Embed Size (px)

Citation preview

www.harriswilliams.com

Investment banking services are provided by Harris Williams LLC, a registered broker-dealer and member of FINRA and SIPC, and Harris Williams & Co. Ltd, which is a private limited company incorporated under English law with its registered office at 5th Floor, 6 St. Andrew Street, London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales (registration number 7078852). Harris Williams & Co. Ltd is authorized and regulated by the Financial Conduct Authority. Harris Williams & Co. is a trade name under which Harris Williams LLC and Harris Williams & Co. Ltd conduct business.

PACKAGING

INDUSTRY UPDATE │ AUGUST 2017

PAGE |

PACKAGING INDUSTRY UPDATE

1

CONTENTS

WHAT WE’RE READING

ECONOMIC UPDATE

KEY THEMES

PUBLIC COMPARABLES

PUBLIC MARKETS OVERVIEW

SELECT M&A ACTIVITY

CONTACTS

Patrick McNultyManaging [email protected]+1 (804) 887-6039

Brad [email protected]+1 (804) 915-0168

Brandt CarrVice [email protected]+1 (804) 887-6018

INTRODUCTION

Harris Williams & Co. is pleased to present our packaging industry update forAugust 2017. This report provides commentary and analysis on current capitalmarket trends and merger and acquisition dynamics within the global packagingindustry.

We hope you find this edition helpful and encourage you to contact us directly ifyou would like to discuss our perspective on current industry trends or our relevantindustry experience.

PACKAGING

INDUSTRY UPDATE │ AUGUST 2017

www.harriswilliams.com

OUR PRACTICE

Harris Williams & Co. is a leading advisor to the packaging industry. Our significantexperience covers a broad range of end markets, industries, and business models.

Bags

Bottles & Cans

Caps & Closures

Flexible

Labels

Pouches

Rigid

Films

Foil

Glass

Laminations

Metal

Paperboard

Plastics

Specialty Paper

Packaging Types Materials Applications

Cosmetics

E-Commerce

Food & Beverage

Healthcare

Industrial

Other

UPCOMING INDUSTRY EVENTS

Harris Williams & Co. will be attending the 2017 PACK EXPOconference on September 25-27th at the Las VegasConvention Center. We hope to see you in attendance.

PACK EXPO Las Vegas

PAGE |

STRONG MOMENTUM ACROSS THE PACKAGING INDUSTRY

2

INDUSTRY UPDATE │ AUGUST 2017

PACKAGING

Manufacturer of paper-based

protective packaging

solutions

has been acquired by

a portfolio company of

Global provider of guiding,

winding, slitting and tension

control systems for web fed

converting applications

has been acquired by

a portfolio company of

and

Manufacturer of flexible

paper-based packaging

solutions

has been acquired by

a portfolio company of

a portfolio company of

Manufacturer of coated and

vacuum metallized paper

products

a portfolio company of

has been acquired by

Provider of flexible packaging

solutions, injection-molded

fitments, and related filling

equipment

has been acquired by

a portfolio company of

Producer of die cut

merchandise bags and film

substrates

a portfolio company of

has been acquired by

Distributor of value-added

rigid packaging solutions

has been acquired by

a portfolio company of

Provider of injection-molded

temporary waste storage

solutions

a portfolio company of

has been acquired by

Provider of innovative

conveyor systems for

packaging-related

applications

a portfolio company of

has been acquired by

PAGE |

WHAT WE’RE READING

INDUSTRY UPDATE │ AUGUST 2017

PACKAGING

3

THE CARBON FOOTPRINT’S TRIUMPHANT RETURN

Packaging Digest 7/24/2017

In April, Walmart announced packaging as one of six primary activity areas for Project Gigaton, its commitment toreduce one gigaton of greenhouse gas emissions by 2030. This summer, Walmart is putting the plan into action, givingsuppliers a concrete directive for lowering the greenhouse gas emissions associated with packaging and asking themto report their progress. Carbon footprints are back on the forefront.

Read the full article here.

SHARING EXPERIENCES: PROMOTIONAL PACKAGING CAMPAIGNS ARE PROVING TO BE SUCCESSFUL

Packaging Gateway 7/10/2017

Using packaging to involve and engage consumers has been a growing trend in the beverage industry as emergingtechnology expands the scope of what is possible. As smart and digitally enriched packaging becomes more widelyadopted, some brands have begun to experiment with innovative ways to use the technology, by employingpackaging as a vehicle for consumer engagement in promotional campaigns.

Read the full article here.

U.S. PAPER RECOVERY RATE REACHES ALL-TIME HIGH

Packaging World 7/12/2017

The American Forest & Paper Association has announced that a record 67.2% of paper consumed in the U.S. wasrecovered for recycling in 2016, up from 66.8% in 2015. The paper recovery rate measured 33.5% back in 1990, whichwas the base year against which the American Forest & Paper Association began setting its recovery goals.

Read the full article here.

STANDING OUT ON THEIR OWN | CATEGORY FOCUS – OWN LABEL

Packaging News 7/5/2017

Own label packaging has changed significantly in recent years, housing better quality products. From high end tobudget supermarkets, impressive, stylishly packaged own label products are successfully competing with the bigbrands, giving consumers greater choice with packs emphasizing quality.

Read the full article here.

A HOLISTIC APPROACH TO MODERN MAINTENANCE

Packaging World 8/1/2017

With the marketplace growing ever more competitive, and ever-changing consumer demand for greater flexibility,beverage producers are pushing the limits of their production equipment to their very maximum. Which maintenanceapproach can best answer those challenges?

Read the full article here.

PAGE |

0

50

100

150

200

250

300

05 07 09 11 13 15 17

WTI Brent Nat Gas

Aug-17:

20.5

(6%)

(4%)

(2%)

0%

2%

4%

05 06 07 08 09 10 11 12 13 14 15 16 17

U.S. EU-28

70

80

90

100

110

120

05 06 07 08 09 10 11 12 13 14 15 16 17

U.S. EU-28

50

60

70

80

90

100

05 06 07 08 09 10 12 13 14 15 16 17

ECONOMIC UPDATE

4

GDP (2,3)

INDUSTRIAL PRODUCTION INDEX (3,4)

CONSUMER SENTIMENT (5)

U.S.

For the second quarter of 2017 as a whole, industrial productionadvanced at an annual rate of 4.7%, primarily as a result of strongincreases for mining and utilities. Capacity utilization for the industrialsector increased 0.2% in June 2017 to 76.6%, a rate that is 3.3% belowits long-run (1972–2016) average.

EU-28

In June 2017 compared with May 2017, seasonally adjusted industrialproduction fell by 0.5% in the EU-28 due to lower production of capitaland consumer goods.

Consumer sentiment for the United States declined slightly to 93.4 inJuly 2017 from 95.1 the previous month, primarily due to consumersexpressing less optimism about future prospects for the overalleconomy.

The size of the decline was tempered by record favorable views ofcurrent economic conditions, which rose to the highest level sinceJuly 2005, mainly due to improvements in consumers' personalfinances.

PACKAGING

INDUSTRY UPDATE │ AUGUST 2017

ENERGY PRICES (1)

Aug-17:

90.7

Aug-17:

82.5

Crude oil prices increased in response to supply-side factors as well asstrong U.S. refinery demand, further supported as Saudi Arabiaannounced a cap on the country's crude oil exports in August.

Higher natural gas exports and growing domestic natural gasconsumption are forecast to contribute to increasing natural gasprices.

U.S.

Real gross domestic product (GDP) increased 1.2% from the firstquarter of 2017 to the second quarter of 2017.

The increase in real GDP in the second quarter reflected positivecontributions from personal consumption expenditures, nonresidentialfixed investment, exports, and federal government spending.

EU-28

Seasonally adjusted GDP in the EU-28 rose by 0.6% in the secondquarter, with 2.1% year-over-year growth.

July-17:

93.4

Q2-17:

0.6%

Q2-17:

1.2%

June-17:

105.2

June-17:

108.3

Energy Prices

(Indexed)

Consumer Sentiment Index

Industrial Production Index

GDP

(Quarter-Over-Quarter Growth)

PAGE |

KEY THEMES

5

CONSUMER LIFESTYLE TRENDS AMONG FACTORS DRIVING FLEXIBLE PACKAGING GROWTH (8)

PACKAGING

INDUSTRY UPDATE │ AUGUST 2017

M&A ACTIVITY IN THE PACKAGING INDUSTRY (6)

Strong M&A activity in the packaging space continued throughthe second quarter of 2017.

– As of the end of Q2 2017, 172 deals have been announcedglobally vs. 154 for the prior year LTM period.

– On an LTM basis as of the end of Q2 2017, $26.7 billion of dealvalue has been announced globally vs. $10.1 billion for the prioryear LTM period.

Packaging industry M&A remains robust globally, with the majority

of 2017 targets located in Western Europe (44%), North America

(33%), and the Asia Pacific region (14%).

More than seven deals over $1 billion have been announced orclosed in 2017.

Global Packaging M&A Volume

(announced deals, LTM)

Shifts in consumer lifestyles and the resulting demand forconvenience products are contributing to continued growth in the

use of flexible packaging, replacing traditional formats such asglass jars and metal cans and driving expected 4.1% annual

growth in global consumer flexible packaging from 2017 to 2022.

Flexible packaging offers several advantages compared to rigidpack formats, including extended shelf life, improved cost

economics, lower pack weight, and freight cost savings.

Pouches, particularly stand-up pouches, are the fastest-growing

product category in the flexible packaging market.

– Pouch equipment manufacturers are delivering machinerycapable of faster production speeds, greater versatility and

improved sealing techniques, which improves the competitiveposition of pouches versus alternative pack formats.

Global Consumer Flexible

Packaging Consumption (million tons)

154172

June 2016 June 2017

HOW E-COMMERCE IS CHANGING THE PACKAGING LANDSCAPE (7)

E-commerce currently accounts for ~$1.5 trillion, or ~7.4%, of the~$22 trillion global retail market; this share is expected to nearly

double by 2020, with more people gaining access to the internet,driving significant change within the packaging industry during this

period.

Packages designed specifically for e-commerce must be durableenough to withstand the often complex supply chains involved in

delivering a product to consumers; this, in turn, is expected to drivestrong demand for protective packaging.

Also, with packaging playing a much bigger part in the e-commerce customer experience, there is greater expectation forthe secondary packaging to deliver brand values as well as

keeping the product safe and secure.

$1.5

$4.1

7.4%

14.6%

2015 2020

Retail E-Commerce Sales

% of Total Retail Sales

Global E-Commerce Retail Sales

($ in trillions)

4.1% CAGR

27.4

33.5

2017 2022

11.7%

Increase

PAGE |

PUBLIC COMPARABLES (6)

6

As of August 9, 2017 ($ in millions, except per share amounts)

PACKAGING

INDUSTRY UPDATE │ AUGUST 2017

Notes: LTM as of most recent reporting; free cash flow conversion defined as EBITDA less capital expenditures divided by EBITDA.

3-Year Free Cash

Current % of Revenue FY 2017E Price / Earnings TEV / EBITDA Flow Net Debt /

Price LTM High Mkt Cap TEV CAGR Revenue EBITDA Margin FY 2017E FY 2018P LTM FY 2017E FY 2018P Conversion EBITDA

Diversified / Specialty

Amcor $12.13 95.1% $14,044 $18,530 (1.6%) $9,507 $1,456 15.3% 20.6x 18.1x 14.0x 12.7x 11.7x 70.5% 3.2x

Berry Global 57.11 96.9% 7,447 13,329 12.8% 7,121 1,335 18.7% 18.9x 16.8x 11.9x 10.0x 9.2x 77.8% 5.0x

Sealed Air Corporation 44.74 88.4% 8,761 12,904 (18.2%) 4,343 830 19.1% 24.5x 18.1x 11.5x 15.5x 14.5x 75.6% 3.7x

Sonoco Products Company 48.53 87.3% 4,824 6,012 (0.5%) 4,936 658 13.3% 17.6x 16.1x 10.0x 9.1x 8.6x 67.6% 1.8x

Aptargroup 82.37 90.7% 5,167 5,784 (2.7%) 2,390 468 19.6% 24.7x 22.6x 12.5x 12.4x 11.5x 70.0% 1.0x

Bemis Company 41.98 79.1% 3,812 5,354 (2.6%) 4,008 551 13.8% 17.6x 15.6x 9.6x 9.7x 8.9x 59.2% 2.7x

Huhtamaki Oyj 38.37 80.6% 4,135 4,916 6.3% 3,561 480 13.5% 17.2x 15.3x 11.8x 10.2x 9.5x 37.4% 2.1x

Greif 55.84 88.6% 2,761 4,325 (6.0%) 3,522 465 13.2% 19.4x 17.0x 9.7x 9.3x 8.7x 76.6% 2.2x

Winpak 41.97 90.6% 2,728 2,498 4.6% 899 203 22.6% 24.5x 22.7x 12.7x 12.3x 11.4x 62.6% (1.3x)

Median 88.6% $4,824 $5,784 (1.6%) $4,008 $551 15.3% 19.4x 17.0x 11.8x 10.2x 9.5x 70.0% 2.2x

Mean 88.6% $5,964 $8,184 (0.9%) $4,476 $716 16.6% 20.6x 18.0x 11.5x 11.3x 10.5x 66.4% 2.3x

Labels

Avery Dennison Corporation $92.83 96.0% $8,205 $9,829 1.0% $6,530 $851 13.0% 19.2x 17.4x 11.7x 11.6x 10.8x 73.8% 1.8x

CCL Industries 44.87 84.6% 7,944 9,659 17.6% 3,806 766 20.1% 22.0x 19.1x 16.4x 12.6x 11.4x 64.4% 2.8x

Multi-Color Corporation 77.65 88.0% 1,318 1,816 6.1% 969 172 17.8% 19.6x 17.8x 11.3x 10.6x 9.9x 71.3% 3.0x

Median 88.0% $7,944 $9,659 6.1% $3,806 $766 17.8% 19.6x 17.8x 11.7x 11.6x 10.8x 71.3% 2.8x

Mean 89.5% $5,822 $7,101 8.2% $3,768 $596 17.0% 20.3x 18.1x 13.1x 11.6x 10.7x 69.8% 2.5x

Paper and Paperboard

International Paper Company $53.36 90.5% $22,033 $32,381 (0.8%) $23,080 $3,867 16.8% 15.3x 12.3x 10.2x 8.4x 7.3x 56.5% 3.2x

WestRock 56.08 92.9% 14,082 20,649 14.6% 14,905 2,339 15.7% 20.9x 15.3x 11.7x 8.8x 7.3x 57.8% 3.6x

Mondi 25.77 95.0% 9,465 14,517 (0.3%) 8,415 1,725 20.5% 14.2x 13.6x 8.0x 8.4x 8.1x 65.8% 0.9x

Packaging Corporation of America 109.17 95.5% 10,300 12,527 2.7% 6,348 1,327 20.9% 18.2x 16.4x 10.2x 9.4x 9.0x 75.4% 1.9x

Smurfit Kappa Group 28.28 90.5% 6,698 10,266 (2.2%) 10,035 1,475 14.7% 11.8x 10.5x 7.8x 7.0x 6.6x 63.0% 2.6x

DS Smith 6.42 97.8% 6,518 7,570 4.0% 6,858 871 12.7% 15.0x 14.0x 10.2x 8.7x 8.0x 57.7% 2.0x

Graphic Packaging Holding Company 13.19 89.7% 4,086 6,304 1.0% 4,374 724 16.5% 19.5x 15.3x 9.1x 8.7x 7.9x 65.7% 3.2x

KapStone Paper and Packaging Corporation 22.21 88.9% 2,153 3,769 12.4% 3,264 422 12.9% 17.5x 13.7x 10.9x 8.9x 7.8x 62.5% 4.6x

P. H. Glatfelter Company 17.14 67.0% 747 1,122 (4.5%) 1,576 164 10.4% 15.0x 11.4x 13.0x 6.9x 6.2x (74.5%) 4.3x

Median 90.5% $6,698 $10,266 1.0% $6,858 $1,327 15.7% 15.3x 13.7x 10.2x 8.7x 7.8x 62.5% 3.2x

Mean 89.8% $8,454 $12,123 3.0% $8,762 $1,435 15.7% 16.4x 13.6x 10.1x 8.4x 7.6x 47.8% 2.9x

Rigid

Ball Corporation $40.20 93.4% $14,075 $21,546 8.1% $10,836 $1,753 16.2% 19.9x 16.8x 16.7x 12.3x 11.2x 54.0% 5.5x

Owens-Illinois 23.82 95.2% 3,880 9,431 0.3% 6,845 1,329 19.4% 9.1x 8.5x 8.4x 7.1x 6.8x 61.3% 4.8x

Silgan Holdings 30.56 94.0% 3,370 6,349 1.3% 4,068 566 13.9% 18.4x 16.0x 13.7x 11.2x 10.1x 63.6% 6.4x

RPC Group 11.31 87.5% 4,681 5,414 33.7% 4,699 770 16.4% 12.6x 11.6x 10.7x 7.0x 6.6x 53.5% 2.7x

Median 93.7% $4,281 $7,890 4.7% $5,772 $1,049 16.3% 15.5x 13.8x 12.2x 9.2x 8.5x 57.6% 5.2x

Mean 92.5% $6,502 $10,685 10.8% $6,612 $1,105 16.5% 15.0x 13.2x 12.4x 9.4x 8.7x 58.1% 4.9x

Overall Median 90.5% $4,995 $6,959 1.2% $4,537 $768 16.3% 18.3x 15.8x 11.1x 9.4x 8.8x 63.3% 2.9x

Overall Mean 89.5% $6,876 $9,874 3.6% $6,265 $1,030 16.4% 18.1x 15.6x 11.3x 9.9x 9.1x 58.1% 3.0x

PAGE |

PUBLIC MARKETS OVERVIEW (6)

7

NET DEBT / LTM EBITDA

3-YEAR EBITDA CAGR (2014 – 2017E)

AVERAGE EBITDA MARGIN (2017E) FREE CASH FLOW CONVERSION (2017E)

TOTAL ENTERPRISE VALUE / 2017E EBITDA

3-YEAR REVENUE CAGR (2014 – 2017E)

PACKAGING

INDUSTRY UPDATE │ AUGUST 2017

PUBLIC COMPARABLES (30-DAY ROLLING AVERAGE OF MEDIAN TEV / LTM EBITDA)

(0.9%)

8.2%

3.0%

10.8%

Diversified / Specialty

Labels

Paper and Paperboard

Rigid

5.2%

13.0%

3.0%

17.6%

Diversified / Specialty

Labels

Paper and Paperboard

Rigid

16.6%

17.0%

15.7%

16.5%

Diversified / Specialty

Labels

Paper and Paperboard

Rigid

66.4%

69.8%

47.8%

58.1%

Diversified / Specialty

Labels

Paper and Paperboard

Rigid

11.3x

11.6x

8.4x

9.4x

Diversified / Specialty

Labels

Paper and Paperboard

Rigid

2.3x

2.5x

2.9x

4.9x

Diversified / Specialty

Labels

Paper and Paperboard

Rigid

Median

Current 3-Year 5-Year

Diversified / Specialty 11.8x 10.6x 9.7x

Labels 11.7x 10.6x 9.3x

Paper and Paperboard 10.2x 8.6x 8.1x

Rigid 12.2x 10.4x 9.7x

Total Packaging 11.1x 9.9x 9.0x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

Feb-12 Aug-12 Feb-13 Aug-13 Feb-14 Aug-14 Feb-15 Aug-15 Feb-16 Aug-16 Feb-17 Aug-17

Paper and Paperboard Diversified / Specialty Rigid Labels

PAGE |

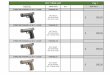

Date Target Target Business Description Acquirer

Pending Constantia Labels

GmbH

Constantia produces plastic labels for leading drinks manufacturers. Multi-Color Corp.

Pending Hanna Group Pty

Ltd.

Hanna manufactures folding carton beverage, food, confectionary, and

healthcare sectors.

WestRock Co.

Pending Salbro Bottle, Inc. Salbro manufactures and distributes plastic and glass bottles and lids. AEA /

TricorBraun, Inc.

Jul-17 Boxmore

Packaging (Pty)

Ltd.

Boxmore provides plastic packaging products such as bottles, plastic containers,

jars, closures, and lids.

ALPLA Werke

Alwin Lehner

GmbH & Co. KG

Jun-17 Clear Lam

Packaging

Clear Lam develops and manufactures flexible and rigid packaging materials

primarily for consumer packaged goods companies.

Sonoco Products

Jun-17 Combined

Container

Industries LLC

Combined Container produces corrugated boxes, sheets, and point-of-purchase

displays.

WestRock Co.

Jun-17 Duravant Duravant designs and manufactures engineered equipment for the food

processing, packaging, and material handling industries.

Warburg Pincus

Jun-17 Faerch Plast Faerch Plast produces rigid plastic packaging for ready meals and protein food

trays.

Advent

International

May-17 Transcendia Transcendia is a manufacturer of custom engineered films for critical product

components across a variety of end markets.

Goldman Sachs

May-17 Charter NEX Charter NEX Films produces specialty films used in flexible packaging and other

critical performance applications.

Leonard Green &

Partners

Apr-17 Consolidated

Container Co.

Consolidated Container develops and manufactures rigid plastic packaging

products, specializing in customized mid-run and short-run packaging solutions.

Loews

Corporation

Apr-17 Trinity Packaging

Corp.

Trinity Packaging manufactures plastic carry-out bags and related products. The Pritzker

Group /

ProAmpac

Feb-17 Excelsior

Technologies

Excelsior Technologies produces flexible packaging solutions, mainly for food

applications, with a packaging technology for microwave steam cooking.

Mondi

Feb-17 Peninsula Peninsula Packaging manufactures containers and other packaging products for

food storage.

Sonoco

Feb-17 Letica Corp. Letica Corp. manufactures paper and plastic packaging products including

buckets, pails, food containers, and lids.

RPC Group

Feb-17 Mauser Group NV Mauser Group manufactures steel and fiber packaging drums and related industrial

packaging products and machineries.

Stone Canyon

Jan-17 Multi Packaging

Solutions

International

Multi Packaging Solutions International specializes in packaging solutions for the

branded and healthcare markets.

WestRock

Jan-17 Westrock Co -

Dispensing

Business

Supplies triggers, pumps, sprayers and dispensing closure solutions. Silgan Holdings

SELECT M&A ACTIVITY (6,9)

8

PACKAGING

INDUSTRY UPDATE │ AUGUST 2017

Energy, Power & Infrastructure

IndustrialsHealthcare & Life Sciences

Transportation & Logistics

Aerospace, Defense & Government

Services

Business Services

Building Products & Materials

Technology, Media & Telecom

Specialty Distribution

Consumer

PAGE |

HARRIS WILLIAMS & CO. OFFICE LOCATIONS

UNITED STATES EUROPE

NETWORK OFFICES

Beijing

Hong Kong

Mumbai

New Delhi

Shanghai

Richmond (Headquarters)1001 Haxall Point9th FloorRichmond, Virginia 23219Phone: +1 (804) 648-0072

San Francisco575 Market Street31st FloorSan Francisco, California 94105Phone: +1 (415) 288-4260

Washington, D.C. 800 17th St. NW2nd FloorWashington, D.C. 20006Phone: +1 202-207-2300

BostonOne International Place Suite 2620Boston, Massachusetts 02110Phone: +1 (617) 482-7501

Cleveland1900 East 9th Street20th FloorCleveland, Ohio 44114Phone: +1 (216) 689-2400

Minneapolis222 South 9th StreetSuite 3350Minneapolis, Minnesota 55402Phone: +1 (612) 359-2700

FrankfurtBockenheimer Landstrasse 33-3560325 FrankfurtGermanyPhone: +49 069 3650638 00

London63 Brook StreetLondon W1K 4HS, EnglandPhone: +44 (0) 20 7518 8900

Industrials

9

PACKAGING

INDUSTRY UPDATE │ AUGUST 2017

Harris Williams & Co. has a broad range of industry expertise, which creates powerful opportunities.Our clients benefit from our deep-sector experience, integrated industry intelligence andcollaboration across the firm, and our commitment to learning what makes them unique. For moreinformation, visit our website at www.harriswilliams.com/industries.

OUR FIRM

PAGE |

HARRIS WILLIAMS & CO.

10

PACKAGING

1. US Energy Information Administration

2. Bureau of Economic Analysis

3. Eurostat

4. Federal Reserve Economic Data

5. University of Michigan

6. Factset

7. Packaging World

8. Packaging Strategies

9. Mergermarket

Harris Williams & Co. (www.harriswilliams.com) is a preeminent middle market investment bank focused on the advisory needs of clients worldwide. The firm has deep industry knowledge, global transaction expertise, and an unwavering commitment to excellence. Harris Williams & Co. provides sell-side and acquisition advisory, restructuring advisory, board advisory, private placements, and capital markets advisory services.

Investment banking services are provided by Harris Williams LLC, a registered broker-dealer and member of FINRA and SIPC, and Harris Williams & Co. Ltd, which is a private limited company incorporated under English law with its registered office at 5th Floor, 6 St. Andrew Street, London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales (registration number 7078852). Harris Williams & Co. Ltd is authorized and regulated by the Financial Conduct Authority. Harris Williams & Co. is a trade name under which Harris Williams LLC and Harris Williams & Co. Ltd conduct business.

THIS REPORT MAY CONTAIN REFERENCES TO REGISTERED TRADEMARKS, SERVICE MARKS AND COPYRIGHTS OWNED BY THIRD-PARTY INFORMATION PROVIDERS. NONE OF THE THIRD-PARTY INFORMATION PROVIDERS IS ENDORSING THE OFFERING OF, AND SHALL NOT IN ANY WAY BE DEEMED AN ISSUER OR UNDERWRITER OF, THE SECURITIES, FINANCIAL INSTRUMENTS OR OTHER INVESTMENTS DISCUSSED IN THIS REPORT, AND SHALL NOT HAVE ANY LIABILITY OR RESPONSIBILITY FOR ANY STATEMENTS MADE IN THE REPORT OR FOR ANY FINANCIAL STATEMENTS, FINANCIAL PROJECTIONS OR OTHER FINANCIAL INFORMATION CONTAINED OR ATTACHED AS AN EXHIBIT TO THE REPORT. FOR MORE INFORMATION ABOUT THE MATERIALS PROVIDED BY SUCH THIRD PARTIES, PLEASE CONTACT US AT THE ABOVE ADDRESSES OR NUMBERS.

The information and views contained in this report were prepared by Harris Williams & Co. (“Harris Williams”). It is not a research report, as such term is defined by applicable law and regulations, and is provided for informational purposes only. It is not to be construed as an offer to buy or sell or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. The information contained herein is believed by Harris Williams to be reliable, but Harris Williams makes no representation as to the accuracy or completeness of such information. Harris Williams and/or its affiliates may be market makers or specialists in, act as advisers or lenders to, have positions in and effect transactions in securities of companies mentioned herein and also may provide, may have provided, or may seek to provide investment banking services for those companies. In addition, Harris Williams and/or its affiliates or their respective officers, directors and employees may hold long or short positions in the securities, options thereon or other related financial products of companies discussed herein. Opinions, estimates and projections in this report constitute Harris Williams’ judgment and are subject to change without notice. The financial instruments discussed in this report may not be suitable for all investors, and investors must make their own investment decisions using their own independent advisors as they believe necessary and based upon their specific financial situations and investment objectives. Also, past performance is not necessarily indicative of future results. No part of this material may be copied or duplicated in any form or by any means, or redistributed, without Harris Williams’ prior written consent.

Copyright© 2017 Harris Williams & Co., all rights reserved.

DISCLOSURES

SOURCES

INDUSTRY UPDATE │ AUGUST 2017