Embed Size (px)

Citation preview

1

Index Insurance: Financial Innovations for

Agricultural Risk Management and Development

Sommarat Chantarat

Arndt-Corden Department of Economics

Australian National University

PSEKP Seminar Series, Gadjah Mada University

30 January 2012

Correspondence should be addressed to [email protected]

2 Correspondence should be addressed to [email protected]

Outline of my talk

Motivations

Development and implement index insurance program

Satellite based livestock insurance in Kenya

Prospects for Indonesia: Interesting research questions

3 Correspondence should be addressed to [email protected]

Insurance and Development

Economic costs of uninsured (weather and natural disaster) risk,

especially w/ threshold-based poverty traps

Insurance protect rural livelihoods and escape poverty

• Provide safety net to prevent collapse

of vulnerable populations

• Encourage investment and asset

accumulation by the poor

• Induce financial deepening by crowding

in credit market and social insurance

Insurance pre-finance effective

emergency response and recovery

• Timely response enhances resilience

to shocks and reduce costs of

humanitarian responses/social protection programs

Motivations Index Insurance Kenya Experience Prospects for Indonesia

4 Correspondence should be addressed to [email protected]

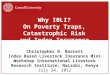

Insurance and Agricultural Risk Management 0

24

68

Density

0 .1 .2 .3 .4Kargi

kernel = epanechnikov, bandwidth = 0.0290

Kernel density estimate

Density

𝐿𝑇 𝐿∗

High frequency/ Low loss/ Idiosyncratic

Self and informal insurance effective

Low frequency/ Extreme loss/ Covariate

Need to transfer to formal risk market

Agricultural Livelihood/Income/Asset Loss

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Two types of formal agricultural insurance

Conventional crop insurance

Compensate actual loss, multi-peril or

named coverage

• High costs of verifying losses

• Moral hazard and adverse selection

• Existing programs are very costly

and largely subsidized

No successful crop insurance in the

world, not likely work in rural areas

Index insurance

Compensate specific loss based on

objectively measured index NOT actual loss

• Low costs – no farm-level loss verification

• Low incentive problems – insured cannot

influence payout probability

• Challenges in minimizing basis risk

Promise as a market viable instruments,

more suitable for rural areas in DCs

5

Developing Index Insurance Program

L*

Πlt 𝐿 𝜃𝑙𝑡 | 𝐿∗

Indem

nity P

ayout

𝐿 𝜃𝑙𝑡

1. Identify loss to be insured (𝑳𝒍𝒕)

• Identify uninsured loss by testing simple consumption risk sharing hypothesis

(e.g., Townsend 1994), 𝐿𝑙𝑡 is uninsured if 𝐻0: 𝑐 = 0 is rejected

∆𝐶𝑙𝑡= 𝑎0 + 𝑎𝑙 + 𝑎𝑡 + 𝑏𝑋𝑙𝑡 + 𝑐𝐿𝑙𝑡 + 휀𝑙𝑡

2. Select objectively measured index (𝜽𝒍𝒕)

• Highly correlated with loss, available reliably in near-real time, non-manipulable

by insured parties, high spatial distribution, at least 20 years historical profiles

3. Quantify insurable loss from index (𝑳 𝜽𝒍𝒕 )

• 𝜃𝑙𝑡 needs to explain most of the loss variations:

𝐿𝑙𝑡 = 𝐿 𝜃𝑙𝑡 + 휀𝑙𝑡 𝐿 𝜃𝑙𝑡

• Use micro data of 𝐿𝑙𝑡 to minimize basis risk

4. Identify optimal contract structure

• Payoff based on 𝐿 𝜃𝑙𝑡 : Πlt 𝐿 𝜃𝑙𝑡 | 𝐿∗ = 𝑚𝑎𝑥 𝐿 𝜃𝑙𝑡 − 𝐿∗, 0 × 𝑠𝑢𝑚 𝑖𝑛𝑠𝑢𝑟𝑒𝑑

• Stand-alone contract, group-based contract, interlinked insurance-loan

Motivations Index Insurance Kenya Experience Prospects for Indonesia

6

Developing Index Insurance Program

5. Actuarial pricing

• Actuarial fair premium: burn rate and/or Monte Carlo simulation based on 𝑓(𝜃𝑙𝑡)

𝑝𝑙 𝐿 𝜃𝑙𝑡 | 𝐿∗ = 𝐸 Πlt 𝐿 𝜃𝑙𝑡 | 𝐿∗ = Πlt 𝐿 𝜃𝑙𝑡 | 𝐿∗ 𝑑𝑓( 𝜃𝑙𝑡)

6. Ex-ante contract evaluation

• Simulated welfare and behavior response impacts using dynamic model/data

• Field experiments to elicit willingness to pay among targeted clients

7. Develop education and extension tools for pilot sale

• Simplified products, financial educational tools, targeted learning network

8. Identify cost effective delivery mechanisms

• Delivery through mobile technology, local financial institutions, network groups

9. Long-term micro-level impact assessment

• Randomized survey and experiments to elicit demand, impacts on welfare,

induced behavior responses from control and treatment groups

Motivations Index Insurance Kenya Experience Prospects for Indonesia

7

Satellite vegetation based livestock insurance in Kenya

(1) Identify loss to be insured: Catastrophic livestock losses from

drought as key uninsured risk in this area

• Observed household welfare co-move with

livestock losses Marsabit

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Seasonal Livestock Loss (%)

Balesa

Maikona

Kalacha

Northhorr

Karare

Korr

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Average Household Consumption ($/day)Maikona

Kalacha

Northhorr

Karare

Korr

Logologo

Ngurunit

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

8

Satellite vegetation based livestock insurance in Kenya

(2) Selecting index: NASA

MODIS Normalized difference

vegetation index (NDVI) as index

• Indication of availability of

vegetation over rangeland

• Spatiotemporal rich (1×1 km2)

• Available in near-real time every

15 day (1982-present)

0

0.2

0.4

0.6

0.8

1

1981

1982

1983

1984

1985

1986

1987

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2009

2010

NDVI (1981-2010) - Lower Marsabit

Karare

Logologo

Ngurunit

Korr

-3

-2

-1

0

1

2

3

4

5

1981

1982

1983

1984

1985

1986

1987

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2009

2010

ZNDVI (1982-2009) - Lower Marsabit

Karare

Logologo

Ngurunit

Korr

1984 1987 1991 1994 1997 2000 2006 2009

Historical

Droughts

ZNDVI (1981-2010) – Lower Marsabit

NDVI (1981-2010) – Lower Marsabit

Normal year (May 2007) Drought year (May 2009)

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

9

Oct Nov Dec Jan Feb Mar Apr May June July Aug Sep

(3) Quantify insurable loss from index: construct predicted livestock loss

from the empirical model: 𝑀𝑙𝑡 = 𝑀 𝑍𝑁𝐷𝑉𝐼𝑙𝑡 + 휀𝑙𝑡

Satellite vegetation based livestock insurance in Kenya

𝑍𝑁𝐷𝑉𝐼𝑙𝑡

𝐶𝑢𝑚𝑢𝑙𝑎𝑡𝑖𝑣𝑒𝑍𝑁𝐷𝑉𝐼𝑙𝑡

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

10

Oct Nov Dec Jan Feb Mar Apr May June July Aug Sep

(3) Quantify insurable loss from index: construct predicted livestock loss

from the empirical model: 𝑀𝑙𝑡 = 𝑀 𝑍𝑁𝐷𝑉𝐼𝑙𝑡 + 휀𝑙𝑡

Satellite vegetation based livestock insurance in Kenya

spreTd

dss zndvipreCzndvi_

sposTd

dss zndviposCzndvi_

spreTd

dss zndvipreCzndvi_

Construct

𝑋 𝑛𝑑𝑣𝑖𝑙𝑠 variables

from cum. ZNDVI

process

𝑍𝑁𝐷𝑉𝐼𝑙𝑡

𝐶𝑢𝑚𝑢𝑙𝑎𝑡𝑖𝑣𝑒𝑍𝑁𝐷𝑉𝐼𝑙𝑡

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

sposTd

dss zndviposCzndvi_

11

Oct Nov Dec Jan Feb Mar Apr May June July Aug Sep

(3) Quantify insurable loss from index: construct predicted livestock loss

from the empirical model: 𝑀𝑙𝑡 = 𝑀 𝑍𝑁𝐷𝑉𝐼𝑙𝑡 + 휀𝑙𝑡

Satellite vegetation based livestock insurance in Kenya

𝑍𝑁𝐷𝑉𝐼𝑙𝑡

𝐶𝑢𝑚𝑢𝑙𝑎𝑡𝑖𝑣𝑒𝑍𝑁𝐷𝑉𝐼𝑙𝑡

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

Regime switching model for zone-specific, seasonal mortality prediction:

𝑀𝑙𝑡 = 𝑀1 𝑋 𝑛𝑑𝑣𝑖𝑙𝑡 + 휀1𝑙𝑡 𝑖𝑓 𝐶𝑧𝑛𝑑𝑣𝑖_𝑝𝑜𝑠𝑙𝑡 ≥ 𝛾 (𝑔𝑜𝑜𝑑 𝑐𝑙𝑖𝑚𝑎𝑡𝑒 𝑟𝑒𝑔𝑖𝑚𝑒)

𝑀2 𝑋 𝑛𝑑𝑣𝑖𝑙𝑡 + 휀2𝑙𝑡 𝑖𝑓 𝐶𝑧𝑛𝑑𝑣𝑖_𝑝𝑜𝑠𝑙𝑡 < 𝛾 (𝑏𝑎𝑑 𝑐𝑙𝑖𝑚𝑎𝑡𝑒 𝑟𝑒𝑔𝑖𝑚𝑒) 𝑀 𝑍𝑁𝐷𝑉𝐼𝑙𝑡

12

Satellite vegetation based livestock insurance in Kenya

(3) Quantify insurable loss from index: construct predicted livestock loss

from the empirical model: 𝑀𝑙𝑡 = 𝑀 𝑍𝑁𝐷𝑉𝐼𝑙𝑡 + 휀𝑙𝑡

Predictive Performance of predicted livestock loss, 𝑀 𝑍𝑁𝐷𝑉𝐼𝑙𝑡

• Out-of-sample prediction errors within +-10% (especially in the bad year)

• Predict historical droughts well

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

Density o

f pre

dic

ted m

ort

alit

y inde

x

13

Satellite vegetation based livestock insurance in Kenya

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

Predicted mortality index

Predicted Seasonal Mortality Index – Laisamis Contract

Predicted mortality index

(4) Identify optimal contract structure

• Insurable loss: Area average livestock loss indicated by 𝑀 𝑍𝑁𝐷𝑉𝐼𝑙𝑡

• Seasonal indemnity payment:

Πlt 𝑀 𝜃𝑙𝑡 | 𝑀∗, 𝑇𝐿𝑈, 𝑃𝑇𝐿𝑈 = 𝑚𝑎𝑥 𝑀 𝑍𝑁𝐷𝑉𝐼𝑙𝑡 − 𝑀∗, 0 × 𝑇𝐿𝑈 × 𝑃𝑇𝐿𝑈

• Coverage: Division level, annual contract (covers two seasonal payouts)

(5) Actuarial fair premium: (% of sum insured)

14

Satellite vegetation based livestock insurance in Kenya

(6) Ex-ante contract evaluation: simulations of stochastic dynamic model

based on observed household dynamic data

Pastoral production function: Herd dynamics with stochastic environment:

Household budget constraint: Household Intertemporal problem:

• In most case, insured herd SOSD uninsured herd: insurance reduces prob. of extreme loss

• Contract seems to be effective despite the existence of basis risk!

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 20 40 60 80

TLU (Beginning Herd = 15 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

IBLI Stabilizes Pathway toward Growth for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 20 40 60 80

TLU (Beginning Herd = 15 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

IBLI Impedes Asset Accumulation for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 20 40 60 80

TLU (Beginning Herd = 15 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

IBLI Stabilizes Pathway toward Growth for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 20 40 60 80

TLU (Beginning Herd = 15 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

IBLI Impedes Asset Accumulation for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 20 40 60 80

TLU (Beginning Herd = 15 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

IBLI Stabilizes Pathway toward Growth for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 20 40 60 80

TLU (Beginning Herd = 15 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

IBLI Impedes Asset Accumulation for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 20 40 60 80

TLU (Beginning Herd = 15 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

IBLI Stabilizes Pathway toward Growth for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 20 40 60 80

TLU (Beginning Herd = 15 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

IBLI Impedes Asset Accumulation for Herd Around Critical Threshold

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

20 30 40 50 60 700 10 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi (Beginning Herd = 30 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Reduces Probability of Extreme Herd Loss for Very Large Herd

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bility

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bility

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 30 TLU, Beta = 1)

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bili

ty

20 30 40 50 60 700 10 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi (Beginning Herd = 30 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Reduces Probability of Extreme Herd Loss for Very Large Herd

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bility

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cu

mula

tive

Pro

ba

bility

0 20 40 60 80Herd (TLU)

No Insurance 10% IBLI

15% IBLI

Kargi ( Beginning herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 20 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

IBLI Eliminates Probability of Falling into Destitution for Herd Around Critical Threshold

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 30 TLU, Beta = 1)

0.2

.4.6

.81

Cum

ula

tive P

rob

ab

ility

0 2345 20 40 60 801

TLU (Beginning Herd = 5 TLU, Beta = 1)

No Insurance 10% IBLI

15% IBLI

Minimal IBLI Performance for Very Small Herd

TLU (Beginning Herd = 30 TLU, Beta = 1)

Motivations Index Insurance Kenya Experience Prospects for Indonesia

15

Satellite vegetation based livestock insurance in Kenya

(6) Ex-ante contract evaluation: Willingness to pay experiments (210 hhs)

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

5%

6%

7%

8%

9%

Pre

miu

m (

% o

f in

su

red

va

lue)

0% 25% 50% 75% 100%

Chosen Coverage (% of household's total herd)

All sample (E = 1.75) Poor group (E=1.77)

Vulnerable group (E = 1.91) Rich group (E = 1.60)

0.0

1.0

2.0

3

Herd

siz

e d

ensity

.5

1

1.5

2

2.5

3

Pri

ce E

lasticity o

f In

su

ran

ce D

em

and

0 10 20 30 40 50 60 70 80

Herd size (TLU)

95% CIlpoly smooth

density: herdtlu

Premium Vs. Chosen Insurance Coverage Price Elasticity of Insurance Demand Vs. Herd Size

Demand determinants

(+) familiarity with fn. product

(+) with interacting financial

experience with risk aversion

(+) perceived loss profile

(+) expected loss

(+) wealth (wealth eff.)

(-) perceived basis risk

(+) credit constraint (buffer stock)

Premium Vs. Chosen Coverage

Modest demand exists at 20%+fair

Less elastic among the rich

16

Satellite vegetation based livestock insurance in Kenya

(7) Develop education and extension tools: using experimental games

with real incentives

• Replicate the pastoral livelihood in the community

• Teach how this insurance work and how it will affect herd dynamics

• The game also allows us to study hh’s behavior responses from insurance!

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

17

Satellite vegetation based livestock insurance in Kenya

(8) Identify cost effective delivery mechanisms to remote clients using

mobile technology

• The contract has been commercialized in northern Kenya since 2010

• Contracts sold to among 10% of populations in the first year

• Local insurance company underwrites the contract with Swiss Re

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Correspondence should be addressed to [email protected]

18

Satellite vegetation based livestock insurance in Kenya

• 4-year panel household survey, baseline (2009) with annual repeat

• Challenges: (i) cannot randomize eligibility for insurance

(ii) low uptake reduces power of estimating avg. treatment effects

• Hence quasi-experiment with encouragement design: use IV approach

with multiple instruments (to generate variation in insurance purchase)

• We randomize 3 instruments:

• Survey instruments: welfare, Induced behavior responses, formal/informal

access to credit, social insurance, environmental impacts

• Empirical estimations of demand determinants and impacts of insurance:

𝐹𝑖𝑟𝑠𝑡 𝑠𝑡𝑎𝑔𝑒: 𝐷𝑖𝑡= 𝛾0 + 𝛾1𝑒𝑖𝑡 + 𝛾2𝑡𝑖𝑡 + 𝛾3𝑑𝑖𝑡 + 휀𝑖𝑡

𝑆𝑒𝑐𝑜𝑛𝑑 𝑠𝑡𝑎𝑔𝑒: ∆𝑌𝑖𝑡= 𝜌0 + 𝜌1𝐷𝑖𝑡 + 𝜌2′𝑋𝑖𝑡 + 𝐷𝑖𝑡𝑋𝑖𝑡′𝜌3 + 𝛿𝑖 + 휀𝑖𝑡

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Cash transfer No cash transfer

Educated 4 sites 4 sites

Not educated 4 sites 4 control sites

(1) Insurance education (𝑒𝑖𝑡) (2) Eligibility for cash transfer (𝑡𝑖𝑡) (3) Discount coupon at 0-60% (𝑑𝑖𝑡)

(9) Long-term micro-level impact assessment

Stay tuned!

19

References

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Barrett, C.B. et al. (2008) “Altering Poverty Dynamics with Index Insurance,”

BASIS Brief 2008-08.

Barrett, C.B. and M.R. Carter (2007) “Asset Thresholds and Social Protection,”

IDS Bulletin 38(3):34-38.

Carter, M.R. et al. (2008). “Insuring the Never-before Insured: Explaining Index

Insurance through Financial Education Games,” BASIS Brief 2008-07.

Chantarat, S. et al. (forthcoming) “Designing Index-based Livestock Insurance for

Managing Asset Risk in Northern Kenya.” Journal of Risk and Insurance

Chantarat, S. et al. (2011) “The Performance of Index-based Livestock Insurance:

Ex Ante Assessment in the Presence of a Poverty Trap.” Mimeo

Chantarat, S. et al. (2011) “Willingness to Pay for Index-based Livestock

Insurance: Results from a Field Experiment.” Mimeo

IBLI official site: http://livestockinsurance.wordpress.com/

20

Prospects for Index Insurance in Indonesia

Motivations Index Insurance Kenya Experience Prospects for Indonesia

Interesting research questions

• The optimal contract design as part of existing risk management system

(complementarities with self-, informal-insurance, government programs)

• Impact assessment on welfare, productive investments, existing risk

management mechanisms

• Designs of financial educational tools

• Viability of flood index insurance (e.g., using satellite imagery?) as part of

overall flood management system