Embed Size (px)

Citation preview

Improving Financial Inclusion through New Channels and Innovative Products A Case Study of Malaysia

Kameel Abdul HalimDeputy Chief Executive of Bank Simpanan Nasional

Seminar on SFIs in the New EditionTuesday 23 August 2016Hosted by Bank of Thailand

Malaysia: At a glance

DFIs in

MalaysiaBSN championing

financial inclusion

agenda

1 2 3

Agenda

Channels

4

Products

5

2

3

Malaysia at a glanceQuick Facts

Household income (B40*)

LabourForce Unemployed

Income per capita

2.7m

Urban Rural

*B40 is bottom 40% that household income less than RM3,855 (based on household survey 2014)Source: Department of Statistic Malaysia

14.7m

$10,570501.8k

@3.4%

63% : 37%

Malaysia at a glanceQuick Facts

Financial Access Points4

1 Department of Statistics Malaysia2 Indexmundi.com

3,4,5 BNM Financial Stability and Payment Systems Report 2015

5 Where 1.00 reflects full inclusion

30.7 mil

Statistics 1

50.7 62 71

1991 2000 2010

Urbanization

Population

27.3Median Age

Kelantan: 42%

Pahang: 50.5%

Perlis: 51.4%

Sarawak:53.3%Sabah:54%

Terengganu: 59.1%

States with urbanization level below 60%

4.5

Access points per 10,000 adults

5.1 ATM

2.3 CDM

2015: 19.8m / 7.3m2011: 11.9m / 1.6m

Internet & Mobile Bnkg Penetration

Rural population (% of total population): 25.30 as of 20152

Transaction

Volume (Mil)

Internet

Banking

Mobile

BankingATM Total

Fund transfer 237.7 17.1 53.1 307.9

Bill payment 74 5.1 1.9 81

Investment in

share & unit trust6.6 0 0.1 6.7

Re-load 24.9 6.9 3 34.8

Card & loan

repayment26 2.2 8.4 36.6

Total 369.2 31.3 66.5 467

Payment3

Financial Inclusion Index score 5 for the general

population in Malaysia

0.90 in 2015

4

Development Financial Institutions (DFI) in Malaysia under the purview of BNM

Specialized financial institutions (sectorial & universal based)

established by the Government with specific roles to play

Bank Simpanan Nasional SME Bank Malaysia Bank Kerjasama Rakyat

Export-Import Bank of Malaysia Agro Bank Malaysia Bank Pembangunan Malaysia

To develop and promote growth of targeted strategic

sectors of the economy

To achieve socio-economic objective

To complement the role of banking institutions

5

DFIs comes under the purview of the central bank through the Development Financial Institution (DFI) Act 2002

Promoting Financial Inclusion

Enhancing intermediation capability

Financial system that provides basic financial services that are affordable, appropriate, convenient and accessible to all

Financial system that effectively and efficiently allocate resources to facilitate the transformation of Malaysia towards a high income economy

Financial Sector Blueprint

Goals of the New Economic Model

Institutional Arrangements

Advisory

• Banking system

• DFIs• Venture capital companies

• Leasing & factoring companies

• Cooperatives

• Government agencies

• Money Lenders

• Pawn Shops

Financing

Credit Guarantees

• SME Corp and SME Bank

• Government. agencies

• Credit Guarantee Corporation

Rescheduling & Restructuring

• Small Debt Resolution Scheme

6

How do DFIs fit in?

7

DFI, 8%

Islamic Banks, 20%

Commercial &

Investment Banks, 72%

Financial Landscape Total Assets (as at December 2014)

Malaysia DFIs have made significant stride since 2002

45.20%

23.20%

14.80%

6.10%

5.50%

5.10%

BR

BSN

BPMB

Agro Bank

EXIM

SME

Total assets in 2014 constitute8% (RM197 bil/USD49 bil) ofbanking sector assets (3%:2002)

Tap the capital markets through Ringgit and Foreign currency bond and sukuk issuances

Regulated by a regulatory framework that emphasises on strengthening capacity and capability• Capital position & asset quality• Enhanced governance standard &

practices

The DFI Act 2002 carries BNM’s policy intent

• As the regulatory framework for DFIs and continue to reflect their unique characteristics.

• Ensure DFIs continue to be safe and sound.

• Lines of accountability and co-ordination with clarity on the roles of Minister, stakeholder Ministries and BNM in regulating DFIs;

• Boundaries to avoid regulatory arbitrage in the areas of market conduct, Shariah and the enforcement framework in the financial services industry; and

• Operations of the law for greater efficiency and effectiveness.

Principle

Outcome

8

In collaboration with stakeholders, BNM will continue to balance multi objectives in regulating and supervising DFIs

Proportionate approach

Ensure sustainable financial performance

Promote stronger risk management practices

Recognize developmental role mandated by Government

Regulatory approach based on suitability, discretion and

readiness

Supervisory approach at par with other institutions

Sound financial performance

Improved governance, greater professionalism and human capital capabilities

Recognize unique role in the financial system

Continue to deliver developmental mandates by serving the targeted sectors

Proportionate in application of capital standards and access to market (agent banking)

Balanced outcome

9

Guidelines Policy objective

Agent BankingTo facilitate the implementation of agent banking in underserved areas, in a reliable, safe andsustainable manner whilst safeguarding the interest of customers.

Microfinance framework (by National SME Development Council)

To encourage financial institutions to provide Microfinance, design right products to meet theneeds of Microenterprises and create wide spread awareness on availability and benefits ofMicrofinance.

Capital Adequacy Framework (also known as the Risk Weighted Capital Adequacy Framework)

To maintain adequate and strong financial capacity to undertake business activities in supportingmandated roles. Also to further strengthen and preserve the capital position of the DFIs.

Risk GovernanceFocuses on applying the principles of sound corporate governance to the assessment andmanagement of risks to ensure that risk-taking activities are aligned with an institution’s capacityto absorb losses and its long-term viability.

Introduction of New ProductsImprove the time-to-market for financial institutions to introduce new products or to effectchanges to existing products, promote sound risk management and strengthen financial capability.

Best Practices for the Management of Credit Risk for DFIs

To lay the initial foundation towards upgrading the prudent conduct of credit granting activities ofDFIs in Malaysia.

Selected Bank Negara Malaysia (BNM) Guidelines & Framework for DFIs

10

Established by the Government of Malaysiawith the following objectives:

To promote and mobilise savings,for the general public particularlyfrom small savers;

To inculcate the habit of thrift andsavings; and

Financing the economic development of the nation.

Establishment of BSN

11

12

BSN by the numbers

766

ATMs

7,237

Employees

403

branch

7,017

Agent Bank

RM31bil

(USD 7.8b)

Total assets

> 9mil

Customer base

46

MFCs

93

VTMs

10

Mobile Units

As of June 2016

51%

Market leader in MF

Government & Central Bank driving national financial inclusion agenda

2005

2006

2009

2011

2012

2014Basic banking services;No frills low cost savings account

Micro-financing framework

Central Bank of Malaysia Act 2009

*Financial Sector Blueprint 2011-2020

Agent Banking

Account ownership for adults from the poorest 40% of householdsin Malaysia increased from 50% to 76%

Malaysia's financial inclusion grew from 66% in 2011 to 81% in2014.

Financial Sector Masterplan 2001 - 2010

*An integrated approach:• Financial inclusion for greater shared prosperity• Effective and efficient intermediation 13

Agent

BankingRemote

Branches

Channels & Products

Microfinance

BSN is embarking into new channels and technology to further improve financial inclusion and to tap various customer segments…

Mandated Roles 14

1 2 3 4

15

Song , Sarawak

• Accessible only via express boat from Sibu• District population as of 2010: 20,046• Began operations: 23 Apr 2009 with 1 Branch

officer & 3 Tellers• As of July 2016: Total deposit stood at RM9.8 mil

(USD2.45mil)

Remote AreasMaking lives better

PlaceBranch opened

year

Population (Census year)

Deposit Size (RM mil/USD

mil)as of July 2016

Distance from KL

Pulau Tioman 2009432

(2008)8.220/2.06 350.3 km

Kota Sarang Semut, Kedah

2010 N/A 9.840/2.25 420.7 km

Beluran, Sabah 2011104,484

(20103.507/0.88 3,981.5 km

Kinabatangan, Sabah 2011146,987 (2010)

5.104/1.28 4,039.3 km

CPI Jeli, Kelantan 201242,882 (2009)

6.068/1.52 360.7 km

Tambunan, Sabah 201635,667 (2010)

0.807/0.20 3,810.8 km

USD Conversion Rate: 1 USD equals RM4

1. Belaga is a small district in Sarawak of EastMalaysia with population as of 2010: 37,102.

2. The nearest town where banks are available isabout 100 km away i.e Town Bintulu, 6 hoursaway via gravel road or 5 hours by river.

3. Dependent on their heads of community orfriends to do banking on their behalf.

4. BSN opened the branch in 2011. As of July 2016,total deposit stood at RM 6.7mil (USD 1.68mil).

The story of Belaga

16

Agent Banking (Banking Beyond Branches)Overview

Aug 2012July 2012Jan 2012

BSN: Pioneer of Agent Bankingmodel in Malaysia• Self-initiated• Started with 200 agents• In support of Malaysian government’s call to

elevate the standard of living of those in ruralcommunities

Agent Banking Framework• Ensure sound & prudent risk

management to minimize riskprofile of FIs as a result ofdependence on 3rd parties

• Safeguard interest of customers• Areas of governance and oversight,

management of agents, customerprotection, awareness andeducation

Pilot run by 3 banks• 2,322 agents• More than RM1mil (USD250k) transactions

worth more than RM190 million (USD48 mil) has been conducted

2015 Enhanced Agent

Banking Regulatory

Framework*

*Effective for 5 years from 30 Apr 201517

Agent Banking (Banking Beyond Branches)As a conduit to greater financial inclusivity

• Financial services through agents or third party intermediaries.

• Prior to the introduction of the Agent Banking service, only 40% of thetotal 837 mukim (sub districts) in Malaysia had been served 1. As of Dec2015: 96% enjoying the convenience of banking services.

• Currently there are four banks in Malaysia offering Agent Banking : BSN,Maybank, AgroBank and RHB.

79%

13%

6%2%

Retail agents Structured agents

Post offices Co-operatives

4,120

6,902

End 2012 End 2015

Number of Agent Banks & Transaction in Malaysia

3 mil (USD 750k)

63 mil(USD 16mil)

Ma

inly

su

pp

ort

ed b

y R

eta

il A

gen

ts in

Ma

lays

ia

Achievements

Cheaper Cost

Scalability

Reach

• Under-served communities 1

• Non-urban areas 2

• Non-economical areas 3

• Under-served areas 4

1 Less than 5 financial touch points2 10 km radius away from town area3 Low business activity areas4 Less than 2,000 people with no financial access

90% Agents by BSN

1 Asian Link: Going Beyond the Conventional (2013)18

Summary of Agent Banking Guideline 2015

Agent Banking Services

• Conducted in identified districts only

• Real-time basis & within business premise

• Daily cash withdrawal • Prohibited services

Agent selection, conduct & monitoring: FIs develop governance and internal control & to establish contract with agents for effective oversight1

Monthly reporting to BNM on transaction statistics, agent details & police reports2

Implement operational requirements (e.g. IT infrastructure) & measures to safeguard customer protections (e.g. display of national Agent Bank logo)

3

National logo

FI logo

http://www.bnm.gov.my/guidelines/08_agent_banking/01_agent_banking_20150430.pdf

Facilitate a reliable, safe and sustainable Agent Banking

19

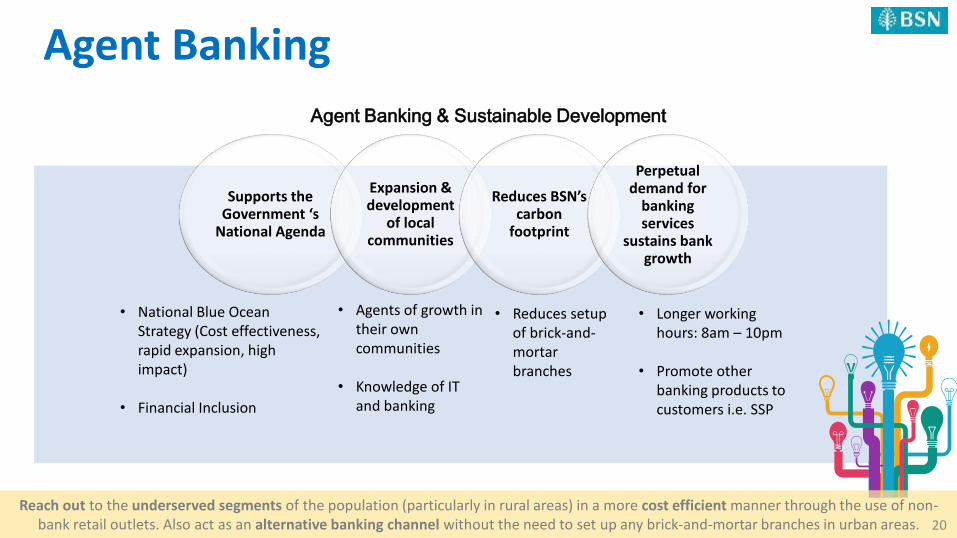

Agent Banking

Supports the Government ‘s

National Agenda

Expansion & development

of local communities

Reduces BSN’s carbon

footprint

Perpetual demand for

banking services

sustains bank growth

Agent Banking & Sustainable Development

• National Blue Ocean Strategy (Cost effectiveness, rapid expansion, high impact)

• Financial Inclusion

• Agents of growth in their own communities

• Knowledge of IT and banking

• Reduces setup of brick-and-mortar branches

• Longer working hours: 8am – 10pm

• Promote other banking products to customers i.e. SSP

Reach out to the underserved segments of the population (particularly in rural areas) in a more cost efficient manner through the use of non-bank retail outlets. Also act as an alternative banking channel without the need to set up any brick-and-mortar branches in urban areas. 20

Agent BankingMechanics

Deposits

Fund withdrawal

Fund transfer

Opening of savingsaccount

Receiving loan/financing repayments

Facilitate bill payments

Formless (MyKad-based)

Automated

Wireless GPRS

Simplified process

Increased coverage

Transaction Switch / Middleware and BSN

Host / System

GPRS Network

P.O.S Terminal

Customer and Agent

21

8,265,052

13,036,438

18,398,914

2013 2014 2015

Agent BankingExperienceCosts Branch

ATM-Off Premise

Agent Banking

Set-up Cost(One-off)

MYR500,000(USD125,000)

MYR45,000(USD11,250)

MYR5,000*(USD1,250)

Yearly Operating Cost

MYR250,000(USD62,500)

MYR40,000(USD10,000)

MYR2,000(USD500)

Cost Overview

49%

EB growth in transaction

CAGR*Includes POS Terminal & Point of Sales Material such as flyers

• 450 transaction per agent per month

Breakeven point

Monthly operating cost: • Fixed cost (GRPS Access Fee)• Variable cost (Commission paid to agents, thermal

paper, marketing expenses)

22

Agent BankingExperience

No of Agents by BSN

BSN will have 5,000 agents by 2015”– Prime Minister (October 2012)

“ ”Served: 5,533Underserved: 1,469Unserved: 15

Peninsular Malaysia : 5,795 (83%)East Malaysia : 1,222 (17%)

Sub-urban /Rural: 5,283Urban: 1,734

RM 81.3 mil

RM 5.7 bil

Transactions

Value

Bill payment65%

Prepaid top-up24%

Cash deposit5%

Cash withdrawal5% Others

1%

Grocery shops51%

Telcos17%

Others32%

23

*

* As of June 2016

ChallengesExperience

Quality of Agents: Recruitment Guideline

Communication: SOPs, instructions & promotions

Ground Support: Coordinators, State EB,

Operations Support

Close Monitoring: Business & Operations

Performance

24

Quality of Agents: Recruitment Guideline

No. Item Descriptions

1 Types of business a. Personal (individual / Sole Proprietorship) b. Partnershipc. Private Limited Company (Sdn Bhd)d. Public Limited Company (Berhad)

2 Business Period a. Operating more than 12 months

3 Location a. Number of population approximately 2,000 (not applicable for unserved)b. The distance not less than 5km radius from BSN branchesc. Premise in good conditiond. The distance between the other agents not less than 10km radiuse. GPRS coverage (minimum requirement)

4 Operating Hours a. Daily basis (8.00am – 10.00pm)

5 Others (dataverification with third parties)

a. Business Search / Credit Reference (BRIS)b. Police reportc. Blacklisted CCRIS

25

● Agent recruitment and termination (administration)

● Monitoring of agents performance

● Monitoring and analysis the suspicious transactions

● Agent selection and interview

● Agent appointment / termination

● Agent supports (marketing, operations and business)

● Agent Helpdesk

● Monitoring of errant agents (manipulation / split transaction)

● Account reconciliation (finance)

HQ Coordinators State EB Staff Operations Support

26

Ground Support: Coordinators, State Agent

Bank, Operations Support

Daily monitoring via system

(web module)

Identify suspicious transactions i.emanipulation /

split

Details investigation

Follow up action taken

• Auto generated daily report on suspicious transactions by agents

• Verify the suspicious transactions by referring agent’s transactions detail

• Visit the suspected errant agents

• 1st attempt: Verbal reminder and warning

• 2nd attempt: Issuance of 1st warning letter

• 3rd attempt: Suspension of agent commission and/or termination

27

Close Monitoring: Business & Operations

Performance

EB Award Night

Outreach programme

EB Campaigns

28

Communication: SOPs, instructions &

promotions

Agent BankingMoving forward

Moving Forward

New products/services

Negotiate New Rate to Billers

Reduce Operating

Costs

Charging Customer

Process Improve-

ment

Technology Enhancem-

ent

• Remittance• Micro Insurance

• Utilities company i.e to increase fee income to RM1.00

• Restructuring agent commission structure

• Online real time payment i.e TM & Astro

• Barcode scanner for bill payment

• Bill payment transactions via cash

• Multi-devices• Enable to

support 3G

29

Synergy between agent banking and microfinancing

30

MicrofinanceOverview

20%

3%

Micro

Services (80%)Manufacturing (57%) Agriculture (56%)

77%

MSMEs1

1SMEcorp.2 World Bank affiliate, Consultative Group to Assist the Poor (CGAP).3&4 BNM Financial Stability and Payment Systems Report 2015.

• Development financial institutions

(DFIs) to provide sustainable

microfinance.

Bank Simpanan Nasional

(National Savings Bank) has

been mandated to provide

microfinance.

• Banking institutions to play a key

role in microfinance.

• Financial institutions complement

the existing Government

sponsored programs (e.g. Amanah

Ikhtiar Malaysia, Tekun).

Microfinance Institutional Framework

“Financial services for poor and low-income clients offered bydifferent types of service providers”2.

Currently offered by 10 banks.

Financing approved: RM3.1 bil (USD775 mil) for more than 185,000accounts (Since inception in 2006until end-2015) 4.

Micro Enterprise Fund(MEF): RM200 million(USD50 mil) revolvingfund by BNM3.

Several Ministries &Agencies i.e. Agro providesmicrocredit schemes.

31

Capturing the underserved market & segmentsMainly from lower income businesses 1,

but viable.

Faced difficulties 2 in obtaining financing/loans due to:

• Lack of income evidence• No collateral• Insufficient documentation

Impact of not assisting them:• Impedes growth of ME• Socio-economic problems

perpetuating poverty cycle, turning to loan sharks for help.

1Sales turnover less than M300,000 OR full time employees less than 5.2 Only 17.4 % of micro establishments relied on financial institutions for financing. 32

33

Market Share

Total Industry: RM930 mil (USD 233mil) 1

(As at 31 May 2016)

BSNRM472 mil

(USD 118 mil)

10 Banks, RM458 mil

(USD 115 mil)

Since 2007, BSN has approved a total of RM1.2 bil (USD 0.3bil) to more than 50,000 customers

• 46 Dedicated MF Centers;• 110 MF Business Relationship Officers

to specifically market and process loans.

BSN championing Microfinance in Malaysia

1 BNM

MicrofinanceExperience2007-2010

BSN launched MF Program on March 15, 2007

Target at all viable

Malaysian owned MEs

2011

Target business operated by New Chinese

Village Residents

Funded by Government

2012-2016

Target Night Market traders & viable MEs

Microplus product up to

RM250k

Developments

Besides provision of credit facilities, BSN also extends:

Access and opportunity to save MF customers are required to maintain savings accounts

with the bank, with regular monthly deposits Insurance/Takaful Coverage

34

01 02 03 04 05 06

Ch

arac

ter

len

din

g

No

pro

per

bu

sin

ess

pro

spec

tIr

regu

lar

Co

llect

ion

s /

Rep

aym

ent

Bu

sin

ess

Via

bili

ty

Poo

r fi

nan

cial

m

anag

emen

t

Illeg

al O

per

ato

r /

No

Op

erat

ing

Lice

nse

ChallengesExperience

Issues & Challenges byMicrofinance Institution

Issues & ChallengesMicro Entrepreneur

• Lack of marketing skills

• Inferior & Outdated

Technology

• Lack of Access To

Financing

• Inadequate Managerial &

Operational Expertise

35

MicrofinanceAspiration

Agent Banking

(EBB)

Micro Finance

(MF)

SynergyProviding MF to the appointed EBB for

business expansion

Existing MF customers to become EBB

MF Financial Inclusion in Context of Current Strategic Direction

36

37

Masnah JinulMonthly sales: ↑ 376% Employed: 2 workers

Goo Boon Tat

Pre Post

Microfinance success stories

Monthly sales: ↑ 198% Employed: 3 workers

Mandated products as part ofFinancial Inclusion

38

Micro Savings

Long-term contractual savings for the period of 5 years

Offers fixed interest rate +‘Anniversary Bonus’

Registered under eKasih aged 18 years old & above with

monthly household income of ≤RM2,300 (USD575)

1 As percentage from no of participants in road shows

Collaboration with Gov. Agencies (NGOs) and Ministries to introduce contractual savings product

• Part of Financial InclusionFramework by BNM

• Bundled with lifemicro-insurance

• Offered by two banks:BSN & Maybank

BSNs achievement: 55% 1 take-up rate as of Dec 2015

39

DepositsSchool DepositObjective:

• Mandated Role: BSN Corporate Social

Responsibility to help School collect donation

via carnival sales.

• Getting to know the social through educationmedium that is 1Malaysia oriented.

Schools (Apr-Nov 2015)

54 BSN Involvements

At least

4 Schools in each state

BSN Deposit Product RateCommercial

bank*

BSN GIRO (Individuals)

0.25% - 0.85% -

BSN Basic Savings 0.25% - 0.95% 0.25% - 0.55%

Premium Savings Certificate

0.25% - 0.85% -

School Deposit 0.35% - 1.70% -

Deposit Pricing

• Savings scheme in the format of a competitionencouraging national primary/secondaryschool student to save and participate.

40*CIMB Bank

Other Mandated Deliverables

Designed to improve opportunities & help change the lives of Malaysians

RM300m/USD75m

RM100m/USD25m

RM200m/USD50m

Loans for school buses & taxi drivers hire purchase

Creativeindustries

Equity schemes

Chinese New villages

Housing for married youths

Micro Finance

BNM Fund (Teman Mesra) 1.5%

RM50m/USD13m

RM300mUSD75m

Government/Regulator assistance

Bank internal fund 41

First in Malaysia

Enabled with videoand audio, withsignature pads andcard identificationfor securetransactions31 branches are equipped with

VTMs sharing, the expertise of 448 tellers.

Embrace technology to increase quality of services

Balances workload between high and low traffic branches

Virtual Teller Machine

42

Riskier, costly

Mandated products

Balancing between sustainability and mandate

Profit for bank

Retail products

Support Government Initiatives

Generate return for stakeholders

Attract customers

43

Continuous support from Government & Regulator is essential in driving Financial Inclusion agenda

Government funds/grants i.e. New Chinese Village Residents Microfinancing

Basel 1

Lower charge to capital i.e. Youth Housing Scheme

01 01

02

Leeway by regulatorSource of funding

44

Concluding Remark: First-mover Advantage

Competitive Advantage

in Agent Banking &

Microfinance

01 Economies of scale

02 Cost-efficient

03 Learning curve

04 Market share

Single/less players in the field a few years back…

Realizing the benefits, Commercial banks start entering the field…

45

46

Concluding Remark: Using Technology for Financial Inclusion

Huge initial

CAPEXinvestment

Cheaper in the long run

Creates Customer

Segmentation

141%Mobile penetration (total mobile users to population) 1

63%Access Internet via phone2

Secular (Customer Neutral)

Technology has always been at the core of Financial Inclusion – it has been ‘the’ driving force

• Mobile wallet• Vodafone M-Pesa

1 TheStar news paper Online, Dec 20152 Malaysian Communications and Multimedia Commission Survey (2014)

Concluding points

Favourable and flexible policies

Continuous efforts by the Central Bank

Support national agenda Product innovations Staying abreast with

market

Financial InstitutionsRegulatorEnsure economic sustainability & increase overall stability of financial system

47