Embed Size (px)

Citation preview

Inflation

Decomposing Sources of

Inflation

Jutimar Boonyingyongstit

1

“Nothing is more important to the conduct of monetary policy than understanding and predicting inflation. Price stability is our responsibility as central banks--it is how, in the long run, we contribute to society's welfare. Achieving and maintaining price stability will be more efficient and effective the better we understand the causes of inflation and the dynamics of how it evolves. ”

Donald L. Kohn

Governor of the Federal Reserve Board

May 20,2005

2

Motivation

• Purpose

• Literature Review

• First Purpose: Decompose Inflation Source

• Second Purpose: Monetary Policy Setting

• Robustness

• Conclusion

Outline

3

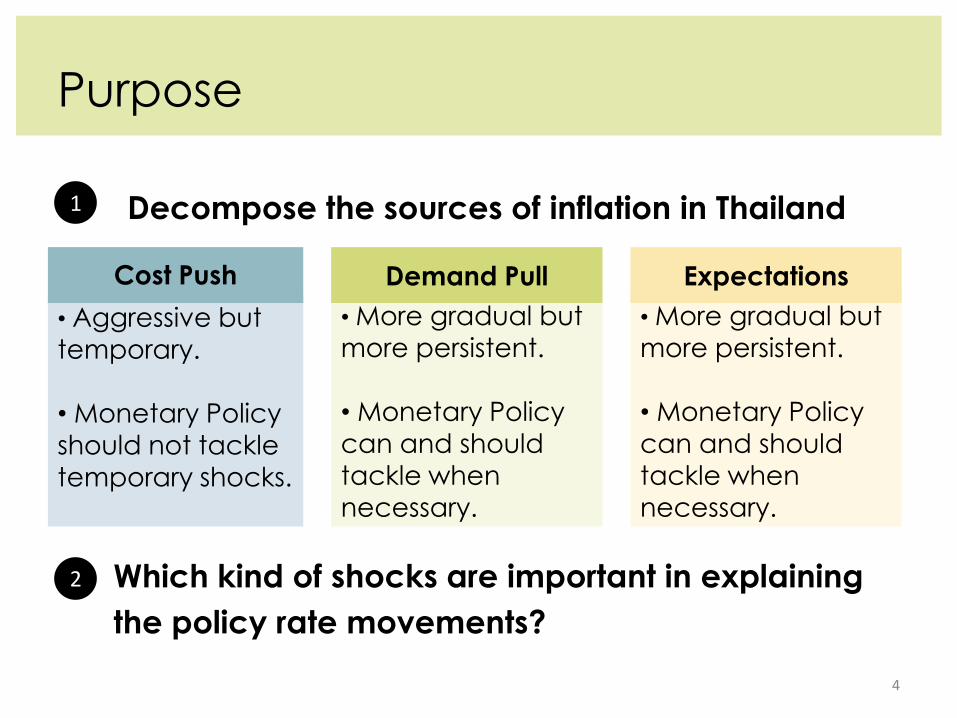

Purpose

Decompose the sources of inflation in Thailand 1

2 Which kind of shocks are important in explaining

the policy rate movements?

4

• Aggressive but

temporary. • Monetary Policy

should not tackle

temporary shocks.

Cost Push •

• More gradual but

more persistent.

• Monetary Policy

can and should

tackle when

necessary.

Demand Pull

• More gradual but

more persistent.

• Monetary Policy

can and should

tackle when

necessary.

Expectations

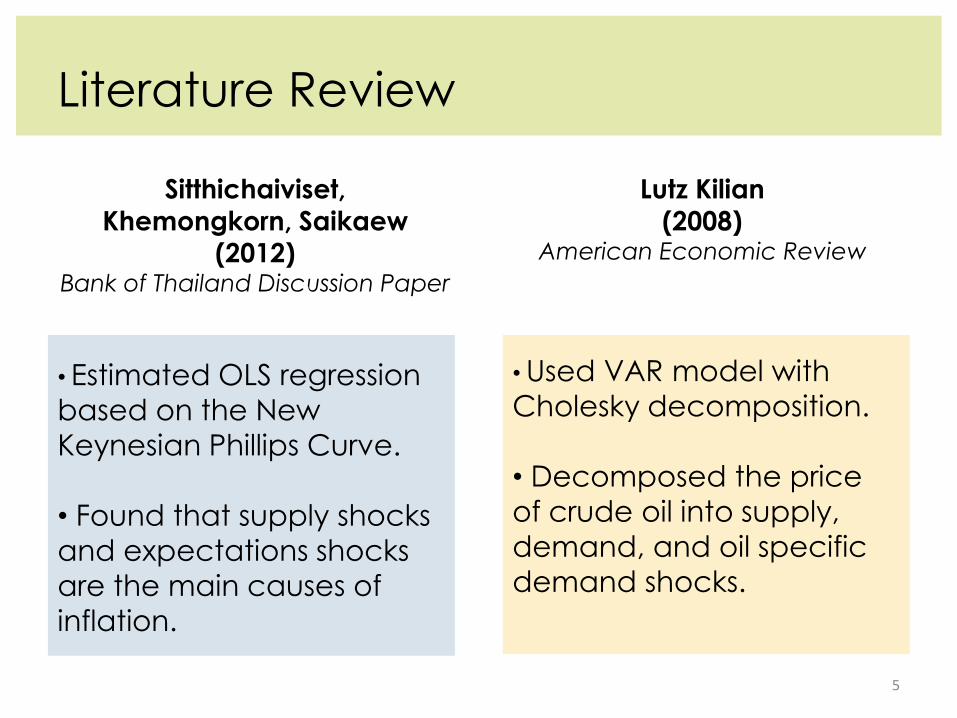

Literature Review

• Estimated OLS regression

based on the New

Keynesian Phillips Curve.

• Found that supply shocks

and expectations shocks

are the main causes of

inflation.

• Used VAR model with

Cholesky decomposition.

• Decomposed the price

of crude oil into supply,

demand, and oil specific

demand shocks.

Sitthichaiviset,

Khemongkorn, Saikaew (2012)

Bank of Thailand Discussion Paper

Lutz Kilian

(2008) American Economic Review

5

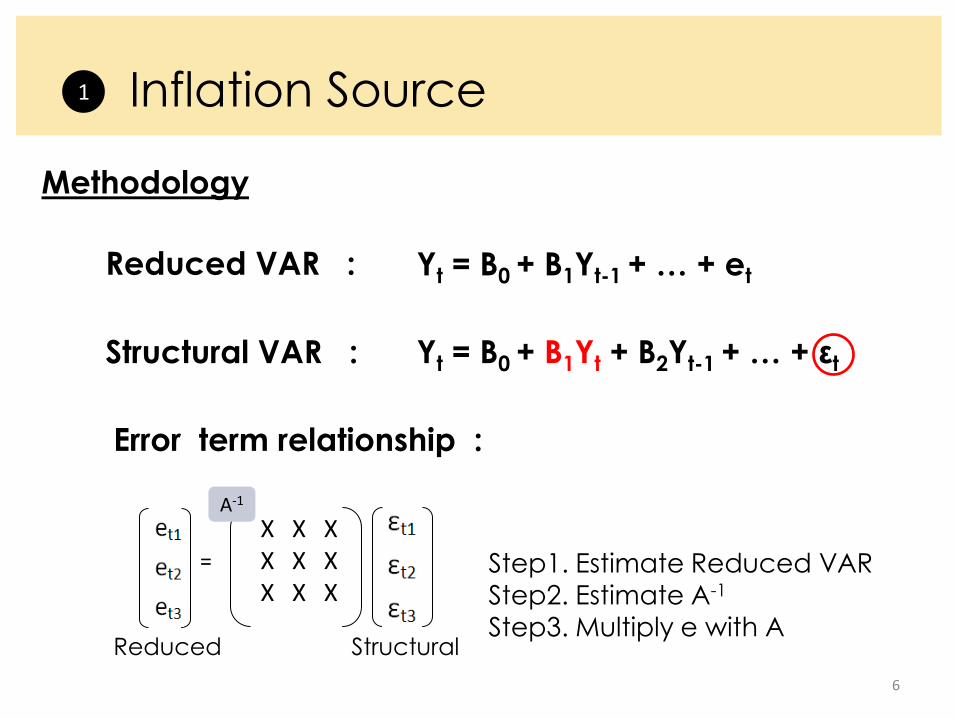

Yt = B0 + B1Yt + B2Yt-1 + … + εt

Inflation Source 1

6

Reduced VAR :

Step1. Estimate Reduced VAR Step2. Estimate A-1

Step3. Multiply e with A

Error term relationship :

=

X X X X X X X X X

Reduced Structural

A-1

Yt = B0 + B1Yt-1 + … + et

Structural VAR :

Methodology

7

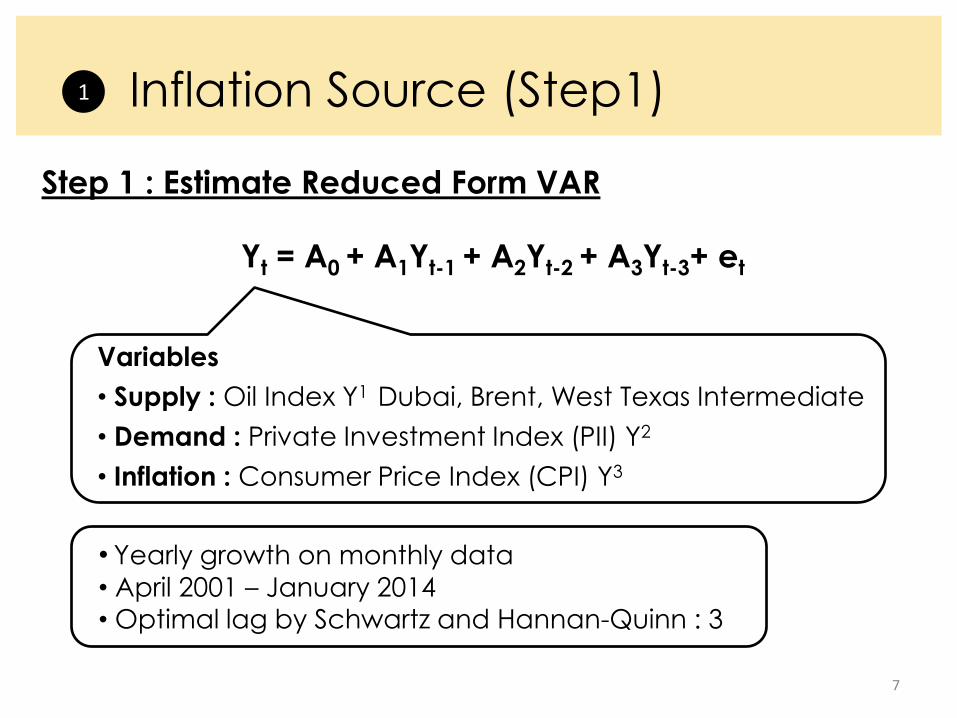

Inflation Source (Step1) 1

Variables

• Supply : Oil Index Y1 Dubai, Brent, West Texas Intermediate

• Demand : Private Investment Index (PII) Y2

• Inflation : Consumer Price Index (CPI) Y3

• Yearly growth on monthly data

• April 2001 – January 2014

• Optimal lag by Schwartz and Hannan-Quinn : 3

Yt = A0 + A1Yt-1 + A2Yt-2 + A3Yt-3+ et

Step 1 : Estimate Reduced Form VAR

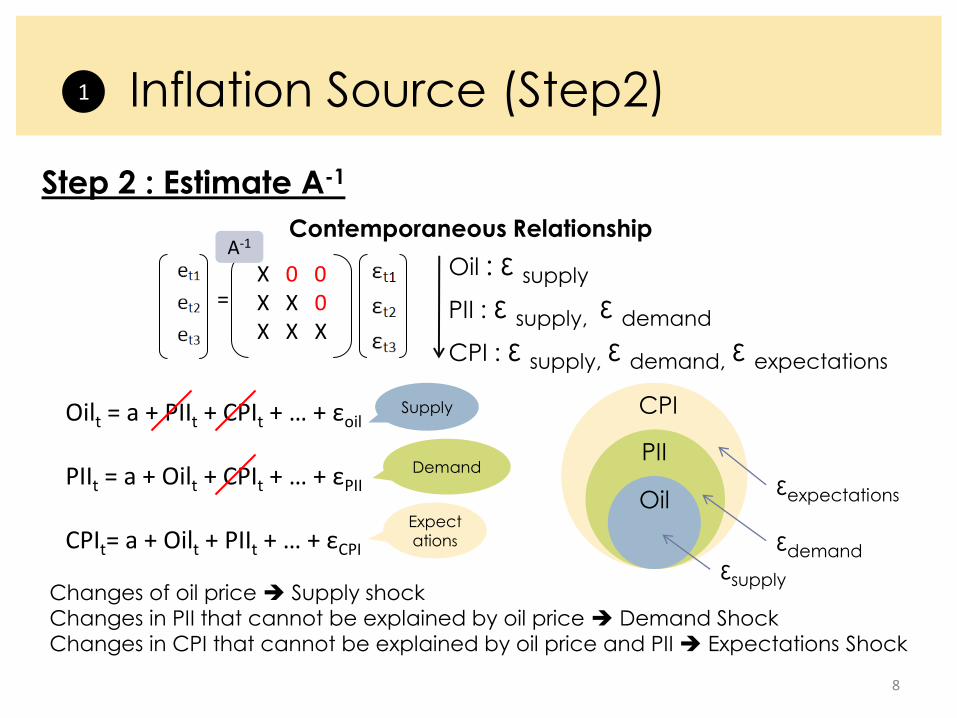

Re Inflation Source (Step2) 1

Step 2 : Estimate A-1

Changes of oil price Supply shock

Changes in PII that cannot be explained by oil price Demand Shock

Changes in CPI that cannot be explained by oil price and PII Expectations Shock

Supply

Demand

Expect

ations

Oil : ε supply PII : ε supply, ε demand CPI : ε supply, ε demand, ε expectations

8

= X 0 0 X X 0 X X X

A-1 Contemporaneous Relationship

Oilt = a + PIIt + CPIt + … + εoil

PIIt = a + Oilt + CPIt + … + εPII CPIt= a + Oilt + PIIt + … + εCPI

PII

CPI

εsupply εdemand

εexpectations Oil

9

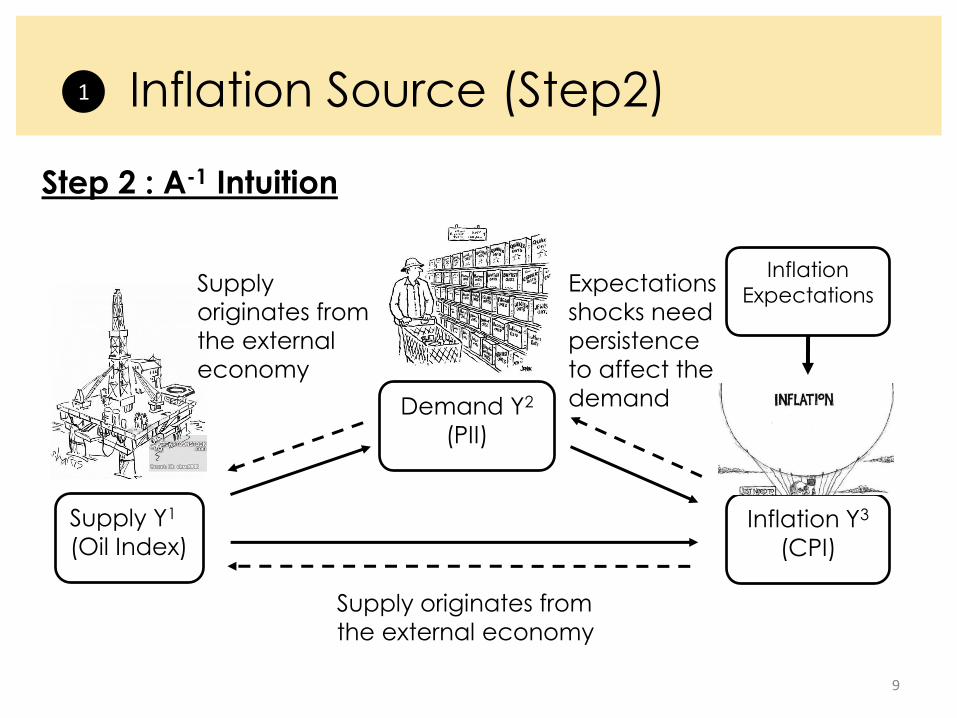

Inflation Source (Step2) 1

Step 2 : A-1 Intuition

Supply Y1

(Oil Index)

Demand Y2

(PII)

Inflation Y3

(CPI)

Expectations

shocks need

persistence

to affect the

demand

Supply

originates from

the external

economy

Supply originates from

the external economy

Inflation

Expectations

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

-1

-0.5

0

0.5

1

1.5

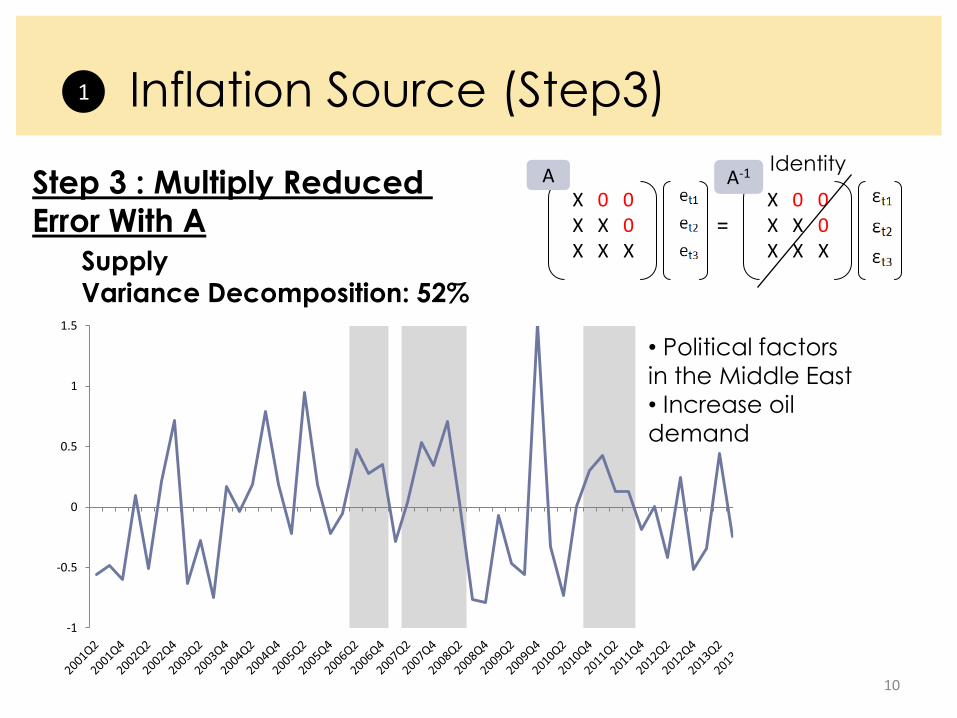

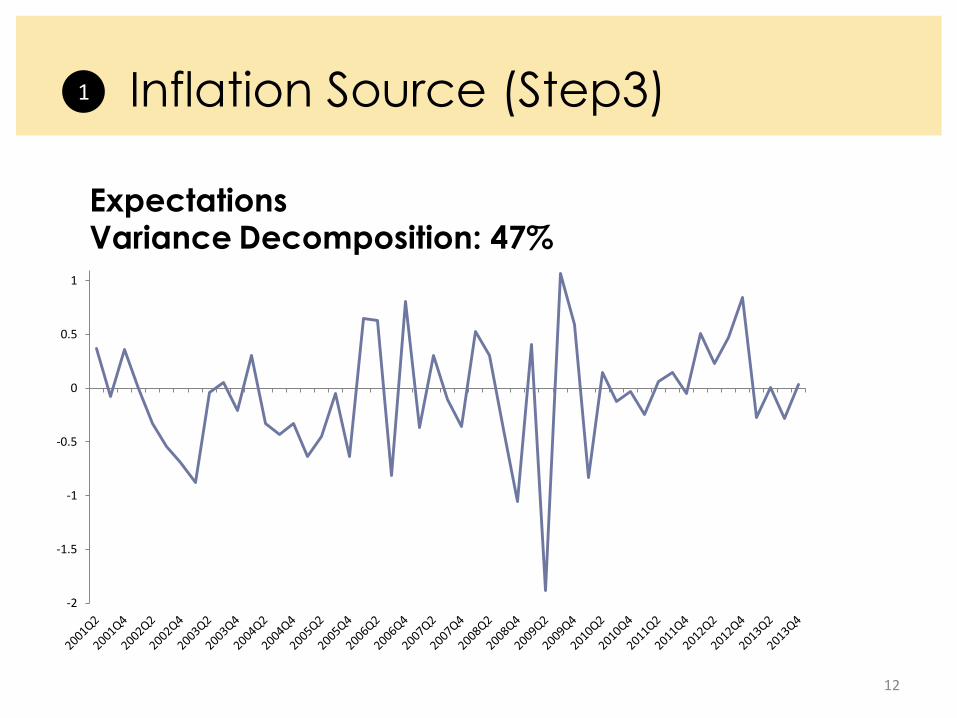

Inflation Source (Step3) 1

Step 3 : Multiply Reduced

Error With A

10

= X 0 0 X X 0 X X X

A X 0 0 X X 0 X X X

Identity A-1

Supply

Variance Decomposition: 52%

• Political factors

in the Middle East

• Increase oil

demand

0

0.2

0.4

0.6

0.8

1

1.2

-1.6

-1.1

-0.6

-0.1

0.4

0.9

1.4

1.9

11

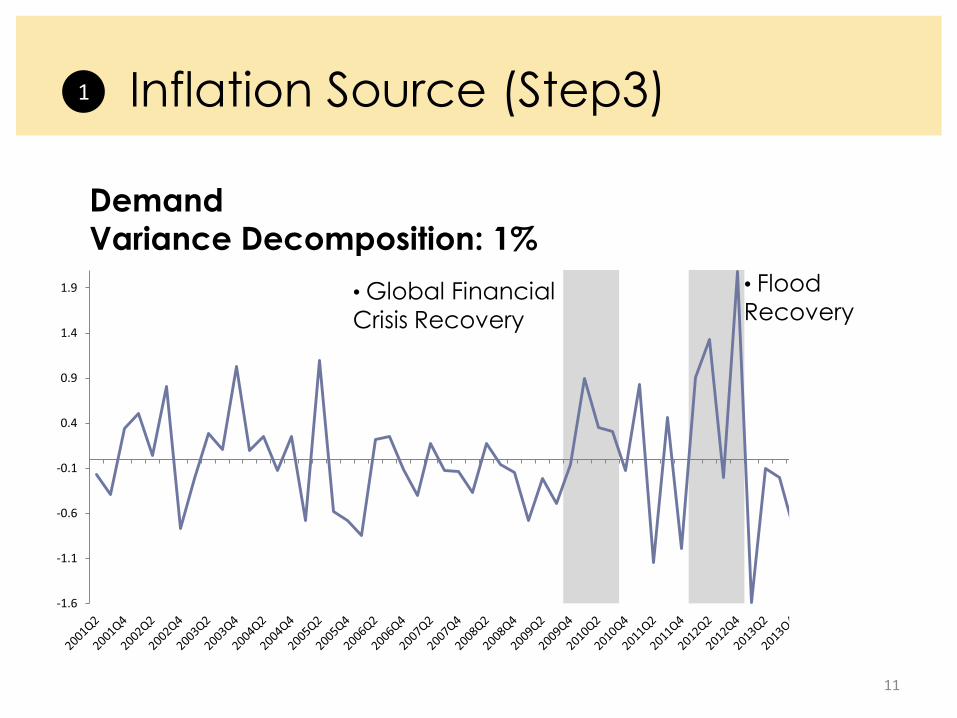

Inflation Source (Step3) 1

Demand

Variance Decomposition: 1%

• Global Financial

Crisis Recovery

• Flood

Recovery

12

Inflation Source (Step3) 1

Expectations Variance Decomposition: 47%

-2

-1.5

-1

-0.5

0

0.5

1

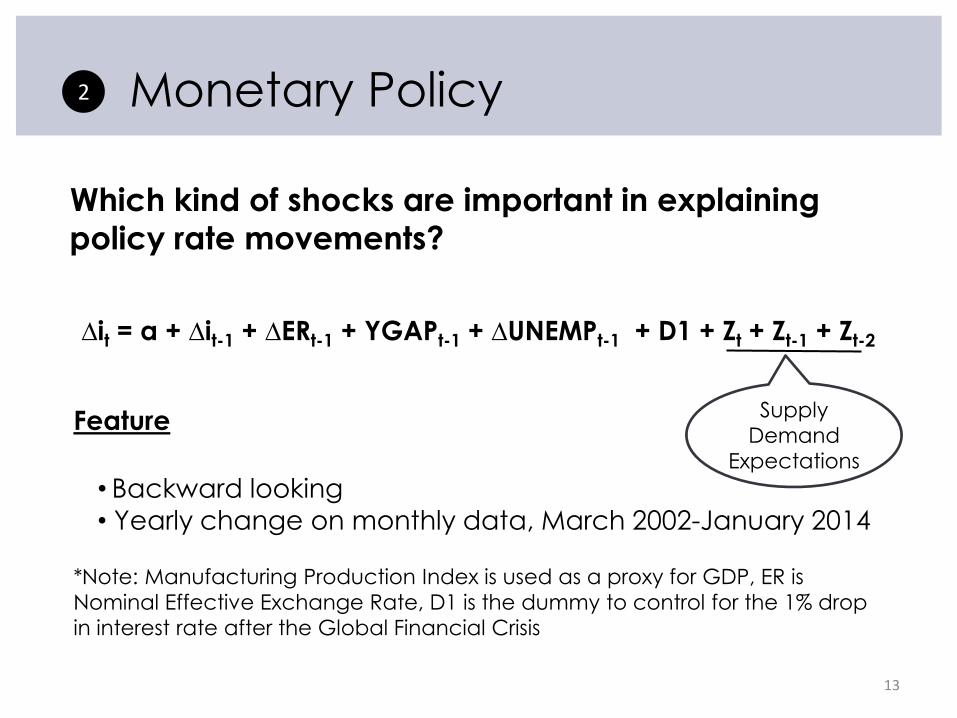

Monetary Policy

Which kind of shocks are important in explaining

policy rate movements?

2

∆it = α + ∆it-1 + ∆ERt-1 + YGAPt-1 + ∆UNEMPt-1 + D1 + Zt + Zt-1 + Zt-2

• Backward looking

• Yearly change on monthly data, March 2002-January 2014

Feature Supply

Demand

Expectations

*Note: Manufacturing Production Index is used as a proxy for GDP, ER is

Nominal Effective Exchange Rate, D1 is the dummy to control for the 1% drop

in interest rate after the Global Financial Crisis

13

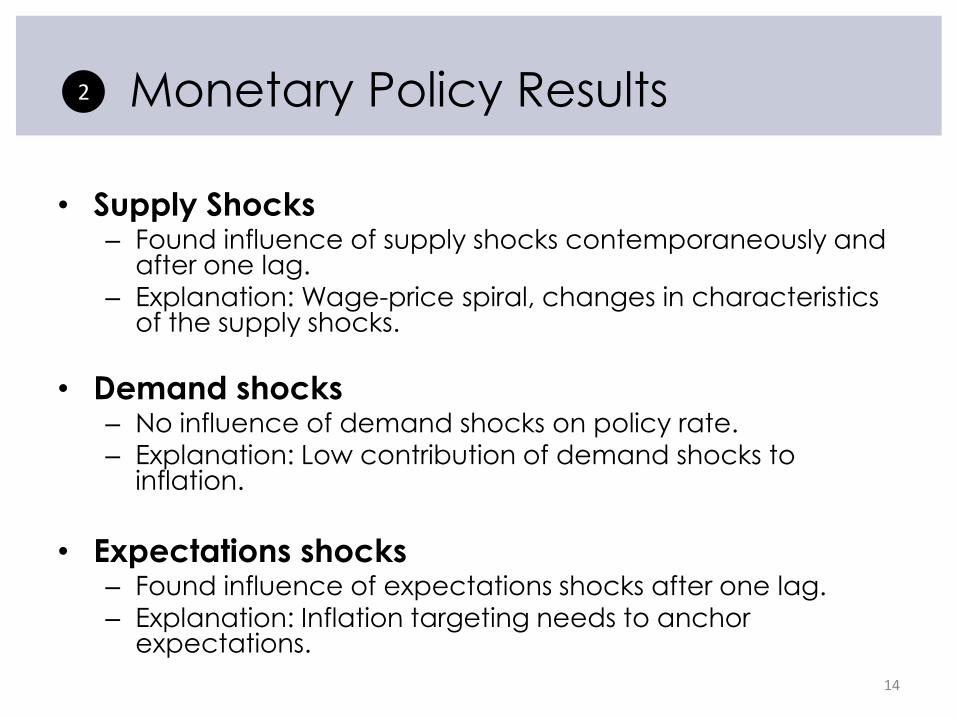

• Supply Shocks – Found influence of supply shocks contemporaneously and

after one lag.

– Explanation: Wage-price spiral, changes in characteristics of the supply shocks.

• Demand shocks – No influence of demand shocks on policy rate.

– Explanation: Low contribution of demand shocks to inflation.

• Expectations shocks – Found influence of expectations shocks after one lag.

– Explanation: Inflation targeting needs to anchor expectations.

Monetary Policy Results 2

14

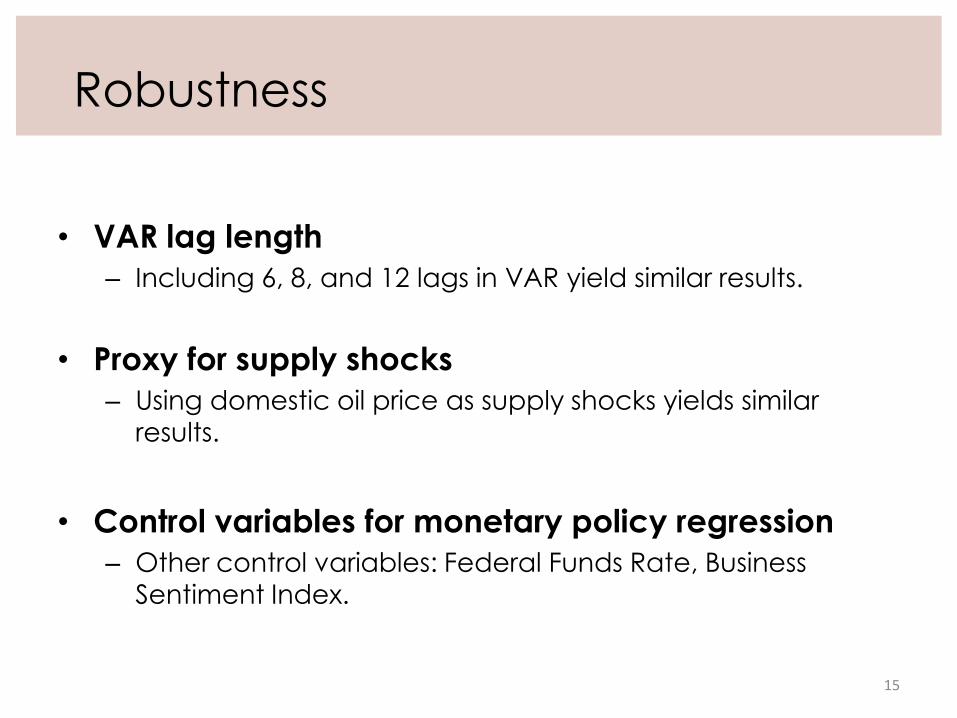

• VAR lag length

– Including 6, 8, and 12 lags in VAR yield similar results.

• Proxy for supply shocks

– Using domestic oil price as supply shocks yields similar

results.

• Control variables for monetary policy regression

– Other control variables: Federal Funds Rate, Business Sentiment Index.

Robustness

15

Conclusion

• Knowing the source of inflation is critical for inflation

targeting central banks, therefore, this paper aims

to decompose inflation source using a method that

does not put the variables under a construction.

• The main sources of inflation in Thailand are from

supply shocks and inflation expectations shocks.

• Practical policy setting may deviate from the

theories to achieve the optimal solution.

16

![3. DUMMY VARIABLES, NONLINEAR VARIABLES AND SPECIFICATIONminiahn/ecn725/cn3_dummy.pdf · 2006-03-07 · DUMMY VARIABLES, NONLINEAR VARIABLES AND SPECIFICATION [1] DUMMY VARIABLES](https://img.pdfslide.us/doc/110x75/5b90b6d509d3f21c788c95bb/3-dummy-variables-nonlinear-variables-and-miniahnecn725cn3dummypdf-2006-03-07.jpg)