Embed Size (px)

Citation preview

Indonesia:A Country Analysis

Prepared by:Adnan Gilani

Jorge MartinezDavid Panzer

Manuel RodriguezCaroline Sheu

April 24, 2000Bus. 487: The Politics & Economics of Development

Professor Marvin Zonis

With thanks to CNA Financial,Deutsche Bank,

Diamond Technology Partners,and Pfizer

for their generous support of this research.

1

Table of contents

executive summary........................................................................................................................................................1

ANALYTICAL FRAMEWORK.................................................................................................................................2

ECONOMIC GROWTH..............................................................................................................................................4

MACROECONOMIC STABILITY......................................................................................................................................4BANK & ENTERPRISE RESTRUCTURING.......................................................................................................................6

Bank restructuring:.................................................................................................................................................6Corporate restructuring:........................................................................................................................................8

COMPETITIVE ADVANTAGE..........................................................................................................................................8

POLITICAL STABILITY.........................................................................................................................................10

JUDICIAL, LEGAL, AND CIVIL SERVICE REFORM......................................................................................................10Reforming the Judicial System..............................................................................................................................10Creating an Effective Civil Service.......................................................................................................................11Establishing the Rule of Law................................................................................................................................12

DEMOCRATIC INSTITUTIONS & THE POLITICAL SYSTEM............................................................................................13Elections................................................................................................................................................................13Indonesia’s government........................................................................................................................................13Role of the Military...............................................................................................................................................14

DECENTRALIZATION...........................................................................................................................................15

APPENDICES.............................................................................................................................................................16

APPENDIX 1 -- MAP OF INDONESIA...........................................................................................................................16APPENDIX 2 -- OVERVIEW OF ASSESSMENT..............................................................................................................17APPENDIX 3 -- MACROECONOMIC VARIABLES...........................................................................................................18APPENDIX 4 -- IMF-MOTIVATED REFORMS..............................................................................................................19APPENDIX 5 -- STRUCTURE OF TRADE.......................................................................................................................20APPENDIX 6 -- 1999 ELECTION RESULTS..................................................................................................................21APPENDIX 7 -- RISK MANAGEMENT IN INDONESIA....................................................................................................22APPENDIX 8 -- PROJECT LOGISTICS...........................................................................................................................23

E X E C U T I V E S U M M A RY

As many of our interviewees characterized Indonesia, “It’s too early to invest today, but too late tomorrow.” While we disagree that Indonesia will be much improved in the near future, we recognize that great rewards can often be achieved during times of great risk. However, based on an analysis of the factors in our model, our outlook for Indonesia over the next four years is pessimistic.

Although Indonesia has achieved macroeconomic stability, it will be difficult for the country to achieve sustainable, long-term growth. There is still substantial cost and effort associated with bank and corporate restructuring, and it is not clear that the Indonesian government has the political willpower and clout to overcome the pain (economic costs and political opposition) associated with restructuring. The debt overhang will continue to hurt existing enterprises and even new ventures. Furthermore, Indonesia has limited competitive advantages compared to its neighbors in Southeast Asia, especially in the area of technical and manufacturing capability.

Fortunately, Indonesia’s transition from the Suharto dictatorship has thus far been remarkably peaceful. President Abdurrahman Wahid has been a strong force for political stability. However, much work remains. The high level of corruption and the inherently slow nature of complicated judicial and legal reforms will make it a difficult environment for foreign investors. There is also substantial risk associated with the upcoming transition from Wahid to a new government, whether it occurs as part of the 2004 elections or earlier. Finally, the decentralization of government power to the provinces, intended to address regional dissatisfaction (including separatist movements), entails a sweeping reform of Indonesia’s government structure. This will introduce further uncertainty, especially since it is not clear that the provinces have the necessary capabilities to govern effectively.

For these reasons, which are analyzed further in this paper, we conclude that there is high risk and limited opportunity for foreign investment in Indonesia over the next four years, especially compared to opportunities in other countries.

1

A N A LY T I C A L F R A M E W O R K

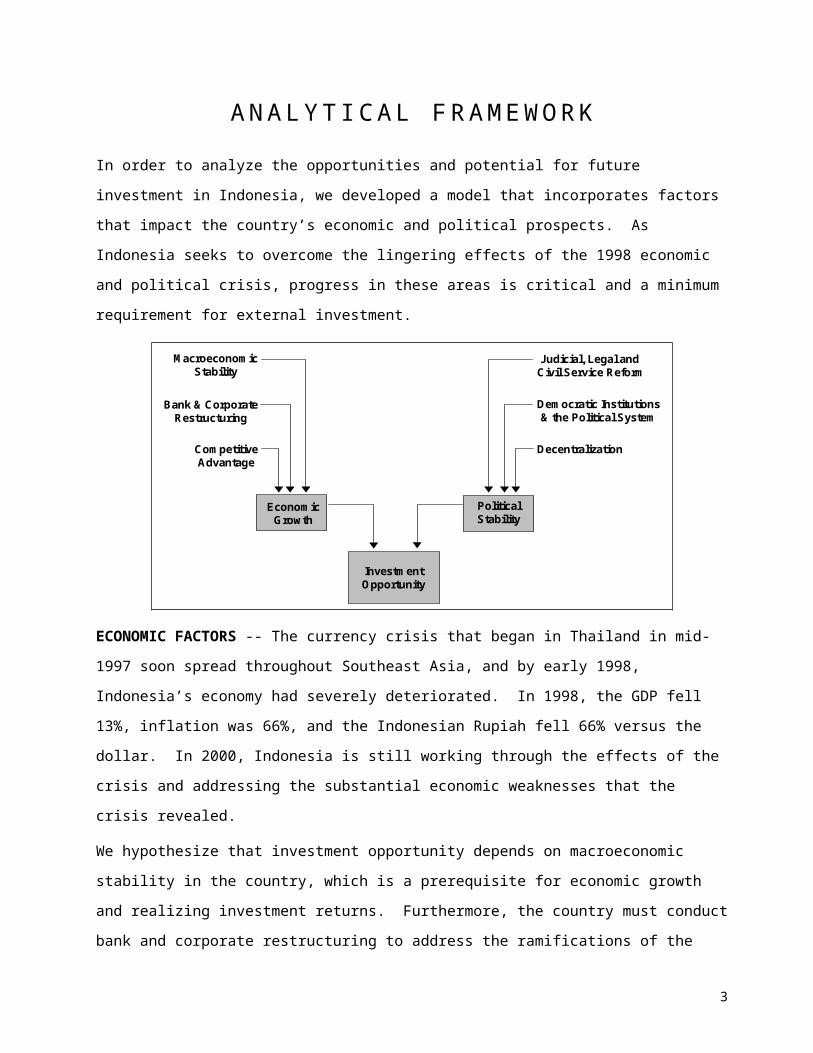

In order to analyze the opportunities and potential for future investment in Indonesia, we developed a model that incorporates factors that impact the country’s economic and political prospects. As Indonesia seeks to overcome the lingering effects of the 1998 economic and political crisis, progress in these areas is critical and a minimum requirement for external investment.

InvestmentOpportunity

EconomicGrowth

PoliticalStability

Judicial, Legal and Civil Service Reform

Democratic Institutions& the Political System

Decentralization

Bank & CorporateRestructuring

MacroeconomicStability

CompetitiveAdvantage

ECONOMIC FACTORS -- The currency crisis that began in Thailand in mid-1997 soon spread throughout Southeast Asia, and by early 1998, Indonesia’s economy had severely deteriorated. In 1998, the GDP fell 13%, inflation was 66%, and the Indonesian Rupiah fell 66% versus the dollar. In 2000, Indonesia is still working through the effects of the crisis and addressing the substantial economic weaknesses that the crisis revealed.

We hypothesize that investment opportunity depends on macroeconomic stability in the country, which is a prerequisite for economic growth and realizing investment returns. Furthermore, the country must conduct bank and corporate restructuring to address the ramifications of the crisis. This is essential for the country to have a healthy financial climate and a viable corporate sector. Finally, for Indonesia to be an attractive investment opportunity, the country must offer compelling competitive advantages or other reasons for investors to single it out.

While Indonesia has now regained macroeconomic stability, we conclude that substantial economic, banking and corporate restructuring remains. Furthermore,

2

Indonesia’s past competitive advantages are now less attractive, although investors that bring the necessary skills can reap rewards while participating in the development of new capabilities in Indonesia.

POLITICAL FACTORS -- Indonesia experienced a unique form of the Southeast Asia crisis. Whereas most of Indonesia’s neighbors had introduced political reforms prior to the crisis, Indonesia had not. As a result, the economic crisis was the impetus for dramatic political reform, i.e., the dissolution of the 30-year Suharto dictatorship. Today, Indonesia is attempting to build a functioning democracy. This requires the reform and/or creation of numerous institutions, such as the judiciary and local government. It has also become clear that the sometimes oppressive dictatorship helped to suppress ethnic and religious tensions. Now that these tensions have risen to the forefront (in the form of secessionist demands and occasional mob violence), Indonesia must adopt a form of government that recognizes the diversity of its population, empowers the populace and provides channels for grievances to be resolved.

Indonesia has broad plans for judicial and legal reform. The country is also gaining experience with democratic institutions and the devolution of power away from the central government. We anticipate that this will be a lengthy process, with a lot of “learning by doing.” As such, there will be lower levels of political stability over the next several years, and foreign investors must deal with this unpredictability.

OTHER NOTES -- Our model does not consider a category of “social factors” to be a primary concern when evaluating investment opportunity in Indonesia. The reason is two-fold. First, we see minimal risk in this area. Although there was an increase in poverty during the 1998 crisis, the government’s relief efforts proved to be very effective. Many observers found Indonesian society to be surprisingly resilient in the face of the crisis, due to population mobility, strong extended families and the abundance of foodstuff that results from Indonesia’s tropic location.1 Furthermore, during the Suharto years, education was of primary importance; in fact, the Minister of Education was typically the most powerful cabinet member. Second, we found that some social factors (e.g., corruption, the implications of religion) were best incorporated into other areas of our model.

However, there is one latent social factor that may impact Indonesia in the future and thus merits a mention. During our interviews, we were told that Indonesia is

3

suffering from an unacknowledged and severe AIDS epidemic. If this is the case, and the government may acknowledge this in the near term, there will be broad ramifications for the allocation of government funds and for the country’s social structure.

In the remaining sections of this paper, we analyze each factor contributing to Indonesia’s economic growth and political stability. While the depth of analysis is limited by the allotted space, this paper explores the key factors that will shape Indonesia’s future and impact the opportunity for foreign investment. We also assess the short term and long term outlook in each area in order to draw conclusions about the prospects for future foreign investment in Indonesia. (Our long-term horizon extends through 2004, the date of the next presidential elections.) Each factor also includes a description of key indicators and the implications for investment.

As suggested in the Executive Summary, we believe that opportunities in Indonesia are best evaluated in comparison to opportunities in other countries. Although this paper does not conduct such a comparative assessment, such analysis should be integral to the decision process of a prospective investor.

4

E C O N O M I C G R O W T H

MACROECONOMIC STABILITY

Short Term Outlook: Indonesia has overcome the macroeconomic effects of the 1998 crisis, allowing the government to focus on deeper economic restructuring and political reforms.Longer Term Outlook: The current signs of economic growth are misleading, because they are merely the inevitable “bounce” following the economic crash. The economic situation remains precarious, because the government has limited fiscal leeway as a result of its huge debt burden. Lasting economic growth will depend on foreign investment and trade, which we suspect is five years away, due to the need for broad restructuring.Key Indicators: GDP growth, levels of foreign trade and investment, and progress in economic restructuring. Implications: Investment opportunities as the economy rebounds, but fiscal austerity and political-economic risk limits the potential.

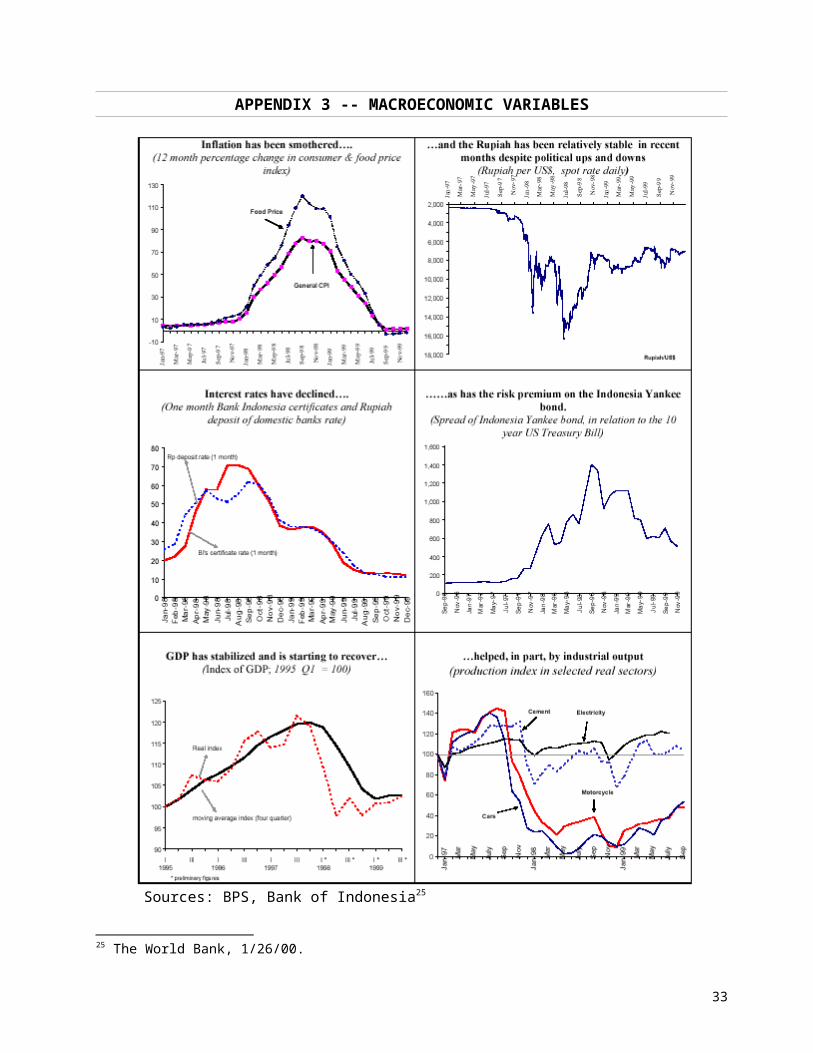

At the least, Indonesia’s macroeconomic environment is solid and stable, and there are signs that it is recovering from the crisis of 1998. This is good news -- compared to Indonesia’s other challenges, the macroeconomy is now of little concern. Key macroeconomic indicators have recovered from the crisis, as shown in the charts in Appendix 3. Inflation is negligible (-0.9% in 1999), the Rupiah is trading within a narrow range, and domestic interest rates have fallen. Interest rates and the foreign exchange swap premium have returned to their pre-crisis levels (domestic rates are 6-7 percentage points above international rates).

The recovery is attributable to two actions: sound monetary management, combined with the initiation of significant institutional reforms (see “Bank & Corporate Restructuring”). However, the current signs of GDP growth (3-4% in 2000) are widely believed to be driven by an increase in domestic consumption, which is a short-term, unsustainable affect. Non-oil exports have been weak, despite the decline in the Rupiah since 1997, so exports are not providing a simple path to recovery.2 Also, total investment contracted by 21% in 1999, and it will take substantial progress in corporate restructuring and improvements in investor confidence for investment to rebound.

In the aftermath of the crisis, the economy has significant excess capacity, which is contributing to the recovery as assets are once again made productive. This over-

5

capacity has several implications. For growth to continue, assets must be returned to use, assuming there is adequate domestic and international demand. However, some of the excess capacity resulted from unwise, and potentially corrupt, investments prior to the crisis. As a result, there is a need for corporations to restructure both their real and their financial assets. While international investment is needed to provide working capital and to help resolve corporate debt issues, international investors also need to contribute management expertise and technology.

Recognizing that foreign investment is critical to future growth, President Wahid is actively encouraging Asian investors to invest in Indonesia, and in 1998, Indonesia reduced regulatory barriers to foreign investment. However, foreign investment has not recovered to pre-crisis levels. (FDI was $4.7 billion in 1997, but -$397 million in 1999.3) Furthermore, domestic investors, who moved their funds to Singapore during the initial stages of the crisis, are just starting to repatriate their funds. Some such investors appear most interested in reacquiring their bankrupt companies at bargain prices, with little intention of necessary restructuring, in order to reestablish the “fiefdoms” that they enjoyed before the crisis. (The IMF has complained that such debtors are often viewed as victims rather than perpetrators.)

As the economy recovers, the poverty rate is slowly declining. The rate had doubled to 20% between Feb. 1996 and Dec. 1998 as the economy fell into disarray during the crisis. Although the rate is now stable and perhaps declining, estimates are that it will take more than five years for poverty to fall to its pre-crisis level.4

A large portion of Indonesia’s economy revolves around oil and gas exports (16% of total 1998 exports). However, in response to the slump in oil markets in the mid-1980s, Indonesia promoted non-oil/gas exports and has thus reduced its dependency on oil and gas. In 1998, Indonesia’s main trading partners were Japan, the U.S. and Singapore, which together accounted for almost half of Indonesia’s imports and exports. Indonesia’s primary imports are intermediate goods (75%), especially industrial raw materials and spare parts.5

Government debt is quite high as a result of the crisis. Debt increased from 23% of GDP in March 1997 to 94% of GDP in March 2000. Three-fourths of the increase was associated with bank restructuring program. Government debt service payments will absorb over 50% of government tax revenues in future years.

6

In 2000, the government anticipates a budget deficit of 4%, a level achieved through increases in taxes and tax compliance, restructuring of foreign debts, and an unanticipated surge in oil prices. Indonesia will must take on additional foreign debt (up to $9 billion) to finance half of this deficit. (Indonesia recently rescheduled $6 billion in existing debt for another 10 to 20 years, leading to an S&P downgrade to “default” status.) The government plans to finance the remainder through asset sales by the bank restructuring program (IBRA). This is an area of significant risk, because as described below, political disagreements and the apprehension of foreign investors hinder the asset sale program. As a result, the government could face a funding crisis. However, the United States and other countries have committed themselves to Indonesia’s recovery (and maturation into the world’s third-largest democracy), so assistance will likely be available in the event of future difficulties.

Organizations such as the IMF are using the release of funds as a club to force the government to finally implement much-discussed reforms. For example, the government has pledged itself to a reduction in fuel subsidies, which is critical to introducing greater market forces and reducing the budget deficit. However, the plan has been delayed by disagreement over the most equitable approach. Thus far, the government has been unable to achieve agreement in this area, and it has frequently abandoned announced plans. It is clear that the necessary economic reforms depend heavily on the political environment. (See Appendix 4 for an overview of IMF-motivated reforms.) For this reason, economic stability depends on the ability of President Wahid to structure a governing coalition that is committed to the difficult, but essential, economic reforms.

In summary, we believe that Indonesia’s macroeconomy has stabilized and is on the rebound from the crisis. However, there are two areas of significant political-economic risk. The first concern is the fiscal strength of the Indonesian government, especially in light of its need to manage debt resulting from the crisis. The second concern is the political will to implement difficult economic reforms. While the country currently offers a stable economic environment, potential investors must recognize that lasting economic growth is possible only if the government implements the necessary reforms and regains the confidence of foreign observers through wise economic policies.

7

BANK & ENTERPRISE RESTRUCTURING

Short-term outlook: Restructuring will continue at a slow pace, likely just fast enough to appease foreign lenders such as the IMF. Many changes will be cosmetic.Long-term outlook: Bank and corporate restructuring will achieve momentum. However, this depends on judicial reforms that guarantee the rule of law and regulatory reforms that enforce corporate/bank accountability, as well as a high degree of political resolve to spur the processKey Indicators: Asset sales by IBRA and progress in bank privatizations. Dissolution of the most insolvent banks. Transparency of bank reporting.Implications: As long as bank restructuring does not progress, companies won’t have access to local lending, and doing business in Indonesia will be more expensive and risky. Slow corporate restructuring would also delay the interconnected bank restructuring, and it would hinder the formation of a flourishing domestic business sector.

Our interviewees frequently emphasized the same point: one of the most important short-term objectives must be to restructure the banking industry and corporations. Currently, Indonesian companies cannot access credit, and no modern economy can operate without credit and financial flows. Improved corporate creditworthiness, which is crucial to achieving sustained economic growth (and avoiding a repeat of the conditions that precipitated the crisis), will require debt and operational restructuring. Also, corporate and bank restructuring are so linked that the progress in one, or lack off, inevitably impacts the other.

BANK RESTRUCTURING:Although everyone recognizes the importance of restructuring the banking sector, it is now more than two years after the crisis and the work has just begun. As a result of the crisis, 66 of the 160 private banks were closed. The state took over twelve banks and, together with the owners, recapitalized eight more. IMF involvement was also critical to the unfolding of events in the banking sector. In response to the crisis, the IMF required Indonesia to reduce liquidity, which increased the number of bankruptcies and further damaged the banking sector. The IMF recommended closing the initial 14 banks. Since each of these 14 banks was partially owned by a member of the ruling Suharto family, their closure demonstrated that no bank was safe from closure or government takeover. Therefore, many banks and companies transferred their remaining assets to foreign countries, especially Malaysia, further worsening the situation.

8

As a result of the bank closures and state intervention, private domestic banks account for only 15% of the banking system today versus a historical 50%. At the same time, state banks now account for 75% of the liabilities of the banking system and 90% of its negative net worth, making the state the most important player in the industry by far.

Another important player in the restructuring process is the Indonesian Bank Restructuring Agency (IBRA), an independent agency created to restructure troubled banks and their assets. Today, IBRA is the third largest non-bank financial institution with assets worth more than US$ 60 billion. The process of liquidating assets, other than cars and paintings, has been terribly slow. The Astra automotive group was a significant asset to be sold. This disposal occurred only in March, and it required two auctions, since the first winners finally withdrew after deciding the situation was untenable. Non-official sources have told us that the main obstacle to restructuring is the political implications, since most of the assets were owned by large, powerful conglomerates that are trying to recover them at an significant discount.

The shift of banking assets to the state was a required measure in the short run to prevent a total collapse. However this is neither desirable nor healthy for long-term development. The bank reform process will encounter the following challenges over the next several years:

Restructuring and privatizing state banks: Bank restructuring is an urgent issue -- the monthly cost of not restructuring banks is estimated to be least US$ 600 million. But progress is slow. For example, the government has not followed through on its plans to merge four banks with Bank Mandiri. The IMF recommends that half of the remaining state banks should be privatized by the end of 2000, with all privatized by the end of 2002. One of the major obstacles is that responsibility falls ambiguously between the Ministry of Finance and the Ministry of State-Owned-Enterprises. As long as there is not a specific, motivated institution responsible and accountable for privatization, we do not believe there will be much progress.

Increasing bank supervision: Bank distress was caused to a large extent by a total lack of supervision by the central bank. This led to one of the most expensive bank bailouts in world history, over 50% of GDP. The following scenario illustrates a common technique that contributed to the crisis.

9

Company X would estimate the cost of a project to be $100M. They would tell the bank, owned by the same corporation as Company X, that the project cost was $600M. The bank would lend $150M, thus apparently this new project (or company) had a D/E of .33, which might seem reasonable. Company X would invest $100M and deposit $50M in their accounts (in foreign banks when things turned sour). The result is a company with negative equity (and nothing to lose in case of bankruptcy). 6

Accelerating asset recovery: As mentioned, IBRA has a huge amount of assets under its control. Liquidating them is urgent to restore the assets to productive owners and generate revenue to assist in the bailout. However, this liquidation is a particularly complex and sensitive task. Liquidation has to be done with no political interference and in a truly transparent way. If this is accomplished, it will set standards of transparency for the rest of the banking industry.

CORPORATE RESTRUCTURING:Corporate restructuring is not at a standstill due to a lack of framework but due to a lack of implementation. By June 1999, only 80 bankruptcy cases had been registered, compared to thousands in Korea. Even though bankruptcy laws have now been revised, most court rulings have proved to be contentious and arbitrary. Corruption of the judiciary is a key obstacle. Under Suharto’s regime, judges and many other officials would purchase their positions (i.e. the chief of police position was worth $2 million). After buying his position, a judge has to recover his “investment” by issuing rulings based on bribes. This process seems to be impacting bankruptcy cases: all of the bankruptcy claims made by banks have gone to one Jakarta court, with the same judge presiding and the same lawyer defending. For example, Bankers Trust filed a case requesting payment of $50 million because of fraud committed by the borrower. Not only did BT recently lose the case, but it was forced to pay $50 million in damages to the defendant!

In summary, bank and corporate restructuring is critical to Indonesia’s success. Assets held by the government must be transferred to the most productive owners, and companies must have access to credit. The regulatory environment must be transformed to prevent the illicit dealings that led to the crisis. Until these issues are addressed, the Indonesian banking and corporate sectors will be inhospitable to foreign investors. At this time, we believe investors still face great difficulty in choosing viable partners and suppliers, in conducting domestic financial transactions, and in operating in the capricious regulatory and legal environment.

10

COMPETITIVE ADVANTAGE

Short Term Outlook: Government reforms will (rightly) transform the natural resource extraction industry, introducing uncertainty for current and potential investors in Indonesia’s most prominent sector.Longer Term Outlook: Investors will start to capitalize on two key opportunities: filling in the gaps in Indonesia’s industrial structure and selling to the lucrative domestic market.Key Indicators: Domestic purchasing power and the composition of imports/exports.Implications: Foreign investors must supply management and technical skills and must overcome several disadvantages compared to other Southeast Asian countries.

Indonesia’s historical advantage has been in its abundance of natural resources. As shown in Appendix 5, a large portion of Indonesia’s exports consist of fuels, ores and metals, as well as agricultural products such as timber and food products. Because it lacks value-added industries to transform these raw commodities prior to export, Indonesia is missing an opportunity to earn additional revenue and increase the productivity of its workforce. Instead, the country must import an unusually high proportion of value-added, manufactured goods, many of which are produced by neighboring countries utilizing Indonesia’s raw materials. (As noted earlier, intermediate goods, especially industrial raw materials and spare parts, comprise 75% of Indonesia’s imports.) As shown by the chart in Appendix 5, Indonesia’s scarcity of value-added industry is especially evident when comparing exports by Asian countries.7

Indonesia’s lack of domestic value-added industries has constrained international investment in the past. For example, the Astra automotive group must import a large proportion of its components from foreign sources, allowing it to focus primarily on vehicle assembly in Indonesia. However, some observers report that the lack of value-added manufacturing could be an area of opportunity for foreign investors who are able to supply capital and, more importantly, technology.

While Indonesia has abundant natural resources, they will not be as easily exploited as in the past. The Indonesian national government is increasing supervision to avoid past abuses (ethical and environmental), to ensure that contracts are awarded without corruption and to ensure that the public collects its share of royalties. Furthermore, with their increasing autonomy, provincial governments are especially

11

interested in ensuring that foreign investors deliver a high return (royalties, infrastructure investments, etc.) to the local region. In fact, as regions gain authority through the decentralization process, there are examples of regions imposing stringent requirements on existing and new investors, a policy that seems to have an aspect of retribution to redress past inequities. For example, Newmont Mining recently agreed to pay disputed back taxes to a local government. To settle the dispute, Newmont also agreed to contribute $1.5 million to establish a community foundation and another $1 million annually for community development.8

Several factors make Indonesia attractive for international investment. The workforce is literate, motivated and amenable to hierarchical organization, as attested to by foreign corporations currently doing business in Indonesia. Infrastructure, especially on the central islands of Java and Bali, where 62% of the population resides (on only 7% of the country’s total land area), is in adequate shape. While travel can become more difficult as you move away from Jakarta, it is still adequate for a developing country, and the government is continuing to make investments (to the extent that its fiscal limitations allow). Of course, transportation in more remote regions, particularly among the many islands, is much more difficult.

Finally, the sheer size of the domestic market -- almost 210 million people, with 76 million in urban areas -- makes this a very attractive market in terms of the potential for domestic sales. According to the World Bank, Indonesia had a 1997 per capita GDP (PPP method) of $3390, which is greater than China ($3070) and much greater than India ($1660). In this respect, the country is wealthier than many people initially suspect (roughly comparable to many countries in South America and Eastern Europe), and Indonesia could comprise an attractive consumer market.

12

P O L I T I C A L S TA B I L I T Y

JUDICIAL, LEGAL, AND CIVIL SERVICE REFORM

Short-Term Outlook: A complete overhaul of the judicial, legal, and civil service systems will be impossible; however, the government can take immediate steps, such as raising government salaries and replacing the old guard, to help reduce corruption and increase competence in the short-term.Long-Term Outlook: Fundamental reform is certainly possible; however, it may take decades, given that over thirty years of Suharto-era corruption must be undone. Key Indicators: Successful prosecution of bankruptcy cases; publication of court decisions; utilization of disciplinary mechanisms for the legal profession; higher legal education standards, higher entry requirements, and transparent promotion procedures; higher performance-tied compensation, establishment of judge rotation system, and annual asset disclosure requirements.Implications: Investors will encounter significant corruption and arbitrary legal and regulatory proceedings.

For three decades, Indonesia’s authoritarian government promoted economic growth without developing the necessary accompanying institutions. Then when the Southeast Asian economic crisis occurred in conjunction with Indonesia’s political transition, Indonesia’s weak institutions failed to respond quickly and justly to the crisis. According to The World Bank,

“[w]eak governance has, if not caused, at least exacerbated the economic crisis from which Indonesia is only just emerging. It spawns corruption, which exacts a toll on all dimensions of the economy. On some counts, corruption in Indonesia costs the country as much as 2 percentage points in annual growth since the mid-sixties. It tends to benefit the rich and tax the poor. It adds to the cost of doing business. It eats into the moral fiber of society.”9

By building strong institutions, the country will be better able to absorb future external shocks to the economy. In fact, The World Bank contends that investing in institutions, rather than physical capital, might actually yield higher social and economic returns.10 While many areas are in need of institutional development, we believe the two critical ones are the judiciary and the civil service, detailed further below.

13

REFORMING THE JUDICIAL SYSTEMFirst and foremost, the reformation of the judiciary is critical to bank and enterprise restructuring. An inept and corrupt judiciary can act as a key bottleneck to quick economic recovery. For instance, IBRA has recently lost several bankruptcy cases against recalcitrant debtors (including the high-profile Bank Bali scandal), despite mounting pressure from the IMF to restructure the country’s $65 billion private debt in return for massive foreign aid. “As long as the courts do not show fair treatment, I don’t really see a lot of hope,” declared Agustus Sani Nugroho, IBRA general counsel and senior vice president.11 Preliminary research by Indonesian Corruption Watch (ICW) claims that only five of the 41 supreme justices in the Supreme Court – the country’s highest court – cannot be bought.12 According to an article written in The Jakarta Post, several young lawyers admitted that bribery was a part of their daily legal work.13 Some lawyers, however, support the longstanding practice: “[judges] only take money from one side and once they receive the money they will never let you down, no matter how impossible the case may seem…It’s first come first served.”14

Several important reasons explain the deep-seated corruption that pervades the country’s judicial system. First, judges are severely underpaid. Even after a 100% salary hike, judges take home only Rp 3 million ($400) per month, while a supreme justice receives only Rp 10 million. Second, judges are overworked. The backlog of cases compels lawyers to oil the wheels of the judicial system. Finally, the judiciary lacks a formal external watchdog. The Supreme Court, although corrupt itself, is the only monitoring body for all the judges in the country.15 Without any accountability, corruption in the courts will continue.

Fortunately, the Indonesian legal profession has already invested considerable thought into analyzing the weaknesses of the legal and judicial system. Recommendations for comprehensive reform include better remuneration of judges, higher entry standards for legal practice, enforcing disciplinary measures, publishing more detailed court decisions, and higher quality of legal education. The government has taken some of the aforementioned recommendations. For example, a special task force in the Attorney-General’s office has been created to investigate and prosecute corrupt judges. Furthermore, the government recently announced plans to reassign up to two-thirds of judges in the capital – including all the chiefs and deputies of the five district courts – to other courts outside Java.16 While such

14

an initiative could reduce corruption in the short-run, fundamental structural changes are necessary in the long-term.

In recognition of this long-term need, on February 16, 2000, Wahid established the National Law Commission to examine the state of legal development and make specific recommendations. The Commission will analyze the justice system, the civil service system, the legal profession, provincial legislation, economic laws, and human rights. Unfortunately, the Commission does not have the mandate to actually implement its recommendations. This is up to the legislature.

CREATING AN EFFECTIVE CIVIL SERVICE Indonesia’s civil service is also prone to corruption. According to the 1999 Transparency International Corruption Perceptions Index, Indonesia is tied for 96 out of 99 countries.17 The reasons appear to be similar to the judiciary – low salaries, poor performance management, and lack of accountability. The salaries of civil service clerks, for instance, are about half of their private sector counterparts while directors-general are about one-tenth to one-fifteenth. As a result of this salary gap, the following phenomena have emerged. First, development budgets and projects are used to pay civil service employees – through honoraria, management and consultant fees, board membership fees, and other function-related pay. Second, kickbacks from contractors are distributed through an elaborate patronage system. Third, since actual income has little to do with performance, the quality of civil service has suffered. Simply raising the salaries of civil servants, however, will not solve the problem (and will also bankrupt the government). Such plans must be accompanied with proper performance incentives and corruption penalties. In addition, the number of civil servants must be reduced while the quality must be raised.18

Indonesia has taken several steps to reform the civil service. Efforts include a new civil service law and an anti-corruption law. Actually implementing such laws, however, take a considerable amount of time and resources. For example, for the anti-corruption law to be effective, the State Audit Commission must have the proper technical training, organizational support, and incentive structure to track the assets and income of all civil servants. Moreover, the commission must be linked effectively with the police and the Attorney-General’s office so that abuse can be followed by quick legal action.19 Similar to the judicial system, reformation of the

15

civil service system is a slow and painful process that requires modification of both structural incentives and cultural attitudes. Thus, foreign investors should expect fundamental reform to take place over generations to come.

ESTABLISHING THE RULE OF LAWDuring the Suharto era, no single financially significant company obtained a contract without some quid pro quo. Foreign corporations received favorable investment terms year after year, operating their mines and oil fields and pulp mills and plantations with minimal concern for the surrounding communities and the environment. Most foreign governments, business leaders, and advisers have now warned that if Indonesia fails to uphold its existing contracts, the country will lose credibility with international investors.

Even under foreign legal systems where the rule of law reigns supreme, many of these contracts might be deemed invalid and unenforceable. For example, a party who wins a contract through unlawful means (i.e., bribery and gift-giving) may not receive any contractual protection under the law. Many existing investment agreements are tainted by evidence of collusion and conflict of interest. As foreign companies seek to maintain their suspect contracts, President Wahid is attempting to insure that Indonesia upholds the rule of law, while salvaging some of the country’s national resources that were sold off to the biggest international gift-givers. Wahid’s approach of requesting additional consideration in exchange for honoring corruption-induced contracts may be the most workable short-term compromise.20

Indonesia’s decision to not enforce unfair contracts does not necessarily indicate that future, fair agreements will be broken. However, we are still concerned about the country’s legal and judicial capacity to enforce fair contracts. As the above analysis indicates, reformation of the judiciary and civil service, along with the application of the rule of law, is a long-term process that cannot be completed within the next 3-5 years. Indeed, over three decades of Suharto-era corruption must be undone. According to Mardjono Reksodiputro21, the law was used primarily as a tool to implement Suharto’s policies. The military viewed “law” as whatever their commander said it was. In other words, law was a means to an end rather than an end in itself. Thus, the entire legal infrastructure, as well as cultural and societal values, must be altered.

16

DEMOCRATIC INSTITUTIONS & THE POLITICAL SYSTEM

Short Term Outlook: Assuming President Wahid remains solidly at the helm, the political transition will continue smoothly.Longer Term Outlook: The major consideration is the health of Wahid and his ability to complete his term (through 2004). If his health wanes, a succession battle is likely, as his Vice President is considered incapable of running the country. If he does complete his term and elections are held as scheduled, his legacy will be the stability he brought and the democracy he helped nurture.Key Indicators: MPR vote in summer 2000; health of President Wahid.Implications: A difficult political transition could lead to social unrest, as well as changes in current government policies.

ELECTIONSIn 1999, Indonesians for the first time changed their government through an open, transparent democratic process. The June 7, 1999 parliamentary election, contested by 48 political parties (who fielded candidates in every district), was widely accepted as open, fair and free. The chart in Appendix 6 shows the results.

The MPR (the upper legislature) is constitutionally the highest authority of the State and meets every five years to elect the president and vice president and to set the broad guidelines for state policy. In October 1999, the MPR elected Abdurrahman Wahid as President and Megawati Soekarnoputri as Vice President.

As in the Suharto era, the military has significant sociopolitical as well as security roles. Members of the military are allotted unelected seats in the DPR (the lower legislature) and in provincial and district parliaments, in partial compensation for not being permitted to vote. Active duty and retired officers occupy important positions at all levels of government. The military thus far has resisted strong pressure from student and reform groups for an immediate end to this arrangement, but incremental change is likely over the next several years.22

INDONESIA’S GOVERNMENT President Wahid heads Indonesia's largest Muslim organization, the NU, which has 30 million members. Wahid’s position as a moral leader was transformed when he and his supporters formed the National Awakening Party (PKB) following the Suharto’s fall. While NU is a conservative religious organization, Wahid has consistently maintained that faith is a personal matter. In the unrest after Suharto, some politicians called for Islam to have an institutionalized role in the state. While

17

some Islamic leaders have been critical of Wahid’s stance, he has gained the respect of many non-Muslims throughout Indonesia, including the Christians and ethnic Chinese. Perhaps more significantly, Wahid has forged links with the influential military elite.23

Wahid previously had close ties with Megawati. Before the election, she considered him one of her key allies, a man who could deliver a huge Muslim following but would be content to follow secular policies. During the campaign, Wahid, Megawati and Amien Rais, Wahid's rival Muslim leader, brought their parties together in the name of safeguarding the democracy process. However, the joint front did not last, and Wahid later argued that a female president would offend conservative Muslims. Relationships soured further as Wahid came to regard Megawati as arrogant and unable to work with other politicians. (Megawati gained the vice-presidency only after widespread protests by her supporters over her defeat for the presidency by Wahid.)

The new government cabinet has been hailed in the international media as a “break from the past,” but its composition reveals the opposite: the Armed Forces (TNI) and the Golkar Party—the two pillars of Suharto's regime—have a powerful presence and continue to hold all the key security ministries. The cabinet resulted from Wahid’s deals with Golkar, the army and a Rais’s coalition of Islamic parties in order to win the presidency. Wahid repaid his debts by allowing his allies to deliver cabinet positions to their supporters.24

By many accounts, Wahid has exceeded all expectations. A skilled political operative, he has excelled in his balancing act during this tumultuous time of political consolidation (which is still only in its early stages). Many believe that he is the only one who can bring about a smooth transition. However, his health is his most significant handicap -- and the greatest political risk for Indonesia. (A brain hemorrhage in 1998 led to his near total blindness). If Wahid’s health wanes (an unfortunate but realistic assumption), there is no clear successor. In the aftermath of the 1999 elections, Megawati is now widely perceived as incapable of leadership. Her initial goodwill, which came through during the election as a result of her family name and the general discontent with the Suharto era, is on the decline. In fact, the MPR will likely change the rules when it meets in summer 2000 in order to keep Megawati from readily assuming the presidency. While the MPR currently

18

votes for the President every five years, they will likely change this “vote of confidence” to occur annually.

Amien Rais is also mentioned as an alternative for the presidency. He wields substantial power through his cabinet appointees, his religious following and his deal-making savvy. However, although it is likely that he will play the role of king-maker again, his is too right-wing to garner the support of moderates, who comprise the majority of the electorate. A seldom-mentioned player is the chairman of Golkar, Akbar Tandjung. Wahid originally selected him as his vice-president but chose Megawati to appease her very vocal supporters.

ROLE OF THE MILITARYFor the last four decades, the military legitimized the authoritarian regime of president Suharto and implemented public policy. In fact, the military has been in charge of duties that usually belong to the civil society in democratic countries. Until recently, the military seemed to be a threat to the new democracy. However, Wahid has been successful in reducing the power of the military. For example, he appointed a civilian to run the Ministry of Defense, and he forced General Wiranto, who had been Suharto’s military commander, to resign. Despite rumors of an impending coup in early 2000 (during the height of the Wahid/Wiranto conflict), most observers now believe that a coup is very unlikely. Wahid enjoys the support of most of the military, as well as support from the general population and the international community.

Investors should also recognize the military’s significant involvement in business, which results from concessions it received during the Suharto regime as a source of further income. This involvement will decline when the country succeeds in creating more transparent legislation and open contracts.

DECENTRALIZATION

Short term: Despite its plans, the government has achieved little with the decentralization process. Indonesia’s lack of institutions and skilled people outside Jakarta makes decentralization difficult.Long term: Decentralization is key to maintain governance under such a diverse country. Thus, we could reasonably expect a higher level of autonomy of the

19

provinces in the following years, but complete decentralization is a process that will take over 5 years.Key Indicators: Creation and strengthening of local institutions.Implications: Decentralization is essential to address regional grievances; delay could exacerbate social and political tensions.

The Indonesian government has historically dictated public policy from Jakarta, even policies that affect distant provinces. Currently, the central government is responsible for over 80% of national spending. Because of their limited role in governance, the provinces lack strong institutions and hold significant resentment

1 Several of our interviewees commented that Indonesia’s lush, tropical environment mitigates poverty (starvation is rare when fruit grows abundantly).2 According to World Bank data, Indonesia’s exports fell 10% in 1998 and remained constant in 1999.3 “Indonesia Quarterly Update.” The World Bank, 3/20/00.4 “Indonesia: Seizing the Opportunity -- Economic Brief for the Consultative Group on Indonesia.” The World Bank, 1/26/00.5 “Indonesia Country Profile.” The Economist Intelligence Unit, 1999-20006 This scenario is not exaggerated; we interviewed executives of an import/export agency (owned by the son-in-law of Suharto), that had no assets and debt of more than $200M.7 World Bank Development Indicators, 1999.8 “Newmont Reaches Settlement With Indonesia's N. Sulawesi.” Asia Pulse newswire, 4/20/00.9 The World Bank, 1/26/00, p. 13.10 “Indonesia: From Crisis to Opportunity.” The World Bank. 7/21/99, p. 3.1.11 Chew, Amy. “IBRA Sees Slow Indonesia Debt Progress.” Reuters, 4/10/00.12 Unidjaja, Fabiola Desy. “Payoffs Prominent in Court System.” The Jakarta Post, 1/22/00, p.2.13 In fact, one lawyer claimed that at the Jakarta provincial court, judges do not even look at your case if you cannot come up with at least Rp 75 million ($10,000). Another attorney recounted the time he represented a business tycoon in a trillion rupiah bank scam: “I remember carrying the suitcase containing all the money. I also handed it over to the judge himself.”14 Unidjaja, Fabiola Desy, p. 2.15 Unidjaja, Fabiola Desy, p. 2.16 “Jakarta Judges Moved Around in Major Government Shift.” The Jakarta Post.com, 4/20/00.17 The higher the ranking, the higher the perceived level of bribery by the 770+ senior executives of multinational companies surveyed.18 The World Bank, 1/26/00, pp. 14-15.19 The World Bank, 1/26/00, p. 16.20 In the recent tax dispute between gold mining company PT Newmont Minahasa Raya, a subsidiary of American mining company Newmont Mining corporation, and the local government of North Sulawesi, the parties agreed to an out-of-court settlement, whereby the government would drop its lawsuit and honor the contract in exchange for $500,000 in overdue taxes and a $1.5 million contribution to the local people (plus an additional contribution of $1 million per year for three years in community development programs). “Newmont Reaches Out-of-Court Settlement.” The Jakarta Post.com, 4/20/00.21 Professor of Law at the University of Indonesia and Secretary of the National Law Commission.22 United States State Department.23 Asiaweek.24 United States State Department.

20

toward center. Regardless of the efforts and good intentions of Wahid, it is unlikely that the planned decentralization will occur soon. A lack of institutions and skilled people outside Jakarta complicates the process, and it is questionable whether the central government would give more taxing and spending autonomy to the provinces, especially to the richer ones, since this would limit the current policy of redistribution.

Legislation has already been implemented that seeks to return over 40% of spending to lower levels of government, but these new laws are still incomplete. For decentralization to succeed, there must be strong institutions and skilled managers at the regional and local level. The central government will likely have to relocate numerous officials from Jakarta to the provinces. The central government must also develop guidelines to hold local authorities accountable for the administration and exercise of their resources. There is also confusion about the division of responsibilities between the central government and local governments.

Another important factor is the separatist movements, some involving isolated violence, in several regions of Indonesia. These movements range from the recently successful independence of East Timor to separatist movements in Aceh , Irian Jaya, and Kalimantan, to frequent rioting in Jakarta, and to religious intolerance in Lombok. The separatist sentiment arises from the fact that in the aftermath of the Suharto regime, many groups in Indonesia want greater control of their lives and a greater share of the revenues that they generate. This is a major issue for Wahid to resolve, because the secession of a separatist group could mean a major loss of revenue (e.g., natural resources) for the country and would set a precedent that would strengthen other separatist movements. This is a great risk for Indonesia, because while the population is concentrated on the island of Java, the remote provinces generate much of the national income through natural resource extraction. For this reason, if separatist movements succeed, it could lead to the disintegration of the country and the impoverishment of much of the population. However, we believe this scenario is very unlikely. The central government recognizes the critical nature of this issue and is introducing decentralization policies to address the grievances.

21

A P P E N D I C E S

APPENDIX 1 -- MAP OF INDONESIA

Source: The World Factbook 1999. The Central Intelligence Agency.

22

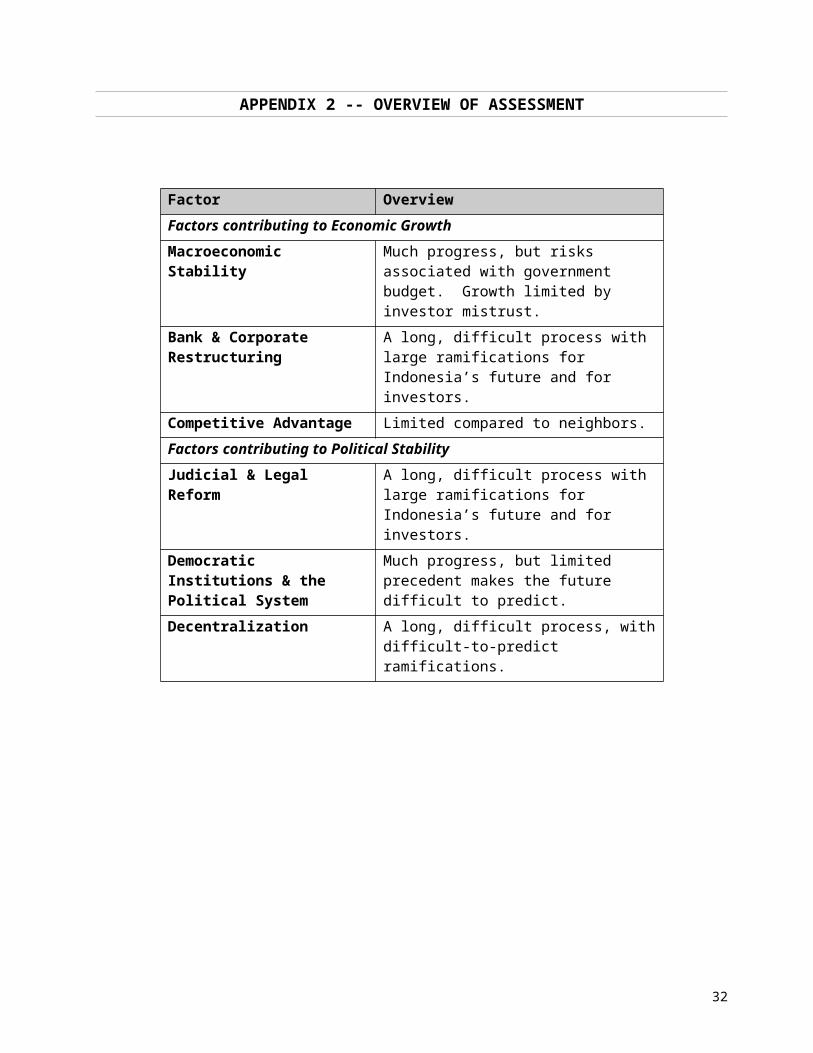

APPENDIX 2 -- OVERVIEW OF ASSESSMENT

Factor Overview Factors contributing to Economic GrowthMacroeconomic Stability

Much progress, but risks associated with government budget. Growth limited by investor mistrust.

Bank & Corporate Restructuring

A long, difficult process with large ramifications for Indonesia’s future and for investors.

Competitive Advantage Limited compared to neighbors.Factors contributing to Political StabilityJudicial & Legal Reform A long, difficult process with large

ramifications for Indonesia’s future and for investors.

Democratic Institutions & the Political System

Much progress, but limited precedent makes the future difficult to predict.

Decentralization A long, difficult process, with difficult-to-predict ramifications.

23

APPENDIX 3 -- MACROECONOMIC VARIABLES

Sources: BPS, Bank of Indonesia25

25 The World Bank, 1/26/00.

24

APPENDIX 4 -- IMF-MOTIVATED REFORMS

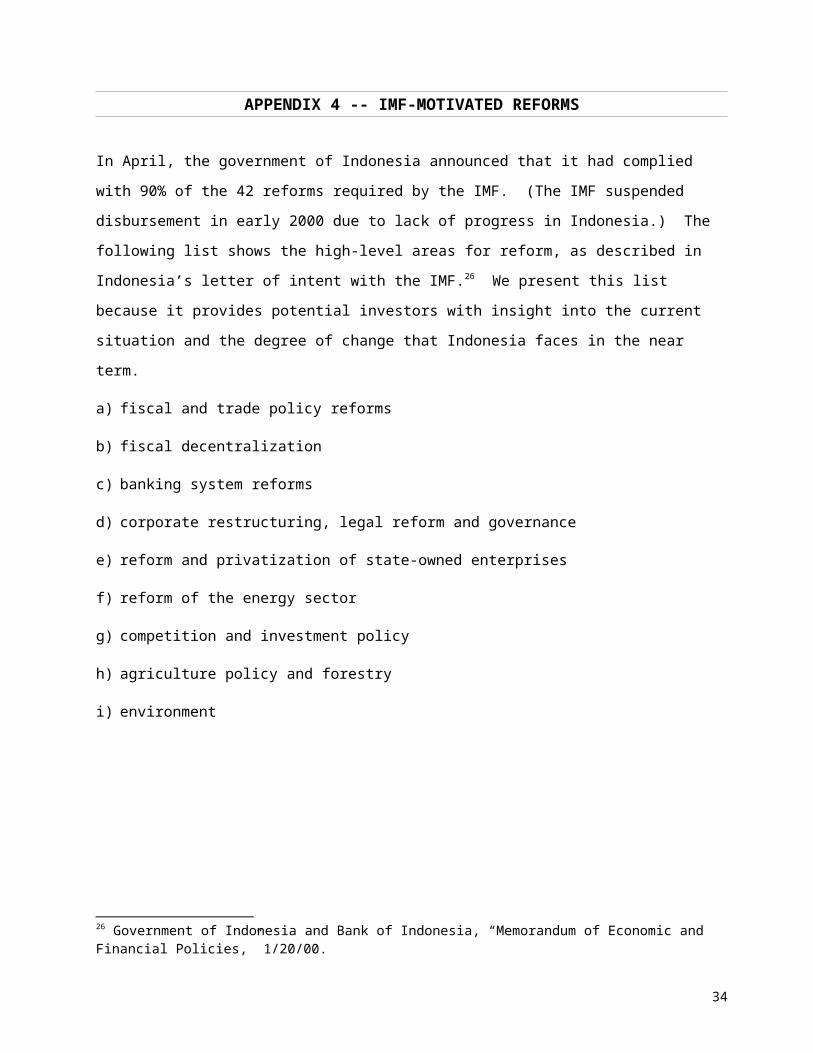

In April, the government of Indonesia announced that it had complied with 90% of the 42 reforms required by the IMF. (The IMF suspended disbursement in early 2000 due to lack of progress in Indonesia.) The following list shows the high-level areas for reform, as described in Indonesia’s letter of intent with the IMF.26 We present this list because it provides potential investors with insight into the current situation and the degree of change that Indonesia faces in the near term.

a) fiscal and trade policy reforms

b) fiscal decentralization

c) banking system reforms

d) corporate restructuring, legal reform and governance

e) reform and privatization of state-owned enterprises

f) reform of the energy sector

g) competition and investment policy

h) agriculture policy and forestry

i) environment

26 Government of Indonesia and Bank of Indonesia, “Memorandum of Economic and Financial Policies,” 1/20/00.

25

APPENDIX 5 -- STRUCTURE OF TRADE

Foreign Trade -- ExportsFood and

agricultural raw materials

18%

Fuels, ores, and metals33%

Manufactures49%

Foreign Trade -- ImportsFood and

agricultural raw materials

14%

Fuels, ores, and metals13%

Manufactures73%

Manufactured Exports as a % of Total Merchandise Exports

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Japa

n

Kor

ea, R

ep.

Hon

g K

ong,

Chi

na

Ban

glad

esh

Chi

na

Sin

gapo

re

Mal

aysi

a

Indi

a

Thai

land

Phi

lippi

nes

Indo

nesi

a

data source: World Bank World Development Indicators, 1999 (using 1997 country data)

26

APPENDIX 6 -- 1999 ELECTION RESULTS

As evident in the chart, Wahid’s party won only 13% of parliament seats, and thus his accession to the Presidency was unexpected.

27

APPENDIX 7 -- RISK MANAGEMENT IN INDONESIA

In our discussions with a major international bank in Indonesia, the bank provided the following risk management areas that any foreign investor must consider.

a) selection of a local partner -- A local partner is essential to navigate the complex local environment. Some foreign investors have selected partners based on cursory, superficial investigation, only to discover that they have been taken advantage of.

b) acquisition of land -- Land titles are complex, and it is difficult to acquire a clear title.

c) application of law -- Foreign investors should not rely on the application of law to resolve disputes.

d) changing markets -- Changing government policies (including subsidies) can drastically change the competitive environment, thus changing the viability of a project.

e) export/import -- There is significant corruption in Indonesia’s harbors.

f) foreign exchange risk -- Indonesia has a rudimentary and expensive derivatives market, which complicates attempts to hedge FX risk.

g) insurance -- Import and political risk insurance is generally unavailable. Other domestic insurance policies is not reliable.

h) financial reporting -- Financial statement standards are regularly flaunted, which complicates acquisitions, alliances, etc.

28

APPENDIX 8 -- PROJECT LOGISTICS

As part of our field research in Indonesia, we met with the following organizations and individuals, all located in Jakarta. This information is provided to document the sources of our information and to assist teams that conduct future analysis of Indonesia. Of course, the conclusions in this paper are our own and should not be attributed to any other organization or individual.

Name/Organization Contact Information NotesABN-AMRO Bank, N.V. Mr. Erik Moen

Vice President, COOJl. Lr. H. Juanda 23-24P.O. Box 2950Jakarta 10029, Indonesia+62 (21) [email protected]

Mr. Clemente EscanoDirector - TreasuryJakarta Stock Exchange BuildingTower II, 11th FloorSudirman Central Business DistrictJl. Jend. Sudirman Kav. 52-55Jakarta 12089, Indonesia+62 (21) 515-6838+62 (21) 515-4470 (fax)[email protected]

ABN-AMRO provided an excellent perspective on surviving the crisis and doing business in Indonesia.

American Chamber of Commerce

Mr. Francis X SheaDirector, Corporate FinancePrasetio Strategic ConsultingArthur AndersenWisma 46 Kota BNI Levels 25-28Jalan Jenderal Sudirman Kav 1Jakarta 10220, Indonesia+62 (21) 575-7906+62 (21) 574-4521 (fax)[email protected]

Mr. Phillip Shaw(see separate entry)

We enjoyed a lively breakfast discussion with six international businessmen.

BAPPENAS(National Development Planning Agency)

Dr. Ir. Sujana RoyatBureau Chief for Human Settlements and Urban

BAPPENAS provides a good perspective on development initiatives and

29

Development

Jl. taman Suropati 2Jakarta 10310, Indonesia+62 (21) 334-819+62 (21) 310-1921 (fax)[email protected]

regional/central relations.

Chase Bank Jakarta, Indonesia Chase provided insight into the banking and business environment.

ECONIT Dr. Arif ArrymanDirector

Jl. Prof. Dr. SoepomoSH. No 47, 4th FloorJakarta 12810, Indonesia+62 (21) 830-4850+62 (21) 835-4743

ECONIT is an economics think tank. Dr. Arryman is also active in Indonesian politics.

Embassy of Mexico in Indonesia

Mr. Ismael Sergio Ley-Lopez, Ambassador

Embassy of MexicoMenara Mulia, Suite 2306J. Gatot Subroto Kav. 9-11Jakarta 12930, Indonesia+62 (21) 520-3980+62 (21) 520-3978 (fax)[email protected]

The Ambassador provided an insightful perspective on Indonesia.

Embassy of Pakistan in Indonesia

Jakarta, Indonesia The Ambassador provided an insightful perspective on Indonesia.

Embassy of the United States of America

Ms. Pamela J. SlutzCounselor for Political Affairs+62 (21) 344-2211 x2280+62 (21) [email protected]

Ms. Judith R. FerginCounselor for Economic Affairs+62 (21) 344-2211+62 (21) [email protected]

Jalan Medan Merdeka Selatan 5Jakarta 10110, Indonesia

The Counselors have deep knowledge of the situation in Indonesia.

International Monetary Fund Mr. John DodsworthSenior Resident Representative

IMF Resident MissionBank IndonesiaJalan Kebon Sirih 82-84

Mr. Dodsworth, who is central to IMF activities in Indonesia, provided a clear assessment of the situation.

30

Jakarta 10002, Indonesia +62 (21) 231-1884

arranged through:Gertrud WindspergerIMF Public Affairs Division+1 (202) 623-4983

Jakarta Stock Exchange Mr. Mas AchmadPresident Director

PT Bursa Efek JakartaJakarta Stock Exchange BuildingJl. Jend. Sudirman Kav. 52-53Jakarta 12190, Indonesia+62 (21) 515-0234+62 (21) 515-0550 (fax)

Mr. Achmad provided a good overview of the state of equity markets.

Prof. Mardjono ReksodiputroProfessor of Law at the University of Indonesia and Secretary of the National Law Commission

The University of IndonesiaJakarta, Indonesia

Prof. Mardjono is an excellent resource in the area of the legal system.

Ministry of Investment and State-Owned Enterprises

Dr. Asril NoerExpert to the Minister on Institutional Relations

Jl.Dr.Wahidin No. 2 Jakarta 10710, Indonesia+62 (21) 386-4448+62 (21) 348-31774

Dr. Noer provided insight into the privatization process and investment objectives.

Mr. Soedarpo SastrosatomoExecutive ChairmanSamudera Shipping Line, Ltd.

Samudera Indonesia Bldg. 8/FLetjen S. Parman Kav. 35Jakarta 11480, Indonesia+62 (21) 548-0088+62 (21) 534-7171 (fax)[email protected]

Mr. Soedarpo is one of the most successful businessmen in Indonesia, and he was involved in the formation of the country.

Mr. Philip J. ShawPundi Stratejasa Indonesia

13th Floor, Wisma Metropolitan IIJl. Jend. Sudirman Kav. 31Jakarta 12920, Indonesia+62 (21) 570-3750+62 (21) 571-1556 (fax)[email protected]

Mr. Shaw operates a consulting firm that assists international companies and is very knowledgeable about Indonesia.

Sucofindo Mr. Zafar D. IdhamDirector of Operations

Jl. Raya Pasar Minggu Kav. 34Jakarta 12780, IndonesiaP.O. Bo 2377, Jakarta 10001+62 (21) 798-3666 x1803+62 (21) 798-6980 (fax)[email protected]

Sucofindo is an inspection and certification company that is very involved in imports/exports. Mr. Idham provided a good overview of commerce.

31

Mdm. Asti SuhartoPresidentPT. Maritosa Coalindo

Jln. Kenali Asam I BJakarta 13240, Indonesia+62 (21) 478-61032+62 (21) 478-64669 (fax)

Mdm. Suharto is a successful businesswoman who operates an export/import company and is very knowledgeable about Indonesian affairs.

Tirtama Comexindo Ms. Tatyana SekarprijastinaBusiness Development

PT Tirtamas ComexindoBidakara Building, 7th FloorJl. Jend. Gatot Subroto Kav.71-73Jakarta 12870, Indonesia+62 (21) [email protected]

Comexindo is an international trading company (specializing in offsets) that was affected hurt by the crisis.

United National Industrial Development Organization (UNIDA)

Mr. Syed Asif HasnainRepresentative

UN BuildingJl. M.H. Thamrin 14P.O. Box 2338Jakarta 10001, Indonesia+62 (21) 314-1308 x601+62 (21) 390-7126 (fax)[email protected]

UNIDA is focused on Indonesia’s post-crisis development.

United Nations Support Facility for Indonesian Recovery

Dr. Satish MishraChief Economist

UN House, 4th FloorJl. M.H. Thamrin 14P.O. Box 2338Jakarta 10240, Indonesia+62 (21) 314-1308 x110+62 (21) 392-1152 (fax)[email protected]

UNSFIR is focused on Indonesia’s post-crisis recovery.

The Wall Street Journal Mr. Jay SolomonIndonesia Correspondent

14th Floor, Deutsche Bank Bldg.J. Imam Bonjol 80Jakarta 10310, Indonesia+62 (21) 3983-1340+62 (21) 3983-1342 (fax)[email protected]

Mr. Solomon has been in Indonesia for five years and has closely watched the many dramatic events since 1998. (Mr. Solomon may be assigned to a new country in the near future.)

The World Bank Mr. Mark BairdIndonesia Country Director

Lippo Life Building, Suite 301Jl. H. R. Rasuna Said, Kav. B-10Kuningan, Jakarta 12940, Indonesia

Mr. Baird provided an extensive assessment of Indonesia’s recovery.

32

+62 (21) 252-0316+62 (21) 252-2438 (fax)

arranged through:Lieke Sastrosatomo, program [email protected]

Additional logistics information: In addition to the organizations listed above, you may wish to attempt to make

contacts with large foreign corporations (e.g., Comexindo, mining companies, Reebock) and with members of the legislature.

We stayed at the Hotel Menara Peninsula, a comfortable business-class hotel that offered very good rates. The hotel is a short taxi ride from the business district, although there are other hotels that are even closer. You can contact the General Manager, Kevin O’Hagan, and mention we sent you. +62 (21) 535-0888, +62 (21) 535-0938 (fax), [email protected].

If you want to see more of Indonesia, consider a trip to Mt. Bromo (fly to Sarabaya). To see Hindu culture, consider Bali, where you may wish to stay at the Hotel Bali Padma (Mayke Boestami, Public Relations Manager, +62 (361) 752140, [email protected]).

33

E N D N O T E S

34

![[Shinobi] Bleach 487](https://img.pdfslide.us/doc/110x75/568befaa1a28ab89338cf732/shinobi-bleach-487.jpg)