Embed Size (px)

Citation preview

PAGE 1 | GRACE HOPPER CELEBRATION INDIA (GHCI) 19 Presented by AnitaB.org and Association for Computing Machinery India (ACM) India #GHCI19

India StackImpact of Population Scale Digital Infrastructure

Dr. Vivek Raghavan, Volunteer ISpirt

Back in 2008…

Diversion and leakage was common

~$50 Bwas spent on direct subsidy

Source : A Demirgüç-Kunt, L Klapper, D Singer, S Ansar, and J Hess, “The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution”, World Bank, 2017 2

Back in 2008…

Financial exclusion was common

17%had bank accounts

Source : A Demirgüç-Kunt, L Klapper, D Singer, S Ansar, and J Hess, “The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution”, World Bank, 2017 3

No Credible Data

Servicing Cost

Sales CostCustomers with

the lowest default rates

have the highest interest rates

For the poor, getting a loan is impossible

4

0.5% commission & Rs.1500 KYC

cost makes investment to

Rs.3L minimum!

Same goes for access to banking and mutual funds

Lack of Papers

KYC Cost

Sales Cost

5

Affects access to skilling and differentiated wages

Lack of portability

Low trust

Expensive ₹Lack of

verifiability and portability of job

credentials makes it a low

performing ecosystem

6

In the last decade, India took a nonlinear path to addressing these

7

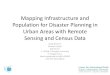

India now runs the world's largest direct cash transfer program

Savings to the tune of $5 Billion as per Govt estimates

>$32 Bnow directly being sent to bank account of the beneficiary

Source: https://www.thehindubusinessline.com/economy/dbt-in-9-months-of-fy19-exceeds-total-of-last-fiscal/article25883568.ece

430+ schemes

647 MillionUnique Aadhaar holders have linked their bank accounts

8

India would have taken 46 years to achieve financial inclusion

2011 fitted line

Source : A Demirgüç-Kunt, L Klapper, D Singer, S Ansar, and J Hess, “The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution”, World Bank, 2017 9

46 years

Source : BIS Analysis

India, 2011

But India only took 6 years!!!

2011 fitted line

Source : A Demirgüç-Kunt, L Klapper, D Singer, S Ansar, and J Hess, “The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution”, World Bank, 2017 10

46 years

Source : BIS Analysis

India, 2018

6 years

India, 2011

This acceleration was due to 3 things

11

World's largest financial inclusion and Digital India

program driven by PM

Innovation friendly regulators and Govt departments

supporting market making

A set of foundational public digital

infrastructure services

Political Will

Proactive Govt and

Regulators

India's Digital Infra

Open Digital Infrastructureas a means to build

decentralized, interoperable, building blocksto unleash inclusive innovation

12

Build Platforms not Pipes

The old way of innovating was to build end-to-end solutions

In the digital world, the method of innovation are through open protocols and platforms.

13

India's Public Digital InfrastructureA set of foundational digital infrastructure services

14

ENABLE

ENGAGE

EMPOWER

Identity Infrastructure

Transaction infrastructure

Data infrastructure

3 Biometric Data Points

1234 5678 9012Aadhaar number

4 Demographic Data Points

Aadhaar - A unique identity for every resident1 Billion digital IDs in 5.5 yrs

15

FoundationalMinimalUnique

Lifetime

Innovation through Open APIs

ELIMINATESPHYSICAL PRESENCE

Are you who you claim to be?

ONLY a yes/no answer

Anytime anywhere

ELIMINATES PAPER BASED KYC

ONLY done with authentication

No more fake documents

Anytime anywhere

Authentication API

Electronic KYC API

16

17

ENABLE

ENGAGE

EMPOWER

Aadhaar, Auth, & eKYC

1.3 BnAadhaar IDs issued

58 BnAadhaar authentications

9+ Bn e-KYC transactions

647 M Aadhaar enabled accounts

PMJDY: Bank account for allNo frill savings account

1 in 25 had ID in 2008$1 per ID, 1 Bn in <7 years

Paperless and instantUsed beyond banking

Inclusive, multi-channelAbout 1 Bn a month

2010

Identity Infrastructure

Aadhaar adoption paves way for the largest increase in financial accounts across 140 countries

20172011Income gap

14 5

Education gap 29 10

Closing the gaps on marginalized groups

35 % with account 80

Gender gap17

6

Employment gap 18 9

Source : A Demirgüç-Kunt, L Klapper, D Singer, S Ansar, and J Hess, “The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution”, World Bank, 2017 18

Application Service Provider (ASP)

One time KYC

eSign Service Providers (ESP)

AadhaarPAN

...

Residents needing to sign a document

Source: http://cca.gov.in/esign

eSignOpen protocol for digital signature

19

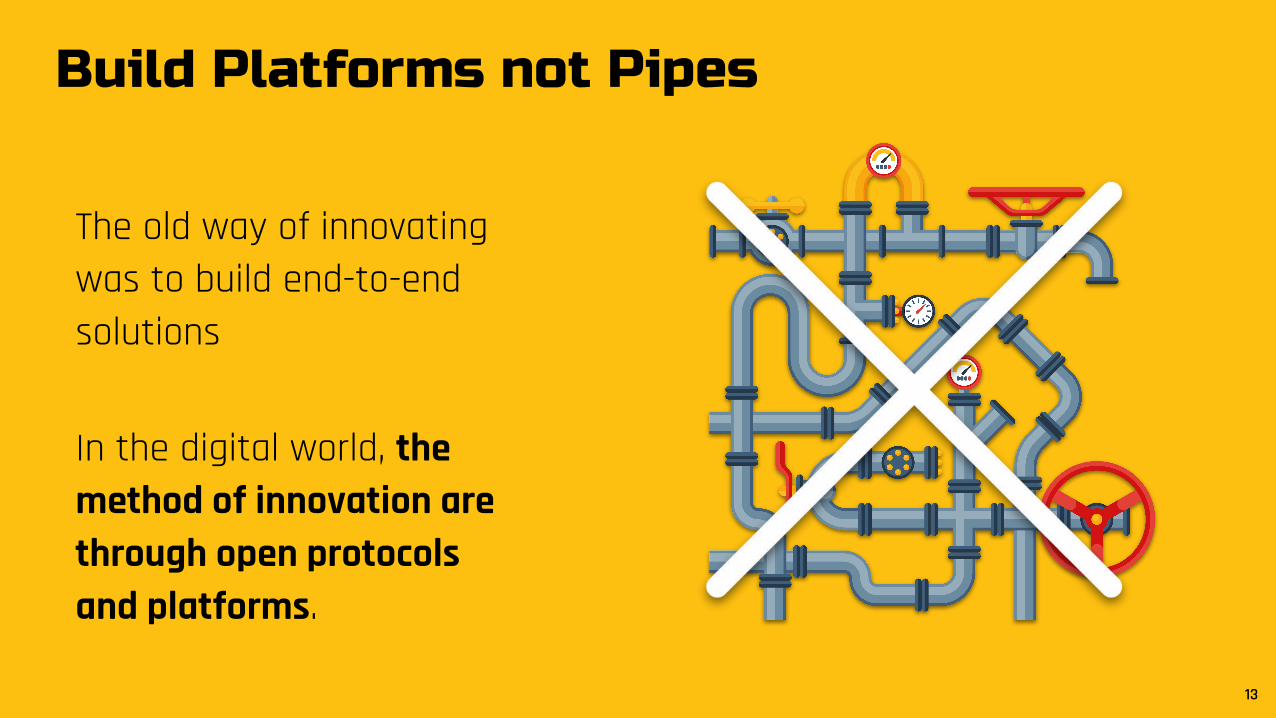

UPI: Any stored value, any app, any device, any currencyAn open protocol for instant money movement

Virtual Addressing layer @ No need to disclose account information.

Allows account portability, enhances privacy

Mobile First 2FATo leverage the increasing proliferation of mobile phones for low cost, onboardingat scale and secure authentication

Push & Pull PaymentsAnyone can send or request money

from any user

Universally InteroperableAnyone with a bank or mobile money account can send money to any other account in India!

Source: https://npci.org.in 20

UPI transactions have overtaken credit and debit card payments

Source : Retail Payment Statistics on NPCI Platformshttps://www.npci.org.in/statistics 21

1.3 Bn

Transaction Infrastructure

ENABLE

ENGAGE

EMPOWER

Aadhaar, PAN,& eKYC

eSign, APB, AEPS, UPI, BBPS, GST

1 Bne-Invoices in GST system

1.3 BnUPI Transactions a month

$32.4 BnDirect Benefit Transfer

$20 Bn transacted per monthCards are at 250 Mn

G2P payment$15 Bn in savings

10M tax payersLargest unified tax reform

200 mn Micro-ATM transactions

Inclusive banking at doorstepInteroperable, ecosystem driven

2010

2015

22

Machine-readable documents

Digitally protected

2.3 Bn documentsissued

Source: https://digilocker.gov.in

DigilockerIssuer Requestor

Users

Issues Documents

Digitally

Accesses Documents

Online

Approves Access

No Physical Papers No Fake Documents

Digital LockerOpen protocol for distributed credential sharing

23

A byproduct of these platforms is the creation of public as well as private data

Digital Identity

Paperless Process

Commerce

Payment

Social

Machine Learning & Algorithms

We need to think about how this data wealth will translate to real wealth for users

24

0 0

0 1 0

1

0 0

0 1 0

1

0 0 0

1 0 1

Data Empowerment and Protection Architecture (DEPA)

India is implementing DEPA across

multiple domains through

interoperable protocols,

digital infrastructure,

& and electronic consent managers

25

The Account Aggregator will facilitate consented sharing of financial information in real-time

Bank

Mutual Fund House

Insurance Provider

Tax / GST Platform

Flow-Based Credit

Personal Finance Management

Wealth Management

Robo Advisors

Financial Information Providers Financial Information Users

Financial Data Access

Fiduciary(NBFC Account

Aggregator)

Request for Data

Consent to Share

Encrypted Data Flow

E2E Encrypted Data Flowbased on User Consent

Data Access Notifications

Consent to share data

Request for Data

Electronic Consent Artefact

Source: https://api.rebit.org.in/ 26

Health Data Fiduciary

Hospital

Lab

Health Apps

Hospital

Hospital

Doctor / Specialist

Insurance Provider

Personal Health Apps

Health Information Providers Health Information Users

PHR Network is Soon Becoming a Reality

Request for Data

Consent to Share

Encrypted Data Flow

27

28

ENABLE

ENGAGE

EMPOWER

Aadhaar, PAN,& eKYC

eSign, APB, AEPS, UPI, BBPS, GST

e-Documents, e-credentials, DEPA, AA

?New Innovation

15 MnDigital Locker Users

3 BnMachine verifiable Docs

Active online locker usersSchool certificates, Driver Licenses, and other credentials

1000's of contextualizedData driven innovation

400+ Fintech Startups

Thriving innovation ecosystem

2010

2015

2018

Data Infrastructure

Architectural PrinciplesKey Principles while building nation scale systems

29

● Build platforms not monolithic applications● Unbundle applications into many micro services● Adopt open standards and open source● Use commodity and heterogeneous computing● Interoperability through open specifications● Privacy and Security by Design● Trust by design through registries, signatures and attestations● Scalability by design● Observability through telemetry● Failure resilience and isolation by design

Cloud Computing, Smartphones

Internet, GPS, Maps Open Protocols

Information Discovery

Knowledge Democratization

Government Services

Social Networking

e-Commerce

e-Learning

UrbanMobility

One Internet, many applications

Internet Infrastructure30

One INDIA STACK, many innovative & inclusive solutions

DEPA, AADigital Locker UPI, AEPS, APB

Aadhaar, eKYC, eSignDirect Benefit Transfer

Jan DhanFinancial inclusion

Health Insurance

FasterPayments

Skilling & Education

Digital Lending

Tax Reform

India Stack Infrastructure31

India is laying digital infrastructure across domains with individuals and small businesses at the center

Bharat Bill Payment System

Goods & Services Tax Network

DIKSHA

National Health Stack

Digital Sky

Electronic Toll Collection - FasTag

Aadhaar, JAM, India Stack 32

Friction ReductionReduces cost of doing

business, and expands markets

Access to learning

Access to healthcare

Access to products & services

Increased TrustDigital & portable

attestations, verifiable claims

ComplianceMake it easier to comply

through automation

… and thus, accelerating formalization

33

34

The old way of innovating was to build end-to-end solutions

In the digital world, the method of innovation is via shared infrastructure

India's technology advancement has left even Silicon Valley standing. India has built the world's first national digital infrastructure, leaping at least two generations of financial technologies and has built something at least as important as the railroad was to the UK or the interstate highways was to the US.

Distributing the ability to solve!

- Leading Macro Investor

34

Nandan Nilekani, 2018

Thank you!Dr. Vivek Raghavan