Embed Size (px)

Citation preview

June 2005

Volume 7 – Number 2

Inflation Report

ISSN 1517-7289

������������� ��������������������

������������������� � � ������ ���� ���� ��� ���� ����������

������������ �

��� �� ����� ��!��������"��#���� �����!��$%%�����&��!! '��(���)�! ����&�**&�'���'�+�����,,,�

-"�����.��(�'��� �%������ �� ������ ���� ��"��/�(���"��� �������"����0����'��"�� ����!������� ������'�( ��"�1

������������ ��� ������ ��2/�%���1�'���!3 ! �(�� 4

������ ����������� ���������'2/�%���1�!����'����3 ! �(�� 4

���������������������������2/�%���1�(� ��3 ! �(�� 4

�������������� �������� �� ������� �� �������� ��������� ������������������� �����������

���������������� ��������

���������������������������������� ������ �!������"� ��������� �#��$��%����� �&'��(��)�����*�+�,�,,�-%.,,� �����$��� ��/� ����0�)1������ 233+'4�"-'-%"�',�����"-'-%"3+�/�(�� 233+'4� "-'-%"+�+#% ���� ����56�6�7���6�

8� 6��� ������� �3,� �����

��������� ���������

������������ ������������6��������������� ���������%�(��������� 1������������������������� �����1���1����1��������7��1�������1���71������������� ���� ����� ����

9�1���6�������������������1����������������� ������7�1����������1�����������:�6���2�4�6������������2'.�,�'.�34��������1�������7�����1�����������������������7�1����������1����������������������������7��� ���������1��� ������� ��1���(�

;���������������������6���������������7��������������������������������7���1��7�������������������7�

<1�����������������������������������6��������7���1����7�������1������������������������

������������������������������� ���

:������� ���������������#��$��%����� ��=���6�������� �!������"� �>�����������,,�-%.,,�����$��� ��/� ����0�

)1����� 233+'4�"-'-� 2����4� � ��-,'���-,����-,"���-,-���-,3���-,+��?� ,*,,� ..�"-3/�(� 233+'4� ""�'%.-3"������� 1��������6�6�7���6�#% ��� ���������56�6�7���6�

��������

�������� ��

��� ����������� ��

���������� ��� � ���1.1 Retail sales __________________________________________________________________ 11

1.2 Output ______________________________________________________________________ 13Crops/livestock _______________________________________________________________ 13

Crop output __________________________________________________________________ 14

Livestock____________________________________________________________________ 19Industrial output ______________________________________________________________ 19

1.3 Labor market _________________________________________________________________ 24

Employment _________________________________________________________________ 24Earnings ____________________________________________________________________ 25

1.4 Gross Domestic Product ________________________________________________________ 26

1.5 Investment __________________________________________________________________ 271.6 Summary ____________________________________________________________________ 31

������ ���2.1 General price indices ___________________________________________________________ 33

2.2 Broad Consumer Price Index _____________________________________________________ 34

2.3 Regulated prices ______________________________________________________________ 352.4 Core inflation_________________________________________________________________ 35

2.5 Market expectations ___________________________________________________________ 36

2.6 Summary ____________________________________________________________________ 37

����� ������ ����������������������� �����3.1 Credit ______________________________________________________________________ 39

Earmarked credit ______________________________________________________________ 40

Non-earmarked credit __________________________________________________________ 413.2 Monetary aggregates __________________________________________________________ 42

Federal public securities and BCB open market operations _____________________________ 46

Real interest rates and market expectations _________________________________________ 47

Capital market ________________________________________________________________ 48

Domestic savings _____________________________________________________________ 48

3.3 Fiscal policy _________________________________________________________________ 49Public sector borrowing requirements _____________________________________________ 49

Federal debt _________________________________________________________________ 51

Net public sector debt __________________________________________________________ 523.4 Summary ____________________________________________________________________ 53

�� ���� ������������� ���4.1 Economic activity _____________________________________________________________ 55

4.2 Monetary policy and inflation ___________________________________________________ 574.3 International financial markets ___________________________________________________ 58

4.4 World trade __________________________________________________________________ 60

4.4.1 Commodities _____________________________________________________________ 624.4.1.1 Oil _______________________________________________________________ 62

4.5 Summary ____________________________________________________________________ 63

��������� �� � �5.1 Foreign exchange flows ________________________________________________________ 65

5.2 Trade balance ________________________________________________________________ 665.3 Services and income ___________________________________________________________ 69

5.4 Capital account _______________________________________________________________ 70

5.5 External sustainability indicators _________________________________________________ 715.6 Summary ____________________________________________________________________ 72

����� ������ ���! ���6.1 Inflation drivers _______________________________________________________________ 78

6.2 Baseline scenario: assumptions and risks __________________________________________ 83

6.3 Inflation forecasts _____________________________________________________________ 87

"���Effects of the Crop Reduction ___________________________________________________ 15

Outlook for GDP in 2005 ________________________________________________________ 28

Evolution of Payroll-Deducted Loans _____________________________________________ 43Balance of Payments Projections _________________________________________________ 73

Twelve-Month Ahead Inflation Expectations ________________________________________ 90

International Experience with Inflation Targeting _____________________________________ 92

#��� ���

����������������������� ��$�

#������ ��$�

����������5�������������� ���5���

������

The Inflation Report is a quarterly publication of the BancoCentral do Brasil, aimed at evaluating the performance ofthe inflation targeting regime and communicating the Bank’soutlook for inflation. The domestic and internationaleconomic conditions underlying the Monetary PolicyCommittee’s (Copom) decisions are also presented.

The Report is divided into six chapters: Economic Activity;Prices; Credit, Monetary, and Fiscal Policies; InternationalEconomy; External Sector; and Prospects for Inflation.The chapter on Economic Activity examines the recentperformance of retail sales, inventories, output, the labormarket, and investment. The following chapter, on Prices,focuses on recent inflation results, the responsiveness ofinflation to monetary policy decisions, and the economicconditions that may impact inflation. The third chapterexamines relevant credit, monetary, and fiscal policies. Thechapter on the International Economy analyzes the mainglobal economic areas and seeks to identify global economicconditions that may affect Brazil’s balance of payments.The External Sector chapter reviews Brazil’s internationaleconomic-financial relations, with an emphasis on recenttrade sector results and external financing conditions.Finally, the chapter on Prospects for Inflation analyzes theinflation outlook.

����������5�������������� ���5���

When compared to the pace of 2004, Brazilian economic growthin early-2005 has clearly moderated. This is confirmed by therecent performance of industrial activity and retail sales, aswell as by the evolution of GDP in the first quarter. Theseindicators posted positive though declining rates of growth whencompared to the same periods of 2004, and relative stability oronly slight growth in comparison to the end of last year. Afterpeaking at historically high levels, the transitory slowdown ineconomic activity is expected to enable more sustainable long-term growth in an environment of price stability.

The more moderate pace of activity has been accompaniedby changes in the composition of demand, as the externalsector has risen in importance, to the detriment of domesticdemand. On the external front, global economic growthcontinues to be the main factor underlying the dynamicperformance of the export sector, and has even neutralizedpossible negative impacts of recent exchange rateappreciation. Domestically, personal consumption has beenimpacted by the self-propagating effects of risingemployment and real earnings and will tend to remain high,despite a slight drop registered in national accounts in thefirst quarter of this year (following six consecutive quartersof growth). Investment has dropped since the end of 2004,after registering high growth for five consecutive quarters.Though, to some extent, this drop resulted from losses infarm machinery demand, it is also a result of the recentmonetary tightening. The favorable performance ofsovereign risk and business sentiment suggest thatinvestment will recover as the uncertainties surrounding theevolution of domestic demand dissipate.

In the first months of 2005, the job market has performedpositively, with significant reductions in the unemploymentrate when compared to the same months of 2004. At thesame time, however, the overall labor force has expandedand new hirings have slowed, consistent with a moderationin economic activity.

��� �������������

*��5�������������� ���5����������

Credit operations expanded steadily in the year, primarily asa result of household demand for bank credit. Consumercredit growth has been mainly driven by payroll-deductedloans, a modality with lower credit risk for financialinstitutions and lower interest costs for borrowers. Businessloans expanded moderately in both the earmarked and non-earmarked segments, consistent with the evolution ofeconomic activity in the period. Businesses have madeincreasingly greater use of alternative financing mechanisms,particularly debenture issuance.

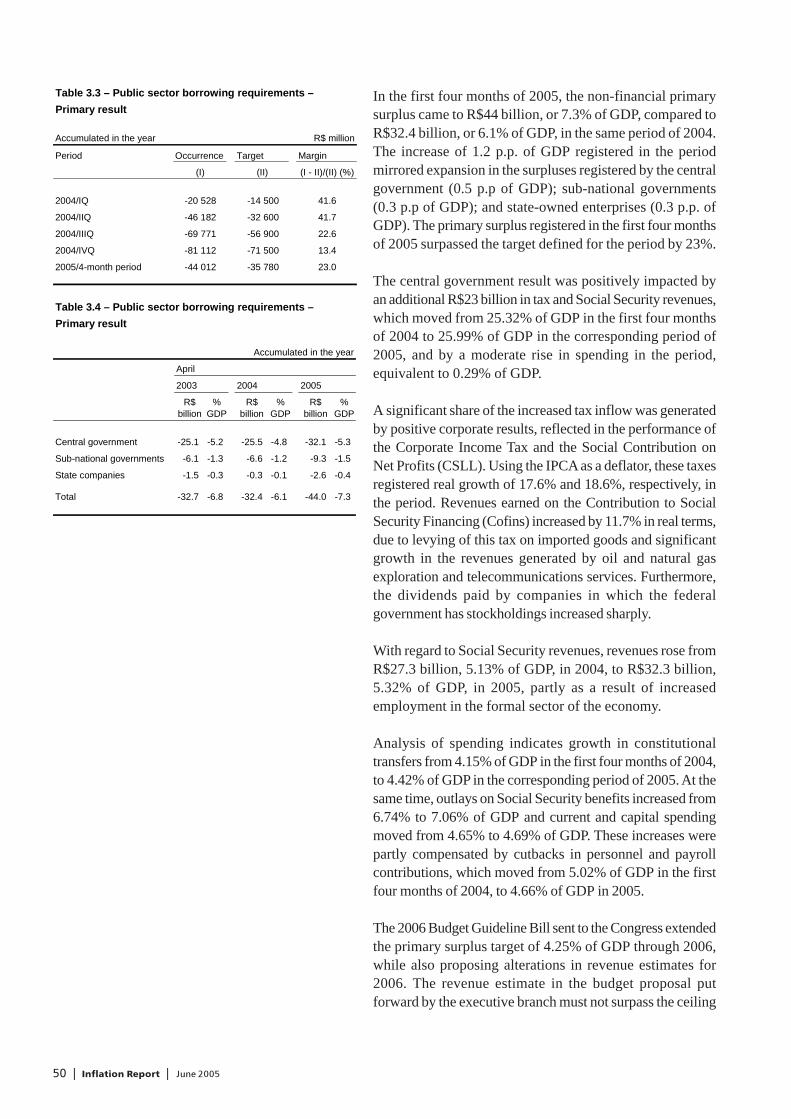

The consolidated public sector primary surplus in the firstfour months of the year surpassed the target for the periodand made it increasingly clear that there are no significantobstacles to achievement of the annual 4.25% of GDPtarget. The fiscal performance was accompanied bycontinued efforts to ensure debt sustainability, encompassingthe budget guidelines proposal for the 2006 fiscal year.

The Net Public Sector Debt/GDP ratio has evolved positively,particularly due to the consolidated fiscal results, growth ofnominal GDP and the behavior of the exchange rate.

Despite import growth, recent trade balance results reinforceexpectations for a robust trade surplus and a positive currentaccount in 2005. In the first five months of the year, thetrade balance registered a surplus of US$ 15.6 billion, whilecurrent unilateral transfers improved sharply when comparedto January–April 2004. Notwithstanding the increase in netservice and income remittances, the current account surplusin the January–April period was four times greater than inthe same period of 2004. The cumulative twelve-month resultregistered a current account surplus of US$ 13.4 billion,equivalent to 2.06% of GDP.

High trade surpluses, reduction in external debt outstanding,rising net foreign direct investment, and stable internationalreserves are variables that strengthen Brazil’s externalposition. Net foreign exchange market flows and recentexternal bond issuance are also factors that suggest nodifficulties in financing the 2005 balance of payments.

Inflation was relatively high in the January–May period,particularly consumer price inflation. Though these indiceshave been significantly affected by seasonal pressures andregulated prices, the broader dissemination of priceincreases and the persistence of core inflation at relativelyhigh levels demonstrated that demand pressures were alsoresponsible for the stickiness of inflation. Despite thisstickiness, the deceleration of inflation in May and the

����������5�������������� ���5��,

outlook for June suggest that recent inflation pressureshave been mostly overcome.

This deceleration is largely attributable to the monetarytightening cycle initiated in September 2004. In comparisonto the beginning of the year, there has been a reduction inthe risks to inflation convergence to the target path. Thepersistence of specific sources of inflationary pressure hasbeen attenuated, at the same time in which improvementshave occurred on the external front, notwithstanding recentinternational oil price increases.

The central forecast for 2005 IPCA inflation in thebenchmark scenario stands at 5.8%. The 0.3 p.p. increasein relation to the forecast in the March Inflation Reportwas caused primarily by higher-than-expected March to Mayinflation, coupled with the upward revision of 2005 regulatedprice inflation, which more than compensated for the effectsof a higher real interest rate and a more appreciatedexchange rate. For 2006, the inflation projection in thebenchmark scenario is 3.7%, 0.1 p.p. below the MarchReport. The fall was due basically to the effects of higherreal interest rates and greater exchange rate appreciation,which more than compensated for the upward revision ofprojections for regulated price inflation in 2006.

The forecasts for the IPCA in the market scenario – basedon the market consensus for interest and exchange ratescompiled by the BCB – stand at 6.3% for 2005 and 4.7%for 2006. These forecasts are above those in the benchmarkscenario, since the market scenario incorporates a declinein interest rates and a depreciation of the exchange rateover the forecast horizon. The current forecast for 2005increased in comparison to the March Report forecast, whilethe forecast for 2006 fell in the period.

In the benchmark scenario, GDP is projected to grow 3.4%in 2005, 0.6% below that estimated in the previous Report.

�������������������������� ��������

���������������

The forecast set out in the March Inflation Report, thatBrazilian economic growth would slow somewhat in early2005, has been confirmed by the recent performance ofindustrial activity and retail sales, as well as by GDP in thefirst quarter of the year. These indicators posted positive –albeit declining – growth, when compared to the sameperiods of 2004, and relative stability or slight growth, whencompared to the final months of 2004. After rising sharply,economic growth has cooled somewhat since the last quarterof 2004. This is a positive development, in light of theobjective of sustainable growth with price stability.

Though the rate of economic growth in early-2005 was quitesimilar to that at end-2004, there was a shift in the relativecomposition of economic activity. Continued export growthhas increased the contribution of external demand to overalloutput. Domestically, following a sharp recovery up to thethird quarter of 2004, investment outlays have diminished,while consumption has been consistently strong, mainly dueto steady credit expansion.

The labor market has posted positive results in 2005, asunemployment dipped below the level registered in the sameperiod of 2004, and new job creation has been strong.

��� ���������

Interrupting the upward trend observed last year, retail salesindicators leveled off at high levels in the early months of2005. This evolution resulted from distinct performanceacross retail sectors, as demand for non-durable goods,which had grown steadily up to January, declined, and salesof durable goods have continued to expand, primarily as aresult of improved credit conditions.

According to the IBGE nationwide survey, the Retail SalesVolume Index dropped 0.5% in the three-month period ended

95

100

105

110

115

Feb2003

Apr Jun Aug Oct Dec Feb2004

Apr Jun Aug Oct Dec Feb2005

Apr

Figure 1.1 – Retail salesSeasonally adjusted data2003=100

Source: IBGE

90

100

110

120

130

140

150

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

90

100

110

120

Furniture and home appliances Supermarkets

Figure 1.2 – Retail salesSeasonally adjusted data2003=100

Source: IBGE

Furniture and home appliances Supermarkets

������������������� ���������������

in April, seasonally adjusted, compared to the previous three-month period. Only the segments of furniture and householdappliances, and fabric, clothing and shoes rose, with growthof 4.8% and 3.3%, respectively, while the other segmentsdeclined, with particularly strong contractions for fuel andlubricant (5.7%), and hypermarket and supermarket (2.9%)sales. Autos, motorcycles and spare parts sales, which arenot included in the general index, fell 8.9%. Despite thisperformance, continued credit growth for automobileacquisitions indicates that this retail segment is clearly onthe path to recovery.

Nominal sales revenues in the first four months of 2005increased 12.3%, compared to the same period of theprevious year. This result reflects 5% growth in volume and7% in retail prices. For comparison, the IPCA rose 7.6% inthe same period. Nominal sales rose sharply in the sectorsof furniture and household appliances, 26.3%; autos andmotorcycles, 16.9%; and fabric, clothing and shoes, 15.9%.

Retail sales increased in all 27 states covered by the IBGEsurvey, in the first four months of 2005, compared to thesame period of 2004. The strongest growth occurred in Acre,26%; Amazonas, 23%; Paraíba, 22.2%; and Rio Grande doNorte, 20%.

According to Fecomercio-RJ, in the year through May, retailsales decelerated more sharply than that registered by thenational IBGE survey. Real earnings on retail sales in Riode Janeiro, deflated by the IPCA, dropped 5.2% in the three-month period through April, compared to the previous threemonths and seasonally adjusted.

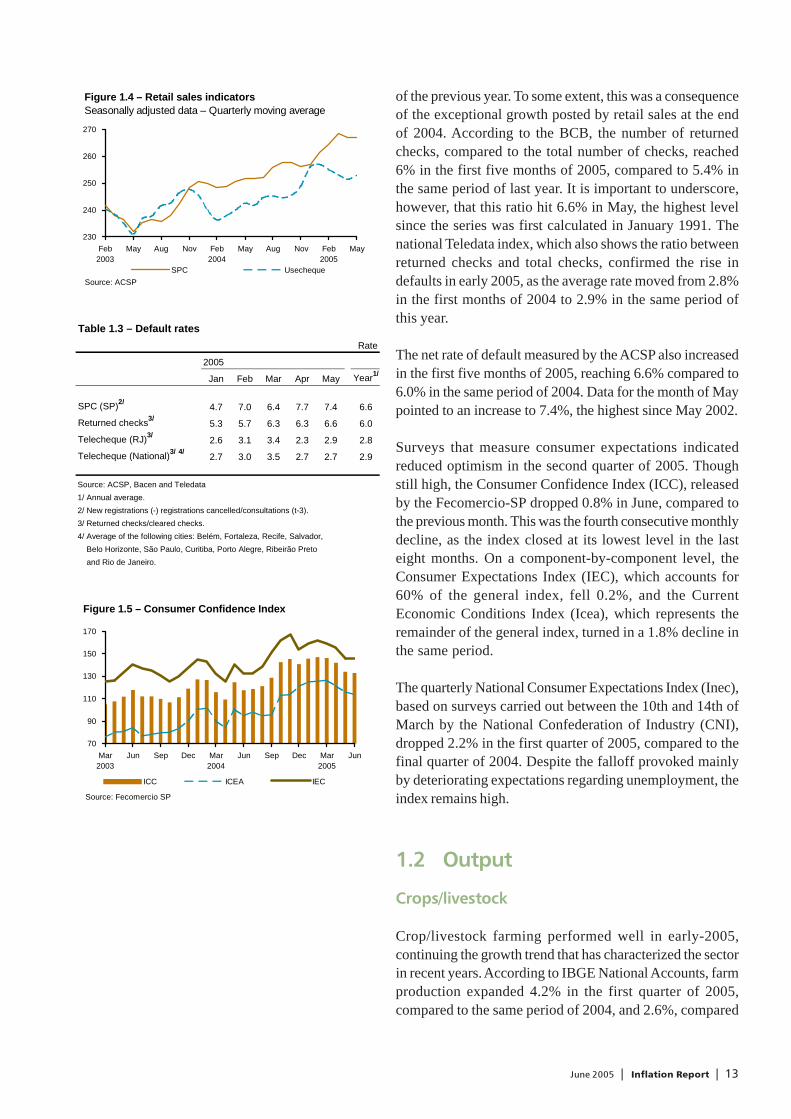

Other indicators confirmed the slowdown in retail sales atthe margin. The number of consultations of the CreditProtection Service (SPC), an indicator of installment salesof goods with higher aggregate value, released by the SãoPaulo Trade Association (ACSP), increased 0.9% in thethree-month period ended in May, comparing to Februaryand seasonally adjusting. On the other hand, consultationsof the Usecheque, an indicator of lower cost upfrontpurchases, dropped 0.9%, in the same period. Since the endof 2004, these two indicators moved in opposite directions,reflecting the different evolution of sales that are moredependent on credit, which expanded steadily during 2004,and those that are more income-sensitive, which cooled inthe early part of this year.

In the first quarter of 2005 and beginning of the secondquarter, default indicators rose, compared to the same period

Table 1.1 – Retail sales

2005, April

% accumulated growth in 2005

Nominal Volume Price

revenue

Retail sector 12.3 5.0 7.0

Fuel and lubricants 11.4 -6.5 19.2

Supermarkets 7.8 3.9 3.8

Fabrics, apparel and footwear 15.9 5.1 10.3

Furniture and home appliances 26.3 19.6 5.6

Vehicles and motorcycles 16.9 4.1 12.3

Source: IBGE

Table 1.2 – Retail sales

% change

2004 2005

Dec Jan Feb Mar Apr

In the month1/

Retail sector 1.9 -0.7 -1.5 1.4 -0.2

Fuel and lubricants 1.9 -2.7 -3.4 -1.3 -1.1

Supermarkets 1.7 -1.8 -2.6 0.6 -0.5

Fabrics, apparel and footwear 4.6 -0.8 -2.7 0.7 13.7

Furniture and home appliances 5.3 -1.9 1.5 3.7 1.1

Vehicles and motorcycles 15.7 -7.7 -8.5 0.9 -1.2

Quarter/previous quarter1/

Retail sector 1.9 2.7 2.1 0.4 -0.5

Fuel and lubricants -0.3 0.4 -1.2 -4.0 -5.7

Supermarkets 2.7 2.2 0.6 -1.9 -2.9

Fabrics, apparel and footwear 1.7 3.9 2.9 0.9 3.3

Furniture and home appliances 2.8 5.6 6.5 4.8 4.8

Vehicles and motorcycles 3.2 5.4 5.2 -4.5 -8.9

In the year

Retail sector 9.2 6.2 4.4 5.9 5.0

Fuel and lubricants 4.6 -1.1 -3.5 -5.4 -6.5

Supermarkets 7.2 6.3 3.6 6.1 3.9

Fabrics, apparel and footwear 4.7 4.2 2.2 1.7 5.1

Furniture and home appliances 26.4 19.6 18.3 18.2 19.6

Vehicles and motorcycles 17.8 11.4 5.5 5.3 4.1

Source: IBGE

1/ Seasonally adjusted data.

1,500

2,000

2,500

3,000

3,500

Feb2003

May Aug Nov Feb2004

May Aug Nov Feb2005

May

90

100

110

120

130

140

Non-earmarked credit for vehicles

Vehicles, motorcycles and parts

Figure 1.3 – Retail salesSeasonally adjusted data

Source: IBGE and Banco Central do Brasil

CreditIn R$ million of May 2005

Vehicles, motorcycles and parts2003=100

�������������������������� ��������

of the previous year. To some extent, this was a consequenceof the exceptional growth posted by retail sales at the endof 2004. According to the BCB, the number of returnedchecks, compared to the total number of checks, reached6% in the first five months of 2005, compared to 5.4% inthe same period of last year. It is important to underscore,however, that this ratio hit 6.6% in May, the highest levelsince the series was first calculated in January 1991. Thenational Teledata index, which also shows the ratio betweenreturned checks and total checks, confirmed the rise indefaults in early 2005, as the average rate moved from 2.8%in the first months of 2004 to 2.9% in the same period ofthis year.

The net rate of default measured by the ACSP also increasedin the first five months of 2005, reaching 6.6% compared to6.0% in the same period of 2004. Data for the month of Maypointed to an increase to 7.4%, the highest since May 2002.

Surveys that measure consumer expectations indicatedreduced optimism in the second quarter of 2005. Thoughstill high, the Consumer Confidence Index (ICC), releasedby the Fecomercio-SP dropped 0.8% in June, compared tothe previous month. This was the fourth consecutive monthlydecline, as the index closed at its lowest level in the lasteight months. On a component-by-component level, theConsumer Expectations Index (IEC), which accounts for60% of the general index, fell 0.2%, and the CurrentEconomic Conditions Index (Icea), which represents theremainder of the general index, turned in a 1.8% decline inthe same period.

The quarterly National Consumer Expectations Index (Inec),based on surveys carried out between the 10th and 14th ofMarch by the National Confederation of Industry (CNI),dropped 2.2% in the first quarter of 2005, compared to thefinal quarter of 2004. Despite the falloff provoked mainlyby deteriorating expectations regarding unemployment, theindex remains high.

��� � �� �

������������

Crop/livestock farming performed well in early-2005,continuing the growth trend that has characterized the sectorin recent years. According to IBGE National Accounts, farmproduction expanded 4.2% in the first quarter of 2005,compared to the same period of 2004, and 2.6%, compared

230

240

250

260

270

Feb2003

May Aug Nov Feb2004

May Aug Nov Feb2005

May

SPC Usecheque

Source: ACSP

Figure 1.4 – Retail sales indicatorsSeasonally adjusted data – Quarterly moving average

Figure 1.5 – Consumer Confidence Index

70

90

110

130

150

170

Mar2003

Jun Sep Dec Mar2004

Jun Sep Dec Mar2005

Jun

ICC ICEA IEC

Source: Fecomercio SP

Table 1.3 – Default rates

Rate

2005

Jan Feb Mar Apr May Year1/

SPC (SP)2/4.7 7.0 6.4 7.7 7.4 6.6

Returned checks3/5.3 5.7 6.3 6.3 6.6 6.0

Telecheque (RJ)3/2.6 3.1 3.4 2.3 2.9 2.8

Telecheque (National)3/ 4/2.7 3.0 3.5 2.7 2.7 2.9

Source: ACSP, Bacen and Teledata

1/ Annual average.

2/ New registrations (-) registrations cancelled/consultations (t-3).

3/ Returned checks/cleared checks.

4/ Average of the following cities: Belém, Fortaleza, Recife, Salvador,

Belo Horizonte, São Paulo, Curitiba, Porto Alegre, Ribeirão Preto

and Rio de Janeiro.

������������������� ���������������

to the fourth quarter of 2004. It is important to note thatthese results did not incorporate the grain harvest reductionsexpected for the current year.

�����������

Estimates released in May by the National Supply Company(Conab) for the 2005 grain harvest reached 113.7 million tons.This represents a reduction of 16.2 million tons compared tothe first estimate made in October, and is 4.6% below theprevious year’s harvest. The IBGE Systematic FarmProduction Survey (LSPA) for May also highlighted the cropreduction caused by the drought in the states of Mato Grossodo Sul, Paraná and Rio Grande do Sul. According to thissurvey, total output of grains, cereals and legumes should reach113.5 million tons this year, or 15.3% below the Octoberestimate (see box "Effects of the Crop Reduction").

The crops most seriously affected by adverse weatherconditions were corn and soybeans. According to Conabestimates, soybean output should close at 50.2 million tonsin 2005, compared to the originally projected 60.2 million. Incomparison to the 2004 harvest, average crop yield isexpected to drop 7.1%, with growth of 8.6% in the areaunder cultivation and 0.8% in the volume harvested. Cornoutput is forecast at 36 million tons, 16.1% below the initialforecast. Production in the current year is expected to drop14.6% compared to 2004, with reductions of 5.2% in areaunder cultivation and 9.9% in average yield.

In the cases of rice and beans, both of which are importantto domestic price dynamics, the change in recent harvestestimates was less accentuated. Rice output is expected toreach 13.2 million tons, up 2.9% over the 2004 results and9.3% greater than the initial estimate. The increase in areaunder cultivation is estimated at 5.5%, while average yieldis expected to drop by 2.5%. Total bean output should closeat 2.9 million tons, down from the initial forecast of 3 milliontons, reflecting a reduction of 2.8% compared to last year’sharvest. Despite the 13.3% cutback in area under cultivation,average yield should increase 12.1%. In the case of beans,domestic supply should be sufficient to meet demand, asdemonstrated by Conab estimates indicating overall supplyof 3.4 million tons and consumption of 3.1 million tons.

According to the May LSPA, the national sugar cane harvestis estimated at 420.2 million tons, up 0.9% compared to 2004.The area under cultivation should expand by 1.2%, whileaverage yield should drop by 0.3%. The same survey

65

75

85

95

105

115

125

1997 1998 1999 2000 2001 2002 2003 2004 2005

Figure 1.6 – Grain productionIn million of tons

Source: Conab1/ Estimate.

1/

Table 1.4 – Farm productionIn 1,000 tons

Production % change

2004 20051/

Grain production 119 114 113 688 -4.6

Cotton (seed) 2 099 2 220 5.8

Rice 12 829 13 198 2.9

Beans 2 978 2 896 -2.8

Corn 42 128 35 989 -14.6

Soybean 49 793 50 195 0.8

Wheat 5 851 5 846 -0.1

Others 3 435 3 343 -2.7

Source: Conab

1/ Estimate.

�������������������������� ��������

������������������ �����

According to the IBGE’s survey for the month ofMay, the 2005 grain harvest will total 113.5 milliontons, a 4.9% decline compared to 2004. The surveyalso reveals a harvest 15.3% below initial forecasts.These results are compatible with the figures releasedby Conab, which issued an April estimate of a totalgrain harvest of 113.7 million tons, 12.5% below theinitial forecast made last October.

The drop in grain production was caused by adverseweather conditions at end-2004 and early-2005 in themajor production regions, particularly the south andcentral-west, which were hit first by drought and laterby excess rainfall. In addition to grains, otherimportant crops are also expected to register areduction in output, including coffee, with a drop of11.4%, and oranges, with a 3% decline, or very slightgrowth, as in the case of sugar cane, of 0.9%,compared to the 2004 harvest year.

Table 1 shows that corn and soybeans were thehardest hit by adverse weather conditions and,therefore, registered the sharpest reductionscompared to pre-planting crop yield estimates.Compared to 2004, soybean output is expected torise 3.1% in the year.

Among the impacts of the crop reduction, three havesignificant implications for the macroeconomicoutlook:

i) The loss of farm income and its impact ondomestic demand;ii) The influence of reduced supply on the evolutionof domestic prices; andiii) The loss of exports.

������������������� ���������������

As far as income losses are concerned, farmers arefacing the dual problem of production shortfalls causedby poor weather and unfavorable prices for variouscrops, in relation to last year. FGV data indicate thatthe prices of soybeans, wheat, corn and rice droppedby 34%, 18.5%, 11.6% and 7.1%, respectively, in realterms, in the first two months of 2005, compared tothe same period of 2004, using the IPCA as deflator.It is important to stress that several products hit byprice reductions had registered strong price increasesin the 2003/2004 period, such as rice (33%), tobacco(27.1%) and soybeans (7.7%).

Table 2 shows the evolution of income on a product-by-product basis, considering output for each yearand average prices as reference. After 2003 – whenthe grain harvest set a new record and the prices ofseveral products, primarily tradables, were relativelyhigh – income stabilized in real terms in 2004 anddropped sharply in 2005.

The estimated falloff in income in 2005 impactedeleven of the fifteen major crops, with particularlystrong effects on soybeans, corn and rice, whichaccount for a significant share of farm income, aswell as wheat and oranges.

The effects of lower rural sector income are alreadyevident in retail sector data. According to the IBGE’snationwide retail survey, sales closed below the nationalaverage in those states hit by adverse weatherconditions (south and central-west regions) and inwhich farm income has significantly higher importance.

Another important consequence of the loss of farmincome is that the sector has been decapitalized. This

Table 1 – Systematic Farm Production Survey (LSPA)

Grain production (1 000 ton) % change

2004

(A) 1st survey – October 2004 May 2005 estimate (C) (C/A) (C/B)

Soybeans 49 522 63 085 51 077 3.1 -19.0

Corn 41 806 43 409 35 470 -15.2 -18.3

Rice 13 277 12 706 13 234 -0.3 4.2

Beans 2 965 3 058 2 999 1.2 -1.9

Others 11 800 11 783 10 688 -9.4 -9.3

Total 119 369 134 042 113 468 -4.9 -15.3

Source: LSPA / IBGE

2005

�������������������������� �������

has direct implications on investment levels andutilization of inputs and, therefore, on productivity.Early data on machinery, equipment and fertilizeracquisitions indicate a decline in 2005, whencompared to previous years.

The impact of the crop reduction on domestic pricesand, particularly, on consumer prices, is expected tobe negligible. The main crops affected by adverseweather conditions have been soybeans and corn, theprices of which are basically determined byinternational markets. At the same time, the impact ofthe crop reduction on the domestic market has beenminimized by recent exchange rate appreciation. Also,these crops do not have a significant participation inthe composition of consumer price indices – soybeanoil has a weight of 0.33% and corn just 0.02% in theIPCA. The largest impacts of reduced supply of theseproducts are indirect, since they are importantingredients in animal feed. However, in recent months,meat prices have trended downward, benefiting notonly from favorable seasonal factors, but also fromthe evolution of the exchange rate.

Table 2 – Income – Main farm products

Crops 2002 2003 2004 2005

Income1/ Income1/ % change % change Income1/ % change % change Income1/ % change % change

IPCA2/ IPP3/ IPCA2/ IPP3/ IPCA2/ 4/ IPP3/ 4/

Soybeans 21 038 31 778 31.7 17.1 32 527 -4.0 -6.9 26 041 -24.1 -24.4

Sugar cane 9 609 11 724 6.4 -5.5 11 657 -6.7 -9.6 12 945 5.3 4.9

Corn 9 260 15 140 42.5 26.7 12 666 -21.5 -23.9 10 156 -24.0 -24.2

Rice 4 084 5 966 27.4 13.2 8 411 32.2 28.2 7 370 -16.9 -17.2

Oranges 6 335 6 370 -12.3 -22.1 6 211 -8.5 -11.3 6 029 -7.9 -8.3

Manioc 1 797 3 161 53.3 36.3 4 519 34.1 30.0 4 648 -2.4 -2.8

Cotton 1 514 2 432 40.0 24.5 4 515 74.2 68.9 4 479 -5.9 -6.3

Banana 2 717 3 449 10.7 -1.6 3 846 4.6 1.4 3 981 -1.8 -2.2

Coffee 2 209 2 610 3.0 -8.4 3 696 32.8 28.7 3 960 1.6 1.2

Beans 3 503 4 479 11.5 -0.9 3 435 -28.1 -30.3 3 805 5.1 4.7

Tobacco 1 762 2 356 16.6 3.6 3 867 54.0 49.2 3 678 -9.8 -10.1

Tomatoes 1 810 2 634 26.9 12.8 3 131 11.5 8.1 2 819 -14.6 -14.9

Wheat 1 093 2 684 114.1 90.3 2 384 -16.7 -19.2 1 978 -21.3 -21.6

Others 4 027 5 040 9.1 -3.0 5 916 10.1 6.7 5 254 -15.8 -16.1

Total 70 757 99 823 23.0 9.3 106 780 0.3 -2.7 97 143 -13.7 -14.0

Source: IBGE and FGV

1/ In R$ million. Estimated by crops, adjusted by average price.

2/ Real % change, deflated by IPCA.

3/ Real % change, deflated by IPP – Prices Paid by Farm Producers.

4/ First two months of 2005, compared to same period of 2004.

Table 3 – Retail sales – Volume

Quarter/previous quarter1/

2005

Jan Feb Mar Apr

Rio Grande do Sul 1.19 1.46 -0.06 -1.89

Paraná 3.86 0.14 -4.24 -7.53

Santa Catarina 2.57 2.56 1.84 -1.07

Minas Gerais 2.77 0.20 -0.73 -3.26

Mato Grosso 3.52 2.61 -2.64 -2.70

Brazil 2.74 2.12 0.41 -0.51

Source: IBGE

1/ Seasonally adjusted data.

������������������ ���������������

On the other hand, products such as rice and beans,which are important components of the consumerbasket – respective weights of 0.76% and 0.48%in the IPCA – were not significantly affected byweather conditions, as is evident in Table 1. Thoughthe price of rice dropped 21.3% in the first twomonths of the year, compared to the same periodof 2004, the price of beans increased 5.5%.

The effects of the crop reduction have beensignificant for some agricultural export products.According to the Foreign Trade Secretariat of theMinistry of Development, Industry and ForeignTrade (SECEX/MDIC), corn export volume totaled1 million tons in the first five months of 2005,dropping 62.4% in relation to the same period of2004. On the other hand, soybean export volumegrew 11.9% in the first five months of the year. Ofnote, despite the soybean crop reduction relative toinitial predictions, this year’s soybean output will begreater than 2004.

Table 4 – Domestic production and sales of farm machines – January to April

2000 2001 2002 2003 2004 2005

Sales of farm machines (units) 6 630 8 657 10 624 9 974 12 146 7 486

% change - 30.57 22.72 -6.12 21.78 -38.37

Growth in production of capital goods for the agricultural sector (%) 3.37 30.11 4.28 15.80 25.06 -31.73

Growth in production of parts for farm machines (%) - - - 44.83 22.93 -67.96

Source: Fenabrave and IBGE

�������������������������� ��������

indicates a coffee harvest of 2.2 million tons, 11.4% lessthan that of 2004, reflecting falloffs of 0.9% in the areaharvested and 10.6% in average yield.

������

According to the IBGE Quarterly Animal Slaughter Survey,beef production came to 1.5 million tons in the fourth quarterof 2004, mirroring growth of 12.5% compared to the sameperiod in 2003. For the year, production expanded by 19%,the highest annual growth rate since 1997 when the serieswas first compiled. To some extent, this performancereflects the export dynamics of the sector. In the first fourmonths of 2005, exports totaled 304.6 thousand tons, up23.6% over the same period of 2004. Recent figures havealso been positive: beef exports expanded by 9.7% in thethree-month period ended in April, compared to January andseasonally adjusted.

The overall volume of poultry slaughtered increased 13.8%in the last quarter of 2004, compared to the same period ofthe previous year, with annual cumulative growth of 13.4%.Compared to the previous year, 2004 exports totaled 2.4million tons, up 26.1%. In 2005, exports have continuedexpanding, posting an increase of 27% in the first four monthsof the year, compared to the same period of 2004.

Output of swine totaled 464.5 thousand tons in the finalquarter of 2004, reflecting a drop of 4.8% compared to thesame period of 2003. Cumulative production for the yeardeclined 2.6%, partly as a result of import quotas adoptedby Russia, the main market for Brazilian pork exports. Porkexports totaled 471 thousand tons in 2004, up 2.8% year-on-year. In the year through April, pork exports reached169.2 thousand tons, up 39.7% over the same period of 2004.

Data from the IBGE Monthly Industrial Survey (PIM) pointto continued growth in livestock production in the current year.Confirming these expectations, beef and pork slaughteringand manufacturing expanded 3.5% in the first quarter, quarter-on-quarter seasonally adjusted, while poultry output rose 0.3%.

�����������������

In the early months of 2005, the level of industrial activityconfirmed the tendency toward more stable, albeit still high,growth evident since the end of 2004, with only slightvariation at the margin.

Figure 1.7 – Livestock – Total slaughters2002=100

90

95

100

105

110

115

120

125

Mar2003

Jun Sep Dec Mar2004

Jun Sep Dec Mar2005

Cattle and swine Poultry

Source: IBGE

Table 1.5 – Livestock production

Total slaughters

% accumulated growth

2004

Sep Oct Nov Dec

Cattle 21.4 19.7 19.8 19.0

Swine -1.9 -3.5 -3.2 -2.6

Poultry 13.2 12.9 13.1 13.4

Source: IBGE

������������������� ���������������

According to the IBGE, industrial production dropped 0.4%in the quarter ended in April, quarter-on-quarter seasonallyadjusted. Production of the manufacturing sector dropped0.5% and mining output, which accounts for 4.96% of totalindustrial production, increased 3.7%. In annual terms,industrial activity expanded 4.5% in the first four months ofthe year, compared to the same period of 2004, with growthof 7.3% in mining and 4.3% for manufacturing.

The leveling off of growth in industrial activity was evidentin the diffusion index. Based on three-month seasonallyadjusted moving averages, 96% of industrial activitiesregistered positive growth at the end of the first half of 2004,dropping to 57% at end-2004, and standing at 61% at theclose of the first four months of 2005.

Analysis of manufacturing activities by use category showshighly different performance. While consumer durable goodsoutput registered results similar to those of 2004, the outputlevels of the other categories stabilized or declined slightly.

Capital goods output has been relatively stable since thesecond half of 2004, registering a reduction of 1.6% in thequarter ended in April, quarter-on-quarter seasonallyadjusted. In the first four months of 2005, production underthis heading expanded 2.8%, in relation to the same periodof 2004, compared to an average of 4.5% for the aggregateindustrial sector. To some extent, the postponement ofbusiness investments, as demonstrated in the negative ratesof gross fixed capital formation in the national accounts forthe last quarter of 2004 and the first quarter of 2005, partlyexplains the recent performance of capital goods output.

Furthermore, the slowdown in capital goods productionreflected the loss of farm sector profitability in the currentyear, with the drop in the output of capital goods concentratedin those to the farm sector. This is clear in reductions of68% in the production of spare parts for farm machineryand 31.7% in the output of capital goods for the farm sector,when the first four months of 2005 are compared to thesame period of 2004. Capital goods production for theconstruction industry increased by 30.3%, followed byelectricity generation and distribution (14%), andtransportation equipment (11.1%). Production of capitalgoods for the industrial sector expanded 5.9%.

Intermediate goods production, which accounts forapproximately 53.3% of total industrial production, diminished1.3% in the quarter ended in April, quarter-on-quarter,seasonally adjusted. Cumulative production in the first four

Table 1.6 – Industrial production% change

2005

Jan Feb Mar Apr

Industry (total)

In the month1/ - 0.5 - 1.4 1.5 0.0

Quarter/previous quarter1/ 0.6 0.3 - 0.2 - 0.4

Same month of the previous year 5.9 4.1 1.8 6.3

Accumulated in the year 5.9 5.0 3.8 4.5

Accumulated in 12 months 8.5 8.6 7.6 7.5

Manufacturing industry

In the month1/ - 0.3 - 1.2 1.0 - 0.5

Quarter/previous quarter1/ 1.0 0.7 0.1 - 0.5

Same month of the previous year 5.9 4.2 1.6 5.9

Accumulated in the year 5.9 5.1 3.8 4.3

Accumulated in 12 months 8.7 8.8 7.8 7.6

Mining

In the month1/ 1.0 0.2 0.5 7.4

Quarter/previous quarter1/ 0.2 1.2 1.5 3.7

Same month of the previous year 7.4 1.5 6.4 13.7

Accumulated in the year 7.4 4.5 5.1 7.3

Accumulated in 12 months 4.9 4.7 5.2 6.3

Source: IBGE

1/ Seasonally adjusted data.

95

105

115

125

135

145

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

Total Manufacturing industry Mining

Figure 1.8 – Industrial productionSeasonally adjusted data2000=100

Source: IBGE

�������������������������� ��������

months of 2005, compared to the corresponding period ofthe previous year, increased 2.1%, the slowest growth amongthe different use categories.

Just as in the case of capital goods, the falloff in intermediategoods output was partly caused by adverse conditions inthe farm sector in the first months of the year. The drop inthe harvest impacted performance in the production offertilizers and soil correction products and pesticides,generating a 1.6% drop under the heading “other chemicalproducts” in the quarter ended in April, quarter-on-quarterseasonally adjusted. Production of intermediate goods alsoreflected the negative performance of petroleum andalcohol1 refining activities, down 7.4% in the same periods.

After peaking in January 2005, production of semi- and non-durable consumer goods dropped 0.7% in the quarter endedin April, quarter-on-quarter. On the one hand, this resultreflected increases in the output of pharmaceutical goods,6.5%; perfumes and cleaning products, 3.6%; clothing andaccessories, 2.5%; and beverages, 1.1%; and, on the otherhand, downturns under food, and shoes and leather goods,with respective declines of 0.6% and 1.9%, in the sameperiods. Cumulative output of this category in the yearthrough April, expanded 6.2%, compared to the first fourmonths of 2004, the year in which growth closed at 4%.

Recent exchange rate appreciation and higher domesticincome levels have favored competitiveness of severalimported semi- and non-durable consumer goods, thoughthis fact has not significantly impacted on domestic output.According to the Foreign Trade Studies Center Foundation(Funcex), in the first quarter of 2005, imports of dairyproducts grew 62%, while clothing imports increased 50.4%and shoes and leather, 22.5%, compared to the same periodof the previous year.

Consumer durable goods was the only category to registerincreased output in the quarter ended in April, quarter-on-quarter seasonally adjusted. The 7.2% growth registered inthe period was due to both the continued expansion inconsumer credit and positive export market figures. In thelatter case, the leading categories were electronics andcommunications devices, and automobiles, pickups and utilityvehicles. Production of electronics and communicationsdevices, which have an estimated weight of 8.8% in thecategory, registered a cumulative increase of 22.2% in thefirst four months of the year, compared to the same period

96

110

124

138

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

Figure 1.9 – Industrial productionCapital goodsSeasonally adjusted data2000=100

Source: IBGE

Table 1.7 – Industrial production by category of use% change

2005

Jan Feb Mar Apr

In the month1/

Industrial production - 0.5 - 1.4 1.5 0.0

Capital goods - 1.0 - 3.3 3.9 - 2.9

Intermediate goods - 1.3 - 1.7 0.7 1.3

Consumer goods 1.5 - 1.4 0.8 - 0.2

Durable - 4.6 9.9 - 0.3 - 0.3

Semi and nondurable 3.7 - 4.0 - 0.1 - 0.3

Quarter/previous quarter1/

Industrial production 0.6 0.3 - 0.2 - 0.4

Capital goods 0.6 0.9 - 0.4 - 1.6

Intermediate goods - 0.8 - 0.9 - 1.7 - 1.3

Consumer goods 2.9 3.2 2.6 0.8

Durable - 0.4 3.3 4.0 7.2

Semi and nondurable 4.0 4.4 3.2 - 0.7

In the year

Industrial production 5.9 5.0 3.8 4.5

Capital goods 6.8 3.8 2.6 2.8

Intermediate goods 4.0 2.5 1.5 2.1

Consumer goods 8.3 8.3 6.7 7.7

Durable 3.3 11.4 12.0 13.5

Semi and nondurable 9.5 7.5 5.4 6.2

Source: IBGE

1/ Seasonally adjusted data.

1/ Around 69.6% of oil and alcohol refining is intermediate consumption.

������������������� ���������������

of 2004. This growth was driven mainly by domestic andexternal sales of cellular telephones. Sectoral Funcex dataindicated 99.4% expansion in exports of electronics in thefirst quarter of this year, compared to the same period ofthe previous year.

According to IBGE data, output of automobiles, pickups andutility vehicles, including engines, which account forapproximately 40% of consumer durables produced, rose16.3% in the first four months of 2004, compared to thesame period of the previous year.

Furthermore, information released by the NationalAssociation of Automotive Vehicle Manufacturers(Anfavea) indicates that production of automotive vehicleshas followed a consistently upward trend, driven by theexport market. While output of the automotive industryexpanded 3.2%, seasonally adjusted in the three-monthperiod ended in May, as against the three months throughFebruary, exports increased 6.7% and domestic sales grewby 3.8% in the same period. In year-on-year terms, theexport/domestic growth ratio was quite similar, as 15.4%growth in automotive vehicle output was fuelled by a 45.5%expansion of exports and 4.2% for domestic sales.

According to figures released by the CNI, real industrialsales grew 0.6% in the quarter ended in April, quarter-on-quarter seasonally adjusted. Cumulative growth in the yearstood at 2.6%, seasonally adjusted, with relative stabilityover the last four months at a historically high level.

Other industrial indicators released by the CNI repeatedthe same picture of stability at a high level. In the three-month period ended in April, the indicator of hours workedremained at practically the same average posted in theprevious three-month period, seasonally adjusted.Employment and overall real wages in the industrial sectorincreased 1% and 0.5%, respectively. Hours worked,employment and overall wages rose 7.1%, 6.9% and 9.0%,respectively, in the first four months of the year, comparedto the same period of 2004.

Installed capacity utilization in the manufacturing sectorremained stable in the first quarter of the year, standing at84.5%, compared to 84.6% in the last quarter of 2004,according to Getúlio Vargas Foundation (FGV) dataseasonally adjusted by the BCB. The intermediate goodssector posted the highest level of installed capacity utilization,

95

106

117

128

139

150

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

Figure 1.11 – Industrial productionConsumer goodsSeasonally adjusted data2000=100

Source: IBGE

94

97

100

103

106

109

112

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

Figure 1.12 – Industrial productionSemi and nondurable goodsSeasonally adjusted data2000=100

Source: IBGE

90

105

120

135

150

165

180

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

Semi-manufactured Manufactured

Figure 1.13 – Industrial exports – VolumeSeasonally adjusted data2002=100

Source: Funcex

103

107

110

114

117

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

Figure 1.10 – Industrial productionIntermediate goodsSeasonally adjusted data2000=100

Source: IBGE

�������������������������� ��������

88.7%, repeating the previous quarter’s result. In thesegment of consumer goods, installed capacity utilizationrose 1.6 p.p. in the quarter, to 79.6%, while for constructionmaterials this indicator increased 1.1 p.p. to 84.8%. Theonly category whose installed capacity utilization decreasedwas the capital goods industry, with 82.3% in the first quarterof 2005, compared to 83.6% in the last quarter of 2004.

According to CNI, installed capacity utilization reached 81.8%in April, 0.8 p.p below the average for the previous year.

Based on the CNI Industrial Survey, industrial companiesposted inventory growth for finished products and stabilityfor raw materials in the first quarter of the year. Theinventory level of inputs is considered normal, but that offinished products was higher than expected – the indicatorreached 54.4 points in the most recent survey, 3.8 pointsabove the same period of the preceding year. The FGVquarterly survey ratified the result of unplanned inventorygrowth, registering a difference of 8 points betweencompanies that consider their inventories excessive and thosethat considered them insufficient. This was the largestdifference since October 2003. The responses provided bybusiness people regarding inventory formation are consistentwith the deceleration in industrial sales in recent months.

In general, expectation indicators remain optimistic, thoughthere has been a certain dampening of enthusiasm in theindustrial sector. The reduction in confidence has been uniformamong executives from large, small and medium businessesand the CNI Industrial Confidence Index (ICEI) dropped from64.9 points in January to 55.8 points in April. The twocomponents of this indicator registered declines. However,the index of current conditions crossed the divider betweenoptimism and pessimism, falling to 46.1 points, reflecting anevident state of dissatisfaction. At the same time, theexpectations index for the coming six months remained above50 points. In other words, business sentiment regarding currentconditions is worse than their prognosis for the near future.

The disparity between perceptions of the current situationand perceptions of the future is repeated in other indicators.According to the quarterly FGV survey, the proportion ofcompanies that point to insufficient demand as the limitinggrowth factor in their activities rose in the survey for thefirst quarter of 2005, compared to the previous quarter. Morethan half of the companies surveyed, nonetheless, expectdemand for their goods to increase in the second quarter ofthe year and fully intend to raise output in that period.

85

95

105

115

125

135

145

Feb2003

May Aug Nov Feb2004

May Aug Nov Feb2005

May

Production Sales

Figure 1.14 – Vehicles – Production and salesSeasonally adjusted data2002=100

Source: Anfavea

100

110

120

130

140

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

Production (IBGE) Sales (CNI)

Figure 1.15 – Industrial production and salesSeasonally adjusted data2000=100

Source: IBGE and CNI

Table 1.8 – Vehicles – Production and sales

% change

2005

Jan Feb Mar Apr May

In the month1/

Production -7.7 8.7 -1.3 3.0 -1.2

Total sales -14.2 7.7 3.0 2.0 4.9

Domestic sales -16.8 2.1 6.9 3.3 -0.3

External sales -0.5 11.5 0.0 -2.2 3.0

Quarter/previous quarter1/

Production -1.1 2.0 0.8 4.7 3.2

Total sales 0.6 3.7 -1.7 3.1 5.7

Domestic sales 1.6 0.9 -6.1 -0.8 3.8

External sales 1.4 12.0 11.0 11.8 6.7

In the year

Production 3.1 11.5 12.6 14.4 15.4

Total sales -4.1 3.8 8.0 12.6 15.0

Domestic sales -11.6 -8.9 -2.1 2.0 4.2

External sales 18.3 45.8 38.1 43.6 45.5

Source: Anfavea

1/ Seasonally adjusted data.

������������������� ���������������

Also according to the FGV survey, the balance of 20 pointsin favor of companies that expect to increase hirings,compared to those that foresee layoffs, confirms theoptimism surrounding industrial evolution in the comingmonths. However, when these data are compared toquarterly CNI figures, the result points to performances thatvary depending on the size of the company.

Small- and medium-sized businesses, with relatively lessaccess to foreign trade and funding, have demonstrated lesswillingness to hire additional labor, though these companiesare already labor intensive. This segment registered areduction in the number of employees in the first quarter of2005, compared to the previous quarter, and stability in thenumber of jobs for the next six months. Large companies,on the other hand, hired additional labor in the first quarterand expressed their intention to continue doing so.

While the tax burden and interest rates remain a point ofconcern among small, medium and large companies, theirpositions differ regarding other factors that may hampershort-term industrial growth. While exchange rateappreciation is cited as the third factor by large companiesand as the ninth by small and medium companies, insufficientdemand is the sixth most important limiting factor accordingto large scale industries, and fourth when judged by smalland medium enterprises.

Therefore, the current scenario suggests an attitude ofrelative caution on the part of businesses, with somewhattempered though still positive expectations regarding industrialsales and inventory formation, coupled with moderate growthin output of capital goods for the industrial sector. It is possiblethat industry has decided to await clearer signs of increaseddemand before deciding on investments and a more dynamicpace of activity.

��� �����������

���������

Unemployment expanded in the first quarter of the year,closing at 10.8% in March (compared to 9.6% in December),stabilized in April and dropped to 10.2% in May, accordingto the IBGE Monthly Employment Survey (PME). Thisbehavior reflected seasonal factors in the period.

Compared to the corresponding period of 2004, averageunemployment in the first five months of the year declined

Figure 1.16 – Utilization of installed capacity in the manufacturing industrySeasonally adjusted data%

78

80

82

84

86

Jan2003

Apr Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

CNI FGV

Source: CNI and FGV

30

50

70

Apr2002

Jul Oct Jan Apr2003

Jul Oct Jan Apr2004

Jul Oct Jan Apr2005

Icei Current conditions

Expectations

Source: CNI

Figure 1.17 – Business Confidence Index

Table 1.9 – Manufacturing industry inventories1/

2004 2005

I II III IV I

Manufacturing industry

Final products 50.6 50.3 49.6 51.3 54.4

Raw materials/intermediate goods 47.6 48.7 48.8 49.8 50.4

Large companies

Final products 52.2 52.1 51.5 53.8 56.6

Raw materials/intermediate goods 49.7 51.5 51.2 53.6 54.0

Small and medium companies

Final products 49.8 49.4 48.6 50.0 53.3

Raw materials and interm. goods 46.5 47.3 47.6 47.8 48.6

Source: CNI

1/ Values over fifty indicate inventories above the planned level.

�������������������������� ��������

1.8 p.p., indicating expansion of 3.8% in the number of jobholders and a 13.5% drop in the number of unemployedworkers. Using the same comparison basis, 712 thousandjobs were created, of which 513 thousand in the formal sectorof the economy and 181 thousand in the informal market.

Ministry of Labor and Employment (MTE) data confirmthe recovery in job generation. According to the GeneralFile of Employed and Unemployed Individuals (CAGED),770.8 thousand formal jobs were created in the January/May period, compared to 826.8 thousand in the same periodof 2004. The service sector accounted for the largest numberof openings, with 304.5 thousand, followed by manufacturing,with 177 thousand openings; crop/livestock activities, 107.1thousand; commerce, 101 thousand; and the civil constructionsector, 41.9 thousand.

A CNI survey among twelve state industrial associationscorroborates the positive evolution of the labor market in themanufacturing sector, showing an increase of 6.9% inemployed workers in the first four months of 2005, comparedto the same period of the previous year. Industrial employmentgrew 1% in the quarter ended in April, quarter-on-quarterseasonally adjusted. However, growth rates have declinedsince the third quarter of 2004. This behavior is fully consistentwith the recent leveling off of activity in the sector.

��������

The average real earnings of workers in the six metropolitanregions covered by the PME expanded by 1.5% in the firstfive months of 2005, compared to the same period of 2004.In nominal terms, average earnings reached R$932.80 inMay, up 7.7% over the same month of 2004.

On May 1, 2005, the minimum wage increased 15.4% toR$300, a real gain of 8.2%, when the cumulative NationalConsumer Price Index (INPC) from May 2004 to April 2005is used as deflator.

According to CNI, overall real wages in the manufacturingindustry, deflated by INPC, expanded 9.0% in the first fourmonths of 2005, compared to the same period of 2004, and0.5%, quarter-on-quarter seasonally adjusted. Similar toemployment in this sector, overall real wages expanded atlower rates in early-2005. Compared to the immediatelypreceding quarters, growth came to 2.7%, 3.5% and 0.5%in the third and fourth quarters of 2004 and first quarter of2005, respectively.

Figure 1.18 – Unemployment rate%

9

10

11

12

13

14

Jan Feb Mar Apr May Jun Jul Ago Sep Oct Nov Dec

2003 2004 2005Source: IBGE

Figure 1.20 – Average real regular earningsIn R$ of May 2005, deflated by INPC

900

925

950

975

1000

1025

Feb2003

May Aug Nov Feb2004

May Aug Nov Feb2005

May

Source: IBGE

-3

-2

-1

0

1

2

3

4

Feb2004

Apr Jun Aug Oct Dec Feb2005

Apr

Source: CNI

Figure 1.19 – Employment in the manufacturing industry – Quarterly moving averageSeasonally adjusted data% change

Table 1.10 – Formal employment

New job openings – Accumulated in the year (1,000 employees)

2004 2005

Jan Feb Mar Apr May

Total 1 523.3 116.0 189.3 292.2 558.3 770.8

Manufacturing industry 504.9 32.8 33.7 51.6 131.1 177.0

Commerce 403.9 11.2 19.8 33.8 67.1 101.0

Services 470.1 54.5 105.2 159.3 246.8 304.5

Building 50.8 7.9 8.8 15.0 29.6 41.9

Crop and livestock 79.3 4.1 2.6 4.2 48.4 107.1

Public utilities 4.6 2.7 4.5 6.1 7.8 8.5

Others1/9.7 2.8 14.7 22.2 27.5 30.8

Source: MTE

1/ Includes mining, public administration and others.

������������������� ���������������

��� ���������� ��� ��

According to IBGE, GDP expanded by 2.9% in the firstquarter of 2005, compared to the same period of 2004. Thisresult confirms the expected deceleration of economic activity,following the strong recovery of 5.9% and 4.7% in the thirdand fourth quarters of 2004, compared to the same quartersof 2003. A component-by-component analysis of this resultshows across-the-board expansion, in terms of either supplyor demand (see box “Outlook for GDP in 2005”).

A sector-by-sector breakdown shows that the sharpestgrowth, 4.2%, occurred under crop/livestock farming. Thisreflected the positive performance of livestock and relevantfirst quarter crops, such as cotton and rice. It is important tohighlight that the impact of the grain harvest decline will befelt more intensely in the second quarter of the year.

Industry posted growth of 3.1% in the quarter, with aparticularly strong recovery in mining. To a great extent,this was due to 3.8% greater oil output, according to datareleased by the National Petroleum Agency (ANP). Themanufacturing sector grew for the eighth consecutivequarter, 3.6%, though this figure decelerated compared toprevious quarters. Public utilities and the construction industryclosed with positive growth, albeit at a somewhat lesser rate.

In the first quarter of 2005, the service sector expanded2%, keeping pace with the positive performance registeredin other sectors of the economy. Here, it is important tounderscore the performance of commerce, transportationand financial institutions, which grew 4.2%, 4.1% and 2.8%,compared to the first quarter of 2004, while communicationsservices dropped 3.2%. This result followed the reductionin fixed telephone services.

In terms of demand, the dynamics of the external sectorcontinued through the first quarter of 2005. Exportsexpanded by 13.6%, while imports rose 12.2%, comparedto the same period of the previous year. Import volumeincreased mainly for capital goods and consumer goods,reflecting the economic activity rebound. Regarding domesticdemand, household consumption increased 3.1%; gross fixedcapital formation, 2.3% and government consumption, 0.7%.

On quarter-on-quarter seasonally adjusted terms, GDPexpanded by 0.3% in the first quarter, driven mainly by the2.6% expansion in crop/livestock activities. Confirming thebehavior of monthly activity level indicators, industryregistered a falloff of 1.0% and services dropped 0.2%,

94

98

102

106

110

114

118

Feb2003

Apr Jun Aug Oct Dec Feb2004

Apr Jun Aug Oct Dec Feb2005

Apr

Figure 1.22 – Real payroll in the manufacturing industrySeasonally adjusted data2000=100

Source: CNI

140

170

200

230

260

290

320

1998 1999 2000 2001 2002 2003 2004 2005

Figure 1.21 – Real minimum wage1/

In R$ of May 2005

Source: MTE1/ On the readjustment month; deflated by INPC.

-4

-2

0

2

4

6

8

10

12

I2003

II III IV I2004

II III IV I2005

Crop and livestock Industry Services GDP

Source: IBGE

Figure 1.23 – Gross Domestic ProductQuarter/same quarter of the previous year% growth

�������������������������� �������

primarily as a consequence of results in the area of telephoneservices. These two sectors registered positive growth inthe seven previous quarters.

As signaled by leading indicators, recent GDP growthconfirms perceptions of a more moderate pace of economicexpansion, after growing continuously since the secondquarter of 2003.

With the disclosure of the first quarter results, the IBGEhas revised the Quarterly National Accounts, which,according to the new methodology, can be done in anyquarter of the year and not just annually, as before. Therevision covered the second, third and fourth quarters of2004, and altered the GDP growth rate for that year, from5.2% to 4.9%.

��! "�#������

According to IBGE’s Quarterly National Accounts,investments excluding inventory variations dropped 3.0% inthe first quarter of 2005, quarter-on-quarter seasonallyadjusted. This was the second consecutive fall. Comparedto the same quarter of 2004, the growth rate came to 2.3%,with a cumulative four-quarter expansion of 11.0%.

The seasonally adjusted result of the first quarter of theyear was anticipated by some leading investment indicators,which indicated negative results in the early months of theyear, especially January and February.

Indicators for the month of April point to a continued declinein gross fixed capital formation. Construction input andcapital goods production declined 1.1% and 2.9% in April,respectively, on a month-on-month seasonally adjusted basis,while exports and imports of these goods increased 6.2%and 3.0%, respectively.

The modest performance of investments was, in part, dueto the reduction of crop/livestock sector revenues, which inturn impacted demand for farm machinery and equipment.As a consequence, output of farm machinery and equipmentplunged 31.7% and 68%, respectively, in the first four monthsof the year, compared to the same period of 2004. Theseresults contrast sharply with the performance of othersegments of capital goods output, particularly products forthe construction industry, electricity production andtransportation, which grew 30.3%, 14% and 11.1%,respectively, in the same period.

Table 1.11 – Gross Domestic Product

Change quarter/same quarter of the previous year

%

2004 2005

I Q II Q III Q IV Q I Q

Crop and livestock 5.8 6.0 5.9 3.0 4.2

Industry 5.5 6.3 7.0 5.9 3.1

Mining 2.2 2.0 2.0 -8.0 3.7

Manufacturing 9.1 6.8 6.6 8.3 3.6

Construction -0.8 6.9 11.6 5.2 0.6

Public utilities 1.5 5.9 5.2 5.8 2.9

Services 2.4 3.2 4.1 3.6 2.0

Commerce 4.8 8.9 10.5 7.3 4.2

Transportation 10.6 5.9 0.4 3.6 4.1

Communications -1.4 -2.7 -1.4 0.1 -3.2

Financial institutions 2.1 4.6 5.2 5.0 2.8

Other services 2.1 7.1 7.1 6.2 2.0

Rents 1.2 1.5 2.2 2.1 3.7

Public administration 2.0 -0.7 1.3 0.9 0.2

Financial dummy 0.4 5.4 6.0 5.7 2.7

Value added at basic prices 4.0 4.7 5.3 4.2 2.6

Taxes on products 4.0 8.5 11.1 8.9 4.7

GDP at market prices 4.0 5.1 5.9 4.7 2.9

Source: IBGE

Table 1.12 – Gross Domestic ProductQuarter/previous quarter

%

2004 2005

I Q II Q III Q IV Q I Q

GDP at market prices 4.0 5.1 5.9 4.7 2.9

Households consumption 1.6 4.3 5.3 5.0 3.1

Government consumption 0.8 -1.4 0.3 0.8 0.7

Gross fixed capital formation 1.8 13.4 19.3 9.3 2.3

Exports 20.5 17.6 18.2 16.2 13.6

Imports 12.5 14.2 17.7 12.8 12.2

Source: IBGE

Table 1.13 – Gross Domestic Product

%

2004 2005

I II III IV I

Accumulated in the year 4.0 4.6 5.0 4.9 2.9

Accumulated in 4 quarters 1.2 2.4 4.0 4.9 4.6

Quarter/same quarter

of the previous year 4.0 5.1 5.9 4.7 2.9

Quarter/previous quarter

seasonally adjusted 1.8 1.1 1.3 0.4 0.3

Source: IBGE

������������������ ���������������

� ���������� ���$$!

The GDP growth estimate for 2005 was reviseddownward from 4.0% to 3.4%, primarily as aconsequence of three factors: recent demanddynamics, the lower than expected agriculturalharvest, and IBGE’s revision of 2004 QuarterlyNational Accounts.

The economy evolved in line with expectations inthe first quarter of the year, with only slight growth,as had occurred in the last quarter of 2004. However,the GDP result demonstrated a greater-than-expected drop in domestic demand, which was onlypartially offset by stronger external demand. Oncechanges in inventories are excluded, both householdconsumption and investment declined in the quarter.In the case of consumption, the decline was a resultof rising inflation at end-2004 and early-2005 and itsimpact on real earnings, of higher credit default rates,and of the reduction in farm revenues. Investments,which have been declining since the end of 2004,also reflected farm revenue losses, as well as theuncertainties surrounding the evolution of demand inthe context of the monetary tightening cycle.

Aside from lower growth in the first quarter of theyear, the increased inflation contributed to a morerestrictive scenario than that originally anticipated forthe second quarter. Indicators for the early months ofthe quarter point to continued very moderate growthin the economy, just as occurred in the two previousquarters. Consequently, growth estimates for householdconsumption and investments in 2005 were reviseddownwards to 2.6% and 2.3%, respectively.

These growth estimates are based on a recovery inthe pace of growth in the second half of the year,made possible by the convergence of inflation to the

�������������������������� ��������

target path, as already shown in the most recentinflation results and forecasts. With regard toinvestment, continued positive macroeconomicfundamentals – as demonstrated by the reduction insovereign risk – point to a recovery in the secondhalf of the year. The correlation between sovereignrisk and investment showed a highly atypical behaviorin the first quarter of the year.

Contrasting with the estimated reduction inhousehold consumption and investments, the GDPforecast indicates that exports will increase, thusensuring that the growing participation of the

Figure 1 – Investment and Brazil-risk

105

115

125

135

I2000

II III IV I2001

II III IV I2002

II III IV I2003

II III IV I2004

II III IV I2005

II III

300

600

900

1 200

1 500

1 800

2 100

Investment Brazil-risk (t-2)

Brazil-risk (t-2)Investment1990=100

Source: IBGE and J P Morgan Chase

Table 1 – GDP%

Period GDP Household Government Total Gross Fixed Exports Imports

consumption consumption consumption Capital Formation1/

Weight (2004) 100.0 55.3 18.8 74.1 21.3 18.0 -13.3

2000 4.4 3.8 1.3 3.2 10.0 10.6 11.6

2001 1.3 0.5 1.0 0.6 -1.1 11.2 1.2

2002 1.9 -0.4 1.4 0.1 -4.3 7.9 -12.3

2003 0.5 -1.5 1.3 -0.8 -4.5 9.0 -1.7

Contribution (p.p.) -0.8 0.3 -0.6 -0.9 1.5 0.2

2004 1st. half-year 5.0 3.0 0.8 2.5 7.5 18.9 13.4

Contribution (p.p.) 1.7 0.2 1.8 1.6 3.4 -1.8

2004 Through 3rd. quarter 5.3 4.0 0.6 3.1 11.5 18.7 14.9

Contribution (p.p.) 2.2 0.1 2.3 2.4 3.4 -2.0

2004 4.9 4.1 0.1 3.1 6.3 18.0 14.3

Contribution (p.p.) 2.2 0.0 2.3 1.3 3.2 -1.9

2005 (forecast) 3.4 2.6 1.6 2.3 2.3 14.8 11.5

Contribution (p.p.) 1.4 0.3 1.7 0.5 2.7 -1.5

Source: IBGE

1/ Includes inventories.

������������������� ���������������

external sector in GDP will continue. Estimatesregarding the evolution of government consumptionin the year remained unchanged.

As far as supply is concerned, the impact of adverseweather conditions on the grain harvest resulted in areduction in estimates of crops/livestock growth. Theimpact of the reduced harvest on the performanceof the sector is expected to be relatively small, dueto the surge in livestock production, which hasregistered record export levels, and to favorableestimates for specific important crops, such as cottonand manioc. However, there is no denying that theharvest reduction will produce impacts in other areas,such as lower demand of inputs for the sector.

In industry, growth forecasts for the manufacturingand construction industries were revised downward,due to the results of the first four months of the year.Despite the downward revision, annual growth inmanufacturing is estimated at 3.7%, as a result ofincreased exports and recovery in domestic demandin the second half of the year. Furthermore, newPetrobrás drilling platforms went into operation in thesecond quarter, raising output estimates for the miningsector in the current year.

Estimates for the service sector were also altered asa result of reduced growth in industry and agriculture(as well as incorporation of first quarter results), withclear impacts on commerce, transportation, financialinstitutions and other services.

Another factor responsible for the downward revisionin estimates for the service sector was theaccentuated IBGE´s revision of growth for thecommunications sub-sector in 2004, from +2% to -1.4%. Such a change impacted the product of thesector in the first quarter of 2005 and the outlook forthe year.

Table 2 – GDP 2005

Weight % accumulated growth

2004 2004 2005

1st Q Year estimate

Crop and livestock 10.1 5.3 4.2 4.0

Industry 38.9 6.2 3.1 3.7

Mining 4.2 -0.7 3.7 8.3

Manufacturing 24.0 7.7 3.6 3.3

Construction 7.3 5.7 0.6 1.7

Public utilities 3.4 4.6 2.9 4.3

Services 55.7 3.3 2.0 2.7

Commerce 7.8 7.9 4.2 4.0

Transportation 2.2 4.9 4.1 3.9

Communications 3.1 -1.4 -3.2 0.0

Financial institutions 6.6 4.2 2.8 3.6

Other services 10.5 5.6 2.0 3.6

Rents 9.4 1.8 3.7 3.1

Public administration 16.1 0.9 0.2 1.2

Taxes on products 11.7 8.2 4.7 4.6

GDP at market prices 100.0 4.9 2.9 3.4

Quarter/previous quarter

(seasonally adjusted data) 0.3 ...

Source: IBGE

�������������������������� ��������

ANFAVEA data corroborate the behavior of investment inthe farm sector. More specifically, output of farm machinerydropped 12.4% in the year through May, when compared tothe same period of 2004. This result was primarily causedby reductions of 62.9% and 5.9% in the production ofharvesters and farm tractors, respectively. On the other hand,production of buses and trucks rose by 31.9% and 16.4%,respectively, powered mainly by exports, using the samecomparison basis.

Despite recent investment results, FGV surveys point to aseries of factors that suggest an upturn in the coming months,such as rising intentions to expand installed capacityutilization, coupled with the downward trend of Braziliancountry risk and expectations of a monetary policy easing.

The FGV February survey that analyzed investmentsprogrammed by companies for the 2005-2007 period, revealsa rather positive outlook for production capacity expansion.Average growth in capacity for 2005 is projected at 8%,and 19% for 2005-2007. These figures are similar to thosefound in the February 2004 survey. The survey also showsthat, among the factors that have inhibited investment growthin 2005, those most commonly cited by companies were thetax burden, with 46% of the respondents, and uncertaintiesregarding demand, with 33%, the highest level under thisquestion since 2000.

��% & ����'

The leveling off of economic activity since the end of 2004has been accompanied by changes in the composition ofdemand, with the external sector assuming a larger role tothe detriment of the domestic market. Externally, worldeconomic growth has driven the export sector, offsettingpossible impacts of recent exchange rate appreciation.Domestically, consumption has been stimulated by self-propagating forces – namely, increased jobs and higher realearnings. As a result, consumer spending tends to remainhigh, despite the slight drop posted in the first quarter of thisyear, following six consecutive quarters of positive growth.On the other hand, investments have trended downwardsince the end of 2004, partly reflecting the loss of farmincome, but also as a reaction to the recent evolution ofdemand in response to recent monetary tightening. Businessconfidence levels, the country risk, as well as the resultsrevealed by surveys within the industrial business communitypoint to an upturn in investments as soon as uncertaintiessurrounding the evolution of internal demand dissipate.

Table 1.14 – Gross Domestic Product

Quarter/previous quarter

Seasonally adjusted

%

2004 2005

I II III IV I

GDP at market prices 1.8 1.1 1.3 0.4 0.3

Crop and livestock 2.4 0.5 -1.6 1.8 2.6

Industry 1.6 1.0 2.6 0.4 -1.0

Services 1.2 1.0 0.9 0.4 -0.2

Source: IBGE

Tabela 1.15 – Investment indicators

% change

2005

Jan Feb Mar Apr

In the month1/

Capital goods

Production -1.0 -3.3 3.9 -2.9

Imports 1.7 -7.1 0.7 3.0

Exports -6.6 -9.4 0.7 6.2

Inputs for the building industry -0.2 -1.5 0.2 -1.1

In the year

Capital goods

Absorption2/6.2 2.8 2.5 2.1

Production 6.8 3.8 2.6 2.8

Imports 34.7 24.4 25.1 21.3

Exports 68.9 55.5 42.7 43.0

Inputs for the building industry 2.8 1.6 0.8 1.4

BNDES financing 69.5 20.0 11.5 -0.6

Source: IBGE, Funcex and BNDES

1/ Seasonally adjusted data.

2/ Production + imports - exports.

- 8

- 4

0

4

8

I2003

II III IV I2004

II III IV I2005

Figure 1.24 – Gross fixed capital formationQuarter/previous quarterseasonally adjusted data%

Source: IBGE

������������������� ���������������

Table 1.16 – Production of capital goods

% change in the year

2005

Jan Feb Mar Apr

Capital goods 6.8 3.8 2.6 2.8

Industrial 1.6 5.9 5.1 5.9

Serial 0.2 5.0 4.5 5.0

Nonserial 10.5 11.0 8.6 12.0

Agricultural -19.7 -26.7 -29.9 -31.7

Farm parts -70.0 -68.3 -68.4 -68.0

Building 33.8 37.6 33.2 30.3

Electric energy 19.0 17.3 13.7 14.0

Transportation 19.3 13.6 11.6 11.1

Mixed 4.2 -0.9 -1.5 -0.3

Source: IBGE

90

100

110

120

130

Apr2003

Jul Oct Jan2004

Apr Jul Oct Jan2005

Apr

88

93

98

103

Capital goods production Construction inputs

Source: IBGE

Figure 1.25 – Capital goods production and construction inputsSeasonally adjusted data2002=100

Capital goods productionConstruction inputs

Table 1.17 – Production of vehicles

% change

2005

Jan Feb Mar Apr May

In the month1/

Farm vehicles 4.9 -8.2 1.3 -5.8 0.8

Busses -3.7 -8.5 16.0 -1.0 0.2

Trucks -6.7 -6.6 9.2 2.1 -2.5

Quarter/previous quarter1/

Farm vehicles -5.6 -7.3 -6.0 -8.2 -6.4

Busses 19.4 4.4 -1.3 -2.7 7.2

Trucks 2.8 -0.6 -3.2 -3.1 2.3

In the year

Farm vehicles 2.9 -7.5 -10.5 -12.1 -12.4

Busses 65.0 43.7 37.1 34.4 31.9