Embed Size (px)

Citation preview

www.bridgetoindia.com

INDIA RENEWABLEMAP 2020JUNE

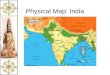

Total utility scale solar and wind capacity as on 30 June 20201

All figures in MW

Leading players1

(Utility scale solar and wind projects commissioned between July 2019 - June 2020, totaling 6,284 MW)

Project developers

Domestic manufacturers

Module suppliers(estimated DC size - 6,373 MW)

Inverter suppliers(AC size - 4,971 MW)

Solar EPC contractors(AC size - 4,971 MW)

Turbine manufacturers(1,313 MW)

KARNATAKA

ANDAMAN &NICOBAR ISLANDSANDHRA PRADESH

BIHAR

CHHATTISGARH

GUJARAT

HARYANA

JHARKHAND

KERALA

MADHYA PRADESH

MAHARASHTRA

ODISHA

Total RE generationfrom July 2019 to June 2020

5-15 billion kWh1-5 billion kWh<1 billion kWh

>15 billion kWh

RAJASTHAN

UTTARAKHAND

UTTAR PRADESH

TAMIL NADU

TELANGANA

PUNJAB

WEST BENGAL

Comm.25

5

25 20Pipeline25

750

1,250500

65

65

1,76

1

313

Pipeline1,315 3,660

1,587

4,0383973

Commissioned7,698

10.5

% R

EN

EW

10.0% NLC

8.8% SB ENERGY

7.6% ADANI

5.6% A

CM

E

5.3% A

ZU

RE

HE

RO

FU

TU

RE

4.8

%

GR

EE

NK

O 4

.6%

FO

RTU

M 4

.0%

SEMBCORP 4.0%

ATHA GROUP 3.2%SPRNG 3.2%

CLEANTECH 2.7%

AVAADA 2.4%

TATA POWER 2.4%

RAYS POWER 2.1%

ENGIE 2.1%

TORRENT 2.0%

ADITYA BIRLA 1.9%

JUN

IPER 1.6%

SITAC

RE 1.6%

ASIA

N F

AB

1.5%

SO

LA

RP

AC

K 1.0%

OT

HE

RS

7.3%

11.4

% R

ISE

N

8.4% SUNTECH

8.0% LONGI

7.2% TRINA

7.1% ZN

SHIN

E

5.7% E

MM

VE

EAD

AN

I 4.

9%

WA

AR

EE

4.5

%

VIK

RA

M 4

.0%

RENESOLA 3.

3%

CANADIAN 3.3%

CSUN 3.2%JINKO SOLAR 3.2%

PREMIER 2.5%

JA SOLAR 1.5%

TALESUN 1.5%

ET SOLAR 1.4%

GOLDI 1.1%

GCL 1.0%

WEBSOL 0.8%

VYINGLI 0.7%

AMERISOLAR 0.4%

REC 0.1%

HH

V SOLAR 0.1%

OT

HE

RS

/ NA

14.61%

28.8% HUAW

EI

18.2% TMEIC

TB

EA

11.

7%

SINENG 10.8%

SUNGROW 10.3%

ABB 6.1%

KEH

UA 6.0%

ME

DH

A 2.0%

DE

LT

A 0.5%

HIT

AC

HI 0.3%

OT

HE

RS

/ NA

5.2%

20.2% S

UZ

LO

N

38.1% SIEMENS GAMESA

ENVISION 17.7%

VESTAS 11.4%

SENVION 4.9%

INO

X WIN

D 3.8%

OT

HE

RS

/ NA 3.8%

NTPC offtake3,922

NTPC offtake 200

DISCOM offtake19,944

DISCOM offtake34,394

DISCOM offtake 1,219

DISCOM offtake9,377

SECI offtake3,700

SECI offtake 8,593

NTPC offtake 1,420

SECI offtake26,382

SECI offtake609

Others4,996

Others3,034

Others 1,244

Others 32

Other PSUs1,000

Other PSUs2,050

Other PSUs 50

Solar32,561

Wind37,247

Wind10,094WW

11WW0000WW00WiWi

,,n0n00nn999d999d444444

Commissioned69,808

Pipeline52,357

Solar42,263

Commissioned106

26

100

Commissioned210

180

30

2,325

5052

0

110 290284 359

500

78

222222222222222 32 332 3,3,3333,33333232323232332323232222525225255252225252555555555

Comm.9,376

Pipeline9,144

2,153

1,579

7,22

36,

286

859

6,1895,163

5,113

2,955

1.02

6

Commissioned156

30

126

Pipeline50

Commissioned24

1,125

1,175

149

115 268

1,140605

3911,745

7,32

5Commissioned12,413

Pipeline1,566 3,861

5,1094,960

1,699

Comm.140

5850

26

92 82

56

Pipeline142

300 220

396

94 2

64 200

424

562

Pipeline1,021

2,3331,551

2,4932,429

624

Commissioned4,826

2,7022222222222222 72 772 722,2,72 72 777,70,77077070707077070707070700770022000202022020002022222222

2,542

3050

391

8658951,582

401

296

5,0284,904

124225

176110

Commissioned6,610

Pipeline3,103

Commissioned437

76

325

520

25

87

Pipeline76

22

908

Commissioned930

Pipeline110

2,109

4884,947

2,350

1,1951,155

Pipeline19,474

4,3114,298

356

900

19,118

15,44512,945

1,834

1,839

1,60

0

Comm.9,258

400261

343

751

3,3893,814

410

750

500

250

8,856

7,355

8001,004

Pipeline1,804

Commissioned12,670

128 123

484

390

3,523

2,649

Pipeline217

Commissioned3,651

94

Comm.953

725

105

150123

1,37

3

Pipeline1,523

Commissioned225

6

219

100

2

6238

Commissioned102

Pipeline10

Associate sponsorLead sponsors

inverters

SELF-EPC 31.3%

10.3

% S

&W

8.9%

TATA

PO

WER

8.5% L&T

6.3% ADANI INFRA

5.0% B-ELECTRIC4.2% REFEX

4.0% K

EC

2.7% R

AYS

PO

WE

R IN

FR

A

2.2% O

RIA

NO

2.0% E

NR

ICH

PR

EM

IER

2.0

%

LN

V 2

.0%

MA

HIN

DR

A S

US

TE

N 1

.8%

RIT

IS M

EE

RA

1.0

%

BH

EL 1

.0%

AM

AR

A R

AJA

1.0%

JAK

SON

0.4%

VIKRAM

SOLA

R 0.

2%

FOURTH

PAR

TNER

0.2%

SWELE

CT 0.1%

BOSCH 0.1%

SIEMENS G

AMESA 0.1%

RANERGY 0.1%

OTHERS/ NA 4.5%

Leading players Prices

Utility Scale Solar | Rooftop Solar | Wind

www.india-re-navigator.com

Top 10 players(projects commissioned between July 2019 to June 2020)

Top 15 project developers(Utility scale solar and wind capacity as on 30 June 2020)

Notes

Electricity generation by source, billion kWh

PEW

+91 124 4204003

www.bridgetoindia.comC-8/5, DLF Phase 1,

Gurugram - 122001 (HR), India

© BRIDGE TO INDIA Energy Private Limited

Current rank

1

2

3

4

5

6

7

8

9

10

Previousrank

Increase/ Decrease

Project developersCompanyName

ReNew

NLC

SB Energy

Acme

Azure Power

Hero Future

Greenko

Adani

Fortum

Sembcorp

3

2

1

-

4

-

-

9

10

-

Previousrank

Increase/ Decrease

Module suppliersCompanyName

Risen

Suntech

Longi

Trina

ZNShine

Emmvee

Adani

Waaree

Vikram

Renesola

1

5

-

10

2

-

-

6

3

-

Previousrank

Increase/ Decrease

Inverter suppliersCompanyName

Huawei

TMEIC

TBEA

Kehua

ABB

Delta

Medha

Hitachi

2

1

5

4

8

-

6

7

Sungrow 3

Sineng -

Previousrank

Increase/ Decrease

Solar EPC contractorsCompanyName

S & W

L&T

Tata Power

KEC

Rays PowerInfra

Refex

Oriano

B-Electric

Enrich,Premier,LNV

Adani Infra

1

2

4

-

7

6

8

-

9

-

Previousrank

Increase/ Decrease

Turbine manufacturersCompanyName

SiemensGamesa

Suzlon

Envision

Vestas

Senvion

Inox Wind

2

1

-

3

7

6

Ratio of RE power generation to total power consumption

Andhra Pradesh

Gujarat

Karnataka

Madhya Pradesh

Maharashtra

Punjab

RajasthanTamil Nadu

Telangana

Uttar Pradesh

Paid reports

India Solar Open Access Market

India Solar Rooftop Market

India Solar Rooftop Market Analytics

Solar park development in India

Subscription packages

India RE Weekly

India Solar Compass

Analyst time

India RE Policy Brief & India RE Market update

Customized rep

INDIA RE CEO SURVEY 2018

Lead sponsor

INDIA SOLAR COMPASS 2018

Surge of new tenders and fall in moduleprices bring hope to the sector

It’s raining tenders

India RE Week

Subscribe to the deepest market insights

0%

5%

10%

15%

20%

25%

30%

35%

40%

FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

RE tariff trend2

Wind power tenders Solar-wind hybrid tendersSolar power tenders

Ca

pa

cit

y a

llo

ca

tio

n,

MW

June 2018 Until June 2020 2019

Tender size

MS

ED

CL

Ma

ha

ras

htr

a S

ola

r, 1

,00

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-I

, 2

,00

0 M

W

SE

CI

An

dh

ra P

rad

es

h S

ola

r, 7

50

MW

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-I

I, 3

,00

0 M

W

GR

IDC

O O

dis

ha

So

lar,

20

0 M

W

NT

PC

Pa

n I

nd

ia S

ola

r, 2

,00

0 M

W

NT

PC

Pa

n I

nd

ia W

ind

, 1

,20

0 M

W

OR

ED

A O

dh

isa

So

lar,

6 M

W

GU

VN

L G

uja

rat

So

lar

Tra

nch

e-I

I, 5

00

MW

SE

CI

Pa

n I

nd

ia W

ind

Tra

nch

e-V

, 1

,20

0 M

W

KR

ED

L K

arn

ata

ka

So

lar,

15

0 M

W

UP

NE

DA

Utt

ar

Pra

de

sh

So

lar,

50

0 M

W

KR

ED

L K

arn

ata

ka

So

lar,

20

0 M

W

SE

CI

Utt

ar

Pra

de

sh

So

lar,

15

0 M

W

UP

NE

DA

Utt

ar

Pra

de

sh

, S

ola

r, 5

50

MW

SE

CI

Pa

n I

nd

ia S

ola

r-W

ind

Hyb

rid

Tra

nch

e-I

, 1

,20

0 M

W

KR

ED

L K

arn

ata

ka

So

lar,

10

0 M

W

SE

CI

Pa

n I

nd

ia W

ind

Tra

nch

e-V

I, 1

,20

0 M

W

MS

ED

CL

Ma

ha

ras

htr

a S

ola

r, 1

,00

0 M

W

GU

VN

L G

uja

rat

So

lar

Tra

nch

e-I

V,

50

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-I

II,

1,2

00

MW

SE

CI

Ra

jas

tha

n S

ola

r Tra

nch

e-I

, 7

50

MW

GU

VN

L G

uja

rat

So

lar

Tra

nch

e-I

II,

70

0 M

W

SE

CI

Ma

ha

ras

htr

a S

ola

r, 2

50

MW

SE

CI

Pa

n I

nd

ia W

ind

Tra

nch

e-V

II,

1,2

00

MW

GU

VN

L G

uja

rat

Win

d T

ran

ch

e-I

I, 1

,00

0 M

W

GU

VN

L G

uja

rat

So

lar

Tra

nch

e-V

, 1

,00

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r-W

ind

Hyb

rid

Tra

nch

e-I

I, 1

,20

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-I

V,

1,2

00

MW

MS

ED

CL

Ma

ha

rash

tra

So

lar,

50

MW

MS

ED

CL

Ma

ha

ras

htr

a S

ola

r, 1

,40

0 M

W

SE

CI

Ra

jas

tha

n S

ola

r Tra

nch

e-I

I, 7

50

MW

UP

NE

DA

Utt

ar

Pra

de

sh

So

lar,

50

0 M

W

MA

HA

GE

NC

O M

ah

ara

sh

tra

So

lar,

18

4 M

W

HP

PC

Ha

rya

na

So

lar,

30

0 M

W

GU

VN

L G

uja

rat

So

lar

Tra

nch

e-V

I, 2

00

MW

GU

VN

L G

uja

rat

So

lar

Tra

nch

e-V

II,

75

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-V

, 1

,20

0 M

W

SE

CI

Pa

n I

nd

ia W

ind

Tra

nch

e-V

III,

1,8

00

MW

AE

ML

Ma

ha

rash

tra

So

lar-

Win

d

Hyb

rid

, 3

50

MW

SE

CI

Pa

n I

nd

ia S

ola

r P

SU

Tra

nch

e-I

, 2

,00

0 M

W

NT

PC

Pa

n I

nd

ia S

ola

r, 1

,20

0 M

W

Ta

ta P

ow

er

Ma

ha

rash

tra

So

lar,

15

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-V

I, 1

,20

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r P

SU

Tra

nch

e-I

I, 1

,50

0 M

W

MS

ED

CL

Ma

ha

ras

htr

a S

ola

r, 5

00

MW

MS

ED

CL

Ma

ha

ras

htr

a S

ola

r, 1

,35

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r, 7

,00

0 M

W

(Ma

nu

factu

rin

g-l

ink

ed

)

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-V

II,

1,2

00

MW

(So

lar-

Win

d-S

tora

ge

Hyb

rid

, P

ea

k P

ow

er)

UP

NE

DA

Utt

ar

Pra

de

sh

So

lar,

50

0 M

W

AP

GC

L A

ssa

m S

ola

r, 7

0 M

W

MS

ED

CL

Ma

ha

ras

htr

a S

ola

r, 1

,35

0 M

W

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-V

III,

12

00

MW

MS

ED

CL

Ma

ha

ras

htr

a S

ola

r, 5

00

MW

GU

VN

L G

uja

rat

So

lar

Tra

nch

e-V

III.

50

0 M

W

RR

EC

L R

aja

sth

an

So

lar,

11

3.5

MW

NH

PC

Pa

n I

nd

ia S

ola

r, 2

,00

0 M

W

SE

CI

Pa

n I

nd

ia R

TC

Tra

nch

e-I

, 4

00

MW

(So

lar-

Win

d-S

tora

ge

Hyb

rid

)

SE

CI

Pa

n I

nd

ia S

ola

r T

ran

ch

e-I

X,

2,0

00

MW

MS

ED

CL

Pa

n I

nd

ia S

ola

r, 1

,00

0 M

W

Ta

riff

, IN

R/

kW

h

2.71

3.09

3.15

2.722.54

2.44

2.71

2.70 2.44

2.44

2.79

2.792.60

2.59

2.83

3.13

3.13

2.45

2.44

2.77

2.76

2.92

2.92

2.89

2.89

3.29

3.293.08

3.02 2.69

2.67

2.91

2.91

2.83

2.82

2.75

2.55

2.68

2.55

2.61

2.48

2.492.65

2.702.87

2.91

2.79

2.83

2.81

2.95

2.75

2.75

2.69

2.69

2.54

2.552.99

2.993.15

3.15

2.50

2.503.02

3.02

3.05

3.05

2.73 2.65

2.65

2.75

2.752.65

2.84 3.24

3.24

3.50

3.50

2.63

2.63

2.83

2.832.72

2.71

3.50

3.50

2.90

2.89

3.14

3.142.92

2.92

4.30

4.04

3.18

3.17

3.99

3.28

2.50

2.51 2.90

2.90

2.61

2.64

3.90

2.55

2.56

3.55

3.55

2.36

2.38

3.90

3.30

2.83

2.53

2.99

2.74

3.23

3.17

2.77

2.00

3.00

4.00

1,000 2,000 2,000 500 150 100 50 100500 550 500 500 250

250

50 10 40 184 241 100

50

480745

600

1,200

680480

440 922

300

150 960500

5

1,104

1,200

184 70 283

1,200

350 350 114 2,000 2,000

40012,000

750840 1,200

1,000

1,200

1,200

1,200

235 75075

6600 700

Allocated capacity

Commissioned69,808

Solar

Sola

r

WindWind

Pipeline52,357

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0 1,000 2,000 3,000 4,000 5,000

Commissioned solar capacityCommissioned wind capacity

Pipeline solar capacityPipeline wind capacity

Total commissioned capacity, MW

To

tal

pip

leli

ne

, M

W

Eden

Renewables

Avaada

Sprng

Energy

NTPCSB Energy

Hero

Sembcorp

Mytrah

Azure Power

Acme

Tata Power

Greenko

ReNew

Adani

Tender issuance and auctions, MW

05,000 5,00010,000 10,00015,000 15,00020,000 20,00025,000 25,000

Q1 2017

Q2 2017

Q3 2017

Q4 2017

Q1 2018

Q2 2018

Q3 2018

Q4 2018

Q1 2019

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Tender issuance Auctions

Wind Solar-wind hybrid Solar-wind-thermal-storage hybridSolar-wind-storage hybridSolar

INDIA RENEWABLEMAP 2020JUNE

Coal Gas Nuclear Hydro Wind Solar Small Hydro Other RE

50

75

100

125

A J A O D DF A J A O F A J A O D F A J A O D F A J A O D F A J

2015 2016 2017 2018 2019 2020

Associate sponsorLead sponsors

inverters

Associate sponsorLead sponsors

inverters

1. Methodology

a. BRIDGE TO INDIA has conducted an

extensive data collection exercise and relied

on multiple market sources including MNRE,

CEA, state nodal agencies, project develop-

ers and equipment suppliers to provide

accurate, factual information as far as

possible. Some suppliers were either

unreachable or did not validate the data

available with us. All data has been

cross-referenced, where possible. However,

we do not guarantee completeness or

accuracy of any information.

b. This report includes only offsite, grid

connected projects. Onsite projects for

captive consumption are not covered in this

report.

c. Market shares for all players are given on

the basis of capacity commissioned by them

in the 12 month period from July 2019-June

2020.

d. Pipeline includes projects that have been

allocated to developers and are under

different stages of development and

construction. It includes projects where

execution of PPA and/ or regulatory approval

may still be pending.

e. For solar-wind hybrid tenders, we have

estimated solar and wind capacity on the

basis of tender specifications and prevalent

market norms.

f. States with less than 20 MW commissioned

capacities are not shown on the map.

g. All tender and project capacity data is stated

in AC MW. For module supplier market share

analysis, we have used DC numbers, where

available, or increased AC project capacities

by 50%.

h. Location for 12,544 MW of pipeline projects

under inter-state transmission tenders is not

available.

i. In many projects, the EPC contractor role is

split between multiple parties. We have used

several criteria including final responsibility

for commissioning and value of contracts for

determining credits.

j. Self-EPC denotes EPC services rendered

in-house by developers or their affiliates,

who are not engaged in providing EPC

services to third party clients.

k. For projects with escalating tariff structure,

levellised tariff has been shown.

l. Cancelled tenders and projects have not

been considered.

m. Renewable power generation data sourced

from CEA includes generation from solar and

wind sources only.

n. Projects where NVVN is the offtaker is

considered under NTPC capacity.

2. Acronyms used:

a. AEML – Adani Electricity Mumbai Limited

b. APGCL – Assam Power Generation Corpora-

tion Limited

c. GRIDCO – Grid Corporation of Odisha

d. GUVNL – Gujarat Urja Vikas Nigam Limited

e. HPPC – Haryana Power Purchase Centre

f. KREDL – Karnataka Renewable Energy

Development Limited

g. NHPC – National Hydroelectric Power

Corporations

h. MAHAGENCO – Maharashtra State Power

Generation Company

i. MSEDCL – Maharashtra State Electricity

Distribution Corporation Limited

j. OREDA – Orissa Renewable Energy

Development Agency

k. RRECL – Rajasthan Renewable Energy

Corporation Limited

l. SECI – Solar Energy Corporation of India

Limited

m. UPNEDA – Uttar Pradesh New & Renewable

Energy Development Agency

3. This report has been sponsored by Longi and

Solis (Lead Sponsors), and STI Norland

(Associate Sponsor) but all production responsi-

bility, editorial rights and copyrights remain with

BRIDGE TO INDIA.