Embed Size (px)

Citation preview

INDUSTRY CHANGE THROUGHVERTICAL DISINTEGRATION:

HOW AND WHY MARKETS EMERGEDIN MORTGAGE BANKING

MICHAEL G. JACOBIDESLondon Business School

This paper provides an inductive theoretical framework that explains how and whyvertical disintegration happens, showing that transaction costs are an incidentalfeature of industry evolution. I find that gains from intrafirm specialization set off aprocess of intraorganizational partitioning, which simplifies coordination along partsof the value chain. Likewise, latent gains from trade foster interfirm cospecialization,which leads to information standardization. Given standardized information andsimplified coordination, new intermediate markets emerge, breaking up the valuechain, allowing new types of vertically specialized firms to participate in an industry,and changing the industry’s competitive landscape.

Industry evolution has long been a central con-cern to management scholars and managers alike.Scholars have studied such facets as the life cycleof an industry’s product and process technology(Abernathy & Utterback, 1978; Klepper, 1997),changes in technology and their impacts on firms’success (Henderson & Clark, 1990; Tushman &Anderson, 1987), and adaptation to changing de-mands (Burgelman, 1991; Winter, 1984). Yet oneaspect of industry evolution that has been rela-tively neglected by management scholars, despiteits great importance, is vertical disintegration: theemergence of new intermediate markets that dividea previously integrated production process be-tween two sets of specialized firms in the sameindustry.

What is particularly interesting about verticaldisintegration is that it often happens even whenthe underlying products, services, and core tech-nologies remain the same. Thus, while it may be arelatively invisible part of industry evolution, itcan radically transform the sectors in which it oc-curs. The automobile sector, once the textbookexample of integration, has been on a steady trajec-tory of vertical disintegration, with automotivecompanies giving up parts of the value chain1 tonew specialists and new intermediate marketsemerging (Fine, 1998; Fine & Whitney, 1996).Similar trends are evident in semiconductor man-ufacturing, with the emergence of “fab-less” (non-manufacturing) chip design companies and the cor-

The paper (and the author) benefited greatly from theadvice of a late friend, colleague, and mentor, SumantraGhoshal: He is sorely missed. Also, I would like to thankSid Winter for his extensive feedback; Freek Vermeulenfor constructive suggestions; Mark Zbaracki, Nick Ar-gyres, Carliss Baldwin, Yiorgos Mylonadis, Julian Birkin-shaw, Phanish Puranam, Costas Markides, Peter Moran,Nikolaos Pisanias, Ranjay Gulati, and Madan Pillutla foruseful remarks; and Peter van Overstraeten for editorialassistance. I would also like to thank the AMJ editor, TomLee, and three anonymous AMJ reviewers for the thor-ough and insightful comments and guidance that helpedshape the paper. Doug Duncan provided invaluable sup-port in the industry of interest. Generous funding fromthe Mortgage Bankers Association of America, the Centerfor the Network Economy, and the Leverhulme TrustDigital Transformations Programme at the London Busi-ness School is gratefully acknowledged. The usual dis-claimers apply.

1 A value chain, as defined in this paper, consists ofthe set of value-adding activities that need to be under-taken for a product to be made or a service rendered. Theconcept of the value chain was originally used to denotethe set of activities that take place within the boundariesof any given firm or business unit, including inboundlogistics, production, outbound logistics, marketing, andservice and support functions (see Porter, 1985); itsmeaning has, however, been enlarged and altered re-cently. My definition is consistent with the general use(e.g., Evans & Wurster, 1999; Grant, 2004: Ch. 13) of theterm to mean the structured set of activities that takeplace in an industry, regardless of whether they takeplace within the boundaries of one integrated or manycospecialized firms. Focusing on activities—the tasksthat need to be taken care of—provides an efficient wayof examining how firm and industry boundaries changeand how these changes create different types of “institu-tional packages” along some or all of the activities (or“steps”) of the value chain that are undertaken in a sector.

� Academy of Management Journal2005, Vol. 48, No. 3, 465–498.

465

responding growth of firms that only make, but donot design, their chips (Macher, 1998); the biotechsector provides yet more evidence, with the emer-gence of specialized research firms, specializeddrug-testing firms, and so on (Arora, Fosfuri, &Gambardella, 2000). The story of the minicomputerand then the personal computer (PC) is a furtherexample of an industry’s witnessing not only tech-nological change but also vertical disintegration.While the minicomputer business started off inte-grated, dominated by companies such as DEC andIBM, it soon opened up, and this process becameeven more pronounced with the advent of PCs.Veering far from the relatively integrated structuresof pioneers like Apple, the PC industry today has amultitude of segments, including component man-ufacturers, software and operating system provid-ers, specialized assemblers, resellers, consultantswho integrate products into client companies, andmore (Baldwin & Clark, 2000; Gawer & Cusamano,2002). Once disintegration occurred, the nature ofthe industry, its very definition, and its competitivedynamics were radically transformed, even for theplayers who chose to remain integrated by keepingall the production processes inside.

Such vertical disintegration has profound impli-cations. First, it changes the nature of the firms thatcan participate in an industry. In semiconductors,for example, the newly available vertically disinte-grated structure enabled engineering firms with noproduction capabilities or facilities to become sig-nificant players. In banking, the fact that data pro-cessing became a separate part of the productionprocess—that, through vertical disintegration,could be procured through the market rather thandone inside—led nonfinancial firms such as EDS,IBM, and Accenture to become key participants inthe financial institutions sector. The nature of ca-pabilities, the types of entrants into an industry,and the structure of competition can all changewhen disintegration happens, as the PC industryvividly illustrates (Baldwin & Clark, 2000; Gawer &Cusamano, 2002). To use a biological analogy, ver-tical disintegration allows a new, vertically cospe-cialized ecosystem to compete and partly cooperatewith the old, integrated structures, thus altering thelandscape for all involved (Jacobides & Winter,2005).

Although vertical disintegration can have pro-found effects, scholars know surprisingly littleabout it beyond what can be garnered from anec-dotal evidence or from the popular business press(e.g., Evans & Wurster, 1999). The contribution ofthis paper is its consideration of how as well as whydisintegration happens, focusing on the underlyingdrivers that bring it about.

THEORETICAL BACKGROUND

Existing Research on Vertical Disintegration

Several research strands have indirectly ad-dressed vertical disintegration, although none hasreally directly focused on it. An exception may bethe work of Stigler (1951), who suggested that thesize of a market limits the extent of specialization(which disintegration represents). But althoughmost industrialized countries and most sectorshave the requisite scale to support vertical special-ization outside firms, it doesn’t always occur. Thus,scale is generally not considered to be a good ex-planation for disintegration (see Langlois & Robert-son, 1995). There are almost no systematic studiesof the emergence of vertical disintegration, despitesubstantial research on the social and institutionaldynamics of product-category creation (Carruthers& Babb, 2000; Porac, Thomas, Wilson, Paton, &Kanfer, 1995; White, 1981); substantial research onthe social institutions of market exchange in gen-eral (Carruthers, 1996; Fligstein, 2001); and newresearch on vertical scope—that is, the amount ofvalue-adding steps in the production process that afirm is active in (Jacobides & Winter, 2005).

The main reason for the relative dearth of knowl-edge is that the literature, particularly transactioncost economics (Williamson, 1985, 1999), haslargely focused on a firms’ decisions to “make ver-sus buy” in given transactions. Such analysis isconducted at a subfirm level, in that the units ofanalysis are particular choices made “on the mar-gin” by individual firms.2 It does not look at entireindustries by examining, for example, how marketsemerge to create vertical disintegration. Nevertheless,transaction cost economics may be a useful startingpoint for understanding vertical disintegration.

Transaction cost economics focuses on thechoices an existing firm makes in deciding whetherto make or buy a particular input (Williamson,2000). If transaction costs—that is, the costs of us-ing markets rather than producing in-house—arehigh, then firms choose to make a particular input,thus bypassing the markets by integrating. If trans-action costs are low, firms rely on markets and buy.Transaction costs largely depend on the risk ofopportunistic renegotiation (Williamson, 1975,

2 Note that the literature also does not address howparticular firms’ choices in terms of making or buyingdifferent products and services are intertwined; that is, itdoes not directly address the question of how the bound-aries of one particular firm are set, and how they evolveover time. For an analysis of the logic underpinning thedesign of a particular firm’s vertical structure, see Jaco-bides and Billinger (2005).

466 JuneAcademy of Management Journal

1985, 1999). The risk of opportunism emergeswhen a potential party to a transaction, such as asupplier, needs to make dedicated, long-lasting in-vestments to make the relationship work, invest-ments that will be valuable in that relationship butnot in other contexts. The party undertaking such“asset-specific” (i.e., relationship-specific) invest-ment may be “held up” by the other party (here, thebuyer), who might have promised to compensatefor the investment but will be tempted to break thatpromise. The supplier, knowing this, is not likelyto make such a valuable but risky investment (Hart,1995). As a result, it is impossible for the buyer toget the benefits of such a specialized investment,unless the buyer gives an ironclad guarantee of noopportunism, which, in a dynamic and unpredict-able environment, is not economically feasible. Sothe main way to achieve specialized investments isvertical integration (Williamson, 1985). Thus, ac-cording to this theory, when asset specificity ishigh, and hence transaction costs owing to oppor-tunism are significant, firms will be integrated.When asset specificity is low, firms will not beintegrated.

The question of integration on the industry level,however, is not examined in transaction cost eco-nomics, nor is the option of using markets. Instead,the theory is informed “by the presumption that ‘inthe beginning, there were markets’ ” (Williamson,1985: 87). It begins with the presumption that thechoice of relying on a market exists and explainswhy firms integrate, bypassing the market. It doesnot extend to the development of new markets.Transaction costs theory does not address how in-dustries or value chain structures evolve and doesnot ask the question of whether firms can choosewhether to make or buy. To use a schematic illus-tration from the computer industry, transactioncost economics can explain why a computer man-ufacturer decides to procure a component from themarket, or make it in-house, but it cannot explainthe fundamental industry change from a structureof integrated entities, active throughout the valuechain, to a structure with a distinct market forcomponents that firms can either make or buy (cf.Baldwin & Clark, 2000, 2003). So, given that re-searchers know that many industries start off inte-grated before breaking up into cospecialized pieceslinked through a market (cf. Christensen, Verlin-den, and Westerman, 2002; Jacobides & Winter,2005; Langlois & Robertson, 1995; Stigler, 1951),the lack of a consistent theory and a correspondingbody of empirical evidence on vertical disintegra-tion leaves both empirical and theoretical gaps.

Some related research pertinent to the analysis of

changes in industry scope exists. In their work onthe historical dimension of transaction costs, forinstance, Argyres and Liebeskind (1999) and Mad-hok (2002) suggested that scholars should considerthe specificities of firms’ histories to understandwhat drives their choices of scope. These authorstoo, however, focused on the individual choices ofspecific firms that can either make or buy. Silver(1984) and then Langlois (1992, 2003; Langlois &Robertson, 1989,1995) have argued that transactioncosts are dynamic or even transient and hence thatthey decline over time as potential suppliers andbuyers learn to work together. Christensen and co-authors (2002) argued that disintegrated structuresare “worse” than integrated ones, but that theybecome “good enough” after a while, without, how-ever, explaining why this is so, and, more to thepoint, without explaining how or why vertical dis-integration emerges in the first place. So, while allthis research has correctly pointed out the need fora historically informed analysis of vertical scope, ithas not offered a framework that explains how anindustry’s scope evolves—in particular, how verti-cal disintegration happens—nor has it explainedwhy rapid disintegration happens in some settingsbut not in others.

Theoretical Gaps and the Contribution of thisPaper

The discussion above raises an interesting set ofopportunities. On the empirical side, it is desirableto better document and explain vertical disintegra-tion and market creation, as this process has signif-icant implications for industries and the firmswithin them. On the theoretical side, the need to doso becomes particularly important inasmuch ascurrent theory is ill suited to explaining disintegra-tion. This is the case for three reasons:

First, existing literature has focused on the indi-vidual transaction, as opposed to the changes in anindustry that enable a market to appear, but factorsthat operate on the industry level of analysis areunlikely to be fully reducible to those operating onthe level of the individual transaction.

Second, most of the arguments in transactioncost economics are designed to explain why firmsabandon markets and opt to integrate instead. Onemight simply argue that to understand why marketsemerge, all one has to do is construct the inverse ofthe story, using the same factors to explain disin-tegration. Yet organizational processes and, in par-ticular, processes of institutional change are rarelysymmetric. To wit, a theory of organizationalgrowth cannot be the mirror inverse of a theory of

2005 467Jacobides

organizational decline (cf. McKinley, 1993), be-cause the factors that explain why and how firmsgrow are qualitatively different from the factors thatexplain why and how firms decline. The causallogic relevant to explaining the processes and mo-tivations of growth and decline may differ in itself,so that one cannot use theories of growth to fullyexplain decline, and vice versa. Likewise, the pro-cesses that bring about vertical disintegration arelikely to differ from those that bring about integra-tion: To explain disintegration, a theory must ac-count for what allows a market to be set up in thefirst place. Existing theory has not done this, nor is itsafe to assume that existing theory could be extendedto account for the initial appearance of markets.

Third, most of the existing literature cannot ex-plain how and why transaction costs can be re-duced, as it does not focus on the dynamics of theevolution of an industry. Moreover, even in thelimited research on “dynamic” transaction costs(Langlois, 1992, 2003), there is not much that canhelp explain why transaction costs decrease insome settings and not others. For all these reasons,it seems that scholars may well obtain new theoret-ical insights by studying the process of verticaldisintegration without being entirely bound by ex-isting theory.

It follows from these observations that the bestway to understand the emergence of vertical disin-tegration is to undertake an inductive analysis that,while building on existing literature, allows newanalytical insights on how the intermediate mar-kets resulting from disintegration emerge. To gleansuch insights, I examined an industry that under-went significant vertical disintegration: mortgagebanking in the United States. Whereas until the late1970s mortgage loans were originated, funded, andserviced by integrated financial institutions (banksor savings and loan associations), by the end of thecentury, the industry had become a collection ofvertically cospecialized entities. To understandwhat drove this vertical disintegration, I examinedthe history of the entire industry as it evolved andfocused on the emergence of three new markets—three episodes of vertical disintegration—over a20-year period. Finally, in addition to studyinghow these new markets emerged, I also examinedwhat drove and motivated this process of verticaldisintegration.

The contribution of this study, then, is twofold.First, it provides an analysis of the market emer-gence process that goes beyond the traditional pur-view of transaction cost economics and examinesthe factors that enable the initial vertical break-upin an industry. Second, it explores the drivers of

this process: it analyzes when and why such disin-tegration and new market creation come about. Byshifting the level of analysis from the transaction tothe industry and the firms within it, this studyprovides a template that can explain when and whyvertical disintegration happens.

As this is an inductive study, I first describe themortgage banking industry and introduce the meth-ods. I then present the induced theoretical frame-work and discuss how it relates to existing theory.I conclude by considering the insights offered bythis new framing and theoretical approach on theorganizational drivers of vertical scope as they af-fect research and practice alike.

METHODS

Analysis and Procedures

This paper presents an inductive theory based onan in-depth, qualitative study of the evolution ofthe mortgage banking industry. The level of analy-sis in the study was the entire value chain of oneindustry. I chose this approach in order to portrayboth the process and the context of change alongwith their interconnections over time (Mohr, 1982;Pettigrew, 1990). As process research, this studyfocused on understanding the causal dynamics of aparticular setting (Mohr, 1982). The central as-sumption was that “causation is neither linear norsingular . . . [hence] explanations of change arebound to be holistic and multifaceted” (Pettigrew,1990: 269). The causal relations derived here areexplained in detail in the main body of the paperand are closely linked to the evidence, so as toallow their internal validity to be assessed (Yin,1994: 33).

This setting was chosen on conceptual grounds,rather than for representativeness (Miles & Huber-man, 1994: 27). The aim was to select a setting thatwould allow isolation of the central concepts per-taining to the research questions. Mortgage bankingwas thus selected because it underwent a processof disintegration and market creation, and in par-ticular because it witnessed several episodes of ver-tical specialization. Furthermore, the decision wasinfluenced by the fact that the product/service of-fered, mortgages, had not changed substantially inthe period of this study. In other settings that Ievaluated (e.g., semiconductors, pharmaceuticals,auto manufacturing), the process of value chainand industry change was often entangled with sig-nificant changes in the product provided. Avoidingthese complications enabled me to identify the ma-

468 JuneAcademy of Management Journal

jor underlying drivers of market creation for a givenproduction sequence.3

This study is based on multiple sources of evi-dence: archival data, industry publications andmanuals, interviews, and direct observation. Al-though it covers a 20-year period of vertical disin-tegration, my direct observation in the field lastedabout 38 months. My primary objective was to cre-ate an accurate depiction of the evolution of theindustry’s value chain, something that did not existwhen I went to the field.4 To do so, I used manysources of evidence: archival data, qualitative evi-dence, and corroborating quantitative evidence; thelatter was used to create a synthetic map of theindustry structure as it evolved.

In terms of data reliability, the study conformswith Yin’s (1994: 32) focus on developing constructvalidity and with Guba and Lincoln’s (1982) em-phasis on confirmability. The theory is built uponrepresentations of phenomena. It is essential forsuch representations to be accurate and meaning-ful; that is, they must reflect the shared views ofindustry participants and observers. I used multi-ple sources of evidence to ensure an accurate rep-resentation of the industry’s evolution. The archi-val data were particularly useful in reconciling thediverse views I obtained through my interviews,which are described below. Thus, whenever I en-countered a new idea or view, I would test itagainst the archival data and reports of the time. Ifdata did not exist, and I had discrepant informa-tion, I tried to determine if different constituenciesin the mortgage sector accepted a particular view orargument. If there was disagreement, I would mod-

ify the argument until a reasonable amount ofagreement could be reached and, failing that,would consider the argument as unsupported.Methodologically, my objective was to ensure I hadan accurate depiction of the industry—of what hadhappened—and to provide an interpretation,through inductive theorizing, of what broughtabout disintegration.

In keeping with Pettigrew’s (1990) directives forinductive, case-based research, while I did ap-proach the organizational field of interest with the-oretical constructs in mind, I did not impose them.Instead, I considered how the detailed evidencegathered in the field might inform existing theoryor constructs, such as transaction costs. To do so, Iexamined how the data informed my understand-ing of (1) the vertical disintegration and marketcreation process and (2) what motivates and drivesit. Then, working within the emerging theoreticalframework, I reconsidered the data and clarifiedparticular issues, which led me to refine the devel-oping theory, and so on. As my theory developed, Iwould communicate it to key industry participants,and in particular the chief economist of the Mort-gage Bankers Association of America, with whom Iworked closely in the project. Thus, I used an iter-ative process of theory development and data anal-ysis (cf. Eisenhardt, 1989, 1991) that led to theframework proposed in this paper. (The next mainsection of this article, “The Setting: Mortgage Bank-ing and the Genesis of Three Sets of IntermediateMarkets,” describes the process of discovery andthen validation of my framework.) As the evidencewas historical, archival evidence was given dueattention. The archival data I used included indus-try manuals, each issue of the monthly publicationMortgage Banking from 1968 onwards, the manualsfor the School of Mortgage Banking (see Lederman,1985, 1995), all mortgage-related bulletins of theFederal Reserve, earlier studies of the industry(e.g., Tuchman, 1986), annual reports of major in-stitutions, regulations and congressional acts re-lated to the sector, all academic research on thesector that I could locate, analysts’ reports (espe-cially from Morgan Stanley, which covers the sec-tor extensively), and other material described below.I also gathered industry statistics and demographics,especially from the Housing Mortgage Disclosure Act(HMDA) database of the Department of Housing andUrban Development, the industry reports of theMortgage Bankers Association (including its an-nual cost and servicing studies), and data fromprivate consultancies, such as Inside Mortgage Fi-nance and Wholesale Access, as well as confiden-tial data assembled by two consultancies.

3 This kind of purposive choice may raise questionsabout the external validity of the theory (Yin, 1994), orthe extent to which the insights from this study aretransferable to other settings (Guba & Lincoln, 1982).However, the usefulness of generalization from this typeof data is analytical rather than statistical (Firestone,1993). While claiming no statistical significance for thesefindings, I suggest that choosing a setting that allowedisolation of key theoretical constructs makes the theoret-ical findings applicable to other industry settings andprovides a grounded theoretical framework that can betested in other settings in subsequent research.

4 As there was no existing theory, either in the indus-try or in academe, on the drivers or even the nature ofdisintegration, my investigation required an intensiveinvolvement so that the basic value chain layout could bederived. I thus had to become familiar with the technicaldetail of the industry, so as to “speak the language” of theparticipants in the various bits of the value chain. Thequestions that I would then ask would not be couched inmy “native” terminology, but rather in that of industryparticipants.

2005 469Jacobides

TA

BL

E1

Sou

rces

and

Act

ivit

ies

for

Pro

ject

Sta

gesa

Ch

arac

teri

stic

sof

Sta

geS

tage

1:A

ugu

st19

98–D

ecem

ber

1998

Sta

ge2:

Jan

uar

y19

99–A

pri

l20

00S

tage

3:M

ay20

00–N

ovem

ber

2001

Obj

ecti

ves

Un

der

stan

din

gin

du

stry

stru

ctu

res

and

pro

cess

esE

xplo

rin

gev

olu

tion

ofin

du

stry

stru

ctu

rean

dm

arke

tcr

eati

onB

ecom

ing

fam

ilia

rw

ith

ind

ust

ryp

arti

cip

ants

Iden

tify

ing

key

par

tici

pan

tsfo

rsu

bseq

uen

tin

terv

iew

s

Exp

lori

ng

inm

ore

det

ail

the

spec

ific

sof

ind

ust

rych

ange

s:p

rod

uct

s,te

chn

olog

y,p

laye

rs,

and

stru

ctu

reF

inal

izin

ga

map

ofth

ein

du

stry

and

its

evol

uti

onC

reat

ing

am

apw

ith

dri

vers

ofve

rtic

ald

isin

tegr

atio

n

Fin

aliz

ing

map

pin

gof

the

mec

han

ics

and

cau

ses

ofin

du

stry

evol

uti

onan

dm

arke

tcr

eati

onC

omp

lem

enti

ng

the

fiel

dev

iden

ceR

esol

vin

gre

mai

nin

gd

iscr

epan

cies

Inte

rvie

ws

18in

terv

iew

sw

ith

exec

uti

ves

from

ind

ust

ryre

gula

tors

and

over

sigh

tag

enci

es,

incl

ud

ing

the

MB

AA

,N

atio

nal

Ass

ocia

tion

ofM

ortg

age

Ban

kers

,H

UD

,O

FH

EO

,F

ann

ieM

ae,

and

Fre

dd

ieM

ac

84in

terv

iew

sw

ith

ind

ust

ryp

arti

cip

ants

,in

clu

din

gba

nke

rs,

brok

ers,

serv

ice

and

tech

nol

ogy

pro

vid

ers,

tech

nol

ogy

pro

vid

ers,

ind

ust

ryan

alys

ts,

fin

ance

con

sult

ants

,an

dre

gula

tors

27in

terv

iew

sw

ith

MB

AA

sen

ior

exec

uti

ves

and

mor

tgag

eba

nke

rsF

ollo

w-u

pp

hon

eca

lls

and

shor

td

iscu

ssio

ns

wit

hm

any

info

rman

ts

32in

terv

iew

sw

ith

exec

uti

ves

from

mor

tgag

eba

nks

,in

du

stry

anal

ysts

,an

dco

nsu

ltan

tsS

econ

dar

yso

urc

esH

isto

rica

lst

ud

ies

Com

pan

ym

anu

als

His

tori

cal

acco

un

tsS

ecto

rd

escr

ipti

ons

Tra

de

arti

cles

Com

pan

ym

anu

als

Tra

de

pu

blic

atio

ns

Pre

ssre

leas

esT

rad

ep

ubl

icat

ion

sH

isto

rica

lac

cou

nts

ofse

ctor

evol

uti

onE

ven

ts19

98M

BA

AN

atio

nal

Con

ven

tion

Tw

o-w

eek

cou

rse

for

mor

tgag

eex

ecu

tive

s19

99M

BA

AN

atio

nal

Con

ven

tion

Tw

oM

BA

Ain

du

stry

mee

tin

gsT

hre

ein

du

stry

rou

nd

tabl

es

Pre

sen

tati

onof

init

ial

fin

din

gsto

ake

ynot

ep

anel

ofth

e20

00M

BA

AN

atio

nal

Con

ven

tion

Pre

sen

tati

onof

fin

din

gsto

the

2001

MB

AA

CE

Oco

nfe

ren

ce

aT

he

MB

AA

isth

eM

ortg

age

Ban

kers

Ass

ocia

tion

ofA

mer

ica.

HU

Dis

the

U.S

.off

ice

ofH

ousi

ng

and

Urb

anD

evel

opm

ent.

Th

eO

FH

EO

isth

eO

ffic

eof

Fed

eral

Hou

sin

gE

nte

rpri

seO

vers

igh

t.

Data Collection

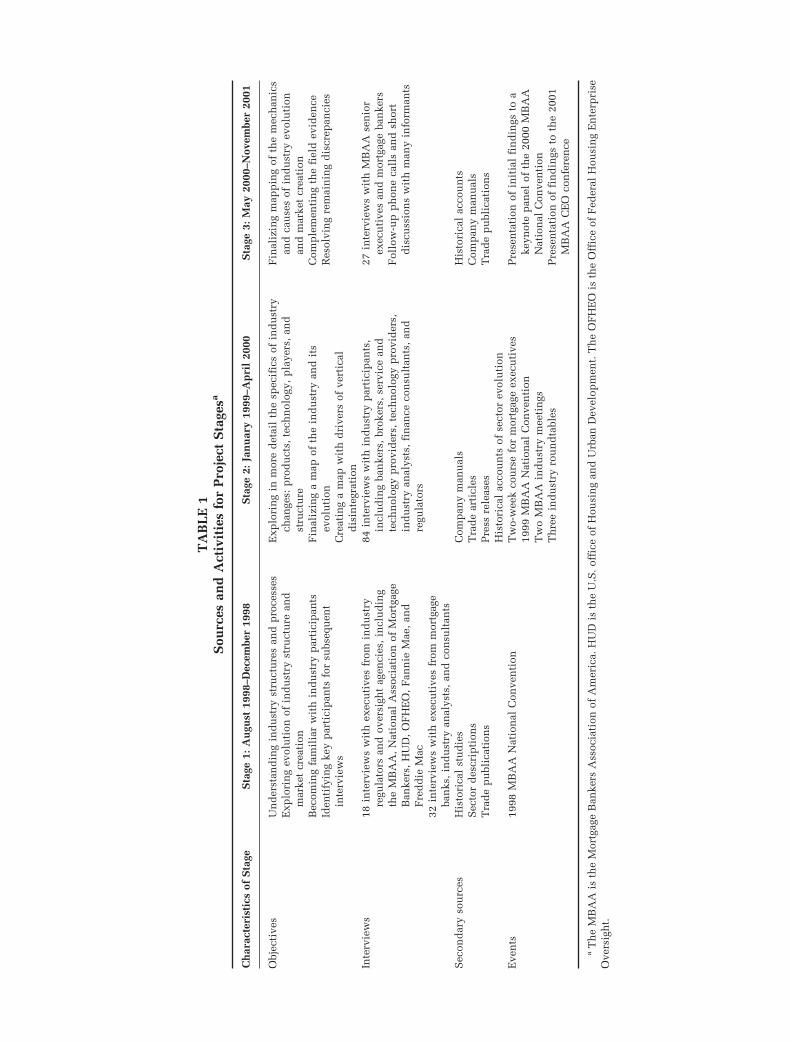

The study was underwritten by the MortgageBankers Association of America (MBAA) and theWharton Financial Institutions Center, a researchcenter sponsored by the Sloan Foundation. It lasted38 months and proceeded in three stages; Table 1summarizes the evidence examined, analyzed, andused in these three stages.

The first stage of the research took place betweenAugust and December 1998 and focused on identi-fying the key industry participants and getting agood idea of the industry and its evolving structure.I conducted 18 interviews with industry regulatorsand oversight agencies (such as the Department ofHousing and Urban Development and the Office ofFederal Housing Enterprise Oversight), as well asthe major government-sponsored “securitizers”(Fannie Mae, Freddie Mac, and Ginnie Mae.5 Theseregulator interviews were followed by 32 semi-structured interviews with executives who hadbeen in the field for a long time and who were ableto provide an overview of the sector and its evolu-tion. The evidence was complemented with docu-ments from secondary sources, including the fewexisting historical studies and descriptions of thesector, and trade publications. During this stage Ialso participated in the 1998 MBAA NationalConvention.

The second stage of the fieldwork and archivalresearch was conducted between January 1999 andApril 2000. During this period, I delved moredeeply into the history of the sector to explore thespecifics of its evolution in more detail, looking atits products, technology, players, and industrystructure. The ongoing support of the MBAAproved particularly helpful at this stage, as it pro-vided me with critical contacts and in-house data. Ifirst attended a two-week course for mortgage ex-ecutives who were either from outside of theUnited States or new to the sector; this course fur-ther familiarized me with the way the industry isorganized in the U.S. and abroad. I then conducted84 semistructured interviews with industry partic-ipants and consulted a large number of articles andmanuals, as well as all the published historical

accounts of the sector. In this stage, I attended the1999 MBAA National Convention and two moreindustry meetings, where I interacted formally andinformally with industry participants. I was alsoallowed to sit in on three industry roundtables or-ganized by the MBAA. From the evidence collectedduring the first two stages, I created a preliminarymap of the industry and its evolution, which waschecked by the chief economist of the MBAA.

The third stage of the research project, conductedbetween May 2000 and November 2001, focused onsolidifying the view of the industry and its evolu-tion, as well as resolving any remaining discrepan-cies and complementing the field evidence. I con-ducted 27 interviews with MBAA senior executivesand mortgage bankers. I also conducted follow-upinterviews with many informants and had numer-ous phone calls and short discussions to confirminformation and fill in gaps. I also communicatedthe basic findings of the research and received ex-tensive feedback on the validity and accuracy of mydescription. This stage culminated in an industrypublication (Jacobides, 2001), which I circulated toseveral executives ahead of time to solicit theirinput.

Throughout the study, I selected interviewees soas to maximize the variety of profiles and hetero-geneity of perspectives in the industry. I choserespondents from different-sized firms, from firmswith vastly different strategies and scope, and fromfirms with various roles (technology, origination,servicing, and so forth). I selected several partici-pants who were not mortgage bankers but wereservice or technology providers, analysts, regula-tors, or consultants. The level of seniority also var-ied, although few interviewees had less than fiveyears of experience in the industry; Figures 1 and 2provide summary statistics of the interviewees forall three stages. The focus of the discussion de-pended on the profile of the individual, and I con-centrated on the respondents’ fields of expertise

5 To “securitize” mortgage loans means to take a set ofrelatively homogeneous loans, bundle them together, andthen create a “security,” which is an instrument that canbe sold (much like a bond) though the capital market.The “securitizer” is the entity buying loans (from com-panies that have issued them to individuals); then creat-ing the infrastructure for making the security; and thenselling the bundled loans to the capital market. SeeFabozzi and Modigliani (1992) or Nadler et al. (1992).

FIGURE 1Interviewees’ Tenures in the Mortgage Sector

2005 471Jacobides

and activity, except when they volunteered to pro-vide their broader assessment.6 Major issues andthreads that emerged in the interviews were incor-porated in subsequent interviews. I undertook all ofthe interviews. Some, but not all, were taped, as theinterviewees were often uncomfortable with taperecordings. For interviews that were not recordedand transcribed, I kept notes, which I consultedagain after the interviews and as I was preparingthe account of industry evolution. Finally, becauseinterviewees were concerned about maintaininganonymity, I sometimes use published sources forquotations, rather than primary evidence, to sup-port my conclusions.

The Setting: Mortgage Banking and the Genesisof Three Sets of Intermediate Markets

A mortgage is a loan collateralized by real estate.To make such a loan possible, a lender, as a conduitfor those with excess funds, must be able to find aborrower who needs a mortgage. Roughly speaking,to make a mortgage possible, either one integratedfirm or a series of vertically cospecialized firmslinked though the market must ensure that the fol-

lowing happens: (1) lenders with excess funds arefound; (2) borrowers willing to take a loan arefound and steered to the appropriate loan type; (3)borrowers are analyzed for creditworthiness, thevalue of their collateral, etc., and are guidedthrough the paperwork and procedures required toinsure titles and deeds and meet all other legalrequirements; (4) the loan is closed, and the trans-action consummated and recorded; (5) the loan isserviced for the duration of its length, which meansreceiving payments from the borrower and manag-ing the account until it is paid off or, alternatively,foreclosing if payments are not received; and (6)payments are made to the lenders or other provid-ers of capital.

These six different functions were originally per-formed in integrated institutions, in particular, inretail banks, which maintained some mortgageloans, or in savings and loan associations (S&Ls),which were primarily focused on mortgage loans.7

The short-term deposits of retail customers andlending from the capital market provided liquidityfor both of these integrated types of firms, allowingthem to fund their loans (Fabozzi & Modigliani,1992; Lederman, 1985). Banks and S&Ls sought outmortgage loan applicants, prepared and processedapplications, and serviced the loans until they ex-6 The four main question areas were (1) How has your

segment evolved? What have been the main differencesthat you observed? Why did these changes occur at thetime that they did? (2) Was there any change in the typesof activities that your segment performs? (3) Has therebeen any change in the scope of activities in your part ofthe mortgage industry? Why did any such changes occurat the time they did? and (4) (if the participants identifiedthe trend toward disintegration), Can you identify whythere has been such a tendency? What factors led to thisbreakup? Why did it not happen before?

7 This study focuses on the evolution of residentialmortgages. The commercial mortgage industry’s struc-ture and evolution is broadly similar, although verticaldisintegration has been less pronounced. The differenceis largely a result of the comparative difficulty of stan-dardizing information (one of the issues I focus on in myinductive framework).

FIGURE 2Backgrounds of Interviewees

472 JuneAcademy of Management Journal

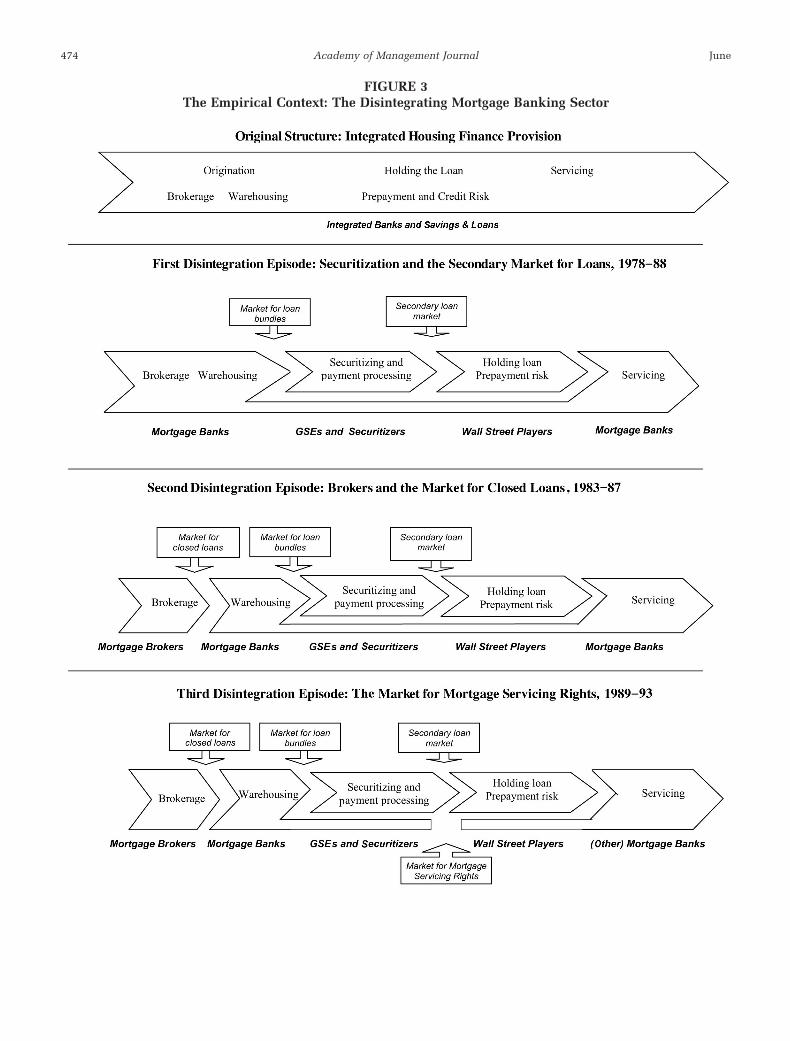

pired. This outline captures the earlier, integratedversion of the industry.

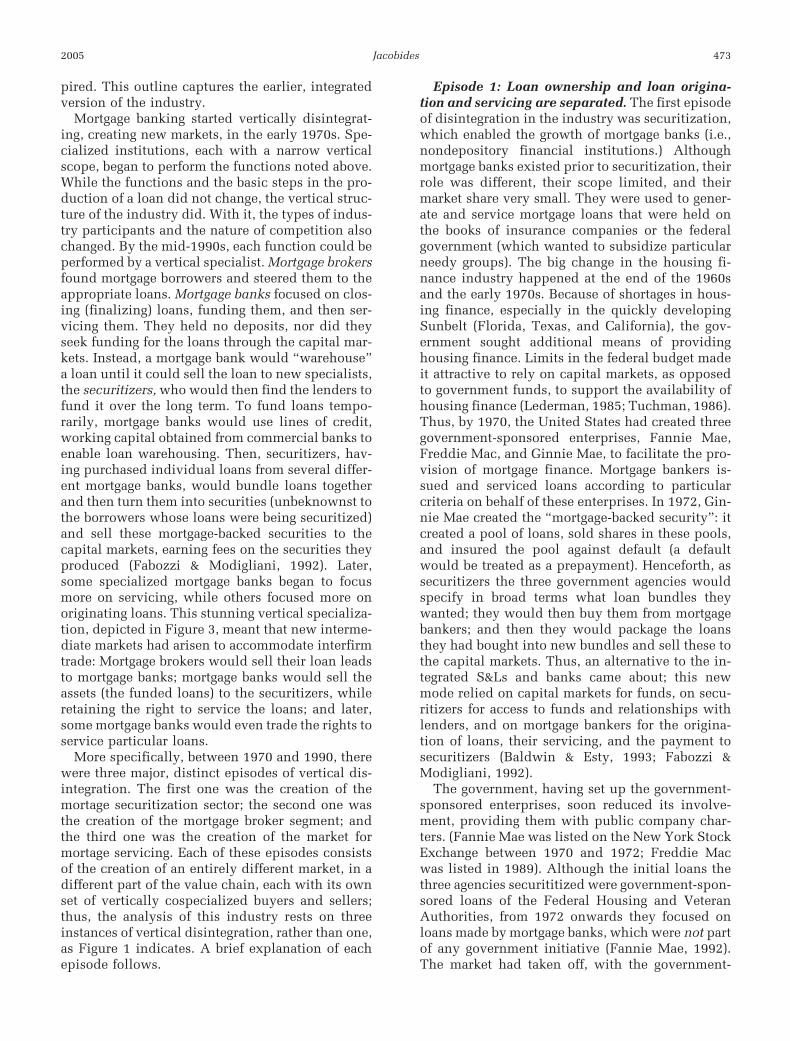

Mortgage banking started vertically disintegrat-ing, creating new markets, in the early 1970s. Spe-cialized institutions, each with a narrow verticalscope, began to perform the functions noted above.While the functions and the basic steps in the pro-duction of a loan did not change, the vertical struc-ture of the industry did. With it, the types of indus-try participants and the nature of competition alsochanged. By the mid-1990s, each function could beperformed by a vertical specialist. Mortgage brokersfound mortgage borrowers and steered them to theappropriate loans. Mortgage banks focused on clos-ing (finalizing) loans, funding them, and then ser-vicing them. They held no deposits, nor did theyseek funding for the loans through the capital mar-kets. Instead, a mortgage bank would “warehouse”a loan until it could sell the loan to new specialists,the securitizers, who would then find the lenders tofund it over the long term. To fund loans tempo-rarily, mortgage banks would use lines of credit,working capital obtained from commercial banks toenable loan warehousing. Then, securitizers, hav-ing purchased individual loans from several differ-ent mortgage banks, would bundle loans togetherand then turn them into securities (unbeknownst tothe borrowers whose loans were being securitized)and sell these mortgage-backed securities to thecapital markets, earning fees on the securities theyproduced (Fabozzi & Modigliani, 1992). Later,some specialized mortgage banks began to focusmore on servicing, while others focused more onoriginating loans. This stunning vertical specializa-tion, depicted in Figure 3, meant that new interme-diate markets had arisen to accommodate interfirmtrade: Mortgage brokers would sell their loan leadsto mortgage banks; mortgage banks would sell theassets (the funded loans) to the securitizers, whileretaining the right to service the loans; and later,some mortgage banks would even trade the rights toservice particular loans.

More specifically, between 1970 and 1990, therewere three major, distinct episodes of vertical dis-integration. The first one was the creation of themortage securitization sector; the second one wasthe creation of the mortgage broker segment; andthe third one was the creation of the market formortage servicing. Each of these episodes consistsof the creation of an entirely different market, in adifferent part of the value chain, each with its ownset of vertically cospecialized buyers and sellers;thus, the analysis of this industry rests on threeinstances of vertical disintegration, rather than one,as Figure 1 indicates. A brief explanation of eachepisode follows.

Episode 1: Loan ownership and loan origina-tion and servicing are separated. The first episodeof disintegration in the industry was securitization,which enabled the growth of mortgage banks (i.e.,nondepository financial institutions.) Althoughmortgage banks existed prior to securitization, theirrole was different, their scope limited, and theirmarket share very small. They were used to gener-ate and service mortgage loans that were held onthe books of insurance companies or the federalgovernment (which wanted to subsidize particularneedy groups). The big change in the housing fi-nance industry happened at the end of the 1960sand the early 1970s. Because of shortages in hous-ing finance, especially in the quickly developingSunbelt (Florida, Texas, and California), the gov-ernment sought additional means of providinghousing finance. Limits in the federal budget madeit attractive to rely on capital markets, as opposedto government funds, to support the availability ofhousing finance (Lederman, 1985; Tuchman, 1986).Thus, by 1970, the United States had created threegovernment-sponsored enterprises, Fannie Mae,Freddie Mac, and Ginnie Mae, to facilitate the pro-vision of mortgage finance. Mortgage bankers is-sued and serviced loans according to particularcriteria on behalf of these enterprises. In 1972, Gin-nie Mae created the “mortgage-backed security”: itcreated a pool of loans, sold shares in these pools,and insured the pool against default (a defaultwould be treated as a prepayment). Henceforth, assecuritizers the three government agencies wouldspecify in broad terms what loan bundles theywanted; they would then buy them from mortgagebankers; and then they would package the loansthey had bought into new bundles and sell these tothe capital markets. Thus, an alternative to the in-tegrated S&Ls and banks came about; this newmode relied on capital markets for funds, on secu-ritizers for access to funds and relationships withlenders, and on mortgage bankers for the origina-tion of loans, their servicing, and the payment tosecuritizers (Baldwin & Esty, 1993; Fabozzi &Modigliani, 1992).

The government, having set up the government-sponsored enterprises, soon reduced its involve-ment, providing them with public company char-ters. (Fannie Mae was listed on the New York StockExchange between 1970 and 1972; Freddie Macwas listed in 1989). Although the initial loans thethree agencies securititized were government-spon-sored loans of the Federal Housing and VeteranAuthorities, from 1972 onwards they focused onloans made by mortgage banks, which were not partof any government initiative (Fannie Mae, 1992).The market had taken off, with the government-

2005 473Jacobides

FIGURE 3The Empirical Context: The Disintegrating Mortgage Banking Sector

474 JuneAcademy of Management Journal

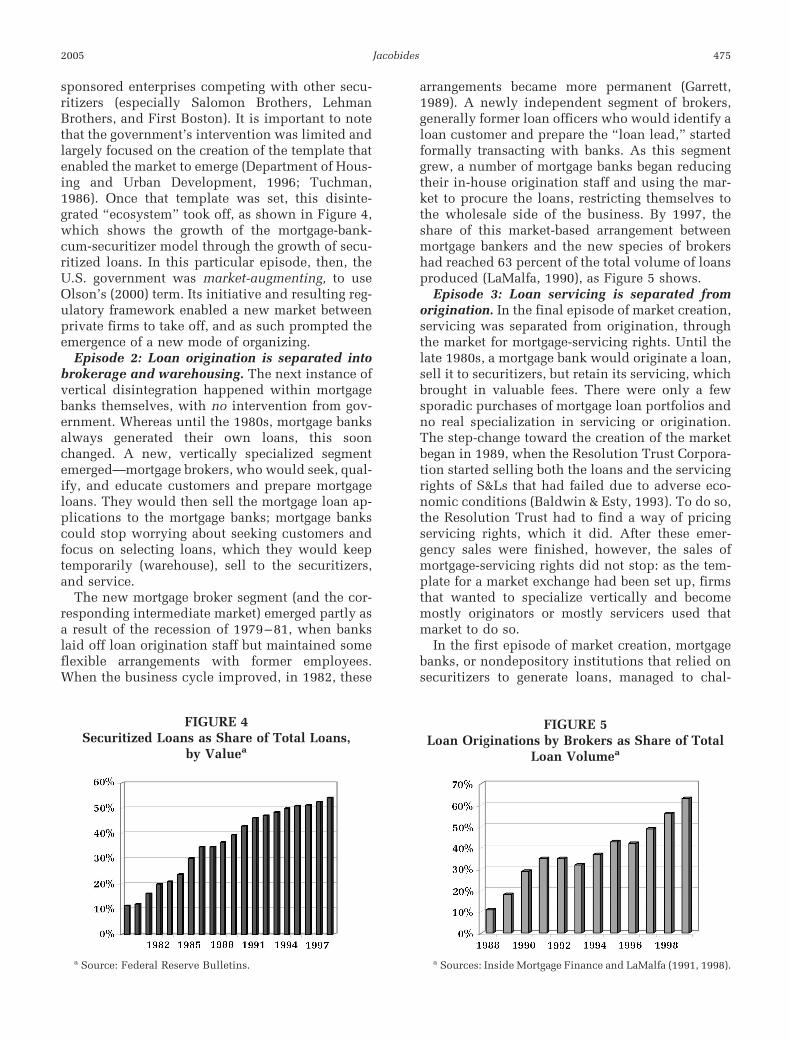

sponsored enterprises competing with other secu-ritizers (especially Salomon Brothers, LehmanBrothers, and First Boston). It is important to notethat the government’s intervention was limited andlargely focused on the creation of the template thatenabled the market to emerge (Department of Hous-ing and Urban Development, 1996; Tuchman,1986). Once that template was set, this disinte-grated “ecosystem” took off, as shown in Figure 4,which shows the growth of the mortgage-bank-cum-securitizer model through the growth of secu-ritized loans. In this particular episode, then, theU.S. government was market-augmenting, to useOlson’s (2000) term. Its initiative and resulting reg-ulatory framework enabled a new market betweenprivate firms to take off, and as such prompted theemergence of a new mode of organizing.

Episode 2: Loan origination is separated intobrokerage and warehousing. The next instance ofvertical disintegration happened within mortgagebanks themselves, with no intervention from gov-ernment. Whereas until the 1980s, mortgage banksalways generated their own loans, this soonchanged. A new, vertically specialized segmentemerged—mortgage brokers, who would seek, qual-ify, and educate customers and prepare mortgageloans. They would then sell the mortgage loan ap-plications to the mortgage banks; mortgage bankscould stop worrying about seeking customers andfocus on selecting loans, which they would keeptemporarily (warehouse), sell to the securitizers,and service.

The new mortgage broker segment (and the cor-responding intermediate market) emerged partly asa result of the recession of 1979–81, when bankslaid off loan origination staff but maintained someflexible arrangements with former employees.When the business cycle improved, in 1982, these

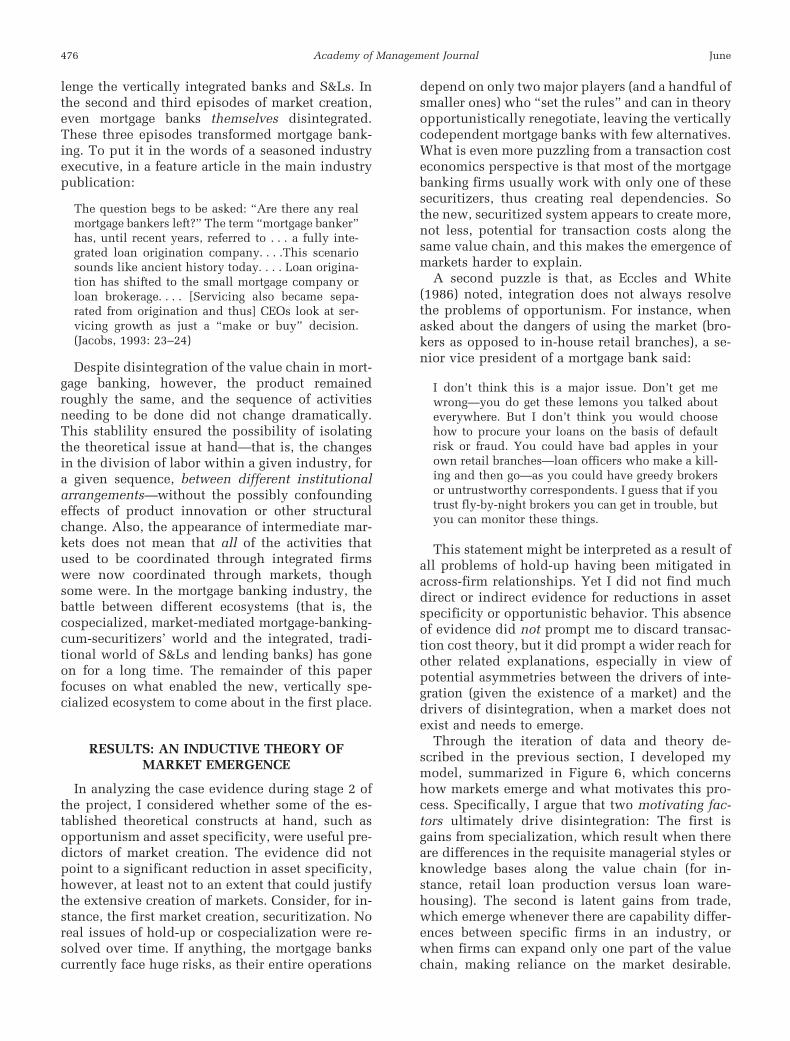

arrangements became more permanent (Garrett,1989). A newly independent segment of brokers,generally former loan officers who would identify aloan customer and prepare the “loan lead,” startedformally transacting with banks. As this segmentgrew, a number of mortgage banks began reducingtheir in-house origination staff and using the mar-ket to procure the loans, restricting themselves tothe wholesale side of the business. By 1997, theshare of this market-based arrangement betweenmortgage bankers and the new species of brokershad reached 63 percent of the total volume of loansproduced (LaMalfa, 1990), as Figure 5 shows.

Episode 3: Loan servicing is separated fromorigination. In the final episode of market creation,servicing was separated from origination, throughthe market for mortgage-servicing rights. Until thelate 1980s, a mortgage bank would originate a loan,sell it to securitizers, but retain its servicing, whichbrought in valuable fees. There were only a fewsporadic purchases of mortgage loan portfolios andno real specialization in servicing or origination.The step-change toward the creation of the marketbegan in 1989, when the Resolution Trust Corpora-tion started selling both the loans and the servicingrights of S&Ls that had failed due to adverse eco-nomic conditions (Baldwin & Esty, 1993). To do so,the Resolution Trust had to find a way of pricingservicing rights, which it did. After these emer-gency sales were finished, however, the sales ofmortgage-servicing rights did not stop: as the tem-plate for a market exchange had been set up, firmsthat wanted to specialize vertically and becomemostly originators or mostly servicers used thatmarket to do so.

In the first episode of market creation, mortgagebanks, or nondepository institutions that relied onsecuritizers to generate loans, managed to chal-

FIGURE 4Securitized Loans as Share of Total Loans,

by Valuea

a Source: Federal Reserve Bulletins.

FIGURE 5Loan Originations by Brokers as Share of Total

Loan Volumea

a Sources: Inside Mortgage Finance and LaMalfa (1991, 1998).

2005 475Jacobides

lenge the vertically integrated banks and S&Ls. Inthe second and third episodes of market creation,even mortgage banks themselves disintegrated.These three episodes transformed mortgage bank-ing. To put it in the words of a seasoned industryexecutive, in a feature article in the main industrypublication:

The question begs to be asked: “Are there any realmortgage bankers left?” The term “mortgage banker”has, until recent years, referred to . . . a fully inte-grated loan origination company. . . .This scenariosounds like ancient history today. . . . Loan origina-tion has shifted to the small mortgage company orloan brokerage. . . . [Servicing also became sepa-rated from origination and thus] CEOs look at ser-vicing growth as just a “make or buy” decision.(Jacobs, 1993: 23–24)

Despite disintegration of the value chain in mort-gage banking, however, the product remainedroughly the same, and the sequence of activitiesneeding to be done did not change dramatically.This stablility ensured the possibility of isolatingthe theoretical issue at hand—that is, the changesin the division of labor within a given industry, fora given sequence, between different institutionalarrangements—without the possibly confoundingeffects of product innovation or other structuralchange. Also, the appearance of intermediate mar-kets does not mean that all of the activities thatused to be coordinated through integrated firmswere now coordinated through markets, thoughsome were. In the mortgage banking industry, thebattle between different ecosystems (that is, thecospecialized, market-mediated mortgage-banking-cum-securitizers’ world and the integrated, tradi-tional world of S&Ls and lending banks) has goneon for a long time. The remainder of this paperfocuses on what enabled the new, vertically spe-cialized ecosystem to come about in the first place.

RESULTS: AN INDUCTIVE THEORY OFMARKET EMERGENCE

In analyzing the case evidence during stage 2 ofthe project, I considered whether some of the es-tablished theoretical constructs at hand, such asopportunism and asset specificity, were useful pre-dictors of market creation. The evidence did notpoint to a significant reduction in asset specificity,however, at least not to an extent that could justifythe extensive creation of markets. Consider, for in-stance, the first market creation, securitization. Noreal issues of hold-up or cospecialization were re-solved over time. If anything, the mortgage bankscurrently face huge risks, as their entire operations

depend on only two major players (and a handful ofsmaller ones) who “set the rules” and can in theoryopportunistically renegotiate, leaving the verticallycodependent mortgage banks with few alternatives.What is even more puzzling from a transaction costeconomics perspective is that most of the mortgagebanking firms usually work with only one of thesesecuritizers, thus creating real dependencies. Sothe new, securitized system appears to create more,not less, potential for transaction costs along thesame value chain, and this makes the emergence ofmarkets harder to explain.

A second puzzle is that, as Eccles and White(1986) noted, integration does not always resolvethe problems of opportunism. For instance, whenasked about the dangers of using the market (bro-kers as opposed to in-house retail branches), a se-nior vice president of a mortgage bank said:

I don’t think this is a major issue. Don’t get mewrong—you do get these lemons you talked abouteverywhere. But I don’t think you would choosehow to procure your loans on the basis of defaultrisk or fraud. You could have bad apples in yourown retail branches—loan officers who make a kill-ing and then go—as you could have greedy brokersor untrustworthy correspondents. I guess that if youtrust fly-by-night brokers you can get in trouble, butyou can monitor these things.

This statement might be interpreted as a result ofall problems of hold-up having been mitigated inacross-firm relationships. Yet I did not find muchdirect or indirect evidence for reductions in assetspecificity or opportunistic behavior. This absenceof evidence did not prompt me to discard transac-tion cost theory, but it did prompt a wider reach forother related explanations, especially in view ofpotential asymmetries between the drivers of inte-gration (given the existence of a market) and thedrivers of disintegration, when a market does notexist and needs to emerge.

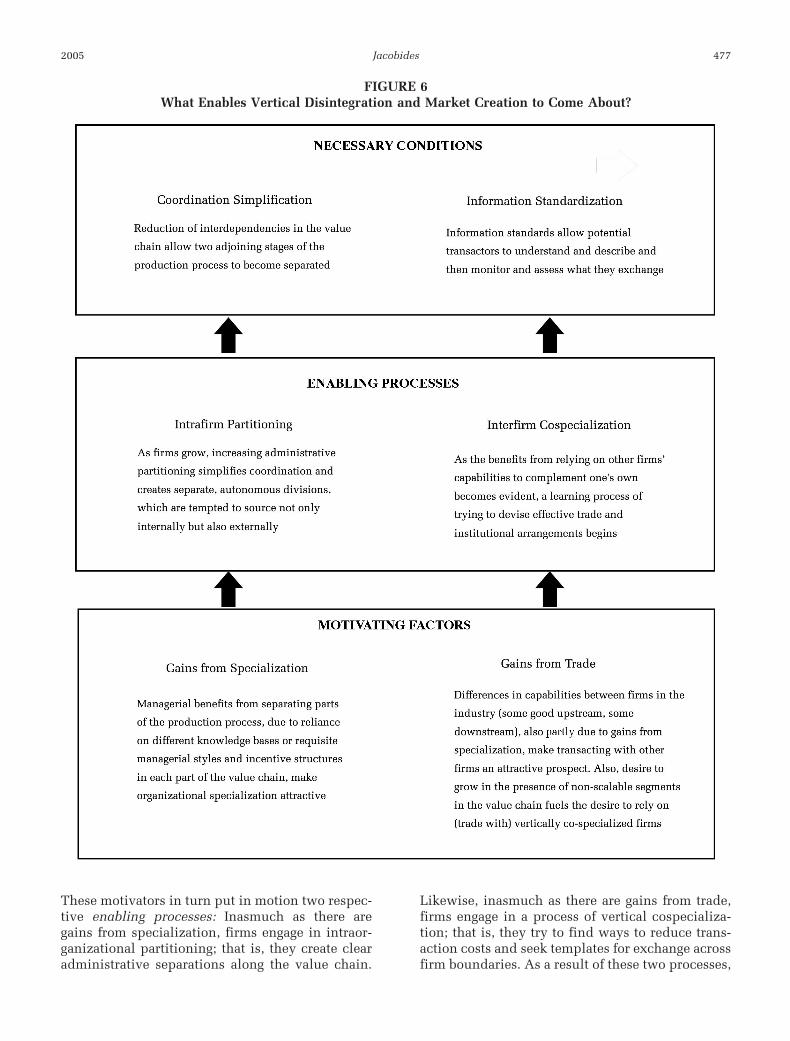

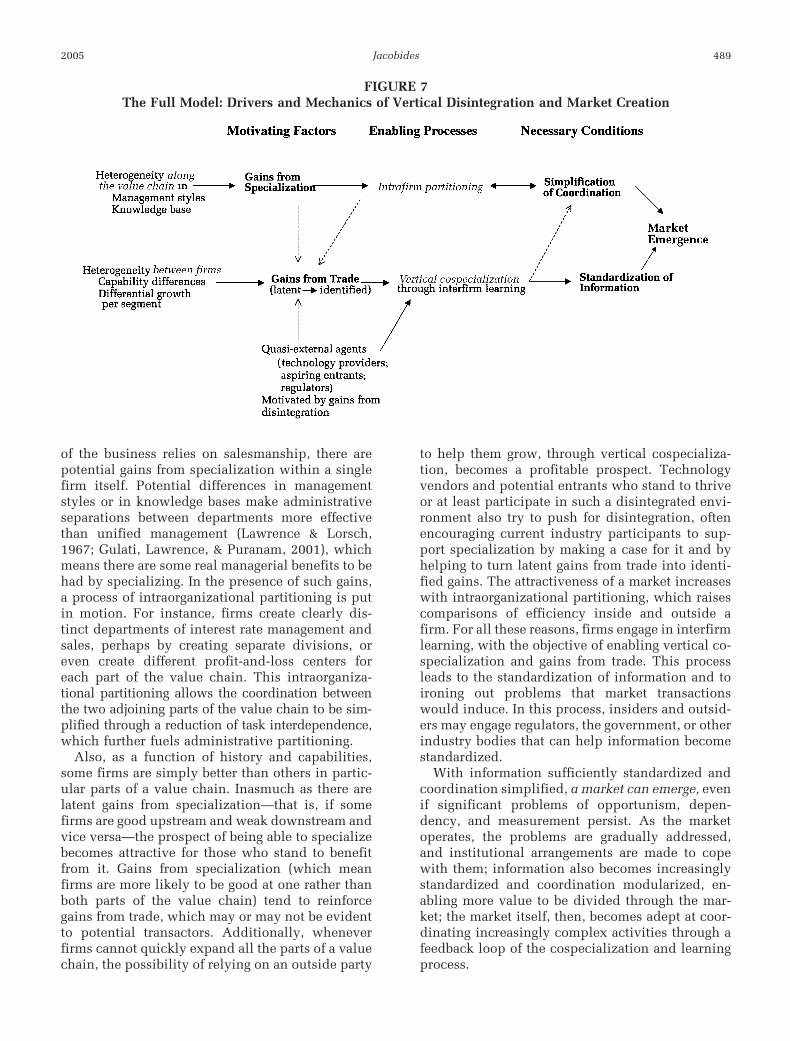

Through the iteration of data and theory de-scribed in the previous section, I developed mymodel, summarized in Figure 6, which concernshow markets emerge and what motivates this pro-cess. Specifically, I argue that two motivating fac-tors ultimately drive disintegration: The first isgains from specialization, which result when thereare differences in the requisite managerial styles orknowledge bases along the value chain (for in-stance, retail loan production versus loan ware-housing). The second is latent gains from trade,which emerge whenever there are capability differ-ences between specific firms in an industry, orwhen firms can expand only one part of the valuechain, making reliance on the market desirable.

476 JuneAcademy of Management Journal

These motivators in turn put in motion two respec-tive enabling processes: Inasmuch as there aregains from specialization, firms engage in intraor-ganizational partitioning; that is, they create clearadministrative separations along the value chain.

Likewise, inasmuch as there are gains from trade,firms engage in a process of vertical cospecializa-tion; that is, they try to find ways to reduce trans-action costs and seek templates for exchange acrossfirm boundaries. As a result of these two processes,

FIGURE 6What Enables Vertical Disintegration and Market Creation to Come About?

2005 477Jacobides

TA

BL

E2

Sou

rces

ofE

vid

ence

for

Iden

tify

ing

and

Val

idat

ing

the

Dri

vers

ofD

isin

tegr

atio

nan

dM

ark

etC

reat

ion

a,

b

Ep

isod

ean

dD

ata

Sou

rce

Gai

ns

from

Tra

de

and

Sp

ecia

liza

tion

Par

titi

onin

gan

dC

osp

ecia

liza

tion

Info

rmat

ion

Sta

nd

ard

izat

ion

Coo

rdin

atio

nS

imp

lifi

cati

on

Ep

isod

e1:

Sec

uri

tiza

tion

Evi

den

ce,s

tage

1;V

alid

atio

n,s

tage

2E

vid

ence

,st

age

2;V

alid

atio

n,

stag

es2

&3

Evi

den

ce,

stag

e1;

Val

idat

ion

,st

ages

1&

2E

vid

ence

,st

age

2;V

alid

atio

n,

stag

es2

&3

Inte

rvie

ws

Fed

eral

Boa

rdof

Res

erve

s;W

all

Str

eet

exec

uti

ves;

fin

ance

con

sult

ants

Wal

lS

tree

tex

ecu

tive

s;M

BA

A;

fin

ance

con

sult

ants

HU

D;

Wal

lS

tree

tex

ecu

tive

s;M

BA

A;

fin

ance

con

sult

ants

Wal

lS

tree

tex

ecu

tive

s;ac

adem

ics;

fin

ance

con

sult

ants

(wea

ksu

pp

ort)

Pu

blic

reco

rds

Aca

dem

icre

sear

chon

secu

riti

zati

on(e

.g.,

All

en&

San

tom

ero,

1997

;F

olla

in&

Zor

n,

1990

)

Des

crip

tion

sof

the

evol

uti

onof

secu

riti

zati

onin

mor

tgag

eba

nki

ng

(e.g

.,T

uch

man

,19

86)

Tec

hn

ical

anal

ysis

onse

curi

tiza

tion

;ac

adem

icre

sear

ch(F

aboz

zi&

Mod

igli

ani,

1992

;N

adle

ret

al.,

1992

);in

du

stry

pu

blic

atio

ns

(Sle

sin

ger,

1994

)

Aca

dem

icre

sear

chon

S&

Lch

ange

s(B

ald

win

&E

sty,

1993

)

Ep

isod

e2:

Bro

ker

mar

ket

crea

tion

Evi

den

ce,s

tage

1;V

alid

atio

n,s

tage

2E

vid

ence

,st

age

1;V

alid

atio

n,

stag

e2

Evi

den

ce,

stag

e1;

Val

idat

ion

,st

ages

1&

2E

vid

ence

,st

age

1;V

alid

atio

n,

stag

es1

&2

Inte

rvie

ws

MB

AA

;N

atio

nal

Ass

ocia

tion

ofM

ortg

age

Bro

kers

;go

vern

men

t-sp

onso

red

ente

rpri

ses;

brok

ers;

ban

kers

;co

nsu

ltan

ts;

anal

ysts

MB

AA

;N

atio

nal

Ass

ocia

tion

ofM

ortg

age

Bro

kers

;br

oker

s;ba

nke

rs;

S&

Lex

ecu

tive

s;co

nsu

ltan

ts

MB

AA

;N

atio

nal

Ass

ocia

tion

ofM

ortg

age

Bro

kers

;br

oker

s;ba

nke

rs;

con

sult

ants

;H

UD

;te

chn

olog

yp

rovi

der

s

MB

AA

;N

atio

nal

Ass

ocia

tion

ofM

ortg

age

Bro

kers

;br

oker

s;ba

nke

rs;

con

sult

ants

;te

chn

olog

yp

rovi

der

sP

ubl

icre

cord

sIn

du

stry

pu

blic

atio

ns

onm

ortg

age

ban

kin

g(L

eder

man

,19

85,

1995

;O

’Don

nel

&D

ivn

ey,

1994

)an

don

brok

erse

gmen

t(e

.g.,

LaM

alfa

,19

90,

1998

;P

rop

per

&F

uri

no,

1994

)

Art

icle

son

chan

ges

inth

ese

ctor

(e.g

.,Ja

cobs

,19

93);

ind

ust

ryp

ubl

icat

ion

son

brok

er/b

anke

rre

lati

ons

(Gar

rett

,19

89,

1993

;L

aMal

fa,

1998

;W

iser

&L

aMal

fa,

1991

)

Ind

ust

ryp

ubl

icat

ion

son

auto

mat

ion

and

brok

erag

e(F

oste

r,19

97;

Leb

owit

z,19

95;

Sch

nei

der

,19

94);

anal

yst

rep

orts

(Mor

gan

Sta

nle

yD

ean

Wit

ter,

2000

)

Ind

ust

ryp

ubl

icat

ion

son

brok

er-

ban

ker

rela

tion

san

dau

tom

atio

n(F

oste

r,19

97,

Gar

rett

,19

89;

Pro

pp

er&

Fu

rin

o,19

94;

Mor

gan

Sta

nle

yD

ean

Wit

ter,

2000

);in

du

stry

man

ual

s(e

.g.,

Led

erm

an,

1985

,19

95)

Ep

isod

e3:

Ser

vici

ng

righ

tsm

ark

etE

vid

ence

,st

age

1;V

alid

atio

n,

stag

es1

&2

Evi

den

ce,

stag

e1;

Val

idat

ion

:N

osi

gnif

ican

tsu

pp

ort

Evi

den

ce,

stag

e1;

Val

idat

ion

,st

age

2E

vid

ence

,st

age

1;V

alid

atio

n,

stag

e2

Inte

rvie

ws

MB

AA

;H

UD

;ba

nke

rs;

con

sult

ants

;an

alys

tsM

BA

A;

ban

kers

;an

alys

tsM

BA

A;

ban

kers

;M

ortg

age

Ele

ctro

nic

Reg

istr

atio

nS

yste

mex

ecu

tive

s;co

nsu

ltan

ts

MB

AA

;N

atio

nal

Ass

ocia

tion

ofM

ortg

age

Bro

kers

;br

oker

s;ba

nke

rs;

con

sult

ants

(wea

ksu

pp

ort)

Pu

blic

reco

rds

An

alys

tre

por

ts;

arti

cles

onse

rvic

ing

(O’D

onn

el&

Div

ney

,19

94;

Wis

er&

LaM

alfa

,19

91)

Art

icle

son

ind

ust

ryu

nbu

nd

lin

g(G

arre

tt,

1993

)A

rtic

les

onse

rvic

ing

mar

ket

evol

uti

on(e

.g.,

Mar

a,19

89;

Wis

er&

LaM

alfa

,19

91)

No

dat

a

a“B

anke

rs”

are

mor

tgag

eba

nke

rs;“

brok

ers”

are

mor

tgag

ebr

oker

s;an

d“a

nal

ysts

”ar

ein

vest

men

tba

nk

anal

ysts

.MB

AA

isth

eM

ortg

age

Ban

kers

Ass

ocia

tion

ofA

mer

ica;

HU

Dis

the

U.S

.Dep

artm

ent

ofH

ousi

ng

and

Urb

anD

evel

opm

ent,

wh

ich

incl

ud

esth

eO

ffic

eof

Fed

eral

Hou

sin

gE

nte

rpri

seO

vers

igh

t(O

FH

EO

).In

terv

iew

sw

ere

wit

hem

plo

yees

ofth

ese

vari

ous

agen

cies

.b

Th

est

age

ofth

ere

sear

chin

wh

ich

init

iale

vid

ence

was

fou

nd

isn

oted

,an

dth

est

age

atw

hic

hva

lid

atio

nw

asob

tain

ed.S

tage

1w

asa

5-m

onth

per

iod

ofex

plo

rin

gm

ortg

age

ban

kin

g,an

dst

age

2w

asa

15-m

onth

per

iod

ofm

app

ing

the

pro

cess

esof

inte

rest

.Fin

ally

,sta

ge3

enta

iled

pre

sen

tin

gth

ere

sult

sto

ind

ust

ryp

arti

cip

ants

and

fin

aliz

ing

the

stu

dy

afer

rece

ivin

gfe

edba

ck.

the market emerges when two necessary conditionsare met: On the one hand, when coordination alongdifferent parts of the value chain is simplified, astask interdependence is reduced; and on the otherhand, when information becomes standardized—that is, when it becomes simple, transmissible, anduniversally understood.

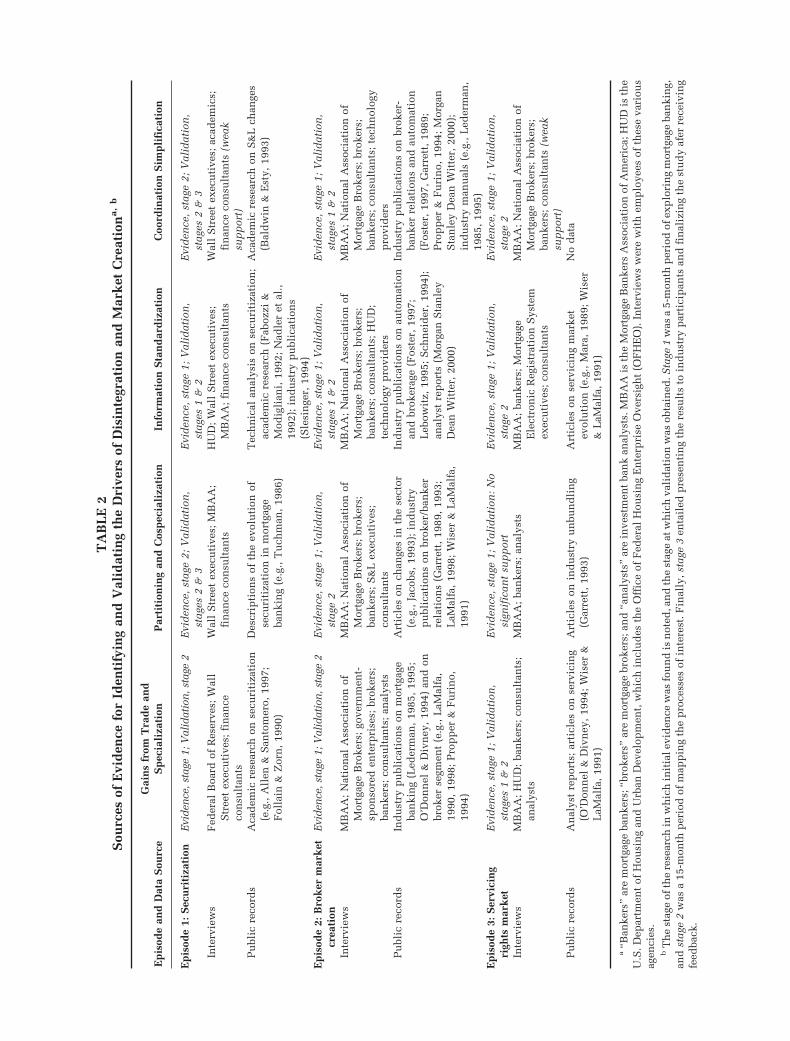

Figure 6 summarizes the argument, and Table 2provides an overview of the process of discovery ofthe different elements of the framework I induced.Table 2 connects the specific factors identified inFigure 6 with the sources used to initially detect orvalidate my analysis, as well as with the researchstage in which I found the initial evidence for, andthen the validation of, each factor. In the remainderof this section, I consider each of the induced fac-tors, starting from the analysis of the necessaryconditions; I then move to the discussion of theenabling processes; and I finally look at what mo-tivates the process of vertical disintegration. Interms of Figure 6, I move from the top to the bot-tom, at each stage going deeper in the chain ofcausation. I thus gradually shift the focus of theanalysis from the question of how vertical disinte-gration happens, to why it happens.

Necessary Conditions: CoordinationSimplification and Information Standardization

Coordination simplification: Evidence. In allthree episodes, the market only emerged after co-ordination was simplified via substantial reductionin task interdependence between the differentstages of the production of mortgage loans (cf.Thompson, 1967). First, securitization became pos-sible when holding a loan did not have to interferewith originating or servicing that loan. Second, thecreation of a separate segment of originating bro-kers became possible when the production andwarehousing of loans became sequentially—ratherthan reciprocally—interdependent. Third, the mar-ket for servicing rights, which enabled servicingand origination to be separated, arose when origi-nation and servicing ceased to have tightconnections.

Securitization, or the separation of the owner-ship of an asset from its origination and servicing,would not have been possible without the arrange-ments that enabled each of the parts to operate inisolation from the others. The key to making secu-ritization work was to create a structure in whichmortgagors would not know who really ownedtheir loans; they would be dealing with the mort-gage banks that originated them. Indeed, many ofthe readers of this paper may not know that theirmortgages are really held by a smattering of finan-

cial institutions around the globe. Likewise, own-ers of the assets do not have any idea of the specificdetails of the loans they own. More important, thesecuritizers do not have to coordinate with themortgage banks on anything more than receivingthe payments from the loans at the prespecifiedintervals; the obligations, in case of foreclosure, arewell defined ex ante; there is no need for any com-munication about the loans among the originator/servicer, securitizer, and owner (Follain & Zorn,1990). Consider loan foreclosure: Securitizationonly became possible when an effective arrange-ment was made that gave mortgage banks an incen-tive to execute unsupervised, effective foreclo-sures, and the holders of the assets (the ultimateloan holders who had the securitized loans) did nothave to worry about when or how foreclosurewould actually occur.8 Such an effective arrange-ment was formalized in the U.S. Universal Com-mercial Code, Article 9. Without a structure to min-imize the requisite coordination among all theseparties, vertical disintegration would have beenvery difficult.

In the creation of the banker-broker market, sim-plification of coordination was also evident. Beforethe mid-1970s, the processes of seeking out cus-tomers and warehousing loans (i.e., preparing themfor sale to the secondary market) were tightly inte-grated, as mortgage banks were keen to originateonly the loans they knew they could sell at a profitto securitizers. From the late 1970s on, however,securitizers introduced optional delivery schemes.These were intended to get business for the securi-tizers offering them, yet they also changed the pro-duction process, as industry handbooks suggest(Lederman, 1985, 1995). As an executive I inter-viewed explained:

What you had to avoid [in the old days] was to bestuck with product the market would not want, be-cause you would have to kill it [incur a loss whenselling or use valuable and scarce capital if holdingit on your books]. On the other hand, if you had anagreed delivery [of closed loans, to an investor], youhad to procure all these loans. . . . The result wasthat you were on the heels of your production guysto fill your quotas. It would distort your pricing, and

8 If a loan was called within its first year and docu-mentation was not foolproof, the securitizer had the rightto force the mortgage bank to buy the loan back. Also,parties further up the value chain evaluated mortgagebanks on the quality of the loans they sold: the pricesthey obtained depended on the overall performance oftheir portfolios over time. Finally, mortgage banks borethe costs of foreclosure, which were fairly high, so theywanted to avoid bad loans.

2005 479Jacobides

you’d have to ensure they were delivering what youwanted or had agreed to. . . . Now with flexibledelivery, you could set your sales guys loose, pro-vided they knew what were the limits they had. Itwas easier to manage, and you could also use leadscoming from outside. It made your life easier as youcould focus separately on each piece of the businesswithout worrying about the other.

Such innovations decreased the coupling be-tween origination and warehousing by reducinginteractions between the two tasks. If a mortgagebanker produced more loans than anticipated, thecompany need not worry about not being able tosell them to an investor; the flexible arrangementsalleviated this concern. Thus, a part of the com-pany could just focus on origination without hav-ing to worry about the next step in the valuechain—in other words, interdependence becamesequential (Thompson, 1967). The availability oflarger and more flexible lines of credit from commer-cial banks had similar effects: it enabled mortgagebankers to construct a buffer between originationand warehousing, reducing task interdependence.

The reduction in coordination difficulties wasfacilitated by changes in information and commu-nication technology (Schneider, 1994). Cheaplyfaxing interest rate sheets en masse every morningto the broker network made real-time loan procure-ment effective; and enterprise information systems(i.e., electronic systems linking banks with outsideagents, brokers, etc.) made it easier for bankers tocoordinate effectively with brokers (Morgan Stan-ley Dean Witter, 2000), especially with the adventof automated underwriting (Foster, 1997), wherebya fixed set of criteria allowed brokers to ensure thatthey could close loans on the behalf of mortgagebankers, and also allowed mortgage bankers toknow that they could sell these loans to securitiz-ers. Managing brokers became only marginallymore complicated than managing the in-house re-tail production network (Lebowitz, 1995). As anexecutive from a mortgage bank put it:

Nowadays you can buy the product as easily fromany source. . . it used to be easier to rely on yourin-house people. . . but nowadays the systems makemanaging the brokers just as easy, so you look to allyour potential channels.

A similar pattern underlay the development ofthe market for servicing rights. In the early days ofthe industry, the activity of servicing a loan waspart and parcel of an integrated process, but in the1980s, the idea of integration started fading away(Garrett, 1993). One reason was that servicing be-came more dependent on computerized systemsthat stored information than on the unarticulated

knowledge of a loan officer in a branch bank thatoriginated a loan (Thinakal, 2001), thus obviatingthe need for integration. As a senior bank vicepresident noted:

Sure, you have these local shops, and they waxlyrical about their being integrated and all. But Ireally don’t see why you should bundle servicingwith origination anymore. I mean, what’s the point?The only value I can see is the emotional link be-tween the customer and the originating bank, interms of cross-selling, and that ain’t high. Perhaps itwas different before, when you didn’t have com-puter systems and the rest of it, but things changedin the 1990s.

Coordination simplification: Theory. The firstcondition that needs to be satisfied for a market toemerge, then, is for the coordination between theadjoining stages of a value chain to be simplified; ifthis does not occur, then it remains impossible forthose completing one stage to turn to an outsideparty to complete the next stage. In the presence ofreciprocal or pooled interdependence (Thompson,1967), it is comparatively hard to enable an activityto be located outside the boundaries of a firm. AsVan de Ven, Delbecq, and Koenig (1976), Nadler,and Tushman (1978), Gulati and Singh (1998), andPuranam and Singh (2000) have demonstrated, ac-tivities that require tight coordination demand theuse of mechanisms that a firm can deploy: commit-tees, meetings, or other authority or coordinationdevices that market-based relations lack, in com-parative terms (Kogut & Zander, 1996; Langlois,2003). Coordination difficulties, then, may be whyRichardson (1972), Teece (1976: 13), and Langloisand Robertson (1989, 1995) argued that integrationis needed to manage a tightly coupled system. Sofor a market to be feasible, interactions along avalue chain must be minimized; production mustbecome modularized (Baldwin & Clark, 2003).

Standardization of information: Evidence. Fordisintegration to occur, however, one more neces-sary condition must be met: Information must be-come standardized—that is, it must become be-come universally understandable and easilyspecified. Information standardization happenedin all three of the market creation episodes.

In the case of securitization, what enabled thesecuritizers to sell loan bundles to the capital mar-kets, and what enabled buyers to raise the capital tobuy them, was that the securitizers standardizedthe information on these loans (Passmore & Sparks,1996). Standardization made it possible for thebuyers to understand what the securitizers wereselling. “Market value was small, that’s whereSalomon Brothers came in. They standardized the

480 JuneAcademy of Management Journal

loans and made them fungible” (an executive ofE. F. Hutton, quoted in Tuchman [1986: 34]).

The information standardization that helpedmake securitization possible had two elements:

The first was standardization of loan characteris-tics; types of loans and their documentation andsupport became homogeneous. The second elementwas standardization of underlying customer cred-itworthiness information: the advent of universallyunderstandable and assessable attributes describingloan applicants and securities (i.e., the mortgage-backed debentures sold through the capital market),and the advent of a language to describe the risk thatloans entailed both to the primary market (the marketfor the mortgage loans that mortgage banks buy frommortgage brokers) and to the secondary market (themarket for securitized mortgage loans, sold by themortgage banks to the securitizers and from thesecuritizers to the capital market). Further detailson these two elements of standardization follow.

First, loan types were standardized. A key ingre-dient of the success in the initial development ofthe market was that “residential mortgages werequite homogeneous in terms of their design, terms,and underwriting standards” (Vandell, 2000: 1). Soa driver for the vertical disintegration process inthis industry was the substantial share of loanswith simpler and more tractable characteristicsthan had been seen in the past—initially, relativelystandardized 15- and 30-year fixed-rate mortgages(Lederman, 1985).

Such product standardization also helped verti-cal disintegration both within the origination pro-cess (addressing the broker-banker split) and be-tween origination and servicing, through themarket for servicing rights. Earlier mortgages hadidiosyncrasies and differing term structures, somoving them from one financial institution to an-other as brokered loans to be warehoused, or trans-ferring their servicing rights, was simply too com-plicated. However, given fixed-rate mortgages withset 15- or 30-year terms, with broadly similar char-acteristics, and given the homogenization withinadjustable-rate mortgages, many of these problemsdisappeared, and specialization became more plau-sible (Aldrich, Greenberg, & Payner, 2001).

The role of standardization in disintegration canalso be inferred from the fact that even today, inte-grated institutions specialize in the more compli-cated adjustable-rate mortgages or other loans withunusual clauses or structures. Because these loansare harder for any financial institution to procurefrom outside brokers, they are produced in-house;their servicing rights are harder to sell to anotherparty, so they are serviced in-house; and finally,they are harder to securitize, so integrated firms