Embed Size (px)

Citation preview

INDUSTRIAL MARKETS

A vision for sustainable

growthThe new factors driving growth in

Chinarsquos chemicals sector

kpmgcomcn

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

a | Section or Brochure name

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

Contents

1 Introduction

2 China as a destination for global companies

bull AfterthecrisisChinaandtheworld

bull ResponseofmultinationalsShiftfromWesttoEa

3 Chinarsquos chemical industry Trends and growth driver

bull Rushtosecureethylenesupplies

bull Issuesfacingdomesticindustry

bull TheroadaheadRampD

4 Renewables sustainability and chemical demand

bull Alternativeenergytargets

bull Roleofchemicalsinmakingsolarenergycheaper

bull WindsofchangeDevelopmentsinpolymers

bull Autoboonforchemicalmanufacturers

bull Constructingagreenfuture

5 Conclusion

6 About KPMG

st

s

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

A vision for sustainable growth | 3

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

Introduction

In 2010 China eclipsed Japan to emerge The chemical industry is now in the as the second largest economy in terms process of transition reaching for new of gross domestic product but the growth drivers A small yet distinct shift nationrsquos policy makers are not cheering has been towards the new energy sector

with governments and enterprises eyeing Glaring contradictions remain within

a green evolution Chemical companies the worldrsquos swiftest growing nation

too are not averse to the demands Chinarsquos per capita income is USD 3600

created by sustainability and the urgent compared with Japan which averages

need for China to beef up research and USD 37800 and the United States with

development nearly USD 46000

In our report last year we focused There is however no stopping Chinarsquos

on agrochemicals and engineering manufacturing speed The countryrsquos

plastics as two sectors serving a more robust industrial health is largely

sophisticated China market This time reflected by the chemical industry

we provide an overview of how a fast China is the worldrsquos second biggest

developing renewable sector in China is consumer of chemicals Chemical

creating new demands and challenges for makers have long derived benefits

the chemical industry from the low cost of labour cheap infrastructure favourable government polices and an immense market

Peter FungPartner in ChargeIndustrial MarketsKPMG China

Norbert MeyringHead of Industrial Markets Asia Pacific Chair ChemicalsKPMG China

Shanghai

Mike ShannonGlobal Head of ChemicalsKPMG in the US

4 | Section or Brochure name

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

A vision for sustainable growth | 5

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

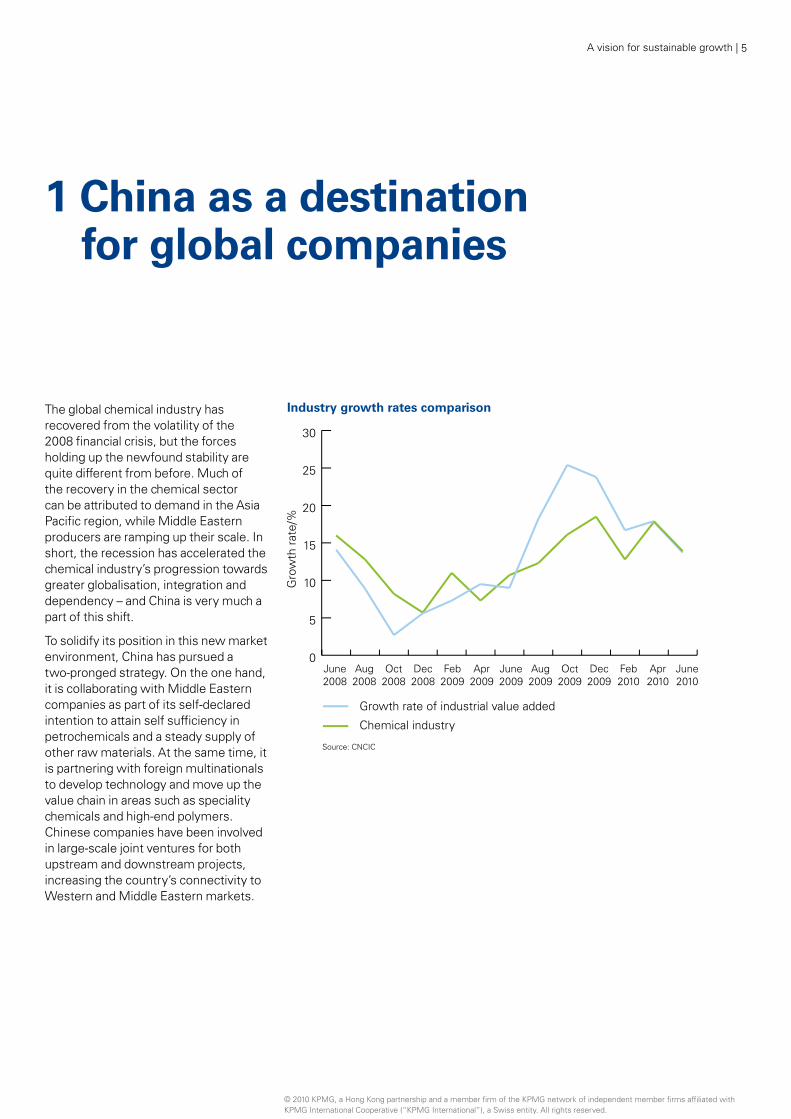

1 China as a destination for global companies

The global chemical industry has recovered from the volatility of the 2008 financial crisis but the forces holding up the newfound stability are quite different from before Much of the recovery in the chemical sector can be attributed to demand in the Asia Pacific region while Middle Eastern producers are ramping up their scale In short the recession has accelerated the chemical industryrsquos progression towards greater globalisation integration and dependency ndash and China is very much a part of this shift

To solidify its position in this new market environment China has pursued a two-pronged strategy On the one hand it is collaborating with Middle Eastern companies as part of its self-declared intention to attain self sufficiency in petrochemicals and a steady supply of other raw materials At the same time it is partnering with foreign multinationals to develop technology and move up the value chain in areas such as speciality chemicals and high-end polymers Chinese companies have been involved in large-scale joint ventures for both upstream and downstream projects increasing the countryrsquos connectivity to WesternandMiddleEasternmarkets

0

5

10

15

20

25

30

200

200

200

200

200

200

200

200

200

200

2010

2010

2010

Industry growth rates comparison

6 | A vision for sustainable growth

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

After the crisis China up and runningThe chemical industry felt the 2008 global recession head on but China andWesternEuropereactedtothecrisisindifferent ways each reaping different results

After the turbulence Chinarsquos chemical industry was one of the first to bounce back thanks largely to the governmentrsquosRMB 4 trillion stimulus package1 Buoyed by improved liquidity major infrastructure investments and the need to restock inventory demand for chemicals rose from the end of December 2008 throughout 2009 An additional factor supporting this has been the governmentrsquos continued intention to make the country self sufficient in basic petrochemicals and plastics Growth in automobile textile and building material industries have all helped stimulate domestic demand as export markets have slowed

According to the China Petroleum and Chemical Industry Association (CPCIA) in 2010 the petrochemical industry is expected to see a total output value of around RMB 857 trillion (USD 126 trillion) up 293 percent from a year earlier2 In the first and second quarterstotal output value grew by 469 percent and 368 percent year on year while it isestimated to slow down in the third and fourth quarter to 252 percent and 165 percent3 Full-year profit for the sector is expected to rise 8 to 10 percent and total investment is expected to grow by 15 percent in 2010 according to estimates given at the beginning of the year

These sector figures seem much glossier than the wider economic picture In the first quarter of 2010 GDPgrew 119 percent year-on-year to RMB 806 trillion (USD 119 trillion) while in the second quarter it slowed to 103 percent in part because the investment side of the economy showed signs of cooling Fixed asset investment growth has slowed considerably since the beginning of 2010 as the policy stimulus measures gradually faded By some estimates it will grow by 20 to 22 percent in real terms in 2010 compared to its 2009 growth of around 30 percent4

Improved global demand and gains in the market share have helped Chinarsquos export volumes recover strongly

However it still took 18 months for volumes to return to the pre-crisis levels of September 2008 In contrast imports recovered more quickly thanks in part to Chinarsquos economic stimulus package

Chinarsquos trade surplus has declined sharply since 2008 due to lower global demand and a continued rise in commodity imports Deteriorating terms of trade have also played a role In the first half of 2010 the trade surplus was 43 percent lower than in the same period in 2009 Analysts expect a slower second half of the year given limited prospects for a recovery in exports to the US and Europe

This uncertain export situation may reemphasise the need for Chinese chemical companies to bank more heavily on domestic growth Although China recently surpassed Japan as the worldrsquos second largest economy there are signs that investment may be slowing

The construction and infrastructure sectors are showing particularly mixed trends Since mid 2009 real estate prices have risen by as much as 90 percent in some second-tier cities To cool the market and curb property speculation the government has raised the reserve ratio requirement the amount of money banks must keep with the government three times during 20105 Banks are now being discouraged to hand out loans to second and third buyers of homes Efforts to cool the economy especially the property sector have depressed sentiments in the chemical markets

Post crisis major Chinese petrochemical companies also increasedMampAactivitiesastheyturnedfocus from attracting inbound foreign investment to establishing themselves on the global stage through outbound acquisitions Chinese state-owned enterprises are going around the world ndash from Middle East to South America ndash picking up stakes in oil companies At home the government continues to encouragemultinationalstoopenRampDand manufacturing centres

However among all products in the industry China has the highest demand for speciality chemicals and has been constructing its own chemical plants and using joint ventures with European players to increase capacity in this sector

Response of multinationals Shift from West to East ThefinancialcrisisbroughtWesternEuropean and North American chemical multinationals face to face with their overcapacity tightening of credit and loss of markets Many imposed significant job cuts as their attention turned to survival According to a KPMG Europe report from January 2010 entitled The Future of the European Chemical Industry a number of the largest companies are being forced to act fast and implement downsizing or massive restructuring This has resulted in the redundancy of approximately

1ldquoFactsampfiguresofthechemicalindustryrdquo5July2010ChemicalampEngineering News

2 ldquoTotal output value of Chinarsquos petchem industry uprdquo 13 August 2010 Plastmartcom

3 ldquoChinarsquos petrochemical output value to reach USD 126 trillion CPCIArdquo 11 August 2010 Trading Marketscom

4 httpwwwgovcnenglish2010-0121content_1516848htm5 May chill grips housing industry 5 May 2010 China Daily

China GDP Structure 2009

10 growth in chemical industry

Chemical

Agriculture forestry animal husbandry and fishery

Industrial and construction sectors

Tertiary industry

2009 2008

10 10

12

A vision for sustainable growth | 7

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

0

10

20

30

40

50

Imported materials by type

12010

200200

6 OutputdeclinesinUSEurope5July2010ChemicalampEngineering News

7 ldquoDownbutnotoutrdquo11January2010ChemistryampIndustry8 ldquoKPMGrsquos views on the economic outlook for the chemical

industryrdquo September 2009

4 percent of the pre-recession chemicaindustry workforce in Europe to date

The chemical industry was particularly affected by weakening industrial demand in the second half of 2008 and the first quarter of 2009 The drop in production coincided with lower production in the key customer industries such as housing construction automotive electrical furniture and paper6

The European chemical industry saw a monthly year-on-year decline of 132 percent as it hit its lowest point in March 20097 The deepest fall occured

l in demand for plastics paint and man-made fibres This fall in demand prompted a wave of de-stocking with some companies (particularly in the base chemicals polymers and speciality chemicals sectors) experiencing declines in output of 30 to 60 percent8

Despite gloomy predictions at the beginning of 2010 Europe has recovered well The European Chemical

Industry Council or Cefic expects a 95 percent increase in output growth in 2010 but expectations for 2011 point to a growth of a meagre 2 percent year on year Thatrsquos because Cefic expects a period of consolidation around the second half of 2010 and early 2011 The Council predicts it will be another two years before European output reaches the high levels of 2007

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

8 | A vision for sustainable growth

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

However the overall economic recovery of Europe is still fragile Any defaults on sovereign debt could trigger renewed problems for banks and the chemicals sector would remain sensitive to these economic shocks9 Cefic has argued that underlying market demand must be rebuilt and growth cannot be built on inventory corrections alone The development of Europersquos chemical industry will also depend on consolidation measures in the face of relentless global competition

In addition to readjusting their workforce figures amid the recovering economy companies will also need to address their capacity excess and competitiveness In particular aging and more inflexible assets in the US andWesternEurope(withthelatterhaving a greater percentage of inflexible naphtha-based crackers) are being challenged by assets with more larger-scale and flexible capacities from the Middle East China and India

Backed by a dependable supply of resources as well as significant cash reserves Middle Eastern countries have been making huge investments to increase capacity in upstream downstream and integrated production facilities More than 19 million tpa of ethylene capacity will come on stream in the Middle East by 2015 according to a recent analysis by SRI Consulting10

Some 50 percent of all new ethylene projects being developed in the world are located in the Middle East Saudi

Arabia holds the bulk of the projects epresenting around 63 percent of total nvestment in the Gulf while Qatar omes second with a 14 percent share he Gulf Petrochemicals and Chemicals ssociation (GPCA) has forecast that

he region will account for 40 percent f total global petrochemical production ithin 10 years11 On this account owever it has also warned that this ay bring fresh challenges to the

egionrsquos producers in terms of the need o secure more feedstock

espite the current and projected rowth levels for the region concerns hat Gulf producers will gobble up uropean companies seem to be xaggerated About 5-6 million tpa f ethylene capacity was projected o come onstream in 2009 but only bout 28 million tpa actually started roduction due to delays and start-up ifficulties

ndeed Middle East production is teadily working its way into the arketplace rather than flooding

he markets The result is that Gulf roducers will gradually step up the ressure on rival exporters in Europe nd North America To prepare any of the worldrsquos leading chemical

ompanies have begun pursuing major estructuring and have been opting for ajor collaborations in the Middle East

s a way to turn the situation to their dvantage

PMG Europersquos The Future of the uropean Chemical Industry report

ricTAtowhmrt

DgtEeotapd

Ismtppamcrmaa

KE

0

5

10

15

20

25

9 EU chemical industry to grow 95 in 2010 7 June 2010 wwwcefic org

10ldquoWillChinaimportmorepetrochemicalsampplasticsrdquoSeptember2009

Exported materials by type

12010

200

200

highlights the gradual shift that is underway from Europe to new markets

Between 1995 and 2005 world chemical production increased by almost 40 percent However over 95 percent of that growth was concentrated in developing countries

bull Between1997and2007globalchemical sales increased by 60 percent but the portion of global EU sales declined by 27 percent

bull From2008to2020globalchemicaldemand will increase 8 percent in the Asia Pacific region but decrease 6percentinWesternEuropeaccording to estimates by BASF

Several factors explain this shift in global market leadership

Firstly the cost of raw material feedstock is significantly higher in WesternEuropethaninmostotherregions of the world and this cost difference will almost certainly continue in the future

Secondly the extensive opportunities and markets offered by emerging economies particularly China had been drawing top global companies even before the recession Multinationals from Dow Chemicals and ExxonMobil to BASF and Shell have set up new manufacturing and research bases in China and have opted for collaborations with Chinese petrochemical giants

As a result there is reason to believe that the global chemical industry will

SRI Consulting11 China Petrochemicals Report Q3 2010

continue its steady shift to the East with a greater portion of chemical majors headquartered outside the EU in the future In 2008 four of the top 10 chemical producers were located in Europe but KPMG estimates that by 2015 only one out of ten remain in Europe while at least six may be based in the Middle East or Asia

The future success of Europersquos chemical companies will be determined by its ability to operate at three different levels moving from bulk chemical production to the speciality end of the value chain leveraging traditional advantages in technology and establishing closer customer and competitor relationships through joint development agreements acquisitions value-added services and other strategic initiatives

All major multinationals have shifted to research and production of speciality chemicals high-end products and niche products To succeed industry analysts say they must push their advantage in technology and bank on their strengths in innovation and niche energy-efficient solutions Multinationals are swiftly making this transition from commodity chemicals to high-end target specific solutions The core strength of multinationals neatly fits into the immense technology gap experienced by Chinese chemical units which continue to thrive on low-end products

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

10 | Section or Brochure name

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

A vision for sustainable growth | 11

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

2 China chemical industry Trends and growth drivers

The chemical industry has been one of the fastest-growing sectors in China in the last decade contributing to more than 10 percent of GDP and accounting for 15 percent of global demand12 The evolution of Chinarsquos chemical sector has been unique and fundamentally differentfromWesternEuropeWhileithas been influenced by macro economic cycles it has also been policy driven to a significant extent

This section gives an overview of how Chinese companies have strengthened their position through a combination of strategies including a well-mapped plan to secure a steady and high-quality supply of ethylene The Chinese domestic industry is dominated by giant state-owned companies who with government backing managed to tackle the recession head-on and even take advantage of it However fragmentation and over-investment have caused alarm and the way forward is for companies toinnovateWhilejointventureswithforeign multinationals have reaped dividends China is now focusing on research and development This is essential given the strong potential domestic companies have for reshaping the industry and moving to the higher end of the value chain

Rush to secure ethylene suppliesSecuring a stable and secure ethylene supply is an essential part of Chinarsquos petrochemical sector policy especially in view of fluctuating oil prices Crude prices will continue to be a determining factor for the chemical industry given that it is a large consumer of oil and

natural gas both as an energy source and feedstock input The accelerating process of industrialisation and urbanisation has caused rapidly increasing demand for petrochemicals in China which in turn is stimulating a major ethylene capacity expansion throughout the country

In response to this growing demand Chinese ethylene production is scheduled to reach 2138 million tonnes per annum (tpa) by 2012 with seven major ethylene projects capable of producing 62 million tpa of ethylene including a 438 million tpa increase in the total production capacity of existing ethylene plants13 Of this 31 million tpa of ethylene capacity under construction is through joint ventures involving BP ExxonMobil BASF and Shell14 By 2015 the total capacity will go up to 23 million tpa15

China has adopted a dual strategy in securing feedstock State-owned companies are encouraged to make overseas acquisitions And to quell any Middle Eastern competition China is opting for collaboration with Gulf producers to ensure it has a steady supply of crude At another level it has opted for joint ventures with multinationals so as to help improve ethylene availability closer to home

In this China enjoys several advantages over other countries which allows it to build with relative ease mega refining and petrochemicals plants with local construction and engineering labour equipment machinery and materials

Some of the new refinery and ethylene projects include

bull PetroChinarsquos200000bpdnewrefinery in Qinzhou of Guangxi Autonomous Region Southwest of China which is going into a test run soon

bull QatarPetroleumplanstoworkwith PetroChina and Shell to build a 400000 barrels per day modern refinery in Tazhou of Zhejiang province and a 39 million tonnes per year olefin plant with Qatarrsquos LPG as the feedstock in Yangpu of Hainan province partnering with CNOOC and Shide Group

bull SaudiAramcosetupanintegratedoil refining and petrochemical complex in China along with ExxonMobil and Sinopec in Quanzhou Fujian province last November The facility has a total investment of around RMB 40 billion It can produce 746 million tonnes of refined oil 128 million tonnes of plastics and huge amounts of other chemical products

bull InNovember2009SABIConeof the worldrsquos leading producers of chemicals inaugurated its new petrochemical complex together with Sinopec in Tianjin The 50-50 joint venture has a total investment of RMB 183 billion The project can produce 1 million tonnes of ethylene annually

12ldquoChinachemicalindustryrdquo11June2010EconomyWatch13 ldquoChina ethylene cracker projects to see rapid capacity growthrdquo 5 March

2010 Energychinaforumcom14 ldquoRefining capacity expansion in China stays in high gearrdquo 17 May 2010

Reuters)15 ldquoEthylene capacity expansions peaking in Chinardquo 26 March 2010 Gerson

Lehrman Group

12 | A vision for sustainable growth

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

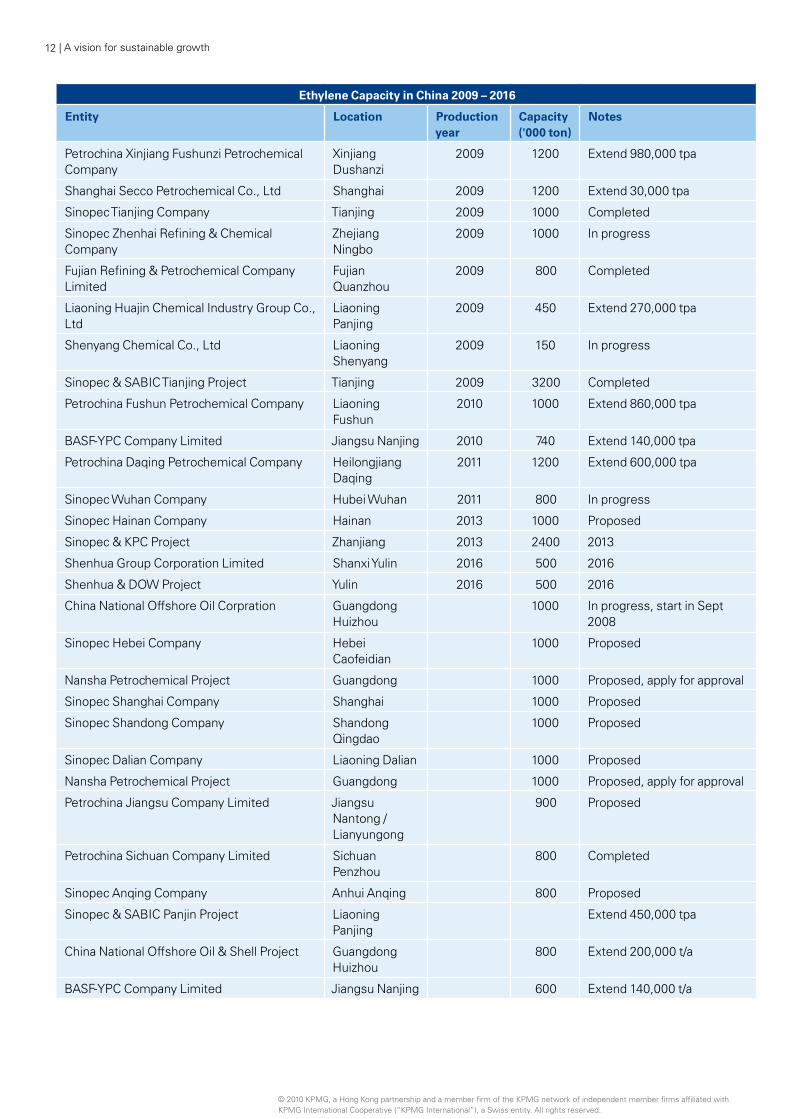

Ethylene Capacity in China 2009 ndash 2016

Entity Location Production Capacity Notesyear (000 ton)

Petrochina Xinjiang Fushunzi Petrochemical Xinjiang 2009 1200 Extend 980000 tpaCompany Dushanzi

Shanghai Secco Petrochemical Co Ltd Shanghai 2009 1200 Extend 30000 tpa

Sinopec Tianjing Company Tianjing 2009 1000 Completed

SinopecZhenhaiRefiningampChemical Zhejiang 2009 1000 In progressCompany Ningbo

FujianRefiningampPetrochemicalCompany Fujian 2009 800 CompletedLimited Quanzhou

Liaoning Huajin Chemical Industry Group Co Liaoning 2009 450 Extend 270000 tpaLtd Panjing

Shenyang Chemical Co Ltd Liaoning 2009 150 In progressShenyang

SinopecampSABICTianjingProject Tianjing 2009 3200 Completed

Petrochina Fushun Petrochemical Company Liaoning 2010 1000 Extend 860000 tpaFushun

BASF-YPC Company Limited Jiangsu Nanjing 2010 740 Extend 140000 tpa

Petrochina Daqing Petrochemical Company Heilongjiang 2011 1200 Extend 600000 tpaDaqing

SinopecWuhanCompany HubeiWuhan 2011 800 In progress

Sinopec Hainan Company Hainan 2013 1000 Proposed

SinopecampKPCProject Zhanjiang 2013 2400 2013

Shenhua Group Corporation Limited Shanxi Yulin 2016 500 2016

ShenhuaampDOWProject Yulin 2016 500 2016

China National Offshore Oil Corpration Guangdong 1000 In progress start in Sept Huizhou 2008

Sinopec Hebei Company Hebei 1000 ProposedCaofeidian

Nansha Petrochemical Project Guangdong 1000 Proposed apply for approval

Sinopec Shanghai Company Shanghai 1000 Proposed

Sinopec Shandong Company Shandong 1000 ProposedQingdao

Sinopec Dalian Company Liaoning Dalian 1000 Proposed

Nansha Petrochemical Project Guangdong 1000 Proposed apply for approval

Petrochina Jiangsu Company Limited Jiangsu 900 ProposedNantong Lianyungong

Petrochina Sichuan Company Limited Sichuan 800 CompletedPenzhou

Sinopec Anqing Company Anhui Anqing 800 Proposed

SinopecampSABICPanjinProject Liaoning Extend 450000 tpaPanjing

ChinaNationalOffshoreOilampShellProject Guangdong 800 Extend 200000 taHuizhou

BASF-YPC Company Limited Jiangsu Nanjing 600 Extend 140000 ta

A vision for sustainable growth | 13

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

200 2004 200 2006 200 2008 200

0

10

20

0

40

0

60

0

2003-2009 Polyethylene Supply and Demand Trend in China

bull Ethylenesupplylineshavealsostrengthened due to Asian suppliers Japanese petrochemicals producers are shifting their investment to eastern Asia and the Middle East to build projects that will eventually export to China Some Taiwanese companies have also invested in the mainland Taiwan has an ethylene capacity of 242 million tpa

The domestic side a large but fragmented industryThe Chinese petrochemical industry is marked by an overall lack of balance with giant state-owned companies dominating one end of the spectrum along with an immense number of private enterprises According to estimates there are more than 100 oil refiners with a capacity of over 1 million tonnes across the country16

Since the petrochemical industry can contribute to local governmentsrsquo revenue every province has had an incentive to increase production over the years The current distribution does not mesh well with a resource-efficient development strategy as only 70 percent of the capacity has been used17 Many small-scale petrochemical firms are burdened by low levels of

16 BMI China Petrochemicals Report Q3 201017 ldquoNew energy market reportrdquo June 2010 Fast Market Research

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

14 | Section or Brochure name

productivity and poor economies of want to move up the value chain For WhilemultinationalslikeBASFDuPontscale They lack investment in research example products like polycarbonate Bayer and DSM have manufacturing and development and rely on imported have a domestic output of 330000 units for high-end productsAs foreign technology tonnes per year yet most of this is companies increase their presence in

produced by foreign enterprises China either through local subsidiaries The government is now attempting to

or joint ventures it is becoming raise the overall global competitiveness Sectors such as agrochemicals also

important to get a clear view of of its oil and petrochemicals sectors suffer from fragmentation and a glut

environmental regulations An accurate This process has involved some of low-end products Cumulative

assessment of regulatory norms with consolidation and the closure of many production of agrochemicals in China

respect to carbon emissions is also smaller privately owned refineries The reached 204 million tonnes by the end

needed An understanding of carbon Chemical and Petrochemical Industries of November 2009 more than double

exposureduringmergersampacquisitionsAssociation (CPCIA) is working towards that of 200518 However the Chinese

is essential for correct structuring of a a plan to pressure smaller producers to pesticide market is dominated by

deal Joint ventures are one way for local modernise their production facilities and generic products making penetration

companies to fill this technology gapincrease energy efficiency using new difficult for high-priced brands of technology wherever possible overseasmanufacturersWithfood The road ahead Research amp

safety now becoming an issue for the DevelopmentOver the years industrial reform

government pressure is mounting on In China vast infrastructure by way of has also led to greater willingness

local makers and opportunities could chemical parks and mega joint ventures for domestic firms to enter into

arise for foreign multinationals with foreign companies are firmly in joint ventures with their foreign

place but investment in research and counterparts China has welcomed Paint is another sector ripe for

development is not entirely in proportion foreign petrochemicals technology and diversification The industry profit

to the scale and sophistication of its is actively encouraging joint ventures margin is only 5 percent here which is

chemical demandwith state-owned companies In return why local units could spread their basket the country offers a growing domestic to specialised products like special At this juncture chemical companies market for their products and low labour coatings for fire retardants thermal need to optimise value chain efficiency and construction costs for greenfield insulation and waterproofing19 by better end product design and drive projects themselves towards greater innovation

Domestic manufacturers have yet to The high number of joint ventures realise the full potential of speciality However this trend is now beginning involving the three state-owned chemicals There is enough scope for tochangeRampDspendinginChinagiantsChinaPetroleumampChemical fluropolymers an important class of including those by foreign companies Corporation (Sinopec) China National products for domestic appliances is rising and is expected to hit 2 percent Petroleum Corporation (CNPC) and High-performance PTFE fluorine rubber of GDP this year up from just 1 percent China National Offshore Oil Corporation and polyethylene FEP are products that in 2000 according to analysis from (CNOOC)indicatethatWestern can be explored along with electronic Research-WorksaShanghai-basedmultinationals have an important role to chemicals manufacturing Products foreign investment research firm At play in the chemical and petrochemical like light emitting diodes with epoxy that level it would still trail Japan (33 value chain and push the sector towards resin or liquid crystal alignment film percent) South Korea and the United greater innovation materials used in LCD TVs are in huge States (26 percent) as a percentage

demand with Greater China making up of GDP but would be higher than the Domestic downstream lagging

the worldrsquos largest market However European Union21 behind

domestic inputs from the chemical Much like its upstream counterparts the According to a study by the Organisation

sector do not match updomestic chemical industry is also beset for Economic Co-operation and by overcapacity and fragmentation It is High-end engineering plastics and Development (OECD) only 39 countries generally concentrated around low-value modified plastics is another area and regions account for 95 percent of bulk products despite growing demand Chinese companies need to explore theworldrsquostotalRampDinputIn2007thefor speciality chemicals and engineering According to the China Engineering RampDinputofthesecountriestotalledplastics from Chinarsquos maturing markets Plastics Industry Association while USD 102 trillion The same year Chinarsquos

foreign cars have 40 percent polymer totalRampDinputamountedtoUSD4879Products running to full capacity remain

content while their Chinese-made billion an increase of USD 1112 billion bulk chemicals including soda ash

counterparts have 25 percent less from 200622

chlor-alkali methanol urea phosphate In addition high-speed railways have

fertilizer pesticides glyphosate and a high consumption of nylon pads

other heavy consumption staple sleeper pad high-strength nylon and

productsother plastic products20

Experts of the China Chemical Industry Economic and Technical Centre indicate

18 Chinarsquos agrochemical production rising at alarming rate 21 April 2010

that traditional chemical products should Agro News19 A profile of the Chinese paint industry Vol 57 Issue 4 2010 Emerald

opt for greater diversification if they Research20 ldquoChinese chemical companies to look for new highlightsrdquo 16 August

2010 Website2010SummitForumChinachemicalindustry21 ldquoPlasticsRampDinChinagrowing5August2010PlasticNewscom22 Science and Technology Statistical Report July 2009 Department of

Development Planning Ministry of Science and Technology

A vision for sustainable growth | 15

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

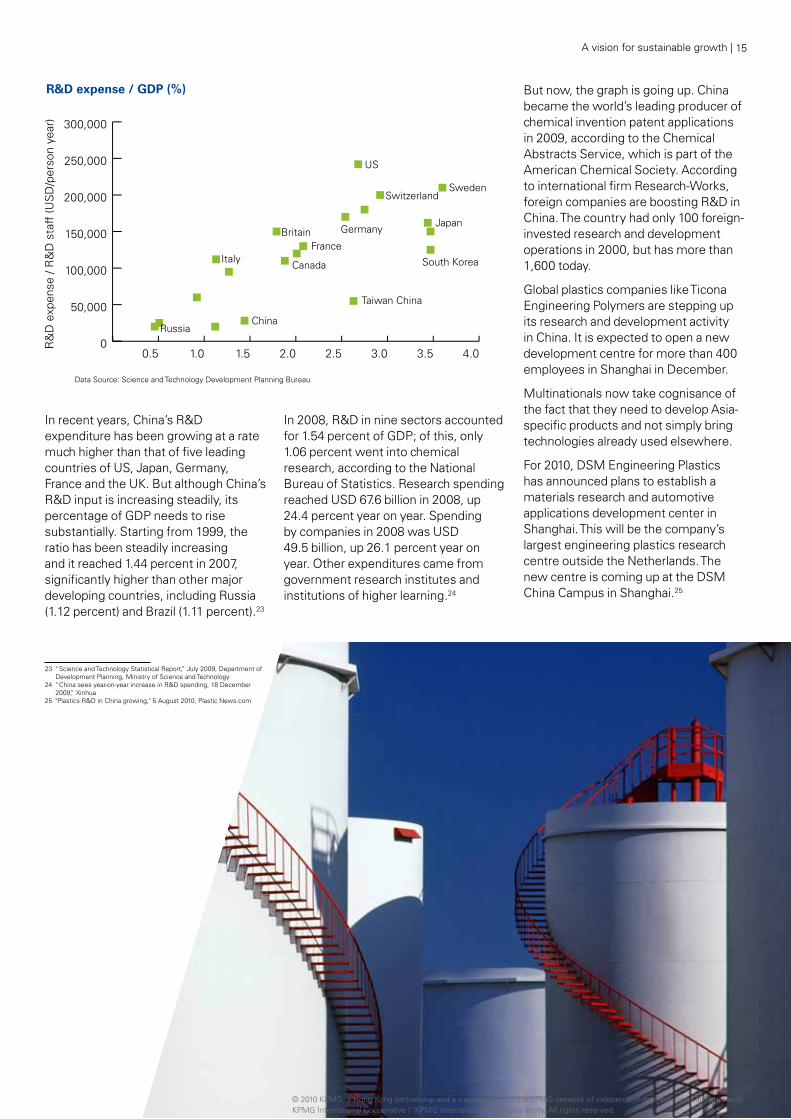

InrecentyearsChinarsquosRampDexpenditure has been growing at a rate much higher than that of five leading countries of US Japan Germany France and the UK But although Chinarsquos RampDinputisincreasingsteadilyitspercentage of GDP needs to rise substantially Starting from 1999 the ratio has been steadily increasing and it reached 144 percent in 2007 significantly higher than other major developing countries including Russia (112 percent) and Brazil (111 percent)23

In2008RampDinninesectorsaccountedfor 154 percent of GDP of this only 106 percent went into chemical research according to the National Bureau of Statistics Research spending reached USD 676 billion in 2008 up 244 percent year on year Spending by companies in 2008 was USD 495 billion up 261 percent year on year Other expenditures came from government research institutes and institutions of higher learning24

But now the graph is going up China became the worldrsquos leading producer of chemical invention patent applications in 2009 according to the Chemical Abstracts Service which is part of the American Chemical Society According tointernationalfirmResearch-WorksforeigncompaniesareboostingRampDinChina The country had only 100 foreign-invested research and development operations in 2000 but has more than 1600 today

Global plastics companies like Ticona Engineering Polymers are stepping up its research and development activity in China It is expected to open a new development centre for more than 400 employees in Shanghai in December

Multinationals now take cognisance of the fact that they need to develop Asia-specific products and not simply bring technologies already used elsewhere

For 2010 DSM Engineering Plastics has announced plans to establish a materials research and automotive applications development center in Shanghai This will be the companyrsquos largest engineering plastics research centre outside the Netherlands The new centre is coming up at the DSM China Campus in Shanghai25

00 05 10 15 20 25 30 35 400

50000

100000

150000

200000

250000

300000

RampD expense GDP ()

23 ldquoScience and Technology Statistical Reportrdquo July 2009 Department of Development Planning Ministry of Science and Technology

24 ldquoChinaseesyear-on-yearincreaseinRampDspending18December2009rdquo Xinhua

25 PlasticsRampDinChinagrowing5August2010PlasticNewscom

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

Company Name Research expenses in 2009 (Million Yuan)

China Petrochemical Corporation中国石油化工集团公司

610

China National Chemical Corporation中国化工集团公司

256

Henan Coal Chemical Group河南煤业化工集团有限公司

248

Zhong Ping Energy Chemical Group中国平煤神马能源化工集团有限责任公司

209

Tianjin Bohai Chemical Industry Group天津渤海化工集团公司

1107

Hubei Yihua Group Limited Liability Company湖北宜化集团有限责任公司

097

26 ldquoAn overview of Dow Chemical Company in Greater Chinardquo Corporate website

27 ldquoDuPont opens new photovoltaic technical center in Chinardquo Corporate website

28 ldquoBASF Greater China corporate website29 ldquoLanxess in China ndashResearch and development innovation hubrdquo

Corporate website30 Plastics research in China growing August 2010 plasticnewscom31 ldquoLanxess in China ndashResearch and development innovation hubrdquo

Corporate website

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

However the industry lacks the sort of Foreign companies launched or Lanxess too has concentrated on tight-knit joint development work that extended a number of research centers establishing a research and innovation goes on among plastics processors in China throughout 2009 The Shanghai network in China In 2007 the semi-machine makers and materials suppliers Dow Center opened in June 2009 in crystalline products business unit in Europe The lsquosuccess trianglersquo Zhangjiang High-Tech Park with over opened a research and development concept is low in China unlike Europe 80 integrated laboratories and 500 testingcenterinWuxiThesameyearwhere three segments - product scientists and engineers The Dow the performance butadiene rubbers development research by the processor Center focuses on developing solutions business unit of Beijing entered into a raw material supplier and the machinery for the construction transportation cooperation agreement with the Beijing maker - make up a lsquotrianglersquo and come energy water electronics and personal ResearchampDesignInsitituteofRubber

with practical solutions30care industries26 up Industry In 2008 Lanxess opened a

center for rubber research in Qingdao29 Chinese companies are still developing DuPont too opened a photovoltaic research capacity and are accustomed technicalcenteratitsChinaglobalRampD Chinese firms too have stepped up to following and introducing existing Center at Zhangjiang Park Shanghai Research institutes funded by the technologies fromabroad They also to support the fast growing crystalline Chinese government have accelerated need to develop frameworks to silicon photovoltaic solar energy market RampDprogrammesandcompaniescapitalise on discoveries and inventions The facility has three labs that focus on like Guangzhou Kingfa Science and made by academics community research development and technical Technology Co have taken advantage of Withoutinnovationscompaniescouldsupport for the specialised needs of available money in areas like advanced be stuck earning minimal profit from customers in the PV industry in China materialslow-end manufacturing31

The lab is fitted with evaluation facilities Chinese companies are still developing

resembling its customersrsquo production In the high-value chemical industry all research capacity and are more lines27 growth options are becoming more and accustomed to following and introducing

more specific In the next decade the BASF has several Asia-focused existing technologies from abroad They key to success could well be lsquosolutions research and development also need to develop frameworks to and materialsrsquo where the focus is on laboratories in Shanghai including a capitalise on discoveries and inventions value creation beyond mere supply of labforPVCplasticizersaRampDunitfor made by the academic community chemicals where companies will offer polyurethanes as well as an innovation Withoutinnovationscompaniescouldservices based on application knowhow center for personal care products be stuck earning minimal profit from low

pharmaceuticals and beverages In end manufacturing2009itupgradeditsRampDcapabilitiesfor mobile emissions catalyst business in Guilin28

member firms affiliated with

A vision for sustainable growth | 17

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

18 | Section or Brochure name

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

A vision for sustainable growth | 19

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

Chemical companies have a role to play in helping to solve some of the worldrsquos most pressing issues relating to pollution sustainability and climate change Government grants are being allocated to support some of these developments and this presents opportunities for chemical companies to partner with academia and niche technology entities to bring ideas to market This chapter explores the changing role of chemical companies in developing new-age products that contribute to a sustainable future

Clean energy especially solar and wind power is getting lsquobig pushrsquo from policy-makers which is generating additional demand for advanced polymers and speciality chemicals China now ranks asone of the most attractive locations for investment in wind and solar projects In terms of volume the chemical sector is also likely to see supplementary demand from the green automotive and construction chemicals sectors

The global renewable chemicals market is expected to grow at an estimated CAGR of 1166 percent from 2010 to 2015 to reach USD 6713 bn in 2015 Renewable ethanol is the most commercialised segment while Iso-butanol and succinic acid are on the verge of commercialization Government support development of new technologies and available feedstock are major drivers for the renewable chemicals market New

3 Renewables sustainability and chemical demand

Use of chemicals in Renewable sector

composite materials

Wind silane coupling agent

lubricant

polysilicon

Solar cutting fluid

sealant

material surface coating

positive electrode film substrate

negative electrode battery grade lithium carbonate lithium hydroxide

Fuel Cell

electrolyte

diaphragm

lithium cobalt oxide lithium iron phosphate

modified graphite

others LiPF6

Sinopec Dalian Company

polypropylene polyethylene microporous membrane

Nansha Petrochemical Project

rare-earth hydrogen storage alloy

markets such as China provide immense opportunities for renewable chemicals32

China has almost doubled consumer subsidies for renewable-power generation in the second half of 2009 In the second quarter of 2010 it attracted more asset-financing for clean technologies than Europe and the US combined33

WhileChinacangeneratemassivedemand and provide vast-scale manufacturing facilities it needs the

cutting-edge technology of more developed nations Needless to say the world of speciality chemicals and new-age polymers used in the renewable energy sector will be one of interdependency

Chemicals used in the renewable energy sector are extremely specific in nature and the trend will increasingly move towards customer-based solutions

32 ldquoRenewable chemicals market worth $6713 bn in 2015rdquo August 2010 Markets and Markets

33 ldquoNation best bet for renewable energy projectsrdquo 9 September 2010 China Daily

20 | A vision for sustainable growth

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

According to the governmentrsquos 2050 China Energy and CO2 Emissions Report published in 2009 the country needs to spend between RMB 500 billion and 600 billion annually to develop energy-conservation and low-carbon technologies So far it has attracted USD 115 billion in asset financing for clean-energy technology in the second quarter more than Europe and the US combined

Role of chemicals in making solar energy cheaperChinalikedevelopedWesterncountriesis investing to make alternative fuel especially solar energy cheaper It is planning to boost its installed capacity of solar-driven generation more than 60-fold to 20000 megawatts by 2020

At present solar panels cost about 10 times more than fossil fuels in terms of cost per unit of energy output The good news is that the price of solar energy has been dropping steadily for 30 years - by about 50 percent every decade - and this could drop further with sufficiently large investments in research and development

A key component of this strategy is providing advanced raw material that would bring down the cost of production This is where speciality chemical companies are playing an unassuming yet ground-breaking role The solar energy sector in China is an evolving case study that encompasses all these factors it is a sector heavily backed by policy-makers huge investments are being made to increase capacity and the key raw material ndash polysilicon ndash is slowly being replaced by speciality chemicals

Pitfalls of polysiliconChinarsquos domestic demand for solar photovoltaic (PV) energy may reach 500000 kilowatts this year But it plans to expand the solar PV energy market gradually to about 5 million kilowatts installation capacity in 2015 and 20 million kilowatts in 2020 according to the National Energy Administration

Photovoltaic is a method of generating electric power by converting solar radiation into direct current electricity by using semiconductors However solar companies across the world are saddled with unpredictable supply and prices of the basic raw material polysilicon which is the key component of solar panel

2000-2009 Wind installation in China (MV)

Wind blade demand forecast

Year 2010 2011~2020(E)

Accumulative forecast of installation capacity (times103 kw)

40000 180000

Demand of wind blades in new wind power installation (times103 kw)

15000 165000

Demandofwindbladesequivalentto15MW(set) 10000 110000

Average annual demand of wind blade (set) 10000 11000SourceChineseWindEnergyAssociation

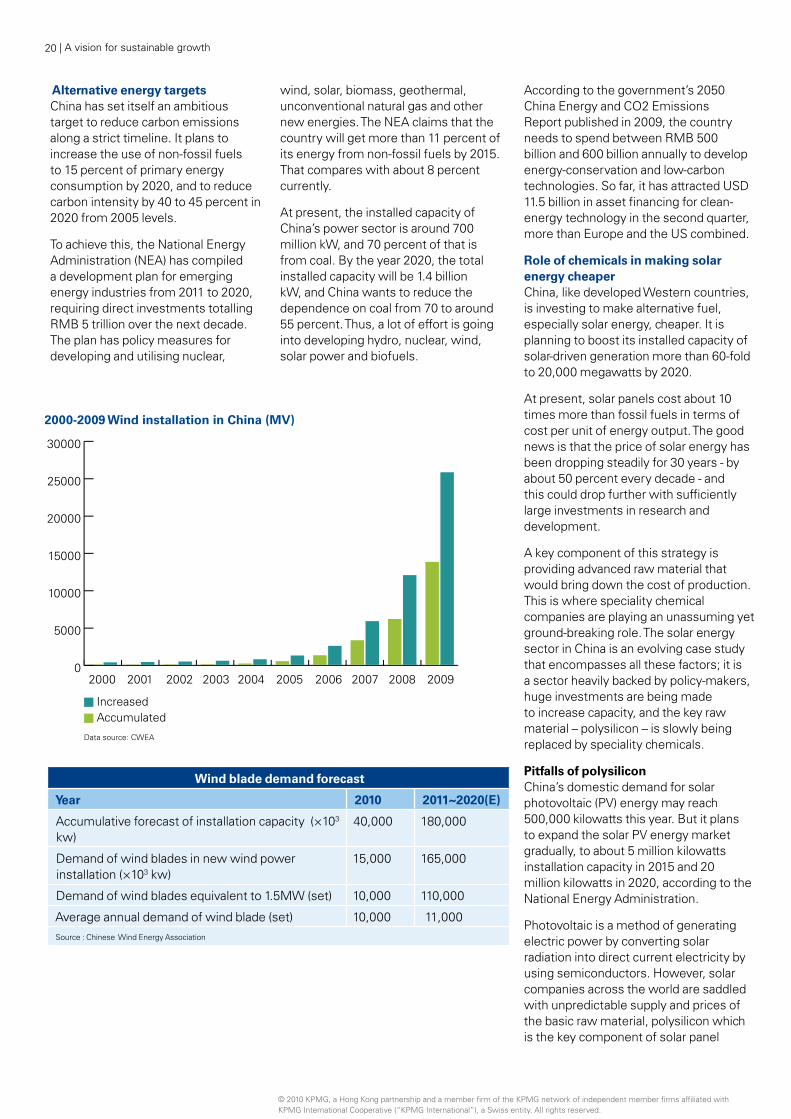

Alternative energy targetsChina has set itself an ambitious target to reduce carbon emissions along a strict timeline It plans to increase the use of non-fossil fuels to 15 percent of primary energy consumption by 2020 and to reduce carbon intensity by 40 to 45 percent in 2020 from 2005 levels

To achieve this the National Energy Administration (NEA) has compiled a development plan for emerging energy industries from 2011 to 2020 requiring direct investments totalling RMB 5 trillion over the next decade The plan has policy measures for developing and utilising nuclear

wind solar biomass geothermal unconventional natural gas and other new energies The NEA claims that the country will get more than 11 percent of its energy from non-fossil fuels by 2015 That compares with about 8 percent currently

At present the installed capacity of Chinarsquos power sector is around 700 millionkWand70percentofthatisfrom coal By the year 2020 the total installed capacity will be 14 billion kWandChinawantstoreducethedependence on coal from 70 to around 55 percent Thus a lot of effort is going into developing hydro nuclear wind solar power and biofuels

A vision for sustainable growth | 21

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

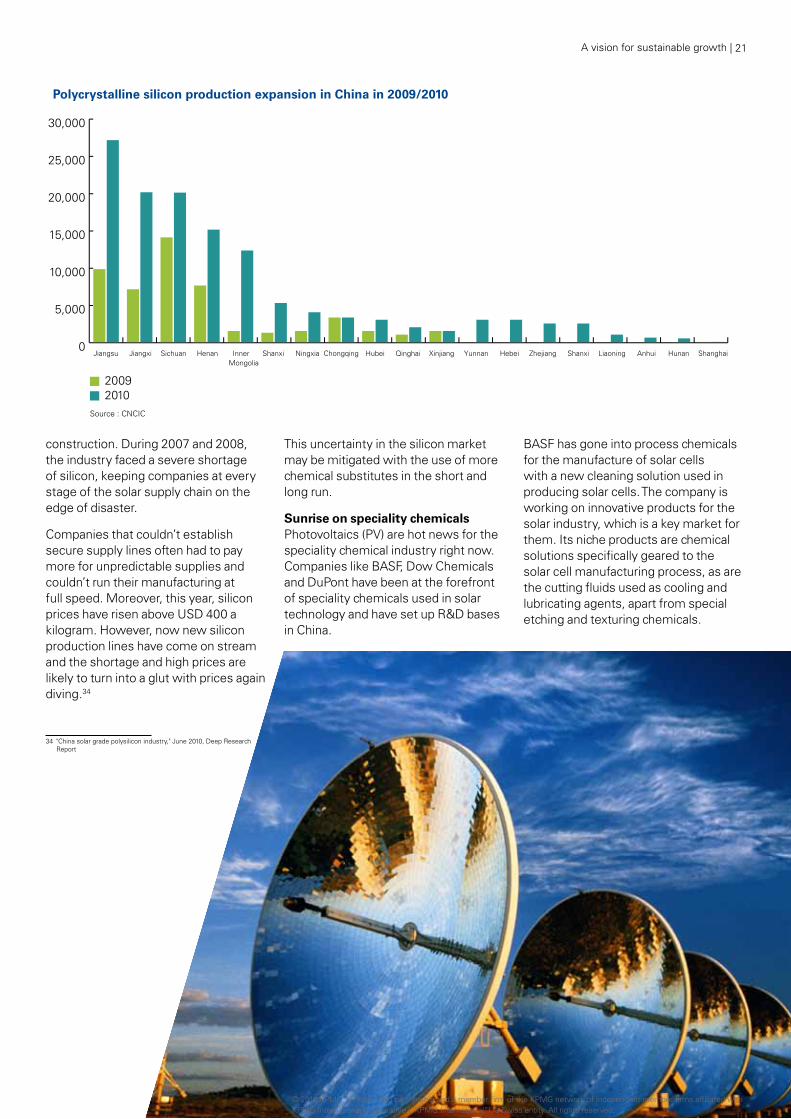

construction During 2007 and 2008 the industry faced a severe shortage of silicon keeping companies at every stage of the solar supply chain on the edge of disaster

Companies that couldnrsquot establish secure supply lines often had to pay more for unpredictable supplies and couldnrsquot run their manufacturing at full speed Moreover this year silicon prices have risen above USD 400 a kilogram However now new silicon production lines have come on stream and the shortage and high prices are likely to turn into a glut with prices again diving34

This uncertainty in the silicon market may be mitigated with the use of more chemical substitutes in the short and long run

Sunrise on speciality chemicalsPhotovoltaics (PV) are hot news for the speciality chemical industry right now Companies like BASF Dow Chemicals and DuPont have been at the forefront of speciality chemicals used in solar technologyandhavesetupRampDbasesin China

BASF has gone into process chemicals for the manufacture of solar cells with a new cleaning solution used in producing solar cells The company is working on innovative products for the solar industry which is a key market for them Its niche products are chemical solutions specifically geared to the solar cell manufacturing process as are the cutting fluids used as cooling and lubricating agents apart from special etching and texturing chemicals

20102009

Polycrystalline silicon production expansion in China in 20092010

0

000

10000

1000

20000

2000

0000

34 China solar grade polysilicon industry June 2010 Deep Research Report

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

Polyurethanes are used for quick and Prospects in solar industry economical framing of photovoltaic China offers enviable volumes Beijing panels and solar modules The UV-stable has opened bids to build and run 13 PU system can replace the aluminium solar-energy plants most of which are frames typically used in the past The located in western China These are production process is known as reaction touted as concession projects which injection molding (RIM process) These have 280 megawatts of total capacity polyurethane frames are said to be UV almost equal to the nationrsquos cumulativeand weather resistant installed solar capacity at the end of

2009 according to Bloomberg New Other leading speciality chemicals Energy Finance data36

companies have announced further investments in the solar energy sector These include a 20-megawatt project inLast year DuPont Apollo opened a WuweiplantinGansuprovinceaHamisilicon-based thin-film PV module facility plant in Xinjiang Uyghur Autonomous in China The new facility in Shenzhen Region a Bayannaoer project in Inner from DuPontrsquos wholly owned DuPont Mongolia and a Hetian project in Apollo subsidiary covers 50000 m2 Xinjiang Two separate 30-megawatt andwillhaveupto50MWperyear photovoltaic plants will be started in of capacity for thin-film-on-glass PV Qingtongxia Ningxia Hui Autonomous modules for the domestic Chinese Region and Gonghe Qinghai provincemarket

Chinarsquos position as the worldrsquos top Thin-film PV modules should be the producer of solar panels and wind fastest growing segment of the solar turbines has up to this point largely module industry according to DuPont been built on exports but now its Indeed the company expects to domestic solar demand is burgeoning generate sales of over EUR 650 million The same goes for wind power smart year in the field by 2012 They can help grid systems electric vehicles and a to reduce the cost of producing solar host of other green marketsenergy as they consume only about 05

percent of the silicon metal in traditional crystalline silicon solar cells35

Winds of change Developments in polymersChina has invested heavily in wind power and by the end of 2009 the total installed capacity of its wind-power stationshadreached251millionkWaccounting for 159 percent of the worldrsquos total

The northeast region saw the fastest growing wind-driven power stations in the country The installed capacity in the region had increased from 240000 kWto754millionkWbytheendof2009 By 2015 the capacity in the regionwillclimbto30millionkWwhichwill exceed that of the Three Gorges hydroelectric project

The growth provides tremendous opportunities chemical companies along with many challenges According toestimatestogenerate1MW37 of electricity using wind power at least 8 tonnes of chemicals are required Of this 60 percent consists of advanced polymers and 25 percent resins apart from PVC and wood

Chemical companies are still testing advanced materials to help harness wind energy as a commercially viable renewable energy solution

BASF is developing products for efficiently manufacturing modern wind turbine components such as blades base and tower It is marketing a two-component epoxy resin and hardener system that can speed up rotor blade manufacturing processes by as much as 30 percent The company also offers polyurethane foams additives for PVC foams and polyurethane-based adhesives for enhanced rotor blade stability

In April this year BASF inaugurated a new section at its Technical Competence Center in Shanghai specialising in the epoxy systems for fiber-reinforced composites which are used for wind turbine blades The company sells these systems under its Baxxodur brand The lab is expected to provide BASFrsquos Asian customers technical support tailored to their needs

35 DuPont opens new photovoltaic technical center in China May 2009 DuPont corporate website

36 China solar projects draw interest from 50 companies 12 August 2010 Bloomberg

37 Source CNCIC

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

A vision for sustainable growth | 23

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

BASF also has a Relius coating system plantinWuhanwhichoffersproductsthat can be used from the base to the for the wind industry including rotor blade edge and resists climatic adhesives hand-wet layup and conditions like wind and water UV-rays infusion systemserosion-and flexural load

Auto boom for chemical Dow too has been in the forefront of the manufacturerswind energy industry with operations Chinarsquos auto market has experienced in China catering to local Chinese spectaculargrowthForWesterndemands Dow Formulated Systems chemical majors the challenge started supplying Airstone Systems remains how best to ensure they from its newly built bulk facility in can play a part in this growth story Tianjin in April this year This facility is Whilecarmanufacturersintheconnected with Dowrsquos manufacturing

What KPMG can do management of carbon and therefore costs across the supply

This year KPMG is focusing on the chain promote performance

rapidly growing renewable energy efficiencies and enhance brand

sector and its relationship with value and reputation

chemical companies China is one of the worldrsquos biggest emitters but the bull Formulatingalsquosustainabilitycountry has devoted considerable strategyrsquo that would position a resources to reducing its carbon business to respond commercially footprint Individual companies too to a range of sustainability drivers are undertaking initiatives to adopt both environmentally and socially clean energy practices In the next

bull Workingonacorporatecarbondecade renewable energy will be a

strategy This would entail significant driving force not simply as

understanding the business a sound business practice but as an

implications of climate change industry and growth driver as well

and facilitating the companyrsquos But despite the strong will to adopt strategy development Verifying clean practices and ambitious corporate GHG and CO2 emission targets the capacity of governments reports conducting carbon andcorporatesareoftenlimitedWe valuation and due diligence at KPMG are committed to helping and assessing carbon value enterprises reduce their carbon implications in merger and footprintWehaveaglobalteam acquisition(MampA)transactionswith experts from around the world are also an important part of the to provide professional advice to strategy governments and corporates

bull DesigningacarbonprofilebyKPMG has a two-fold approach calculating the direct carbon to help organisations achieve emissions of the company as well their carbon reduction targets At as the emissions caused along one level it can provide advice to the value chaingovernment-related organisations

bull Makingstrategicdecisionsinon how to strategise and promote

emissions trading or investment sustainable practices At another

in emission reduction projects level it can aid individual companies

Climate change risk management in executing their green agenda and

is also a critical area This includes targets

understanding mitigating and To achieve this there are several managing climate-change risks critical sustainable strategies which which could be physical financial organisations need to implement or regulatory These include

The KPMG team in China endeavours bull Creatingalsquosustainablesupply to address these issues at a time

chainrsquo that would improve the when corporates and governments are moving towards a more sustainable future

European Union and US spent last year struggling with the crippling effects of the recession on their industry China moved to become the fastest-growing automotive market in 2009 soaring a stunning45percentlastyearWhilethisgrowth is expected to slow down in the coming years there are few markets which can boast of a similar size

ManyWesternchemicalmanufacturersare looking for ways to capitalise on this volume and meet the demands of Chinese car manufacturers for innovative technologies and materials that enhance performance reduce fuel consumption and ensure lower emissions

According to industry experts Chinese manufacturers have been quick to adopt new technology compared with their counterparts in other countries and unlike some mature markets are ready to transition from engineering plastics straight to the next-generation of polypropylene compounds

The Chinese governmentrsquos initiative to encourage the development of environmentally friendly cars in particular electric vehicles will put greater emphasis on replacing metal parts with plastic ones Chinese car producers have a large potential to reduce the weight of vehicles by using more plastics In Europe cars use an average of 190kg of plastics while cars in China use an average of less than 100kg38

Companies like LyondellBasell and Lanxess are active in this field Basellrsquos forecasts for this year and the next few for polypropylene (PP) composite materials remain extremely positive especially its lsquoinnovative resinrsquo products like Softell PP compounds used for car interiors Basell has also set up an internationalRampDcentreinShanghaiwhich aims to develop engineering plastics for the automotive markets including for the local market

Germany-based Lanxess is also working in China to provide innovative plasticmetal hybrids and metal replacement solutions These products help reduce weight while cutting down on overall energy consumption and carbon emissions from vehicles These are used for constructing vehicle parts ndash

38 ldquoAsgrowthinChinarsquosautomarketsoarshowcanWesternproducersbenefitrdquo 2 June ICIS

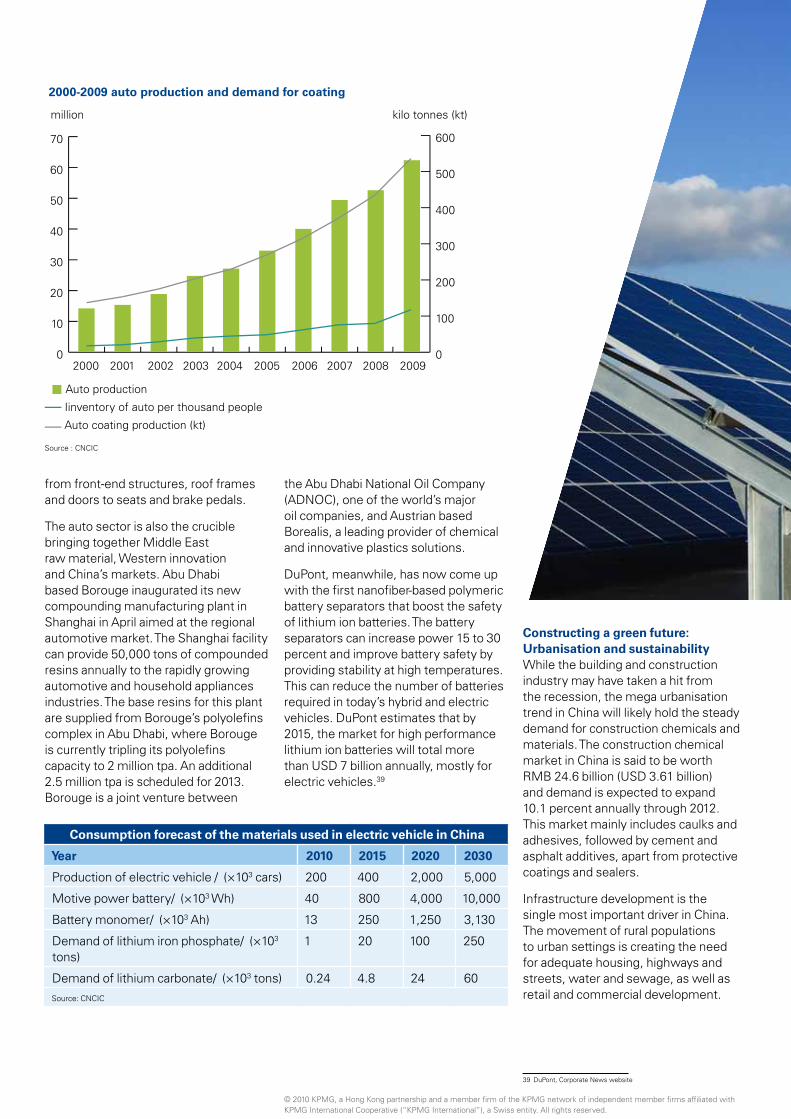

from front-end structures roof frames the Abu Dhabi National Oil Company and doors to seats and brake pedals (ADNOC) one of the worldrsquos major

oil companies and Austrian based The auto sector is also the crucible Borealis a leading provider of chemical bringing together Middle East and innovative plastics solutionsrawmaterialWesterninnovationand Chinarsquos markets Abu Dhabi DuPont meanwhile has now come up based Borouge inaugurated its new with the first nanofiber-based polymeric compounding manufacturing plant in battery separators that boost the safety Shanghai in April aimed at the regional of lithium ion batteries The battery automotive market The Shanghai facility separators can increase power 15 to 30 can provide 50000 tons of compounded percent and improve battery safety by resins annually to the rapidly growing providing stability at high temperatures automotive and household appliances This can reduce the number of batteries industries The base resins for this plant required in todayrsquos hybrid and electric are supplied from Borougersquos polyolefins vehicles DuPont estimates that by complex in Abu Dhabi where Borouge 2015 the market for high performance is currently tripling its polyolefins lithium ion batteries will total more capacity to 2 million tpa An additional than USD 7 billion annually mostly for 25 million tpa is scheduled for 2013 electric vehicles39 Borouge is a joint venture between

Consumption forecast of the materials used in electric vehicle in China

Year 2010 2015 2020 2030

Production of electric vehicle (times103 cars) 200 400 2000 5000

Motive power battery (times103Wh) 40 800 4000 10000

Battery monomer (times103 Ah) 13 250 1250 3130

Demand of lithium iron phosphate (times103 tons)

1 20 100 250

Demand of lithium carbonate (times103 tons) 024 48 24 60Source CNCIC

39 DuPont Corporate News website

Constructing a green future Urbanisation and sustainabilityWhilethebuildingandconstructionindustry may have taken a hit from the recession the mega urbanisation trend in China will likely hold the steady demand for construction chemicals and materials The construction chemical market in China is said to be worth RMB 246 billion (USD 361 billion) and demand is expected to expand 101 percent annually through 2012 This market mainly includes caulks and adhesives followed by cement and asphalt additives apart from protective coatings and sealers

Infrastructure development is the single most important driver in China The movement of rural populations to urban settings is creating the need for adequate housing highways and streets water and sewage as well as retail and commercial development

2000 2001 2002 2003 2004 2005 2006 2007 2008 20090

100

200

300

400

500

600

0

10

20

30

40

50

60

70

2000-2009 auto production and demand for coating

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

A vision for sustainable growth | 25

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

Change Corpcom

According to the American Chemistry to 20 percent in 2006 and is estimated The ministry of construction estimated Council (ACC) the rise of manufacturing to shoot up to 35 percent by 2020 in 2007 that only 5 percent of existing in China has also lead to increased according to a study by the Asia large public buildings had adopted investment for factories and industrial Business Council energy efficiency measures The structures and constructions40 ministry estimates the total cost of

Improving the energy efficiency of retrofitting existing buildings to be Even with the downturn chemical buildings is crucial for China to realise completed by 2020 with energy saving companies have continued to invest in its national energy strategy42 The systems will be 193 billion RMB the development and commercialisation governmentrsquos key target is to cut of construction chemicals which are building energy use in all cities by 50 Shift in material usemore sustainable Now multinational percent by the end of 2010 and 65 As the emphasis on sustainability suppliers of construction chemicals and percent by 2020 using the average increases and more pressure is materials will be hoping that builders in energy efficiency of Chinese buildings applied on governments there is emerging economies will change their in 1980 as the base point Beijing a shift towards reducing the use routine of buying solely on price in order Shanghai Tianjin and Chongqing ndash the of some raw materials common in to switch to higher value speciality four largest cities in China ndash have targets construction chemicals43 These include products41 to cut building energy use by 65 percent formaldehyde phthalates volatile

by 2010 organic compound (VOC) contributors Energy efficient buildings and hydrochlorofluorocarbons (HCFCs)Nearly half of the worldrsquos new building Standardsconstruction will be in China by 2015 In 2005 the government introduced Advanced concrete admixtures not only accordingtotheWorldBankAforecast mandatory design standards aimed at improve the performance of concrete by McKinsey Global Institute estimates conserving energy in public buildings but also its workability thus reducing that China will build a massive 40-billion In 2006 a new voluntary rating system the amount of energy used in its square feet floor area over the next was introduced which also included application According to the American 20 years adding up to 50000 new sustainability aspects such as site skyscrapers Energy consumption planning land use water conservation 40 ldquoUrbanisation trend boosts constructionrdquo ICIS Chemical Business

12 July 2010

by buildings in China grew from 10 and internal air quality 41 ldquoEmerging markets and green building lead construction materials out of recessionrdquo ICIS Chemical Business 18 January 2010

percent of the national total in 1970s 42 Emerging markets and green building lead construction materials out of recession 18 January 2010 ICIS Chemical Business

43 The future of green buildings in China 17 March 2009 Climate

26 | A vision for sustainable growth

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

Concrete Institutersquos International Dow Chemical also formed its Dow Conference on Advancements in Construction Chemicals business unit Concrete Technology and Sustainable in September 2009 which will focus on Development cement consumption providing sustainable building materials globally is expected to more than double to the construction industry The unitrsquos by 2020 to 4 billion tonnes from 2003 Aquaset acrylic thermoset binders levels of 16 billion tonnes with most are specifically designed to replace of that growth coming from developing formaldehyde-based resins in fiberglass countries By then China is projected insulation Dow Construction Chemicals to be producing 60 percent of the inherited the technology from US cement used worldwide For greener speciality chemical company Rohm and use cement can be customised with Haas which Dow acquired in April 2009the help of the supply of supplementary cementitious materials (SCMs) and However monitoring the use of other admixtures to reduce costs and sustainable building methods remains raise the quality of the concrete difficult in China especially in in second-

and third-tier According to industry Low-carbon or zero-emissions watchers the real green building technologies as a major platform revolution in China will start when the for construction business is one smaller cities start adhering to green sector where MNCs are setting up a standards and create a greater demand benchmark and pushing Chinarsquos industry for environmentally friendly building to adopt more sustainable approaches materials

Chinarsquos massive High Speed Railways (HSR-Bullet) project is also consuming a large number of new chemical materials These chemicals play a pivotal role replacing traditional metal cement and wood Third generation concrete admixtures are being used to lay the tracks China will lay over 30000 km of HSR track by 2020 all of which whill be laid on newly constructed concrete structures It is estimated that the project will consume 117 million tonnes of concrete and the country will spend an estimated USD 300 billion on the high speed project44

Dow Chemical is also trying to develop products which are in line with future regulations in China Insulation standards in particular are being upgraded to be more energy efficient worldwide

Dowrsquos wall system is based on rigid and spray polyurethane (PU) foam technologies which can improve the energy performance of an average building by up to 40 percent In China the business introduced its External Insulation Finishing Systems (EIFS) which support Chinarsquos mandate for energy efficiency improvements by 2010

44 A look at Chinas high-speed rail investment 4 May 2010 Solar Feeds News Network

A vision for sustainable growth | 27

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

A vision for sustainable growth | 29

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

Conclusion

China has set for itself not only a goal Multinationals once dealing in bulk of self sufficiency in the petrochemical chemicals are now emphasising their and chemical sectors but it is now green credentials by producing and determined to steer itself up the value researching on high-end speciality chain As the country works on an polymersandnicheproductsWhilethisambitious agenda of reducing carbon addresses the issue of sustainability emissions it becomes all the more it also makes economic sense for important to establish a mature and companies which are trying to capitalise streamlined chemical value chain on the strength of their technological

innovationsA significant part of this blueprint is to ensure that the industry improves In this foreign multinationals have a its processes In this endeavour head-start Most of the big companies RampDisakeystrategywhichthe have undergone a change of philosophy government state-owned enterprises and major internal restructuring to and the innumerable private chemical orient themselves to providing for companies will have to encourage More a sustainable future It can be said investment in research infrastructure at for companies that being green is a every level will be an essential element responsibility and a revolution rolled into of promoting sustainability The success oneof upgrading Chinarsquos chemical value

But a lsquogreen portfoliorsquo also needs a chainwilllieinnurturingthelsquoRampDto

market to survive This is where China is sustainabilityrsquo focus

in a position to make a difference given WithRampDbecomingcentraltothe its sheer volume and will to orient itself industry the Chinese government and to a more sustainable mission Chinarsquos industry decision makers realise this can quick response time will neatly dovetail be executed only through more mergers with the attempts of multinationals to ampacquisitionsandjointventureswith produce a greener economy Foreign foreign companies China is keen to companies are gearing up to see fill the skill and technological gap that how best they can respond to Chinarsquos exists in the high end chemicals sector increasing appetite for high-end

products and how swiftly they can Luckily China has given itself

address the gap in the sustainability tremendous advantages by way of

marketinfrastructure The mega chemical parks built across the nation are now being put to more rational use as they become crucial incubators of technology and talent Foreign ventures have always beenwelcometosetupRampDfacilitiesat the chemical parks attracted by a range of incentives

Green Agenda of Chemical Companies

2015 sustainability goals

Dow Chemical Company

Double the percentage of sales to 10 for products which are advantaged by sustainable chemistry bullReducegreenhousegasintensity25peryearbullReduceenergyintensity25bullPublishproductsafetyassessmentsforallproductsbullAchieveonaveragea75improvementofkeyindicatorsforenvironment

healthampsafetyoperatingexcellencefrom2005baselinebullBuildhighperformanceepoxiesthatenablelighterandstrongerwindbladesbullProduceadvancedfiltrationsystemsthatenablecleanwaterwhereneededbullProvideplasticsandbondingsolutionthatmakevehiclesfuelefficientDataSourcehttpwwwdowcomcommitmentsDOWSustainability

DuPont

bullReducecompanyrsquosgreenhousegasemissionsby15frombaseyearof2004

bullReducewaterconsumptionbyatleast30overthenexttenyearswhererenewable freshwater supply is scarce

bullDoubleinvestmentinRampDprogramswithdirectenvironmentalbenefitsbullIncreaseannualrevenuesbyatleast$2billionfromproductsthatcreate

energy efficiency andor reduce greenhouse gas emissions Data SourceDuPont Sustainability Goals DuPontcom

Sinopec

bullDevelopandusecleancoaltechnologytoreduceCO2emissionbullEngageinmoreRampDtoimproveenergyefficiencyandreduceemissionbullStepupresearchinsubstitutingfossilenergywithbiomassfuelbullMorefocusonsanitationofproductionprocessandcontrollingpollutantsData Source httpenglishsinopeccom Sinopec Sustainable Development Report

ChemChina

bullContinuelsquozeroemissionrsquotargetprograminitiatedin2008bullSetupenvironmentalprotectionplanenergy-savingandemission-reduction

responsibility systems bullMoreemphasisonfuelconservationinhighenergy-consumingsubsidiariesbullFast-tracktechnologicalinnovationandmakestructuraladjustmentto

implement sustainable practiceshttpwwwchemchinacomwpswcmconnectlibchemchinasiteenglishareacareareaenvironment

Sinochem

bullFertilizermanufacturershavereducedaverageelectricityconsumptionby148

bullSinochemShandongFertilizersincreasedproductionby29withzerowastewater emission

bullSinochemChongqingChemicalsincreasedproductionwithnoriseinwastewater emission from previous year COD emission dropped by 175

bullSYRICIinvestedRMB8milliononwastewatertreatmenttechnologyanda desulfurization device reduced waste water by100000 tonnes cut COD emission by 36 and sulfur dioxide by 70

httpwwwsinochemcomtabid713Defaultaspx

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

A vision for sustainable growth | 31

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved

copy 2010 KPMG a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity All rights reserved