Embed Size (px)

Citation preview

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. For full details of our professional regulation please refer to ‘Regulatory Information’ at www.kpmg.com/uk

Document Classification - KPMG Public

INDEPENDENT EXPERT REPORT

OF PHILIP TIPPIN FIA

In the matters of

ACE EUROPEAN GROUP LIMITED

AND

CHUBB INSURANCE COMPANY OF EUROPE SE

AND

CHUBB BERMUDA INTERNATIONAL INSURANCE IRELAND DESIGNATED ACTIVITY COMPANY

AND IN THE MATTER OF PART VII OF THE FINANCIAL

SERVICES AND MARKETS

ACT 2000

IN THE HIGH COURT OF JUSTICE

DATED 11 NOVEMBER 2016

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 2 of 61 11/11/2016

Document Classification - KPMG Public

Contents

1. INTRODUCTION 4

Purpose of the report 4 Independent Expert 5 Proposed Transfers 5 Scope 6 Reliances 6 Use and limitations 7 Professional guidance 8 Terminology 8

2. EXECUTIVE SUMMARY & CONCLUSIONS 9

Overview of the Transfers 9 Purpose of the Transfers 10 Key Assumptions 11 Findings 12 Expert’s declaration 14

3. BACKGROUND 15

Chubb Limited (“Chubb”) 15 ACE European Group Limited (“AEGL”) 16 Chubb Insurance Company of Europe SE (“CICE”) 17 Chubb Bermuda International Insurance Ireland Designated Activity Company (“CBII”)18 Insurance business of the Transfer Companies 19 Outwards reinsurance programmes 21 Prudential capital requirements 21 Capital management policy 22 Guarantees / risk sharing arrangements 23

4. EFFECTS OF THE TRANSFERS 24

Effect of the Transfers on group structure 24 Effect of the Transfers on Transfer Company balance sheets 26 Non-financial effect of the Transfers 28

5. POTENTIAL IMPACT OF TRANSFERS ON STAKEHOLDERS 31

Overview of analysis performed 31 Identification of policyholder groups 31 Future intentions of AEGL 33 Governance and management framework 33 Cyber-security 34 Claims and policy administration 34 Conduct risk 34 Impact of changes in regulatory regime and jurisdiction 34 Financial and economic information considered 35 Consideration of capital and risk 36 Impact of Transfers on capital available to policyholders 38 Impact on existing reinsurers 39 Pension scheme obligations 40

6. METHODOLOGY, STRESS AND SCENARIO ANALYSIS 42

Overview 42 Loss modelling approach 42

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 3 of 61 11/11/2016

Document Classification - KPMG Public

Stress test analysis 44

7. SUMMARY OF FINDINGS 47

Summary of changes in circumstances of transferring CICE policyholders 47 Summary of changes in circumstances of transferring CBII policyholders 47 Summary of changes in circumstances of existing AEGL policyholders 48

APPENDIX 1 CURRICULUM VITAE OF THE INDEPENDENT EXPERT 49

APPENDIX 2 EXTRACT FROM LETTER OF ENGAGEMENT 50

APPENDIX 3 LETTER OF REPRESENTATION 51

APPENDIX 4 LIST OF INFORMATION PROVIDED 53

APPENDIX 5 GLOSSARY OF TERMS AND DEFINITIONS 54

APPENDIX 6 LIST OF INTERVIEWS CARRIED OUT 58

APPENDIX 7 DETAILS OF PROPOSED POLICYHOLDER COMMUNICATION (SUMMARISED FROM WITNESS STATEMENTS) 59

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 4 of 61 11/11/2016

Document Classification - KPMG Public

1. Introduction

Purpose of the report

1.1 ACE Limited acquired The Chubb Corporation in January 2016 and the group is now trading as Chubb Limited (“Chubb”) and based in Switzerland. Following the acquisition it has been proposed to re-organise the European group structure. All companies involved in the transfers described in this report write solely non-life business.

The largest entity of the three companies involved is ACE European Group Limited (“AEGL”) which will be the “Transferee”. AEGL is a subsidiary of Chubb Insurance S.A/N.V and ACE European Holdings Limited as of 2 November 2016 and has branches in 20 different countries including a head office in the United Kingdom. The insurance and reinsurance business of Chubb Insurance Company of Europe SE (“CICE”) will be transferred to AEGL under the provision of Part VII of the Financial Services and Markets Act 2000 (“FSMA”) under a transfer to be approved by the High Court of Justice, England (“the UK Court”).

Chubb Bermuda International Insurance Ireland Designated Activity Company (“CBII”) will also be transferred to AEGL through a similar process to a Part VII, under a transfer to be approved by the High Court in Ireland (“the Irish Court”). This will be under the provisions of section 13 of the Assurance Companies Act 1909 of the Irish Statute Book, section 36 of the Insurance Act 1989 and the European Union (Insurance and Reinsurance) Regulations 2015.

Where I refer henceforth to CICE in this report, it will be assumed that it is the business of CICE after the Swiss business has been transferred out, unless otherwise stated. All numerical information presented with respect to CICE is also shown after the Swiss business has been transferred out, unless otherwise stated.

In addition to the UK and Irish transfers a parallel transfer to AEGL is proposed in Jersey in respect of business written by CICE in Jersey. The transfer of businesses carried on in or from within Jersey must be approved by the Royal Court of Jersey. For the avoidance of doubt, I have specifically considered the position of Jersey policyholders and my conclusions equally apply to those policyholders affected by the Jersey transfer.

The proposed transfers move the insurance and reinsurance policies and certain related contracts from CICE and CBII into AEGL. The proposed date for all the transfers to be finalised is 1 May 2017. Immediately after this it is proposed that CICE and CBII are legally merged into AEGL through a European Cross-Border Merger (“CBM”) process.

I refer to the transfers of insurance business of CICE and CBII as the “Transfers”. I refer to CICE, CBII and AEGL as the “Transfer Companies”. I refer to CICE and CBII as the “Transferring Companies”. I refer to the UK and Irish Courts as “the Courts”.

1.2 Under FSMA, a proposed transfer of (re)insurance business from one entity to another can only take place if it has been approved by the Courts for the appropriate jurisdictions. As part of the approval process a report is required from an expert (the “Independent Expert”) to aid the relevant Courts in their deliberations.

1.3 This report describes the proposed transfers and discusses their possible effects on the relevant policyholder groups, including effects on security and levels of service.

This report is organised into seven sections as follows:

Section 1 – The purpose of this report and the role of the Independent Expert

Section 2 – Executive summary and conclusions

Section 3 – Relevant background information on Chubb and each of the Transfer Companies

Section 4 – Setting out the effect of the Transfers on the Transfer Companies

Section 5 – Discussion of the potential impact of the Transfers on stakeholders

Section 6 – Consideration of the appropriateness of the information provided to me which informs my opinion, including consideration of methodologies for calculations

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 5 of 61 11/11/2016

Document Classification - KPMG Public

used in provision of data and scenarios following the Transfers taking effect that may affect policyholder security.

Section 7 - Summary of findings

Independent Expert

1.4 I, Philip Tippin, am a partner in the actuarial practice of KPMG LLP (“KPMG”). I have been a Fellow of the Institute and Faculty of Actuaries for 18 years. My detailed curriculum vitae is included in Appendix 1.

1.5 I have been appointed by AEGL to act as the Independent Expert in connection with the Transfers. My appointment has subsequently been approved by the Prudential Regulation Authority (“PRA”) on 23 March 2016. Central Bank of Ireland approval is not required; Irish regulations do not stipulate the appointment of an Independent Expert, however it is seen as best practice.

1.6 To the best of my knowledge, information and belief, I have no conflicts of interest in connection with the parties involved in the proposed Transfers and I therefore consider myself able to act as an Independent Expert on this transaction.

1.7 I can confirm that I have no financial interest in the Transfer Companies, nor do I work for any entity belonging to Chubb. Neither I, nor any of my immediate team assisting me in producing this report, have carried out any work with the Transfer Companies or any of the wider Chubb group companies over the last three years.

1.8 I can confirm that the contribution of Chubb and its subsidiaries to KPMG’s global fee income has not exceeded 0.01% over the last 3 years.

1.9 The costs and expenses associated with my appointment as Independent Expert and the production of this report will be charged to AEGL.

1.10 In reporting to the Courts on the proposed Transfers my overriding duty is to the Courts. This duty applies irrespective of any person or firm from whom I have been instructed or paid.

Proposed Transfers

1.11 The Transfer Companies are owned indirectly by Chubb, and the Transfers represent an internal reorganisation of Chubb’s UK and Ireland general insurance business.

It is proposed that the insurance and reinsurance policies of the Transferring Companies and certain related contracts will be transferred to AEGL. This is intended to take effect on 1 May 2017 (the “Effective Date”). The transferring policies cover a broad range of insurance types, mostly written through brokers.

1.12 On 23 June 2016, the UK Government held a referendum which resulted in the electorate voting to leave the European Union (“EU”). I assume in my Report that should this happen before the Effective Date, the UK will still follow the EU-wide prudential regulatory regime known as Solvency II, or an equivalent, going forward. I note though that the negotiations to lead to any exit of the EU can last up to two years from the point at which the UK Government formally gives notice to leave, which most likely extends long beyond the proposed Effective Date of these Transfers.

1.13 Under the proposed terms of the Transfers, all assets and liabilities relating to the policies and certain related contracts will transfer to AEGL, and the remaining assets and liabilities of the Transferring Companies will transfer to AEGL under the CBM which is explained further below. The ultimate goal is to bring CICE, AEGL and CBII into one entity through the mechanism of a CBM so that they can be managed collectively and centrally in an efficient manner. It is intended that the CBM completes on the same day as the Transfers.

A CBM is a particular type of merger that involves at least one company formed and registered in the UK and at least one company formed and registered in a European Economic Area (“EEA”) state other than the UK. It is subject to the legislation detailed in the EU Cross Border Mergers Directive (2005/56/EC) and the Companies (Cross-Border Mergers) Regulations 2007/2974. In undertaking a CBM, Chubb will carry forward tax losses from the Transferring Companies into AEGL.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 6 of 61 11/11/2016

Document Classification - KPMG Public

I note that a conditional order is being requested from the Courts as part of the Transfers, whereby if the Transfers are sanctioned but the CBM is not or the Jersey transfer is not (see below), the Transfers will not occur on a standalone basis. For the purposes of this Report, I assume that the CBM and the Jersey transfer will also be sanctioned, as if this does not happen then the conditional order would apply and there would be no change to policyholders of any of the Transfer Companies.

Jersey policies issued by CICE will not transfer unless the Jersey transfer is approved by the Royal Court of Jersey. The Jersey transfer, which provides for the transfer of policies on the same terms as the UK Transfers, is conditional on the sanction of the UK transfers by the High Court of Justice, England. The Jersey transfer will have the same effective date as the Transfers’ Effective Date.

1.14 The Transfers theoretically provide for the possibility of there being a limited number of policies which may not be capable of being transferred by law under the Transfers ("residual policies"). To the extent there are any such residual policies, they would be in the minority and those policies would remain with CICE or CBII (as applicable). However, given that the Transfers and the CBM are intended to occur simultaneously and the scheme is conditional on the CBM, in practice, any residual policies and associated assets would then transfer to AEGL under the CBM as CICE would no longer exist following the CBM. For that reason, it is therefore currently expected that there will be no residual policies and I assume in my Report that this is the case.

If the Transfers were not to occur then the CBM would not either. Policyholders would remain with their existing insurers, but the changes in executive management and overall operating model described in this report would still occur.

1.15 Certain policies sold by the Transferring Companies cover policyholders in non-EEA countries. Such policies fall under the law of the location of the policyholder, under which it may not be clear if the Transfers are to be recognised. I have considered whether from the point of view of these policyholders, it is likely to be any more difficult to bring a claim against AEGL than it would be to do so against the relevant Transferring Company. In theory there would be an issue arising if a party claimed that the Transfers were not effective in the relevant jurisdictions. However this would only be an issue if AEGL were to decline otherwise valid claims as a result of this which, as this would be in breach of the terms of the Courts’ orders approving the Transfers, I do not consider to be a realistic scenario. I therefore consider that there is no real risk of the Transfers making it more difficult for a policyholder outside the EEA to bring a claim under a policy from a Transferring Company.

For the avoidance of doubt I have not taken legal advice on this as I do not believe it is necessary. I have considered the two types of situation that an overseas Court could refuse to acknowledge: the rights of a non-EEA policyholder to assert a claim, which I do not see as a risk especially given that there is no incentive for policyholders to seek such a judgement, and that a reinsurer could petition that they do not need to respect existing policies as they did not recognise the Transfers. For the latter, I am comfortable that the risk does not change my conclusion. I discuss this further in section 5.16.

Scope

1.16 As Independent Expert, it is my duty to the Courts to consider the impact of the Transfers on the policyholders of the Transfer Companies, along with any other policyholders affected by the Transfers. In particular, it is my duty to consider the impact on their security and service levels for their benefits as set out in Appendix 2. In this instance, I have not identified any policyholders other than those of the Transfer Companies to be potentially affected.

1.17 This report does not consider any possible alternative arrangements to those referred to in sections 1.11 to 1.14. I am not aware of any other significant transaction relating to the Transfer Companies other than those set out in sections 1.11 to 1.14.

Reliances

1.18 I understand that my role is to produce a report in a form approved by the PRA for submission to the Courts. Whilst I have been assisted by my team, the report is written in the first person singular and the opinions expressed are my own.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 7 of 61 11/11/2016

Document Classification - KPMG Public

1.19 My work has been based on the data and other information made available to me by the Transfer Companies. A list of data and other information that I have considered is shown in Appendix 4.

I have not sought independent verification of data and information provided to me by the Transfer Companies, nor does my work constitute an audit of the financial and other information provided to me. Where indicated, I have reviewed the information provided for reasonableness and consistency and with the benefit of my experience this has not raised any concerns. I note that the information has been provided to me by members of the senior management of the Transfer Companies or by responsible senior professionals from the Transfer Companies’ advisors.

Where possible I have obtained audited financial information, and have received reports from independent third parties. In any case I have considered the sources of all data I have received before placing any reliance on it, and have sought representations where I consider it appropriate.

I have met in person or conducted conference calls with representatives of the Transfer Companies to discuss the information provided to me and specific matters arising out of the considerations and analysis conducted. This includes the legal advisers and the tax advisers to the Transfers, where appropriate.

Where significant pieces of information have been provided orally I have requested and received written confirmation.

Use and limitations

1.20 This report must be read in its entirety. Reading individual sections in isolation may be misleading.

1.21 Copies of this report will be sent to the relevant UK, Irish and Jersey financial regulators: the PRA and the FCA, the Central Bank of Ireland and the Jersey Financial Services Commission. This report will be used in evidence in the applications submitted to the UK and Irish Courts, and the Royal Court of Jersey. It will also be made available to policyholders and other members of the public as required by the relevant legislation and will be made available on www.chubb.com/CICE-transfer.

This report has been prepared under section 109 of FSMA in a form expected to be approved shortly by the PRA in consultation with the FCA.

This report is prepared solely in connection with, and for the purposes of, informing the UK and Irish Courts, the PRA, the FCA, the Central Bank of Ireland, and policyholders of the Transfer Companies of my findings in respect of the impact of the Transfers on the security and service levels of policyholders and may only be relied on for this purpose. This report is subject to the terms and limitations, including limitation of liability, set out in my firm’s engagement letter of 7 March 2016. An extract from this letter describing the scope of my work is contained in Appendix 2.

This report should not be regarded as suitable to be used or relied on by any party wishing to acquire any right to bring action against KPMG LLP in connection with any other use or reliance. To the fullest extent permitted by law, KPMG LLP will accept no responsibility or liability in respect of this report to any other party, other than as defined in my firm’s engagement letter referenced above.

1.22 In the normal course of conducting my role as Independent Expert, I have been provided with a significant and appropriate amount of information and data about the Transfer Companies’ activities and performance. In forming my view as set out in this report, this information has served a necessary and vital contribution. Due to a combination of legal, regulatory and commercial sensitivities some of the information I have relied upon to reach my conclusions cannot be disclosed in a public report such as this. However I can confirm that appropriate detailed information has been provided to me to enable me to form the opinions I express to the UK and Irish Courts in this report.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 8 of 61 11/11/2016

Document Classification - KPMG Public

Professional guidance

1.23 This report has been prepared in accordance with the guidance set out in Part 35 of the Civil Procedure Rules and the accompanying practice direction, including the protocol/guidance for the instruction of experts to give evidence in civil claims (2014) issued by the Civil Justice Council.

This report also complies with the guidance for transfers reports set out in the Statement of Policy issued by the PRA in April 2015 entitled “The Prudential Regulation Authority’s Approach to Insurance Business Transfers” and in Chapter 18 of the FCA Supervision Handbook, in particular, sections 18.2.31 to 18.2.41 inclusive, regarding the content and considerations of the report.

In preparing this report I have taken into account the requirements of the Technical Actuarial Standards (“TASs”) issued by the Financial Reporting Council. The TAS Standards which apply to the work performed in preparing this report are Transformations, Modelling, Data, Insurance and Reporting Actuarial Information. In my opinion, there are no material departures from any of these TASs in my performance of this work and this report. I have also followed the guidance set out in APS X2: Review of Actuarial Work.

I understand that my duty in preparing my report is to help the UK and Irish Courts on all matters within my expertise and that this duty overrides any obligations I have to those instructing me and/or paying my fee. I confirm that I have complied with this.

Terminology

1.24 In my discussion of the effects of the proposed Transfers on the Transfer Companies concerned, I use various technical terms. The definitions of these terms as used in this report are contained in the Glossary in Appendix 5.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 9 of 61 11/11/2016

Document Classification - KPMG Public

2. Executive Summary & Conclusions

Overview of the Transfers

2.1 This report considers the impact of the proposed transfers of the insurance business of CICE and CBII to AEGL. The transferring policyholders are both businesses and individual retail clients. Products offered to business clients include: property, casualty, accident and health, financial lines, excess liability and political risk insurance. Individual clients’ policies include: home and contents, jewellery, fine art and motor cover.

As a consequence of the Transfers the insurance and reinsurance obligations and certain other assets and liabilities of CICE and CBII will transfer to AEGL. The existing policyholders of AEGL are a mix of business and individual clients. Policies offered to business clients include: primary and excess casualty, financial lines, political risks, marine cargo, construction, aviation, energy, property and accident and health insurance. Personal lines include accident and health and travel insurance alongside speciality personal lines insurance mainly for mobile phone handsets. AEGL also provide reinsurance for property and casualty classes.

AEGL has the permissions to write all the classes being transferred into it.

2.2 The Transfers are primarily a legal and financial reorganisation of selected non-life businesses operating from the UK and Ireland, aiming to gather simplification and efficiency gains throughout the businesses and in particular more effective management of capital following the introduction of Solvency II.

2.3 CICE and CBII intend to communicate details of the Transfers to their policyholders. Policyholders of CBII are all to be individually notified, policyholders of AEGL are not to be individually notified, and policyholders of CICE are to be informed excepting the following groups:

underlying beneficiaries of group policies (though CICE will notify the group policyholder);

policyholders who are individuals, subsidiaries or affiliates under directors and officers insurance;

any individual whose name is not written in policy documents or with an incorrect or incomplete address;

policyholders whose policy has expired (with some exceptions, as discussed in Appendix 7);

policyholders who purchased their coverage through a corporate partner or scheme offered by a sponsoring broker and who are not individually notified by the partner or broker (as applicable) or the partner or broker has not provided CICE with data to enable it to individually notify such policyholders; and

policyholders of a particular corporate partner (instead it is anticipated that notice will be given through the inclusion of a message in policyholder banking statements).

Although it is not part of my scope as Independent Expert I have been asked to comment on the appropriateness of the communications waivers requested. I provide my reasoning in Appendix 7. I note and accept though that the Courts are the ultimate arbiter on the communication and any non-circularisation, and the regulators will also have their own opinions on these issues.

When considering the proposed approach to notifications, I have considered a number of factors, including the likelihood of a policyholder having a claim, whether the policyholder’s policy is transferring and the impact of the Transfers on the security of the policyholders. I have also considered the practicality of notifying policyholders.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 10 of 61 11/11/2016

Document Classification - KPMG Public

I consider the proposed approach to communicating the Transfers to be appropriate, reasonable and proportionate. I consider that the non-circularisation to the specific groups of policyholders of CICE (as set out above in summary and in Appendix 7 in detail) is appropriate, reasonable and proportionate given the circumstances of those policyholders.

2.4 Background of the Transfer Companies

AEGL is a legal entity of Chubb which operates under four divisions: Chubb Europe, Chubb Global Markets, Chubb Tempest Re Europe, and Combined Insurance. Chubb Europe specialises in providing property, primary and excess casualty, financial lines, political risk, marine cargo and construction-related risks insurance for multinational and large commercial clients. In addition, they provide accident and health, travel and mobile phone handset insurance for individuals. Chubb Global Markets is a London Market speciality international business offering excess and surplus lines, marine, aviation, energy, political risks, property, financial lines and accident and health insurance. Chubb Tempest Re Europe provide casualty and property reinsurance. Combined Insurance provides accident and healthcare insurance. As of 2 November 2016, AEGL operates as a subsidiary of ACE European Holdings Limited and Chubb Insurance S.A/N.V.

As of 2 November 2016, CICE operates as a wholly owned subsidary of ACE European Holdings No. 2 Limited, with policyholders including small to multinational businesses and individuals. CICE offer commercial lines, accident and health and financial lines for business clients. They provide home and contents, jewellery, fine art and motor insurance for individuals.

CBII operates as a wholly owned subsidary of ACE European Holdings No. 2 Limited as of 2 November 2016, specialising in providing commercial insurance on an excess basis. Exposures are high in severity and low in frequency, with a global client base.

All of the Transfer Companies have credit ratings of A++ from AM Best. For the avoidance of doubt, I have placed no reliance on the Transfer Companies’ credit ratings in this report, but note this as it can be a reason that policyholders choose to do business with Chubb companies.

Purpose of the Transfers

2.5 The proposed Transfers constitute an internal reorganisation of selected non-life UK and Irish subsidiaries of Chubb, aiming to gather simplification and efficiency gains throughout the businesses and in particular more effective management of capital following the introduction of the new prudential regulatory regime known as Solvency II.

2.6 My approach to assessing the likely effects of the Transfers on policyholders is to:

Understand the businesses of the entities affected by the Transfers; and

Understand the effect of the Transfers on the assets and liabilities of the companies and businesses involved.

The above stages are contained in sections 3 and 4 of this report.

Having identified the effects of the Transfers on the various companies and businesses, I then do the following in section 5:

Identify the relevant groups of policyholders within each company;

Consider the impact of the Transfers on the security of each group of policyholders and other stakeholders; and

Consider other non-financial aspects of the impact of the Transfers (for example, policyholder service and the claims handling process).

I note that the Transfer Companies operate in markets which may require market participants to maintain higher standards of financial security than the regulatory minimum in order to

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 11 of 61 11/11/2016

Document Classification - KPMG Public

continue to access new business. All Transfer Companies are part of Chubb, a leading, publicly traded, global property and casualty insurer, and benefit from this association; for example referencing of their ownership in their marketing and group rating benefits.

Given the levels of capital cover (as a proportion of the regulatory minimum requirement) held by all Transfer Companies, I expect the chance that any one of them would not be able to meet its respective future obligations in full to be remote, and I therefore conclude that no existing, or transferring policyholder will suffer detriment to their security if the Transfers proceed.

2.7 Financial and economic information considered

In order to consider the effect of the proposed Transfers on each of the entities and groups of policyholders concerned, I have been provided with comparative information for each legal entity, including:

Balance sheet information based on the most recently audited balance sheet figures as at 31 December 2015 for all entities;

External actuarial reserve reviews for AEGL, CBII and CICE as at 31 December 2015;

Internal actuarial reserve reviews for AEGL, CBII and CICE as at 31 December 2015;

Estimates of the regulatory capital required for each entity as at 31 December 2015; and

Internal management information provided over the course of preparing this report.

I will issue a supplemental report containing the most up-to-date financial information prior to the final hearing.

In forming my opinion, I have conducted a number of interviews with key personnel responsible for core functions in the Transfer Companies (a complete list of interviewees is provided in Appendix 6), and I have placed reliance on, amongst other information, estimates of the capital required to be held by the Transfer Companies (such that the companies are able to fulfil their policyholder obligations in the event of an extreme event or scenario) provided by the Transfer Companies. I describe how I have used this information in performing my analysis in more detail in section 5.13. In order to satisfy myself that these estimates are an appropriate basis on which to form an opinion, I have considered:

The appropriateness of the methods used by the Transfer Companies to calculate the estimates of capital requirements; and

The impact of a set of specific severe adverse events on each of the Transfer Companies pre and post Transfers in order to gain comfort that, at a high level, the capital estimates are reasonable.

The above stages are contained in section 6 of this report.

Key Assumptions

2.8 In conducting my analysis I have assumed the following:

There will be no policyholders left in the Transferring Companies after the Transfers, as all existing policyholders of the Transferring Companies, will become policyholders of AEGL as a consequence of the Transfers. As discussed in 1.14, I assume there are no residual policies.

The Transfers are to be broadly tax neutral for all of the Transfer Companies. There may be a small tax liability that arises in CBII of less than £3m, which I do not consider material

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 12 of 61 11/11/2016

Document Classification - KPMG Public

in the context of the balance sheet of AEGL after the Transfer. This has been confirmed by the management of the Transfer Companies as discussed in section 4.6.

Post Transfer, AEGL will be adhering to the overarching capital management policy that is being implemented across the Transfer Companies following the acquisition. The minimum regulatory capital cover levels within the capital management policy are sufficiently in excess of the regulatory minimum such that the probability of default remains remote. The policy is discussed further in 3.25;

The same level of assets and liabilities will exist within AEGL as compared to the Transfer Companies in aggregate after the Transfers and the CBM as before the Transfers (when valued on the same accounting basis before and after); and

AEGL will continue to operate and has no current intentions to cease underwriting or carry out a further restructuring of their business as a consequence of the Transfers, other than that of the planned CBM.

In the unlikely event of the UK leaving the EU before the Effective Date, the UK will still follow the EU-wide prudential regulatory regime known as Solvency II, or an equivalent, going forward

The above assumptions underlie the analysis and conclusions in my report. If these assumptions were to change my opinion may also change. At the time of writing my report the above assumptions are the current intentions for the Transfers and the Transfer Companies and I have received written representations from the Transfer Companies substantially similar to Appendix 3 confirming my understanding.

Findings

2.9 The findings of my report are summarised below. The detailed explanation behind these conclusions follows in the body of this report:

I have identified three distinct policyholder groups. These are:

i) Existing AEGL policyholders;

ii) Transferring CICE policyholders; and

iii) Transferring CBII policyholders.

I have considered using other policyholder groupings within my report as summarised below, however I have not identified any material difference in impact on policyholders when split differently to that above. I considered the following alternative groupings but came to the conclusion that each subsets interests were aligned:

i) Insurance and Reinsurance policyholders;

ii) Policyholders of compulsory and non-compulsory insurance; and

iii) Policyholders related to latent risks and the remainder of the book.

With respect to the CICE policyholders transferring to AEGL under the Transfers, I do not expect any adverse impact on policyholder security as a consequence of the Transfers, as none of the metrics I have considered show deterioration as a result of the Transfers.

With respect to the CBII policyholders, I do not expect any material adverse impact as a result of the Transfers; the Transfers leave CBII policyholders with a much larger and better diversified capital base to support their risks, and the probability that policyholders will not be paid in full will remain remote. The absolute capital coverage ratio for regulatory capital

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 13 of 61 11/11/2016

Document Classification - KPMG Public

does decrease, but given the resulting broader capital base I do not find this to have a material impact on CBII policyholder security.

With respect to the existing policyholders of AEGL, I expect there to be a favourable impact on policyholders’ security as a consequence of the Transfers; CBII holds substantially more capital than required by regulation, and the transfer of this additional capital produces a policyholder security benefit to both AEGL and CICE policyholders. However, in taking on guarantees for CICE’s UK pension scheme, AEGL will be taking on responsibility for a scheme which is open to accrual, unlike AEGL’s current pension obligations. Further to this, CBII and AEGL policyholders will be protected by an entity that will guarantee pension schemes, whereas CBII and AEGL did not previously do so. However, considering the size of the existing pension deficit (which is recognised in the UK GAAP and Solvency II balance sheets) relative to the capital resources available to the enlarged AEGL post-Transfer, I do not believe this will cause a materially adverse change to the security available to AEGL or CBII policyholders. I consider that the increased capital available to AEGL policyholders after the Transfers outweighs the additional liability taken on through the pension scheme guarantee, and therefore that the Transfers have an overall favourable impact on AEGL policyholders. .

There is no change for CICE pension obligations as a result of the Transfers other than the change of guarantor to AEGL, which has a larger capital base.

In terms of regulatory supervision, and the protections available to policyholders in the event of the failure to pay claims of one of the Transfer Companies, there is no change for policyholders of CICE or AEGL. CBII will change from being supervised by the Central Bank of Ireland to being supervised by the PRA and Financial Conduct Authority (“FCA”). I do not identify any adverse effect on the policyholders by a change in prudential regulator due to the common prudential regulatory framework seen across the EU and the expectation that the UK will continue to adopt a Solvency II equivalent regime in the event of leaving the EU before the Transfers.

There will be no change in executive management, governance or risk committee structure, or capital management as a result of the Transfers. As a result of ACE Limited acquiring The Chubb Corporation, these services are, or have already been integrated, and would have been regardless of the Transfers.

There will be no substantial change in the standards of service which the policyholders will receive as a consequence of the Transfers. Following the acquisition, the administration and operational services used by the Transfer Companies are being organised to create a unified business model whether or not the Transfers go ahead, as would be expected. Claims administration and administration for the Transfer Companies share common, similar processes.

As part of the integration the AEGL complaints model is being extended to cover CICE customers. This represents an improvement in the complaints process for former CICE customers because of the additional governance involved in the AEGL model. Furthermore, there is no expectation that the protection of any of the Transfer Companies’ customers’ data will diminish as a result of the Transfers.

2.10 I have considered the Transfers and their likely effect on each of the policyholder groups, including Jersey policyholders. I have concluded that the risk of any policyholder being adversely affected by the proposed Transfers is sufficiently remote for it to be appropriate to proceed with the proposed Transfers as described in this report. For the avoidance of doubt, this conclusion equally applies to those policyholders affected by the Jersey transfer.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 14 of 61 11/11/2016

Document Classification - KPMG Public

Expert’s declaration

2.11 I confirm that I have made clear which facts and matters referred to in this report are within my own knowledge and which are not. Those that are within my own knowledge I confirm to be true. The opinions I have expressed represent my true and complete professional opinions on the matters to which they refer.

Philip Tippin Fellow of the Institute of Actuaries Partner, KPMG LLP 11 November 2016

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 15 of 61 11/11/2016

Document Classification - KPMG Public

3. Background

Chubb Limited (“Chubb”)

3.1 ACE Limited acquired The Chubb Corporation in January 2016 and the group is now trading as Chubb. Chubb operates in over 54 countries and offers insurance to both business and individual clients. Core products offered to business clients include: accident and health, property, casualty and life insurance. Chubb provide reinsurance for property, casualty and life insurers. Chubb also provides mobile assurance through network operators to provide personal insurance cover. Chubb work with small and medium sized businesses to provide specialised packages to meet their insurance needs. For individual clients, Chubb provides a diverse range of personal insurance products both directly and through brokers. Products include: accidental death, motor, small electronic goods, identity theft protection, life insurance protection, savings products, prescription drug, recreational marine, personal accident, medical, travel and home insurance.

As at 31 December 2015 on a pro-forma basis, Chubb had gross written premiums of $37,379m and a net income of $4,578m.

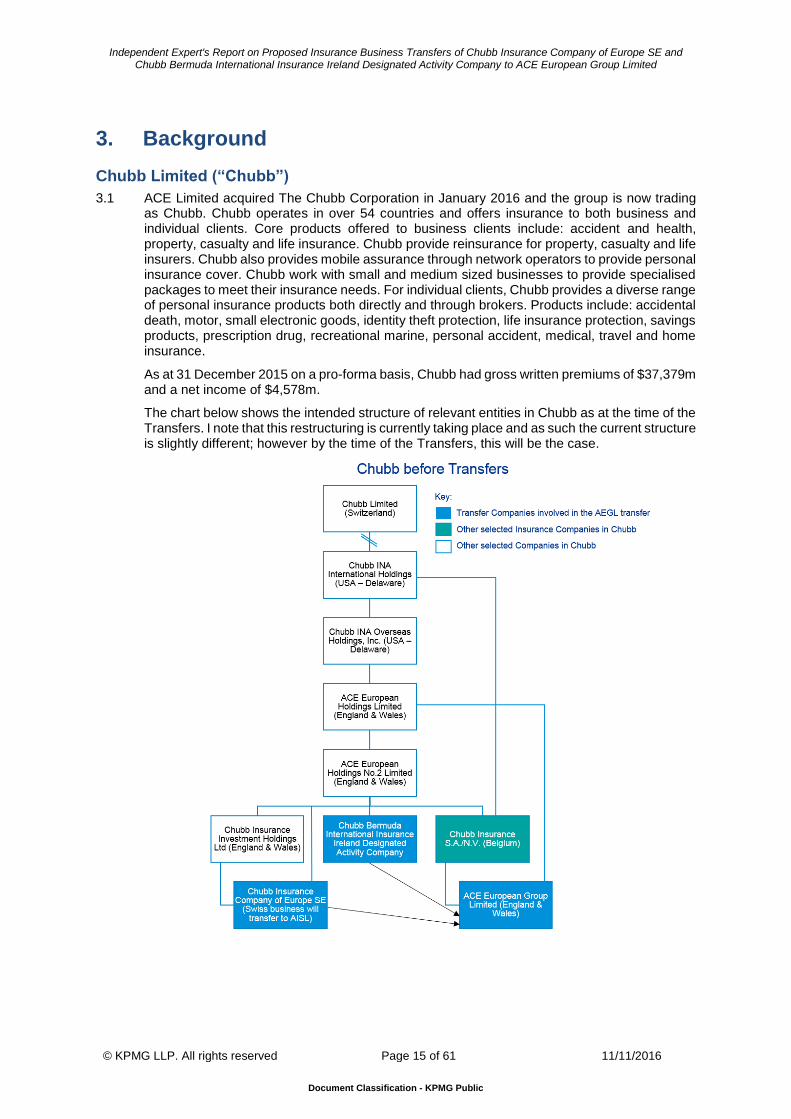

The chart below shows the intended structure of relevant entities in Chubb as at the time of the Transfers. I note that this restructuring is currently taking place and as such the current structure is slightly different; however by the time of the Transfers, this will be the case.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 16 of 61 11/11/2016

Document Classification - KPMG Public

ACE European Group Limited (“AEGL”)

3.2 AEGL is a legal entity of Chubb which operates under four divisions:

Chubb Europe, which specialises in providing property, primary and excess casualty, financial lines, political risk, marine cargo and construction-related risks insurance for multinational and large commercial clients. It also underwrites accident and health and travel insurance for individuals and employee and affinity groups across Europe, and Speciality Personal Lines business, which is primarily mobile phone handset insurance. Chubb Europe’s clients are throughout Europe, the Middle East and Africa.

Chubb Global Markets, which is a London Market speciality international business. Lines include excess and surplus lines business, marine, aviation, energy and political risk as well as property, financial lines and accident and health.

Chubb Tempest Re Europe, which writes a range of treaty reinsurance portfolio across both property and casualty classes.

Combined Insurance, which is a provider of accident and healthcare on both an individual and business basis. Products offered include short-term disability, critical condition and hospitalisation, which are offered across various European countries. AEGL provides the general insurance products whilst another of Chubb’s subsidiaries, ACE Europe Life Limited, provide the life assurance and permanent healthcare products.

AEGL sources its business primarily through broker channels.

3.3 AEGL is authorised by the PRA, regulated by the PRA and the FCA, and is a member of the Financial Services Compensation Scheme (“FSCS”), a statutory scheme funded by members of the UK financial services industry that provides protection to policyholders. Under current FSCS rules, claims made by UK private individuals and compulsory commercial policyholders are protected in the event of a default of a covered insurer. However, most non-compulsory commercial policyholders are not covered by the FSCS.

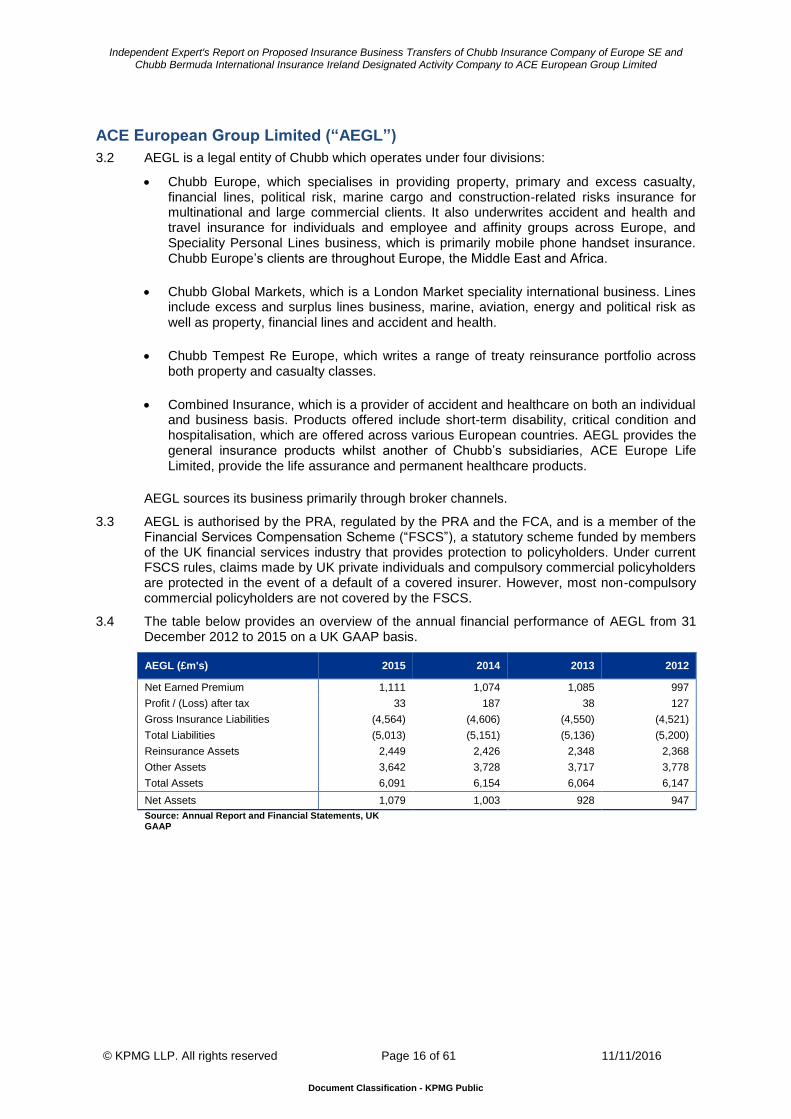

3.4 The table below provides an overview of the annual financial performance of AEGL from 31 December 2012 to 2015 on a UK GAAP basis.

AEGL (£m's) 2015 2014 2013 2012

Net Earned Premium 1,111 1,074 1,085 997

Profit / (Loss) after tax 33 187 38 127

Gross Insurance Liabilities (4,564) (4,606) (4,550) (4,521)

Total Liabilities (5,013) (5,151) (5,136) (5,200)

Reinsurance Assets 2,449 2,426 2,348 2,368

Other Assets 3,642 3,728 3,717 3,778

Total Assets 6,091 6,154 6,064 6,147

Net Assets 1,079 1,003 928 947

Source: Annual Report and Financial Statements, UK GAAP

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 17 of 61 11/11/2016

Document Classification - KPMG Public

AEGL’s net assets have been relatively stable over the last number of years. The combined ratio for the business has remained relatively stable too, with fluctuations in profitability driven by investment return and foreign exchange changes.

3.5 The table below provides an overview of the Solvency II balance sheet as at 31 December 2015.

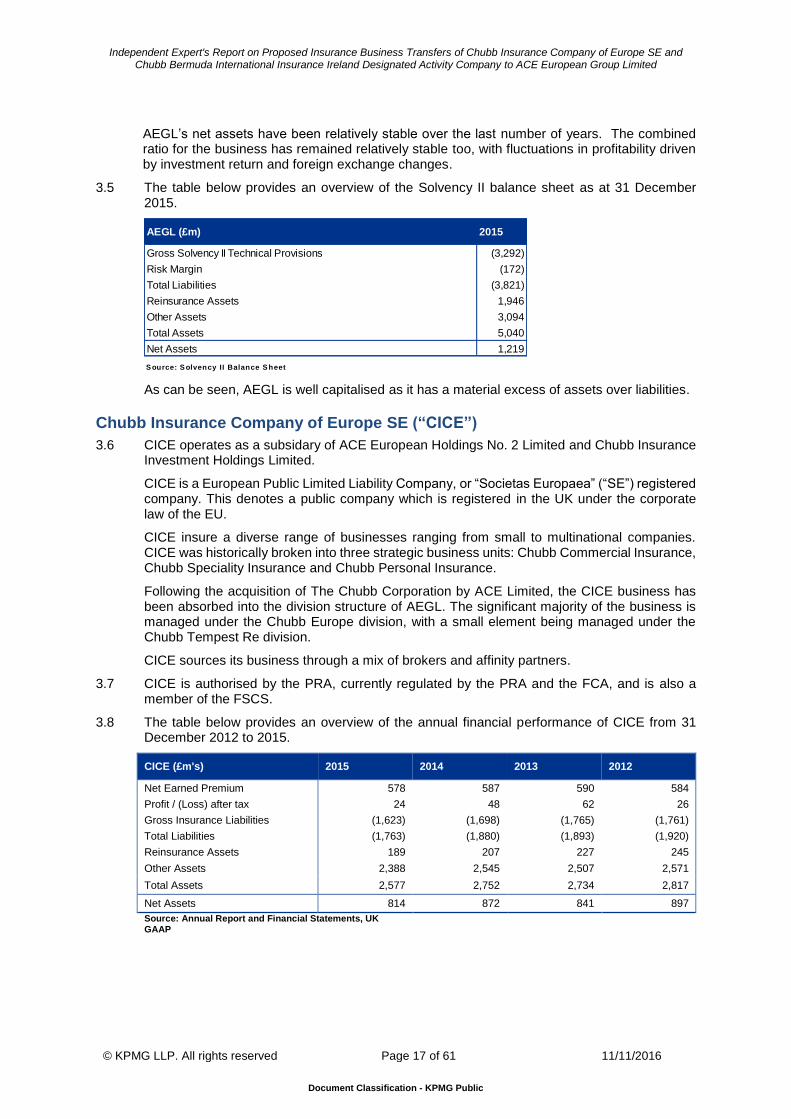

As can be seen, AEGL is well capitalised as it has a material excess of assets over liabilities.

Chubb Insurance Company of Europe SE (“CICE”)

3.6 CICE operates as a subsidary of ACE European Holdings No. 2 Limited and Chubb Insurance Investment Holdings Limited.

CICE is a European Public Limited Liability Company, or “Societas Europaea” (“SE”) registered company. This denotes a public company which is registered in the UK under the corporate law of the EU.

CICE insure a diverse range of businesses ranging from small to multinational companies. CICE was historically broken into three strategic business units: Chubb Commercial Insurance, Chubb Speciality Insurance and Chubb Personal Insurance.

Following the acquisition of The Chubb Corporation by ACE Limited, the CICE business has been absorbed into the division structure of AEGL. The significant majority of the business is managed under the Chubb Europe division, with a small element being managed under the Chubb Tempest Re division.

CICE sources its business through a mix of brokers and affinity partners.

3.7 CICE is authorised by the PRA, currently regulated by the PRA and the FCA, and is also a member of the FSCS.

3.8 The table below provides an overview of the annual financial performance of CICE from 31 December 2012 to 2015.

CICE (£m's) 2015 2014 2013 2012

Net Earned Premium 578 587 590 584

Profit / (Loss) after tax 24 48 62 26

Gross Insurance Liabilities (1,623) (1,698) (1,765) (1,761)

Total Liabilities (1,763) (1,880) (1,893) (1,920)

Reinsurance Assets 189 207 227 245

Other Assets 2,388 2,545 2,507 2,571

Total Assets 2,577 2,752 2,734 2,817

Net Assets 814 872 841 897

Source: Annual Report and Financial Statements, UK GAAP

AEGL (£m) 2015

Gross Solvency II Technical Provisions (3,292)

Risk Margin (172)

Total Liabilities (3,821)

Reinsurance Assets 1,946

Other Assets 3,094

Total Assets 5,040

Net Assets 1,219

S ource: S olvency II Balance S heet

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 18 of 61 11/11/2016

Document Classification - KPMG Public

CICE’s net assets have been relatively stable over the last several years, and profits have been stable, with less volatility than AEGL in investment returns and foreign exchange.

3.9 The table below provides an overview of the Solvency II balance sheet as at 31 December 2015.

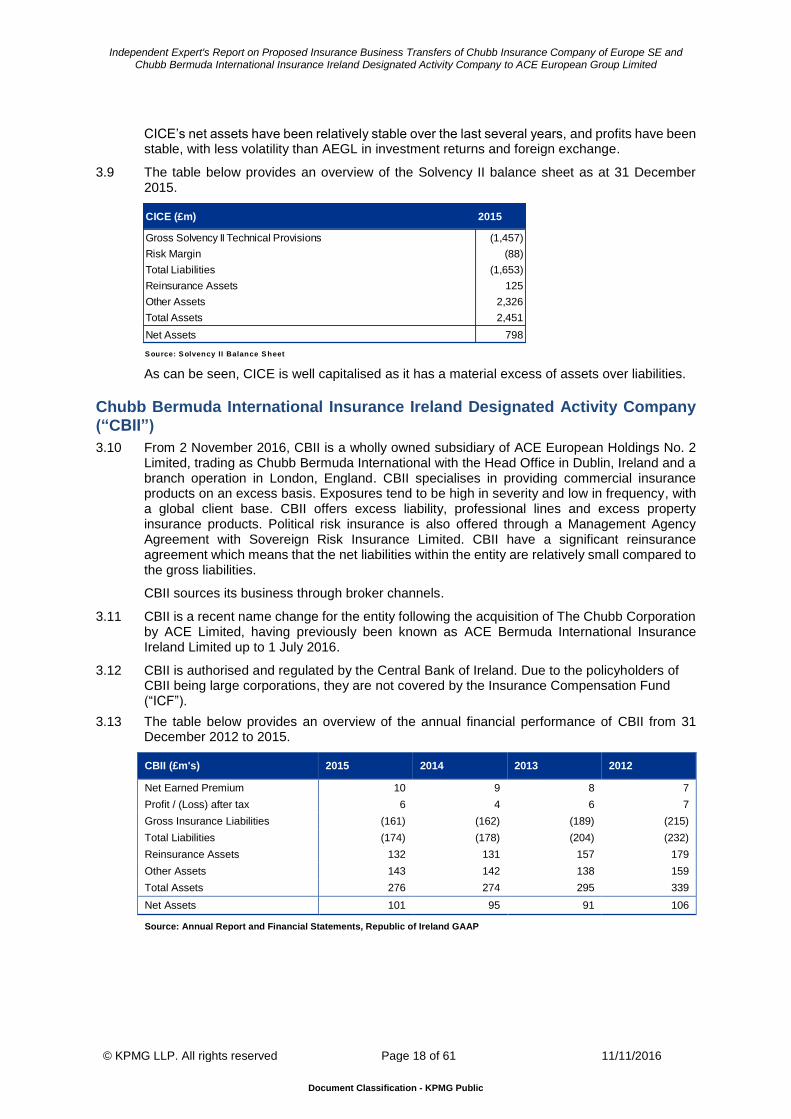

As can be seen, CICE is well capitalised as it has a material excess of assets over liabilities.

Chubb Bermuda International Insurance Ireland Designated Activity Company (“CBII”)

3.10 From 2 November 2016, CBII is a wholly owned subsidiary of ACE European Holdings No. 2 Limited, trading as Chubb Bermuda International with the Head Office in Dublin, Ireland and a branch operation in London, England. CBII specialises in providing commercial insurance products on an excess basis. Exposures tend to be high in severity and low in frequency, with a global client base. CBII offers excess liability, professional lines and excess property insurance products. Political risk insurance is also offered through a Management Agency Agreement with Sovereign Risk Insurance Limited. CBII have a significant reinsurance agreement which means that the net liabilities within the entity are relatively small compared to the gross liabilities.

CBII sources its business through broker channels.

3.11 CBII is a recent name change for the entity following the acquisition of The Chubb Corporation by ACE Limited, having previously been known as ACE Bermuda International Insurance Ireland Limited up to 1 July 2016.

3.12 CBII is authorised and regulated by the Central Bank of Ireland. Due to the policyholders of CBII being large corporations, they are not covered by the Insurance Compensation Fund (“ICF”).

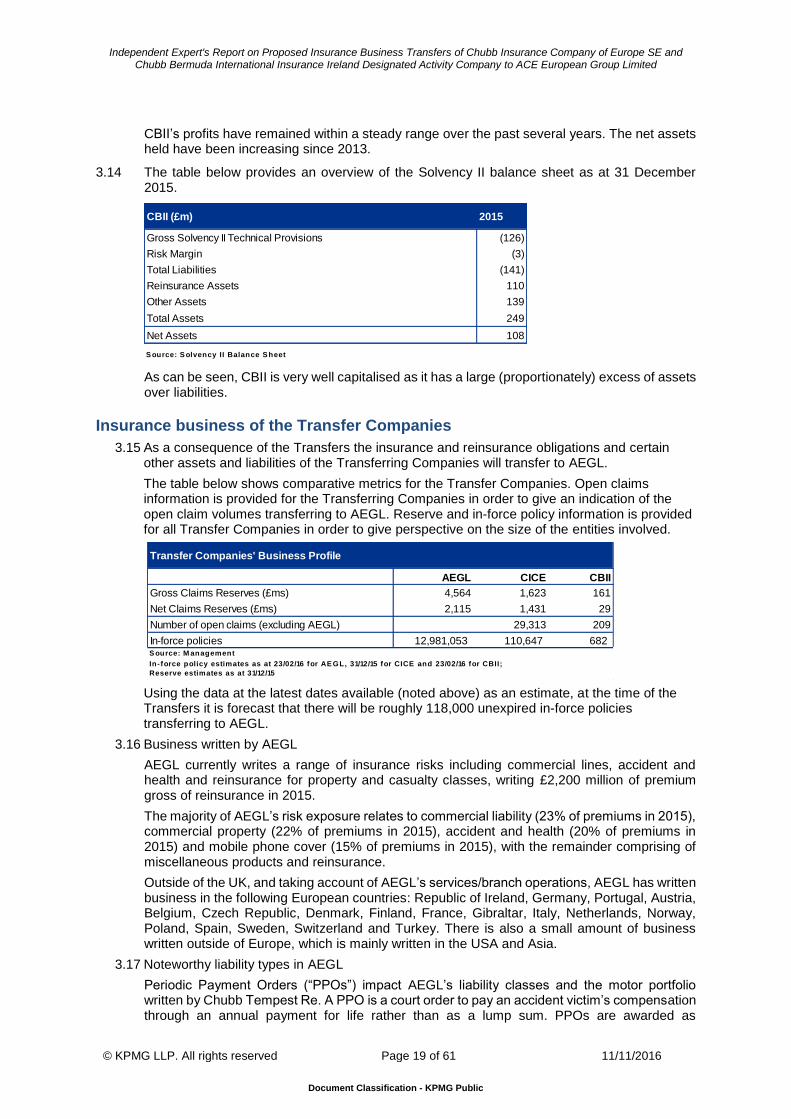

3.13 The table below provides an overview of the annual financial performance of CBII from 31 December 2012 to 2015.

CBII (£m's) 2015 2014 2013 2012

Net Earned Premium 10 9 8 7

Profit / (Loss) after tax 6 4 6 7

Gross Insurance Liabilities (161) (162) (189) (215)

Total Liabilities (174) (178) (204) (232)

Reinsurance Assets 132 131 157 179

Other Assets 143 142 138 159

Total Assets 276 274 295 339

Net Assets 101 95 91 106

Source: Annual Report and Financial Statements, Republic of Ireland GAAP

CICE (£m) 2015

Gross Solvency II Technical Provisions (1,457)

Risk Margin (88)

Total Liabilities (1,653)

Reinsurance Assets 125

Other Assets 2,326

Total Assets 2,451

Net Assets 798

S ource: S olvency II Balance S heet

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 19 of 61 11/11/2016

Document Classification - KPMG Public

CBII’s profits have remained within a steady range over the past several years. The net assets held have been increasing since 2013.

3.14 The table below provides an overview of the Solvency II balance sheet as at 31 December 2015.

As can be seen, CBII is very well capitalised as it has a large (proportionately) excess of assets over liabilities.

Insurance business of the Transfer Companies

3.15 As a consequence of the Transfers the insurance and reinsurance obligations and certain other assets and liabilities of the Transferring Companies will transfer to AEGL.

The table below shows comparative metrics for the Transfer Companies. Open claims information is provided for the Transferring Companies in order to give an indication of the open claim volumes transferring to AEGL. Reserve and in-force policy information is provided for all Transfer Companies in order to give perspective on the size of the entities involved.

Using the data at the latest dates available (noted above) as an estimate, at the time of the Transfers it is forecast that there will be roughly 118,000 unexpired in-force policies transferring to AEGL.

3.16 Business written by AEGL

AEGL currently writes a range of insurance risks including commercial lines, accident and health and reinsurance for property and casualty classes, writing £2,200 million of premium gross of reinsurance in 2015.

The majority of AEGL’s risk exposure relates to commercial liability (23% of premiums in 2015), commercial property (22% of premiums in 2015), accident and health (20% of premiums in 2015) and mobile phone cover (15% of premiums in 2015), with the remainder comprising of miscellaneous products and reinsurance.

Outside of the UK, and taking account of AEGL’s services/branch operations, AEGL has written business in the following European countries: Republic of Ireland, Germany, Portugal, Austria, Belgium, Czech Republic, Denmark, Finland, France, Gibraltar, Italy, Netherlands, Norway, Poland, Spain, Sweden, Switzerland and Turkey. There is also a small amount of business written outside of Europe, which is mainly written in the USA and Asia.

3.17 Noteworthy liability types in AEGL

Periodic Payment Orders (“PPOs”) impact AEGL’s liability classes and the motor portfolio written by Chubb Tempest Re. A PPO is a court order to pay an accident victim’s compensation through an annual payment for life rather than as a lump sum. PPOs are awarded as

CBII (£m) 2015

Gross Solvency II Technical Provisions (126)

Risk Margin (3)

Total Liabilities (141)

Reinsurance Assets 110

Other Assets 139

Total Assets 249

Net Assets 108

S ource: S olvency II Balance S heet

Transfer Companies' Business Profile

AEGL CICE CBII

Gross Claims Reserves (£ms) 4,564 1,623 161

Net Claims Reserves (£ms) 2,115 1,431 29

Number of open claims (excluding AEGL) 29,313 209

In-force policies 12,981,053 110,647 682 S ource: M anagement

In- force policy estimates as at 23/02/16 for AE GL, 31/12/15 for CICE and 23/02/16 for CBII;

Reserve estimates as at 31/12/15

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 20 of 61 11/11/2016

Document Classification - KPMG Public

compensation following injury and affect Motor and General Liability Insurance in the UK. This creates the potential for very long term exposure (in excess of 20 years) and exposure to a range of risks including those arising from future investment returns and economic factors such as inflation and longevity risk.

AEGL has exposure to Asbestos, Pollution and Health Hazard (“APH”) losses from its run off book of business, which covers any losses due to health hazards. The nature of these health issues mean that previously unknown claims can develop from unexpired policies. Given the age of the liabilities it can be difficult for some companies to identify all of the potentially affected policyholders.

AEGL has exposure to financial large losses arising from the financial crisis during 2007 - 2008. Loss estimates arising from such claims have been relatively stable over recent years.

I discuss the PPO and APH liabilities further in 3.21.

3.18 Business written by CICE

The predominant policy types written by CICE are third-party liability, property, accident and health, and household, which account for 44%, 17%, 12% and 11% of the premium respectively in 2015. Within third-party liability the most predominant policies written were Directors & Officers (“D&O”), Errors & Omissions (“E&O”), Commercial General and Excess Liability Insurance, and Employers’ Liability Insurance.

Outside of the UK, and taking account of CICE’s services/branch operations, CICE has written business in the following European countries: Republic of Ireland, Spain, Germany, France, Italy, Holland, Denmark, Sweden and Austria. There is also a small amount of business written outside of Europe. There are also some policyholders in Jersey and Guernsey.

3.19 Noteworthy liability types in CICE

CICE has exposure to the Madoff Ponzi Scheme investment fraud and Sub-prime lending financial catastrophes arising from the financial crisis during 2007 – 2008. Loss estimates arising from such claims have been relatively stable over recent years.

There is some exposure in CICE to APH losses which relate to the 2000 and prior years.

CICE underwrites a significant portfolio of High Net Worth Individuals homeowners and motor business.

I discuss the PPO and APH liabilities further in 3.21.

3.20 Business written by CBII

CBII primarily write property and liability business, which make up 46% and 31% of the premium respectively in 2015.

CBII have a significant reinsurance agreement which means that the net liabilities within the entity are relatively small compared to the gross liabilities.

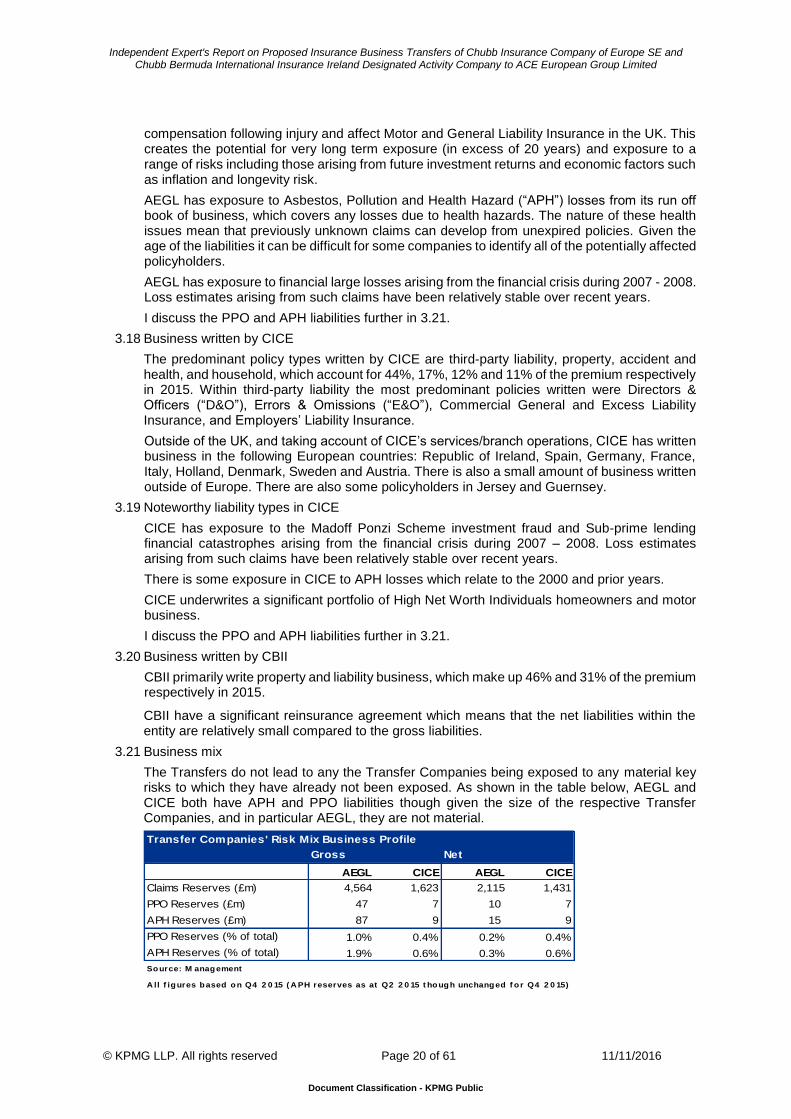

3.21 Business mix

The Transfers do not lead to any the Transfer Companies being exposed to any material key risks to which they have already not been exposed. As shown in the table below, AEGL and CICE both have APH and PPO liabilities though given the size of the respective Transfer Companies, and in particular AEGL, they are not material.

Transfer Companies' Risk Mix Business Profile

AEGL CICE AEGL CICE

Claims Reserves (£m) 4,564 1,623 2,115 1,431

PPO Reserves (£m) 47 7 10 7

APH Reserves (£m) 87 9 15 9

PPO Reserves (% of total) 1.0% 0.4% 0.2% 0.4%

APH Reserves (% of total) 1.9% 0.6% 0.3% 0.6%

Source: M anagement

A ll f igures based on Q4 2 0 15 ( A PH reserves as at Q2 2 0 15 t hough unchanged f o r Q4 2 0 15)

Gross Net

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 21 of 61 11/11/2016

Document Classification - KPMG Public

In CICE the PPO is in respect of an employer’s liability risk and therefore there is a limit on the original policy that cannot be exceeded. For AEGL the PPOs are emerging in the motor reinsurance book of Chubb Tempest Re. Since 2012 these policies have been written with limits under £5m (and mostly under £2m), and all of the PPOs in AEGL are protected by substantial outwards reinsurance. I have considered the extent to which these PPO liabilities could grow as a proportion of the existing reserves if economic conditions or mortality assumptions were to change for the worse, but the mitigating factors above mean that they do not grow so materially as to change my conclusions as set out in this report.

Outwards reinsurance programmes

3.22 The Transfer Companies have purchased reinsurance protections to mitigate their insurance risks. These protections are typical of those used by other insurance companies for the types of insurance business underwritten by the Transfer Companies. CICE have historically had a much larger net retention than AEGL and CBII. However, changes to the CICE reinsurance programmes commencing in April 2016 mean that the protections are largely aligned with the other Transfer Companies’ prior to the Transfers for unexpired risks. This change in purchasing has not changed the retentions on expired risks.

3.23 The key risk protections are:

Catastrophe Reinsurance is purchased by AEGL, CICE and CBII to mitigate the effect of large claim events. Such reinsurance is designed to mitigate the financial impact of the catastrophic events that may lead to material claims across a number of different types of insurance and a number of entities – for example, severe weather affecting large areas of the UK leading to multiple property damage claims from wind damage and flooding.

Excess of Loss Reinsurance is purchased by AEGL and CICE to mitigate the effect of individual large claims such as high value liability claims in the case of CICE and high value property claims in the case of AEGL.

AEGL, CICE and CBII all have proportional reinsurance arrangements in place whereby it shares a percentage of all premiums and claims with a reinsurer.

AEGL has material reinsurance recoveries expected to offset the gross liabilities, both intra-group and external to the group. To manage the credit risk in the event of a default of the largest single reinsurance counterparty, I understand that AEGL hold assets in trust arrangements. These arrangements will continue to apply to the new combined AEGL post Transfers. The incoming Transfers do not increase the exposure to this one particular counterparty, so these arrangements will provide the same level of support as they did before the Transfers.

Prudential capital requirements

3.24 The Transfer Companies are currently subject to a prudential capital regime which requires them to meet a solvency capital requirement calibrated to ensure that policyholders are secure at the 99.5% confidence level of potential future liability outcomes.

This is part of a new EU wide regulatory regime for insurance companies known as “Solvency II”, which was introduced with effect from 1st January 2016.

Other key requirements of this regime are as follows:

Insurance entities must calculate their Solvency II capital requirement either using a complex set of rules specified in EU legislation (the “Standard Formula”), or, subject to the approval of their regulator, using an internally developed economic capital model (an “Internal Model”). In either case, the determinants of the solvency capital requirement relate to the nature of the risks within the regulated entity, including market related investment risk, insurance risk arising from new business or existing liabilities, and other business risks including credit risk and operational risk.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 22 of 61 11/11/2016

Document Classification - KPMG Public

To use the Internal Model method, entities must complete a lengthy approval process with the regulator.

The Transfer Companies currently use the Standard Formula, though AEGL was a substantial way through the approval process to use the internal model, pausing its application in order to perform this integration. Should the Transfers proceed, it is planned for the new combined AEGL entity to resume the path to their Internal Model approval.

Regulatory capital requirements are defined in terms of a Solvency Capital Requirement (“SCR”) and a Minimum Capital Requirement (“MCR”). The requirements are calculated based on a complex formula based on the technical provisions, written premiums, reinsurance, deferred tax and administrative expenses.

The method with which insurance entity balance sheets and the definition of capital are calculated for regulatory purposes is now based on largely economic measures of assets and liabilities, rather than accounting based measures.

A range of minimum standards relating to insurance entity governance and disclosure have been introduced (known as “Pillar II” and “Pillar III”), including a requirement to perform and document an “Own Risk and Solvency Assessment” or “ORSA”.

If an insurer's available resources fall below the SCR, then supervisors are required to take action with the aim of restoring the insurer’s finances back to the level of the SCR as soon as possible. If, however, the financial situation of the insurer continues to deteriorate, then the level of supervisory intervention will be progressively intensified. The aim of this 'supervisory ladder' of intervention is to identify any ailing insurers before a serious threat to policyholders' interests is realised. If, despite supervisory intervention, the available resources of the insurer fall below the MCR, then 'ultimate supervisory action' will be triggered. This means that the insurer's liabilities could be transferred to another insurer, the licence of the insurer withdrawn, the insurer closed to new business and its in-force business liquidated.

I note that:

I have looked at the Solvency II Standard Formula calculations of the Transfer Companies to compare the relative difference in policyholder positions before and after the Transfers of liabilities. The appropriateness of this approach and more detailed description of this analysis can be found in section 5.13 and 5.15 below.

I have considered the stress tests included within the ORSAs produced by each of the Transfer Companies in determining the stress-tests to apply when considering the policyholder security for each group in section 6 below.

Capital management policy

3.25 Although the Transfer Companies are capitalised individually, Chubb is implementing an overarching capital management policy to oversee AEGL and CICE. This is to ensure consistent interpretation of the capital requirements and a consistent risk appetite applied to each, meaning that each entity will be managed so policyholder security is maintained above a minimum level of regulatory capital cover. Beyond this minimum level of regulatory capital cover, Chubb may manage its capital as it sees appropriate. For example, it may consider alternative uses for the excess capital above the capital management policy minimum, whilst considering the level required to maintain particular credit rating agencies’ ratings (which may be an important criterion to policyholders when selecting a policy). This will be happening regardless of the Transfers. CBII has a similar capital management policy that was approved by its Board in December 2015, and similarly requires an excess amount of capital over the regulatory capital requirements to be maintained.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 23 of 61 11/11/2016

Document Classification - KPMG Public

3.26 The minimum regulatory capital cover levels implied by the risk appetites within the intended capital management policy are sufficiently in excess of the regulatory minimum such that the probability of policyholder default remains a remote possibility.

Guarantees / risk sharing arrangements

3.27 ACE European Holdings Limited, which is a parent company of AEGL, has guarantees for four Defined Benefit pension schemes currently in place. AEGL itself currently provides no such guarantee.

CICE currently provide two guarantees over their UK pension scheme, of which the sponsor is ACE INA Services Limited. After the Transfer, AEGL will take over provision of the guarantees in the same forms.

There are no intragroup guarantees in place supporting any insurance liabilities for any of the Transfer Companies.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 24 of 61 11/11/2016

Document Classification - KPMG Public

4. Effects of the Transfers

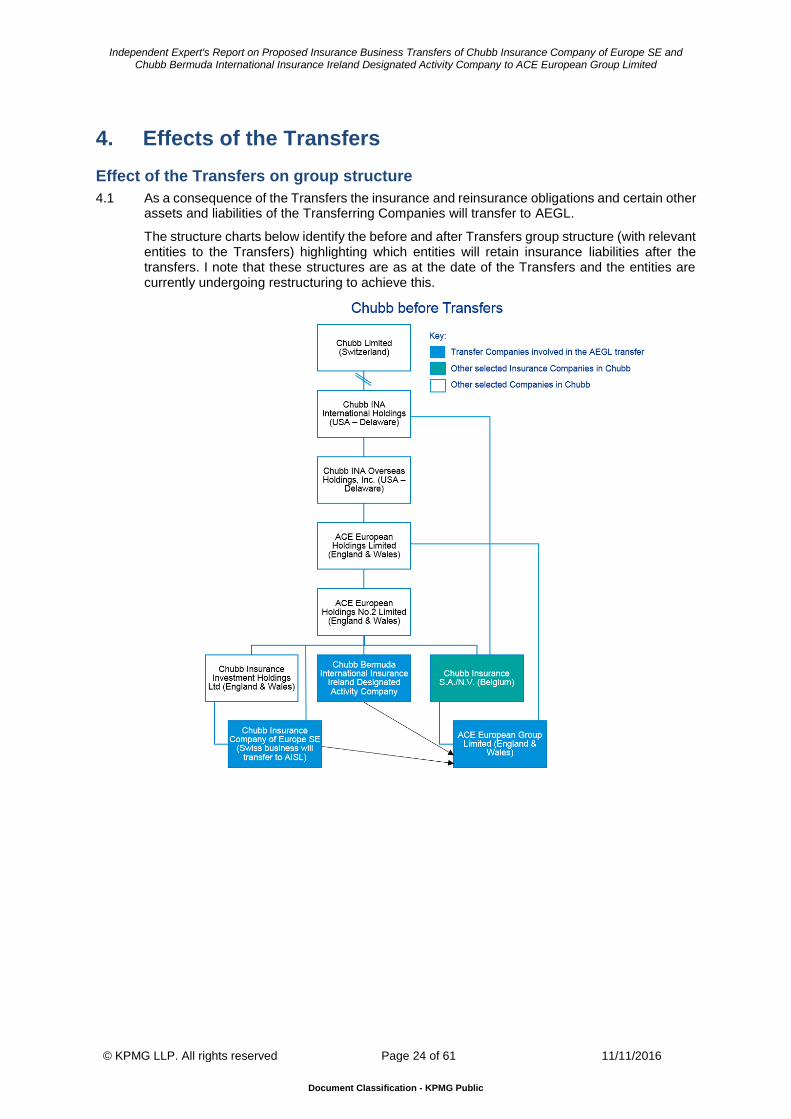

Effect of the Transfers on group structure

4.1 As a consequence of the Transfers the insurance and reinsurance obligations and certain other assets and liabilities of the Transferring Companies will transfer to AEGL.

The structure charts below identify the before and after Transfers group structure (with relevant entities to the Transfers) highlighting which entities will retain insurance liabilities after the transfers. I note that these structures are as at the date of the Transfers and the entities are currently undergoing restructuring to achieve this.

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 25 of 61 11/11/2016

Document Classification - KPMG Public

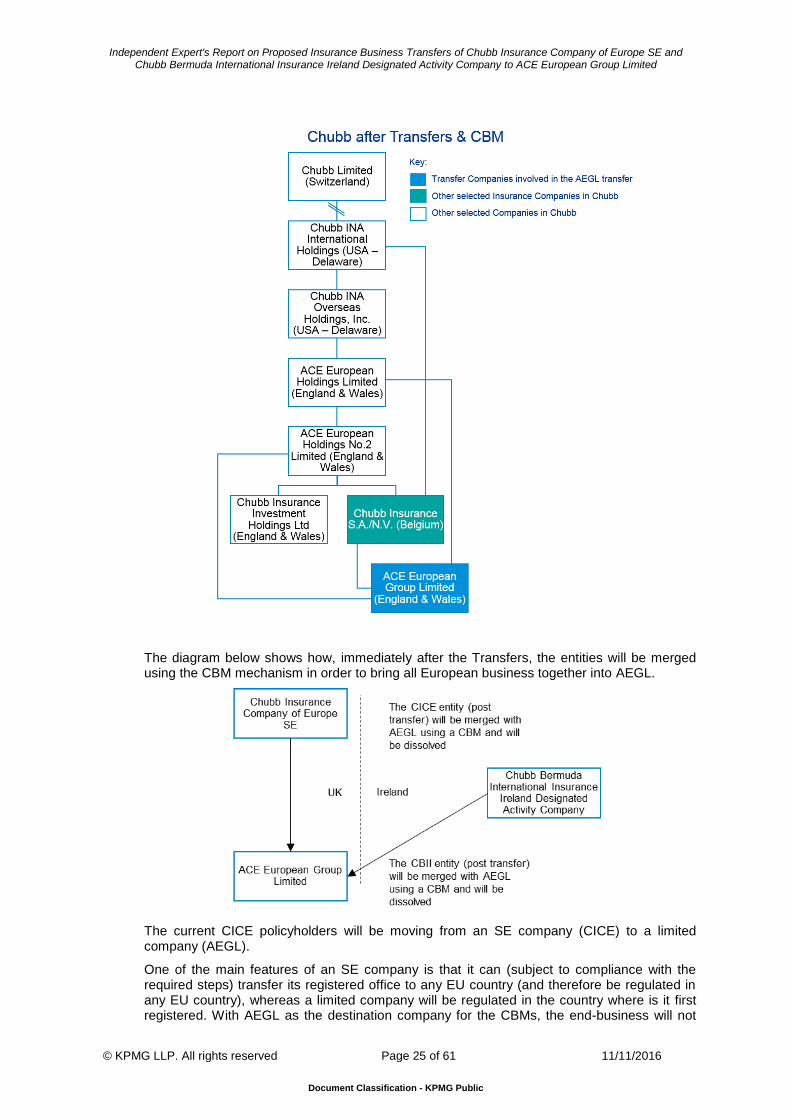

The diagram below shows how, immediately after the Transfers, the entities will be merged using the CBM mechanism in order to bring all European business together into AEGL.

The current CICE policyholders will be moving from an SE company (CICE) to a limited company (AEGL).

One of the main features of an SE company is that it can (subject to compliance with the required steps) transfer its registered office to any EU country (and therefore be regulated in any EU country), whereas a limited company will be regulated in the country where is it first registered. With AEGL as the destination company for the CBMs, the end-business will not

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 26 of 61 11/11/2016

Document Classification - KPMG Public

have the same portability that CICE enjoys currently. The portability is however over a prudential regulatory environment which, particularly with the introduction of Solvency II, is consistent across the EU.

Effect of the Transfers on Transfer Company balance sheets

4.2 I have carried out my analyses based on figures as at 31 December 2015 for the purposes of this Independent Expert Report, however I will update the analyses to the most up-to-date in a supplemental report.

4.3 There are no material differences between the accounting treatments of items in the statutory accounts of the Transfer Companies as presented in Section 3, with all figures reported on a UK or Republic of Ireland GAAP basis.

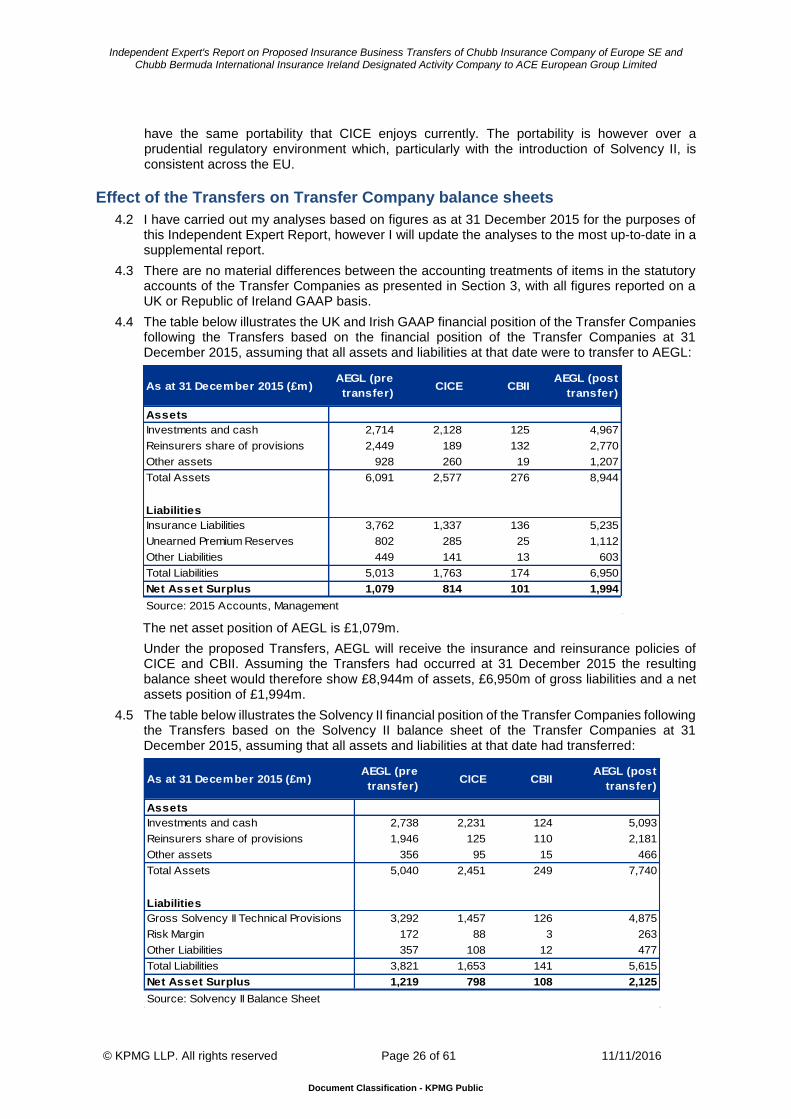

4.4 The table below illustrates the UK and Irish GAAP financial position of the Transfer Companies following the Transfers based on the financial position of the Transfer Companies at 31 December 2015, assuming that all assets and liabilities at that date were to transfer to AEGL:

As at 31 December 2015 (£m)AEGL (pre

transfer)CICE CBII

AEGL (post

transfer)

Assets

Investments and cash 2,714 2,128 125 4,967

Reinsurers share of provisions 2,449 189 132 2,770

Other assets 928 260 19 1,207

Total Assets 6,091 2,577 276 8,944

Liabilities

Insurance Liabilities 3,762 1,337 136 5,235

Unearned Premium Reserves 802 285 25 1,112

Other Liabilities 449 141 13 603

Total Liabilities 5,013 1,763 174 6,950

Net Asset Surplus 1,079 814 101 1,994

Source: 2015 Accounts, Management

The net asset position of AEGL is £1,079m.

Under the proposed Transfers, AEGL will receive the insurance and reinsurance policies of CICE and CBII. Assuming the Transfers had occurred at 31 December 2015 the resulting balance sheet would therefore show £8,944m of assets, £6,950m of gross liabilities and a net assets position of £1,994m.

4.5 The table below illustrates the Solvency II financial position of the Transfer Companies following the Transfers based on the Solvency II balance sheet of the Transfer Companies at 31 December 2015, assuming that all assets and liabilities at that date had transferred:

As at 31 December 2015 (£m)AEGL (pre

transfer)CICE CBII

AEGL (post

transfer)

Assets

Investments and cash 2,738 2,231 124 5,093

Reinsurers share of provisions 1,946 125 110 2,181

Other assets 356 95 15 466

Total Assets 5,040 2,451 249 7,740

Liabilities

Gross Solvency II Technical Provisions 3,292 1,457 126 4,875

Risk Margin 172 88 3 263

Other Liabilities 357 108 12 477

Total Liabilities 3,821 1,653 141 5,615

Net Asset Surplus 1,219 798 108 2,125

Source: Solvency II Balance Sheet

Independent Expert's Report on Proposed Insurance Business Transfers of Chubb Insurance Company of Europe SE and Chubb Bermuda International Insurance Ireland Designated Activity Company to ACE European Group Limited

© KPMG LLP. All rights reserved Page 27 of 61 11/11/2016

Document Classification - KPMG Public

The net asset position of AEGL on a Solvency II valuation basis is £1,219m.

Under the proposed Transfers, AEGL will receive the insurance and reinsurance policies of CICE and CBII. Assuming the Transfers had occurred at 31 December 2015 the resulting Solvency II balance sheet would therefore show £7,740m of assets, £5,615m of gross liabilities and a net assets position of £2,125m.

4.6 Cost and tax impact of the Transfers

I have received confirmation from the management of the Transfer Companies that no significant tax liabilities will be realised as the result of the Transfers and CBMs, following advice from independent advisers, because the ultimate CBMs will preserve their aggregate tax position. There is a risk that a small tax charge may arise from any gains realised from the transfer of the UK branch of CBII into AEGL, but I am satisfied that any such charge would be immaterial in the context of the combined AEGL balance sheet post-Transfers. This potential tax impact is expected to be less than £3m. Whilst there are some potential additional tax liabilities that may emerge (such as VAT on professional fees), it is expected that there will be no material change of the tax position once the ultimate sequence of Transfers has been completed, and therefore I am satisfied that they would not be sufficient to change any of my conclusions within this report. The Transfer Companies have performed due diligence including commissioning analysis from specialist tax advisors on the tax implications of the Transfers, which I have seen, in order to make this statement.

I understand that most costs associated with the Transfers will be incurred whether or not the Transfers proceed, as the majority of these costs relate to activities occurring prior to the sanction hearing (for example, with respect to legal fees and policyholder communications). Therefore I identify no significant additional costs arising from the implementation of the Transfers. AEGL will meet these costs.

4.7 Outwards reinsurance

Following the Transfers, it is intended that the reinsurance arrangements of CICE and CBII will be transferred with the reinsured policies, such that AEGL and former CICE and CBII policyholders will still be protected by the same reinsurance contracts as was the case before the Transfers. Any reinsurance contracts that do not transfer with the Transfers are anticipated to transfer with the CBM.

There is a risk that non-EEA reinsurers of the Transfer Companies may not recognise the Transfers and decline payment of future reinsurance recoveries. For reinsurance policies originally purchased by AEGL the subject business will not be transferring, and so there is no such risk for these protections. For CBII and CICE the total expected reinsurance recoveries anticipated from reinsurance outside the Chubb group of companies are less than 3% of the total reinsurance asset of AEGL after the Transfer. The amounts at risk are therefore very small in the context of the Transfer Companies’ balance sheets. I also note that in section 6.10 I consider a stress test of a major reinsurer failure that is larger than the total amount at risk from the non-recognition of the Transfers by non-EEA reinsurers, and this stress test does not change my overall conclusions. As a result I do not believe that this risk has a material adverse impact on any groups of policyholders involved in the Transfers.

4.8 Guarantees