Embed Size (px)

Citation preview

Income SolutionsOctober 2, 2012

For plan sponsor and consultant use only. Not for use with the public.

Today’s presenters

Abigail PancoastVP & Chief CounselRetirement Plan ServicesLincoln Financial [email protected]

James Veneruso, CFAVice PresidentFund Sponsor ConsultingCallan Associates [email protected]

2

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: Driving Forces

The Big Macro

•Ten years of trauma:– Last decade saw the two largest bear markets since the depression – Recent recession was the longest and deepest since the 1930s– Increased correlations– Increased volatility, 2011 saw 61 days (nearly 1 in 4 trading days) where the

S&P 500 moved by more than 2%

•Ten years of trauma:– Property markets lack of stability……– Oil prices rise….– Europe completely implodes……– US indebtedness and continued political paralysis/psychosis

3

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: Driving Forces

• Micro factors– Longevity risk– Inflation risk– Drawdown rates– “Cognitive risk”– Sequence of return risk

4

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: Is Volatility Here to Stay?

5

99 00 01 02 03 04 05 06 07 08 09 10 11 120.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

for 13 Years Ended June 30, 2012for a $1 Mandate

Growth of a Dollar

Gro

wth

of

a D

o lla

r

1.7 - CAI Tgt Dt Idx 2025

1.3 - S&P:500

2.2 - Barclays Aggregate Index

For plan sponsor and consultant use only. Not for use with the public.

Product Offerings

• Traditional Annuities

Provide a guaranteed income stream. They can be tailored to fit various needs such as inflation-adjusted (COLA) or survivorship. They can be inflexible and costly.

• Longevity Insurance

Provides a safety net against longevity risk, but only receive a benefit if the insured lives beyond certain age. This provides a hedge against “cognitive risk” and longevity risk.

6

For plan sponsor and consultant use only. Not for use with the public.

Product Offerings

• Managed Payout

A type of distribution system that provides no guarantee. Rather, based un the underlying investment options provides orderly regular payments. Participants retain control of their assets.

•Guaranteed Minimum Withdrawal Benefits

More complicated, costs vary

7

For plan sponsor and consultant use only. Not for use with the public.

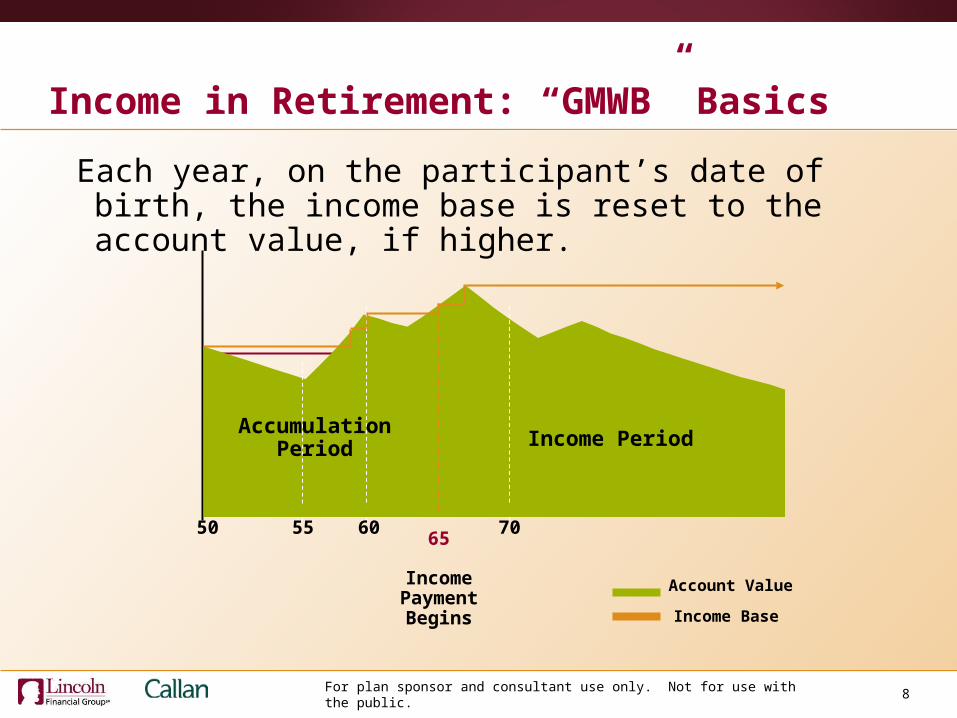

Income in Retirement: “GMWB” Basics

8

65

Income Payment Begins

Account Value

Income Base

50 55 60 70

Accumulation Period Income Period

Each year, on the participant’s date of birth, the income base is reset to the account value, if higher.

For plan sponsor and consultant use only. Not for use with the public.

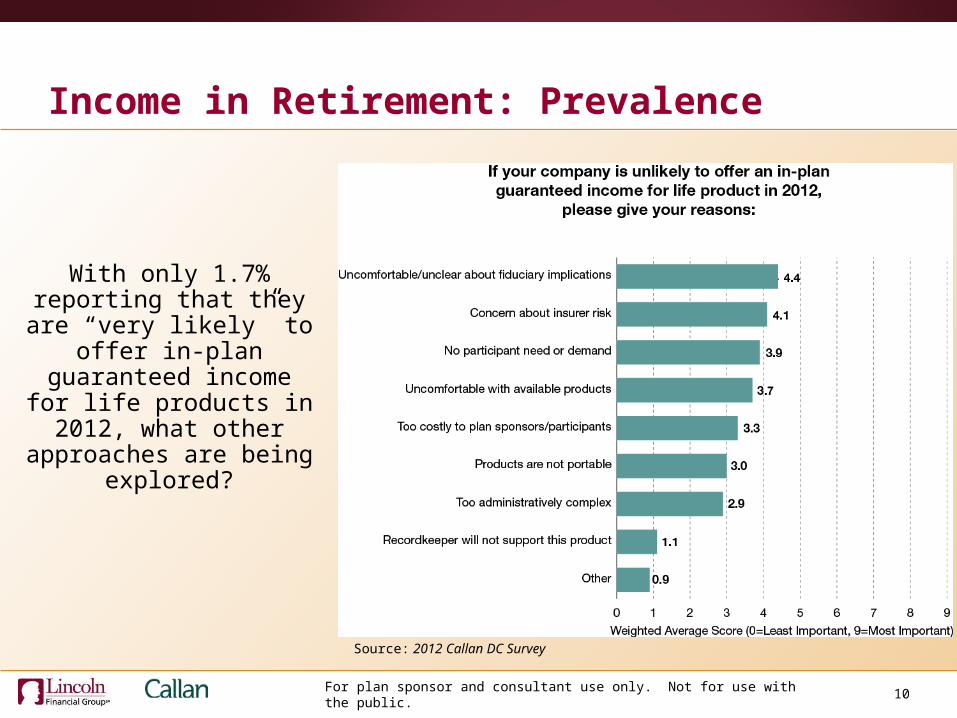

Income in Retirement: Prevalence

9

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: Prevalence

With only 1.7% reporting that they are “very likely” to

offer in-plan guaranteed income for life products in

2012, what other approaches are being

explored?

Source: 2012 Callan DC Survey

10

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: Why the Lack of Interest?

Many considerations with offering any of the in-plan annuities that are currently available.• Insurer risk, counterparty risk• Cost• Portability• Recordkeeper support• Participant interest/difficulty communicating• Comfort with being early adopter/trend setter• Legal considerations

11

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: Legal Considerations

The bad news• Current safe harbor for fiduciaries selecting annuity providers is too

vague• No guidance on how to educate participants without providing

investment advice• Burdensome annuity notice and consent rules• RMD rules inhibit use of longevity insurance

12

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: Legal Considerations

The good news

• DOL would like to make the annuity selection safe harbor easier

• DOL considering expanding investment education guidance to include retirement income education

• IRS guidance has clarified notice and consent rules for in-plan annuities; expect similar guidance for GMWBs

• Service providers can assist with notice and consent administration

• IRS has issued proposed rules to facilitate longevity insurance

• DOL and Congress considering addition of retirement income illustrations to participant benefit statements

____________________________________________________Bottom line--Congress and regulators are very interested

in making it easier.

13

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: One Plan Sponsor’s Experience

A plan sponsor is set to unroll an income guarantee as part of their custom target date strategy. Unique features include:

•Multiple insurers (counter party risk, fiduciary selection risk)

•Guaranteed insurance charge (cost)

•Insurers compete on how much of the pie they guarantee, through the guarantee rate they offer (cost, fiduciary selection risk)

•As with the custom target date fund, the guarantee piece is plug-and-play through a third party (i.e., not recordkeeper) who also provides a call center and communication program (portability)

But issues still remain, the biggest being the lack of a workable safe harbor provision.

14

For plan sponsor and consultant use only. Not for use with the public.

Income in Retirement: Next Generation of Offerings

The next generation of offerings seek to address the aforementioned concerns. Some ideas currently in the offing include:

• Managed account products with a guaranteed/managed payout scheme (Financial Engines)

• Laddered bond products which seek to match payouts to participants with income received from underlying fixed income products (PIMCO)

• Target date products with a guaranteed payout component introduced in the near retirement vintages (Alliance Bernstein and others)

•Longevity insurance bundled with other drawdown solutions

15