Embed Size (px)

Citation preview

INCENTIVIZED TAX POLICY AND ITS

IMPACT ON INVESTMENT IN PAKISTAN

Khalid Mahmood Lodhi

Registration No. 051-11-114477

A Thesis Submitted in

Partial Fulfillment of the

Requirements for the Degree of

Doctorate of Philosophy in Business

Administration

Department of Business Administration

Iqra University Islamabad Campus

2017

i

THESIS APPROVAL SHEET

It is certified that PhD Dissertation titled “Incentivized Tax Policy and its Impact on

Investment in Pakistan” has been prepared by Mr. Khalid Mahmood Lodhi, Enrollment No.

051-11-114477 and approved for submission.

Supervisor,

_______________________

Prof. Dr. S M Younus Jafri

Dated:

ii

ABSTRACT

The aim of this research is to study the incentivized tax policy and its impact on investments

in Pakistan. Study period is spanned over 25 years ranging from 1990 to 2014. For data

collection and analysis, the quantitative method is predominantly used. Specifically,

inferential statistics are used and for time series data analysis multiple regressions and ARDL

approach techniques are used. The researcher adopted a model comprising variables of

incentivized tax policy like corporate tax rates and custom tariffs to analyze its impact on

(FDI) and domestic investment in Pakistan in aggregate. Findings of the study reveal that

corporate tax rate is significantly negatively associated with domestic investment.

Furthermore, tax rates for companies have important but negative relationship with FDI. In

addition the study indicates that tariff rate has no statistically significant relationship with

foreign direct investment as well as with domestic investment. Findings lead to the way

forward for economic policy makers in Pakistan. Tax incentives need to be viewed as a

component of larger picture of Pakistan’s vision and policy for the economy which aims at

creating a fair and competitive economic environment. There is need to bear the short term

results arising out of tax incentives in shape of complicated systems, inequities and untapped

revenue. In market segments, tax policy needs to be implemented with a view to eradicate

inefficiencies. Incentives should be used to promote investments in business with focus on

research and development in industry. Decrease in corporate tax rate results in significant

increase domestic investment and FDI, so government should take steps to rationalize the tax

rates, so that economic activities may be accelerated and investment may grow for overall

economic growth. Moreover, unlike many other countries, non-tax factors like political

instability, security situation, less ease and cost of doing business, lack of business

competitiveness, difficult and complicated regulatory procedures and weak physical

infrastructure immensely and negatively affect growth of domestic and foreign investment in

iii

Pakistan. The government policies should also focus on addressing and improving the

situation regarding these non-tax factors, along with providing tax incentives to promote

investment and boost economic development in the country.

Key words: Tax policy, Tax incentives, Foreign direct investment, Domestic investment,

Corporate tax rate, Tariff rate, Tax holiday, Tax exemption, Preferential treatment, Non-tax

factors, Economic development, Ease and Cost of doing business, Business Competitiveness

iv

DECLARATION FORM

I Khalid Mahmood Lodhi hereby declare that the thesis titled “Incentivized Tax Policy and

Its Impact on Investment in Pakistan” submitted by me in fulfillment of the requirements

for the degree of PhD (Management Sciences). This thesis represents research carried out at

Iqra University Islamabad Campus and aims at encouraging discussion and comment. The

observations and viewpoints expressed are the sole responsibility of the author. It does not

necessarily represent the position of Iqra University Islamabad Campus or its faculty. I also

understand that if evidence of plagiarism is found in my thesis at any stage, even after the

award of a degree, the work may be cancelled and the degree revoked.

Khalid Mahmood Lodhi

Registration # 051-11-114477

v

DEDICATION

I thankfully dedicate this piece of research to my parents, my wife and beloved children and

friends for always praying, supporting and motivating me in my endeavors.

vi

ACKNOWLEDGEMENT

In the name of Allah Almighty, the Most Gracious and the Merciful, the only Creator of the

Universe and the Source of all knowledge and wisdom, who opened the directions in my

mind and enabled me to think philosophically and bestowed upon me the guidance of my

learned teachers to accomplish this research with audacity, perseverance and success. I am

extremely grateful to my worthy and learned supervisor Dr. S.M. Younus Jafri, who provided

me consistent encouragement and guidance and contributed immensely in completion of this

thesis. I acknowledge that without his guidance and support, I would not have been able to

successfully bring out this research thesis. I am deeply indebted to Dr. Muhammad Islam who

provided me encouragement, inspiration and continued support in completing this

challenging task. I am also indebted to my family who provided me a conducive environment

and encouragement to conduct my research and complete my assignment. I should also

acknowledge the support and assistance of my friends, class fellows and colleagues who

provided me unceasing support, help, advice and aid of statistical tools during the process of

preparing this research thesis.

vii

TABLE OF CONTENTS

ABSTRACT ................................................................................................................................................................II

DEDICATION ............................................................................................................................................................ V

ACKNOWLEDGEMENT ....................................................................................................................................... VI

LIST OF TABLES .................................................................................................................................................... IX

LIST OF FIGURES .................................................................................................................................................... X

LIST OF ABBREVIATIONS .................................................................................................................................. XI

CHAPTER 1 ................................................................................................................................................................. 1

INTRODUCTION ....................................................................................................................................................... 1

1.1 Background of the Study .................................................................................................... 1

1.3 Problem Identification ....................................................................................................... 6

1.4 Statement of Problem........................................................................................................ 12

1.5 Research Questions .......................................................................................................... 13

1.6 Significance of Study ......................................................................................................... 13

1.7 Objectives of the Study ..................................................................................................... 17

1.8 Justification of the Study .................................................................................................. 17

1.9 Scope of Study ................................................................................................................... 21

1.10 Organization of the Study .............................................................................................. 22

CHAPTER 2 ............................................................................................................................................................... 23

NEXUS BETWEEN TAX POLICY AND INVESTMENT IN PAKISTAN ........................................................ 23

2.1 Tax Policy Theories ........................................................................................................... 23

2.2 Theoretical framework of Investment ............................................................................. 26

2.2.1 Domestic Investment ..................................................................................................... 26

2.2.2 Foreign Direct Investment ....................................................................................... 27

2.3 Theoretical foundations .................................................................................................... 29

2.4 Theories of FDI .................................................................................................................. 30

2.3 Investment Policy .............................................................................................................. 35

2.4 Fiscal Policy ....................................................................................................................... 38

2.4.1 Tax Policy ................................................................................................................ 38

2.4.2 Government Expenditures ....................................................................................... 42

2.5 Tax Policy and Investment Relationship ......................................................................... 42

2.6 Investment Profile of Pakistan and other countrieis ..................................................... 45

2.7 Competitiveness of Pakistan’s Economy ......................................................................... 56

2.8 Tax Reforms in Pakistan .................................................................................................. 58

2.9 Tax Policy Incentives for Investment .............................................................................. 62

CHAPTER 3 ............................................................................................................................................................... 82

LITERATURE REVIEW ......................................................................................................................................... 82

3.1 Tax Policy Incentives and Investment ............................................................................. 87

viii

3.2 Tax Incentives’ impact on FDI ......................................................................................... 99

3.3 Tax Incentives .................................................................................................................. 105

3.4 Tax and Tariff.................................................................................................................. 121

3.5 Non Tax Factors Affecting FDI...................................................................................... 130

3.6 Research Gap ................................................................................................................... 138

3.7 Theoretical Foundation .................................................................................................. 138

3.8 Hypothesis Statement ..................................................................................................... 139

CHAPTER 4 ............................................................................................................................................................. 140

RESEARCH METHODOLOGY AND MODEL ESTIMATION ....................................................................... 140

4.1 Data Description .............................................................................................................. 140

4.2 Research Design............................................................................................................... 140

4.3 Data Collection Methods ................................................................................................ 140

4.4 Methods of Data Analysis ............................................................................................... 141

4.5 Statistical Method ............................................................................................................ 141

4.6 Definitions of Variables ............................................................................................. 142

4.6.1 Domestic Investment ............................................................................................. 142

4.6.2 Foreign Direct Investment ................................................................................... 142

4.6.3 Corporate Tax Rates Concessions/Reductions .................................................... 142

4.6.4 Custom Duty Tariff Concessions/Reductions ...................................................... 142

4.6.5 Tax Holidays ......................................................................................................... 143

4.7 Model Estimation ............................................................................................................ 143

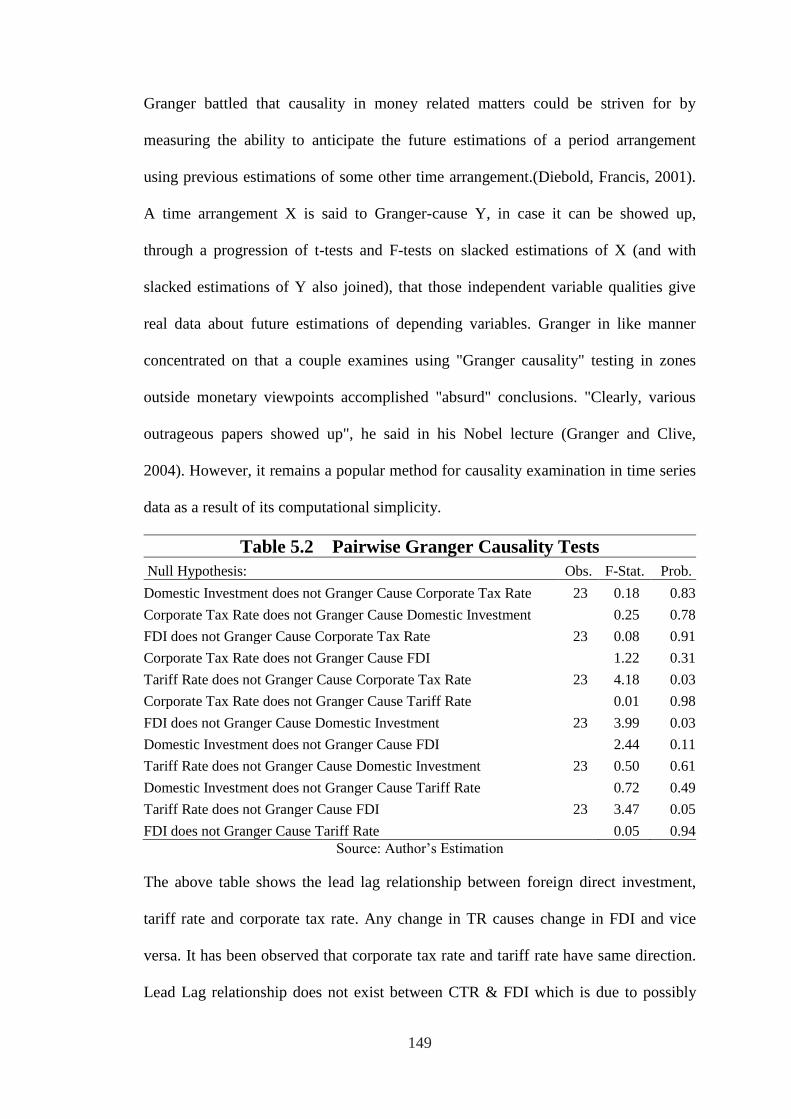

CHAPTER 5 ............................................................................................................................................................. 147

DATA ANALYSIS, EMPIRICAL RESULTS AND DISCUSSION .................................................................... 147

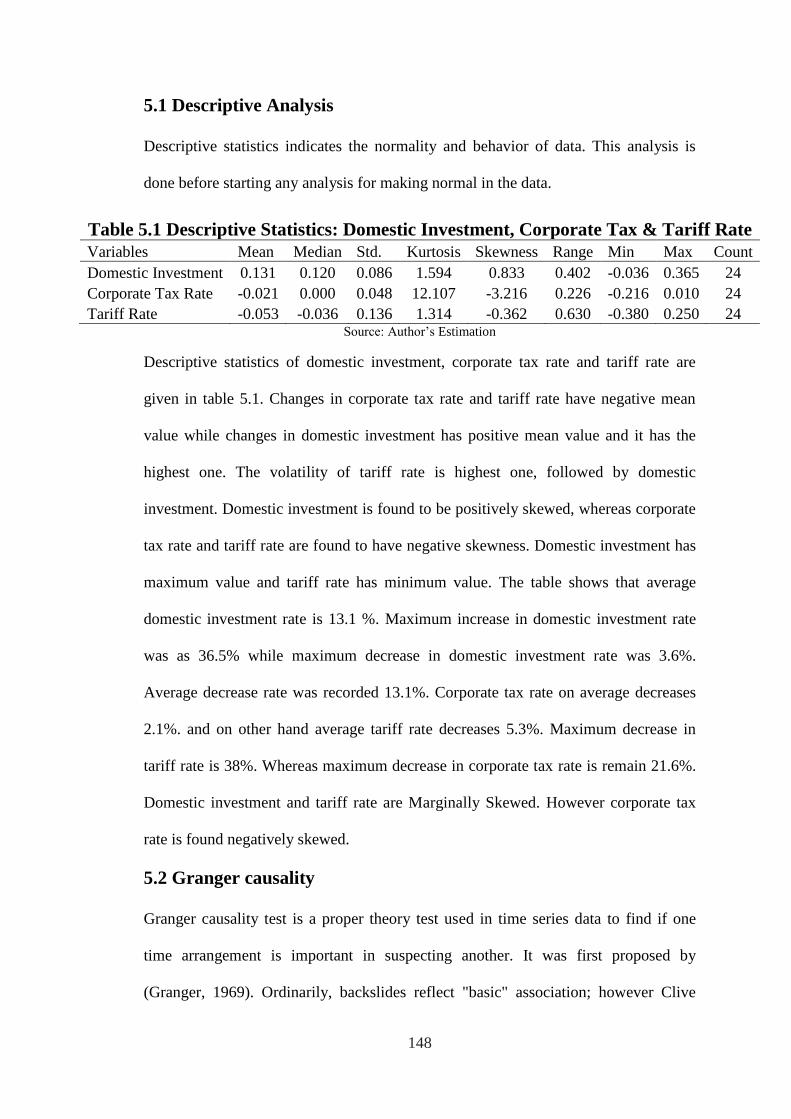

5.1 Descriptive Analysis ........................................................................................................ 148

5.2 Granger causality ............................................................................................................ 148

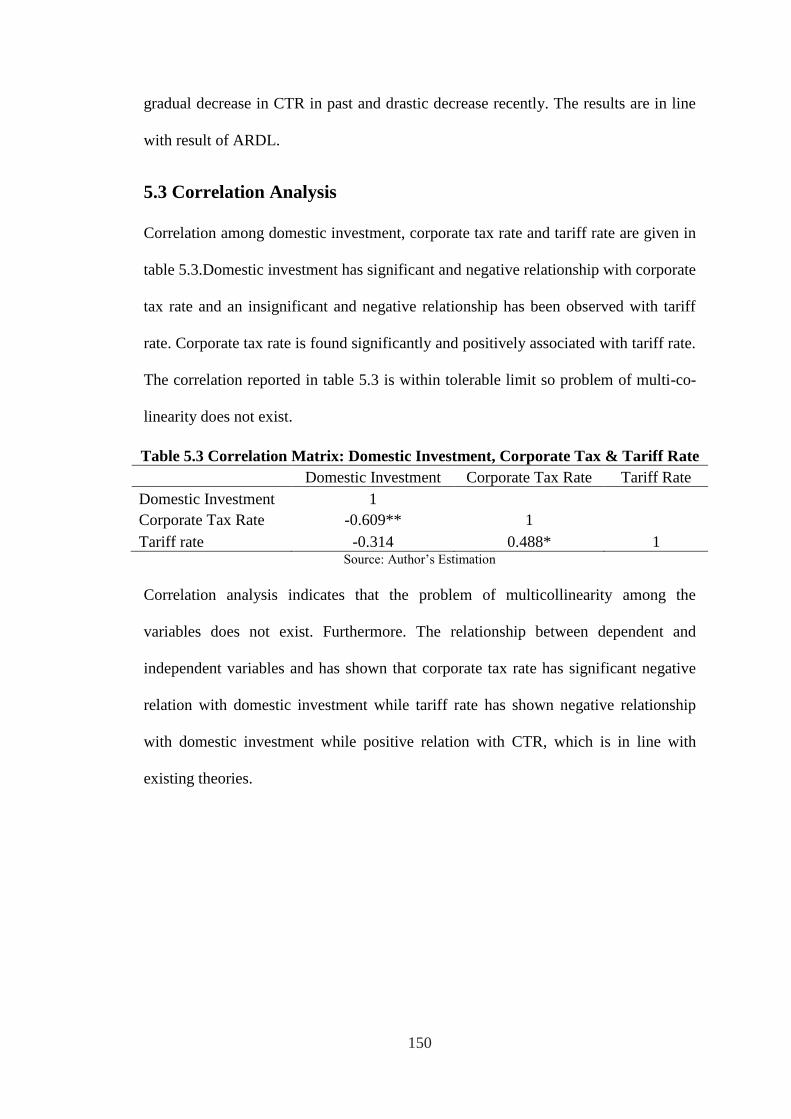

5.3 Correlation Analysis ....................................................................................................... 150

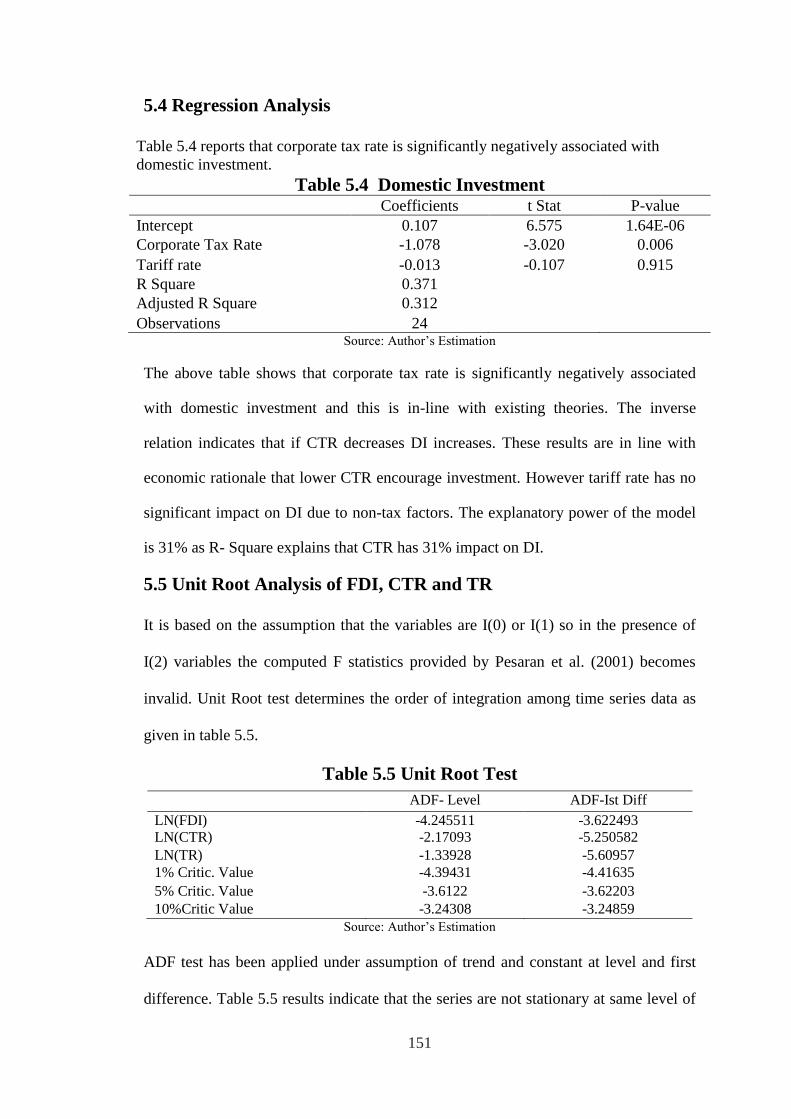

5.4 Regression Analysis ......................................................................................................... 151

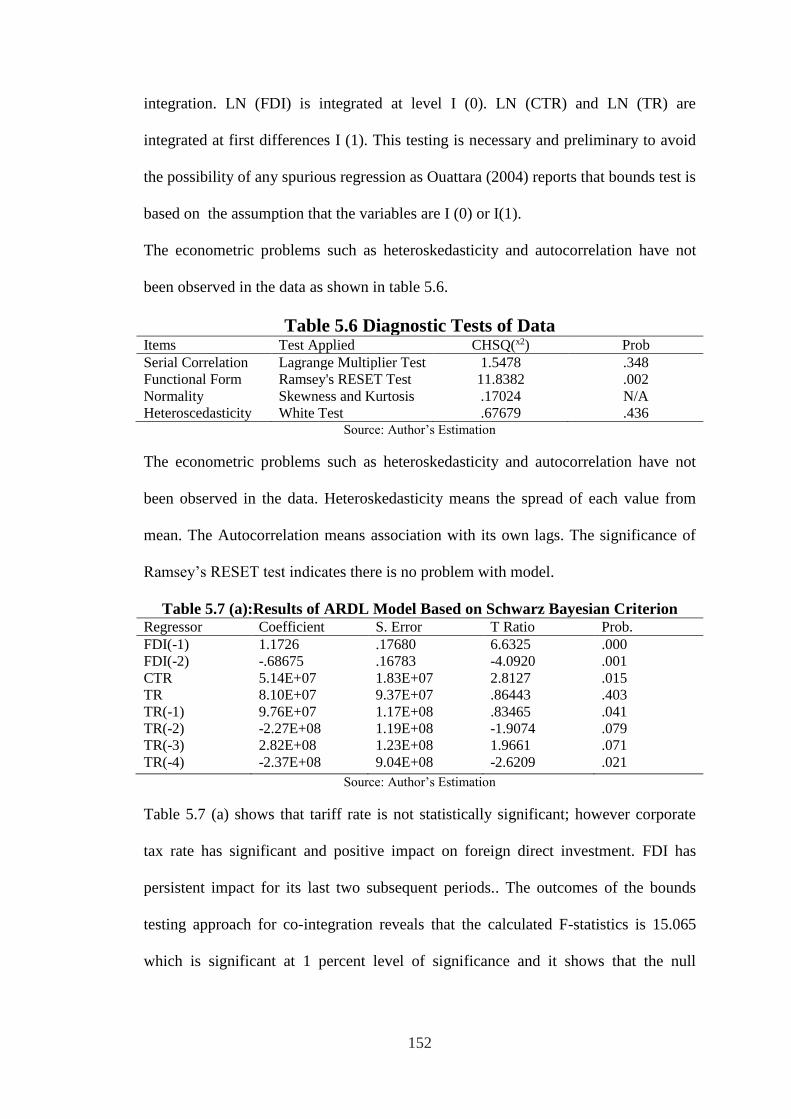

5.5 Unit Root Analysis of FDI, CTR and TR ...................................................................... 151

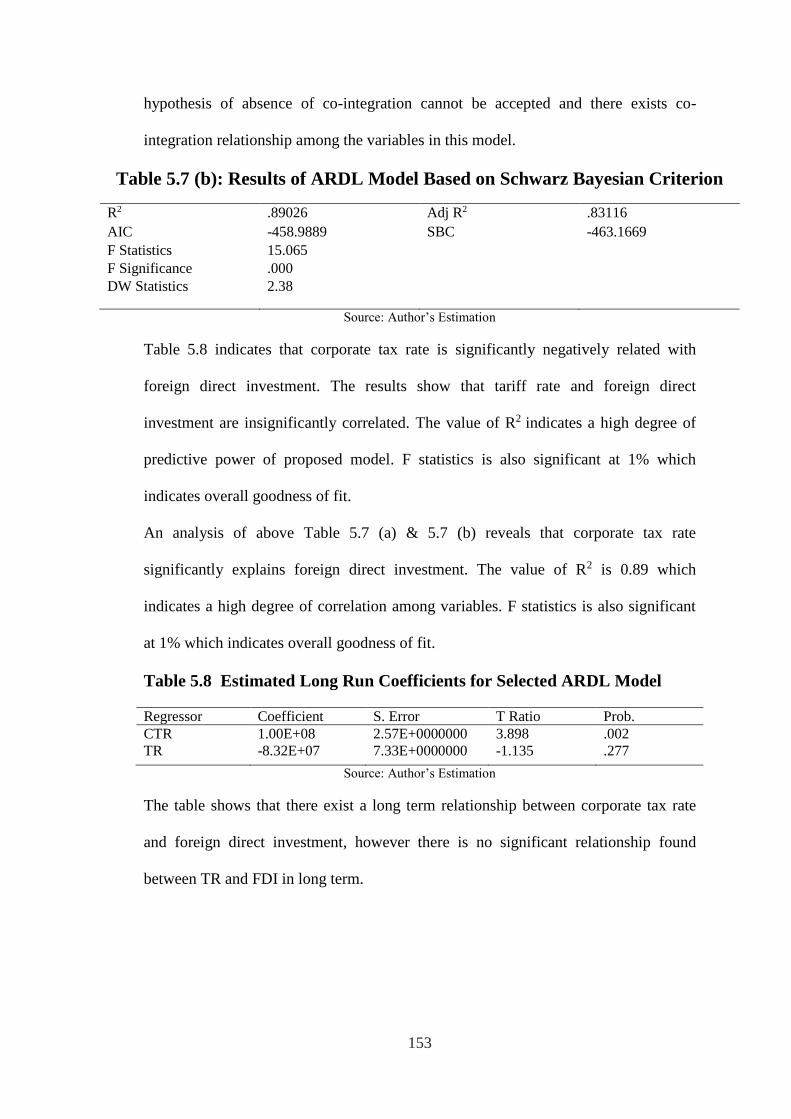

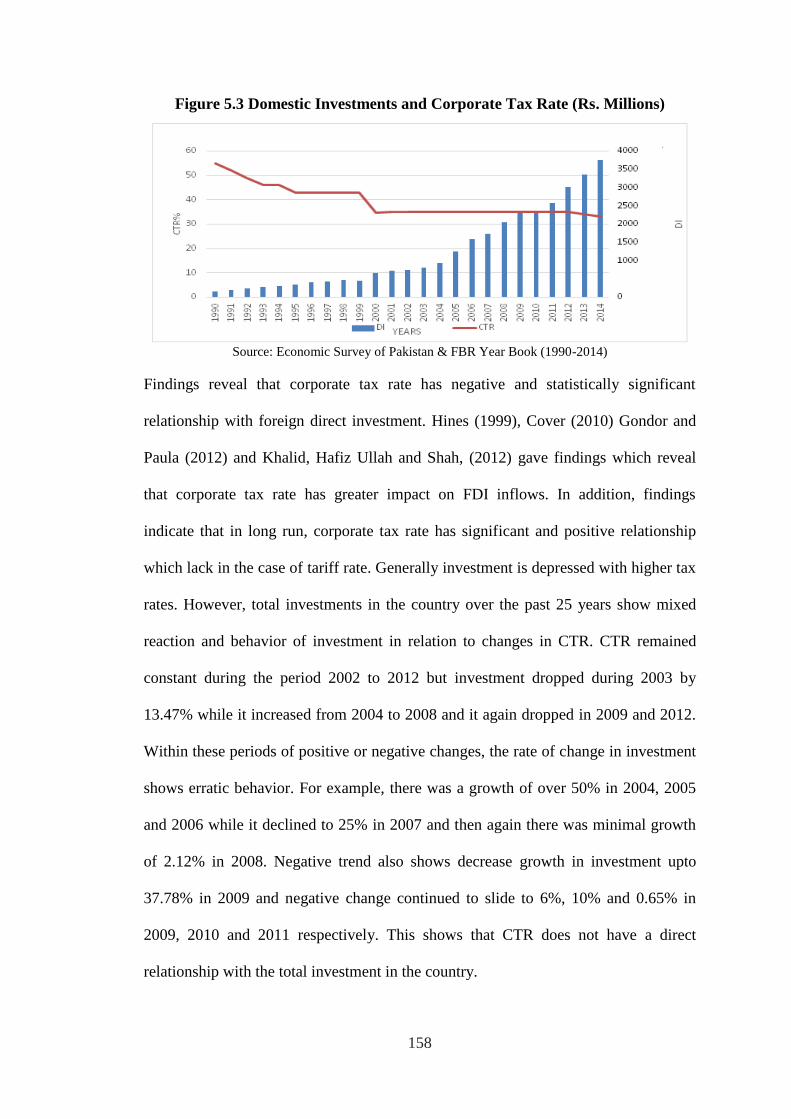

5.6 Discussion ......................................................................................................................... 155

CHAPTER 6 ............................................................................................................................................................. 164

CONCLUSION AND RECOMMENDATIONS ................................................................................................... 164

6.1 Conclusion ........................................................................................................................ 164

6.2 Recommendations ........................................................................................................... 170

6.3 Practical Implication ....................................................................................................... 175

6.4 Future Research Directions ............................................................................................ 176

6.4 Limitations of the Study ................................................................................................. 176

REFERENCES ........................................................................................................................................................ 178

ix

LIST OF TABLES

Table 2.1 Foreign Investment Inflows in Pakistan ($Millions) ....................................................47

Table 2.2 Country Wise FDI Inflows ($ Million) .........................................................................48

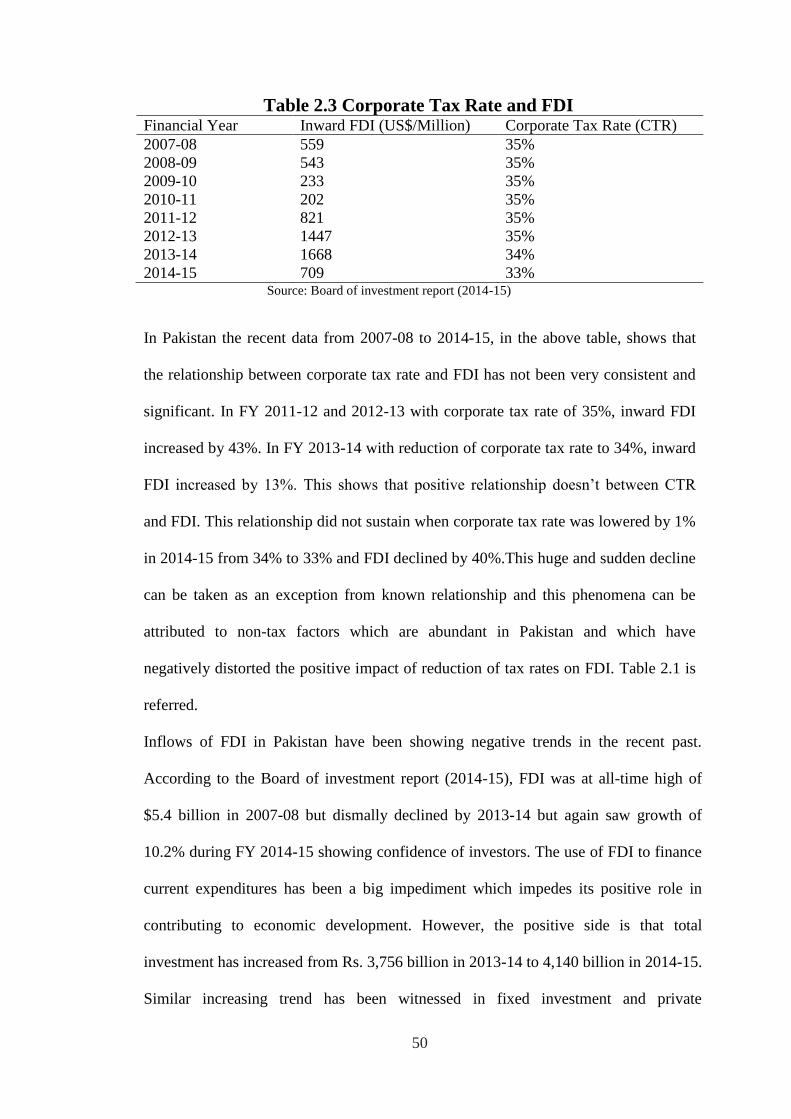

Table 2.3 Corporate Tax Rate and FDI ..........................................................................................50

Table 2.4 Structure of Savings and Investment (% of GDP) .........................................................54

Table 2.5 Growth Rate of GDP Over Per Capita Income ..............................................................56

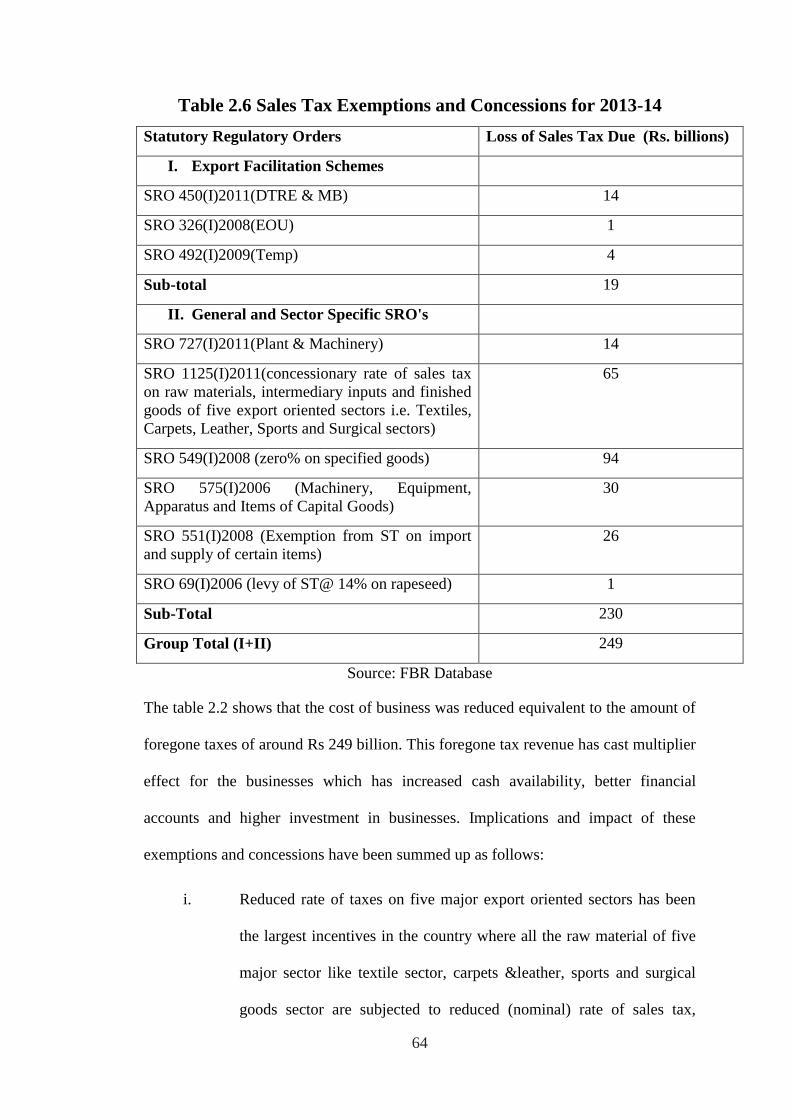

Table 2.6 Sales Tax Exemptions and Concessions for 2013-14 ....................................................64

Table 2.7 Corporate Tax Rates by Country ...................................................................................66

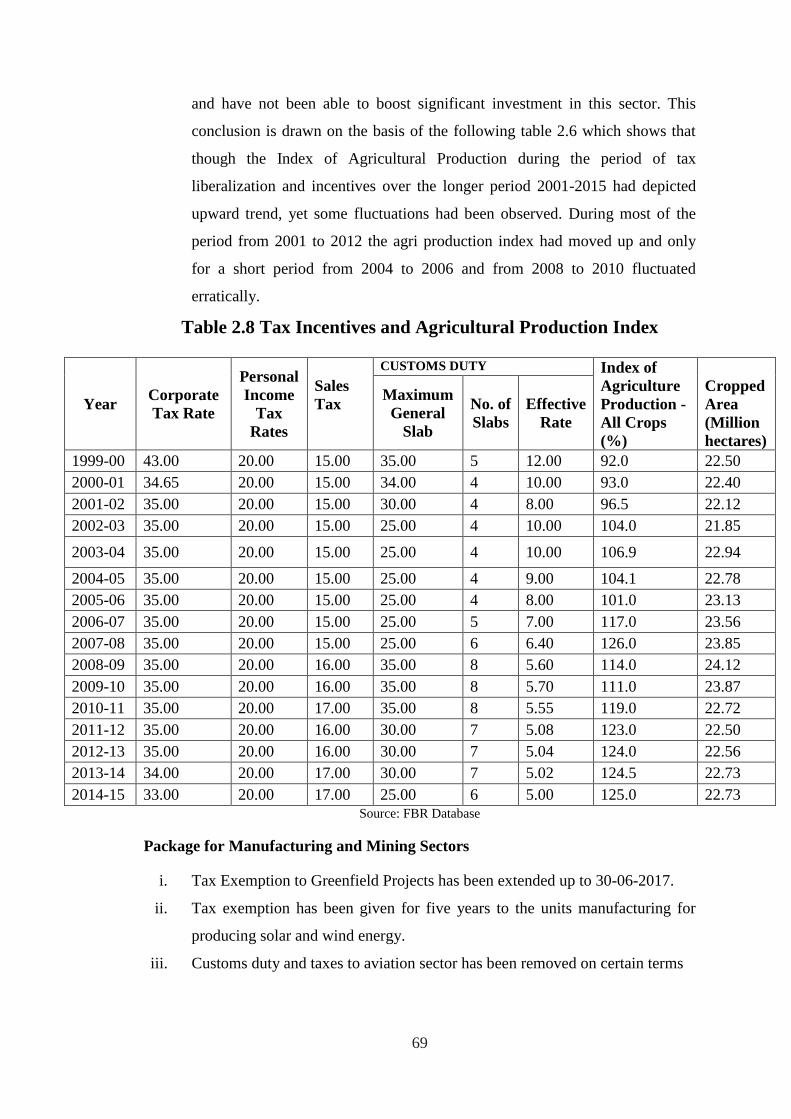

Table 2.8 Tax Incentives and Agricultural Production Index ........................................................69

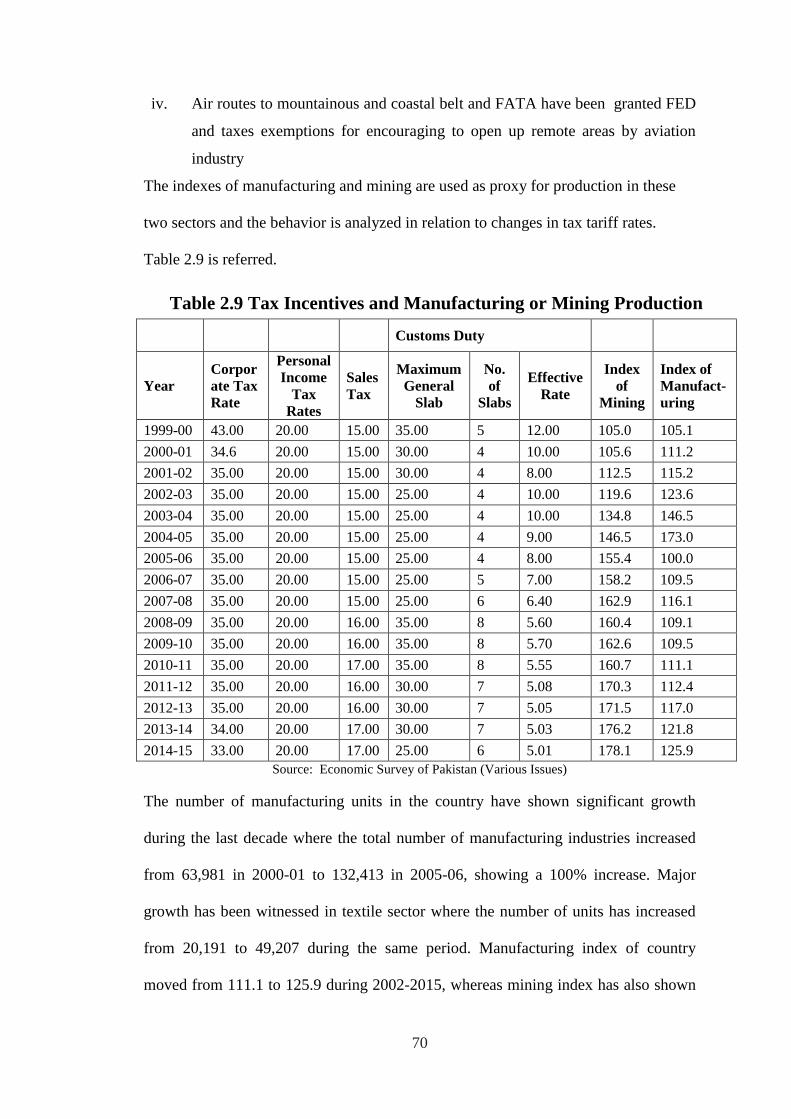

Table 2.9 Tax Incentives and Manufacturing and Mining Production ..........................................70

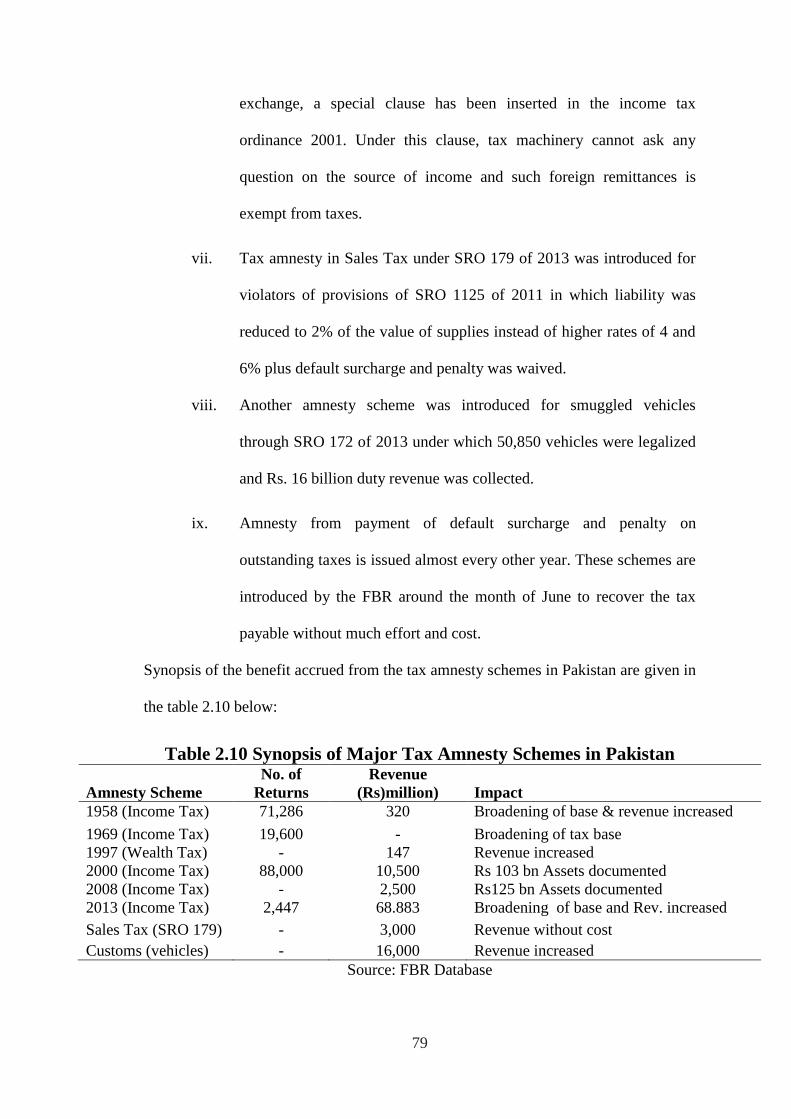

Table 2.10 Synopsis of Major Tax Amnesty Schemes in Pakistan ...............................................79

Table 5.1 Descriptive Statistics: Domestic Investment, Corporate Tax and Tariff Rate .............148

Table 5.2 Pairwise Granger Causality Tests ................................................................................149

Table 5.3 Correlation Matrix: Domestic Investment, Corporate Tax and Tariff Rate ................150

Table 5.4 Domestic Investment ...................................................................................................151

Table 5.5 Unit Root Test ..............................................................................................................151

Table 5.6 Diagnostic Tests of Data ..............................................................................................152

Table 5.7 (a) Results of ARDL Model Based on Schwarz Bayesian Criterion ...........................152

Table 5.7 (b) Results of ARDL Model Based on Schwarz Bayesian Criterion ...........................153

Table 5.8 Estimated Long Run Coefficients for selected ARDL Model .....................................153

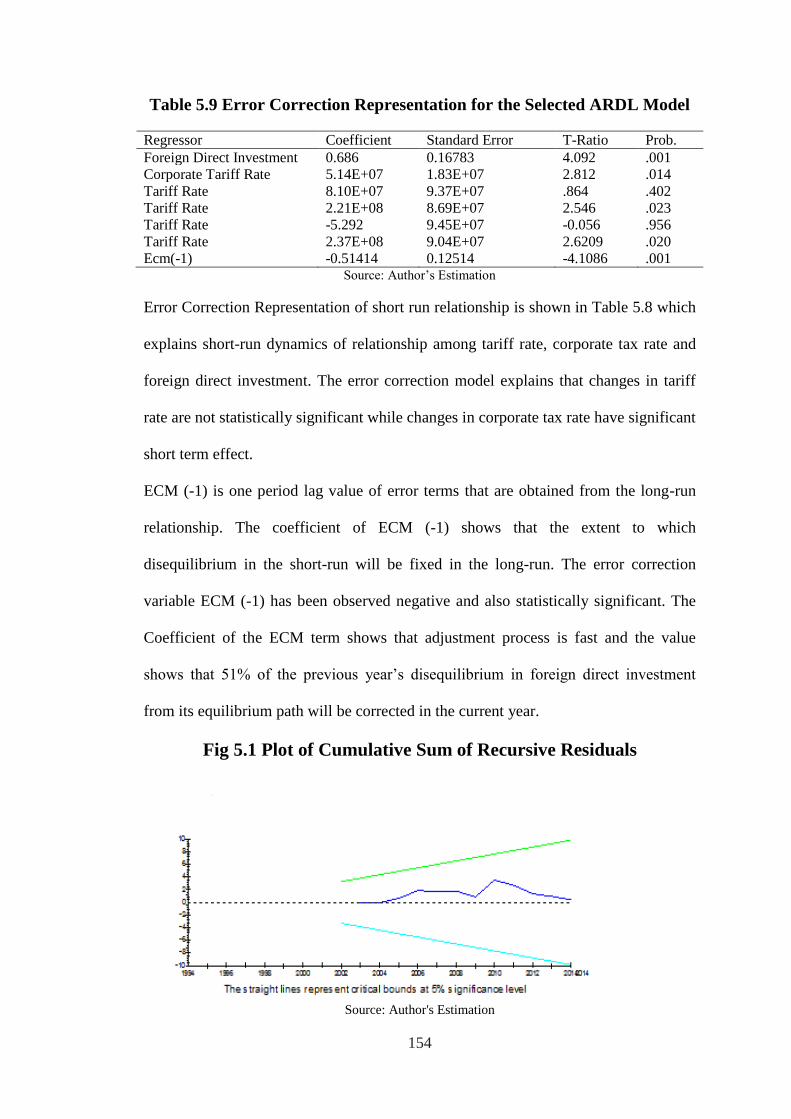

Table 5.9 Error Correction Representation for the Selected ARDL Model ................................154

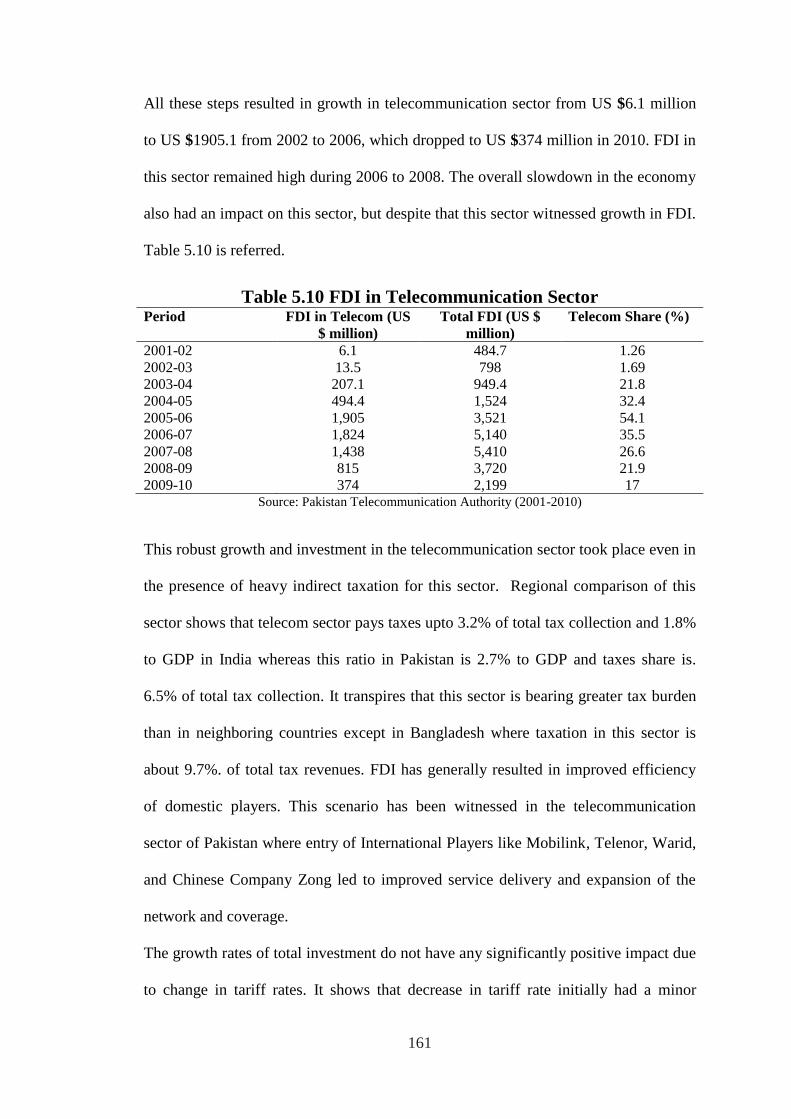

Table 5.10 FDI in Telecommunication Sector .............................................................................161

x

LIST OF FIGURES

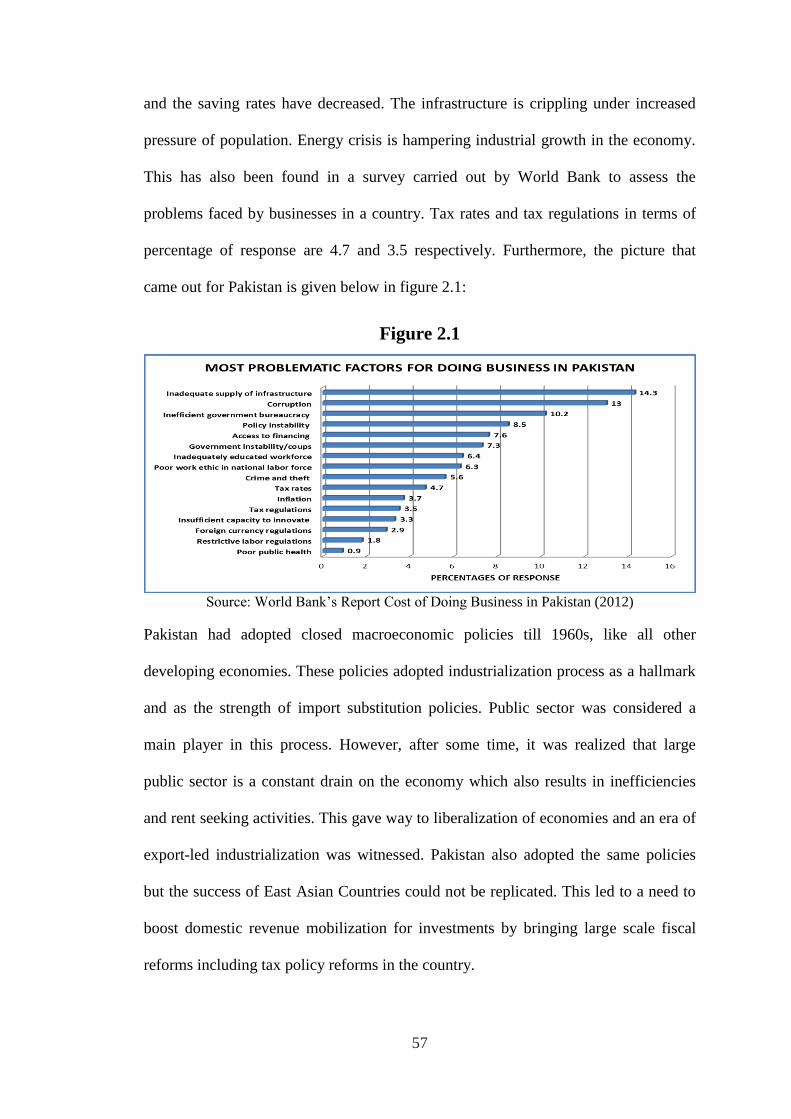

Figure 2.1 Most Problematic Factors for Doing in Pakistan .........................................................57

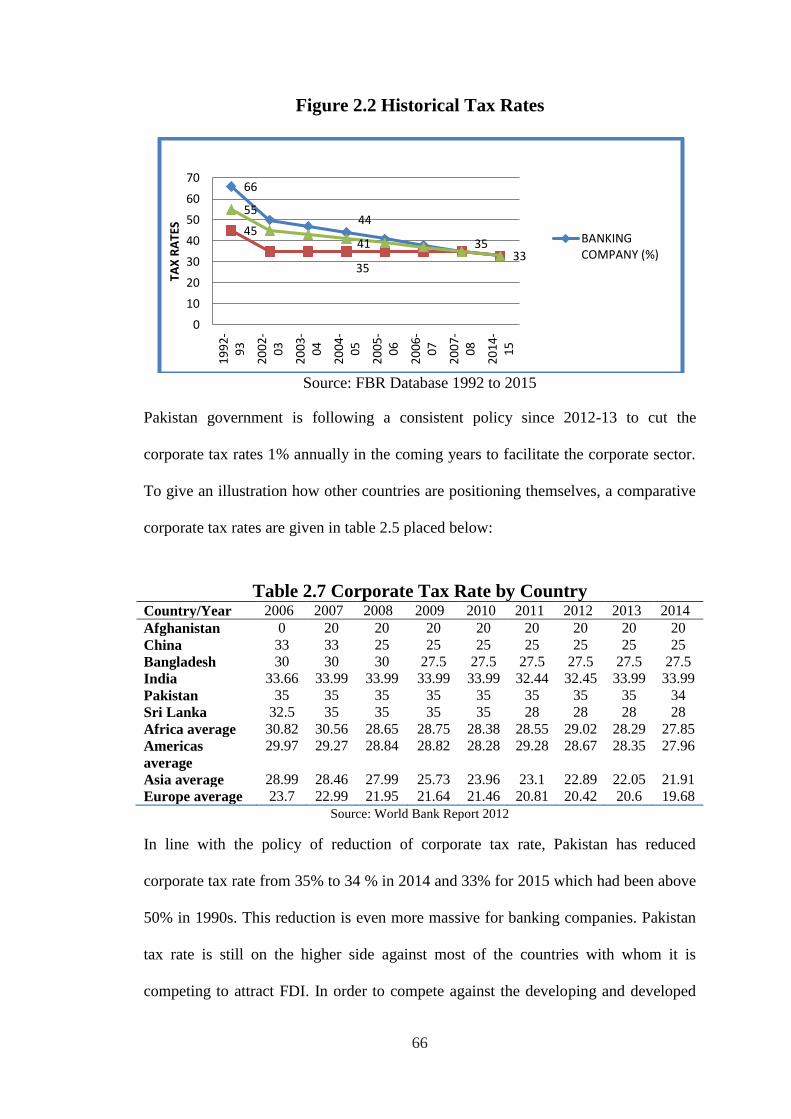

Figure 2.2 Historical Tax Rates .....................................................................................................66

Figure 5.1 Plot of Cumulative Sum of Recursive Residuals .......................................................154

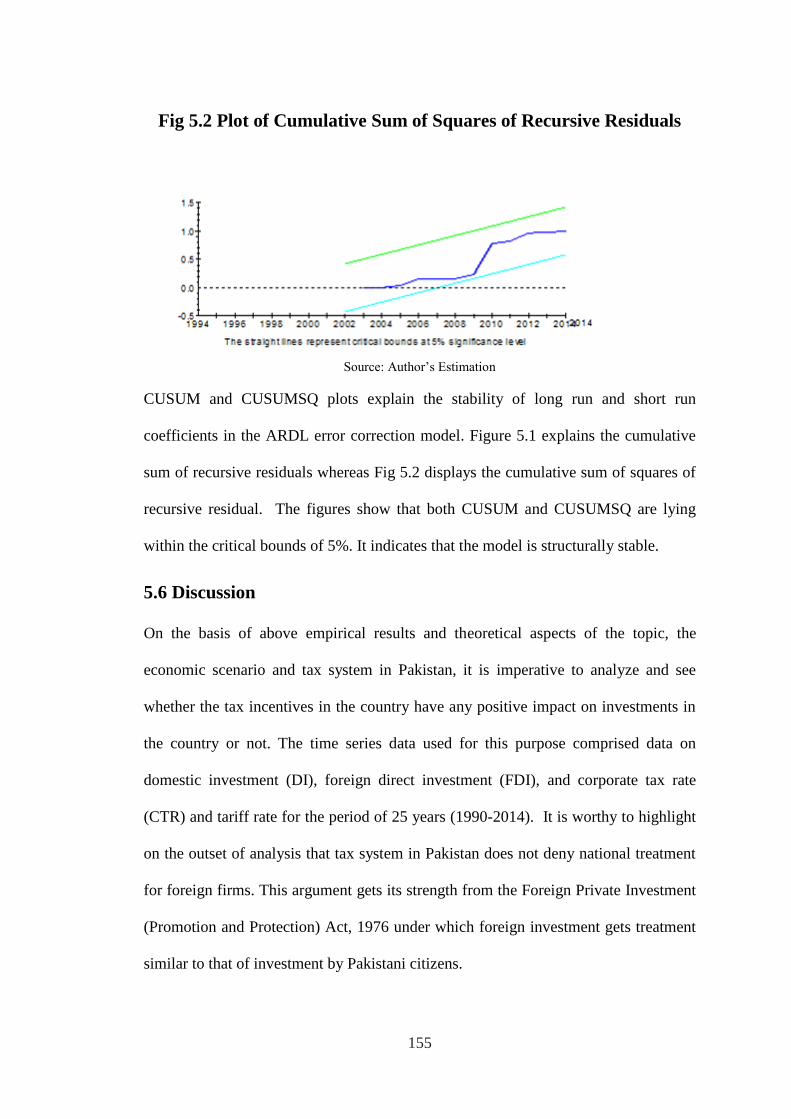

Figure 5.2 Plot of Cumulative Sum of Squares of Recursive Residuals .....................................155

Figure 5.3 Domestic Investments and Corporate Tax Rate .........................................................158

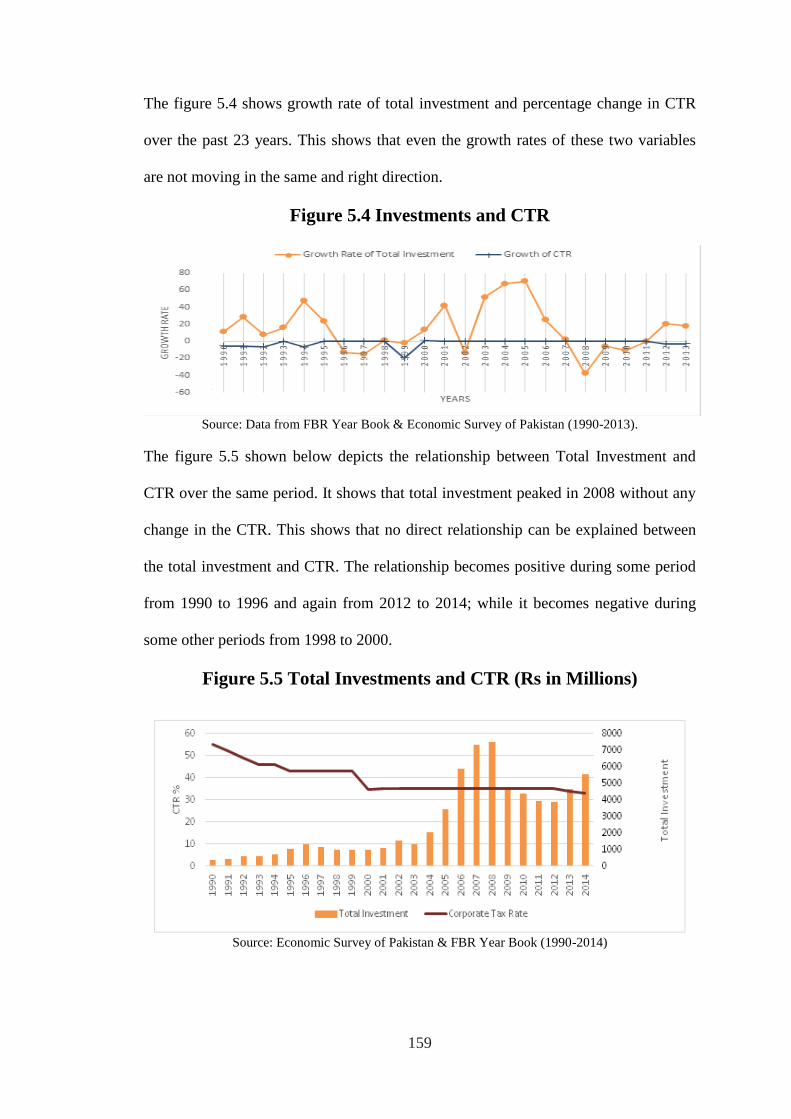

Figure 5.4 Investments and CTR .................................................................................................159

Figure 5.5 Total Investments and CTR ........................................................................................159

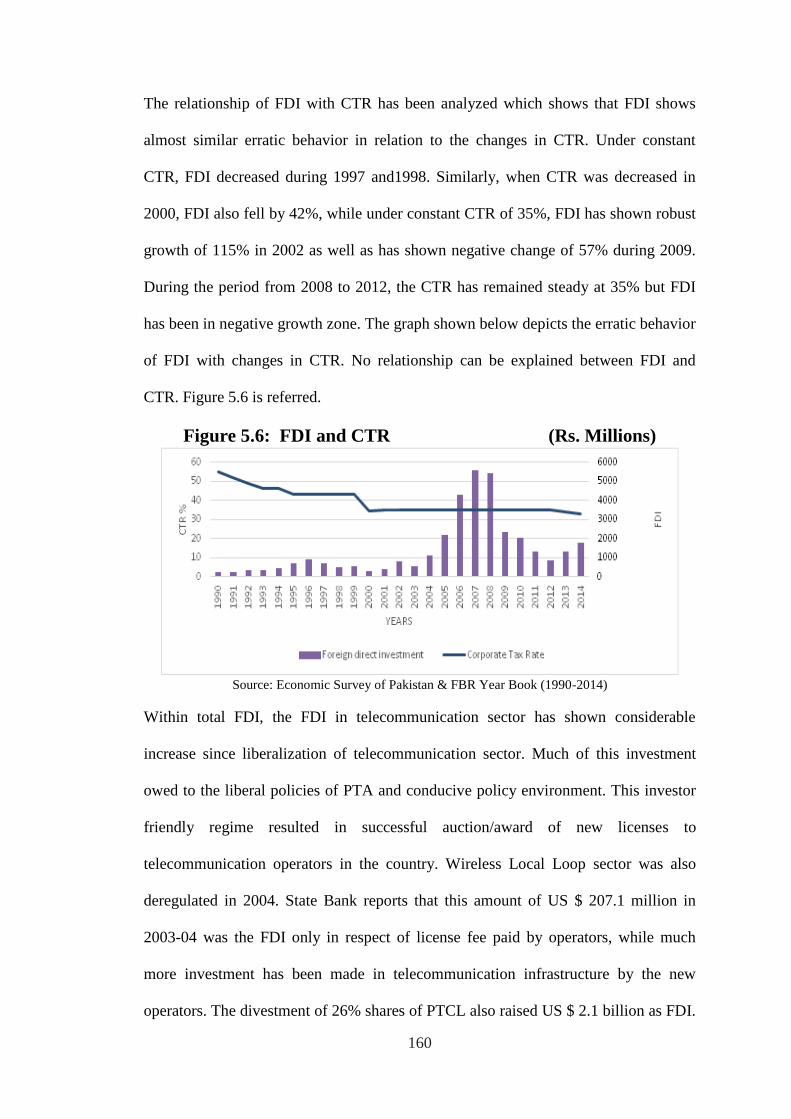

Figure 5.6 FDI and CTR ..............................................................................................................160

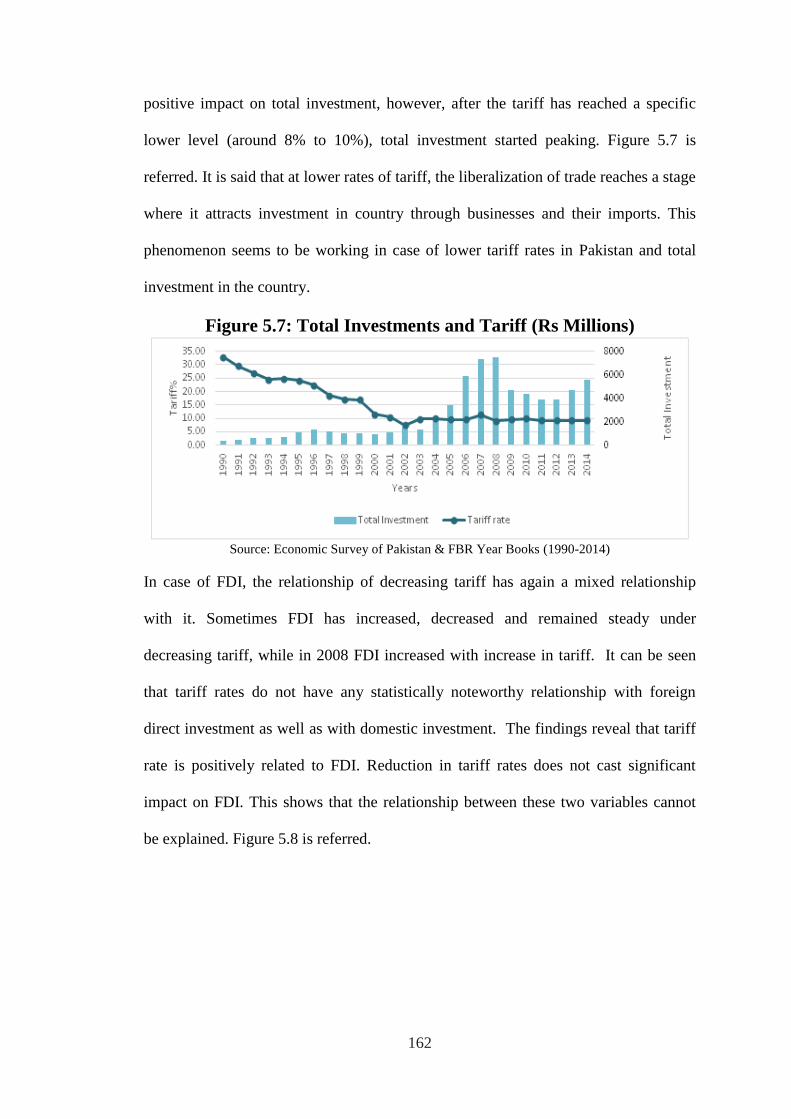

Figure 5.7 Total Investments and Tariff ......................................................................................162

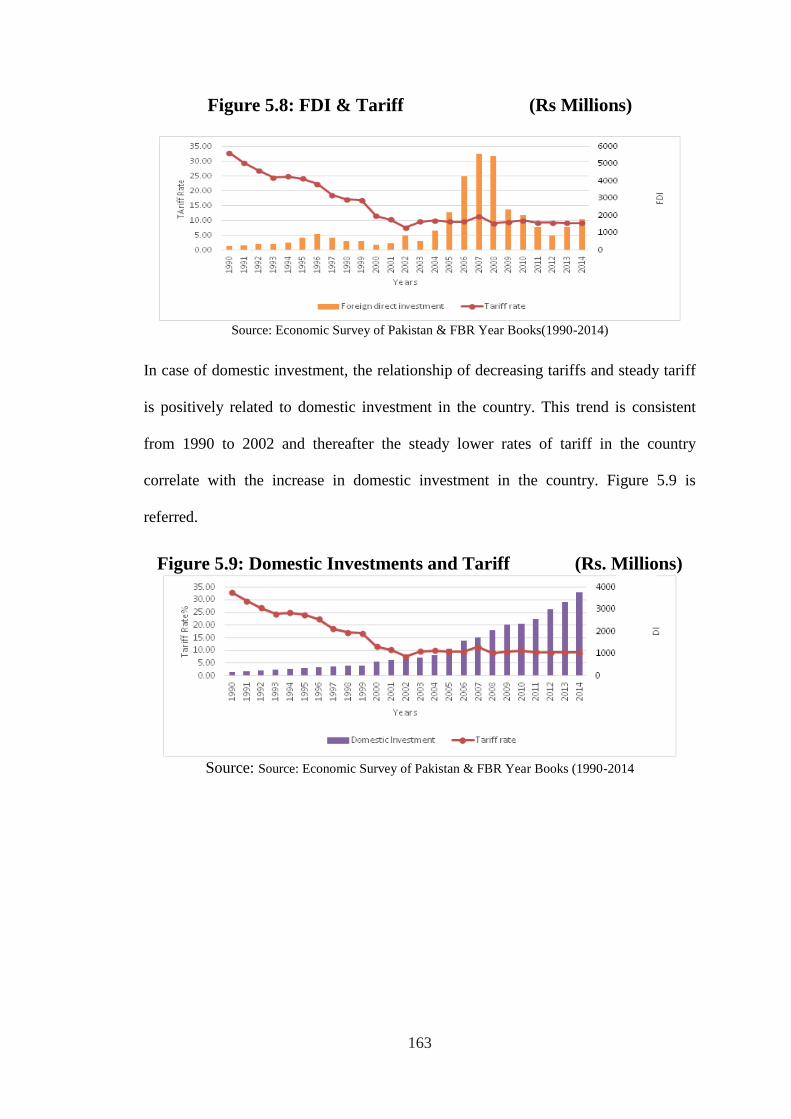

Figure 5.8 FDI & Tariff ...............................................................................................................163

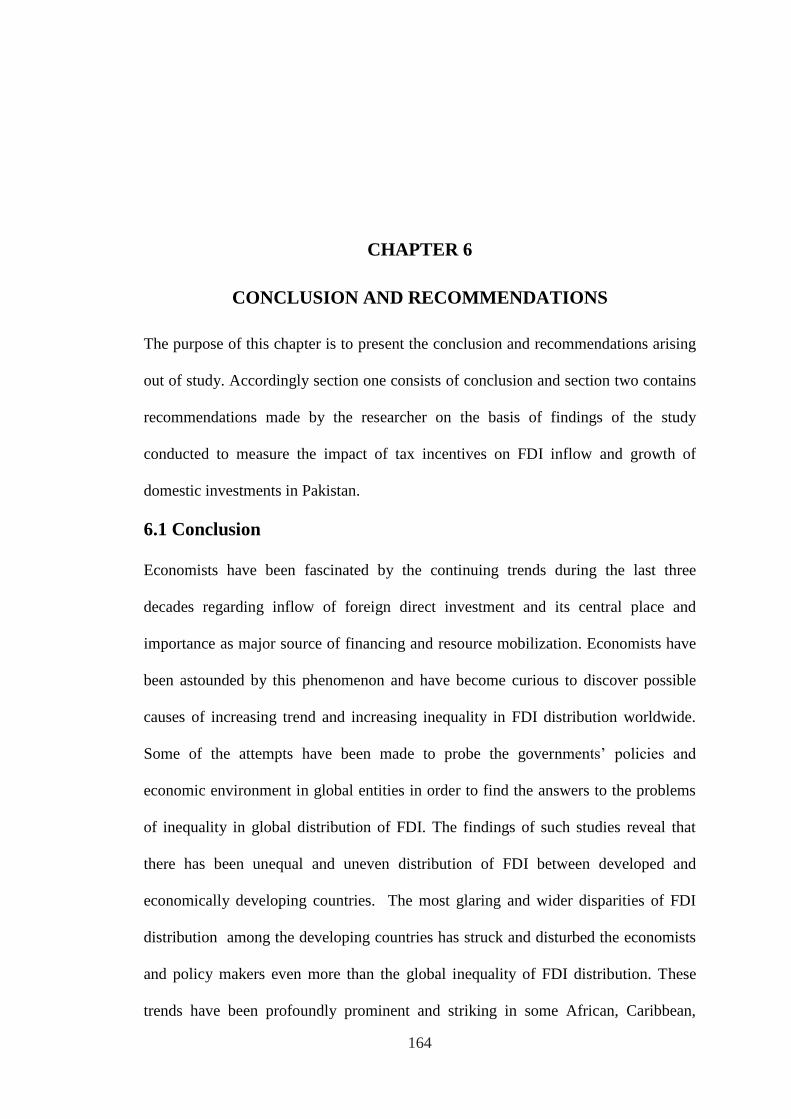

Figure 5.9 Domestic Investments and Tariff ...............................................................................163

xi

LIST OF ABBREVIATIONS

ARDL Autoregressive-Distributed Lag

BMR Balancing, Modernization and Replacement

BOI Board of Investment

CET Common External Tariffs

CIT Corporate income tax

CPEC China Pakistan Economic Corridor

CTR Corporate Tax Rate

DI Domestic Investment

EPZ Export Promotion Zone

ERP Economic Reforms Program

FATA Federal Administrated Tribal Agencies

FBR Federal Board of Revenue

FDI Foreign Direct Investment

FED Federal Excise Duty

GDP Gross Domestic Product

GMM Generalized Method of Moments

GNP Gross National Product

IRS Inland Revenue Service

LDCs Less Developed Countries

M&A Merger and Acquisition

MNCs Multinational National Corporations

MNEs Multi-National Enterprises

MPT Modern portfolio theory

NPVDEVD Net Present Value in Developed Area

ODA Official Development Assistance

OECD Organization for Economic Cooperation and Development

PME Plant, Machinery and Equipment

PRAL Pakistan Revenue Automation Limited

PRGF Poverty Reduction and Growth Facility

R&D Research and Development

REIT Real Estate Investment Trust

SEZs Special Economic Zones

SME Small and Medium Enterprises

SROs Statutory Regulatory Orders

TR Tariff Rate

VDIS Voluntary Disclosure of Income and Wealth Scheme

WAPDA Water and Power Development Authority

1

CHAPTER 1

INTRODUCTION

This chapter consists of background of the study, brief detail of FDI, domestic

investment, fiscal policy, and objectives of the research, problem identification,

problem statement, research questions, and significance of study, scope and

organization of study.

1.1 Background of the Study

Economic development of a country is a process where various factors act in cohesion

towards achieving the goal. These factors include investment in human and physical

capital, effective governance, use of technology and innovation for transformation to

a modern economy, putting institutional structures and economic reforms in place,

overcoming structural constraints, providing strong industrial base, robust services

sector, successful foreign policy, rule of law, transparent and friendly business

environment and so on. These factors are combined together to achieve economic

development of any country in relation to increase in the GDP of the country and

provide better standard of living for the population. These factors are in one way

independently required while on the other hand; these are inter-dependent on one

another. It also happens that these factors align themselves in a sequential order where

one factor leads to the other, ultimately leading to economic development in a

country.

2

Pakistan has introduced broad ranging tax reforms as part of the overall fiscal agenda.

FBR has brought major structural and policy changes to enhance revenue generation,

boosting tax to GDP ratio and broadening of tax base on the one hand while it has

introduced many fiscal measures to encourage FDI inflow and growth in domestic

investments. Government has offered many tax incentives overtime to achieve these

objectives. These incentives as part of fiscal instrument to promote growth include tax

cuts, tax holidays, tariff reductions, tax rebates and some tax amnesty schemes. Other

fiscal and tax policy incentives were offered which included import duty variations

and provision of depreciation allowance on capital assets. Mintz (1990) explores the

effectiveness of offering tax holidays simultaneously with allowing depreciation

allowances on plant and machinery and has found that tax holidays end up with

negative implications for capital formation, contrary to the objective of increasing

capital formation. Mintz’s conclusion hinges upon an assumption that in case of long

term assets, tax system provides for deduction of accelerated depreciation on capital

assets, and cannot be deferred whereas ,the tax holidays, may actually punish

investors during early days of tax holiday duration. A tax system may be generous in

supporting and providing incentives, resulting in capital formation and providing

deferred depreciation allowance.

This trend has also been witnessed in Pakistan’s tax system where accelerated

depreciation cannot be deferred during tax holidays. Once tax holiday expires, normal

depreciation can be claimed. When this situation is compared between areas with tax

holidays and without tax holidays, the areas without tax holidays can claim

accelerated depreciation as well as normal depreciation. Similarly, import duty

concessions are also focused more towards underdeveloped areas. It can be inferred

here that tax and tariff incentives affect investment differently in different regions and

3

under different conditions. Consequently various incentives impact capital cost and

investment differently.

Decreased investments are one of the most important factors impeding economic

growth in Pakistan. Tax policy of government has not always been focused on

introducing measures to attract and increase investment (both domestic and foreign)

in the country. Generally it has been focused on revenue mobilization rather than

promoting investments. Sometimes, government took some measures aimed at

attracting investments and sometimes some ancillary steps were taken to attract

investors like providing conducive and business friendly environment. FDI is a long

term venture which is dependent on many other factors beyond tax policy measures

which most of the governments have been trying to achieve through trade

liberalization and trade incentives for the investors. It is important to understand that

domestic investment is directly dependent on the economic indicators of the country,

investment opportunities in the economy, consistency of policies, law and order

situation, availability of cheap skilled labor, availability of low cost of energy and

other inputs. Pakistan is a developing country with huge potential, but it is stuck with

many other economic problems like low GDP growth, low tax to GDP ratio and

limited fiscal space. According to the economic survey of Pakistan (2014-2015) the

current state of economy in Pakistan is such that Pakistan is spending only 20% of its

GDP through public sector, which is quite low and is far less than international

standards. This problem gets aggravated as the private sector in the country is not

developed to jump in with investment to fill the social and infrastructural gap.

Another side of the story of government expenditures according to Keynesian school

of economics is that if increase in government expenditure is not wisely planned, it

may lead to undesirable impact on the economy. This negative impact is usually due

4

to crowding out effect coming into play through decrease in disposable income (due

to increase in taxes). In absence of other impetus of growth in Pakistan, government

has to resort to more public sector investment in public good and importantly to

attract private sector investment. However, due to low level of public investment and

absence of other favorable factors in the economy, the overall level of domestic

investment is also low resulting in low job opportunities and economic activity in the

country. According to the economic survey of Pakistan (2014-2015) Pakistan is facing

economic deflation, despite low fuel cost and decrease in interest rates from 9.5% to

6%, private sector credit to GDP is only 9.7 % in 2014-15 as compared to 12.8 % in

2007-08. This shows that there is a genuine flaw in the public policies which is dis-

incentivizing investments from the private sector. As successive governments have

failed to bring about structural changes in the economy, there is no visible

improvement in reversing the declining trend in private investments.

Initiatives to boost domestic investment include major reform in the tax policy to

review and refresh the tax incentives in the country. These incentives include

deregulation of sectors (from taxation point of view), tax cuts, tax rebates, tariff cuts,

tax holidays and tax amnesty schemes. Tax cuts and rebates have been aimed at

putting more money back in the pockets of the consumers, industry and businesses.

Ideally, this extra money is then spent and invested in the economy which increases

the economic activity in the country. More cash flow means more investment, which

has a direct bearing on economic growth and prosperity in the country. Governments

have been introducing several tax incentives in the country but most of them failed to

achieve desired object due to lack of consistency and credibility of tax policies,

adhoc-ism, lack of transparency and trust deficit between government officials and

business community.

5

Developing countries use fiscal policy as an important tool for promoting investment

and ensuring long term economic development. As part of tax incentives, tax

holidays have an important role in promoting industrialization in such countries.

Pakistan has also employed the same tools in anticipation of achieving the same

positive results of industrialization of backward areas. Besides tax holidays, other

measures such as changes in tariff rates, reduction in corporate tax rates and

depreciation allowances have also been used to achieve the objectives of promoting

investment, business growth and industrialization. However, the success of such

measures has been far from satisfactory and the desired results have not been fully

achieved due the various issues like inconstancy of policies, bad law and order

situation, poor infrastructure, energy crisis and lower tax revenue and narrow tax base

in Pakistan.

FDI makes contribution to economic activity through development finance, transfer of

technology and technical expertise, transfer of managerial skills and improved

efficiency. It also casts healthy impact on economic growth and prosperity and also

helps government to generate employment opportunities and additional indirect taxes.

For instance, major share of tax collection is composed of withholding taxes;

therefore, FDI can cast substantial and positive effect on revenues in Pakistan.

FDI has shown an upward trend in global scenario since early 1980’s. As companies

fiercely compete in the global market, they look for exploiting comparative advantage

that different countries offer in order to gain competitive edge. Therefore, we see that

there is a growing pattern of relocation of manufacturing concerns and businesses

worldwide. Many of Fortune 500 companies are generating over 60 percent of their

revenue from outside their home countries. Developed economies have greater choice

of investors and sources of finance, but they still prefer FDI over domestic

6

investment. Preference for foreign investors is due to the fact that they tend to bring

with them benefits which domestic investors cannot bring into the economy.

Monetary policy also influences investment decisions through changes in interest

rates. In order to induce investment in the economy, lower interest rates provide

attractive business environment. If demand of the economy requires contraction,

interest rates are increased to suppress investment. Western Europe and North

America witness high FDI. Conversely FDI is low in Africa and Asia. However, there

are examples of countries such as China where growth rate has grown in tandem with

huge FDI. Some studies have found out that economic growth in Asian countries is

significantly related to exports and FDI. However, relationship with aid was found to

be insignificant.

Generally, investors make their off-shore investment decisions on the basis of overall

socio-economic and enabling business environment in a particular economy. This

environment is usually based on many economic factors like locational advantage,

trade and industrial policies, tax rates, tariff structure, lower labor cost, access and

cost of other inputs like energy and exchange rate regime and non-economic factors

like law and order situation, infrastructure, good governance, efficient and effective

system of contract enforcement and dispute resolution. Similarly, fiscal policy also

affects investment through changes in the taxes and expenditure. These decisions

convey the message about business environment of the economy based on which

investment decisions are made.

1.3 Problem Identification

Economic development of a country is a process where various factors act in cohesion

towards achieving the common goal. These factors include investment in human and

physical capital, effective governance, use of technology and innovation for

7

transformation to a modern economy, putting institutional structures and economic

reforms in place, security, overcoming structural constraints, providing strong

industrial base, robust services sector, successful foreign policy, rule of law,

transparent and friendly business environment and so on. The government of Pakistan

undertook business process reengineering for attracting foreign investment and

provided investment friendly environment in the country. It is necessary to measure

impact of tax reforms foreign investment inflows as a huge amount has been ploughed

with the help of donors which entailed other invisible costs. Unfortunately, the tax-

GDP ratio has not been increased through reforms despite taxpayers’ facilitation,

simplification of procedures and minimization of contacts between taxpayers and tax

collector.

Pakistan’s economy is factor driven as well as situational where policies especially

fiscal policy is adopted and implemented accordingly. Taxation policies have

simultaneously been very unpopular and controversial in Pakistan. There have been

limited studies to empirically analyze whether these policies have led to sustainable

economic development. The main objective of these policies has been revenue

generation and facilitating the business community. Tax policies are usually based on

two premises i.e. firstly, more investment is essential for rapid economic growth, and

that the tax incentives can stimulate greater investment. Tax polices formulated over

the years have been inconsistent, incongruous and heavily reliant on the corporate

sector. Investment is the backbone of any country especially for developing countries

like Pakistan, but unfortunately domestic and foreign investors have been reluctant to

make big investment decisions due to unfavorable investment environment in the

country.

8

The complexity of tax structure and nature of tax of Pakistan has been the foremost

obstacle in the way of creating business friendly environment. Multiplicity of various

federal, provincial and local taxes is the basic problem in this regard. At national

level, there are different slabs of tax rates including Sales Tax, Customs Tariff,

Federal Excise duty and Income Tax. Consequent to most fundamental problem of

high tax rates, there are various prohibitions and exemptions, which offer climb to

compelling distortion. Noteworthy tax policy issue in Pakistan is the improper,

rigorous, retrogressive, unreasonable taxation arrangement, extremely narrow tax base

and a structure prompting lower tax-GDP ratio. The lack of consistency, continuity,

clarity, transparency and business unfriendly tax policy is a major cause of concern

for the investors. Historically, the governments’ primary motive of imposition of

taxes has been to boost tax collections for resource mobilization for government

spending. This would also have been helpful if this spending was made on

development which in turn stimulates overall economic development in the country

and which was not the case in this instance. Tax to GDP ratio has been hovering

around 9% for many years which is one the lowest in the region. Out of populace of

180 million, just 3.6 million are the National Tax Number (NTN) holders and less

than 1% file their annual tax returns (Financial Survey 2013-14). Pakistan has

extremely low tax GDP proportion, in comparison with other creating nations like

India and Sri Lanka.

Tax structure in Pakistan contrasts from that of the majority of other nations. While

overwhelming contribution of taxes in most growing nations is domestic taxes

whereas, in Pakistan, generous segments of taxes are earned from imports levies.

There has been a unreasonable and unhealthy tax share Vs. share to GDP of different

sectors, in which industrial sector suffers the major burden while the major

9

contributor of GDP, agriculture is exempted from federal taxes. Then, income tax

rates in Pakistan are one the highest in the world which encourages tax evasion and

impacts growth of domestic investment as well as inflows of FDI in the country. In

Pakistan, government reports have revealed that prior to tax reforms measures,

corporate income tax rate was 66% which was gradually reduced to 35% gradually

during the last half decade and further reduced to 34% for banking companies and

33% for non-banking companies.

The World Bank Study (2009) has shown that in Pakistan there is still a huge

potential of around Rs.1000 billion due to distorted tax policies, and corruption in the

organization. This tax gap can be turned into resource pool if tax policies are

appropriately prepared and fully implemented. Kemal (2001), states that the Structural

Adjustment Program policies have resulted in multiplicity of poverty level as most of

the taxes collected are indirect taxes or in indirect or withholding mode and this

passes on the burden of taxes to the poor, thus increasing poverty. Government

decided to undertake major tax policy reforms with the assistance of IMF and World

Bank in 2001.The purpose of these tax reforms was to make necessary corrections in

the tax system and machinery, remove distortions, eradicate corruption, create a

motivated and efficient tax administration broadening of narrow tax base,

simplification of tax laws and procedures and creating trust between tax collectors and

taxpayers by intruding tax friendly environment tax friendly environment.

According to the Economic Survey of Pakistan (2014-2015) Tax to GDP ratio was 9.4

in 2005-06 and reached 9.7 in 2014-15 with fluctuations during this period. The tax to

GDP fell to 8.5 in 2010-11 showing that some drastic changes are required in the tax

structure and policy. The profile of sectoral mix of taxes has also changed a lot during

the last two decades. Direct taxes share has grown to a larger extent than indirect taxes.

10

It has reached the level of 42% during 2014-15 which is quite higher from 31.5 %

during 2005-06. The share of sales tax has also simultaneously increased from 41.3 %

in 2005-06 to 44.2% during 2013-14. The share of customs duty has decreased due to

tariff exemptions and reduction, in the wake of trade liberalization and expansion of

trade agreements. The direct taxes in the country consist of tax on salaries, income

from business or profession, interest on securities, property income and capital gains

etc. Indirect taxes are comprised of sales tax and FED, whereas customs duty is levied

on imports and rarely on exports.

There are various distortions in the taxation systems which include regressive taxes

and rates of taxes higher than the capacity of the taxpayers to pay. There are different

rates for all taxes, including sales tax, customs duty, federal excise and income tax. In

addition to high tax and tariff rates, there is lack of consistency in tax policy

formulation and implementation which leads to growing trust deficit among business

enterprises and investors in Pakistan. Economists are of the opinion that higher

corporate tax rates negatively affect investment and it also generates more corruption,

encourages tax evasion, lower tax collection and consequently leads to low GDP and

low investment retarding the economic growth. Only possibility for resource

generation is a sound tax system with broad tax base, lower rates, high tax-GDP ratio

and strict enforcement for tax compliance

In this economic scenario, domestic investment has been suffering from lack of

growth for a long time. Foreign Direct Investment has also been drying up in Pakistan

due to many tax and non-tax factors. FDI inflows into Pakistan have been becoming

scarce in the course of recent years. Foreign Direct Investment (FDI) inflows into

Pakistan have been declining in the recent years. After hitting record high of $5.4

billion in 2007-08, net FDI has come to dismal low of $1,667.6 in 2013-14. Tax

11

arrangement in Pakistan differs massively from those of the many other countries.

High taxes and tariff rates on worldwide exchange moderate monetary action, making

industry less focused, and encourage tax evasion. With expanded globalization and

local incorporation, tax frameworks and strategies must be equivalent to other

comparatively stronger nations, and not operated in isolation.

In order to attract foreign investment in the country, governments offer many tax

benefits or incentives in different forms. In Pakistan governments have also been

offering many tax policy incentives to the investors but the investment has not shown

any growth or higher inflows in the country over last two decades. There is a need to

analyze as to why investments in Pakistan (domestic and FDI) have not been growing

despite the fact that government of Pakistan has taken a number of taxation and non-

taxation measures to boost investment and provide investment friendly environment

in the country to attract foreign investors. Many tax incentives like massive reduction

in corporate tax rates, reduction and even waiver of import tariffs on import of plant,

machinery and other related items, have been announced by successive governments

as part of holistic fiscal and investment policy in Pakistan. But the data has revealed

that correspondingly, growth in domestic investment and increase in FDI inflows have

not been witnessed in the investment horizon of Pakistan. Moreover, as the literature

also suggests, that there may be some non-tax factors, which have been hampering the

increase in domestic and foreign investment in Pakistan? It is, therefore, imperative to

investigate and analyze this complex problem facing the country and hindering

economic progress and to explore whether these tax incentives have cast any impact

on the investments. It would also necessary to identify the cause of success or failure

of tax reform initiatives to further reach at some conclusion and to propose further

policy recommendations to resolve the issues. Hence, after identification of the

12

problem, the researcher aims to present the problem statement to carry on the research

on the subject.

1.4 Statement of Problem

Tax Incentives are likely to continue to be part of development policy in many

developing nations around the world. In the last two decades, many governments have

actively promoted their countries as investments locations, to attract private capital

investment, technology and managerial skills associated with the idea of achieving the

development targets. Many countries, including Pakistan, have adopted measures to

facilitate the attraction of both domestic and foreign direct investment. Tax incentives

are among the important measures that are used to boost investment. As revealed by

the literature on the subject, tax incentives play a very important role in encouraging

both domestic and foreign investments. Government of Pakistan has introduced broad

ranging tax reforms as part of the overall fiscal agenda. This study attempts to analyze

the impact of various tax policy incentives on investments, both domestic and Foreign

Direct Investment in the context of Pakistan. Government has been providing

incentives like reduced CTR and Tariff rates to attract both domestic as well as

foreign investors. However, the desired increase in investment has not been observed.

This study aims to find out relationship among different variables like domestic

investment and FDI, and corporate tax rates and customs tariff rates. Moreover, it

would analyze why desired growth in domestic investment and inflows of FDI has not

been witnessed despite the tax incentives offered. The study also tries to find out the

causes of success or failure of the existing tax policy incentives and to explore any

non-tax factors which may have been affecting FDI and domestic investment. The

study will suggest future measures to be adopted to boost investments in Pakistan by

giving a clear path for future tax policy and reforms.

13

Government has been providing incentives like reduced CTR and Tariff rates to

attract both domestic as well as foreign investors. However, the desired increase in

investment has not been observed. The literature shows that there is a relationship

between tax and tariff rates and investment. The relationship has to be analyzed in

context of Pakistan. This study attempts to explore the relationship between

incentivized tax policy and investment (domestic and foreign) and also to analyze

their impact on investments. This study aims to explain how variables like corporate

tax rates and tariff rates affect growth and inflow of investment in Pakistan. The study

will further suggest future measures to be adopted to boost investments in Pakistan by

giving a clear path for future tax policy and reforms.

1.5 Research Questions

1. Does an incentivized tax policy affect domestic investment and FDI in

Pakistan?

2. What is the impact of change in Corporate tax rates and Tariff rates on

domestic investment in Pakistan

3. What is the impact of changes of CTR and TR on Foreign direct investment in

Pakistan?

4. What type of relationship exists between Tax and Tariff rates and Foreign

direct investment

1.6 Significance of Study

Economy of Pakistan is the 26th largest in the world. Pakistan was an extremely poor

country at the time of its inception. It was an agrarian economy with an insignificant

industrial base. The businesses growth was initiated with the most nominal and

underdeveloped infrastructure in the country. Pakistan's normal economic growth rate

in the initial stages had been not compatible with growth rates of the regional

14

countries and the world economy during the same period. However, the economy

started picking up in the 1960s. Normal yearly genuine GDP growth rates were 6.8%

in the 1960s, 4.8% in the 1970s, and 6.5% in the 1980s. Normal yearly growth

tumbled to 4.6% in the 1990s with essentially brought down economic growth in the

country.

Pakistan is a factor driven economy and tax policy is a tool of fiscal policy applied for

achieving all objectives like revenue generation, control money supply in the country

and to increase investment in the economy. Tax polices formulated over the years

have been inconsistent, incongruous and heavily reliant on the corporate sector.

Investment is known as the backbone of any country especially for developing

countries like Pakistan, but unfortunately investors feel hesitation in investment and

not willing to invest in Pakistan due to various tax and non- tax factors.

Successive governments in Pakistan have been making efforts to correct distortions in

the taxation systems and improve the efficiency and robustness in taxation

framework. The key issues in Pakistan’s tax system during pre-reform period 2001 in

Pakistan were: discretionary forces with tax authorities, debasement, restricted tax

base, high tax rates, SRO culture, and low share of direct taxes, substantial

dependence on indirect and withholding taxes, deferred discount installments and a

non-accommodating environment in tax workplaces (World Bank Report 2009).

Government of Pakistan took the tax reform initiative in 1985 and the task force

conducted detailed diagnosis of the tax systems and gave some recommendations for

administrative and legal and procedural reforms but unfortunately due to the political

stability, the recommendations could not be implemented. After World Bank report,

government commissioned a high power commission on tax reforms which gave out a

report known as Shahid Hussain Report 2001. It deeply analyzed the ills and

15

distortions in Pakistan’ taxation systems and gave recommendations for policy and

administrative tax reforms. Subsequently reform project named as TARP was

implemented with financial and technical assistance of World Bank during 2004 to

2012. As part of this program, the government of Pakistan undertook business process

reengineering for attracting foreign investment and provided investment friendly

environment in the country. It is necessary to measure impact of tax reforms foreign

investment inflows as a huge amount has been ploughed with the help of donors

which entailed other invisible costs. Unfortunately, the tax-GDP ratio has not

increased despite tax reforms focused on taxpayers’ facilitation, simplification of

procedures and minimization of contacts between taxpayers and tax collector. This

aspect of reforms along with tax rates rationalization is a core subject for attraction of

investment which is to be taken into account. Many important tax policy changes have

been undertaken to facilitate the foreign investors in Pakistan and tariff structure has

also been rationalized accordingly. Pakistan’s tax policy has undergone massive

reforms during the period from 2004 to 2012. The latest tax reforms were initiated in

the year 2004 and no appraisal has so far been carried out to explore the effects on

investments of different tax measures undertaken and incentives provided in Pakistan.

It is there very critical to investigate and explore what has been the impact of these tax

reforms and tax measures adopted on the overall economy of Pakistan and on

investments in particular. Hence this study is an attempt to analyze the situation and

find out the level of success of these tax measures and also find whether any further

measures are desired to be undertaken in future to achieve the desired objectives.

The studies have revealed that tax policy changes affect inflow of FDI and growth of

domestic investment, either positively or negatively. It suggests that a significant

relationship exists between tax incentives and tariff incentives and FDI and domestic

16

investments. Various tax and tariff incentives have also been provided in Pakistan to

the local and foreign investors during the last two and half decades. There is no

empirical evidence available to prove whether, any such relationship exists between

tax and tariff incentives and FDI and domestic investment in case of Pakistan and if

yes, whether this relationship is positive or negative. There has been no significant

research or study whether tax incentives have any impact on investments (FDI and

domestic) in Pakistan. There is no empirical evidence as to what relationship exists

between CTR/Tariffs with FDI and domestic investment in Pakistan. It also aims to

explore, what are the non-tax factors which may have been affecting FDI and

domestic investment. Moreover, the study also suggests measures to be adopted to

enhance investments in Pakistan.

FDI inflow into Pakistan touched its peak in 2008 and since then it has been on the

downward spiral. The key factors which have adversely affected FDI inflow are

explored with special focus on mapping the effect of tax policy measures adopted

during the last 25 years. What impact did these key taxation variables have on the

inflow of FDI and domestic investments and how altering/readjusting various tax

policy determinants can help enhance FDI and domestic investment in Pakistan.

Hence, this study tries to evaluate impact of tax policy on investment, both FDI and

domestic investments, in the country. The study also tries to find out the causes of

success or failure, whatever the case may be, of the existing tax policy in promoting

investment if any. Moreover, the study also suggests measures to be adopted to

enhance investments in Pakistan.

17

1.7 Objectives of the Study

Following are the focused objectives of this study.

To provide insight about the impact of change in Tax and Tariff rates on

domestic investment in Pakistan.

To examine and evaluate the short run impact of Tax and Tariff rates on

Foreign direct investment in Pakistan.

To explore long run relationship between Tax and Tariff rates and Foreign

direct investment

1.8 Justification of the Study

The government of Pakistan undertook business process reengineering for attracting

foreign investment and provided investment friendly environment in the country. It is

necessary to measure impact of tax reforms foreign investment inflows as a huge

amount has been ploughed with the help of donors which entailed other invisible

costs. Unfortunately, the tax-GDP ratio has not been increased through reforms

despite taxpayers’ facilitation, simplification of procedures and minimization of

contacts between taxpayers and tax collector. This aspect of reforms along with tax

rates rationalization is a core subject for attraction of investment which is to be taken

into account. Many important tax policy changes have been undertaken to facilitate

the foreign investors in Pakistan and tariff structure has also been rationalized

accordingly.

FDI inflow into Pakistan has been on the downward spiral. There is a dire need to

explore as to what are the reasons and implications of this decline in investments in

Pakistan despite the fact that government has offered various tax incentives to

encourage domestic and foreign investments. It is imperative to identify the key

factors which have adversely affected FDI inflow are explored with special focus on

impact of tax incentives adopted in the past. What impact did these key taxation

18

variables (like CTR and Customs Tariffs) have had on the inflow of FDI and domestic

investments and how altering/readjusting various tax policy determinants can help to

enhance FDI and domestic investment in Pakistan? Hence, this study tries to gauge

the impact of tax policy on investment, both FDI and domestic investments, in the

country. The study also tries to find out the causes of success or failure, whatever the

case may be, of the existing tax policy incentives in promoting investment if any. It

also aims to explore, what are the non-tax factors which may have been affecting FDI

and domestic investment along with suggesting further measures to be adopted to

enhance investments in Pakistan.

In the absence of concrete findings of impact of changes on investments (FDI and

domestic), it will be unclear whether previous and current tax policies have borne

any fruit and achieved the desired objectives or further tax policy reforms are still

required in coming years to increase the investment regime in Pakistan. If the desired

results are not materialized, it would be a great setback for the national exchequer on

one hand and for the social and economic fabric of the society on the other. In this

context, there is a need to conduct a thorough study regarding impact of the changes

and reforms in tax policy brought about in Pakistan by providing various incentives to

taxpayers and investors and its impact on the level of investments (FDI and domestic

investment). The studies on the topic suggest that various incentives measures of tax

policy significantly affect flow and growth of investments, either positively or

negatively. But it is not known whether tax policies prior to 2004 and current

reformed and incentivized tax policies have affected the flow of FDI and growth in

domestic investments in Pakistan and if yes, whether it has affected positively or

negatively? What is the relationship of tax incentives like corporate tax rates and

customs tariff rate with domestic investment and foreign direct investment. This study

19

aims to explore too whether the current tax policy is rational and appropriate to attract

FDI in Pakistan or what further recommended changes are still needed? Moreover,

the study tries to provide a clear cut direction for future tax policy and reforms needed

in a well- focused and result-oriented manner. Thus, this study undertakes to measure

the effect of tax policies on investments in Pakistan during the last 25 years. The

analysis period of the study is from fiscal year 1990 to fiscal year 2014. It is regarded

as breakthrough effort in the area and is useful for the government, academia, and

donor agencies policy formulation and implementation.

Previous studies on the subject revealed that tax policy changes affect inflow of FDI

and growth of domestic investment, either positively or negatively. It suggests that a

significant relationship exists between tax incentives and tariff incentives and FDI and

domestic investments. Various tax and tariff incentives have also been provided in

Pakistan to the local and foreign investors during the last two and half decades. There

is no empirical evidence available to prove whether, any such relationship exists

between tax and tariff incentives and FDI and domestic investment in case of Pakistan

and if yes, whether this relationship is positive or negative. There has been no

significant research or study whether tax incentives have any impact on investments

(FDI and domestic) in Pakistan. There is no empirical evidence what relationship

exists between CTR/Tariffs with FDI and domestic investment in case of Pakistan

which has been proved by the literature reviewed above. Hence, this study attempts to

explore the relationship of tax policy incentives with the investments (FDI &

domestic) in Pakistan during the last 25 years. This study has filled the research gap in

case of Pakistan where there is no empirical research to establish relationship on tax

policy incentives on investments. This relationship has been proved in case of many

other countries but not in respect of Pakistan. The available data on the topic shows

20

inconsistent trend but statistically it has given concrete findings of the relationship

among selected variables. There are many non-tax factors which affect domestic and

foreign investment growth in Pakistan which have not been taken into account by

policy makers and also these factors do not figure out in other studies carried out on

this subject in other countries. This study has added this aspect of the research to the

body of existing body of knowledge and literature in this area of knowledge which

will be very useful for policy makers, economists, business enterprises, investors,

academia and researchers with practical implications.

It is also pertinent to mention here that studies on this topic have been carried out in

various other developing and some developed countries but no focused empirical

study has been conducted in Pakistan in view of the wide range policy changes and

reforms. This study is different from other studies conducted abroad and the study

justifies its usefulness and practicability on the following grounds:

i) In Pakistan the corporate tax rates are exorbitantly higher than many other

economies leading to lower investment, both domestic and FDI. In other

countries the tax rates are rationalized to attract FDI.

ii) World Bank and IMF have supported/financed tax reform programs in

many other developing countries which successfully achieved the desired

objectives of revenue collection and investment growth but in Pakistan

TARP has not been a success story and desired outcomes have not been

achieved due to unexplored reasons presumably non-tax factors.

iii) The tax policies in Pakistan have not been very consistent and focused for

decades. The major objective of most of the policies has been time-based

revenue enhancement instead of consistent policy directed at sustainable

economic growth, and hardly any focus on promoting investments.

21

iv) The tax policies in Pakistan have not met major success due to the frequent

introduction of tax amnesty schemes, ill-timed tax incentives and irrational

tax exemptions/subsidies unlike other countries which discourage the

domestic and foreign investors, hampering FDI, simultaneously

demotivating the genuine taxpayers for honest and voluntary tax

compliance.

v) As contrary to many other countries, cost of doing business in Pakistan is

considerably high. Moreover, the business friendly environment coupled

with suitable security environment has not been provided in Pakistan.

vi) Unlike other economies, the sectorial contribution to taxes in Pakistan

(like agriculture, industry and services) is not proportionate to the sectoral

contribution of GDP. It has resulted in increasing tax burden on industrial

and services sectors as agriculture sector is exempted from federal taxes.

1.9 Scope of Study

This study attempts to analyze the impact of various tax policy incentives on

investments, both domestic and FDI in the context of Pakistan. It aims to find out

relationship among different variables like domestic investment and FDI, and

Corporate tax rates and customs tariff rates. Data of the study variables has been

collected for 25 years from FY 1990 to 2014. This study does not include any non-tax

factors which may influence inflows of FDI and growth of domestic investment. This

study is focused on the investment in Pakistan only and the results of this study

cannot be implemented on the tax rates and investment figures of countries other than

Pakistan. The selected variables in the study are domestic investment and foreign

direct investment treated as dependent variables and corporate tax rates and tariff rates

are used as independent variables.

22

1.10 Organization of the Study

The study consists of six chapters. Nature, rationale, and objectives of study, behavior

of investment, tax policy and reforms undertaken in Pakistan during the period 1990-

2015, Problem identification, problem statement, research questions, justification,

scope and organization of the study are discussed in chapter 1. Chapter 2 explores and

discusses the theoretical background and underlying factors of FDI and domestic

investments in Pakistan. It explores relationship of investment with tax incentives and

measures the effect of tax policy incentives on FDI and domestic investments and also

provides justification of the study. Chapter 3 comprises of relevant literature review to

support identification of research gap, need of study and hypothesis statement.

Chapter 4 discusses the research methodology and model of the study. Chapter 5 deals

with analysis and findings of study in relation to impact of tax policy incentives on

investments. Finally, Chapter 6 provides the conclusion, recommendations, and

practical implications for the policymakers as well as for academia. In this chapter, it

has also been outlined as to what limitations this study has, and what are the future

directions in which further research can be conducted in this area.

23

CHAPTER 2

NEXUS BETWEEN TAX POLICY AND INVESTMENT IN

PAKISTAN

Theories of investment and taxation and their relationship in the perspective of

Pakistan have been discussed here. The analysis of external relationship between

taxes and investment also provides justification of the study. More specifically, this

chapter comprises brief introduction of tax policy and investment theories based on

political risk and country risk, economy of Pakistan, theories of FDI, foreign direct

investment strategy, tax policies in Pakistan, tax reforms in Pakistan, macro-

economic reforms/incentives, tariff structure, tax amnesty schemes, tax holidays in

Pakistan and trends in global perspective.

2.1 Tax Policy Theories

Keynes (1930) argued that by changing tax rates and expenditure, as main

instruments of fiscal policy, the governments can bring about economic development.

Fiscal policy is defined as combined measure of imposing taxes and varied

government expenditure to achieve macroeconomic objectives. By expanding fiscal

policy governments aim at achieving higher economic growth and employment while

by adopting expansionist fiscal policy measure, it aims to slow the economic growth.

Fiscal policy expansion is aimed at enhanced government expenditure and/or

reduction in taxes, whereas contracting policy is contrary to the earlier one which

involves reducing government spending and/or increasing tax rates.

24

Tax policies of a government aim at determining, which taxes and how and at what

rate these should be levied which have micro-economic and macro-

economic implications. Micro-economic impact brings in fairness principle i.e. whom

to tax and efficiency principle provides for manner of levy i.e. how to ley taxes.

Revenue generation is the major macro-economic impact of tax policy. Taxes usually

distort decisions which can have impact on the economic activity, therefore, any such

policy has to keep in view all such consequences. Moreover, taxes can be imposed in a

progressive or regressive manner which takes to the question of tax incidence. An ideal

or efficient tax system can be one which has zero or minimal distortionary effect.

Economists have come up with various theories of taxes and tariffs which are part of

tax policy, indicating the direction and purpose of fiscal policy of a country.

Conduit Theory states that corporate taxes should not be imposed on an investment

company in the same manner and same tax burden as done in case of other regular

firms because the investment firm further distributes its capital gains, interest and

profits to its customers/shareholders, unlike the regular firms with a different business

strategy.

Trickle-Down Theory suggests that financial benefits and incentives in capital gains

tax should be offered to large businesses investors and entrepreneurs because it will

enhance business activities in such enterprises and will also stimulate overall

economic growth. This theory is based on two assumptions: all citizens should benefit

from growth; and this growth would be generated with the resources and skills to

increase productivity.

Tariffs, as a revenue source, formed a major chunk of national revenue collection in

the past whereas this is now mostly used as fiscal tool in developed economies.

Revenue mobilization source has shifted to levy of income taxes, at personal and

25

corporate level. Tariffs are divided into two categories: Revenue ones are levied on

imports while protective tariffs are imposed on domestic produced goods. Tariffs are

a type of tax which is passed on to the consumers leading to higher prices of imported

goods with an outcome of reduced consumption. In this perspective, domestic

producers increase their output and consumption of domestically produced goods

rises.

Tax policies indicate the level, incidence and rates of taxation and also indicate tax to

GDP ratio changes and tariff structures. Direct and indirect taxes are used for resource

mobilization and fiscal readjustments including controlling the inflation in developing

countries. Theoretically, the tax policy focusing on providing incentives for

investment, both domestic and FDI, should be one of the top priorities of government

for economic growth. Indirect taxes are ones in which the burden of tax can be passed

on. Direct taxes are usually relaxed when country’s policy is to attract investment (e.g.

tax holidays, tax credits, tax rates reduction, tax exemptions and exemptions from

import duty for new investment and on related imports).

Tax policies (tax rates, burden of taxes, level of depreciation etc.) in a country affect

investment in any country. It affects the expected rate of returns which is the prime

motive behind investment decisions. Higher returns and lower tax rates and tariffs

immensely influence investment decisions. Tax policy instrument of lowering of

Corporate Tax Rates (CTR) has been found to be a significant fiscal measure used to

attract FDI. CTR is seen to cast greater impact in attracting FDI. Lower CTRs are

generally found to cast positive impact on the investment and encourage the foreign

investors, especially Multi-National Companies, to make investment and location

decisions in such countries.

26

2.2 Theoretical framework of Investment

Classical economics see investment and saving as one phenomenon. Therefore, saving/

investment are a desire to save/invest today to have more in the future, i.e. forego

consumption today and invest for higher return in future. Keynes, on the other hand,

looks at saving and investment as two different phenomena, where investment is

motivated by optimism. Investment in economics has quite a different connotation,

from the one used in general. In general we use investment as use of money to earn

income, while in economics; it means the activities that promote the capital stock in an

economy. This point of view is very critical because it is interlinked with the

consumption pattern of the economy. The decision about how much to save arises

from the decision about how to consume. Higher consumption means lower savings

which in turn means lower investments. Higher investment means higher capital stock

of the economy which in turn means higher GDP. Investment comprises of two key

components i.e. domestic and foreign investment.

2.2.1 Domestic Investment

Domestic investment is the investment by local companies in the domestic market.

Gross private domestic investment shows the level of physical investment in any

economy. It includes addition of new capital assets, inventories and replacement

purchases. Gross investment minus depreciation is the net investment. Investment is

one of the most unsteady components of GDP. There are three types of gross private

domestic investment which include:

Non-residential investment: It is the expense by firms on tools, machinery, and

factories.

Residential Investment: It is the expense on structures and equipment.

Change in inventories.

Gross private domestic investment shows the level of physical investment in any

economy. It includes addition of new capital assets, inventories and replacement

27

purchases. As defined earlier, gross investment minus depreciation is the net

investment. Investment is one of the most unstable components of GDP. There are

three types of private domestic investments: Non-fixed investment: Investment

spending by firms on capital assets like factories: Fixed Investment: Investment

spending on structures: Change in inventories. (Inventory: means goods produced but

kept in stock inventory for future sales).

2.2.2 Foreign Direct Investment

The concept of FDI can be defined as an entity established in one country controlling

ownership of a business enterprise in another country. FDI can be distinguished

through the element of “control” from portfolio foreign inflow of investment as this is

regarded as passive investment in foreign country. FDI largely consists of

establishing new assets, mergers, reinvestment of profits etc. FDI is often explained as

a long-standing investment in a foreign country. It has three modes like equity,

investment of retained earnings and loans within the company. FDI is the investment

made by someone , may be made either "inorganically" by obtaining an association in

the target country or "normally" by developing operations of a present business in that

country. Completely, outside direct theory fuses "mergers and acquisitions, gathering

new workplaces, reinvesting advantages earned from abroad operations and intra

association credits".

Types of FDI

Foreign Direct Investment is usually of three types as under:

i) Horizontal type FDI is the one serving local market. It is aimed at reducing

cost of supplies by investing in the plants producing supplies in that

market. This allows the investment to benefit from local resources.

28

i. Vertical FDI is one which acts for cost reduction by investing in low cost

countries. This allows the investors to benefit more from the cheaper raw

materials and labor available in that foreign market.

ii. Agglomeration includes utilization and benefitting from both horizontal

and vertical FDI simultaneously.

Factors Affecting Investment

Investment fluctuates very quickly because it is easily affected even on the basis of

mere rumors. People make investment decisions on the basis of expected returns.

General perception is a big factor during the decision making process for investments.

Uncertainty and incomplete knowledge of expected returns are important factors

influencing investment decisions. Introduction of new technology attracts investment,

as new technology usually brings in higher rates of expected returns. Inventions,

innovations and new products themselves are dependent on investments but they also

tend to generate more investment.

The political climate of a country is also very important for investors as it tells a lot

about the stability in the economy and consistency of policies. Strong political setup

and culture of entrepreneurship attract investment while unrest and political turmoil

cast adverse impact on investment. Economic policies are strongly linked with the

political climate of the country. Higher levels of income, greater capital stock in the

economy and population bulge are all factors that positively attract investment in any

economy. All these factors mean that there will be greater consumption in the

economy and this greater demand can only be fulfilled through greater economic

activity, and greater economic activity requires greater level of investments in the

economy.

29

2.3 Theoretical foundations

From the periods of Adam Smith and Karl Marx, it has been believed that investment

is the monetary growth stimulant as well as the basic cause of economic retardation

simultaneously. Scholars of economics have taken long to understand the concept of

investment and implications of its variations and growth. There have been typical

concepts of investment in capital assets and in equity capital. Classical economics see

investment and saving as one phenomenon where investment/saving is a desire to

save/invest today to have more in the future, i.e. forego consumption today and invest

for higher return in future. Keynes, on the other hand, looks at saving and investment

as two different phenomenon, where investment is motivated by optimism.

Capital theory. Fisherian theory of capital describes investment in purview of

optimal decision-making in the long run. Irving Fisher is pioneer in giving first proper

analysis of the viewpoint of wealth, revenue, consumption, investment and savings,

and the consequences of such decisions through market equilibrium and growth in

resource allocation.

Investment theory of firm. On micro level, investment entails the capital investment.

In neo-classical theory, the investment in equipment and plant occurs in economical

markets, focusing on one output from two inputs, usually classified as labor and

capital. This theory illuminates the association between investment and interest rates