Embed Size (px)

Citation preview

Inaugural 1 Year Bond Issuance

5.00% in USD4.50% in GBP3.50% in EUR

Expected Rating : A+ (ARC Ratings)

from aUSD500mio

Bond Issuance Programme

Listed in Luxembourg and authorised by the CSSF (Luxembourg Regulator)

1

2

Transaction Highlights

- Unique opportunity for investors to receive an above-market return from trade finance

- Investment grade bond structure that is independently assessed by ARC Ratings as being higher grade

than many well known corporate bonds

- Experienced management team

- Fixed, semi-annual returns from a bond that is listed and issued from a program authorised by the

Luxembourg Regulator (CSSF)

Termsheet and Timeline

Page 4

3

What is Structured Trade Finance?

Page 8

Our Strategy

Page 14

Transaction Structure

Page 19

Our People

Page 23

Termsheet and Timeline

4

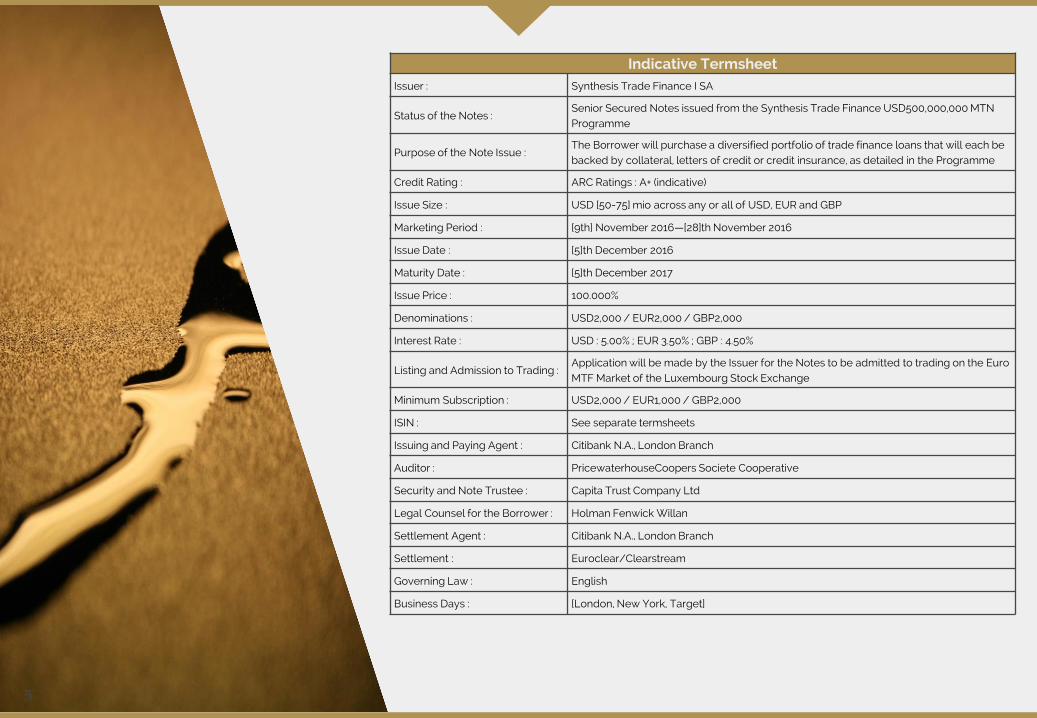

Indicative TermsheetIssuer : Synthesis Trade Finance I SA

Status of the Notes :Senior Secured Notes issued from the Synthesis Trade Finance USD500,000,000 MTN Programme

Purpose of the Note Issue :The Borrower will purchase a diversified portfolio of trade finance loans that will each be backed by collateral, letters of credit or credit insurance, as detailed in the Programme

Credit Rating : ARC Ratings : A+ (indicative)

Issue Size : USD [50-75] mio across any or all of USD, EUR and GBP

Marketing Period : [9th] November 2016—[28]th November 2016

Issue Date : [5]th December 2016

Maturity Date : [5]th December 2017

Issue Price : 100.000%

Denominations : USD2,000 / EUR2,000 / GBP2,000

Interest Rate : USD : 5.00% ; EUR 3.50% ; GBP : 4.50%

Listing and Admission to Trading :Application will be made by the Issuer for the Notes to be admitted to trading on the Euro MTF Market of the Luxembourg Stock Exchange

Minimum Subscription : USD2,000 / EUR1,000 / GBP2,000

ISIN : See separate termsheets

Issuing and Paying Agent : Citibank N.A., London Branch

Auditor : PricewaterhouseCoopers Societe Cooperative

Security and Note Trustee : Capita Trust Company Ltd

Legal Counsel for the Borrower : Holman Fenwick Willan

Settlement Agent : Citibank N.A., London Branch

Settlement : Euroclear/Clearstream

Governing Law : English

Business Days : [London, New York, Target]

5

3rd October

Synthesis Management

Limited receives MIFID

Licence from the UK‘s FCA

27th October

Synthesis Trade

Finance S.A. Bond

Issuance Program

receives formal

approval from

Luxembourg‘s CSSF

9th November –28th November

Synthesis Trade Finance

bonds are marketed

24th November –27th November

Expected size of the issuance

will be announced and

investors will be asked to

place firm orders for the

bonds

28th November

Final size of the bond issue is

determined and published

and investors will receive

their allocations from their

authorised distributor

9th November

Final Timeline for Bond

Issuance by Synthesis Trade

Finance I SA is agreed

28th November

Investors provide full

settlement instructions to the

Authorised Distributor

5th December

SETTLEMENT DATE

Investor Timeline

Borrower Timeline

6

Synthesis Trade Finance SA

Bond Issuance

Synthesis Trade Finance SA intend to issue the first in a series of bonds

during November 2016 following the approval of our bond programme by

the Luxembourg financial regulator, the CSSF.

The notes will be :

- Listed on the Luxembourg Stock Exchange

- With a minimum denomination of USD2,000 or equivalent

- Available for trading on the Euro-MTF market

- Assigned a credit rating that is expected to be A+

- Allocated an ISIN code and deliverable in Euroclear, Clearstream and

CREST

The proceeds of the notes will be used to finance short-dated, secured,

trade finance loans to a diverse pool of borrowers. Every loan will have

either a Letter of Credit or Credit Insurance backing it, as well as

appropriate legal charges over the financed goods. The underlying loans

will have no market risk because we are simply financing existing back-to-

back contracts. The goods themselves will primarily be commodities. The

loans will be originated by Synthesis Structured Commodity Trade Finance

Limited and purchased by Synthesis Trade Finance I SA.

This document gives an overview of our planned issuance programme.

Stock Exchange listed

Investment Grade

Retail-denominated

Secured

7

What is Structured Trade

Finance?

8

Structured Trade Finance keeps the global economy running. It

touches all of us each day.

Traditionally it has been a business controlled by banks, but in recent years more and more opportunities have arisen for non-bank participants to lend in the sector. By focussing on the transactions with the strongest security, it has become possible to create strong returns with minimal risk.

9

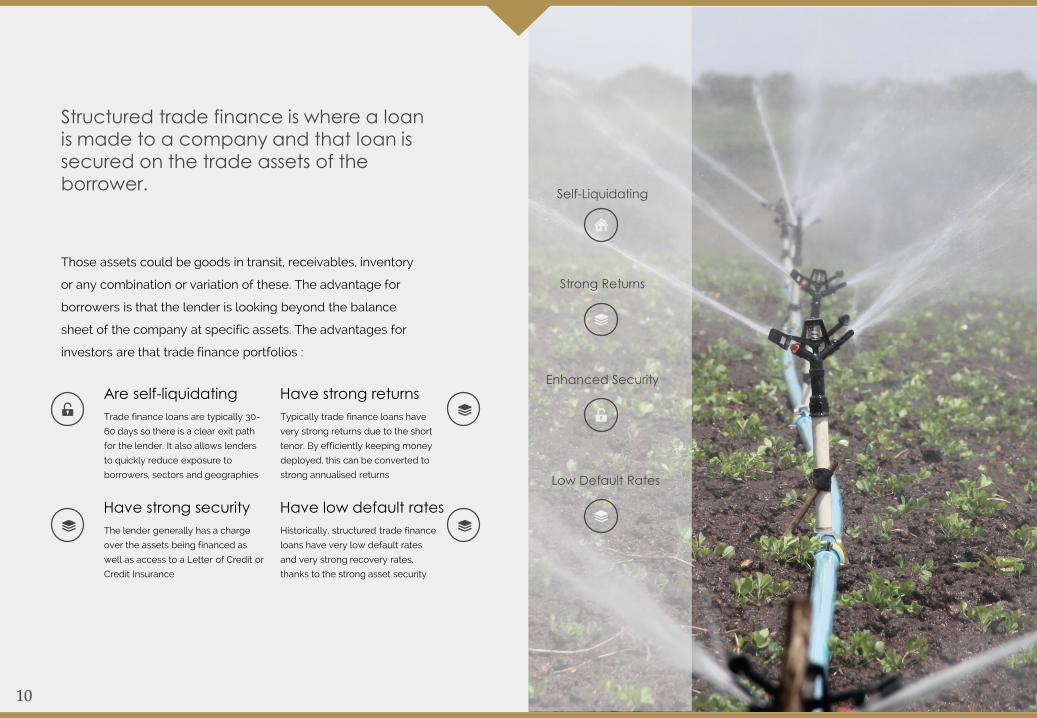

Structured trade finance is where a loan is made to a company and that loan is secured on the trade assets of the borrower.

Those assets could be goods in transit, receivables, inventory

or any combination or variation of these. The advantage for

borrowers is that the lender is looking beyond the balance

sheet of the company at specific assets. The advantages for

investors are that trade finance portfolios :

Strong Returns

Enhanced Security

Self-Liquidating

Low Default Rates

The lender generally has a charge

over the assets being financed as

well as access to a Letter of Credit or

Credit Insurance

Have strong security

Trade finance loans are typically 30-

60 days so there is a clear exit path

for the lender. It also allows lenders

to quickly reduce exposure to

borrowers, sectors and geographies

Are self-liquidating

Historically, structured trade finance

loans have very low default rates

and very strong recovery rates,

thanks to the strong asset security

Have low default rates

Typically trade finance loans have

very strong returns due to the short

tenor. By efficiently keeping money

deployed, this can be converted to

strong annualised returns

Have strong returns

10

$6 trillion

Despite global economic uncertainty, international trade continues to grow

SMEs continue to globalise, moving their goods in greater size,

across greater distances

However, as deliveries take longer, SMEs turn to

trade finance to bridge the cashflow gap between

production and payment

According to the International Chamber of

Commerce Report in 2011, default rates in trade

finance stood at around 0.02%, better than

investment grade bonds*

WTO Member Exports per year

>50%

SME share of that trade

80%

Of the SME share requires trade

finance

0.02%

Is the historical default rate

Structured Trade Finance in numbers

11

* http://iccreport2015

Product Total Exposure ($mio) Total Defaulted Exposure ($mio) Exposure-weighted Default Rate Transaction Default Rate

Export L/C 988,434 235 0.02% 0.01%

Import L/C 1,656,528 1,210 0.07% 0.08%

Performance Guarantees 1,023,561 1,154 0.11% 0.17%

Loans for Import/Export 3,154,407 5,323 0.17% 0.22%

Why is there an opportunity for investors in Structured Trade Finance?

Banks are less likely to provide trade finance credit lines now than in the past. There are several reasons for this. First, the operational costs of financing small transactions can be quite high as it can require large teams of people for a very small margin per transaction. Secondly, many transactions are cross-border and where a bank does not operate in both jurisdictions they may decline to take on such business. Finally, many trade finance transactions are for large amounts compared with the equity value of the company.

With banks less willing to lend to SMEs, despite the strong asset qualities in trade finance, an opportunity has been created for smaller, more nimble financial organisations to enter the market. With the right experience and understanding of global trade flows, a new breed of trade finance houses is emerging who can lend based upon assets, increasing security whilst maintaining strong returns.

The Global Financial Crisis created a gap

With the phased implementation of Basel III and tighter lending criteria from banks, many SMEs have lost access to the funding that they previously had.

12

13

Anatomy of a trade

Pre-production Finance

Inland Inventory Finance

Export port Inventory Finance

Marine Transport Finance

Processing Finance

Receivable Discounting

Transit Finance Transit Finance Transit Finance Transit Finance

Import port Inventory Finance

Cash in Advance Letter of Credit Cash against Document Open Account

Open Account Cash against Document Letter of Credit Cash in Advance

Supplier

Buyer

Most Secure

Least Secure

Our Strategy

14

Strong client base

B.Strong business

model

Strong management

A.

C.

Synthesis chooses who to lend to based on these

criteria

MARKET KNOWLEDGE

How do we choose our clients?

Here at Synthesis, a large part of our success within the group comes from working exclusively with borrowers who have a strong track record in their industry. We look for a minimum of three years of successful trading by the management team and a strong business model with good margins across their product range.

15

What goods do we finance?

Oil and Energy Products

Eg petrol, aviation fuel

With buoyant consumption of oil

products around the world and

long delivery times, there is

continual demand for funding

Soft commodities

Eg grains and beans

Soft commodities are often

seasonal which makes it harder for

small companies to raise finance.

Using our strong market

knowledge we can seek out

mutualy beneficial relationships

Hard commodities

Eg polymers, metals

Metals and polymers are businesses that

often have regular contracts that allow us

to remain well invested by continually

moving money from one contract to the

next

Semi-finished or finished goods

Eg generic pharmaceuticals

A proportion of our portfolio may

be used to finance non-

commodities as long as the

margins are strong and the

products are generic and liquid

16

Underlying asset

The underlying asset must be something that we can take control of, check the quality of and re-sell if necessary. It is always non-perishable

Credit Enhancement

The transactions that we finance are always backed by a Letter of Credit or Credit insurance from an investment grade counterparty

Loan-to-value

Typically we look at a “real” valuation of the asset in terms of what price it can be sold at in a variety of jurisdictions

Monitoring

Are we able to identify, monitor and exercise control over the asset at any point during the transaction?

Deal selection

In Structured Trade Finance the key to a successful portfolio is not just to choose the right counterparties, but also to select the deals with the right characteristics. Each commodity has its own idiosyncrasies, but in all transactions we seek verification of the value of the goods and will, where possible, take a charge over the goods. In the event of non-payment, we would liquidate the assets, hence our preference for non- perishable, generic commodities.

17

Inventory Finance

Transit Finance

Where goods need to move from one point to another, whether by ship, plane, road or rail, we help to provide finance for that movement.

Pre-Export Finance

Pre-export financing solutions allow buyers and off-takers to place orders and enter into contracts at advantageous rates.

Receivables Finance

Receivables financing differs from inventory financing in that the goods have already been sold but payment has not been made. In this case, the security for the lender is based upon the value of the unmade payments. Receivables financing is often done by “factoring”, where the lender purchases the invoices and becomes the legal owner of the debt, or “invoice discounting” where the lender becomes the borrower AND remains responsible for collection and enforcement of the debt.

Inventory finance is primarily for sold goods. It frees up valuable cashflow for smaller commodity sellers, allowing them to re-finance stock. Goods are evidenced by warehouse warrants/warehouse receipts

I

Transaction Types

18

TransactionStructure

19

Bankruptcy remoteThe SPV structure means

that each issuer is

independent of the others

and dependent only upon

its underlying investments

Excess spreadEach Issuer retains its

excess spread (the

difference between where it

borrows and where it

invests), less management

costs, to provide a buffer for

investors

Luxembourg regulated

All bonds are authorised by

the CSSF and application will

be made for them to be traded

on the Euro-MTF market

Pari passuAll bonds issued

with the same

maturity date are

pari passu and

senior secured

Synthesis

Trade

Finance I SA

Bond Structure

20

Loan

documensts

confirmed by

SSCTF

STF I SA purchases

loan and underlying

security from SSCTF

STF I SA secures

repayment and re-

invests the

proceeds

Loan

originated

by SSCTF

Loan

offered to

STF I SA

SSCTF monitors

loan performance

for its duration

Securitisation Structure

As a securitisation vehicle, Synthesis Trade Finance I SA (STF I SA) has no ability to make loans directly. This provides additional protection to investors because loans are originated by a separate company with a separate decision making process (Synthesis Structured Commodity Trade Finance Ltd) and only purchased with the approval of the separate board of Synthesis Trade Finance SA.

21

Risk Mitigation

Key Risk Factors

Risk of non-payment

- Synthesis only lends to companies or management teams with a significant track record in the relevant commodity

- Both the arranger of the deal and the debtor are required to pass our KYC process

- Each transaction will have in place a Letter of Credit or Credit Insurance to act as a safeguard

Risk of rejection of goods- Goods are checked for quality where necessary and certified by an

independent inspector before the loan is extended

Country Risk

- In conjunction with leading trade finance law firm Holman Fenwick Willan, Synthesis Trade Finance SA continually monitors any potential risks, in particular those relating to currency restrictions, sanctions or embargoes

Commodity Price Risk

- Synthesis Trade Finance SA does not engage in transactions where the return is in any way linked to the price of the underlying goods. Each transaction will have a sales contract at a pre-agreed price so that the return is fixed

- In the event of non-payment by a borrower, Synthesis Trade Finance SA would first look to enforce the terms of the contract. It would then seek to sell the commodity to another buyer. It is only after that that they would seek recovery through the Letter of Credit or Credit Insurance. By concentrating on fungible, hard commodities, the risk of depreciation of the asset is minimised

Risk of Documentary Failure- Facility Documentation is arranged by Holman Fenwick Willan and

all transactions are documented by experienced professionals

All foreign exchange risk will be hedged on a transactional or full portfolio basis

The bond will hold a well diversified pool of loans (minimum 15 different borrowers) to protect investors

The bond will be diversified across asset classes in order to minimise risks of over-exposure

22

Our People

23

Synthesis Structured Commodity Trade Finance Ltd Management

David

Phipps

Having worked in the financial industry

for almost 30 years, David has built up

significant and broad experience in

Commodity Risk Management,

Commodity Trading and Financing of

Commodities. David has held senior

positions at investment banks,

including Head of Commodities at

ABN AMRO Bank NV, Co-Global Head

of Commodities at ETD UBS AG, and

CEO of a London Stock Exchange

listed trading company. David has

extensive knowledge of market and

credit risk management including risk

mitigation products in physical, on

exchange and OTC products.

Frances

Walsh

Frances is a highly experienced

structured trade financier with

comprehensive knowledge of and

extensive practical experience in

providing finance within the

international trade sector. Frances’

expertise encompasses traditional

trade finance, factoring and forfaiting

in the export markets. This experience

is complemented by a strong legal

background and 25 years’ exposure to

the international banking and finance

markets, having held senior positions

with UK-based firms London

Forfeiting Company, BCI Soditic Trade

Finance Company, Fairfax Gerrard and

Trade Finance Partners Limited,

latterly as Structured Finance Director.

Andy

Sweeney

Andy has over 16 years of experience

in debt capital markets, all gained

working in major global investment

banks. He began his career at

Citigroup with a focus on raising short

term finance for companies via the

commercial paper market.

Subsequently he worked in the note

syndication teams at RBC Capital

Markets and Mizuho International,

advising banks, governments and

corporates on issuing notes across a

range of currencies for periods of

anything from one year to fifty years,

and in sizes ranging into the billions of

pounds sterling. Andy graduated from

Cambridge University with an MA

(Hons) in Law

24

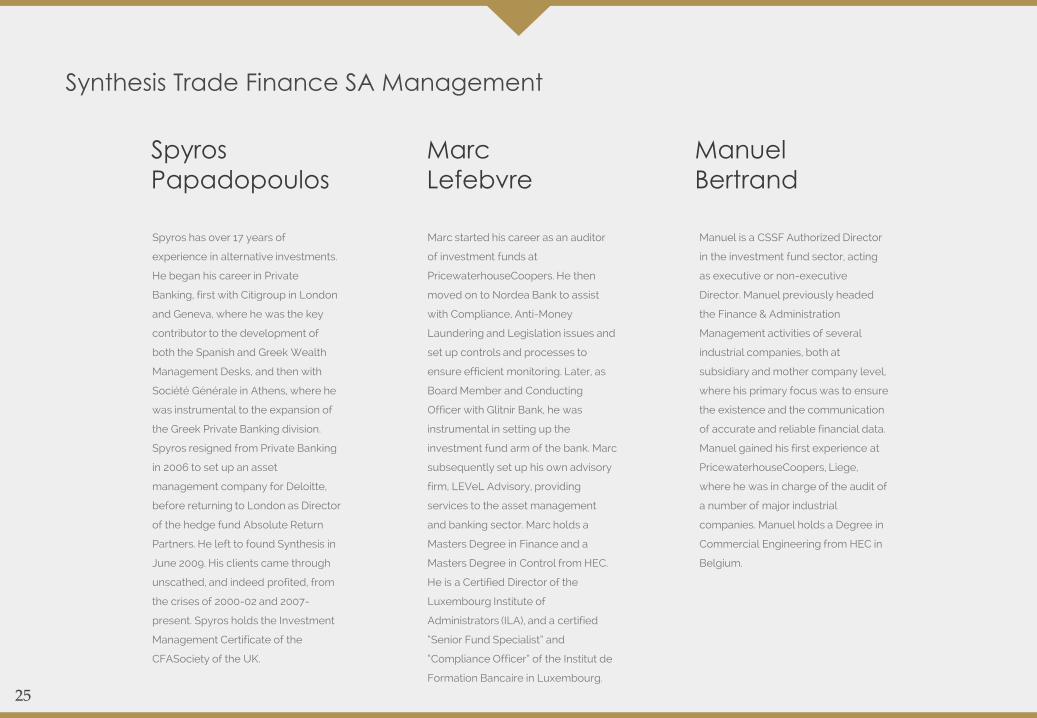

Synthesis Trade Finance SA Management

Spyros

Papadopoulos

Spyros has over 17 years of

experience in alternative investments.

He began his career in Private

Banking, first with Citigroup in London

and Geneva, where he was the key

contributor to the development of

both the Spanish and Greek Wealth

Management Desks, and then with

Société Générale in Athens, where he

was instrumental to the expansion of

the Greek Private Banking division.

Spyros resigned from Private Banking

in 2006 to set up an asset

management company for Deloitte,

before returning to London as Director

of the hedge fund Absolute Return

Partners. He left to found Synthesis in

June 2009. His clients came through

unscathed, and indeed profited, from

the crises of 2000-02 and 2007-

present. Spyros holds the Investment

Management Certificate of the

CFASociety of the UK.

Marc

Lefebvre

Marc started his career as an auditor

of investment funds at

PricewaterhouseCoopers. He then

moved on to Nordea Bank to assist

with Compliance, Anti-Money

Laundering and Legislation issues and

set up controls and processes to

ensure efficient monitoring. Later, as

Board Member and Conducting

Officer with Glitnir Bank, he was

instrumental in setting up the

investment fund arm of the bank. Marc

subsequently set up his own advisory

firm, LEVeL Advisory, providing

services to the asset management

and banking sector. Marc holds a

Masters Degree in Finance and a

Masters Degree in Control from HEC.

He is a Certified Director of the

Luxembourg Institute of

Administrators (ILA), and a certified

“Senior Fund Specialist” and

“Compliance Officer” of the Institut de

Formation Bancaire in Luxembourg.

Manuel

Bertrand

Manuel is a CSSF Authorized Director

in the investment fund sector, acting

as executive or non-executive

Director. Manuel previously headed

the Finance & Administration

Management activities of several

industrial companies, both at

subsidiary and mother company level,

where his primary focus was to ensure

the existence and the communication

of accurate and reliable financial data.

Manuel gained his first experience at

PricewaterhouseCoopers, Liege,

where he was in charge of the audit of

a number of major industrial

companies. Manuel holds a Degree in

Commercial Engineering from HEC in

Belgium.

25

DisclaimerThis communication is being furnished solely on a confidential basis to the recipient. This communication is directed at persons having professional experience in matters related to investments and any investment or investment activity to which this communication relates is available only to such persons or will be engaged in only with such persons (or other persons to whom such investment can lawfully be made available or with whom such investment activity can lawfully be engaged). If you do not have professional experience in matters relating to investments you should not rely on this communication. Neither this Communication nor any of the associated documents may be reproduced, re-transmitted or further distributed to any other person or published, in whole or in part, for any other purpose than that stated above. The information in this document, which is in draft form and incomplete, is subject to updating, completion, revision, further verification and/or amendment. In particular, the documents refer to certain events having occurred which have not yet occurred at the date these documents are made available, but which are expected to occur prior to the publication of an approved prospectus in final form. Recipients of this Communication (or any of the associated documents) who are considering purchasing or subscribing for Notes in any of the issuers are reminded that any such purchase or subscription must be made only on the basis of information contained in the approved prospectus its final form, which may be different from the information contained in this document. Notes may not at this time be offered by any of the issuers directly to the public. Neither this Communication nor any of the attached documents constitutes an offer of Notes. By accepting delivery of this Communication, you agree to keep it and its content (including the attached documents) confidential, and not copy, publish, distribute, pass on or disclose any of it except with the prior written consent of Synthesis. To the extent permitted by applicable law and regulation, Synthesis Trade Finance S.A. and its affiliated companies expressly disclaims and excludes any and all liability that may be based on this communication and the attached documents, any errors in it/them or omissions from it/them.

26