Embed Size (px)

Citation preview

Alan Stein & Suzan HeatlyOphir Energy Company Limited

Independents in Deepwater Africa

APPEX ConferenceLondon, 20 – 22 March 2007

Independents?

Majors: Vertically integrated super-sized corporations, with a focus upon selling refined product. “Gas Pumpers”.

NOCs: State and quasi-State companies. Traditionally representing the interests of host countries, but increasingly active internationally, sometimes with strategic objectives.

Independents: Focus on the exploration for and production of crude oil and natural gas. Wide range of sizes, nationalities and capabilities. Subdivided into those who produce and those who wished they produced.

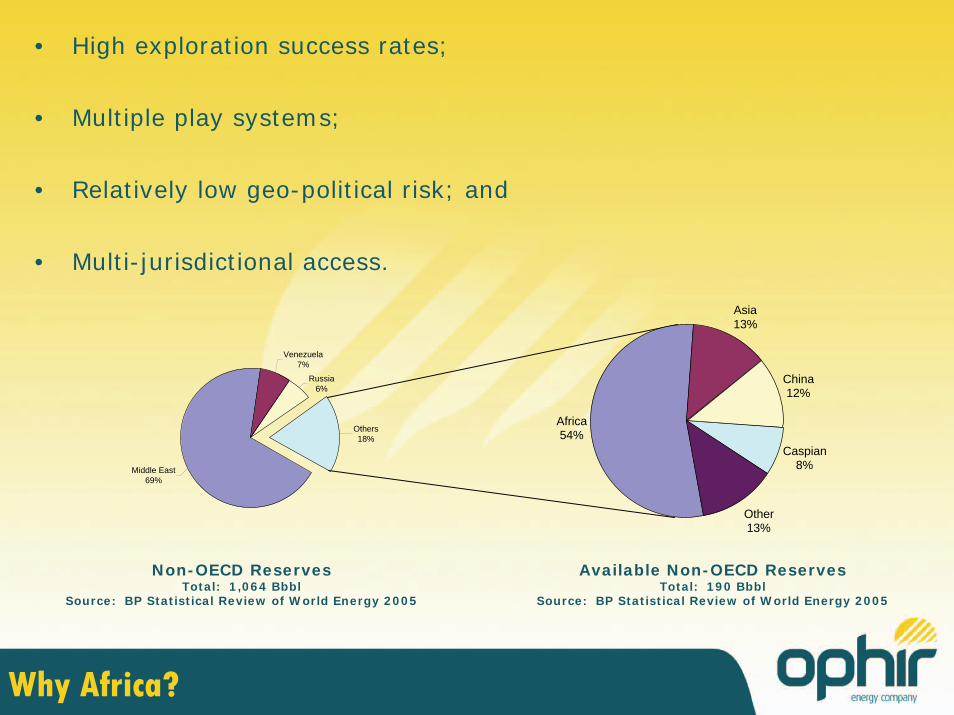

Why Africa?

• High exploration success rates;

• Multiple play systems;

• Relatively low geo-political risk; and

• Multi-jurisdictional access.

Why Africa?

Non-OECD ReservesTotal: 1,064 Bbbl

Source: BP Statistical Review of World Energy 2005

Available Non-OECD ReservesTotal: 190 Bbbl

Source: BP Statistical Review of World Energy 2005

Venezuela7%

Russia6%

Middle East69%

Others18%

Africa54%

Asia13%

China12%

Caspian8%

Other13%

World Exploration Potential

Source: Global Pacific & Partners, Africa Upstream 2006

Why Deepwater Africa?

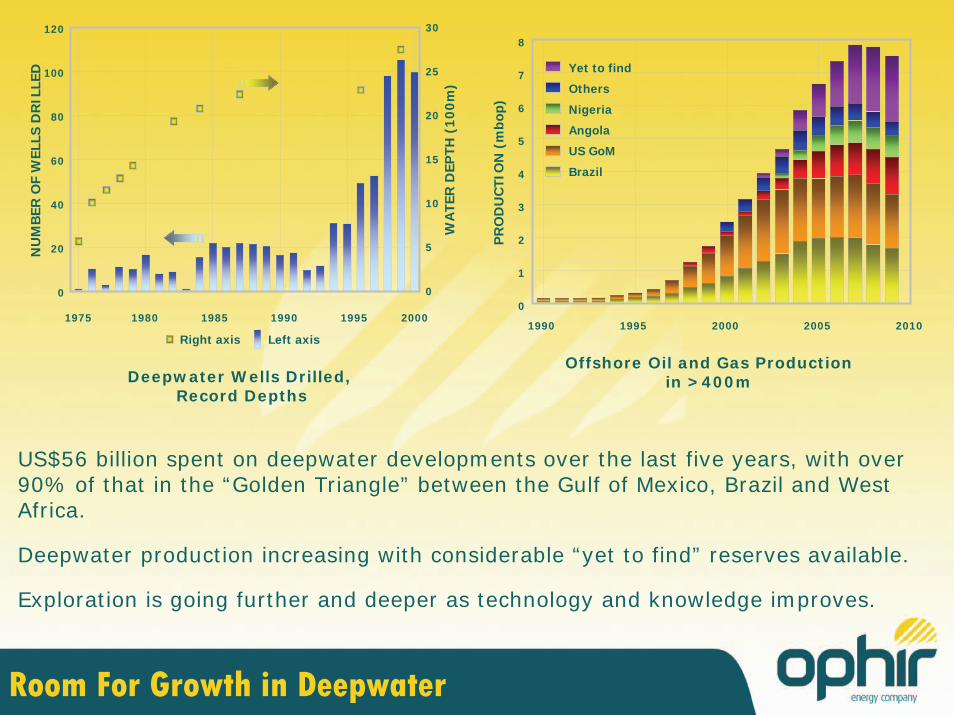

US$56 billion spent on deepwater developments over the last five years, with over 90% of that in the “Golden Triangle” between the Gulf of Mexico, Brazil and West Africa.

Deepwater production increasing with considerable “yet to find” reserves available.

Exploration is going further and deeper as technology and knowledge improves.

NU

MB

ER O

F W

ELLS

DR

ILLE

D

1975 200019851980 19951990

WA

TER

DEP

TH (

100m

)

Right axis Left axis

120

20

100

80

60

40

0

30

5

25

20

15

10

0

PR

OD

UC

TIO

N (

mbo

p)

Deepwater Wells Drilled, Record Depths

Offshore Oil and Gas Productionin >400m

2010200019951990 2005

Yet to find

Others

Nigeria

Angola

US GoM

Brazil

8

7

1

6

5

4

3

2

0

Room For Growth in Deepwater

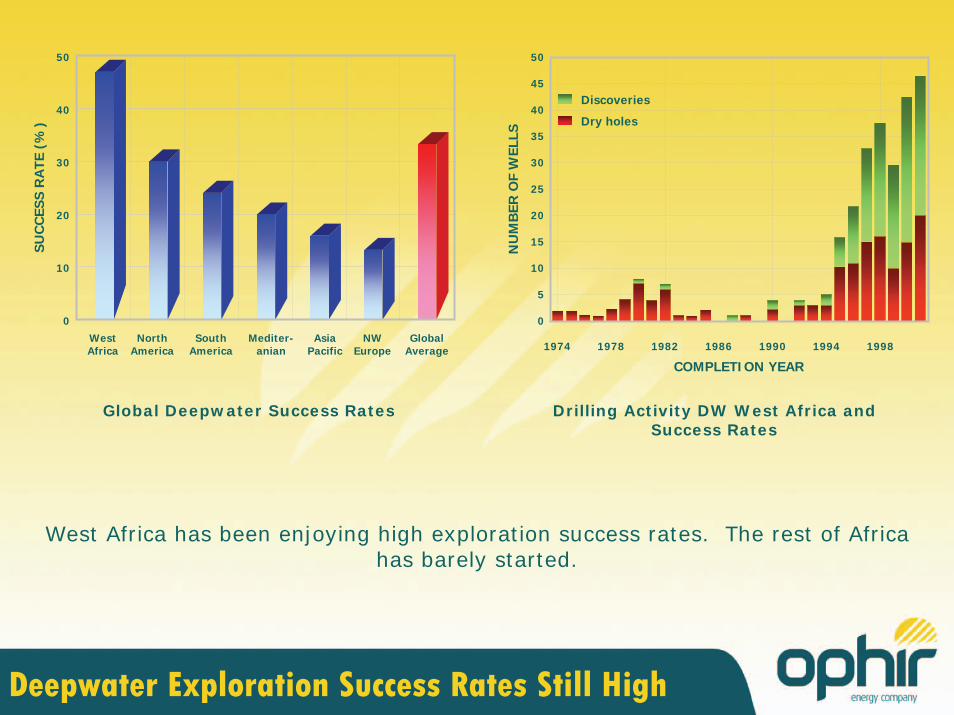

Deepwater Exploration Success Rates Still High

West Africa has been enjoying high exploration success rates. The rest of Africa has barely started.

Global Deepwater Success Rates Drilling Activity DW West Africa andSuccess Rates

NU

MB

ER O

F W

ELLS

1982 1990 19981994198619781974

COMPLETION YEAR

Discoveries

Dry holes

50

45

15

40

35

30

25

20

0

10

5

WestAfrica

SUC

CES

S R

ATE

(%

)

Global Average

SouthAmerica

NorthAmerica

AsiaPacific

Mediter-anian

NWEurope

50

40

30

20

10

0

3D Seismic

A risk reduction toolenabling independents to compete in deepwater.

Image courtesy of PGS Exploration Ltd

Source: Internet

Thousand Barrels/day

>2,000501-2,000101-50011-100Not significant/unavailable

OIL IMPORTS

Oil trade flow

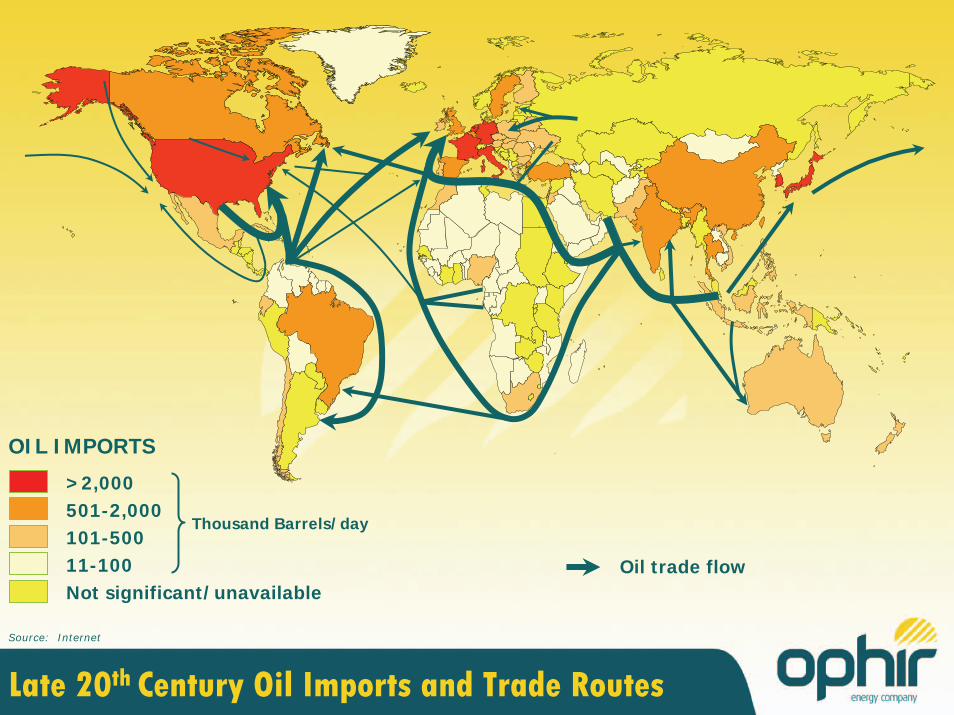

Late 20th Century Oil Imports and Trade Routes

Potential strategic bottlenecks

Oil trade flow

Anticipated oil trade flow

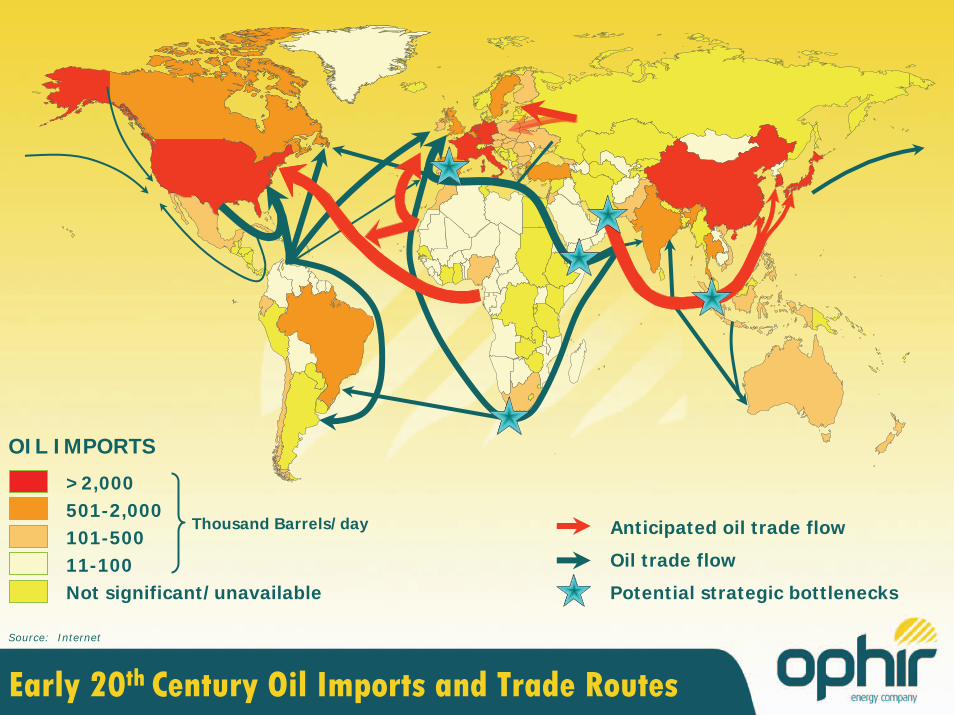

Early 20th Century Oil Imports and Trade Routes

Source: Internet

Thousand Barrels/day

>2,000501-2,000101-50011-100Not significant/unavailable

OIL IMPORTS

The role of Independents

Leaders or Followers?

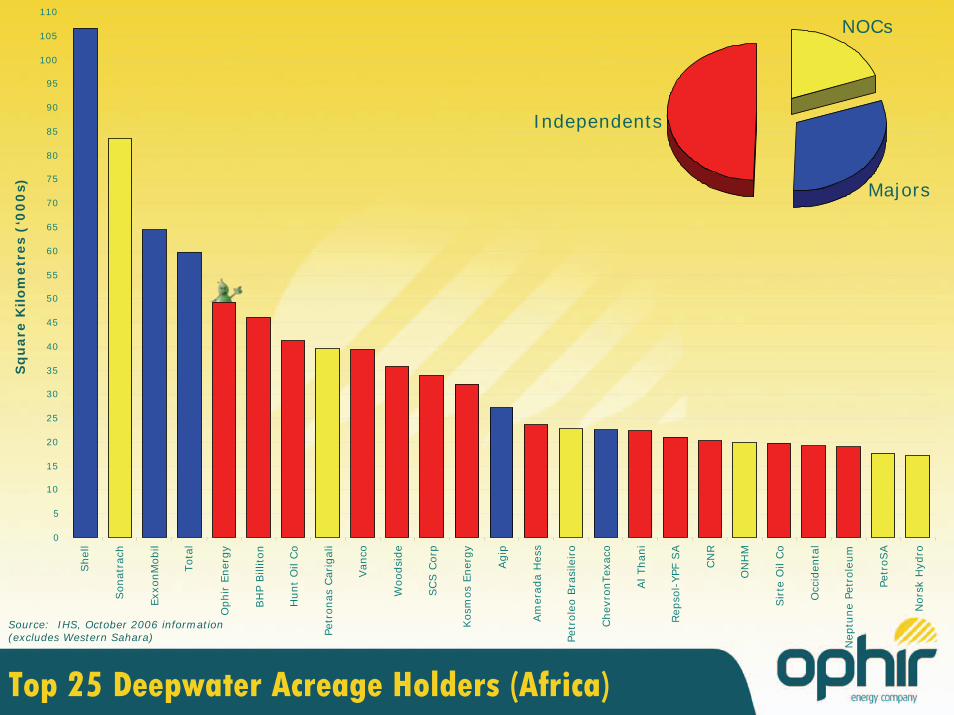

Top 25 Deepwater Acreage Holders (Africa)

Source: IHS, October 2006 information(excludes Western Sahara)

Sq

uare

Kilo

metr

es

(‘0

00

s)

Shel

l

Sonat

rach

Exx

onM

obil

Tota

l

Ophir

Ener

gy

BH

P B

illiton

Hunt

Oil

Co

Petr

onas

Car

igal

i

Van

co

Woodsi

de

SC

S C

orp

Kosm

os

Ener

gy

Agip

Am

erad

a H

ess

Petr

ole

o B

rasi

leiro

Chev

ronTex

aco

Al Than

i

Rep

sol-

YPF

SA

CN

R

ON

HM

Sirte

Oil

Co

Occ

iden

tal

Nep

tune

Petr

ole

um

Petr

oSA

Nors

k H

ydro

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

105

110

NOCs

Majors

Independents

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

32

34

36

38

40

42

44

46

48

BH

P B

illiton

Hunt

Oil

Van

co E

ner

gy

Hyp

erdyn

amic

s

Ophir

Ener

gy

Al Than

i

Dev

on E

ner

gy

Can

adia

n N

atura

l Res

ourc

es

Tow

er R

esourc

es

Enig

ma

Woodsi

de

Gre

endal

e

Sonangol

TO

TAL

SA

The

Atlas

Gro

up

Petr

oSA

Petr

obra

s

ON

HM

Dan

a Pe

trole

um

Exx

onM

obil

Occ

iden

tal Pe

trole

um

Eni SpA

Rep

sol-

YPF

SA

Roya

l D

utc

h S

hel

l

Petr

onas

Sq

uare

Kilo

metr

es

(‘0

00

s)

Top 25 Deepwater Acreage Holders (West Africa)Source: IHS, October 2006 information

NOCs

Majors

Independents

Wells Drilled – NFWs West Africa Deepwater (1980 to 2006)

Source: IHS, October 2006 information

02468

1012141618202224262830323436384042444648505254565860626466

Ker

r M

cGee

02468

1012141618202224262830323436384042444648505254565860626466

Tota

l

Exx

on

BP

Chev

ronTex

aco

Shel

l

Agip

Soek

or

(Pty

) Lt

d

Woodsi

de

Am

erad

a H

ess

CN

R I

nt'l

Conoco

Phill

ips

Oce

an

South

Atlantic

Fore

st E

xplo

ration

Sta

toil

Murp

hy

Occ

iden

tal

Dan

a Pe

trole

um

Hunt

Oil

Sonangol

BH

P P

etro

leum

Dev

on E

ner

gy

Nors

k H

ydro

ASA

Alli

ed E

ner

gy

Bra

soil

Fam

fa O

il Lt

d

Nex

en P

etro

leum

Nore

ast

Petr

ole

um

Van

co E

ner

gy

Zeb

bra

Ener

gy

Ltd

Addax

Pet

role

um

Anad

arko

Atlas

Pet

role

um

British

Gas

Eag

le E

ner

gy

His

pan

ica

Mar

athon P

etro

leum

Nuev

o

Pere

nco

Oil

& G

as

Sas

ol Lt

d

NOCs

Majors

Independents

Nu

mb

er

of

Wells

Dri

lled

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

32

34

36

38

40

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Nu

mb

er

of

Wells

Dri

lled

YearSource: IHS, October 2006 information

NOCs

Majors

Independents

Wells Drilled – NFWs West Africa Deepwater (1980 to 2006)

0

20,000,00040,000,00060,000,00080,000,000

100,000,000120,000,000140,000,000160,000,000180,000,000200,000,000220,000,000240,000,000260,000,000280,000,000300,000,000320,000,000340,000,000360,000,000380,000,000400,000,000420,000,000440,000,000460,000,000480,000,000500,000,000520,000,000540,000,000560,000,000

Exx

onM

obil

TO

TAL

SA

BP p

lc

Dev

on E

ner

gy

Eni SpA

Chev

ron

Sta

toil

Hes

s

Nors

k H

ydro

SN

PC

GEPe

trol

Sonangol

Roya

l D

utc

h S

hel

l

Tullo

w

Woodsi

de

Gove

rnm

ent

of

Port

ugal

Cort

icei

ra A

morim

GALP

Har

dm

an

Soc

Mauri

tanie

nne

des

Hyd

roca

rbure

s

BG

Gro

up

Pre

mie

r O

il

Gru

po I

ber

dro

la

Roc

Oil

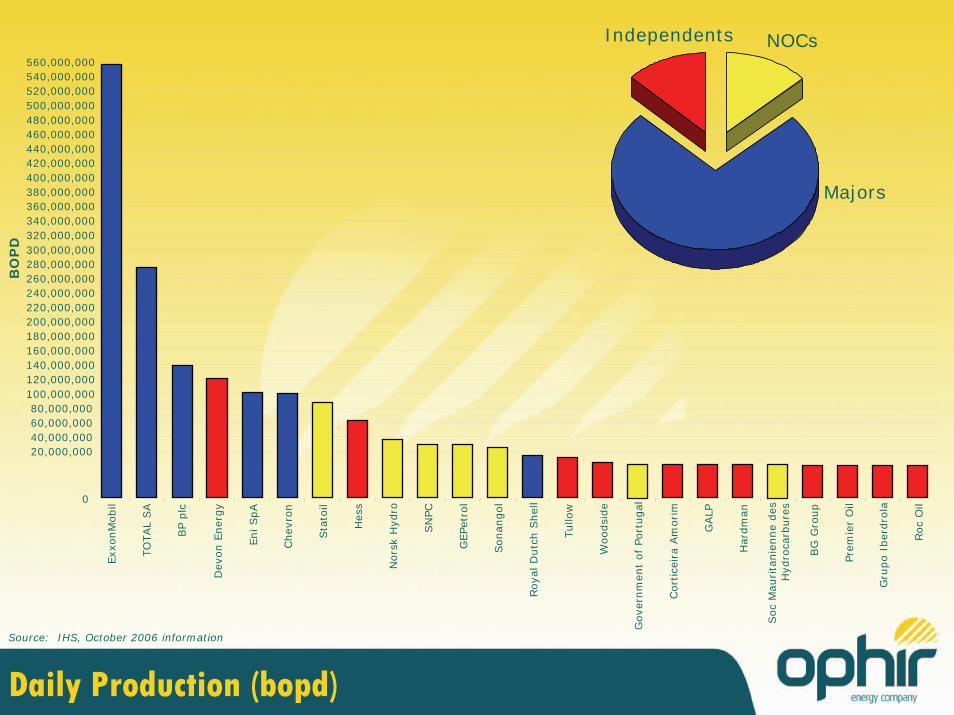

Daily Production (bopd)

NOCs

Majors

Independents

Source: IHS, October 2006 information

BO

PD

Where have all the

explorers gone?

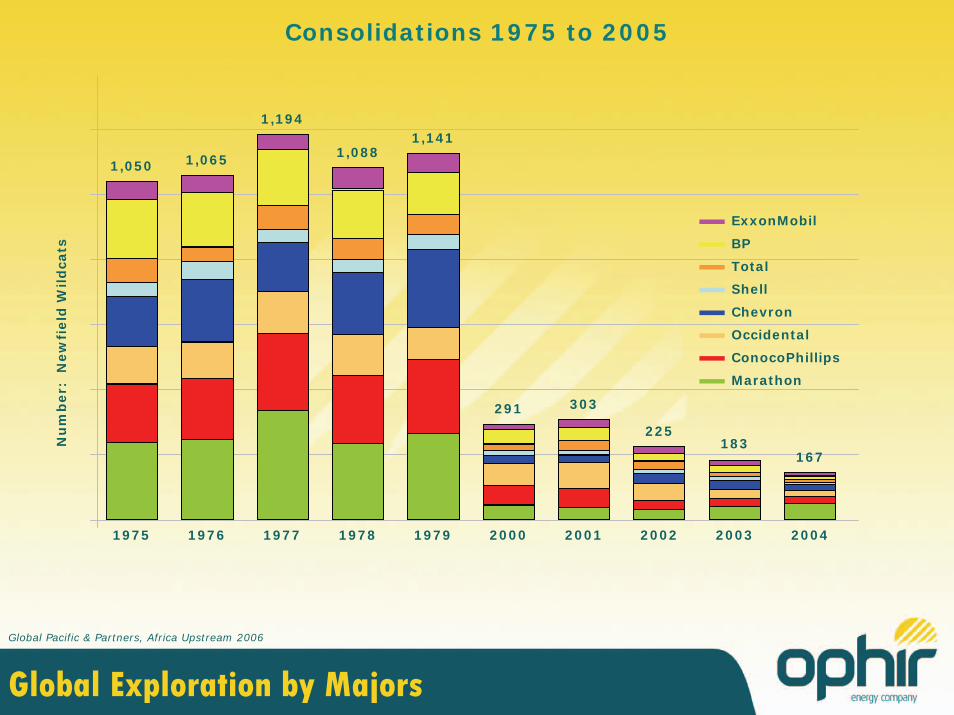

Global Exploration by Majors

Consolidations 1975 to 2005

ExxonMobil

BP

Total

Shell

Chevron

Occidental

ConocoPhillips

Marathon

1975 1976 1977 1978 1979

1,050 1,065

1,194

1,0881,141

Nu

mb

er:

N

ew

field

Wild

cats

Global Pacific & Partners, Africa Upstream 2006

2000

291

2001

303

2002

225

2003

183

2004

167

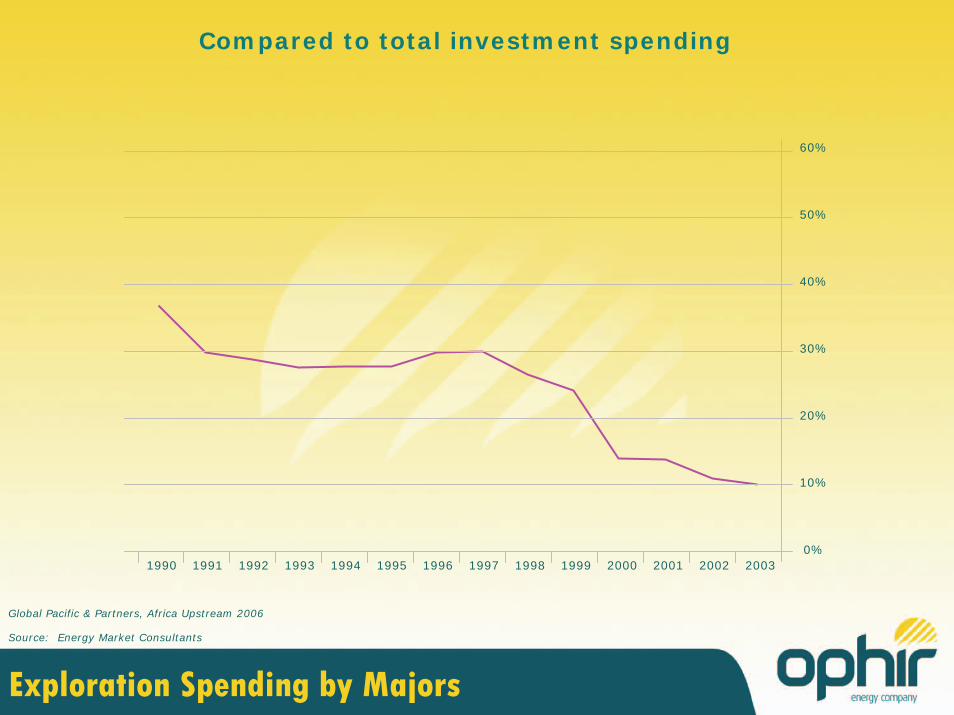

Exploration Spending by Majors

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

60%

50%

40%

30%

20%

10%

0%

Compared to total investment spending

Source: Energy Market Consultants

Global Pacific & Partners, Africa Upstream 2006

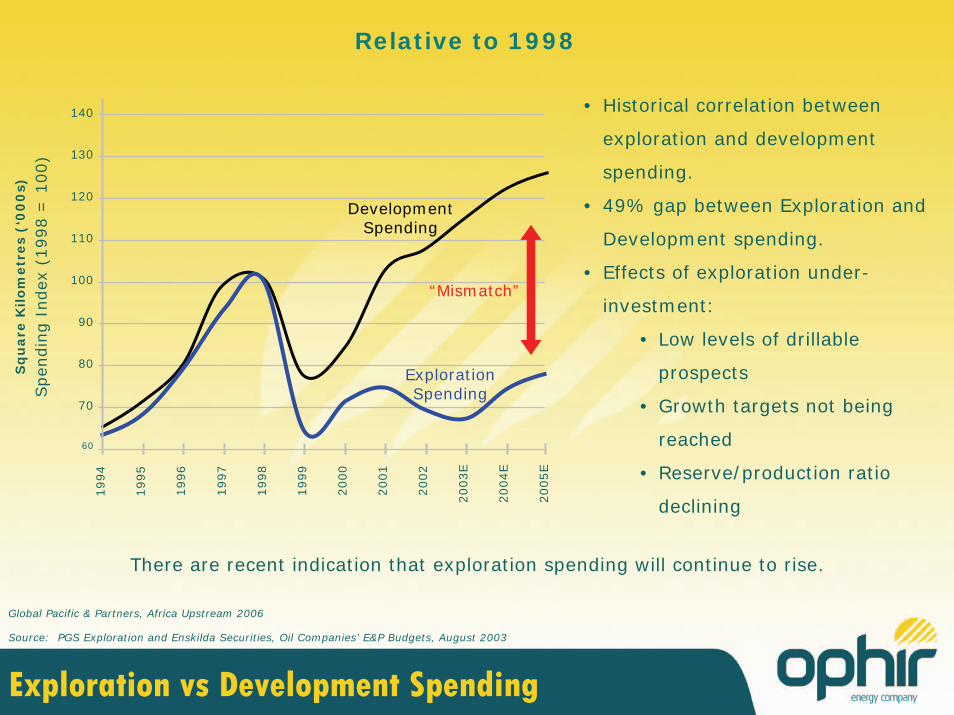

Exploration vs Development SpendingSource: PGS Exploration and Enskilda Securities, Oil Companies’ E&P Budgets, August 2003

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003E

2004E

2005E

140

130

120

100

80

70

60

110

90

Development Spending

Exploration Spending

“Mismatch”

Spen

din

g I

ndex

(1998 =

100)

• Historical correlation between

exploration and development

spending.

• 49% gap between Exploration and

Development spending.

• Effects of exploration under-

investment:

• Low levels of drillable

prospects

• Growth targets not being

reached

• Reserve/production ratio

declining

Sq

uare

Kilo

metr

es

(‘0

00

s)

There are recent indication that exploration spending will continue to rise.

Relative to 1998

Global Pacific & Partners, Africa Upstream 2006

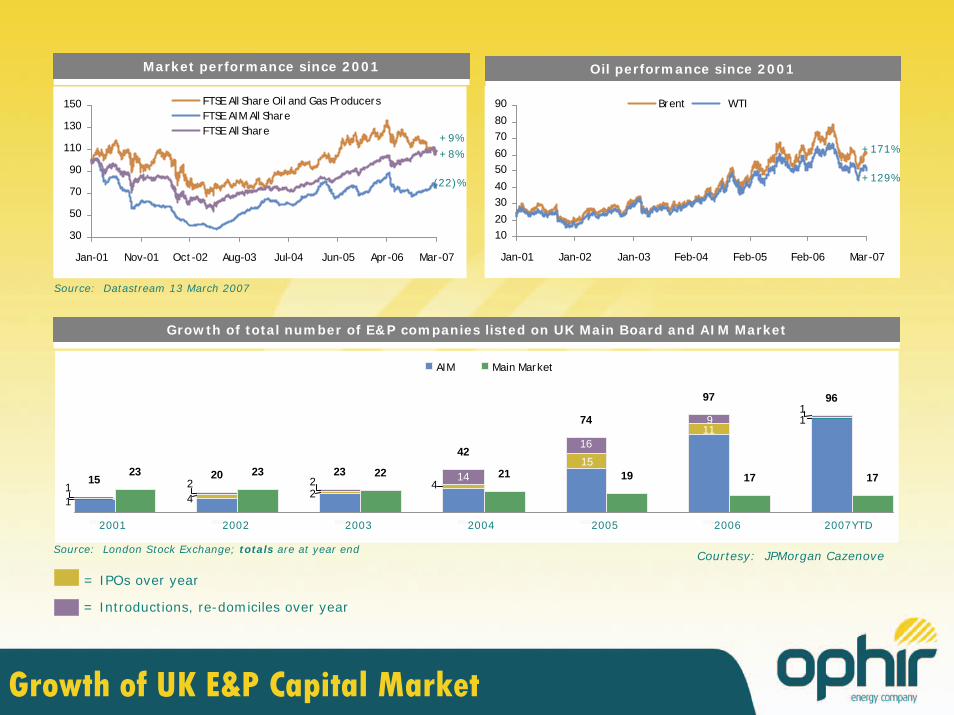

Oil price is up

Investors are back

but……………

Growth of UK E&P Capital Market

Source: Datastream 13 March 2007

Market performance since 2001Market performance since 2001

1523 20 23 23 22

42

21

74

19

97

17

96

17

111

15

421

4

9

16

1

1422

1

2001 2002 2003 2004 2005 2006 2007YT D

AIM Main Market

Growth of total number of E&P companies listed on UK Main Board and AIM MarketGrowth of total number of E&P companies listed on UK Main Board and AIM Market

Source: London Stock Exchange; totals are at year end

30

50

70

90

110

130

150

Jan-01 Nov-01 Oct-02 Aug-03 Jul-04 Jun-05 Apr-06 Mar-07

FTSE All Share Oil and Gas Producers FTSE AIM All Share FTSE All Share

1020

3040

5060

7080

90

Jan-01 Jan-02 Jan-03 Feb-04 Feb-05 Feb-06 Mar-07

Brent WTI

Oil performance since 2001Oil performance since 2001

+8%

+9%

(22)%

+171%

+129%

2001 2002 2003 2004 2005 2006 2007YTD

= IPOs over year

= Introductions, re-domiciles over year

Courtesy: JPMorgan Cazenove

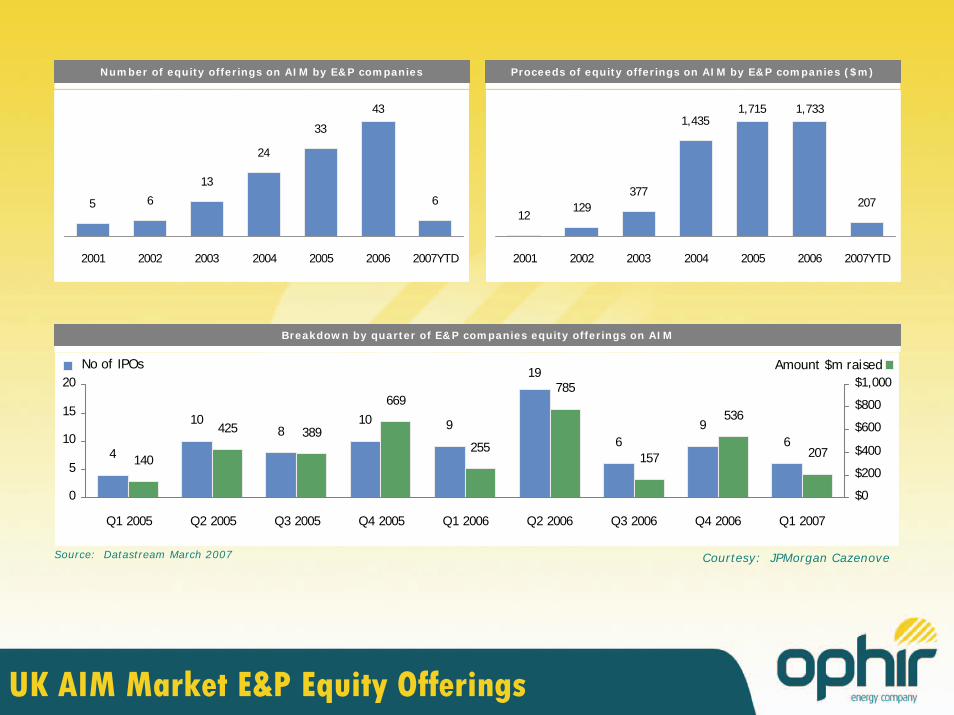

UK AIM Market E&P Equity Offerings

5 6

13

24

33

43

6

2001 2002 2003 2004 2005 2006 2007YTD

Number of equity offerings on AIM by E&P companiesNumber of equity offerings on AIM by E&P companies

Proceeds of equity offerings on AIM by E&P companies ($m)Proceeds of equity offerings on AIM by E&P companies ($m)

12129

377

1,4351,715 1,733

207

2001 2002 2003 2004 2005 2006 2007YTD

Breakdown by quarter of E&P companies equity offerings on AIMBreakdown by quarter of E&P companies equity offerings on AIM

Source: Datastream March 2007

4

108

10 9

19

69

6140

425 389

669

255

785

157

536

207

0

5

10

15

20

Q1 2005 Q2 2005 Q3 2005 Q4 2005 Q1 2006 Q2 2006 Q3 2006 Q4 2006 Q1 2007

$0

$200

$400

$600

$800

$1,000No of IPOs Amount $m raised

Courtesy: JPMorgan Cazenove

• Africa is in a state of Ultra Competition.

Capital to Spend But………

• Resource war between conventional and emerging consumers.

• Asian Tigers and NOCs making a big impact.

• Resource nationalisation.

• Speculators are back (telcos and biotechs can breathe a sigh of relief).

• Is there any room left for those of us that do this for a living?

• And if that were all not bad enough………………………………

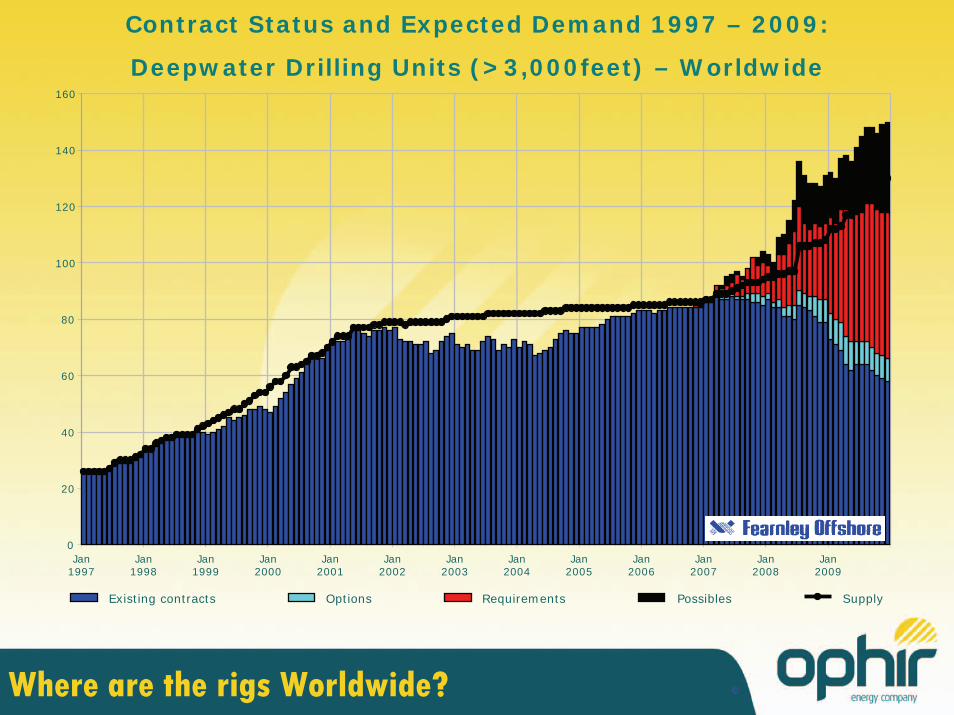

Where are the rigs Worldwide?

Contract Status and Expected Demand 1997 – 2009:

Deepwater Drilling Units (>3,000feet) – Worldwide

Existing contracts Options Requirements Possibles Supply

©

0

20

40

60

80

100

120

140

160

Jan1997

Jan1998

Jan1999

Jan2000

Jan2001

Jan2002

Jan2003

Jan2004

Jan2005

Jan2006

Jan2007

Jan2008

Jan2009

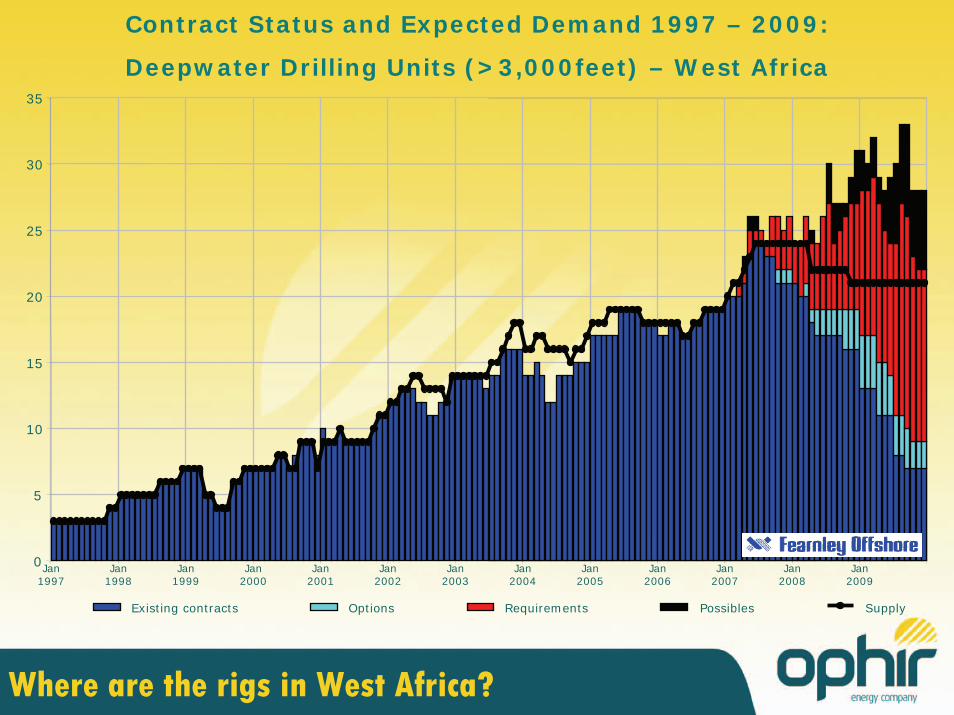

Where are the rigs in West Africa?

Contract Status and Expected Demand 1997 – 2009:

Deepwater Drilling Units (>3,000feet) – West Africa

0

5

10

15

20

25

30

35

Existing contracts Options Requirements Possibles Supply

Jan1997

Jan1998

Jan1999

Jan2000

Jan2001

Jan2002

Jan2003

Jan2004

Jan2005

Jan2006

Jan2007

Jan2008

Jan2009

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

32

34

36

38

40

42

44

46

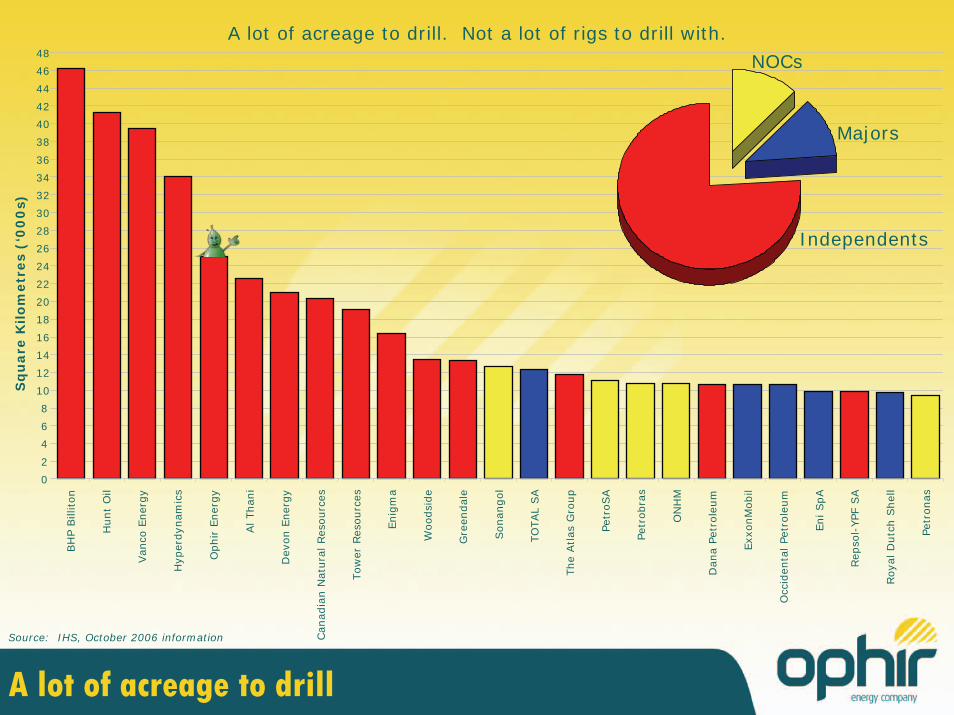

48

BH

P B

illiton

Hunt

Oil

Van

co E

ner

gy

Hyp

erdyn

amic

s

Ophir

Ener

gy

Al Than

i

Dev

on E

ner

gy

Can

adia

n N

atura

l Res

ourc

es

Tow

er R

esourc

es

Enig

ma

Woodsi

de

Gre

endal

e

Sonangol

TO

TAL

SA

The

Atlas

Gro

up

Petr

oSA

Petr

obra

s

ON

HM

Dan

a Pe

trole

um

Exx

onM

obil

Occ

iden

tal Pe

trole

um

Eni SpA

Rep

sol-

YPF

SA

Roya

l D

utc

h S

hel

l

Petr

onas

Sq

uare

Kilo

metr

es

(‘0

00

s)

NOCs

Majors

Independents

A lot of acreage to drillSource: IHS, October 2006 information

A lot of acreage to drill. Not a lot of rigs to drill with.

So how are the

Independents going to drill

all that acreage?

The Ophir Solution

• Ophir has recently entered long term rig sharing agreements.

• The agreements cover 14.5 months of rig time over the period 2008 –2011.

• Day rate in excess of US$400,000 per day.

• Significant upfront investment of capital required to secure contracts.

• Tying up capital would have been challenging had Ophir been in the public domain.

• Public markets punish lack of rig capacity.

• It was never meant to be easy but it shouldn’t really be this hard.

Artists impression of DS “West Polaris”courtesy of Seadrill.

Independents have the acreage.

Role of Independents in Deepwater Africa?

Majors have the production.

Asian Tigers are on the prowl.

NOCs are taking a bigger share.

We all need to drill more exploration wells.

Somebody else has all the rigs!

It’s all about to get very interesting.