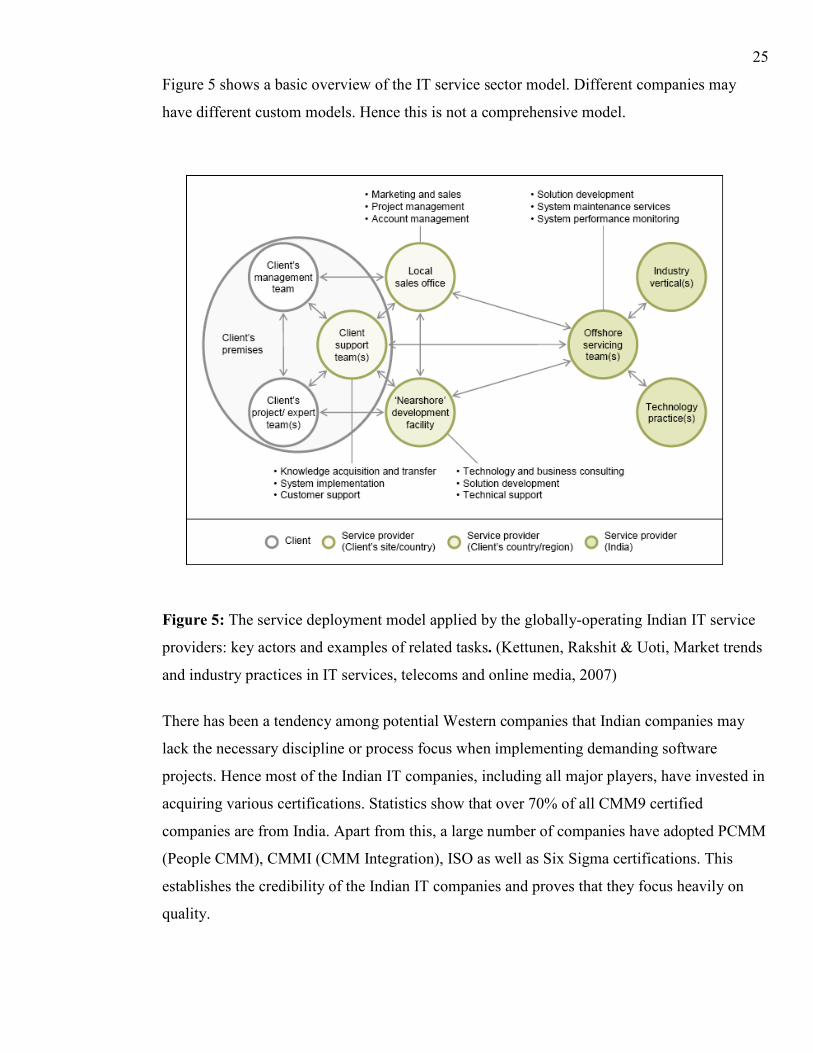

Embed Size (px)

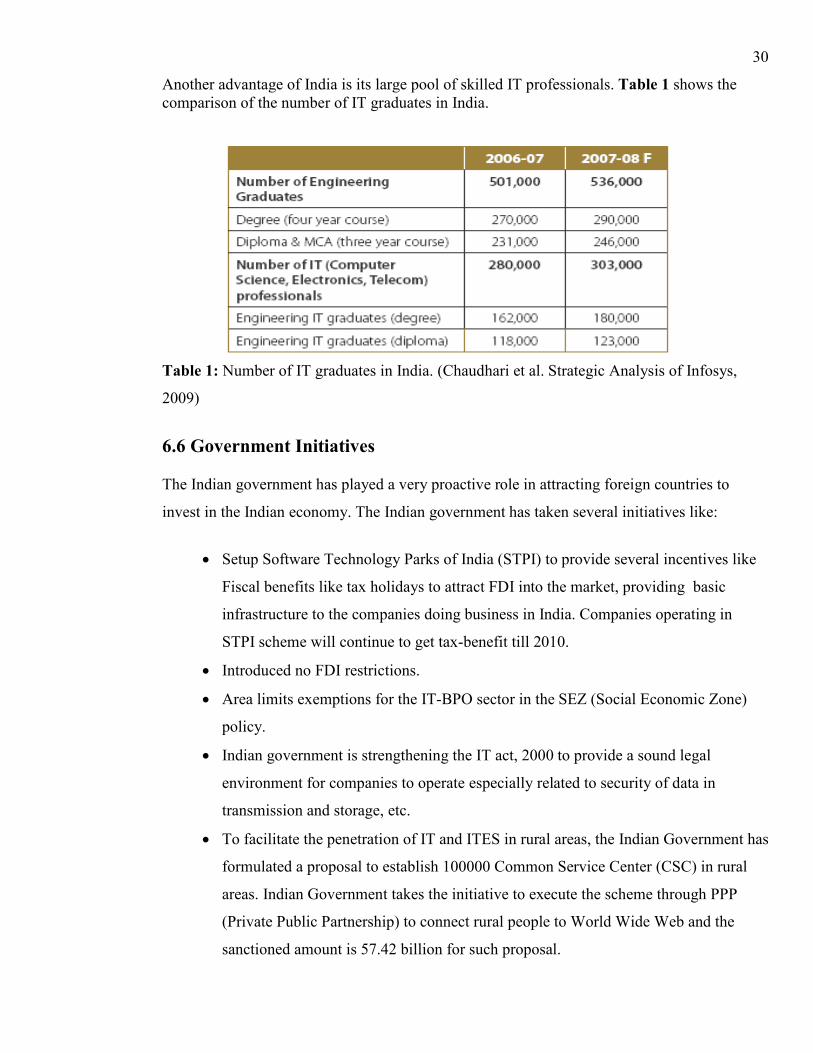

Citation preview

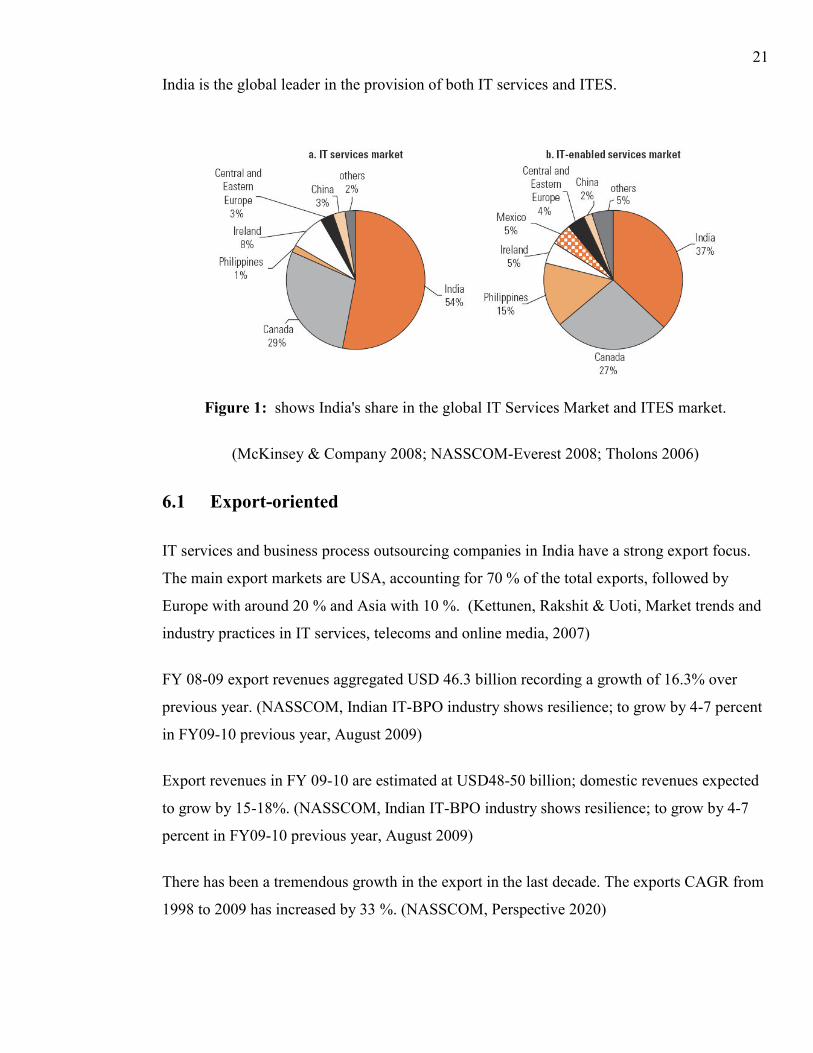

!"#$%&%'()*+,(-"$.(#/*%0*)&&'("1*.2(",2".*

3%4".23%%'*(,3%''),1*+,(-"$.(#/*%0*)&&'("1*.2(",2".*

"+$%&"),*5+.(,"..*)1!(,(.#$)#(%,*1"4$""*&$%4$)!!"*

**

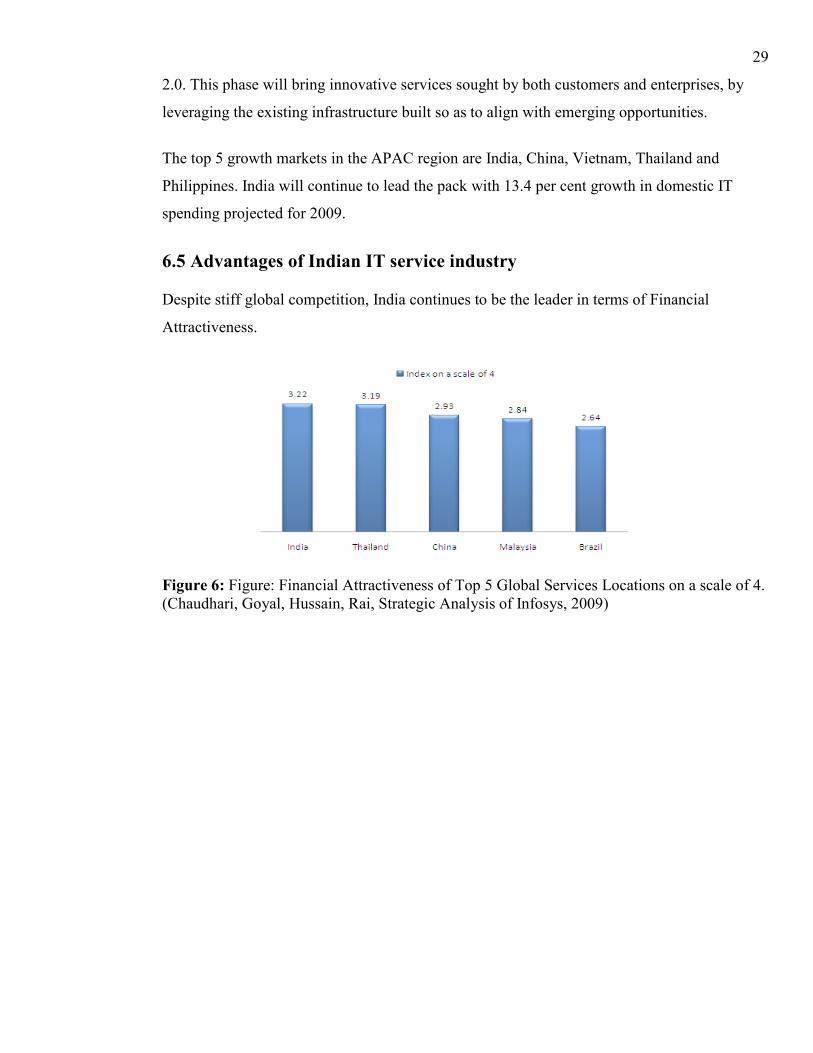

**

**

*

*

**

**

(67896*(#*.:;<8=:*.:=>?;@A*7:<:B?CD:6>*%CC?;>E68>8:A*

***

**

*

*

*

*

*

*

*

*

*

&9;D867:;*&9EB*"5)*FGH(5!.*

18AA:;>9>8?6*

)EIEA>*JFFK*

0018-9162/05/$20.00 © 2005 IEEE January 2005 71

C O V E R F E A T U R E

P u b l i s h e d b y t h e I E E E C o m p u t e r S o c i e t y

India’s IT ServicesIndustry: A Comparative Analysis

I n the past decade, India’s information tech-nology services industry emerged as an impor-tant player in the global IT services market.The country’s share of this market, valued atmore than $350 billion, increased from 1.5

percent in 2000-2001 to 1.9 percent in 2002-2003.While worldwide revenue of IT services grew lessthan 2 percent during this period, India’s IT ser-vices industry experienced 22 percent revenuegrowth1,2—a pace comparable to the rise in HongKong’s electronics industry during the 1970s.3

The outsourcing of IT services by multinationalcorporations (MNCs) is driving this rapid growth.For example, General Electric’s oft-cited 70-70-70strategy mandates the outsourcing of 70 percent ofits IT service requirements, of which 70 percent aregiven to strategic suppliers, who in turn execute 70percent of the work outside high-wage countries.GE currently subcontracts more than $500 millionworth of IT services to India, representing about 8percent of the country’s IT services export market.1

A major factor underlying the boom in IT serviceoutsourcing is the need for MNCs to remain glob-ally competitive by relocating labor-intensive oper-ations overseas to low-wage countries. By movingaway from the traditional corporate model of verti-cal integration to a more flexible “quasi-integrated”model that links various networks of suppliers and distributors, firms seek to complement higheconomies of scale with low input costs.3-7

INDIA-BASED IT SERVICE NETWORKSEach IT service provider in India is part of a larger

MNC production network that “combines a leadfirm, its subsidiaries and joint ventures, its suppli-ers and subcontractors, its distribution channels,VARs [value-added resellers], as well as its R&Dalliances and a variety of cooperative agreements....The lead firm outsources not only manufacturing,but also a variety of high-end support services.”8

In general, these production networks can be cat-egorized as intrafirm, interfirm, or joint venture net-works.6-11 An intrafirm network consists of sub-sidiaries that the MNC wholly owns. A joint ven-ture is an equity-based partnership between theMNC and another firm. An interfirm network is abusiness relationship between the MNC andanother company that can have a long-term con-tractual basis or involve informal short-term, pro-ject-based, one-off services.12

MNCs source India-based IT services accordingto one of three models—subsidiary, subsidiary plusIT service provider, or IT service provider—that caninclude one or more production network subtypesdepending on the business relationship between the MNC and its IT service provider(s). Table 1describes each model and the possible MNC-IT ser-vice provider relationships and production networksubtypes, along with a few key examples.

The subsidiary plus IT service provider model iscurrently becoming the dominant MNC model. To

India’s rapidly growing IT services industry has many parallels—and somedifferences—with East Asia’s electronics and computer hardware industries.

PratyushBharatiUniversity of MassachusettsBoston

Authorized licensed use limited to: San Jose State University. Downloaded on August 23, 2009 at 00:46 from IEEE Xplore. Restrictions apply.

72 Computer

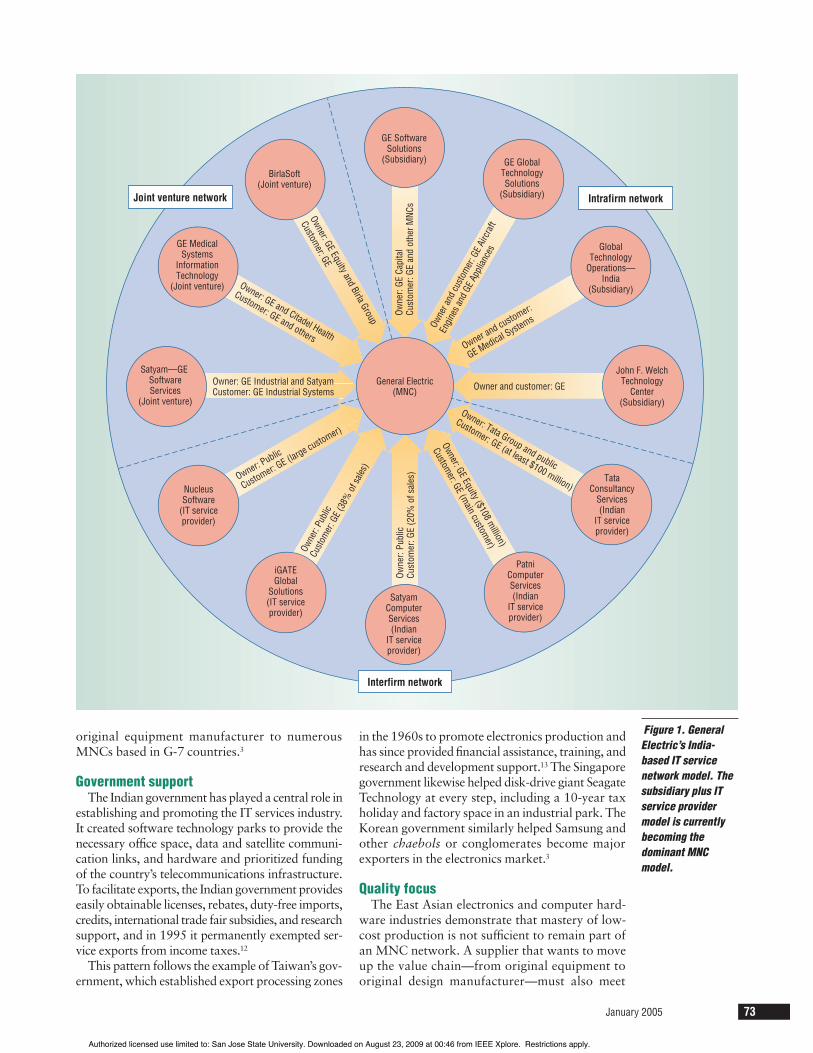

better understand India’s IT services industry, it isuseful to compare GE’s IT service network, shownin Figure 1, with production networks in East Asia’selectronics and computer hardware industries.

Single supply tierA unique feature of India-based IT service net-

works is the absence of multiple tiers of suppliers.GE and other MNCs have only one tier of suppli-ers, compared to leading firms in Taiwan’s computerhardware industry, which typically have several lay-ers of suppliers. For example, major computer mak-ers such as Apple, Dell, IBM, NEC, Packard Bell,and Siemens source motherboards from TaiwaneseOEMs including Elite, First International Computer,and Tatung, which employ numerous small andmedium-size enterprises to source parts.3,13 Thenature of IT services makes it difficult to subdividework among multiple suppliers. Direct interactionwith IT service providers allows the MNC to exertgreater control over IT services.

Dependency on MNCIn many production networks, the lead firm and

its suppliers and distributors are loosely boundtogether through equity and debt holdings, shareddirectors, and equipment leases.6 India-based IT ser-vice networks, though limited to a single supply tier,are closely bound together in dependency relation-ships similar to those in East Asian production net-works. MNCs in India influence their suppliers bothas owners and buyers, impacting IT service pro-viders’ decisions, offerings, strategies, and prices.

MNC as owner. GE owns all four of its India-basedIT service subsidiaries. GE Software Solutions pro-vides implementation, consulting, development, tran-sition, maintenance, and support services to GE andother MNCs. GE Global Technology Solutions pro-vides advanced mainframe software solutions devel-opment, client-server solutions, e-commerce tech-nology, and enterprise resource planning for GE Air-

craft Engines and GE Appliances. Global TechnologyOperations—India, owned by GE Medical Systems,designs and develops products and solutions for several computer platforms. The John F. Welch Tech-nology Center is the company’s first and largest mul-tidisciplinary R&D facility outside the US.

In addition, GE Equity has a $108 million stakein Patni Computer Services. PCS is India’s seventh-largest IT service provider with a focus on enter-prise application solutions, e-business, implemen-tation, and consulting.

Finally, GE has joint ventures with three IT ser-vice providers. Satyam—GE Software Services, alsoknown as the India Design Center, is owned bySatyam Computer Services, India’s fourth-largestIT service provider, and GE Industrial Systems; itdesigns and develops new products and softwaresolutions for embedded systems, e-commerce, andhuman-machine interaction. GE Medical SystemsInformation Technology is a joint venture betweenGE Medical Systems and Citadel Health, a nicheIndian IT firm. GE Equity and the Birla Groupformed BirlaSoft to develop software solutions.

MNC subsidiaries and joint ventures likewise playan important role in Taiwan’s computer hardwareindustry. For example, Texas Instruments and Acerhave a joint venture to produce dynamic RAM.3

MNC as buyer. GE is a major customer of its India-based subsidiaries and joint venture firms as wellas a number of independent companies. In addi-tion, it negotiated a $100 million deal with TataConsultancy Services (TCS), India’s largest IT ser-vice provider. GE also accounts for 20 percent ofSatyam’s business and 38 percent of revenues ofiGATE Global Solutions, a midsize provider ofapplication maintenance and data managementsolutions. Nucleus Software likewise provides con-sulting, software development, support, and main-tenance services for GE Capital.

Hong Kong’s electronics industry also has MNCsas major buyers. For example, VTech serves as an

Table 1. India-based IT service network models.

Firm network Possible Possible model Description relationships network subtypes Examples

Subsidiary model The MNC’s Indian subsidiary provides all Wholly owned Intrafirm OracleIT services to the firm.

Subsidiary plus IT The MNC’s Indian subsidiary provides IT Wholly owned Intrafirm General Electric, service provider services along with one or more Indian or Equity-based partnership Joint venture Citibank, model non-Indian IT service provider(s). Contractual (long-term) or Interfirm Hewlett-Packard,

informal, project-based (short-term) IBM IT service The MNC does not have any Indian Equity-based partnership Joint venture Pyxis (aprovider model subsidiary and employs Indian or a Contractual (long-term) or Interfirm manufacturer of

combination of Indian and non-Indian IT informal, project-based (short-term) automated service providers either independently or medication and with the assistance of outsourcing firms. supply dispensing

systems)

Authorized licensed use limited to: San Jose State University. Downloaded on August 23, 2009 at 00:46 from IEEE Xplore. Restrictions apply.

original equipment manufacturer to numerousMNCs based in G-7 countries.3

Government supportThe Indian government has played a central role in

establishing and promoting the IT services industry.It created software technology parks to provide thenecessary office space, data and satellite communi-cation links, and hardware and prioritized fundingof the country’s telecommunications infrastructure.To facilitate exports, the Indian government provideseasily obtainable licenses, rebates, duty-free imports,credits, international trade fair subsidies, and researchsupport, and in 1995 it permanently exempted ser-vice exports from income taxes.12

This pattern follows the example of Taiwan’s gov-ernment, which established export processing zones

in the 1960s to promote electronics production andhas since provided financial assistance, training, andresearch and development support.13 The Singaporegovernment likewise helped disk-drive giant SeagateTechnology at every step, including a 10-year taxholiday and factory space in an industrial park. TheKorean government similarly helped Samsung andother chaebols or conglomerates become majorexporters in the electronics market.3

Quality focusThe East Asian electronics and computer hard-

ware industries demonstrate that mastery of low-cost production is not sufficient to remain part ofan MNC network. A supplier that wants to moveup the value chain—from original equipment tooriginal design manufacturer—must also meet

January 2005 73

Owner: GE Industrial and SatyamCustomer: GE Industrial Systems

Owne

r: GE

Cap

ital

Cust

omer

: GE

and

othe

r MNC

s

Owne

r and

custo

mer

: GE A

ircra

ft

Engin

es an

d GE A

pplia

nces

Owner and customer:

GE Medical Systems

Owner and customer: GE

Owner: Tata Group and public

Customer: GE (at least $100 million)

Owner: GE Equity ($108 million)

Customer: GE (m

ain customer)

Owner: GE and Citadel Health

Customer: GE and others

Owner: GE Equity and Birla Group

Customer: GE

Satyam—GE SoftwareServices

(Joint venture)

SatyamComputerServices(Indian

IT serviceprovider)

GE MedicalSystems

InformationTechnology

(Joint venture)

GlobalTechnology

Operations—India

(Subsidiary)

BirlaSoft(Joint venture)

John F. WelchTechnology

Center(Subsidiary)

GE GlobalTechnologySolutions

(Subsidiary)

NucleusSoftware

(IT serviceprovider)

Owner: Public

Customer: GE (large customer)

Owne

r: Pu

blic

Custo

mer

: GE (

38%

of sa

les)

iGATEGlobal

Solutions(IT serviceprovider)

PatniComputerServices(Indian

IT serviceprovider)

TataConsultancy

Services(Indian

IT serviceprovider)

GE SoftwareSolutions

(Subsidiary)

Owne

r: Pu

blic

Cust

omer

: GE

(20%

of s

ales

)

General Electric(MNC)

Interfirm network

Intrafirm networkJoint venture network

Figure 1. GeneralElectric’s India-based IT service network model. Thesubsidiary plus ITservice providermodel is currentlybecoming the dominant MNCmodel.

Authorized licensed use limited to: San Jose State University. Downloaded on August 23, 2009 at 00:46 from IEEE Xplore. Restrictions apply.

74 Computer

stringent quality, time-to-market, and flexibilityrequirements.8 Following this example, IT serviceproviders in India put a premium on quality. ByDecember 2002, 254 firms had acquired qualitycertification—including International Organizationfor Standardization 9001, Capability MaturityModel, CMM Integrated, People CMM, and SixSigma—with 77 more in the pipeline. Forty-eight ofthese had CMM Level 5 certification—the most inthe world. All 12 of GE’s IT service-providing enti-ties are quality certified.

Traditionally, application development constitutedabout 80 percent of India’s IT service exports. Indianfirms are now beginning to offer other services suchas system integration, package implementation, IToutsourcing, R&D outsourcing, and IT consulting.They have also expanded from banking andtelecommunications to include utilities, healthcare,and retailing. Wipro and TCS recently won large IToutsourcing contracts from British utilities, andInfosys is providing mission-critical support for aleading network-equipment-manufacturing MNC.

This parallels the East Asian experience. In thelate 1960s, US MNCs established cheap produc-tion locations in the region, but by the early 1980sthey had started to upgrade their assembly plat-forms and source more parts and components fromlocal firms. In the 1990s, these MNCs furtherupgraded their subsidiaries and significantlyincreased sourcing from local firms, which evendesigned key components.9 MNCs have startedupgrading some of their Indian subsidiaries, such asGE’s establishment of the John F. Welch TechnologyCenter in 2000, and sourcing higher value-addedIT services from local service providers.

AN INDUSTRY IN FLUXA decade ago, MNCs relied on interim IT service

contractors in India, known as “body-shopping”

in industry terminology. Today, however, a sub-stantial portion of this work is performed in Indiarather than at client sites in G-7 countries. In 1999-2000, revenue from IT services work done in themajor industrialized countries was roughly doublethat of work performed in India; in 2002-2003,revenue of India-based IT service firms increased49 percent, more than four times the growth rateof IT service companies based in G-7 locations.1

Table 2 lists the total revenue of the leading IT ser-vice firms in India by firm type.

This shift has just begun, with fewer than 40 ITservice contracts valued at more than $20 million.According to a 2000 Organization of EconomicCooperation and Development report, a typicalproject in India is “small (less than 10 man-years),has a value of less than $1 million, and involvesmaintenance, porting an existing application froma legacy platform to a client-server platform orY2K work.”14 However, the size of IT service pro-jects is increasing, and conglomerates capable ofconducting large projects are emerging in India.For example, TCS recently won three contractsworth more than $40 million, while Wipro earneda $70 million deal.

MNCs headquartered in G-7 countries alreadyaccount for nearly one-quarter of India’s IT serviceexports, and they continue expanding operations.Major IT MNCs IBM and Oracle mandate Indiandevelopment centers as part of all global applicationdevelopment projects—for example, IBM GlobalServices has six such centers in India with 3,000employees. Electronic Data Systems and ComputerSciences Corporation have also substantially in-creased their presence. As the example of GE shows,non-IT MNCs are also vying to provide India-basedIT services. Other major MNCs with Indian sub-sidiaries that export IT services include Hughes,Hewlett-Packard, Siemens, Motorola, Texas Instru-ments, Intel, i2, and Cisco.

Although India’s IT services industry is dividedamong many firms, a relatively small group of themhave emerged as the main players. The top five ITservice companies in India have grown faster thanthe rest of the industry and now have 32 percentof the market share; the next 50 firms have hadconsiderably slower growth and have only 35 per-cent of the market share.1 Thus, India’s IT servicesindustry is not as consolidated as the East Asianelectronics and computer hardware industries. InTaiwan, for example, the top 10 PC manufacturerscontrol 80 percent of total production.11

The rapid growth of India’s IT services industryis largely fueled by the country’s relatively low IT

Table 2. IT service firms in India.

World HQ/Stock Global revenue Firm Firm type market listing* ($billion)

Infosys Indian startup India/Nasdaq 0.75 (2002-2003)HCL Technologies Indian startup India/BSE 0.39 (2002-2003)Tata Consultancy Indian conglomerate India/BSE and NSE 1.04 (2002-2003)ServicesWipro Indian conglomerate India/NYSE 0.90 (2002-2003)BirlaSoft Joint venture India/Private 0.05 (2001-2002)IBM IT MNC US/NYSE 81.20 (2003)Oracle IT MNC US/Nasdaq 9.48 (2003)General Electric Non-IT MNC US/NYSE 131.70 (2003)Citibank Non-IT MNC US/NYSE 71.30 (2003)Syntel Midsize US/Nasdaq 0.16 (2003)Covansys Midsize US/Nasdaq 0.38 (2003)

*BSE = Bombay Stock Exchange; Nasdaq = National Assoc. of Securities Dealers AutomatedQuotation (system); NSE = National Stock Exchange (India); NYSE = New York Stock Exchange

Authorized licensed use limited to: San Jose State University. Downloaded on August 23, 2009 at 00:46 from IEEE Xplore. Restrictions apply.

employee costs, which average only $5,880 peryear.1 The wholesale shifting of industry locationsdue to international wage differentials is nothingnew. Logitech, the world’s largest producer of com-puter tracking devices, shifted production from theUS to Taiwan in 1987 and, eight years later, movedits manufacturing operations from Taiwan toChina.8,10 Several other MNCs have likewise relo-cated their production networks to China and otherlow-wage countries including the Philippines,Argentina, the Czech Republic, and Russia. In fact,several Indian IT service providers, in large part tosecure even cheaper labor, have recently openedoffices in China and elsewhere.

W ith some differences, particularly theabsence of multiple supply tiers, India’s ITservices industry is undergoing a transfor-

mation similar to that of East Asia’s electronics andcomputer hardware industries. Currently, thisindustry is dependent on MNCs, partly as ownersand mostly as buyers, who are outsourcing moreIT service operations to remain internationallycompetitive. MNCs have adopted different pro-duction models, with the subsidiary plus IT serviceprovider emerging as the dominant one.

India-based IT service providers, includingMNCs, have significantly enhanced their opera-tions in size, sophistication, and quality to increasemarket share and vie for higher value-added ser-vices. Local as well as MNC IT service providerscontinue to pursue new locations in India and othercountries that provide skill and cost advantages. Asthese providers achieve quality parity, price-basedcompetition is likely to increase, and industry con-solidation along the lines of its East Asian coun-terparts is likely to follow.!

References1. National Assoc. of Software and Service Companies,

Strategic Review 2003: The IT Industry in India,Nasscom Publications, 2003.

2. National Assoc. of Software and Service Companies,Strategic Review 2004: The IT Industry in India,Nasscom Publications, 2004.

3. J. Dedrick and K.L. Kraemer, Asia’s Computer Chal-lenge: Threat or Opportunity for the United Statesand the World?, Oxford Univ. Press, 1998.

4. M. Aoki, Information, Incentives, and Bargaining inthe Japanese Economy, Cambridge Univ. Press, 1988.

5. C.A. Bartlett and S. Ghoshal, Managing Across Bor-ders: The Transnational Solution, 2nd ed., HarvardBusiness School Press, 1998.

6. M. Castells, The Rise of the Network Society, 2nded., Blackwell, 2000.

7. M. Kenny and R. Florida, Beyond Mass Production:The Japanese System and Its Transfer to the U.S.,Oxford Univ. Press, 1993.

8. D. Ernst, From Partial to Systemic Globalization:International Production Networks in the Electron-ics Industry, working paper 98, Berkeley Roundtableon the International Economy, 1997.

9. M. Borrus, “The Resurgence of US Electronics: AsianProduction Networks and the Rise of Wintelism,”International Production Networks in Asia: Rivalryor Riches?, S. Haggard, D. Ernst, and M. Borrus,eds., Routledge, 2000.

10. D. Ernst, “Global Production Networks and theChanging Geography of Innovation Systems: Impli-cations for Developing Countries,” Economics ofInnovation and New Technology, vol. 11, no. 6,2002, pp. 497-523.

11. D. Ernst, “What Permits David to Grow in theShadow of Goliath? The Taiwanese Model in theComputer Industry,” International Production Net-works in Asia: Rivalry or Riches?, S. Haggard, D.Ernst, and M. Borrus, eds., Routledge, 2000.

12. R.B. Heeks, India’s Software Industry, Sage Publica-tions, 1996.

13. T.S. Poon, Competition and Cooperation in Taiwan’sInformation Technology Industry: Inter-Firm Net-works and Industrial Upgrading, Quorum Books,2002.

14. A. Arora, “Software Development in Non-memberCountries: The Indian Case,” OECD InformationTechnology Outlook 2000: ICTs, E-Commerce, andthe Information Economy, Organization for Eco-nomic Cooperation and Development, 2000, pp.131-150.

Pratyush Bharati is an assistant professor of man-agement information systems at the University ofMassachusetts Boston’s College of Management.His research interests include management infor-mation systems and strategy, diffusion of e-com-merce technology in small and medium-sizeenterprises, information systems and service qual-ity, the global digital divide, and global productionof software and services. Bharati received a PhDin IT strategy from Rensselaer Polytechnic Insti-tute. He is a member of the ACM, the Associationfor Information Systems, and the InformationResources Management Association. Contact himat [email protected].

January 2005 75

Authorized licensed use limited to: San Jose State University. Downloaded on August 23, 2009 at 00:46 from IEEE Xplore. Restrictions apply.