Embed Size (px)

Citation preview

India Card Payment

Report FY 13-14

1

Contents

About Worldline ...................................................................................... 2

Foreword ................................................................................................ 4

Credit Cards ............................................................................................ 5

Debit Cards ............................................................................................. 6

POS Terminals ......................................................................................... 7

Transaction and Spends .......................................................................... 8

Emerging Trends ................................................................................... 10

Appendix ............................................................................................... 11

COPYRIGHT INFORMATION:

All information contained in this report is the property of Worldline India. Reproduction of

information, tables, charts etc. is permitted subject to the condition that the source is

acknowledged as follows: “Source: Worldline India Research”

This report can be viewed on our website: http://in.worldline.com/

Disclaimer:

The data presented is based on feedback from relevant people in various banks and from various

other sources. Worldline, India makes no representation or warranty, expressed or implied, is

made as to their accuracy or completeness. It has not been validated with actual records.

Wherever published information was available it has been used. The analysis done is purely on the

data collected and the views expressed thereof are on the basis of the analysis. In certain cases,

where data was not forthcoming, best effort estimates have been used. This report is not to be

relied upon in substitution for exercise of independent judgment and use of this data by any

individual or entity for any of their business decisions or for any other purpose is solely at their

own risk and responsibility and Worldline India shall not be responsible and accepts no liability for

any loss arising from the use of the information presented in this report for what so ever.

2

About Worldline

About Worldline

Worldline, an Atos subsidiary, is the European leader and a global player in the

payments and transactional services industry. Worldline delivers new generation

services, enabling its customers to offer seamless and innovative solutions to the

end consumer. Key actor for B2B2C industries for over 40 years, Worldline is

ideally positioned to support and contribute to the success of all businesses and

administrative services in a perpetually evolving market. Worldline offers a

unique and flexible business model built around a global and growing portfolio,

thus enabling end-to-end support. Worldline activities are organized around

three axes: Merchant Services & Terminals, Mobility & eTransactional Services,

Financial Processing Services & Software Licensing. In 2012, Worldline's

activities within the Atos Group generated (pro forma) revenues of 1.1 billion

euros. The company employs more than 7,200 people worldwide.

About Worldline India

Founded in 1996, Worldline India provides end-to-end services for critical

electronic transactions in the country. It specializes in electronic payment

services in India, partnering with banks, merchants and government institutions.

Through the use of its infrastructure, Worldline India pioneered the concept of

shared services, through the use of its infrastructure, for card and transaction

services across the country and offers comprehensive acquiring and issuing

related services under the Design, Build, Host and Operate model.

Today, it is the largest acquiring processor in India with a 30% market share,

and has a 90% share of the outsourced market. It processes over 200 Mn

acquiring transactions each year worth ~INR 500 Billion and a peak volume of

over 1 million transactions per day. A key strength is its pan-India reach; it

services over 250,000 terminals in more than 1600 cities and towns, managing

terminals even in inaccessible locations.

Worldline is also a significant player in Card issuance in the country, with over

15 million credit, debit and prepaid cards issued and managed for various

customers. It also provides business critical value added services such as

Dynamic Currency Conversion, loyalty management and fraud & risk

management to its partners. It is a leader in innovation and works closely with

its partners to enable new channels for card acceptance, such as internet

payments and mobiles.

3

Worldline has a wide range of client coverage, with over 30+ contracts in the

Banking and Finance space and several large contracts in the Energy & Utilities

and the Retail space.

Powered by a robust infrastructure with world class data centers in Mumbai and

Bangalore, Worldline maintains its vast communication network through 19 hub

locations and is an ISO 9001:2008, ISO 27001 and a PCI DSS 2.0 certified

organization.

People are at the core of the organization, and Worldline services its customers

through a unique blend of 350+ experts spanning across banking, technology

and payment domains. It strives for operational and business excellence in a

dynamic, growing and competitive market which is demonstrated by several

awards and recognitions over the years from customers and industry

organizations.

For more information please visit: in.worldline.com

4

Foreword

I’m glad to present to you the India Card Payment Report for

FY13-14, a year which saw the payments ecosystem in India

continue on its high growth track despite a challenging

environment and regulatory changes.

The growth in card base, transactions and spends has

continued in both credit and debit cards, while acquiring again

grew at a fast pace sustained by focused expansion by a few

large banks.

For the next year we see several trends already emerging: products which cater

to needs of specific merchant and cardholder segments and increased

prevalence of the multichannel environment (physical, internet and mobile).

Based on the positive feedback we received from you, we continue to present

the report in the format adopted last year, covering a 5 year period from FY10-

FY14 to examine how trends have evolved across the board during this period.

We would like to thank all those who provided their valuable suggestions,

comments and feedback. Please mail your suggestions to us.

Regards,

Deepak Chandnani Chief Executive Officer, Worldline South Asia

5

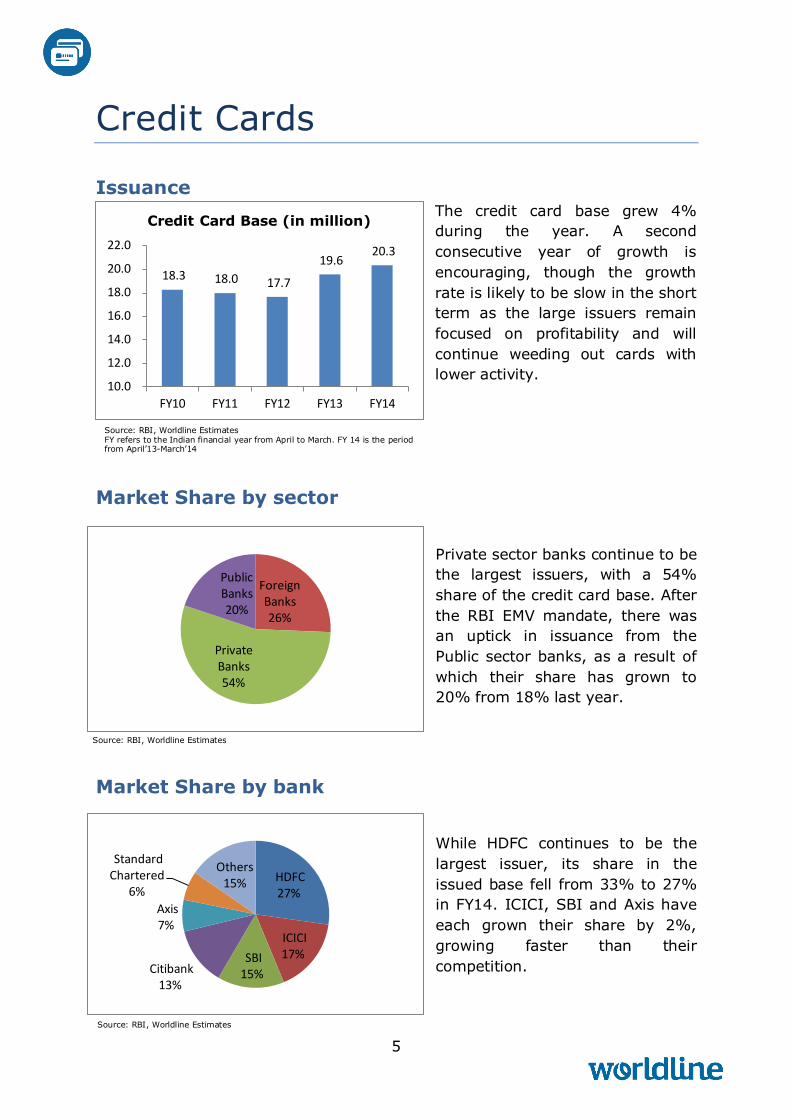

18.3 18.0 17.7

19.6 20.3

10.0

12.0

14.0

16.0

18.0

20.0

22.0

FY10 FY11 FY12 FY13 FY14

Credit Card Base (in million)

Foreign Banks 26%

Private Banks 54%

Public Banks 20%

HDFC 27%

ICICI 17% SBI

15% Citibank 13%

Axis 7%

Standard Chartered

6%

Others 15%

Credit Cards

Issuance The credit card base grew 4%

during the year. A second

consecutive year of growth is

encouraging, though the growth

rate is likely to be slow in the short

term as the large issuers remain

focused on profitability and will

continue weeding out cards with

lower activity.

Market Share by sector

Private sector banks continue to be

the largest issuers, with a 54%

share of the credit card base. After

the RBI EMV mandate, there was

an uptick in issuance from the

Public sector banks, as a result of

which their share has grown to

20% from 18% last year.

Market Share by bank

While HDFC continues to be the

largest issuer, its share in the

issued base fell from 33% to 27%

in FY14. ICICI, SBI and Axis have

each grown their share by 2%,

growing faster than their

competition.

Source: RBI, Worldline Estimates FY refers to the Indian financial year from April to March. FY 14 is the period from April’13-March’14

Source: RBI, Worldline Estimates

Source: RBI, Worldline Estimates

6

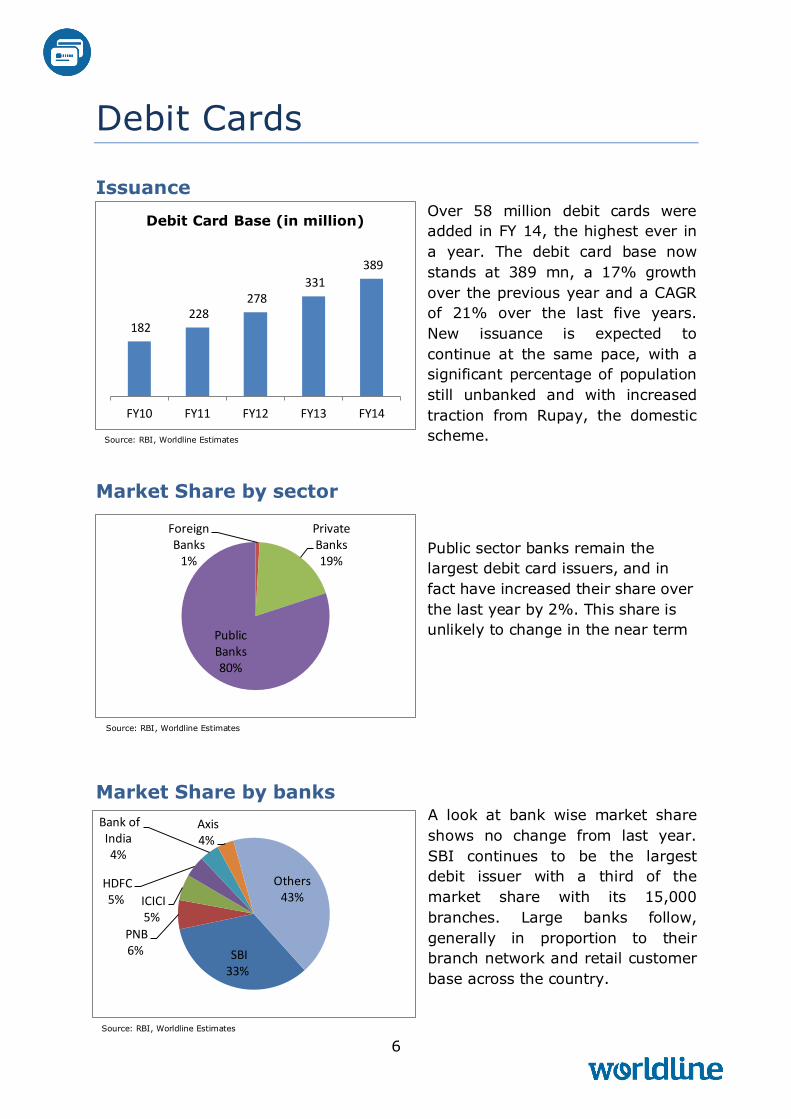

182 228

278 331

389

FY10 FY11 FY12 FY13 FY14

Debit Card Base (in million)

Foreign Banks

1%

Private Banks 19%

Public Banks 80%

SBI 33%

PNB 6%

ICICI 5%

HDFC 5%

Bank of India 4%

Axis 4%

Others 43%

Debit Cards

Issuance Over 58 million debit cards were

added in FY 14, the highest ever in

a year. The debit card base now

stands at 389 mn, a 17% growth

over the previous year and a CAGR

of 21% over the last five years.

New issuance is expected to

continue at the same pace, with a

significant percentage of population

still unbanked and with increased

traction from Rupay, the domestic

scheme.

Market Share by sector

Public sector banks remain the

largest debit card issuers, and in

fact have increased their share over

the last year by 2%. This share is

unlikely to change in the near term

Market Share by banks A look at bank wise market share

shows no change from last year.

SBI continues to be the largest

debit issuer with a third of the

market share with its 15,000

branches. Large banks follow,

generally in proportion to their

branch network and retail customer

base across the country.

Source: RBI, Worldline Estimates

Source: RBI, Worldline Estimates

Source: RBI, Worldline Estimates

7

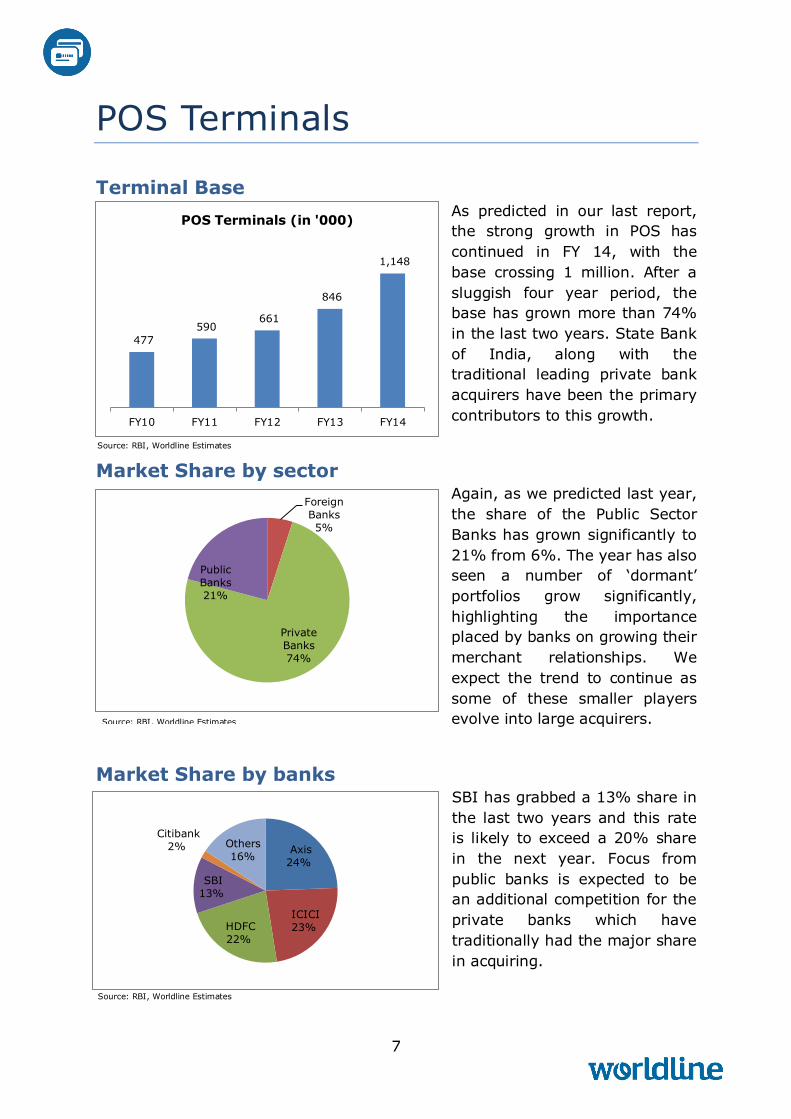

477

590 661

846

1,148

FY10 FY11 FY12 FY13 FY14

POS Terminals (in '000)

Foreign

Banks

5%

Private

Banks

74%

Public

Banks

21%

Axis

24%

ICICI

23% HDFC

22%

SBI

13%

Citibank

2% Others

16%

POS Terminals

Terminal Base As predicted in our last report,

the strong growth in POS has

continued in FY 14, with the

base crossing 1 million. After a

sluggish four year period, the

base has grown more than 74%

in the last two years. State Bank

of India, along with the

traditional leading private bank

acquirers have been the primary

contributors to this growth.

Market Share by sector Again, as we predicted last year,

the share of the Public Sector

Banks has grown significantly to

21% from 6%. The year has also

seen a number of ‘dormant’

portfolios grow significantly,

highlighting the importance

placed by banks on growing their

merchant relationships. We

expect the trend to continue as

some of these smaller players

evolve into large acquirers.

Market Share by banks SBI has grabbed a 13% share in

the last two years and this rate

is likely to exceed a 20% share

in the next year. Focus from

public banks is expected to be

an additional competition for the

private banks which have

traditionally had the major share

in acquiring.

Source: RBI, Worldline Estimates

Source: RBI, Worldline Estimates

Source: RBI, Worldline Estimates

8

Transactions and Spends

Transactions

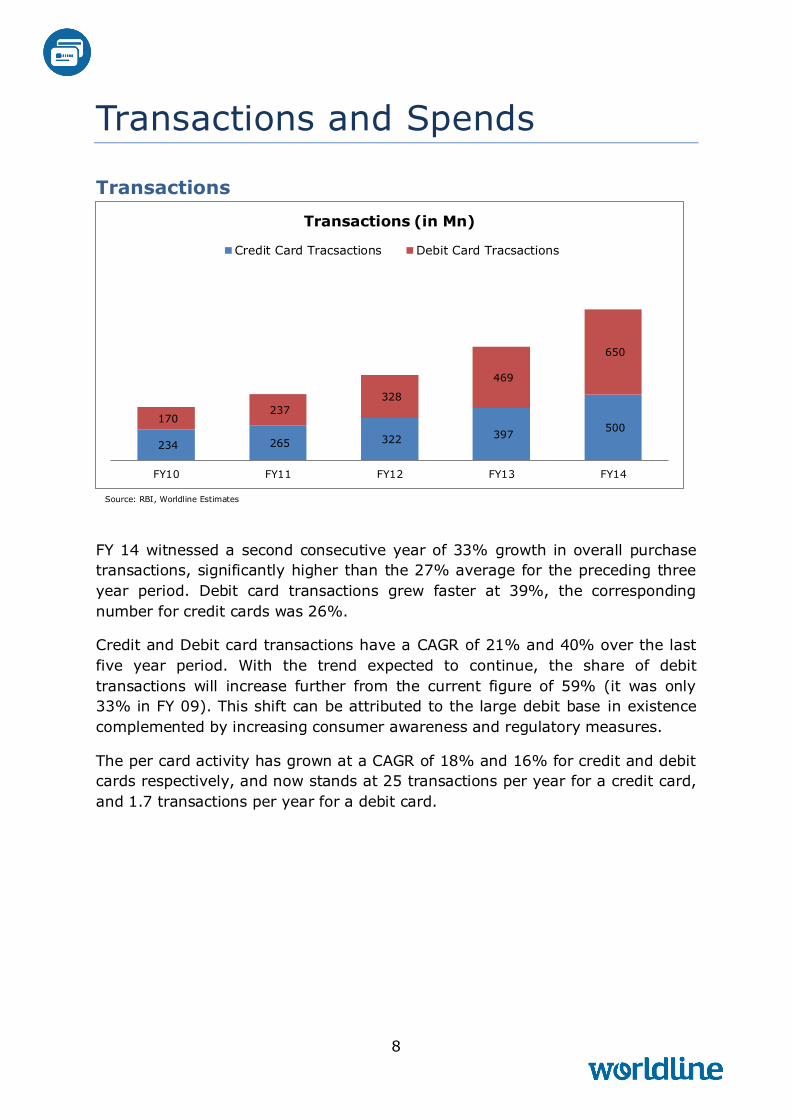

FY 14 witnessed a second consecutive year of 33% growth in overall purchase

transactions, significantly higher than the 27% average for the preceding three

year period. Debit card transactions grew faster at 39%, the corresponding

number for credit cards was 26%.

Credit and Debit card transactions have a CAGR of 21% and 40% over the last

five year period. With the trend expected to continue, the share of debit

transactions will increase further from the current figure of 59% (it was only

33% in FY 09). This shift can be attributed to the large debit base in existence

complemented by increasing consumer awareness and regulatory measures.

The per card activity has grown at a CAGR of 18% and 16% for credit and debit

cards respectively, and now stands at 25 transactions per year for a credit card,

and 1.7 transactions per year for a debit card.

234 265 322 397 500

170 237

328

469

650

FY10 FY11 FY12 FY13 FY14

Transactions (in Mn)

Credit Card Tracsactions Debit Card Tracsactions

Source: RBI, Worldline Estimates

9

629 755 978 1,229 1,443 264

387

534

743

999

FY10 FY11 FY12 FY13 FY14

Spends (in INR Bn)

Credit Card Spends Debit Card Spends

Retail Fashion 30%

Departmental Stores 12%

Supermarkets 10%

Hospital 8%

Hotels 10%

Restaurants 4%

Fuel 4%

Others 22%

Spends

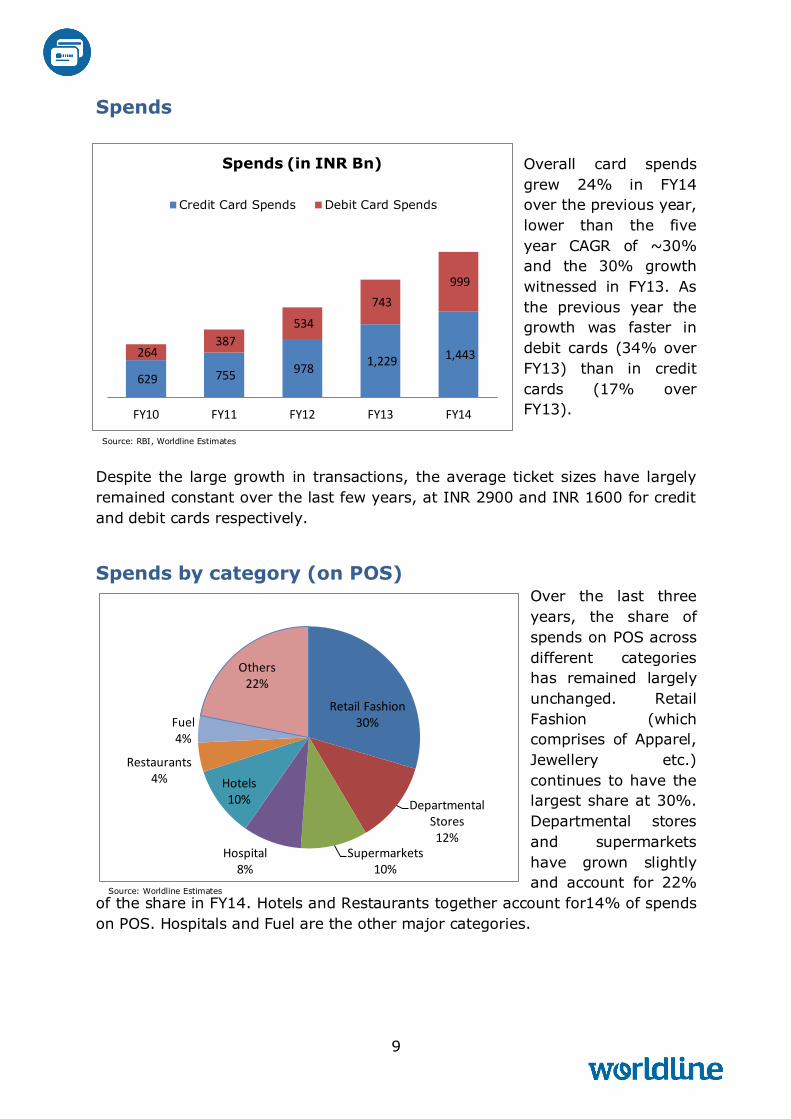

Overall card spends

grew 24% in FY14

over the previous year,

lower than the five

year CAGR of ~30%

and the 30% growth

witnessed in FY13. As

the previous year the

growth was faster in

debit cards (34% over

FY13) than in credit

cards (17% over

FY13).

Despite the large growth in transactions, the average ticket sizes have largely

remained constant over the last few years, at INR 2900 and INR 1600 for credit

and debit cards respectively.

Spends by category (on POS) Over the last three

years, the share of

spends on POS across

different categories

has remained largely

unchanged. Retail

Fashion (which

comprises of Apparel,

Jewellery etc.)

continues to have the

largest share at 30%.

Departmental stores

and supermarkets

have grown slightly

and account for 22%

of the share in FY14. Hotels and Restaurants together account for14% of spends

on POS. Hospitals and Fuel are the other major categories.

Source : RBI, WORLDLINE Estimates

Source: Worldline Estimates

Source: RBI, Worldline Estimates

10

Emerging Trends

Segment focus Differentiation has become key for acquirers and issuers to counter increasing

competition. To achieve this, one key trend emerging is to design specific

solutions for customer segments as opposed to the one size fits all approach. As

the completion further heats up, banks and their partners will have to focus on

innovative and efficient ways of addressing the unique need of the key merchant

segments and end consumers. Accurate insight and development of niche but

simple solutions and business models will be critical to drive adoption and

succeed. Worldline has been a pioneer in this approach with solutions like

Dynamic Currency Conversion for the hospitality segment; EMI enabling

solutions for organized retail and continues to work with other large merchant

segments for addressing specific needs.

OmniChannel Commerce The growing mobile POS solution has added mobile to the existing physical and

internet acceptance channels, and the next area of focus will be to have an

integrated approach across these multiple channels.

Omnichannel is a global trend, characterized by the delivery of the seamless

experience to the consumer. Different service providers for each channel is the

biggest friction point in this area, and finding a single partner to service all

channels will be the most critical aspect for banks and merchants to be able to

achieve the omnichannel objective. Worldline offers its partners acceptance

services across all channels: physical, internet and mobile.

Fraud Monitoring With another large retailer breach this year (Target), fraud remains a global

topic of discussion and presents a constant challenge for banks and merchants

alike. While the regulator focus on security will help contain the fraud, the banks

still need to implement best practices and technology to have an efficient fraud

and risk management framework. Worldline offers fraud monitoring services,

which help issuers and acquirers effectively monitor and control card payment

related fraud.

11

Appendix

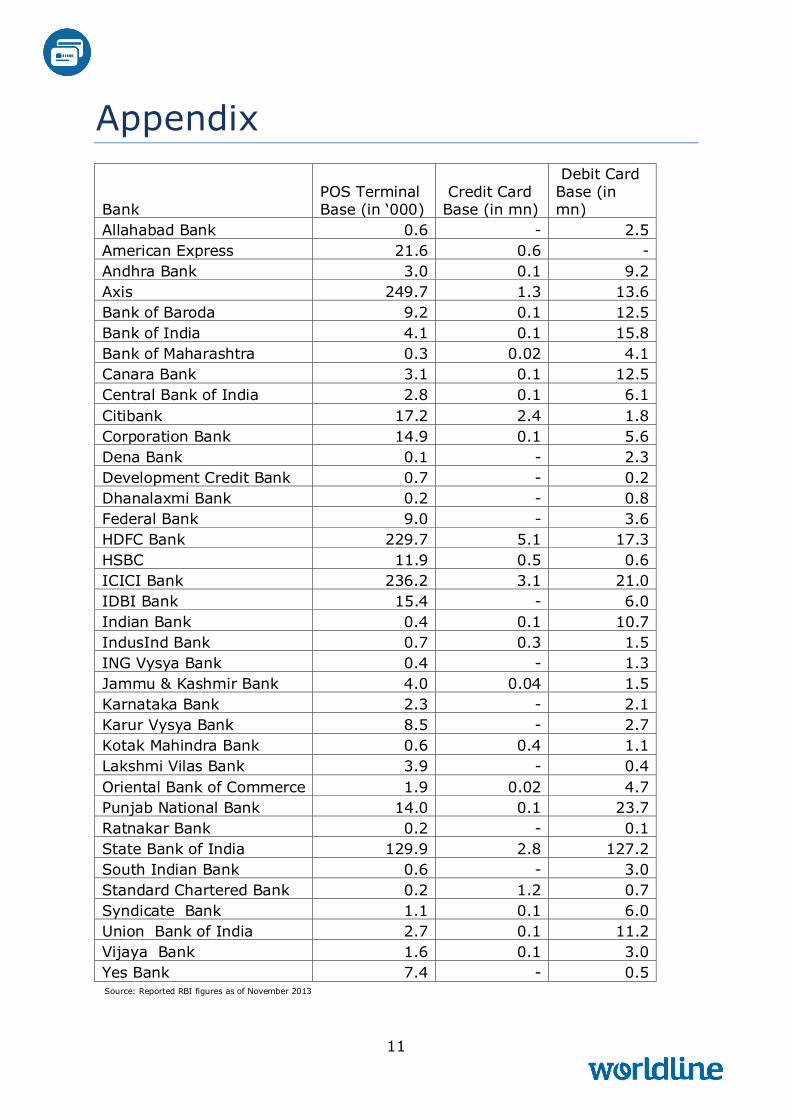

Bank POS Terminal Base (in ‘000)

Credit Card Base (in mn)

Debit Card Base (in mn)

Allahabad Bank 0.6 - 2.5

American Express 21.6 0.6 -

Andhra Bank 3.0 0.1 9.2

Axis 249.7 1.3 13.6

Bank of Baroda 9.2 0.1 12.5

Bank of India 4.1 0.1 15.8

Bank of Maharashtra 0.3 0.02 4.1

Canara Bank 3.1 0.1 12.5

Central Bank of India 2.8 0.1 6.1

Citibank 17.2 2.4 1.8

Corporation Bank 14.9 0.1 5.6

Dena Bank 0.1 - 2.3

Development Credit Bank 0.7 - 0.2

Dhanalaxmi Bank 0.2 - 0.8

Federal Bank 9.0 - 3.6

HDFC Bank 229.7 5.1 17.3

HSBC 11.9 0.5 0.6

ICICI Bank 236.2 3.1 21.0

IDBI Bank 15.4 - 6.0

Indian Bank 0.4 0.1 10.7

IndusInd Bank 0.7 0.3 1.5

ING Vysya Bank 0.4 - 1.3

Jammu & Kashmir Bank 4.0 0.04 1.5

Karnataka Bank 2.3 - 2.1

Karur Vysya Bank 8.5 - 2.7

Kotak Mahindra Bank 0.6 0.4 1.1

Lakshmi Vilas Bank 3.9 - 0.4

Oriental Bank of Commerce 1.9 0.02 4.7

Punjab National Bank 14.0 0.1 23.7

Ratnakar Bank 0.2 - 0.1

State Bank of India 129.9 2.8 127.2

South Indian Bank 0.6 - 3.0

Standard Chartered Bank 0.2 1.2 0.7

Syndicate Bank 1.1 0.1 6.0

Union Bank of India 2.7 0.1 11.2

Vijaya Bank 1.6 0.1 3.0

Yes Bank 7.4 - 0.5

Source: Reported RBI figures as of November 2013

12

For more details contact:

Prateek Sanghi

DGM, Business and Strategy Development

ATOS WORLDLINE INDIA PVT. LTD. 701, INTERFACE 11, MALAD WEST,

MUMBAI 400 064, INDIA

Tel: + 91 (22) 4042 4000 +91 98199 70983

Website: in. worldline.com Email: [email protected]