Embed Size (px)

Citation preview

1

Indian Commercial Vehicle Industry Sector Report

Auto & Auto Ancillary Outlook : BULLISH

Ashok Leyland - Buy CMP: Rs69 Target price : Rs85 Upside: 23.1% Atul Auto – Buy CMP: Rs583 Target price : Rs740 Upside: 26.9% Eicher Motors – Buy CMP: Rs16938 Target price : Rs20079 Upside: 18.5% Force Motors - Accumulate CMP: Rs1413 Target price : Rs1538 Upside: 8.8% SML Isuzu - Buy CMP: Rs1005 Target price : Rs1222 Upside: 21.5% Indag Rubber- Buy CMP: Rs876 Target price : Rs1092 Upside: 24.7% Vidrum Mehta Research Analyst [email protected] Arun Gopalan VP – Research & Investments [email protected] February 19, 2015

The Indian Commercial Vehicle (CV) Industry is all set for a cyclical revival in demand going forward. The green shoots are visible as the overall domestic CV volumes is likely to grow by 10% in FY15 as against de-growth of 20% and 2% during FY14 and FY13 respectively. The recovery further looks promising as the volumes of Medium & Heavy Commercial Vehicle (M&HCV) one of the leading indicator grew by 13.9% in 9MFY15 as against a de-growth of more than 20% each in FY13 and FY14. Further the strong correlation between GDP and the growth in CV Industry emphasis that overall revival in the economy is bound to have a positive impact on the CV. The Government’s policy actions like diesel deregulation, opening up infrastructure and mining activity, plans to construct 30kms of road a day from FY16 onwards, faster project clearances is likely to result into higher industrial activities. The health of fleet operators is also better, after the steep fall in crude prices has resulted in lower fuel costs (which account for 40%-50% of operating cost), higher freight rates, improved utilization and softening of interest rates is likely to lower the cost of borrowing. With overall economic and industrial activity likely to improve we expect the demand for CVs to revive from FY16E and expect a cyclical revival in the entire CV segment. The bigger growth opportunities lies in the smaller companies and hence are positive on Ashok Leyland, Eicher Motors, Atul Auto and SML Isuzu. We are also positive on Indag rubber, which is a leading tyre re-treading company and would benefit directly from a revival in the CV cycle.

The new Central Government focuses on reforms --

Acceleration in reforms – The Government has undertaken various measures/steps and initiatives like faster clearances of projects, opening up mining sector are likely to boost Industrial activity. According to media reports, the Goa state government has issued an order revoking its 2012 decision that had halted over 60-year-old-mining industry. The new order will pave the way for the resumption of mining activities in the states. In addition government has taken various indirect measures like 100% FDI allowance under the automatic route in the road and highways sector and Standardized processes for PPP projects resulting into clear policy framework relating to bidding and tolling. We believe the governments reformist actions is a key positive for overall economic and the CV Industry growth going forward.

Focus on infrastructure development - The government has kept infrastructure development as one of its key priority to revive the economic growth. At present India has an extensive road network of 4.9 million kms and is the 2

nd largest in the

world after US. Government is focusing on construction of roads, extension and expansion of national highways (NH) (2 lanes to 4 lanes to 6 lanes) which is likely to boost infrastructure in India. According to reports, Road Transport and Highways minister has set the road construction target of 30 km per day from FY16 onwards. The actual road construction during 8MFY15 (April to Nov 2014) was ~8.5 km/day as against the targeted of 17 km/day. Of the total road network, NH accounts less than 2%, ~92,850 kms as of FY14 and is likely to touch 100,000 kms by FY17. Since ~40% of the vehicle traffic is carried by NH, development of the same is likely positive for the overall Auto industry and especially CV space.

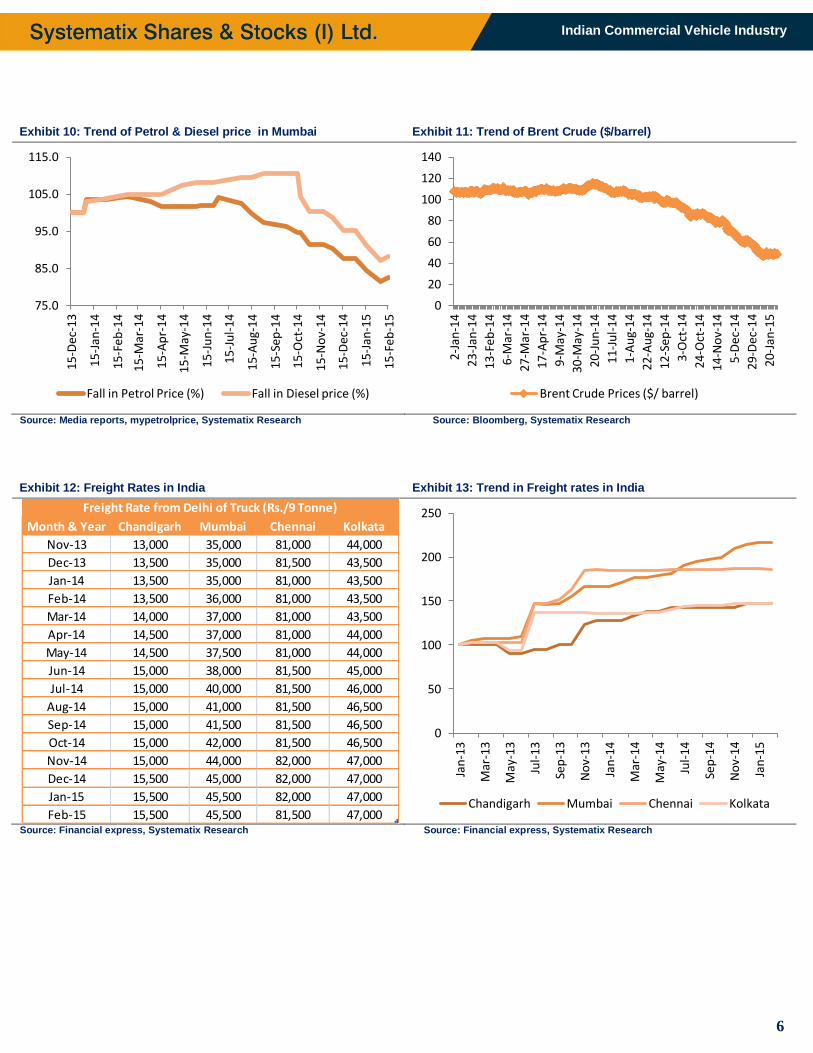

Fleet operators in a much better state: The fleet operating cost is likely to come down mainly after lower diesel prices and softening of interest rates. Over the last 8 months, Brent Crude prices have declined ~46% to $62 per barrel (at five and half year low) resulting into lower fuel cost. Even though the benefit is not fully passed on, the prices of petrol and diesel are down ~20% each during the same period. The operating cost of the fleet owners has also reduced as fuel accounts for 40%-50% of the overall cost. Despite the fall in fuel cost, domestic freight rates in India have not fallen over the last 6 to 8 months. We believe this is positive for the fleet owners which faced severe headwinds in the past 3 years and are now likely to generate higher cash flows not only from lower operating cost but also from steady realizations. RBI also lowered the interest rate which is likely to reduce the cost of borrowing and aid profitability of the fleet-owners.

Green shoots visible: The overall CV volumes are likely to grow ~ 10% for FY15 as compared to de-growth of 20% in FY14 and 2% in FY13. We believe strong revival in demand coupled with governments focus towards infrastructure development and favorable industry dynamics like lower fuel cost and softening of interest rates would further revive the CV demand going forward and hence we are positive of the CV Industry.

2

Indian Commercial Vehicle Industry

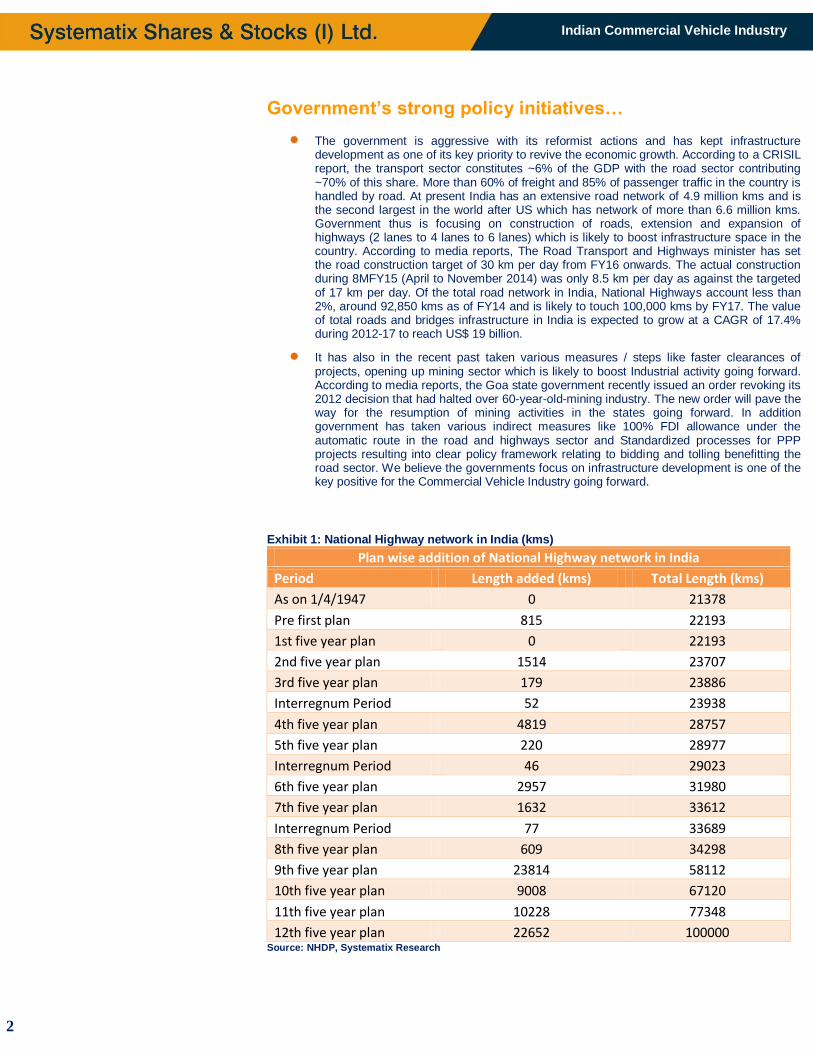

Government’s strong policy initiatives…

The government is aggressive with its reformist actions and has kept infrastructure development as one of its key priority to revive the economic growth. According to a CRISIL report, the transport sector constitutes ~6% of the GDP with the road sector contributing ~70% of this share. More than 60% of freight and 85% of passenger traffic in the country is handled by road. At present India has an extensive road network of 4.9 million kms and is the second largest in the world after US which has network of more than 6.6 million kms. Government thus is focusing on construction of roads, extension and expansion of highways (2 lanes to 4 lanes to 6 lanes) which is likely to boost infrastructure space in the country. According to media reports, The Road Transport and Highways minister has set the road construction target of 30 km per day from FY16 onwards. The actual construction during 8MFY15 (April to November 2014) was only 8.5 km per day as against the targeted of 17 km per day. Of the total road network in India, National Highways account less than 2%, around 92,850 kms as of FY14 and is likely to touch 100,000 kms by FY17. The value of total roads and bridges infrastructure in India is expected to grow at a CAGR of 17.4% during 2012-17 to reach US$ 19 billion.

It has also in the recent past taken various measures / steps like faster clearances of projects, opening up mining sector which is likely to boost Industrial activity going forward. According to media reports, the Goa state government recently issued an order revoking its 2012 decision that had halted over 60-year-old-mining industry. The new order will pave the way for the resumption of mining activities in the states going forward. In addition government has taken various indirect measures like 100% FDI allowance under the automatic route in the road and highways sector and Standardized processes for PPP projects resulting into clear policy framework relating to bidding and tolling benefitting the road sector. We believe the governments focus on infrastructure development is one of the key positive for the Commercial Vehicle Industry going forward.

Exhibit 1: National Highway network in India (kms)

Plan wise addition of National Highway network in India

Period Length added (kms) Total Length (kms)

As on 1/4/1947 0 21378

Pre first plan 815 22193

1st five year plan 0 22193

2nd five year plan 1514 23707

3rd five year plan 179 23886

Interregnum Period 52 23938

4th five year plan 4819 28757

5th five year plan 220 28977

Interregnum Period 46 29023

6th five year plan 2957 31980

7th five year plan 1632 33612

Interregnum Period 77 33689

8th five year plan 609 34298

9th five year plan 23814 58112

10th five year plan 9008 67120

11th five year plan 10228 77348

12th five year plan 22652 100000 Source: NHDP, Systematix Research

3

Indian Commercial Vehicle Industry

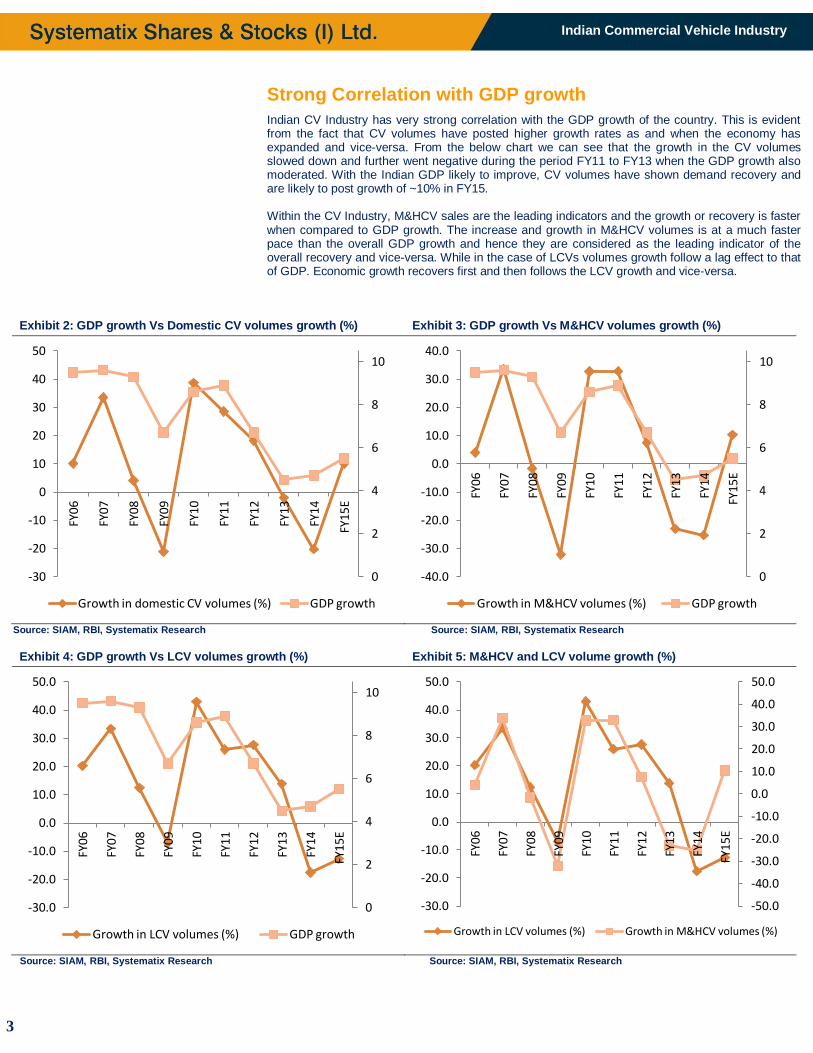

Strong Correlation with GDP growth

Indian CV Industry has very strong correlation with the GDP growth of the country. This is evident from the fact that CV volumes have posted higher growth rates as and when the economy has expanded and vice-versa. From the below chart we can see that the growth in the CV volumes slowed down and further went negative during the period FY11 to FY13 when the GDP growth also moderated. With the Indian GDP likely to improve, CV volumes have shown demand recovery and are likely to post growth of ~10% in FY15. Within the CV Industry, M&HCV sales are the leading indicators and the growth or recovery is faster when compared to GDP growth. The increase and growth in M&HCV volumes is at a much faster pace than the overall GDP growth and hence they are considered as the leading indicator of the overall recovery and vice-versa. While in the case of LCVs volumes growth follow a lag effect to that of GDP. Economic growth recovers first and then follows the LCV growth and vice-versa.

Exhibit 2: GDP growth Vs Domestic CV volumes growth (%) Exhibit 3: GDP growth Vs M&HCV volumes growth (%)

Source: SIAM, RBI, Systematix Research Source: SIAM, RBI, Systematix Research

Exhibit 4: GDP growth Vs LCV volumes growth (%) Exhibit 5: M&HCV and LCV volume growth (%)

Source: SIAM, RBI, Systematix Research Source: SIAM, RBI, Systematix Research

0

2

4

6

8

10

-30

-20

-10

0

10

20

30

40

50

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

E

Growth in domestic CV volumes (%) GDP growth

0

2

4

6

8

10

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

E

Growth in M&HCV volumes (%) GDP growth

0

2

4

6

8

10

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY15

E

Growth in LCV volumes (%) GDP growth

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY1

5E

Growth in LCV volumes (%) Growth in M&HCV volumes (%)

4

Indian Commercial Vehicle Industry

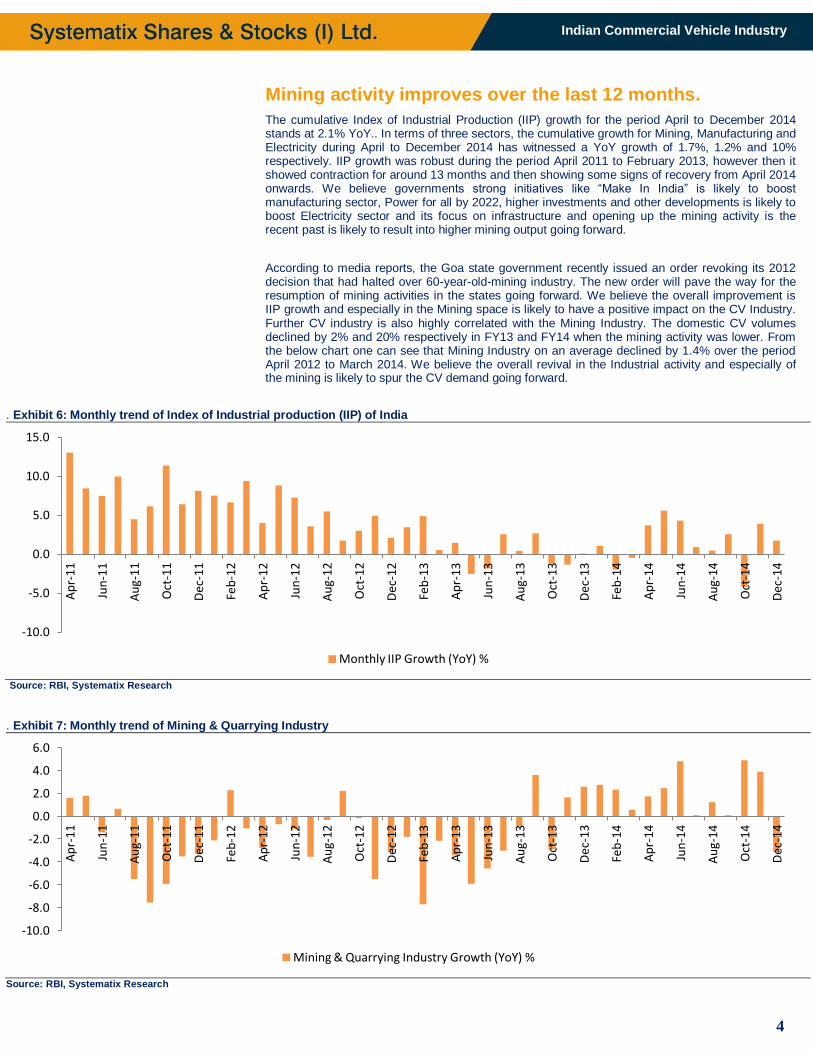

Mining activity improves over the last 12 months.

The cumulative Index of Industrial Production (IIP) growth for the period April to December 2014 stands at 2.1% YoY.. In terms of three sectors, the cumulative growth for Mining, Manufacturing and Electricity during April to December 2014 has witnessed a YoY growth of 1.7%, 1.2% and 10% respectively. IIP growth was robust during the period April 2011 to February 2013, however then it showed contraction for around 13 months and then showing some signs of recovery from April 2014 onwards. We believe governments strong initiatives like “Make In India” is likely to boost manufacturing sector, Power for all by 2022, higher investments and other developments is likely to boost Electricity sector and its focus on infrastructure and opening up the mining activity is the recent past is likely to result into higher mining output going forward.

According to media reports, the Goa state government recently issued an order revoking its 2012 decision that had halted over 60-year-old-mining industry. The new order will pave the way for the resumption of mining activities in the states going forward. We believe the overall improvement is IIP growth and especially in the Mining space is likely to have a positive impact on the CV Industry. Further CV industry is also highly correlated with the Mining Industry. The domestic CV volumes declined by 2% and 20% respectively in FY13 and FY14 when the mining activity was lower. From the below chart one can see that Mining Industry on an average declined by 1.4% over the period April 2012 to March 2014. We believe the overall revival in the Industrial activity and especially of the mining is likely to spur the CV demand going forward.

. Exhibit 6: Monthly trend of Index of Industrial production (IIP) of India

Source: RBI, Systematix Research

. Exhibit 7: Monthly trend of Mining & Quarrying Industry

Source: RBI, Systematix Research

-10.0

-5.0

0.0

5.0

10.0

15.0

Ap

r-1

1

Jun

-11

Au

g-11

Oct

-11

Dec

-11

Feb

-12

Ap

r-1

2

Jun

-12

Au

g-12

Oct

-12

Dec

-12

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-13

Oct

-13

Dec

-13

Feb

-14

Ap

r-1

4

Jun

-14

Au

g-14

Oct

-14

Dec

-14

Monthly IIP Growth (YoY) %

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Ap

r-11

Jun

-11

Au

g-11

Oct

-11

Dec

-11

Feb

-12

Ap

r-12

Jun

-12

Au

g-12

Oct

-12

Dec

-12

Feb

-13

Ap

r-13

Jun

-13

Au

g-13

Oct

-13

Dec

-13

Feb

-14

Ap

r-14

Jun

-14

Au

g-14

Oct

-14

Dec

-14

Mining & Quarrying Industry Growth (YoY) %

5

Indian Commercial Vehicle Industry

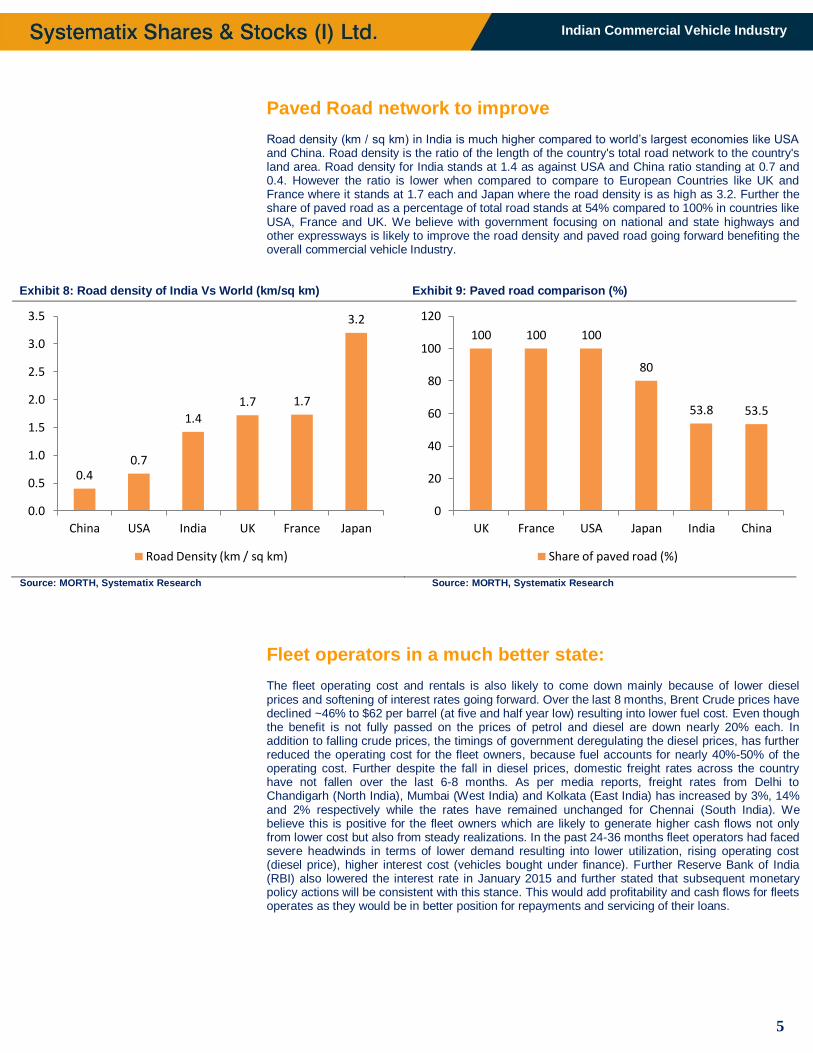

Paved Road network to improve Road density (km / sq km) in India is much higher compared to world’s largest economies like USA and China. Road density is the ratio of the length of the country's total road network to the country's land area. Road density for India stands at 1.4 as against USA and China ratio standing at 0.7 and 0.4. However the ratio is lower when compared to compare to European Countries like UK and France where it stands at 1.7 each and Japan where the road density is as high as 3.2. Further the share of paved road as a percentage of total road stands at 54% compared to 100% in countries like USA, France and UK. We believe with government focusing on national and state highways and other expressways is likely to improve the road density and paved road going forward benefiting the overall commercial vehicle Industry.

Exhibit 8: Road density of India Vs World (km/sq km) Exhibit 9: Paved road comparison (%)

Source: MORTH, Systematix Research Source: MORTH, Systematix Research

Fleet operators in a much better state: The fleet operating cost and rentals is also likely to come down mainly because of lower diesel prices and softening of interest rates going forward. Over the last 8 months, Brent Crude prices have declined ~46% to $62 per barrel (at five and half year low) resulting into lower fuel cost. Even though the benefit is not fully passed on the prices of petrol and diesel are down nearly 20% each. In addition to falling crude prices, the timings of government deregulating the diesel prices, has further reduced the operating cost for the fleet owners, because fuel accounts for nearly 40%-50% of the operating cost. Further despite the fall in diesel prices, domestic freight rates across the country have not fallen over the last 6-8 months. As per media reports, freight rates from Delhi to Chandigarh (North India), Mumbai (West India) and Kolkata (East India) has increased by 3%, 14% and 2% respectively while the rates have remained unchanged for Chennai (South India). We believe this is positive for the fleet owners which are likely to generate higher cash flows not only from lower cost but also from steady realizations. In the past 24-36 months fleet operators had faced severe headwinds in terms of lower demand resulting into lower utilization, rising operating cost (diesel price), higher interest cost (vehicles bought under finance). Further Reserve Bank of India (RBI) also lowered the interest rate in January 2015 and further stated that subsequent monetary policy actions will be consistent with this stance. This would add profitability and cash flows for fleets operates as they would be in better position for repayments and servicing of their loans.

0.4 0.7

1.4 1.7 1.7

3.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

China USA India UK France Japan

Road Density (km / sq km)

100 100 100

80

53.8 53.5

0

20

40

60

80

100

120

UK France USA Japan India China

Share of paved road (%)

6

Indian Commercial Vehicle Industry

Exhibit 10: Trend of Petrol & Diesel price in Mumbai Exhibit 11: Trend of Brent Crude ($/barrel)

Source: Media reports, mypetrolprice, Systematix Research Source: Bloomberg, Systematix Research

Exhibit 12: Freight Rates in India Exhibit 13: Trend in Freight rates in India

Source: Financial express, Systematix Research Source: Financial express, Systematix Research

75.0

85.0

95.0

105.0

115.0

15-D

ec-1

3

15-J

an-1

4

15-F

eb-1

4

15-M

ar-1

4

15-A

pr-

14

15-M

ay-1

4

15-J

un

-14

15-J

ul-

14

15-A

ug-

14

15-S

ep-1

4

15-O

ct-1

4

15-N

ov-

14

15-D

ec-1

4

15-J

an-1

5

15-F

eb-1

5

Fall in Petrol Price (%) Fall in Diesel price (%)

0

20

40

60

80

100

120

140

2-Ja

n-1

4

23-J

an-1

4

13-F

eb-1

4

6-M

ar-1

4

27-M

ar-1

4

17-A

pr-

14

9-M

ay-1

4

30-M

ay-1

4

20-J

un

-14

11-J

ul-

14

1-A

ug-

14

22-A

ug-

14

12-S

ep-1

4

3-O

ct-1

4

24-O

ct-1

4

14-N

ov-

14

5-D

ec-1

4

29-D

ec-1

4

20-J

an-1

5

Brent Crude Prices ($/ barrel)

Month & Year Chandigarh Mumbai Chennai Kolkata

Nov-13 13,000 35,000 81,000 44,000

Dec-13 13,500 35,000 81,500 43,500

Jan-14 13,500 35,000 81,000 43,500

Feb-14 13,500 36,000 81,000 43,500

Mar-14 14,000 37,000 81,000 43,500

Apr-14 14,500 37,000 81,000 44,000

May-14 14,500 37,500 81,000 44,000

Jun-14 15,000 38,000 81,500 45,000

Jul-14 15,000 40,000 81,500 46,000

Aug-14 15,000 41,000 81,500 46,500

Sep-14 15,000 41,500 81,500 46,500

Oct-14 15,000 42,000 81,500 46,500

Nov-14 15,000 44,000 82,000 47,000

Dec-14 15,500 45,000 82,000 47,000

Jan-15 15,500 45,500 82,000 47,000

Feb-15 15,500 45,500 81,500 47,000

Freight Rate from Delhi of Truck (Rs./9 Tonne)

0

50

100

150

200

250

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-13

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-14

Jan

-15

Chandigarh Mumbai Chennai Kolkata

7

Indian Commercial Vehicle Industry

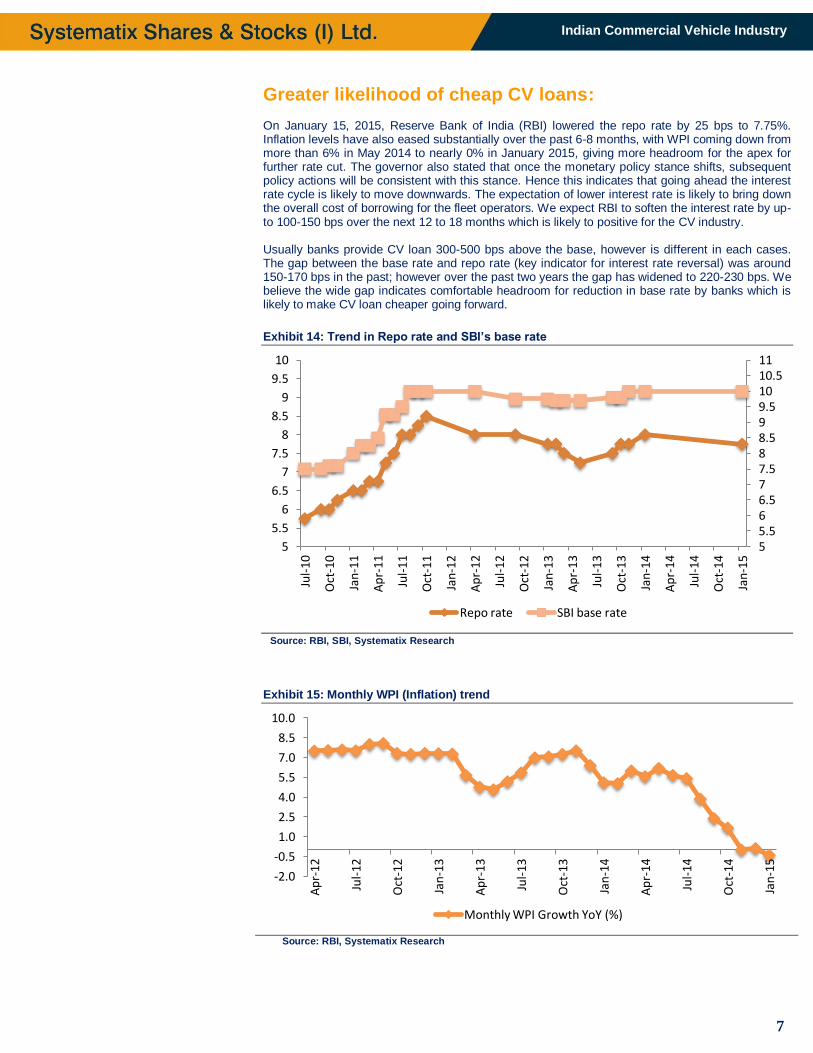

Greater likelihood of cheap CV loans: On January 15, 2015, Reserve Bank of India (RBI) lowered the repo rate by 25 bps to 7.75%. Inflation levels have also eased substantially over the past 6-8 months, with WPI coming down from more than 6% in May 2014 to nearly 0% in January 2015, giving more headroom for the apex for further rate cut. The governor also stated that once the monetary policy stance shifts, subsequent policy actions will be consistent with this stance. Hence this indicates that going ahead the interest rate cycle is likely to move downwards. The expectation of lower interest rate is likely to bring down the overall cost of borrowing for the fleet operators. We expect RBI to soften the interest rate by up-to 100-150 bps over the next 12 to 18 months which is likely to positive for the CV industry. Usually banks provide CV loan 300-500 bps above the base, however is different in each cases. The gap between the base rate and repo rate (key indicator for interest rate reversal) was around 150-170 bps in the past; however over the past two years the gap has widened to 220-230 bps. We believe the wide gap indicates comfortable headroom for reduction in base rate by banks which is likely to make CV loan cheaper going forward.

Exhibit 14: Trend in Repo rate and SBI’s base rate

Source: RBI, SBI, Systematix Research

Exhibit 15: Monthly WPI (Inflation) trend

Source: RBI, Systematix Research

5 5.5 6 6.5 7 7.5 8 8.5 9 9.5 10 10.5 11

5

5.5

6

6.5

7

7.5

8

8.5

9

9.5

10

Jul-

10

Oct

-10

Jan

-11

Ap

r-11

Jul-

11

Oct

-11

Jan

-12

Ap

r-12

Jul-

12

Oct

-12

Jan

-13

Ap

r-13

Jul-

13

Oct

-13

Jan

-14

Ap

r-14

Jul-

14

Oct

-14

Jan

-15

Repo rate SBI base rate

-2.0

-0.5

1.0

2.5

4.0

5.5

7.0

8.5

10.0

Ap

r-12

Jul-

12

Oct

-12

Jan

-13

Ap

r-13

Jul-

13

Oct

-13

Jan

-14

Ap

r-14

Jul-

14

Oct

-14

Jan

-15

Monthly WPI Growth YoY (%)

8

Indian Commercial Vehicle Industry

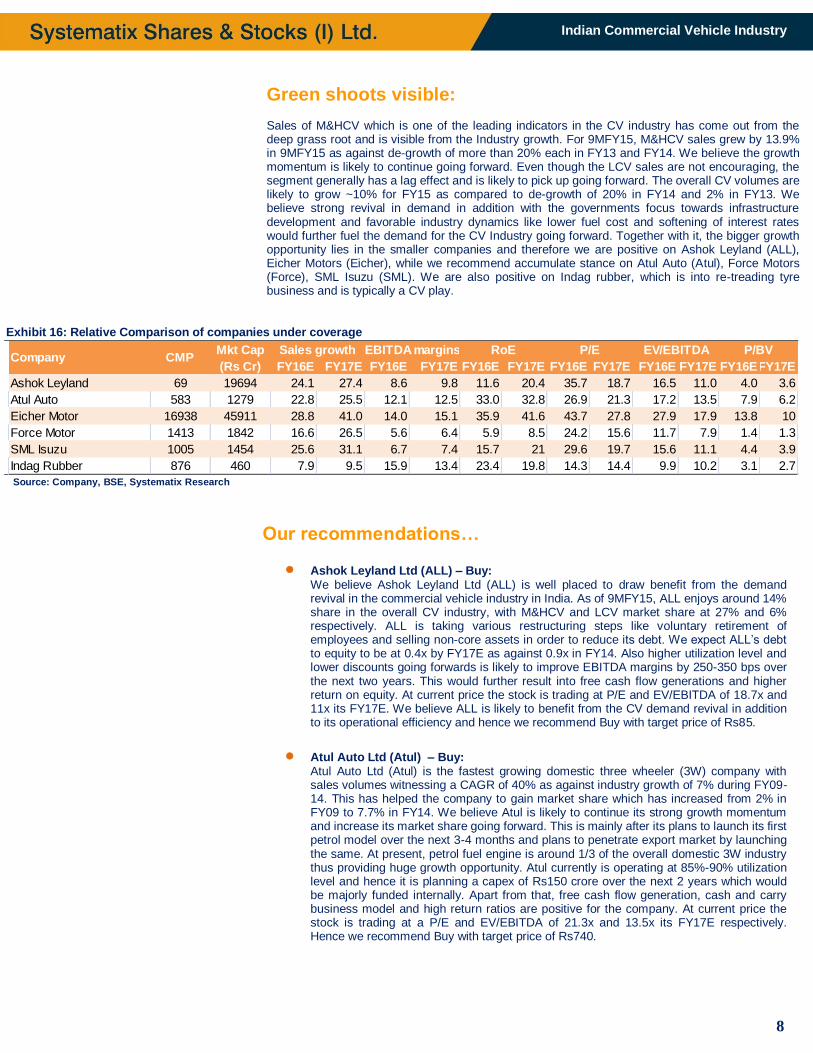

Green shoots visible: Sales of M&HCV which is one of the leading indicators in the CV industry has come out from the deep grass root and is visible from the Industry growth. For 9MFY15, M&HCV sales grew by 13.9% in 9MFY15 as against de-growth of more than 20% each in FY13 and FY14. We believe the growth momentum is likely to continue going forward. Even though the LCV sales are not encouraging, the segment generally has a lag effect and is likely to pick up going forward. The overall CV volumes are likely to grow ~10% for FY15 as compared to de-growth of 20% in FY14 and 2% in FY13. We believe strong revival in demand in addition with the governments focus towards infrastructure development and favorable industry dynamics like lower fuel cost and softening of interest rates would further fuel the demand for the CV Industry going forward. Together with it, the bigger growth opportunity lies in the smaller companies and therefore we are positive on Ashok Leyland (ALL), Eicher Motors (Eicher), while we recommend accumulate stance on Atul Auto (Atul), Force Motors (Force), SML Isuzu (SML). We are also positive on Indag rubber, which is into re-treading tyre business and is typically a CV play.

Exhibit 16: Relative Comparison of companies under coverage

Source: Company, BSE, Systematix Research

Our recommendations…

Ashok Leyland Ltd (ALL) – Buy: We believe Ashok Leyland Ltd (ALL) is well placed to draw benefit from the demand revival in the commercial vehicle industry in India. As of 9MFY15, ALL enjoys around 14% share in the overall CV industry, with M&HCV and LCV market share at 27% and 6% respectively. ALL is taking various restructuring steps like voluntary retirement of employees and selling non-core assets in order to reduce its debt. We expect ALL’s debt to equity to be at 0.4x by FY17E as against 0.9x in FY14. Also higher utilization level and lower discounts going forwards is likely to improve EBITDA margins by 250-350 bps over the next two years. This would further result into free cash flow generations and higher return on equity. At current price the stock is trading at P/E and EV/EBITDA of 18.7x and 11x its FY17E. We believe ALL is likely to benefit from the CV demand revival in addition to its operational efficiency and hence we recommend Buy with target price of Rs85.

Atul Auto Ltd (Atul) – Buy: Atul Auto Ltd (Atul) is the fastest growing domestic three wheeler (3W) company with sales volumes witnessing a CAGR of 40% as against industry growth of 7% during FY09-14. This has helped the company to gain market share which has increased from 2% in FY09 to 7.7% in FY14. We believe Atul is likely to continue its strong growth momentum and increase its market share going forward. This is mainly after its plans to launch its first petrol model over the next 3-4 months and plans to penetrate export market by launching the same. At present, petrol fuel engine is around 1/3 of the overall domestic 3W industry thus providing huge growth opportunity. Atul currently is operating at 85%-90% utilization level and hence it is planning a capex of Rs150 crore over the next 2 years which would be majorly funded internally. Apart from that, free cash flow generation, cash and carry business model and high return ratios are positive for the company. At current price the stock is trading at a P/E and EV/EBITDA of 21.3x and 13.5x its FY17E respectively. Hence we recommend Buy with target price of Rs740.

FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16EFY17E

Ashok Leyland 69 19694 24.1 27.4 8.6 9.8 11.6 20.4 35.7 18.7 16.5 11.0 4.0 3.6

Atul Auto 583 1279 22.8 25.5 12.1 12.5 33.0 32.8 26.9 21.3 17.2 13.5 7.9 6.2

Eicher Motor 16938 45911 28.8 41.0 14.0 15.1 35.9 41.6 43.7 27.8 27.9 17.9 13.8 10

Force Motor 1413 1842 16.6 26.5 5.6 6.4 5.9 8.5 24.2 15.6 11.7 7.9 1.4 1.3

SML Isuzu 1005 1454 25.6 31.1 6.7 7.4 15.7 21 29.6 19.7 15.6 11.1 4.4 3.9

Indag Rubber 876 460 7.9 9.5 15.9 13.4 23.4 19.8 14.3 14.4 9.9 10.2 3.1 2.7

P/BVCMP

Mkt Cap

(Rs Cr)Company

Sales growth EBITDA margins RoE P/E EV/EBITDA

9

Indian Commercial Vehicle Industry

Eicher Motors Ltd (Eicher) - Buy: Eicher Motors Ltd is a dual play on sustained strong growth from its motorcycle business and Volvo Eicher Commercial Vehicles (VECV) which is well placed to grab the CV recovery in India. Its motorcycle business owns the iconic brand “Royal Enfield” and its volumes have witnessed a CAGR of 42% over CY09-14. It has consistently increased its motorcycle capacity over the last 3-4 years and is likely to maintain its strong growth momentum going forward too. On the other hand, VECV is well placed to grab the demand revival in Indian CV space. As of December 2014, VECV market share stands at ~6% in the overall CV industry and ~12% share in the M&HCV segment. The launch of Pro-series along with the expected recovery in demand is likely to expand its overall share in the CV space. With VECV expected to post better performance, consolidated EBITDA margins is likely to expand from 10.5% in CY13 to 15% in CY16 further boosting profitability. At current price the stock is trading at P/E and EV/EBITDA of 27.8x and 17.9x its CY16E respectively. We believe higher earnings growth from VECV segment would eventually bring down the valuation multiple going forward and hence we recommend Buy with target of Rs20079.

Force Motors Ltd (Force) - Accumulate: Force Motors Ltd (Force) is a fully integrated automobile company with a focus on design and development of vehicles (mainly into LCV, UV’s and tractors) and auto components in India. The company has strong brand recall with Traveller being one of the prominent names enjoying the market leadership position of 41% share in the LCV passenger segment in India. Force also has technical collaboration with Daimler AG, Germany in respect of multi-purpose passenger vehicles. Further as per media reports, Indian arm of German luxury auto maker BMW is likely to partner Force motors, in its strategy for localization of its resources at its Chennai plant. We believe the company has diversified business segment and is well placed to benefit from the revival in the overall recovery in the automobile industry in India. Higher demand is likely to improve the utilization level and operating performance resulting into margin expansion going forward. At current price the stock is trading at trading at P/E and EV/EBITDA of 15.6x and 7.9x its FY17E respectively. Hence we are positive on the stock with a target price of Rs1538.

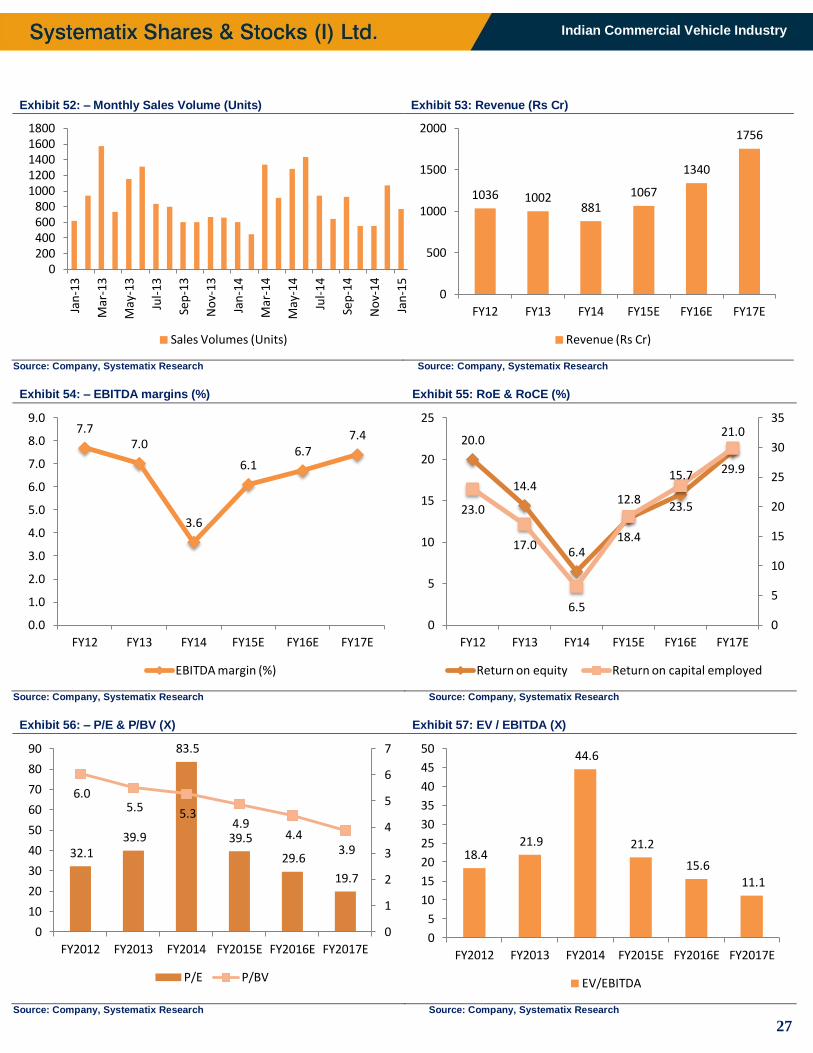

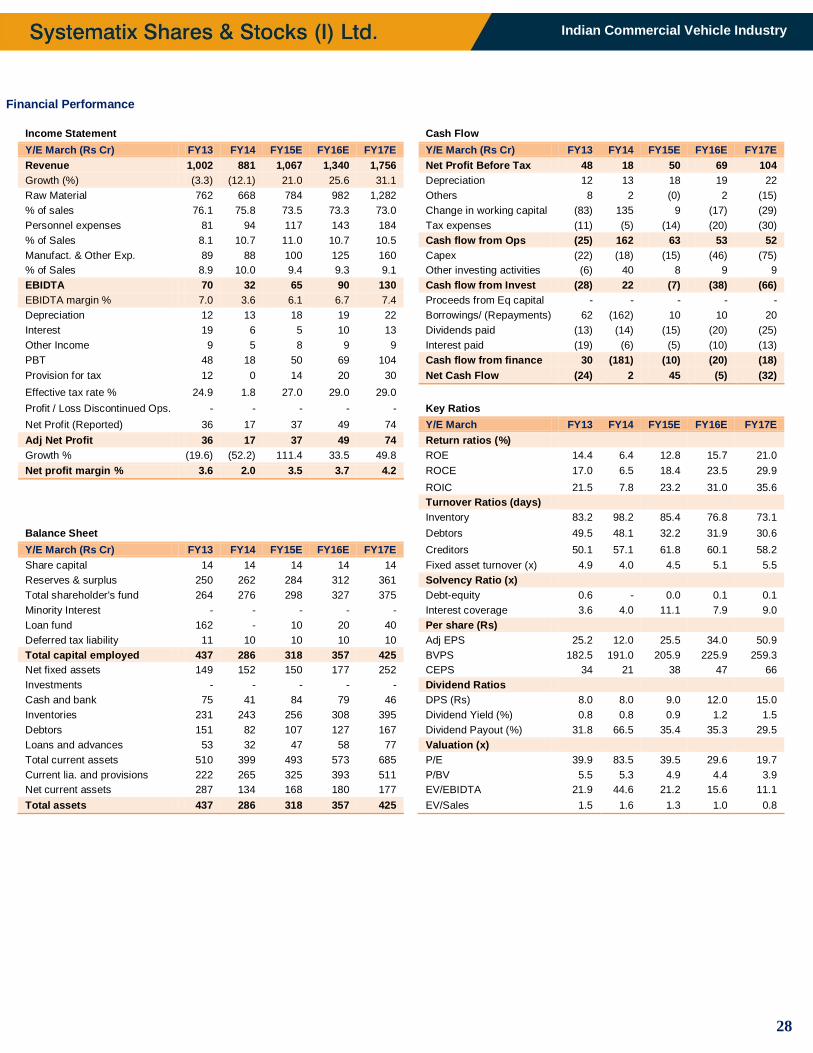

SML Isuzu Ltd (SML) - Buy: SML Isuzu Ltd (SML) is a small player with market share of 2% in the overall CV industry in India. It operates in 5-12 tonne gross vehicle weight (GVW) segment with passenger/cargo sales volume mix at 55:45 respectively. During 9MFY15, SML volume grew by 13% YoY to 7,988 units outpacing the overall CV industry volume which declined by 6% YoY (M&HCV grew by 10% while LCV declined 13%). With the expectation of revival in demand in addition with company’s focus on new launches is likely to increase its share to 15% from 9.7% in FY14 in the 5-12 tonne category over the next 2-3 years. Higher utilization level would result into operating efficiencies and margin expansion going forward. At current price the stock is trading at P/E and EV/EBITDA of 19.7x and 11.1x its FY17E earnings. Considering its strong financial performance, net cash, free cash flow and consistent dividend payout could result into re-rating of the stock. Hence we recommend Buy with target of Rs1222.

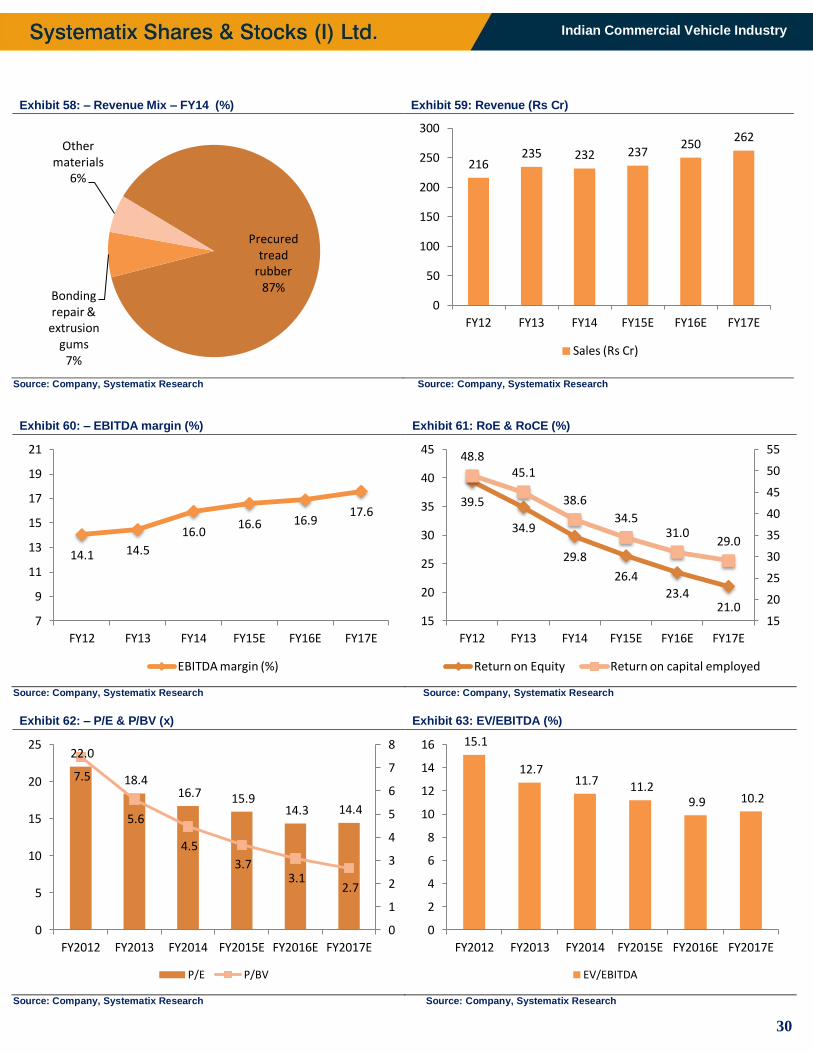

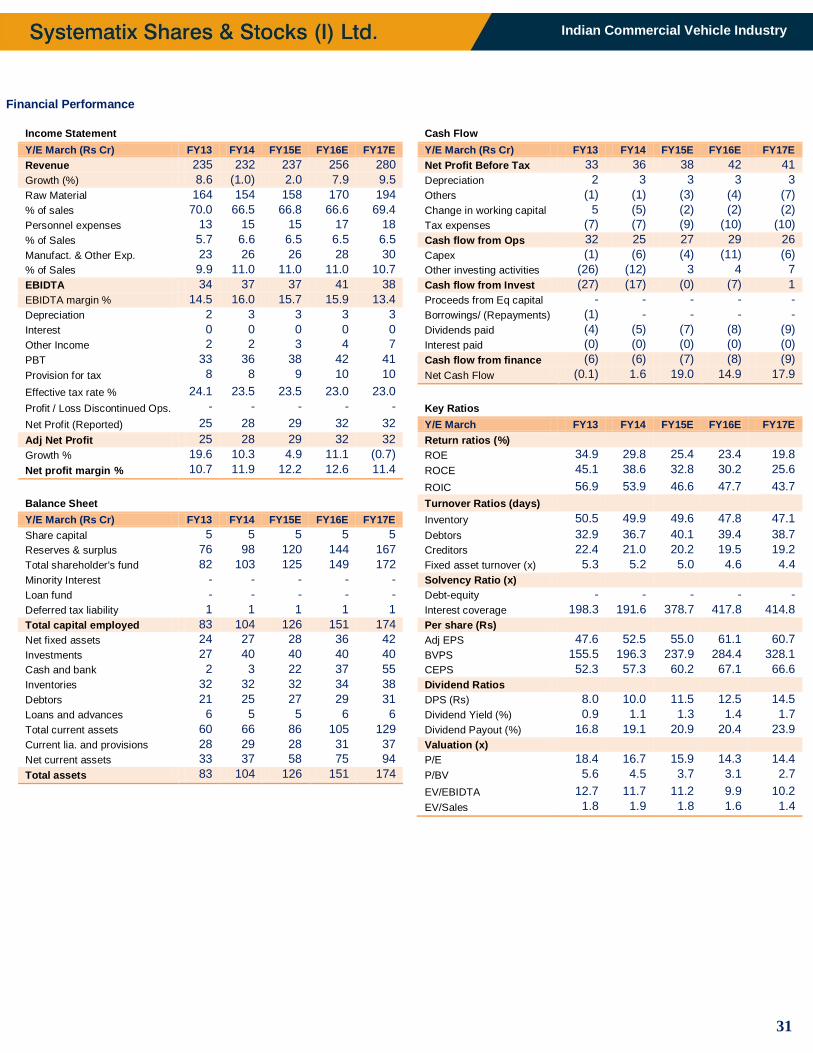

Indag Rubber Ltd (Indag) - Buy: Indag Rubber is into tyre re-treading business with market share of ~23% in the organized cold process tread manufacturing in India. The re-treading of tyre is particularly done in case of commercial vehicle in India. With the demand expected to revive in the CV space we expect the demand for re-treading to also gather momentum. Indag has large distribution network with 25 depots, 600 re-treader and 150 dealers across India. Re-treading of the tyre is cost effective (saves 50%-70% compared to new tyre), and is safer and durable similar to new tyre thus improving fleet operators margins and ensuring similar kind performance. Further the likely implementation of GST would reduce the pricing gap of 12%-25% which currently unorganized players enjoy over the organized players. Indag is debt free, free cash flow generating with high return on equity of 30%. At current price the stock is trading at P/E of 14.4x its FY17E EPS of Rs61. We believe Indag is well placed to capture the growth opportunity rising from the recovery of the Indian CV industry going forward. Hence we recommend Buy with target price of Rs1092 .

10

Indian Commercial Vehicle Industry

Indian Automobile Industry

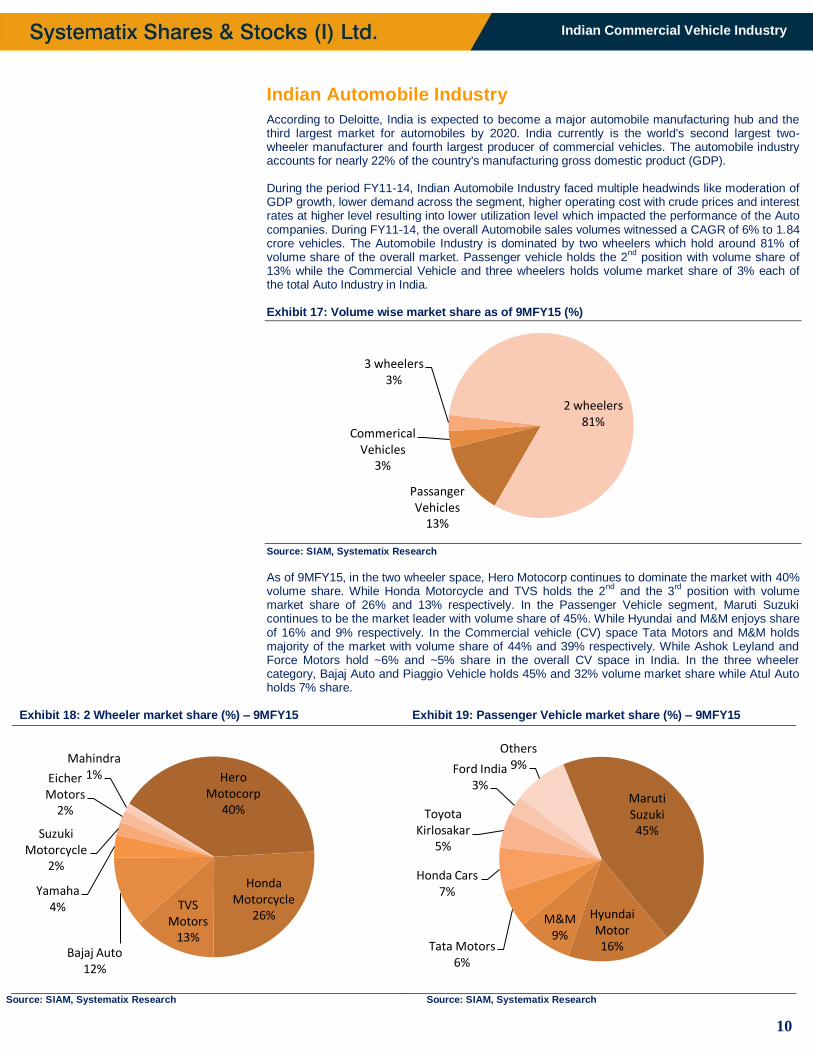

According to Deloitte, India is expected to become a major automobile manufacturing hub and the third largest market for automobiles by 2020. India currently is the world's second largest two-wheeler manufacturer and fourth largest producer of commercial vehicles. The automobile industry accounts for nearly 22% of the country's manufacturing gross domestic product (GDP). During the period FY11-14, Indian Automobile Industry faced multiple headwinds like moderation of GDP growth, lower demand across the segment, higher operating cost with crude prices and interest rates at higher level resulting into lower utilization level which impacted the performance of the Auto companies. During FY11-14, the overall Automobile sales volumes witnessed a CAGR of 6% to 1.84 crore vehicles. The Automobile Industry is dominated by two wheelers which hold around 81% of volume share of the overall market. Passenger vehicle holds the 2

nd position with volume share of

13% while the Commercial Vehicle and three wheelers holds volume market share of 3% each of the total Auto Industry in India. Exhibit 17: Volume wise market share as of 9MFY15 (%)

Source: SIAM, Systematix Research

As of 9MFY15, in the two wheeler space, Hero Motocorp continues to dominate the market with 40% volume share. While Honda Motorcycle and TVS holds the 2

nd and the 3

rd position with volume

market share of 26% and 13% respectively. In the Passenger Vehicle segment, Maruti Suzuki continues to be the market leader with volume share of 45%. While Hyundai and M&M enjoys share of 16% and 9% respectively. In the Commercial vehicle (CV) space Tata Motors and M&M holds majority of the market with volume share of 44% and 39% respectively. While Ashok Leyland and Force Motors hold ~6% and ~5% share in the overall CV space in India. In the three wheeler category, Bajaj Auto and Piaggio Vehicle holds 45% and 32% volume market share while Atul Auto holds 7% share.

Exhibit 18: 2 Wheeler market share (%) – 9MFY15 Exhibit 19: Passenger Vehicle market share (%) – 9MFY15

Source: SIAM, Systematix Research Source: SIAM, Systematix Research

Passanger Vehicles

13%

Commerical Vehicles

3%

3 wheelers 3%

2 wheelers 81%

Hero Motocorp

40%

Honda Motorcycle

26% TVS

Motors 13%

Bajaj Auto 12%

Yamaha 4%

Suzuki Motorcycle

2%

Eicher Motors

2%

Mahindra 1%

Maruti Suzuki 45%

Hyundai Motor 16%

M&M 9%

Tata Motors 6%

Honda Cars 7%

Toyota Kirlosakar

5%

Ford India 3%

Others 9%

11

Indian Commercial Vehicle Industry

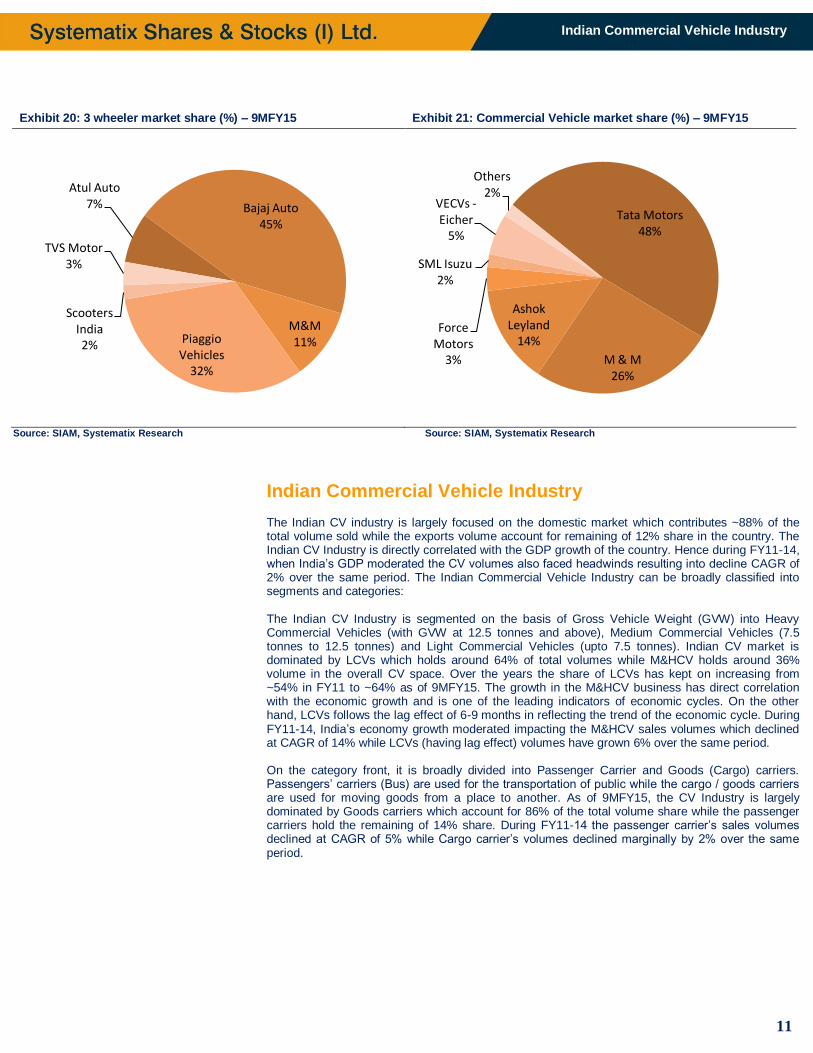

Exhibit 20: 3 wheeler market share (%) – 9MFY15 Exhibit 21: Commercial Vehicle market share (%) – 9MFY15

Source: SIAM, Systematix Research Source: SIAM, Systematix Research

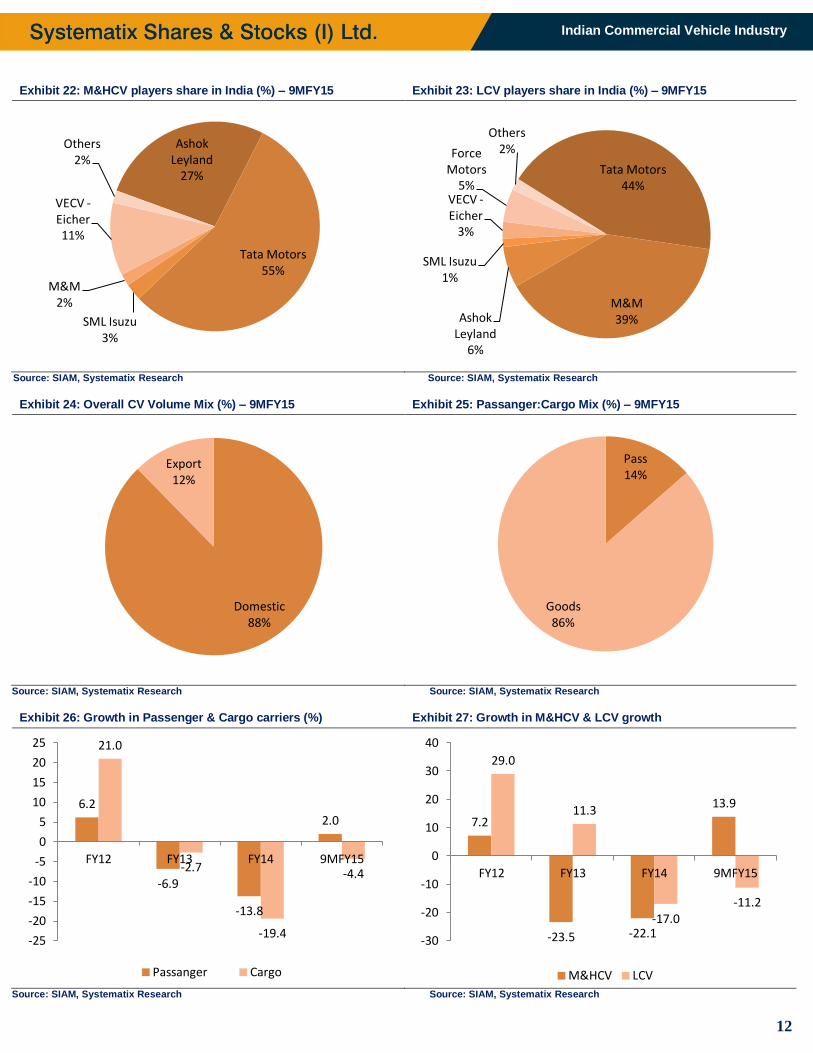

Indian Commercial Vehicle Industry The Indian CV industry is largely focused on the domestic market which contributes ~88% of the total volume sold while the exports volume account for remaining of 12% share in the country. The Indian CV Industry is directly correlated with the GDP growth of the country. Hence during FY11-14, when India’s GDP moderated the CV volumes also faced headwinds resulting into decline CAGR of 2% over the same period. The Indian Commercial Vehicle Industry can be broadly classified into segments and categories: The Indian CV Industry is segmented on the basis of Gross Vehicle Weight (GVW) into Heavy Commercial Vehicles (with GVW at 12.5 tonnes and above), Medium Commercial Vehicles (7.5 tonnes to 12.5 tonnes) and Light Commercial Vehicles (upto 7.5 tonnes). Indian CV market is dominated by LCVs which holds around 64% of total volumes while M&HCV holds around 36% volume in the overall CV space. Over the years the share of LCVs has kept on increasing from ~54% in FY11 to ~64% as of 9MFY15. The growth in the M&HCV business has direct correlation with the economic growth and is one of the leading indicators of economic cycles. On the other hand, LCVs follows the lag effect of 6-9 months in reflecting the trend of the economic cycle. During FY11-14, India’s economy growth moderated impacting the M&HCV sales volumes which declined at CAGR of 14% while LCVs (having lag effect) volumes have grown 6% over the same period. On the category front, it is broadly divided into Passenger Carrier and Goods (Cargo) carriers. Passengers’ carriers (Bus) are used for the transportation of public while the cargo / goods carriers are used for moving goods from a place to another. As of 9MFY15, the CV Industry is largely dominated by Goods carriers which account for 86% of the total volume share while the passenger carriers hold the remaining of 14% share. During FY11-14 the passenger carrier’s sales volumes declined at CAGR of 5% while Cargo carrier’s volumes declined marginally by 2% over the same period.

Atul Auto 7% Bajaj Auto

45%

M&M 11% Piaggio

Vehicles 32%

Scooters India 2%

TVS Motor 3%

Tata Motors 48%

M & M 26%

Ashok Leyland

14% Force

Motors 3%

SML Isuzu 2%

VECVs - Eicher

5%

Others 2%

12

Indian Commercial Vehicle Industry

Exhibit 22: M&HCV players share in India (%) – 9MFY15 Exhibit 23: LCV players share in India (%) – 9MFY15

Source: SIAM, Systematix Research Source: SIAM, Systematix Research

Exhibit 24: Overall CV Volume Mix (%) – 9MFY15 Exhibit 25: Passanger:Cargo Mix (%) – 9MFY15

Source: SIAM, Systematix Research Source: SIAM, Systematix Research

Exhibit 26: Growth in Passenger & Cargo carriers (%) Exhibit 27: Growth in M&HCV & LCV growth

Source: SIAM, Systematix Research Source: SIAM, Systematix Research

Ashok Leyland

27%

Tata Motors 55%

SML Isuzu 3%

M&M 2%

VECV - Eicher 11%

Others 2%

Tata Motors 44%

M&M 39% Ashok

Leyland 6%

SML Isuzu 1%

VECV - Eicher

3%

Force Motors

5%

Others 2%

Domestic 88%

Export 12%

Pass 14%

Goods 86%

6.2

-6.9

-13.8

2.0

21.0

-2.7

-19.4

-4.4

-25

-20

-15

-10

-5

0

5

10

15

20

25

FY12 FY13 FY14 9MFY15

Passanger Cargo

7.2

-23.5 -22.1

13.9

29.0

11.3

-17.0 -11.2

-30

-20

-10

0

10

20

30

40

FY12 FY13 FY14 9MFY15

M&HCV LCV

13

Indian Commercial Vehicle Industry

Risk to our call

Delay in demand recovery After two years of down cycle in CV Industry, the volumes are now showing some signs of demand recovery which is positive for the Industry. With government taking reformist action in addition with other favorable factors like lower crude prices and the softening of interest rate going forward we believe India’s GDP growth is likely to pick up over the next couple of years. Indian CV industry has direct correlation with GDP growth of the country and delay in economic recovery is likely to be negative for the CV industry.

Infrastructure and mining activity remain subdued: Slower and subdued infrastructure activity is likely to result in lower Industrial Production. Commercial Vehicle industry is heavily depended on construction and roads sector in addition with the mining activity in the country. Any delay in executing infrastructure projects would impact CV industry.

Rupee depreciation or increase in crude prices: Any sharp rise in crude prices or depreciation of rupee would further increase the fuel cost for the fleet operators. Fuel accounts for 40%-50% operating cost for the fleet owners. Lower operating margins would impact fleet operator’s profitability.

Interest rates fall if extended: Almost 90% of the CV purchased is through some kind of financing hence credit availability and cost of borrowing plays a significant role in influencing the demand for CVs. If the Inflation level again moves higher then we believe it would restrict RBI to cut rate further keeping the cost of borrowing at the higher levels.

14

Indian Commercial Vehicle Industry

Ashok Leyland Ltd Initiating Coverage Auto & Auto Ancillary Rating: BUY

Date February 19, 2015 CMP (Rs.) 69 Target (Rs.) 85 Potential Upside (%) 23.1 BSE Sensex 29320 NSE Nifty 8869

Scrip Code Bloomberg Al in equity Reuters Ashok.bo BSE Group A BSE Code 500477 NSE Symbol ashokley Market Data Market Cap.(Rs. Cr) 19694 Equity Sh.Cap.(Rs Cr) 266 52 Wk High/Low 70/15 Avg. Qtrly Volume 2335741 Face Value (Rs.) 1 Shareholding Pattern (As on 31

th Dec 2014)

FII 19.6 DII 13.2 Promoters 38.8 Public & Others 28.4 Total 100 Comparative Price Chart

Vidrum Mehta Research Analyst [email protected] Arun Gopalan VP – Research & Investments [email protected]

“ALL is well” in the CV cycle revival….

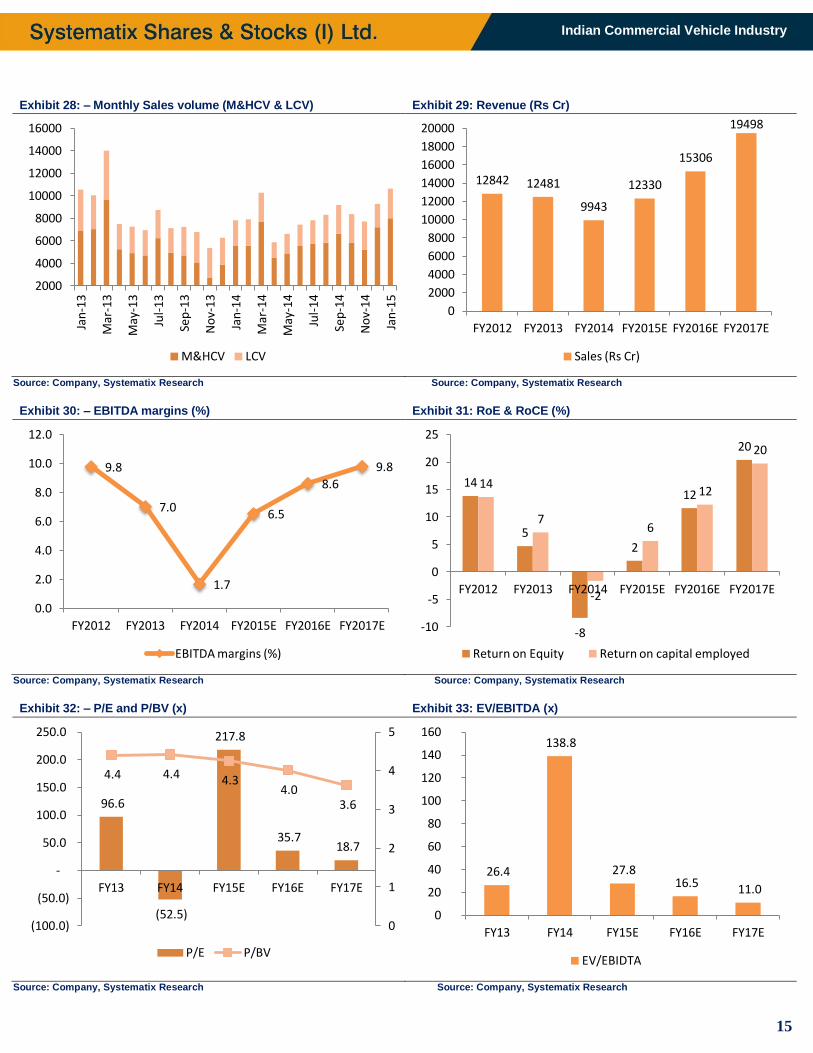

We believe Ashok Leyland Ltd (ALL) is well placed to gain benefit from the demand revival in the commercial vehicle industry. As of 9MFY15, ALL enjoys ~14% share in the overall CV industry, with M&HCV and LCV market share at 27% and 6% respectively. ALL is taking various restructuring steps like voluntary retirement of employees and selling non-core assets in order to reduce its debt levels. We expect ALL’s debt to equity to be at 0.4x by FY17E as against 0.9x in FY14. Also higher utilization level and lower discounts going forwards is likely to improve EBITDA margins by 250-350 bps over the next 2 years. This would further result into free cash flow generations and higher return on equity. At current price the stock is trading at P/E and EV/EBITDA of 18.7x and 11x its FY17E respectively. We believe ALL is pure CV revival play and is likely to benefit from the demand revival in addition with its operational efficiency and hence we recommend Buy with target of Rs85. M&HCV segment to drive growth: Ashok Leyland is the 2

nd largest CV manufacturer in India and 4

th largest manufacturer of buses in

the world. At present, category volume mix stands at 70:30 for passenger and cargo carriers. While the truck and bus market share of ALL stands at 37.5% and 25.2% respectively. We believe ALL is well placed to gain benefit from the demand revival in the CV space mainly after M&HCV (one of the leading indicators) volume contribute ~73% of its total volume. As of 9MFY15, ALL’s M&HCV sales volume grew by 24% YoY as against the industry growth of 10% during the same period helping the company to gain market share of 300 bps YoY to 26%. On the other hand, LCV volumes contribute around 27% of its total volume, declined by 11% YoY. ALL’s LCV volumes have shown some signs of improvement and we expect company to post higher volume growth from FY16 onwards. Management expects the overall CV industry to grow by 10% and 15% for FY15 and FY16 respectively and ALL to outperform the industry growth going forward. EBITDA margins to be ~10% levels by FY17: We expect ALL’s EBITDA margins to improve by 250-350 bps to ~10% by FY17 driven by both internal and external factors. Operational efficiencies like voluntary retirement of employees and other cost saving measures is likely to improve margins on the internal front while external factors include higher demand, better revenue mix (higher contribution from M&HCV) and lower discounts levels is likely to expand margin going forward. According to management, the current discount per vehicle is at its highest level of Rs 175,000. The discount level 5 years ago when the CV industry had good demand stood ~Rs20,000 per vehicle thus huge scope of lowering the discounts going forward. As of FY14, company’s utilization level stood at 60%. With economic recovery the demand for CV is likely to improve which is likely to result into higher utilization for the company. We expect ALL’s utilization to gradually improve from 68% in FY15 to 94% by FY17. We believe higher margins would boost ALL’s profitability going forward. Free cash flow to reduce debt: Improvement in demand is likely to result into higher utilization and better margins generating cash flows for the company. Since the company is operating at lower utilization level management has guided that it is not planning any major capex in the near to medium term. We believe company’s free cash flow would be used to repay its debt and expect debt to equity to improve from 0.9x in FY14 to 0.4x by FY17. This would further improve return ratio, with return on equity and return on capital employed to 20% each by FY17. We believe company would also resume its 50% payout resulting into dividend yield of 3% by FY17. Valuation: At current price the stock is trading at P/E and EV/EBITDA of 18.7x and 11x its FY17E respectively. We believe ALL is pure CV revival play and is likely to benefit from the demand revival in addition with its operational efficiency. Hence we recommend Buy with target of Rs85.

Year (Rs Cr) Revenue Growth YoY (%)

EBITDA EBITDA margin

(%) PAT

Growth YoY (%)

EPS (Rs)

PE (x) EV/

EBITDA (x)

RoE (%)

FY13 12,481 -2.8 877 7.0 203 -64.0 0.7 96.6 26.4 4.7

FY14 9,943 -20.3 167 1.7 (374) -284.0 -1.3 -52.5 138.8 -8.4

FY15E 12,330 24.0 807 6.5 90 -124.1 0.3 217.8 27.8 2.0

FY16E 15,306 24.1 1,320 8.6 551 510.7 1.9 35.7 16.5 11.6

FY17E 19,498 27.4 1,913 9.8 1,051 90.9 3.7 18.7 11.0 20.4

0

100

200

300

400

500

Feb

-14

Ap

r-14

Jun

-14

Au

g-14

Oct

-14

Dec

-14

Feb

-15

Ashok Leyland Sensex

15

Indian Commercial Vehicle Industry

Exhibit 28: – Monthly Sales volume (M&HCV & LCV) Exhibit 29: Revenue (Rs Cr)

Source: Company, Systematix Research Source: Company, Systematix Research

Exhibit 30: – EBITDA margins (%) Exhibit 31: RoE & RoCE (%)

Source: Company, Systematix Research Source: Company, Systematix Research

Exhibit 32: – P/E and P/BV (x) Exhibit 33: EV/EBITDA (x)

Source: Company, Systematix Research Source: Company, Systematix Research

2000

4000

6000

8000

10000

12000

14000

16000

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-13

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-14

Jan

-15

M&HCV LCV

12842 12481

9943

12330

15306

19498

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

Sales (Rs Cr)

9.8

7.0

1.7

6.5

8.6

9.8

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

EBITDA margins (%)

14

5

-8

2

12

20

14

7

-2

6

12

20

-10

-5

0

5

10

15

20

25

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

Return on Equity Return on capital employed

96.6

(52.5)

217.8

35.7 18.7

4.4 4.4 4.3 4.0

3.6

0

1

2

3

4

5

(100.0)

(50.0)

-

50.0

100.0

150.0

200.0

250.0

FY13 FY14 FY15E FY16E FY17E

P/E P/BV

26.4

138.8

27.8 16.5 11.0

0

20

40

60

80

100

120

140

160

FY13 FY14 FY15E FY16E FY17E

EV/EBIDTA

16

Indian Commercial Vehicle Industry

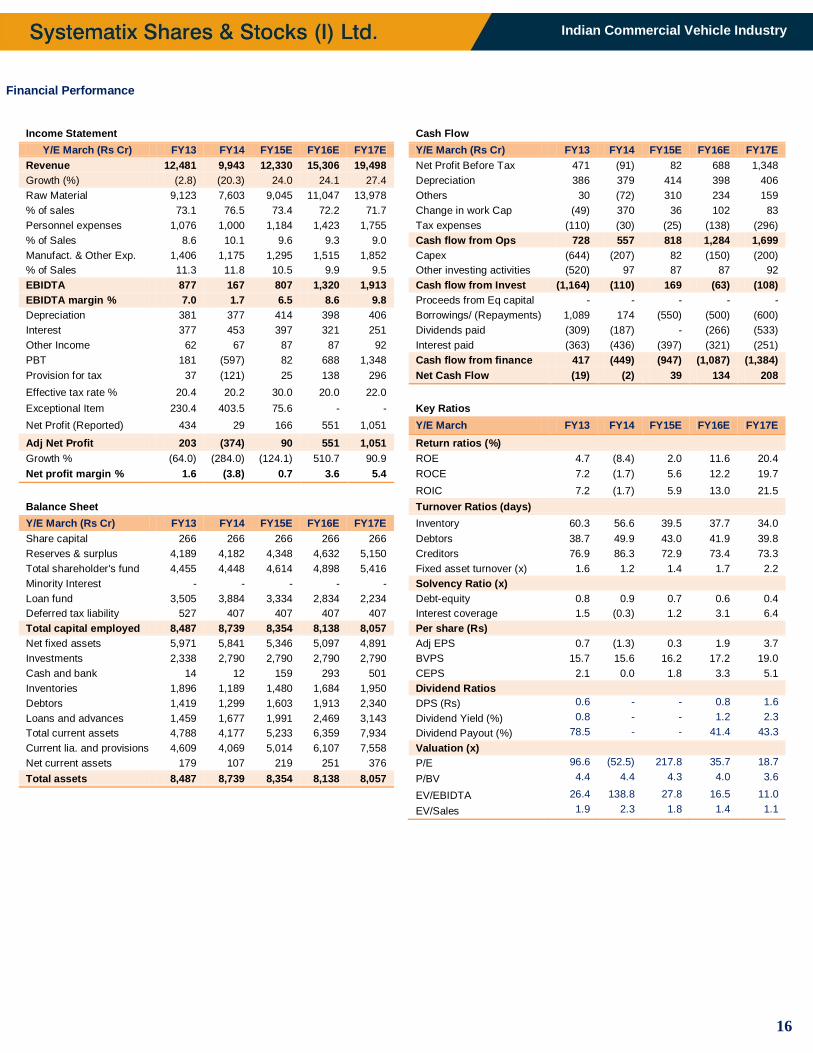

Financial Performance

Income Statement

Cash Flow

Y/E March (Rs Cr) FY13 FY14 FY15E FY16E FY17E

Y/E March (Rs Cr) FY13 FY14 FY15E FY16E FY17E

Revenue 12,481 9,943 12,330 15,306 19,498

Net Profit Before Tax 471 (91) 82 688 1,348

Growth (%) (2.8) (20.3) 24.0 24.1 27.4

Depreciation 386 379 414 398 406

Raw Material 9,123 7,603 9,045 11,047 13,978

Others 30 (72) 310 234 159

% of sales 73.1 76.5 73.4 72.2 71.7

Change in work Cap (49) 370 36 102 83

Personnel expenses 1,076 1,000 1,184 1,423 1,755

Tax expenses (110) (30) (25) (138) (296)

% of Sales 8.6 10.1 9.6 9.3 9.0

Cash flow from Ops 728 557 818 1,284 1,699

Manufact. & Other Exp. 1,406 1,175 1,295 1,515 1,852

Capex (644) (207) 82 (150) (200)

% of Sales 11.3 11.8 10.5 9.9 9.5

Other investing activities (520) 97 87 87 92

EBIDTA 877 167 807 1,320 1,913

Cash flow from Invest (1,164) (110) 169 (63) (108)

EBIDTA margin % 7.0 1.7 6.5 8.6 9.8

Proceeds from Eq capital - - - - -

Depreciation 381 377 414 398 406

Borrowings/ (Repayments) 1,089 174 (550) (500) (600)

Interest 377 453 397 321 251

Dividends paid (309) (187) - (266) (533)

Other Income 62 67 87 87 92

Interest paid (363) (436) (397) (321) (251)

PBT 181 (597) 82 688 1,348

Cash flow from finance 417 (449) (947) (1,087) (1,384)

Provision for tax 37 (121) 25 138 296

Net Cash Flow (19) (2) 39 134 208

Effective tax rate % 20.4 20.2 30.0 20.0 22.0

Exceptional Item 230.4 403.5 75.6 - -

Key Ratios

Net Profit (Reported) 434 29 166 551 1,051

Y/E March FY13 FY14 FY15E FY16E FY17E

Adj Net Profit 203 (374) 90 551 1,051

Return ratios (%)

Growth % (64.0) (284.0) (124.1) 510.7 90.9

ROE 4.7 (8.4) 2.0 11.6 20.4

Net profit margin % 1.6 (3.8) 0.7 3.6 5.4

ROCE 7.2 (1.7) 5.6 12.2 19.7

ROIC 7.2 (1.7) 5.9 13.0 21.5

Balance Sheet

Turnover Ratios (days)

Y/E March (Rs Cr) FY13 FY14 FY15E FY16E FY17E

Inventory 60.3 56.6 39.5 37.7 34.0

Share capital 266 266 266 266 266

Debtors 38.7 49.9 43.0 41.9 39.8

Reserves & surplus 4,189 4,182 4,348 4,632 5,150

Creditors 76.9 86.3 72.9 73.4 73.3

Total shareholder's fund 4,455 4,448 4,614 4,898 5,416

Fixed asset turnover (x) 1.6 1.2 1.4 1.7 2.2

Minority Interest - - - - -

Solvency Ratio (x)

Loan fund 3,505 3,884 3,334 2,834 2,234

Debt-equity 0.8 0.9 0.7 0.6 0.4

Deferred tax liability 527 407 407 407 407

Interest coverage 1.5 (0.3) 1.2 3.1 6.4

Total capital employed 8,487 8,739 8,354 8,138 8,057

Per share (Rs)

Net fixed assets 5,971 5,841 5,346 5,097 4,891

Adj EPS 0.7 (1.3) 0.3 1.9 3.7

Investments 2,338 2,790 2,790 2,790 2,790

BVPS 15.7 15.6 16.2 17.2 19.0

Cash and bank 14 12 159 293 501

CEPS 2.1 0.0 1.8 3.3 5.1

Inventories 1,896 1,189 1,480 1,684 1,950

Dividend Ratios

Debtors 1,419 1,299 1,603 1,913 2,340

DPS (Rs) 0.6 - - 0.8 1.6

Loans and advances 1,459 1,677 1,991 2,469 3,143

Dividend Yield (%) 0.8 - - 1.2 2.3

Total current assets 4,788 4,177 5,233 6,359 7,934

Dividend Payout (%) 78.5 - - 41.4 43.3

Current lia. and provisions 4,609 4,069 5,014 6,107 7,558

Valuation (x)

Net current assets 179 107 219 251 376

P/E 96.6 (52.5) 217.8 35.7 18.7

Total assets 8,487 8,739 8,354 8,138 8,057

P/BV 4.4 4.4 4.3 4.0 3.6

EV/EBIDTA 26.4 138.8 27.8 16.5 11.0

EV/Sales 1.9 2.3 1.8 1.4 1.1

17

Indian Commercial Vehicle Industry

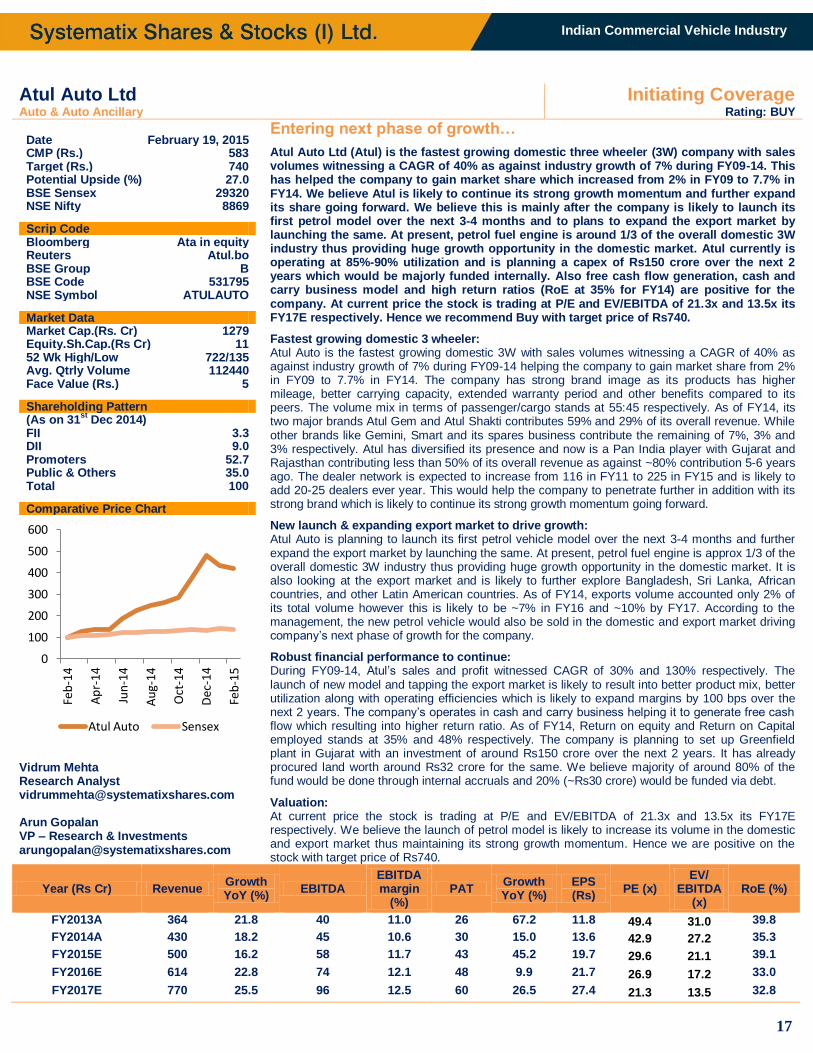

Atul Auto Ltd Initiating Coverage Auto & Auto Ancillary Rating: BUY

Date February 19, 2015 CMP (Rs.) 583 Target (Rs.) 740 Potential Upside (%) 27.0 BSE Sensex 29320 NSE Nifty 8869

Scrip Code Bloomberg Ata in equity Reuters Atul.bo BSE Group B BSE Code 531795 NSE Symbol ATULAUTO Market Data Market Cap.(Rs. Cr) 1279 Equity.Sh.Cap.(Rs Cr) 11 52 Wk High/Low 722/135 Avg. Qtrly Volume 112440 Face Value (Rs.) 5 Shareholding Pattern (As on 31

st Dec 2014)

FII 3.3 DII 9.0 Promoters 52.7 Public & Others 35.0 Total 100 Comparative Price Chart

Vidrum Mehta Research Analyst [email protected] Arun Gopalan VP – Research & Investments [email protected]

Entering next phase of growth…

Atul Auto Ltd (Atul) is the fastest growing domestic three wheeler (3W) company with sales volumes witnessing a CAGR of 40% as against industry growth of 7% during FY09-14. This has helped the company to gain market share which increased from 2% in FY09 to 7.7% in FY14. We believe Atul is likely to continue its strong growth momentum and further expand its share going forward. We believe this is mainly after the company is likely to launch its first petrol model over the next 3-4 months and to plans to expand the export market by launching the same. At present, petrol fuel engine is around 1/3 of the overall domestic 3W industry thus providing huge growth opportunity in the domestic market. Atul currently is operating at 85%-90% utilization and is planning a capex of Rs150 crore over the next 2 years which would be majorly funded internally. Also free cash flow generation, cash and carry business model and high return ratios (RoE at 35% for FY14) are positive for the company. At current price the stock is trading at P/E and EV/EBITDA of 21.3x and 13.5x its FY17E respectively. Hence we recommend Buy with target price of Rs740.

Fastest growing domestic 3 wheeler: Atul Auto is the fastest growing domestic 3W with sales volumes witnessing a CAGR of 40% as against industry growth of 7% during FY09-14 helping the company to gain market share from 2% in FY09 to 7.7% in FY14. The company has strong brand image as its products has higher mileage, better carrying capacity, extended warranty period and other benefits compared to its peers. The volume mix in terms of passenger/cargo stands at 55:45 respectively. As of FY14, its two major brands Atul Gem and Atul Shakti contributes 59% and 29% of its overall revenue. While other brands like Gemini, Smart and its spares business contribute the remaining of 7%, 3% and 3% respectively. Atul has diversified its presence and now is a Pan India player with Gujarat and Rajasthan contributing less than 50% of its overall revenue as against ~80% contribution 5-6 years ago. The dealer network is expected to increase from 116 in FY11 to 225 in FY15 and is likely to add 20-25 dealers ever year. This would help the company to penetrate further in addition with its strong brand which is likely to continue its strong growth momentum going forward.

New launch & expanding export market to drive growth: Atul Auto is planning to launch its first petrol vehicle model over the next 3-4 months and further expand the export market by launching the same. At present, petrol fuel engine is approx 1/3 of the overall domestic 3W industry thus providing huge growth opportunity in the domestic market. It is also looking at the export market and is likely to further explore Bangladesh, Sri Lanka, African countries, and other Latin American countries. As of FY14, exports volume accounted only 2% of its total volume however this is likely to be ~7% in FY16 and ~10% by FY17. According to the management, the new petrol vehicle would also be sold in the domestic and export market driving company’s next phase of growth for the company.

Robust financial performance to continue: During FY09-14, Atul’s sales and profit witnessed CAGR of 30% and 130% respectively. The launch of new model and tapping the export market is likely to result into better product mix, better utilization along with operating efficiencies which is likely to expand margins by 100 bps over the next 2 years. The company’s operates in cash and carry business helping it to generate free cash flow which resulting into higher return ratio. As of FY14, Return on equity and Return on Capital employed stands at 35% and 48% respectively. The company is planning to set up Greenfield plant in Gujarat with an investment of around Rs150 crore over the next 2 years. It has already procured land worth around Rs32 crore for the same. We believe majority of around 80% of the fund would be done through internal accruals and 20% (~Rs30 crore) would be funded via debt.

Valuation: At current price the stock is trading at P/E and EV/EBITDA of 21.3x and 13.5x its FY17E respectively. We believe the launch of petrol model is likely to increase its volume in the domestic and export market thus maintaining its strong growth momentum. Hence we are positive on the stock with target price of Rs740.

Year (Rs Cr) Revenue Growth YoY (%)

EBITDA EBITDA margin

(%) PAT

Growth YoY (%)

EPS (Rs)

PE (x) EV/

EBITDA (x)

RoE (%)

FY2013A 364 21.8 40 11.0 26 67.2 11.8 49.4 31.0 39.8

FY2014A 430 18.2 45 10.6 30 15.0 13.6 42.9 27.2 35.3

FY2015E 500 16.2 58 11.7 43 45.2 19.7 29.6 21.1 39.1

FY2016E 614 22.8 74 12.1 48 9.9 21.7 26.9 17.2 33.0

FY2017E 770 25.5 96 12.5 60 26.5 27.4 21.3 13.5 32.8

0

100

200

300

400

500

600

Feb

-14

Ap

r-14

Jun

-14

Au

g-14

Oct

-14

Dec

-14

Feb

-15

Atul Auto Sensex

18

Indian Commercial Vehicle Industry

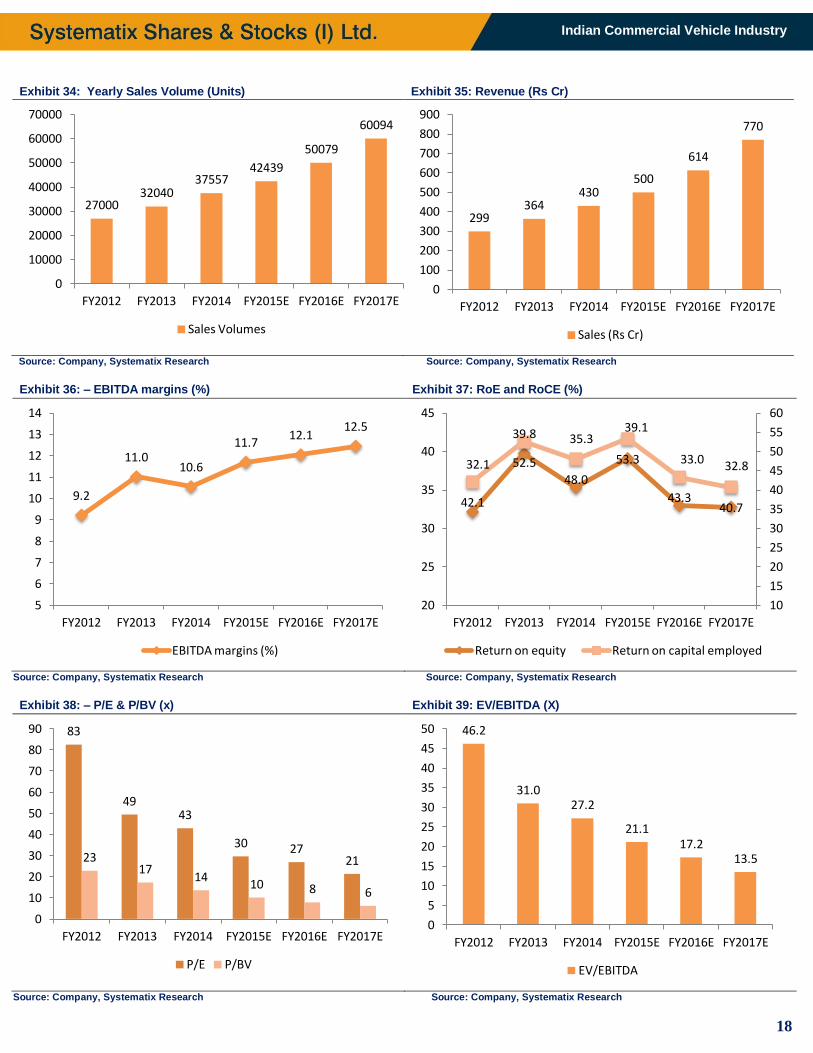

Exhibit 34: Yearly Sales Volume (Units) Exhibit 35: Revenue (Rs Cr)

Source: Company, Systematix Research Source: Company, Systematix Research

Exhibit 36: – EBITDA margins (%) Exhibit 37: RoE and RoCE (%)

Source: Company, Systematix Research Source: Company, Systematix Research

Exhibit 38: – P/E & P/BV (x) Exhibit 39: EV/EBITDA (X)

Source: Company, Systematix Research Source: Company, Systematix Research

27000 32040

37557 42439

50079

60094

0

10000

20000

30000

40000

50000

60000

70000

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

Sales Volumes

299 364

430 500

614

770

0

100

200

300

400

500

600

700

800

900

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

Sales (Rs Cr)

9.2

11.0 10.6

11.7 12.1

12.5

5

6

7

8

9

10

11

12

13

14

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

EBITDA margins (%)

32.1

39.8 35.3 39.1

33.0 32.8

42.1

52.5

48.0

53.3

43.3 40.7

10

15

20

25

30

35

40

45

50

55

60

20

25

30

35

40

45

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

Return on equity Return on capital employed

83

49 43

30 27 21 23

17 14

10 8 6

0

10

20

30

40

50

60

70

80

90

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

P/E P/BV

46.2

31.0 27.2

21.1 17.2

13.5

0

5

10

15

20

25

30

35

40

45

50

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

EV/EBITDA

19

Indian Commercial Vehicle Industry

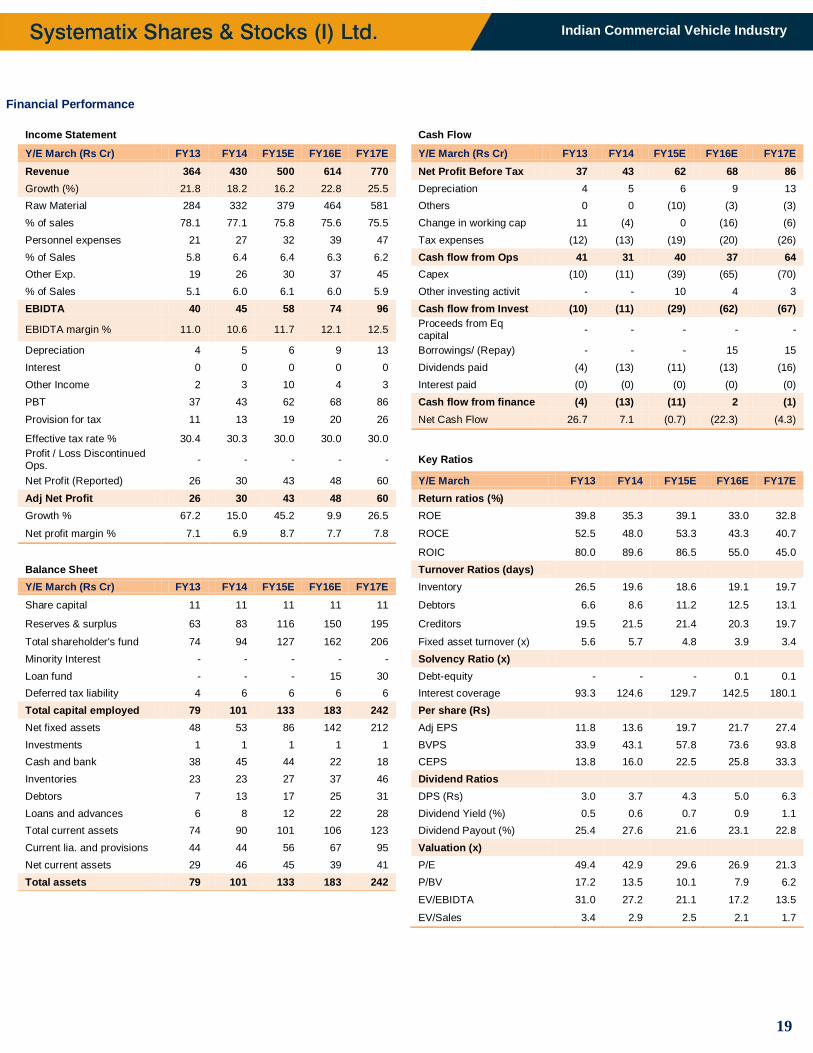

Financial Performance

Income Statement

Cash Flow

Y/E March (Rs Cr) FY13 FY14 FY15E FY16E FY17E

Y/E March (Rs Cr) FY13 FY14 FY15E FY16E FY17E

Revenue 364 430 500 614 770

Net Profit Before Tax 37 43 62 68 86

Growth (%) 21.8 18.2 16.2 22.8 25.5

Depreciation 4 5 6 9 13

Raw Material 284 332 379 464 581

Others 0 0 (10) (3) (3)

% of sales 78.1 77.1 75.8 75.6 75.5

Change in working cap 11 (4) 0 (16) (6)

Personnel expenses 21 27 32 39 47

Tax expenses (12) (13) (19) (20) (26)

% of Sales 5.8 6.4 6.4 6.3 6.2

Cash flow from Ops 41 31 40 37 64

Other Exp. 19 26 30 37 45

Capex (10) (11) (39) (65) (70)

% of Sales 5.1 6.0 6.1 6.0 5.9

Other investing activit - - 10 4 3

EBIDTA 40 45 58 74 96

Cash flow from Invest (10) (11) (29) (62) (67)

EBIDTA margin % 11.0 10.6 11.7 12.1 12.5

Proceeds from Eq capital

- - - - -

Depreciation 4 5 6 9 13

Borrowings/ (Repay) - - - 15 15

Interest 0 0 0 0 0

Dividends paid (4) (13) (11) (13) (16)

Other Income 2 3 10 4 3

Interest paid (0) (0) (0) (0) (0)

PBT 37 43 62 68 86

Cash flow from finance (4) (13) (11) 2 (1)

Provision for tax 11 13 19 20 26

Net Cash Flow 26.7 7.1 (0.7) (22.3) (4.3)

Effective tax rate % 30.4 30.3 30.0 30.0 30.0

Profit / Loss Discontinued Ops.

- - - - -

Key Ratios

Net Profit (Reported) 26 30 43 48 60

Y/E March FY13 FY14 FY15E FY16E FY17E

Adj Net Profit 26 30 43 48 60

Return ratios (%)

Growth % 67.2 15.0 45.2 9.9 26.5

ROE 39.8 35.3 39.1 33.0 32.8

Net profit margin % 7.1 6.9 8.7 7.7 7.8

ROCE 52.5 48.0 53.3 43.3 40.7

ROIC 80.0 89.6 86.5 55.0 45.0

Balance Sheet

Turnover Ratios (days)

Y/E March (Rs Cr) FY13 FY14 FY15E FY16E FY17E

Inventory 26.5 19.6 18.6 19.1 19.7

Share capital 11 11 11 11 11

Debtors 6.6 8.6 11.2 12.5 13.1

Reserves & surplus 63 83 116 150 195

Creditors 19.5 21.5 21.4 20.3 19.7

Total shareholder's fund 74 94 127 162 206

Fixed asset turnover (x) 5.6 5.7 4.8 3.9 3.4

Minority Interest - - - - -

Solvency Ratio (x)

Loan fund - - - 15 30

Debt-equity - - - 0.1 0.1

Deferred tax liability 4 6 6 6 6

Interest coverage 93.3 124.6 129.7 142.5 180.1

Total capital employed 79 101 133 183 242

Per share (Rs)

Net fixed assets 48 53 86 142 212

Adj EPS 11.8 13.6 19.7 21.7 27.4

Investments 1 1 1 1 1

BVPS 33.9 43.1 57.8 73.6 93.8

Cash and bank 38 45 44 22 18

CEPS 13.8 16.0 22.5 25.8 33.3

Inventories 23 23 27 37 46

Dividend Ratios

Debtors 7 13 17 25 31

DPS (Rs) 3.0 3.7 4.3 5.0 6.3

Loans and advances 6 8 12 22 28

Dividend Yield (%) 0.5 0.6 0.7 0.9 1.1

Total current assets 74 90 101 106 123

Dividend Payout (%) 25.4 27.6 21.6 23.1 22.8

Current lia. and provisions 44 44 56 67 95

Valuation (x)

Net current assets 29 46 45 39 41

P/E 49.4 42.9 29.6 26.9 21.3

Total assets 79 101 133 183 242

P/BV 17.2 13.5 10.1 7.9 6.2

EV/EBIDTA 31.0 27.2 21.1 17.2 13.5

EV/Sales 3.4 2.9 2.5 2.1 1.7

20

Indian Commercial Vehicle Industry

Eicher Motors Ltd Initiating Coverage Auto & Auto Ancillary Rating: BUY

Date February 19, 2015 CMP (Rs.) 16938 Target (Rs.) 20079 Potential Upside (%) 18.5 BSE Sensex 29320 NSE Nifty 8869

Scrip Code Bloomberg Eim in equity Reuters Eich.bo BSE Group A BSE Code 505200 NSE Symbol eichermot Market Data Market Cap.(Rs. Cr) 45911 Equity Sh.Cap. (Rs Cr) 27 52 Wk High/Low 16895/4525 Avg. Qtrly Volume 4509 Face Value (Rs.) 10 Shareholding Pattern (As on 31

st Dec 2014)

FII 19.4 DII 4.7 Promoters 55.0 Public & Others 20.9 Total 100 Comparative Price Chart

Vidrum Mehta Research Analyst [email protected] Arun Gopalan VP – Research & Investments [email protected]

A Sweet Spot – CV and premium 2-wheelers

Eicher Motors Ltd is a dual play on sustained strong growth from its motorcycle business and Volvo Eicher Commercial Vehicles (VECV) which is well placed to grab the CV recovery in India. Its motorcycle business owns the iconic brand “Royal Enfield” and its volumes have witnessed a CAGR of 42% over CY09-14. It has consistently increased its motorcycle capacity over the last 3-4 years and is likely to maintain its strong growth momentum going forward too. On the other hand, VECV is well placed to grab the demand revival in Indian CV space. As of December 2014, VECV market share stands at ~6% in the overall CV industry and ~12% share in the M&HCV segment. The launch of Pro-series along with the expected recovery in demand is likely to expand its overall share in the CV space. With VECV expected to post better performance, consolidated EBITDA margins is likely to expand from 10.5% in CY13 to 15% in CY16 further boosting profitability. At current price the stock is trading at P/E and EV/EBITDA of 27.8x and 17.9x its CY16E respectively. We believe higher earnings growth from VECV segment would eventually bring down the valuation multiple going forward and hence we recommend Buy with target of Rs20079. Motorcycle segment to continue its robust growth: Eicher Motors Ltd owns the iconic brand “Royal Enfield” which caters to premium and niche segment in India. Motorcycle sales volume has consistently witnessed robust growth with CAGR of 42% over CY09-14. Management has consistently increased its motorcycle capacity from 1.8 lacs units in CY13 to around 3.0 lacs units in CY14 and is expected to be in the range of 4.3 lacs to 4.5 lacs units in CY15. Despite huge capacity addition, the growth momentum continues to remain strong for RE, with the demand situation robust and the motorcycle still commanding nearly 5 months of waiting periods. We believe the company is likely to continue with its strong volume growth momentum on the back of new launches, delaer network addition of 70-80 dealers p.a. and inherent demand from the Tier 2/3 cities which are yet to be played out. The company is further penetrating the export market which would continue its strong growth momentum. VECV to revive performance: VECV is a 54:46 joint venture (JV) between Eicher Motors and Volvo group. As of December 2014, VECV has overall market share of ~6% in the CV industry with ~12% share in the M&HCV segment. The company in the past launched Eicher Pro-1000 and Pro-3000 range of trucks and buses which was well responded by the customers. We believe the launch of Pro series of vehicles along with the expected recovery in demand is likely to expand its overall share in the CV space going forward. Improvement is VECV performance is expected to expand consolidated margins further boosting profitability for the company. Strong financial performance to continue: During CY09-13, when overall Automobile industry witnessed slowdown, Eicher’s continued to show strong financial performance. Consolidated sales and profit witnessed a CAGR of 23% and 42% respectively during the same period. This is mainly after strong growth from its standalone (motorcycle business) which witnessed sales and profit CAGR of 46% and 53% respectively. For CY13, Motorcycle business contributed 25% and 49% of its consolidated revenue and profit of the company. Further the management has guided capex of Rs600 crore for CY15 at its Oragadam plant. The company is net cash with high return on equity of 40% for CY14 despite the regular capex incurred in the past. We believe company is likely to continue with its strong financial performance, cash flow generation and higher return ratios going forward. Valuation: The stock is currently trading at P/E and EV/EBITDA of 27.8x and 17.9x its CY16E respectively. Eicher is dual play with Motorcycle business to continue its robust growth momentum and VECV to witness a strong demand recovery. We believe higher earnings growth from VECV segment would bring down the valuation multiple and hence we recommend Buy with target of Rs20079.

Year (Dec Ending) (Rs Cr)

Revenue Growth YoY (%)

EBITDA EBITDA margin

(%) PAT

Growth YoY (%)

EPS (Rs)

PE (x) EV/

EBITDA (x)

RoE (%)

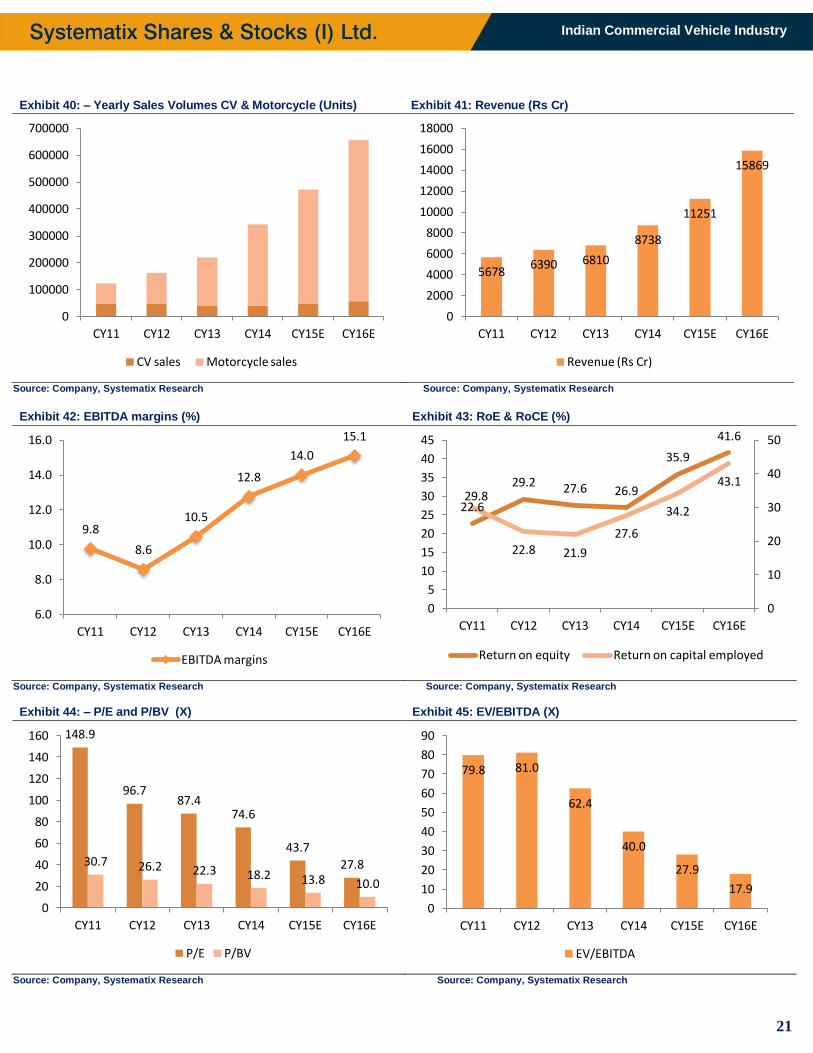

CY12 6,390 12.5 549 8.6 475 54.0 175.2 96.7 81.0 29.2

CY13 6,810 6.6 713 10.5 525 10.6 193.8 87.4 62.4 27.6

CY14 8,738 28.3 1,115 12.8 702 33.6 227.0 74.6 40.0 26.9

CY15E 11,251 28.8 1,575 14.0 1,050 49.7 387.5 43.7 27.9 35.9

CY16E 15,869 41.0 2,396 15.1 1,649 57.0 608.5 27.8 17.9 41.6

0

50

100

150

200

250

300

350

Feb

-14

Ap

r-14

Jun

-14

Au

g-14

Oct

-14

Dec

-14

Feb

-15

Eicher Motors Sensex

21

Indian Commercial Vehicle Industry

Exhibit 40: – Yearly Sales Volumes CV & Motorcycle (Units) Exhibit 41: Revenue (Rs Cr)

Source: Company, Systematix Research Source: Company, Systematix Research

Exhibit 42: EBITDA margins (%) Exhibit 43: RoE & RoCE (%)

Source: Company, Systematix Research Source: Company, Systematix Research

Exhibit 44: – P/E and P/BV (X) Exhibit 45: EV/EBITDA (X)

Source: Company, Systematix Research Source: Company, Systematix Research

0

100000

200000

300000

400000

500000

600000

700000

CY11 CY12 CY13 CY14 CY15E CY16E

CV sales Motorcycle sales

5678 6390 6810

8738

11251

15869

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

CY11 CY12 CY13 CY14 CY15E CY16E

Revenue (Rs Cr)

9.8

8.6

10.5

12.8

14.0

15.1

6.0

8.0

10.0

12.0

14.0

16.0

CY11 CY12 CY13 CY14 CY15E CY16E

EBITDA margins

22.6

29.2 27.6 26.9

35.9

41.6

29.8

22.8 21.9

27.6

34.2

43.1

0

10

20

30

40

50

0

5

10

15

20

25

30

35

40

45

CY11 CY12 CY13 CY14 CY15E CY16E

Return on equity Return on capital employed

148.9

96.7 87.4

74.6

43.7

27.8 30.7 26.2 22.3 18.2 13.8 10.0

0

20

40

60

80

100

120

140

160

CY11 CY12 CY13 CY14 CY15E CY16E

P/E P/BV

79.8 81.0

62.4

40.0

27.9

17.9

0

10

20

30

40

50

60

70

80

90

CY11 CY12 CY13 CY14 CY15E CY16E

EV/EBITDA

22

Indian Commercial Vehicle Industry

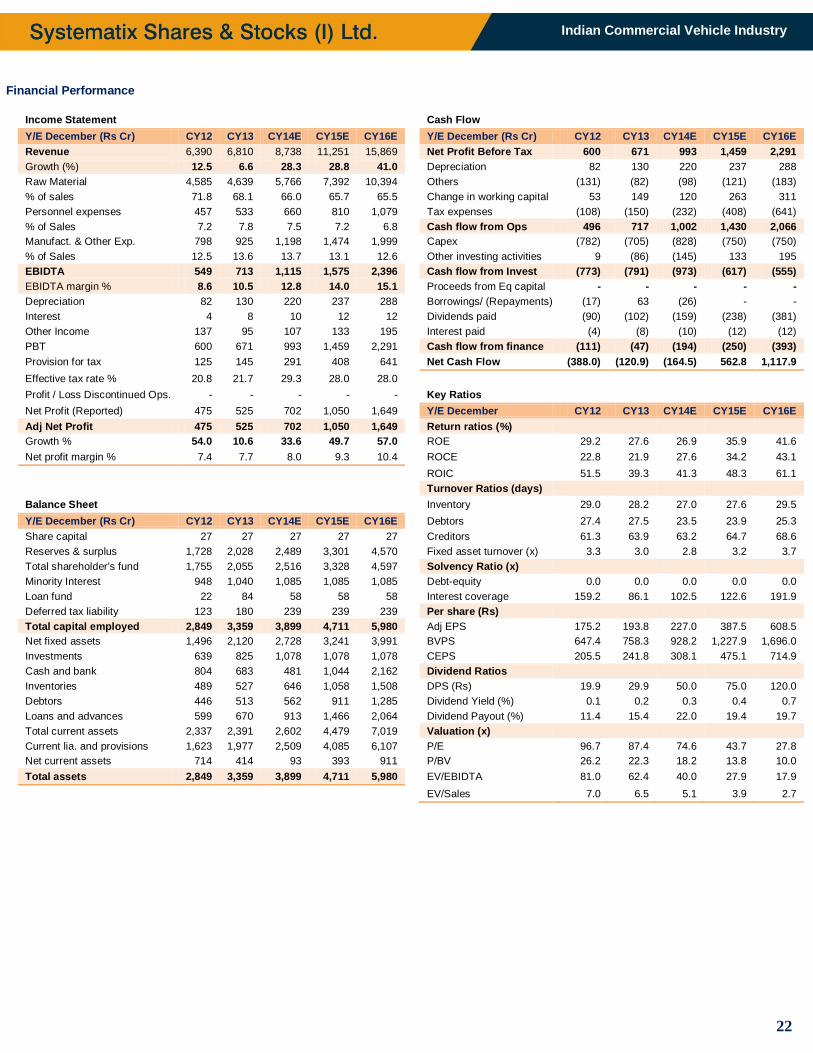

Financial Performance

Income Statement

Cash Flow

Y/E December (Rs Cr) CY12 CY13 CY14E CY15E CY16E

Y/E December (Rs Cr) CY12 CY13 CY14E CY15E CY16E

Revenue 6,390 6,810 8,738 11,251 15,869

Net Profit Before Tax 600 671 993 1,459 2,291

Growth (%) 12.5 6.6 28.3 28.8 41.0

Depreciation 82 130 220 237 288

Raw Material 4,585 4,639 5,766 7,392 10,394

Others (131) (82) (98) (121) (183)

% of sales 71.8 68.1 66.0 65.7 65.5

Change in working capital 53 149 120 263 311

Personnel expenses 457 533 660 810 1,079

Tax expenses (108) (150) (232) (408) (641)

% of Sales 7.2 7.8 7.5 7.2 6.8

Cash flow from Ops 496 717 1,002 1,430 2,066

Manufact. & Other Exp. 798 925 1,198 1,474 1,999

Capex (782) (705) (828) (750) (750)

% of Sales 12.5 13.6 13.7 13.1 12.6

Other investing activities 9 (86) (145) 133 195

EBIDTA 549 713 1,115 1,575 2,396

Cash flow from Invest (773) (791) (973) (617) (555)

EBIDTA margin % 8.6 10.5 12.8 14.0 15.1

Proceeds from Eq capital - - - - -

Depreciation 82 130 220 237 288

Borrowings/ (Repayments) (17) 63 (26) - -

Interest 4 8 10 12 12

Dividends paid (90) (102) (159) (238) (381)

Other Income 137 95 107 133 195

Interest paid (4) (8) (10) (12) (12)

PBT 600 671 993 1,459 2,291

Cash flow from finance (111) (47) (194) (250) (393)

Provision for tax 125 145 291 408 641

Net Cash Flow (388.0) (120.9) (164.5) 562.8 1,117.9

Effective tax rate % 20.8 21.7 29.3 28.0 28.0

Profit / Loss Discontinued Ops. - - - - -

Key Ratios

Net Profit (Reported) 475 525 702 1,050 1,649

Y/E December CY12 CY13 CY14E CY15E CY16E

Adj Net Profit 475 525 702 1,050 1,649

Return ratios (%)

Growth % 54.0 10.6 33.6 49.7 57.0

ROE 29.2 27.6 26.9 35.9 41.6

Net profit margin % 7.4 7.7 8.0 9.3 10.4

ROCE 22.8 21.9 27.6 34.2 43.1

ROIC 51.5 39.3 41.3 48.3 61.1

Turnover Ratios (days)

Balance Sheet

Inventory 29.0 28.2 27.0 27.6 29.5

Y/E December (Rs Cr) CY12 CY13 CY14E CY15E CY16E

Debtors 27.4 27.5 23.5 23.9 25.3

Share capital 27 27 27 27 27

Creditors 61.3 63.9 63.2 64.7 68.6

Reserves & surplus 1,728 2,028 2,489 3,301 4,570

Fixed asset turnover (x) 3.3 3.0 2.8 3.2 3.7

Total shareholder's fund 1,755 2,055 2,516 3,328 4,597

Solvency Ratio (x)

Minority Interest 948 1,040 1,085 1,085 1,085

Debt-equity 0.0 0.0 0.0 0.0 0.0

Loan fund 22 84 58 58 58

Interest coverage 159.2 86.1 102.5 122.6 191.9

Deferred tax liability 123 180 239 239 239

Per share (Rs)

Total capital employed 2,849 3,359 3,899 4,711 5,980

Adj EPS 175.2 193.8 227.0 387.5 608.5

Net fixed assets 1,496 2,120 2,728 3,241 3,991

BVPS 647.4 758.3 928.2 1,227.9 1,696.0

Investments 639 825 1,078 1,078 1,078

CEPS 205.5 241.8 308.1 475.1 714.9

Cash and bank 804 683 481 1,044 2,162

Dividend Ratios

Inventories 489 527 646 1,058 1,508

DPS (Rs) 19.9 29.9 50.0 75.0 120.0

Debtors 446 513 562 911 1,285

Dividend Yield (%) 0.1 0.2 0.3 0.4 0.7

Loans and advances 599 670 913 1,466 2,064

Dividend Payout (%) 11.4 15.4 22.0 19.4 19.7

Total current assets 2,337 2,391 2,602 4,479 7,019

Valuation (x)

Current lia. and provisions 1,623 1,977 2,509 4,085 6,107

P/E 96.7 87.4 74.6 43.7 27.8

Net current assets 714 414 93 393 911

P/BV 26.2 22.3 18.2 13.8 10.0

Total assets 2,849 3,359 3,899 4,711 5,980

EV/EBIDTA 81.0 62.4 40.0 27.9 17.9

EV/Sales 7.0 6.5 5.1 3.9 2.7

23

Indian Commercial Vehicle Industry

Force Motors Ltd Initiating Coverage Auto & Auto Ancillary Rating: ACCUMULATE

Date February 19, 2015 CMP (Rs.) 1413 Target (Rs.) 1538 Potential Upside (%) 8.8 BSE Sensex 29320 NSE Nifty 8869

Scrip Code Bloomberg Fml in equity Reuters Forc.bo BSE Group B BSE Code 500033 NSE Symbol Not listed Market Data Market Cap.(Rs. Cr) 1842 Equity Sh. Cap.(Rs Cr) 13 52 Wk High/Low 1463/282 Avg. Qtrly Volume 141617 Face Value (Rs.) 10 Shareholding Pattern (As on 31

st Dec 2014)

FII 5.4 DII 0.7 Promoters 59.4 Public & Others 34.5 Total 100 Comparative Price Chart

Vidrum Mehta Research Analyst [email protected] Arun Gopalan VP – Research & Investments [email protected]

A unique blend of CVs and auto components…

Force Motors Ltd (Force) is fully integrated automobile company with focus on design and development of vehicles (mainly into LCV, UV’s and tractors) and auto components in India. The company has strong brand recall with Traveller being one of the prominent name enjoying the market leadership position of 41% share in the LCV passenger segment in India. Force also has technical collaboration with Daimler AG, Germany in respect of multi-purpose passenger vehicles. Further as per media reports, Indian arm of German luxury auto maker BMW is likely to partner Force motors, in its strategy for localization of its resources at its Chennai plant. We believe the company is has diversified business segment and is well placed to benefit from the revival in the overall recovery in the automobile industry in India. Higher demand is likely to improve the utilization level and operating performance resulting into margin expansion going forward. At current price the stock is trading at trading at P/E and EV/EBITDA of 15.6x and 7.9x its FY17E respectively. Hence we are positive on the stock with a target price of Rs1538.

A niche player with a strong brand recall : Force is a diversified company with focus and design and developments of automotive vehicles in India. As of FY14, 72% of the total revenue is in terms of sales of automotive vehicles, 27% through sales of auto component and remaining of 1% is others. Within the Automotive segment, Commercial vehicles (LCV & SCV contributing around 50% of volume), passenger vehicle (UV & SUV accounts for 39% of volume) and the remaining of 12% are through sales of tractors. The company has strong brand recall in each of the segment with Traveller, Trax and Trump (into CV segment), Force Gurkha, Force One (PV) and Balwan and Orchard (tractors). The brand Traveller is one of the prominent names and enjoying market leadership position with 41% share in the LCV passenger segment in India. Domestic sales volume accounted for 91% of auto sales volume while the remaining of 9% is through exports. The company is penetrating in the export market through appointment of dealers in various countries like Nepal, Bangladesh, Sri Lanka and some of the African and Latin American countries which is likely to drive its sales growth going forward.

Component business likely to gain traction: Force motors components business currently accounts for 27% of the total revenue and has witnessed a CAGR of 28% over FY10-14. The Company has technical collaboration with Daimler AG, Germany in respect of multi-purpose passenger vehicles. Further as per media reports, Indian arm of German luxury auto maker BMW is likely to partner Force motors in its strategy for localization of its resources at its Chennai plant. The company is likely to produce engine and gearboxes and other auto ancillary for BMW. We believe company’s auto component segment is likely to continue its strong growth momentum and to some extent cushions the overall financial performance when there is slowdown in the automotive segment.

Financial performance to improve: After 2 years of decline in sales volume of 4% and 7% in FY13 and FY14, the company is well placed to gain from the revival in the demand. We expect company’s sales volume to witness a CAGR of 8% over FY14-17. Improved demand scenario is further likely to improve the overall utilization levels and operating efficiencies which are likely to improve EBITDA margins from 4.8% in FY14 to 6.4% in FY17. As of FY14, Force is net cash company with cash and cash equivalent of Rs225 crore. As of FY14, book value of the company stands at Rs931 and hence it is trading P/BV of 1.2x. Its return on equity is likely to gradually increase from 6% in FY14 to 9% in FY17.

Valuations: At current price the stock is trading at trading at P/E and EV/EBITDA of 15.6x and 7.9x its FY17E respectively. We believe company is well diversified player in the automobile business and is likely to benefit from the revival in the overall automobile industry going forward. Further any positive tie-ups with global auto OEMs would further fuel the growth. Hence we are positive on the stock with a target price of Rs1538

Year (Rs Cr) Revenue Growth YoY (%)

EBITDA EBITDA margin

(%) PAT

Growth YoY (%)

EPS (Rs)

PE (x) EV/

EBITDA (x)

RoE (%)

FY13A 1,973 -5.4 54 2.7 14 -65.4 10.9 130.3 31.1 1.2

FY14A 2,022 2.5 97 4.8 78 443.6 59.0 24.0 17.2 6.5

FY15E 2,122 5.0 102 4.8 54 -29.9 41.3 34.2 16.1 4.4

FY16E 2,475 16.6 139 5.6 77 41.4 58.5 24.2 11.7 5.9

FY17E 3,131 26.5 200 6.4 119 54.8 90.5 15.6 7.9 8.5

0

100

200

300

400

500

Feb

-14

Ap

r-14

Jun

-14

Au

g-14

Oct

-14

Dec

-14

Feb

-15