Embed Size (px)

Citation preview

Industrial Real Estate Market TrendsA Bearcat Perspective

Kristian Bjorson, SIORInternational DirectorRetail/e-commerce Distribution Practice+1 312 282 [email protected] March, 2014

Discussion agenda

March 14, 2014 1

• My real estate journey• Understanding supply chain drivers• The retail omnichannel evolution• US industrial real estate market forecast• Why (why not) in Cincinnati?

Month 00, 2014 2

CLEVELAND

CINCINNATI

CHICAGO

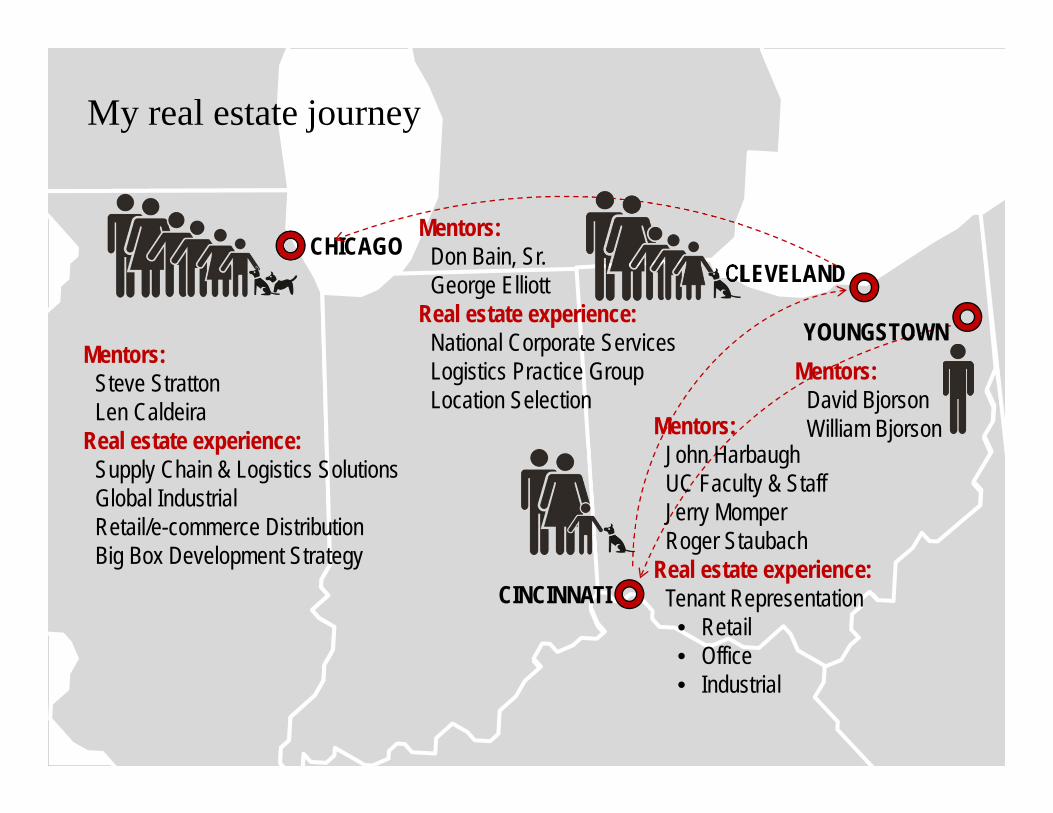

YOUNGSTOWNMentors:

David BjorsonWilliam BjorsonMentors:

John HarbaughUC Faculty & StaffJerry MomperRoger Staubach

Real estate experience:Tenant Representation• Retail• Office• Industrial

Mentors:Don Bain, Sr.George Elliott

Real estate experience:National Corporate ServicesLogistics Practice GroupLocation Selection

Mentors:Steve StrattonLen Caldeira

Real estate experience:Supply Chain & Logistics SolutionsGlobal IndustrialRetail/e-commerce DistributionBig Box Development Strategy

My real estate journey

Loyal to my favorite brands/clients

Month 00, 2014 3

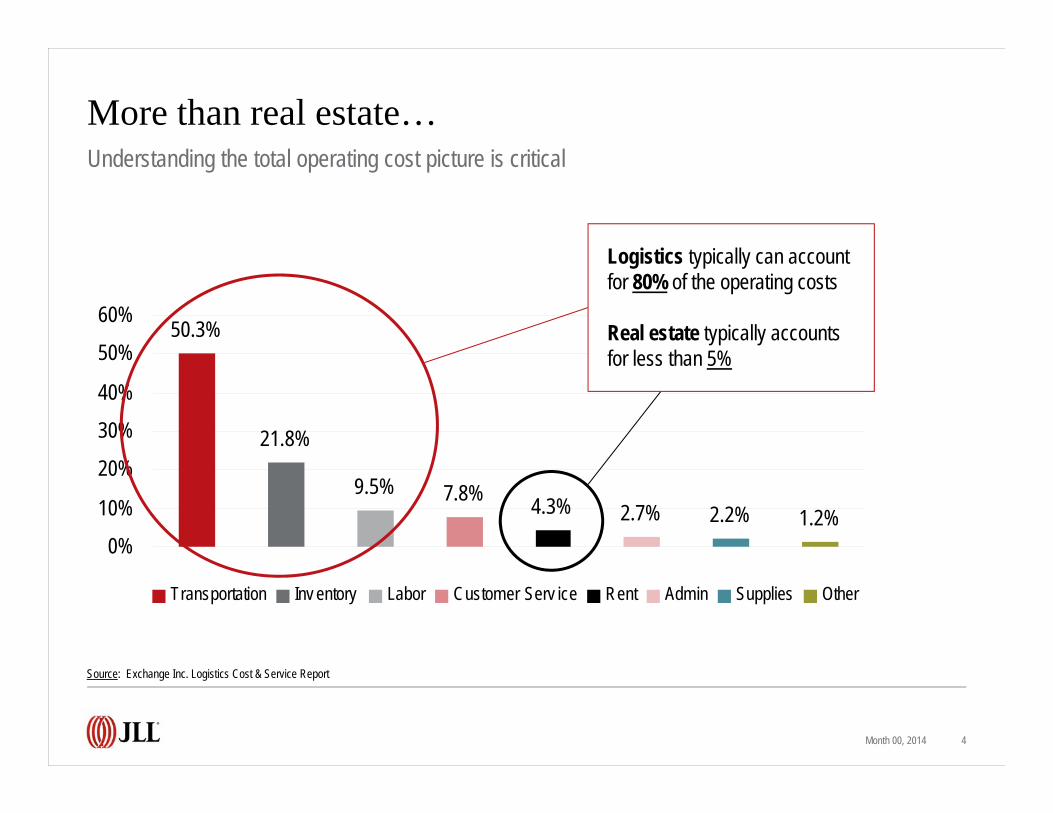

More than real estate…

Month 00, 2014 4

Understanding the total operating cost picture is critical

Source: Exchange Inc. Logistics Cost & Service Report

50.3%

21.8%

9.5% 7.8% 4.3% 2.7% 2.2% 1.2%0%

10%

20%

30%

40%

50%

60%

Transportation Inv entory Labor Customer Serv ice Rent Admin Supplies Other

Logistics typically can account for 80% of the operating costs

Real estate typically accounts for less than 5%

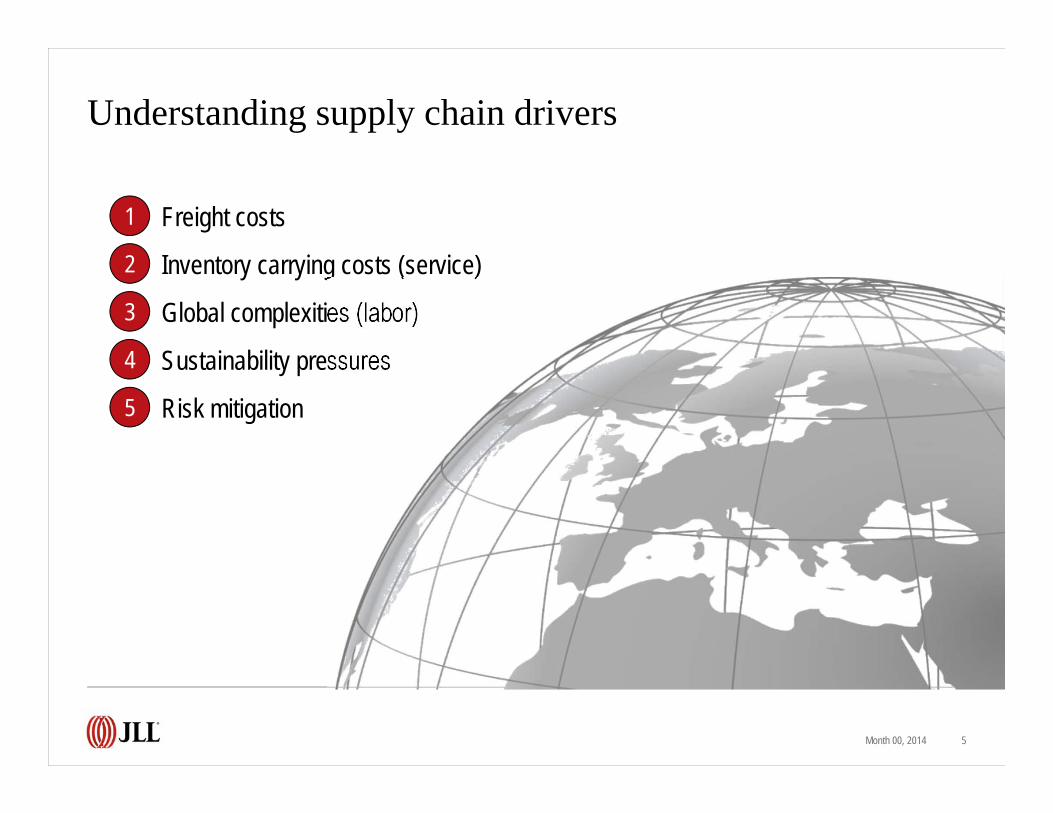

Understanding supply chain drivers

Month 00, 2014 5

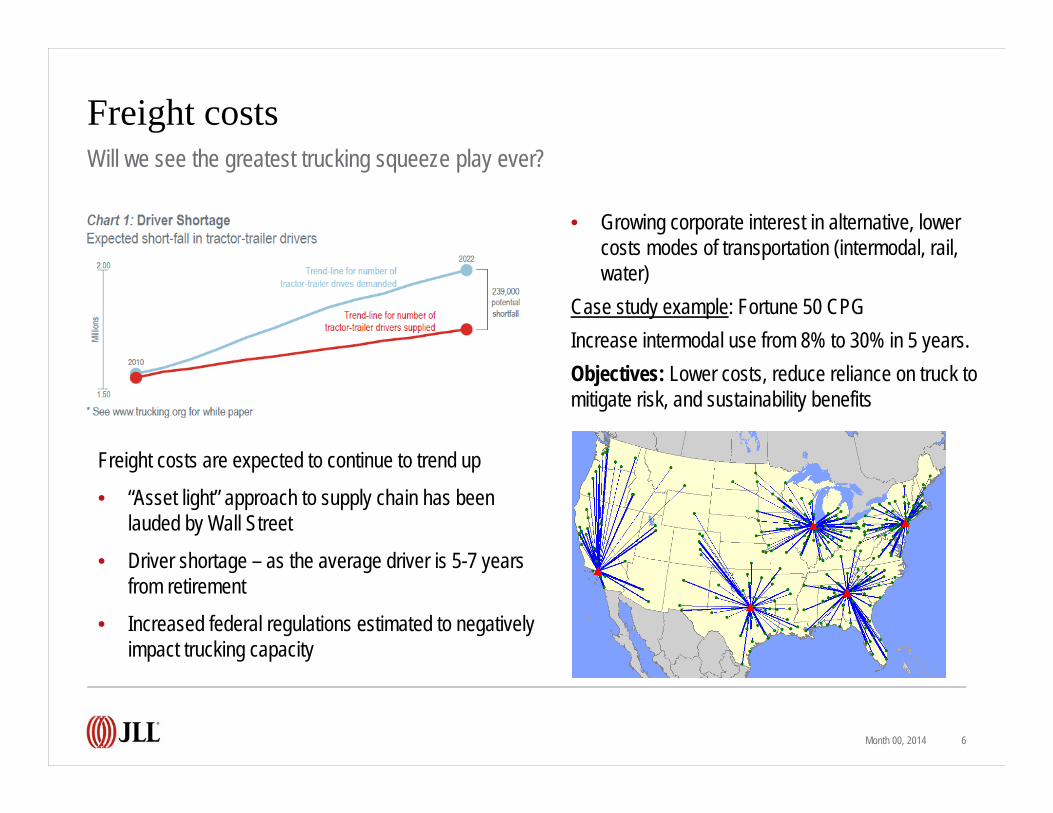

Freight costs

Inventory carrying costs (service)

Global complexities (labor)

Sustainability pressures

Risk mitigation

1

2

3

4

5

Freight costs

Month 00, 2014 6

Will we see the greatest trucking squeeze play ever?

Freight costs are expected to continue to trend up

• “Asset light” approach to supply chain has been lauded by Wall Street

• Driver shortage – as the average driver is 5-7 years from retirement

• Increased federal regulations estimated to negatively impact trucking capacity

• Growing corporate interest in alternative, lower costs modes of transportation (intermodal, rail, water)

Case study example: Fortune 50 CPGIncrease intermodal use from 8% to 30% in 5 years.Objectives: Lower costs, reduce reliance on truck to mitigate risk, and sustainability benefits

Inventory carrying costs (service)

• Continued effort for corporations to “lean out” inventories

• A faster recovering economy will likely result in rising interest rates

• Customers now requiring more strategic positioning of inventories for same-day service

March 14, 2014 7

Can interest rates go any lower than zero?

Global complexities (labor)

• “There will always be a lower cost country. We will no longer chase low-cost labor.” – from CEO of Fortune 10 manufacturer

• China still #1 representing one-third of all off-shoring investments; India #2; Eastern Europe #3

• Chinese wages rising an average of 15-20% per year due to demand/supply imbalance for skilled labor

• Expect greater corporate focus on the cost to service trade-offs and considerations (nearshoring)

Month 00, 2014 8

The only constant is “change”

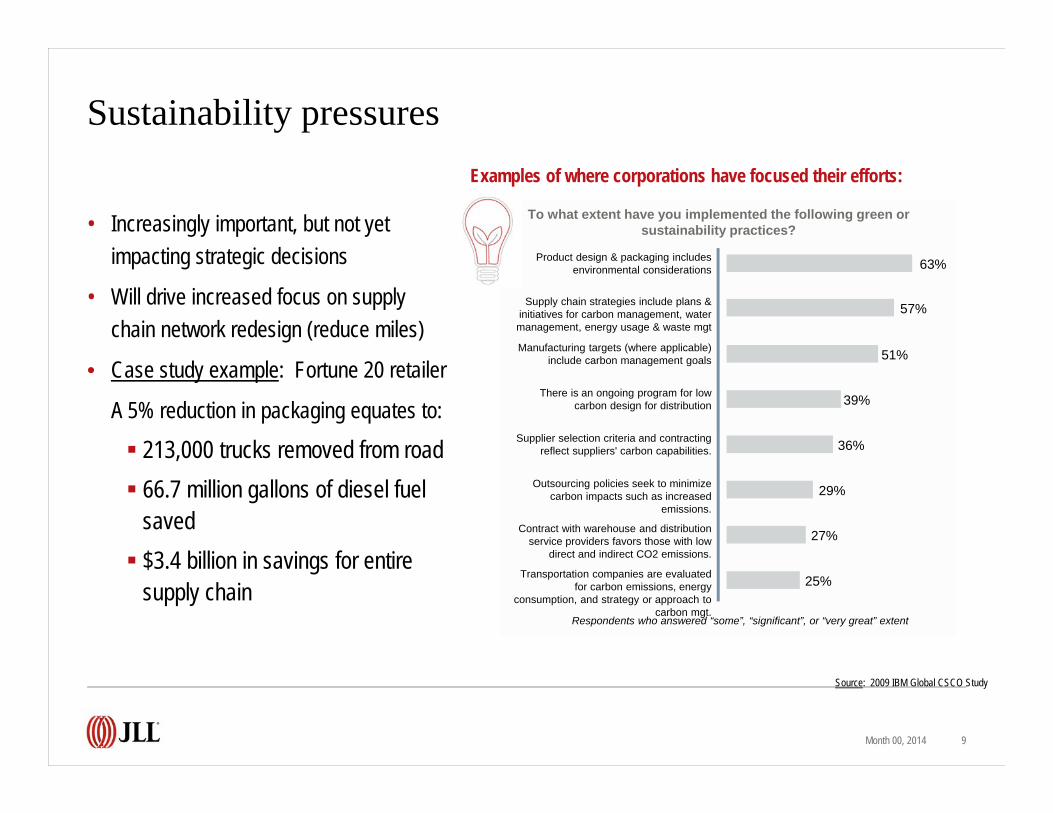

Sustainability pressures

• Increasingly important, but not yet impacting strategic decisions

• Will drive increased focus on supply chain network redesign (reduce miles)

• Case study example: Fortune 20 retailer

A 5% reduction in packaging equates to:

213,000 trucks removed from road 66.7 million gallons of diesel fuel

saved $3.4 billion in savings for entire

supply chain

Month 00, 2014 9

To what extent have you implemented the following green or sustainability practices?

Transportation companies are evaluated for carbon emissions, energy

consumption, and strategy or approach to carbon mgt.

Contract with warehouse and distribution service providers favors those with low

direct and indirect CO2 emissions.

Outsourcing policies seek to minimize carbon impacts such as increased

emissions.

Supplier selection criteria and contracting reflect suppliers' carbon capabilities.

There is an ongoing program for low carbon design for distribution

Manufacturing targets (where applicable) include carbon management goals

Supply chain strategies include plans & initiatives for carbon management, water management, energy usage & waste mgt

Product design & packaging includes environmental considerations

Respondents who answered “some”, “significant”, or “very great” extent

25%

27%

29%

36%

39%

51%

57%

63%

Source: 2009 IBM Global CSCO Study

Examples of where corporations have focused their efforts:

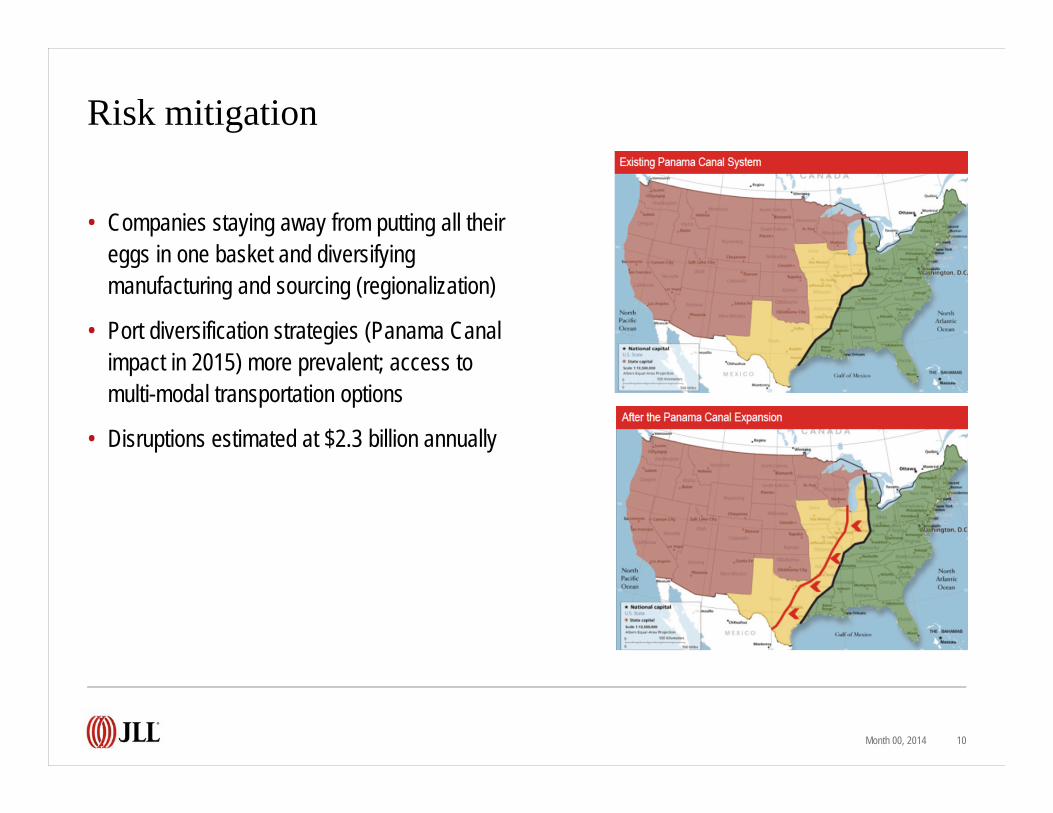

Risk mitigation

Month 00, 2014 10

• Companies staying away from putting all their eggs in one basket and diversifying manufacturing and sourcing (regionalization)

• Port diversification strategies (Panama Canal impact in 2015) more prevalent; access to multi-modal transportation options

• Disruptions estimated at $2.3 billion annually

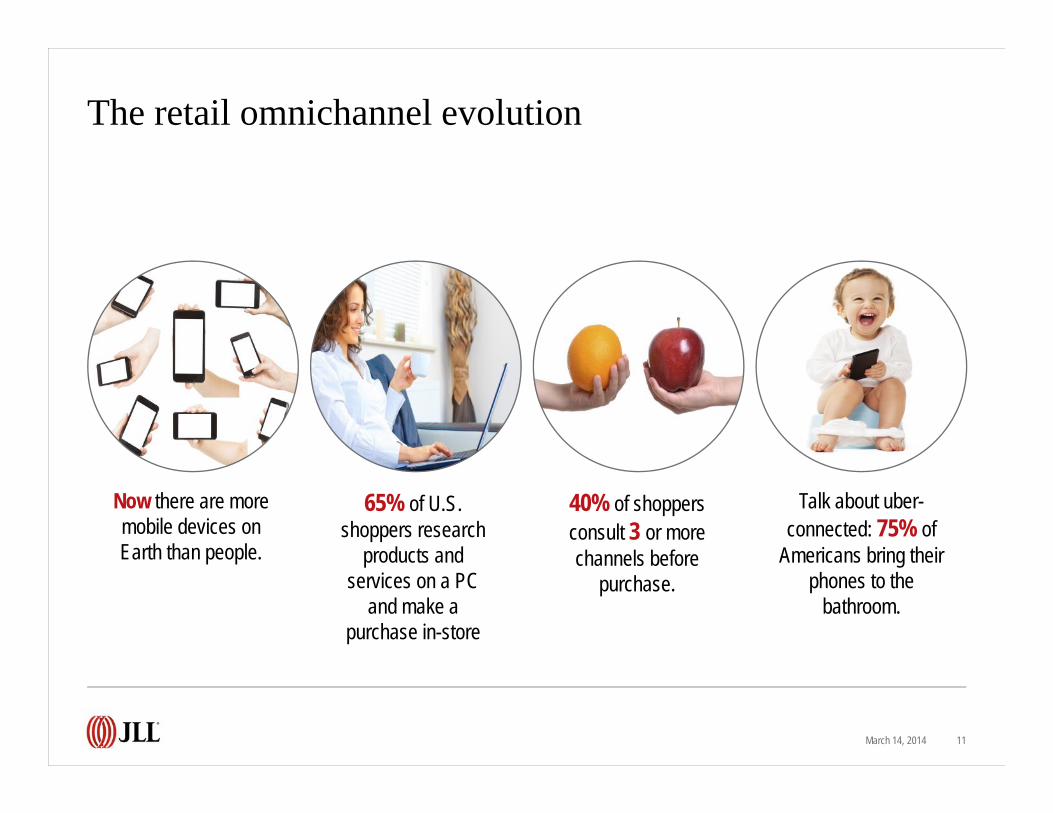

The retail omnichannel evolution

March 14, 2014 11

Now there are more mobile devices on Earth than people.

65% of U.S. shoppers research

products and services on a PC

and make a purchase in-store

40% of shoppers consult 3 or more channels before

purchase.

Talk about uber-connected: 75% of

Americans bring their phones to the

bathroom.

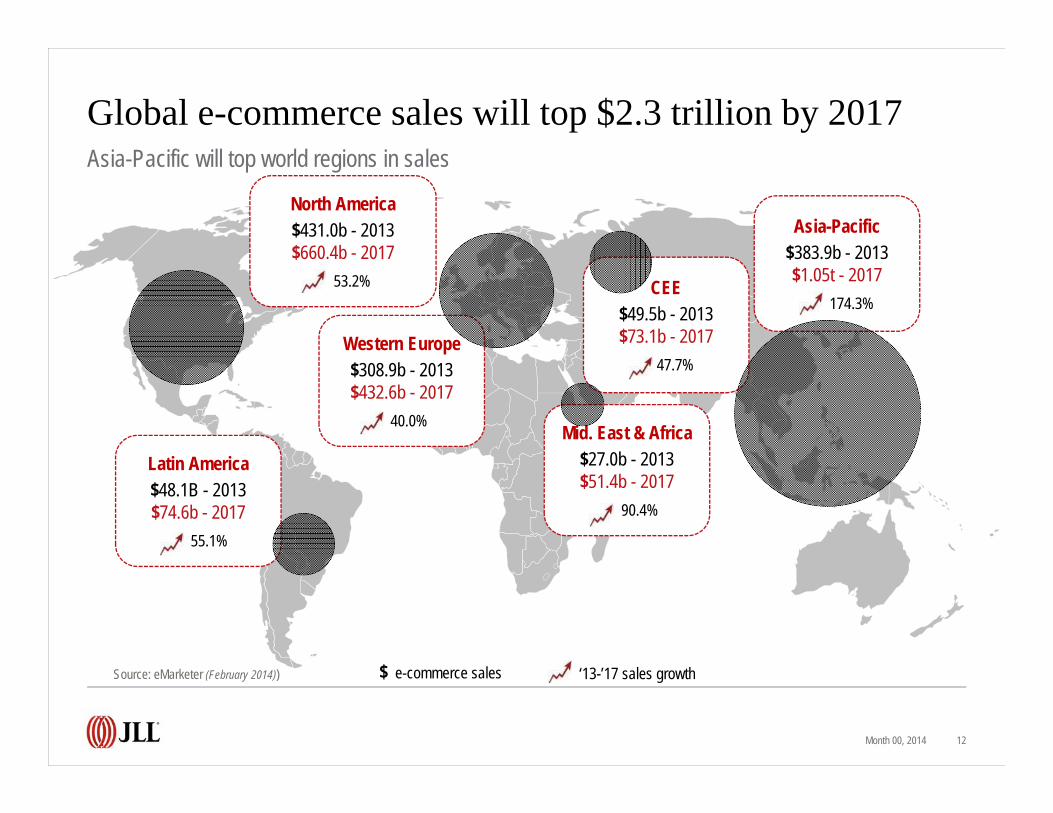

Global e-commerce sales will top $2.3 trillion by 2017

Month 00, 2014 12

Asia-Pacific will top world regions in sales

Western Europe$308.9b - 2013$432.6b - 2017

40.0% Mid. East & Africa$27.0b - 2013$51.4b - 2017

90.4%

Asia-Pacific$383.9b - 2013$1.05t - 2017

174.3%CEE

$49.5b - 2013$73.1b - 2017

47.7%

Latin America$48.1B - 2013$74.6b - 2017

55.1%

North America$431.0b - 2013$660.4b - 2017

53.2%

Source: eMarketer (February 2014)) $ e-commerce sales ‘13-’17 sales growth

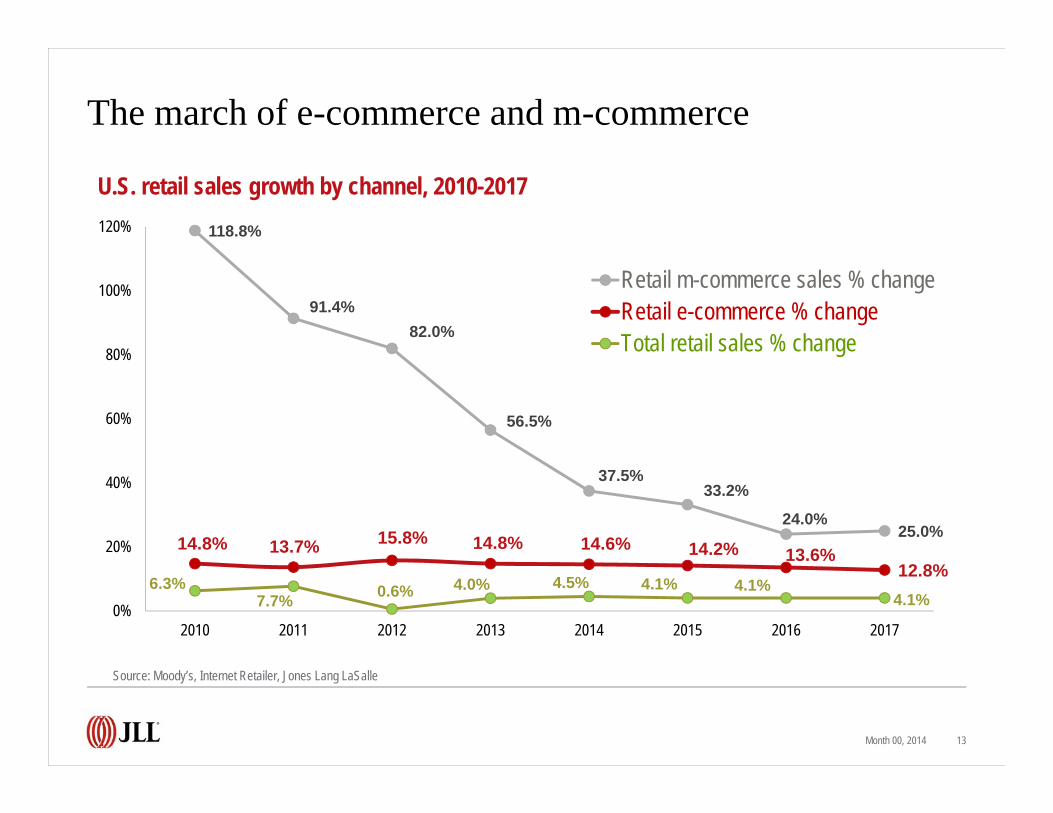

The march of e-commerce and m-commerce

Month 00, 2014 13

118.8%

91.4%82.0%

56.5%

37.5%33.2%

24.0%25.0%

14.8% 13.7% 15.8% 14.8% 14.6% 14.2% 13.6%12.8%

6.3%7.7% 0.6% 4.0% 4.5% 4.1% 4.1%

4.1%0%

20%

40%

60%

80%

100%

120%

2010 2011 2012 2013 2014 2015 2016 2017

Retail m-commerce sales % changeRetail e-commerce % changeTotal retail sales % change

U.S. retail sales growth by channel, 2010-2017

Source: Moody’s, Internet Retailer, Jones Lang LaSalle

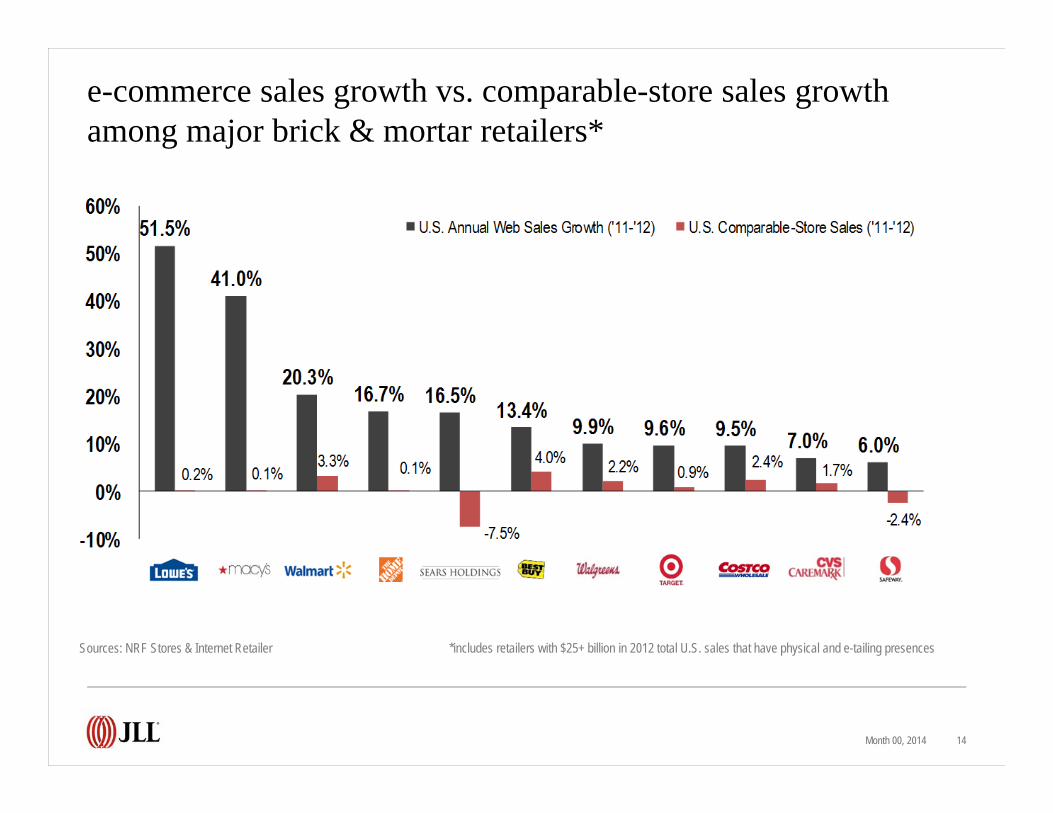

e-commerce sales growth vs. comparable-store sales growthamong major brick & mortar retailers*

Month 00, 2014 14

*includes retailers with $25+ billion in 2012 total U.S. sales that have physical and e-tailing presencesSources: NRF Stores & Internet Retailer

Evolving technology continues to reshape:

1. What consumers expect and demand from their shopping experience

2. Consumers’ awareness of their options3. How consumers make decisions about

how, what, when and where they buy4. How retailers are balancing consumer

demands with their own capabilities and objectives (aka the “consumer” promise”)

5. Where retailers place distribution, e-fulfillment and urban logistics centers, their relative sizes, the SKU’s in them and their overall supply chain network

Month 00, 2014 15

Month 00, 2014 16

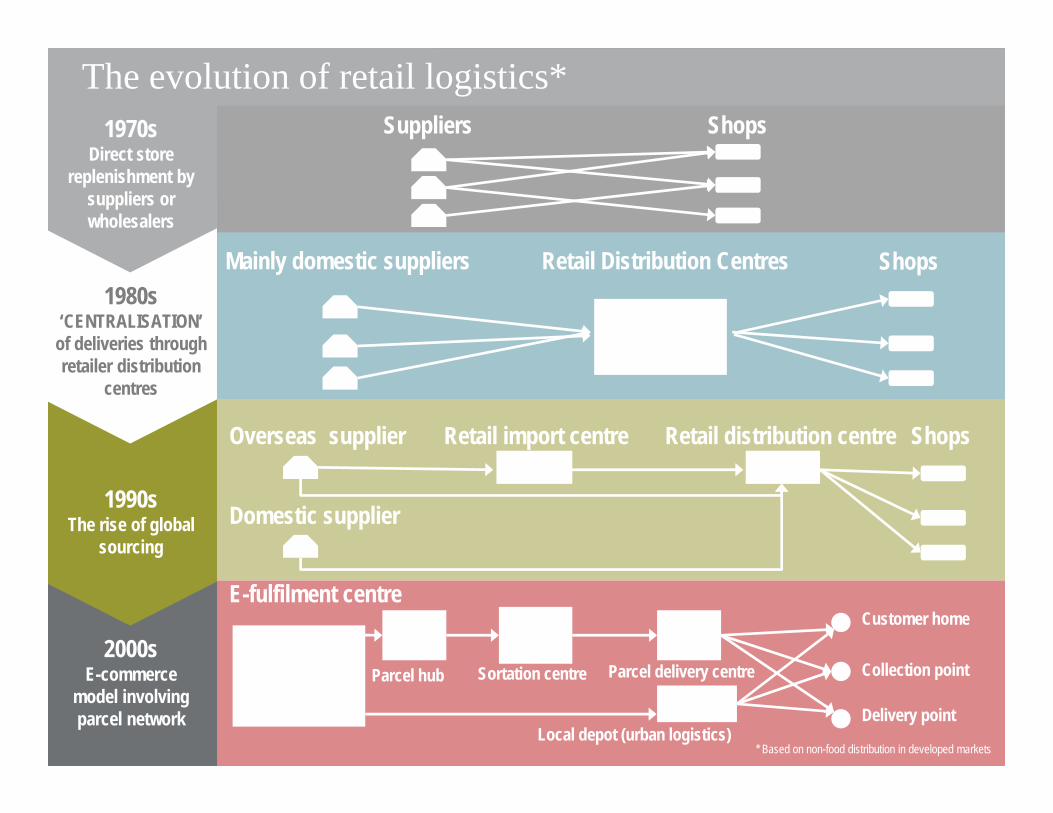

2000sE-commerce

model involving parcel network

1990sThe rise of global

sourcing

The evolution of retail logistics*

1980s‘CENTRALISATION’of deliveries through retailer distribution

centres

1970sDirect store

replenishment by suppliers or wholesalers

Suppliers Shops

Mainly domestic suppliers

Overseas supplier

Retail Distribution Centres

Domestic supplier

Retail import centre

Shops

ShopsRetail distribution centre

E-fulfilment centre

Parcel hub Parcel delivery centreSortation centre

Customer home

Collection point

Delivery point

* Based on non-food distribution in developed marketsLocal depot (urban logistics)

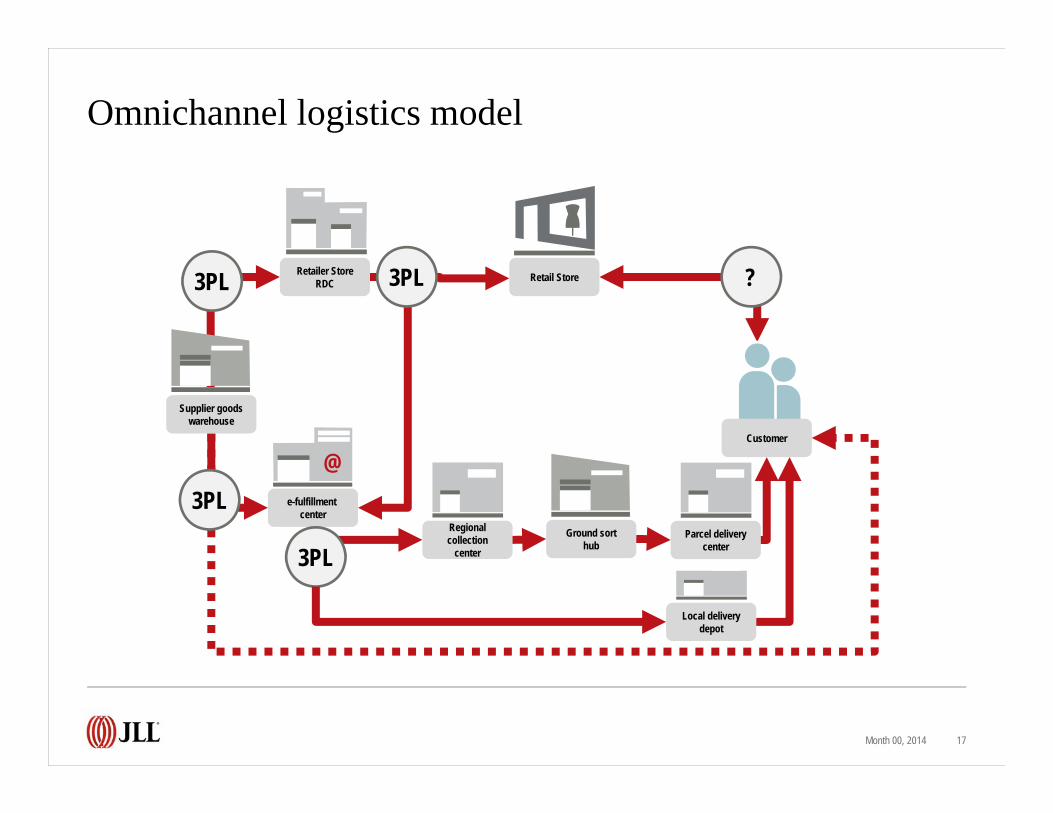

Omnichannel logistics model

Month 00, 2014 17

Parcel delivery center

Ground sort hub

Regional collection

center

Retailer Store RDC Retail Store

@e-fulfillment

center

Supplier goods warehouse

3PL

3PL

3PL 3PL ?

Customer

Local delivery depot

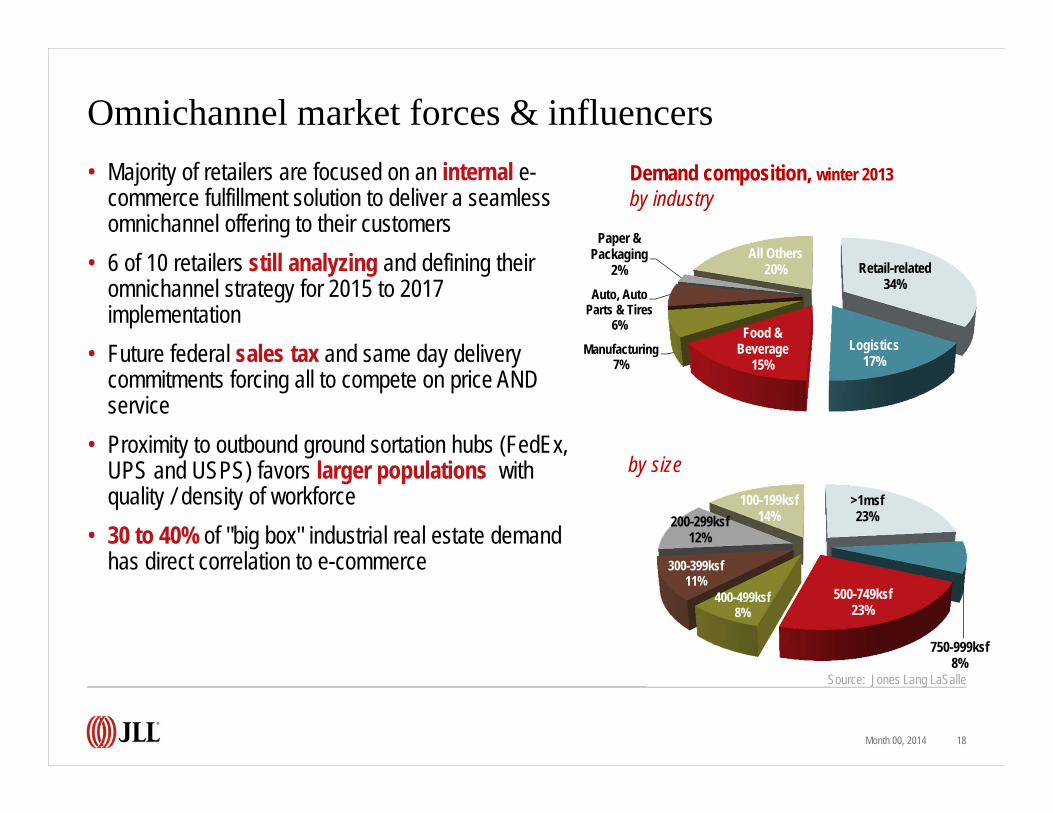

Omnichannel market forces & influencers• Majority of retailers are focused on an internal e-

commerce fulfillment solution to deliver a seamless omnichannel offering to their customers

• 6 of 10 retailers still analyzing and defining their omnichannel strategy for 2015 to 2017 implementation

• Future federal sales tax and same day delivery commitments forcing all to compete on price AND service

• Proximity to outbound ground sortation hubs (FedEx, UPS and USPS) favors larger populations with quality / density of workforce

• 30 to 40% of "big box" industrial real estate demand has direct correlation to e-commerce

Month 00, 2014 18

Retail-related34%

Logistics17%

Food & Beverage

15%Manufacturing

7%

Auto, Auto Parts & Tires

6%

Paper & Packaging

2%All Others

20%

>1msf23%

750-999ksf8%

500-749ksf23%

400-499ksf8%

300-399ksf11%

200-299ksf12%

100-199ksf14%

Demand composition, winter 2013by industry

by size

Source: Jones Lang LaSalle

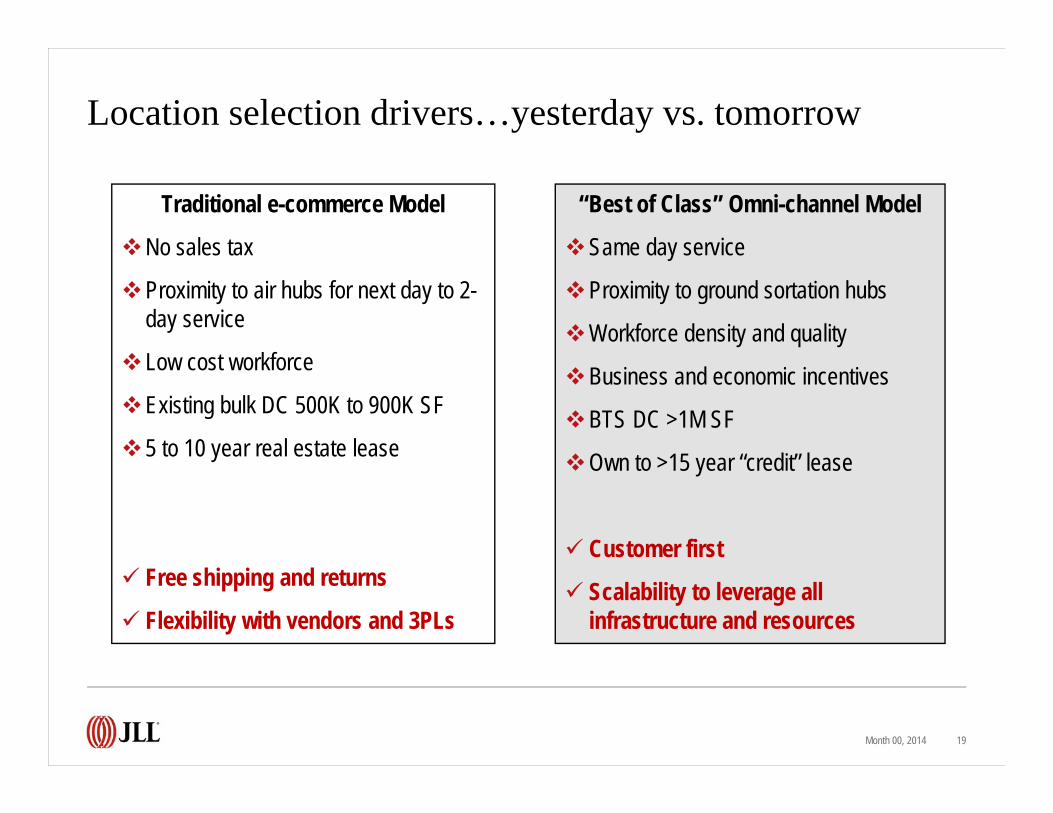

Location selection drivers…yesterday vs. tomorrow

Month 00, 2014 19

Traditional e-commerce Model

No sales tax

Proximity to air hubs for next day to 2-day service

Low cost workforce

Existing bulk DC 500K to 900K SF

5 to 10 year real estate lease

Free shipping and returns

Flexibility with vendors and 3PLs

“Best of Class” Omni-channel Model

Same day service

Proximity to ground sortation hubs

Workforce density and quality

Business and economic incentives

BTS DC >1M SF

Own to >15 year “credit” lease

Customer first

Scalability to leverage all infrastructure and resources

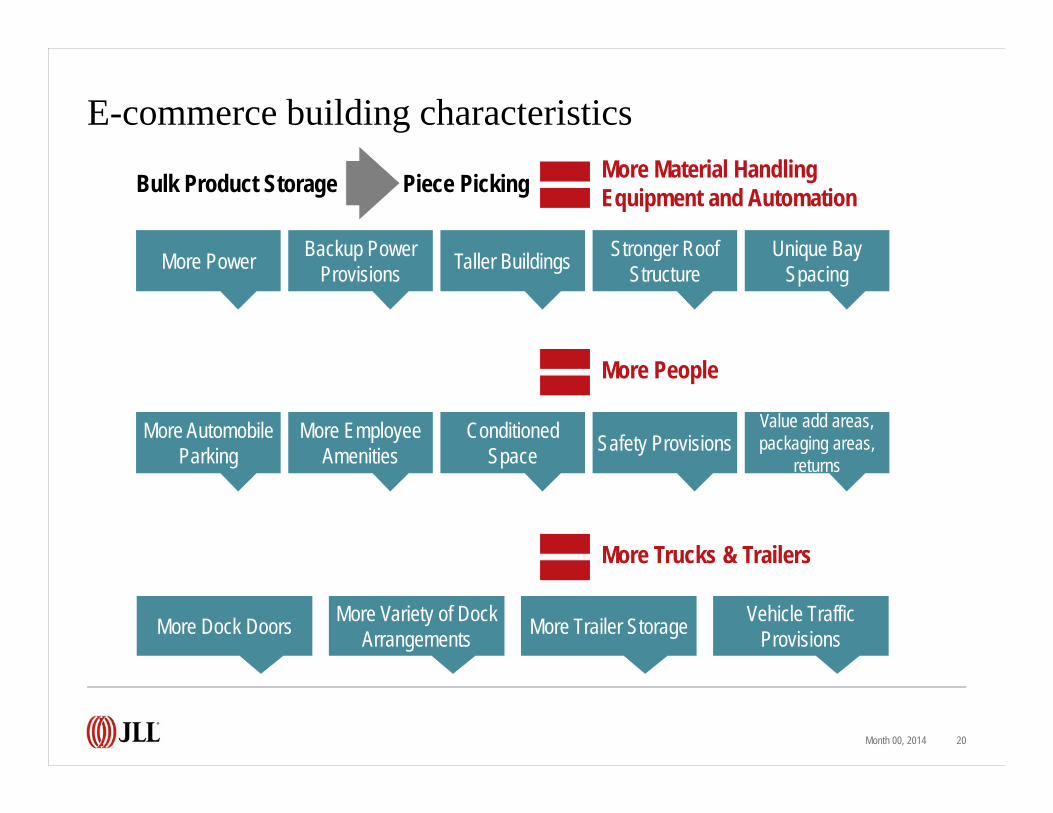

E-commerce building characteristics

Month 00, 2014 20

Bulk Product Storage Piece Picking More Material Handling Equipment and Automation

More People

More Trucks & Trailers

More Power Backup Power Provisions Taller Buildings Stronger Roof

StructureUnique Bay

Spacing

More Automobile Parking

More Employee Amenities

Conditioned Space Safety Provisions

Value add areas, packaging areas,

returns

More Dock Doors More Variety of Dock Arrangements More Trailer Storage Vehicle Traffic

Provisions

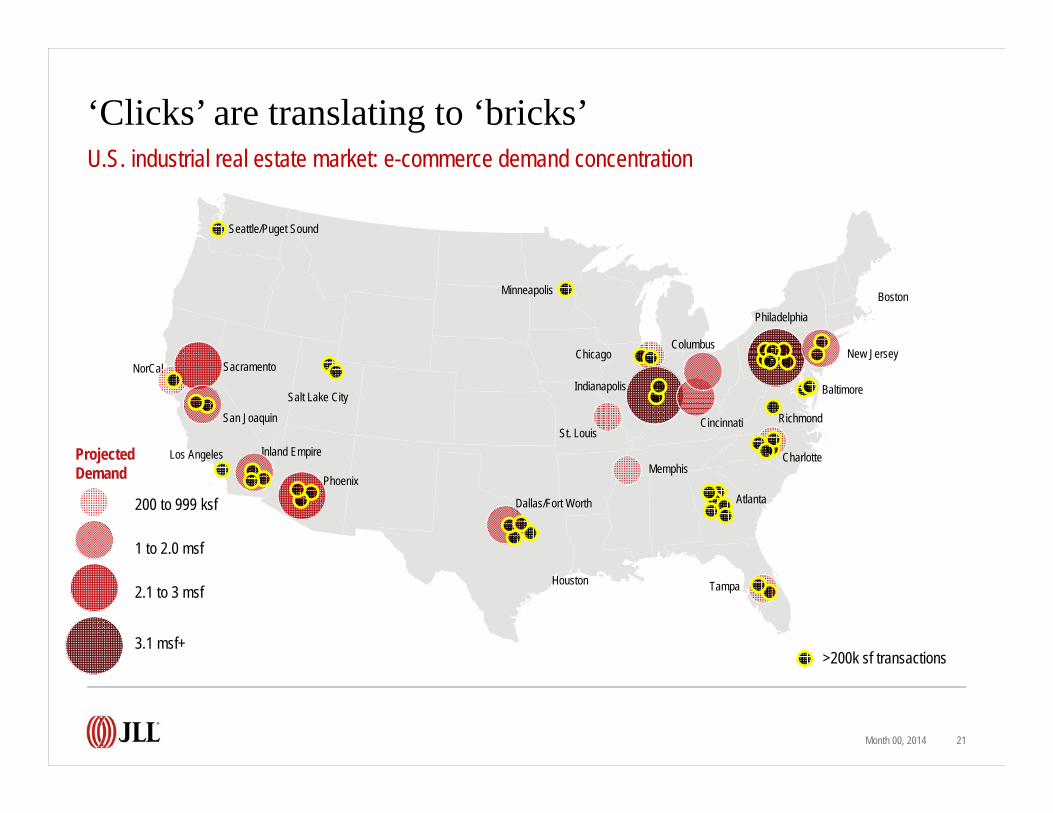

‘Clicks’ are translating to ‘bricks’

Month 00, 2014 21

U.S. industrial real estate market: e-commerce demand concentration

Baltimore

New Jersey

Philadelphia

St. Louis

NorCal

Phoenix

Dallas/Fort Worth

Memphis

ColumbusChicago

Indianapolis

Tampa

Seattle/Puget Sound

Cincinnati

Salt Lake City

Sacramento

San Joaquin

Inland Empire

Houston

Atlanta

Los Angeles

Minneapolis

>200k sf transactions

Charlotte

Richmond

Boston

2.1 to 3 msf

200 to 999 ksf

1 to 2.0 msf

3.1 msf+

Projected Demand

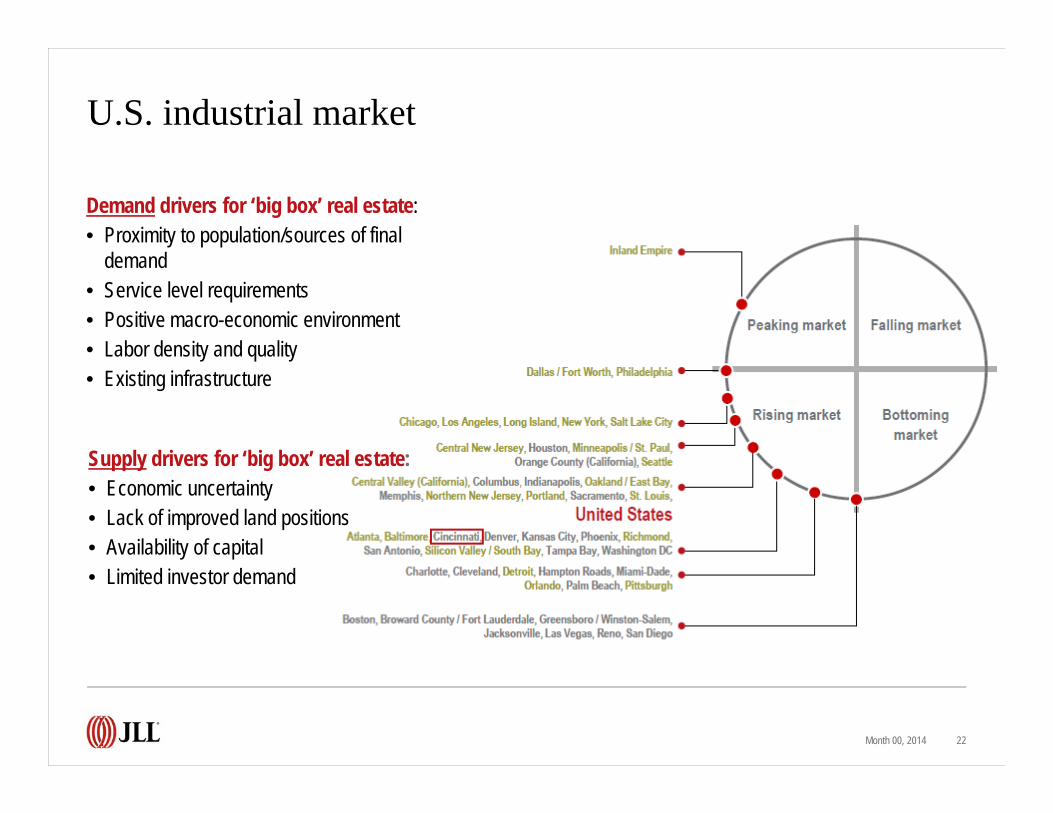

U.S. industrial market

Month 00, 2014 22

Demand drivers for ‘big box’ real estate:• Proximity to population/sources of final

demand• Service level requirements• Positive macro-economic environment• Labor density and quality• Existing infrastructure

Supply drivers for ‘big box’ real estate:• Economic uncertainty• Lack of improved land positions• Availability of capital• Limited investor demand

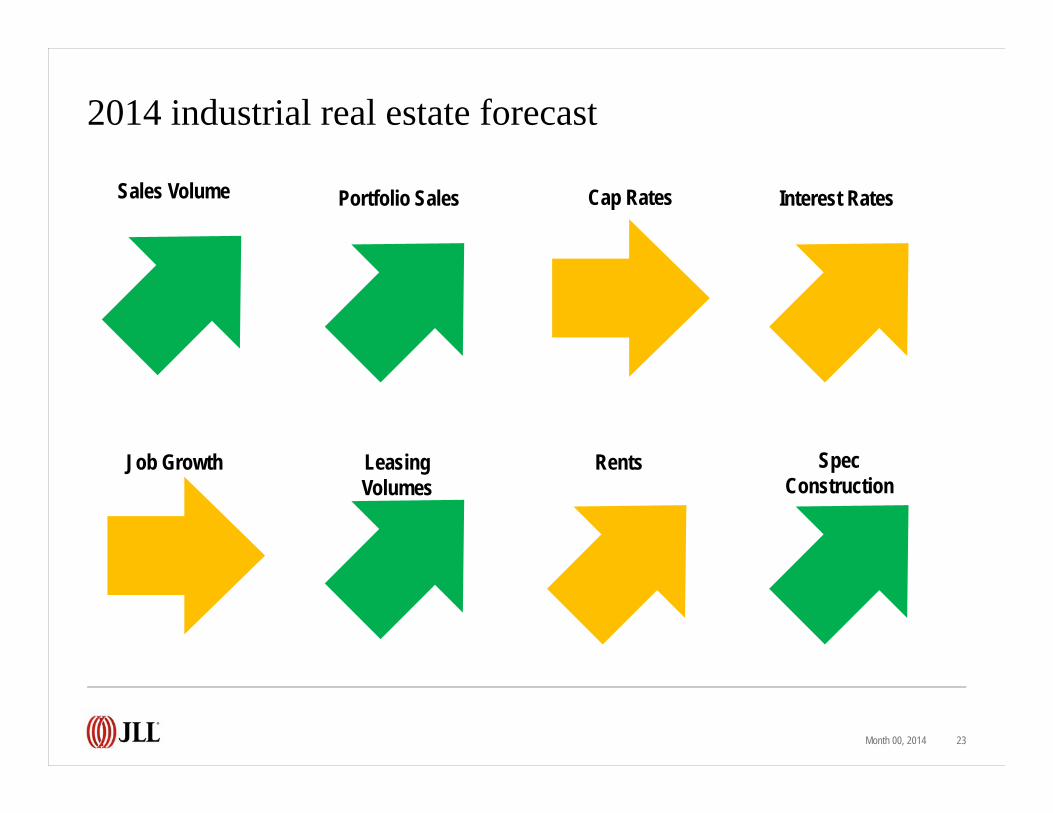

2014 industrial real estate forecast

Month 00, 2014 23

Sales Volume Portfolio Sales Cap Rates Interest Rates

Spec Construction

Job Growth Leasing Volumes

Rents

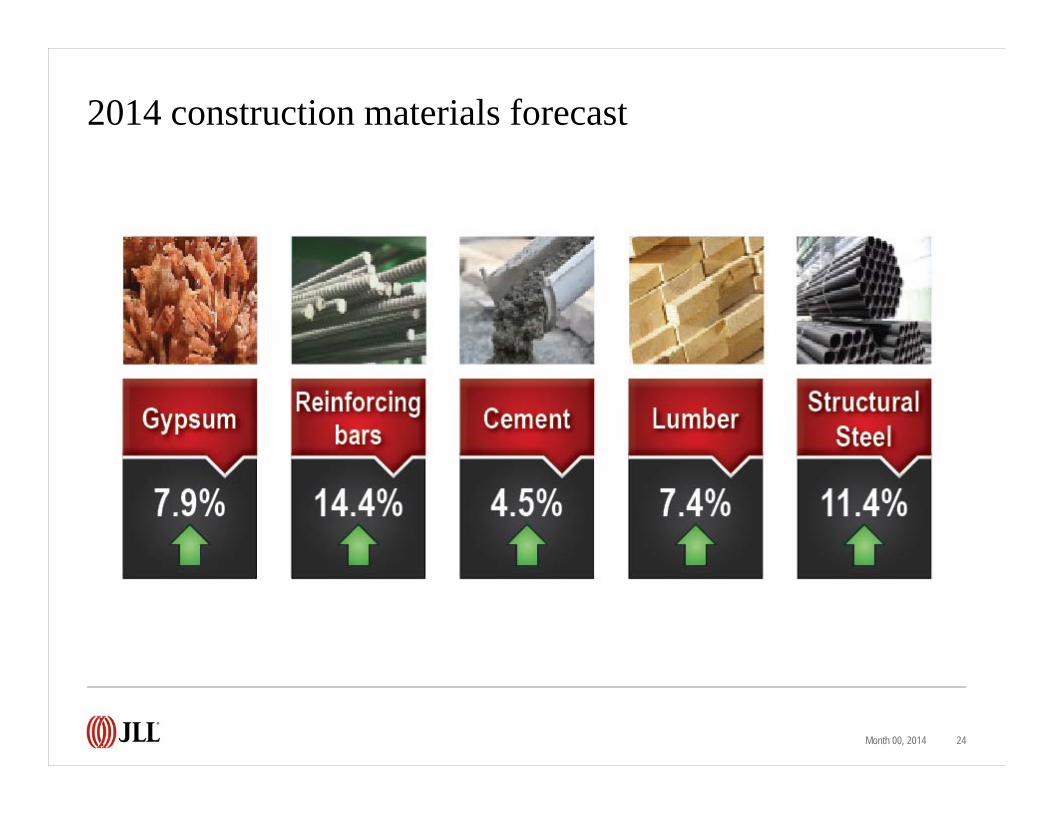

2014 construction materials forecast

Month 00, 2014 24

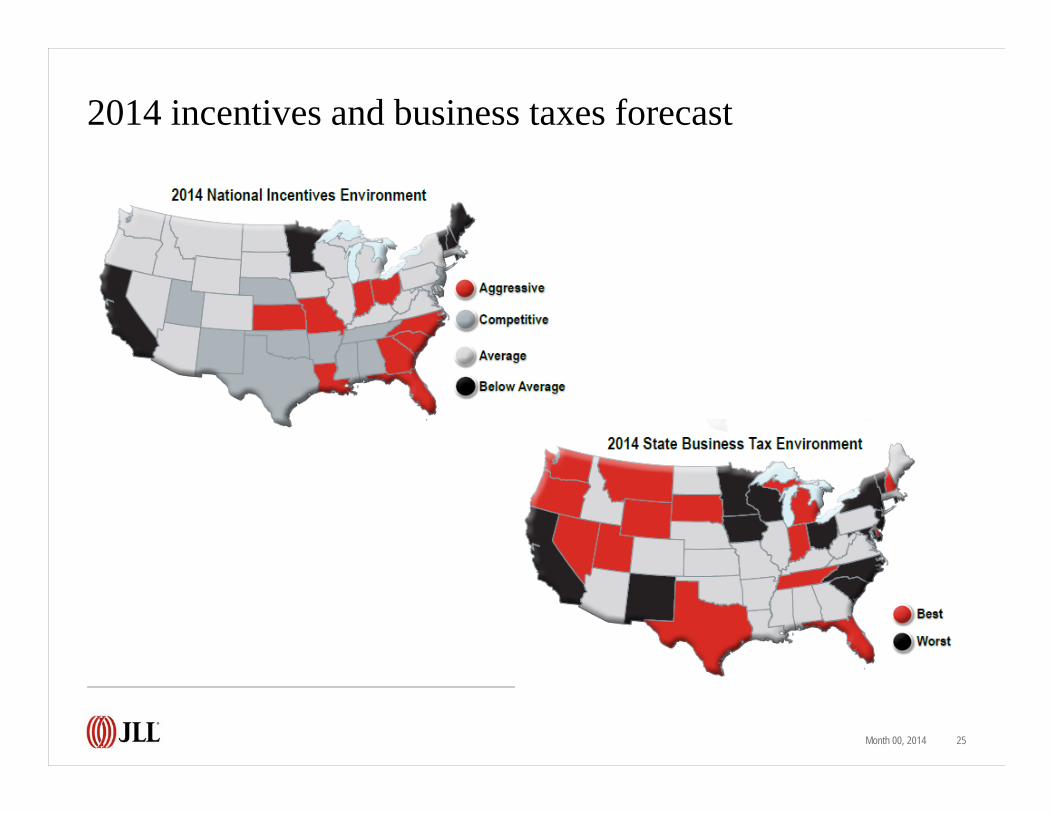

2014 incentives and business taxes forecast

Month 00, 2014 25

Why (why not) in Cincinnati?

March 14, 2014 26

Q & A

Thank you!