Embed Size (px)

Citation preview

1

Importance of the oversight function for

financial market infrastructures: General

framework and objectives

Workshop on payments systems oversight

Kingston, Jamaica

5 December 2012

Klaus Löber

CPSS Secretariat

Bank for International Settlements

1 * Views expressed are those of the author and not necessarily those of the BIS

2

Outline

The role of the Committee on Payment and Settlement Systems

(CPSS)

Concept: What is oversight?

Purpose: Why is oversight performed?

Scope: What should be overseen?

Method: How should it be done?

3

The Committee on Payment and Settlement Systems (CPSS)

Central bank membership (24)

Canada Sweden ECB Russia Japan

USA UK Germany Turkey Korea

Mexico Switzerland Netherlands India China

Brazil Belgium Saudi Arabia Hong Kong

France South Africa Singapore

Italy Australia

The CPSS serves as a forum for central banks to monitor and

analyse developments in the field of FMIs and to set common policies

and recommendations

From G10 (1990) to G10-plus (late 1990s) to approximately G20 (2009)

Originally reported to G10 Governors, now reports to “Global Economy”

Governors (also approximately G20)

Secretariat based at the BIS in Basel, Switzerland

Part of the “Basel process” (also including BCBS, FSB, IAIS, IADI, …)

4

Role of the committee

Two key functions:

Standard Setting (including setting common policies and

recommendations)

eg. Principles for financial market infrastructures (2012)

Settlement risk in foreign exchange transactions (1996)

Central bank oversight of payment and settlement systems (2005)

Descriptive/Analytical (sharing information, carrying out analysis,

discussing issues, increasing mutual understanding …)

eg. Role of central bank money in payment systems (2003)

New developments in large value payment systems (2005)

The interdependencies of payment and settlement systems (2008)

Innovations in retail payments (2012)

5

What is oversight?

“Oversight of payment and settlement systems is a central

bank function whereby the objectives of safety and efficiency

are promoted by monitoring existing and planned systems,

assessing them against the objectives and, where necessary,

inducing change.”

Oversight of payment and settlement systems, BIS, 2005

6

Two “old” CPSS definitions

A central bank task, principally intended to promote the

smooth functioning of payment systems and to protect the

financial system from possible “domino effects” which may

occur when one or more participants in the payment system

incur credit or liquidity problems. Payment systems oversight

aims at a given system (e.g. a funds transfer system) rather

than individual participants

Glossary of terms, BIS, March 2003

A public policy activity principally intended to promote the

safety and efficiency of payment systems and in particular to

reduce systemic risk

Core principles, BIS, January 2001

7

A form of “regulation”

FINANCIAL SYSTEM

INSTITUTIONS

SUPERVISION

INFRASTRUCTURES

OVERSIGHT

MARKETS

SURVEILLANCE

All can be described as “regulatory” activities in a very

broad sense of “involvement” by the authorities

8

Monitor

Assess

Induce change

Policy

(setting)

Oversight is a “regulatory” activity:

“Regulating” infrastructures, not their participants

9

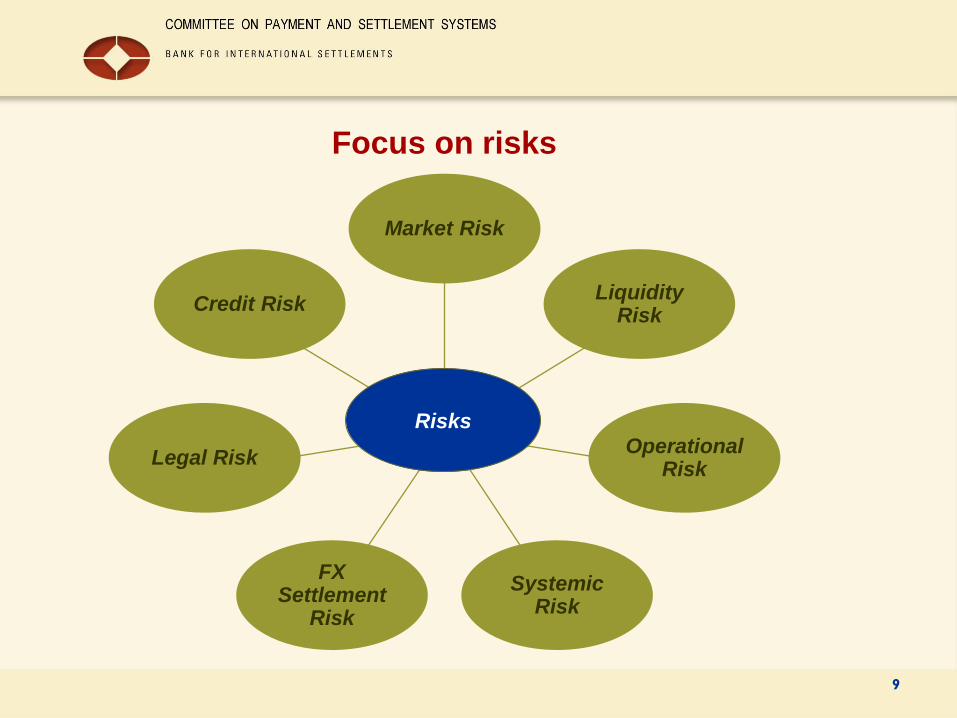

Focus on risks

Market Risk

Liquidity Risk

Operational Risk

Systemic Risk

FX Settlement

Risk

Legal Risk

Credit Risk

Risks

10

Oversight process

Enforcement

Collecting and

assessing relevant

information

Formulation of the

oversight policy stance

• Monitoring and

analysing relevant

developments

(legal, technical,

business environment)

and risks

Setting standards

(binding or non-

binding)

Formulating policy

framework

Regular oversight activities

Ad-hoc assessments

• Collection of data/information

• Identification of potential weaknesses

• Recommendations to operators

Inducing change

• Binding legal instruments

• Informal tools (e.g. moral

suasion)

• Voluntary agreements

• Cooperation with other

authorities

Oversight is an iterative process

11

Financial Market Infrastructures (FMIs)

Facilitate recording, clearing and settlement of monetary and other financial

transactions

Strengthen the markets they serve

Mitigate systemic risk

FMIs play a critical role in fostering financial stability

On the other hand, FMIs also concentrate risk – not the least through

interdependencies.

if this risk is not properly managed, FMIs can be sources of:

Credit losses

Liquidity and collateral dislocations

Financial shocks

FMIs could be major channels through which shocks are transmitted

across domestic and international financial markets

International standards for FMIs have been established over the years to

address these risks

12

Criticality of safety and effciiency of FMIs for financial

markets, because of the impact of:

• Intransparency and inefficiencies

• Market failures

• Concentration and lack of substitutability

• Network effects and interdependencies

• Systemic risk

However, some implications:

• Primary responsibility of FMIs for their activities

• Moral hazard

• Financial costs

Why is oversight carried out?

13

Who should perform oversight? – a “central bank

function”

Central bank advantages:

Expertise and experience

Operator and user perspective

Relevance for financial and monetary stability

Relevance for lender-of-last-resort role

But some implications:

• Regulatory overlap with other authorities (supervisors,

competition authorities, etc.)

• Potential conflicts of interest

• Reputational risk

14

Central bank rationale

Ensure the safety and

efficiency of financial market

infrastructure

Contribute to financial

stability

Contribute to the smooth

implementation of

monetary policy

Maintain the public

confidence in the currency

15

Main public policy objectives in view of limiting systemic risk and

fostering transparency and financial stability (see PFMIs):

Safety

Robust management of risks such as: legal, credit, liquidity, general

business, operational risks etc.

Efficiency

Best use of resources by financial market infrastructures and their

participants in view of performing effectively their functions and the

wider market they serve

Public policy objectives

16

Scope of oversight - which “systems”?

PFMIs:

Systemically relevant payment systems (large value vs. retail)

Central securities depositories and securities settlement systems

Central counterparties

Trade repositories

What about:

Critical service providers?

Other retail payment systems?

Payments instruments/schemes?

Quasi-systems (correspondent banks and custodians)?

17

1974 1989

Herstatt

G-10 Committee

on Payment and

Settlement

Systems

G-10 Ad hoc

Committee on

Interbank

Netting

Schemes

(Lamfalussy)

1990

(Allsopp)

Report on

Settlement

Risks in FX

CPSS Core

Principles

for SIPS

1996

CLS

2002 2001 1980

G-10 Group

of Experts

on Payment

Systems

1985 1991 1992 2004

CPSS Report

on Oversight

Development and scope of the oversight role

1999

CPSS/IOSCO

Recommen-

dations for SSS

CPSS/IOSCO

Recommen-

dations for

CCPs

2005 2003 2007 2008

CPSS-IOSCO

guidance on OTC

derivatives

FX settle-

ment risk

Interdepen-

dencies

Lehman

2009 2011 2012

CPSS-IOSCO

PFMIs

18

Large-Value Payment Systems

Backbone of the financial markets

RTGS or DNS, multicurrency: CLS

Retail Payment Systems

used for the bulk of payments between individuals and corporates

may have a role with respect to the safety and efficiency of the

financial system and citizens’ confidence in the currency

may be systemically relevant (PFMIs)

Policy issues for central banks in retail payments (BIS, 2003)

“Each central bank should examine developments in its markets … in order to form a view on whether [policy] issues arise. Where such issues are judged to arise, [central banks] may decide to take action …”

19

Clearing and settlement infrastructure –

CSDs, SSSs and CCPs

Embedded payment arrangements

Central banks have a strong interest in CCPs and SSSs due to

their relevance for financial stability, monetary policy and the

smooth operation of payments systems

Frequent need to cooperate with other competent authorities

(e.g. securities regulators), at national or cross-border level

20

Trade repositories (TRs)

TRs are data warehouses that record trade-related data, and which

are connected to CCPs by a relationship of data feed

TRs not comparable with CCPs in terms of systemic risk

implications, but their safety, resilience and efficiency is significant

from a financial stability perspective in view of the reliance of a

large number of market participants, public authorities and market

infrastructures on the availability and accuracy of the data

Need for a framework for the operation of trade repositories (i.a.

access/participation, disclosure of data, protection of data, legal

certainty/status of registered contracts)

21

Payment instruments

Arrangements rather than system

Non-cash payment instruments (means to transfer (retail) funds

between accounts), e.g. cards, credit transfer schemes, e-money

schemes, mobile payments, remittance services, cheques

Essential part of payment infrastructure

Low risks, but important for both maintaining confidence in the

currency and promoting an efficient economy

Frequently focus on security

22

Third-party service providers

provide key services to FMIs

critical for the functioning of the financial markets (e.g. SWIFT)

Annex F to the PFMIs

• Risk identification and manadement

• Information security

• Reliability and resilience

• Technilogy planning

• Communication with users

23

Quasi-systems –

Correspondent banks and custodian banks

key components of an economy’s payment and settlement arrangements

potential for strong concentration, giving rise to possible financial and operational risks

B

Central bank

or FMI

C

A

D

24

A question of “territory”

Large value payment system

Efficiency Risk

= central bank

overseer

= consumer

protection agency

= banking

supervisor

RTGS

CLS

Bank’s capital

and liquidity

Bank charges

Retail payment system

Securities settlement system

Central counterparty

Quasi system

Individual institutions (eg banks)

Direct debit conditions

= securities

regulator

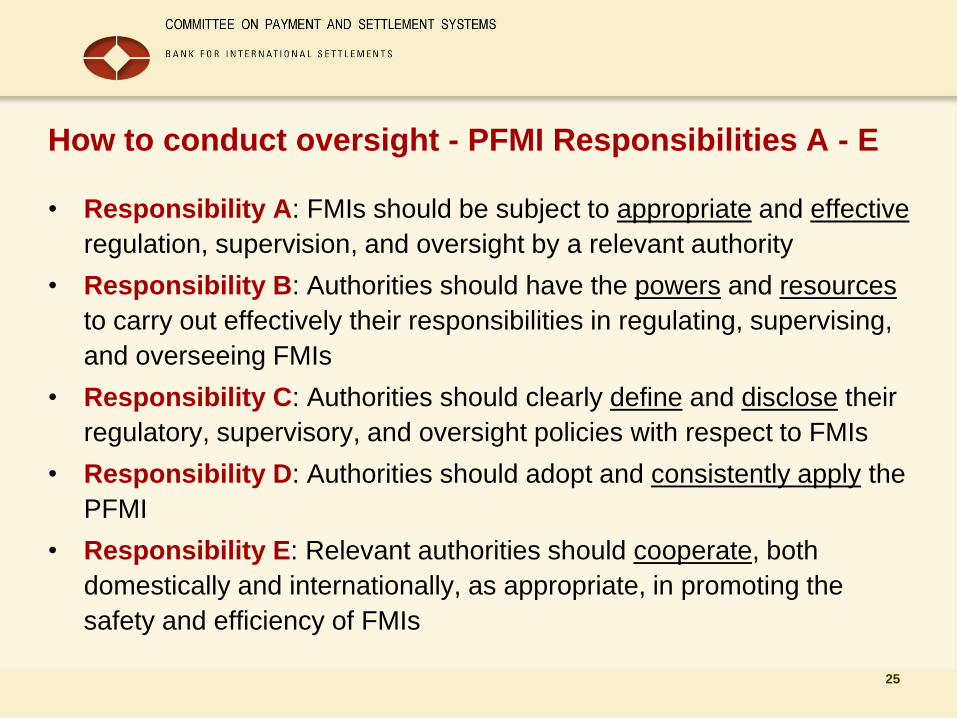

How to conduct oversight - PFMI Responsibilities A - E

• Responsibility A: FMIs should be subject to appropriate and effective

regulation, supervision, and oversight by a relevant authority

• Responsibility B: Authorities should have the powers and resources

to carry out effectively their responsibilities in regulating, supervising,

and overseeing FMIs

• Responsibility C: Authorities should clearly define and disclose their

regulatory, supervisory, and oversight policies with respect to FMIs

• Responsibility D: Authorities should adopt and consistently apply the

PFMI

• Responsibility E: Relevant authorities should cooperate, both

domestically and internationally, as appropriate, in promoting the

safety and efficiency of FMIs

25

26

Central bank oversight of payment and settlement

systems, CPSS, May 2005

Described how CPSS central banks currently do oversight

Set out five general principles for oversight (GOPs):

GOP A: Transparency

GOP B: Use of international standards

GOP C: Effective powers and capacity

GOP D: Consistency

GOP E: Cooperation with other authorities

Set out five additional principles for international cooperative

oversight (eg for CLS, SWIFT)

26

27

Evolution of the central bank responsibilities in

the new principles

CSIPS RSSS RCCP GOP

Responsibility A: A 18 15 B

Responsibility B: C 18 15 C

Responsibility C: A 18 15 A

Responsibility D: B, C – – D

Responsibility E: D 18 15 E

27

28

Responsibility A: Regulation, supervision and

oversight of FMIs

• Authorities should clearly define and publicly disclose the criteria used

to identify FMIs that should be subject to regulation, supervision, and

oversight

• FMIs that have been identified using these criteria should be

regulated, supervised, and overseen by a central bank, market

regulator, or other relevant authority

Typically requires setting out responsibilities, objectives and criteria

for determining who the standards apply to

Necessity to clarify roles in case of multiple authorities

29

Responsibility B: Regulatory, supervisory and

oversight powers and resources

• Authorities should have powers or other authority consistent with their

relevant responsibilities, including:

• ability to obtain timely information

• ability to induce change or enforce corrective action

• Authorities should have sufficient resources to fulfil their responsibilities

Powers could be statutory or non-statuotory

Safeguards to ensure confidentiality

Who has to provide information (e.g. outsourcees)?

Adequate funding, qualified and experienced personel - complexity

Organisational structure - separation of functions?

30

Formal responsibilities

Should the central bank have statutory responsibilities and powers, i.e. set

out in law, explicitly and perhaps in some detail?

Possible advantages

transparency

binding effects

Possible disadvantages

less flexibility to adapt

Enforcement tools

• Formal legal instruments (guidelines, regulations, instructions)

• Sanctions (financial, criminal, closure of systems)

• Informal tools (e.g. moral suasion)

• Cooperation with other authorities

• Voluntary agreements

Are non-binding instruments enough?

31

Responsibility C: Disclosure of policies with respect

to FMIs

• Authorities should clearly define their policies with respect to FMIs,

which include the authorities’ objectives, roles, and regulations

• Authorities should publicly disclose their relevant policies with respect to

the regulation, supervision, and oversight of FMIs

Transparency supports consistency, accountability and effectiveness

Typically involves a public document setting out the policies (see

responsibility A)

32

PFMI Responsibility C is silent about this

Advantages:

– Useful information to help markets to make its own judgment

– A useful oversight “power” for the central bank

– Promotes central bank accountability

Disadvantages:

– Confidentiality of information

– Competition issues

– May create adverse effects on market confidence

Transparency of assessments?

33

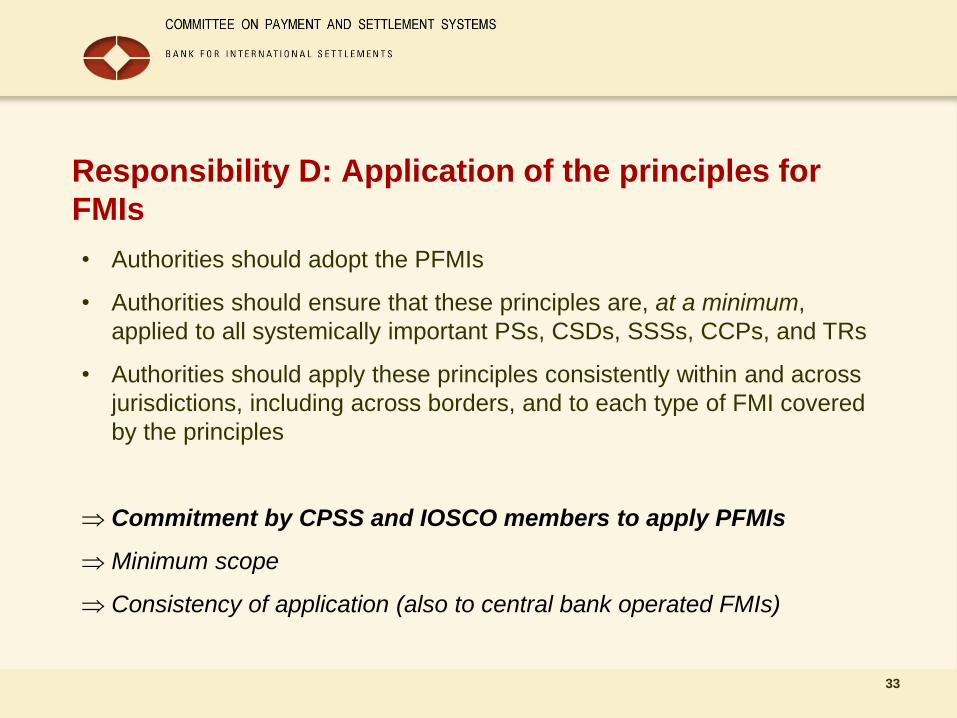

Responsibility D: Application of the principles for

FMIs

• Authorities should adopt the PFMIs

• Authorities should ensure that these principles are, at a minimum,

applied to all systemically important PSs, CSDs, SSSs, CCPs, and TRs

• Authorities should apply these principles consistently within and across

jurisdictions, including across borders, and to each type of FMI covered

by the principles

Commitment by CPSS and IOSCO members to apply PFMIs

Minimum scope

Consistency of application (also to central bank operated FMIs)

34

Consistency

Important where systems are in competition with each other

Central banks should indicate criteria for “comparability”

(e.g. types of instruments, value, types of participants, risk

attributes)

Consistency also needed where a central bank operates a

system itself to avoid competition issues and conflict of

interests (e.g. by organisational separation)

35

Responsibility E: Cooperation with other authorities

• Relevant authorities should cooperate with each other in fulfilling their

respective mandates with respect to FMIs

• both domestically and internationally

• to foster efficient and effective communication and consultation in

order to support each other

• Cooperation needs to be effective in normal circumstances

• Cooperation should be adequately flexible to facilitate effective

communication, consultation, or coordination, as appropriate, during

periods of market stress, crisis situations, and the potential recovery,

wind-down, or resolution of an FMI

36

Responsibility E: Cooperation with other authorities

• Cooperation may take a variety of forms. The form, degree of

formalization and intensity of cooperation should promote the efficiency

and effectiveness of the cooperation, and should be appropriate to the

nature and scope of each authority’s responsibility for the supervision or

oversight of the FMI and commensurate with the FMI’s systemic

importance in the cooperating authorities’ various jurisdictions.

Cooperative arrangements should be managed to ensure the efficiency

and effectiveness of the cooperation with respect to the number of

authorities participating in such arrangements

MoUs

Formal colleges

Information sharing arrangements

37

Between central banks

in the context of cooperative oversight of cross-

border and multicurrency systems

Between central banks at international level (I.e.

CPSS)

to define and implement oversight requirements

for global infrastructures

With securities regulators at international level (e.g

CPSS-IOSCO)

to define common standards

With other regulators (MoUs, colleges)

to reconcile the “infrastructure” and the

“institution” perspective

With financial stability authorities

to foster the macroprudential perspective on

systemic risks

With resolution authorities

to ensure safe and effective resolution of FMIs

Co-operation

• align conflicting objectives

• promote consistency of oversight requirements and approaches and avoid duplication and overlaps

• access to comprehensive and timely information on factors that may impact on the safety and resilience of infrastructures

• clarification of responsibilities and procedures for cooperation among authorities during crisis situations

Aim to:

38

Responsibility E: Cooperation with other authorities

• If an authority has identified an actual or proposed operation of a cross-

border or multicurrency FMI in its jurisdiction, the authority should, as

soon as it is practicable, inform other relevant authorities that may have

an interest in the FMI’s observance of the CPSS-IOSCO Principles for

financial market infrastructures

Notification duty (in advance where possible)

39

Responsibility E: Cooperation with other authorities

• When assessing an FMI’s payment and settlement arrangements and

its related liquidity risk-management procedures in any currency for

which the FMI’s settlements are systemically important against the

principles, the authority or authorities with primary responsibility with

respect to the FMI should consider the views of the central banks of

issue. If a central bank of issue is required under its responsibilities to

conduct its own assessment of these arrangements and procedures, the

central bank should consider the views of the authority or authorities

with primary responsibility with respect to the FMI

Role of the central bank of issue for settlement and liquidity

arrangement in its currency

Duty to consider, not to jointly agree

What can be done in case of disagreement (e.g. discourage of use of

FMI)?

40

Responsibility E: Cooperation with other authorities

• For an FMI where cooperative arrangements are appropriate, at least

one authority should accept responsibility for establishing efficient and

effective cooperation among all relevant authorities. In international

cooperative arrangements where no other authority accepts this

responsibility, the presumption is the authority or authorities with primary

responsibility in the FMI’s home jurisdiction should accept this

responsibility

• At least one authority should ensure that the FMI is periodically

assessed against the principles and should, in developing these

assessments, consult with other authorities that conduct the supervision

or oversight of the FMI and for which the FMI is systemically important

appoint an authority with primary responsibility

consider appropriate cooperative arrangements

assessment of the system as a whole by that authority, in consultation

with the other authorities

41

Cooperative oversight and the concept of lead overseer

Basis: “Lamfalussy principles” for cooperative oversight of cross-border and

multicurrency netting and settlement systems

– One central bank (the lead overseer) assumes primary oversight

responsibility

– The lead overseer consults the (most representative) other central banks

with a valid interest

– The settlement procedures are overseen jointly by the lead overseer and

the central banks of issue of relevant currencies

– Central banks involved in cooperative oversight undertake efforts to reach

consensus

42

Responsibility E: Cooperation with other authorities

• Relevant authorities should provide advance notification, where

practicable and otherwise as soon as possible thereafter, regarding

pending material regulatory changes and adverse events with respect to

the FMI that may significantly affect another authority’s regulatory,

supervisory, or oversight interests

• Relevant authorities should coordinate to ensure timely access to trade

data recorded in a TR

cf. the work being conducted by the CPSS and IOSCO on access to

data by competent authorities

43

Challenges for oversight

• Market infrastructure changes:

increased attention of overseers to the clearing and settlement

infrastructures or security of payments

• Developing oversight framework:

evolving legal and regulatory environment, i.e new legislation and

international standards

• Need for co-operation and sharing of information:

between central banks, securities regulators, supervisors and other

relevant authorities for emerging cross-border and global FMIs

![Federal Oversight of the Debt Relief Industry: A More ... · 2014] FEDERAL OVERSIGHT OF THE DEBT RELIEF INDUSTRY 43 debtor’s problems, enrolling in a debt settlement program always](https://img.pdfslide.us/doc/110x75/60483001e452914ec57f43df/federal-oversight-of-the-debt-relief-industry-a-more-2014-federal-oversight.jpg)