Embed Size (px)

Citation preview

IND AS 109 FINANCIAL INSTRUMENTS

IND AS

Faculty : CA R. Venkata Subramani Ind AS Certification Course Secretariat, Accounting Standards Board

The Institute of Chartered Accountants of IndiaNew Delhi, India

Disclaimer: The views expressed herein are solely those of the Faculty/Presenter and not that of the ICAI or any ofits committees. The ICAI or the Faculty or Preparer of this material do not accept any responsibility for omissionor inadequacy of the contents in this document and also for loss caused to any person who acts or refrains fromacting in reliance on the contents of this document irrespective of the cause of / reason for the loss.

Ind AS Course ICAI

AGENDA

2

1 Basic Accounting Entries2 Classification of Financial Assets3 Classification of Financial Liabilities4 Fair Value Option5 Reclassifications6 Effective Interest Rate7 Impairment8 Recognition & Dereccognition

Ind AS Course ICAI

ILLUSTRATION 1 – EQUITY SHARES HELD FORTRADING

3

v On 5th Jan bought 100 shares of ABC @ Rs.850/-v Market rate on 31st March - Rs. 875/-v The equity shares were held for the purpose of making short term

profits (for trading purposes)Show the journal entries, carrying value and P&L Account

Ind AS Course ICAI

ILLUSTRATION 1 – EQUITY SHARES HELD FORTRADING

4

v Solution:

Ind AS Course ICAI

ILLUSTRATION 1 – EQUITY SHARES HELD FORTRADING

5

v Solution:

Ind AS Course ICAI

ILLUSTRATION 1 –SHARES HELD FORTRADING

6

Ind AS Course ICAI

ILLUSTRATION 2 – BOND HELD FORTRADING

7

v On 1st April-X1 bought 6% 1000 Bonds of ABC @ Rs.85/- maturing on 31-Mar-X5

v Market rate on 31st March-X2 - Rs. 89/-v The bonds were held for trading purposes

Show the journal entries, carrying value and P&L Account and interest income for the year.

Ind AS Course ICAI

ILLUSTRATION 2 – BONDS- HELD FORTRADING

8

Date Particulars Debit Credit

1-Apr Investment Account – FVPL 85,000

To Bank 85,000

(Being the 6% bonds bought as trading security)

Ind AS Course ICAI

ILLUSTRATION 2 – BONDS- HELD FORTRADING

9

Date Particulars Debit Credit

31-Mar Bank 6,000

To Interest Income (P&L) 6,000

(Being the interest received on 6% bonds held as trading security)

Ind AS Course ICAI

ILLUSTRATION 2 – BONDS- HELD FORTRADING

10

Ind AS Course ICAI

ILLUSTRATION 2 – BONDS- HELD FORTRADING

11

Date Particulars Debit Credit

31-Mar Investment Account – FVPL 2,460

To Interest Income 2,460 (Being the amount amortized to account for interest based on Effective Interest Rate and adjustment of the carrying amount of the 6%bonds)

[Rs.8,460 effective interest less Rs.6,000 interest received]

Ind AS Course ICAI

ILLUSTRATION 2 – BONDS- HELD FORTRADING

12

Date Particulars Debit Credit

31-Mar Investment Account – FVPL 1,540 To Unrealized gains on Bonds – trading

(P&L) 1,540

(Being the unrealized gains on 6% bonds held as trading security transferred to P&L)

Ind AS Course ICAI

ILLUSTRATION 2 – BONDS- HELD FORTRADING

13

Ind AS Course ICAI

ILLUSTRATION 3 – BONDS- AMORTIZED COST

14

v On 1st April-X1 bought 6% 100 Bonds of ABC @ Rs.85/- maturing on 31-Mar-X5

v Bond to be valued at amortized costv Market rate on 31st March-X2 - Rs. 89/-

Show the journal entries, carrying value and P&L Account and interest income for the year.

Ind AS Course ICAI

ILLUSTRATION 3 – BONDS- AMORTIZED COST

15

Solution:

Ind AS Course ICAI

ILLUSTRATION 3 – BONDS- AMORTIZED COST

16

Solution:

Ind AS Course ICAI

ILLUSTRATION 3 – BONDS- AMORTIZED COST

17

Ind AS Course ICAI

ILLUSTRATION 3 – BONDS- AMORTIZED COST

18

Ind AS Course ICAI

ILLUSTRATION 3 – BONDS- AMORTIZED COST

19

Ind AS Course ICAI

ILLUSTRATION 4 – BONDS- FVOCI

20

v On 1st April-X1 bought 6% 100 Bonds of ABC @ Rs.85/- maturing on 31-Mar-X5

v Market rate on 31st March-X2 - Rs.89/-v The financial asset is held to achieve an objective by both collecting contractual

cash flows and selling financial assetsShow the journal entries, carrying value and P&L Account and interest income for the year.

Ind AS Course ICAI

ILLUSTRATION 4 – BONDS- FVOCI

21

Ind AS Course ICAI

ILLUSTRATION 4 – BONDS- FVOCI

22

Ind AS Course ICAI

ILLUSTRATION 4 – BONDS- FVOCI

23

Ind AS Course ICAI

ILLUSTRATION 4 – BONDS- FVOCI

24

Ind AS Course ICAI

ILLUSTRATION 4 – BONDS- FVOCI

25

Ind AS Course ICAI

ILLUSTRATION 4 – BONDS- FVOCI

26

Ind AS Course ICAI

OBJECTIVES OF INDAS 109

27

v Establish principles for recognizing and measuring financial assets, financial liabilities and certain contracts to buy or sell non-financial items

v Establish principles for de-recognition of financial assets and financial liabilities

v Specify principles for hedge accounting

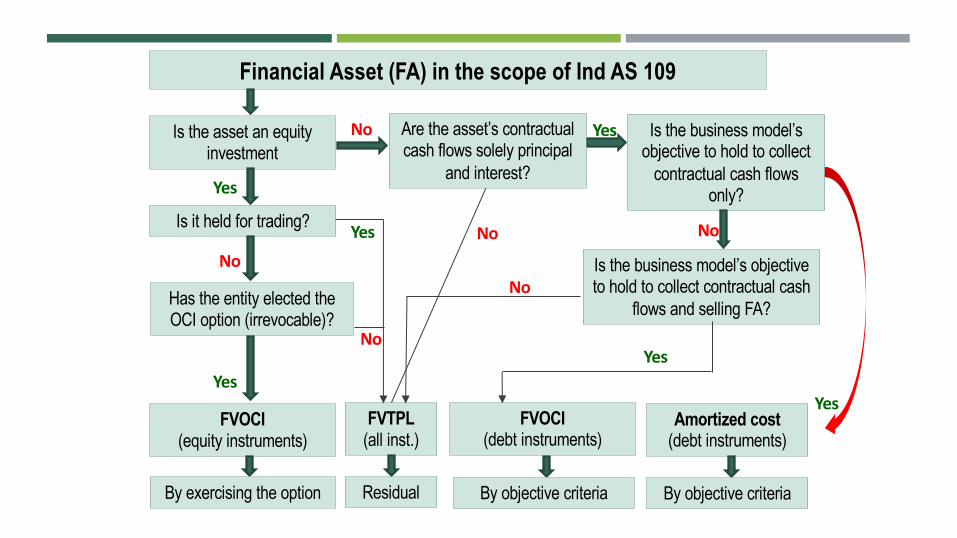

Financial Asset (FA) in the scope of Ind AS 109

Is the asset an equity investment

Is it held for trading?

Has the entity elected the OCI option (irrevocable)?

No

Yes

Is the business model’s objective to hold to collect

contractual cash flows only?

Yes

Yes

No

FVOCI(equity instruments)

Is the business model’s objective to hold to collect contractual cash

flows and selling FA?

FVTPL(all inst.)

FVOCI(debt instruments)

Amortized cost (debt instruments)

No

Yes

Are the asset’s contractual cash flows solely principal

and interest?

No

Yes No

Yes

No

By exercising the option Residual By objective criteria By objective criteria

Ind AS Course ICAI

CLASSIFICATION OF FINANCIALASSETS

29

Category TreatmentFVOCI (Equity instruments) • Dividends generally recognized in P&L

• Changes in fair value recognized in OCI• No reclassification of gains and losses to P&L on derecognition and no

impairment recognized in P&L

FVOCI (debt instruments)

• Interest revenue, credit impairment and foreign exchange gain or loss recognized in P&L (in the same manner as for amortized cost assets)

• Other gains and losses recognized in OCI• On derecognition, cumulative gains and losses in OCI reclassified to P&L

FVPL • Changes in fair value recognized in P&LAmortized cost • Interest revenue, credit impairment and foreign exchange gain or loss

recognized in P&L• On de-recognition, gains or losses recognized in P&L

Ind AS Course ICAI

FVOCI-EQUITY INSTRUMENT

30

vAccounting for FVOCI category for debt instruments is different from FVOCI forequity instruments due to the following:

vImpairment requirements are not applicablevForeign exchange differences are not recognized in OCIvAmounts recognized in OCI are never reclassified to profit or loss

Ind AS Course ICAI

SPPI TEST

31

vAn entity shall assess whether contractual cash flows are Solely Payments ofPrincipal and Interest (SPPI) on the principal amount outstanding for the currencyin which the financial asset is denominated

Ind AS Course ICAI

SPPI TEST

32

Category Treatment

Principal Principal is the fair value of the financial asset at initial recognition. However, principal may change over time – e.g. if there are repayments of principal

Interest Interest is consideration for:• The time value of money; and• The credit risk associated with the principal amount outstanding during a

particular period of timeInterest can also include:• Consideration for other basic lending risks (e.g. liquidity risk) and costs (e.g.

administrative costs); and• A profit margin

Ind AS Course ICAI

33

INTEREST

Ind AS Course ICAI

34

SPPI TEST- EXAMPLE 1

SituationInstrument B is a bond with a stated maturity datePayments of principal and interest on the principal amount outstanding are linked to

a) Case 1 - debtor’s performance (e.g. the debtor’s net income) b) Case 2 - an equity index

Ind AS Course ICAI

35

SPPI TEST- EXAMPLE 1

Answerv The contractual cash flows are not payments of principal and interest on the

principal amount outstanding

v That is because the interest payments are not consideration for the time value of money and for credit risk associated with the principal amount outstanding

v There is variability in the contractual interest payments that is inconsistent with market interest rates

Ind AS Course ICAI

36

BUSINESS MODEL - ASSESSMENT

v Not dependent on management’s intention & abilityv Not instrument by instrumentv Assessed at a high level of aggregationv Not at the entity levelv Applied at portfolio or sub-portfolio levelv May have more than one business model for managing Financial Assetsv Matter of fact and is typically observablev Standard acknowledges that judgment is needed

E.g., ‘Bright line’ for sales activity

Ind AS Course ICAI

37

EXAMPLE

An entity may hold a) a portfolio of investments that it manages in order to collect contractual cash flows

and b) another portfolio of investments that it manages in order to trade to realize fair

value changes

Ind AS Course ICAI

38

HELD TO COLLECT & FOR SALE

v Possible to have both modelsv Key management personnel to decide (Ind AS 24)v Examples

v Financial Institutions holding Financial Assets to meet its every day liquidity needs

v Insurer holding Financial Assets to fund insurance contract liabilitiesv Will involve greater frequency / value of salesv No threshold or ‘bright line’ for sales activity

Ind AS Course ICAI

39

EXCEPTIONS

The entity need not hold all of those instruments until maturity. Thus an entity’s business model can be to hold financial assets to collect contractual cash flows even when sales of financial assets occurThe entity may sell a financial asset if: [Exceptions]a) the financial asset no longer meets the entity’s investment policy (e.g. the credit rating

of the asset declines below that required by the entity’s investment policy);b) an insurer adjusts its investment portfolio to reflect a change in expected duration (i.e.

the expected timing of payouts); orc) an entity needs to fund capital expenditures

Ind AS Course ICAI

40

FINANCIAL LIABILITIES

Financial Liabilities

Ind AS Course ICAI

41

MEASURED AT AMORTIZED COST

An entity shall classify all financial liabilities as subsequently measured at amortized cost using the effective interest method, except for:

v financial liabilities at fair value through profit or loss. Such liabilities, including derivatives that are liabilities, shall be subsequently measured at fair value

v financial liabilities that arise when a transfer of a financial asset does not qualify for derecognition or when the continuing involvement approach applies

Ind AS Course ICAI

42

CLASSIFICATION OF FINANCIAL LIABILITIES

S.No Financial liabilities that are not measured at amortized cost Measurement requirements

A Held for trading – including derivatives FVTPLB Designated as at FVPL on initial recognition FVTPL

Ind AS Course ICAI

43

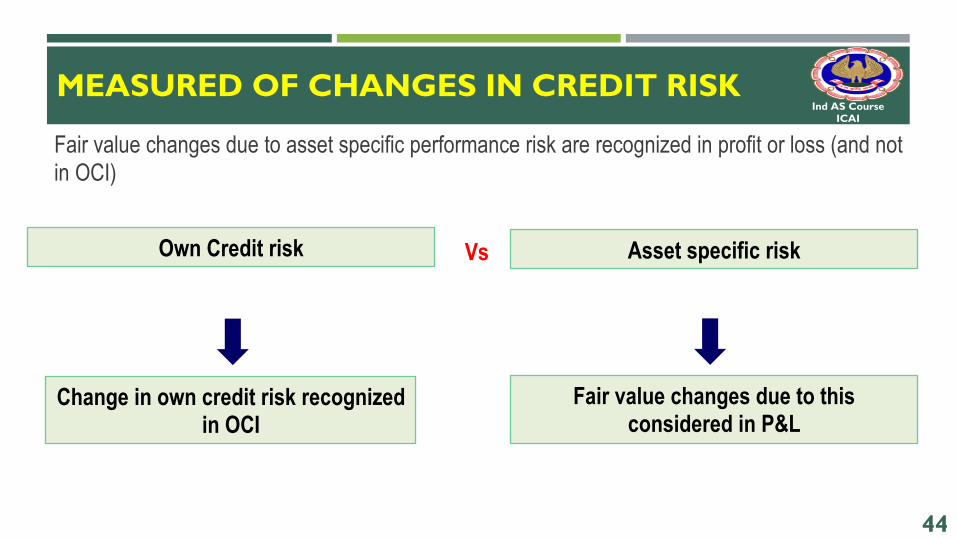

FAIR VALUE OPTION

Eligibility criteriav Reduce measurement or recognition inconsistencyv Managing a group of Financial Liabilities or Financial Assets / Financial Liabilities on a

fair value basisv Embedded derivatives & host is not a Financial Asset as per Ind AS 109 then the

entire hybrid can be designated as FVTPL

Accounting treatmentv Fair value changes due to credit risk taken to OCIv Fair value changes not due to credit risk taken to Profit or loss

Ind AS Course ICAI

44

MEASURED OF CHANGES IN CREDIT RISK

Own Credit risk Asset specific riskVs

Change in own credit risk recognized in OCI

Fair value changes due to this considered in P&L

Fair value changes due to asset specific performance risk are recognized in profit or loss (and not in OCI)

Ind AS Course ICAI

45

FVO LIABILITIES AS PER IND AS 109

As per Ind AS 109:v FV changes attributable to changes in own credit risk is presented in Other

Comprehensive Incomev Remaining (FV changes other than own credit risk) presented in P&Lv Amounts presented in OCI is never reclassified to P&Lv FV Option once exercised is irrevocablev Should be designated at the inceptionv FVO will be allowed only to rectify an accounting mismatch

Ind AS Course ICAI

46

FINANCIAL ASSET - DERECOGNITION

An entity shall derecognize a financial asset when and only when

1. The contractual rights to the cash flows from the financial assets expire or2. Transfers the contractual rights to receive the cash flows of the financial asset or3. Retains the contractual rights to receive the cash flows of the financial asset, but

assumes a contractual obligation to pay the cash flows meeting certain conditions

Final test:Ensure that both risk & rewards as well as control are not retained by the entity

Ind AS Course ICAI

47

CONTRACTUAL OBLIGATION- CONDITIONS

When assuming contractual obligation to pay cash flows the following three conditions should be met

a) No obligation to pay unless it collects equivalent amountsb) Prohibition to sell or pledge the original assetc) Obligation to pay cash flows without material delay

Ind AS Course ICAI

48

DE RECOGNITION OF ASSET-SUMMARY

Ind AS Course ICAI

49

APPLICATION OF DE RECOGNITION PRINCIPLES

Repurchase agreements and securities lending

AssetFinancial asset is sold under an agreement to repurchase it at a fixed price or at the sale price plus a lender’s return

AnswerNot derecognized – transferor retains substantially all the risks and rewards of ownership

Ind AS Course ICAI

50

APPLICATION OF DE RECOGNITION PRINCIPLES

Repurchase right of first refusal

AssetFinancial asset is sold but retains only a right of first refusal to repurchase the transferred asset at fair value

AnswerDerecognized – as the entity has substantially transferred all the risks and rewards of ownership

Ind AS Course ICAI

51

APPLICATION OF DE RECOGNITION PRINCIPLES

Put and call options deeply in the money

AssetIf Financial asset can be called back by the transferor and the call option is deeply in the money

AnswerNot derecognized – as the entity has substantially retained all the risks and rewards of ownership

Ind AS Course ICAI

52

EFFECT OF DE RECOGNITION

The difference between v the carrying amount measured at the date of derecognition and v the consideration received (including any new asset obtained less any new

liability assumed)shall be recognized in profit or loss

Ind AS Course ICAI

53

TRANSFER THAT DO NOT QUALIFY DE RECOGNITION

If the transfer does not result in de recognition thena) The entity shall continue to recognize the transferred asset in its entirety andb) Shall recognize a financial liability for the consideration received

v In subsequent periods, the entity shall recognize any income on the transferred asset and any expense incurred on the financial liability

v The entity shall continue to recognize any income arising on the transferred asset to the extent of its continuing involvement and shall recognize any expense incurred on the associated liability

Ind AS Course ICAI

54

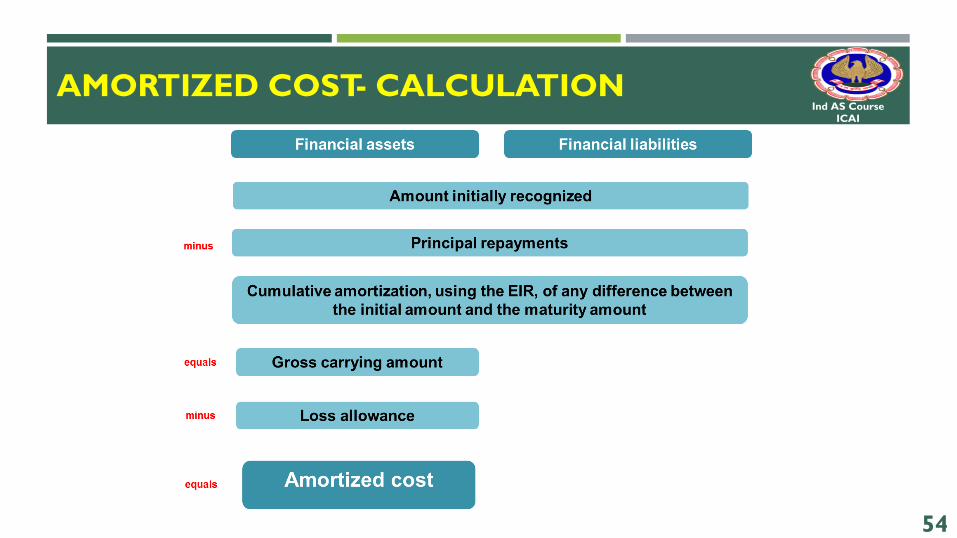

AMORTIZED COST- CALCULATION

Ind AS Course ICAI

55

REQUIREMENT OF IMPAIRMENT MODEL

v Based on entity’s expected credit losses on financial instrumentsv Recognize expected credit losses at all times and update the changes in the credit

risk of financial instrumentsv Model is forward-looking v Eliminates the threshold for the recognition of expected credit lossesv More timely information provided about expected credit lossesv Same impairment model applied to all financial instruments

Ind AS Course ICAI

56

SCOPE OF IMPAIRMENT MODEL

In scopev Financial assets – debt instruments

measured at AC or FVOCI including loans, trade receivables and debt securities

v Loan commitments – not measured at FVTPL

v Financial guarantee contracts – not measured at FVTPL

v Lease receivables in the scope of Ind AS 116

v Contract assets in the scope of Ind AS 115

Out of scope

v Equity investmentsv Loan commitments – measured at

FVTPLv Other financial instruments measured

at FVTPL

Ind AS Course ICAI

57

EQUITY INVESTMENT

Investments in equity instruments are outside the scope because they are accounted for eitherv At FVTPL orv At FVOCI with no reclassification of any fair value gains or losses to P&L

Accordingly equity investments are no longer tested for impairment[‘Significant or prolonged’ decline test has proved difficult to apply]

Ind AS Course ICAI

58

GENERAL APPROACH TO IMPAIRMENT

v Incurred loss model replaced with expected credit loss modelv Expected losses are the present value of all cash shortfalls over the expected life

of the financial instrumentsv Requires entities to recognize expected credit losses in P&L for all financial assetsv Akin to day one loss

Cash shortfall: Difference between the cash flows due to the entity in accordance with the contract and the cash flows that the entity expects to receive

Ind AS Course ICAI

59

EXPECTED CREDIT LOSS MODEL

Impairment is measured as either

v 12 month expected credit losses orv Lifetime expected credit losses

v Definition: The portion of lifetime expected credit losses that represents the expected credit losses that result from default events on the financial instrument that are possible within the 12 months after the reporting date

Ind AS Course ICAI

60

DEFINITION OF CREDIT IMPAIRED ASSET

v An asset is credit-impaired if one or more events have occurred that have detrimental impact on the estimated future cash flows of the asset

Example of such events:v Significant financial difficulty of the issuer or the borrowerv A breach of contract –e.g. a default or past due eventv A lender having granted a concession to the borrower that the lender would not otherwise

considerv It becoming probable that the borrower will enter bankruptcy or other financial

reorganizationv The disappearance of an active market for that financial asset because of financial

difficultiesv The purchase of a financial asset at a deep discount that reflects the incurred credit losses

Ind AS Course ICAI

61

GENERAL APPROACH

v Under Ind AS 109, the EIR is used to allocate interest revenue or expense over the expected life of the financial instrument

v Generally, interest revenue and expense are calculated as follows

Revenue Apply the EIR to the gross carrying amount of a financial asset

Expense Apply the EIR to the amortized cost of a financial liability

Ind AS Course ICAI

62

DEFINITION OF DEFAULT

v No definition of the term defaultv Each entity should do sov Should be consistent with that used for internal credit risk management purposesv Qualitative indicators – breaches of covenants to be consideredv Standard contains a rebuttable presumption that default does not occur later than

90 days past due

Ind AS Course ICAI

63

WHEN TO RECOGNIZE LIFETIME ECL

v When the credit risk on a financial instrument has increased significantly since initial recognition

Definition of significant increase in credit riskv No definition in the standardv Entity uses the change in the risk of default occurring over the expected life of the

financial instrumentv Whether risk of default has increased significantly since initial recognition

Ind AS Course ICAI

64

OVERVIEW - IMPAIRMENT REQUIREMENTS

Stage 1v 12 month expected credit losses recognized in profit or loss through a loss

allowance as soon as a financial instrument is purchased

v Proxy for initial expectation of credit losses

v For financial assets, interest revenue is calculated on the gross carrying amount (before adjusting for the expected credit losses)

Ind AS Course ICAI

65

OVERVIEW IMPAIRMENT REQUIREMENTS

v Stage 1 includes financial instruments that have not had a significant increase in credit risk since initial recognition or that have low credit risk at the reporting date

v For these assets, 12-month expected credit losses (‘ECL’) are recognized and interest revenue is calculated on the gross carrying amount of the asset (that is, without deduction for credit allowance)

Ind AS Course ICAI

66

OVERVIEW IMPAIRMENT REQUIREMENTS

Stage 2v If the credit risk increases significantly and the resulting credit quality

is not considered to be low credit risk, full life-time expected credit losses are recognized

v For financial assets, interest revenue is calculated on the gross carrying amount (before adjusting for the expected credit losses) –Same as for Stage 1

Ind AS Course ICAI

67

OVERVIEW IMPAIRMENT REQUIREMENTS

v Stage 2 includes financial instruments that have had a significant increase in credit risk since initial recognition (unless they have low credit risk at the reporting date) but that do not have objective evidence of impairment

v For these assets, lifetime ECL are recognized, but interest revenue is still calculated on the gross carrying amount of the asset

v Lifetime ECL are the expected credit losses that result from all possible default events over the expected life of the financial instrument

v Expected credit losses are the weighted average credit losses with the probability of default (‘PD’) as the weight

Ind AS Course ICAI

68

OVERVIEW IMPAIRMENT REQUIREMENTS

Stage 3v If the credit increases to the point that it is considered credit-impaired,

full life-time expected credit losses are recognized – Same as in Stage 2

v For financial assets, interest revenue is calculated on the amortized cost (gross carrying amount less life-time expected credit losses)

v Financial assets in Stage 3 will generally be individually assessed

Ind AS Course ICAI

69

IMPAIRMENT REQUIREMENTS-STAGE 3

v Stage 3 includes financial assets that have objective evidence of impairment at the reporting date

v For these assets, lifetime ECL are recognised and interest revenue is calculated on the net carrying amount (that is, net of credit allowance)

Ind AS Course ICAI

70

OVERVIEW IMPAIRMENT REQUIREMENTS

Increase in credit risk since initial recognition

Ind AS Course ICAI

Copyright Notice

"This presentation contains copyright © material of the IFRS Foundation and The Institute of CharteredAccountants of lndia. All rights reserved. Published by The institute of Chartered Accountants of lndia underlicence from the IFRS Foundation. Reproduction and use rights are strictly limited. For more information about theIFRS Foundation and rights to use its material please visit www.ifrs.org".

![ga¥J.t~~~~~~~~~~~~ ¥J.t~~~€¦ · 8 THEGAZETTEOFINDIA: EXTRAORDINARY [PARTII-SEC. 3(i)] "(6) Onand after 1stApril 2016, the driver of motor vehicle of Ml category, manufactured](https://img.pdfslide.us/doc/110x75/602e1d0f87726568cc7b10d7/gajt-jt-8-thegazetteofindia-extraordinary-partii-sec-3i.jpg)