Embed Size (px)

Citation preview

Improving Access to Financial Services in Indonesia

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

THE WORLD BANK OFFICE JAKARTA

Indonesia Stock Exchange Building, Tower II/12-13th Fl.Jl. Jend. Sudirman Kav. 52-53Jakarta 12910Tel: (6221) 5299-3000Fax: (6221) 5299-3111

THE WORLD BANK

1818 H Street N.W.Washington, D.C. 20433 USATel: (202) 458-1876Fax: (202) 522-1557/1560Email : [email protected] : www.worldbank.org

Printed in April 2010

Improving Access to Financial Services in Indonesia was produced by staff of the World Bank with fi nancial support provided by the Dutch Government. The fi ndings, interpretations and conclusions expressed in this report do not necessarily refl ect the views of the Board of Executive Directors of the World Bank or the governments they represent.

The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denomination and other information shown on any map in this work do not imply any judgment on the part of the World Bank concerning the legal status of any territory or the endorsement of acceptance of such boundaries.

Improving Access to Financial Services in Indonesia

Improving Access to Financial Services in Indonesia2

ForewordIn many developing countries less than half of the population has an account with a formal fi nancial institution. The Indonesian situation is only marginally better - just about half the population has such access. Recent developments in theoretical and empirical literature have shown that providing access to fi nance for a greater share of the population is critical for reducing income inequality, as well as enabling more rapid economic growth. Inclusive fi nancial systems free poor individuals and small enterprises from the need to rely on their own limited savings and earnings to build their assets safely, mitigate risks they face from unexpected events, invest in their education, become entrepreneurs, or take advantage of promising growth opportunities. Failure to provide more households and small and medium enterprises with the fi nancial services they need acts as a brake on development. Sound fi nancial sector policies that encourage competition, provide the right incentives to individuals, and help overcome barriers to access are thus central not only to stability but also to growth, poverty reduction, and more equitable distribution of resources and capacities. Reforms to promote access to fi nancial services should therefore be high on the list of policy makers’ priorities.

The Government of Indonesia has long had improvement of access to credit as one of the cornerstones of its development agenda. While an impressive amount of data and analysis exists on the state of access to credit by small and medium enterprises (SMEs) in Indonesia, there is little hard data and analysis on which to base policies for extending access to broader fi nancial services (beyond credit) to a greater share of the population. What is the demand-side view of the constraints to improved access to fi nance? What do consumers and the currently un-banked population think of fi nancial services? What access do they have and what products and services do they need? This report is an attempt to plug this important data gap and address such questions. It is intended to support the Government’s policy agenda in this critical area.

The key feature of this report is a nationwide household survey of access to fi nancial services on the basis of which it provides data, analysis, and recommendations that can assist the authorities as well as other stakeholders such as the fi nancial services industry in getting an insight into access to fi nancial services in Indonesia. The report aims to identify who does (and does not) have access to fi nancial services in Indonesia, the constraining factors for broader access, and measures that can lower barriers to access for un-banked households.

The World Bank Group has long recognized that well-functioning fi nancial systems that are stable, effi cient, and accessible are essential for economic development. As part of this, it is supporting ongoing eff orts to measure access to fi nance, its determinants, its impact, as well as design and implementation of policies and programs to promote access in several countries across the globe. I hope that this report serves to begin the process of discussions and dialog on this important issue across stakeholders in Indonesia. The World Bank Group stands ready to support the Government of Indonesia as it works to enable those currently outside the formal fi nancial system to join it and reap the benefi ts of such access to formal fi nancial services.

Joachim von AmsbergCountry Director

Indonesia

3

Acknowledgements

This report is the result of a team eff ort involving staff and consultants of the World Bank. The team was led by P.S. Srinivas, Task Team Leader, Yoko Doi, Clarita Cynthia Kusharto, Bilal Husnain Zia, I Gede Putra Arsana, Djauhari Sitorus, Neni Lestari Lloyd Kenward, Chitra Buchori and Fitria Fitrani. The team wishes acknowledge the support provided by Achmad Budiman for his contribution to mobile phone banking section, Sumantoro Martowijoyo on reviewing regulatory frameworks, Irfan Timothy Kortchack for editing work and Hasbi Akhir for designing the report. The team also wishes to thank the peer reviewers: Mohammad Ikhsan, Special Staff to the Vice President, the Vice President Offi ce and Professor, University of Indonesia, and Anjali Kumar, Lead Economist, IEGCG.

The report was prepared under the overall guidance of Tunc Uyanik, Sector Manager, Finance & Private Sector Development, East Asia &the Pacifi c Region; Vikram Nehru, Sector Director, Poverty Reduction & Economic Management, East Asia & the Pacifi c Region; and Joachim von Amsberg, Country Director Indonesia.

The team gratefully acknowledges government support from the Coordinating Ministry of Economic Aff airs, Ministry of Finance, and Bank Indonesia. The survey work was conducted by Regional Economic Development Institute (REDI). The team would like to acknowledge the collaborative work with Dr. Shawn A. Cole and Thomas Sampson from Harvard Business School on the experimental fi nancial literacy program for the unbanked households in East Java undertaken during the household survey implementation.

Preliminary fi ndings of the report were presented to senior offi cials of Bank Indonesia, Bappenas, Ministry of Finance, Bapepam-LK, Coordinating Ministry of Economic Aff airs (CMEA) and other line ministries during a meeting organized by the CMEA in June 2009. During December 9-10, 2009, an international workshop on enhancing access to formal fi nancial services in Indonesia was held with more than 250 participants of senior policy makers, senior management of fi nancial service providers, academics and donors to disseminate the fi ndings from the report and stimulate discussions among and feedback from participants on this issue. The report has taken inputs and feedback from these events into account.

The team also acknowledges the fi nancial support from the Government of the Netherlands (through the Dutch Trust Fund for Improving Indonesia’s Investment Climate and the Multi-Donor Facility for Trade and Investment Climate).

Improving Access to Financial Services in Indonesia4

List of Abbreviations

A2F Access to Finance

ADB Asian Development Bank

AML Anti-Money Laundering

APEC Asia-Pacifi c Economic Cooperation

API Arsitektur Perbankan Indonesia (Indonesian Banking Architecture)

ATM Automated Teller Machine

Bapepam-LK Indonesia Capital Market and Financial Institution Supervisory Agency

BEE Black Economic Empowerment

BI Bank Indonesia

BKD Badan Kredit Desa (Rural Credit Bank)

BPD Bank Pembangunan Daerah (Regional Development Bank)

BPR Bank Perkreditan Rakyat (People’s Credit Bank)

BPS Badan Pusat Statistik (Central Bureau of Statistics)

BRI Bank Rakyat Indonesia

CGAP Consultative Group to Assist the Poor

FAO Food and Agriculture Organization

FATF Financial Action Task Force

GDP Gross Domestic Product

GoI Government of Indonesia

GTZ Gesellschaft fur Technische Zusammenarbeit

ICD Islamic Corporation for Development of the Private Sector

IDIC Indonesian Deposit Insurance Corporation (LPS)

IFAD International Fund for Agricultural Development

IFC International Finance Corporation

IFI International Financial Institution

ILO International Labour Organization

IPO Initial Public Off ering

Inpres Presidential Instruction

IT Information Technology

KSP Kelompok Sains Petani (Farmer’s Science Group; Savings and Loan Cooperative)

KTP Kartu Tanda Penduduk (National Identity Card)

KUK Kredit Usaha Kecil (Small Scale Business Loan)

Kupedes Kredit Umum Pedesan (Village Credit Program)

KUR Kredit Usaha Rakyat (Peoples Business Credit)

KYC Know Your Customer

5

LDKP Lembaga Dana Kredit Pedesaan (Rural Credit Fund Institution)

LPS Lembaga Penjamin Simpanan (Deposit Insurance Organization)

MASS Microfi nance Access and Services Survey

MCSME Ministry of Cooperatives and Small and Medium Enterprises

MoF Ministry of Finance

MSME Micro Small and Medium Enterprises

NBFI Non-Bank Financial Institution

NGO Non-Government Organization

NPWP Nomor Pokok Wajib Pajak (Taxpayer Number)

OECD Organization for Economic and Cultural Development

OJK Otoritas Jasa Keuangan (Financial Services Authority)

PJTKI Perusahaan Jasa Tenaga Kerja Indonesia (Indonesian Workforce Service Company)

PODES Statistik Potensi Desa (Village Potential Statistics)

PP Perum Pegadaian (State-owned Pawnbroker)

PPATK Pusat Pelaporan dan Analisis Transaksi Keuangan (Financial Intelligence Unit)

ProFI Promotion of Small Financial Institutions

Puskesmas Pusat Kesehatan Masyarakat (Community Health Center)

RICA Rural Investment Climate Assessment

SAF Survey of Access to Finance

SEACEN South East Asian Central Banks

SID Sistem Informasi Debitur (Debtor Reporting System)

Simpedes Simpanan Pedesaan (Village Saving Program)

SIUP Surat Ijin Usaha Perdagangan (Business Trading License)

SKB Surat Keputusan Bersama (Joint Ministerial Decree)

SME Small and Medium Enterprises

SoB State-Owned Bank

Susenas Survey Sosial Ekonomi Nasional (National Socio-Economic Survey)

UNDP United Nations Development Programme

Improving Access to Financial Services in Indonesia6

Table of Contents Foreword 2

Acknowledgments 3

List of Abbreviations 4

Table of Contents 6

List of Tables 8

List of Figures 8

List of Boxes 10

Chapter 1 Executive Summary 11

Chapter 2 The Current Supply of Financial Services in Indonesia 19

2.1 Overview of Indonesia’s Financial Sector 19

2.2 The Commercial Banking System 21

2.3 Regional Reach of Indonesia’s Commercial Banks 25

2.4 People’s Credit Banks (BPRs) 30

2.5 Microfi nance Institutions 32

2.6 Sharia Finance and Banking 36

2.7 Non-Bank Financial Institutions (NBFIs) 39

2.8 Financial Services in Support of Remittances 40

2.9 Summary of Policy Issues, by Area 44

Chapter 3 Demand-side Aspects: What do People Want? 47

3.1 Introduction and Overview 47

3.2 Survey Results: Supply of Financial Services 50

3.3 Survey Results: Demand for Types of Financial Services 55

3.4 Survey Results: Demand for Savings Accounts 55

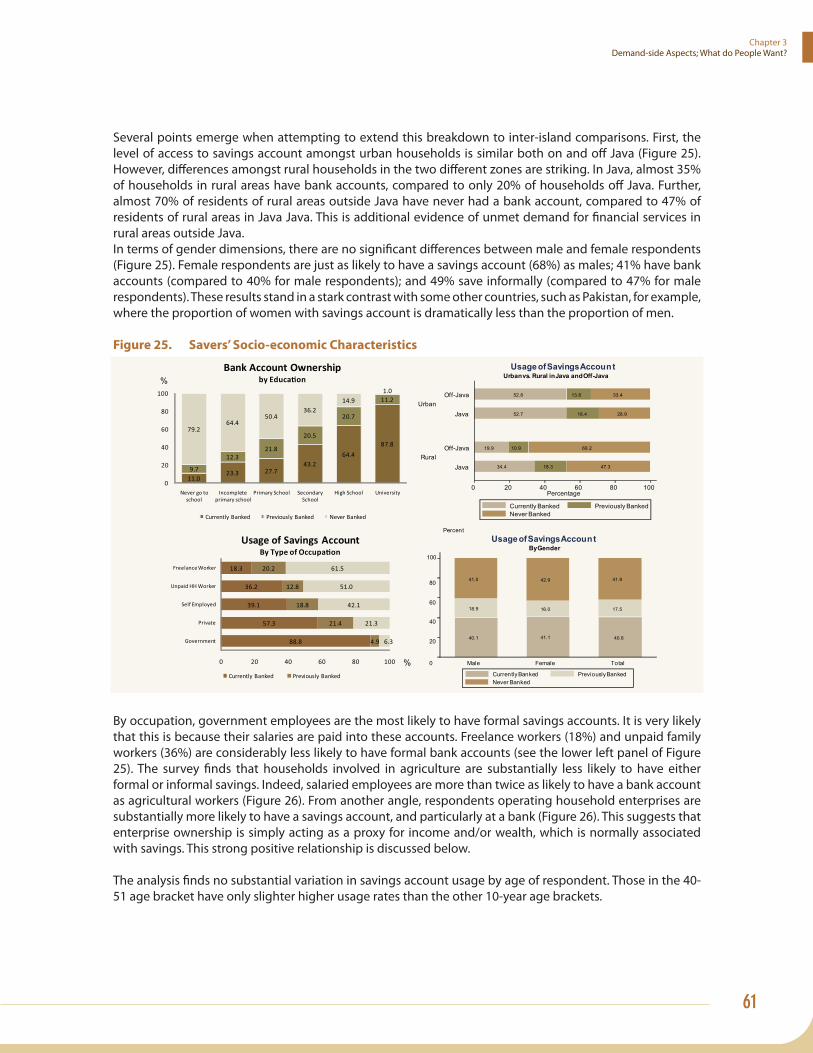

3.4.1 Barriers to Accessibility: Reasons for Savers Being Unbanked 57

3.4.2 Key Socio-economic Characteristics of Indonesia’s Savers 60

3.4.3 Econometric Analysis of Savings 63

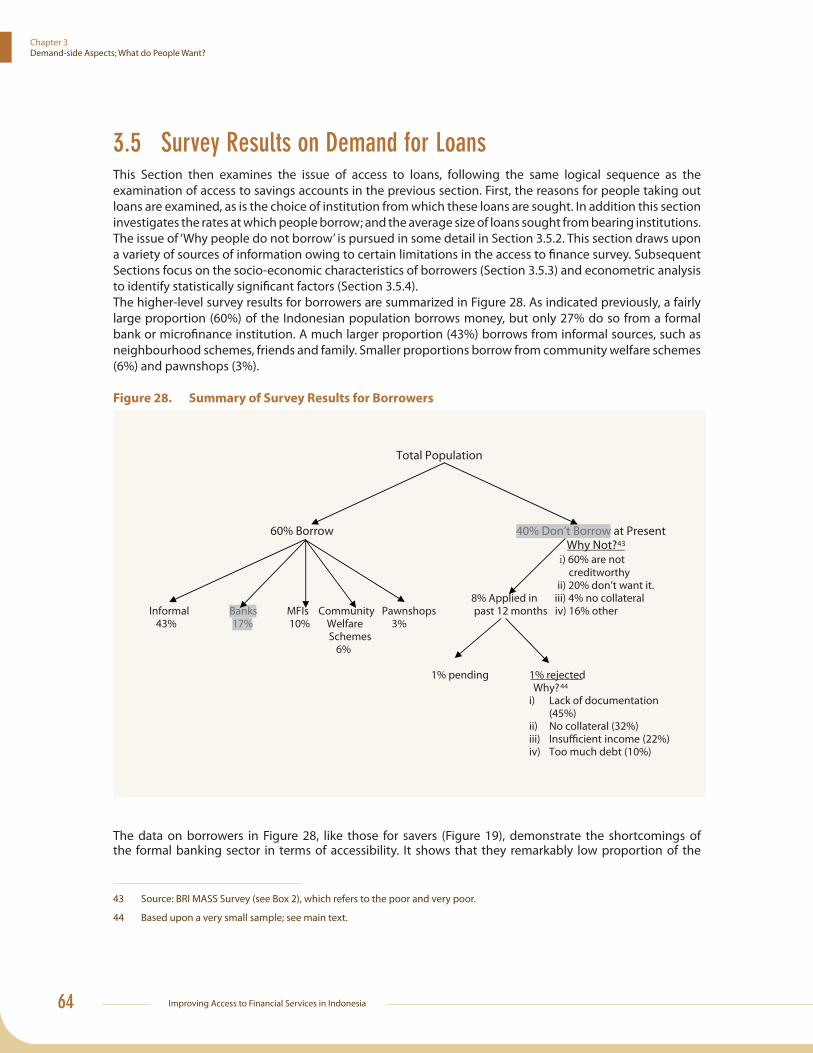

3.5 Survey Results on Demand for Loans 64

3.5.1 Who Does Not Borrow? 69

3.5.2 Barriers to Accessibility: Why Do People Not Borrow? 70

3.5.3 Key Socio-Economic Characteristics of Indonesia’s Borrowers 71

3.5.4 Econometric Results for Loans 76

3.6 The ‘Truly Financially Excluded’: No Loans And No Savings Accounts 77

3.7 Survey Results on Demand for Insurance 79

3.7.1 Econometric Results for Insurance 83

3.8 Other Survey Results: Risks to Financial Well-Being 84

3.8.1 Other Survey Results: Demand for Other Financial Instruments 84

3.8.2 Other Survey Results: Expressed Demand for Financial Products 86

3.9 Summary of Policy Issues 88

Chapter 4 Regulatory Impediments to Access 91

7

4.1 Introduction 91

4.1.1 Indonesia’s Financial Regulators & Supervisors 93

4.2 Assessment of the Current Regulatory System, by Service Provider 95

4.2.1 Regulatory Barriers to Access: Commercial Banks 95

4.2.2 Regulatory Barriers to Access: Bank Perkreditan Rakyat (BPRs) 99

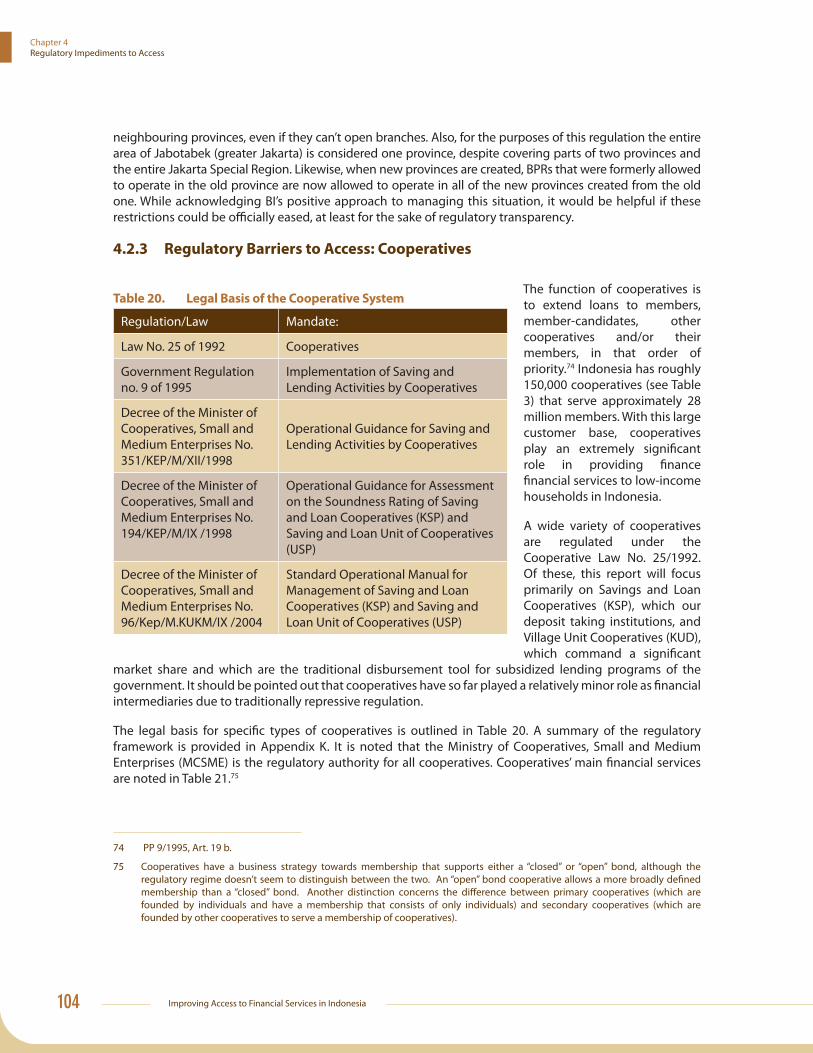

4.2.3 Regulatory Barriers to Access: Cooperatives 104

4.2.4 LPS’s Role in the Regulatory Environment 106

4.2.5 Regulatory Barriers to Access: Finance Companies 107

4.2.6 Regulatory Barriers to Access: Insurance Companies 108

4.2.7 Barriers to Access: Pawnshops 109

4.3 Summary of Policy Issues, by Service Provider 111

Chapter 5 Special Topics Concerning Access to Finance 115

5.1 MSMEs and Access to Finance 115

5.1.1 Key Findings of Bank Indonesia’s Survey of MSMEs 116

5.1.2 MSME Lending & Policies in Indonesia 118

5.2 Migrant Workers and Access to Finance 122

5.2.1 A2F Findings on Indonesian Migrant Workers 122

5.2.2 Migrants & Access to Financial Services 125

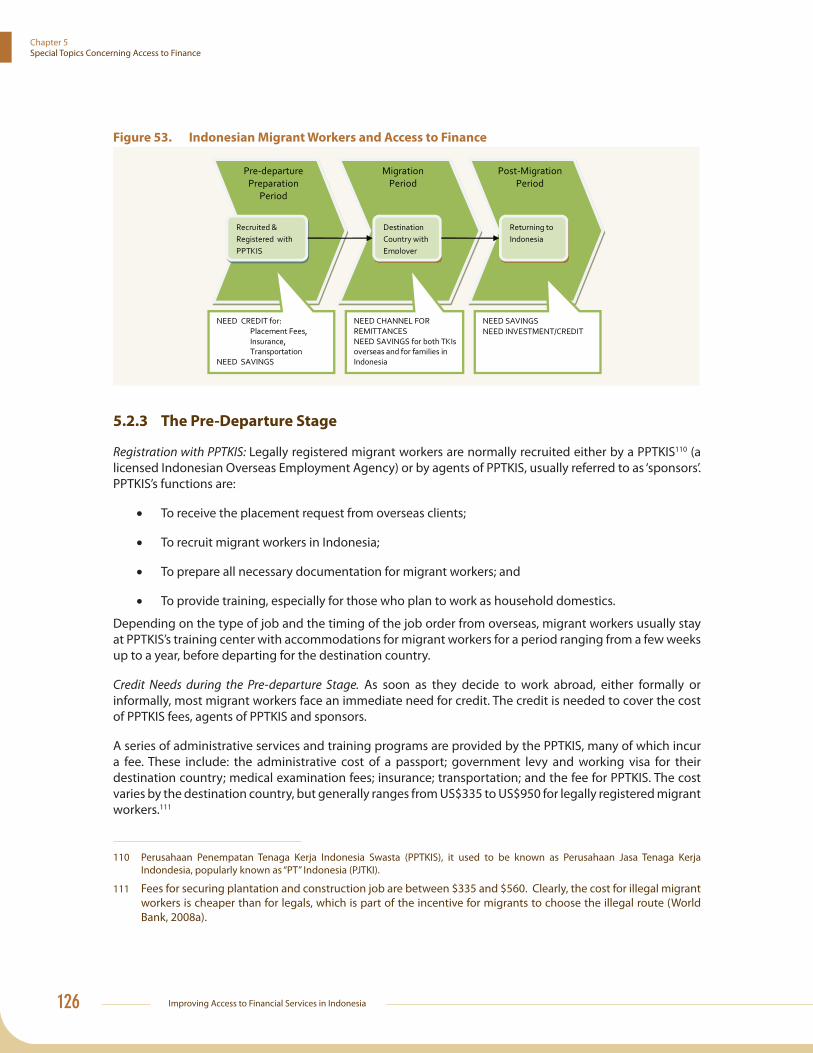

5.2.3 The Pre-Departure Stage 126

5.2.4 Financial Service Needs During Migration 131

5.2.5 The Post-Migration Period 137

5.3 Mobile Banking 137

5.3.1 The International Context 137

5.3.2 The State of Mobile Banking in Indonesia 140

5.3.3 Mobile Banking to Improve Access to Financial Services 142

5.4 Policy Issues 143

Chapter 6 Policy Recommendations for Improved Access to Financial Services 147

6.1 General Strategic Matters 147

6.2 Regulatory Issues 148

6.2.1 Mobile Banking 148

6.2.2 Commercial Banks 149

6.2.3 BPRs 149

6.2.4 LPS 150

6.2.5 Cooperatives 150

6.2.6 Pawnshops 150

6.2.7 Other Financial Institutions 150

6.3 MSMEs 150

6.4 Overseas Workers and Remittances 151

6.5 Matters of More Limited Concern 151

Improving Access to Financial Services in Indonesia8

Annexes 155

References 194

List of Tables

Table 1. International Comparison of Financial Sectors: Selected Financial Indicators 20

Table 2. International Comparison of Bank Branch Density 20

Table 3. Indonesia, Number of Financial Institutions 22

Table 4. Number of Kabupaten/Kotamadya With and Without Branches of Commercial Banks 29

Table 5. Sharia Banking Offi ces (number of banks, etc.) 36

Table 6. Sharia Rural Bank Performance Indicators 37

Table 7. Offi cial Overseas Worker Placement, 2004 40

Table 8. Cost of Domestic Remittances, April 2009 43

Table 9. Travel to Banks, Time & Cost 52

Table 10. Saver’s Travel to Banks, by Urban/Rural & Java/Off Java 53

Table 11. Non-savers’ Travel to Banks, Urban/Rural & Java/Off -Java 53

Table 12. Summary of Indonesian Savers’ Characteristics 63

Table 13. Household Indebtedness 72

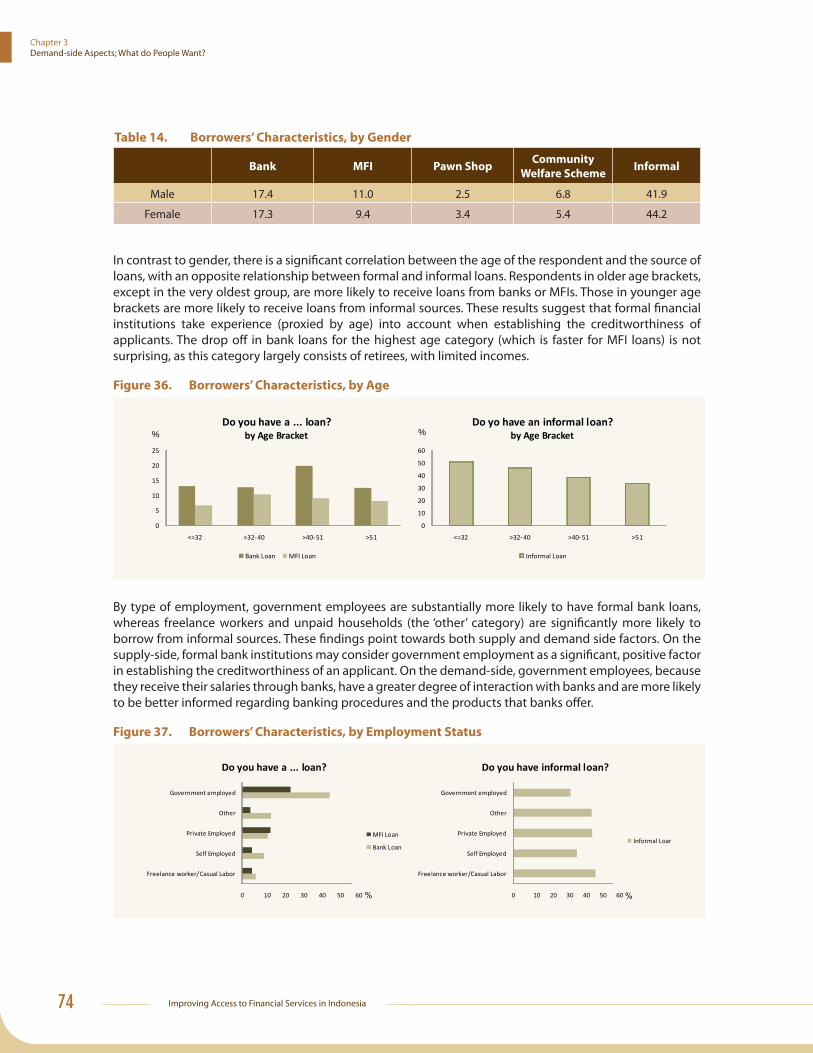

Table 14. Borrowers’ Characteristics, by Gender 74

Table 15. Summary of Insurance Holders’ Characteristics 83

Table 16. Summary of Households Use & Interest in Formal Financial Products 89

Table 17. Financial Providers and Financial Services in Indonesia 94

Table 18. BPR Start-up Capital Requirement 99

Table 19. Access to Finance Indicators-Loans and Deposits 103

Table 20. Legal Basis of the Cooperative System 104

Table 21. Financial Services of Savings and Loan Cooperatives 105

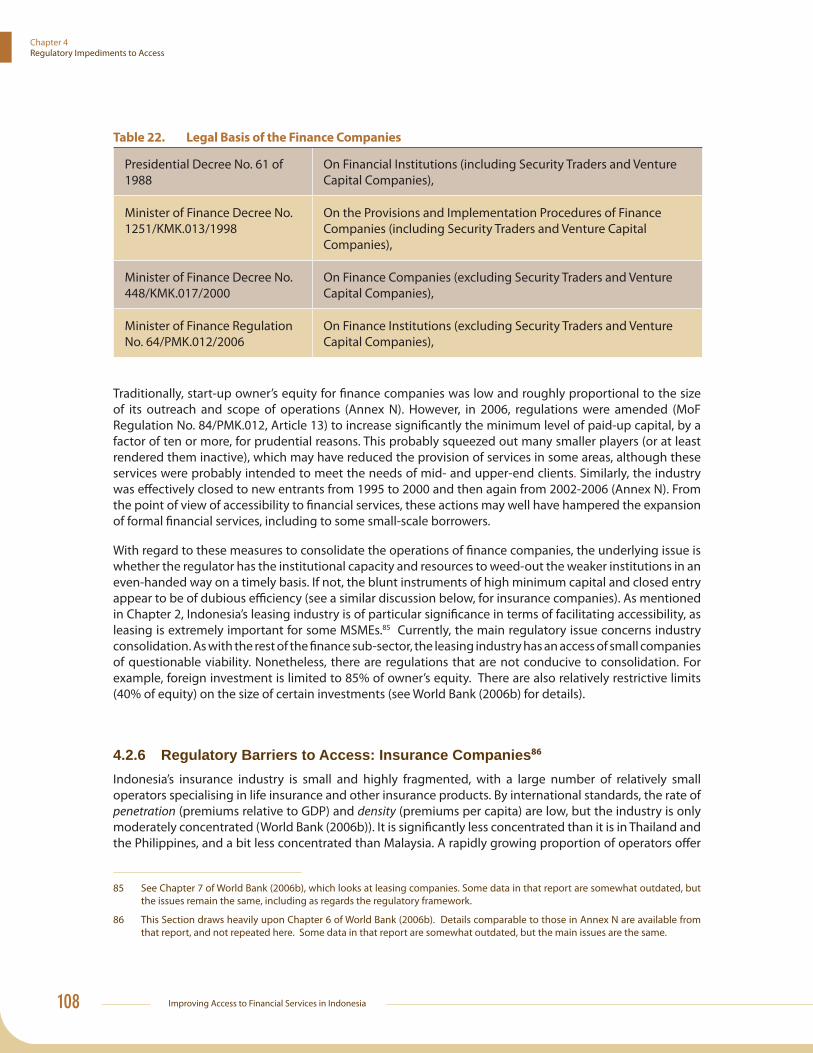

Table 22. Legal Basis of the Finance Companies 108

Table 23. Sample Savings Product Off ered by Banks and the Post Offi ce 130

Table 24. Indicative Cost of Remitting Money from a Middle-East Country 134

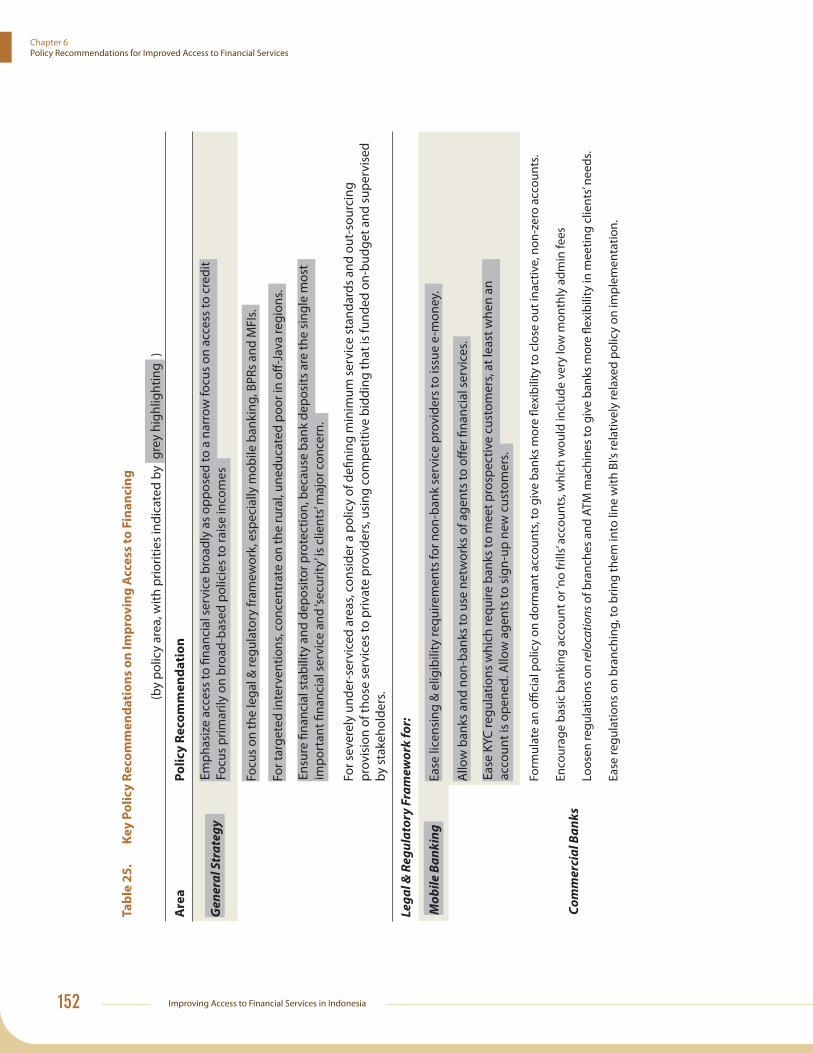

Table 25. Key Policy Recommendations on Improving Access to Financing 152

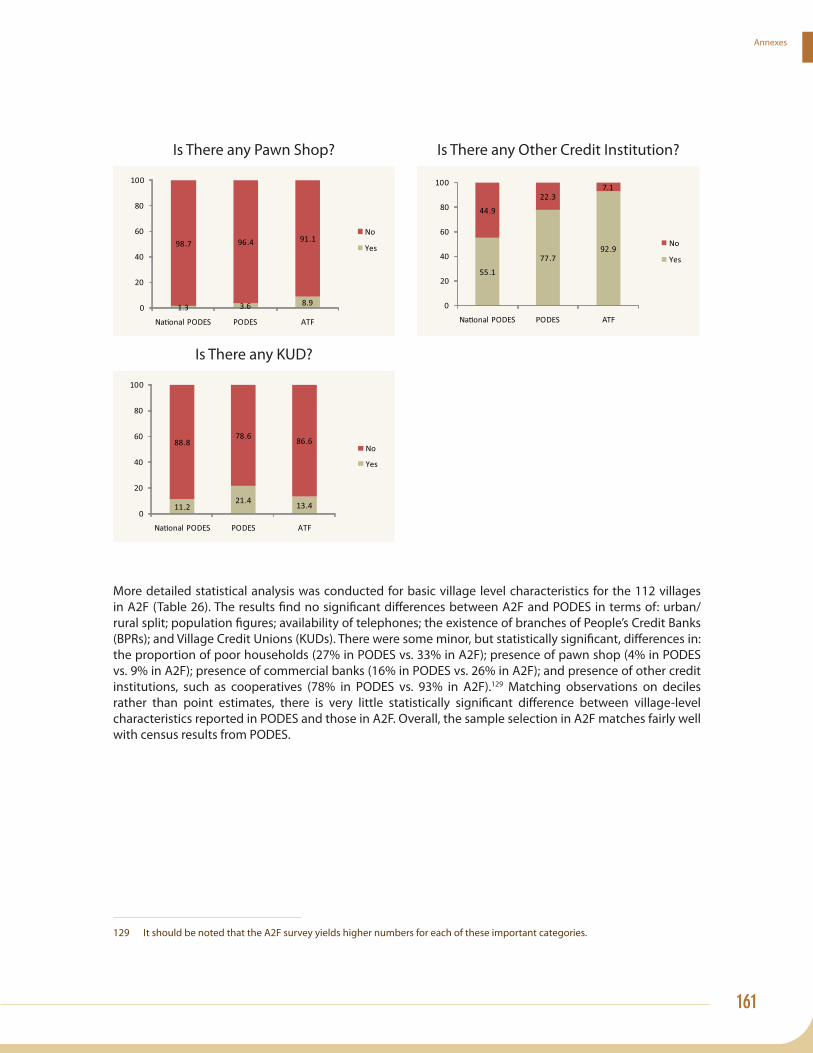

Table 26. Statistical Comparison of Village-Level Variables in the A2F Survey and PODES 162

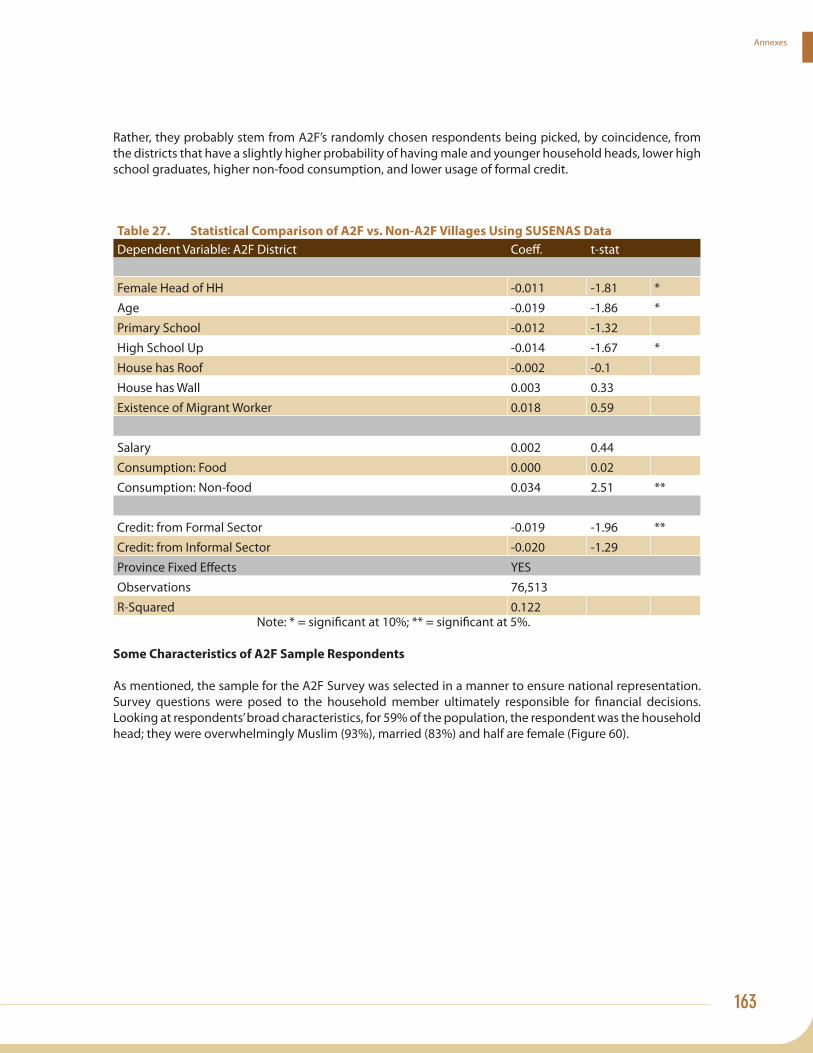

Table 27. Statistical Comparison of A2F vs. Non-A2F Villages Using SUSENAS Data 163

List of Figures

Figure 1. Share of the Population with formal fi nancial access 12

Figure 2. Savers’ Financial Inclusion 13

Figure 3. Borrowers’ Financial Inclusion 13

Figure 4. Financial Structure (December 2008) 21

Figure 5. Total Banks by Type of Bank 21

Figure 6. Number of Bank Branches and ATMs, by Type of Bank 23

Figure 7. Bank Head Offi ces & Branches, by Province 25

Figure 8. Bank Branches & Density Vs. Per Capita Income, by Province 26

9

Figure 9. Total ATMs & Density Vs. Per Capita Income, by Province 28

Figure 10. Number of Kabupaten without Bank Branches, by Province 30

Figure 11. Financial Performance of BPRs 32

Figure 12. Top 20 Developing-country Recipients of Remittances, 2005 41

Figure 13. Bank Account Distribution, by Type of Bank 51

Figure 14. Bank Branch Locations 51

Figure 15. Travel Time to Nearest Bank Branch 52

Figure 16. Average Time to Reach Select Institutions 54

Figure 17. Waiting Time to be Served in a Bank 54

Figure 18. Financial Products Used by Households 55

Figure 19. Summary of Survey Results for Savers 56

Figure 20. Overlap Among Savings Providers 56

Figure 21. Reasons for Having a Bank Account, by Type of Bank 57

Figure 22. Main Reasons for Not Having a Bank Account 58

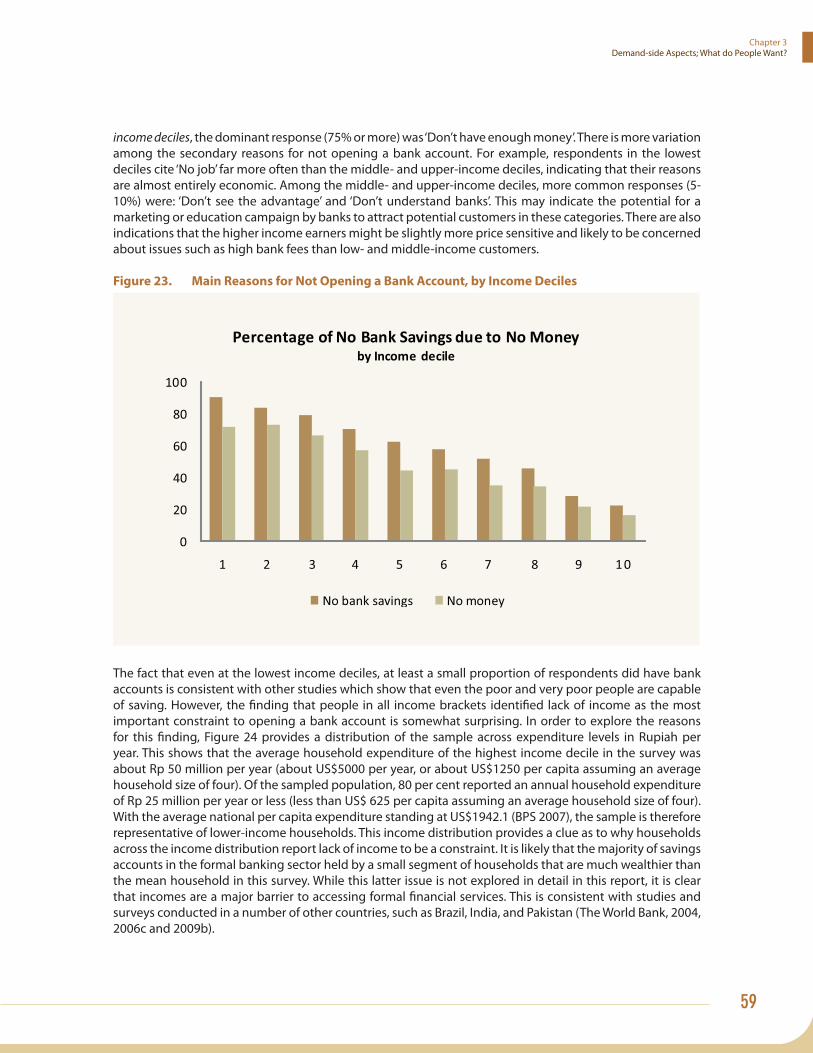

Figure 23. Main Reasons for Not Opening a Bank Account, by Income Deciles 59

Figure 24. Yearly Total Household Expenditure 60

Figure 25. Savers’ Socio-economic Characteristics 61

Figure 26. More Savers’ Socio-economic Characteristics 62

Figure 27. Savings by Per Capita Expenditure 62

Figure 28. Summary of Survey Results for Borrowers 64

Figure 29. Purpose of Loan, by Service Provider 66

Figure 30. Loan Sizes, by Institution 67

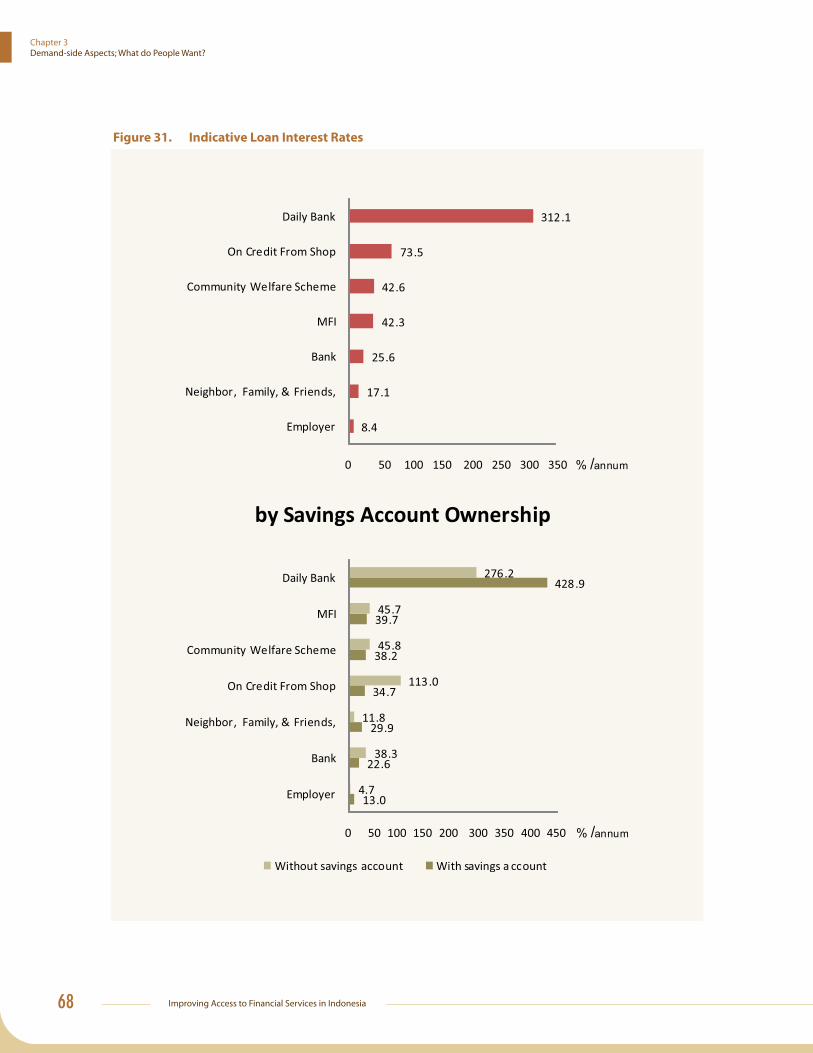

Figure 31. Indicative Loan Interest Rates 68

Figure 32. Non-Borrowers by Per Capita Expenditure 69

Figure 33. Non-Borrowers’ Characteristics 70

Figure 34. Characteristics of Borrowers 73

Figure 35. Borrowers’ Characteristics, Urban/Rural 73

Figure 36. Borrowers’ Characteristics, by Age 74

Figure 37. Borrowers’ Characteristics, by Employment Status 74

Figure 38. Borrowers’ Characteristics, by Type of Job 75

Figure 39. Borrowers’ Characteristics, by Enterprise Ownership 75

Figure 40. Borrowers, by Region, by per Capita Expenditure 76

Figure 41. Bank Loan, by Region, by per Capita Expenditure 76

Figure 42. Characteristics of ‘Truly Financially Excluded’, by per Capita Expenditure 77

Figure 43. Characteristics of the ‘Truly Financially Excluded’ 78

Figure 44. Characteristics of the ‘Truly Financially Excluded’, continued 79

Figure 45. Insurance Holders, by per capita Expenditure 80

Figure 46. Types of Insurance Ownership 81

Figure 47. Characteristics of Holders of Insurance 82

Figure 48. Characteristics of Insurance Holders, continued 83

Figure 49. MSME Lending 119

Figure 50. MSME Characteristics 121

Improving Access to Financial Services in Indonesia10

Figure 51. Characteristics of Migrant Workers 124

Figure 52. Migrant Workers, by Type of Work and Legal Status (in per cent) 125

Figure 53. Indonesian Migrant Workers and Access to Finance 126

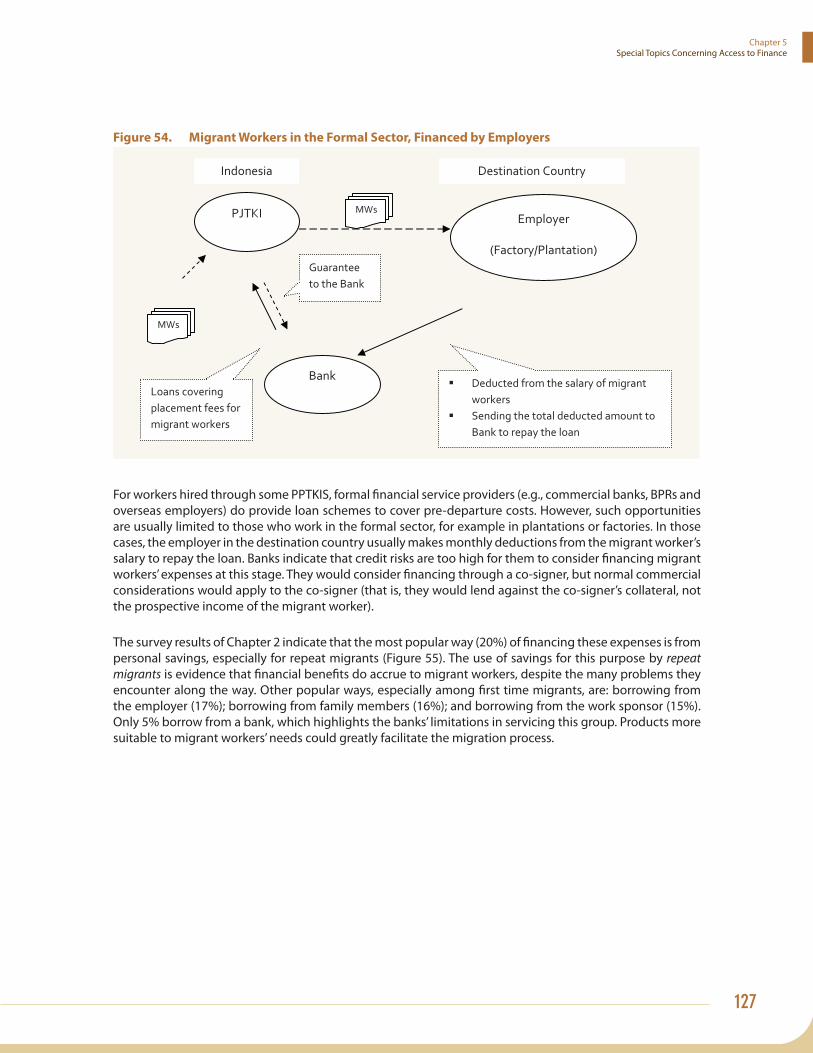

Figure 54. Migrant Workers in the Formal Sector, Financed by Employers 127

Figure 55. How Migrant Workers Finance Pre-departure Expenses 128

Figure 56. Method of Receiving Remittances, by Host Country (in percent) 135

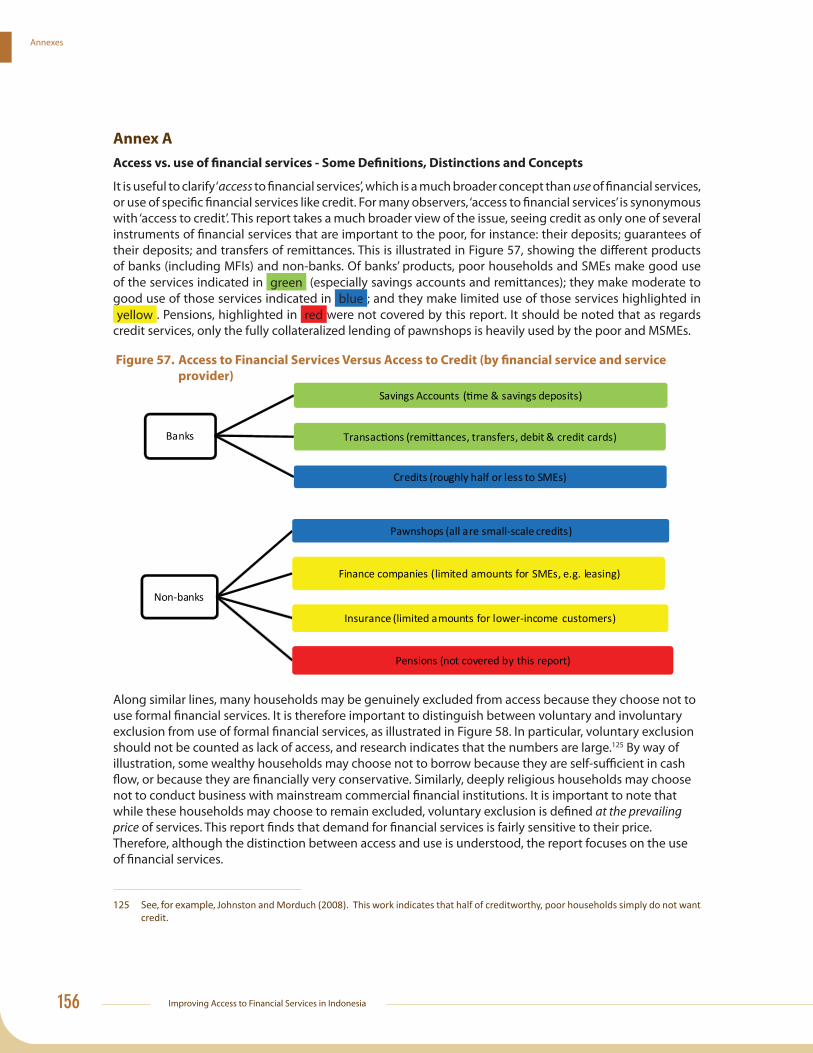

Figure 57. Access to Financial Services Versus Access to Credit 156

Figure 58. Diff erence Between Access to and Usage of Services 157

Figure 59. Samples in PODES 2005 vs. Access to Finance 2007, at Village Level 160

Figure 60. A2F Sample Characteristics 164

Figure 61. Urban/Rural Split 164

Figure 62. Respondents, by Province 165

Figure 63. Sample Characteristics, Age by Gender 165

Figure 64. Respondents, by Employment & Education 166

Figure 65. Respondent Wage Composition 166

List of Boxes

Box 1. The Role of State Vs. Private Banks in Indonesia 24

Box 2. BRI’s MASS Survey: Insights to Banks’ Capacity to Reach the Poor 31

Box 3. The Shadowy Faces of Indonesia’s Lintah Darat 34

Box 4. BRI’s Unit Desa System 35

Box 5. Wider Access to Financial Services through Sharia Mobile Banking 38

Box 6. What Do Household Surveys in Other Countries Tell Us? 48

Box 7. What Do Other Surveys for Indonesia Tell Us? 49

Box 8. Sampling Methodology of the Indonesian Survey 49

Box 9. Some Details on Insurance in the Survey 80

Box 10. Survey Results on Mobile Banking 85

Box 11. Survey Results on Financial Literacy 86

Box 12. Evidence on Easing Constraints to Opening Bank Accounts 88

Box 13. South Africa’s Approach to Improving Access to Financial Services 92

Box 14. Some History on the Regulation of Other Microfi nance Institutions 101

Box 15. Legal Framework for Microfi nance Institutions in Indonesia 111

Box 16. Case Study: Migrant Workers Bound for Taiwan 129

Box 17. Perum Pegadaian (The State-owned Pawnshop) & Access to Credit 129

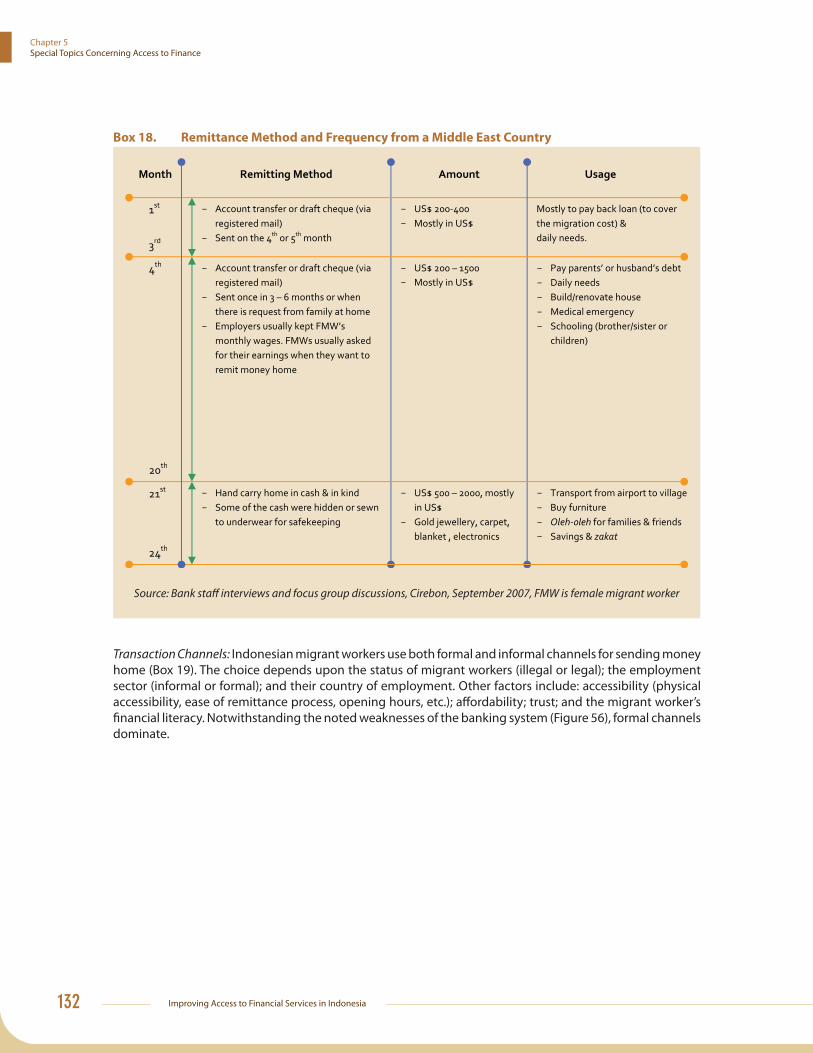

Box 18. Remittance Method and Frequency from a Middle East Country 132

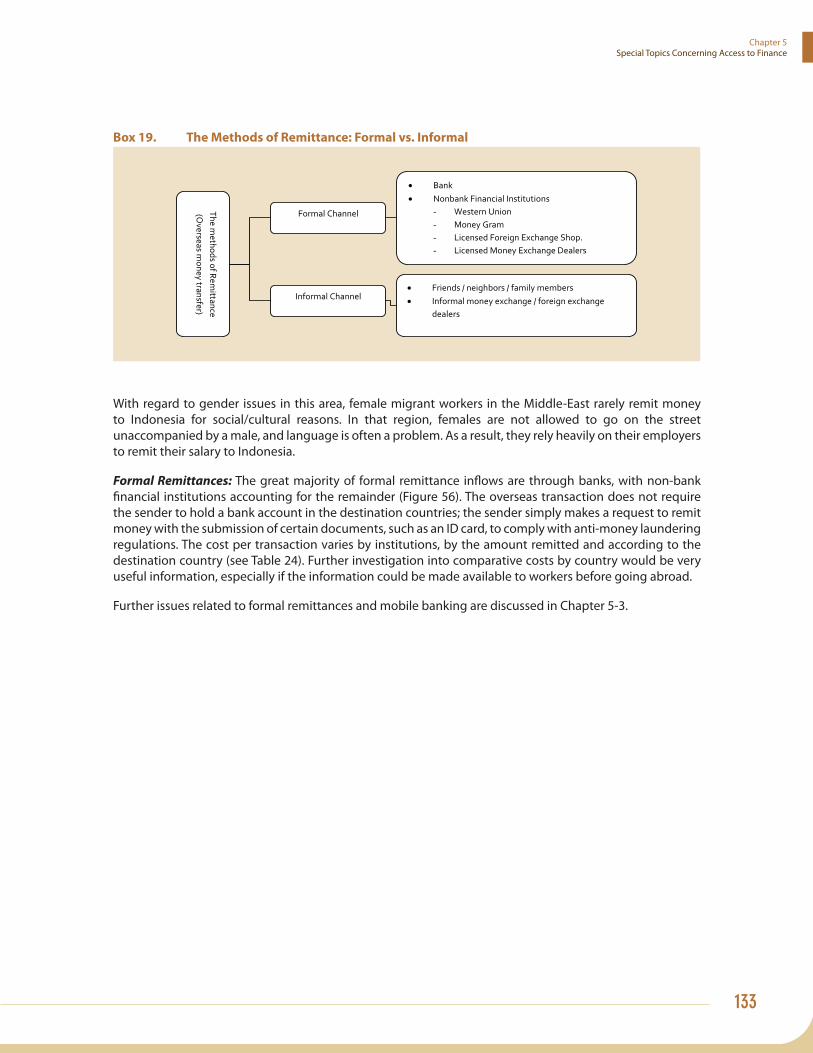

Box 19. The Methods of Remittance: Formal vs. Informal 133

Box 20. Voices of Hard Experience 136

Box 21. Promising Technologial Advances – South Africa’s WIZZIT 138

Box 22. International Experience in Reducing the Cost of Mobile Banking 139

Box 23. Mobile Banking Product Development in Indonesia 141

Box 24. Weaknesses in the Regulatory Environment for Branchless Banking in Indonesia 142

11

Chapter 1

Executive Summary

There is an impressive amount of evidence to support the proposition that access to formal fi nancial services is a critically important factor for the achievement of poverty alleviation1. There is a growing recognition that increasing access to formal fi nancial services has both private and social benefi ts. Extending access to fi nancial services encourages economic growth and can improve income distribution.

In light of the evidence for the benefi ts of expanded access to fi nancial services, fi nancial inclusion is high on the policy agenda of a number of developing countries worldwide. This is often particularly necessary in such countries, where banking and fi nancial systems are often underdeveloped and often cater only to large fi rms in the formal sector and/or high-income individuals. Improving access requires actions on both the supply and demand side, by both the public and private sectors. It also requires changes in the institutional environment. Recent experiences in several countries show that with the right information on who lacks access and for what reasons, policies can be adjusted and products can be designed to scale up access, especially with new technology.

The Government of Indonesia has also placed high importance on the issue of improved access. The Indonesian government acknowledges that limited access to fi nancial services is a constraint to development, and the authorities are initiating policies aimed at overcoming this constraint. One of the key constraints to concrete policy action in improving access to fi nancial services, in particular at the household level, is the lack of concrete data and sound analysis on what exactly the demand-side view of the constraints. Before attempting to address the issue of extending access, it is necessary to answer the following questions: What

1 See, for example, the work of Beck, Demirguc-Kunt and Martinez Peria (2004), (2005) and (2006). Banking the Poor (2009c), Access to Finance Study: Brazil (2004), India (2006c), Nepal (2007b), and Pakistan (2009b)

Improving Access to Financial Services in Indonesia12

Chapter 1Executive Summary

do consumers and the currently un-banked population think of fi nancial services? What products and services do they need? Are these products and services are available to them? If not, why not? Evidence-based answers to these questions can provide a solid basis to inform policy and product development. While there is a signifi cant amount of data and analysis on the issue of access to credit, particularly by Small and Medium Enterprises (SMEs) 2, there is very little data or analysis on matters related to broader access to fi nancial services.

The basis for this report is a nationwide household survey related to issues of access to fi nancial services. On the basis of this survey, data, analysis, and recommendations are presented as inputs for regulatory authorities and other stakeholders, including those in the fi nancial services industry. The report begins with a review of the supply side of fi nancial services from an access perspective, followed by an examination of the demand side of access to those services. It then looks at the regulatory barriers to fi nancial inclusion and discusses the means by which these barriers may be addressed. Finally, it addresses a number of topics that are of particular relevance to issues of access, including MSMEs, overseas migrant workers and mobile banking.

The immediate purpose of the report is to inform policy-makers and the industry on where and in which sectors of the population constraints to access to fi nancial services exist. The objective is to identify—as specifi cally as possible—measures that can lower barriers to access for poorer households, especially measures that work in cost-eff ective ways.

Survey Results on the Demand for Financial Services

Just about half of Indonesia’s population has access to formal fi nancial services. This is better than countries such as China, Pakistan, Bangladesh, and the Philippines. It is, however, worse than countries such as Sri Lanka, Thailand, and Malaysia. In short, there is much room for improvement.

Figure 1. Share of the Population with formal fi nancial

access

0

20

40

60

80

100%

Sources: World Bank (2008d); World Bank (2009b)

Commercial banks, which dominate the Indonesian fi nancial sector, serve a relatively small proportion of Indonesian households. One-third of Indonesians don’t save at all, and can be considered truly ‘fi nancially excluded’ (see Figure 2 below). Similarly, less than half of Indonesians save at banks, and of those who do save at banks, two-thirds also save at some other type of service providers. Considering the overlap between banks and the informal sector, informal institutions actually service more savers than do banks.

2 World Bank (2006e),“Making the New Indonesia Work for the Poor,”; World Bank (2006):“Revitalizing the Rural Economy: An assessment of the investment climate faced by non-farm enterprises at the District level” ; Signifi cant work done by GTZ on rural banks: See http://www.profi .or.id/; FAO and IFAD on rural fi nance: http://www.ruralfi nance.org/ and http://www1.deptan.go.id/kln/FAO%20in%20%20Indonesia.htm. ILO on migrant workers: See http://www.ilobkk-migration.org/, IFC/GTZ, and CGAP (2009d), ADB (2007): “Low Income Households’ Access to Financial Services” (2007)

13

Chapter 1Executive Summary

Figure 2. Savers’ Financial Inclusion A mere 17% of Indonesians borrow from banks, with about one third more borrowing from the informal sector. On this basis, roughly 40% of the population is ‘fi nancially excluded’ from credit (see the Figure 3: below). The most important reason for exclusion appears to be diffi culties satisfying documentation requirements. The evidence suggests that lack of collateral is a secondary reason.

The single most important fi nancial service identifi ed by households in the

survey is a bank savings account. The most important stated reason for having a bank account is ‘security’. By far, the most common stated reason for not having a bank account is ‘lack of income’ or not having a job. While the survey’s respondents claimed that access to credit from banks was also important, it was considerably further down the list of priorities than access to a savings account. Credit is still concentrated in the informal sector, with sources of credit being widely diversifi ed among service providers.

Figure 3. Borrowers’ Financial InclusionTaken together, the above fi ndings underscore the importance of expanding fi nancial services institutions abilities to off er both savings and credit services, while raising depositors’ incomes through broader policies of economic development. These fi ndings also underscore the challenge to Indonesia’s formal fi nancial system, especially the banks, of signifi cantly expanding its client base, to reach a much larger portion of the population. The ‘truly fi nancially excluded’, or those who have

neither a savings account nor a loan, are predominantly poor, poorly educated, live off -Java in rural areas, and do not own non-farm enterprises. Off Java residents are more than twice as likely to have neither a bank account nor a loan, than are on Java residents.

Physical access to formal fi nancial services is not generally regarded as a signifi cant constraint. The vast majority (some 95%) of Indonesians rated the physical and geographical accessibility of banking facilities as ‘convenient’ or ‘very convenient’. The exception is in rural, off -Java regions, especially where water transport is involved. Nonetheless, it is notable that average travel times to reach bank branches compare favorably to the average travel times taken to reach key public services such as hospitals, schools and other health facilities.

One simple, low-cost solution for borrowers who want to access bank credit at a lower interest rate is for them to open a bank account. Banks and MFIs both charge nominal interest rates of about 30% per annum, with both institutions off ering lower rates to borrowers who hold a savings account. Nominal interest rates from other formal and informal sources of credit, except for loans from employers, friends and neighbors, tend to be higher.

Improving Access to Financial Services in Indonesia14

Chapter 1Executive Summary

Consumers do respond to more attractive pricing of fi nancial services, particularly lower charges on savings accounts. However, the demand looks somewhat price inelastic, which implies that banks need to carefully consider whether it is in their fi nancial interest to reduce fees. This is consistent with identifi ed bank policies that set deposit rates and administration fees in a way that discourages small savers. One policy option in this regard is to encourage banks to off er basic banking services or ‘no frills’ accounts, an initiative that has already begun and appears set to grow in 2010. It should be noted that banks in a number of countries around the world are implementing such ‘no frills’ schemes, although in diff erent ways. Another option would be to encourage regulatory and technological advances to foster the development of services such as mobile banking, which allows service providers to reach more customers at lower cost. Another innovation, especially given Indonesia’s geography, would be to permit and encourage banks to form partnerships with non-bank in institutions and outlets as a means of increasing access to their services.

Some new products that would be of interest to consumers are contractual savings products for urban residents or mobile savings services for rural residents. As for extending the reach of formal bank services so that it better served lower income earners, the most promising avenue looks like mobile banking – even if at fi rst, it is likely that mobile banking is largely likely to be focused on payments services. Even the poorest people in remote villages often have access to mobile phones, and the survey uncovers considerable interest in mobile banking among those with a mobile phone, but with no bank account at present.

Key Aspects of the Current Supply of Financial Services

Although the number of banks has declined substantially since the 1997/98 crisis, banks have signifi cantly expanded the reach of their fi nancial services by expanding their network of branches and through the use of ATMs. Other formal sector providers such as cooperatives and the state owned pawnshop have also expanded their physical outreach. Per capita income and population density go a long way towards explaining the reach of Indonesia’s commercial banking system and the diff erences between the provinces in terms of its reach. The only notable exceptions relative to the average are Jakarta (which is ‘over-serviced’) and East Kalimantan (which is large, resource rich, sparsely populated and ‘under-serviced’). In considering banks, it is important to distinguish between the commercial banks and People’s Credit Banks (BPRs), which are regional in nature and much smaller in size. Among the former, only a relatively small number currently provide fi nancial services to a signifi cant number of lower income households. And even among these, their focus tends to be on better-off clients. However, the commercial banks do make important contributions in other ways. For instance, a number of large commercial banks are involved in so-called ‘linkage program’ with BPRs. In addition, their numbers include one of the largest micro fi nance institutions in the world (BRI’s Unit Desa system). Also, commercial banks are aggressive, opportunistic competitors who are quick to move into promising new markets. Such characteristics imply that the commercial banks are the institutions most likely to introduce new cost-cutting technologies and to put competitive pressure on other fi nancial institutions. Still, they are only a part of the short-term answer to improving access to fi nancial services, because they do not currently have the facilities and infrastructure to serve the lower strata of Indonesian society, particularly for members of the community living in remote, rural areas.

By contrast, in terms of improving access to fi nancial services, the BPRs and other small fi nancial institutions off er much more promise in the near- to medium-term. Despite a great deal of diversity, they are often on the frontline of the delivery of fi nancial services to MSMEs and poorer households, including those in very remote parts of Indonesia. As detailed below, much can be done on the regulatory front to extend their reach.

Sharia banking (and more generally, sharia fi nancing) currently commands a small market share, although this market share has been expanding rapidly for about a decade. These institutions are particularly

15

Chapter 1Executive Summary

important because they cater almost exclusively to the lower end of the market, including in rural regions. Also, Indonesia’s fi rst sharia bank (established in 1992) is a leading innovator in terms of extending fi nancial services to poor remote areas through mobile banking.

Among other fi nancial institutions that provide access to fi nancial services for the poor, three are especially notable: the state-owned pawnshop; cooperatives; and other micro fi nance institutions. Each faces its own particular constraints to which there are specifi c solutions, which are discussed further below. Non-Bank Financial Institutions (NBFIs) play a less signifi cant role in terms of the services they off er to lower income earners, although there has been some encouraging progress in a few areas in recent years. In particular, a number of these institutions off er micro insurance and leasing products that are of particular relevance to MSMEs.

Main Recommendations

Improved access to fi nancial services by lower-income Indonesians requires both public and private sector interventions and innovative public-private partnerships. Based on the self-identifi ed needs of lower income Indonesians, the focus should be on access to a broad range of fi nancial services, rather than merely on access to credit. Credit is important for the poor, but savings facilities rank much higher. A signifi cant proportion of lower income earners fi nd existing fi nancial products to be inappropriate to their needs. Designing and pilot testing appropriate products through partnerships could potentially facilitate access to formal fi nancial sector by a greater proportion of the population, to the benefi t of both clients and fi nancial institutions themselves.

From a public sector perspective, strengthening the existing legal and regulatory framework for various formal fi nancial institutions would be a good fi rst step in aiding the process. For every important service provider, there are aspects of the regulatory framework that could be reformed for the sake of improving access to fi nancial services, without compromising prudential safety.

For commercial banks, the most promising simple, low-cost regulatory reform would involve steps to create a conducive environment for mobile banking, which holds considerable promise in terms of improving access to fi nancial services. Mobile banking holds great promise for reducing costs and extending reach – although, in line with international experience, it is likely to initially focus on payments services and remittances. BI has recently made notable regulatory advances, although much more is still possible. For instance, revised regulations now permit non-bank service providers to issue e-money, but only for payment purposes. If non-bank service providers want to off er person-to-person services, they need a remittance license. At present, eligibility requirements are a signifi cant, unintended barrier to entry. Simpler ways are available to accomplish the same regulatory purpose, without creating such barriers.

To deliver mobile banking services cheaply, the economies of scale off ered by a network of non-bank retail agents is vital. This would entail allowing banks the discretion to outsource services using a network of non-bank third parties, with the banks remaining responsible for their agents’ activities. For mobile banking to be able to meet the needs of the ‘fi nancially excluded’, there are also important Know Your Client (KYC) issues to be addressed. For example, simplifi ed KYC requirements for low-risk, low-value accounts and transactions would permit the remote opening of bank accounts in isolated areas, allowing non-bank agents to facilitate the opening of new accounts.

Smaller regulatory changes involving commercial banks might also be helpful. For example, an offi cial policy on dormant accounts might help reduce banks’ monthly administration fees. Policies to make it easier for banks to unilaterally close inactive, non-zero accounts could be developed, with institutional arrangements in place for the management of such accounts after they are closed. Bank Indonesia’s recent arrangement

Improving Access to Financial Services in Indonesia16

Chapter 1Executive Summary

with major commercial banks to introduce basic banking services, with the proposed launch of a new saving product called TabunganKu (My Saving) in early 2010, is also a step in the right direction. In the area of reporting requirements, annual business plans could be combined with the banks’ annual reports. Regulations concerning the relocation of branches and ATM machines are currently unnecessarily restrictive, with a reporting and approval process required even for minor relocations within the same geographical area. Instead, the regulations should require general descriptions of the location of such facilities. It would also be useful to ease offi cial regulations on the establishment of new branches, at least to bring them into line with Bank Indonesia’s current, relatively liberal interpretation of theoretically stringent regulations.

Concerning BPRs, there are several regulatory barriers that could be eased to improve access, although Bank Indonesia seems to be re-thinking policy in this area already. Consideration could be given to a lower tier of minimum start-up capital for small BPRs in remote locations. Also, NGOs and foreign investors could be allowed to participate in BPRs that are looking for capital. Reporting requirements could be revised for small BPRs in locations without adequate communications services. Written disclosure requirements could be waived in areas of low fi nancial literacy, to be replaced by oral briefi ngs for new customers, perhaps using the local language if appropriate.

As with commercial banks, Know Your Customer (KYC) regulations that demand the presentation of a full set of documentation to access fi nancial services could be eliminated or simplifi ed for small accounts. Similarly, the requirements for taxpayer numbers could be waived for small loans below a pre-specifi ed threshold. Again, as was the case with commercial banks, while the regulations regarding the establishment of new branches are theoretically quite restrictive, in practice these are interpreted fairly liberally. However, the regulations should perhaps be revised so that they refl ect actual practice. In other areas, to enforce regulations on BPRs, BI is already working hard to augment its capacity. As an additional interim step, BI might seek additional, temporary assistance by outsourcing certain tasks to fi rms that specialize in micro-fi nance, a measure for which there are already precedents, with BRI already been charged with the supervision of certain fi nancial institutions in specifi c areas. Important regulatory steps could be taken to improve the capacities of cooperatives, pawnshops and other microfi nance institutions and to ensure that they are better able to provide increased access to fi nancial services. With cooperatives, the most important issues appear to be prudential. These should be addressed on a sector-wide basis before any signifi cant problems surface and potentially erode memberships’ existing access to fi nancial services. Concurrently, there needs to be an upgrading of the MSME’s regulatory and supervisory capacity. Measures to address this could include the temporary outsourcing of certain functions to fi rms specializing in micro-fi nance.

With pawnshops, the state-owned monopoly could be offi cially opened up to competition from the private sector. At present, a number of private pawnshops are already off ering services on the fringes of legality, so opening up this sector would serve the double purpose of encouraging healthy competition and facilitating better regulation of the currently unsupervised and unregulated private pawnshops. In parallel, there needs to be a discussion on the extent to which these institutions needs to be brought under a formal regulatory umbrella, keeping in mind international experience.

With regard to other microfi nance institutions, the most productive step is probably to restore momentum to the drafting of a new Micro-Finance Law. A vital part of this process would involve encouraging public debate on the relevant issues. It is important that the new Law emphasizes facilitation and access, taking into account emerging global experience regarding regulation and supervision of such institutions. In support, linkage programs between commercial banks and BPRs could be expanded to include non-bank MFIs. In addition, it would be helpful if a similar role could be defi ned for NGOs.

17

Chapter 1Executive Summary

In the area of insurance, a stronger foundation is needed for healthy expansion of this industry, with this industry being challenged by several fundamental structural issues. In particular, the industry is currently characterized by the existence of a number of weak and unviable fi rms. This needs to be addressed before the industry can play a signifi cant role in expanding access to fi nancial services. An important exception is the micro-insurance business, which is currently expanding rapidly, with the benefi t of a successful public-private partnership. This could serve as a model for other products targeting lower income earners. There are also emerging models being developed elsewhere in the world that should be explored to determine their relevance to the Indonesian context.

This report also addresses issues relating to MSMEs and migrant workers as special topics of interest in the context of accessibility to fi nancial services. MSMEs’ issues of access to fi nancial services are virtually one-dimensional: that is, the most signifi cant issue by far involves access to credit, with the level of diffi culty being in the inverse proportion to the size of the business. While Indonesia has striven to develop policies to promote access to fi nance by MSME, there is general dissatisfaction with results to date, despite the large expenditures by the government. This is due in large part to the past emphasis of the government’s programs, which has been on subsidized credit programs. In line with international experience, these subsidized credit programs have not been overwhelmingly successful. The Government continues to make access to credit for MSMEs a major policy issue. As part of its endeavors in this regard, it has initiated the Kredit Usaha Rakyat (KUR) program as a means to consolidate the existing programs and put in place an integrated credit guarantee scheme to bring previously unbanked MSMEs into the formal banking sector. While a formal review of this program was underway at the time of writing of this report, the Government has also announced a signifi cant scaling up of the program. Depending upon the results of the assessment, the government may consider strengthening or modifying the existing KUR program.

Issues related to migrant workers and their access to fi nancial services are also high on the Government’s agenda. From an access to fi nance perspective, this group should be of particular interest to fi nancial institutions, given the large remittances that these workers send home. In general, in several areas, to assist migrant workers, Indonesia could seek to re-negotiate the terms of its Memoranda of Understanding on Migrant Workers with recipient countries3 in order to better balance the interests of the workers themselves with the interests of employers and recruitment agencies. From the perspective of increasing access to fi nancial services, specifi c points of negotiation could include a discussion of acceptable forms of identifi cation and the exemption of small transfers from these formal identifi cation requirements keeping in mind global AML/CFT eff orts.

To convince banks of the commercial value of this market, it might be useful to explore the possibility of developing innovative public private partnerships to bring greater segments of these workers into the formal fi nancial sector. One possibility is to encourage the wider use of domestic guarantors (or co-signers) for pre-departure loans to migrant workers. Development partners (or NGOs) with particular interests in migrant worker issues might consider acting as a guarantor in pilot projects that may perhaps later be scaled up. Another possibility would be steps to encourage the design of innovative savings instruments that would permit these workers to save their earnings for use over a longer period of time.

The Way Ahead

In order to facilitate fi nancial inclusion in a manner that truly meets the needs of lower income earners, it is clear that the government must strive to improve access to a broad range of fi nancial services, rather than merely focusing on improved access to credit. A number of developing countries have implemented

3 A recent World Bank study makes several practical suggestions in this regard; see The Malaysia-Indonesia Remittance Corridor (2008a).

Improving Access to Financial Services in Indonesia18

Chapter 1Executive Summary

policies and strategies to achieve this result. Access to fi nance is an issue that involves a number of diff erent stakeholders, including government agencies and authorities such as Bank Indonesia, Bapepam-LK, Ministry of Finance, Ministry of Cooperatives and SMEs; fi nancial institutions from the private sector, including state owned and private banks, non-bank fi nancial institutions; and NGOs, foundations, development agencies and think-tanks working in this area. Technology and education will play a key role in scaling up access rapidly. Thus, telecommunications service providers, academic institutions and fi nancial literacy providers are also signifi cant stake holders. Indonesia’s international development partners can provide knowledge and fi nancial inputs. With all these stakeholders working together, it is possible to signifi cantly improve access to fi nancial services by a large segment of the population. In the short and medium term, this will provide signifi cant benefi ts both to the individuals who are able to access the services and to the fi nancial institutions that provide them. In the longer term, improving access to fi nancial services in this fashion will facilitate the achievement of broader economic development and poverty alleviation goals.

19

Chapter 2

The Current Supply of Financial Services in Indonesia

This Chapter looks at the current supply of fi nancial services in Indonesia. It begins with an overview of the Indonesian fi nancial sector and attempts to put the diff erent service providers in context, particularly in terms of the diff erent segments that each of the varying service providers caters to.

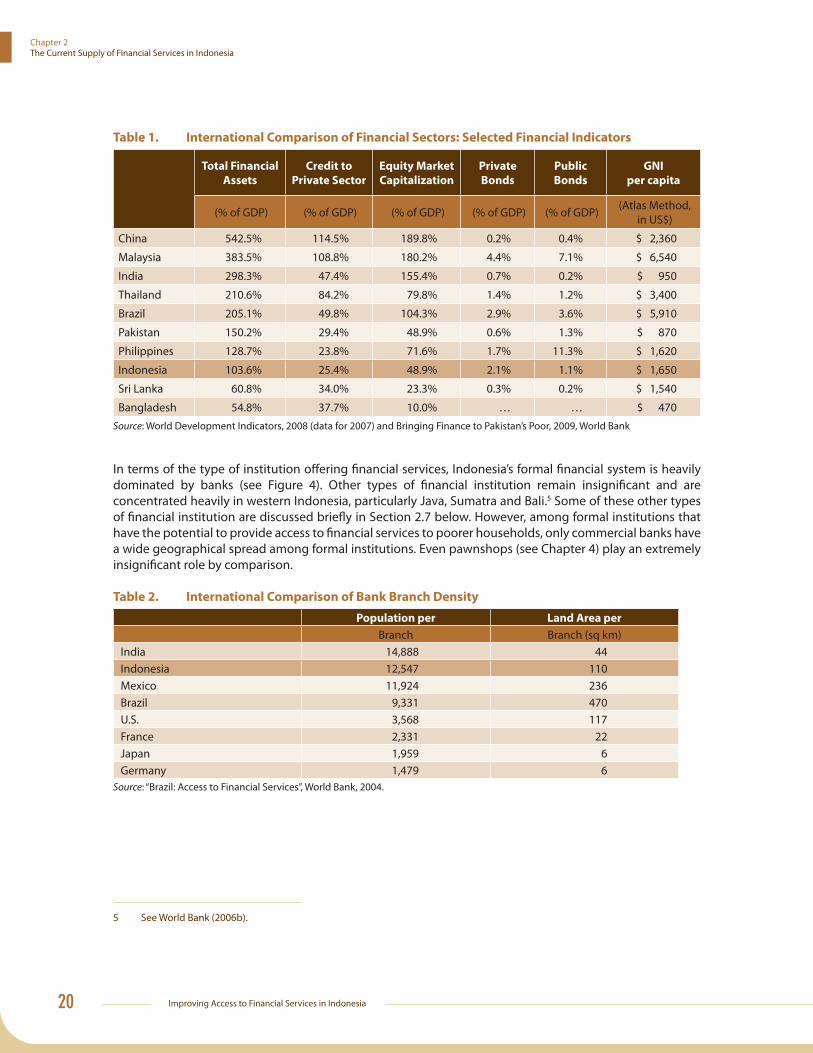

2.1 Overview of Indonesia’s Financial SectorBy international standards, Indonesia’s fi nancial sector is still small in relation to GDP (see Table 1 and World Bank [2006a]). In terms of the nation’s total fi nancial assets, the size of the fi nancial sector is equivalent to only slightly more than 100% of GDP. This is considerably less than the size of the fi nancial sectors in large Asian economies such as those of India and China, where the equivalent fi gures are 300% and 500% respectively. Rather, the size of Indonesia’s fi nancial sector is barely comparable to those of countries such as the Philippines and Pakistan. Among other indicators, as a proportion of national GDP, the value of credit made available by Indonesian banks to the private sector is lower than almost any other comparable country in the region (Table 1). In addition, in terms of the geographical area and the number of people served by each branch, Indonesia has a relatively low rate of bank branch density (Table 2).4 The number of people served by each branch is high relative to that in other comparable countries, while the geographical territory is served by each branch is about average, although notably lower than Mexico and Brazil.

4 The data in Table 2 include BRI’s Unit Desa system, which account for almost 1/3 of all bank branches in Indonesia.

Improving Access to Financial Services in Indonesia20

Chapter 2The Current Supply of Financial Services in Indonesia

Table 1. International Comparison of Financial Sectors: Selected Financial Indicators

Total Financial

Assets

Credit to

Private Sector

Equity Market

Capitalization

Private

Bonds

Public

Bonds

GNI

per capita

(% of GDP) (% of GDP) (% of GDP) (% of GDP) (% of GDP) (Atlas Method, in US$)

China 542.5% 114.5% 189.8% 0.2% 0.4% $ 2,360

Malaysia 383.5% 108.8% 180.2% 4.4% 7.1% $ 6,540

India 298.3% 47.4% 155.4% 0.7% 0.2% $ 950

Thailand 210.6% 84.2% 79.8% 1.4% 1.2% $ 3,400

Brazil 205.1% 49.8% 104.3% 2.9% 3.6% $ 5,910

Pakistan 150.2% 29.4% 48.9% 0.6% 1.3% $ 870

Philippines 128.7% 23.8% 71.6% 1.7% 11.3% $ 1,620

Indonesia 103.6% 25.4% 48.9% 2.1% 1.1% $ 1,650

Sri Lanka 60.8% 34.0% 23.3% 0.3% 0.2% $ 1,540

Bangladesh 54.8% 37.7% 10.0% … … $ 470

Source: World Development Indicators, 2008 (data for 2007) and Bringing Finance to Pakistan’s Poor, 2009, World Bank

In terms of the type of institution off ering fi nancial services, Indonesia’s formal fi nancial system is heavily dominated by banks (see Figure 4). Other types of fi nancial institution remain insignifi cant and are concentrated heavily in western Indonesia, particularly Java, Sumatra and Bali.5 Some of these other types of fi nancial institution are discussed briefl y in Section 2.7 below. However, among formal institutions that have the potential to provide access to fi nancial services to poorer households, only commercial banks have a wide geographical spread among formal institutions. Even pawnshops (see Chapter 4) play an extremely insignifi cant role by comparison.

Table 2. International Comparison of Bank Branch Density

Population per Land Area per

Branch Branch (sq km)India 14,888 44Indonesia 12,547 110Mexico 11,924 236Brazil 9,331 470U.S. 3,568 117France 2,331 22Japan 1,959 6Germany 1,479 6

Source: “Brazil: Access to Financial Services”, World Bank, 2004.

5 See World Bank (2006b).

21

Chapter 2 The Current Supply of Financial Services in Indonesia

Figure 4. Financial Structure (December 2008)

Rural Inst, Pawnshop, VC

2%

Mutual Funds 2%

Securities Firm 2%

Finance Companies 5%

Insurer 6%

Pension Funds 4%

Banks 79%

Source: Bank Indonesia, Bapepam LK, Ministry of Cooperatives, Association, Infobank magazine

2.2 The Commercial Banking SystemSince the fi nancial crisis of 1997/98, there have been signifi cant changes in the composition of fi nancial institutions in Indonesia in terms of the number and range of service providers and the number of branches operated by these providers. In particular, the number of commercial banks (especially private banks; see Figure 5), people’s credit banks (BPRs) and multi-fi nance companies have all declined markedly (Table 3). This is largely a result of government policies aimed at consolidating the number of institutions in these sub-sectors (see Chapter 4).6 By contrast, the numbers of bank branches, bank ATMs, pawnshop branches and cooperatives have all increased signifi cantly (Table 3).

Figure 5. Total Banks by Type of Bank

0

20

40

60

80

100

120

140

160

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Num

bers

State Owned Banks Private Com. BanksRegional Banks Foreign & Joint Banks

Source: Bank Indonesia

6 For example, during 2007, Bank Indonesia approved 105 BPRs for consolidation into 19 entities and 5 others had their operating licenses revoked. BI issued approvals in principle for 27 new ones (Bank Indonesia (2007), p. 131).

Improving Access to Financial Services in Indonesia22

Chapter 2The Current Supply of Financial Services in Indonesia

This change in composition has been defi ned by at least two key signifi cant characteristics. First, although the number of fi nancial service providers, including both banks and BPR, has fallen, the reach of existing fi nancial service providers has increased signifi cantly. For example, the number of bank branches has increased by 70% since 2000, while the number of ATMs has almost tripled (Figure 6). Secondly, the expansion has been most signifi cant amongst institutions that serve lower income groups, particularly cooperatives and pawnshops. At the same time, when formal banks have expanded, they have often done so by expanding low-cost facilities, such as new branches, ATMs and mobile banking facilities. It is likely that the expansion of such facilities is making these banks increasingly better positioned to serve lower end markets.

Table 3. Indonesia, Number of Financial Institutions

Banks Bank Branches,

including cash

offi ces

Bank

ATMs

BPRs Venture

Capital

Multi-

fi nance

Pawnshop

(branches)

Cooperatives

2000 151 6,374 7,114 2,419 59 245 692 103,077

2001 145 6,657 8,997 2,355 60 245 722 110,766

2002 142 6,844 10,613 2,143 60 244 739 118,644

2003 138 7,554 11,837 2,141 60 239 774 123,181

2004 134 7,808 13,772 2,158 60 237 806 130,730

2005 131 7,918 15,862 2,009 60 237 840 134,963

2006 131 8,980 16,991 1,880 60 214 869 141,326

2007 130 9,535 18,596 1,817 60 211 899 147,000

2008 124 10,868 20,792 1,772 60 210 1,331 149,913Source: BI, Bapepam-LK, Annual Report of Perum Pegadaian, Ministry of Cooperatives & SMEs

23

Chapter 2 The Current Supply of Financial Services in Indonesia

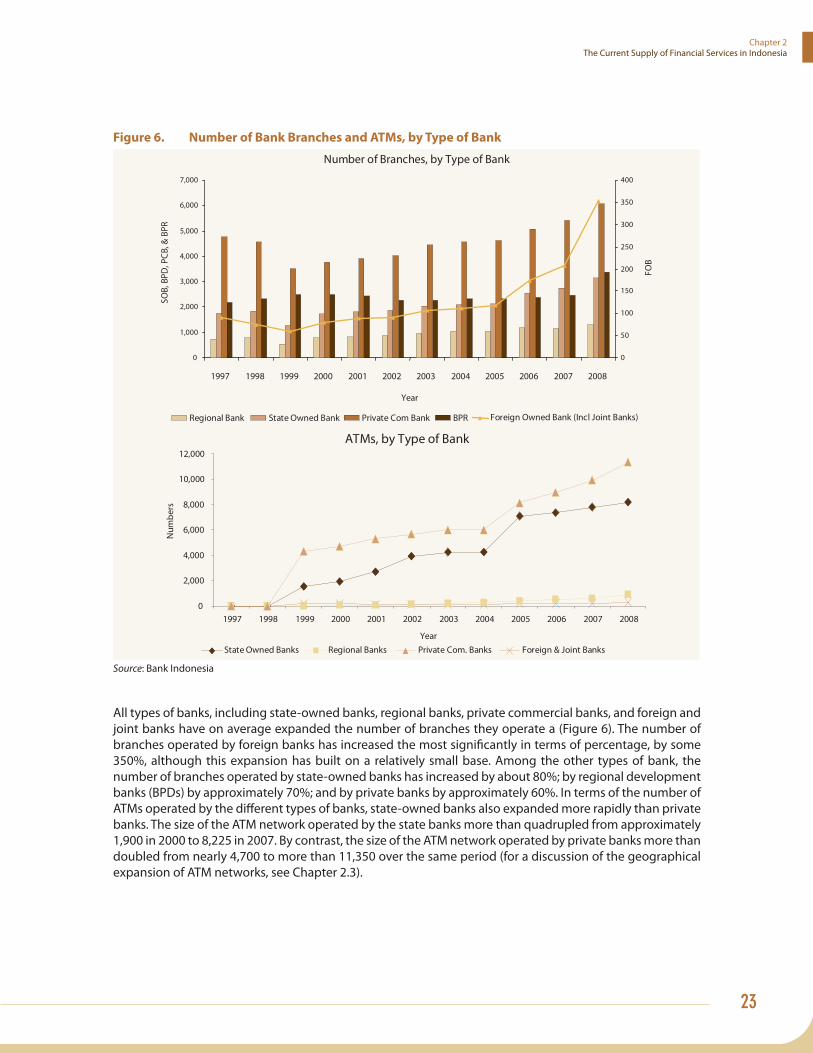

Figure 6. Number of Bank Branches and ATMs, by Type of Bank

Number of Branches, by Type of Bank

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Year

SOB,

BPD

, PC

B, &

BPR

0

50

100

150

200

250

300

350

400

FOB

Regional Bank State Owned Bank Private Com Bank BPR Foreign Owned Bank (Incl Joint Banks)

ATMs, by Type of Bank

0

2,000

4,000

6,000

8,000

10,000

12,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Year

Num

bers

State Owned Banks Regional Banks Private Com. Banks Foreign & Joint Banks

Source: Bank Indonesia

All types of banks, including state-owned banks, regional banks, private commercial banks, and foreign and joint banks have on average expanded the number of branches they operate a (Figure 6). The number of branches operated by foreign banks has increased the most signifi cantly in terms of percentage, by some 350%, although this expansion has built on a relatively small base. Among the other types of bank, the number of branches operated by state-owned banks has increased by about 80%; by regional development banks (BPDs) by approximately 70%; and by private banks by approximately 60%. In terms of the number of ATMs operated by the diff erent types of banks, state-owned banks also expanded more rapidly than private banks. The size of the ATM network operated by the state banks more than quadrupled from approximately 1,900 in 2000 to 8,225 in 2007. By contrast, the size of the ATM network operated by private banks more than doubled from nearly 4,700 to more than 11,350 over the same period (for a discussion of the geographical expansion of ATM networks, see Chapter 2.3).

Improving Access to Financial Services in Indonesia24

Chapter 2The Current Supply of Financial Services in Indonesia

Box 1. The Role of State Vs. Private Banks in Indonesia

Prior to the fi nancial deregulation drive in the 1980s, Indonesia’s seven state banks dominated the local fi nancial sector. This was largely due to the establishment of these banks on the basis of the nationalization of Dutch banks in the 1950s and 1960s. Each state bank had a somewhat specialized focus, with offi cial statements underscoring their ‘social and development role’. For example, Bank Ekspor Impor (ExIm) focused on international trade and fi nance; Bank Pembangunan Indonesia (Bapindo) was a development bank; Bank Tabungan Negara focused on facilitating the needs of housing development; and Bank Rakyat Indonesia (BRI) concentrated on the provision of rural credit. The other three, Bank Dagang Nasional (BDN), Bank Bumi Daya (BDN) and Bank Negara Indonesia (BNI; the fi rst and largest) leaned more towards the provision of services to the corporate sector.

On a system-wide basis, licensing, credit and interest rates were tightly regulated by the central bank. There were also a large number of central bank re-fi nancing schemes targeting politically important sectors. All of the state banks—some more than others—suff ered internal governance problems. Much of this changed during the 1980s, when a series of so-called deregulation packages lowered entry barriers and increased the level of competition in the sector (see, for example, Cole and Slade [1996] and Binhadi [1995]). The state banks lost market share rapidly, although their offi cial roles were little changed.

Two subsequent developments had a major impact on the role, composition, and structure of the state banks. The fi rst was the fi nancial crisis of 1997/98, which led to the merger of Bank Exim, BDN, BBD and Bapindo into Bank Mandiri. The second was a series of partial privatizations through the listing of the state-owned banks on public stock exchanges and the release of minority stake holdings on these exchanges, beginning with the listing of the BNI in 1996. Within a decade or so, all the state-owned banks except BTN had been partially privatized. During this same period, critical changes were made to the management of a number of state banks, with these changes improving internal governance appreciably.

Today, of the state banks, only BTN and BRI largely retain specialized roles. Bank Mandiri and BNI operate in direct competition with the private banks, with few special privileges. The state banks main advantages are at present mainly derived from their size. Mandiri is the largest bank in the country, accounting for almost 16% of the total assets of the fi nancial sector. BRI and BNI occupy third and fourth place respectively, with each controlling a market share of approximately 10%. BRI has an operational advantage over other banks in the fi eld of micro-fi nance because of its extremely wide network of branches that reach down to the village level, with the width of this network making it diffi cult for any newcomer to challenge this banks position. Nevertheless, and despite the large growth in the number of branches and facilities such as ATMs (noted in the main text), the share of the state banks’ assets in the banking sector has continued to decline over the long-term. By 2007, the share of the state banks assets have declined to 37%, compared with 49% in 2001 and almost 80% in the early 1980s.

It should also be mentioned that the government, as the majority shareholder, still makes occasional special demands of state banks. For example, the state-owned banks are often the target of ‘moral suasion’ when particular policies prove diffi cult to implement by conventional means; the source of temporary expertise in times of crisis, for instance when weak banks need to be closed; and the leading edge of special programs, like the Kredit Usaha Rakyat (KUR) and the Linkage Program between commercial banks on the one side and BPRs and cooperatives on the other.

25

Chapter 2 The Current Supply of Financial Services in Indonesia

2.3 Regional Reach of Indonesia’s Commercial BanksIn a country as large and diverse as Indonesia, when examining issues related to access to fi nancial services, it is very important to look at the regional distribution of commercial bank services. Unfortunately, data on the dispersion of banking services is not available in suffi cient detail to permit a robust spatial analysis across the country. For many purposes, data for provinces and special regions, such as DKI Jakarta, are the best that available. However, these data played a great deal of residual diversity in and between Jakarta, Banten and East Java, for example.

Using a relatively coarse indicator (see Figure 7), it is obvious that the density of bank outlets is considerably higher in the more heavily populated regions. Specifi cally, it is highest in Jakarta, West Java, Central Java and East Java. It is arguable whether this unequal distribution of bank services can be accounted for by population (or land mass) and income levels.

Figure 7. Bank Head Offi ces & Branches, by Province

-100

100

300

500

700

900

1100

1300

1500

1700

1900

2100

2300

2500

2700

Aceh

West Sumatera

Jambi

Bengkulu

Bangka Belitu

ng

Jakarta

Banten

Yogyakarta Bali

East Nusa Tenggara

Central K

alimantan

East Kalim

antan

Gorontalo

South Sulawesi

Southeast Sulawesi

North M

aluku

Papua

Head Quarters

Source: Bank Indonesia

To investigate this issue, the number of branches and branch density existing at the end of 2006 are regressed in terms of real per capita GDP on a provincial basis. The results are presented in Figure 8 with branch density measured in two ways: on a population-adjusted basis (see the middle panel in Figure 8) and on a land areas basis (see the lower panel in Figure 8).7

7 The size of the bubble in the top panel of Figure 8 indicates the relative size of GDP in that province. In the middle panel, it indicates relative population; in the lower panel, relative land mass.

Improving Access to Financial Services in Indonesia26

Chapter 2The Current Supply of Financial Services in Indonesia

Figure 8. Bank Branches & Density Vs. Per Capita Income, by Province

Riau Riau Islands

Jakarta

West Java

Central Java

East Java

Bali East Kalimantan

-250

250

750

1250

1750

2250

2750

-1500 3500 8500 13500 18500 23500 28500 33500 38500

Bran

ches

Total Branches, at Dec 2006

Riau

Riau Islands

Jakarta

Central Java

East Java

Bali

East Kalimantan

-1

4

9

14

19

24

29

-1500 3500 8500 13500 18500 23500 28500 33500 38500

Tota

l Bra

nche

s pe

r 100

,000

pe

rson

s

Branch Density per 100,000 persons, at December 2006

Riau

Riau Islands

Jakarta

East Kalimantan

North Maluku

Papua

-600

400

1400

2400

3400

-1500 3500 8500 13500 18500 23500 28500 33500 38500

Tota

l Bra

nche

s pe

r 1,0

00 k

m2

Constant GDP per Capita (IDR Thousand)

Branch Density per 1,000 sq km persons, at December 2006

Source: Bank Indonesia, BPS, staff calculation

27

Chapter 2 The Current Supply of Financial Services in Indonesia

As indicated in Figure 8, there is clearly a strong positive correlation between the number of branches and branch density and real per capita income. The relationships are all statistically signifi cant (t statistics on real capita GDP ranging from 2.3 to 5.1), with reasonably good fi ts (R2s ranging from .38 to .67). Statistical signifi cance and fi ts are better for branch density (that is, for the lower 2 panels in Figure 8) than for the number of branches. This implies that adjusting for land mass or population is helpful in explaining the relationship.

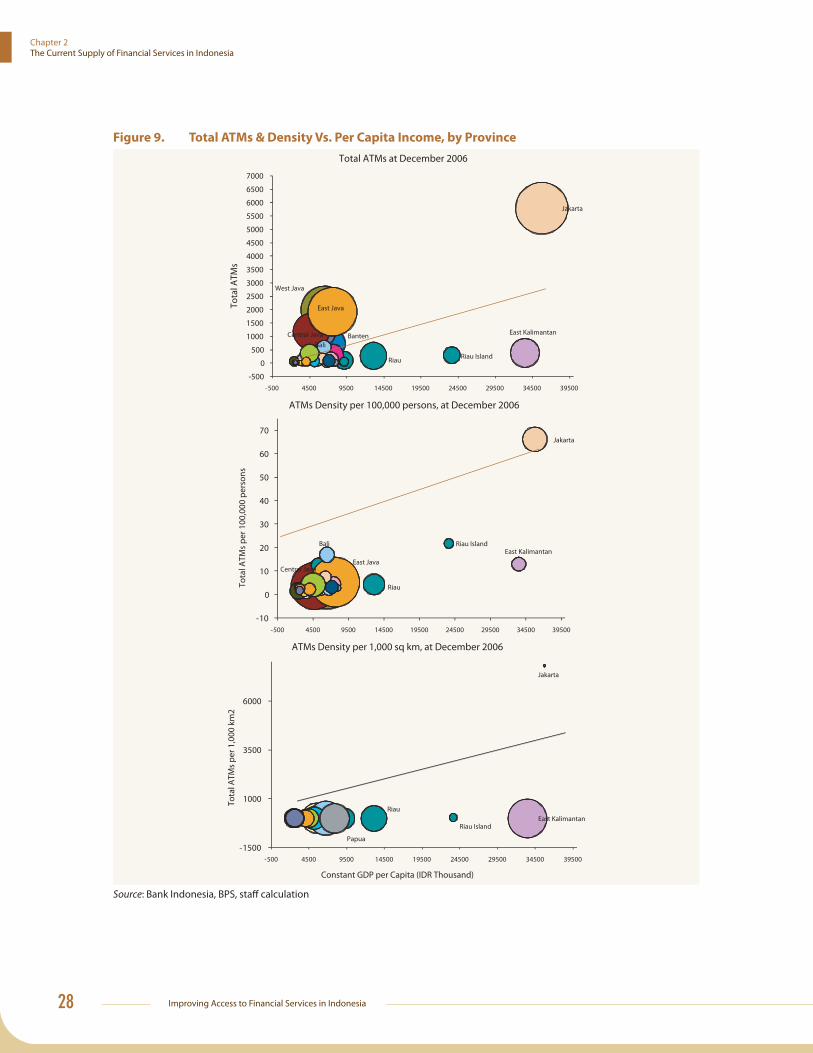

Exactly the same conclusions hold when ATMs are used as the metric instead of bank branches (see Figure 9). Indeed, the statistical fi ts are slightly tighter and the statistical signifi cance slightly higher. This is important for policy purposes. Specifi cally, the relatively low-cost of service provided by ATMs is more responsive to income levels than are the relatively high-cost services provided by bank branches. By implication, if service costs can be further reduced through means such as mobile banking, it is likely that banks would become more deeply involved in regional markets.

Looking at Figures 8 and 9, it is clear that Jakarta is consistently a large, high-side outlier. Jakarta has far more bank branches and ATMs than would be expected on the basis of population, land mass and income. All other provinces8 fall more or less in line with expectations after adjustment for income and population or land mass.

How can the fi gures for Jakarta be explained? Two explanations are plausible. First, agglomeration theory (see the World Development Report 2009) postulates that economic development tends to occur disproportionately in clusters. Specifi cally, economic development is likely to occur in relatively small, densely-populated regions like Jakarta. The second explanation concerns income inequality. The relatively large number of very wealthy people and businesses in Jakarta probably lead to a disproportionately large number of bank services in that region. This underlines the fact that the use of average income as an explanatory variable doesn’t necessarily capture the eff ect.

And what can be said by way of policy conclusions? This analysis provides strong prima facie evidence that variations in the existing supply of fi nancial services at the provincial level are largely explained by variation in population, land mass and income. Only Jakarta and East Kalimantan are clear exceptions, Jakarta being ‘over-serviced’ and East Kalimantan ‘under-serviced’. By implication, targeted eff orts on ‘fi nancially under-served’ areas will need to operate below the provincial level and they will need to take clear account of banks’ demonstrated capacity to respond to broad market conditions.

8 Another exception is the resource rich, but sparsely populated province of East Kalimantan. It is consistently a low-side outlier, implying that it has fewer bank branches and ATMs than would be expected on the basis of income, population and land mass.

Improving Access to Financial Services in Indonesia28

Chapter 2The Current Supply of Financial Services in Indonesia

Figure 9. Total ATMs & Density Vs. Per Capita Income, by Province

Riau Riau Island

Jakarta

West Java

BantenCentral Java

East Java

Bali

East Kalimantan

-500

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

6500

7000

-500 4500 9500 14500 19500 24500 29500 34500 39500

Tota

l ATM

s

Total ATMs at December 2006

Riau

Riau Island

Jakarta

Central JavaEast Java

BaliEast Kalimantan

-10

0

10

20

30

40

50

60

70

-500 4500 9500 14500 19500 24500 29500 34500 39500

Tota

l ATM

s pe

r 100

,000

per

sons

ATMs Density per 100,000 persons, at December 2006

Riau

Riau Island

Jakarta

East Kalimantan

Papua-1500

1000

3500

6000

-500 4500 9500 14500 19500 24500 29500 34500 39500

Tota

l ATM

s pe

r 1,0

00 k

m2

Constant GDP per Capita (IDR Thousand)

ATMs Density per 1,000 sq km, at December 2006

Source: Bank Indonesia, BPS, staff calculation

29

Chapter 2 The Current Supply of Financial Services in Indonesia

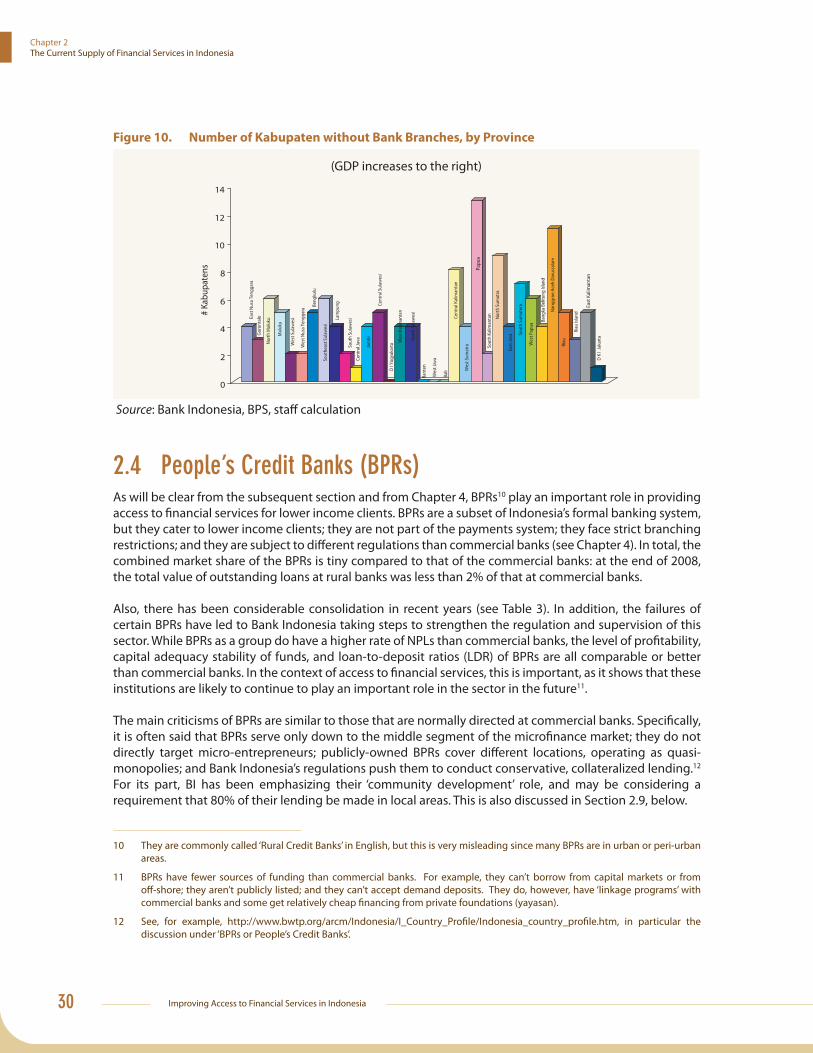

Some data are available on the number of local jurisdictions (kabupaten in rural areas and kotamadya in urban areas) with no commercial bank branches. Surprisingly, this number has gone up substantially from 16 in 1997 to 156 in 2007 (Table 4). Upon closer inspection, this larger number appears to be entirely due to the creation of new local government jurisdictions, with the total number of such jurisdictions having increased from nearly 314 to 464 over the same period (Table 4). By contrast, the number of local jurisdictions with branches has remained fairly constant at around 300. On this basis, it seems clear that banks do not move into new regions just because political boundaries have been re-defi ned. Rather, the decision to open new branches is based upon commercial viability, which is normally insensitive to political segmentation of existing jurisdictions.

Table 4. Number of Kabupaten/Kotamadya With and Without Branches of Commercial Banks

Year # of Kabupaten/

Kotamadya

with Branches

Total Kabupaten/

Kotamadya

Percentage # of Kabupaten/

Kotamadya

with no Branches

Percentage

1997 298 314 94.9% 16 5.1%

1998 304 314 96.8% 10 3.2%

1999 299 316 94.6% 17 5.4%

2000 306 334 91.6% 28 8.4%

2001 268 349 76.8% 81 23.2%

2002 304 362 84.0% 58 16.0%

2003 303 384 78.9% 81 21.1%

2004 311 424 73.3% 113 26.7%

2005 305 448 68.1% 143 31.9%

2006 309 448 69.0% 139 31.0%

2007 308 464 66.4% 156 33.6%

Source: Bank Indonesia, Ministry of Home Aff airs, Decentralization Support Facility and World Bank Estimates

The regional distribution of the local jurisdictions without a branch of a commercial bank provides additional evidence that Indonesia’s banks are sensitive to commercial opportunities as measured by population density. Most ‘unserved kabupaten’ are in the relatively remote, sparsely populated provinces of Papua, Kalimantan and Sulawesi (see Figure 10).9 However, there is no strong relationship between ‘unserviced’ locations and per capita income (see Figure 10).

9 The ‘unserviced’ jurisdictions were Sumatra (56); Sulawesi (23); Kalimantan (22); the Papua island group (19); the Malukus (11); and Nusa Tenggara (6). As of 2007, there were only a handful (6) on Java and none on Bali.

Improving Access to Financial Services in Indonesia30

Chapter 2The Current Supply of Financial Services in Indonesia

Figure 10. Number of Kabupaten without Bank Branches, by Province

(GDP increases to the right)

East

Nus

a Te

ngga

ra

Goro

ntal

o

Nor

th M

aluk

u

Mal

uku

Wes

t Sul

awes

i

Wes

t Nus

a Te

ngga

ra

Beng

kulu

Sout

heas

t Sul

awes

i

Lam

pung

Sout

h Su

law

esi

Cent

ral J

ava

Jam

bi

Cent

ral S

ulaw

esi

D I

Yogy

akar

ta

Wes

t Kal

iman

tan

Nor

th S

ulaw

esi

Bant

en

Wes

t Jav

a

Bali

Cent

ral K

alim

anta

n

Wes

t Sum

atra

Papu

a

Sout

h Ka

liman

tan

Nor

th S

umat

ra

East

Java So

uth

Sum

ater

a

Wes

t Pap

ua

Bang

ka B

elitu

ng Is

land

Nan

ggro

e Ac

eh D

arus

sala

m

Riau

Riau

Isla

nd

East

Kal

iman

tan

D K

I Ja

kart

a

0

2

4

6

8

10

12

14

# Ka

bupa

tens

Source: Bank Indonesia, BPS, staff calculation

2.4 People’s Credit Banks (BPRs)As will be clear from the subsequent section and from Chapter 4, BPRs10 play an important role in providing access to fi nancial services for lower income clients. BPRs are a subset of Indonesia’s formal banking system, but they cater to lower income clients; they are not part of the payments system; they face strict branching restrictions; and they are subject to diff erent regulations than commercial banks (see Chapter 4). In total, the combined market share of the BPRs is tiny compared to that of the commercial banks: at the end of 2008, the total value of outstanding loans at rural banks was less than 2% of that at commercial banks.

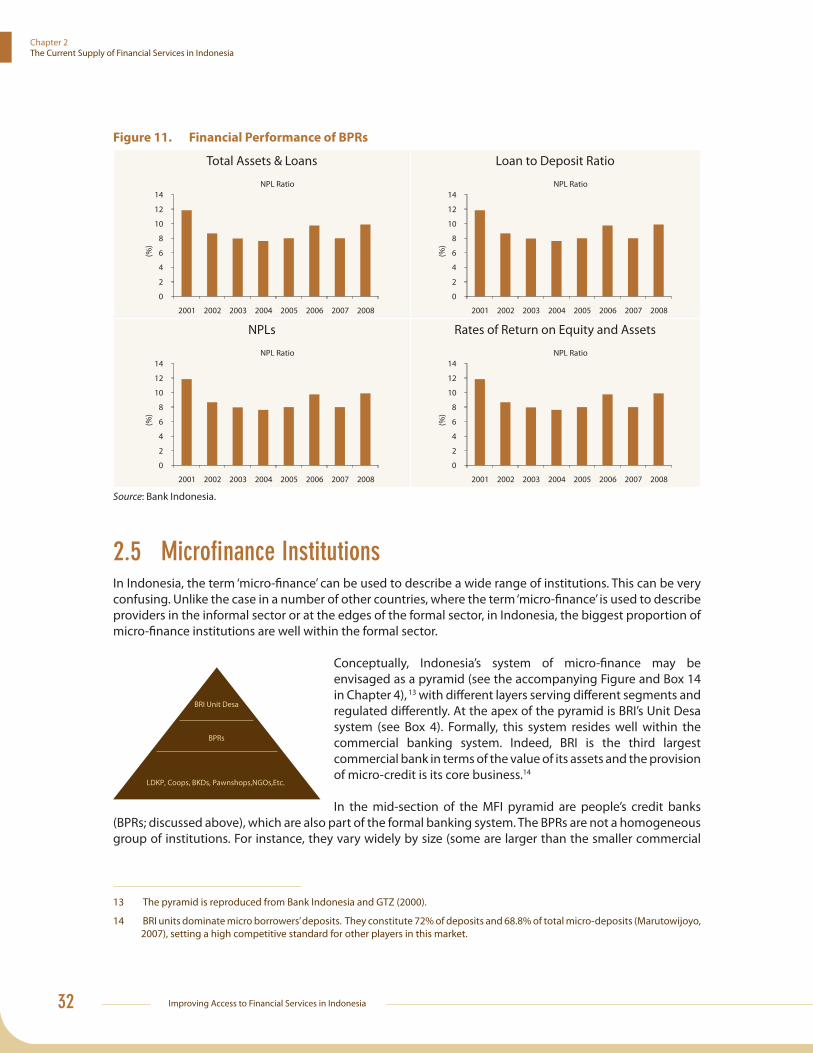

Also, there has been considerable consolidation in recent years (see Table 3). In addition, the failures of certain BPRs have led to Bank Indonesia taking steps to strengthen the regulation and supervision of this sector. While BPRs as a group do have a higher rate of NPLs than commercial banks, the level of profi tability, capital adequacy stability of funds, and loan-to-deposit ratios (LDR) of BPRs are all comparable or better than commercial banks. In the context of access to fi nancial services, this is important, as it shows that these institutions are likely to continue to play an important role in the sector in the future11.

The main criticisms of BPRs are similar to those that are normally directed at commercial banks. Specifi cally, it is often said that BPRs serve only down to the middle segment of the microfi nance market; they do not directly target micro-entrepreneurs; publicly-owned BPRs cover diff erent locations, operating as quasi-monopolies; and Bank Indonesia’s regulations push them to conduct conservative, collateralized lending.12 For its part, BI has been emphasizing their ‘community development’ role, and may be considering a requirement that 80% of their lending be made in local areas. This is also discussed in Section 2.9, below.

10 They are commonly called ‘Rural Credit Banks’ in English, but this is very misleading since many BPRs are in urban or peri-urban areas.

11 BPRs have fewer sources of funding than commercial banks. For example, they can’t borrow from capital markets or from off -shore; they aren’t publicly listed; and they can’t accept demand deposits. They do, however, have ‘linkage programs’ with commercial banks and some get relatively cheap fi nancing from private foundations (yayasan).

12 See, for example, http://www.bwtp.org/arcm/Indonesia/I_Country_Profi le/Indonesia_country_profi le.htm, in particular the discussion under ‘BPRs or People’s Credit Banks’.

31

Chapter 2 The Current Supply of Financial Services in Indonesia

Box 2. BRI’s MASS Survey: Insights to Banks’ Capacity to Reach the Poor

As noted in the main text, Bank Rakyat Indonesia (BRI) is Indonesia’s premier lender to MSMEs, having built upon a long history of micro-lending in Indonesia (see Box 4). In the fall of 2002, BRI conducted a Microfi nance Access and Services Survey (MASS) of 1438 households in six provinces (roughly half the size of the Survey of Chapter 3) to map the fi nancial landscape and to gauge potential markets. The enumerators were BRI loan offi cers and other staff . The survey, which provided a unique opportunity to assess the creditworthiness of households using BRI’s standard commercial procedures, included other detailed information on assets, businesses and economic and social changes. Many of the results are useful for the purposes of this report, as summarized immediately below.