Embed Size (px)

Citation preview

INDEPENDENT AUDITORS’ REPORT

TO THE MEMBERS OF JAMSHEDPUR UTILITIES & SERVICES COMPANY LIMITED

Report on the Standalone Indian Accounting Standards (Ind AS) Financial Statements

1. We have audited the accompanying standalone financial statements of Jamshedpur Utilities &Services Company Limited (“the Company”), which comprise the Balance Sheet as at March31, 2018 the Statement of Profit and Loss (including Other Comprehensive Income), the Cash FlowStatement and the Statement of Changes in Equity for the year then ended, and a summary of thesignificant accounting policies and other explanatory information.

Management’s Responsibility for the Standalone Ind AS Financial Statements

2. The Company’s Board of Directors is responsible for the matters stated in Section 134(5) of theCompanies Act, 2013 (“the Act”) with respect to the preparation of these Standalone Ind ASfinancial statements to give a true and fair view of the financial position, financial performance(including other comprehensive income), cash flows and changes in equity of the Company inaccordance with the accounting principles generally accepted in India, including the IndianAccounting Standards specified in the Companies (Indian Accounting Standards) Rules, 2015 (asamended) under Section 133 of the Act. This responsibility also includes maintenance of adequateaccounting records in accordance with the provisions of the Act for safeguarding of the assets of theCompany and for preventing and detecting frauds and other irregularities; selection andapplication of appropriate accounting policies; making judgments and estimates that arereasonable and prudent; and design, implementation and maintenance of adequate internalfinancial controls, relevant to the preparation and presentation of the standalone Ind AS financialstatements that give a true and fair view and are free from material misstatement, whether due tofraud or error.

Auditors’ Responsibility

3. Our responsibility is to express an opinion on these Standalone Ind AS financial statements basedon our audit.

4. We have taken into account the provisions of the Act and the Rules made thereunder including theaccounting and auditing standards and matters which are required to be included in the auditreport under the provisions of the Act and the Rules made thereunder.

5. We conducted our audit of the Ind AS financial statements in accordance with the Standards onAuditing specified under Section 143(10) of the Act and other applicable authoritativepronouncements issued by the Institute of Chartered Accountants of India. Those Standards andpronouncements require that we comply with ethical requirements and plan and perform the auditto obtain reasonable assurance about whether the Standalone Ind AS financial statements are freefrom material misstatement.

6. An audit involves performing procedures to obtain audit evidence about the amounts and thedisclosures in the Standalone Ind AS financial statements. The procedures selected depend on theauditors’ judgment, including the assessment of the risks of material misstatement of theStandalone Ind AS financial statements, whether due to fraud or error. In making those riskassessments, the auditor considers internal financial control relevant to the Company’s preparationof the Standalone Ind AS financial statements that give a true and fair view, in order to design auditprocedures that are appropriate in the circumstances, An audit also includes evaluating theappropriateness of the accounting policies used and the reasonableness of the accounting estimatesmade by the Company’s Directors, as well as evaluating the overall presentation of the StandaloneInd AS financial statements.

INDEPENDENT AUDITORS’ REPORTTo the Members of Jamshedpur Utilities & Services Company LimitedReport on the Financial StatementsPage 2 of 3

7. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basisfor our audit opinion on the Standalone Ind AS financial statements.

Opinion

8. In our opinion and to the best of our information and according to the explanations given to us, theaforesaid Standalone Ind AS financial statements give the information required by the Act in themanner so required and give a true and fair view in conformity with the accounting principlesgenerally accepted in India, of the state of affairs of the Company as at March 31, 2018, and its totalcomprehensive income (comprising of profit and other comprehensive income), its cash flows andthe changes in equity for the year ended on that date.

Other Matter

9. The Ind AS financial statements of the Company for the year ended March 31,2017 , were auditedby another firm of chartered accountants under the Companies Act, 2013 who, vide their reportdated April 21,2017 expressed an unmodified opinion on those financial statements. Our opinionis not qualified in respect of this matter.

Report on Other Legal and Regulatory Requirements

10 As required by the Companies (Auditor’s Report) Order, 2016, issued by the Central Governmentof India in terms of sub-section (11) of section 143 of the Act (“the Order”), and on the basis of suchchecks of the books and records of the Company as we considered appropriate and according to theinformation and explanations given to us, we give in the Annexure B a statement on the mattersspecified in paragraphs 3 and 4 of the Order.

11 As required by Section 143 (3) of the Act, we report that:

(a) We have sought and obtained all the information and explanations which to the best of ourknowledge and belief were necessary for the purposes of our audit.

(b) In our opinion, proper books of account as required by law have been kept by the Company so faras it appears from our examination of those books.

(c) The Balance Sheet, the Statement of Profit and Loss (including other comprehensive income), theCash Flow Statement and the Statement of Changes in Equity dealt with by this Report are inagreement with the books of account.

(d) In our opinion, the aforesaid standalone Ind AS financial statements comply with the IndianAccounting Standards specified under Section 133 of the Act.

(e) On the basis of the written representations received from the directors as on March 31, 2018taken on record by the Board of Directors, none of the directors is disqualified as onMarch 31, 2018 from being appointed as a director in terms of Section 164 (2) of the Act.

(f) With respect to the adequacy of the internal financial controls with reference to financialstatements of the Company and the operating effectiveness of such controls, refer to our separateReport in Annexure A.

INDEPENDENT AUDITORS’ REPORTTo the Members of Jamshedpur Utilities & Services Company LimitedReport on the Financial StatementsPage 3 of 3

(g) With respect to the other matters to be included in the Auditors’ Report in accordance withRule 11 of the Companies (Audit and Auditors) Rules, 2014, in our opinion and to the best of ourknowledge and belief and according to the information and explanations given to us:

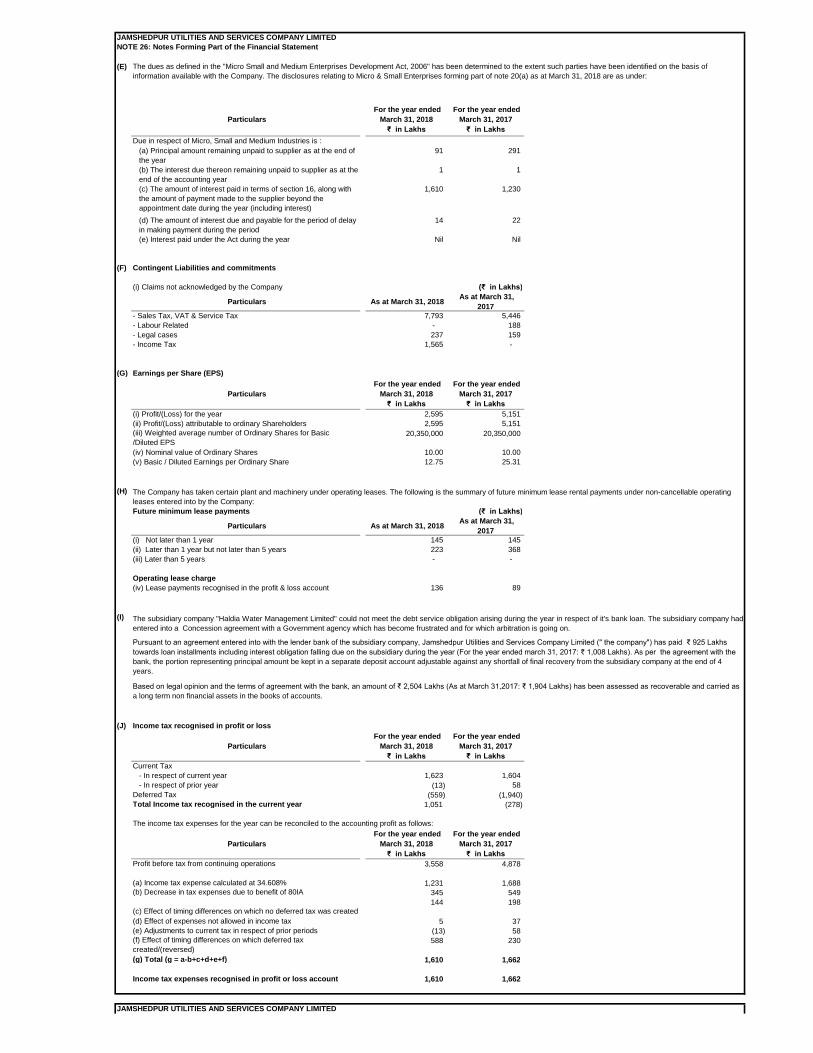

i The Company has disclosed the impact, if any, of pending litigations as at March 31, 2018 on itsfinancial position in its standalone Ind AS financial statements – Refer Note 26 F;

ii. The Company has made provision as at March 31, 2018, as required under the applicable law oraccounting standards, for material foreseeable losses, if any, on long-term contracts. The companydid not have any derivative contracts as at March 31, 2018.

iii. There were no amounts which were required to be transferred to the Investor Education andProtection Fund by the Company during the year ended March 31, 2018.

iv. The reporting on disclosures relating to Specified Bank Notes is not applicable to the Companyfor the year ended March 31, 2018

For Pricewaterhouse & Co Chartered Accountants LLPFirm Registration Number: FRN 304026E / E 300009Chartered Accountants

Avijit MukerjiKolkata PartnerApril 16, 2018 Membership Number 056155

Annexure A to Independent Auditors’ Report

Referred to in paragraph 11(f) of the Independent Auditors’ Report of even date to the members of

Jamshedpur Utilities & Service Company Limited on the financial statements for the year ended March

31, 2018

Page 1 of 2

Report on the Internal Financial Controls under Clause (i) of Sub-section 3 of Section 143of the Act

1. We have audited the internal financial controls over financial reporting of (“the Company”) as ofMarch 31, 2018 in conjunction with our audit of the financial statements of the Company for the yearended on that date.

Management’s Responsibility for Internal Financial Controls

2. The Company’s management is responsible for establishing and maintaining internal financial controlsbased on the internal control over financial reporting criteria established by the Company consideringthe essential components of internal control stated in the Guidance Note on Audit of Internal FinancialControls Over Financial Reporting issued by the Institute of Chartered Accountants of India (ICAI).These responsibilities include the design, implementation and maintenance of adequate internalfinancial controls that were operating effectively for ensuring the orderly and efficient conduct of itsbusiness, including adherence to company’s policies, the safeguarding of its assets, the prevention anddetection of frauds and errors, the accuracy and completeness of the accounting records, and the timelypreparation of reliable financial information, as required under the Act.

Auditors’ Responsibility

3. Our responsibility is to express an opinion on the Company's internal financial controls over financialreporting based on our audit. We conducted our audit in accordance with the Guidance Note on Auditof Internal Financial Controls Over Financial Reporting (the “Guidance Note”) and the Standards onAuditing deemed to be prescribed under section 143(10) of the Act to the extent applicable to an audit ofinternal financial controls, both applicable to an audit of internal financial controls and both issued bythe ICAI. Those Standards and the Guidance Note require that we comply with ethical requirements andplan and perform the audit to obtain reasonable assurance about whether adequate internal financialcontrols over financial reporting was established and maintained and if such controls operatedeffectively in all material respects.

4. Our audit involves performing procedures to obtain audit evidence about the adequacy of the internalfinancial controls system over financial reporting and their operating effectiveness. Our audit of internalfinancial controls over financial reporting included obtaining an understanding of internal financialcontrols over financial reporting, assessing the risk that a material weakness exists, and testing andevaluating the design and operating effectiveness of internal control based on the assessed risk. Theprocedures selected depend on the auditor’s judgement, including the assessment of the risks of materialmisstatement of the financial statements, whether due to fraud or error.

5. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour audit opinion on the Company’s internal financial controls system over financial reporting.

Meaning of Internal Financial Controls Over Financial Reporting

6. A company's internal financial control over financial reporting is a process designed to providereasonable assurance regarding the reliability of financial reporting and the preparation of financialstatements for external purposes in accordance with generally accepted accounting principles. Acompany's internal financial control over financial reporting includes those policies and procedures that(1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect thetransactions and dispositions of the assets of the company; (2) provide reasonable assurance that

Annexure A to Independent Auditors’ Report

Referred to in paragraph 11(f) of the Independent Auditors’ Report of even date to the members of

Jamshedpur Utilities & Service Company Limited on the financial statements for the year ended March

31, 2018

Page 2 of 2

transactions are recorded as necessary to permit preparation of financial statements in accordance withgenerally accepted accounting principles, and that receipts and expenditures of the company are beingmade only in accordance with authorizations of management and directors of the company; and (3)provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use,or disposition of the company's assets that could have a material effect on the financial statements.

Inherent Limitations of Internal Financial Controls Over Financial Reporting

7. Because of the inherent limitations of internal financial controls over financial reporting, including thepossibility of collusion or improper management override of controls, material misstatements due toerror or fraud may occur and not be detected. Also, projections of any evaluation of the internal financialcontrols over financial reporting to future periods are subject to the risk that the internal financialcontrol over financial reporting may become inadequate because of changes in conditions, or that thedegree of compliance with the policies or procedures may deteriorate.

Opinion

8. In our opinion, the Company has, in all material respects, an adequate internal financial controls systemover financial reporting and such internal financial controls over financial reporting were operatingeffectively as at March , 31, 2018 , based on the internal control over financial reporting criteriaestablished by the Company considering the essential components of internal control stated in theGuidance Note on Audit of Internal Financial Controls Over Financial Reporting issued by the Instituteof Chartered Accountants of India.

For Price Waterhouse & Co Chartered Accountant LLPFirm Registration Number: FRN 304026E / E 300009Chartered Accountants

Avijit MukerjiKolkata PartnerApril 16, 2018 Membership Number 056155

Annexure B to Independent Auditors’ ReportReferred to in paragraph 10 of the Independent Auditors’ Report of even date to the members ofJamshedpur Utilities & Services Company Limited of the Company financial statements as of and for theyear ended March 31, 2018

i. (a) The Company is maintaining proper records showing full particulars, including quantitativedetails and situation, of fixed assets.

(b) The fixed assets of the Company have been physically verified by the Management during the yearand no material discrepancies have been noticed on such verification. In our opinion, the frequencyof verification is reasonable.

(c) The title deeds of immovable properties, as disclosed in Note 02 on fixed assets to the financialstatements, are held in the name of the Company. According to the information and explanationgiven to us and the records examined by us, we report that immovable properties of buildingamounting to Rs 403 lakhs have been constructed on land not owned by the Company. Based onthe examination of the registered transfer deed/agreement provided to us, we report that the titledeed/agreements comprising all the immovable properties of land are held in the name of theCompany as at the balance sheet date.

ii. The physical verification of inventory have been conducted at reasonable intervals by theManagement during the year .The discrepancies noticed on physical verification of inventory ascompared to book records were not material

iii. The Company has granted unsecured loans, to one of its Subsidiary Company companies coveredin the register maintained under Section 189 of the Act.

(a) In respect of the aforesaid loans, the terms and conditions under which such loans were grantedare not prejudicial to the Company’s interest.

(b) In respect of the aforesaid loan, the schedule of repayment of principal and payment of interesthas been stipulated and the repayments of the principal amounts and interest have not beenregular as per the stipulation.

(c) In respect of the aforesaid loans, the total amount overdue for more than ninety days as at March31,2018 is Rs 1,750 lakhs (including interest of Rs 100 lakhs for the period May 31,2012 to May31,2013) ,recoverability of which is considered doubtful as the subsidiary company has ceased itsoperation. Accordingly the amounts have been fully provided for in the financial statements.

iv. In our opinion, and according to the information and explanations given to us, the Company hascomplied with the provisions of Section 185 and 186 of the Companies Act, 2013 in respect of theloans and investments made, and guarantees and security provided by it.

v. In our opinion, and according to the information and explanations given to us, the Company hascomplied with the provisions of Sections 73, 74, 75 and 76 or any other relevant provisions of theAct and the Rules framed thereunder to the extent notified, with regard to the deposits acceptedfrom the public. According to the information and explanations given to us, no order has beenpassed by the Company Law Board or National Company Law Tribunal or Reserve Bank of Indiaor any Court or any other Tribunal on the Company in respect of the aforesaid deposits.

Annexure B to Independent Auditors’ ReportReferred to in paragraph 10 of the Independent Auditors’ Report of even date to the members of Jamshedpur Utilities& Services Company Limited on the financial statements for the year ended March 31, 2018Page 2 of 4

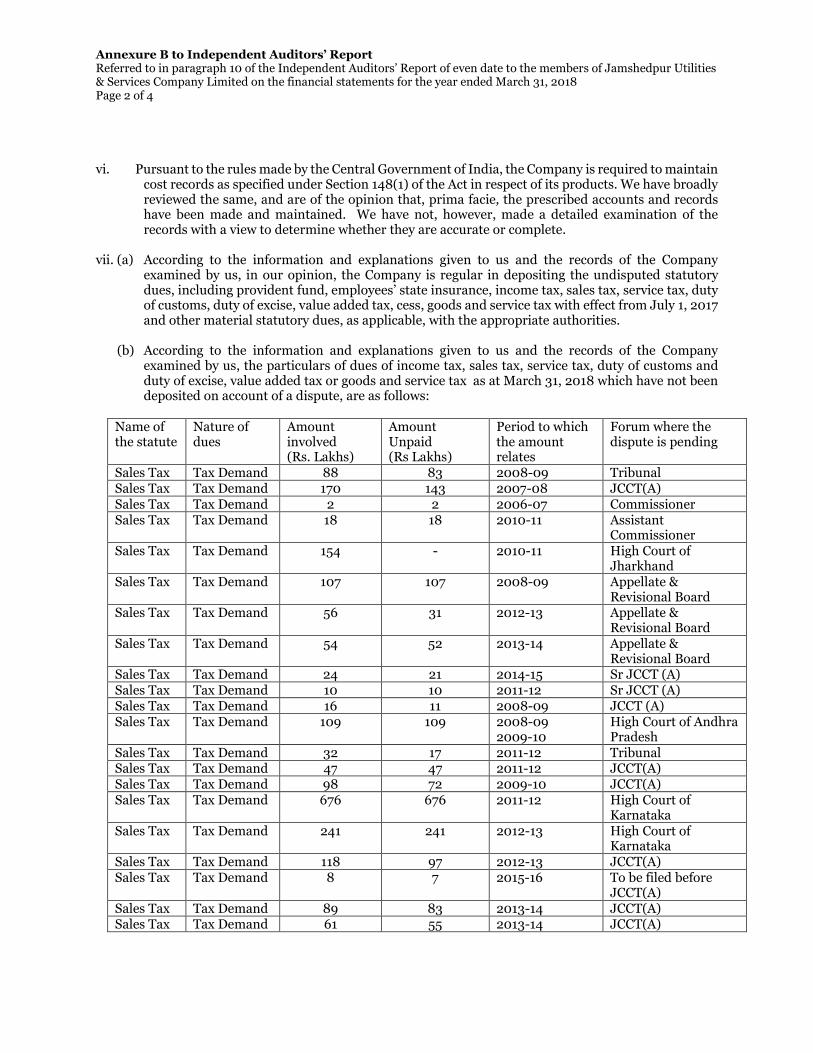

vi. Pursuant to the rules made by the Central Government of India, the Company is required to maintaincost records as specified under Section 148(1) of the Act in respect of its products. We have broadlyreviewed the same, and are of the opinion that, prima facie, the prescribed accounts and recordshave been made and maintained. We have not, however, made a detailed examination of therecords with a view to determine whether they are accurate or complete.

vii. (a) According to the information and explanations given to us and the records of the Companyexamined by us, in our opinion, the Company is regular in depositing the undisputed statutorydues, including provident fund, employees’ state insurance, income tax, sales tax, service tax, dutyof customs, duty of excise, value added tax, cess, goods and service tax with effect from July 1, 2017and other material statutory dues, as applicable, with the appropriate authorities.

(b) According to the information and explanations given to us and the records of the Companyexamined by us, the particulars of dues of income tax, sales tax, service tax, duty of customs andduty of excise, value added tax or goods and service tax as at March 31, 2018 which have not beendeposited on account of a dispute, are as follows:

Name ofthe statute

Nature ofdues

Amountinvolved(Rs. Lakhs)

AmountUnpaid(Rs Lakhs)

Period to whichthe amountrelates

Forum where thedispute is pending

Sales Tax Tax Demand 88 83 2008-09 TribunalSales Tax Tax Demand 170 143 2007-08 JCCT(A)Sales Tax Tax Demand 2 2 2006-07 CommissionerSales Tax Tax Demand 18 18 2010-11 Assistant

CommissionerSales Tax Tax Demand 154 - 2010-11 High Court of

JharkhandSales Tax Tax Demand 107 107 2008-09 Appellate &

Revisional BoardSales Tax Tax Demand 56 31 2012-13 Appellate &

Revisional BoardSales Tax Tax Demand 54 52 2013-14 Appellate &

Revisional BoardSales Tax Tax Demand 24 21 2014-15 Sr JCCT (A)Sales Tax Tax Demand 10 10 2011-12 Sr JCCT (A)Sales Tax Tax Demand 16 11 2008-09 JCCT (A)Sales Tax Tax Demand 109 109 2008-09

2009-10High Court of AndhraPradesh

Sales Tax Tax Demand 32 17 2011-12 TribunalSales Tax Tax Demand 47 47 2011-12 JCCT(A)Sales Tax Tax Demand 98 72 2009-10 JCCT(A)Sales Tax Tax Demand 676 676 2011-12 High Court of

KarnatakaSales Tax Tax Demand 241 241 2012-13 High Court of

KarnatakaSales Tax Tax Demand 118 97 2012-13 JCCT(A)Sales Tax Tax Demand 8 7 2015-16 To be filed before

JCCT(A)Sales Tax Tax Demand 89 83 2013-14 JCCT(A)Sales Tax Tax Demand 61 55 2013-14 JCCT(A)

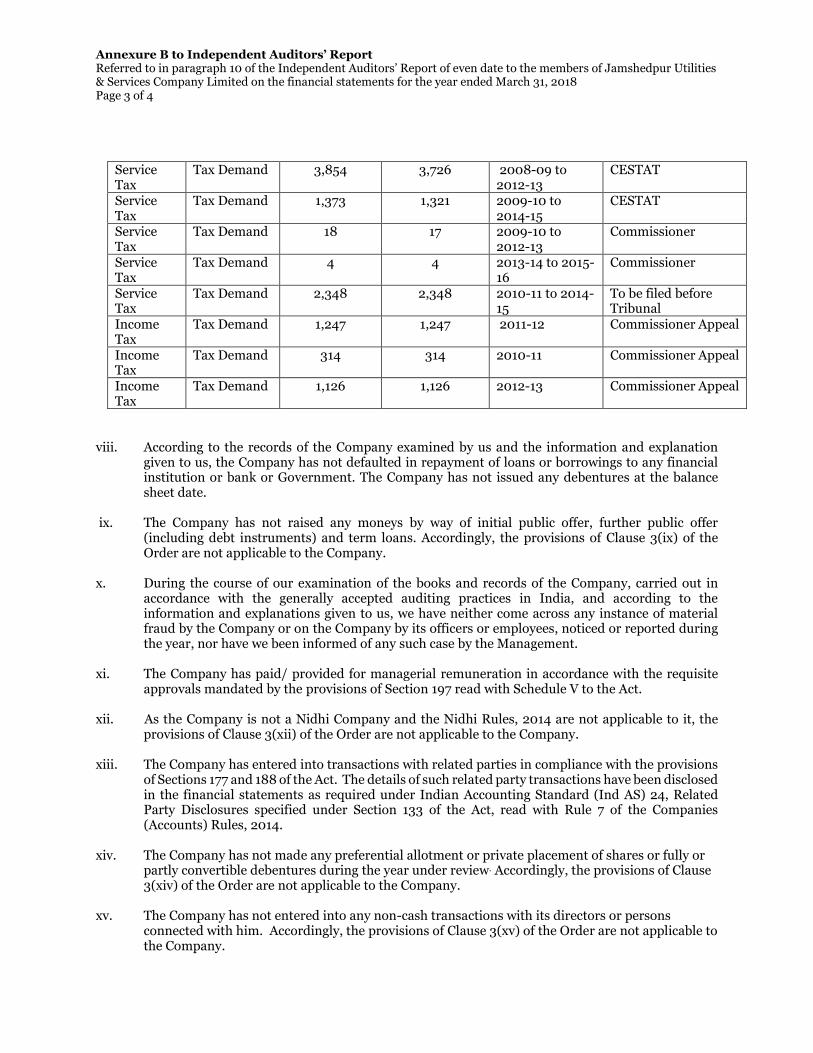

Annexure B to Independent Auditors’ ReportReferred to in paragraph 10 of the Independent Auditors’ Report of even date to the members of Jamshedpur Utilities& Services Company Limited on the financial statements for the year ended March 31, 2018Page 3 of 4

ServiceTax

Tax Demand 3,854 3,726 2008-09 to2012-13

CESTAT

ServiceTax

Tax Demand 1,373 1,321 2009-10 to2014-15

CESTAT

ServiceTax

Tax Demand 18 17 2009-10 to2012-13

Commissioner

ServiceTax

Tax Demand 4 4 2013-14 to 2015-16

Commissioner

ServiceTax

Tax Demand 2,348 2,348 2010-11 to 2014-15

To be filed beforeTribunal

IncomeTax

Tax Demand 1,247 1,247 2011-12 Commissioner Appeal

IncomeTax

Tax Demand 314 314 2010-11 Commissioner Appeal

IncomeTax

Tax Demand 1,126 1,126 2012-13 Commissioner Appeal

viii. According to the records of the Company examined by us and the information and explanationgiven to us, the Company has not defaulted in repayment of loans or borrowings to any financialinstitution or bank or Government. The Company has not issued any debentures at the balancesheet date.

ix. The Company has not raised any moneys by way of initial public offer, further public offer(including debt instruments) and term loans. Accordingly, the provisions of Clause 3(ix) of theOrder are not applicable to the Company.

x. During the course of our examination of the books and records of the Company, carried out inaccordance with the generally accepted auditing practices in India, and according to theinformation and explanations given to us, we have neither come across any instance of materialfraud by the Company or on the Company by its officers or employees, noticed or reported duringthe year, nor have we been informed of any such case by the Management.

xi. The Company has paid/ provided for managerial remuneration in accordance with the requisiteapprovals mandated by the provisions of Section 197 read with Schedule V to the Act.

xii. As the Company is not a Nidhi Company and the Nidhi Rules, 2014 are not applicable to it, theprovisions of Clause 3(xii) of the Order are not applicable to the Company.

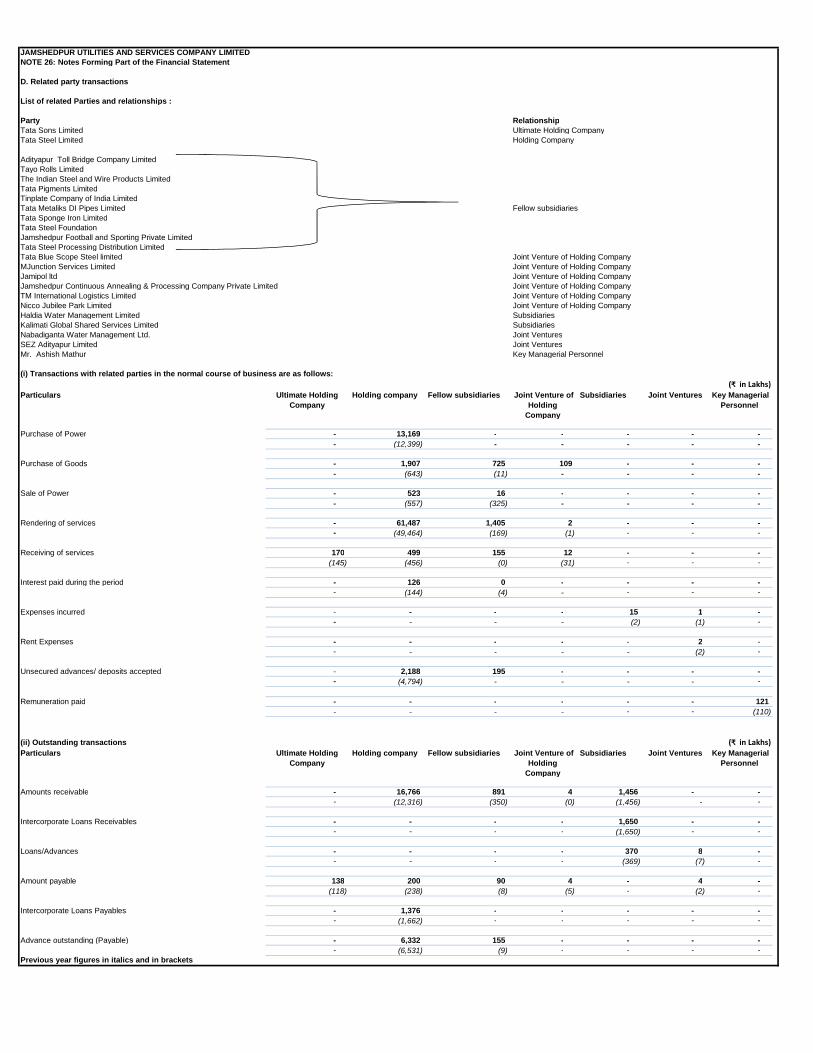

xiii. The Company has entered into transactions with related parties in compliance with the provisionsof Sections 177 and 188 of the Act. The details of such related party transactions have been disclosedin the financial statements as required under Indian Accounting Standard (Ind AS) 24, RelatedParty Disclosures specified under Section 133 of the Act, read with Rule 7 of the Companies(Accounts) Rules, 2014.

xiv. The Company has not made any preferential allotment or private placement of shares or fully orpartly convertible debentures during the year under review. Accordingly, the provisions of Clause3(xiv) of the Order are not applicable to the Company.

xv. The Company has not entered into any non-cash transactions with its directors or personsconnected with him. Accordingly, the provisions of Clause 3(xv) of the Order are not applicable tothe Company.

Annexure B to Independent Auditors’ ReportReferred to in paragraph 10 of the Independent Auditors’ Report of even date to the members of Jamshedpur Utilities& Services Company Limited on the financial statements for the year ended March 31, 2018Page 4 of 4

xvi. The Company is not required to be registered under Section 45-IA of the Reserve Bank of IndiaAct, 1934. Accordingly, the provisions of Clause 3(xvi) of the Order are not applicable to theCompany.

For Price Waterhouse & Co Chartered Accountants LLPFirm Registration Number: FRN 304026E / E 300009Chartered Accountants

Avijit MukerjiKolkata PartnerApril 16, 2018 Membership Number 056155

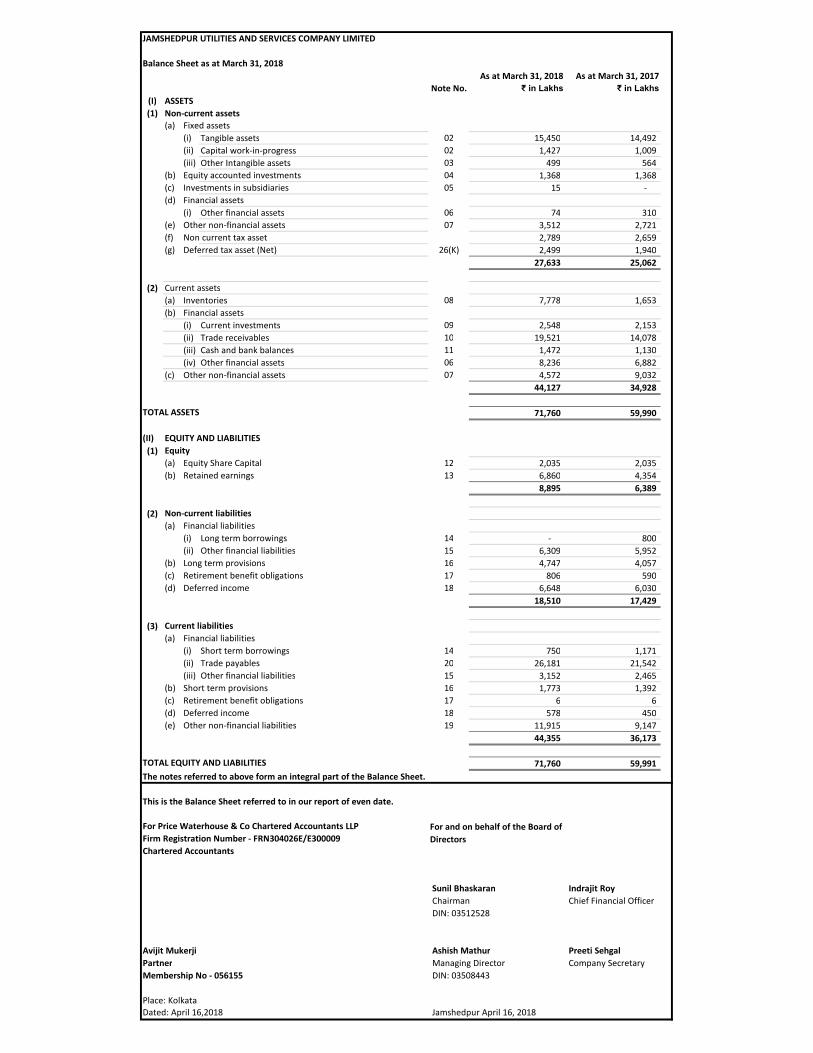

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITED

Balance Sheet as at March 31, 2018

As at March 31, 2018 As at March 31, 2017

Note No. ₹ in Lakhs ₹ in Lakhs

(I) ASSETS

(1) Non-current assets

(a) Fixed assets

(i) Tangible assets 02 15,450 14,492

(ii) Capital work-in-progress 02 1,427 1,009

(iii) Other Intangible assets 03 499 564

(b) Equity accounted investments 04 1,368 1,368

(c) Investments in subsidiaries 05 15 -

(d) Financial assets

(i) Other financial assets 06 74 310

(e) Other non-financial assets 07 3,512 2,721

(f) Non current tax asset 2,789 2,659

(g) Deferred tax asset (Net) 26(K) 2,499 1,940

27,633 25,062

(2) Current assets

(a) Inventories 08 7,778 1,653

(b) Financial assets

(i) Current investments 09 2,548 2,153

(ii) Trade receivables 10 19,521 14,078

(iii) Cash and bank balances 11 1,472 1,130

(iv) Other financial assets 06 8,236 6,882

(c) Other non-financial assets 07 4,572 9,032

44,127 34,928

TOTAL ASSETS 71,760 59,990

(II) EQUITY AND LIABILITIES

(1) Equity

(a) Equity Share Capital 12 2,035 2,035

(b) Retained earnings 13 6,860 4,354

8,895 6,389

(2) Non-current liabilities

(a) Financial liabilities

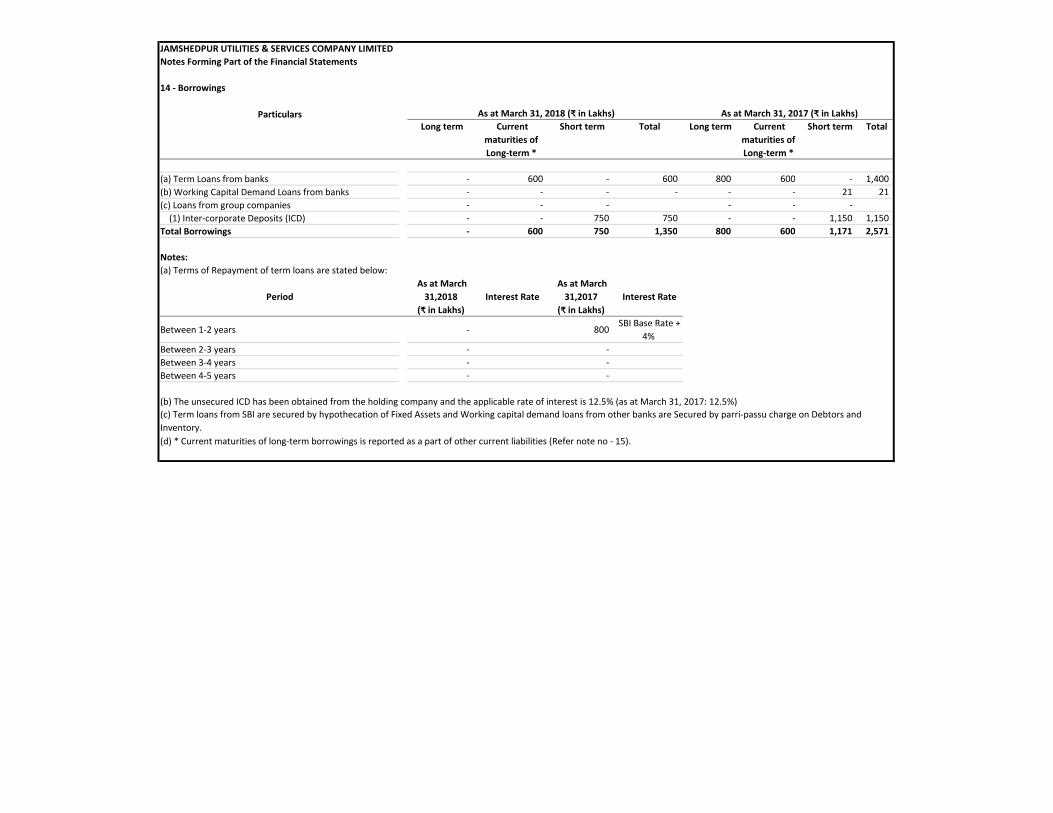

(i) Long term borrowings 14 - 800

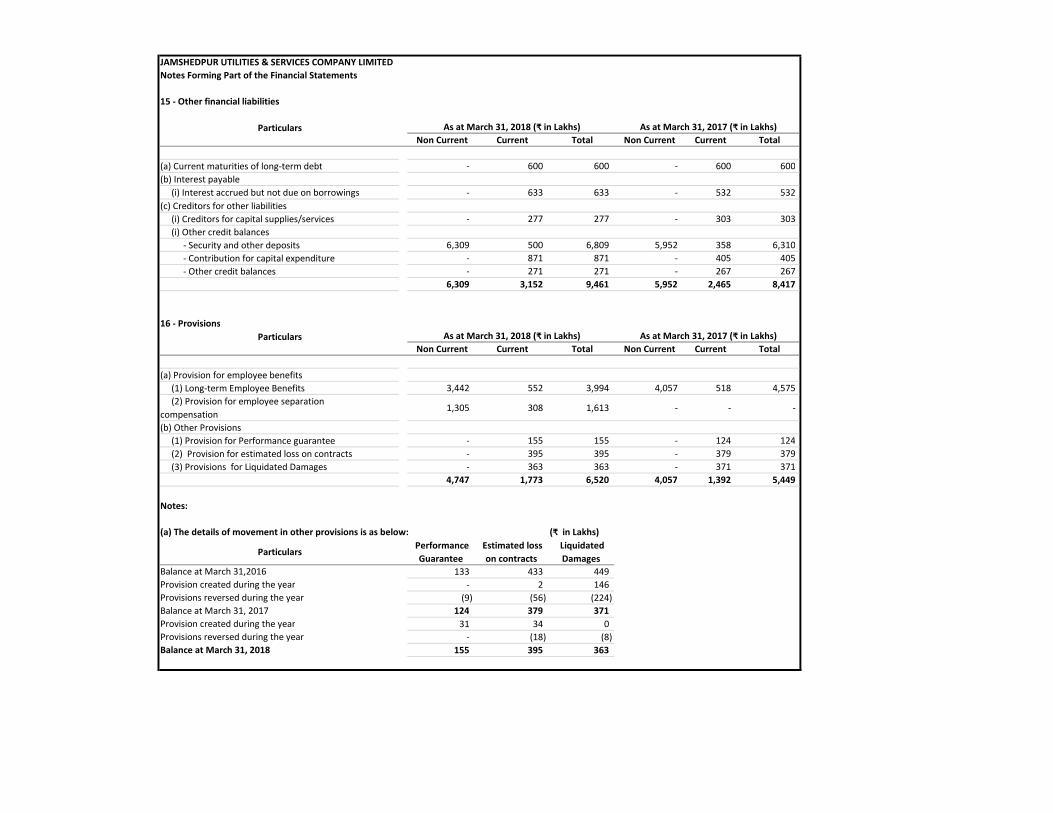

(ii) Other financial liabilities 15 6,309 5,952

(b) Long term provisions 16 4,747 4,057

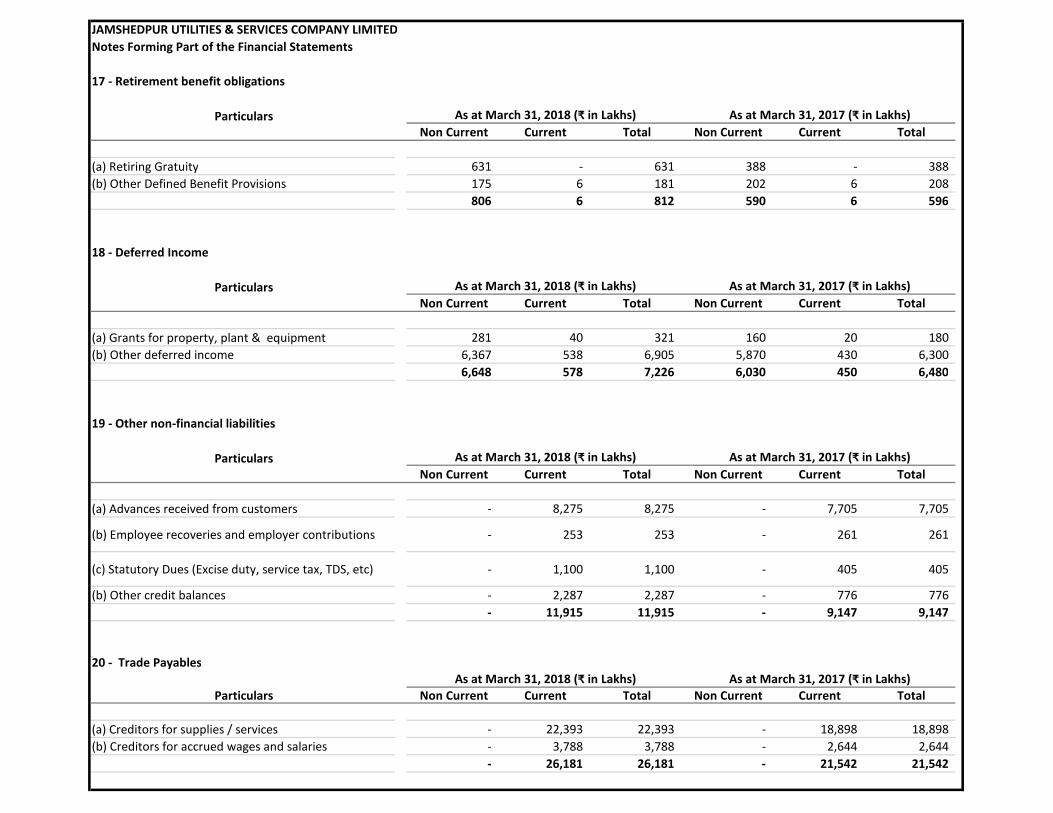

(c) Retirement benefit obligations 17 806 590

(d) Deferred income 18 6,648 6,030

18,510 17,429

(3) Current liabilities

(a) Financial liabilities

(i) Short term borrowings 14 750 1,171

(ii) Trade payables 20 26,181 21,542

(iii) Other financial liabilities 15 3,152 2,465

(b) Short term provisions 16 1,773 1,392

(c) Retirement benefit obligations 17 6 6

(d) Deferred income 18 578 450

(e) Other non-financial liabilities 19 11,915 9,147

44,355 36,173

TOTAL EQUITY AND LIABILITIES 71,760 59,991

The notes referred to above form an integral part of the Balance Sheet.

This is the Balance Sheet referred to in our report of even date.

For Price Waterhouse & Co Chartered Accountants LLP

Firm Registration Number - FRN304026E/E300009

Chartered Accountants

Sunil Bhaskaran Indrajit Roy

Chairman Chief Financial Officer

DIN: 03512528

Avijit Mukerji Ashish Mathur Preeti Sehgal

Partner Managing Director Company Secretary

Membership No - 056155 DIN: 03508443

Place: Kolkata

Dated: April 16,2018 Jamshedpur April 16, 2018

For and on behalf of the Board of

Directors

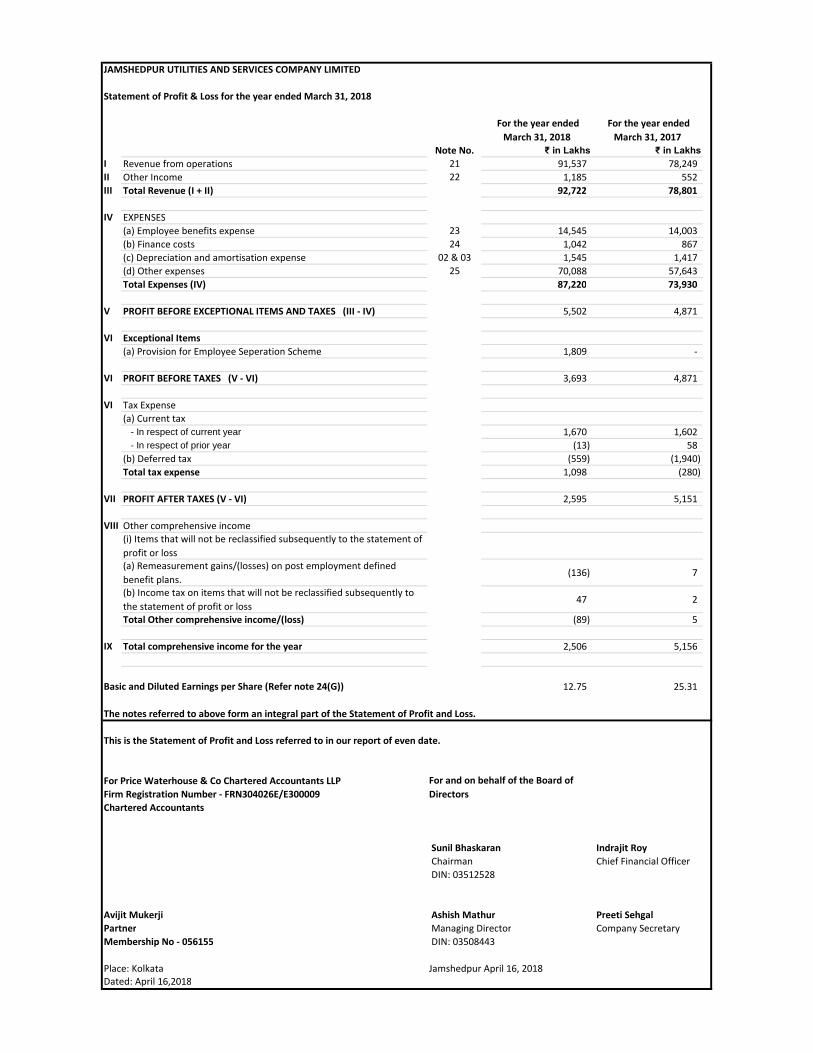

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITED

Statement of Profit & Loss for the year ended March 31, 2018

For the year ended

March 31, 2018

For the year ended

March 31, 2017

Note No. ₹ in Lakhs ₹ in Lakhs

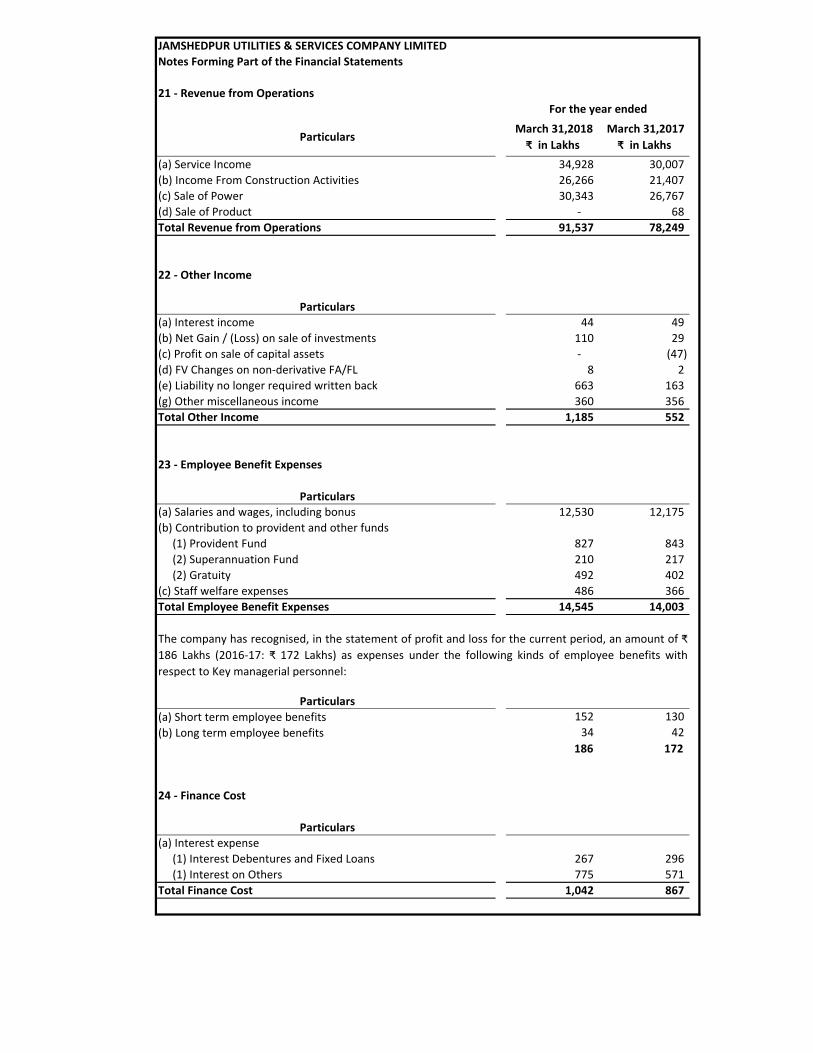

I Revenue from operations 21 91,537 78,249

II Other Income 22 1,185 552

III Total Revenue (I + II) 92,722 78,801

IV EXPENSES

(a) Employee benefits expense 23 14,545 14,003

(b) Finance costs 24 1,042 867

(c) Depreciation and amortisation expense 02 & 03 1,545 1,417

(d) Other expenses 25 70,088 57,643

Total Expenses (IV) 87,220 73,930

V PROFIT BEFORE EXCEPTIONAL ITEMS AND TAXES (III - IV) 5,502 4,871

VI Exceptional Items

(a) Provision for Employee Seperation Scheme 1,809 -

VI PROFIT BEFORE TAXES (V - VI) 3,693 4,871

VI Tax Expense

(a) Current tax

- In respect of current year 1,670 1,602

- In respect of prior year (13) 58

(b) Deferred tax (559) (1,940)

Total tax expense 1,098 (280)

VII PROFIT AFTER TAXES (V - VI) 2,595 5,151

VIII Other comprehensive income

(i) Items that will not be reclassified subsequently to the statement of

profit or loss(a) Remeasurement gains/(losses) on post employment defined

benefit plans.(136) 7

(b) Income tax on items that will not be reclassified subsequently to

the statement of profit or loss47 2

Total Other comprehensive income/(loss) (89) 5

IX Total comprehensive income for the year 2,506 5,156

Basic and Diluted Earnings per Share (Refer note 24(G)) 12.75 25.31

The notes referred to above form an integral part of the Statement of Profit and Loss.

This is the Statement of Profit and Loss referred to in our report of even date.

For Price Waterhouse & Co Chartered Accountants LLP

Firm Registration Number - FRN304026E/E300009

Chartered Accountants

Sunil Bhaskaran Indrajit Roy

Chairman Chief Financial Officer

DIN: 03512528

Avijit Mukerji Ashish Mathur Preeti Sehgal

Partner Managing Director Company Secretary

Membership No - 056155 DIN: 03508443

Place: Kolkata Jamshedpur April 16, 2018Dated: April 16,2018

For and on behalf of the Board of

Directors

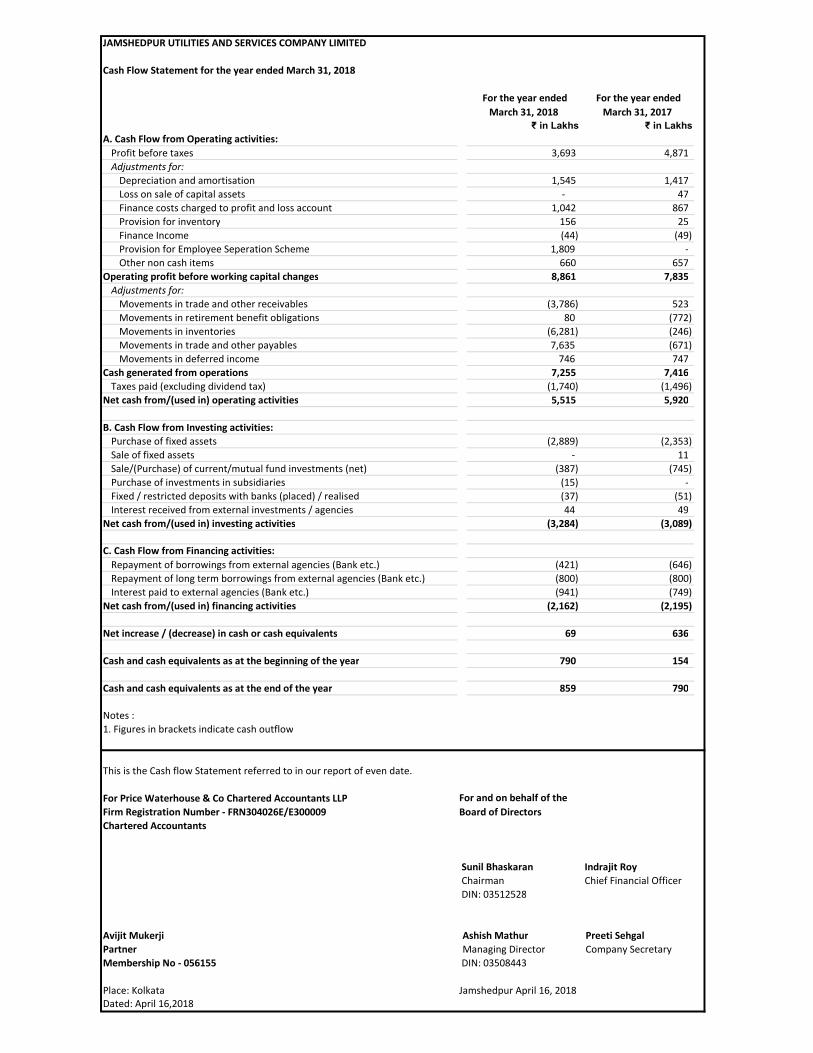

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITED

Cash Flow Statement for the year ended March 31, 2018

For the year ended

March 31, 2018

For the year ended

March 31, 2017 ₹ in Lakhs ₹ in Lakhs

A. Cash Flow from Operating activities:

Profit before taxes 3,693 4,871

Adjustments for:

Depreciation and amortisation 1,545 1,417

Loss on sale of capital assets - 47

Finance costs charged to profit and loss account 1,042 867

Provision for inventory 156 25

Finance Income (44) (49)

Provision for Employee Seperation Scheme 1,809 -

Other non cash items 660 657

Operating profit before working capital changes 8,861 7,835

Adjustments for:

Movements in trade and other receivables (3,786) 523

Movements in retirement benefit obligations 80 (772)

Movements in inventories (6,281) (246)

Movements in trade and other payables 7,635 (671)

Movements in deferred income 746 747

Cash generated from operations 7,255 7,416

Taxes paid (excluding dividend tax) (1,740) (1,496)

Net cash from/(used in) operating activities 5,515 5,920

B. Cash Flow from Investing activities:

Purchase of fixed assets (2,889) (2,353)

Sale of fixed assets - 11

Sale/(Purchase) of current/mutual fund investments (net) (387) (745)

Purchase of investments in subsidiaries (15) -

Fixed / restricted deposits with banks (placed) / realised (37) (51)

Interest received from external investments / agencies 44 49

Net cash from/(used in) investing activities (3,284) (3,089)

C. Cash Flow from Financing activities:

Repayment of borrowings from external agencies (Bank etc.) (421) (646)

Repayment of long term borrowings from external agencies (Bank etc.) (800) (800)

Interest paid to external agencies (Bank etc.) (941) (749)

Net cash from/(used in) financing activities (2,162) (2,195)

Net increase / (decrease) in cash or cash equivalents 69 636

Cash and cash equivalents as at the beginning of the year 790 154

Cash and cash equivalents as at the end of the year 859 790

Notes :

1. Figures in brackets indicate cash outflow

This is the Cash flow Statement referred to in our report of even date.

For Price Waterhouse & Co Chartered Accountants LLP

Firm Registration Number - FRN304026E/E300009

Chartered Accountants

Sunil Bhaskaran Indrajit Roy

Chairman Chief Financial Officer

DIN: 03512528

Avijit Mukerji Ashish Mathur Preeti Sehgal

Partner Managing Director Company Secretary

Membership No - 056155 DIN: 03508443

Place: Kolkata Jamshedpur April 16, 2018Dated: April 16,2018

For and on behalf of the

Board of Directors

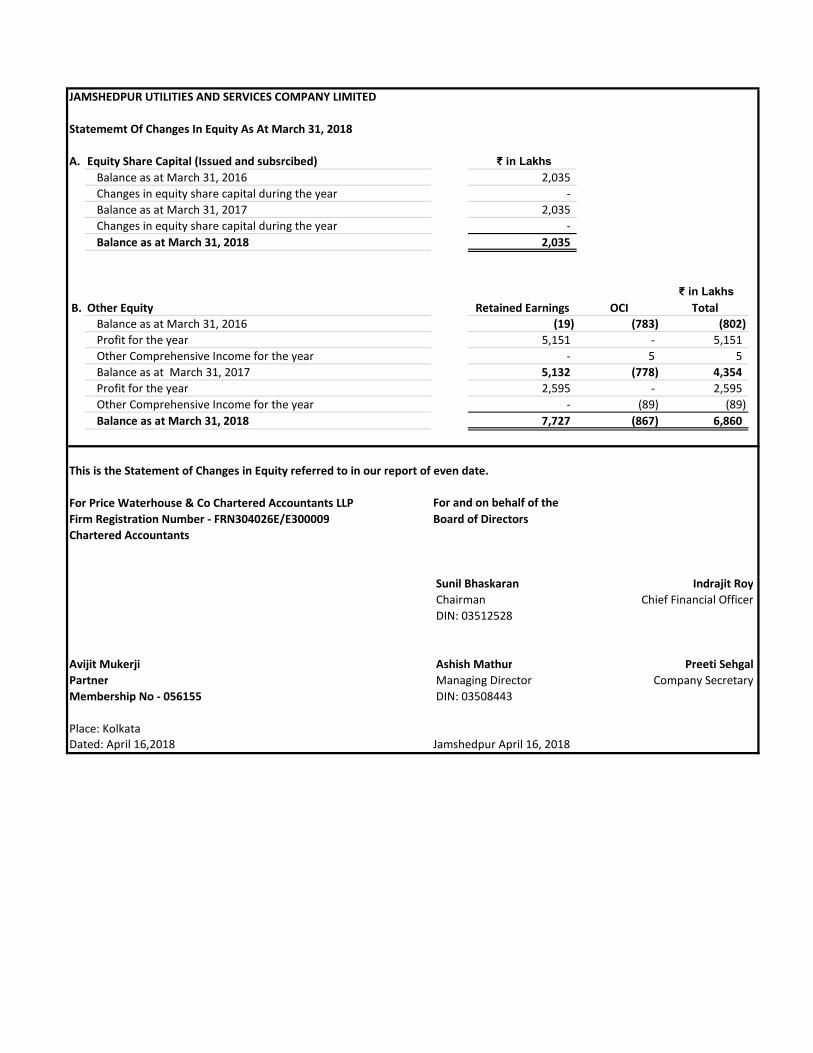

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITED

Statememt Of Changes In Equity As At March 31, 2018

A. Equity Share Capital (Issued and subsrcibed) ₹ in Lakhs

Balance as at March 31, 2016 2,035

Changes in equity share capital during the year -

Balance as at March 31, 2017 2,035

Changes in equity share capital during the year -

Balance as at March 31, 2018 2,035

₹ in Lakhs

B. Other Equity Retained Earnings OCI Total

Balance as at March 31, 2016 (19) (783) (802)

Profit for the year 5,151 - 5,151

Other Comprehensive Income for the year - 5 5

Balance as at March 31, 2017 5,132 (778) 4,354

Profit for the year 2,595 - 2,595

Other Comprehensive Income for the year - (89) (89)

Balance as at March 31, 2018 7,727 (867) 6,860

This is the Statement of Changes in Equity referred to in our report of even date.

For Price Waterhouse & Co Chartered Accountants LLP

Firm Registration Number - FRN304026E/E300009

Chartered Accountants

Sunil Bhaskaran Indrajit Roy

Chairman Chief Financial Officer

DIN: 03512528

Avijit Mukerji Ashish Mathur Preeti Sehgal

Partner Managing Director Company Secretary

Membership No - 056155 DIN: 03508443

Place: KolkataDated: April 16,2018 Jamshedpur April 16, 2018

For and on behalf of the

Board of Directors

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITEDNote 1: Significant Accounting Policies

(1) Company Information

Jamshedpur Utilities and Services Company Limited (‘JUSCO’ or ‘the Company’) is a public limited Company

incorporated in India with its registered office in Jamshedpur, Jharkhand, India.

JUSCO is India’s first private sector comprehensive urban infrastructure service provider. Carved out of Tata Steel in

2004, it has the legacy of over ten decades of experience in providing these services-water, waste water, power

distribution, municipal solid waste management and town planning- at Jamshedpur.

The financial statements for the year ended March 31, 2018 were approved by the board of directors and authorised forissue on April 16, 2018.

The significant accounting policies applied by the Company in the preparation of its financial statements are listed below.Such accounting policies have been applied consistently to all the periods presented in these financial statements.

(2) Basis for preparation

The financial statements have been prepared under the historical cost convention with the exception of certain assets and

liabilities that are required to be carried at fair values by Ind-AS.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction betweenmarket participants at the measurement date.

(3) Use of estimates and critical accounting judgments

In preparation of the financial statements, the Company makes judgments, estimates and assumptions about the carryingvalues of assets and liabilities that are not readily apparent from other sources. The estimates and the associatedassumptions are based on historical experience and other factors that are considered to be relevant. Actual results maydiffer from these estimates.

The estimates and the underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates arerecognised in the period in which the estimate is revised and future periods affected.

Significant judgments and estimates relating to the carrying values of assets and liabilities include useful lives of property,plant and equipment and intangible assets, impairment of property, plant and equipment, intangible assets andinvestments, provision for employee benefits and other provisions, recoverability of deferred tax assets, commitments andcontingencies.

(4) Intangible Assets (excluding goodwill)

Licenses and software costs are included in the balance sheet as intangible assets where they are clearly linked to long

term economic benefits for the company. In this case they are measured initially at purchase cost and then amortized on a

straight-line basis over their estimated useful lives. All other costs on Licenses and software are expensed in the

statement of profit and loss as incurred.

(5) Property, plant and equipment

An item of property, plant and equipment is recognized as an asset if it is probable that future economic benefits

associated with the item will flow to the company and its cost can be measured reliably. This recognition principle is

applied to the costs incurred initially to acquire an item of property, plant and equipment and also to costs incurred

subsequently to add to, replace part of, or service it. All other repair and maintenance costs, including regular servicing,

are recognized in the statement of profit and loss as incurred. When a replacement occurs, the carrying amount of the

replaced part is derecognized. Where an item of Property, plant and equipment comprises major component having

different useful lives, these components are accounted for as separate items.

Property, plant and equipment are stated at cost, less accumulated depreciation and impairment losses. Cost includes all

direct costs and expenditures incurred to bring the asset to its working condition and location for its intended use.

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITEDNote 1: Significant Accounting Policies

The gain or loss arising on disposal of an asset is determined as the difference between the sale proceeds and the

carrying amount of the asset, and is recognized in the statement of profit and loss.

(6) Depreciation and amortization of property, plant and equipment and intangible assets

Depreciation or amortization is provided so as to write off, on a straight-line basis, the cost of property, plant and

equipment and other intangible assets, including those held under finance leases to their residual value. These charges

are commenced from the dates the assets are available for their intended use and are spread over their estimated useful

economic lives or, in the case of leased assets, over the lease period if shorter. The estimated useful lives of assets and

residual values are reviewed regularly and, when necessary, revised. No further charge is provided in respect of assets

that are fully written down but are still in use. For Tangible and Intangible Property, plant and equipment of power

business depreciation is provided on straight line basis at the rates specified in Electricity Act, 2003

Depreciation on assets under construction commences only when the assets are ready for their intended use.

The estimated useful lives for the main categories of property, plant and equipment and other intangible assets are:

(i) Leasehold buildings – over the remaining lease

(ii) Plant and Machinery – 6 to 40 years

(iii) Furniture, fixture and office equipment – 3 to 25 years

(iv) Vehicles– 4 to 20 years

(v) Computer software – maximum 8 years

Assets value upto ₹5,000 are fully depreciated in the year of acquisition.

(7) Impairment

At each balance sheet date, the company reviews the carrying amounts of its property, plant and equipment and

intangible assets to determine whether there is any indication that the carrying amount of those assets may not be

recoverable through continuing use. If any such indication exists, the recoverable amount of the asset is reviewed in order

to determine the extent of impairment loss (if any). Where the asset does not generate cash flows that are independent

from other assets, the company estimates the recoverable amount of the cash generating unit to which the asset belongs.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated

future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market

assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows

have not been adjusted. An impairment loss is recognized in the statement of profit and loss as and when the carrying

amount of an asset exceeds its recoverable amount.

Where an impairment loss subsequently reverses, the carrying amount of the asset is increased to the revised estimate of

its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have

been determined had no impairment loss been recognized for the asset in prior years. A reversal of an impairment loss is

recognized as income immediately.

(8) Leases

The company determines whether an arrangement contains a lease by assessing whether the fulfillment of a transaction

is dependent on the use of a specific asset and whether the transaction conveys the right to use that asset to the

company in return for payment. Where this occurs, the arrangement is deemed to include a lease and is accounted for

either as finance or operating lease.

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITEDNote 1: Significant Accounting Policies

Leases are classified as finance leases where the terms of the lease transfer substantially all the risks and rewards of

ownership to the lessee. All other leases are classified as operating leases.

The company as lessee

i) Operating lease – Rentals payable under operating leases are charged to the statement of profit and loss in a

straight line basis over the term of the relevant lease unless another systematic basis is more representative of the time

pattern in which economic benefits from the leased asset are consumed. Contingent rentals arising under operating

leases are recognized as an expense in the period in which they are incurred.

In the event that lease incentives are received to enter into operating leases, such incentives are recognized as a liability.

The aggregate benefit of incentives is recognized as a reduction of rental expense on a straight line basis, except where

another systematic basis is more representative of the time pattern in which economic benefits from the leased asset are

consumed.

ii) Finance lease – Finance leases are capitalized at the commencement of lease, at the lower of the fair value of the

property or the present value of the minimum lease payments. The corresponding liability to the lessor is included in the

balance sheet as a finance lease obligation. Lease payments are apportioned between finance charges and reduction of

the lease obligation so as to achieve a constant rate of interest on the remaining balance of the liability. Finance charges

are charged directly against income over the period of the lease.

The company as lessor

i) Operating lease – Rental income from operating leases is recognized in the statement of profit and loss on a straight

line basis over the term of the relevant lease unless another systematic basis is more representative of the time pattern in

which economic benefits from the leased asset is diminished. Initial direct costs incurred in negotiating and arranging an

operating lease are added to the carrying amount of the leased asset and recognized on a straight line basis over the

lease term.

ii) Finance lease – When assets are leased out under a finance lease, the present value of the minimum lease

payments is recognized as a receivable. The difference between the gross receivable and the present value of the

receivable is recognized as unearned finance income. Lease income is recognized over the term of the lease using the

net investment method before tax, which reflects a constant periodic rate of return.

(9) Financial Instruments

Financial assets and financial liabilities are recognized when the company becomes a party to the contractual provisions

of the instrument. Financial assets and liabilities are initially measured at fair value. Transaction costs that are directly

attributable to the acquisition or issue of financial assets and financial liabilities (other than financial assets and financial

liabilities at fair value through profit or loss) are added to or deducted from the fair value measured on initial recognition of

financial asset or financial liability. The transaction costs directly attributable to the acquisition of financial assets and

financial liabilities at fair value through profit and loss are immediately recognized in the statement of profit and loss.

Effective interest method

The effective interest method is a method of calculating the amortized cost of a financial instrument and of allocating

interest income or expense over the relevant period. The effective interest rate is the rate that exactly discounts future

cash receipts or payments through the expected life of the financial instrument, or where appropriate, a shorter period.

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITEDNote 1: Significant Accounting Policies

a) Financial assets

Cash and Bank Balances

Cash and bank balances consist of:

i) Cash and cash equivalents - which includes cash in hand, deposits held at call with banks and other short termdeposits which are readily convertible into known amounts of cash, are subject to an insignificant risk of change invalue and have maturities of less than one year from the date of such deposits. These balances with banks areunrestricted for withdrawal and usage.

ii) Other bank balances - which includes balances and deposits with banks that are restricted for withdrawal and

usage.

Financial assets at amortized cost

Financial assets are subsequently measured at amortized cost if these financial assets are held within a business model

whose objective is to hold these assets in order to collect contractual cash flows and the contractual terms of the financial

asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount

outstanding.

Financial assets measured at fair value

Financial assets are measured at fair value through other comprehensive income if these financial assets are held within

a business model whose objective is to hold these assets in order to collect contractual cash flows or to sell these

financial assets and the contractual terms of the financial asset give rise on specified dates to cash flows that are solely

payments of principal and interest on the principal amount outstanding.

Financial asset not measured at amortized cost or at fair value through other comprehensive income is carried at fair

value through profit or loss.

Impairment of financial assets

Loss allowance for expected credit losses is recognized for financial assets measured at amortized cost and fair valuethrough other comprehensive income.

The Company recognises life time expected credit losses for all trade receivables that do not constitute a financingtransaction.

For financial assets whose credit risk has not significantly increased since initial recognition, loss allowance equal totwelve months expected credit losses is recognised. Loss allowance equal to the lifetime expected credit losses isrecognised if the credit risk on the financial instruments has significantly increased since initial recognition.

Derecognition of financial assets

The company derecognizes a financial asset only when the contractual rights to the cash flows from the asset expire, or it

transfers the financial asset and substantially all risks and rewards of ownership of the asset to another entity. If the

company neither transfers nor retains substantially all the risks and rewards of ownership and continues to control the

transferred asset, the company recognizes its retained interest in the assets and an associated liability for amounts it may

have to pay. If the company retains substantially all the risks and rewards of ownership of a transferred financial asset, the

company continues to recognize the financial asset and also recognizes a collateralized borrowing of the proceeds

received.

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITEDNote 1: Significant Accounting Policies

b) Financial liabilities and equity instruments

Financial Liabilities

Trade and other payables are initially measured at fair value, net of transaction costs, and are subsequently measured at

amortized cost, using the effective interest rate method.

Interest-bearing bank loans, overdrafts and issued debt are initially measured at fair value and are subsequently

measured at amortized cost using the effective interest rate method. Any difference between the proceeds (net of

transaction costs) and the settlement or redemption of borrowings is recognized over the term of the borrowings in

accordance with the company’s accounting policy for borrowing costs.

Derecognition of financial liabilities

The company derecognizes financial liabilities when, and only when, the company obligations are discharged, cancelled

or they expire.

(10) Retirement benefit costs

Payments to defined contribution plans are charged as an expense as they fall due. Payments made to state managed

retirement benefit schemes are dealt with as payments to defined contribution schemes where the Company’s obligations

under the schemes are equivalent to those arising in a defined contribution retirement benefit scheme.

For defined benefit retirement schemes the cost of providing benefits is determined using the Projected Unit Credit

Method, with actuarial valuation being carried out at each balance sheet date. Re-measurement gains and losses of the

net defined benefit liability/ (asset) are recognized immediately in other comprehensive income. The service cost, net

interest on the net defined benefit liability/ (asset) is treated as a net expense within employment costs.

Past service cost is recognized as an expense when the plan amendment or curtailment occurs or when any related

restructuring costs or termination benefits are recognized, whichever is earlier.

The retirement benefit obligation recognized in the balance sheet represents the present value of the defined-benefit

obligation as reduced by the fair value plan assets.

(11) Taxation

Tax expense for the year comprises current and deferred tax.

The tax currently payable is based on taxable profit for the year. Taxable profit differs from net profit as reported in the

statement of profit and loss because it excludes items of income or expense that are taxable or deductible in other years

and it further excludes items that are never taxable or deductible. The company’s liability for current tax is calculated using

tax rates and tax laws that have been enacted or substantively enacted in countries where the Company operates by the

end of the reporting period.

Deferred tax is the tax expected to be payable or recoverable on differences between the carrying amounts of assets and

liabilities in the financial statements and the corresponding tax bases used in the computation of taxable profit, and is

accounted for using the balance sheet liability method. Deferred tax liabilities are generally recognized for all taxable

temporary differences. In contrast, deferred tax assets are only recognized to the extent that it is probable that future

taxable profits will be available against which the temporary differences can be utilized.

The carrying amount of deferred tax assets is reviewed at the end of each reporting period and reduced to the extent that

it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered.

Deferred tax is calculated at the tax rates that are expected to apply in the period when the liability is settled or the asset

is realized based on the tax rates and tax laws that have been enacted or substantially enacted by the end of the reporting

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITEDNote 1: Significant Accounting Policies

period. The measurement of deferred tax liabilities and assets reflects the tax consequences that would follow from the

manner in which the company expects, at the end of the reporting period, to cover or settle the carrying amount of its

assets and liabilities.

Deferred tax assets and liabilities are offset to the extent that they relate to taxes levied by the same tax authority andthere are legally enforceable rights to set off current tax assets and current tax liabilities within that jurisdiction.

Current and deferred tax are recognized as an expense or income in the statement of profit and loss, except when they

relate to items credited or debited either in other comprehensive income or directly in equity, in which case the tax is also

recognized in other comprehensive income or directly in equity.

(12) Inventories

Inventories are stated at the lower of cost and net realizable value. Costs comprise direct materials and, where applicable,

direct labor costs and those overheads that have been incurred in bringing the inventories to their present location and

condition. Net realizable value is the price at which the inventories can be realized in the normal course of business after

allowing for the cost of conversion from their existing state to a finished condition and for the cost of marketing, selling and

distribution.

(13) Onerous contracts

A provision for onerous contracts is recognised when the expected benefits to be derived by the Company from a contract

are lower than the unavoidable cost of meeting its obligations under the contract. The provision is measured at the

present value of the lower of the expected cost of terminating the contract and the expected net cost of continuing with the

contract. Before a provision is established, the Company recognises any impairment loss on the assets associated with

that contract.

(14) Provisions

Provisions are recognized in the balance sheet when the company has a present obligation (legal or constructive) as a

result of a past event, which is expected to result in an outflow of resources embodying economic benefits which can be

reliably estimated. Each provision is based on the best estimate of the expenditure required to settle the present

obligation at the balance sheet date.

Constructive obligation is an obligation that derives from an entity’s actions where:

(a) by an established pattern of past practice, published policies or a sufficiently specific current statement, the entity has

indicated to other parties that it will accept certain responsibilities; and

(b) As a result, the entity has created a valid expectation on the part of those other parties that it will discharge those

responsibilities.

(15) Contribution from Customers

Contribution received from consumers towards installation of assets pertaining to distribution of power and water,are credited to Deferred Income on capitalization of related assets . An amount in proportion to the depreciation chargefor the year on such assets is transferred to the statement of profit and loss.

(16) Government grants

Government grants related to expenditure on property, plant and equipment are credited to the statement of profit and

loss over the useful lives of qualifying assets. Total grants received less the amounts credited to the statement of profit

and loss at the balance sheet date are included in the balance sheet as deferred income.

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITEDNote 1: Significant Accounting Policies

(17) Insurance

Insurance premiums in respect of insurance placed and reinsurance premiums in respect of risks are charged to the

statement of profit and loss in the period to which they relate.

(18) Revenue

Income from Services

Income from Service is recognized on accrual basis on rendering of the services and excludes service tax.

Income from Sale of Power

Income from sale of power is recognized on accrual basis (billed revenue) on rendering of services and excludes

electricity duty.

Revenue from Construction Contracts

When the outcome of a construction contract can be estimated reliably, contract revenue and contract costs associatedwith the construction contract are recognized as revenue and expenses respectively by reference to the percentage ofcompletion of the contract activity at the reporting date. The percentage of completion of a contract is determinedconsidering the proportion that contract costs incurred for work performed upto the reporting date bear to the estimatedtotal contract costs

For the purposes of recognizing revenue, contract revenue comprises the initial amount of revenue agreed in the contract,the variations in contract work, claims and incentive payments to the extent that it is probable that they will result inrevenue and they are capable of being reliably measured.

The percentage of completion method is applied on a cumulative basis in each accounting period to the current estimatesof contract revenue and contract costs. The effect of a change in the estimate of contract revenue or contract costs, or theeffect of a change in the estimate of the outcome of a contract, is accounted for as a change in accounting estimate andthe effect of which are recognized in the Statement of Profit and Loss in the period in which the change is made and insubsequent periods.

When the outcome of a construction contract cannot be estimated reliably, revenue is recognized only to the extent ofcontract costs incurred of which recovery is probable and the related contract costs are recognized as an expense in theperiod in which they are incurred.

When it is probable that total contract costs will exceed total contract revenue, the expected loss is recognized as anexpense in the Statement of Profit and Loss in the period in which such probability occurs.

Sale of Goods

Sales are recognized on transfer of significant risks and rewards of ownership to the buyer, which generally coincides withthe delivery of goods to customers. Sales include excise duty but exclude sales tax and value added tax.

Interest income

Interest income is accrued on a time proportion basis, by reference to the principal outstanding and the effective interest

rate applicable.

(19) Foreign currency transactions and translation

The financial statements of the company are presented in INR, which are the functional currency of the company and the

presentation currency for the financial statements.

JAMSHEDPUR UTILITIES AND SERVICES COMPANY LIMITEDNote 1: Significant Accounting Policies

In preparing the individual financial statements of the individual entities, transactions in currencies other than the entity’s

functional currency are recorded at the rates of exchange prevailing on the date of the transaction. At the end of each

reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at the end of

the reporting period. Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated

at the rates prevailing on the date when the fair value was determined. Non-monetary items that are measured in terms of

historical cost in a foreign currency are not translated.

(20) Borrowing Costs

Borrowings costs directly attributable to the acquisition, construction or production of qualifying assets, which are assets

that necessarily take a substantial period of time to get ready for their intended use or sale are added to the cost of those

assets, until such time as the assets are substantially ready for the intended use or sale. Investment income earned on

the temporary investment of specific borrowings pending their expenditure on qualifying assets is deducted from the

borrowing costs eligible for capitalization.

(21) Earnings per Share

Basic EPS amounts are calculated by dividing the profit for the year attributable to equity holders of the company by the

weighted average number of Equity shares outstanding during the year.

Diluted EPS amounts are calculated by dividing the profit attributable to equity holders of the company by the weighted

average number of Equity shares outstanding during the year plus the weighted average number of Equity shares that

would be issued on conversion of all the dilutive potential Equity shares into Equity shares.

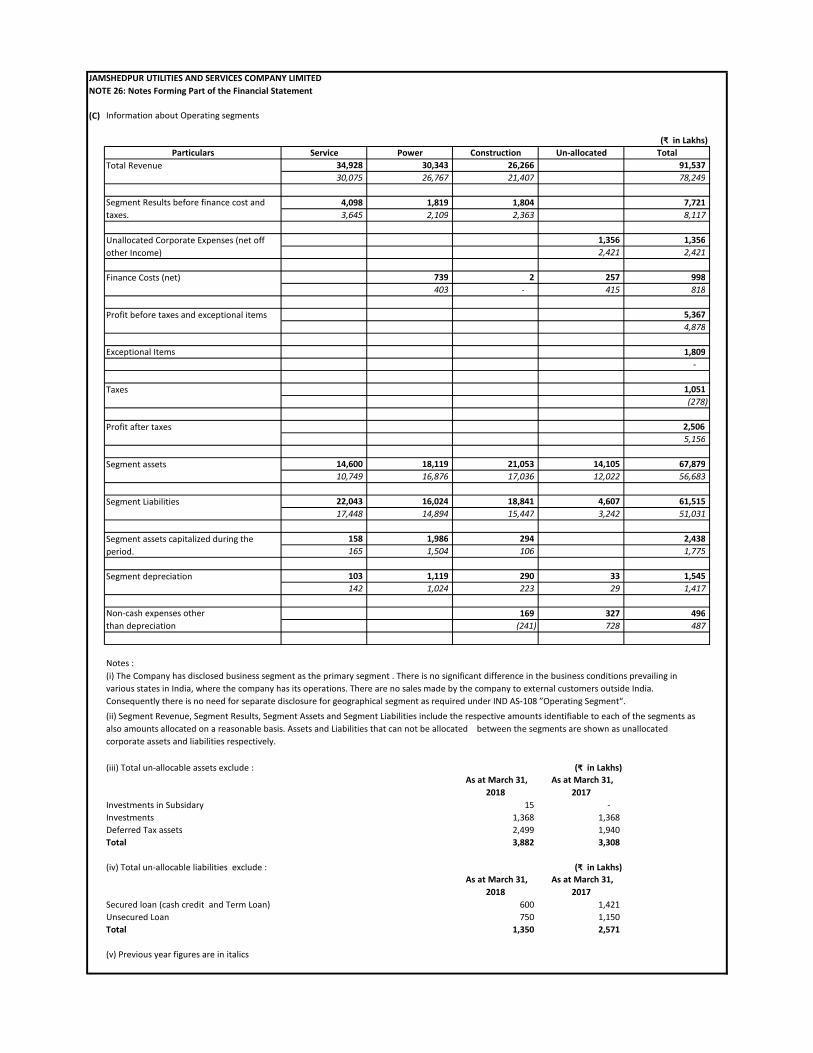

(22) Segment Reporting

The Company identifies primary segments based on the dominant source, nature of risks and returns and the internal

organization and management structure. The operating segments are the segments for which separate financial

information is available and for which operating profit/loss amounts are evaluated regularly by the executive Management

in deciding how to allocate resources and in assessing performance.

The accounting policies adopted for segment reporting are in line with the accounting policies of the Company. Segment

revenue, segment expenses, segment assets and segment liabilities have been identified to segments on the basis of

their relationship to the operating activities of the segment.

Revenue, expenses, assets and liabilities which relate to the Company as a whole and are not allocable to segments on

reasonable basis have been included under “unallocated revenue / expenses / assets / liabilities”.

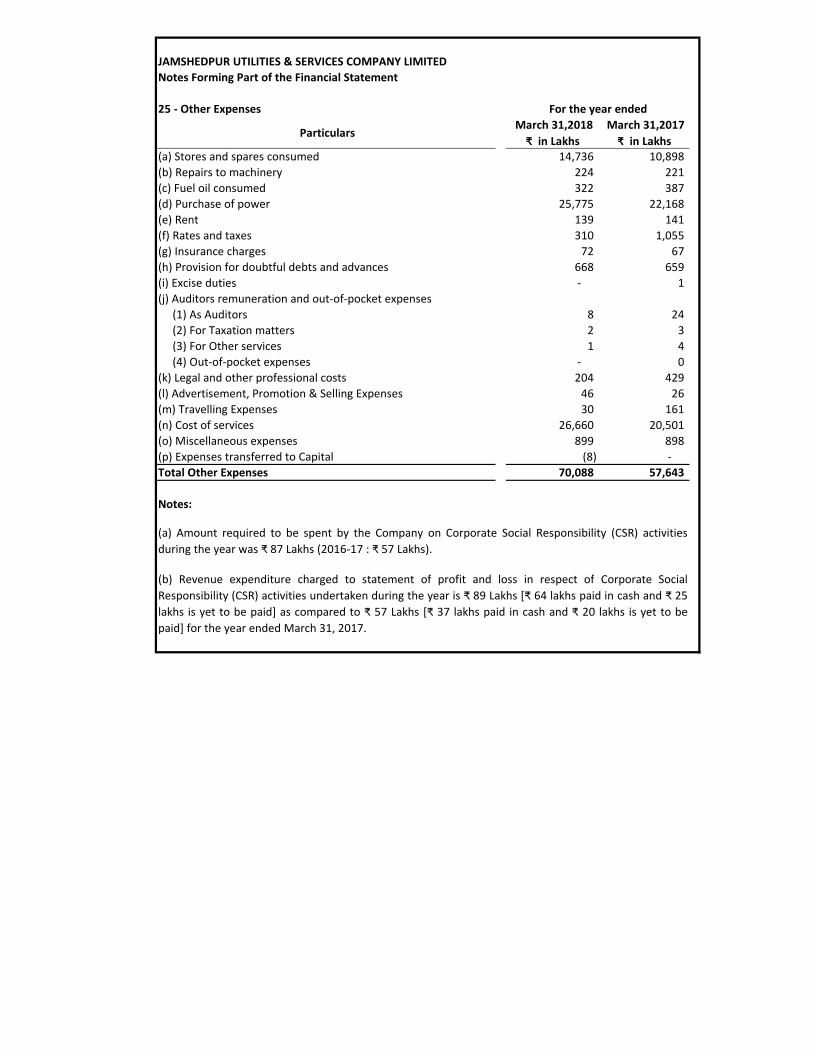

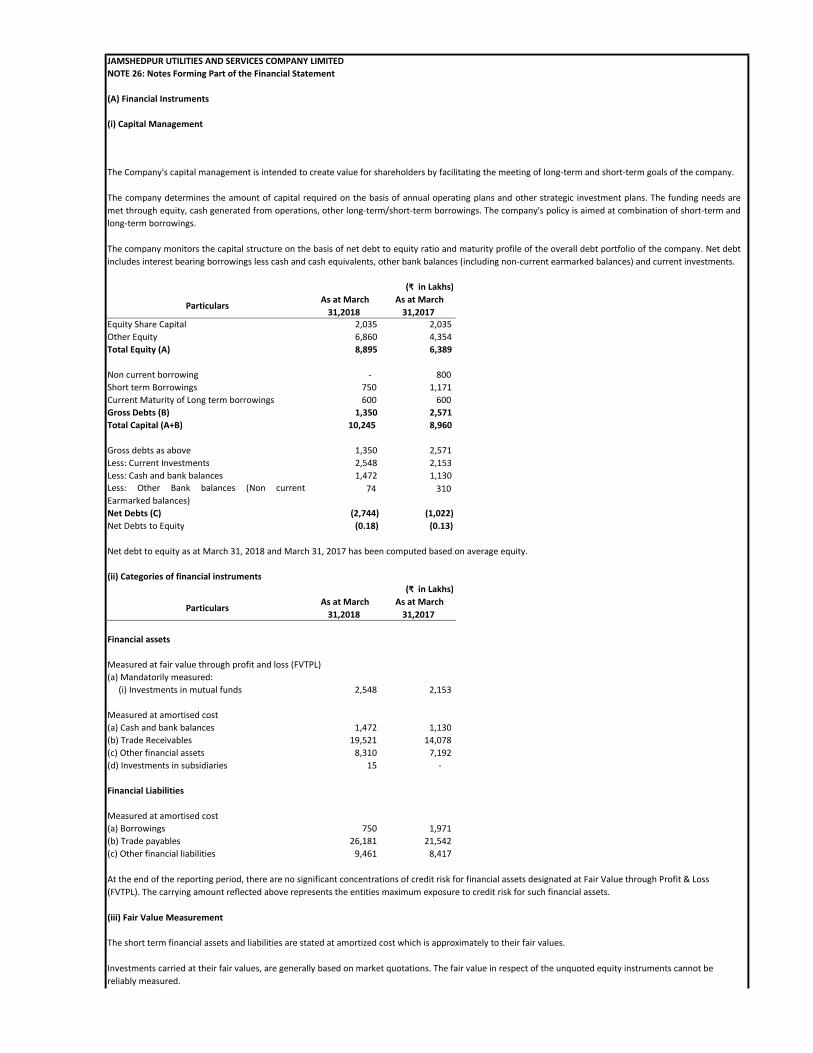

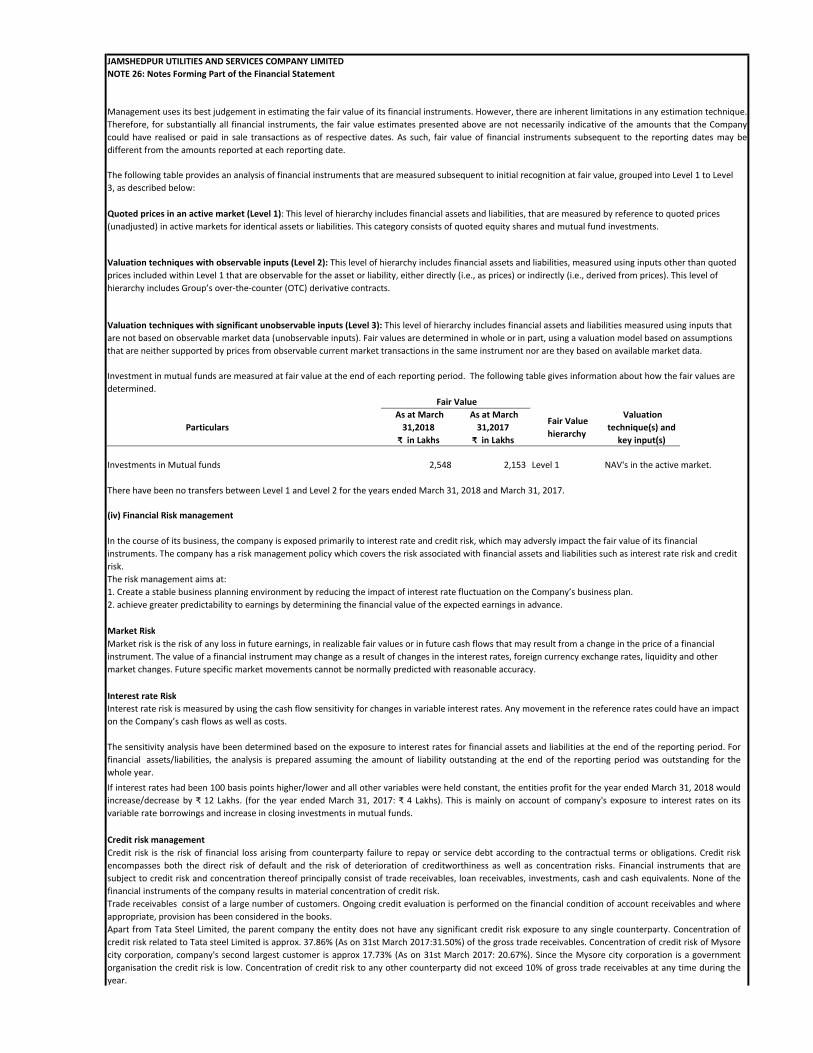

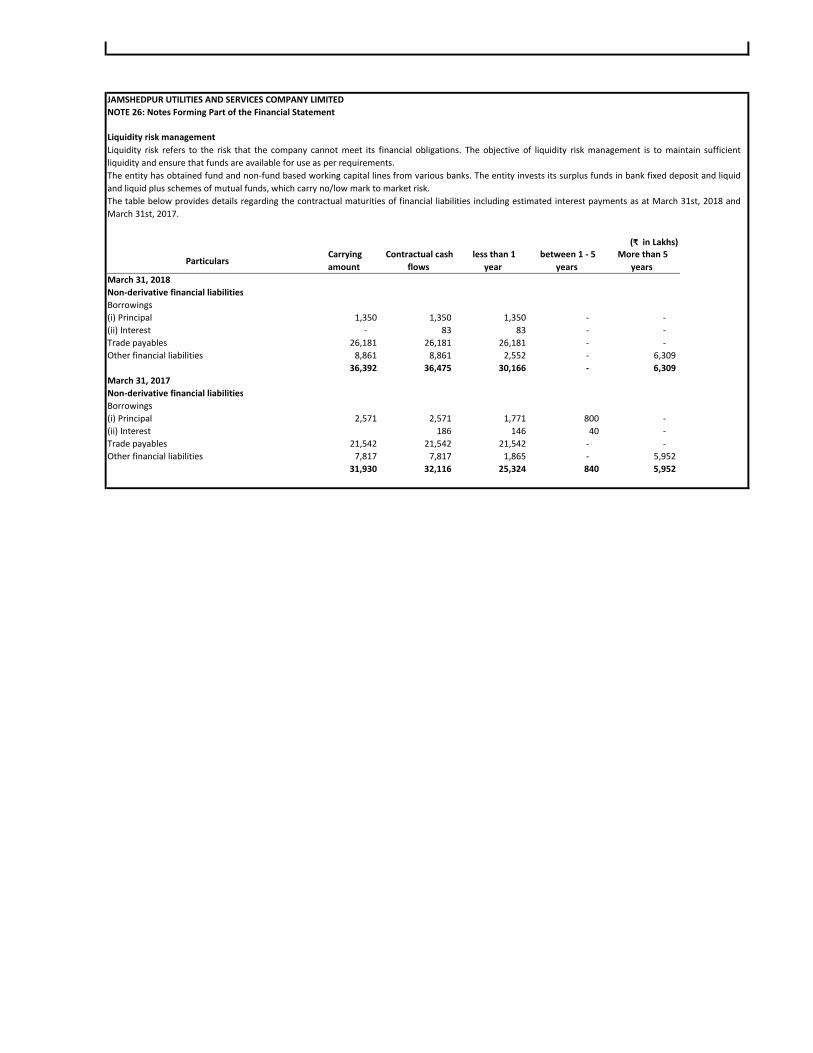

JAMSHEDPUR UTILITIES & SERVICES COMPANY LIMITED

Notes Forming Part of the Financial Statements

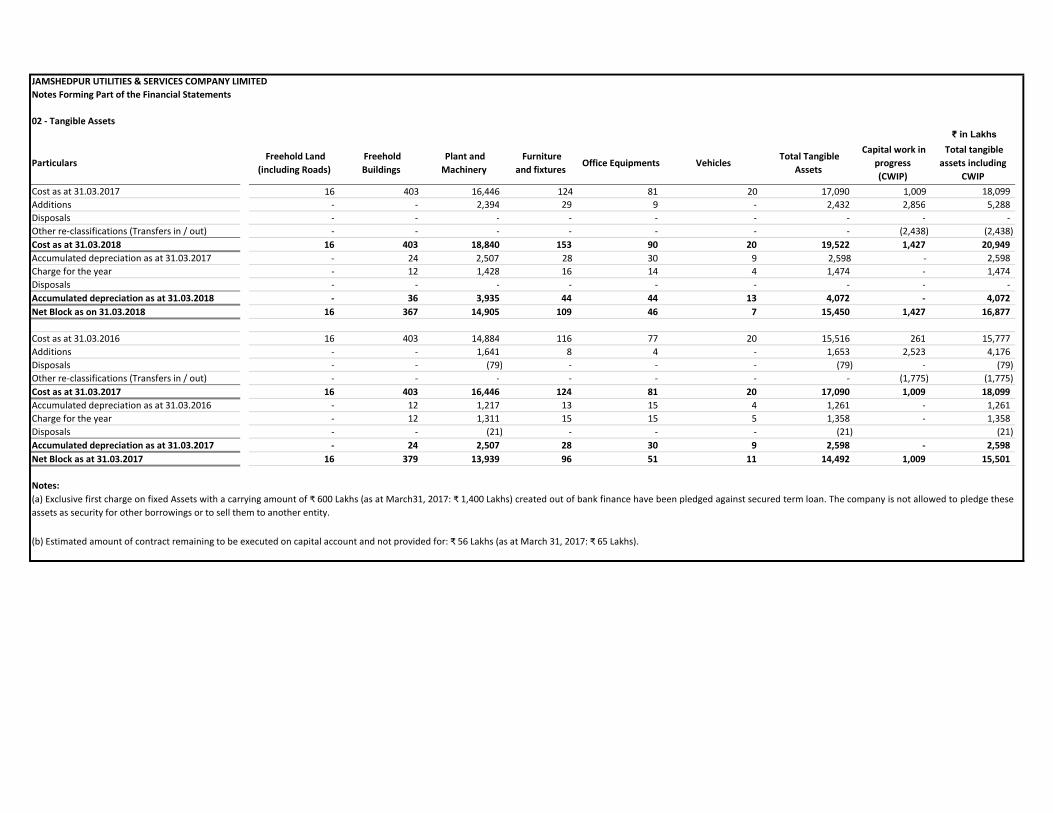

02 - Tangible Assets

₹ in Lakhs

ParticularsFreehold Land

(including Roads)

Freehold

Buildings

Plant and

Machinery

Furniture

and fixturesOffice Equipments Vehicles

Total Tangible

Assets

Capital work in

progress

(CWIP)

Total tangible

assets including

CWIP

Cost as at 31.03.2017 16 403 16,446 124 81 20 17,090 1,009 18,099

Additions - - 2,394 29 9 - 2,432 2,856 5,288

Disposals - - - - - - - - -

Other re-classifications (Transfers in / out) - - - - - - - (2,438) (2,438)

Cost as at 31.03.2018 16 403 18,840 153 90 20 19,522 1,427 20,949

Accumulated depreciation as at 31.03.2017 - 24 2,507 28 30 9 2,598 - 2,598

Charge for the year - 12 1,428 16 14 4 1,474 - 1,474

Disposals - - - - - - - - -

Accumulated depreciation as at 31.03.2018 - 36 3,935 44 44 13 4,072 - 4,072

Net Block as on 31.03.2018 16 367 14,905 109 46 7 15,450 1,427 16,877

Cost as at 31.03.2016 16 403 14,884 116 77 20 15,516 261 15,777

Additions - - 1,641 8 4 - 1,653 2,523 4,176

Disposals - - (79) - - - (79) - (79)

Other re-classifications (Transfers in / out) - - - - - - - (1,775) (1,775)

Cost as at 31.03.2017 16 403 16,446 124 81 20 17,090 1,009 18,099

Accumulated depreciation as at 31.03.2016 - 12 1,217 13 15 4 1,261 - 1,261

Charge for the year - 12 1,311 15 15 5 1,358 - 1,358

Disposals - - (21) - - - (21) (21)

Accumulated depreciation as at 31.03.2017 - 24 2,507 28 30 9 2,598 - 2,598

Net Block as at 31.03.2017 16 379 13,939 96 51 11 14,492 1,009 15,501

Notes:

(a) Exclusive first charge on fixed Assets with a carrying amount of ₹ 600 Lakhs (as at March31, 2017: ₹ 1,400 Lakhs) created out of bank finance have been pledged against secured term loan. The company is not allowed to pledge these

assets as security for other borrowings or to sell them to another entity.

(b) Estimated amount of contract remaining to be executed on capital account and not provided for: ₹ 56 Lakhs (as at March 31, 2017: ₹ 65 Lakhs).

JAMSHEDPUR UTILITIES & SERVICES COMPANY LIMITED

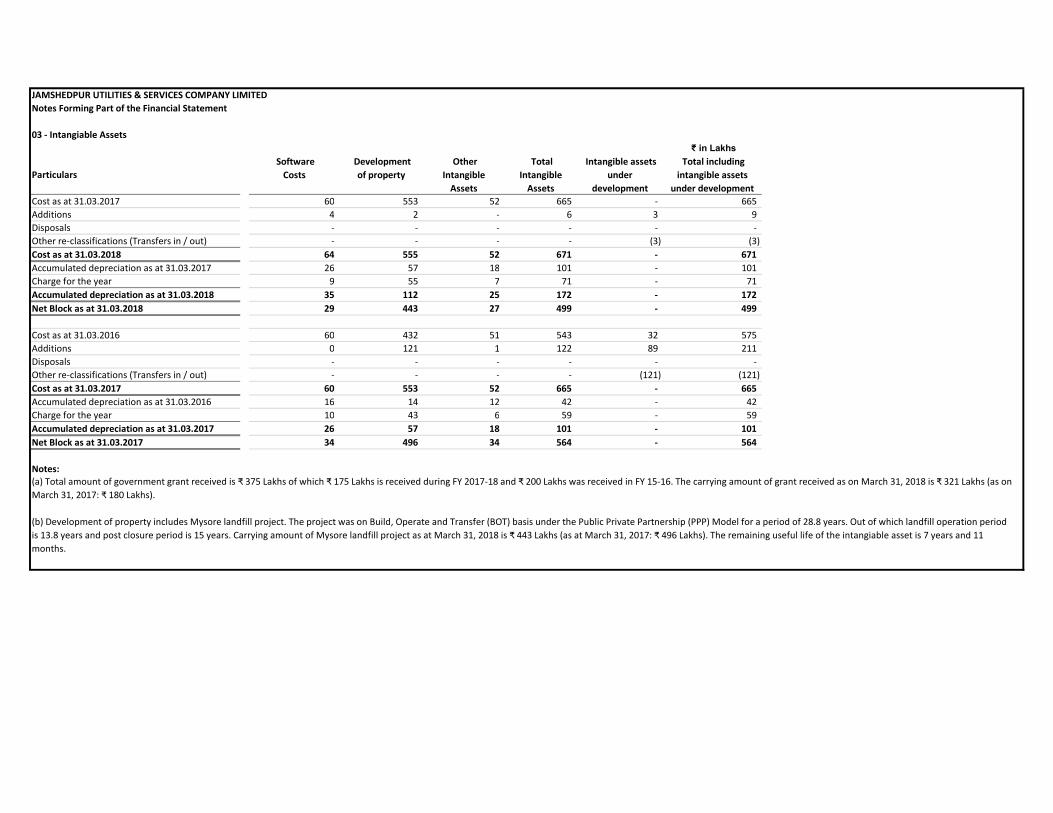

Notes Forming Part of the Financial Statement

03 - Intangiable Assets

₹ in Lakhs

Particulars

Software

Costs

Development

of property

Other

Intangible

Assets

Total

Intangible

Assets

Intangible assets

under

development

Total including

intangible assets

under development

Cost as at 31.03.2017 60 553 52 665 - 665

Additions 4 2 - 6 3 9

Disposals - - - - - -

Other re-classifications (Transfers in / out) - - - - (3) (3)

Cost as at 31.03.2018 64 555 52 671 - 671

Accumulated depreciation as at 31.03.2017 26 57 18 101 - 101

Charge for the year 9 55 7 71 - 71

Accumulated depreciation as at 31.03.2018 35 112 25 172 - 172

Net Block as at 31.03.2018 29 443 27 499 - 499

Cost as at 31.03.2016 60 432 51 543 32 575

Additions 0 121 1 122 89 211

Disposals - - - - - -

Other re-classifications (Transfers in / out) - - - - (121) (121)

Cost as at 31.03.2017 60 553 52 665 - 665

Accumulated depreciation as at 31.03.2016 16 14 12 42 - 42

Charge for the year 10 43 6 59 - 59

Accumulated depreciation as at 31.03.2017 26 57 18 101 - 101

Net Block as at 31.03.2017 34 496 34 564 - 564

Notes:(a) Total amount of government grant received is ₹ 375 Lakhs of which ₹ 175 Lakhs is received during FY 2017-18 and ₹ 200 Lakhs was received in FY 15-16. The carrying amount of grant received as on March 31, 2018 is ₹ 321 Lakhs (as on

March 31, 2017: ₹ 180 Lakhs).

(b) Development of property includes Mysore landfill project. The project was on Build, Operate and Transfer (BOT) basis under the Public Private Partnership (PPP) Model for a period of 28.8 years. Out of which landfill operation period

is 13.8 years and post closure period is 15 years. Carrying amount of Mysore landfill project as at March 31, 2018 is ₹ 443 Lakhs (as at March 31, 2017: ₹ 496 Lakhs). The remaining useful life of the intangiable asset is 7 years and 11

months.

JAMSHEDPUR UTILITIES & SERVICES COMPANY LIMITED

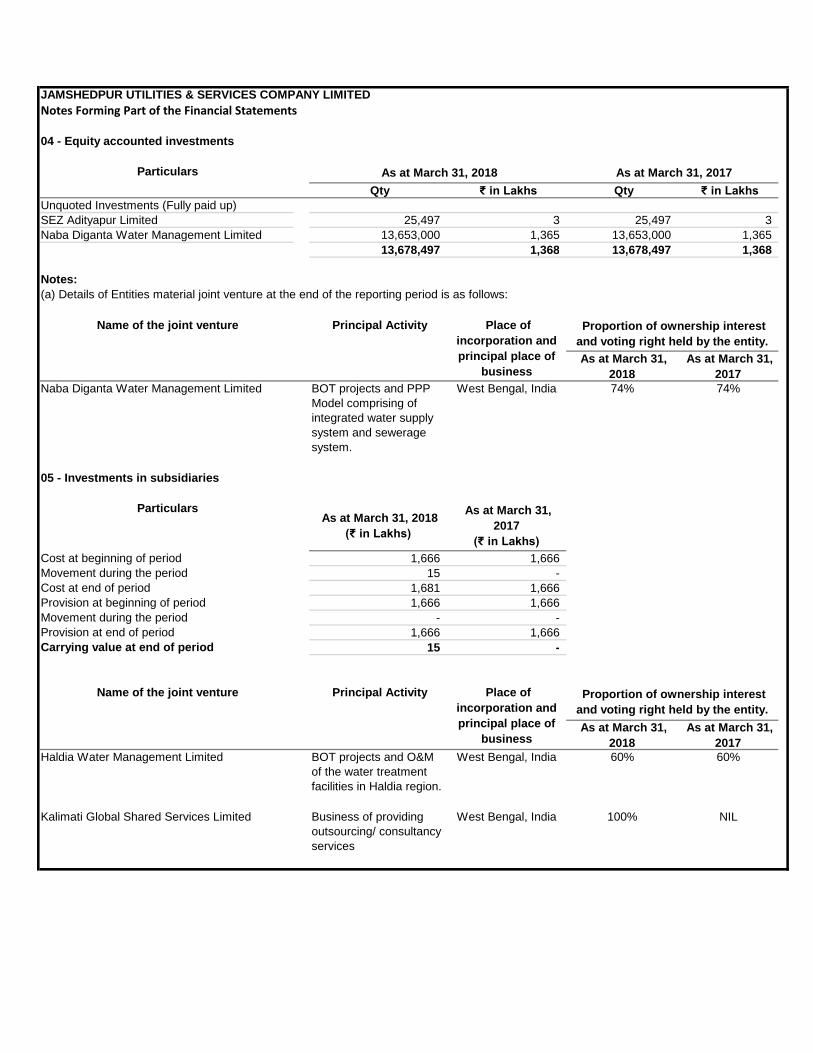

Notes Forming Part of the Financial Statements

04 - Equity accounted investments

Qty ₹ in Lakhs Qty ₹ in Lakhs Unquoted Investments (Fully paid up)

SEZ Adityapur Limited 25,497 3 25,497 3

Naba Diganta Water Management Limited 13,653,000 1,365 13,653,000 1,365

13,678,497 1,368 13,678,497 1,368

Notes:

(a) Details of Entities material joint venture at the end of the reporting period is as follows:

As at March 31,

2018

As at March 31,

2017Naba Diganta Water Management Limited BOT projects and PPP

Model comprising ofintegrated water supplysystem and seweragesystem.

West Bengal, India 74% 74%

05 - Investments in subsidiaries

ParticularsAs at March 31, 2018

(₹ in Lakhs)

As at March 31,

2017

(₹ in Lakhs)

Cost at beginning of period 1,666 1,666Movement during the period 15 -Cost at end of period 1,681 1,666Provision at beginning of period 1,666 1,666Movement during the period - -Provision at end of period 1,666 1,666Carrying value at end of period 15 -

As at March 31,

2018

As at March 31,

2017Haldia Water Management Limited BOT projects and O&M

of the water treatmentfacilities in Haldia region.

West Bengal, India 60% 60%

Kalimati Global Shared Services Limited Business of providingoutsourcing/ consultancyservices

West Bengal, India 100% NIL

Particulars As at March 31, 2018 As at March 31, 2017

Name of the joint venture Principal Activity Place of

incorporation and

principal place of

business

Proportion of ownership interest

and voting right held by the entity.

Name of the joint venture Principal Activity Place of

incorporation and

principal place of

business

Proportion of ownership interest

and voting right held by the entity.

JAMSHEDPUR UTILITIES & SERVICES COMPANY LIMITED

Notes Forming Part of the Financial Statements

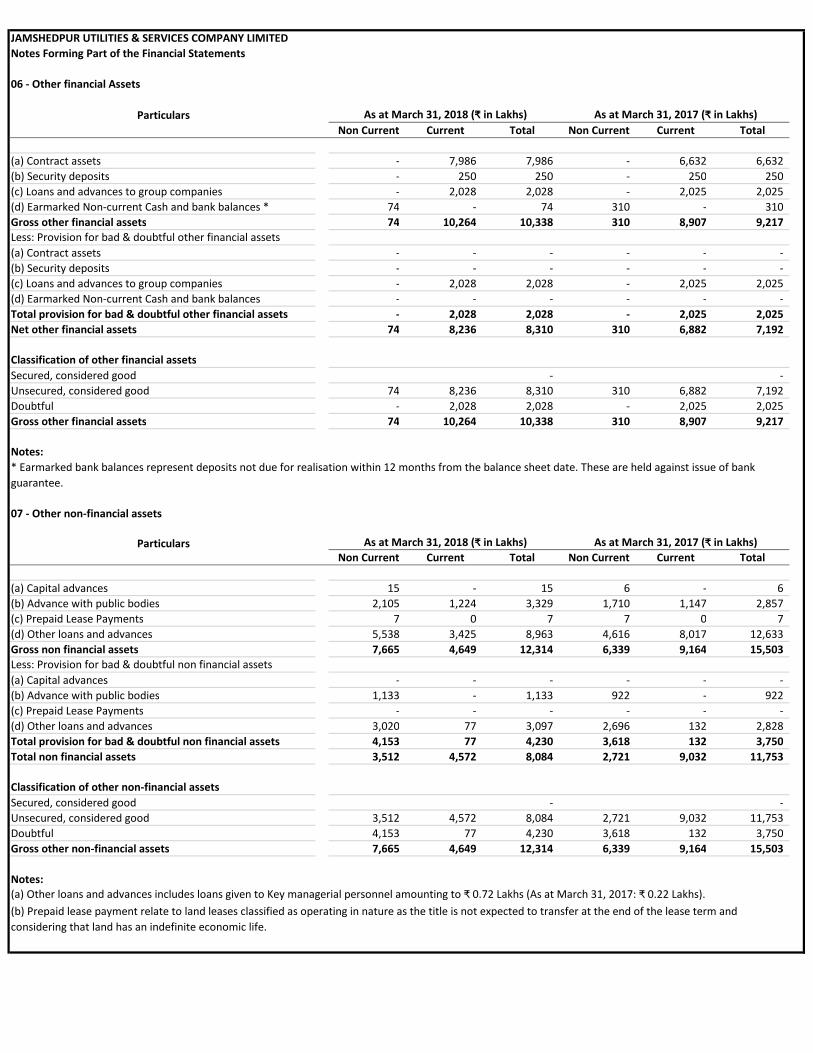

06 - Other financial Assets

Non Current Current Total Non Current Current Total

(a) Contract assets - 7,986 7,986 - 6,632 6,632

(b) Security deposits - 250 250 - 250 250

(c) Loans and advances to group companies - 2,028 2,028 - 2,025 2,025

(d) Earmarked Non-current Cash and bank balances * 74 - 74 310 - 310

Gross other financial assets 74 10,264 10,338 310 8,907 9,217

Less: Provision for bad & doubtful other financial assets

(a) Contract assets - - - - - -

(b) Security deposits - - - - - -

(c) Loans and advances to group companies - 2,028 2,028 - 2,025 2,025

(d) Earmarked Non-current Cash and bank balances - - - - - -

Total provision for bad & doubtful other financial assets - 2,028 2,028 - 2,025 2,025

Net other financial assets 74 8,236 8,310 310 6,882 7,192

Classification of other financial assets

Secured, considered good - -

Unsecured, considered good 74 8,236 8,310 310 6,882 7,192

Doubtful - 2,028 2,028 - 2,025 2,025

Gross other financial assets 74 10,264 10,338 310 8,907 9,217

Notes:

07 - Other non-financial assets

Non Current Current Total Non Current Current Total

(a) Capital advances 15 - 15 6 - 6

(b) Advance with public bodies 2,105 1,224 3,329 1,710 1,147 2,857

(c) Prepaid Lease Payments 7 0 7 7 0 7

(d) Other loans and advances 5,538 3,425 8,963 4,616 8,017 12,633

Gross non financial assets 7,665 4,649 12,314 6,339 9,164 15,503

Less: Provision for bad & doubtful non financial assets

(a) Capital advances - - - - - -

(b) Advance with public bodies 1,133 - 1,133 922 - 922

(c) Prepaid Lease Payments - - - - - -

(d) Other loans and advances 3,020 77 3,097 2,696 132 2,828

Total provision for bad & doubtful non financial assets 4,153 77 4,230 3,618 132 3,750

Total non financial assets 3,512 4,572 8,084 2,721 9,032 11,753

Classification of other non-financial assets

Secured, considered good - -

Unsecured, considered good 3,512 4,572 8,084 2,721 9,032 11,753

Doubtful 4,153 77 4,230 3,618 132 3,750

Gross other non-financial assets 7,665 4,649 12,314 6,339 9,164 15,503

Notes:

Particulars As at March 31, 2018 (₹ in Lakhs) As at March 31, 2017 (₹ in Lakhs)

(a) Other loans and advances includes loans given to Key managerial personnel amounting to ₹ 0.72 Lakhs (As at March 31, 2017: ₹ 0.22 Lakhs).

(b) Prepaid lease payment relate to land leases classified as operating in nature as the title is not expected to transfer at the end of the lease term and

considering that land has an indefinite economic life.

Particulars As at March 31, 2018 (₹ in Lakhs) As at March 31, 2017 (₹ in Lakhs)

* Earmarked bank balances represent deposits not due for realisation within 12 months from the balance sheet date. These are held against issue of bank

guarantee.

JAMSHEDPUR UTILITIES & SERVICES COMPANY LIMITED

Notes Forming Part of the Financial Statements

08 - Inventories

Particulars

Inventories (lower of cost or net realizable value)

- Land, plots and construction in progress

- Stores & Spares

Total Inventories

Notes:

09 - Current Investments

Unquoted Investments

(a) Investment in mutual funds

TATA Mutual Fund

Reliance Liquid Fund

SBI Premier Liquid Fund

Birla Sun Life Cash Plus

Total Current Investments

10 - Trade Receivables

Particulars

(a) Secured, Considered good

(b) Unsecured, Considered good

(c) Unsecured, Considered Doubtful

Less: Allowance for Credit losses

Notes:

(a) Ageing of trade receivables and credit risk arising therefrom is as below:

Gross Credit Risk Allowance for

Credit loss

Net Credit Risk

Amount not yet due 11,970 11,970

One month overdue 3,122 3,122

Two months overdue 218 218

Three months overdue 540 540

Between three to six months overdue 764 764

Greater than six months overdue 5,912 3,005 2,907

22,526 3,005 19,521

Gross Credit Risk Allowance for

Credit loss

Net Credit Risk

Amount not yet due 9,241 9,241

One month overdue 1,750 1,750

Two months overdue 65 65

Three months overdue 43 43

Between three to six months overdue 84 84

Greater than six months overdue 5,716 2,821 2,895

16,899 2,821 14,078

(c) Movement in Allowance for Credit Losses:

Particulars

Balance at the beginning of the period

Provision created during the year

Provisions reversed during the year

Balance at the end of the year

1,044

502

501

2,548

676

376

550

551

2,153

As at March 31,2018 (₹ in Lakhs)

As at March 31,2017 (₹ in Lakhs)

19,521 14,078

2,821

2,8213,005

3,005

7,778 1,653

6,019 -

1,759 1,653

As at March 31,2018

(₹ in Lakhs)

As at March 31,2017

(₹ in Lakhs)

(a) The value of inventories above is stated after impairment of ₹ 181 Lakhs (March 31, 2017: ₹ 25 Lakhs) for write-downs

to net realisable value and provision for slow moving and obsolete item.

Particulars As at March 31,2018 As at March 31,2017

As at March 31,2018

(₹ in Lakhs)

As at March 31,2017

(₹ in Lakhs)

₹ in Lakhs ₹ in Lakhs

501

11,561

2,517

16,404

3,117

(d) There are no outstanding debts due from directors or other officers of the company.

(b)The Company considers its maximum exposure to credit risk with respect to customers as at March 31, 2018 to be ₹

19,521 Lakhs (March 31, 2017: ₹ 14,078 Lakhs), which is the fair value of trade receivables (after allowance for credit

losses).

Of the trade receivable balance as at March 31,2018 ₹ 8,502 Lakhs (March 31, 2017 of ₹ 5,298 Lakhs) is due from Tata Steel

Limited and ₹ 3,287 Lakhs (March 31, 2017 of ₹ 2,907 Lakhs) is due from Mysore city corporation, the entities largest

customers There are no other customers who represents more than 10% of the total balance of Trade Receivables.

As at March 31,2018

(₹ in Lakhs)

As at 31.03.2017

(₹ in Lakhs)

2,821 2,939

187 200

(3) (318)

3,005 2,821

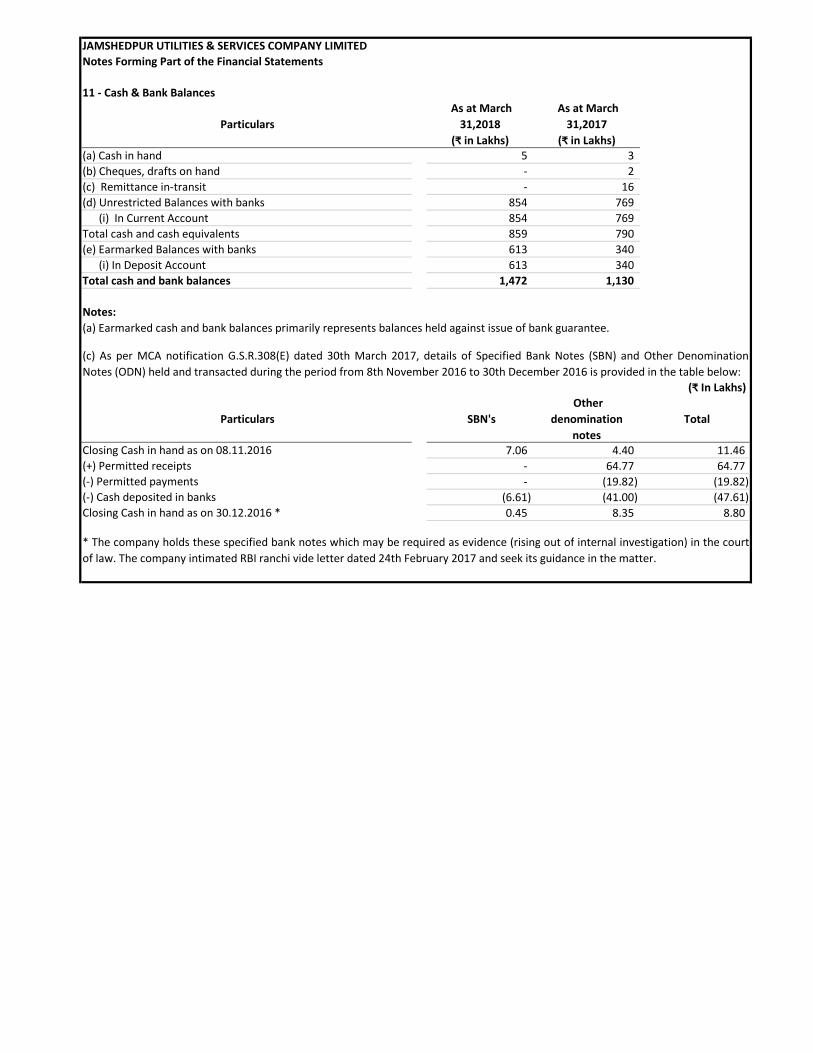

JAMSHEDPUR UTILITIES & SERVICES COMPANY LIMITED

Notes Forming Part of the Financial Statements

11 - Cash & Bank Balances

Particulars

As at March

31,2018

(₹ in Lakhs)

As at March

31,2017

(₹ in Lakhs) (a) Cash in hand 5 3

(b) Cheques, drafts on hand - 2

(c) Remittance in-transit - 16

(d) Unrestricted Balances with banks 854 769

(i) In Current Account 854 769

Total cash and cash equivalents 859 790

(e) Earmarked Balances with banks 613 340

(i) In Deposit Account 613 340

Total cash and bank balances 1,472 1,130

Notes:

(₹ In Lakhs)

Particulars SBN's

Other

denomination

notes

Total

Closing Cash in hand as on 08.11.2016 7.06 4.40 11.46

(+) Permitted receipts - 64.77 64.77

(-) Permitted payments - (19.82) (19.82)

(-) Cash deposited in banks (6.61) (41.00) (47.61)

Closing Cash in hand as on 30.12.2016 * 0.45 8.35 8.80

(c) As per MCA notification G.S.R.308(E) dated 30th March 2017, details of Specified Bank Notes (SBN) and Other Denomination

Notes (ODN) held and transacted during the period from 8th November 2016 to 30th December 2016 is provided in the table below:

* The company holds these specified bank notes which may be required as evidence (rising out of internal investigation) in the court

of law. The company intimated RBI ranchi vide letter dated 24th February 2017 and seek its guidance in the matter.

(a) Earmarked cash and bank balances primarily represents balances held against issue of bank guarantee.

JAMSHEDPUR UTILITIES & SERVICES COMPANY LIMITED

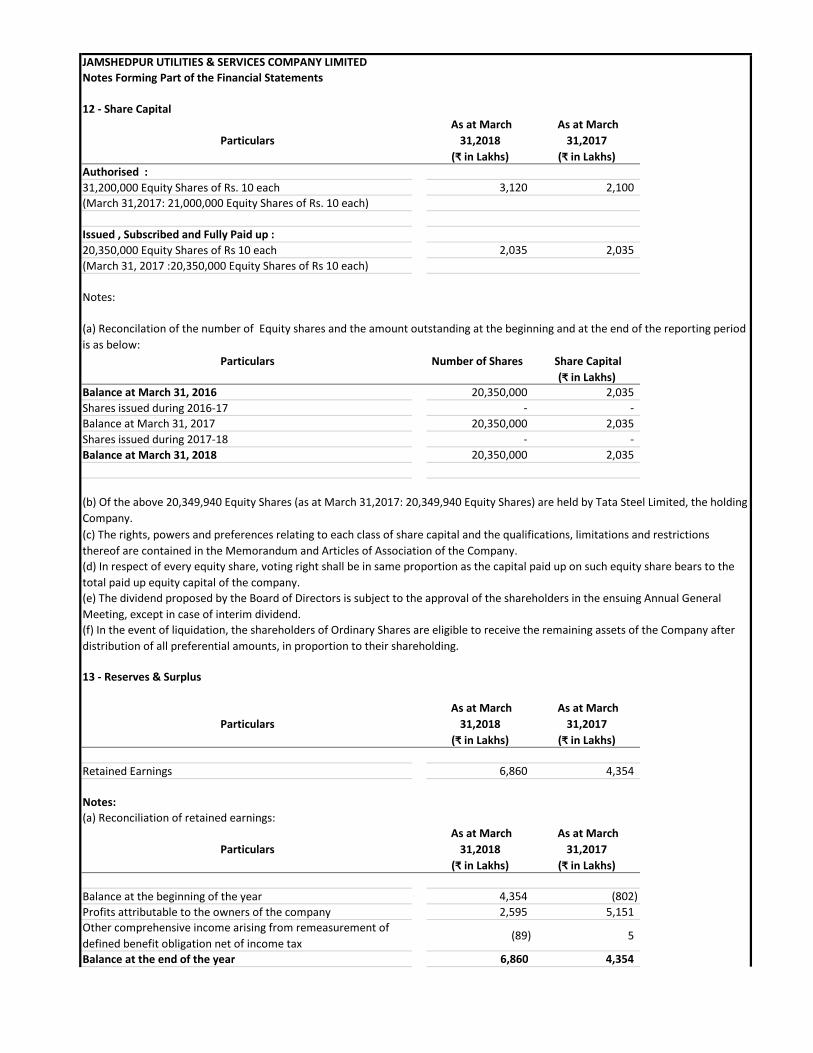

Notes Forming Part of the Financial Statements

12 - Share Capital

Particulars

As at March

31,2018

(₹ in Lakhs)

As at March

31,2017

(₹ in Lakhs) Authorised :

31,200,000 Equity Shares of Rs. 10 each 3,120 2,100

(March 31,2017: 21,000,000 Equity Shares of Rs. 10 each)

Issued , Subscribed and Fully Paid up :

20,350,000 Equity Shares of Rs 10 each 2,035 2,035

(March 31, 2017 :20,350,000 Equity Shares of Rs 10 each)

Notes:

Particulars Number of Shares Share Capital

(₹ in Lakhs) Balance at March 31, 2016 20,350,000 2,035

Shares issued during 2016-17 - -

Balance at March 31, 2017 20,350,000 2,035

Shares issued during 2017-18 - -

Balance at March 31, 2018 20,350,000 2,035

13 - Reserves & Surplus

Particulars

As at March

31,2018

(₹ in Lakhs)

As at March

31,2017

(₹ in Lakhs)

Retained Earnings 6,860 4,354

Notes:

(a) Reconciliation of retained earnings:

Particulars

As at March

31,2018

(₹ in Lakhs)

As at March

31,2017

(₹ in Lakhs)

Balance at the beginning of the year 4,354 (802)

Profits attributable to the owners of the company 2,595 5,151

Other comprehensive income arising from remeasurement of

defined benefit obligation net of income tax(89) 5

Balance at the end of the year 6,860 4,354

(b) Of the above 20,349,940 Equity Shares (as at March 31,2017: 20,349,940 Equity Shares) are held by Tata Steel Limited, the holding

Company.

(c) The rights, powers and preferences relating to each class of share capital and the qualifications, limitations and restrictions

thereof are contained in the Memorandum and Articles of Association of the Company.

(d) In respect of every equity share, voting right shall be in same proportion as the capital paid up on such equity share bears to the

total paid up equity capital of the company.

(e) The dividend proposed by the Board of Directors is subject to the approval of the shareholders in the ensuing Annual General

Meeting, except in case of interim dividend.

(f) In the event of liquidation, the shareholders of Ordinary Shares are eligible to receive the remaining assets of the Company after

distribution of all preferential amounts, in proportion to their shareholding.

(a) Reconcilation of the number of Equity shares and the amount outstanding at the beginning and at the end of the reporting period

is as below: