Embed Size (px)

Citation preview

2010 Increasing the Use of Wood in New Brunswick Public Buildings

A study of the potential for increasing the use of wood in non-residential construction with recommendations for moving forward, undertaken for the New Brunswick Forest Products Association by the University of New Brunswick Wood Science & Technology Centre and Patrice Tardif Consulting. March 31, 2010

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

i

Cover Photo Credits:

B e than y B i ble Co l le g e , Sussex, New Brunswick – 2007 Architects: Ar c hi te c ts Fo ur Ltd. Photo: Courtesy Goodfellow

Tr e e Se e dl i n g s Photo: Gérard Sirois Source: Images of New Brunswick

This publication may not be reproduced, published or transmitted, in whole or in part, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, whether or not in translated form, without the prior written permission of the New Brunswick Forest Products Association. Exempt from this requirement are the author, Patrice Tardif, representatives from the University of New Brunswick Wood Science and Technology Centre and Business New Brunswick who were involved during the preparation of the document, and funding partners.

This publication is designed to provide accurate information. Any errors and omissions are unintentional. The author is not responsible for consequences arising from the use of any information contained herein.

Fo r m o r e i n fo r m ati o n , p le ase c o n tac t:

New Brunswick Forest Products Association Mark L. Arsenault, President and CEO Hugh John Flemming Forestry Centre 1350 Regent Street Fredericton, New Brunswick Canada, E3C 2G6 Telephone: 506-452-6930 Email: [email protected]

Thi s publ i c ati o n i s avai lable at:

http://n bfo r e str y.c o m ///uplo ads//We bsi te _Asse ts/ NB FPA_In c r e asi n g _the _Use _o f_Wo o d.pdf

http://www.unb.ca/fredericton/forestry/wstc/publications.html

© Patrice Tardif Consulting All rights reserved

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

ii

Execut ive Summary

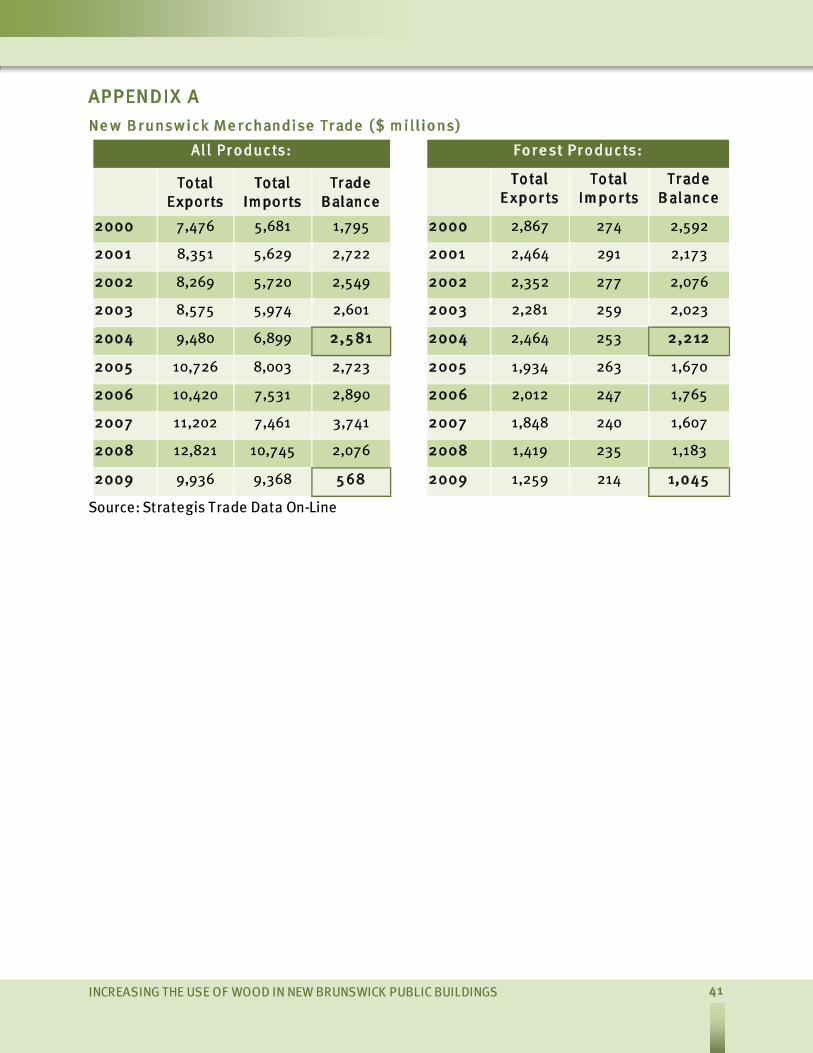

The New Brunswick wood products industry has not been immune to the economic turmoil of the last several years. Lower housing starts in the United States, the main export market for New Brunswick softwood lumber, a strong Canadian dollar, off-shore competition, and competition from the rest of Canada following resolution of the softwood lumber tariffs have all contributed to the effects on the province. The result for New Brunswick’s wood products industry has been mill closures, reductions in production capacities and job losses. The province had a near 2.2$ billion decline in balance of trade between 2004 and 2009, more than half of which was directly attributable to the forest products sector. There is an immediate need to strengthen the New Brunswick forestry sector and create new demand for wood products.

To fully appreciate the current position of the forest products sector in New Brunswick, an investigation into the existing reality for the sector was undertaken. The forestry sector was explored as was its relationship to the provincial economy. This was followed by an evaluation of the potential for increased wood use in the non-residential construction market, the ability of the design and construction community to design and build with wood, and other potential market considerations. Regulations affecting the built environment in the province were studied and any barriers and preconceptions affecting the potential for increasing wood use were identified. The efforts of various jurisdictions, in Canada and abroad, were reviewed to understand their responses to similar challenges. The recommendations, policies and regulations implemented in these jurisdictions were studied in an effort to understand what was successful and what wasn’t, with an eye to the relevance for the New Brunswick situation.

Based on the current reality for the forestry sector in New Brunswick and experiences in other jurisdictions striving for increased wood use, recommendations were developed to help direct the New Brunswick forest products industry on how to strengthen its position moving forward. The major components identified are listed below.

THE NEED FOR GOVERNMENT TO SET LIMITS ON THE CARBON FOOTPRINT OF THE BUILT ENVIRONMENT, an initiative which would spur the use of wood.

THE NEED FOR AN INDUSTRY COALITION, based on representation from all sectors, to develop a unified industry vision.

THE NEED FOR AN INDUSTRY VISION, based on positioning wood as helping to meet climate change reduction goals.

THE NEED FOR A MULTI-SECTORIAL COALITION, a group to coordinate industry initiatives in the context of sustainable development on socio, economic and environmental levels for the province.

THE NEED FOR A WoodWORKS! PROGRAMME, to support the design and construction community.

THE NEED FOR APPROPRIATE CURRICULUM AT UNIVERSITY, COLLEGE AND TRADE SCHOOL LEVELS, for adequate preparation of the manufacturing, design and construction workforces.

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

iii

THE NEED FOR RESEARCH AND DEVELOPMENT, to help develop products that meet specialized demands in world-wide markets. Consideration should be given to the needs for disaster relief housing, drawing upon an existing expertise in the province in the factory-built housing sector and in timber engineering.

CONSIDERATION OF A PAN-ATLANTIC APPROACH, to achieve maximum momentum for efforts in the Atlantic region on a global scale.

Activities related to each of these components can be found in the Recommendations portion of the report.

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

iii

THE NEED FOR RESEARCH AND DEVELOPMENT, to help develop products that meet specialized demands in world-wide markets. Consideration should be given to the needs for disaster relief housing, drawing upon an existing expertise in the province in the factory-built housing sector and in timber engineering.

CONSIDERATION OF A PAN-ATLANTIC APPROACH, to achieve maximum momentum for efforts in the Atlantic region on a global scale.

Activities related to each of these components can be found in the Recommendations portion of the report.

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

iv

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

v

Table o f Con ten ts

Executive S um m ary ..............................................................................................................ii

I ntroduction.......................................................................................................................... 1

The New Brunswick R eality .................................................................................................2

Forests................................................................................................................................ 3

Wood Products...................................................................................................................... 4

The Economy ........................................................................................................................ 5

The Non-residential Construction Market (ICI: Industrial, Commercial and Institutional).................... 7

Design/Construction Expertise in the Province ........................................................................... 9

Provincial Regulations Affecting the Forest Products Industry and the Built Environment..................13

Current Barriers to the Use of Wood in Non-Residential Applications .............................................15

Ef forts in O ther J urisdictions ............................................................................................. 18

British Columbia ................................................................................................................. 18

Quebec.............................................................................................................................. 20

Finland.............................................................................................................................. 24

France ............................................................................................................................... 26

New Zealand ...................................................................................................................... 29

O ther J urisdictions .............................................................................................................30

S um m ary ............................................................................................................................ 31

S trategic A pproach ............................................................................................................33

R ecom m endations..............................................................................................................35

Bibliography .......................................................................................................................38

A cknowledgem ents ............................................................................................................40

A PPENDI X A ........................................................................................................................ 41

A PPENDI X B ........................................................................................................................42

A PPENDI X C ........................................................................................................................49

A PPENDI X D ........................................................................................................................ 51

A PPENDI X E ........................................................................................................................52

A PPENDI X F.........................................................................................................................53

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

vi

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

1

In t roduct ion

Wood-specific policies implemented in various jurisdictions, here in Canada and abroad, have helped spur the use of wood in construction. The province of New Brunswick, with its strong wood industry presence, could be poised to help both its local industry and its built environment reap the benefits of increased wood use. More wood use in buildings would lead to a stronger regional economy and result in a more sustainable built environment. A more diversified value-added wood product sector would open markets for New Brunswick and create long-term growth and stability in the industry.

Environmental concerns, such as green house gas emissions and global warming, govern more and more of our daily choices; wood should be the natural choice. It is the only building material made from a renewable feedstock – trees. The use of more wood in New Brunswick buildings would also lead to buildings with a lower carbon footprint. Unfortunately, wood is not the natural choice in the non-residential construction sector. In eastern Canada, less than 10% of non-residential buildings (which include institutional, commercial, industrial and multi-residential buildings) are built using wood.1

In order to determine a future direction for growing the wood products industry in New Brunswick, it is important to first characterize the current context. To that end, information on the impact of the forest industry on the provincial economy was sought. An exploration of forestry practices in the province was undertaken, as was an inventory of products manufactured and their applicability to the built environment in New Brunswick. Incentives available to manufacturers for technological advances through government programmes were identified. The non-residential construction market was studied to determine the potential for growth in wood use for the sector as was the competence of current and future design professionals and builders to design and build non-residential buildings in wood. There was an examination of any disincentives to using wood in construction in the province as well as an identification of current legislation governing construction.

Once an understanding of the current context was reached, various jurisdictions were studied in an effort to glean useful information pertinent to the New Brunswick circumstance. The provinces of British Columbia and Quebec have both made recent changes to spur the use of wood in those provinces and the pertinence of their programmes in the North American context is key. Various players in Finland, France and New Zealand have also been active in attempting to validate and grow their respective wood consumption, with varying degrees of success. The study of all the aforementioned jurisdictions, with their respective experiences, provided invaluable information in determining an approach for the New Brunswick forest products industry. Industry and government will be shown to be essential ingredients to a successful campaign, but the interaction between the two, in conjunction with other important players, needs to strike a pertinent and effective balance.

It was not within the tasks identified for this project to elaborate on the environmental responsibility of wood products based on a convincing body of scientific evidence (e.g. responsible energy use and low polluting practices for harvesting the raw resource and manufacturing, carbon sequestration, thermal properties, renewability, etc.). There are many sources for such information and the reader is referred to the Canadian Wood Products

________________________________________________________________________________________________________ 1 Canadian Wood Council

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

2

Information Portal at www.planetfriendlycanada.com. Comments in this report will be limited to the fact that, the superiority of wood products as regards their overall environmental impact, from material extraction, through product manufacturing, to the use of the products and their maintenance throughout their lifetime, has been demonstrated through the use of life cycle assessment (LCA). LCA is a scientific method of assessment used to determine the burdens placed on the environment by a product through all stages of its life. The model of record for life cycle assessments in North America, with worldwide recognition, is the Athena model, developed here in Canada.2

The goal of the currentproject was to elaborate on a plan of action for the New Brunswick wood products industry moving forward, in terms of strategies for growing market share as well as spurring production and product mix. This is done in such a way as to clearly determine what actions can be implemented easily and in a timely fashion, and what can be done in the medium and long terms to meet a common vision. Suggestions are presented on how to arrive at a common vision, and recommendations are made for the actions that will support it. There are also references in the report to aspects worthy of further investigation.

The New B run s wick Real i ty

In order to determine where to orient the future of wood use in New Brunswick, it is important to understand the current context. In this section, the New Brunswick forest industry will be put into a geographic and an economic context. The non-residential construction sector will be evaluated to determine the potential for appearance and structural wood product use; provincial regulations governing construction will be identified, along with any barriers keeping wood from reaching its full potential in the sector. Provincial incentive programmes are identified to clarify opportunities available to industry. Through these programmes there is a potential for assistance in responding to an increased demand for specialized products which would come from an increase in wood use in the non-residential construction sector or from emerging markets. The competence of the design and construction community is also estimated, as are existing programmes for the education of design and construction professionals and of forest industry employees (forestry and manufacturing). Changes needed in educational programmes could then be identified to insure appropriate expertise in wood processing, and design and construction disciplines for the province.

________________________________________________________________________________________________________ 2 Athena Institute – www.athenasmi.org.

Photo: Bil l Miller Source: Images of New Brunswick

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

3

Fo r e sts

There is no doubt that New Brunswick is a forested province. Of the 71,290 km2 which comprise the province, 87% or 6.1 million hectares is forested.3 These forests and adjacent watersheds are home to over 40 different mammals, from the tiny Maritime Shrew to the impressive moose, over 100 birds, some amphibians and over 40 species of fish, native and naturalized freshwater and diadromous4 species.5

For the most part, New Brunswick’s forest is considered in the Acadian Forest region. The forest in the northern part of the province is considered in the Great Lakes – Saint Lawrence region. A mix of approximately 20 commercial species can be found in New Brunswick’s forests; certain areas are dominated by hardwoods (about 25% of the forested area), while softwoods dominate other areas (approximately 44%). The remainder of the forested lands are a mixture of softwoods and hardwoods.

The mix of private vs. public forested lands for New Brunswick is as follows:

Ow n e r shi p % o f To tal

Pr o vi n c i al Cr o w n Lan ds Public 51

Fe de r al Cr o w n Lan ds Public 2

In dustr i al Fr e e ho ld Lan ds Private 18

Pr i vate Wo o dlo ts Private 29

The federal Crown lands are protected (military base and National park lands) and approximately one-quarter of the provincial Crown lands are classified as Conservation Forest. The remainder of provincial Crown lands are managed primarily for timber production, although those lands also have recreational uses and other non-timber values. Forest management strategies are employed to ensure well-distributed self-supporting populations of vertebrates (mammals, birds, amphibians) and fishes on crown lands, including six old-forest wildlife habitat types on which approximately 50 species of vertebrates depend. Approximately 1.2% of all New Brunswick forest lands are harvested yearly. There were no recorded losses due to insect infestation from 2006 to 2008 and negligible loss due to forest fires during that time (0.015%).6 The latter is in large part due to easy access networks resulting in quick response times, as well as the province’s humid climate.

As of 2002, public lands have been required to meet third-party certification to a sustainable forest management programme so there is virtually no deforestation in these areas. There is

________________________________________________________________________________________________________ 3 Source: Natural Resources Canada 4 Encarta Dictionary: describes fish that migrate between fresh and salt water 5 NB Department of Natural Resources 6 ibid

Fundy National Park of Canada, Southern New Brunswick Photo: J.-F. Bergeron Source: Images of New Brunswick

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

4

an increasing amount of plantation forest in the province, 13% of Crown lands are now plantation forests, leading to an increase in stands with similar-aged trees.7 Nearly 100% of Crown lands and industrial freehold lands are certified to the Sustainable Forestry Initiative’s sustainable forest management programme (SFI). Very little of the private woodlots are certified to sustainable forest management programmes. Seven marketing boards8 were established to help market primary forest products from private woodlots. The boards oversee silviculture programmes for private woodlot owners but certification is not required. As of 2007, New Brunswick had nearly three-quarters of its forests (4.7 million hectares) certified to sustainable forest management programmes.9

Wo o d Pr o duc ts

There are many different products manufactured in the province although volumes have decreased considerably in the last five years, mostly as a result of the economic downturn and resultant production slowdowns and mill closures. The United States being the primary export market for the province keeps the New Brunswick forest industry very dependent on the economy there. Just over 75% of NB’s sawn lumber is destined for the U.S. market each year.10 Unfortunately, during the time that this report was prepared, there were no published or unpublished sources of information available to ascertain volumes for wood products classified in the secondary (wood I-joists, panel products, etc.) and value-added sectors (kitchen cabinets, manufactured housing, mouldings, etc.) in New Brunswick. Most of the information amassed is for the Atlantic region in general. As such, it is difficult to ascertain the availability of products being manufactured within the geographic extent of the province to meet current or a potential increased demand.

A list of wood products manufactured in the province can be found in Table 1.

Table 1 – Wo o d pr o duc ts m an ufac tur e d i n Ne w B r un sw i c k:

Pr i m ar y Se c o n dar y Value -Adde d

dimension lumber (structural softwood)

cedar lumber hardwood lumber

planks/boards (HW)

heavy timber

I-joists (with captive MSR graded lumber)

floor trusses MDF

particleboard

finger-jointed white pine and SPF veneers

fencing, railing, decking, newel posts

shingles and shakes siding

MDF mouldings kitchen cabinets

doors and windows

cabinet doors pressure-treated

products thermally modified wood

pallets

manufactured housing timber-framed housing

Other products, such as poplar plywood and glued-laminated timber, were once manufactured in the province put those facilities now lie dormant. An oriented strand board facility which currently is not operational may be coming back online in the near future. At present, poplar

________________________________________________________________________________________________________ 7 The diversity of species and age-mix of forest tracts were not quantified for this report 8 Marketing Boards were empowered by the New Brunswick Natural Products Act. 9 Source: Canadian Sustainable Forestry Coalition/FPAC/FAO 10 Source: Maritime Lumber Bureau

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

5

plywood, OSB and glulams, along with thick MDF for moulding production, MSR lumber, laminated veneer lumber and other elements, have to be imported to meet market demands.

Other than wood products, the forest industry also comprises pulp and paper production, pulp for the textile industry, Christmas tree farming, pellets for bio-energy, and maple sugar operations. Although these sectors were not examined for this report, it should be noted that in November 2008, the provincial government announced the New Brunswick Crown Land Forest Biomass Harvesting Policy11 following several years of research at the University of New Brunswick in Fredericton. The policy applies to 3.3 million hectares of Crown land and will make one million cubic metres of forest biomass available yearly. This material, according to the Minister of Natural Resources at the time (Hon. Donald Arsenault), will “help reduce energy costs … explore new forest market opportunities … (and) support other economic development initiatives …”

The E c o n o m y

New Brunswick can be said to have the most forest dependent economy of any province in Canada. The forest products industry, which includes primary forestry operations, pulp and paper, as well as wood products manufacturing, contributed 5.2% to New Brunswick’s Gross Domestic Product in 2008, down from 8.4% in 2004.12 New Brunswick is the dominant player when it comes to the forest products industry in the Atlantic region, contributing 72% of the total output of wood products and 58% of the total pulp and paper output for all four provinces. As of 2005, there were approximately 50 communities in the province that were dependent on the forest products industry13 but this has eroded somewhat since then with several more plant closures in recent years.

In 2008, 12,800 people (that’s one out of every 15 New Brunswickers) were directly employed by the province’s forest products industry – 70% of them in rural areas. This number can create two to four times that number in indirect employment. Approximately 8,800 of those employed worked in the forestry, logging, and wood products manufacturing sectors (i.e. excluding pulp and paper). It should be noted that these figures are down 25% from just two years prior – the harsh reality of our economic times – and there is a continual decline. The Miramichi/Bathurst/Dalhousie region was particularly hard hit as mill closures in the area resulted in a loss of employment for nearly 15% of the workforce. Private woodlot owners have been particularly hard hit in the past few years as these producers have borne the brunt of many mill closures. Pulp mill closures in particular have impacted harvest levels and the rural communities where they were the primary employers. In addition to job losses due to mill closures and production slowdowns, the New Brunswick forestry industry workforce is

________________________________________________________________________________________________________ 11 Effective October 22, 2008 – Policy No. FMB 019 2008, www.gnb.ca 12 APEC 13 ibid

New Brunswick Sawmill Photo: Gérard Sirois Source: Images of New Brunswick

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

6

diminishing, in general – an increasingly aging labour force will be hit with a large wave of retirements in the near future without a real upswing of new recruits to take up the slack. The allure of higher paying jobs in provinces such as Alberta is too much to ignore.

An APEC report published in 200814 takes a comprehensive look at market fluctuations in the past 10 to 15 years in the Atlantic region that have affected the forestry economy. Market fluctuations can be attributed to exemption from the U.S. softwood lumber tariffs on the up side, and the strength of the Canadian dollar and a reversal of Asian reliance on North American wood and paper products as their own mills ramped up domestic production on the down side, among other pressures. The economic downturn which has severely affected North America resulting in important declines of housing starts in the U.S. has resulted in a sharp decline of exports for New Brunswick. Always an important component of New Brunswick’s balance of trade, a balance of trade which saw a decline of nearly 2.2$ billion between 2004 and 2009; 1.2$ billion of that decline was directly attributed to forest products.15 This reality has been exacerbated by competition from the rest of Canada following the “resolution” of the lumber tariffs. Prices for New Brunswick lumber have also been high when compared with B.C. beetle lumber which has inundated the market, adding more pressure to a beleaguered industry. The fallout has been, as elsewhere in North America, consolidations and mill closures. It must be said that capital investments in the New Brunswick forest industry in the last few years have been limited. Smaller, more outdated facilities cannot benefit from the economies of scale that larger more modern facilities can take advantage of during difficult economic times.

The New Brunswick wood products industry cannot be said to be high up the value chain as regards its wood products mix, having largely relied on the U.S. demand for its superior quality softwood lumber products. It is becoming apparent, however, that reliance on U.S. markets may be a thing of the past. There is a need for a broader vision; one might say a vision to “abroad.” New Brunswick is strategically placed, with access to marine shipping that would be envied by most and which will need to be capitalized upon moving forward. There will be a need to think globally in the development of the New Brunswick industry, with higher value products, to fill specific needs in order to create new markets. The U.S. may not be a reliable export market in the long term.

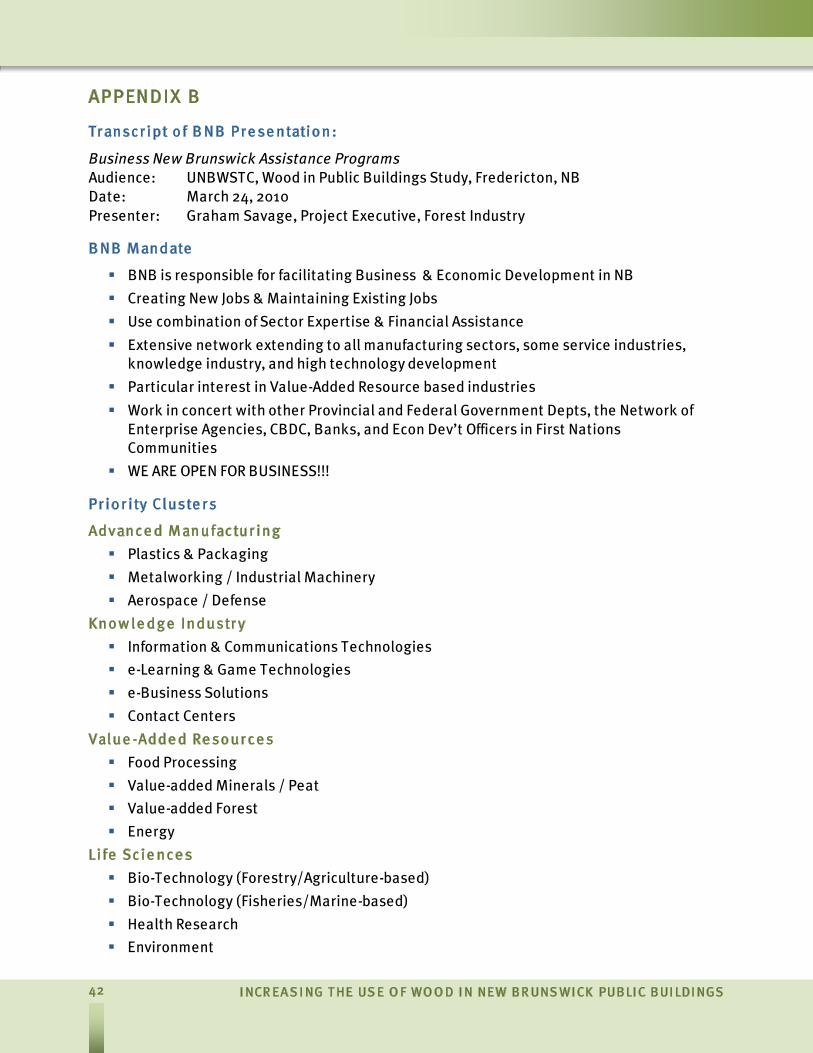

G o ve r n m e n t Assi stan c e Pr o g r am m e s

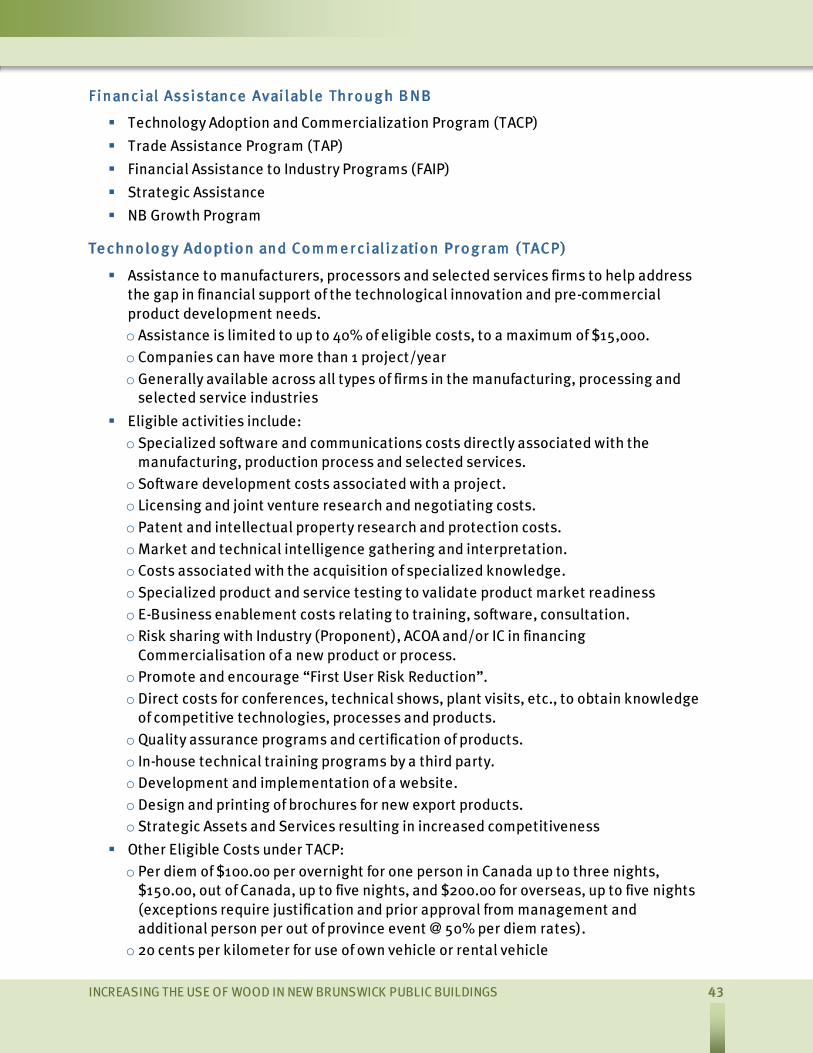

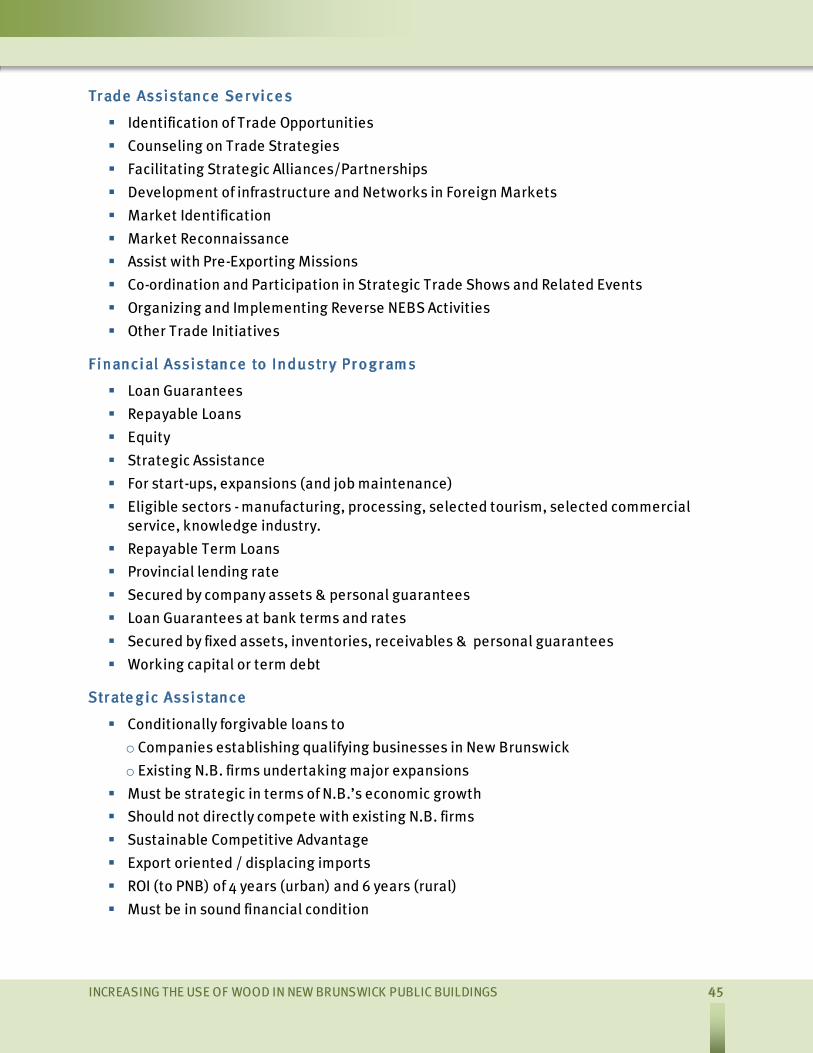

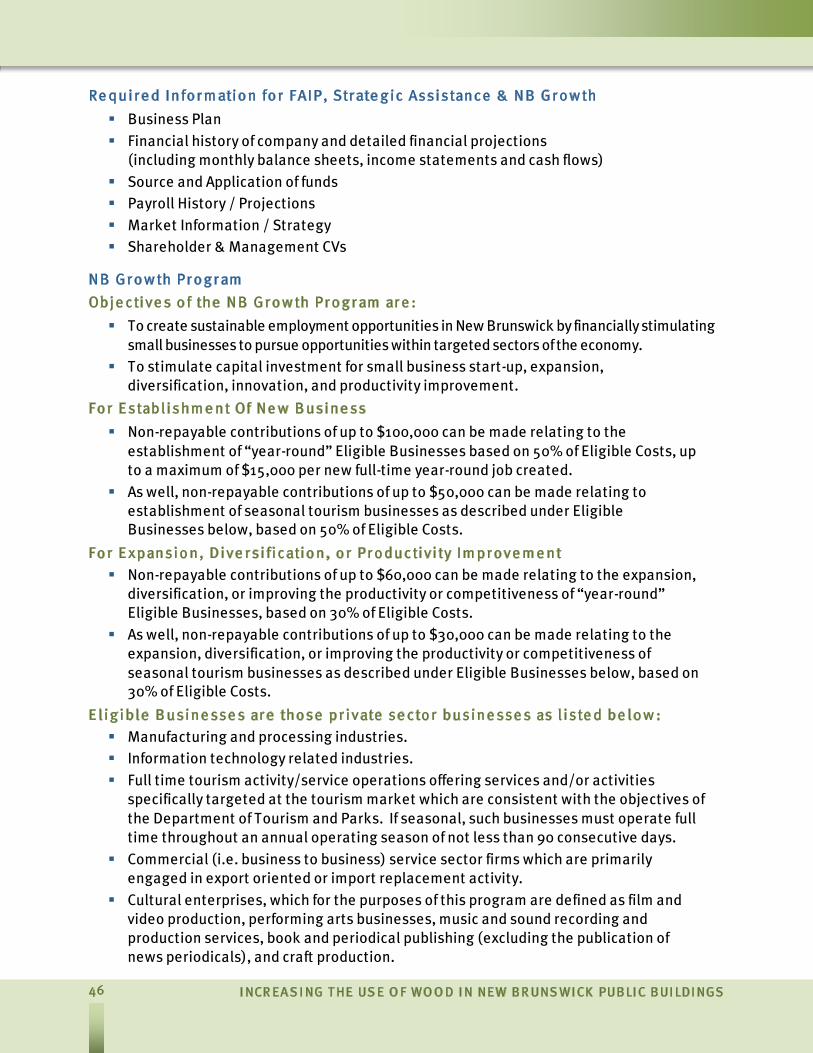

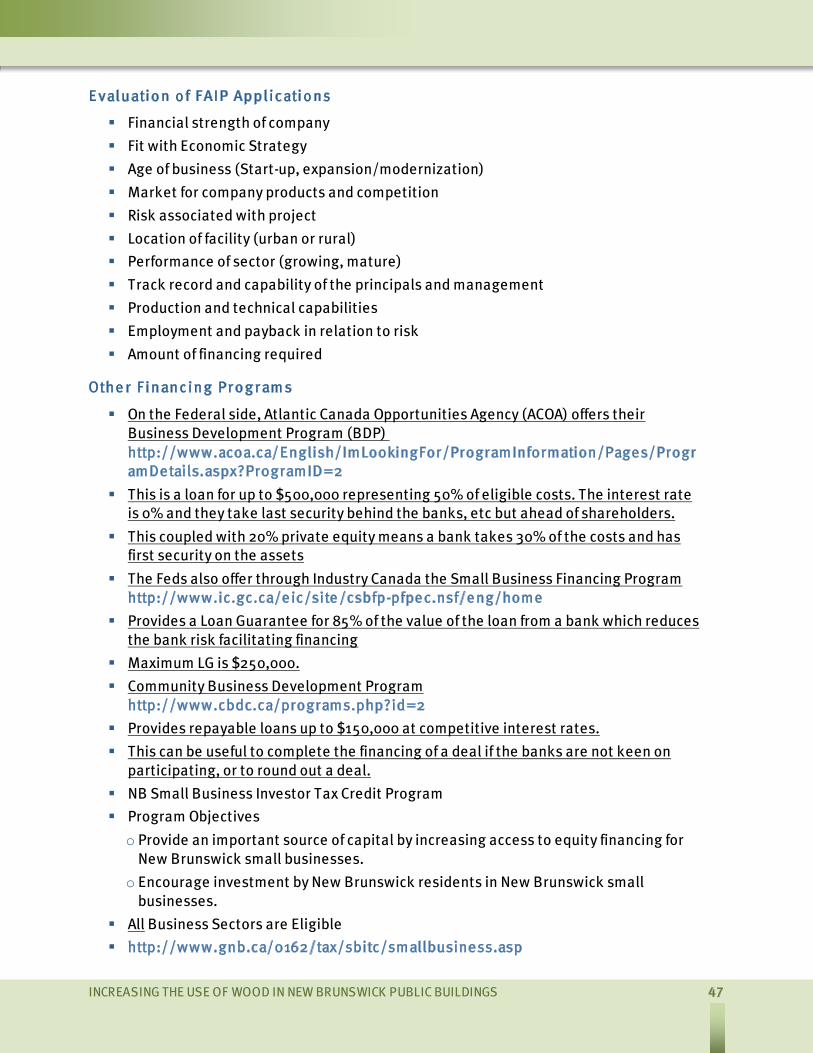

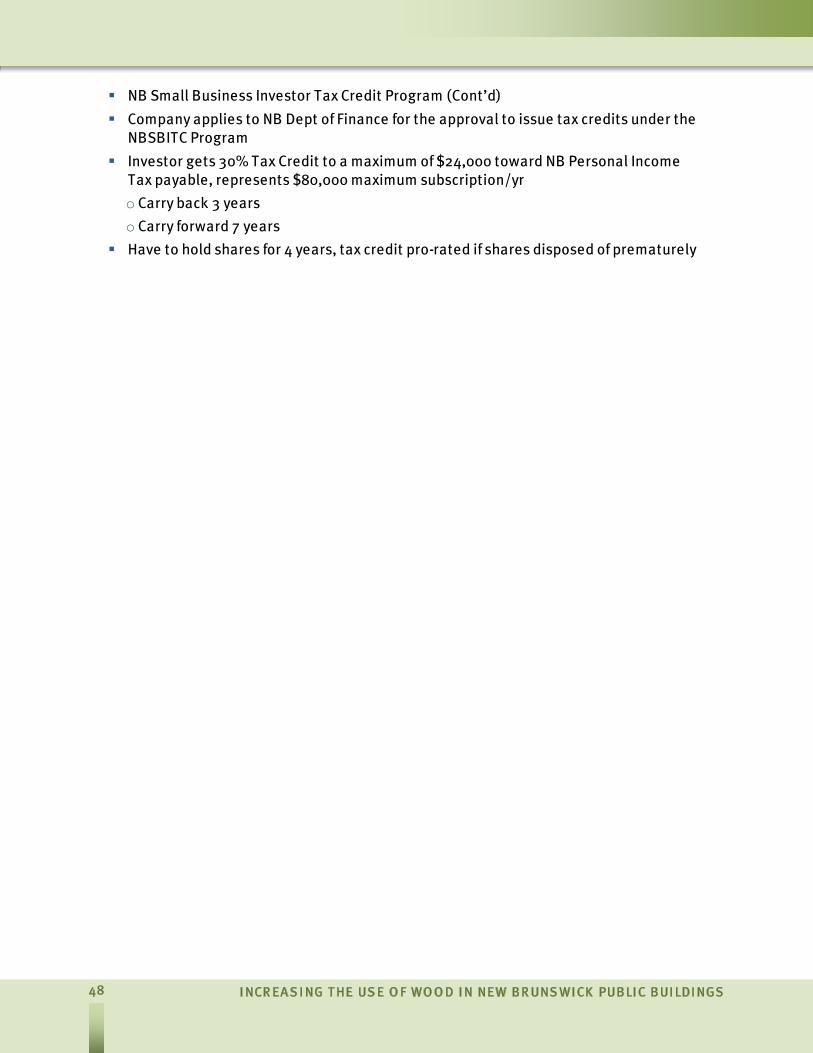

Business New Brunswick (BNB), a provincial government department with the responsibility for facilitating business and economic development in the province, has several assistance programmes that could be of benefit to the value-added sector of the forest industry moving forward. Of the Priority Clusters identified by BNB, the Value-Added Resource Cluster (Value-Added Forest and Energy) and the Life Sciences Cluster (Bio-Technologies and Environment) have the potential to help New Brunswick’s forest products industry. Specific programmes worthy of note include:

Technology Adoption and Commercialization Programme (technological innovation and pre-commercial product development);

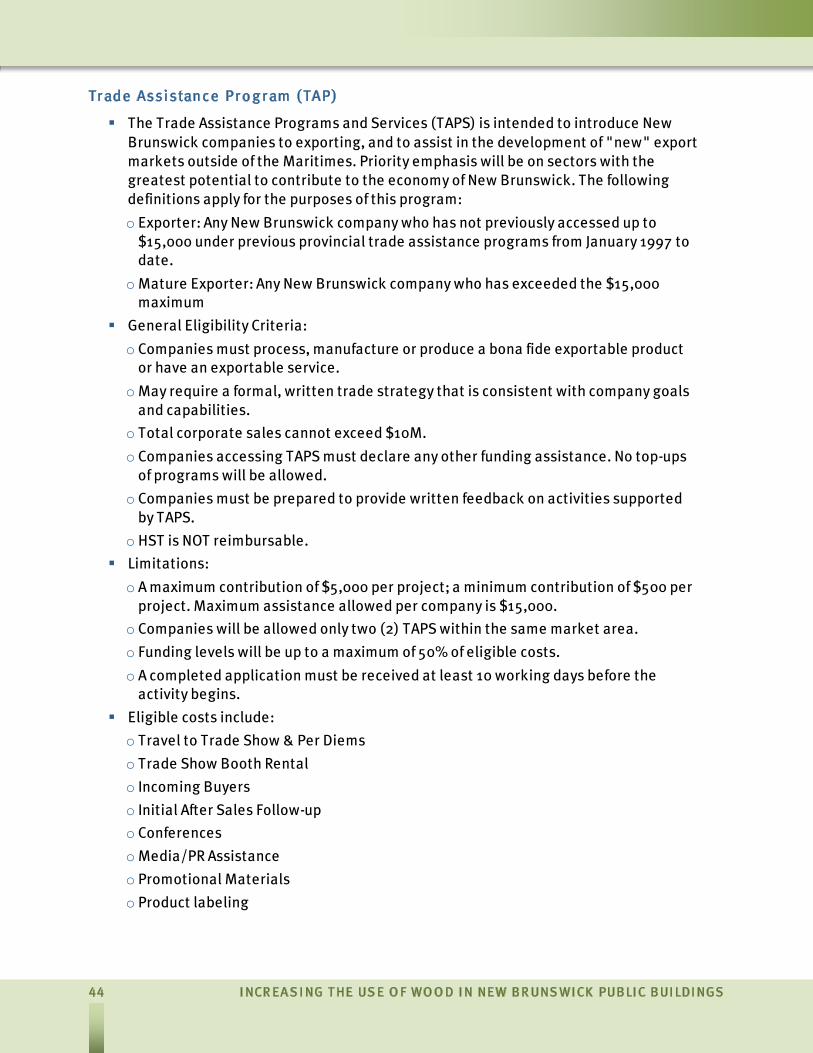

Trade Assistance Programme (development of new export markets);

________________________________________________________________________________________________________ 14 Atlantic Provinces Economic Council, August 2008, Building Competitiveness in Atlantic Canada’s Forest Industries: A Strategy for Future Prosperity 15 Statistics Canada – See Appendix A

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

7

Financial Assistance to Industry Programmes (start-ups, expansions, job maintenance);

Strategic Assistance (non-competing business development strategic to NB’s economic growth);

New Brunswick Growth Programme (sustainable employment, new business opportunities).

There are also some federally-funded programmes for industry to consider:

Atlantic Canada Opportunities Agency (ACOA) – Business Development Programme

Industry Canada – Small Business Financing Programme

More detailed information can be found on these and other programmes in Appendix B: a transcript of the presentation given at the University of New Brunswick Wood Science and Technology Centre by Business New Brunswick, in March of 2010.

Unfortunately, New Brunswick’s softwood lumber producers are not able to benefit from these programmes without jeopardizing Atlantic Canada’s exemption status as stipulated in the Atlantic Canada Special Exemption Clause under the Canada / U.S. Softwood Lumber Agreement. As a consequence, softwood lumber producers wishing to modernize or expand into the value-added sector must do so with no reliance whatsoever on funding assistance from government, whether in the form of grants, subsidies or non-repayable loans.

The No n -r e si de n ti al Co n str uc ti o n M ar ke t ( ICI: In dustr i al , Co m m e r c i al an d In sti tuti o n al)

The non-residential construction sector in New Brunswick, which includes industrial, commercial, institutional and multi-residential buildings, is often referred to as the ICI sector. Although the New Brunswick housing stock is primarily wood-frame construction, similar to the North American housing stock in general, the same cannot be said of buildings in the ICI sector.

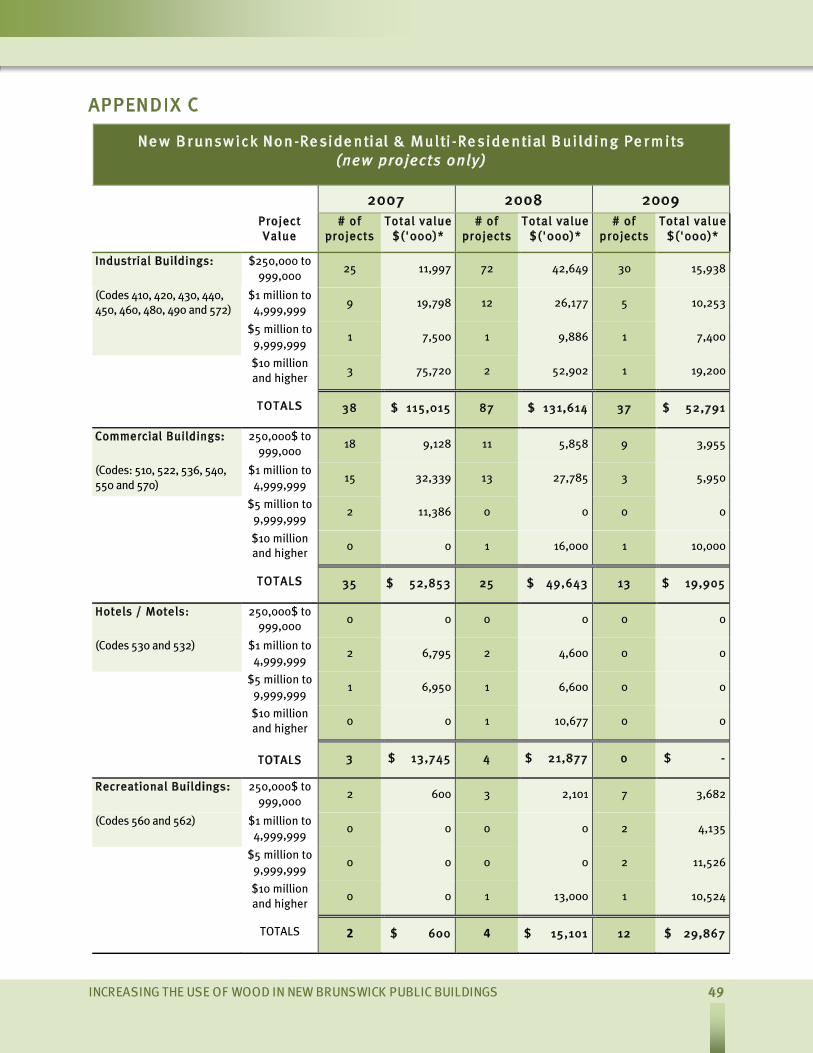

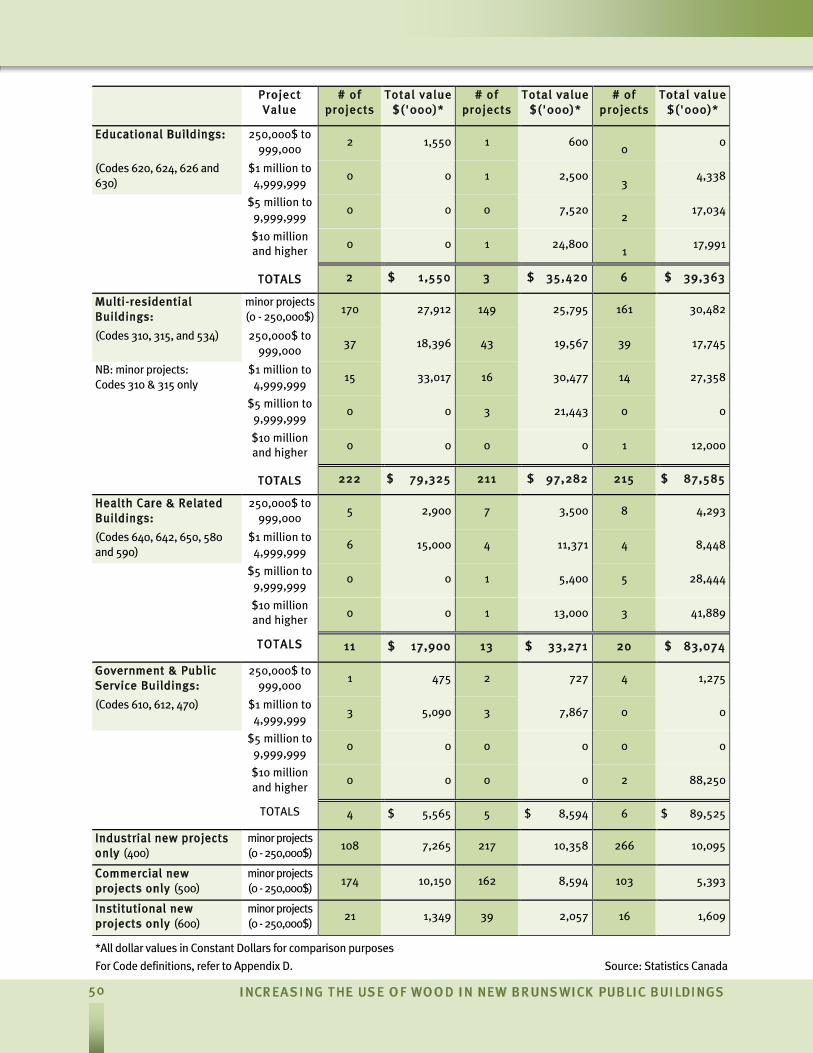

Since October 1, 2009, the governing building code in New Brunswick has been the 2005 National Building Code of Canada (NBCC). The NBCC would allow for 70%, if not more, of non-residential buildings typically built in New Brunswick to be constructed using wood structural systems. The actual number of ICI buildings built using wood is far less than that; in general the percentage falls between 7 and 9%. Values for New Brunswick building permits in the ICI and multi-residential construction sectors as prepared by Statistics Canada for 2007 to 2009 can be found in Appendix C. The permit values demonstrate where the potential for wood products exists, according to major construction types and size (or permit values). They also show important changes in investment for the province in the past three years. Several statistics are worthy of note, namely:

The industrial sector has seen a 60% drop in new construction since 2008 and a 55% drop when compared with 2007.

Aboriginal Heritage Gardens, Eel River, New Brunswick– 2006 Architects: David Foulem Architect Inc. Photos: Courtesy Goodfellow

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

8

Commercial buildings have seen a 62% drop since 2007.

The construction of recreational buildings has seen an increase in activity for each of the past two years with only two facilities built in 2007, but with 12 facilities built in 2009.

Educational building needs have been consistent for the past two years in terms of investment but smaller schools were built in 2009 – the number of schools built doubled but the permit values were very similar for the last two years. There was a large increase in educational building permit values between 2007 and 2008 due to one large facility being constructed.

Multi-residential buildings, primarily in the 0 to 250,000$ range, have maintained their market share, for the most part throughout the period, both in terms of permit values and numbers of buildings. This is an important sector, which is typically predominated by wood-frame construction, although larger, higher permit value projects may not be built in wood. This was not, however, able to be ascertained.

Health care and related building account for a large portion of the ICI permit budget for 2009, up considerably from previous years; 2009 permit values more than quadrupled since 2007, and more than doubled the 2008 values.

The government building and public service building sectors saw a marked increase in 2009 with two projects claiming permit values over 10$ million each.

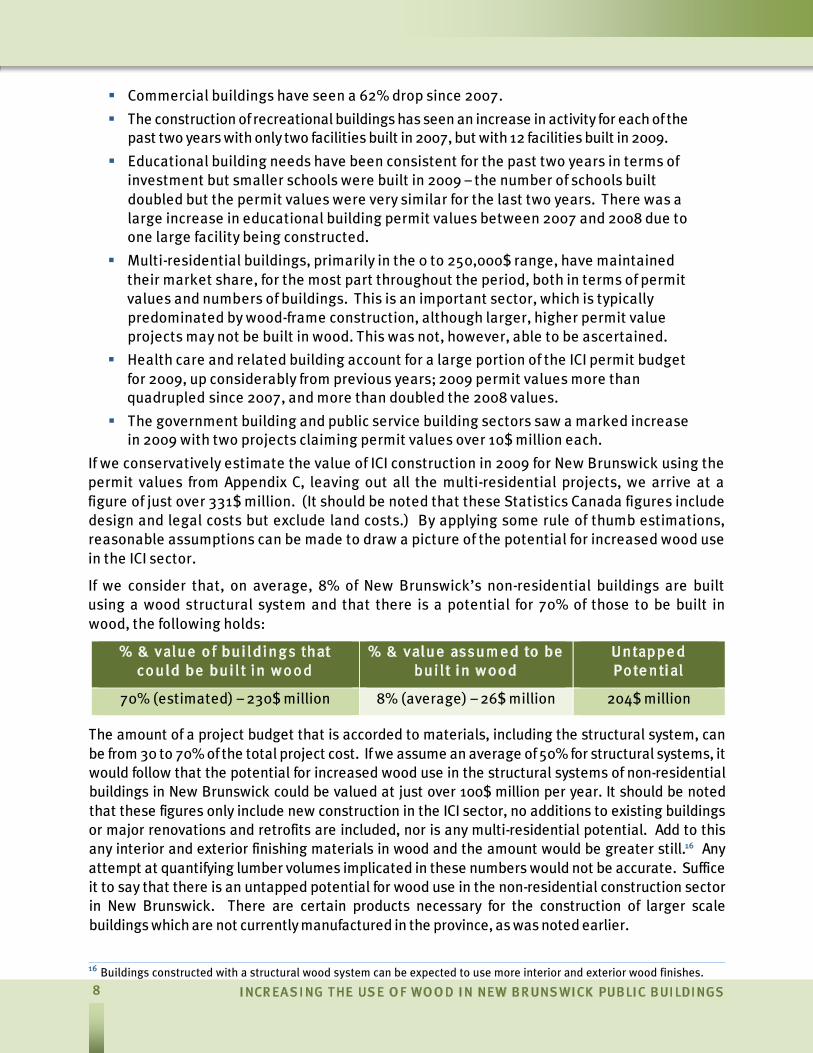

If we conservatively estimate the value of ICI construction in 2009 for New Brunswick using the permit values from Appendix C, leaving out all the multi-residential projects, we arrive at a figure of just over 331$ million. (It should be noted that these Statistics Canada figures include design and legal costs but exclude land costs.) By applying some rule of thumb estimations, reasonable assumptions can be made to draw a picture of the potential for increased wood use in the ICI sector.

If we consider that, on average, 8% of New Brunswick’s non-residential buildings are built using a wood structural system and that there is a potential for 70% of those to be built in wood, the following holds:

% & value o f bui ldi n g s that c o uld be bui l t i n w o o d

% & value assum e d to be bui l t i n w o o d

Un tappe d Po te n ti al

70% (estimated) – 230$ million 8% (average) – 26$ million 204$ million

The amount of a project budget that is accorded to materials, including the structural system, can be from 30 to 70% of the total project cost. If we assume an average of 50% for structural systems, it would follow that the potential for increased wood use in the structural systems of non-residential buildings in New Brunswick could be valued at just over 100$ million per year. It should be noted that these figures only include new construction in the ICI sector, no additions to existing buildings or major renovations and retrofits are included, nor is any multi-residential potential. Add to this any interior and exterior finishing materials in wood and the amount would be greater still.16 Any attempt at quantifying lumber volumes implicated in these numbers would not be accurate. Suffice it to say that there is an untapped potential for wood use in the non-residential construction sector in New Brunswick. There are certain products necessary for the construction of larger scale buildings which are not currently manufactured in the province, as was noted earlier.

________________________________________________________________________________________________________ 16 Buildings constructed with a structural wood system can be expected to use more interior and exterior wood finishes.

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

9

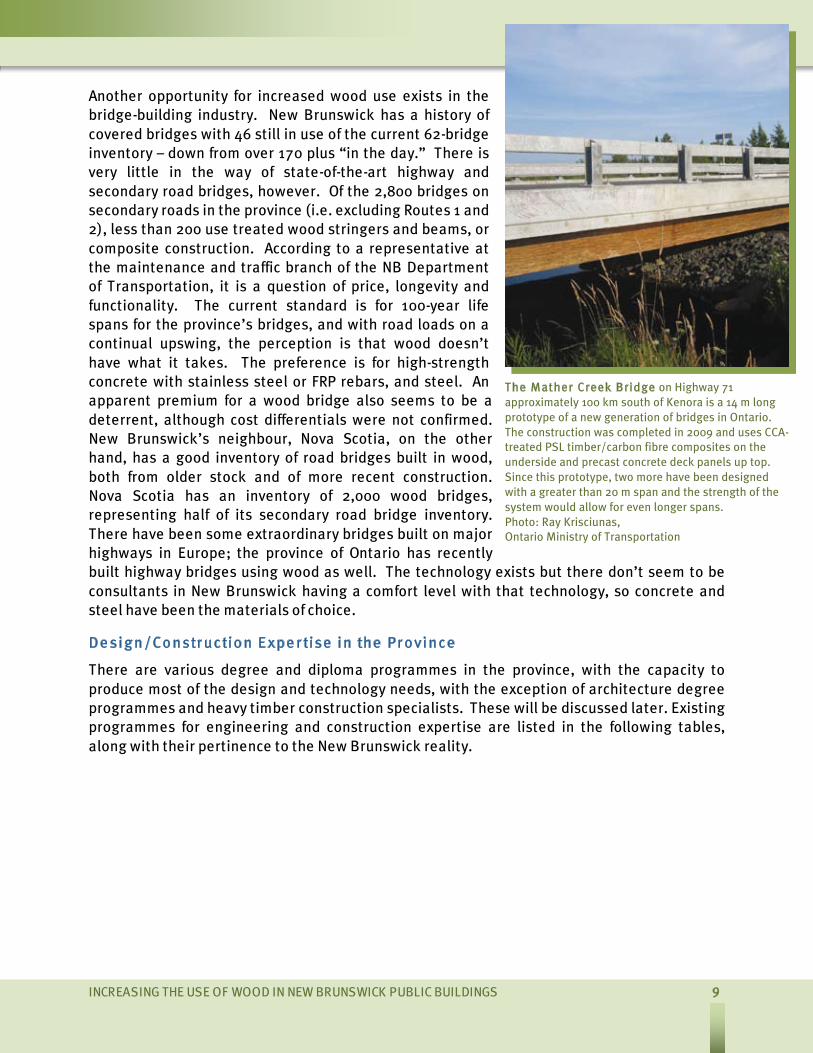

Another opportunity for increased wood use exists in the bridge-building industry. New Brunswick has a history of covered bridges with 46 still in use of the current 62-bridge inventory – down from over 170 plus “in the day.” There is very little in the way of state-of-the-art highway and secondary road bridges, however. Of the 2,800 bridges on secondary roads in the province (i.e. excluding Routes 1 and 2), less than 200 use treated wood stringers and beams, or composite construction. According to a representative at the maintenance and traffic branch of the NB Department of Transportation, it is a question of price, longevity and functionality. The current standard is for 100-year life spans for the province’s bridges, and with road loads on a continual upswing, the perception is that wood doesn’t have what it takes. The preference is for high-strength concrete with stainless steel or FRP rebars, and steel. An apparent premium for a wood bridge also seems to be a deterrent, although cost differentials were not confirmed. New Brunswick’s neighbour, Nova Scotia, on the other hand, has a good inventory of road bridges built in wood, both from older stock and of more recent construction. Nova Scotia has an inventory of 2,000 wood bridges, representing half of its secondary road bridge inventory. There have been some extraordinary bridges built on major highways in Europe; the province of Ontario has recently built highway bridges using wood as well. The technology exists but there don’t seem to be consultants in New Brunswick having a comfort level with that technology, so concrete and steel have been the materials of choice.

De si g n /Co n str uc ti o n E xpe r ti se i n the Pr o vi n c e

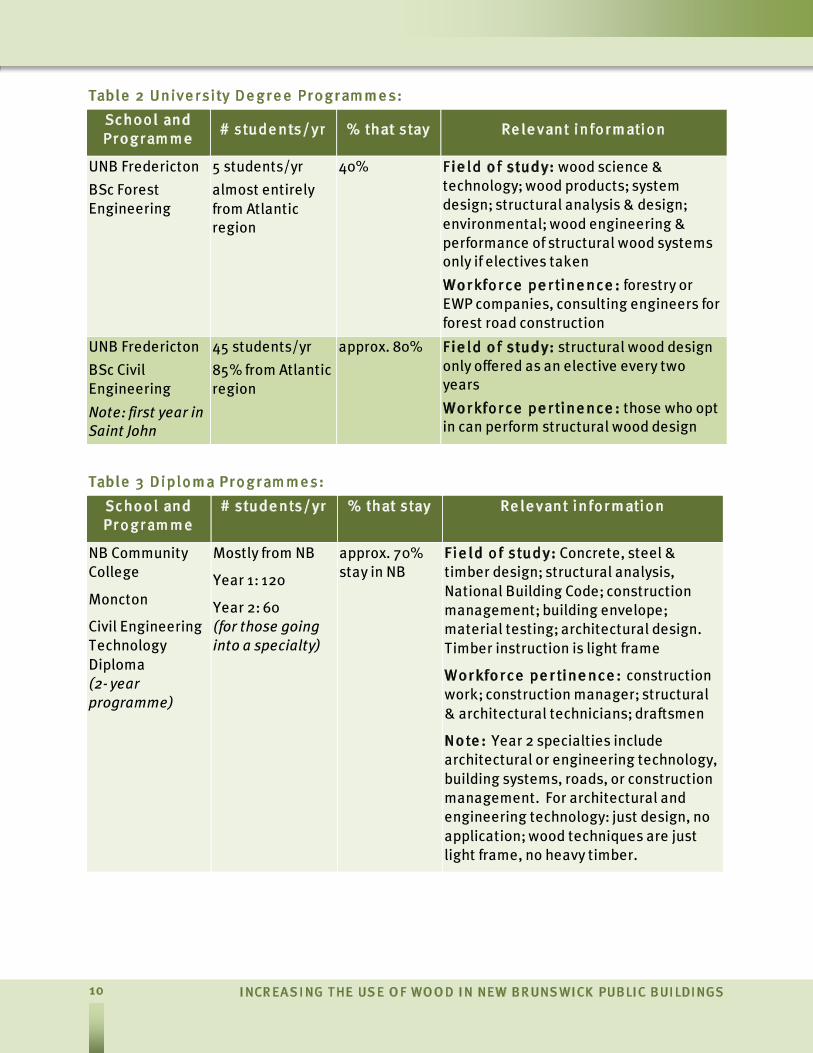

There are various degree and diploma programmes in the province, with the capacity to produce most of the design and technology needs, with the exception of architecture degree programmes and heavy timber construction specialists. These will be discussed later. Existing programmes for engineering and construction expertise are listed in the following tables, along with their pertinence to the New Brunswick reality.

The Mather Creek Bridge on Highway 71 approximately 100 km south of Kenora is a 14 m long prototype of a new generation of bridges in Ontario. The construction was completed in 2009 and uses CCA-treated PSL timber/carbon fibre composites on the underside and precast concrete deck panels up top. Since this prototype, two more have been designed with a greater than 20 m span and the strength of the system would allow for even longer spans. Photo: Ray Krisciunas, Ontario Ministry of Transportation

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

10

Table 2 Un i ve r si ty De g r e e Pr o g r am m e s:

Sc ho o l an d Pr o g r am m e

# stude n ts/yr % that stay Re le van t i n fo r m ati o n

UNB Fredericton

BSc Forest Engineering

5 students/yr

almost entirely from Atlantic region

40% Fi e ld o f study: wood science & technology; wood products; system design; structural analysis & design; environmental; wood engineering & performance of structural wood systems only if electives taken

Wo r kfo r c e pe r ti n e n c e : forestry or EWP companies, consulting engineers for forest road construction

UNB Fredericton

BSc Civil Engineering

Note: first year in Saint John

45 students/yr

85% from Atlantic region

approx. 80%

F i e ld o f study: structural wood design only offered as an elective every two years

Wo r kfo r c e pe r ti n e n c e : those who opt in can perform structural wood design

Table 3 Di plo m a Pr o g r am m e s:

Sc ho o l an d Pr o g r am m e

# stude n ts/yr % that stay Re le van t i n fo r m ati o n

NB Community College

Moncton

Civil Engineering Technology Diploma (2- year programme)

Mostly from NB

Year 1: 120

Year 2: 60 (for those going into a specialty)

approx. 70% stay in NB

Fi e ld o f study: Concrete, steel & timber design; structural analysis, National Building Code; construction management; building envelope; material testing; architectural design. Timber instruction is light frame

Wo r kfo r c e pe r ti n e n c e : construction work; construction manager; structural & architectural technicians; draftsmen

No te : Year 2 specialties include architectural or engineering technology, building systems, roads, or construction management. For architectural and engineering technology: just design, no application; wood techniques are just light frame, no heavy timber.

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

11

Table 4 Tr ade Sc ho o l Ce r ti fi c ate s:

Sc ho o l an d Pr o g r am m e

# stude n ts/yr % that stay Re le van t i n fo r m ati o n

NB Community College system (several campuses)

Carpentry Certificate

77 students/yr

100% from the Atlantic region

Nearly all stay in the Atlantic region

F i e ld o f study: wood & wood products; building envelope; National Building Code; wood framing techniques; footings & foundations

Wo r kfo r c e pe r ti n e n c e : carpenters for building companies; contractors

Campbellton College

Woodworking Production Management Certificate (40 wks in two years) and Woodworking and Cabinetmaking Certificate (40 wks in one year)

Year 1: 24

Year 2: 15

Mostly from the Atlantic region; a few from Quebec

75% stay in the Atlantic region

25% go to QC

Fi e ld o f study: CAD; wood working techniques; CNC; production operation management; tooling; drafting fundamentals; cabinet making techniques

Wo r kfo r c e pe r ti n e n c e : wood product manufacturing personnel; supervisor or manager

Carpenter Training Centre of NB

Carpentry Training Certificate (40 wks)

100 students in three in-takes during the year – all from the Atlantic region

90% remain in the Atlantic region

F i e ld o f study: Form work; framing techniques; drafting and blueprint reading; operations of hand & power tools & equipment

Wo r kfo r c e pe r ti n e n c e : qualified carpenter for residential, commercial & industrial job sites

Bay Tech College

Carpentry Certificate (14 weeks)

18 students in three in-takes during the year – all from NB

100% stay in NB

Fi e ld o f study: Materials of construction; interior & exterior finishes; building codes & standards; blueprint reading; framing techniques; formwork; operation of tools & equipment

Wo r kfo r c e pe r ti n e n c e : carpenters for building companies, contractors & cabinet makers

There is no architecture programme in the province of New Brunswick but there is one at the Dalhousie University School of Architecture. The programme does not have required courses dealing specifically with wood design. There are courses to impart general knowledge on the following relevant topics:

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

12

building technology, for the fundamentals in building construction and materials, as well as mediating the relationship between interior and exterior environments;

building systems integration, to understand the effect of forces on building systems interaction with envelope systems; and to understand the relationship between buildings, their systems and the people who use them.

There are no specific courses for wood use in design, however there are two graduate level elective courses dealing with wood. They are:

From Timber to Lumber – The course syllabus reads more like a forestry class than a wood design class. It deals with the state of the Acadian forest, logging practices, wood lot management,17 primary and some secondary transformation. The course also includes an introduction to life cycle assessment, carbon sequestration and timber framing.

From Lumber to Structure – This course contains the “wood design” programme at the Dalhousie School of Architecture. It teaches how to design a residential-scale sawn-lumber home. Most of the reference books date from the 50’s, 70’s and 90’s. There are two documents dating from 2001 and one reference document dating back to 1897. There were no references to the National Building Code of Canada or to CSA O86, the Canadian standard for structural wood design, in the syllabus.

For all intents and purposes, even if students opt into the elective courses dealing with wood, they would not be prepared to enter the design market with an adequate knowledge of available materials or wood-frame construction and techniques.

The trades’ schools do not have any training for building with heavy timber although, if the demand were there, two of the schools surveyed would be interested in moving forward with such a specialty. One was private; the other was a community college.

There are a handful of large architectural firms in New Brunswick, located primarily in Moncton, Fredericton and Saint John. A number of smaller firms and single architect firms exist as well; they are located throughout the province but primarily in the same aforementioned city centres. There seems to be a predilection for joint offices in the Moncton area, where architects share common studio space to facilitate collaboration on larger projects, if need be. There are several architectural firms in New Brunswick interested in wood construction with the knowledge and desire to design non-residential wood structures but there have been difficulties in getting initial designs past the engineers who seem to have more of an interest, and facility, with steel and concrete designs. It is often the engineer on a project that will determine the eventual structural system used, according to those interviewed. The Architects’ Association of New Brunswick represents the province’s architects; a requirement for continuing education units is overseen by the Association.

A spokesperson for the association representing professional engineers in New Brunswick, The Consulting Engineers of New Brunswick, stated that all their structural engineering members have the capability of designing with wood. That expertise, however, may not lie with engineered heavy timber structures; most such buildings that have been built in the province in the recent past have used engineering services from provinces west of the Atlantic region. The local engineering expertise seems to lay more in the design and construction of

________________________________________________________________________________________________________ 17 There is more private forest land in Nova Scotia than in New Brunswick.

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

13

light-frame wood buildings, whether residential scale or larger scale, and steel or concrete buildings for the non-residential sector.

The Construction Association of New Brunswick is a federation of associations which represents the building community in the province. There are associations representing electrical, mechanical, roofing and masonry contractors, and a few general construction associations; one in Moncton, one in Fredericton and one in Saint John. As far as construction companies with expertise in erecting engineered heavy timbered structures, there aren’t many. Steel erectors have been used to build such wood structures in New Brunswick in the recent past. There is a design and build firm in the Miramichi region which designs and erects their own post and beam structures. There is also at least one expert in the Fredericton area who does some heavy timber erection. Expertise does exist with a few other individuals in the province who are not currently working in the sector.

Pr o vi n c i al Re g ulati o n s Affe c ti n g the Fo r e st Pr o duc ts In dustr y an d the B ui l t E n vi r o n m e n t

As previously stated, the 2005 National Building Code of Canada (NBCC) is the building code of record for the province of New Brunswick. The NBCC applies to buildings under provincial and federal jurisdictions, as well as to those under the various municipal and Local Service District jurisdictions. Wood structures (referred to as combustible construction in the NBCC) are allowed in all occupancy categories, not only in Residential Occupancies of four storeys and under (Group C). The 2005 NBCC permits wood structures in certain Assembly Occupancies (Group A, Divisions 1, 2 and 3), Care or Detention Occupancies (Group B, Division 2), Business and Personal Services Occupancies (Group D), Mercantile Occupancies (Group E), and Industrial Occupancies (Group F, Divisions 1, 2 and 3). As with the four-storey stipulation for residential applications, there are also stipulations for structural wood use in these other occupancies dealing with the maximum number of storeys permitted, the need for sprinklers, fire-resistance ratings of assemblies within the building, building area, occupant loads, etc. Wood elements (referred to as combustible elements in the NBCC) are also allowed in buildings with non-combustible structural systems.18 There is much opportunity for wood use in New Brunswick’s non-residential buildings.

There exist opportunities for the forest products industry in New Brunswick in the context of the 2007-2010 New Brunswick Climate Change Action Plan launched in June 2007. The Plan outlines the government’s vision for a sustainable future by setting a series of targets and policy actions. The Climate Change Plan defines targets for renewable energy, waste reduction (diversion and recycling) and energy efficiency, among others, in an effort to mitigate greenhouse gas emissions and reduce them to 1990 levels by 2012 (in conjunction with other federal programmes), and a further 10% reduction by 2020. Funding is available for environmentally-focused research with an eye to creating markets for environmentally preferable products; and for energy efficiency and pollution prevention efforts in the public and private sectors as well as for non-profit initiatives throughout the province. Some forest products companies have implemented actions to improve efficiency and reduce their greenhouse gas emissions, with a resultant increase in direct and indirect employment.

________________________________________________________________________________________________________ 18 Refer to section 3.1 of the 2005 NBCC

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

14

The provincial government intends to lead by example by adopting best environmental practices and sharing lessons learned with other levels of government and with the public. The government recently released a sustainable development policy, in line with energy reduction targets in the Climate Change Action Plan, which will be implemented in three phases. The Provincial Green Building Policy for New Construction and Major Renovations addresses energy performance requirements, the use of an integrated design process, as well as green building rating programme requirements (LEED® and Green Globes™). All new buildings and major renovations that are funded in whole or in part by the Government of New Brunswick will be affected by this policy.19

The province of New Brunswick is working toward a lower environmental footprint in general, and the wood products industry is in a position to be a significant player in helping them to

achieve that. Wood products are viewed as the most environmentally-responsible construction material, according to life cycle assessments, when considering environmental impacts such as acid rain, smog, global warming potential, ozone depletion, air and water pollution, fossil fuel depletion, water use, habitat alteration, health, and other impacts through life cycle stages.20 The use of structural wood systems leads to lowered environmental footprints for buildings.

In line with the desire for a lowered environmental footprint and with targets identified in the Climate Change Action Plan, there exists another opportunity for the government to further the cause: the recycling of construction and demolition (C&D) waste for certain products. Half of the waste generated that ends up in landfill sites is C&D waste, and a good part of that is wood. C&D waste is regulated through the New Brunswick Department of Environment and landfill sites in the province are mostly operated by solid waste commissions that have been established in accordance with provincial legislation. Tipping fees vary from site to site and are set by site owners – they are not regulated.21 C&D waste materials aren’t sorted for the most part except at the Westmorland-Albert Solid Waste facility. On their own initiative, Westmorland sorts all of their C&D waste; lumber pallets are ground and used as biomass to

fuel their two boilers which supply all the necessary heat for their wet and dry waste management. Although sorted, other than the pallets, the rest of the construction waste goes unutilized.

Without the incentive or requirement to recycle, very little wood from C&D waste is recycled, regardless of the recyclability of the materials. In areas across Canada where increased

________________________________________________________________________________________________________ 19 The square footage of the building will determine the level of compliance that will be required. 20 Life cycle stages include resource extraction, manufacturing, construction, occupancy and maintenance, demolition, recycling/reuse and demolition. 21 There are no provincial waste disposal sites.

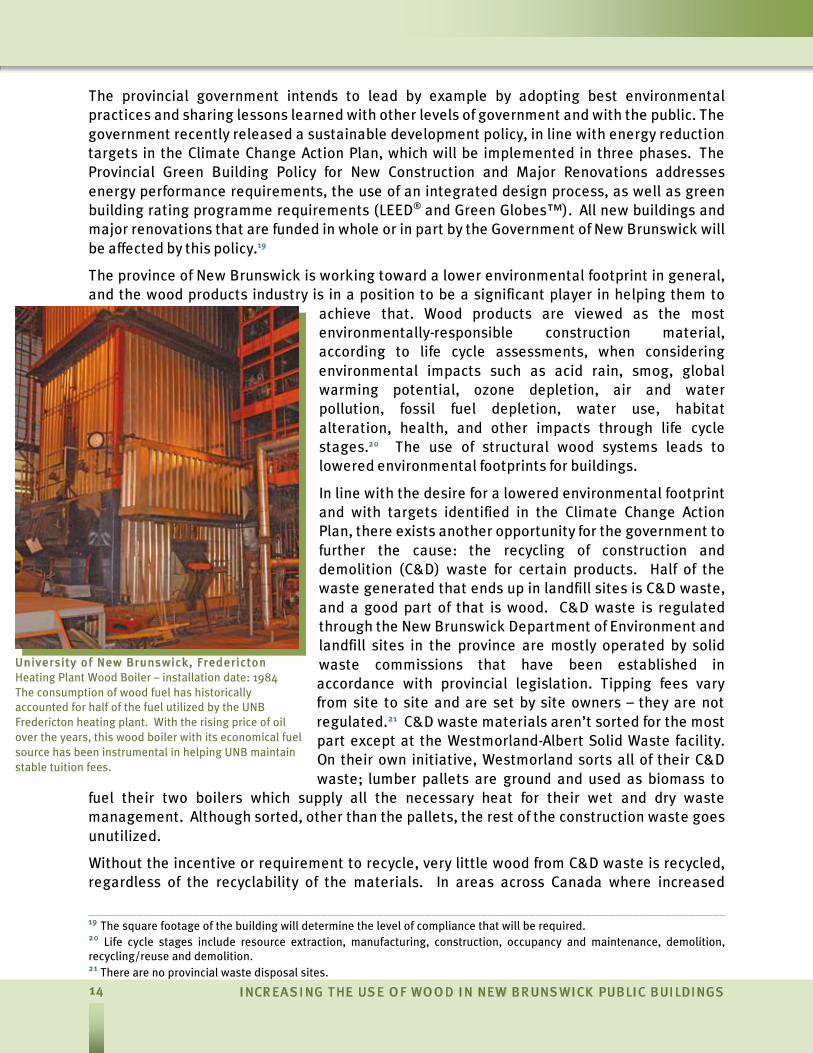

University of New Brunswick, Fredericton Heating Plant Wood Boiler – installation date: 1984 The consumption of wood fuel has historically accounted for half of the fuel utilized by the UNB Fredericton heating plant. With the rising price of oil over the years, this wood boiler with its economical fuel source has been instrumental in helping UNB maintain stable tuition fees.

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

15

tipping fees have been implemented for recyclable C&D waste, industries were developed to use construction waste and take-back programs were implemented by manufacturers. The technology exists to “clean” wood and render it suitable for further processing; there is the possibility of sourcing wood waste for biomass. New Brunswick’s budding wood pellet industry could potentially benefit from such sources. New Brunswick already has a history of wood use for energy generation. Wood is the second most important energy provider in the province after petroleum, at 16% of the energy generation.22 This is in large part a result of government initiatives in the 1970’s which resulted in a significant number of government buildings using wood for their primary energy needs (e.g. schools, hospitals). There exists a clearly untapped potential in C&D waste in the province.

Although the wood products industry touts the recyclability of wood as an important attribute, the incentive for actually putting that into practice is lacking. Consideration should be given to the Canada-Wide Action Plan for Extended Producer Responsibility, as put forth by the Canadian Council of Ministers of the Environment in October 2009.23 Policies implemented in line with the Plan would provide incentives to producers for taking responsibility of the end-of-life management of their products.

Cur r e n t B ar r i e r s to the Use o f Wo o d i n No n -Re si de n ti al Appl i c ati o n s

There are no regulations in New Brunswick specifically dealing with a restriction on the use of wood in non-residential buildings, except of course as regards the building code of record. The 2005 NBCC limits wood frame construction to four storeys high. The majority of New Brunswick’s non-residential buildings would fall under that height restriction yet wood is not the material of choice. There are several reasons for this, a major one dealing with perceptions.

There is a perception that wood is not a “modern” material. Since Canada’s history with wood-frame construction is so long-standing, and the majority of the architectural and engineering programmes do not have required courses in wood, there is a lack of knowledge as regards the advances in the industry in the last 20 years and its applicability to modern structures. This leads to common misconceptions as regards the possibilities for wood and just how current it can be as a building material.

As the NBCC limits wood construction to four storeys, the perception is that wood is only applicable to residential applications, whether single family or multi-residential. Compound this misconception with another – that only Part 9 buildings can be built in wood – and the perception becomes: because non-residential buildings are not built according to Part 9, then they can’t be built in wood. In fact,

________________________________________________________________________________________________________ 22 Source: New Brunswick Department of Energy – statistics for the early 2000’s. 23 http://www.ccme.ca/assets/pdf/epr_cap.pdf

Cathedral of Christ the Light, Oakland, California – 2008. Architects: Skidmore, Owings & Merril l , San Francisco. Photo: César Rubio

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

16

many non-residential buildings that fall under Part 3 of the NBCC can be built using wood. The only buildings that absolutely cannot be built in wood are certain detention facilities and certain high-hazard industrial buildings. As has been shown in Ontario, even hospitals can include wood construction. Only specialized courses in wood construction would concentrate on this interpretation of the Code but such courses are only available as electives and no evidence was found of such information forming a part of the curriculum for those elective courses.

There are concerns regarding the harvesting of our forest resources. The perception exists that the forest industry is irresponsible as regards logging practices. That New Brunswick has a higher percentage of forest lands certified to third party sustainable forestry management schemes than most other provinces in Canada is a little-known fact. What is perceived is that the forest is being indiscriminately exploited without thought to biodiversity or reforestation.

There is a perception that building larger structures with wood is more expensive. It has been ascertained that there is an apparent lack in expertise for the design of engineered heavy timber structures in the province. There is definitely a lack of engineered wood manufacturing facilities within the provincial boundaries (glulams, LVL, parallel strand lumber) making it necessary to source these materials from outside the province. It may very well be that these circumstances have painted an unrealistic picture with regards to the cost of heavy timber structures. The reality is that heavy timber structures are comparable if not more economical than steel or concrete buildings, when considering construction costs, delay times, building operations and management, and life-time use of the buildings.

As regards the potential use of forest biomass for energy (co-gen facilities, pelletization), the perception is that not only will we harvest our resources indiscriminately for lumber products, we will endanger the future generations of forest by depleting the soil of its nutrients when we remove slash from harvesting sites for biomass. Very important studies were undertaken at the University of New Brunswick in Fredericton on that very topic – results for which have garnered interest world-wide due to the scientific data which clearly demonstrates the needs of the forest for regeneration and the potential for biomass use. The responsibility that industry holds its forestry practices to is as yet an unknown phenomenon.

Another misconception which exists deals with the success of the concrete industry to position concrete as green. The perception is that aggregates and water are locally sourced and that it’s only the manufacturing process that creates greenhouse gases. There appears to be a lack of understanding as regards the levels of pollutants resulting from the concrete manufacturing processes and from life cycle impacts of building materials in general.

Thunder Bay Regional Health Services Centre, Thunder Bay, Ontario – 2004 Architects: Salter Farrow Pilon Architects Inc. Photo: Peter Sellar, KLIK Photography, courtesy of Farrow Partnership Architects Inc.

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

17

There are certain municipal inspectors that will refuse wood on a construction site for just cause – if the wood does not meet the standard requirements specified in the NBCC. This typically arises when a woodlot owner / builder uses his own wood on a building site without going through the standard grading and stamping procedures. There also exist some general concerns over moisture problems, fire resistance and durability when considering wood use. The lack of familiarity with the use of wood in larger-scale buildings has led to a lack of knowledge in detailing – detailing which is important in dealing with these potential problems in any structural system. As well, a lack of understanding in operation and maintenance of buildings can also lead to problems in a building, no matter what materials are used. The results of these knowledge gaps are problems which make the news (e.g. B.C. Leaky Condos) and give the perception of problems with the materials, which are in fact problems in detailing and competence.

These above-mentioned perceptions and misconceptions lead to misgivings about the products and a distrust of industry – huge challenges to overcome. Couple this with another major component in current disincentives to using wood, the green building movement, and we approach a perfect storm scenario. Although wood is the most environmentally sound building material choice, certain green building rating programmes paint another picture. The green building rating system which is making the most headway in North America is LEED, which stands for Leadership in Energy and Environmental Design. For reasons which are beyond the scope of this paper, the LEED rating system excludes all wood not sourced from FSC (Forest Stewardship Council) certified forests from their requirements for certified wood. This excludes nearly 100% of the wood harvested in New Brunswick; the certification scheme primarily used in New Brunswick is SFI (Sustainable Forestry Initiative). Other aspects of the LEED certification system result in other materials having access to more point value than does wood, giving the perception that wood isn’t as green as other materials. With LEED being implemented in various regulatory initiatives (including initiatives at the New Brunswick Department of Supplies and Services – DSS) this propagates a disincentive to using wood, when science tells us we should be going in the other direction. There are green building rating programmes with more comprehensive approaches, using life cycle assessment to determine the environmental footprint of buildings, and recognizing all three forest management schemes utilized in Canada (FSC, SFI, CSA). One such programme is Green Globes. NB DSS representatives have understood the merits of this programme and have recently modified their requirements for new public buildings to include Green Globes as an alternative rating scheme.

The New Brunswick construction industry could definitely benefit from having more engineered wood products (EWP) manufactured within its boundaries. The lack of glulam, laminated veneer lumber (LVL), oriented strand board (OSB) and other EWPs limits a design professional’s choices, which in and of itself is a barrier. The current economic downturn

Zénith Concert Hall , Limoges, France – 2006 Architects: Bernard Tschumi Architects Photo: © Christian Richters

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

18

makes it difficult for companies to consider investing in new technologies and bringing new production on-line when the markets are slow. So, in the interim, most non-residential buildings are built in steel and concrete.

There are several jurisdictions, here in Canada and abroad, that have battled the same perceptions and barriers noted above with varying degrees of success. In determining the best approach for New Brunswick, it was beneficial to study these other jurisdictions to evaluate their pertinence to the New Brunswick reality. In doing so, it will be possible to learn from the victories as well as the defeats in an effort to move forward with a new era for wood use in this province.

Efforts in O ther Juris dict ion s

B r i ti sh Co lum bi a

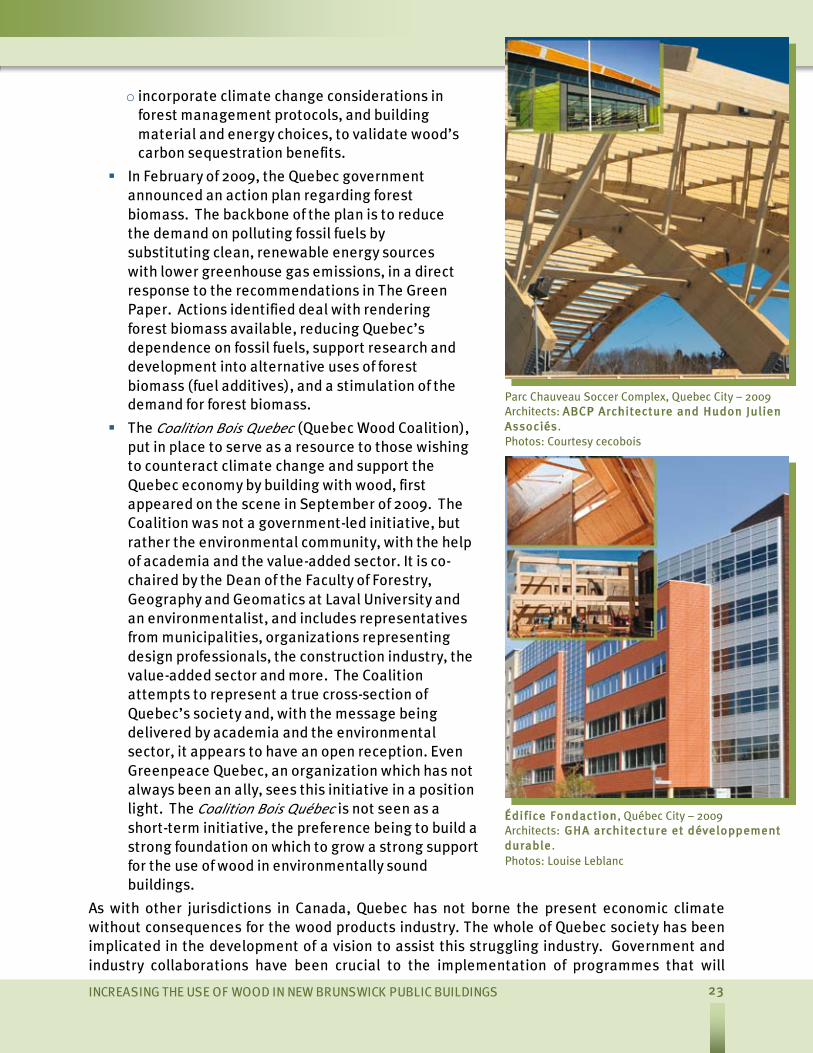

BC’s land mass is 947,800 km2; BC’s forest lands are 64% of that, or 60 million hectares – the forested area alone is larger than France, and more than eight times the size of New Brunswick. Crown lands account for 95% of the forested area. There were 54.3 million hectares certified to sustainable forestry management programmes as of January 2009 – representing more than 90% of the forest resource in BC. Although containing less than 20% of Canada’s forested land, BC produces 24% of Canada’s merchantable wood, manufacturing the lion’s share of Canada’s sawn lumber and plywood. Predominantly coniferous forests account for BC’s forested lands, which account for one-half of Canada’s softwood inventory. There are 84,000 direct jobs in the manufacturing sector alone. The wood products industry manufactures one-half of BC’s manufactured goods and one-half of BC’s exports. There is no doubt of the importance of the wood products industry in British Columbia – for British Columbians and for Canada.

Currently, less than 0.5% of BC’s forest is harvested yearly – less than is planted in the province over the same period. Only 2% of

BC’s forest lands have been lost over the province’s history (to urbanization, ranching and agriculture). Regardless of these facts, the forest industry has a history of being plagued with controversy over the logging of old growth forests (the coast forest, Clayoquot Sound, Vancouver Island). This long standing issue has been in the public eye for many years and on the government’s radar screen as well. Some government regulations for the responsible harvesting of the wood resource in BC that have been implemented over the years include:

1949 – Allowable Annual Cuts (ACCs) for public and some private lands;

mid-1989’s – three acts were put in place by the BC legislature to help the Ministry of Forests oversee their responsibilities of forest management;

1996 – Forest Practices Code came into force, put in place to ensure sustainable development of BC’s forest resources;

January 2004 – The Forest and Range Practices Act and supporting regulations were put in place to govern the practices of forest and range licensees.

Richmond Olympic Oval, Richmond, British Columbia – 2008. The largest structure to be built for the Vancouver 2010 Olympic Winter Games Design Team: CannonDesign Photo: Stephanie Tracey, Photography West

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

19

BC’s wood products industry can be said to have a unified vision, especially in light of having to stick together through adversity (harvesting issues, US lumber tariffs, the pine beetle infestation, the recent economic crisis). With the size of the industry, a common vision, and the importance of the industry for British Columbia, there has been a good working relationship established between industry and government. This has led to various initiatives in the province over the past decade, the combination of which has succeeded in raising the profile for wood construction and paved the way for the decision to enact Bill 9 – the Wood First Act, in October of 2009. Here are some of the important contributing initiatives:

development of Forest Innovation Investment (FII), set up by the BC government in 2003, to help support the BC forest economy in an environmentally sustainable and prosperous fashion. Included in its mandate: o position BC as global supplier of environmentally responsible wood products;

o assure demand for BC forest products in Canada and in world markets;

o combat market barriers; o help maintain the BC forest product industry’s contribution to the province’s

economy.

WoodWORKS! BC – an initiative of the Canadian Wood Council, in place in BC since 2000, has succeeded in raising the profile of wood construction in the province by providing education, training and technical expertise to the design community, municipal planning and building departments, etc., for the non-residential construction sector. A few WWs initiatives include:

o the creation of wood champions to help spread the word and develop buy-in; o 2010 initiative for the Olympics, to insure wood construction and products figured

prominently in Olympic venues (five-year initiative); o wood design competitions and wood design awards;

o technical assistance at all levels (construction, codes and standards, etc.);

o WWs is recognized by the province as a resource to help communities moving forward with the new Wood First Act requirements as well as local wood first resolutions and by-laws.

The Wood First Initiative, established by BC’s Ministry of Forests and Range to promote the choice of BC wood products in construction, had as a key component to prepare the groundwork for implementing the Wood First Act. As part of this initiative, a vision was developed and presented in February 2009, a vision in support of the development of the value-added industry in BC. Key elements for implementation of this vision will exist in the development of: o the Wood Enterprise Centre, to champion implementation of the Wood First policy,

for technology transfer, market expansion and training; o the Value for Wood Secretariat, to facilitate access to government, encourage

investment in the sector and spur strategic alliances.

Amendments to the BC Building Code, based on the National Building Code of Canada, 6 April 2009, to allow for six-storey wood-frame construction for residential buildings (an initiative spurred on by efforts to increase low-rise solutions in the Pacific Rim).

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

20

As can be seen from the long-standing initiatives in British Columbia, setting the stage for the development of a wood culture in British Columbia has been a long-term, many facetted process with much support from industry and government. Couple this phenomenon with a Premier who believes in the wood products industry and the timing was ripe for the development of a policy regarding the use of wood in public buildings. Stakeholder consultations focused on wood industry sectors were held before deciding on an approach. On October 9 of 2009, the BC legislature enacted Bill 9 – the Wood First Act. Its stated purpose: to “facilitate a culture of wood by requiring the use of wood as the primary building material in all new provincially funded buildings” to be consistent with the BC building code and in support of forest dependent communities.

No one can argue about the front and center visibility that wood products and wood construction received at the Olympics, for which the BC forest products industry is sure to reap benefits (and so will Canada). However, the backlash from competing industries in the province following the enactment of the Wood First Act, especially from the concrete industry, was immediate. In hindsight, the stakeholder process prior to moving forward with this initiative may have benefitted from having a more open, multi-industry approach. A certain amount of energy moving forward will be concentrated on responding to concerns expressed from a number of fronts. This may have been inevitable, regardless.

Since the implementation of Bill 9, very positive fallout has been the adoption by responsible parties in various municipalities of the Wood First Act tenets for their jurisdictions – seven municipalities at last count. These initiatives could prove to be as significant in helping to move BC’s wood culture forward in the long run as the Act itself. The current government has shown its commitment to the wood products industry and is committed to continuing its support through any subsequent mandates.

Que be c

Quebec is Canada’s largest province at 1.67 million km2. Of that area, 761,000 km2 is densely forested – 46% of the province, the size of Norway and Sweden combined. This represents 20% of Canada’s forest lands. Commercial forests account for 55% of the forested area in Quebec, or 418,550 km2 – that’s nearly 42 million hectares, about six times the size of the province of New Brunswick. Publically owned Crown lands account for 92% of Quebec’s forests; the remainder are privately owned.

The forest in Quebec has three distinct forest types in latitudinal lines from north to south, the boreal forest to the north is dominated by black spruce; 35% of this sector is set aside for commercial forestry but only about 20% is accessible and suitable. The mixed forest is a transitional zone between the boreal and deciduous forests. The latter, composed primarily of hardwoods, is in the south. Less than 1% of Quebec’s managed forest is harvested yearly. There are 120,000 direct jobs in the forest products industry in this province, a number which excludes indirect employment. More than 250 communities are considered forestry dependent. The forest products industry is the most significant contributor to the manufacturing sector in Quebec.

Quebec’s geography is special in that it is surrounded by water on three sides, in addition to which it is intersected by the Saint Lawrence Seaway – a main thoroughfare and shipping lane linking the Atlantic with the Great Lakes. Nearly 90% of Quebec’s population lives along the Seaway in the southern deciduous forest region.

INCREASING THE USE OF WOOD IN NEW BRUNSWICK PUBLIC BUILDINGS

21

Throughout the history of Quebec’s forest industry, one would be hard put to find an event which has polarized the Quebec people more than has the documentary released in 1999 by Richard Desjardins and Robert Monderie: l’Erreur boréale (Forest Alert). The film exposes, rightly or wrongly, an impression of the forest harvesting practices in northern Quebec that has been nearly impossible to shake and which has left an indelible mark on the attitude of Quebecers as regards the use of wood in construction – a 200 year-old tradition in Quebec.

Notwithstanding the indisputable scientific evidence of the environmental responsibility of wood products and their use, the belief in the general population of Quebec can be paraphrased thusly: we shouldn’t be cutting trees … period. This attitude combined with the long-standing US lumber tariffs, waves of insect infestation, reductions in logging quotas and a fragile economy have created a harsh climate for the Quebec wood products industry. In the face of such adversity, industry has nonetheless succeeded in developing a much sought after value-added sector. Forest products account for one-third of Quebec’s exports.

Some history worthy of note leading up to the current climate of change in Quebec as regards the use of wood and a new vision for a beleaguered industry is noted below.

The Forest Act, 1986, established methods and requirements for management of the forest resources. The latest revision was in 2007, with other changes announced in “The Green Paper.”

In 2000, chemical pesticide use for the eradication of insects and disease was discontinued, in line with the Forest Protection Strategy (1994).

In 2003, the government of Quebec placed a northern limit on timber allocations in the boreal forest.

In 2004, the Coulombe report identified errors made in calculations for allowable forest cuts, setting the stage for considerable decreases in available commercial forest resources (Bill 71 – 2005; 25% reduction implemented in 2008), the appointment of a chief forester (Bill 94 – 2005) and a different approach to forest management (Bill 49 – 2006).

The WoodWorks! programme (CWC programme) was officially implemented in the province in 2004, following a pilot project in 1998. An action plan was developed by industry to increase the use of wood in non-residential construction. Funding was procured from industry and from provincial and federal governments. In 2007, the programme oversight transferred to a Quebec entity and was renamed cecobois. Programme representatives provide services to design professionals to help with interpretation of the Building Code, designing with wood in non-residential applications, product availability, understanding the environmental responsibility of wood as a building material and the impacts to the life cycle implications for buildings that use wood.

In October 2006, the Quebec Government announced the Forest Sector Support Plan, a $720 million package to assist the forest sector. The Plan was put in place to provide assistance with job losses in the sector, for communities affected by mill closures, for new approaches to forest management, and in support of business investments and restructuring efforts.

In 2007, a multi-stakeholder summit was organized by Laval University to discuss the future of the Quebec forest sector. There were representatives from industry,

I NCR EA S I NG THE US E O F WO O D I N NEW BR UNS WI CK PUBLI C BUI LDI NGS

22