Embed Size (px)

Citation preview

Broiler sector scenarios study

Peter van Horne and Ferry Leenstra

Wageningen UR

Jakarta, september 2015

Indonesian-Dutch programme on

food secturity: poultry sector

Important Long term goals:

� Poultry farmers have a reasonable income

� Sustained employment in the supply chain

� Poultry meat marketed with safe standards

� Affordable price of chicken meat for consumers

Indonesian-Dutch programme on

food secturity: poultry sector

Short term goals:

� Tool for scenario study with:

● Comparsion supply chains

● Future situation with growth in numbers and

change in supply chain

� Tool especially relevant for government policy

Sector development scenarios

Part of Work Package 1:

Indonesian Poultry Industry towards 2025

Peter van Horne and Ferry Leenstra, Wageningen UR

In cooperation with IPB and Rabobank Int.

Focus on west Java

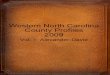

Source: Rabobank, 2015

0

1,000

2,000

3,000

4,000

5,000

6,000

Sheep Pork Beef Poultry

1,000 tonnes

90s Asia Crisis

00s 2010-2014 2014-2023f

Chicken: +8.5%

Beef: +5.1%

Pork: +1.1%

Chicken: +4.7%

Beef: +4.2%

Pork: +1.2%

Chicken:-19.3%

Beef: -2.0%

Pork: +1.8%

Chicken:+6.4%

Beef: +2.0%

Pork: +5.4%

Chicken: +6.0%

Beef: +2.8%

Pork: +3.4%

Meat: +5.5% Meat:-9.1%

Meat: +3.9%

Meat:+5.1%

Meat: +5.0%

67%

16%

14%

Indonesian meat market: Poultry the protein of choice and the fastest growing marketFuture: Ongoing growth, but slower than in the past.

-

50,000

100,000

150,000

200,000

250,000

300,000

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

Urban

Rural

X Million

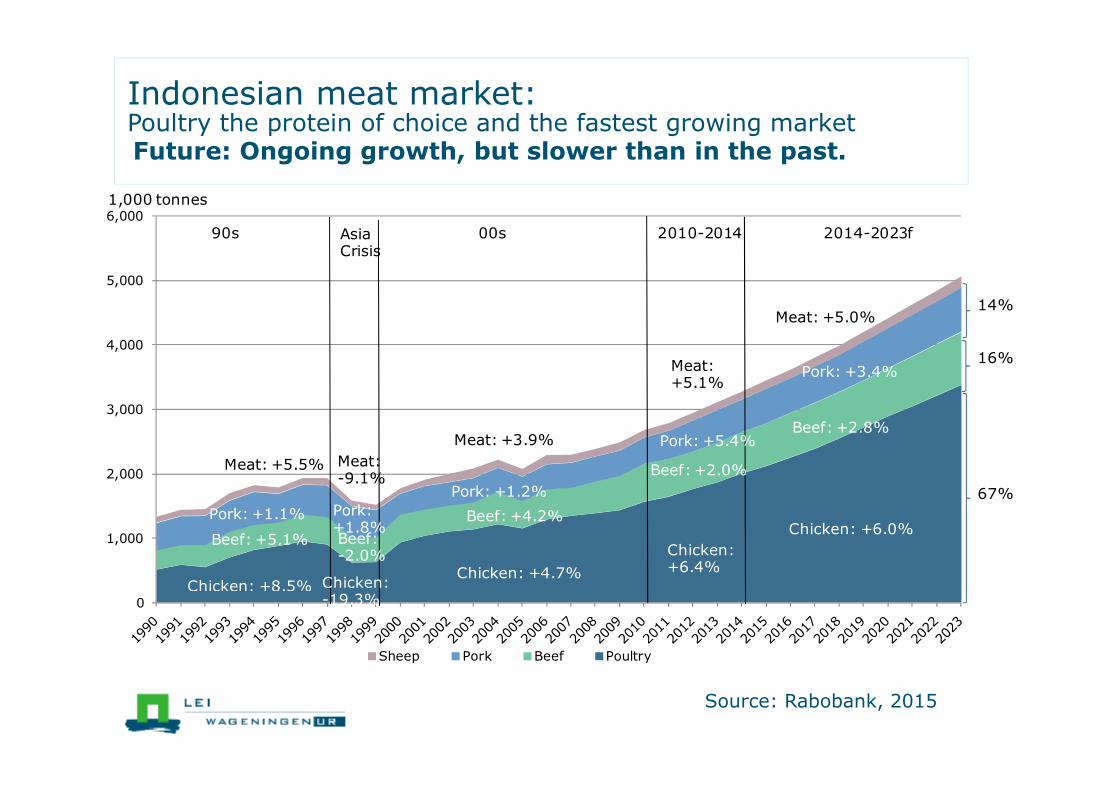

Key drivers for market growth in the poultry industry

� Source: Rabobank projections based on FAO, OECD, GIRA, WHO, IMF

Urbanisation level 2014-2023f from 53% to 59% GDP Growth per capita 2014-2020f: +55%

Population growth 2014-2023f: +10% Poultry per capita consumption 2014-2023f: +27%

+28%

+45%

+53%+16%

+14%

+10%

31%

53%

59%

+62%

+115%

+55%

191.1 221.3

252.8 277.1

0

50

100

150

200

250

300

1994 2004 2014 2023f

X Million

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1994 2004 2014 2023f

kg/head

7691,243

2,676

4,155

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1994 2004 2014 2023f

GDP/capita

Source: Rabobank, WUR 2015

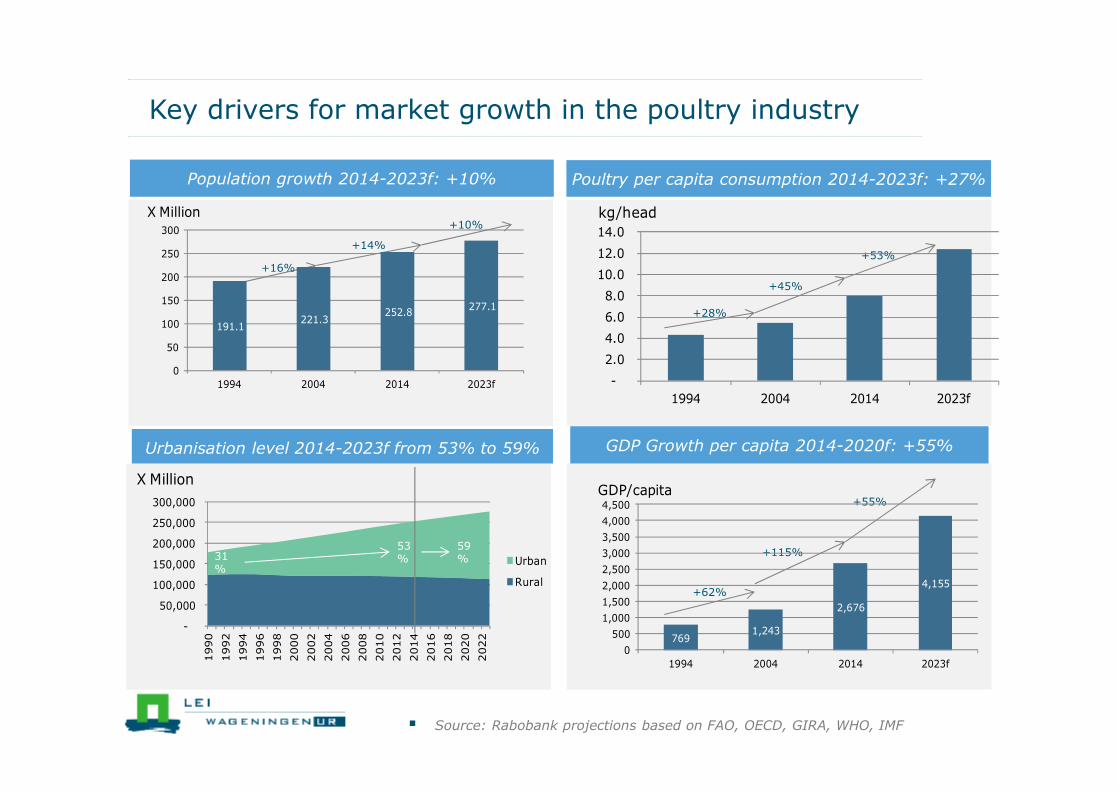

Key drivers for market growth in the poultry sector

Religion

Feed efficiency

Supply: short pay back time

Convenience

Health

Pricing

• Price: low price

compared to other

meat types

• Religion

• Convenience

• Health

• Range in products

• QS resto’s

• .....

Source: Rabobank, 2015

Poultry meat consumption in other countries

0

5

10

15

20

25

30

35

40

45

50

Poultry consumption (kg/year)

Income per capita (USD 1000)

-Hybrid between Wet market and

grocery retail

- Wide assortment of meat, poultry

and seafood

- Non-airconditioned but with

cooling facilities

- Linked to local night markets

Malaysia: NSK Trade City

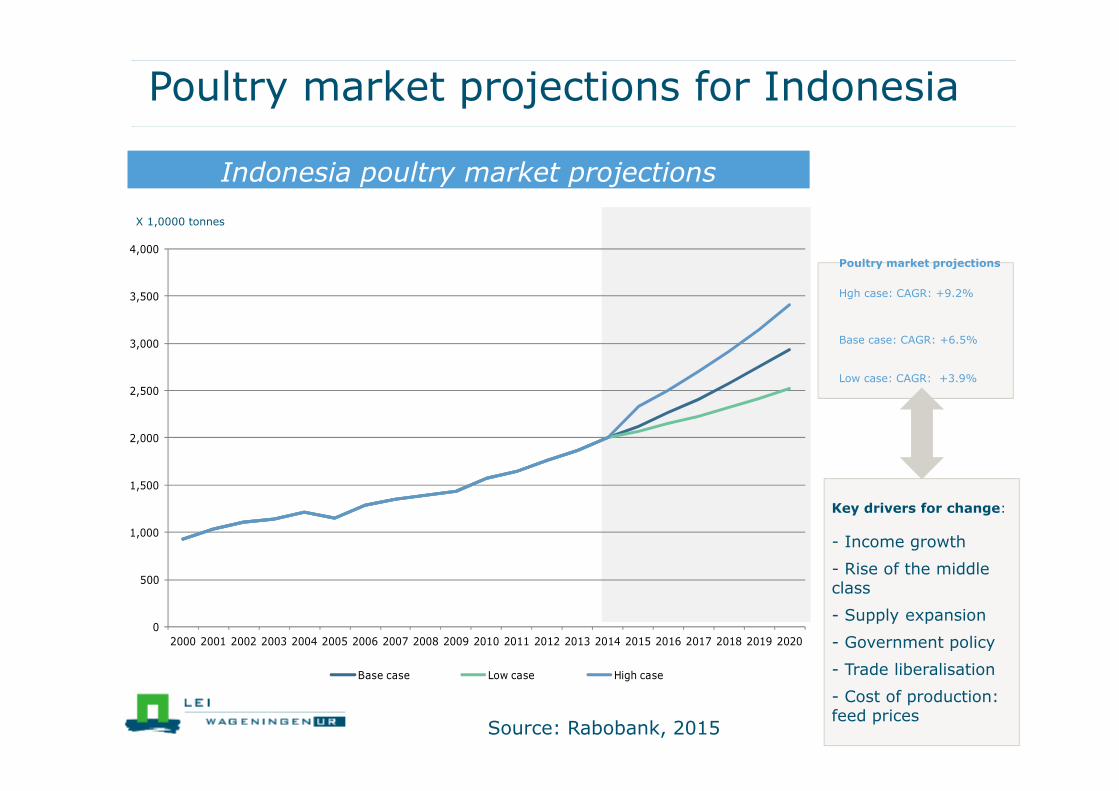

Poultry market projections for Indonesia

Indonesia poultry market projections

X 1,0000 tonnes

Key drivers for change:

- Income growth

- Rise of the middleclass

- Supply expansion

- Government policy

- Trade liberalisation

- Cost of production: feed prices

Hgh case: CAGR: +9.2%

Base case: CAGR: +6.5%

Low case: CAGR: +3.9%

Poultry market projections

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Base case Low case High case

Source: Rabobank, 2015

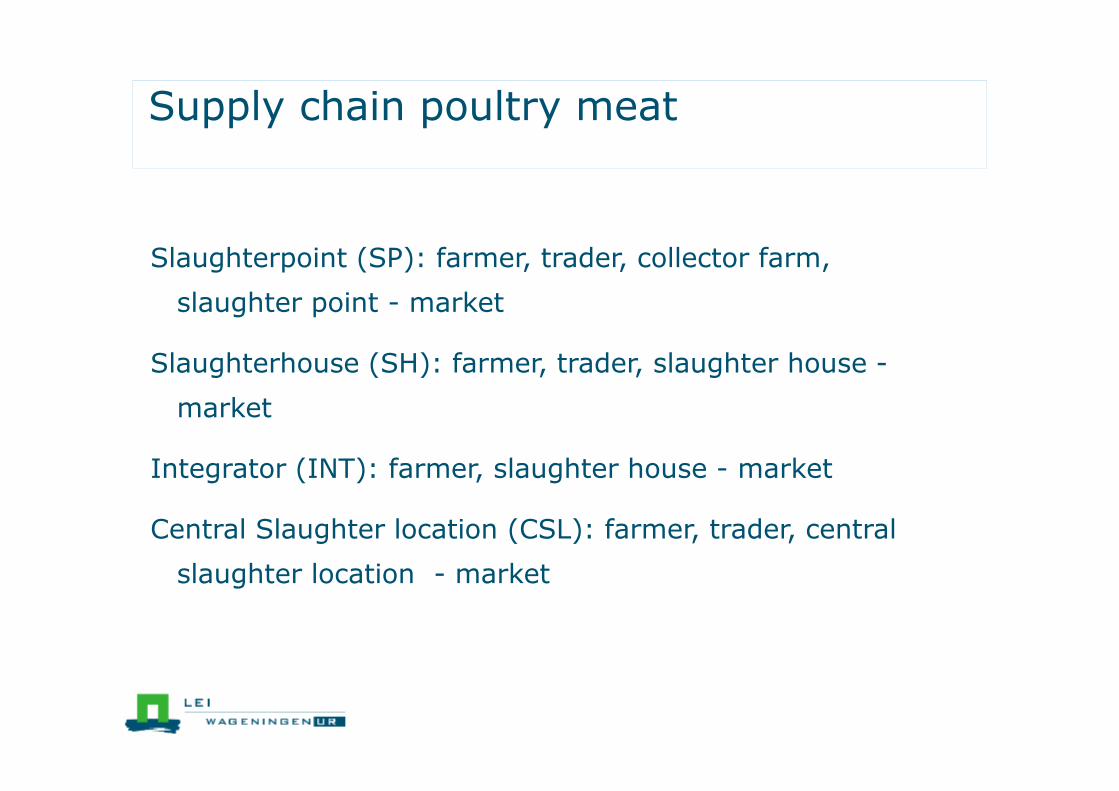

Supply chain poultry meat

Slaughterpoint (SP): farmer, trader, collector farm,

slaughter point - market

Slaughterhouse (SH): farmer, trader, slaughter house -

market

Integrator (INT): farmer, slaughter house - market

Central Slaughter location (CSL): farmer, trader, central

slaughter location - market

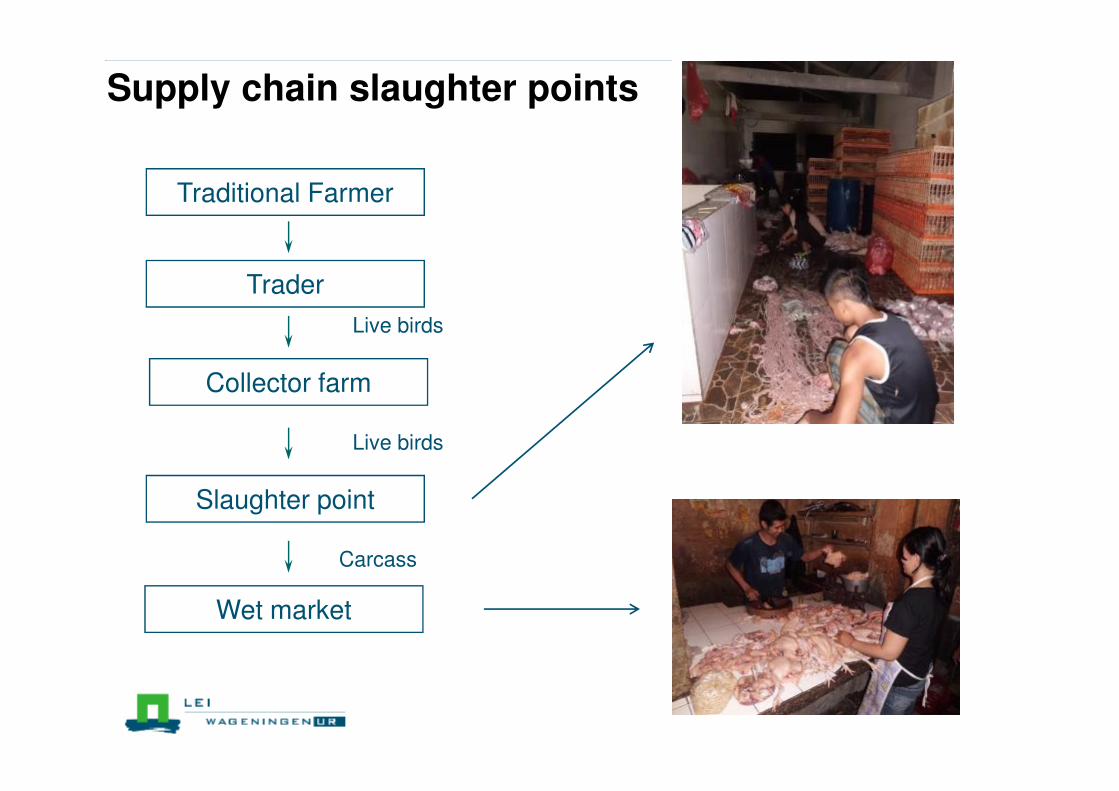

Supply chain slaughter points

Live birds

Traditional Farmer

Trader

Collector farm

Slaughter point

Wet market

Live birds

Carcass

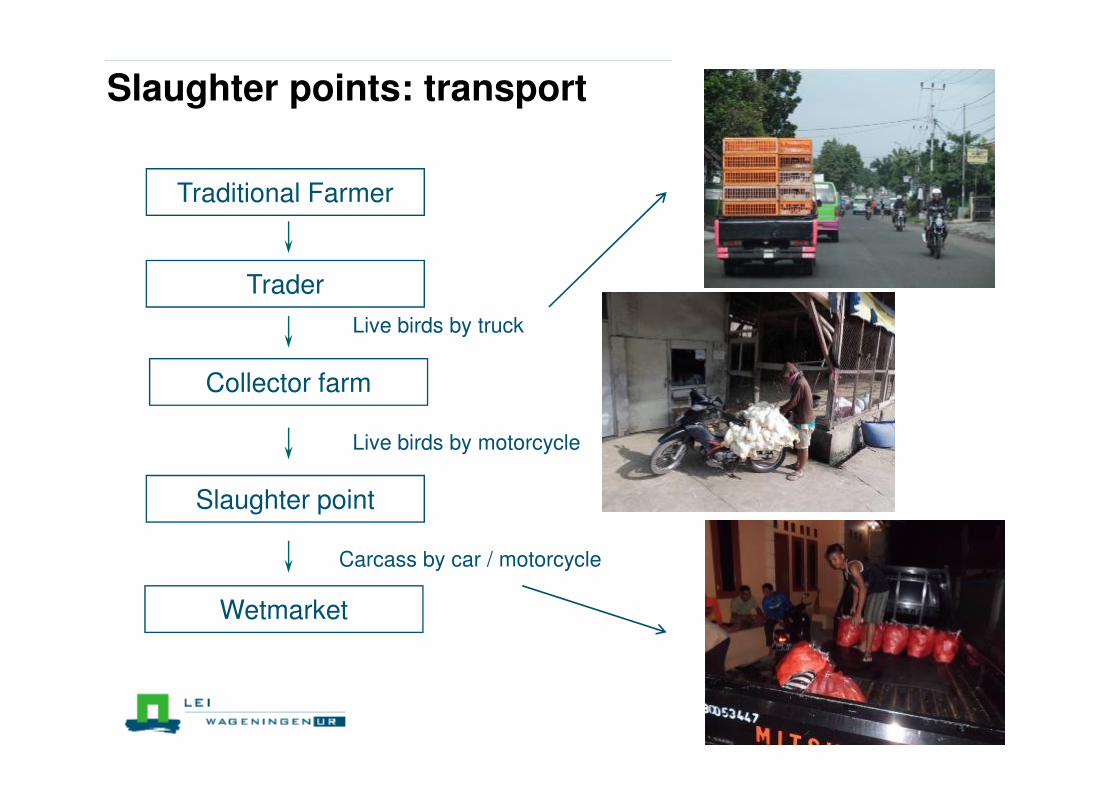

Slaughter points: transport

Live birds by truck

Traditional Farmer

Trader

Collector farm

Slaughter point

Wetmarket

Live birds by motorcycle

Carcass by car / motorcycle

Supply chain: central slaughter location

Live birds

Traditional Farmer

Trader

Collector farm

Slaughter point

Wetmarket

Central

slaughter

location

Central slaughter location: advantages

Live birds

Traditional Farmer

Trader

Collector farm

Slaughter point

Wetmarket

Central

slaughter

location

Supply chain small slaughter house

Live birds

Traditional Farmer

Trader

Slaughter house

Market

- Farmer / trader

- Small – medium scale

slaughterhouse

- Market: kiosk, resto,

wet market

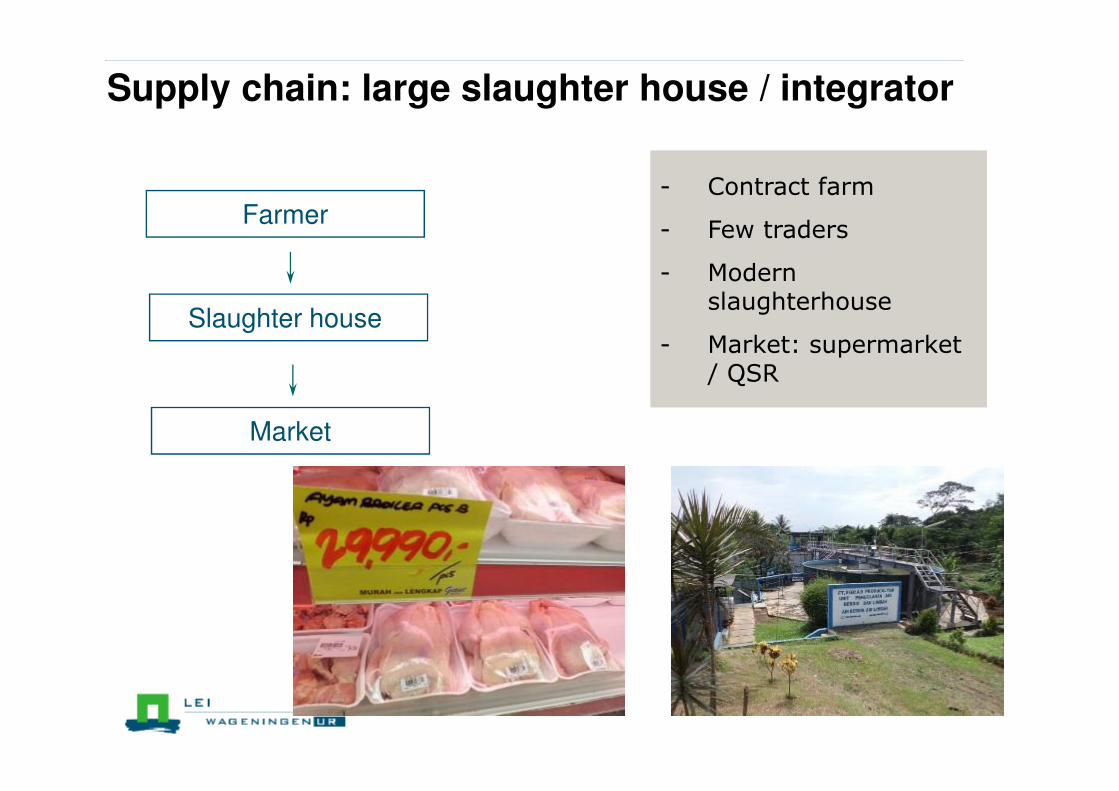

Supply chain: large slaughter house / integrator

Farmer

Slaughter house

Market

- Contract farm

- Few traders

- Modern slaughterhouse

- Market: supermarket / QSR

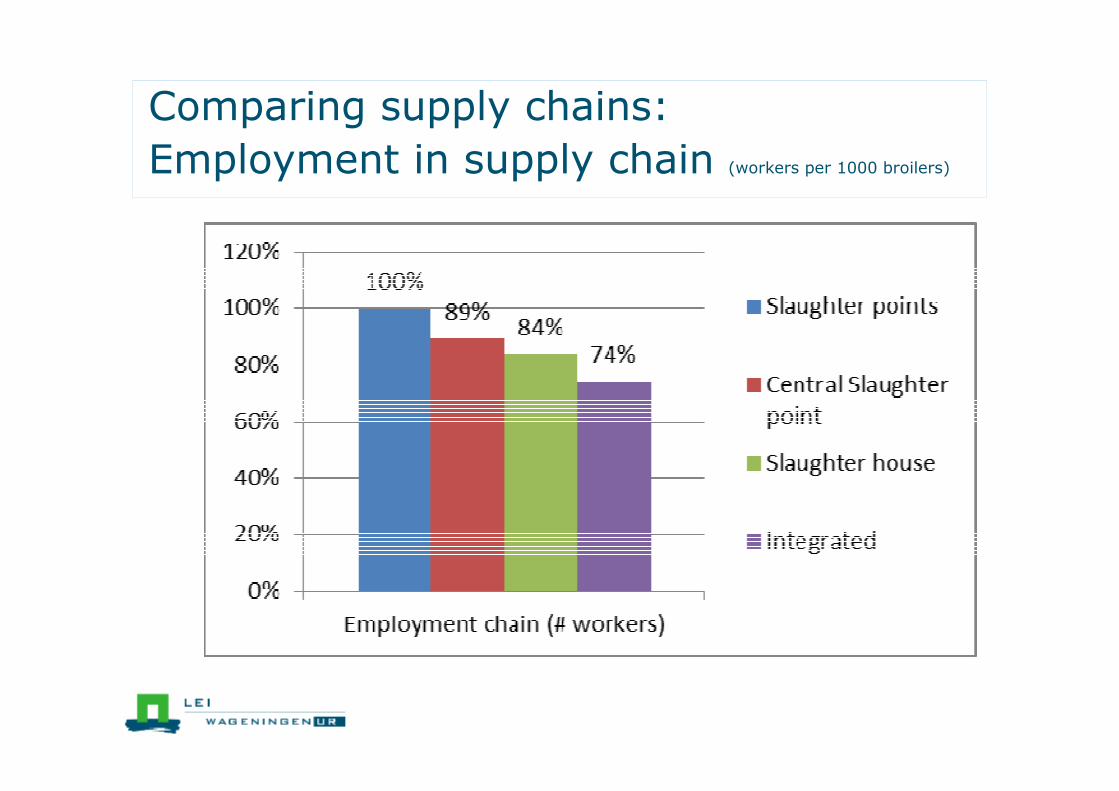

Comparing supply chains:

Employment in supply chain (workers per 1000 broilers)

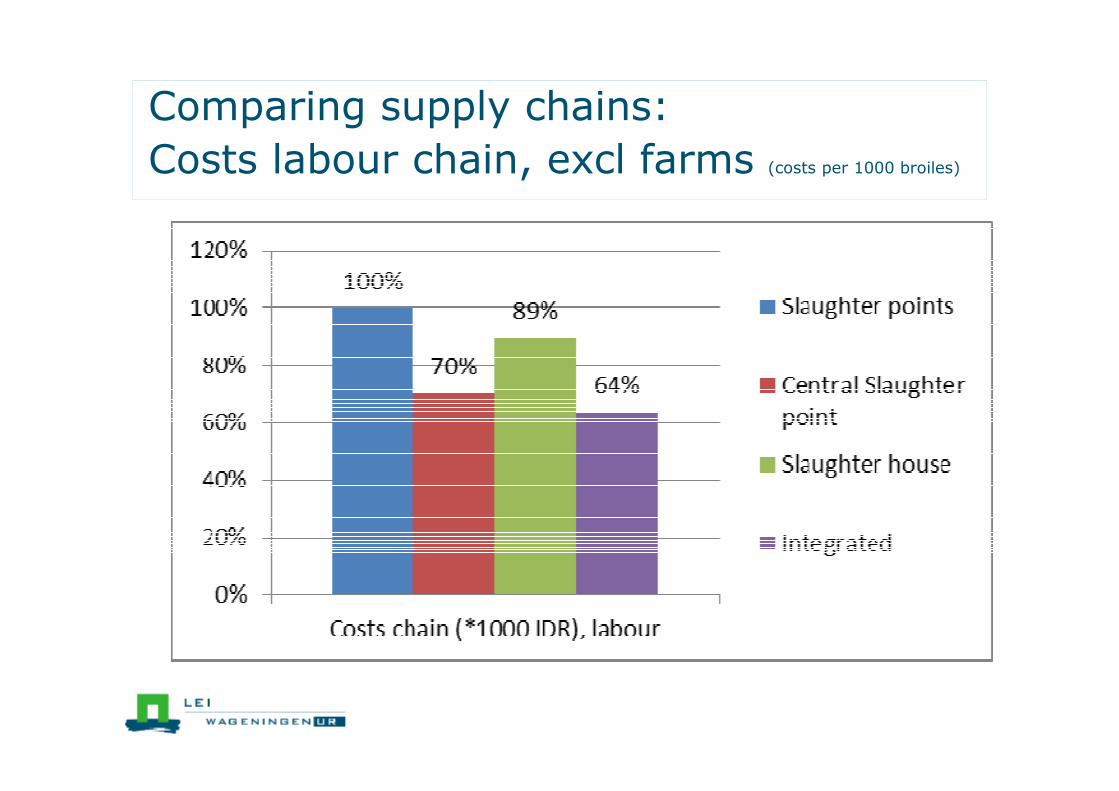

Comparing supply chains:

Costs labour chain, excl farms (costs per 1000 broiles)

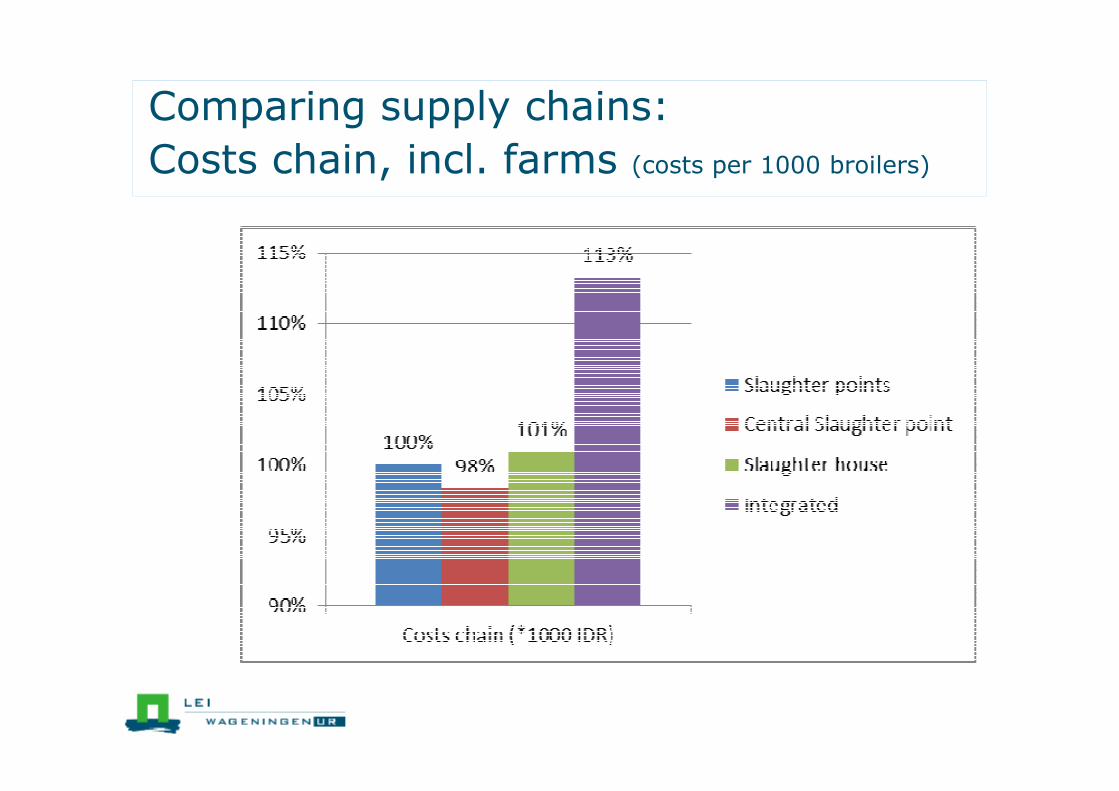

Comparing supply chains:

Costs chain, incl. farms (costs per 1000 broilers)

Comparing supply chains:

Transport by truck / motorcylce (km per 1000 broilers)

Motorcycle:

233,000 km/day.

Half with live birds

Comparing supply chains:

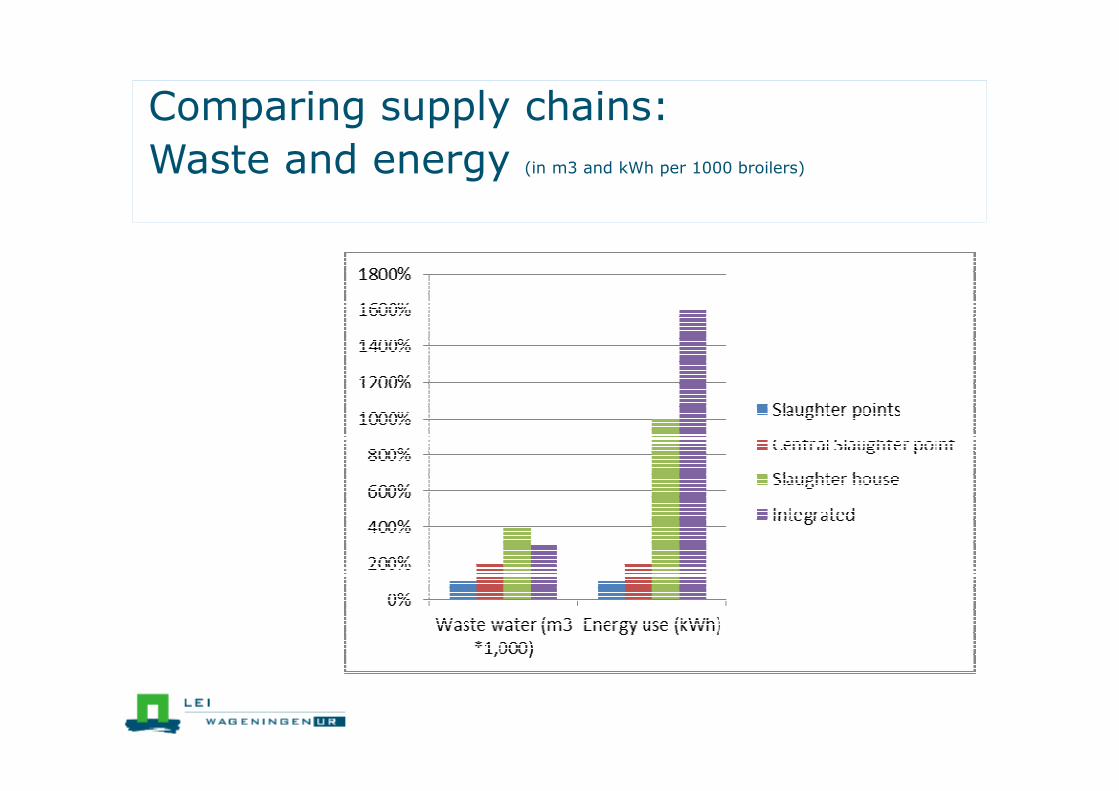

Waste and energy (in m3 and kWh per 1000 broilers)

Supply chain development: a scenario

Slaughter

points

Central

slaughter

point

Slaughter-

houses Integrated

in 2015: 70% 0% 10% 20%

in 2020: 35% 30% 10% 25%

in 2025: 0% 60% 10% 30%

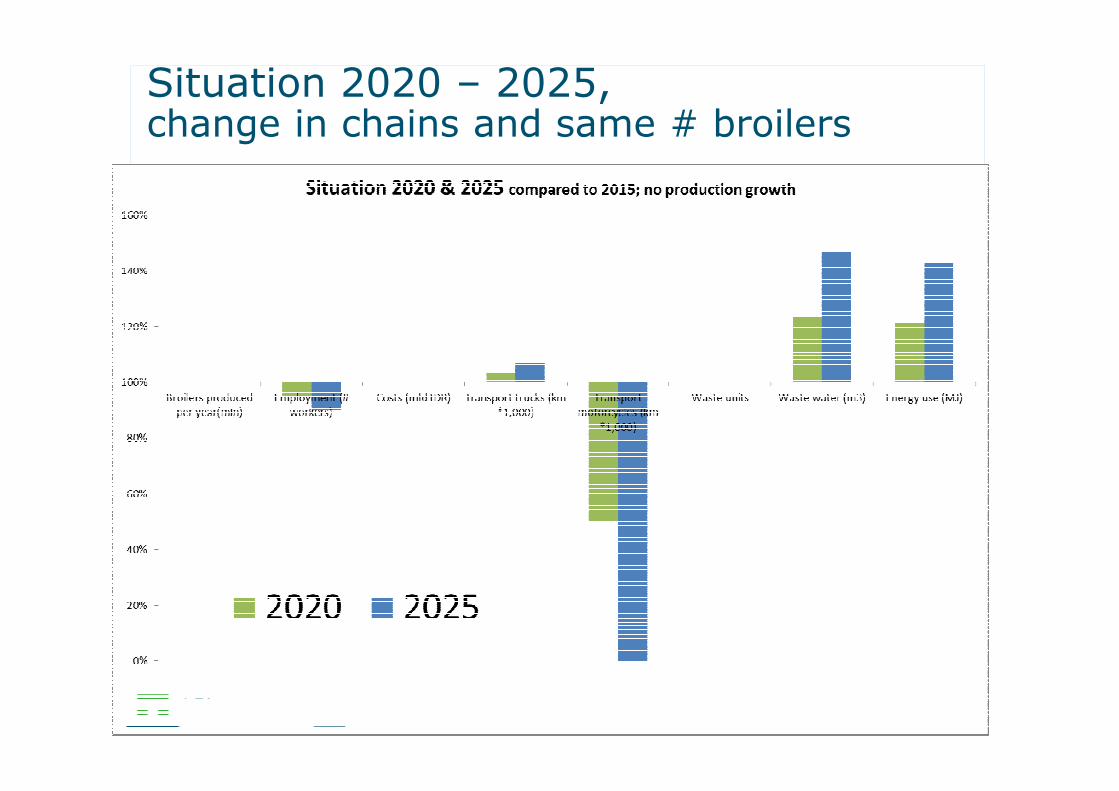

Situation 2020 – 2025, change in chains and same # broilers

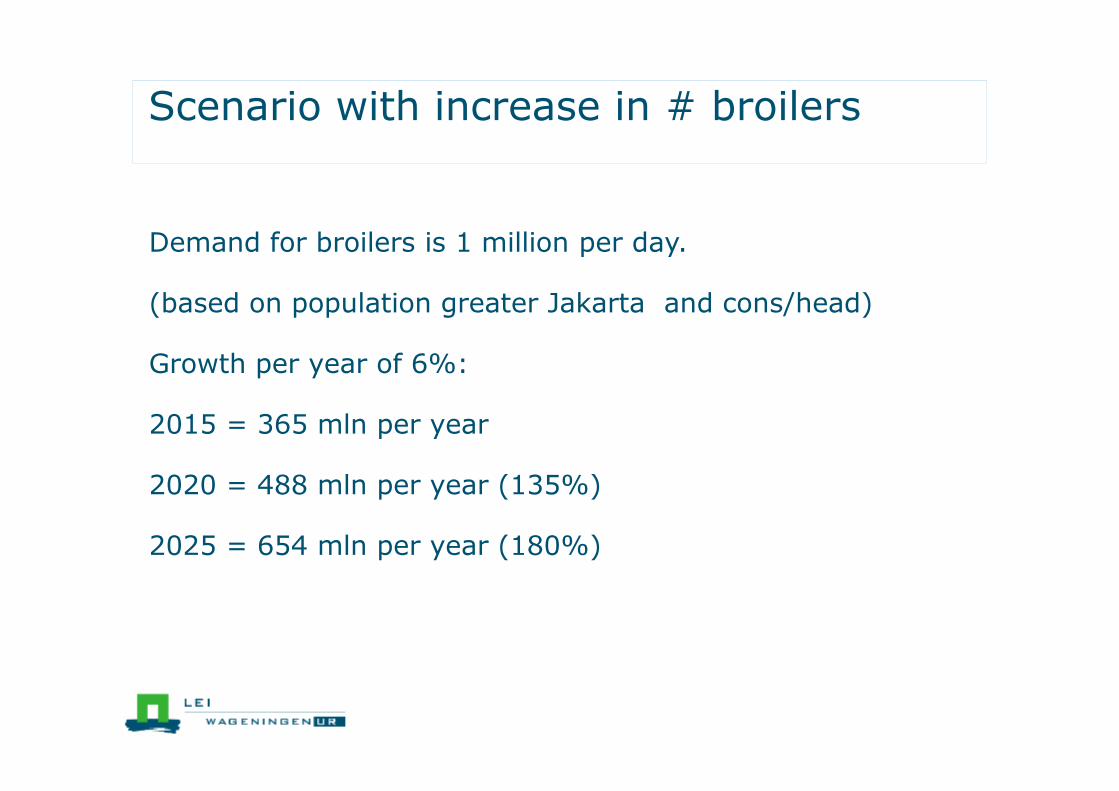

Scenario with increase in # broilers

Demand for broilers is 1 million per day.

(based on population greater Jakarta and cons/head)

Growth per year of 6%:

2015 = 365 mln per year

2020 = 488 mln per year (135%)

2025 = 654 mln per year (180%)

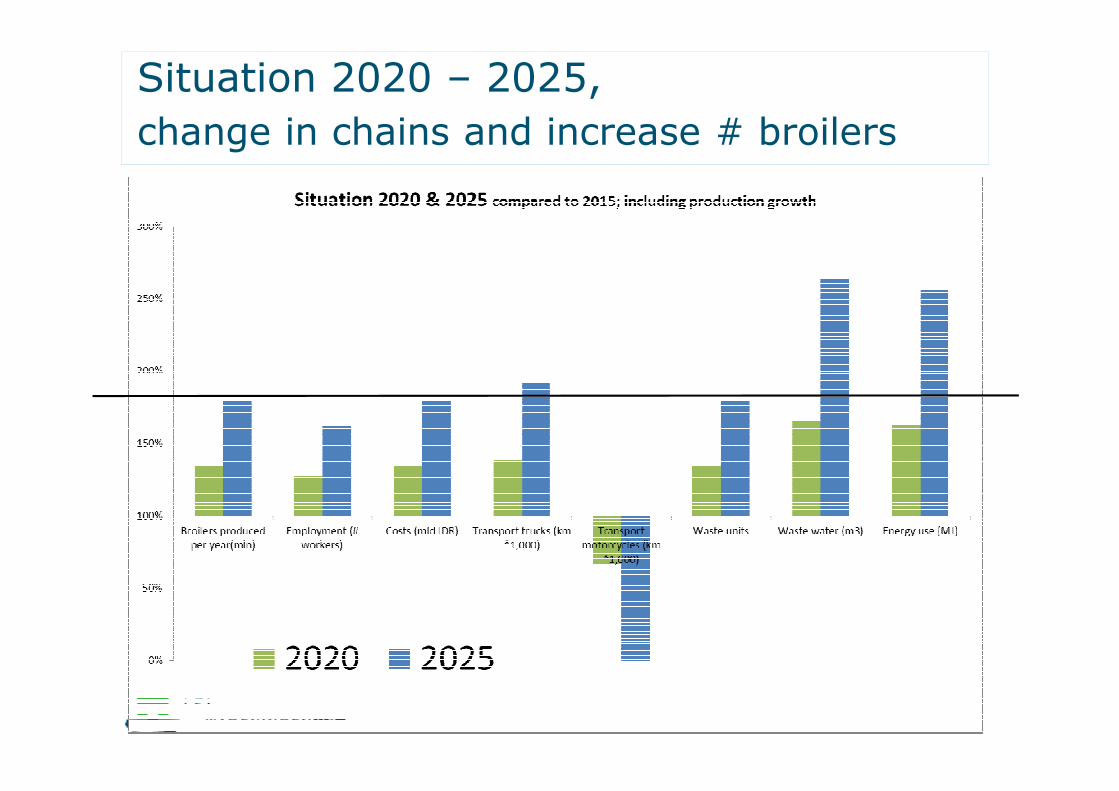

Situation 2020 – 2025,

change in chains and increase # broilers

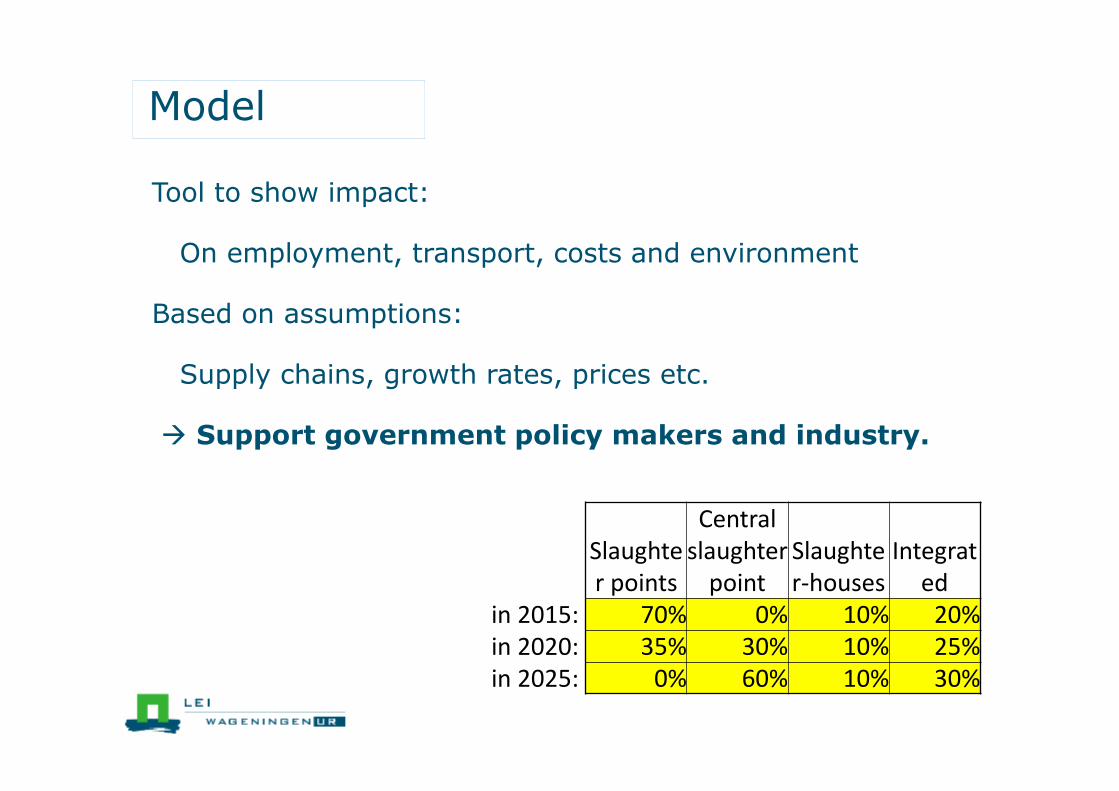

Model

Tool to show impact:

On employment, transport, costs and environment

Based on assumptions:

Supply chains, growth rates, prices etc.

� Support government policy makers and industry.

Slaughte

r points

Central

slaughter

point

Slaughte

r-houses

Integrat

ed

in 2015: 70% 0% 10% 20%

in 2020: 35% 30% 10% 25%

in 2025: 0% 60% 10% 30%

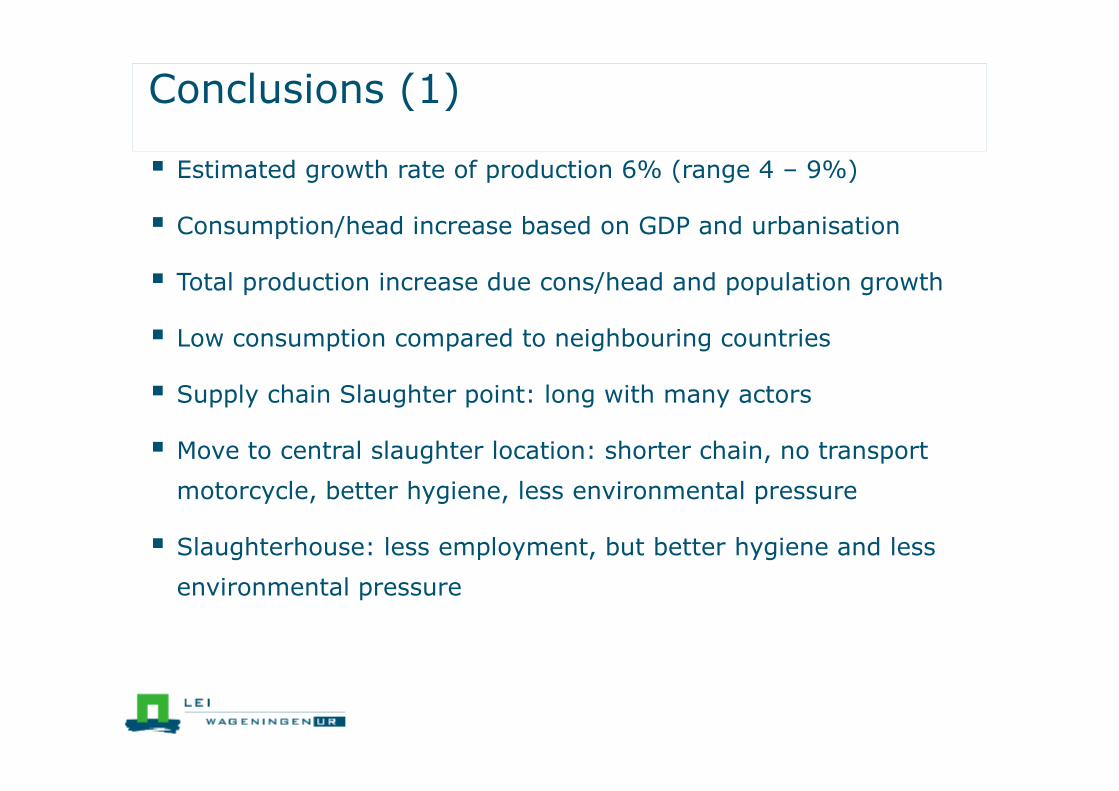

Conclusions (1)

� Estimated growth rate of production 6% (range 4 – 9%)

� Consumption/head increase based on GDP and urbanisation

� Total production increase due cons/head and population growth

� Low consumption compared to neighbouring countries

� Supply chain Slaughter point: long with many actors

� Move to central slaughter location: shorter chain, no transport

motorcycle, better hygiene, less environmental pressure

� Slaughterhouse: less employment, but better hygiene and less

environmental pressure

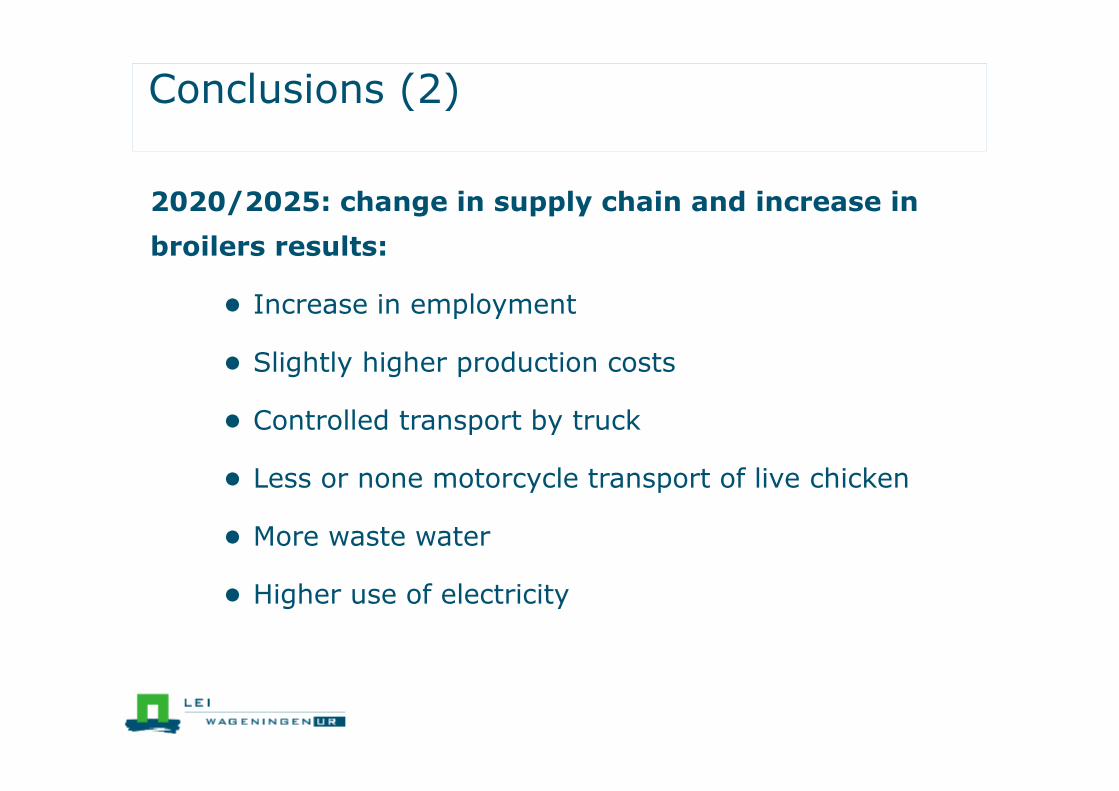

Conclusions (2)

2020/2025: change in supply chain and increase in

broilers results:

● Increase in employment

● Slightly higher production costs

● Controlled transport by truck

● Less or none motorcycle transport of live chicken

● More waste water

● Higher use of electricity