Embed Size (px)

Citation preview

www.eia.gov U.S. Energy Information Administration Independent Statistics & Analysis

Implications of the U.S. Shale Revolution

For US-Canada Energy Summit October 17, 2014 | Chicago, IL By Adam Sieminski, Administrator U.S. Energy Information Administration

0

5

10

15

20

25

30

0.0

10.0

20.0

30.0

40.0

50.0

60.0

U.S. is the largest producer of petroleum and natural gas in the world

US-Canada Energy Summit October 17, 2014 2

estimated U.S., Russia, and Saudi Arabia petroleum and natural gas production quadrillion Btu million barrels per day of oil equivalent

United States

Russia

Saudi Arabia

petro-leum

natural gas

2008 2009 2010 2011 2012 2013 2014e Source: U.S. Energy Information Administration Note: Petroleum production includes crude oil, natural gas liquids, condensates, refinery processing gain, and other liquids, including biofuels; barrels per day oil equivalent were calculated using a conversion factor of 1 barrel oil equivalent=5.55 million British thermal units (Btu)

3 US-Canada Energy Summit October 17, 2014

4 US-Canada Energy Summit October 17, 2014

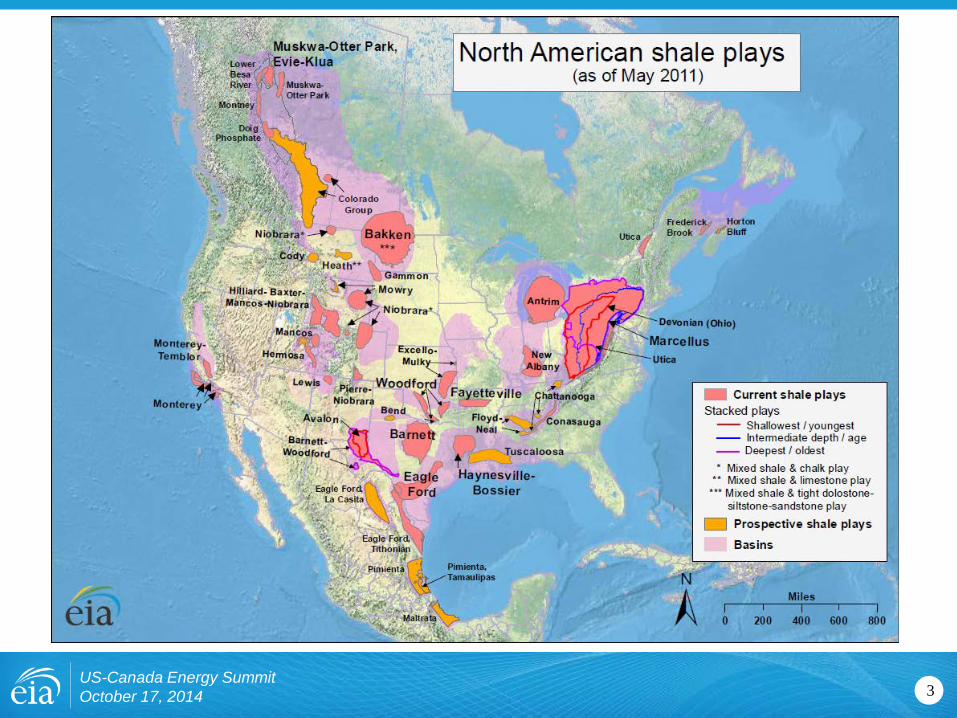

These seven regions accounted for 95% of U.S. oil production growth and all U.S. natural gas production growth from 2011-2013

Source: EIA, Drilling Productivity Report

The U.S. has experienced a rapid increase in natural gas and oil production from shale and other tight resources

5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2000 2002 2004 2006 2008 2010 2012 2014

Eagle Ford (TX)Bakken (MT & ND)Spraberry (TX & NM Permian)Bonespring (TX & NM Permian)Wolfcamp (TX & NM Permian)Delaware (TX & NM Permian)Yeso-Glorieta (TX & NM Permian)Niobrara-Codell (CO, WY)HaynesvilleUtica (OH, PA & WV)MarcellusWoodford (OK)Granite Wash (OK & TX)Austin Chalk (LA & TX)Monterey (CA)

U.S. tight oil production million barrels of oil per day

0

5

10

15

20

25

30

35

40

2000 2002 2004 2006 2008 2010 2012 2014

Marcellus (PA & WV)

Haynesville (LA & TX)

Eagle Ford (TX)

Fayetteville (AR)

Barnett (TX)

Woodford (OK)

Bakken (ND)

Antrim (MI, IN, & OH)

Utica (OH, PA & WV)

Rest of US 'shale'

U.S. dry shale gas production billion cubic feet per day

Sources: EIA derived from state administrative data collected by DrillingInfo Inc. Data are through August 2014 and represent EIA’s official tight oil & shale gas estimates, but are not survey data. State abbreviations indicate primary state(s).

US-Canada Energy Summit October 17, 2014

U.S. shale gas leads growth in total gas production through 2040, when production exceeds 100 billion cubic feet per day

6

U.S. dry natural gas production trillion cubic feet

Source: EIA, Annual Energy Outlook 2014, Reference case

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35

40

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Associated with oil Coalbed methane

Tight gas

Shale gas

Alaska Non-associated offshore

Non-associated onshore

projections history 2012

US-Canada Energy Summit October 17, 2014

billion cubic feet per day

7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2005 2012 2020 2025 2030 2035 2040

U.S. dry gas consumption trillion cubic feet

Source: EIA, Annual Energy Outlook 2014, Reference case

projections history

industrial*

electric power

commercial

residential

transportation**

11.2

4.1

1.7

11.0

3.6

9.1

4.2

0.7

8.5

2.9

*Includes combined heat-and-power and lease and plant fuel **Includes pipeline fuel

Natural gas consumption growth is driven by electric power, industrial, and transportation use

US-Canada Energy Summit October 17, 2014

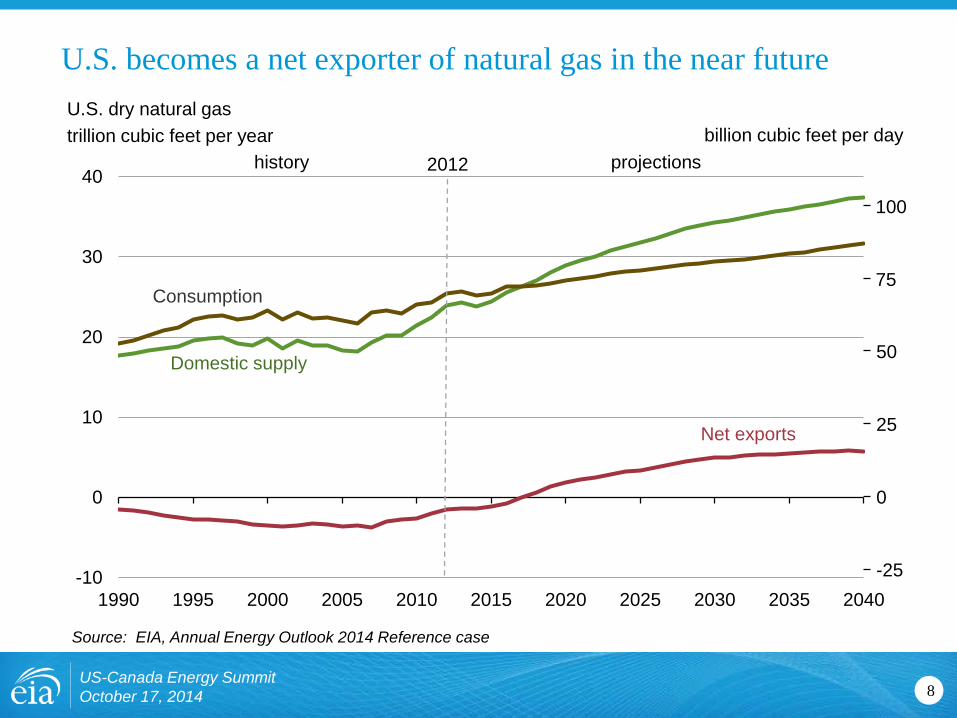

U.S. becomes a net exporter of natural gas in the near future

8

U.S. dry natural gas trillion cubic feet per year

Source: EIA, Annual Energy Outlook 2014 Reference case

US-Canada Energy Summit October 17, 2014

-10

0

10

20

30

40

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

projections history 2012

Consumption

Domestic supply

Net exports

100

75

50

25

0

-25

billion cubic feet per day

Source: EIA, Annual Energy Outlook 2014, Reference case and High Oil and Gas Resource case

9 US-Canada Energy Summit October 17, 2014

-4

-2

0

2

4

6

8

2010 2015 2020 2025-4

-2

0

2

4

6

8

2010 2015 2020 2025

Projected U.S. natural gas trade depends on assumptions regarding resources and future technology advances

Reference case trillion cubic feet per year

exports to Mexico exports to Canada

lower 48 LNG exports

imports from Canada

LNG imports

High Oil and Gas Resource case trillion cubic feet per year

billion cubic feet per day

0

5

20

15

10

-5

-10

Shale gas in eastern Canada

10

Source: Advanced Resources International, “Technically Recoverable Shale Oil and Shale Gas Resources: An Assessment of 137 Shale Formations in 41 Countries Outside the United States”

US-Canada Energy Summit October 17, 2014

• Of the four shale plays in Eastern Canada, two have been assessed by ARI

– Utica in Quebec has 31.1 Tcf of technically recoverable resources

– Horton Bluff in Nova Scotia has 3.4 Tcf of technically recoverable resources

• These shale resource volumes are not included in NEB’s 2013 estimates

• Quebec enacted a hydraulic fracturing moratorium

in 2012 pending further research • New Brunswick permits hydraulic fracturing, but

has imposed strict rules surrounding it

• Nova Scotia, similar to Quebec, will not permit hydraulic fracturing until the completion of a review, due mid-2014

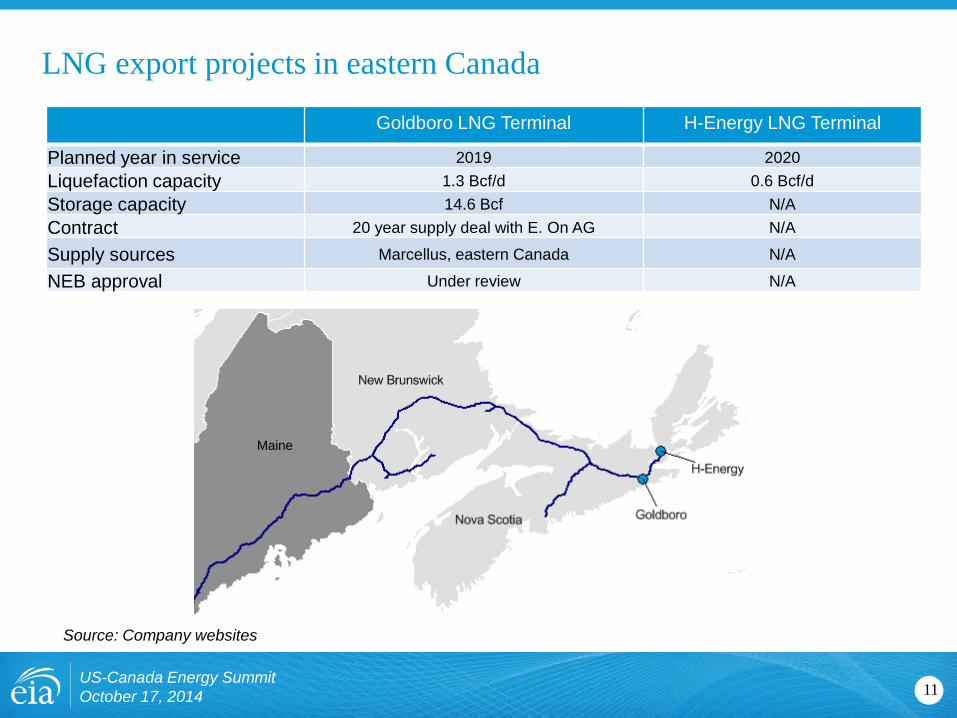

LNG export projects in eastern Canada

11

Source: Company websites

US-Canada Energy Summit October 17, 2014

Goldboro LNG Terminal H-Energy LNG Terminal

Planned year in service 2019 2020 Liquefaction capacity 1.3 Bcf/d 0.6 Bcf/d Storage capacity 14.6 Bcf N/A Contract 20 year supply deal with E. On AG N/A

Supply sources Marcellus, eastern Canada N/A

NEB approval Under review N/A

Maine

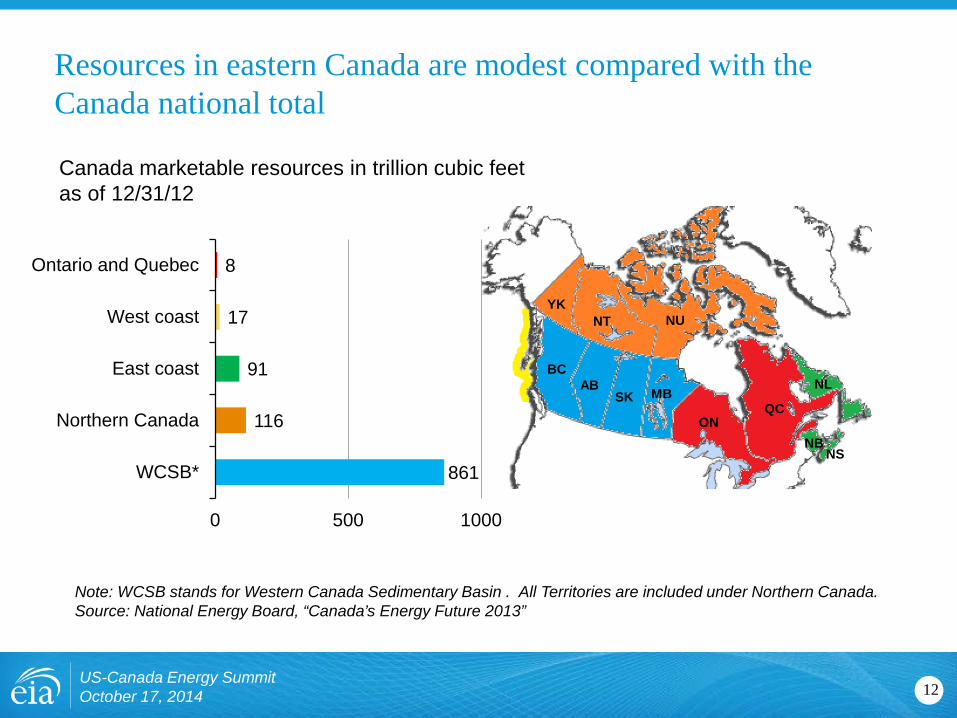

Resources in eastern Canada are modest compared with the Canada national total

Note: WCSB stands for Western Canada Sedimentary Basin . All Territories are included under Northern Canada. Source: National Energy Board, “Canada’s Energy Future 2013”

12

Canada marketable resources in trillion cubic feet as of 12/31/12

US-Canada Energy Summit October 17, 2014

861

116

91

17

8

WCSB*

Northern Canada

East coast

West coast

Ontario and Quebec

0 500 1000

BC AB

YK NT

SK MB

ON QC

NS NB

NL

NU

Resource and technology assumptions have major implications for projected U.S. crude oil production beyond the next few years

0

2

4

6

8

10

12

14

1990 2000 2010 20200

2

4

6

8

10

12

14

1990 2000 2010 2020

13

Source: EIA, Annual Energy Outlook 2014; Short Term Energy Outlook, October 2014

Alaska

tight oil

other lower 48 states onshore

lower 48 states offshore

STEO October 2014 U.S. crude oil projection

2012 projections history projections history

2012

Alaska

tight oil

other lower 48 states onshore

Reference case million barrels per day

High Oil and Gas Resource case million barrels per day

lower 48 states offshore

US-Canada Energy Summit October 17, 2014

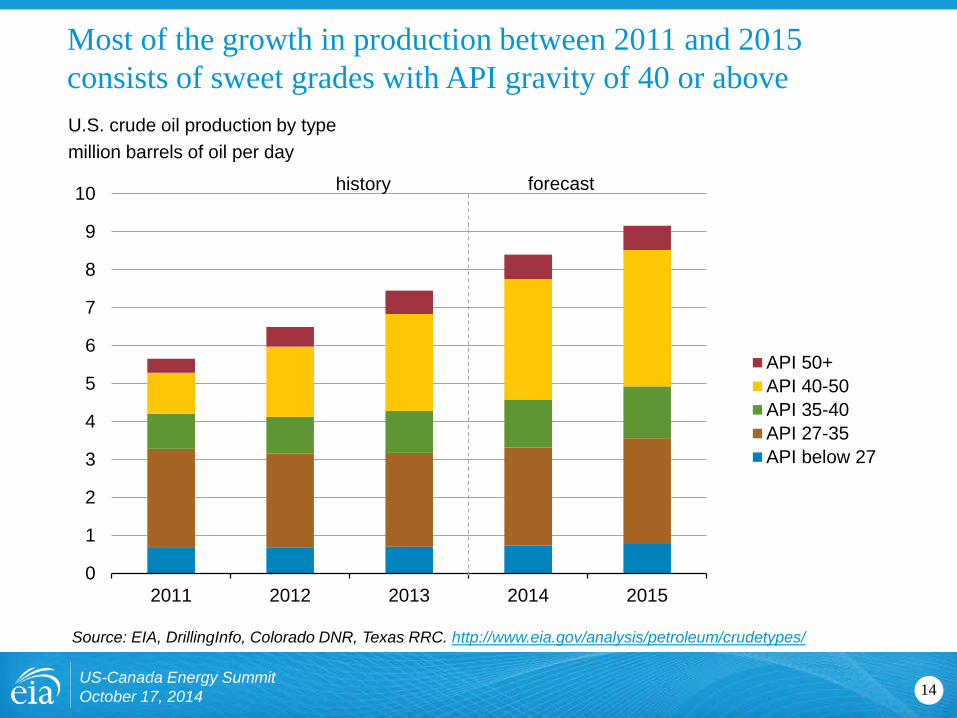

Most of the growth in production between 2011 and 2015 consists of sweet grades with API gravity of 40 or above

0

1

2

3

4

5

6

7

8

9

10

2011 2012 2013 2014 2015

API 50+API 40-50API 35-40API 27-35API below 27

U.S. crude oil production by type million barrels of oil per day

Source: EIA, DrillingInfo, Colorado DNR, Texas RRC. http://www.eia.gov/analysis/petroleum/crudetypes/

US-Canada Energy Summit October 17, 2014 14

forecast history

U.S. rail carloads of crude oil and petroleum products exceed 1.5 million b/d in 2014

US-Canada Energy Summit October 17, 2014 15

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

number of rail carloads per week

Source: U.S. Energy Information Administration, based on Association of American Railroads

million barrels per day

U.S. petroleum product net exports million barrels per day

-3

-2

-1

0

1

2

3

1950 1960 1970 1980 1990 2000 2010

Source: EIA, Annual Energy Outlook 2014 Reference case and Short Term Energy Outlook

US-Canada Energy Summit October 17, 2014 16

U.S. is already a major net exporter of petroleum products

2015(e)

17 US-Canada Energy Summit October 17, 2014

Over 60% of U.S. petroleum product exports go to the Americas, with Mexico and Canada as its largest global trading partners

Source: EIA Americas Report

0

500

1000

1500

2000

2500

3000

3500

4000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

U.S. petroleum product gross exports million barrels per day

Canada

Mexico

Other Americas

Other Global

Most significant contributors to non-OPEC crude and lease condensate production: Canada, Brazil, U.S., Kazakhstan, Russia

0

6

12

18

24

Canada United States Mexico Brazil Kazakhstan Russia Other

2010 2025 2040

non-OPEC crude and lease condensate production, Reference case million barrels per day

Source: EIA, International Energy Outlook 2014

US-Canada Energy Summit October 17, 2014 18

Tight oil production will spread to nations outside of the United States and Canada over the projection

0

1

2

3

4

5

6

7

8

United States Canada Mexico Russia Argentina China Rest of world

2010 2025 2040

tight oil production, Reference case million barrels per day

Source: EIA, International Energy Outlook 2014

US-Canada Energy Summit October 17, 2014 19

2.9 MMbbl/d in 2013

3.9 MMbbl/d in 2014 (STEO)

AEO2014 High Resource case

5.0 MMbbl/d in 2015 (STEO)

Growing U.S. oil production and rising demand in China have together made China the world’s largest net oil importer

US-Canada Energy Summit October 17, 2014 20

0

1

2

3

4

5

6

7

8

9

10

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15

U.S. net imports

China net imports

net imports for China and the United States million barrels per day

Note: Net oil imports are defined as total liquid fuels consumption less domestic production Source: EIA, Short-Term Energy Outlook, October 2014

projections history

Aug-14

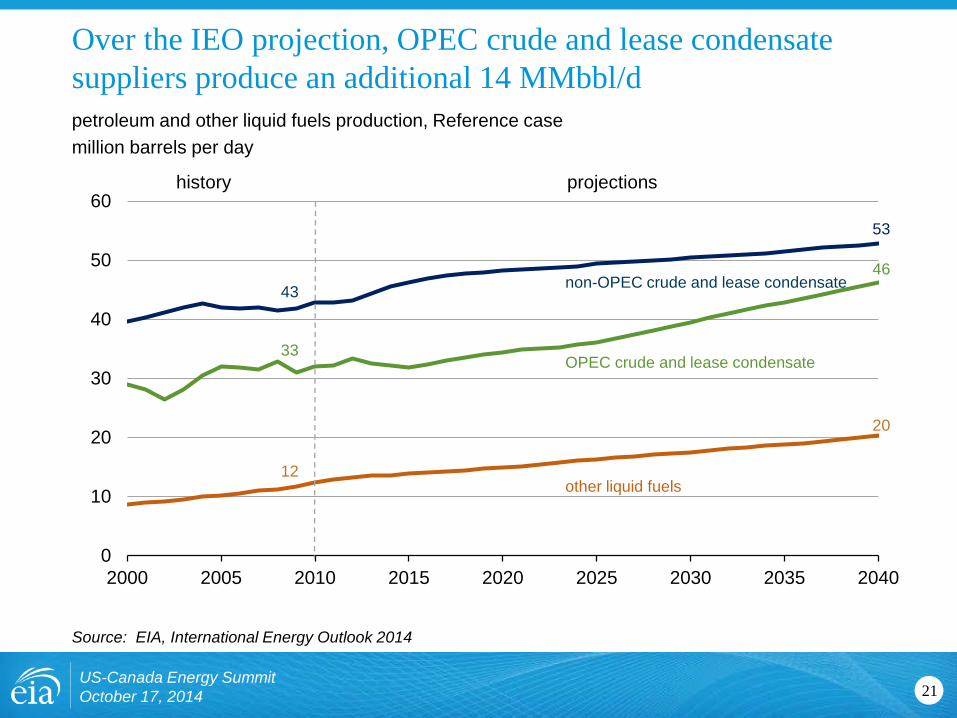

Over the IEO projection, OPEC crude and lease condensate suppliers produce an additional 14 MMbbl/d

0

10

20

30

40

50

60

2000 2005 2010 2015 2020 2025 2030 2035 2040

OPEC crude and lease condensate

non-OPEC crude and lease condensate

other liquid fuels

petroleum and other liquid fuels production, Reference case million barrels per day

Source: EIA, International Energy Outlook 2014

US-Canada Energy Summit October 17, 2014 21

projections history

43

33

12

53

46

20

Areas of uncertainty in the outlook

• China’s energy demand growth; particularly in transportation – EIA is working with MIT and others to upgrade the structural and macroeconomic

determinates of transportation demand in all regions for IEO2015

• Increasing global trade of natural gas and HGL in addition to oil – EIA is integrating the representation of oil and natural gas supply and other

hydrocarbons

• Global development of tight oil and shale gas resources – EIA is gathering geology and production information, and conducting outreach

• Impact of geopolitical tensions on energy supply – EIA exploring options for representing these uncertainties in the outlook

US-Canada Energy Summit October 17, 2014 22

For more information

US-Canada Energy Summit October 17, 2014 23

U.S. Energy Information Administration home page | www.eia.gov

Annual Energy Outlook | www.eia.gov/aeo

Short-Term Energy Outlook | www.eia.gov/steo

International Energy Outlook | www.eia.gov/ieo

Monthly Energy Review | www.eia.gov/mer

Today in Energy | www.eia.gov/todayinenergy

State Energy Portal | www.eia.gov/state

Drilling Productivity Report | www.eia.gov/petroleum/drilling/