ ROA. The netincome reinvestment rate is positively related to informal finance and trade credit. Theresult suggest that private firms’ with limited formal financing channels depend moreon self-accumulated funds and constrained by financing sources. Informal finance andtrade finance can only relieve the cash chain tension while cannot solve the financingconstraints. At the same time, the variable that if the SME has bank credit ornot(loan_y)do not significantly explain the ROA and net income reinvestment rate ofprivate firms. The reason might be that bank credit is not the main financing source forprivate firms on one hand and bank credit did not solve the SME funding constraintson the other. The result is robust by using other measures as the informal financepercentage as of total debt and the number of trade finance partners as the mainvariables and delete the state-owned, listed and joint venture firms sample.

Variables Nonf Trade

Trade/nonf 1.051 0.918(1.96) * (1.70) *

Loan_y 21.186 20.993(2.60) * * (2.05) *

Leverage 2.193 0.749(1.12) (0.43)

Size1 20.456 20.105(2.29) * (0.63)

Age 0.029 0.009(0.45) (0.16)

Manu_indus , y 1.201 0.412(2.69) * * (1.26)

Founder_edu 20.438 n/a(1.84) * n/a

Ceo_exp 2 (0.07) n/a(1.65) * n/a

Busisness_year n/a 0.101n/a (1.71) *

All 2 (0.40) 2 (0.06)(2.02) * (0.33)

Pseudo R 2 0.1935 0.0739Firm number 224 216

Note: Significance at: *10, * *5 and * * *1 percent levels

Table XI.Factors influencinginformal finance andtrade credit behavior ofprivate firms

NBRI2,4

396

Besides the dummy variables used in regressions (Tables VII and VIII), we also triedthe ratios of informal finance to sales and trade credit to sales to be the dependentvariables while the results were not significant using the new variables. The reasonmight be that informal finance is better than formal banking finance in flexibility andtiming in supplying cash needed in short period of time but not the financing scale thatmatters. While bank credit is always higher in scale while cannot meet quick needs.The result exactly proved that the necessity of informal finance channels to privatefirms and the informal finance help to increase the credit allocation efficiency of thecredit market (Lin and Sun, 2005). The result is also in accordance with our surveyresult on advantages of informal finance[5]: easy application and can get funding inshorter period of time. While the interest of banking credit is relatively lower than thatof informal finance, banking credit is still a good choice for private firms for largerscale and longer period financing.

6. ConclusionBased on a survey on private firms, we empirically tested the influence of informalfinance and trade credit on private firm performance measured by ROA and net incomereinvestment rate. We found that informal finance and trade credit can significantlyinfluence private firms’ ROA level and positively influence private firms’ net incomereinvestment rate. A private firm having limited access to formal finance is moreinclined to rely on self-funds and are more limited by financing choices. Informalfinancing and trade credit can relieve the tension of cash flow chain while cannot solvethe financing constraints. The empirical result also shows that banking credit is still notthe main financing choice and has not played promoting roles on private firms’performance and growth yet. The result shows that the coexistence viability of informalfinancing channels and formal financial institutions in China. The policy implication

Variables (1) (2) (3) (4) (5) (6)

Nonf 0.053 0.052 n/a 0.022 0.013 n/a(2.89) * * (2.76) * * n/a (0.83) (0.50) n/a

Trade n/a 0.003 0.011 n/a 0.046 0.047n/a (0.20) (0.82) n/a (3.11) * * (3.19) * *

Leverage 20.049 0.048 20.026 0.015 0.007 0.008(0.70) (0.68) (0.36) (0.19) (0.10) (0.10)

Size 20.023 0.023 20.026 20.022 20.020 20.020(3.62) * * * (3.61) * * * (4.19) * * * (3.11) * * * (2.88) * * (2.94) * *

Age 20.002 0.002 20.002 20.003 20.004 20.004(1.08) (1.08) (1.22) (1.44) (1.55) (1.53)

Loan_y 0.043 0.043 0.031 20.013 20.007 20.008(2.15) * (2.15) * (1.54) (0.67) (0.36) (0.45)

All 0.003 0.003 0.002 20.003 20.004 20.005(0.36) (0.37) (0.23) (0.46) (0.67) (0.71)

Adjusted R 2 0.1544 0.1604 0.1222 0.1079 0.1612 0.1659Firm number 153 153 153 143 143 143

Notes: Significance at: *10, * *5 and * * *1 percent levels; aregressions (1) to (3) use sample data in themanufacturing industry; bregressions (4) to (6) use sample data in the non-manufacturing relatedtrading industry

Table XII.OLS regressions onindustrial effects of

informal finance andtrade credit

Informal finance

397

is that the government should take careful steps to regulate informal financing sourcesto promote the positive facet and avoid the destabilizing role and set up multi-facetedfunding resources for private firms to better meet private firms’ financing needs. Theresult empirically proves the theory by Lin and Sun (2005) that informal finance isnecessary and can improve the financing efficiency of the credit market. Informalfinance is more important to promote performance in manufacturing industry whiletrade credit is more effective in wholesale and trading industry.

Living conditions of private firms need to be improved continuously and thecountry should consider private sector financing conditions before deciding onmacroeconomic policies. While it is a long process for capital markets development,private firms enjoy little opportunity in direct financing. Venture capital and privateequity developed fast in the past several years, while they mostly concentrate onhigh-tech or mature pre-IPO firms and their help to most private firms are neglect able.Banking-led financing market still plays a major financing role for state-ownedenterprises in China. Private firms of course sought to bank credit in the first placewhile retained earnings, informal finance and trade credit are life-blood of private firmswhich supplement immediate cash needs. The China Government should createa multi-faceted financing system for private firms such as accelerating private firms’access to capital market, encourage private sector credit in small banks, prudentlyregulate informal finance and trade credit and other informal financing channels andset up SME credit guarantee system to support private firms long time development.

Large enterprises and groups gradually seek financing through capital marketinstead of from banking credit and private firms are becoming the steady client sourceof commercial banks. Banks should re-engineer process and adjust organizationstructure to catering to private firms needs, and innovate on new financial products.Private firms are generally lack of collateral and the banks are better off to innovate onrelationship based, pure credit based, bundling based, sales order based or supplychain based products especially for private firms.

Comparing to bank credit, informal finance and trade credit are popular amongprivate firms. Chinese private firms borrow from informal sources and make full use oftrade credit. It is believed that informal finance and trade credit are easier to obtain andcan immediate meet their needs. Of course, besides the positive effects, informalfinance sometimes causes trouble such as delayed payments and defaults, which arenot easily supported by current legal systems. A series of carefully designedalternative financing mechanisms by China Government would help on the growth ofChina private sector development.

Notes

1. National Bureau of Statistics of China.

2. Refer to www.stats.gov.cn/tjbz/t20061018_402369829.htm

3. Refer to www.stats.gov.cn/tjbz/

4. There are 39 state-owned, listed and joint venture firms in total consist of 6.84 percent of thewhole sample.

5. In the answer of advantages of informal finance, 77.40 percent SMEs surveyed agree thatinformal finance is easy in application process; 76.60 percent agree that they can get thefunding in the quicker way; 38.70 percent agree that informal finance need no collateral.

NBRI2,4

398

References

Allen, F., Qian, J. and Qian, M. (2005), “Law, finance, and economic growth in China”, Journal ofFinancial Economics, Vol. 77, pp. 57-116.

Audretsch, B.D. (2003), “Standing on the shoulders of midgets: the US small business innovationresearch program (SBIR)”, Small Business Economics, Vol. 20, pp. 129-35.

Ayyagari, M., Demirguc-Kunt, A. and Maksimovic, V. (2008), “Formal versus informal finance:evidence from China”, World Bank Policy Research Working Paper, No. 4465, available at:SSRN: http://ssrn.com/abstract¼1080690

Besley, T. and Coate, S. (1995), “Group lending, repayment incentives and social collateral”,Journal of Development Economics, Vol. 46 No. 1, pp. 1-18.

Bose, P. (1998), “Formal-informal sector interaction in rural credit markets”, The Journal ofDevelopment Economics, Vol. 56, pp. 265-80.

Berger, A.N. and Udell, G.F. (1992), “Some evidence on the empirical significance of creditrationing”, Journal of Political Economy, Vol. 100 No. 5, pp. 1047-77.

Berger, A.N. and Udell, G.F. (1995), “Relationship lending and lines of credit in small firmfinance”, Journal of Business, Vol. 68 No. 3, pp. 351-82.

Bottomley, A. (1975), “Interest rate determination in underdeveloped rural areas”, AmericanJournal of Agricultural Economics, Vol. 57 No. 2, pp. 279-91.

Cull, R. and Xu, C.L. (2005), “Institutions, ownership, and finance: the determinants of profitreinvestment among Chinese firms”, Journal of Financial Economics, Vol. 77, pp. 117-46.

De Meza, D.D. and Webb, D.C. (1987), “Too much investment: a problem of asymmetricinformation”, The Quarterly Journal of Economics, Vol. 102 No. 2, pp. 281-92.

Fan, G., Wang, X. and Zhu, H. (2006), NERI Index of Marketization of China’s Provinces 2006Report, Economic Science Press, Beijing.

Gao, B. (2008), “Legalization boundary and path of informal finance”, Chinese Legal Studies,Vol. 4 (in Chinese).

Lei, L.-J. and Deng, X.-D. (2009), “The evolution and way out of ordos informal finance”, Journalof Inner Mongolia University (Philosophy and Social Sciences), Vol. 41 No. 5 (in Chinese).

Li, F. and Kuang, H. (2010a), “An explanation of high interest rate of informal finance based onshort-term partial equilibrium”, Economic Survey, Vol. 1 (in Chinese).

Li, F. and Kuang, H. (2010b), “Why financing on informal financial market? Analysis based onborrower’s choice”, Nankai Economic Studies, Vol. 2 (in Chinese).

Lin, Y. and Li, Y. (2001), “Promoting the growth of medium and small-sized enterprises throughthe development of medium and small-sized financial institutions”, Economic ResearchJournal, Vol. 6, pp. 10-18 (in Chinese).

Lin, Y. and Sun, X. (2005), “Information, informal finance and SME financing”, EconomicResearch Journal, Vol. 7, pp. 35-44 (in Chinese).

Mauri, A. (2000), “Informal finance in developing economies”, UNIMI Economics Working Paper,No. 9, available at: SSRN: http://ssrn.com/abstract¼667262

Pan, S. and Luo, D. (2009), “Why the informal financial market plays an important role inChina?”, Southern Economy, Vol. 5 (in Chinese).

Peng, X. (2008), “The growth of informal finance: an analysis based on society transition”,Journal of Finance and Economics, Vol. 34 (in Chinese).

Petersen, M.A. and Rajan, R.G. (1994), “The benefits of lending relationships: evidence fromsmall business data”, The Journal of Finance, Vol. XLIX No. 1, pp. 3-37.

Informal finance

399

Ren, S.-M. and Zheng, Y. (2010), “Empirical study on reducing impacts of informal finance on thefinancial constraints of private enterprises”, Tongji University Journal Social ScienceSection, Vol. 21 No. 5 (in Chinese).

Stiglitz, J.E. (1990), “Peer monitoring and credit markets”, World Bank Economic Review, Vol. 4No. 3, pp. 393-410.

Stiglitz, J.E. and Weiss, A. (1981), “Credit rationing in markets with imperfect information”,The American Economic Review, Vol. 71 No. 3, pp. 393-410.

Wang, L., Wu, H.-F. and Yao, G.-N. (2009), “Complementation, substitution and transformation –the relationship between regular and irregular finance”, Economic Survey, Vol. 5(in Chinese).

Wu, L. and Deng, M. (2010), “The symbiosis model between formal and informal finance and itsempirical study from financial ecosystem”, Collected Essays on Finance and Economics,September (in Chinese).

Yang, F. (2008), “Researches on the informal financial ecology on a perspective of financialecological environment”, Economist, Vol. 5 (in Chinese).

Yao, Y.-J. (2009), “Regional differences of informal financial: development and its impact oneconomic growth”, Journal of Finance and Economics, Vol. 35 No. 12 (in Chinese).

Zhang, X.-H. (2009), “Study on the normative development boundary of civil finance in China”,The Theroy and Practice of Finance and Economics, Vol. 30 No. 157 (in Chinese).

Further reading

Allen, B.N. and Gregory, F.U. (1995), “Relationship lending and lines of credit in small firmfinance”, Journal of Business, Vol. 68 No. 3, pp. 351-82.

Beck, T., Demirguc-Kunt, A. and Maksimovic, V. (2008), “Financing patterns around the world:are small firms different”, Journal of Financial Economics, Vol. 89, pp. 467-87.

Montiel, P.J., Agenor, P.R. and Haque, N.U. (1993), Informal Financial Markets in DevelopingCountries, Basil Blackwell, Oxford.

Peng, W.-P. and Xiao, J.-H. (2008), “The growth of informal finance: an analysis based on societytransition”, Journal of Finance and Economics, Vol. 34 (in Chinese).

Petersen, M.A. and Raghuram, R.G. (1994), “The benefits of lending relationships: evidence fromsmall business data”, The Journal of Finance, Vol. XLIX No. 1, pp. 3-37.

Stiglitz, J.E. and Andrew, W. (1981), “Credit rationing in markets with imperfect information”,The American Economic Review, Vol. 71 No. 3, pp. 393-410.

Yao, Y.-J. (2009), “Informal financial market: reactive or autonomous, an ampirical study oninterest rate of informal financial market in Wenzhou”, Journal of Finance and Economics,Vol. 35 No. 4 (in Chinese).

About the authors

Jun Su received a Finance PhD degree from the Chinese University of Hong Kongin 2009. She is now an Assistant Professor in the Business School of BeijingTechnology and Business University, teaching Financial Management. She isalso a member of CFA Institute, American Accounting Association, AmericanFinance Association, and Asian Finance Association. She has published refereedjournal papers in Chinese Journals and in SSCI indexed journals such as FinanceForum, Journal of Business Ethics and The Chinese Economy over recent years.

NBRI2,4

400

Yuefan Sun received her Management PhD degree from Renmin University ofChina in 2009. She was also co-trained by Paul Merage School of Business atUniversity of California, Irvine, sponsored by China Scholarship Council. She isnow an Assistant Professor in the Business School of Beijing Technology andBusiness University. She is also a post-doctor in Guanghua School ofManagement, Peking University. She is also a member of American AccountingAssociation, American Management Association, Chinese Institute of Certified

Public Accountants, and China Certified Tax Agents Association. In the past three years, she hasbeen published in top Chinese journals such as Accounting Research and presented andmoderated in famous international conferences such as American Accounting AssociationAnnual Meeting, and Asian Pacific Conference on International Accounting Issues. Yuefan Sunis the corresponding author and can be contacted at: [email protected]

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints

Informal finance

401