Embed Size (px)

Citation preview

May 2018Introduction

Industry 4.0 / Digitalisering

18.04.18

www.pwc.com/digitalStrictly private and confidential

PwC’s Digital Services

In 2017 we have published over 20 digital pieces; a significant uplift compared to the past couple of years

2

Further, the current pipeline contains >10 pieces

about digital topics we intent to publish this year

Digital Champion – How industry leaders

build operations ecosystems to deliver

end-to-end customer solutions

Global Digital Operations Study 2018

PwC’s Digital Services

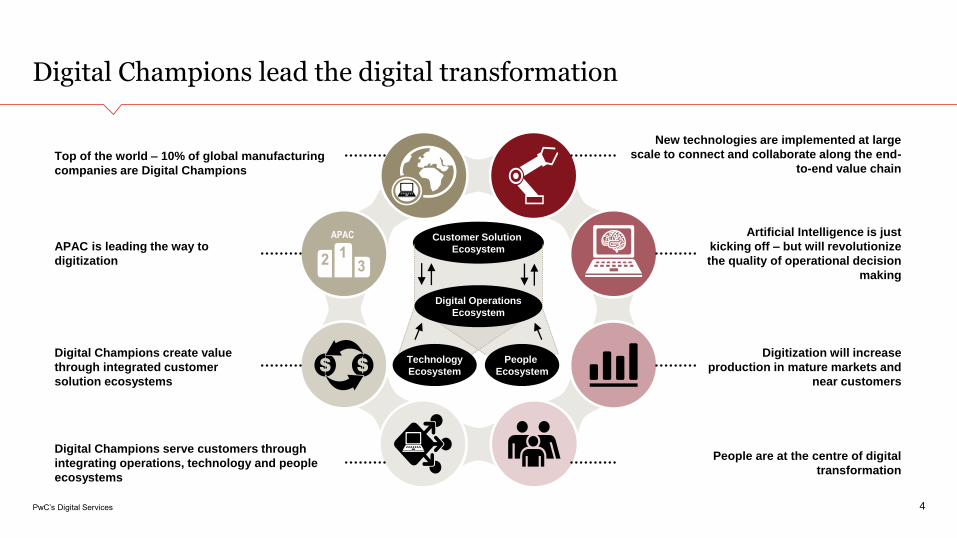

Digital Champions lead the digital transformation

4

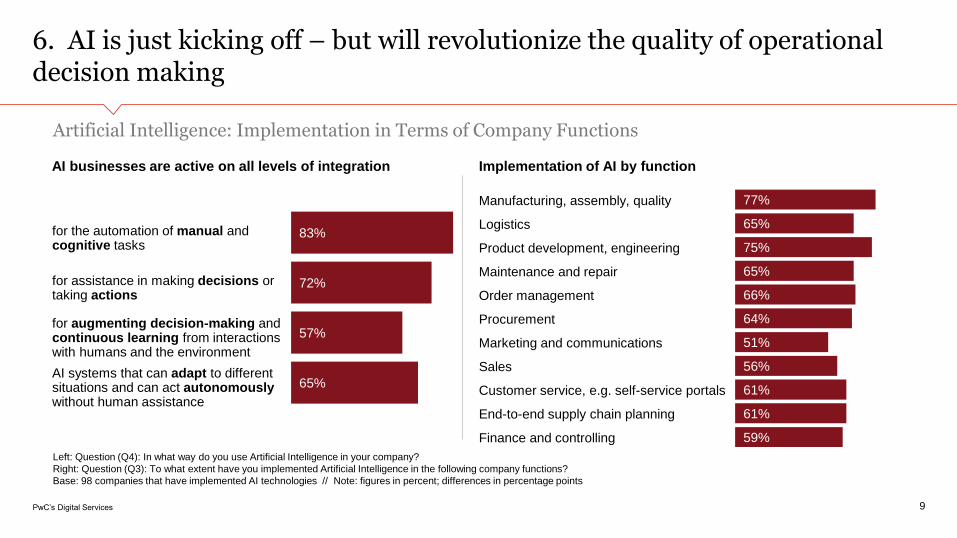

Artificial Intelligence is just

kicking off – but will revolutionize

the quality of operational decision

making

Digitization will increase

production in mature markets and

near customers

People are at the centre of digital

transformation

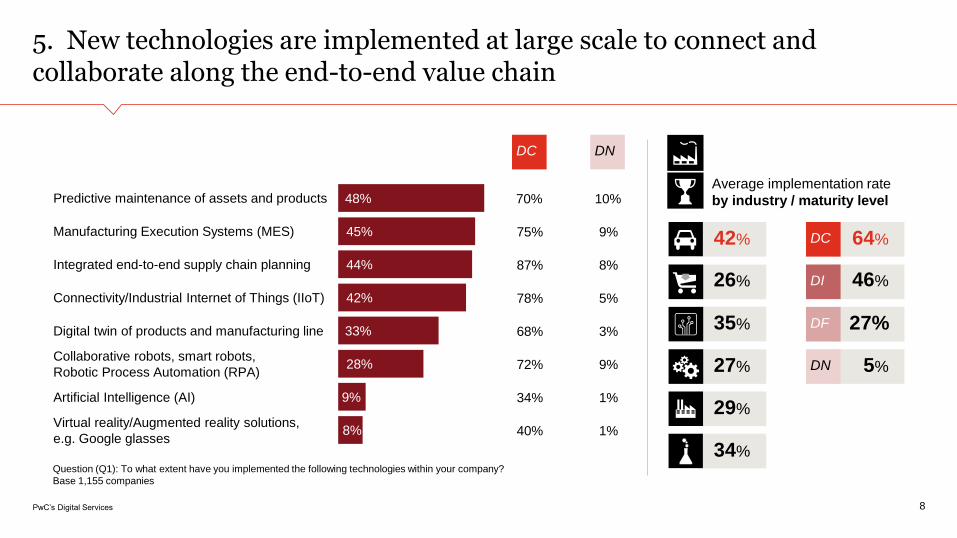

New technologies are implemented at large

scale to connect and collaborate along the end-

to-end value chain

APAC is leading the way to

digitization

Digital Champions create value

through integrated customer

solution ecosystems

Digital Champions serve customers through

integrating operations, technology and people

ecosystems

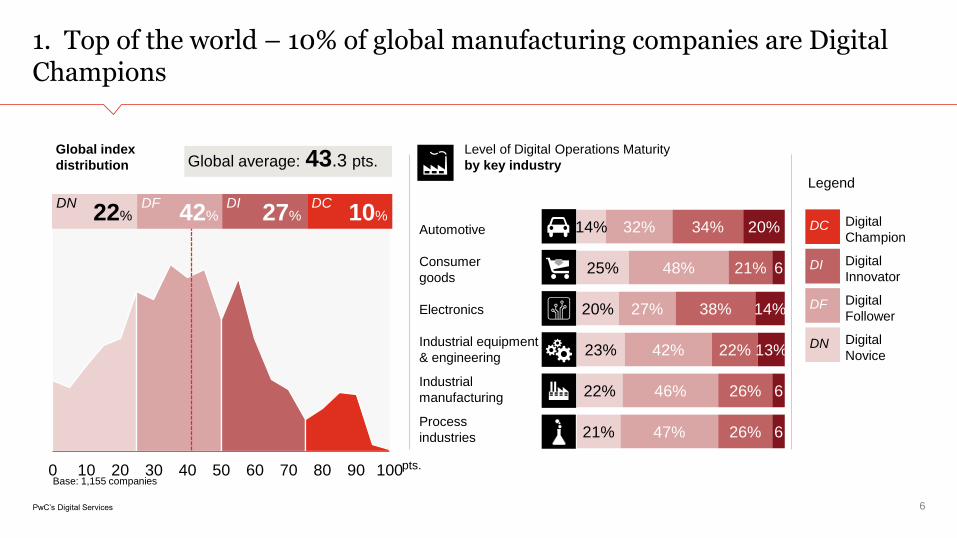

Top of the world – 10% of global manufacturing

companies are Digital Champions

APAC Customer Solution

Ecosystem

Digital Operations

Ecosystem

Technology

Ecosystem

People

Ecosystem

PwC’s Digital Services

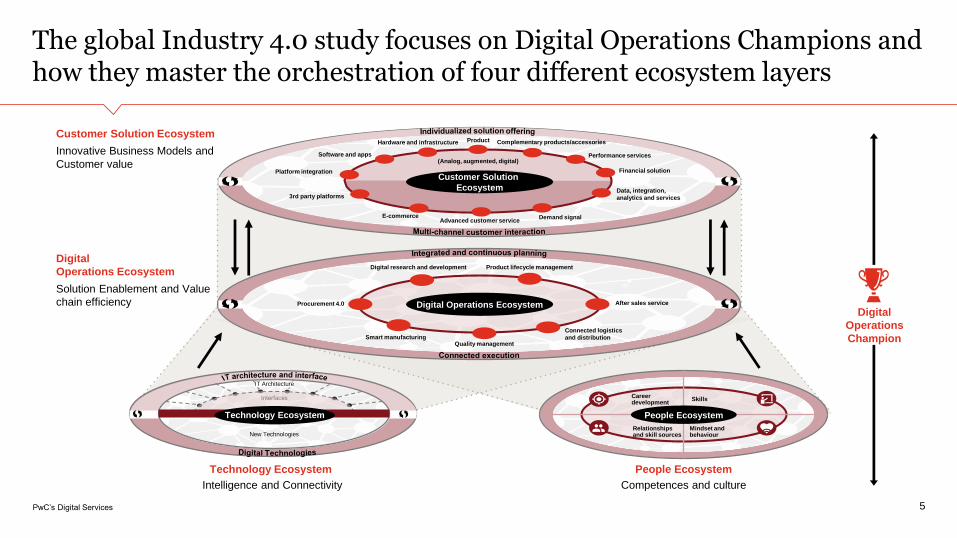

The global Industry 4.0 study focuses on Digital Operations Champions and how they master the orchestration of four different ecosystem layers

5

Digital

Operations

Champion

Interfaces

New Technologies

IT Architecture

Mindset and behaviour

Skills

Relationshipsand skill sources

Careerdevelopment

People Ecosystem

Digital Operations EcosystemProcurement 4.0

Smart manufacturingConnected logistics

and distribution

Digital research and development Product lifecycle management

After sales service

Quality management

Customer Solution

Ecosystem

Platform integration

E-commerce Advanced customer service

Software and apps

Hardware and infrastructure

(Analog, augmented, digital)

Complementary products/accessories

Performance services

Financial solution

3rd party platforms

Demand signal

Data, integration,

analytics and services

Product

Technology Ecosystem

Customer Solution Ecosystem

Innovative Business Models and

Customer value

Digital

Operations Ecosystem

Solution Enablement and Value

chain efficiency

Technology Ecosystem

Intelligence and Connectivity

People Ecosystem

Competences and culture

PwC’s Digital Services

Automotive

Consumer

goods

Electronics

Industrial equipment

& engineering

Industrial

manufacturing

Process

industries

0 10 20 30 40 50 60 70 80 90 100

1. Top of the world – 10% of global manufacturing companies are Digital Champions

6

pts.

Global index

distribution Global average: 43.3 pts.

DN22%

DF42%

DI27%

DC10%

14%

25%

20%

23%

22%

21%

32%

48%

27%

42%

46%

47%

34%

21%

38%

22%

26%

26%

20%

6

14%

13%

6

6

Level of Digital Operations Maturity

by key industry

DC

DI

DF

DN

Legend

Digital

Champion

Digital

Innovator

Digital

Follower

Digital

Novice

Base: 1,155 companies

PwC’s Digital Services

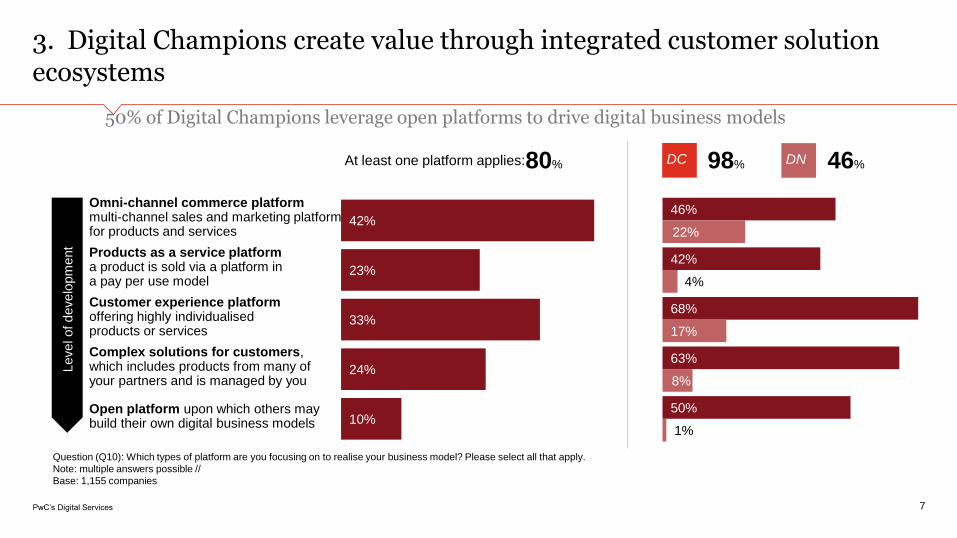

Omni-channel commerce platformmulti-channel sales and marketing platform for products and services

Products as a service platforma product is sold via a platform in a pay per use model

Customer experience platform offering highly individualised products or services

Complex solutions for customers, which includes products from many of your partners and is managed by you

Open platform upon which others may build their own digital business models

3. Digital Champions create value through integrated customer solution ecosystems

7

50% of Digital Champions leverage open platforms to drive digital business models

42%

23%

33%

24%

10%

At least one platform applies: 80%

46%

42%

68%

63%

50%

22%

4%

17%

8%

1%

DC DN98% 46%

Level of develo

pm

ent

Question (Q10): Which types of platform are you focusing on to realise your business model? Please select all that apply.

Note: multiple answers possible //

Base: 1,155 companies

PwC’s Digital Services

Predictive maintenance of assets and products

Manufacturing Execution Systems (MES)

Integrated end-to-end supply chain planning

Connectivity/Industrial Internet of Things (IIoT)

Digital twin of products and manufacturing line

Collaborative robots, smart robots,

Robotic Process Automation (RPA)

Artificial Intelligence (AI)

Virtual reality/Augmented reality solutions,

e.g. Google glasses

48%

45%

44%

42%

33%

28%

9%

8%

5. New technologies are implemented at large scale to connect and collaborate along the end-to-end value chain

8

Average implementation rate

by industry / maturity level

46%

27%

5%

DC

DI

DF

DN

64%

26%

35%

27%

42%

29%

34%

DC DN

70% 10%

75% 9%

87% 8%

78% 5%

68% 3%

72% 9%

34% 1%

40% 1%

Question (Q1): To what extent have you implemented the following technologies within your company?

Base 1,155 companies

PwC’s Digital Services

77%

65%

75%

65%

66%

64%

51%

56%

61%

61%

59%

Manufacturing, assembly, quality

Logistics

Product development, engineering

Maintenance and repair

Order management

Procurement

Marketing and communications

Sales

Customer service, e.g. self-service portals

End-to-end supply chain planning

Finance and controlling

6. AI is just kicking off – but will revolutionize the quality of operational decision making

9

Artificial Intelligence: Implementation in Terms of Company Functions

for the automation of manual and cognitive tasks

for assistance in making decisions or taking actions

for augmenting decision-making and continuous learning from interactions with humans and the environment

AI systems that can adapt to different situations and can act autonomouslywithout human assistance

83%

72%

57%

65%

AI businesses are active on all levels of integration Implementation of AI by function

Left: Question (Q4): In what way do you use Artificial Intelligence in your company?

Right: Question (Q3): To what extent have you implemented Artificial Intelligence in the following company functions?

Base: 98 companies that have implemented AI technologies // Note: figures in percent; differences in percentage points

PwC’s Digital Services

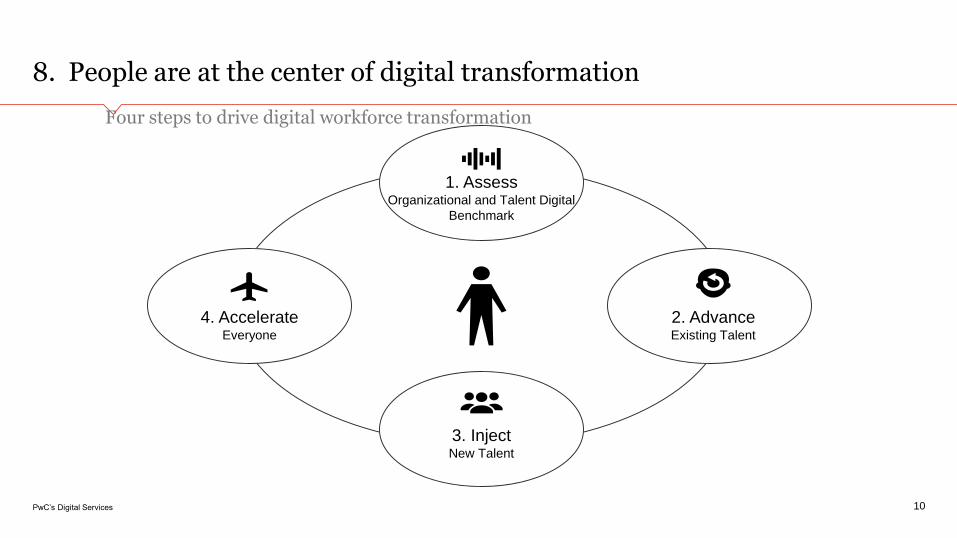

8. People are at the center of digital transformation

10

Four steps to drive digital workforce transformation

4. AccelerateEveryone

1. AssessOrganizational and Talent Digital

Benchmark

2. AdvanceExisting Talent

3. InjectNew Talent

PwC’s Digital Services

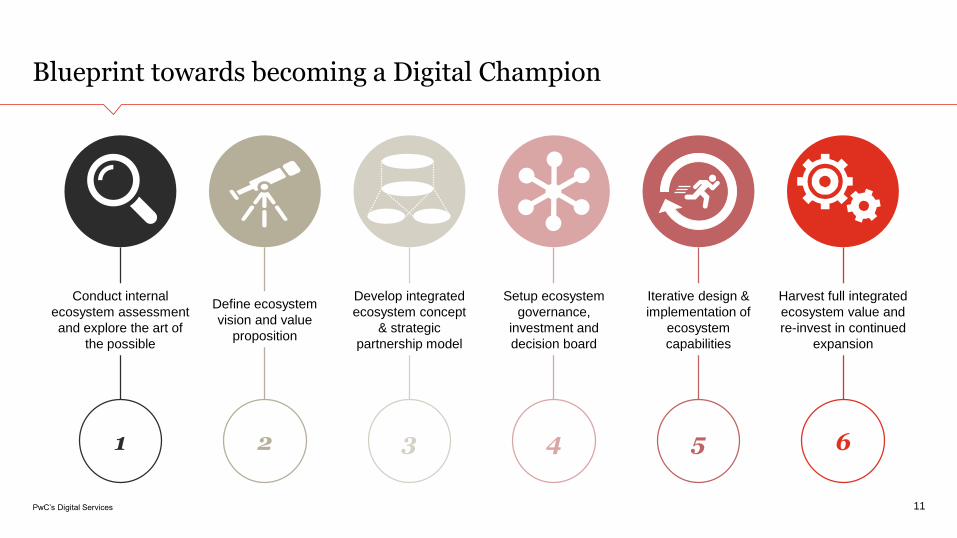

Blueprint towards becoming a Digital Champion

11

4

Setup ecosystem

governance,

investment and

decision board

3

Develop integrated

ecosystem concept

& strategic

partnership model

6

Harvest full integrated

ecosystem value and

re-invest in continued

expansion

1

Conduct internal

ecosystem assessment

and explore the art of

the possible

2

Define ecosystem

vision and value

proposition

5

Iterative design &

implementation of

ecosystem

capabilities

PwC’s Digital Services

Previous study 2016

Confidential information for the sole benefit and use of PwC’s client.

12

02

PwC’s Digital ServicesPwC 13

April 2016

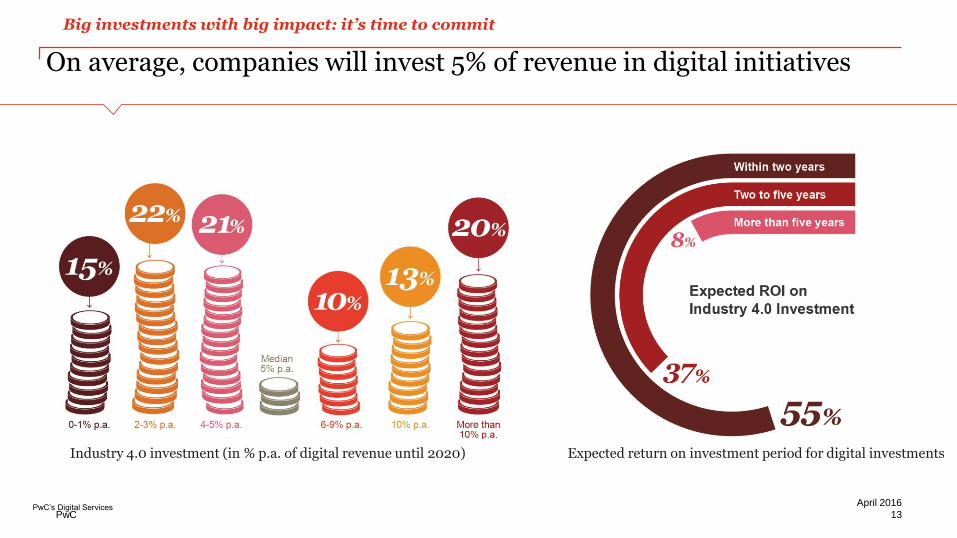

Industry 4.0 investment (in % p.a. of digital revenue until 2020) Expected return on investment period for digital investments

Big investments with big impact: it’s time to commit

On average, companies will invest 5% of revenue in digital initiatives

PwC’s Digital Services

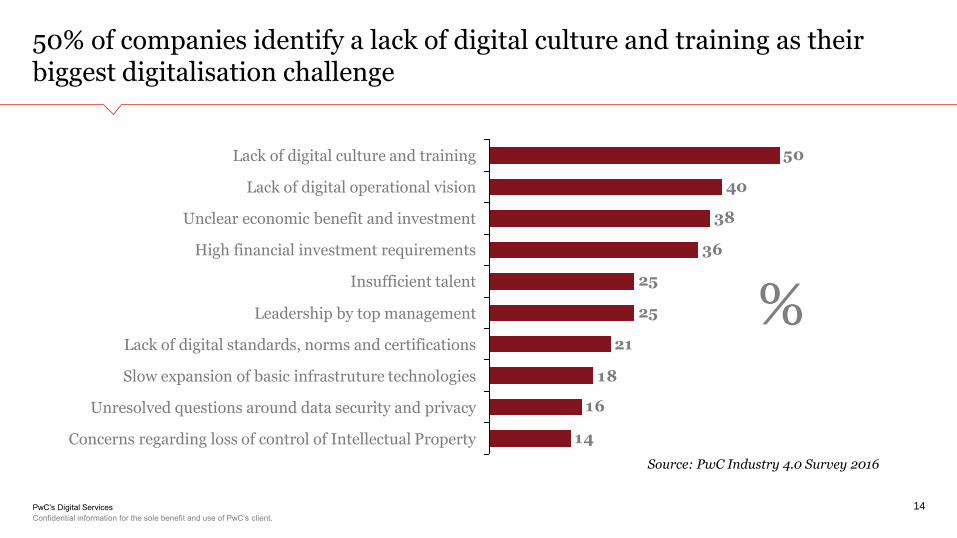

50% of companies identify a lack of digital culture and training as their biggest digitalisation challenge

Confidential information for the sole benefit and use of PwC’s client.

14

Source: PwC Industry 4.0 Survey 2016

14

16

18

21

25

25

36

38

40

50

High financial investment requirements

Unclear economic benefit and investment

Lack of digital operational vision

Lack of digital culture and training

Lack of digital standards, norms and certifications

Leadership by top management

Insufficient talent

Concerns regarding loss of control of Intellectual Property

Unresolved questions around data security and privacy

Slow expansion of basic infrastruture technologies

%

PwC’s Digital Services

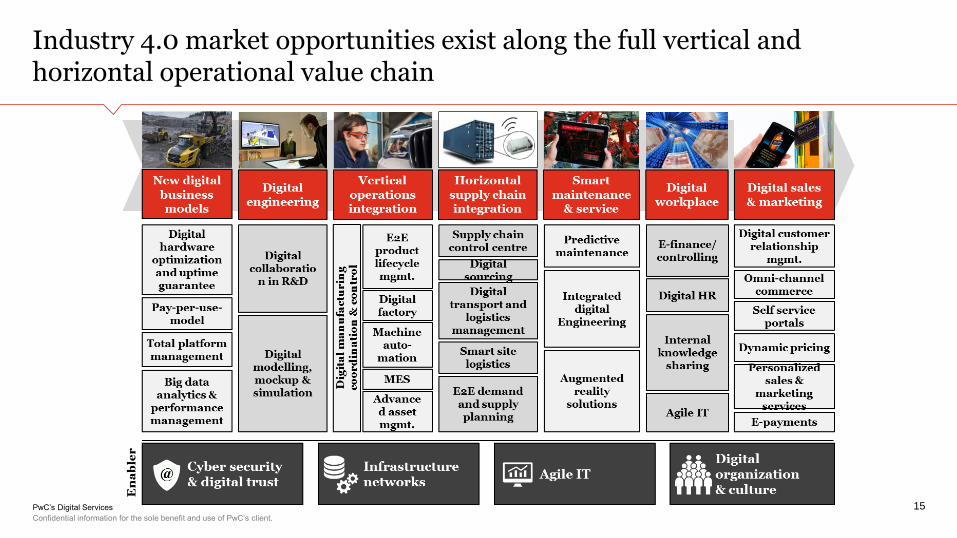

Industry 4.0 market opportunities exist along the full vertical and horizontal operational value chain

Confidential information for the sole benefit and use of PwC’s client.

15

PwC’s Digital Services

PwC ekspert

Confidential information for the sole benefit and use of PwC’s client.

16

Jesper Vedsø

Partner, PwC

Jesper is a partner with PwC’s Consulting group and responsible for digitisation projects in the private sector.

Part of Global Industry 4.0 Leadership.

He is part of the PwC Global group, focusing on helping companies with their digital development. Jesper has vast experience from a wide range of international companies and industries, which enables him to discuss the specific digital possibilities of the individual company. Jesper has also worked extensively with change management which is often part of a digital initiative.

PwC’s Digital Services

End of session Time for Coffee

Confidential information for the sole benefit and use of PwC’s client.

PwC’s Digital ServicesPwC’s Digital Services 17

PwC’s Digital Services

Thank you!

Confidential information for the sole benefit and use of PwC’s client.

© 2015 PwC. All rights reserved. Not for further distribution without the permission of PwC. “PwC” refers to the network of member firms of

PricewaterhouseCoopers International Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Each

member firm is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services

to clients. PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of their

professional judgment or bind them in any way. No member firm is responsible or liable for the acts or omissions of any other member firm

nor can it control the exercise of another member firm’s professional judgment or bind another member firm or PwCIL in any way.

18