Embed Size (px)

Citation preview

Improving Access to Finance for Dairy Farmers in Nicaragua

Authors:

Chris Parks, Hiroki Ichikawa, Matheus Terentin, Namiko Sawaki, Natalie

Souffront, Sebastian Posada, and Zhiyue Tu

Faculty Advisor:

Dr. Sara Guerschanik Calvo Prepared for the Inter-American Development Bank by Columbia University, School of International and Public Affairs Spring 2016 Capstone Team

Table of Contents

Executive Summary ....................................................................................................................3

1. Introduction .....................................................................................................................7

1.1 Background and Purpose of the Project ............................................................................ 7

2. Milk Market .....................................................................................................................9

2.1 International Market.......................................................................................................... 9

2.1.1 Current Situation (Actors and Economic Issues) ................................................................ 9

2.1.2 Global Responses ........................................................................................................... 11

2.2 Domestic Market .............................................................................................................. 13

2.2.1 Market Size .................................................................................................................... 13

2.2.2 Domestic Market Characteristics .................................................................................... 14

2.2.3 Nicaraguan Export Market .............................................................................................. 15

3. Value Chain Description .................................................................................................16

3.1 Value Chain and Stakeholders Defined ........................................................................... 17

4. Key Stakeholder Analysis ...............................................................................................20

4.1 Producers .......................................................................................................................... 20

4.1.1 Producer (Associate) Profile............................................................................................ 20

4.1.2 Producers and Credit ...................................................................................................... 23

4.2 Nicacentro (Cooperatives) ................................................................................................ 25

4.2.1 Cooperatives and incentives to be a member ................................................................. 25

4.2.2 Nicacentro and Strategy ................................................................................................. 26

4.2.3 Nicacentro Market Constraints and Infrastructure Needs ............................................... 27

4.3 Banking Sector ................................................................................................................. 29

4.3.1 Banco Produzcamos ....................................................................................................... 30

4.3.2 FDL (Fondo de Desarrollo Local) ..................................................................................... 32

4.3.3 FUNDESER ...................................................................................................................... 33

4.3.4 Loan strategy for Nicacentro .......................................................................................... 34

5. Strategies for Lending Options ..........................................................................................35

5.1 Financing Channels .......................................................................................................... 35

5.2 Financial Model ................................................................................................................ 36

5.2.1 Rationale of the Model ................................................................................................... 36

5.2.2 Assumptions ................................................................................................................... 36

5.2.3 Expected Outcomes ........................................................................................................ 37

5.2.4 Individual loan structures ............................................................................................... 38

5.2.5 Credit Model using a Guarantee fund ............................................................................. 40

6. Conclusion .........................................................................................................................45

Bibliography .............................................................................................................................47

1

2

List of Figures

Figure 1: Global Dairy Trade Price Index .............................................................................................. 10

Figure 2: Government programs for dairy markets ................................................................................. 13

Figure 3: Nicacentro Value Chain .......................................................................................................... 16

Figure 4: Average Cow Productivity ...................................................................................................... 21

Figure 5: Summary of term of loan and interest rate for visited financial institutions .............................. 29

Figure 6: FDL Methods for Loan Servicing ........................................................................................... 32

Figure 7: Lending Channel Comparison ................................................................................................. 35

Figure 8: Model assumptions ................................................................................................................. 37

Figure 9: Calculated performance of lending.......................................................................................... 38

Figure 10: Payoff Profile of two loan types ............................................................................................ 40

Figure 11: Performance at 2% and 1% Excess Spread ............................................................................ 44

3

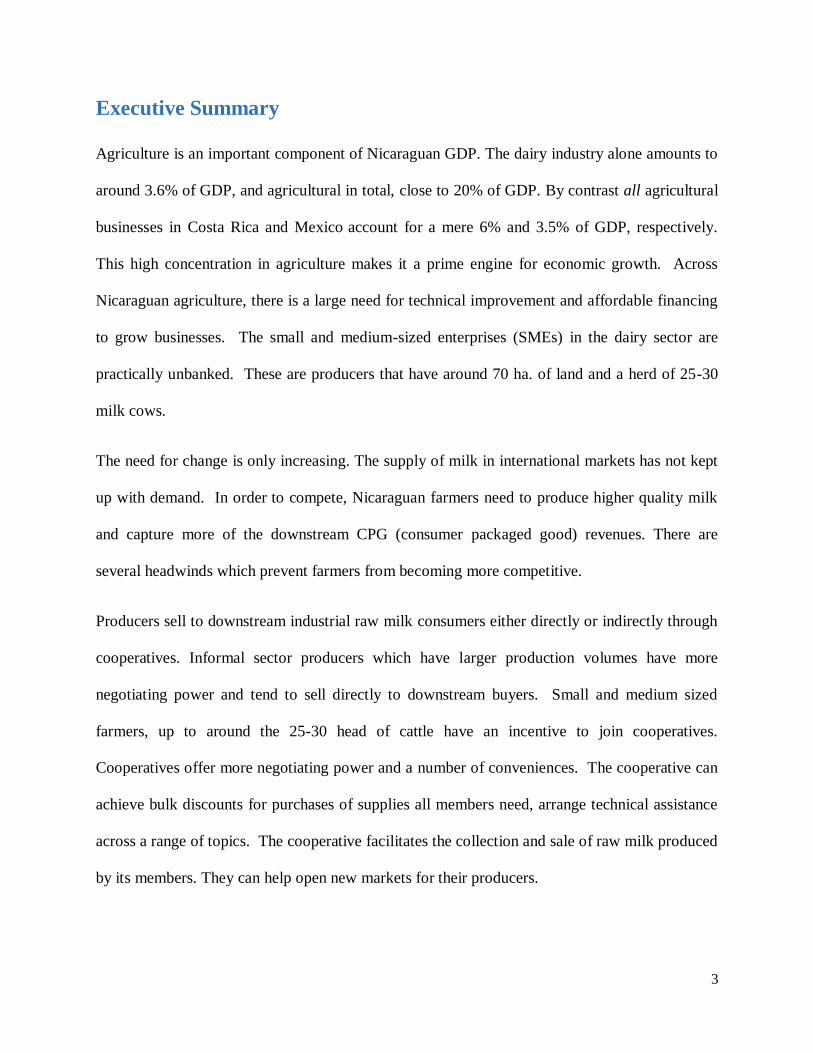

Executive Summary

Agriculture is an important component of Nicaraguan GDP. The dairy industry alone amounts to

around 3.6% of GDP, and agricultural in total, close to 20% of GDP. By contrast all agricultural

businesses in Costa Rica and Mexico account for a mere 6% and 3.5% of GDP, respectively.

This high concentration in agriculture makes it a prime engine for economic growth. Across

Nicaraguan agriculture, there is a large need for technical improvement and affordable financing

to grow businesses. The small and medium-sized enterprises (SMEs) in the dairy sector are

practically unbanked. These are producers that have around 70 ha. of land and a herd of 25-30

milk cows.

The need for change is only increasing. The supply of milk in international markets has not kept

up with demand. In order to compete, Nicaraguan farmers need to produce higher quality milk

and capture more of the downstream CPG (consumer packaged good) revenues. There are

several headwinds which prevent farmers from becoming more competitive.

Producers sell to downstream industrial raw milk consumers either directly or indirectly through

cooperatives. Informal sector producers which have larger production volumes have more

negotiating power and tend to sell directly to downstream buyers. Small and medium sized

farmers, up to around the 25-30 head of cattle have an incentive to join cooperatives.

Cooperatives offer more negotiating power and a number of conveniences. The cooperative can

achieve bulk discounts for purchases of supplies all members need, arrange technical assistance

across a range of topics. The cooperative facilitates the collection and sale of raw milk produced

by its members. They can help open new markets for their producers.

4

Nicacentro, the cooperative focus of our research, has 992 individual members. Through the

team’s inquiry we learned nearly all members lack at least one of three basic milking area

components, namely a ceiling, a concrete floor, and clean running water plus drainage. The

impact of this absence is that otherwise grade A milk may not be grade A by the time it reaches

the collection point. Two components dictate prices paid for raw milk. One is milk content, the

other is bacteria content. The higher the bacteria content, the lower the grade.

The lack of milking facilities interacts negatively with Nicacentro’s collection methods. A

principal inefficiency at milk collection stations which are scattered throughout the region is no

holding area for newly delivered milk. When a lower grade milk is mixed with a higher grade

milk, in the case of bacteria count, the milk is downgraded. This affects the price that everyone

that uses the collection station receives on that day. A holding refrigerator at the collection point

for incoming “pichingas” (a milk can that is frequently used) would help to protect grade A

deliveries.

Nicacentro members are financially conservative, and understandably so. Trying new things

could mean not eating if they aren’t successful. They frequently are not willing to offer property

as collateral for loans; when they do borrow they do so to finance short term business needs such

as food or veterinarian supplies. Credit terms are onerous; most commercial banks won’t make

such small scale commercial or agricultural loans and MFIs charge very high rates of interest for

very short time horizons. Additionally, many MFI loans are structured with a pro-rata principal

pay-down. This means that the largest payments on the loan are in the first months, likely the

hardest to pay. The statement was made that loans are structured this way so that farmers have

to pay less interest. This is true over the life of the loan, farmers do pay less interest. But the

5

savings aren’t very large and when compared to the liquidity crunch of making the early

payments, the difference may be worth the charge.

Another way to bring interest costs down is to reduce the servicing burden. A natural servicer of

loans are the cooperatives that market the production of its members. Most cooperatives likely

have bank accounts and can aggregate funds and pay back providers of credit. This would

reduce servicing costs to almost zero and enable small loans (i.e. $1,000) at reasonable interest

rates and for reasonable terms. From the team’s research, the interbank market doesn’t charge

lenders to the informal agricultural sector more than 10%, and at times charges much less.

Credit guarantees are another method to bring down borrowing costs. PCGs, or Partial Credit

Guarantees, have been offered to cover SME loans in Chile, with a unique auction to set

coverage ratios. Mexico has also used loan credit guarantees. The purpose of such guarantees is

to spur lending along. While empirical results indicate this works, with credit expanding in

markets seeing these sorts of guarantees at work, it is ambiguous whether or not real gains occur.

A more capital efficient way to guarantee SME loans may be to create a reserve fund which

passively tracks the amount of collateral guaranteed, and releases funds back to the entity

offering the guarantee as the guaranteed loan pool pays down (pay downs can include defaults).

Rather than having to ensure that 70% of the value of outstanding loans will be available in times

of crisis, a reserve fund capitalized with a fraction of the balance of loans outstanding can

provide a growing amount of support during good times and a buffer against losses during bad.

To keep the guarantee fund stable, excess spread can be taken out of the loans. For example,

borrowers pay 15% = 13% +2%. The 2% goes to the reserve fund, 13% goes to the lender.

Because the loans pay down, cash is available for release from the reserve fund. The reserve

6

fund is levered against losses, and its return can vary wildly. But it can cover losses during

normal operating conditions and quickly ramp up additional support once the loans have been

written.

Nicaraguan dairy farmers need production facilities that enable consistency of quality. They

need reasonable financial terms to do so. They need access to markets with more than one buyer

of production. They need to fix the tax code which penalizes cooperatives for growing too large.

They need technical assistance from trusted sources in order to take risks to grow herds. They

need a stronger commercial code to protect the quality of their sales.

Sequencing is important. The list of items needed for growth is very achievable; Nicaraguan

dairy represents a sector with high growth potential if problems can be worked out.

7

1. Introduction

1.1 Background and Purpose of the Project

Nicaragua, like many emerging markets, has an economy that relies heavily on agriculture. The

country has agricultural zones with vastly under-utilized potential. A year-round growing

season, volcanic soil, and more moderate temperatures in the highlands make Nicaragua’s

agricultural zones ideal for all manner of cultivation and livestock. While Nicaragua’s chief

agricultural exports are coffee and cocoa, the dairy industry is a large and important component

of local agribusiness, amounting to 3.6 % of national GDP (Galetto & Berra, 2011); the dairy

industry is a major income source for Nicaragua’s livestock sector. The general livestock sector

accounted for roughly 39% of Nicaragua’s agricultural contribution to GDP and it generated

81,921 permanent jobs in rural areas, amounting to almost 60% of employment in in those areas

(ILRI, 2014). A functional dairy industry needs collection and processing facilities in close

proximity to producers, and most Nicaraguan dairy farmers are small to medium sized businesses

that do not own refrigerated transportation or storage, thus they tend to cluster together. Much of

Nicaragua’s dairy capacity exists within a regional band known as the “Via Láctea”, or “Milky

Way” in English.

The Inter-American Development Bank is exploring the potential for lending facilities to develop

this important part of the agricultural sector, and the Via Láctea region will see some of the most

direct benefits. The dairy industry’s growth can help diversify national agricultural revenues and

provide higher quality dairy products for both export and domestic consumption.

The average Nicaraguan dairy farmer is under-banked. Servicing of loans is difficult and can be

expensive, especially for smaller loan sizes. Many producers require technical assistance; access

8

to credit is not helpful if the loan isn’t used in an efficient way to expand production. The chief

goal of our study is to identify bottlenecks within the raw milk production process which need to

be fixed, and consider what amount of credit, applied through which channels, would be most

likely to be accessible to, and help small and medium producers in the country.

In order to facilitate this study, we have conducted qualitative interviews with key stakeholders

in the value chain, in depth interviews with industry experts, and requested data on the

businesses that operate in the Nicaraguan dairy space, with close attention paid to the

cooperative (coop) Nicacentro and individual producers. We sought to understand the operation

of their dairy-related businesses through their eyes. We took careful consideration of their

international and domestic market concerns, day to day operating procedures, and Nicaraguan

laws regarding health and sanitation, banking, and property. We also considered the food

production health and sanitation regulations of markets they may export to, and the competitive

conditions in domestic markets. Food safety regulations can act as non-tariff barriers to trade. In

consideration of this research, we constructed some basic models of financing, and considered

the impact of revenue improvement on a farmer’s ability to pay to finance those improvements.

We also consider the business condition of several financial actors within Nicaragua, namely a

government-run bank with a development mission, and two independently operating

microfinance organizations.

9

2. Milk Market

2.1 International Market

2.1.1 Current Situation (Actors and Economic Issues)

The milk market is a complex market to price. Different grades of milk are used for all manner

of industrial production of dairy consumer packaged goods, or CPGs, and it seems that only the

very lowest grades of milk are discarded. Higher grades of milk are used for producing

pasteurized drinking milk, but the grocery store is awash with all manner of dairy-based CPGs,

from yogurts and cheeses to butters, ice creams, and even curds. Before a global cold chain

network existed, dairy products often had to be consumed locally; marketing dairy products

outside of a particular region was impossible due to the perishable nature of even the most

processed CPGs. This has changed in the past 30 years. Now a diverse array of CPGs can be

created on one continent and delivered to another across oceans. Producers in higher income

countries are responding to this new global market. The European Union (EU) let milk quotas

expire in March, 2015 and did so with the explicit purpose of giving producers access to this new

export market, a market that didn’t exist in the same scale when quotas were introduced in 1984.

As the European Economic Community (EEC) opened up markets for trade the quota system

was a way to cap the production of each farmer, many of who were overproducing, thus offering

a passive price floor as opposed to direct government subsidy. In the press release to remove

quotas, the European Commission specifically states “The primary reasons for deciding to end

milk quotas was that there has been a considerable increase in consumption of dairy products in

recent years, especially on the world market – projected to continue in future – while the quota

regime is preventing EU producers from responding to this growing demand.” (EC,2015). The

release further goes on to state that Korean consumption of EU milk has doubled in 4 years.

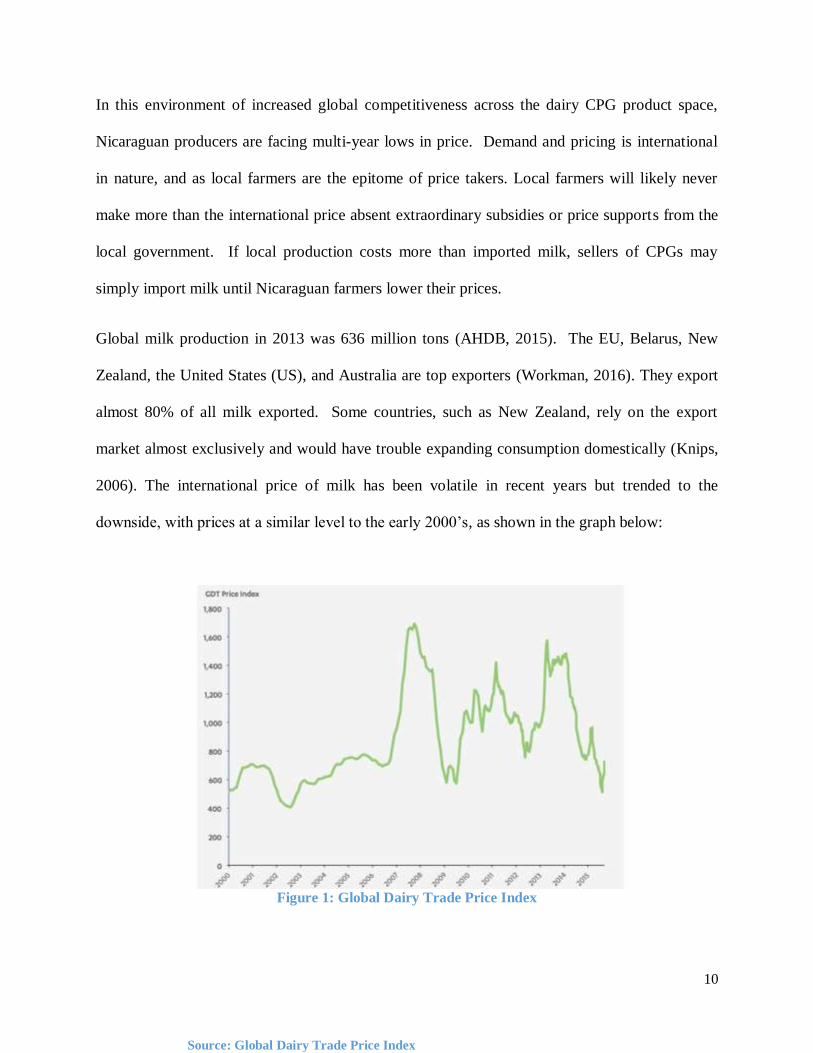

10

Source: Global Dairy Trade Price Index

In this environment of increased global competitiveness across the dairy CPG product space,

Nicaraguan producers are facing multi-year lows in price. Demand and pricing is international

in nature, and as local farmers are the epitome of price takers. Local farmers will likely never

make more than the international price absent extraordinary subsidies or price supports from the

local government. If local production costs more than imported milk, sellers of CPGs may

simply import milk until Nicaraguan farmers lower their prices.

Global milk production in 2013 was 636 million tons (AHDB, 2015). The EU, Belarus, New

Zealand, the United States (US), and Australia are top exporters (Workman, 2016). They export

almost 80% of all milk exported. Some countries, such as New Zealand, rely on the export

market almost exclusively and would have trouble expanding consumption domestically (Knips,

2006). The international price of milk has been volatile in recent years but trended to the

downside, with prices at a similar level to the early 2000’s, as shown in the graph below:

Figure 1: Global Dairy Trade Price Index

11

Supply and demand have had trouble finding balance, with recent declines in demand from

China being particularly impactful. Current price levels could see less efficient producers forced

out of the market, as they give up on struggling to hang on while barely breaking even. There is

some hope that such a turnover, in addition to major exporters reducing supply, will lead to

higher prices as demand returns and supply is curtailed by the loss of weaker producers who may

decide to slaughter their herd to sell in the beef market.

2.1.2 Global Responses

In the current environment, producers in countries with some form of price support scheme are

most likely to survive the downturn, as long as the price supports are left in place. Because of

the extended nature of the downturn, and the fact that it extends across many agricultural

products, some countries have taken additional measures to support agricultural producers.

In Uruguay, producers of dairy products have been affected by purchases on credit by

Venezuela, a country whose capacity to pay back loans is suffering from low oil prices. A line

of credit has been designed to help producers fund this $96 million receivable; it can also be used

to finance payables and other bills coming due for the major manufacturing companies

Conaprole, Calcer, Claldy, and Pili during the current environment of extended low prices.

Conaprole, the national Uruguayan dairy cooperative, had a counter-cyclical stabilization fund

designed to help offset downside price volatility for its individual producers. This fund has been

severely depleted due to the unexpectedly long term nature of the downturn. They have also

been forced to idle two plants for lack of demand at economically viable prices. In an effort to

curtail spillover from the slow dairy business, the government has created and maintained a

Value Added Tax (VAT) exemption for the purchases of inputs in the agricultural sector.

12

Argentina has also recently adopted measures to help milk producers. The nation subsidized 50

cents per liter of milk up to 3000 liters per day for producers in February and March 2016. The

VAT on feed and other inputs has been lowered from 6% to 1% for 4 months and extended

subsidies to all dairy producers, a 30% increase over existing beneficiaries. A lending facility

has been created through Banco de la Nación de Argentina to lend up to 100% of the cost of

improving or expanding dairy businesses, with longer maturities out to 8 years and with an 8-

month grace period.

While EU quotas have recently been removed to help EU dairies, causing much of the

oversupply, EU countries are suffering from the low prices as well. Spain and other EU

countries are providing temporary aid through market-oriented assistance commercializing

products and emergency lines of credit to some producers.

In times past, countries could simply institute local quotas, or rather production ceilings, in order

to stem the tide of rampant price declines in an oversupplied market. But with modern cold

chains and rapidly scalable distribution and logistics, production quotas typically mean missed

revenue by being left out of the export market. And if the local quota forces prices higher than

the world price, imports can quickly replace locally produced dairy CPGs on grocery store

shelves and in restaurants. Quotas and other attempts to prevent farmers from producing have

undesirable side effects that tend to drive governments implementing such ill-fated programs in

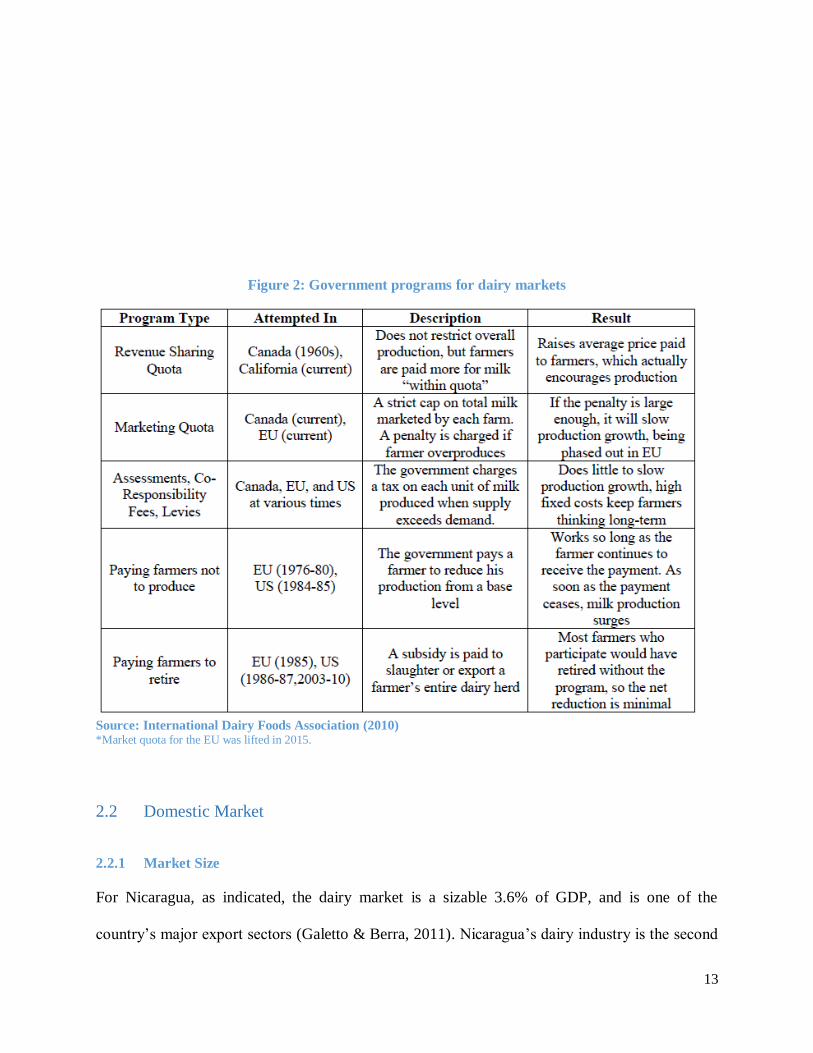

dairy markets to change course. Please see Figure 2 for examples of such programs and their

results.

13

Source: International Dairy Foods Association (2010) *Market quota for the EU was lifted in 2015.

Figure 2: Government programs for dairy markets

2.2 Domestic Market

2.2.1 Market Size

For Nicaragua, as indicated, the dairy market is a sizable 3.6% of GDP, and is one of the

country’s major export sectors (Galetto & Berra, 2011). Nicaragua’s dairy industry is the second

14

largest in Central America after Costa Rica. Nicaragua produced 753,281 tons in 2010. In 2015,

Nicaragua exported 121,956 tons of milk, and in a typical year exports account for around 15%

of total dairy production.

2.2.2 Domestic Market Characteristics

A chief difficulty of the dairy business in Nicaragua is its long history of informality. According

to the Food and Agriculture Organization (FAO), in 2005 86% of the sales of raw milk by small

producers occurred in the informal sector, and 14% was sold by cooperatives or other entities. A

primary disadvantage of the informal sector is its lack of access to affordable credit. The

informal milk sector has shrunk slightly since then but it still accounts for 70-80% of producers,

closer to the practices of producers in neighboring countries. There are several key policy issues

in Nicaragua which need to be addressed to encourage milk producers to abandon the informal

sector. Without such changes, it is unlikely informal practices will recede from the market. In

the long run, cooperatives and formal business practices among producers would likely bring

sustained growth to dairy farmers who have available, yet under-utilized access to a global

marketplace. The recent multi-year decline in internal demand suggest that, at least in the short

run, there is little ability for the Nicaraguan market to absorb additional dairy production

(International Livestock , 2011).

Recent market consolidation has occurred among downstream buyers in the dairy sector. La

Perfecta, a domestically owned 57-year veteran of the Nicaraguan dairy CPG business that

produces milk, processed dairy products, and juices was purchased in early 2016 by Grupo Lala,

a Mexican dairy company with similar business lines. Eskimo, a locally owned 72-year veteran

of the Nicaraguan market producing milk, ice cream, yogurt and beverages, was purchased in

2014 by Grupo Lala. Parmalat was operating a dairy business in Nicaragua until selling it to

15

Centrolac in 2009. These two downstream processors, Lala and Centrolac, buy most of

Nicaragua’s milk production. Currently Grupo Lala alone purchases around 75% of production.

In spite of recent infrastructure investment by Lala, opening a 300,000 liter plant in 2015

(Olivares, 2015), Nicaraguan dairy production faces an oversupply with a growing lack of

processing capacity, especially as regards powdered milk (Central American Data, 2015). Such

creates a further downside risk to price stability.

2.2.3 Nicaraguan Export Market

The Nicaraguan export market seems healthy with steady demand. On a value basis, dairy

products constituted 9% of the total value of Nicaraguan exports. Pasteurized fluid milk exports

increased 70% over 2014 and 2015. The major importers of Nicaragua’s fluid milk are close

geographically. Venezuela, Costa Rica, El Salvador, Guatemala, and Honduras are the largest

buyers of Nicaraguan exports (Central American Data, 2015). Just recently however, Nicaragua

has accused Honduras of a non-tariff barrier to trade in the form of a delay of plant re-

certification by its health service. A move that clearly benefits Honduran producers by blocking

750,000 liters of milk per month from Nicaragua (Central American Data, 2016). As

international prices for milk stay low, Nicaraguan farmers may suffer from emerging

protectionist dairy policies initiated by its principal importers.

Anecdotally, the team was told there is unmet demand for pasteurized fluid milk in the

Caribbean region, but Nicaraguan producers do not produce enough at high enough quality to

sell to this market. United States Department Agriculture (USDA) standards are difficult for

producers to meet in the category of pasteurized milk, and the most commonly produced

Nicaraguan cheeses don’t have an established US market.

16

Source: Adapted and updated from HERRERA MENDOZA, CADENA DE VALOR

Upon examination of the current market for Nicaraguan dairy products, increases in quality and

adding downstream buyers to compete for producer supply would likely benefit producers

greatly.

This is the commercial and business environment that we are considering within the context of

Nicacentro and its 992 producers active market for raw milk and processed goods.

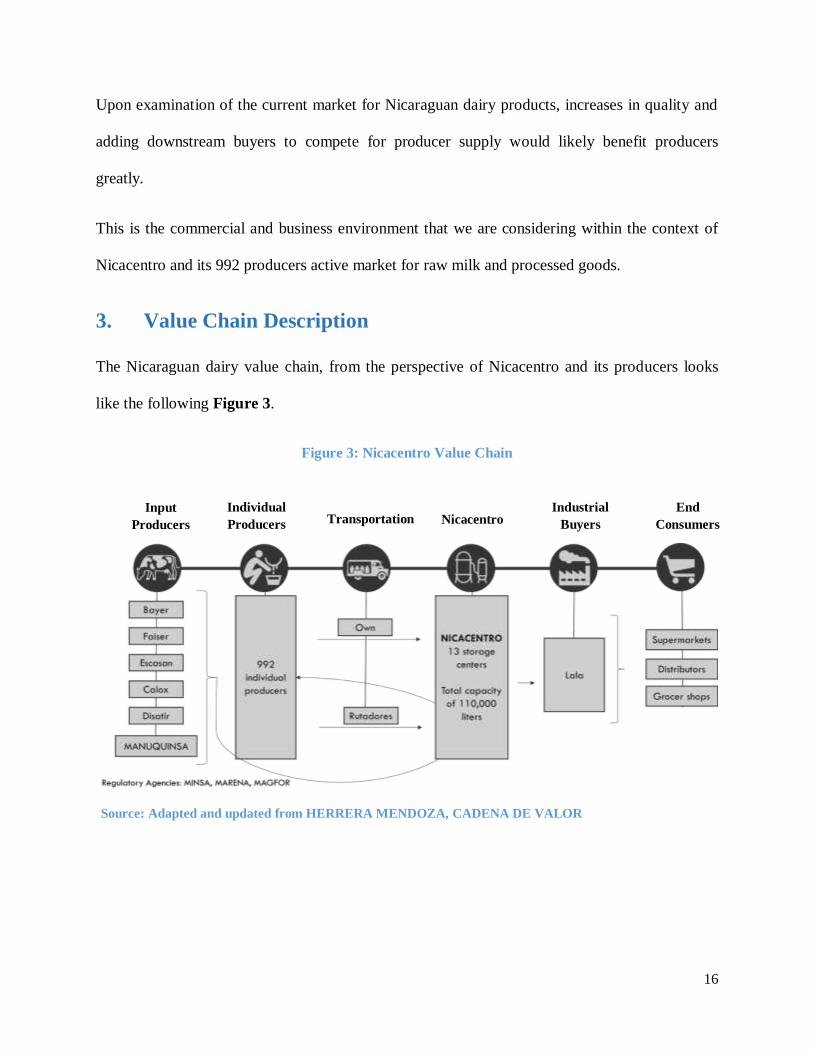

3. Value Chain Description

The Nicaraguan dairy value chain, from the perspective of Nicacentro and its producers looks

like the following Figure 3.

Figure 3: Nicacentro Value Chain

Input

Producers

Individual

Producers

Transportation

Nicacentro

Industrial

Buyers

End

Consumers

17

The simplified value chain surrounding Nicacentro contains links at 6 high level groupings, as

illustrated in the table.

3.1 Value Chain and Stakeholders Defined

The leftmost link represents input producers, these are companies that manufacture and sell all

types of products associated with milk production, including food supplements, construction

materials, seed, veterinary supplies, test chemicals and equipment, machine parts, and many

similar items. The company names supplying such are listed in the chart. The geographic

distances between suppliers on the input link and raw milk producers can be significant; the

cooperative mitigates some of this by buying in bulk, shipping, storing and distributing closer to

producers. If major construction projects are to be undertaken through a financing program

offered to many farmers, it would likely be the most economical to plan to supply multiple

projects simultaneously, as warehousing supplies may be cheaper than purchasing and shipping

them piecemeal to individual producers. Additional warehousing capacity for supplies for

cooperative members could be an investment that would pay off in bulk purchase discounts,

convenience, time, and shipping costs.

Second from the left, the link represents the 992 individual producers of the cooperative,

Nicacentro, known as associates. Nicacentro is a dairy cooperative (coop) which operates

collection and refrigeration stations for the benefit of its associates. Nicacentro’s associates are

mostly smaller producers as per the coop business model, with farms averaging around 70 Ha

and possessing a herd of around 25 dairy cows. Associate producers face a wide array of

constraints, from poor local communal infrastructure like paved roads, water, and higher voltage

18

electrical access, to lack of capital or access to financial services to finance the most basic of

farm improvements. Those needed improvements and their potential impact on revenues to

individual producers will be discussed in greater depth later.

Transportation of milk from individual producers to collection stations is accomplished by

“rutadores”, or by the producing associates themselves. This is the third link in the chart. The

“rutadores” are local truck owners who are hired by the cooperative to facilitate this transfer for

producers without delivery assets. Through our interviews, we learned that inefficiencies in this

system are the least pressing among producers, as very little cross-contamination occurs. Cross

contamination between different quality milks stored together can downgrade the whole batch, as

bacteria count is one measure of milk quality, another being fat content. The delivery method is

not the chief source of this problem, but rather collection sites, discussed later.

The 4th

link on the chain and already described in brief, Nicacentro is one of several dairy

cooperatives in Nicaragua. The organization works with the 992 individual associates described

above, and their main service to the value chain is the cooling and storage of the collected milk

until that milk is picked up by a downstream consumer like Grupo Lala. Nicacentro has the

negotiating power their small farmers lack, and fight for the best price for their farmers. They

also try to smooth out price fluctuations between seasons. They offer important services such as

technical assistance, a modest amount of credit at very competitive rates, veterinary services, and

the sale of production inputs purchased from the first link in the chart, input producers.

Nicacentro currently operates 13 storage centers spread through a geographic band known as

the “Via Lactea”. As already noted, the Nicaraguan market is oversupplied due to a lack of

processing capacity. This oversupply has a negative impact on revenues. Another inefficiency

facing Nicacentro’s collection methods is the lack of an ability to store milk until its quality can

19

be verified. Collection centers only have one main refrigerated holding tank and no refrigerated

holding area for individual deliveries to be segregated, so milk must be mixed into the tank

before individual delivery test results are known. When high bacterial count milk and low are

mixed, the result is usually a downgrading of quality, leading to a lower market price realized per

volume of milk sold. Another problem with quality testing is a lack of independent verification

of quality; the dominant price is what the purchasing agent claims the quality to be and there are

only two chief buyers in the market. If an incorrect downgrade is suspected, there is little

recourse as regards changing end buyers or contesting prices paid.

Nicacentro would like to be able to offer credit to its associates, but it has a very limited

maximum size of its loan book ($150,000), simply due to lack of excess funds to lend. When it

does lend, it lends at rates well below what micro finance organizations charge. Nicacentro will

typically only charge 12-15% for a loan, compared to banks who charge on average 7.5-9.5%

and microfinance institutions 18-36%. Servicing loans is cheap for them because they can net

loan proceeds from the associate’s production, but they lack funds to lend. Another constraint

for Nicacentro is that its collection centers are sometimes provided by Lala, so much of the milk

that goes through those centers is locked up by contract for in-kind financing recoupment.

From Nicacentro’s 13 storage locations, industrial buyers collect each day’s production. That

is the 5th

link in the presented chart. Currently Lala is Nicacentro’s only customer, and they take

all the raw milk produced to their plants for processing. CENTROLAC is cited to be much

worse on a pricing basis to the point that farmers can’t break even; Lala’s bid is the best and only

available. Because Lala has a limited capacity and is the only valid bidder in the market,

Nicacentro is forced to produce below capacity. It also faces the risk of losing its only buyer,

which would be disastrous in the short term. Additionally, Lala is beginning to use additives in

20

in place of raw milk in its dairy CPGs, sold in supermarkets. Retail grocery sellers are the final

link in the value chain.

Not contained within the dairy value chain but having a high impact on it are the financial sector

and regulatory agencies. We will cover financial sector institutions converging with this value

chain in depth later. We did not make a deep survey of regulatory agencies affecting the

Nicaraguan dairy industry, although the absence of independent testing agents to promote fair

treatment of suppliers by large industrial buyers seemed conspicuous.

4. Key Stakeholder Analysis

4.1 Producers

The individual producers and the cooperative, Nicacentro, are the two key stakeholders in the

value chain which we were asked to consider. In many ways, they are the same because

Nicacentro works for the benefit of producers. But in many ways, they are very different.

4.1.1 Producer (Associate) Profile

From our field interviews, and confirmed by the industry expert from SNV, Nicacentro

producers are more conservative than average when it comes to taking on additional business

risks. This includes being slow adopters of new technology, being slow to mechanize, and

lagging behind larger producers on switching the genetics of their herds to enhance production

quality and quantity. Nicacentro producers are smaller than the country average and frequently

raise their herds as dual use, for both milk production and eventual slaughter. Their on-premises

milking facilities may include a stool and a bucket and little else. Nicacentro’s objective is to

have 100% of its associates at least with the basics of a top-notch milking facility including three

items - clean water, a roof, and a concrete floor. Many producers have at least one of these but

21

Source: (Estrada & Holmann, 2008) (Instituto Nacional de Tecnologia Agropecuaria, 2015)

(Agro Informe, 2012)

few have all three. The coop is currently in the process of quantifying these needs among its

members. An accurate survey will allow it to seek better financing terms for participating

associates and purchase needed materials in bulk. We attempt to quantify the impact of such

improvements on revenue later through a simple model. Lowering the bacterial content of milk

is as simple as employing a roof, concrete floor, and clean water. But without these three,

contamination at the point of collection from the cow is a daily risk, and a risk with a reasonable

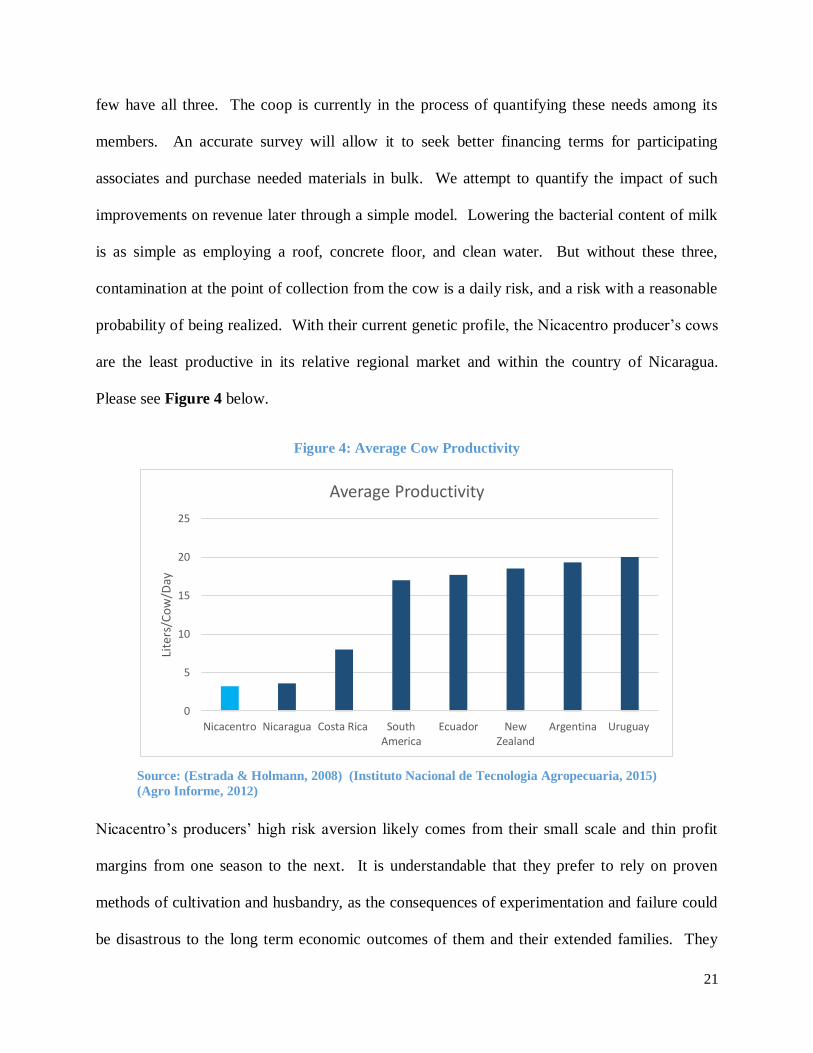

probability of being realized. With their current genetic profile, the Nicacentro producer’s cows

are the least productive in its relative regional market and within the country of Nicaragua.

Please see Figure 4 below.

Figure 4: Average Cow Productivity

Nicacentro’s producers’ high risk aversion likely comes from their small scale and thin profit

margins from one season to the next. It is understandable that they prefer to rely on proven

methods of cultivation and husbandry, as the consequences of experimentation and failure could

be disastrous to the long term economic outcomes of them and their extended families. They

0

5

10

15

20

25

Nicacentro Nicaragua Costa Rica SouthAmerica

Ecuador NewZealand

Argentina Uruguay

Lite

rs/C

ow

/Day

Average Productivity

22

have little capacity to absorb losses in the quest for longer term gains. This risk aversion further

drives them to avoid financing any parts of their business unless absolutely necessary, and never

to mortgage essential property items such as land or herd. This risk aversion is further enhanced

by the sub-par lending options typically available to associates of the coop.

The coop’s first goal for its associates is to provide all with an opportunity to upgrade their

milking facilities. Many producers are in need of much more technical assistance, but ensuring

quality at the point of milking must come first. Sequencing is important for improving

associates’ revenues. Skipping early steps will inevitably lead to sub-optimal results. Improving

the genetics of the cows before improving their milking conditions is not the most efficient way

to improve prices earned. For more advanced technical assistance, such as changing individual

associate’s herd genetics, changing their planting methods and cattle feeding patterns, associates

need to see very concretely that these changes will not lead to ruin. The industry expert

consulted agrees that a very visible demonstration of these technical assistance changes executed

by a farmer that other farmers trust would go a long way towards fostering the adoption of new

programs. In order for an associate to agree to be a test subject, he will likely need some

insurance he will not come to ruin for it.

Additional infrastructure needs include fence and enclosure improvements, and productivity

enhancing machines such as one known as a pasture mincer. Since cows in the region are mostly

fed by being put out to pasture, the conditions of pastureland can dramatically improve

productivity through food availability. In some cases, pasture is supplemented with other locally

produced feed products or commercial supplements, the use of both is less common among

Nicacentro producers. Rather than providing round-the-clock access to nutrition and water,

23

farmers are frequently constrained to provide less, this can deplete a cow’s productive ability

measurably.

4.1.2 Producers and Credit

Of the producers in the cooperative who have come into contact with financing, their experiences

haven’t always been positive. These past experiences directly affect their views on credit and

their trust of various financial agents offering them credit. Overwhelmingly, associates prefer to

borrow through the cooperative, as opposed to banks or microfinance institutions. It is easy to

understand why. The cooperative is viewed as being aligned with the farmers, and also offers

rates of interest drastically below the market. It is hard for the producers within the cooperative

to get bank loans because they are too small, have difficulty with loan servicing, and are

frequently on the line between formal and informal sector. It is difficult for most associates to

produce the detailed financial records needed for a bank loan. By contrast, a microfinance

institution will lend to associates of the coop but at rates that greatly exceed the rate the coop can

offer when it can offer financing (recall that the max loan book size for Nicacentro is $150,000).

The lowest rate quoted by a microfinance institution (MFI) was 18%, and that was with servicing

through the cooperative or through other specific arrangements as with long term clients. If

servicing is not administered by the cooperative, rates of interest often exceed 24%.

In almost all cases, loan servicing through the coop makes the most sense. Farmers do not have

checking accounts with which to pay periodic loan payments, only 19% of Nicaraguan

population have a checking account (Demirguc-Kunt, Klapper, Singer, & Van Oudheusden,

2014). And no close-by postal route to take the check to the bank. Because of this, physical

collection is needed. Because farmers generate cash by delivering milk, the easiest servicing

method available is to net loan proceeds from deliveries to pay the periodic loan payments, this

24

is also their preferred method. MFIs, if they would agree to expand such servicing, would be

able to lower rates and still be profitable, employ less manpower, and have better borrower

surveillance.

When borrowing, farmers tend to borrow from MFIs in small amounts for production inputs

rather than infrastructure improvements. This is likely driven by the short duration of loans

offered (almost always less than 36 months and frequently less than 24), and high rates of

interest charged. It is difficult for farmers to see the gains from improving productivity through

improving sanitation at the harvest site when short term cash flow burden is high from a short

dated, large infrastructure loan.

Another issue related to financing of infrastructure for farmers is project size. If the size of the

loan goes over a certain threshold, different among lenders but usually no more than $15,000,

more secure collateral can become necessary, including real property. Farmers are almost never

going to be willing to mortgage their land to borrow for facilities improvement as that is their

sole source of survival, and thus never make valuable facilities improvements.

Nicacentro associates could benefit greatly from facilities improvements. Increasing the

productivity of cows and the quality of production would greatly enhance their revenues. But in

the Nicaraguan economy there is a clear mismatch between the needs of producers like the

associates of Nicacentro and the financial products ready to be offered to them. Nicacentro

producers have unique circumstances and require infrastructure buildout which requires loans

with maturities longer than 24 months, and at interest rates lower than 24%. It is in the best

interest of both financial institutions and Nicacentro associates to find financial products that

25

allow associates to grow production without over-extending their cash flow commitments or

risking their most valuable asset, their production lands.

4.2 Nicacentro (Cooperatives)

4.2.1 Cooperatives and incentives to be a member

In 2001 the government created FondeAgro, a dairy development project to finance the buildout

of the milk cooling and storage network that became the foundations of Nicacentro, along with 3

other dairy coops. This effort to grow production by offering the power of market share to small

producers was successful. Eventually 5 larger coops began competing in the market. Nicacentro

started in 2005 with 288 members, it has grown to 992 members. On average, Nicacentro’s

producers have 70 hectares and 25 milk cows. Each cow produces around 3 liters of milk a day.

The cooperative collects, stores, and markets milk from its associates daily, aggregated at 13

refrigerated collection sites distributed around the region.

Noted in a study from 2007, the cooling network assets in the country, primarily consisting of

distributed collection and temporary storage depos, belong to 3 categories of owner, with 45.2%

owned by cooperatives like Nicacentro, 42.9% owned by private individuals, and 11.9% owned

by the association of cattle producers. Nicacentro’s 13 collection stations would be included in

the above national numbers. It is worth noting that even though a coop may own a collection

center, it may be financed by in-kind delivery to the market’s principal buyer, Grupo Lala. In

such a case, the coop can’t control the destination of the production delivered to the collection

site until it is paid off.

The cooperatives were formed with the idea of improving the bargaining power of smaller

farmers, and allowing collective decision making among producers in a localized area. Some

26

cooperatives also have ambitions to expand downstream and to manufacture dairy CPGs, citing

Dos Pinos of neighboring Costa Rica as an example.

4.2.2 Nicacentro and Strategy

In addition to bargaining power, cooperatives offer some price stability between dry and wet

seasons, working to pay similar prices to farmers throughout the year. By contrast, farmers in

the informal sector experience price fluctuations between dry and wet seasons. Larger farmers

tend to have more bargaining power in the informal sector, driving smaller producers to

cooperatives to compete. The coop’s prices are more stable, but not always higher than the

prices paid to informal producers during low production, high demand seasons. Nicacentro

management recognizes the risk to revenue by this seasonal temptation. Coop members must

commit to selling to the cooperative year round and are sanctioned if they violate their

agreement. The cooperative takes one Cordoba per liter sold through its facilities and passes the

rest on to associates. As of February 9th

, the price for grade A milk posted at a collection station

was per liter was 9.50; an associate would receive 8.50.

The daily production of the cooperative ranges from 56,000 to 85,000 liters per day, while the

total storage capacity of the network it controls is 110,000 liters. According to coop leadership,

associates do have the capacity to produce more but there is simply no bid for higher production.

The demand of buyers who will take delivery of raw milk from Nicacentro, namely Lala

subsidiaries, is limited and shrinking. Currently all milk goes through one of two Grupo Lala

subsidiaries, La Perfecta (66%) and Eskimo (34%). Nicacentro management is rightly concerned

that there is no competition among milk buyers in their market. Prices are negotiated weekly and

agreed to verbally, they have no guaranteed income. In addition to the reduced negotiating

capacity from selling to only one bidder, the coop is also at the whim of Grupo Lala’s business

27

outcomes. Without alternative buyers in the market, production at times must be curtailed. They

have already seen a 4,000 liter a day reduction in demand driven by Lala’s exposure to the

dwindling Venezuelan market. As Lala adopts more non-dairy fillers in its dairy CPGs, the coop

is worried about further reduction in demand.

Nicacentro offers technical assistance and limited financial services to its members. Technical

assistance focuses on topics such as: hygiene, emergency veterinary services, herd management,

animal nutrition, food preservation, and farm skill certifications. The financial services offered

usually come in the form of small loans to producers at below market interest rates, relative to

MFI lending.

Nicacentro adds value to its associates buying power in the form of operating as a distributor of

agricultural inputs. It can act as a bulk buyer and receive a better price and pass on the cost

savings to members, then offer physical products in a location that is convenient to them.

4.2.3 Nicacentro Market Constraints and Infrastructure Needs

In order to alleviate two of the cooperative’s biggest perceived market problems, dependency on

a single buyer and a demand for milk that is lower than the amount the system can produce, the

coop is pursuing strategies to increase quality and utilize more milk. They are trying to develop

their commercial competencies and learn how to promote their products nationally and

internationally. They want to diversify their clients and markets. Milk quality is a major

constraint for developing new markets and maximizing revenue in existing markets, as lower

grade milk is sold locally in the informal market for cheese production. Grade A milk has higher

and more consistent demand than B or C, typically sold on to cheese producers in Honduras or El

Salvador.

28

Nicacentro currently faces several constraints to improving milk quality; one comes from within

its own cooling network. The test to grade a milk of type A, B, or C is done using Methylene

blue, a disappearing dye that bacteria consume. The faster it disappears, the lower the milk

quality. In order to find out if a milk has the highest quality, one must wait 4 hours to complete

the test. Nicacentro’s collection stations lack a refrigerated holding area where each milk

delivery can be stored separately until quality can be established. Deliveries go immediately into

the same refrigerated holding tank. This means that grade A milk is potentially mixed with

lower grades upon delivery; the quality of the mixture can be downgraded by nature of bacterial

growth spreading. The only method the coop currently has to mitigate such risk is to suspend

receipt of delivery from consistently low-quality deliverers until they improve hygiene. As

already mentioned in the producer section, system-wide milking facility upgrades at the farm

level would be ideal to improve delivered quality. A refrigerated holding area wound ensure this

upgrade wasn’t wasted with contaminated mistakes which can downgrade a whole day’s

production.

The addition of independent lab testing of batches of milk to ensure that downstream buyers pay

fairly for the right quality level would also help to ensure that an investment in milking

infrastructure would realize returns. There have been mismatches between the tested quality at

the collection and cooling station, and the tested quality by the downstream buyer. The buyer’s

quality test prevails when determining what price the coop receives. An independent testing

regimen would prevent conflicts of interest from arising in how quality control impacts pricing.

A second strategy Nicacentro is developing to better utilize its production capacity is converting

a collection station to a plant to process packaged cheese for sale on the domestic and export

market, El Salvador was cited as an ideal market for such exports. The plan is for the plant to

29

Source: Own elaboration based on information gathered in trip to Nicaragua.

have an initial capacity to process 4,000 liters of milk. The idea is to presell the cheese to buyers

in El Salvador and then raise capital for the plant conversion, an estimated $350,000. It is

unclear who is currently meeting this demand, but there are certainly market risks to this sort of

investment. It would give Nicacentro associates a better price for their lower quality milk and

bypass downstream buyers.

4.3 Banking Sector

There are several financing channels within the Nicaraguan dairy industry by which lent funds

make it to producers. According to International Livestock Research Institute, the number of

livestock producers who receive loans is exceptionally small in Nicaragua, totaling around 3.5%

of producers (ILRI, 2014). Dairy farmers are hesitant to use credit because of negative

connotations, and the credit available to them has terms which prohibit its broader application to

their business. Dairy producers could use credit for all manner of things around the farm,

starting with the cited essential improvements of milking facilities. These consist of water,

ceiling, and floor. Other uses include machinery, and herd expansion. Because of the informal

nature of their businesses, and the small loan sizes required, small Nicaraguan dairy farmers have

few credit options. Banks aren’t interested in the small commercial loans, and MFIs charge rates

of interest that are too high and for maturities that are too short.

Figure 5: Summary of term of loan and interest rate for visited financial institutions

30

4.3.1 Banco Produzcamos

Banco Produzcamos is in the midst of reconfiguration. Originally created as a state run bank

tasked with lending to domestic financial institutions, it is in the process of focusing itself on

lending to financial intermediary and large end users of funds for the specific purpose of

development. Within that context, its mission aligns with the IDB; Produzcamos could become

an institution through which IDB money can be lent into financial channels. Ultimately, such

lending could benefit dairy farmers and spur economic development of the region in which they

operate. Banco Produzcamos’s loan book is 66% committed to financial institutions, with the

remainder to large commercial entities, and cooperatives. Of the remainder, 70% is lent to

agriculture related businesses. Only around 3% of their current loan book is exposed to the dairy

industry. Banco Produzcamos seeks a return on equity but has no cost of funds, their balance

sheet is primarily financed by equity contributions from government entities. Total asset size is

around $185 million, $145 million of which is financed by equity. Such a structure should make

them more willing to take risk than a commercial structure, although they are explicitly not in the

business of making loans to make losses. As the new management tries to shift the culture of the

bank, they have an opportunity to make better use of the bank’s balance sheet, and new

management is attempting to define a stronger culture and direction.

Banco Produzcamos is willing to use cooperatives as credit intermediaries to make small loans to

farmers and has ample room to increase its exposures to dairy. It recognizes that coops may be

best suited to offer longer term loans to credit-worthy customers by knowing those customers in

an otherwise informal and anonymous market, and is willing to let them underwrite loans and

make credit decisions. Its primary concern with this method of operation, however, is the lack of

corporate governance among cooperatives like Nicacentro. The management of these

31

organizations are untrained in how to run an organization which can be accountable to upstream

lenders as downstream credit agents. Yet coops are uniquely positioned to service loans and

collect surveillance on borrowers by the natural day-to-day operation of their business. So

Banco Produzcamos has planned on offering technical assistance and business education to

coops to facilitate lending through them. Coops are the only credit agents that seem to have the

implicit trust of farmers, thus strengthening the likelihood of repayment. In addition to corporate

governance of cooperatives, Banco Produzcamos is worried about its eventual recourse to end

borrowers should loan performance deteriorate. End borrowers, dairy producers, are highly

informal and it is difficult to seek repayment when end borrowers have no bank accounts, tax

status, or assets collateralizing loans.

Another lending channel through which Banco Produzcamos can make funds available to dairy

farmers is through microfinance organizations (MFIs). These organizations can borrow from

Banco Produzcamos at rates ranging from 7-10%, it hasn’t always been easy to meet the bank’s

requirements for specific lending programs. The proceeds are used to make development loans

to individual producers. MFIs are the principal lenders to the informal sector, as they are willing

to take tremendous risk as regards documentation quality and servicing difficulty. Their tenacity

seems to pay off, as both MFI lenders we spoke with reported exceptionally low default rates for

loans to the dairy sector, especially when considering the high interest rate. These low default

rates are likely driven by farmers’ often cited use of MFI loans, to bridge small short-term input

expenses. The team had the opportunity to speak with two MFIs making loans to the Nicaraguan

dairy industry. FDL and FUNDESER both make small loans to small producers, loans typically

classified as microfinance.

32

4.3.2 FDL (Fondo de Desarrollo Local)

FDL makes loans across many different industries, it has 4,161 agricultural loans in its book as

of 2015. For dairy producers, loan servicing is structured in two ways and this determines

interest rate offered and term of the loan. FDL is innovative and used Nicacentro as the servicer

for one of its loan programs, the first of two mentioned here. These loans were typically around

24 months or less and an 18% interest rate was charged. This lower rate, by MFI standards, is

possible because of the coop servicing arrangement. Milk is netted against the loan payments

due, so Nicacentro sends FDL a check after conducting business on behalf of its associates who

have borrowed from FDL. The second method for servicing is cash, and FDL charges 24-28%

for these loans, they are varying term but are offered out to five years on occasion. Please see

the figure below for an illustration of the two cases.

In both types of loans, FDL requires some form of technical assistance to ensure loans are used

to the farmers’ greatest benefit. In the case of Nicacentro serviced loans, the coop acts as the

technical assistance agent. In the case of cash serviced loans, the technical assistance agency

Nitalapa offers technical assistance and provides borrower surveillance back to FDL. Typically,

FDL will make loans for less than $10,000 and sometimes will receive the “carta de venta”, or

registration of ownership of individual cows, as collateral for the loans. For loans greater than

$10,000, physical collateral is usually required.

Figure 6: FDL Methods for Loan Servicing

(Case 1) (Case 2)

33

Source: Own elaboration based on FDL’s information gathered during trip to Nicaragua.

4.3.3 FUNDESER

FUNDESER is the second microfinance organization we spoke with. It only uses a cash loan

servicing model and is in the process of deploying an automated system for collecting loan

documentation. It only lends to small, end producers, typically with microfinance sized loans.

In the past it hasn’t had a strong focus on the dairy industry and doesn’t have a significant loan

book dedicated to the business. Loan terms are relatively short, and interest rates range from

18% to 30%, but usually hover around 30%. Fundeser has a cost of funds around 7-9%, and can

borrow from Banco Produzcamos for cheaper. Fundeser hopes to be positively impacted by the

change in management at Banco Produzcamos. Previously, Fundeser found it uneconomical to

borrow from Banco Produzcamos because of documentation requirements. Because Fundeser

lends primarily to the informal sector, its borrowers have low default rates but limited

documentation. Banco Produzcamos has traditionally required collateralization of any loans to

Fundeser be collateralized by loans from Fundeser’s loan book. Because of the poor

documentation, Banco Produzcamos had required 150% of the loan value to be collateralized by

loans from Fundeser’s portfolio. Because of this unsustainable requirement, Fundeser is not in

34

the habit of borrowing from Banco Produzcamos, although it would like to do so. When asked

why Fundeser didn’t simply improve their documentation process to produce a portfolio of loans

that would accumulate enough size to be acceptable to Banco Produzcamos as collateral on a 1:1

ratio, management stated it preferred to let Banco Produzcamos change its practices. At the

same time Fundeser is in the midst of a rollout of technology aimed at increasing efficiency of

producing loan documentation and hopes to create a database of consumer behaviors and credit

history. Fundeser has plans to explore an IPO and is in the process of converting itself to a

potentially public traded company.

4.3.4 Loan strategy for Nicacentro

It would seem that the most optimal lending arrangement for Nicacentro producers would be to

borrow through the cooperative, and Banco Produczcamos could best put its money to work by

charging low rates of interest for longer term loans, breaking the cycle of an inability to finance

infrastructure buildout by milk producers. Educating Nicacentro on how to achieve better

corporate governance and better administer loans could facilitate extensive lending to dairy

producers and rates well below MFIs, with easy servicing and stronger psychological motivation

to pay back loans. Default rates to MFIs are low, yet they continue to lend at 24% or higher, such

risk spreads are hard to justify while claiming to be in the business of facilitating impact

investing and development.

One method of diversifying Nicacentro’s purchaser base will be to improve milk quality, this can

be accomplished through loans to associates which they use to build out milking facilities to

include three essential components, floor, ceiling, and clean water. In order for a lending

program to producers to work, it must fit into their cash flow profile, thus likely have a lower

rate of interest and longer term. We built a basic model to calculate the net benefit a farmer

35

would gain from improving quality outcomes, we assume that improving milking quality will

increase quality across the system. We consider the net present value (NPV) and varying

internal rates of return (IRR) for each producer, given an enhancement to milking facilities using

borrowed funds. Our model allows us to vary interest rate, term, annual maintenance cost, and

additional revenue achieved from consistent quality improvement.

5. Strategies for Lending Options

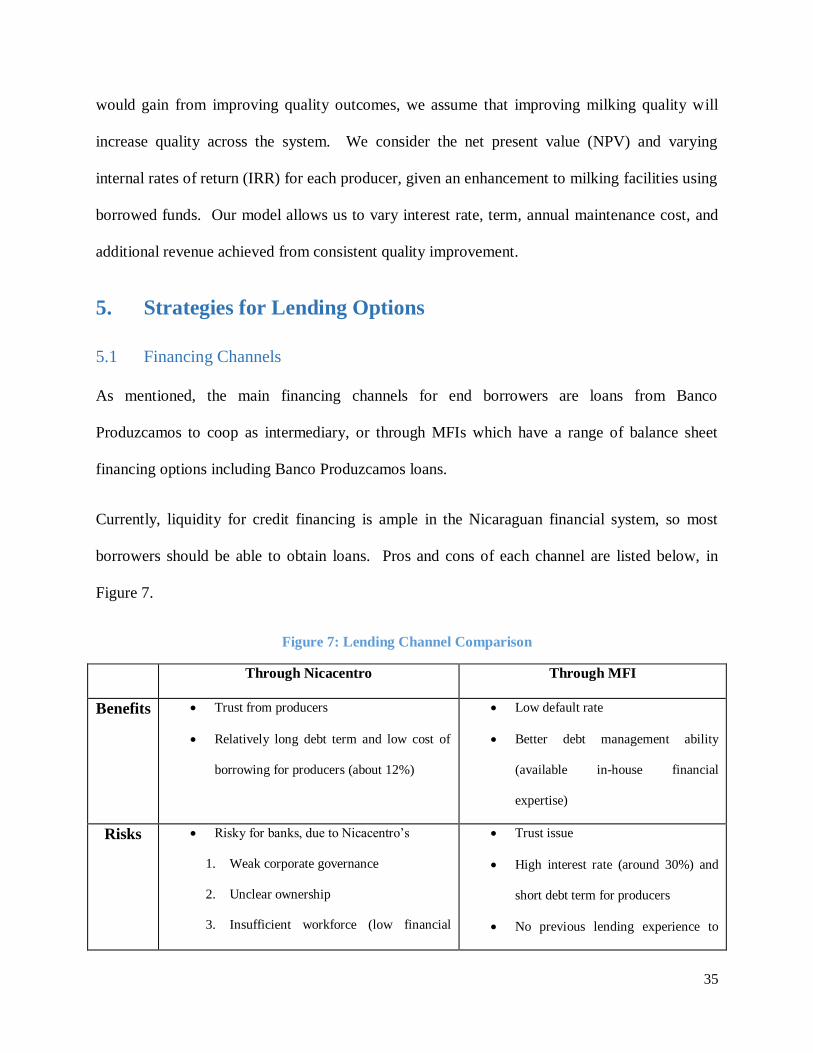

5.1 Financing Channels

As mentioned, the main financing channels for end borrowers are loans from Banco

Produzcamos to coop as intermediary, or through MFIs which have a range of balance sheet

financing options including Banco Produzcamos loans.

Currently, liquidity for credit financing is ample in the Nicaraguan financial system, so most

borrowers should be able to obtain loans. Pros and cons of each channel are listed below, in

Figure 7.

Figure 7: Lending Channel Comparison

Through Nicacentro Through MFI

Benefits Trust from producers

Relatively long debt term and low cost of

borrowing for producers (about 12%)

Low default rate

Better debt management ability

(available in-house financial

expertise)

Risks Risky for banks, due to Nicacentro’s

1. Weak corporate governance

2. Unclear ownership

3. Insufficient workforce (low financial

Trust issue

High interest rate (around 30%) and

short debt term for producers

No previous lending experience to

36

expertise) milk industry

No employees who can process

appropriate documentation

Unattractive lending term for it to

gain fund from BP and IDB

Source: Own elaboration based on market research in Nicaragua.

5.2 Financial Model

5.2.1 Rationale of the Model

The model attempts to roughly estimate the total financing needs of all coop members by

modeling a typical borrowing member’s cash flows. The inputs include producer information on

the number of producers, average number of cows per producer, and percentage of producers

who need each infrastructure and the cost of infrastructure. The cost of each infrastructure item

was established through some basic market research, and the estimated increases in quantity and

quality are used to calculate increases in revenue.

The input and maintenance costs are netted from estimated production benefits for each producer

and are modeled into cash forecasts for an average producer. Loan servicing is included in cost.

Finally, these net benefit increases are discounted back to the present using an appropriately high

rate considering the borrower risk profile. And an internal rate of return is calculated, assuming

both levered and unlevered return. It is unlikely that many borrowers will contribute equity so

IRR will typically consist of cash flows on investment through debt. Please find a description of

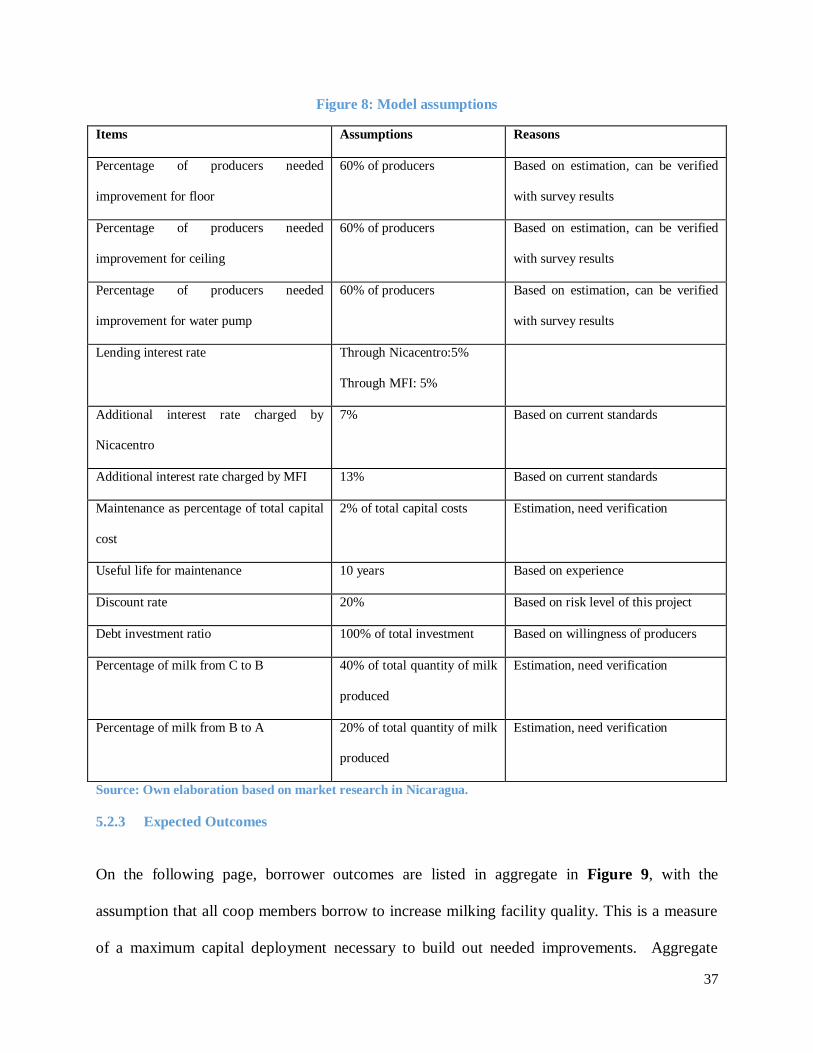

model assumptions in Figure 8 on the following page.

5.2.2 Assumptions

37

Figure 8: Model assumptions

Items Assumptions Reasons

Percentage of producers needed

improvement for floor

60% of producers Based on estimation, can be verified

with survey results

Percentage of producers needed

improvement for ceiling

60% of producers Based on estimation, can be verified

with survey results

Percentage of producers needed

improvement for water pump

60% of producers Based on estimation, can be verified

with survey results

Lending interest rate Through Nicacentro:5%

Through MFI: 5%

Additional interest rate charged by

Nicacentro

7% Based on current standards

Additional interest rate charged by MFI 13% Based on current standards

Maintenance as percentage of total capital

cost

2% of total capital costs Estimation, need verification

Useful life for maintenance 10 years Based on experience

Discount rate 20% Based on risk level of this project

Debt investment ratio 100% of total investment Based on willingness of producers

Percentage of milk from C to B 40% of total quantity of milk

produced

Estimation, need verification

Percentage of milk from B to A 20% of total quantity of milk

produced

Estimation, need verification

Source: Own elaboration based on market research in Nicaragua.

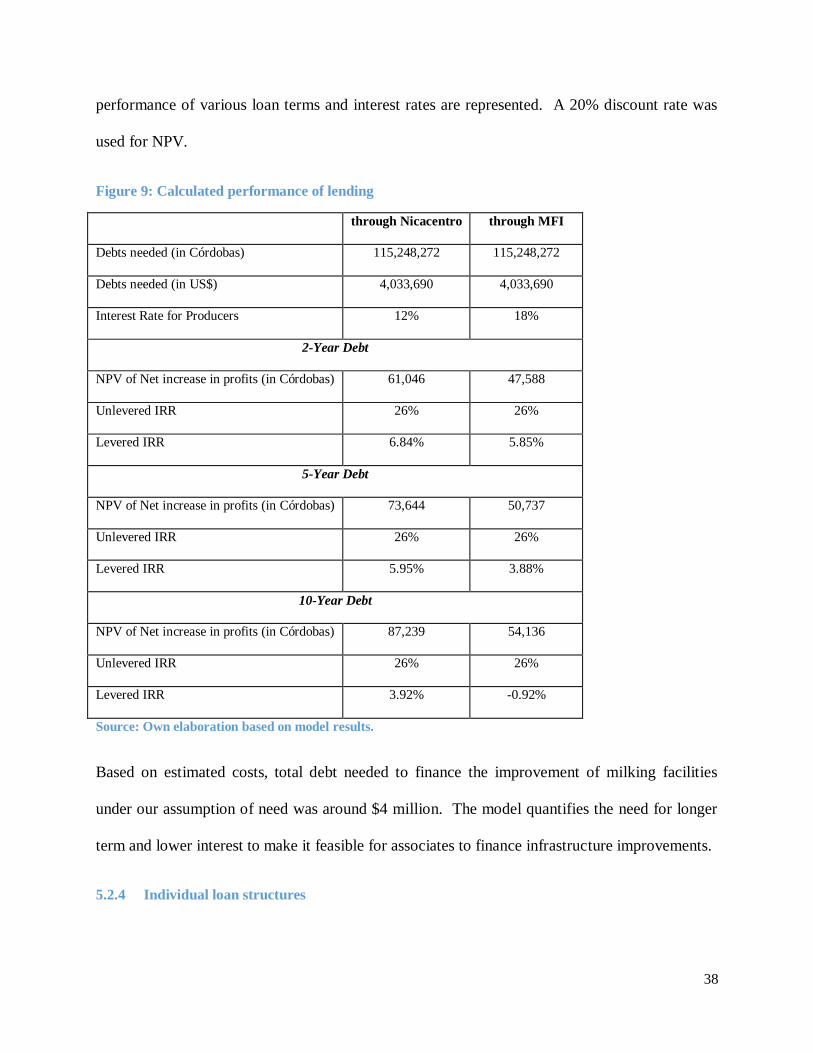

5.2.3 Expected Outcomes

On the following page, borrower outcomes are listed in aggregate in Figure 9, with the

assumption that all coop members borrow to increase milking facility quality. This is a measure

of a maximum capital deployment necessary to build out needed improvements. Aggregate

38

performance of various loan terms and interest rates are represented. A 20% discount rate was

used for NPV.

Figure 9: Calculated performance of lending

through Nicacentro through MFI

Debts needed (in Córdobas) 115,248,272 115,248,272

Debts needed (in US$) 4,033,690 4,033,690

Interest Rate for Producers 12% 18%

2-Year Debt

NPV of Net increase in profits (in Córdobas) 61,046 47,588

Unlevered IRR 26% 26%

Levered IRR 6.84% 5.85%

5-Year Debt

NPV of Net increase in profits (in Córdobas) 73,644 50,737

Unlevered IRR 26% 26%

Levered IRR 5.95% 3.88%

10-Year Debt

NPV of Net increase in profits (in Córdobas) 87,239 54,136

Unlevered IRR 26% 26%

Levered IRR 3.92% -0.92%

Source: Own elaboration based on model results.

Based on estimated costs, total debt needed to finance the improvement of milking facilities

under our assumption of need was around $4 million. The model quantifies the need for longer

term and lower interest to make it feasible for associates to finance infrastructure improvements.

5.2.4 Individual loan structures

39

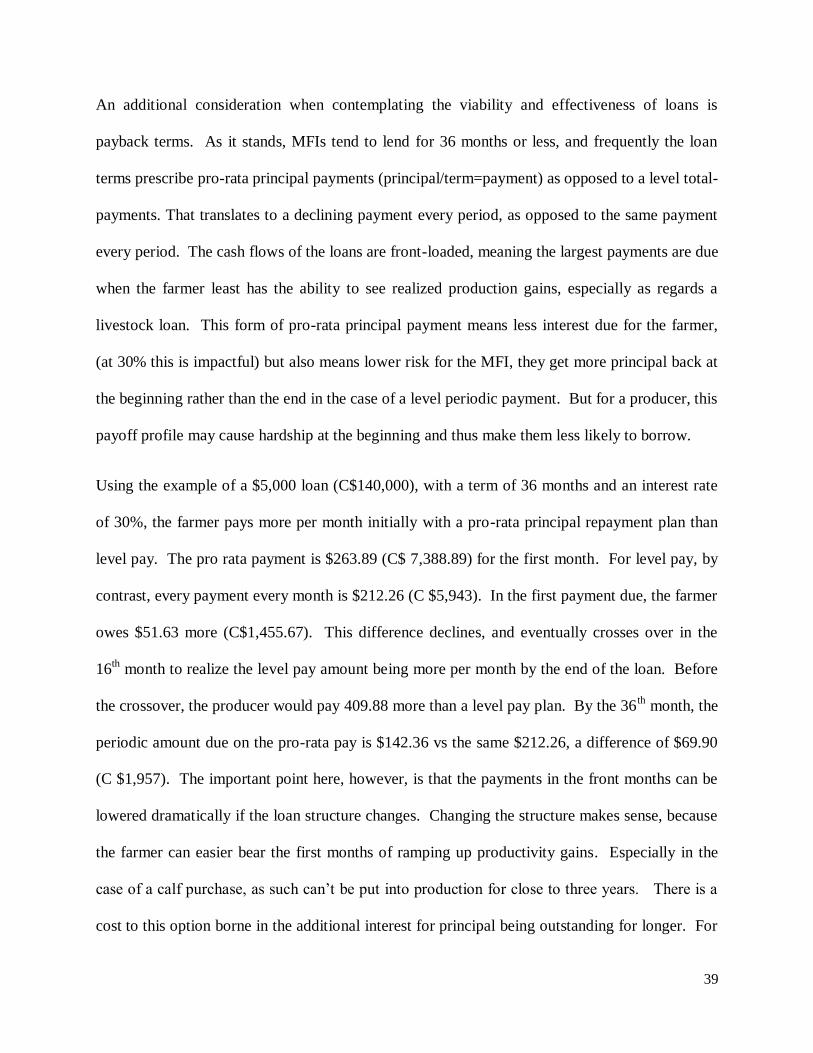

An additional consideration when contemplating the viability and effectiveness of loans is

payback terms. As it stands, MFIs tend to lend for 36 months or less, and frequently the loan

terms prescribe pro-rata principal payments (principal/term=payment) as opposed to a level total-

payments. That translates to a declining payment every period, as opposed to the same payment

every period. The cash flows of the loans are front-loaded, meaning the largest payments are due

when the farmer least has the ability to see realized production gains, especially as regards a

livestock loan. This form of pro-rata principal payment means less interest due for the farmer,

(at 30% this is impactful) but also means lower risk for the MFI, they get more principal back at

the beginning rather than the end in the case of a level periodic payment. But for a producer, this

payoff profile may cause hardship at the beginning and thus make them less likely to borrow.

Using the example of a $5,000 loan (C$140,000), with a term of 36 months and an interest rate

of 30%, the farmer pays more per month initially with a pro-rata principal repayment plan than

level pay. The pro rata payment is $263.89 (C$ 7,388.89) for the first month. For level pay, by

contrast, every payment every month is $212.26 (C $5,943). In the first payment due, the farmer

owes $51.63 more (C$1,455.67). This difference declines, and eventually crosses over in the

16th

month to realize the level pay amount being more per month by the end of the loan. Before

the crossover, the producer would pay 409.88 more than a level pay plan. By the 36th

month, the

periodic amount due on the pro-rata pay is $142.36 vs the same $212.26, a difference of $69.90

(C $1,957). The important point here, however, is that the payments in the front months can be

lowered dramatically if the loan structure changes. Changing the structure makes sense, because

the farmer can easier bear the first months of ramping up productivity gains. Especially in the

case of a calf purchase, as such can’t be put into production for close to three years. There is a

cost to this option borne in the additional interest for principal being outstanding for longer. For

40

the example loan of $5,000, this amounts to around $2.28 per week, over the life of the loan

totaling $329, for the option of paying a minimum of $212.26. Of course the farmer can pay

more if they want, that ultimately shortens the time until the terminal payment. Please see Figure

10 below for an illustration of payoff profiles over 36 months with no prepayment of principal.

Figure 10: Payoff Profile of two loan types

Source: Own elaboration based on model results.

5.2.5 Credit Model using a Guarantee fund

One way to encourage greater lending to the dairy space is to reduce the credit risk faced by

lenders. If credit risk to lenders is reduced, lower rates of interest can be charged, and more risk

can be taken. While it is not ideal to create moral hazard by providing lenders a bail out of their

0.00

50.00

100.00

150.00

200.00

250.00

300.00

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

Pro-rata Loan

Interest

Principal

0.00

50.00

100.00

150.00

200.00

250.00

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

Level Pay Loan

Interest

Principal

41

bad risk decisions, neither is it ideal to constrain credit to the economy on the basis of the severe

information asymmetry that exists between lenders and informal-sector borrowers.

Credit risk faced by lenders can be reduced by creating a guarantee, or reserve, fund for loans. A

risk in offering such a guarantee fund is that it ties up resources that could otherwise be used for

lending, imposing an opportunity cost. Another risk is that it is difficult to gauge how much a

guarantee will ultimately cost; it is also difficult to dis-incentivize reckless lending practices in

the face of credit support.

A model of basic cash flows and a reserve fund to guarantee those cash flows was built. In it,

defaults and losses are applied to loans in constant annualized rates to simulate defaults and

recoveries.

The structure is simplified; in the model realized losses are refunded monthly, along with missed

interest from defaults. If loans produce losses, but if no losses are sustained by lenders, the cash

flows to lenders will be the same in amount as initially scheduled, but different in timing. Losses

and recoveries come back as prepayments. The model includes a switch to cover or not cover

missed interest due with guarantee funds.

Currency is irrelevant for the sake of this model; any currency can be implied by the model. The

basic mechanics of it are as such, start with a pool of loans, for example $1,000,000 outstanding.

Create a guarantee fund that collateralizes a percentage of total loans, for example guarantee

10% of the balance with cash or cash-like instruments. If we have an overcollateralization

amount of $100,000 on $1,000,000, we have a 10% credit support amount. The reserve fund is

capitalized by the guaranteeing party. If future defaults and losses can be accurately estimated,

there is no need to provide 100% credit support. Such would be fully guaranteeing the loans,

42

dollar for dollar. In the proposed structure of a partial guarantee through overcollateralization,

the lender is still exposed to risk and hopefully such will mitigate moral hazard coming from a

guarantee.

Additionally, in the model the guarantee fund receives excess spread from the loans every

month. This is accomplished by charging borrowers one rate, taking a nominal amount of the

payment, then allowing lenders to claim the rest. If borrowers pay 15%, the reserve fund is paid

2%, and the lenders receive 13% on the outstanding balance. This 2% helps to recapitalize the

guarantee fund in the event losses begin to deplete it. This excess spread can be set to any

amount.

The reserve fund is leveraged against defaults and losses. A 5% guarantee fund’s return is

levered 20x against losses, a 10% guarantee is levered 10x, and a 20% guarantee is levered 5x.

What this means is that a 1% loss wipes out 20% of the reserve fund in the case that it is a 5%

reserve, but only 5% in the case of a 20% reserve

This leverage generates spectacular returns to the reserve fund if the loan pool is high

performing, and losses if the pool performs poorly. This makes sense within basic thoughts

about credit and interest rates, namely higher risk needs higher returns to attract sponsorship.

The reserve fund is a partial credit guarantee scheme, but it is structured to operate more

efficiently than PCGSs implemented in the past. Rather than offer a high coverage ratio, and

force lenders to shoulder some of the default, it is a dynamic fund which adjusts the support level

over time and attempts to cover principal losses and interest losses in each period. Rather than

offering a coverage ratio of 50-70% of principal exposure, it covers 10% of an outstanding

43