Embed Size (px)

Citation preview

© 2013 Research Academy of Social Sciences http://www.rassweb.com 52

International Journal of Empirical Finance

Vol. 1, No. 3, 2013, 52-64

Influence of Interest Rates Regimes on Deposit Money Banks’ Credit

in Nigeria: An Econometric Assessment

Nwakanma Prince Chinaecherem1, Ifeanyi Mgbataogu

2

Abstract

The paper examines the impact of interest rates reform on the financial intermediation function of the

commercial banks in Nigeria using the dummy variables approach to Chow test for Structural Stability. The co-integration and error correction model were also used to capture both the long-run and short-run dynamics

of the variables used in the model. The empirical results reveal that though the intermediation function of the

commercial banks has significantly improved as a result of the deregulation of the interest rate, it has not translated into improved standard of living of the populace as the incidence of poverty is still on the increase.

Also, the results show that lending rates do not influence demand for domestic credits in Nigeria, unlike

deposit rates which proved to be a major determinant for amount of credits extended by the commercial

banks. We conclude that though, interest rates deregulation has improved credit extension to the domestic economy, the link between interest rates, domestic credit extension and economic growth is not automatic.

Hence, the need for partial deregulation of interest rates that will ensure concessionary interest rates to the

productive sector of the economy. Commercial banks are also advised to device better strategies that will boost their credit mobilization ability to ensure their profitability and sustain credit extension to the

productive sector of the economy.

1. Introduction

Deposit money banks tend to wield tremendous influence on every nation’s financial landscape. This makes them the primary focus of the monetary authorities in the task of managing the country’s economy. As

financial intermediaries they serve as a conduit through which funds are drawn from surplus economic

entities for allocation to deficit economic units. The essence of financial intermediation is to facilitate the process of economic growth and its concomitant economic development, all things being equal. A critical

factor in the act of financial intermediation is interest rate, which is the compensation borrowers pay to

lenders for making use of their money for a period of time after which the initial amount they borrowed is

returned to the lender. The attainment of efficient financial intermediation is therefore the primary objective of monetary authorities both in developed and emerging economies.

Efficient financial intermediation ensures the optimal mobilization and allocation of funds in the

economy. This enhances productivity and accelerates the pace of economic growth and development. Thus, the banking sector which is the core of the financial system is a major factor in determination of interest

rates. It is generally known that interest rates exhibit a term structure, which is to say that the interest rate

payable on a loan is, in most cases, predicated on its tenure. It is therefore characteristic of an efficient financial system to channel funds to their most productive uses. Since by definition long-term investments

are more productive than short-term investments it is expected that interest rates on short-term funds should

lag behind the rates on long-term funds needed for developmental activities. If however, interest rates in the money markets are upward bound the tendency is for those of the capital markets to drift even higher with

the unfavourable consequence of discouraging investment.

1 Senior Lecturer, University of Port Harcourt, Choba. 2 Research Assistant, University of Port Harcourt. Choba.

International Journal of Empirical Finance

53

Given the quest for the rapid economic growth and development of Nigeria the Central Bank of Nigeria was in addition to its traditional functions required to engineer the overall economic development of the

country. Consequently, in consonance with the then prevailing era of financial regulation the nation through

its central bank conformed to the general tendency towards financial regulation involving administrative

allocation of credit and fixing of interest rates. This mode of credit allocation and interest rate determination is what McKinnon (1973) and Shaw (1973) in their separate seminal papers referred to as financial

repression. This is characteristic of a country which keeps its deposit and lending nominal interest rates at

low levels relative to inflation.

Severe macroeconomic and financial disequilibrium prevalent in the early 1980’s coerced the Nigerian

state to initiate series of economic and financial policy reforms beginning with the Structural Adjustment

Programme (SAP) in 1986, a policy instrument designed to free the economy from the shackles of regulation and launch it on the path of deregulation. This would mark the entry of Nigeria into the league of emerging

markets. One of the foremost markets to be deregulated was the foreign exchange market, which commenced

on a gradual note whereby the exchange rate of the naira was partially determined by the forces of supply and demand. This was followed by interest rate deregulation in August 1987, (Ikhide and Alawode, 2001).

As a matter of fact, interest rate reform, which was geared towards financial sector liberalization was

cardinally designed to instill efficiency in the financial sector and coextensively lead to its deepening, Obamuyi (2009). This was also to rebuild what was allegedly referred to as the “tunnel-like” structure of

interest rate with its propensity to discourage savings and retard growth because of the perceived nexus

between savings, investment and economic growth, Ojo(1976). The problem which this study addresses is: if interest rate liberalization policy is indeed a panacea for enhancing financial intermediation, has the policy

had any positive influence on the potentials of the banking sector to increase resource allocation to the

domestic private sector so as to enable it drive the economy towards the desired level of economic growth

and development?

Banks allocate credit to the productive sectors in the form of loans and advances. The ability of banks to

mobilize funds underscores their capacity to allocate those funds to various uses in the economy. This

lending function ensures that developmental projects like industrial, housing, commercial and agricultural activities in the economy are well funded. In this way, the lending function of banks can be said to be

directly related to the development of the economy.

This study aims to investigate the relationship between interest rates reform policy and the level of financial intermediation in Nigeria. This is important because the idea behind the reform policies was for

interest rates to act as a kind of incentive by which sufficient deposits will be mobilized for onward lending

to deserving borrowers within the domestic economy. In the process the level of investment will increase and consequently the level of economic growth and development of the country. This paper is an attempt to shed

more light on interest rate policy and its implications for the lending operations of deposit money banks. It is

hoped that the country’s policy makers would as a result gain more insight into the vital role of interest rates on credit to the economy.

2. Literature Review and theoretical framework

The neoclassical growth model and the McKinnon-Shaw hypothesis x-rayed the association between

interest rates and economic growth. McKinnon-Shaw (1973) argued that financial repression reduces real rate of growth. Financial repression according to the authors refers to indiscriminate distortions of financial

prices including interest rates. In McKinnon-Shaw model, an investment function responds negatively to the

effective real loan rate of interest and positively to the growth rate. Those that follow this school of thought

expect financial liberalization to exert a positive effect on the rate of economic growth in both the short and medium runs.

Prior to McKinnon-Shaw model, the Fisher (1930) hypothesis suggests that expected inflation is the main determinant of interest rates as the inflation rate increases by one percent, the rate of interest increases

N. P. Chinaecherem & I. Mgbataogu

54

by one percent. This suggests that expected interest rates changes in proportion to the changing expected inflation, or expected real interest rates are invariant to the expected inflation. Mundell (1963) concluded that

nominal interest rate with expected inflation rate do not have one for one adjustable relations. It is the

Mundell-Tobin effect that nominal interest rates would rise less than one-for-one with inflation because in

response to inflation the public would hold less in money balances and more in other assets, which would drive interest rates down.

Emery (1971) in a paper presentation titled “the use of interest rate policies as a stimulus to economic growth”, submitted that government of few less developed countries were beginning to view interest rate

policy as one of their major discretionary policy variables – along with monetary and fiscal policy - in their

efforts to stimulate economic growth and – when appropriate – to reduce inflationary pressure. According to

him “this change in attitude has been caused in part by the experience of Taiwan, Korea and Indonesia following the introduction of substantial change in the interest rate structure, particularly for time and

savings deposits”.

Omole and Falokun (1999) analyzed empirically the linkages among and leverage ratios (debt-to-equity ratio and debt-to-capital ratio) of selected firms, their investment, turnover and profits. The result of the study

showed a link between interest rates and corporate financing strategies and profitability of firms. It also

revealed that interest rate liberalization has a link with growth of the equity market but on sector by sector analysis it does not seem to have the same effect on all investigated quoted companies.

Oosterbaan et al (2000) estimated the relationship between the annual rate of economic growth and the

real rate of interest. The study shows the effect of a rising real interest rate on growth and claimed that growth is maximized when the real rate of interest lies within the normal range of say -5 to 15 per cent. De

Gregorio and Guidotti (1995) cited in Oosterbaan et al (2000) suggest that the relationship between real

interest rates and economic growth might resemble an inverted U-curve - very low (and negative) real interest rates tend to cause financial disintermediation and hence reduce growth. However, the World Bank

reports, cited in Oosterbaan et al (2000) show a positive and significant cross-section relationship between

average growth and real interest rates over the period 1965 to 1985.

Adebiyi and Babatope-Obasa (2004) investigated the impact of interest rates and other macroeconomic factors on manufacturing performance in Nigeria using co-integration and an error correction mechanism

(ECM) technique with annual time series covering the period between 1970 and 2002. The study revealed that interest rate spread and government deficit financing have negative impact on the growth of

manufacturing sub-sector in Nigeria. Again, the liberalization of the economy has promoted manufacturing

growth during the period covered by the study.

Albu (2006) used two partial models to investigate the impact of investment on GDP growth rate and the relationship between interest rate and investment in the case of Romanian economy. He found that the

behavior of the national economic system and the interest rate-investment-economic growth relationships

tend to converge to those demonstrated in a normal economy.

Amidu (2006) examined whether bank lending is constrained by monetary policy in Ghana. The study

revealed that Ghanaian banks’ lending behaviors are affected significantly by the country’s economic activities and changes in money supply, supporting previous studies that the Ghanaian Central Bank’s prime

rate and inflation rate negatively but statistically insignificantly affect bank lending.

Shelile (2006) examined the predictive ability of the term structure of interest rates on economic activity, and the effects of different monetary policy regimes on the predictive ability of the term spread.

Results of the study established that the term structure successfully predicted real economic activity during

the entire research period with the exception of the last sub-period (2000-2004) when using the multivariate

model. In the periods of financial market liberalization and interest rates deregulation, the term structure was to be a better predictor of economic activity in South Africa.

Ologunde et al (2006) in a study titled “Stock Market Capitalization and Interest Rate in Nigeria: A Time Series Analysis”, examined the relationship between stock market capitalization rate and interest rate

International Journal of Empirical Finance

55

from 1981 to 2000. The result revealed that the prevailing interest rate exerted positive influence on stock market capitalization rate. Government development stock rate exerted negative influence on stock market

capitalization rate and prevailing interest rate exerted negative influence on government development stock

rate during the period of the study.

Nnamdi (2007) attempted to evaluate the dynamic impacts and relationships between deposit structure, lending rates and risk assets created in the Nigerian banking system. The results indicated a significant

multiple correlation between risk assets and a combination of the independent variables; savings deposit, time deposit, demand deposits and lending rates. However, the multiple regression technique shows only the

coefficient of savings deposit as significant among the independent variables with demand deposit exhibiting

a negative relationship and insignificant impact on risk assets. The results radically departed from the

traditional “Least cost” approach to deposit marketing vis-à-vis risk asset funding.

Obamuyi (2009) investigated the relationship between interest rates and economic growth in Nigeria,

using time series analysis and annual data from 1970 to 2006. The co-integration and error correction were

used to capture both the long-run and short-run dynamics of the variables in the model. The results indicated that real lending rates have significant effect on economic growth. There also existed a unique long-run

relationship between economic growth and its determinants, including interest rates. Therefore, the results

imply that the behavior of interest rate is important for economic growth in view of the relationships between interest rates and investment and investment and economic growth.

Alao (2010) in a study “Interest Rates Determination in Nigeria: An Econometric X-ray ”, x-rayed and

investigated the Nigerian financial sector which in his words ‘assumes interest rates to be a combination of a domestic rate in autarky and the uncovered interest parity rate in a completely open economy’. The study

employed Interest Rate Spreads (IRS) as the dependent variable and domestic interest rate which is the

difference between average interest rate earned on interest earning assets (loans) and average interest rate paid on deposits. The investigation captured both the long run and the short run dynamics of domestic

interest rate behavior by estimating an error correction model (ECM) using the Engle-Granger methodology

with discovery of an appropriate negative ECM term which is significant and less than one. Inflation rate

adjustment to the long-run equilibrium is the fastest while exchange rate adjustment towards equilibrium is the slowest. Econometric analysis notwithstanding suggested that as the Nigerian financial sector integrates

more with global markets, returns on foreign assets will play a significant role in the determination of

domestic interest rates.

Amassoma et al (2011) examined the nexus of interest rate deregulation, lending rate and agricultural

productivity in Nigeria by employing co-integration and error correction techniques on annual data spanning

1986 to 2009. The findings showed that interest rate deregulation has a positive and significant effect on agricultural productivity.

Olokoyo (2011) examined the determinants of commercial banks’ lending behavior in Nigeria. From her

findings, commercial banks’ deposits have the greatest impact on their lending behavior.

3. Theoretical Framework

Loan Pricing Theory

Banks cannot always set high interest rates, e.g. trying to earn maximum interest income. Banks should consider the problems of adverse selection and moral hazard since it is very difficult to forecast the borrower

type at the start of the banking relationship (Stiglitz and Weiss, 1981). If banks set interest rates too high,

they may induce adverse selection problems because high-risk borrowers are willing to accept these high rates. Once these borrowers receive the loans, they may develop moral hazard behaviour or so called

borrower moral hazard since they are likely to take on highly risky projects or investments (Chodechai,

2004). From the reasoning of Stiglitz and Weiss, it is usual that in some cases we may not find that the

interest rate set by banks is commensurate with the risk of the borrowers.

N. P. Chinaecherem & I. Mgbataogu

56

Firm Characteristics Theories

These theories predict that the number of borrowing relationships will be decreasing for small, high-

quality, informationally opaque and constraint firms, all other things been equal. (Godlewski & Ziane, 2008)

Theory of Multiple-Lending

It is found in literature that banks should be less inclined to share lending (loan syndication) in the

presence of well developed equity markets and after a process consolidation. Both outside equity and mergers and acquisitions increase banks’ lending capacities, thus reducing their need of greater

diversification and monitoring through share lending. (Carletti et al, 2006; Ongene & Smith, 2000; Karceski

et al, 2004; Degryse et al, 2004). This theory has a great implication for banks in Nigeria in the light of the

recent 2005 consolidation exercise in the industry.

Hold-up and Soft-Budget-Constraint Theories

Banks choice of multiple-bank lending is in terms of two inefficiencies affecting exclusive bank-firm relationships, namely the hold-up and the soft-budget-constraint problems.1 According to the hold-up

literature, sharing lending avoids the expropriation of informational rents. This improves firms’ incentives to

make proper investment choices and in turn it increases banks’ profits (Von Thadden, 2004; Padilla and Pagano, 1997). As for the soft-budget-constraint problem, multiple-bank lending enables banks not to extend

further inefficient credit, thus reducing firms’ strategic defaults. Both of these theories consider multiple-

bank lending as a way for banks to commit towards entrepreneurs and improve their incentives. None of

them, however, addresses how multiple-bank lending affects banks’ incentives to monitor, and thus can explain the apparent discrepancy between the widespread use of multiple-bank lending and the importance of

bank monitoring. But according to Carletti et al (2006), when one considers explicitly banks’ incentives to

monitor, multiple-bank lending may become an optimal way for banks with limited lending capacities to commit to higher monitoring levels. Despite involving free-riding and duplication of efforts, sharing lending

allows banks to expand the number of loans and achieve greater diversification. This mitigates the agency

problem between banks and depositors, and it improves banks’ monitoring incentives. Thus, differently from the classical theory of banks as delegated monitors, their paper suggested that multiple-bank lending may

positively affect overall monitoring and increase firms’ future profitability.

The Signalling Arguments

The signalling argument states that good companies should provide more collateral so that they can

signal to the banks that they are less risky type borrowers and then they are charged lower interest rates.

Meanwhile, the reverse signaling argument states that banks only require collateral and or covenants for relatively risky firms that also pay higher interest rates (Chodechai, 2004; Ewert and Schenk, 1998).

Credit Market Theory

A model of the neoclassical credit market postulates that the terms of credits clear the market. If collateral and other restrictions (covenants) remain constant, the interest rate is the only price mechanism.

With an increasing demand for credit and a given customer supply, the interest rate rises, and vice versa. It is

thus believed that the higher the failure risk of the borrower, the higher the interest premium (Ewert et al, 2000).

Point of Deviation

This study is an improvement on other studies for the following reasons. Firstly, while most of the

studies reviewed focused more on the relationship between interest rates and Gross Domestic Product – as a

measure of economic growth, it recognizes the fact that the level of financial accommodation function of the banking system is a major determinant of economic growth and that without favorable interest rates policy

measure, the desired level of financial accommodation for sustainable economic growth in Nigeria might

remain a mirage. Secondly, it could be conjectured from the works reviewed in the previous section that the

lending of commercial banks in Nigeria is determined by some factors both at the micro and macro level. Thus, recognizing the fact that interest rates policy is a major determinant of commercial banks’ lending

International Journal of Empirical Finance

57

behavior at the macro level, we disaggregate the micro and macro determinants, to ascertain the impact government interest rates policy reform on the lending behavior (financial intermediation) of Nigerian

commercial banks. Thirdly, the study period covers 1970 to 2000, to capture specifically the activities of the

commercial banks in the country. This is in recognition of the fact that the universal banking system which

enlarges the scope of the commercial banks to include both merchant banking and other banking and non banking activities took effect from 2001 in Nigeria. Further, the study captures only the operations of the

commercial banks to give credence and possible policy directions to the monetary authority in its bid to

restore commercial banking bearing in mind that it is the most conventional banking that serve the majority of the populace and also a dominant banking institutions in Nigeria.

4. Methodology

The paper made use of both descriptive and econometric analyses. The descriptive approach of trend

analysis was used to determine the relationship between interest rates and level of credits extended by the deposit money banks. Again, in order to achieve the purpose of the study as stated above, a dummy variables

approach to Chow test is adopted. According to Brooks (2008), in the case of the Chow test, the unrestricted

regression would contain dummy variables for the intercept and for all of the slope coefficients. Thus, the model of this study is presented as:

= ------------- (1)

In the model above, Dt = 0 for t in Period 1 and 1 Period 2. In other words, Dt takes the value zero for

the observation during the regulated interest rate period and one during the deregulated period. Equation 1

above can be reduced thus;

= ---- (2)

Where; is the Aggregate Domestic Credit extended by the Commercial Banks during the study

period, represent weighted average lending rates, weighted average deposit rates, minimum rediscount rate (monetary policy rate), exchange rate Nigerian Naira with US Dollar,

inflation rate respectively. is dummy variable to capture the change in financial policy from regulated to

deregulated periods of interest rate policy. represents the constant term, is a white noise disturbance term

and are parameters to be estimated.

The a priori expectation is summarized as follows:

There is no exact a priori sign for the coefficient on exchange rate and inflation. Theoretical models

suggest that any sign is possible. Cukierman and Hercowitz (1989) in Amidu (2006) present a model where

loan demand is positively related to inflation. In their model, firms make use of both money and bank loans to pay for working capital. High inflation penalizes money holdings by firms and makes bank loans more

attractive. By contrast, De Gregorio and Sturzenegger (1997) also in Amidu (2006) develop a model where

the demand for bank credit by firms reduces with inflation because, in their model, higher inflation is related to lower productivity levels, which, in turn, reduces the demand for labor; Huybens and Smith (1999) in

Amidu (2006) show that both outcomes are actually possible depending on the nature of the steady-state

equilibrium in the economy.

Before our estimation, we tried to ascertain the time series properties of all the variables (both

dependent and independent) to avoid spurious regression, which arises as a result of the regression of two or

more non-stationary time series data. This means that the time series have to be de-trended before any meaningful analysis can be performed. According to Brooks (2008), if standard regression techniques are

applied to non-stationary data, the end result could be regression that “looks” good under standard measures

(significant coefficient estimates and a high R2) but which is really valueless. Thus, time series analysis was

carried out to examine the data for stationarity or non-stationarity problems using Augmented Dickey-Fuller

N. P. Chinaecherem & I. Mgbataogu

58

(ADF), an extension of Dickey-Fuller test for stationarity. After this, we proceeded to Co-integration test ascertain the long-run relationship of the variables. This was done by the Johansen test to Co-integration to

confirm the existence of a long-run equilibrium relationship between the variables. Having established Co-

integration, an Error Correction Model (ECM) is specified to present the short run dynamics while

preserving the long-run relationship.

All the econometric analysis covered the period of 1970 to 2000. Data were obtained from the Central

Bank of Nigeria’s Statistical Bulletin.

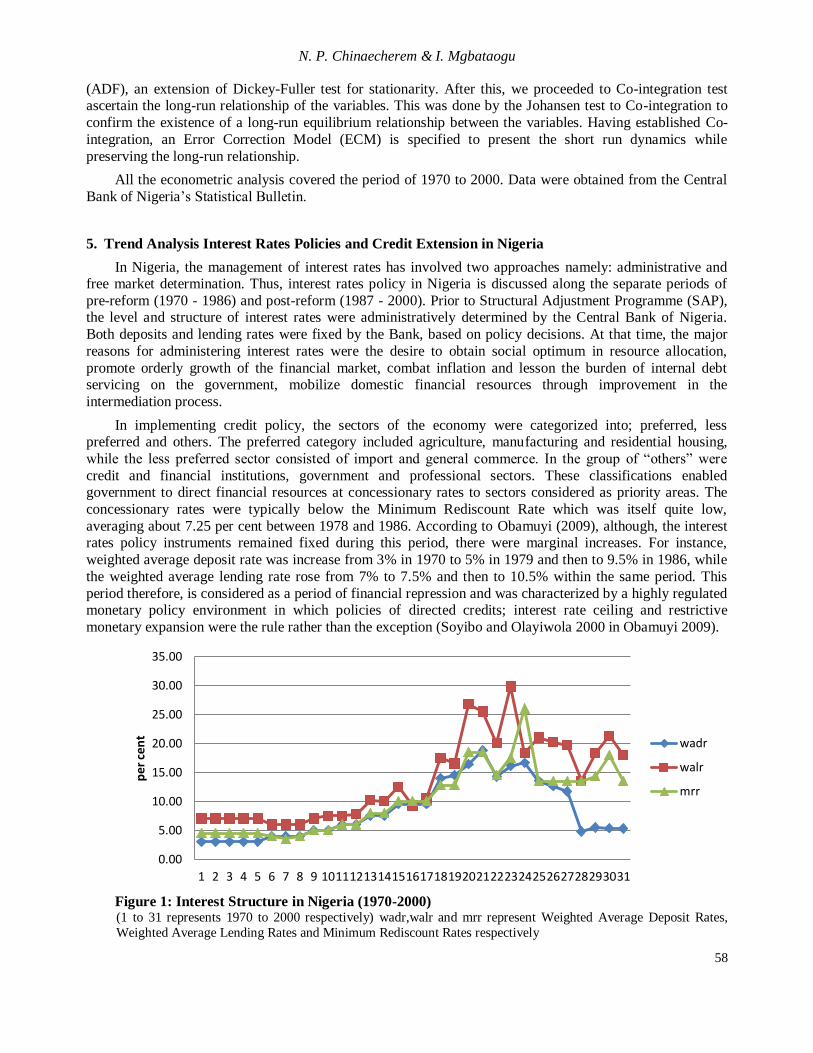

5. Trend Analysis Interest Rates Policies and Credit Extension in Nigeria

In Nigeria, the management of interest rates has involved two approaches namely: administrative and free market determination. Thus, interest rates policy in Nigeria is discussed along the separate periods of

pre-reform (1970 - 1986) and post-reform (1987 - 2000). Prior to Structural Adjustment Programme (SAP), the level and structure of interest rates were administratively determined by the Central Bank of Nigeria.

Both deposits and lending rates were fixed by the Bank, based on policy decisions. At that time, the major

reasons for administering interest rates were the desire to obtain social optimum in resource allocation,

promote orderly growth of the financial market, combat inflation and lesson the burden of internal debt servicing on the government, mobilize domestic financial resources through improvement in the

intermediation process.

In implementing credit policy, the sectors of the economy were categorized into; preferred, less preferred and others. The preferred category included agriculture, manufacturing and residential housing,

while the less preferred sector consisted of import and general commerce. In the group of “others” were

credit and financial institutions, government and professional sectors. These classifications enabled government to direct financial resources at concessionary rates to sectors considered as priority areas. The

concessionary rates were typically below the Minimum Rediscount Rate which was itself quite low,

averaging about 7.25 per cent between 1978 and 1986. According to Obamuyi (2009), although, the interest rates policy instruments remained fixed during this period, there were marginal increases. For instance,

weighted average deposit rate was increase from 3% in 1970 to 5% in 1979 and then to 9.5% in 1986, while

the weighted average lending rate rose from 7% to 7.5% and then to 10.5% within the same period. This

period therefore, is considered as a period of financial repression and was characterized by a highly regulated monetary policy environment in which policies of directed credits; interest rate ceiling and restrictive

monetary expansion were the rule rather than the exception (Soyibo and Olayiwola 2000 in Obamuyi 2009).

Figure 1: Interest Structure in Nigeria (1970-2000) (1 to 31 represents 1970 to 2000 respectively) wadr,walr and mrr represent Weighted Average Deposit Rates,

Weighted Average Lending Rates and Minimum Rediscount Rates respectively

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31

pe

r ce

nt

wadr

walr

mrr

International Journal of Empirical Finance

59

In the deregulated periods, deposit and lending rates were allowed to be determined by market forces and the interest rates of course, increased as expected. However, the Minimum Rediscount Rate (MRR)

which influences other interest rates continued to be determined by the Central Bank in line with changes in

overall economic conditions. For instance, the weighted average deposit and lending rates rose from 9.5%

and 10.5% in 1986 to 14% and 17.5% respectively in 1987 as a result of interest rates deregulation in Nigeria. The MRR which was 15% in August 1987 was reduced to 12.75% in December 1987 with the

objective of stimulating investment and growth in the economy. However, inflation began to rear its ugly

head in the economy. In 1987, it jumped to 10.2% from 5.4% in 1986 and then snowballed to 38.3% in 1988. Consequently, in 1989, the MRR was raised to 18.5% in order to contain inflation. However, inflation

continues unabated. By December 1989, it stood at 40.9% and as a result, the cap on interest rate was lifted

1992 and re-imposed in 1994 when inflationary spiral could not be contained.

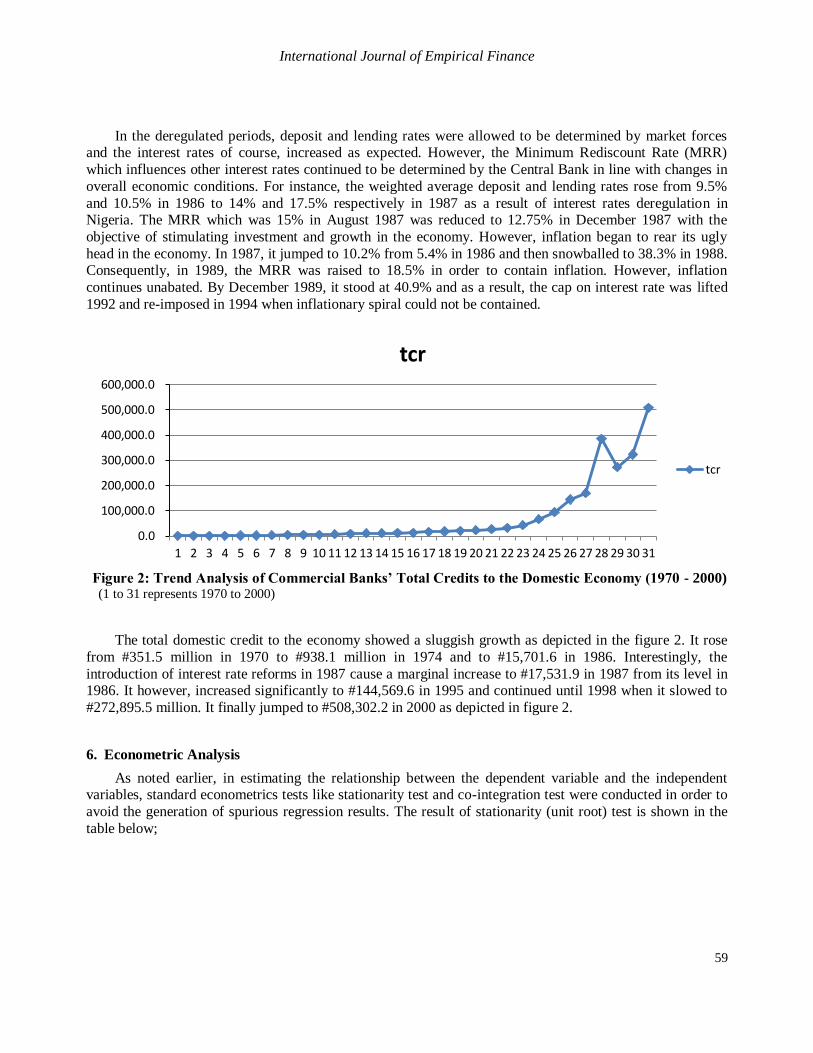

Figure 2: Trend Analysis of Commercial Banks’ Total Credits to the Domestic Economy (1970 - 2000) (1 to 31 represents 1970 to 2000)

The total domestic credit to the economy showed a sluggish growth as depicted in the figure 2. It rose

from #351.5 million in 1970 to #938.1 million in 1974 and to #15,701.6 in 1986. Interestingly, the

introduction of interest rate reforms in 1987 cause a marginal increase to #17,531.9 in 1987 from its level in 1986. It however, increased significantly to #144,569.6 in 1995 and continued until 1998 when it slowed to

#272,895.5 million. It finally jumped to #508,302.2 in 2000 as depicted in figure 2.

6. Econometric Analysis

As noted earlier, in estimating the relationship between the dependent variable and the independent variables, standard econometrics tests like stationarity test and co-integration test were conducted in order to

avoid the generation of spurious regression results. The result of stationarity (unit root) test is shown in the

table below;

0.0

100,000.0

200,000.0

300,000.0

400,000.0

500,000.0

600,000.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31

tcr

tcr

N. P. Chinaecherem & I. Mgbataogu

60

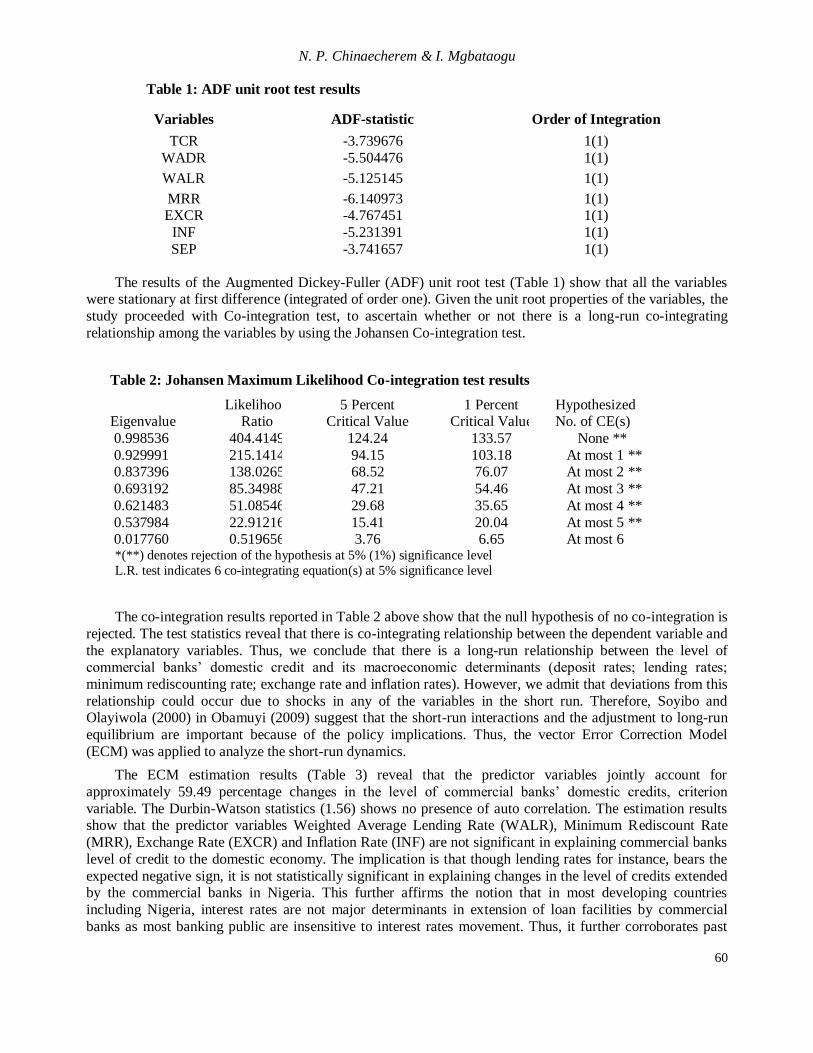

Table 1: ADF unit root test results

Variables ADF-statistic Order of Integration

TCR -3.739676 1(1)

WADR -5.504476 1(1)

WALR -5.125145 1(1)

MRR -6.140973 1(1) EXCR -4.767451 1(1)

INF -5.231391 1(1)

SEP -3.741657 1(1)

The results of the Augmented Dickey-Fuller (ADF) unit root test (Table 1) show that all the variables were stationary at first difference (integrated of order one). Given the unit root properties of the variables, the

study proceeded with Co-integration test, to ascertain whether or not there is a long-run co-integrating

relationship among the variables by using the Johansen Co-integration test.

Table 2: Johansen Maximum Likelihood Co-integration test results

Likelihood 5 Percent 1 Percent Hypothesized Eigenvalue Ratio Critical Value Critical Value No. of CE(s)

0.998536 404.4149 124.24 133.57 None **

0.929991 215.1414 94.15 103.18 At most 1 ** 0.837396 138.0265 68.52 76.07 At most 2 **

0.693192 85.34988 47.21 54.46 At most 3 **

0.621483 51.08546 29.68 35.65 At most 4 **

0.537984 22.91216 15.41 20.04 At most 5 ** 0.017760 0.519656 3.76 6.65 At most 6 *(**) denotes rejection of the hypothesis at 5% (1%) significance level

L.R. test indicates 6 co-integrating equation(s) at 5% significance level

The co-integration results reported in Table 2 above show that the null hypothesis of no co-integration is

rejected. The test statistics reveal that there is co-integrating relationship between the dependent variable and

the explanatory variables. Thus, we conclude that there is a long-run relationship between the level of commercial banks’ domestic credit and its macroeconomic determinants (deposit rates; lending rates;

minimum rediscounting rate; exchange rate and inflation rates). However, we admit that deviations from this

relationship could occur due to shocks in any of the variables in the short run. Therefore, Soyibo and Olayiwola (2000) in Obamuyi (2009) suggest that the short-run interactions and the adjustment to long-run

equilibrium are important because of the policy implications. Thus, the vector Error Correction Model

(ECM) was applied to analyze the short-run dynamics.

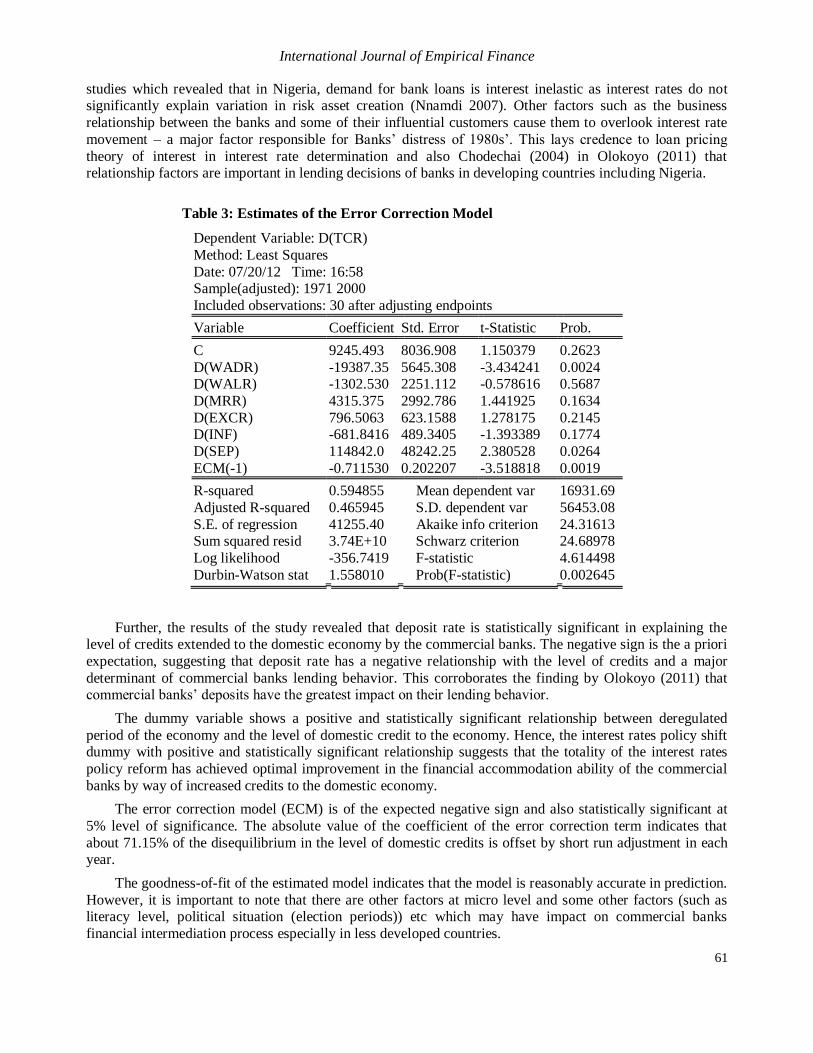

The ECM estimation results (Table 3) reveal that the predictor variables jointly account for

approximately 59.49 percentage changes in the level of commercial banks’ domestic credits, criterion

variable. The Durbin-Watson statistics (1.56) shows no presence of auto correlation. The estimation results show that the predictor variables Weighted Average Lending Rate (WALR), Minimum Rediscount Rate

(MRR), Exchange Rate (EXCR) and Inflation Rate (INF) are not significant in explaining commercial banks

level of credit to the domestic economy. The implication is that though lending rates for instance, bears the

expected negative sign, it is not statistically significant in explaining changes in the level of credits extended by the commercial banks in Nigeria. This further affirms the notion that in most developing countries

including Nigeria, interest rates are not major determinants in extension of loan facilities by commercial

banks as most banking public are insensitive to interest rates movement. Thus, it further corroborates past

International Journal of Empirical Finance

61

studies which revealed that in Nigeria, demand for bank loans is interest inelastic as interest rates do not significantly explain variation in risk asset creation (Nnamdi 2007). Other factors such as the business

relationship between the banks and some of their influential customers cause them to overlook interest rate

movement – a major factor responsible for Banks’ distress of 1980s’. This lays credence to loan pricing

theory of interest in interest rate determination and also Chodechai (2004) in Olokoyo (2011) that relationship factors are important in lending decisions of banks in developing countries including Nigeria.

Table 3: Estimates of the Error Correction Model

Dependent Variable: D(TCR)

Method: Least Squares

Date: 07/20/12 Time: 16:58 Sample(adjusted): 1971 2000

Included observations: 30 after adjusting endpoints

Variable Coefficient Std. Error t-Statistic Prob.

C 9245.493 8036.908 1.150379 0.2623

D(WADR) -19387.35 5645.308 -3.434241 0.0024 D(WALR) -1302.530 2251.112 -0.578616 0.5687

D(MRR) 4315.375 2992.786 1.441925 0.1634

D(EXCR) 796.5063 623.1588 1.278175 0.2145 D(INF) -681.8416 489.3405 -1.393389 0.1774

D(SEP) 114842.0 48242.25 2.380528 0.0264

ECM(-1) -0.711530 0.202207 -3.518818 0.0019

R-squared 0.594855 Mean dependent var 16931.69

Adjusted R-squared 0.465945 S.D. dependent var 56453.08

S.E. of regression 41255.40 Akaike info criterion 24.31613 Sum squared resid 3.74E+10 Schwarz criterion 24.68978

Log likelihood -356.7419 F-statistic 4.614498

Durbin-Watson stat 1.558010 Prob(F-statistic) 0.002645

Further, the results of the study revealed that deposit rate is statistically significant in explaining the level of credits extended to the domestic economy by the commercial banks. The negative sign is the a priori

expectation, suggesting that deposit rate has a negative relationship with the level of credits and a major

determinant of commercial banks lending behavior. This corroborates the finding by Olokoyo (2011) that commercial banks’ deposits have the greatest impact on their lending behavior.

The dummy variable shows a positive and statistically significant relationship between deregulated

period of the economy and the level of domestic credit to the economy. Hence, the interest rates policy shift dummy with positive and statistically significant relationship suggests that the totality of the interest rates

policy reform has achieved optimal improvement in the financial accommodation ability of the commercial

banks by way of increased credits to the domestic economy.

The error correction model (ECM) is of the expected negative sign and also statistically significant at

5% level of significance. The absolute value of the coefficient of the error correction term indicates that

about 71.15% of the disequilibrium in the level of domestic credits is offset by short run adjustment in each year.

The goodness-of-fit of the estimated model indicates that the model is reasonably accurate in prediction.

However, it is important to note that there are other factors at micro level and some other factors (such as literacy level, political situation (election periods)) etc which may have impact on commercial banks

financial intermediation process especially in less developed countries.

N. P. Chinaecherem & I. Mgbataogu

62

7. Conclusion and Recommendations

A major policy thrust of interest rate reform was a boost on domestic savings and a consequent increase

in and availability of loanable funds in the banking system. The ultimate goal is to ensure that funds are

available to the productive sector of the economy to ensure a sustained economic growth and development. The paper examined the impact of this interest rates reform on intermediation process of commercial banks

in Nigeria. The results from both descriptive and econometric analyses reveal that deregulation of interest

rates in Nigeria have significantly boosted financial intermediation process of commercial banks in Nigeria by way of increased lending to the domestic economy. However, this has not translated into commensurate

level of economic development as incidence of poverty and underdevelopment in Nigeria is still

unacceptably high. The implication of this is that the link between interest rates, domestic credit extension

and economic growth is not automatic. This is explained by the fact that most commercial banks’ credits are not channeled to productive sectors of the economy like industrial, manufacturing and agricultural sectors.

Most of the loans are extended to borrowers for debt settlement, speculative activities in the financial

markets etc thereby stifling available funds and denying the productive sectors the needed funds for sustainable economic development.

From the foregoing, it is instructive that the monetary authority should formulate and implement interest

rates policies that will encourage channeling of funds to the productive sectors of the economy. We advise that the interest rates should not be entirely left for the market forces to determine. We recommend partial

deregulation of the interest rates, where there is concessionary interest rate for genuine entrepreneurs in the

economy. This will ensure investment-friendly environment and also guarantee profitability to genuine investors. Bank supervision arm of the Central Bank should adopt an efficient and effective policy that will

ensure close monitor of commercial banks’ borrowers. This will ensure that borrowed funds are channeled to

the productive sectors of the economy for sustainable economic development. Again, deposit rates have

proven to be a major determinant of commercial banks’ lending behavior. Thus, commercial banks should device means of attracting and retaining more deposits to improve their lending performance. Sound banking

habit should be encouraged among Nigerian through massive enlightenment campaign to educate the public.

This will cause them to be rational and sensitive to interest rate movement in this market driven economy, thereby reducing the incidence of loan default.

References

Adebiyi and Babatope-Obasa (2004): Institutional-Framework, Interest rate Policy and the Financing of the

Nigerian Manufacturing Sub-sector. African Development and Poverty Reduction: The Macro-Micro Linkage Forum Paper 2004.

Ajie et al (2006): Financial Institutions, Markets and Contemporary Issues, Port Harcourt, Pearl Publishers.

Alao (2010): Interest Rates Determination in Nigeria: An Econometric X-ray. International Research Journal of Finance and Economics ISSN 1450-2887 Issue 47 (2010)

Albu (2006): Trends in the Interest Rate-Investment-GDP Growth Relationship. Romanian J. Econ. Forecast No. 3.

Amassoma et al (2011): The nexus of Interest Rate Deregulation, Lending and Agricultural Productivity in

Nigeria. Current Research Journal of Economic Theory 3(2): 53-61, 2011 ISSN: 2042-4841

Amidu (2006): The Link between Monetary policy and Bank lending Behavior: The Ghanaian Case. Banks

and Bank Systems / Volume 1, Issue 4, 2006

Brooks (2008): Introductory Econometrics for Finance. Cambridge University Press, the Edinburgh Building, Cambridge CB2 8RU, UK

Cameron et al (1967): Banking in the Early Stages of Industrialization. New York, OUP

Cameron et al (1972): Banking and Economic Development. Some Lessons of History, New York OUP

International Journal of Empirical Finance

63

Carletti et al (2006): Multiple-Bank Lending: Diversification and Free-riding in Monitoring, Working Paper, Department of Statistics: Universita degli Studi di Milano-Bicocca.

Chodechai, (2004), Determinants of Bank Lending in Thailand: An Empirical Examination for the years

1992 – 1996, Unpublished Thesis.

Cukierman and Hercowitz (1989): Oligopolistic Financial Intermediation, Inflation and the Interest Rate

Spread’, Foerder Institute for Economic Research, Tel-Aviv University, Working Paper n. 17-89.

De Gregorio and Sturzenegger (1997): Financial Markets and Inflation under Imperfect Information’. Journal of Development Economics, 54(1): 149-168.

Degryse et al (2004): SMEs and Bank Lending Relationships: the Impact of Mergers, National Bank of Belgium Working Paper, No. 46.

Emery (1971): The Use of Interest Rate Policies as a Stimulus to Econometric Growth. International Finance

Discussion Papers (#676 in RFD Series)

Ewert et al (2000): Determinants of Bank Lending Performance in Germany. Schmalenbach Business

Review (SBR), 52, pp. 344 – 362

Ewert and Schenk (1998): Determinants of Bank Lending Performance, Working Paper, Center for Financial Studies, University of Frankfurt.

Ezirim and Emenyonu (1998): Bank Lending & Credit Administration: A Lender’s Perspective with Cases & Suggested Solutions. Markowitz Centre For Research & Development, Port Harcourt.

Godlewski and Ziane (2008): How Many Banks Does it Take to Lend? Empirical Evidence from Europe,

Working Paper, Laboratoire de Recherche en Gestion & Economie

Gujarati, N. D. (1995), Basic Econometrics, Third Edition, McGraw-Hill.

Huybens, and Smith (1999): Inflation, financial markets and long-run real Activity. Journal of Monetary Economics, 43(2): 283-315.

Ikhide and Alawode (2001): Financial Sector Reforms, Microeconomic Instability and the Order of

Economic Liberation: The Evidence from Nigeria’, Afr. Econ. Res. Paper 112: ISBN 9966-944-53-2.

Karceski et al (2004): The Impact of Bank Consolidation on Commercial Borrower Welfare. Journal of

Finance, 60(4), 2043-2082, doi:10.1111/j.1540-6261.2005.00787.x, http://dx.doi.org/10.1111/j.1540-

6261.2005.00787.x,

Mckinnon (1973): Money and Capital in Economic Development. Washington, D.C.: Brookings Institution.

Mundell (1963): Inflation and Real Interest. Journal of Political Economy, Vol. 71 (3), p.280-3

Nnamdi (2009): Deposit Structure, Lending Rates and Risk Asset Creation in the Nigerian Banking System.

Nigerian Journal of Economic and Financial Research, Vol. 1, No. 2

Obamuyi (2009): An Investigation of the relationship between interest rates and economic growth in Nigeria, 1970 – 2006. Journal of Economics and International Finance Vol. 1(4), pp. 093-098, September,

2009 Available online at http://www.academicjournals.org/JEIF © 2009 Academic Journals

Ojo (1976): The Nigerian Financial System. University of Wales Press, Cardiff.

Olokoyo (2011): Determinants of Commercial Banks’ Lending Behavior. www.sciedu.ca/ijfr International

Journal of Financial Research Vol. 2, No. 2; July 2011

Ologunde et al (2006): Stock Market Capitalization and Interest Rate in Nigeria: A Time Series Analysis.

International Research Journal of Finance and Economics ISSN 1450-2887 Issue 4 (2006) ©

EuroJournals Publishing, Inc. 2006 http://www.eurojournals.com/finance.htm

N. P. Chinaecherem & I. Mgbataogu

64

Omole and Falokun (1999) The Impact of Interest rate Liberalization on Corporate Financing Strategies of Quoted Companies in Nigeria. The Proceeding of the Conferences on African Economic Research

Consortium (AERC 99), Kenya PG 52

Ongena and Smith (2000): What Determines the Number of Bank Relationships? Cross Country Evidence”, Journal of Financial Intermediation, 9, pp. 26-56, doi:10.1006/jfin.1999.0273,

http://dx.doi.org/10.1006/jfin.1999.0273

Oosterbaan et al (2000): Determinants of Growth: Available at http://books.google.co.uk/books.

Padilla and Pagano (1997): Endogenous Communication among Lenders and Entrepreneurial Incentives.

Review of Financial Studies, 10, pp. 205-236, doi:10.1093/rfs/10.1.205,

http://dx.doi.org/10.1093/rfs/10.1.205

Patrick (1966): Financial Development and Economic Growth in Underdeveloped Countries. Economic and

Cultural Change, vol. 14, No. 2 January

Porter (1966): The Promotion of the Banking Habit and Economic Development. Journal of Development

Studies, Vol. 2, No. 4

Shaw, E. (1973): Financial Deepening in Economic Development. Oxford University Press, London.

Shelile (2006): The term structure of Interest Rates and Economic Activity in South Africa. Unpublished

Thesis in Partial Fulfillment of Master of Commerce, Financial Markets in Department of

Economics and Economic History Rhodes University, Grahams-town

Soyibo and Olayiwola (2000): Interest rate Policy and the Promotion of Savings Investment and Resource

Mobilization in Nigeria. Research Report 24, Development Policy Centre, Ibadan.

Stiglitz, J. E and Weiss, A. (1981): Credit Rationing in Markets with Imperfect Information. American

Economic Review, June, pp. 393-410.